In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”) included throughout this

presentation, the Company has provided information regarding “income before interest, other expense and income taxes,” “income before interest, other

expense, income taxes, restructuring costs and other special items, excluding the divested Interior business” (core operating earnings), “pretax income

before restructuring costs and other special items” and “free cash flow” (each, a non-GAAP financial measure). Other expense includes, among other

things, non-income related taxes, foreign exchange gains and losses, discounts and expenses associated with the Company’s asset-backed securitization

and factoring facilities, minority interests in consolidated subsidiaries, equity in net income of affiliates and gains and losses on the sale of assets. Free

cash flow represents net cash provided by operating activities before the net change in sold accounts receivable, less capital expenditures. The Company

believes it is appropriate to exclude the net change in sold accounts receivable in the calculation of free cash flow since the sale of receivables may be

viewed as a substitute for borrowing activity.

Management believes the non-GAAP financial measures used in this presentation are useful to both management and investors in their analysis of the

Company’s financial position and results of operations. In particular, management believes that income before interest, other expense and income taxes,

core operating earnings and pretax income before restructuring costs and other special items are useful measures in assessing the Company’s financial

performance by excluding certain items (including those items that are included in other expense) that are not indicative of the Company's core operating

earnings or that may obscure trends useful in evaluating the Company’s continuing operating activities. Management also believes that these measures

are useful to both management and investors in their analysis of the Company's results of operations and provide improved comparability between fiscal

periods. Management believes that free cash flow is useful to both management and investors in their analysis of the Company’s ability to service and

repay its debt. Further, management uses these non-GAAP financial measures for planning and forecasting in future periods.

Income before interest, other expense and income taxes, core operating earnings, pretax income before restructuring costs and other special items and

free cash flow should not be considered in isolation or as a substitute for pretax income, net income, cash provided by operating activities or other income

statement or cash flow statement data prepared in accordance with GAAP or as a measure of profitability or liquidity. In addition, the calculation of free

cash flow does not reflect cash used to service debt and therefore, does not reflect funds available for investment or other discretionary uses. Also, these

non-GAAP financial measures, as determined and presented by the Company, may not be comparable to related or similarly titled measures reported by

other companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures to the most directly comparable financial measures calculated

and presented in accordance with GAAP. Given the inherent uncertainty regarding special items, other expense and the net change in sold accounts

receivable in any future period, a reconciliation of forward-looking financial measures to the most directly comparable financial measures calculated and

presented in accordance with GAAP is not feasible. The magnitude of these items, however, may be significant.

Non-GAAP Financial Information

28

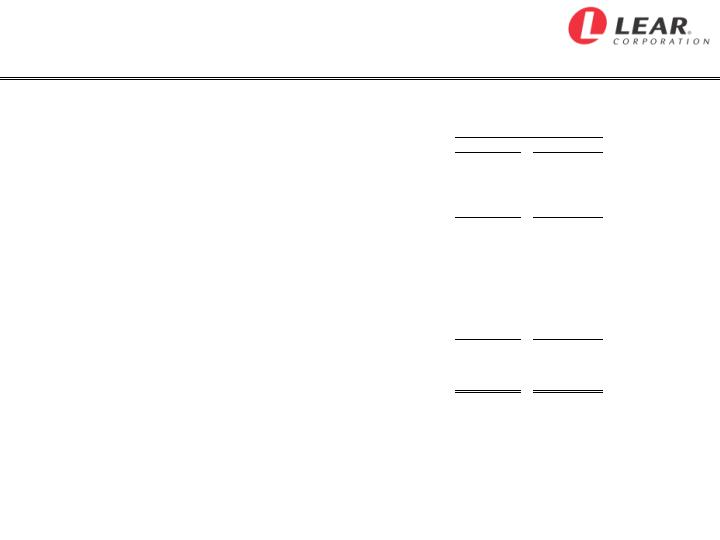

Non-GAAP Financial Information

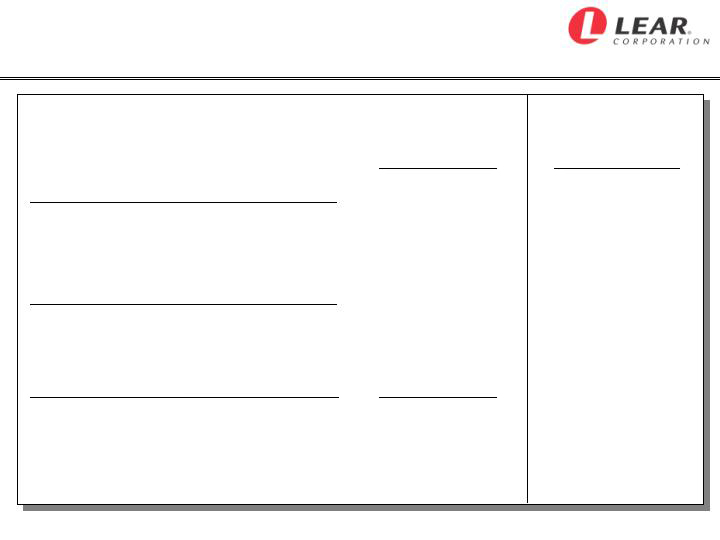

Core Operating Earnings

Three Months

(in millions)

Q1 2008

Q1 2007

Pretax income

$ 109.5

$ 82.3

Divestiture of Interior business

-

25.6

Interest expense

47.4

51.5

Other expense, net *

6.0

25.0

Income before interest, other expense and income taxes

$ 162.9

$ 184.4

Restructuring costs and other special items -

Costs related to restructuring actions

23.6

15.8

Additional costs related to Interior divestiture (COS and SG&A)

-

8.2

Costs related to merger transaction

-

9.4

U.S. salaried pension plan curtailment gain

-

(36.4)

Less: Interior business

-

(11.2)

Income before interest, other expense, income taxes,

restructuring costs and other special items, excluding the

divested Interior business

$ 186.5

$ 170.2

(core operating earnings)

* Includes minority interests in consolidated subsidiaries and equity in net income of affiliates.

29

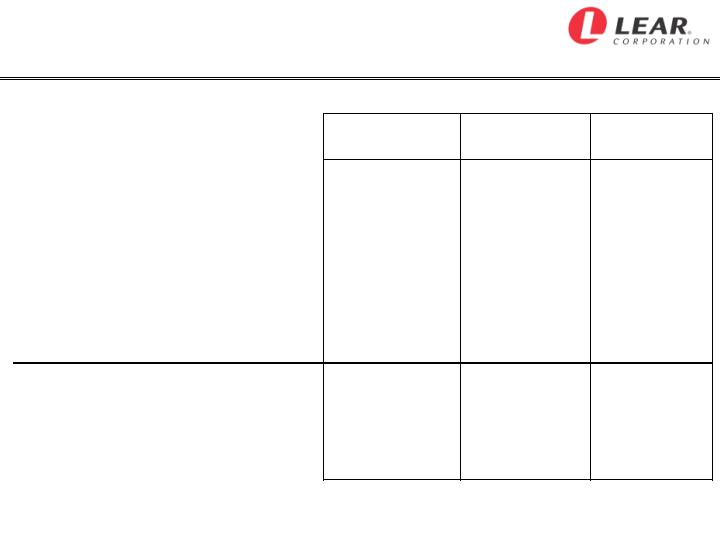

Non-GAAP Financial Information

Segment Earnings Reconciliation

Three Months

(in millions)

Q1 2008

Q1 2007

Seating

$ 183.3

$ 197.1

Electrical and electronic

35.3

17.5

Interior

-

8.8

Segment earnings

218.6

223.4

Corporate and geographic headquarters and elimination of

intercompany activity

(55.7)

(39.0)

Income before interest, other expense and

income taxes

$ 162.9

$ 184.4

Divestiture of Interior business

-

25.6

Interest expense

47.4

51.5

Other expense, net

6.0

25.0

Pretax income

$ 109.5

$ 82.3

30

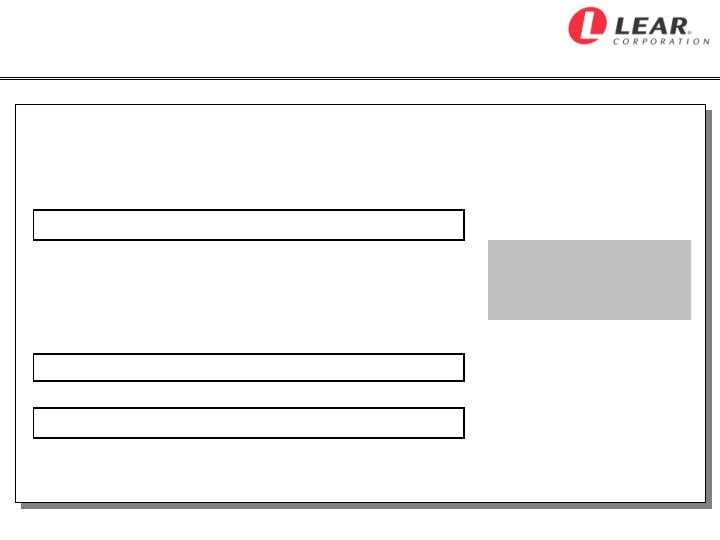

Non-GAAP Financial Information

Adjusted Segment Earnings

Three Months Q1 2008

Three Months Q1 2007

Electrical and

Electrical and

(in millions)

Seating

Electronic

Seating

Electronic

Sales

3,036.1

$

821.5

$

2,994.2

$

788.7

$

Segment earnings

183.3

$

35.3

$

197.1

$

17.5

$

Costs related to restructuring actions

13.6

9.5

(4.6)

20.0

Adjusted segment earnings

196.9

$

44.8

$

192.5

$

37.5

$

31

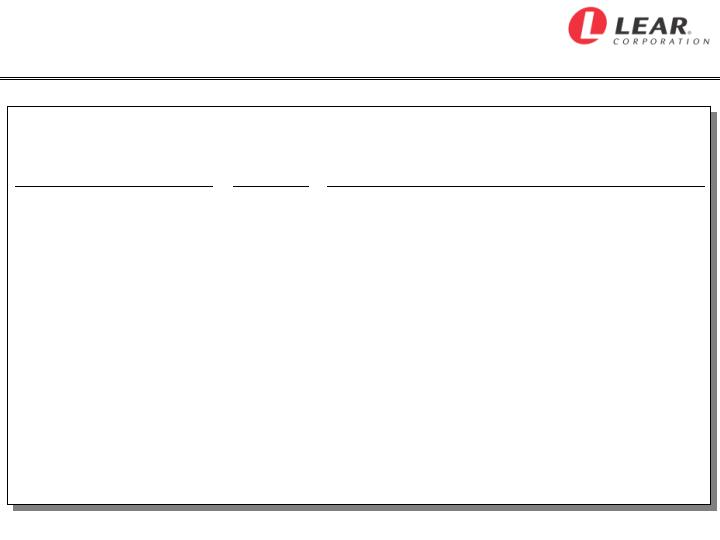

Non-GAAP Financial Information

Cash from Operations and Free Cash Flow

Three Months

(in millions)

Q1 2008

Net cash provided by operating activities

125.8

$

Net change in sold accounts receivable

(111.7)

Net cash provided by operating activities before net

change in sold accounts receivable

(cash from operations)

14.1

Capital expenditures

(45.5)

Free cash flow

(31.4)

$

32

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of

1995, including statements regarding anticipated financial results and liquidity. Actual results may differ materially from

anticipated results as a result of certain risks and uncertainties, including but not limited to, general economic conditions in

the markets in which the Company operates, including changes in interest rates or currency exchange rates, the financial

condition of the Company’s customers or suppliers, fluctuations in the production of vehicles for which the Company is a

supplier, changes in the Company’s current vehicle production estimates, the loss of business with respect to, or the lack

of commercial success of, a vehicle model for which the Company is a significant supplier, disruptions in the relationships

with the Company’s suppliers, labor disputes involving the Company or its significant customers or suppliers or that

otherwise affect the Company, the outcome and duration of the American Axle strike, the Company's ability to achieve

cost reductions that offset or exceed customer-mandated selling price reductions, the outcome of customer productivity

negotiations, the impact and timing of program launch costs, the costs, timing and success of restructuring actions,

increases in the Company's warranty or product liability costs, risks associated with conducting business in foreign

countries, competitive conditions impacting the Company's key customers and suppliers, the cost and availability of raw

materials and energy, the Company's ability to mitigate any increases in raw material, energy and commodity costs, the

outcome of legal or regulatory proceedings to which the Company is or may become a party, unanticipated changes in

cash flow, including the Company’s ability to align its vendor payment terms with those of its customers and other risks

described from time to time in the Company's Securities and Exchange Commission filings. In particular, the Company’s

financial outlook for 2008 is based on several factors, including the Company’s current vehicle production and raw material

pricing assumptions. The Company’s actual financial results could differ materially as a result of significant changes

in these factors.

The forward-looking statements in this presentation are made as of the date hereof, and the Company does not assume

any obligation to update, amend or clarify them to reflect events, new information or circumstances occurring after the

date hereof.

33