Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of February, 2015

Commission file number: 1-10110

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

(Exact name of Registrant as specified in its charter)

BANK BILBAO VIZCAYA ARGENTARIA, S.A.

(Translation of Registrant’s name into English)

Paseo de la Castellana, 81

28046 Madrid

Spain

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ¨ No x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ¨ No x

Table of Contents

Table of Contents

Quarterly report

Results

2014

Table of Contents

BBVA Group Highlights

(Consolidated figures)

| 31-12-14 | D% | 31-12-13 | 31-12-12 | |||||||||||||

Balance sheet (million euros) | ||||||||||||||||

Total assets | 651,511 | 8.7 | 599,517 | 637,785 | ||||||||||||

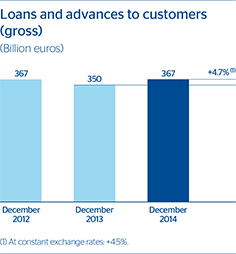

Loans and advances to customers (gross) | 366,536 | 4.7 | 350,110 | 367,415 | ||||||||||||

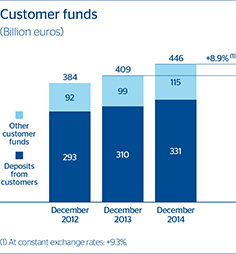

Deposits from customers | 330,686 | 6.6 | 310,176 | 292,716 | ||||||||||||

Other customer funds | 115,274 | 16.2 | 99,213 | 91,776 | ||||||||||||

Total customer funds | 445,960 | 8.9 | 409,389 | 384,493 | ||||||||||||

Total equity | 51,609 | 15.1 | 44,850 | 43,802 | ||||||||||||

Income statement (million euros) | ||||||||||||||||

Net interest income | 15,116 | 3.4 | 14,613 | 15,122 | ||||||||||||

Gross income | 21,357 | (0.2 | ) | 21,397 | 21,892 | |||||||||||

Operating income | 10,406 | 2.1 | 10,196 | 11,106 | ||||||||||||

Income before tax | 4,063 | 47.7 | 2,750 | 749 | ||||||||||||

Net attributable profit | 2,618 | 17.5 | 2,228 | 1,676 | ||||||||||||

Data per share and share performance ratios | ||||||||||||||||

Share price (euros) | 7.85 | (12.2 | ) | 8.95 | 6.96 | |||||||||||

Market capitalization (million euros) | 48,470 | (6.4 | ) | 51,773 | 37,924 | |||||||||||

Net attributable profit per share (euros) | 0.44 | 15.7 | 0.38 | 0.30 | ||||||||||||

Book value per share (euros) | 8.01 | 0.1 | 8.00 | 8.00 | ||||||||||||

P/BV (Price/book value; times) | 1.0 | 1.1 | 0.9 | |||||||||||||

PER (Price/Earnings; times) | 17.3 | 23.2 | 21.5 | |||||||||||||

Yield (Dividend/Price;%) | 4.5 | 4.1 | 6.0 | |||||||||||||

Significant ratios (%) | ||||||||||||||||

ROE (Net attributable profit/average equity) | 5.6 | 5.0 | 4.0 | |||||||||||||

ROTE (Net attributable profit/average tangible equity) | 6.5 | 6.0 | 5.0 | |||||||||||||

ROA (Net income/average total assets) | 0.50 | 0.48 | 0.37 | |||||||||||||

RORWA (Net income/average risk-weighted assets) | 0.90 | 0.91 | 0.70 | |||||||||||||

Efficiency ratio | 51.3 | 52.3 | 49.3 | |||||||||||||

Cost of risk | 1.25 | 1.59 | 2.15 | |||||||||||||

NPA ratio | 5.8 | 6.8 | 5.1 | |||||||||||||

NPA coverage ratio | 64 | 60 | 72 | |||||||||||||

Capital adequacy ratios (%)(1) | ||||||||||||||||

Core capital | 12.0 | 11.6 | 10.8 | |||||||||||||

Tier I | 12.0 | 12.2 | 10.8 | |||||||||||||

BIS II Ratio | 15.1 | 14.9 | 13.0 | |||||||||||||

Other information | ||||||||||||||||

Number of shares (millions) | 6,171 | 6.7 | 5,786 | 5,449 | ||||||||||||

Number of shareholders | 960,397 | (1.4 | ) | 974,395 | 1,012,864 | |||||||||||

Number of employees(2) | 108,770 | (0.5 | ) | 109,305 | 115,852 | |||||||||||

Number of branches(2) | 7,371 | (0.7 | ) | 7,420 | 7,878 | |||||||||||

Number of ATMs(2) | 22,104 | 8.3 | 20,415 | 20,177 | ||||||||||||

Memorandum item: this quarterly information has not been audited. The consolidated accounts of the BBVA Group have been drawn up according to the International Financial Reporting Standards (IFRS) adopted by the European Union and in accordance with Bank of Spain Circular 4/2004 and with its subsequent amendments. As regards the stake in the Garanti Group, the information is presented as in previous periods and consolidated in proportion to the percentage of the Group’s stake. See pages 47 and 48 for the reconciliation of the BBVA Group’s financial statements.

| (1) | The capital ratios in 2014 have been calculated under the Basel III phased-in regulations. For previous periods, the calculation was done in accordance with the Basel II regulations in force at the time. |

| (2) | Excluding Garanti. |

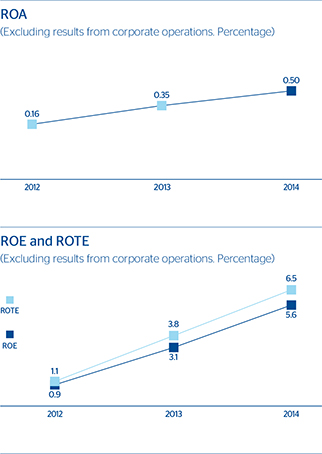

Information about the net attributable profit (excluding results from corporate operations)(1) | 31-12-14 | D% | 31-12-13 | 31-12-12 | ||||||||||||

Net attributable profit | 2,618 | 86.4 | 1,405 | 373 | ||||||||||||

Net attributable profit per share (euros) | 0.44 | 83.6 | 0.24 | 0.08 | ||||||||||||

ROE | 5.6 | 3.1 | 0.9 | |||||||||||||

ROTE | 6.5 | 3.8 | 1.1 | |||||||||||||

ROA | 0.50 | 0.35 | 0.16 | |||||||||||||

RORWA | 0.90 | 0.66 | 0.31 | |||||||||||||

| (1) | In 2013 and 2012 the figures include the results from the pension business in Latin America, including the capital gains from their sale; the capital gains from the sale of BBVA Panama; the capital gains generated by the reinsurance operation on the individual life and accident insurance portfolio in Spain; the equity-accounted earnings from CNCB (excluding dividends), together with the effect of the mark-to-market valuation of BBVA’s stake in CNCB following the agreement concluded with the CITIC group, which included the sale of 5.1% of CNCB. |

| 2 | BBVA Group Highlights |

Table of Contents

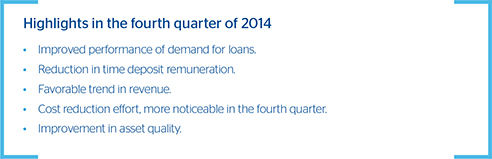

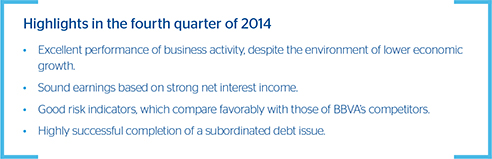

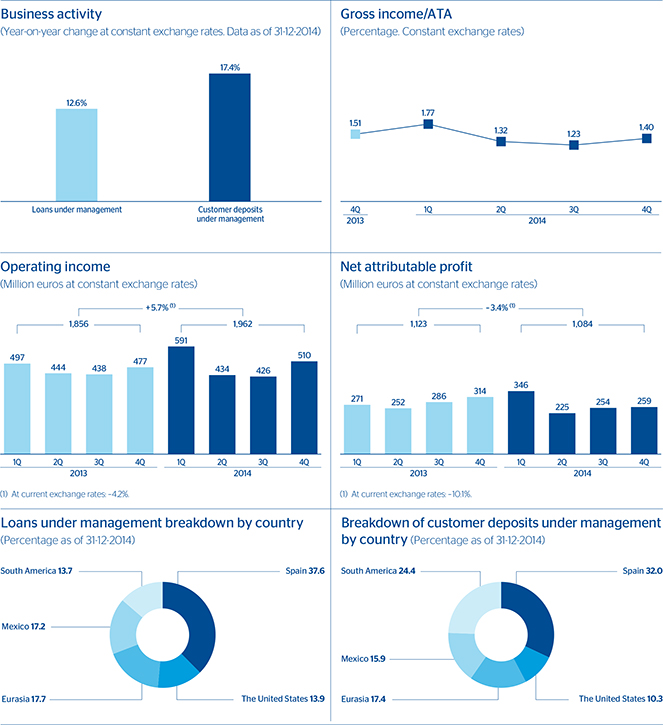

Thefourth quarter of 2014 has been generally favorable for BBVA across our global footprint.

| 1. | Theexchange rates of most currencies have continued to recover against the euro (except for the Mexican and Colombian pesos) and their cumulative negative effect over the last 12 months has moderated further. |

| 2. | From the point of view ofearnings, it has been a very positive quarter, with net income from ongoing operations growing 9.8% on the previous quarter and 41.7% compared with the figure for the same period in 2013. The excellent performance of gross income, strongly supported by recurring revenue and net trading income (NTI) largely explains this trend, although moderate cost growth has also been a positive influence. However, the figure for provisions (net) and other gains/losses is more negative over the quarter, mainly as a result of the increased restructuring costs announced in previous quarters. Nevertheless, net attributable profit in 2014 stands at €2,618m, up 17.5% year-on-year (42.5% at constant exchange rates), despite the fact that a positive figure of €823m was registered in 2013 from corporate operations. |

| 3. | With respect tobusiness activity, the level of production of new loans was very positive in practically all the geographical areas in which BBVA operates. This is particularly notable in Spain, and has limited the decline in the balance of loans managed by the area compared with previous periods. |

| 4. | As regardsliquidity, the situation of the wholesale funding markets has remained favorable and BBVA and its franchises have continued to have access to the market. In addition, the new targeted longer-term refinancing operations (TLTRO) program announced by the European Central Bank (ECB) and the increased proportion of retail deposits continue to strengthen the Group’s liquidity position and improve its funding structure. BBVA borrowed €2.6 billion at the TLTRO auction held in December. |

| 5. | Insolvency, BBVA has increased its phased-in and fully-loaded capital ratios, thanks to the organic generation of earnings and the capital increases completed during the period (one to implement the “dividend option” in October and the other through an accelerated bookbuilt offering of shares among qualified investors in November). As a result, BBVA continues to maintain its capital levels well above the minimum regulatory requirements. The leverage ratio (fully-loaded) stands at 5.9%, a percentage that continues to compare very favorably with its peer group. |

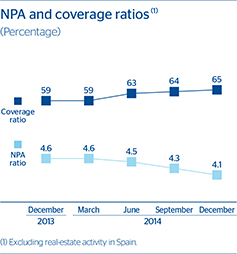

| 6. | The mainrisk indicators have continued to improve, with a 29 basis-point reduction in the Group’s NPA ratio over the last three months to 5.8%. This is due to a further decline in the non-performing portfolio and the increase in total risks. The coverage ratio has also improved to 64%, as has the cost of risk, which for the year to December 2014 fell 34 basis points in year-on-year terms and stands at 1.25%. |

| 7. | Other highlights in the period, apart from the capital increase completed in November and mentioned in the solvency paragraph, include: |

| • | The announcement of severalcorporate operations, which are expected to be closed in the first half of 2015. |

| • | Agreement to increase by 14.89% the stake in Garanti (November) to 39.9%. This operation gives BBVA a majority position on the Board of Directors of Garanti. |

| • | The sale agreement in December of the 29.68% holding in Citic International Financial Holdings Ltd. (CIFH) to China Citic Bank (CNCB). The disposal of this asset will improve even further the Group’s fully-loaded CET 1 (Common Equity Tier 1) capital position. |

| • | Agreement for the sale in January 2015 of a 4.9% stake in CNCB. This operation will also have a positive impact on the bank’s fully-loaded CET 1 ratio. |

| • | With respect toshareholder remuneration, a new capital increase was carried out in December to implement the “dividend option”. On this occasion, the holders of 86.0% of the free allocation rights chose to receive new shares, which once more demonstrates the success of this remuneration system. |

| • | Lastly, BBVA continues to make progress with itsdigital transformation process. Moreover, the year 2014 ends with 9 million digital customers who interact with the Entity via the Internet or cell phone. Of these, 4.2 million are mobile banking customers. In addition, is worth mentioning the acquisition of Madiva Soluciones, a Spanish startup specializing in services based on Big Data and cloud computing. |

| Relevant events | 3 |

Table of Contents

As a result of the adoption of the IFRIC 21 Interpretation on levies issued by the IFRS Interpretation Committee, the accounting policy related to the contributions made to the Deposit Guarantee Fund in Spain was amended in 2014. This change entails that levies are booked when the payment obligation is produced, regardless of when the actual payment is done. In accordance with the International Accounting Standards, this change has been applied retroactively, and therefore certain amounts from previous years have been re-expressed, exclusively for comparison purposes. The main effect of this amendment is that, with respect to the previously published income statements for the year 2013, the amount of the “other operating income and expenses” heading has been modified and, consequently, changes have also been made to the “gross income”, “operating income”, “income before tax”, “net income from ongoing operations”, “net income” and the Group’s “net attributable profit” headings. In 2013, “net attributable profit” would be €2,084m, instead of the €2,228m published under the previous regulations. Additionally, the

Group’s total equity in 2013 would change from €44,850m published with the previous regulation to €44,565m. However, in the explanations contained in this quarterly information, the 2013 figures have been maintained as presented previously, in order to isolate the effect of the aforementioned modification on the year-on-year variations in the various income headings. Pages 47 and 48 of this document present a reconciliation between the Group’s financial statements presented in this quarterly information and the audited financial statements.

The Group’s earnings in thefourth quarter of 2014 have been very favorable, with the main headings continuing the trend observed throughout the year. Their most relevant features are summarized below:

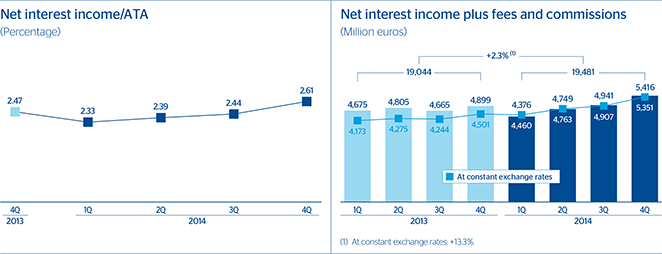

| 1. | Another upturn inrecurring revenue, registering the best quarterly figure of the year, thanks to growth in net interest income in all the geographical areas and high income from fees and commissions. |

Consolidated income statement: quarterly evolution(1)

(Million euros)

| 2014 | 2013 | |||||||||||||||||||||||||||||||

| 4Q | 3Q | 2Q | 1Q | 4Q | 3Q | 2Q | 1Q | |||||||||||||||||||||||||

Net interest income | 4,248 | 3,830 | 3,647 | 3,391 | 3,760 | 3,551 | 3,679 | 3,623 | ||||||||||||||||||||||||

Net fees and commissions | 1,168 | 1,111 | 1,101 | 985 | 1,139 | 1,114 | 1,126 | 1,052 | ||||||||||||||||||||||||

Net trading income | 514 | 444 | 426 | 751 | 609 | 569 | 630 | 719 | ||||||||||||||||||||||||

Dividend income | 119 | 42 | 342 | 29 | 114 | 56 | 176 | 19 | ||||||||||||||||||||||||

Income by the equity method | 3 | 31 | 16 | (14 | ) | 53 | 9 | 11 | (1 | ) | ||||||||||||||||||||||

Other operating income and expenses | (287 | ) | (234 | ) | (215 | ) | (90 | ) | (353 | ) | (113 | ) | (153 | ) | 7 | |||||||||||||||||

Gross income | 5,765 | 5,223 | 5,317 | 5,051 | 5,321 | 5,186 | 5,470 | 5,419 | ||||||||||||||||||||||||

Operating expenses | (2,905 | ) | (2,770 | ) | (2,662 | ) | (2,613 | ) | (2,852 | ) | (2,777 | ) | (2,814 | ) | (2,758 | ) | ||||||||||||||||

Personnel expenses | (1,438 | ) | (1,438 | ) | (1,359 | ) | (1,375 | ) | (1,423 | ) | (1,452 | ) | (1,454 | ) | (1,458 | ) | ||||||||||||||||

General and administrative expenses | (1,147 | ) | (1,037 | ) | (1,017 | ) | (959 | ) | (1,134 | ) | (1,042 | ) | (1,080 | ) | (1,025 | ) | ||||||||||||||||

Depreciation and amortization | (320 | ) | (296 | ) | (286 | ) | (279 | ) | (295 | ) | (283 | ) | (279 | ) | (276 | ) | ||||||||||||||||

Operating income | 2,860 | 2,453 | 2,655 | 2,438 | 2,469 | 2,410 | 2,656 | 2,661 | ||||||||||||||||||||||||

Impairment on financial assets (net) | (1,168 | ) | (1,142 | ) | (1,073 | ) | (1,103 | ) | (1,210 | ) | (1,854 | ) | (1,336 | ) | (1,376 | ) | ||||||||||||||||

Provisions (net) | (513 | ) | (199 | ) | (298 | ) | (144 | ) | (196 | ) | (137 | ) | (130 | ) | (167 | ) | ||||||||||||||||

Other gains (losses) | (201 | ) | (136 | ) | (191 | ) | (173 | ) | (382 | ) | (198 | ) | (172 | ) | (287 | ) | ||||||||||||||||

Income before tax | 978 | 976 | 1,092 | 1,017 | 682 | 221 | 1,017 | 831 | ||||||||||||||||||||||||

Income tax | (173 | ) | (243 | ) | (292 | ) | (273 | ) | (114 | ) | (13 | ) | (261 | ) | (205 | ) | ||||||||||||||||

Net income from ongoing operations | 805 | 733 | 800 | 744 | 568 | 208 | 756 | 626 | ||||||||||||||||||||||||

Results from corporate operations | — | — | — | — | (1,245 | ) | 160 | 593 | 1,315 | |||||||||||||||||||||||

Net income | 805 | 733 | 800 | 744 | (677 | ) | 368 | 1,349 | 1,941 | |||||||||||||||||||||||

Non-controlling interests | (116 | ) | (132 | ) | (95 | ) | (120 | ) | (172 | ) | (172 | ) | (202 | ) | (206 | ) | ||||||||||||||||

Net attributable profit | 689 | 601 | 704 | 624 | (849 | ) | 195 | 1,147 | 1,734 | |||||||||||||||||||||||

Net attributable profit (excluding results from corporate operations)(2) | 689 | 601 | 704 | 624 | 396 | 35 | 554 | 420 | ||||||||||||||||||||||||

Basic earnings per share (euros) | 0.11 | 0.10 | 0.12 | 0.10 | (0.14 | ) | 0.03 | 0.19 | 0.29 | |||||||||||||||||||||||

Basic earnings per share (excluding results from corporate operations) (euros)(2) | 0.11 | 0.10 | 0.12 | 0.10 | 0.07 | 0.01 | 0.09 | 0.07 | ||||||||||||||||||||||||

| (1) | Pro forma financial statements with the revenues and expenses of the Garanti Group consolidated in proportion to the percentage of the Group’s stake. |

| (2) | In 2013 the figures include the results from the pension business in Latin America, including the capital gains from their sale; the capital gains from the sale of BBVA Panama; the capital gains generated by the reinsurance operation on the individual life and accident insurance portfolio in Spain; the equity-accounted earnings from CNCB (excluding dividends), together with the effect of the mark-to-market valuation of BBVA’s stake in CNCB following the agreement concluded with the CITIC group, which included the sale of 5.1% of CNCB. |

| 4 | Group information |

Table of Contents

Consolidated income statement(1)

(Million euros)

| 2014 | D% | D% at constant exchange rates | 2013 | |||||||||||||

Net interest income | 15,116 | 3.4 | 15.6 | 14,613 | ||||||||||||

Net fees and commissions | 4,365 | (1.5 | ) | 6.1 | 4,431 | |||||||||||

Net trading income | 2,135 | (15.5 | ) | (7.0 | ) | 2,527 | ||||||||||

Dividend income | 531 | 45.5 | 46.7 | 365 | ||||||||||||

Income by the equity method | 35 | (51.9 | ) | (48.1 | ) | 72 | ||||||||||

Other operating income and expenses | (826 | ) | 34.8 | 260.3 | (612 | ) | ||||||||||

Gross income | 21,357 | (0.2 | ) | 8.5 | 21,397 | |||||||||||

Operating expenses | (10,951 | ) | (2.2 | ) | 4.3 | (11,201 | ) | |||||||||

Personnel expenses | (5,609 | ) | (3.1 | ) | 2.7 | (5,788 | ) | |||||||||

General and administrative expenses | �� | (4,161 | ) | (2.8 | ) | 5.1 | (4,280 | ) | ||||||||

Depreciation and amortization | (1,180 | ) | 4.2 | 9.9 | (1,133 | ) | ||||||||||

Operating income | 10,406 | 2.1 | 13.2 | 10,196 | ||||||||||||

Impairment on financial assets (net) | (4,486 | ) | (22.3 | ) | (19.2 | ) | (5,776 | ) | ||||||||

Provisions (net) | (1,155 | ) | 83.4 | 108.4 | (630 | ) | ||||||||||

Other gains (losses) | (701 | ) | (32.5 | ) | (32.1 | ) | (1,040 | ) | ||||||||

Income before tax | 4,063 | 47.7 | 97.9 | 2,750 | ||||||||||||

Income tax | (981 | ) | 65.5 | 118.8 | (593 | ) | ||||||||||

Net income from ongoing operations | 3,082 | 42.8 | 92.1 | 2,158 | ||||||||||||

Results from corporate operations | — | — | — | 823 | ||||||||||||

Net income | 3,082 | 3.4 | 27.6 | 2,981 | ||||||||||||

Non-controlling interests | (464 | ) | (38.4 | ) | (19.8 | ) | (753 | ) | ||||||||

Net attributable profit | 2,618 | 17.5 | 42.5 | 2,228 | ||||||||||||

Net attributable profit (excluding results from corporate operations)(2) | 2,618 | 86.4 | 155.1 | 1,405 | ||||||||||||

Basic earnings per share (euros) | 0.44 | 0.38 | ||||||||||||||

Basic earnings per share (excluding results from corporate operations) (euros)(2) | 0.44 | 0.24 | ||||||||||||||

| (1) | Pro forma financial statements with the revenues and expenses of the Garanti Group consolidated in proportion to the percentage of the Group’s stake. |

| (2) | In 2013 the figures include the results from the pension business in Latin America, including the capital gains from their sale; the capital gains from the sale of BBVA Panama; the capital gains generated by the reinsurance operation on the individual life and accident insurance portfolio in Spain; the equity-accounted earnings from CNCB (excluding dividends), together with the effect of the mark-to-market valuation of BBVA’s stake in CNCB following the agreement concluded with the CITIC group, which included the sale of 5.1% of CNCB. |

| 2. | The figures forNTI have also been positive, largely as a result of the capital gains generated from the sale of the ALCO (Assets and Liabilities Committee) portfolio and the recovery of European markets after a modest third quarter. |

| 3. | Accounting for thedividend from Telefónica. |

| 4. | Under theother operating income and expenses heading, a very negative adjustment for hyperinflation in Venezuela in the quarter and accounting for the Tax on Deposits in Financial Institutions (IDEC) in Spain. Both charges are partially offset by the positive performance of insurance activities over the period. |

| 5. | Moderate growth inoperating expenses, above all because they have been kept firmly in check in Spain and the Corporate Center. |

| 6. | Impairment losses on financial assets similar to the third quarter. |

| 7. | Provisions (net) and other gains (losses) have been more negative in the quarter, due mainly to higher restructuring costs, in line with what was announced in the third quarter. |

| 8. | Overall,net income from ongoing operations from October to December amounted to €805m, the highest figure in 2014, and well above the €568m reported in the same period in 2013. |

| 9. | Recovery in theexchange rates of most of the currencies against the euro, except for the Mexican and Colombian peso. |

Gross income

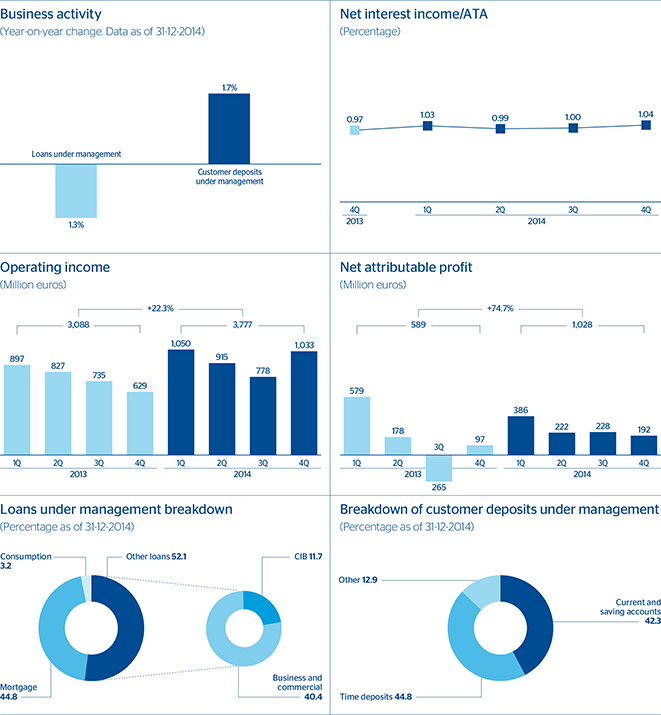

As mentioned above, one of the most notable elements in the fourth quarter has been the increase innet interestincome across BBVA’s global footprint. In Spain, the increase is mainly the result of the decline in the cost of deposits, although it is also influenced by the lower level of deleveraging. In Turkey and Mexico, the key has been the quarterly growth in activity and the increased contribution from the securities portfolio. In the United States, there has also been a positive effect from the strength of business activity, in a quarter where the narrowing of spreads has been far less pronounced. Lastly, in South America, the increase is supported by growing business volumes and improved spreads. As a result of the above factors, net interest income from October to December has been 10.9% higher than in the third quarter and 13.0% higher than in the same period in 2013. For the year as a whole, net interest income stands at €15,116m, up 3.4% on the figure for 2013, or 15.6% excluding the negative impact of exchange rates.

| Earnings | 5 |

Table of Contents

The trend inincome from fees and commissions has also been positive in the quarter. In Spain, the improvement is largely due to the strong activity in the Group’s wholesale banking businesses, as is the case in the United States. In the other geographical areas, this positive performance is very closely related to the increased banking activity mentioned above. As a result, the cumulative income from fees and commissions decreased by 1.5% in 2014. This is below the figure for the previous year, but excluding the negative currency effect, the rise is 6.1%. It should be noted that this growth has been affected by certain regulatory constraints. In the case of Spain, they include certain regulations limiting revenue from credit cards and pension fund management.

Overall,more recurring revenue has performed very well. The cumulative total for 2014 increased by 2.3% year-on-year (13.3% at constant exchange rates).

At €2,135m,NTI is below last year’s figure. It should be noted that the figure for the fourth quarter includes capital gains generated by the sale of the ALCO portfolios, as well as an increased contribution from the Global Markets unit in the different geographical areas.

The figure fordividends in the quarter includes those from the Group’s stake in Telefónica.

Income by the equity method basically includes income from the Group’s stake in the Chinese entity CIFH until the month of November.

Breakdown of yields and costs

| 4Q14 | 3Q14 | 2Q14 | 1Q14 | 4Q13 | ||||||||||||||||||||||||||||||||||||

| % of ATA | % yield/ Cost | % of ATA | % yield/ Cost | % of ATA | % yield/ Cost | % of ATA | % yield/ Cost | % of ATA | % yield/ Cost | |||||||||||||||||||||||||||||||

Cash and balances with central banks | 4.4 | 0.49 | 3.9 | 0.40 | 4.6 | 0.51 | 4.5 | 0.56 | 4.8 | 0.57 | ||||||||||||||||||||||||||||||

Financial assets and derivatives | 29.2 | 2.65 | 29.1 | 2.56 | 28.7 | 2.68 | 27.5 | 2.89 | 26.7 | 3.04 | ||||||||||||||||||||||||||||||

Loans and advances to credit institutions | 4.3 | 1.01 | 4.4 | 1.10 | 4.1 | 1.24 | 3.9 | 1.53 | 4.5 | 1.98 | ||||||||||||||||||||||||||||||

Loans and advances to customers | 54.3 | 5.81 | 54.8 | 5.51 | 54.9 | 5.54 | 56.2 | 5.34 | 56.2 | 5.63 | ||||||||||||||||||||||||||||||

Euros | 28.7 | 2.46 | 30.0 | 2.52 | 31.1 | 2.63 | 32.4 | 2.68 | 32.6 | 2.62 | ||||||||||||||||||||||||||||||

Foreign currencies | 25.5 | 9.58 | 24.7 | 9.15 | 23.8 | 9.33 | 23.8 | 8.95 | 23.6 | 9.80 | ||||||||||||||||||||||||||||||

Other assets | 7.8 | 0.54 | 7.9 | 0.50 | 7.7 | 0.40 | 7.8 | 0.48 | 7.9 | 0.29 | ||||||||||||||||||||||||||||||

Total assets | 100.0 | 4.04 | 100.0 | 3.87 | 100.0 | 3.91 | 100.0 | 3.92 | 100.0 | 4.11 | ||||||||||||||||||||||||||||||

Deposits from central banks and credit institutions | 14.6 | 1.64 | 12.9 | 1.74 | 13.9 | 1.89 | 14.2 | 1.80 | 14.5 | 1.82 | ||||||||||||||||||||||||||||||

Deposits from customers | 50.9 | 1.43 | 52.1 | 1.45 | 51.4 | 1.57 | 51.2 | 1.60 | 50.7 | 1.65 | ||||||||||||||||||||||||||||||

Euros | 25.2 | 0.87 | 26.7 | 0.98 | 26.7 | 1.14 | 26.8 | 1.28 | 26.3 | 1.20 | ||||||||||||||||||||||||||||||

Foreign currencies | 25.7 | 1.97 | 25.4 | 1.94 | 24.7 | 2.03 | 24.4 | 1.95 | 25.2 | 1.75 | ||||||||||||||||||||||||||||||

Debt certificates and subordinated liabilities | 12.5 | 2.25 | 13.2 | 2.24 | 13.7 | 2.36 | 13.9 | 2.40 | 14.0 | 2.63 | ||||||||||||||||||||||||||||||

Other liabilities | 14.1 | 1.28 | 14.1 | 1.10 | 13.5 | 1.00 | 13.1 | 1.33 | 13.1 | 1.28 | ||||||||||||||||||||||||||||||

Equity | 7.8 | — | 7.6 | — | 7.5 | — | 7.5 | — | 7.6 | — | ||||||||||||||||||||||||||||||

Total liabilities and equity | 100.0 | 1.43 | 100.0 | 1.43 | 100.0 | 1.53 | 100.0 | 1.59 | 100.0 | 1.64 | ||||||||||||||||||||||||||||||

Net interest income/average total assets (ATA) | 2.61 | 2.44 | 2.39 | 2.33 | 2.47 | |||||||||||||||||||||||||||||||||||

| 6 | Group information |

Table of Contents

Lastly,other operating income and expenses for the quarter includes an adjustment for hyperinflation in Venezuela that is more negative than in previous periods, as well as the aforementioned charge for payment of the IDEC deposit tax in Spain. It is important to remember that in the fourth quarter of 2013 this heading included the extraordinary payment to the Deposit Guarantee Fund in Spain in compliance with Royal Decree-Law 6/2013.

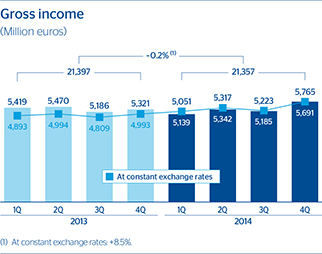

In short, BBVA generatedgross income for the quarter of €5,765m, the highest figure in the last two years. For the year as a whole, gross income amounted to €21,357m, a similar amount to 2013 at current exchange rates, but 8.5% higher at constant exchange rates.

Operating income

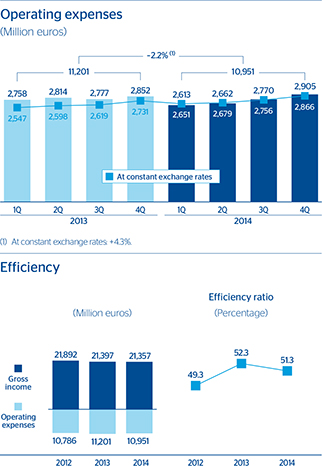

Operating expenses for the quarter stand at €2,905m, giving a cumulative figure for 2014 of €10,951m, 2.2% below the figure for 2013 (although up 4.3% at constant exchange rates), despite the effect of high inflation in some countries (Venezuela and Argentina) and the digital transformation plans being implemented by the Group. By geographical area, there has

been a year-on-year reduction in operating expenses in Spain and in the rest of Europe; they were held in check in the United States (despite the impact of the incorporation of Simple); and they grew, as expected, in the rest of the geographical areas.

Breakdown of operating expenses and efficiency calculation

(Million euros)

| 2014 | D% | 2013 | ||||||||||

Personnel expenses | 5,609 | (3.1 | ) | 5,788 | ||||||||

Wages and salaries | 4,268 | (2.8 | ) | 4,392 | ||||||||

Employee welfare expenses | 826 | (4.6 | ) | 866 | ||||||||

Training expenses and other | 515 | (2.7 | ) | 530 | ||||||||

General and administrative expenses | 4,161 | (2.8 | ) | 4,280 | ||||||||

Premises | 963 | (0.4 | ) | 966 | ||||||||

IT | 831 | 3.8 | 801 | |||||||||

Communications | 288 | (8.0 | ) | 313 | ||||||||

Advertising and publicity | 346 | (11.3 | ) | 391 | ||||||||

Corporate expenses | 103 | (2.6 | ) | 106 | ||||||||

Other expenses | 1,194 | (5.8 | ) | 1,268 | ||||||||

Levies and taxes | 437 | 0.1 | 437 | |||||||||

Administration expenses | 9,771 | (3.0 | ) | 10,068 | ||||||||

Depreciation and amortization | 1,180 | 4.2 | 1,133 | |||||||||

Operating expenses | 10,951 | (2.2 | ) | 11,201 | ||||||||

Gross income | 21,357 | (0.2 | ) | 21,397 | ||||||||

Efficiency ratio (Operating expenses/gross income, in %) | 51.3 | 52.3 | ||||||||||

| Earnings | 7 |

Table of Contents

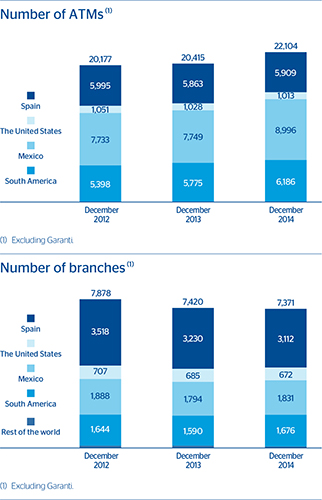

The number ofATMs continues to grow. It has done so in practically all the geographical areas over the quarter. In contrast, the number ofbranch offices has fallen, as a result of the boost to alternative channels.

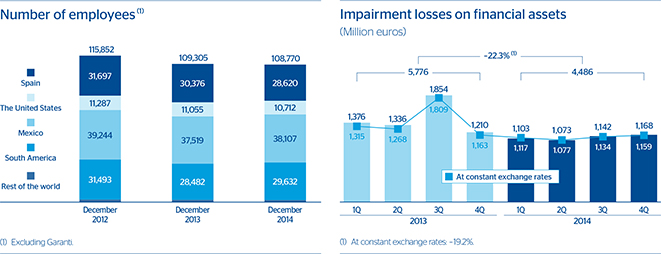

With respect to theworkforce, the number of employees in the Group stood at 108,770 as of 31-Dec-2014. This figure is practically the same as at the close of September (108,920) and 0.5% below the figure for the close of 2013. By geographical area, the numbers continued to fall in Spain and in the United States, while there were new hirings in the rest of the areas.

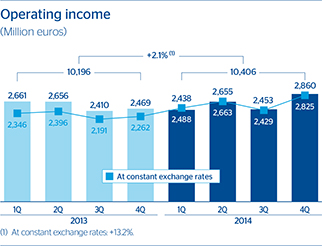

For 2014 as a whole, the year-on-year increase in expenses has been below that of gross income, thus improving the efficiency ratio to 51.3% from the figure of 52.3% in 2013, and boostingoperating income to €10,406m, a year-on-year increase of 2.1%, or 13.2% excluding the impact of exchange rates.

Provisions and others

Impairment losses on financial assets for the last three months of the year are similar to those booked between June and September 2014, so the cumulative total for the year amounts to €4,486m. This figure represents a year-on-year decline of 22.3% (down 19.2% at constant exchange rates), due largely to its steady return to normal in Spain. The Group’s cumulative cost of risk in 2014 closed at 1.25%, compared with 1.59% the previous year.

Provisions include items such as restructuring costs, provisions for contingent liabilities and contributions to pension funds. In the last quarter, this heading includes a greater volume of restructuring costs associated with the digitization and transformation process underway in the Group, in line with the announcement made in the third quarter.

| 8 | Group information |

Table of Contents

The main component ofother gains (losses) is the provisions for real-estate and foreclosed or acquired assets in Spain, which in 2014 have declined year-on-year by 32.5% (down 32.1% at constant exchange rates).

As a result of the above,net income from ongoing operations in the year grew year-on-year by 42.8% (up 92.1% at constant exchange rates).

Lastly, no transaction has been recorded in 2014 under theresults from corporate operations heading, unlike the case in 2013, when it included the following items: the reinsurance operation on the individual life-risk insurance portfolio in Spain (first quarter); the earnings from the Group’s pension business in Latin America (including the capital gains from the sale of the Afore pension manager in Mexico in the first quarter, the pension fund administrators in Colombia and Peru in the second quarter and the pension fund administrator in Chile in the fourth quarter); the capital gains from the sale of BBVA Panama (fourth quarter); and, lastly, the effect of the signing of the agreement with CITIC Limited (fourth quarter), which involved the disposal of 5.1% of CNCB, valuing BBVA’s entire stake in CNCB at mark-to-market (fourth quarter). The equity-accounted income (excluding dividends) of CNCB had been included in the first, second and third quarters of 2013.

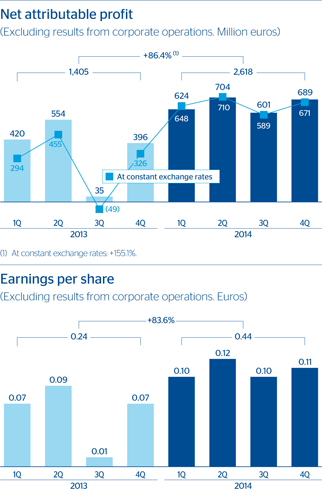

Net attributable profit

BBVA’snet attributable profit in 2014 stands at €2,618m, up 17.5% on the figure for 2013 (up 42.5% at constant exchange rates), despite the fact that in 2013 earnings for an amount of €823m were registered from the corporate operations mentioned in the above paragraph.

Bybusiness area, banking activity in Spain has contributed €1,028m, real-estate activity in Spain generated a loss of €876m, while the United States contributed €428m, Eurasia €565m, Mexico €1,915m and South America €1,001m.

| Earnings | 9 |

Table of Contents

Balance sheet and business activity

The Group’s balance sheet and business activity in thelast quarter of 2014 was marked by:

| • | Theexchange-rate gains against the euro of the main currencies that have an influence on the Group’s financial statements, except for the Mexican and Colombian peso, which depreciated by 4.9% and 12.2%, respectively, between October and December. Over the last 12 months, the appreciation of the Mexican peso, U.S. dollar, Peruvian new sol and Turkish lira has had a positive effect on the year-on-year changes in the headings of the Group’s balance sheet and its business activity. |

| • | Faster growth ingross lending to customers, which at the close of the year was up 1.5% in the quarter and 4.7% over the year as a whole, at current exchange rates. As regards performance by area, the deleveraging process has slowed in Spain, thanks to the recovery of the production of new loans, while in the United States, Mexico, Turkey and South America the loan book has grown at double-digit year-on-year growth rates. |

Consolidated balance sheet(1)

(Million euros)

| 31-12-14 | D% | 31-12-13 | 30-09-14 | |||||||||||||

Cash and balances with central banks | 33,908 | (8.5 | ) | 37,064 | 23,121 | |||||||||||

Financial assets held for trading | 83,427 | 15.4 | 72,301 | 88,023 | ||||||||||||

Other financial assets designated at fair value | 3,236 | 18.3 | 2,734 | 3,227 | ||||||||||||

Available-for-sale financial assets | 98,734 | 22.1 | 80,848 | 98,322 | ||||||||||||

Loans and receivables | 386,839 | 6.4 | 363,575 | 379,715 | ||||||||||||

Loans and advances to credit institutions | 28,254 | 16.7 | 24,203 | 27,561 | ||||||||||||

Loans and advances to customers | 351,755 | 5.1 | 334,744 | 346,103 | ||||||||||||

Debt securities | 6,831 | 47.6 | 4,628 | 6,051 | ||||||||||||

Held-to-maturity investments | — | — | — | — | ||||||||||||

Investments in entities accounted for using the equity method | 661 | (55.8 | ) | 1,497 | 1,443 | |||||||||||

Tangible assets | 8,014 | 3.8 | 7,723 | 7,762 | ||||||||||||

Intangible assets | 8,840 | 8.3 | 8,165 | 8,621 | ||||||||||||

Other assets | 27,851 | 8.7 | 25,611 | 27,465 | ||||||||||||

Total assets | 651,511 | 8.7 | 599,517 | 637,699 | ||||||||||||

Financial liabilities held for trading | 56,990 | 24.5 | 45,782 | 59,084 | ||||||||||||

Other financial liabilities designated at fair value | 3,590 | 29.5 | 2,772 | 3,615 | ||||||||||||

Financial liabilities at amortized cost | 509,974 | 6.2 | 480,307 | 497,179 | ||||||||||||

Deposits from central banks and credit institutions | 97,735 | 11.4 | 87,746 | 84,199 | ||||||||||||

Deposits from customers | 330,686 | 6.6 | 310,176 | 329,610 | ||||||||||||

Debt certificates | 59,393 | (9.3 | ) | 65,497 | 61,181 | |||||||||||

Subordinated liabilities | 14,118 | 33.5 | 10,579 | 14,265 | ||||||||||||

Other financial liabilities | 8,042 | 27.5 | 6,309 | 7,923 | ||||||||||||

Liabilities under insurance contracts | 10,471 | 6.4 | 9,844 | 10,624 | ||||||||||||

Other liabilities | 18,877 | 18.3 | 15,962 | 18,808 | ||||||||||||

Total liabilities | 599,902 | 8.2 | 554,667 | 589,310 | ||||||||||||

Non-controlling interests | 2,511 | 5.9 | 2,371 | 2,253 | ||||||||||||

Valuation adjustments | (348 | ) | (90.9 | ) | (3,831 | ) | (879 | ) | ||||||||

Shareholders’ funds | 49,446 | 6.8 | 46,310 | 47,015 | ||||||||||||

Total equity | 51,609 | 15.1 | 44,850 | 48,389 | ||||||||||||

Total equity and liabilities | 651,511 | 8.7 | 599,517 | 637,699 | ||||||||||||

Memorandum item: | ||||||||||||||||

Contingent liabilities | 37,070 | 1.7 | 36,437 | 36,864 | ||||||||||||

| (1) | Pro forma financial statements with the assets and liabilities of the Garanti Group consolidated in proportion to the percentage of the Group’s stake. |

| 10 | Group information |

Table of Contents

| • | Non-performing loans have continued to decline throughout the year, although at a faster pace in the second half. The steepest declines have been registered in Spain. Non-performing assets fell 3.4% in the quarter and 10.3% over the year, also at current exchange rates. |

| • | Customer deposits closed December at a similar level to 30-Sep-2014 and are up 6.6% over the year as a whole, at current exchange rates. This heading continues to perform well in the non-domestic sector. In the domestic sector it is down in time deposits and in the public sector segment. This decline is the result of the reduction in the cost of time deposits, which has led to a transfer of money to current and savings accounts and to mutual and pension funds. |

Loans and advances to customers

(Million euros)

| 31-12-14 | D% | 31-12-13 | 30-09-14 | |||||||||||||

Domestic sector | 162,652 | (3.0 | ) | 167,670 | 162,301 | |||||||||||

Public sector | 23,362 | 5.6 | 22,128 | 23,302 | ||||||||||||

Other domestic sectors | 139,290 | (4.3 | ) | 145,542 | 138,999 | |||||||||||

Secured loans | 87,371 | (6.5 | ) | 93,446 | 88,880 | |||||||||||

Other loans | 51,920 | (0.3 | ) | 52,095 | 50,119 | |||||||||||

Non-domestic sector | 180,719 | 15.4 | 156,615 | 174,800 | ||||||||||||

Secured loans | 72,836 | 16.7 | 62,401 | 71,063 | ||||||||||||

Other loans | 107,883 | 14.5 | 94,214 | 103,737 | ||||||||||||

Non-performing loans | 23,164 | (10.3 | ) | 25,826 | 23,983 | |||||||||||

Domestic sector | 18,563 | (11.5 | ) | 20,985 | 19,243 | |||||||||||

Non-domestic sector | 4,601 | (5.0 | ) | 4,841 | 4,740 | |||||||||||

Loans and advances to customers (gross) | 366,536 | 4.7 | 350,110 | 361,084 | ||||||||||||

Loan-loss provisions | (14,781 | ) | (3.8 | ) | (15,366 | ) | (14,980 | ) | ||||||||

Loans and advances to customers | 351,755 | 5.1 | 334,744 | 346,103 | ||||||||||||

| • | Lastly,off-balance-sheet customer funds continue to perform very favorably, above all in Spain (up 2.4% over the last three months and 17.6% in year-on-year terms), due to the aforementioned transfer of funds; however, their performance has also been positive in the rest of the geographical areas (up 14.1% year-on-year at current exchange rates). |

Customer funds

(Million euros)

| 31-12-14 | D% | 31-12-13 | 30-09-14 | |||||||||||||

Deposits from customers | 330,686 | 6.6 | 310,176 | 329,610 | ||||||||||||

Domestic sector | 145,251 | (3.9 | ) | 151,070 | 150,840 | |||||||||||

Public sector | 10,651 | (26.2 | ) | 14,435 | 16,240 | |||||||||||

Other domestic sectors | 134,600 | (1.5 | ) | 136,635 | 134,600 | |||||||||||

Current and savings accounts | 59,509 | 11.1 | 53,558 | 55,236 | ||||||||||||

Time deposits | 60,783 | (13.1 | ) | 69,977 | 65,636 | |||||||||||

Assets sold under repurchase agreement and other | 14,308 | 9.2 | 13,100 | 13,729 | ||||||||||||

Non-domestic sector | 185,435 | 16.5 | 159,106 | 178,770 | ||||||||||||

Current and savings accounts | 113,795 | 12.1 | 101,515 | 108,154 | ||||||||||||

Time deposits | 62,705 | 27.3 | 49,266 | 60,580 | ||||||||||||

Assets sold under repurchase agreement and other | 8,935 | 7.3 | 8,325 | 10,035 | ||||||||||||

Other customer funds | 115,274 | 16.2 | 99,213 | 114,630 | ||||||||||||

Spain | 69,943 | 17.6 | 59,490 | 68,301 | ||||||||||||

Mutual funds | 28,695 | 28.7 | 22,298 | 27,552 | ||||||||||||

Pension funds | 21,880 | 7.1 | 20,428 | 21,677 | ||||||||||||

Customer portfolios | 19,368 | 15.5 | 16,763 | 19,073 | ||||||||||||

Rest of the world | 45,332 | 14.1 | 39,723 | 46,329 | ||||||||||||

Mutual funds and investment companies | 24,087 | 13.7 | 21,180 | 25,294 | ||||||||||||

Pension funds | 5,484 | 29.5 | 4,234 | 5,079 | ||||||||||||

Customer portfolios | 15,761 | 10.1 | 14,309 | 15,956 | ||||||||||||

Total customer funds | 445,960 | 8.9 | 409,389 | 444,240 | ||||||||||||

| Balance sheet and business activity | 11 |

Table of Contents

In thefourth quarter of 2014, BBVA has continued to carry out active management of its capital. The most relevant events that have influenced the Group’s capital base are as follows:

| • | Acapital increase was completed last November for €2,000m through an accelerated bookbuilt offering targeted at institutional investors, which has strengthened the Group’s capital adequacy ratios by 58 basis points at the date of its execution. |

| • | RWAs stood at €350,588m as of 31-Dec-2014, up 1.5% since the end of September, due basically to exchange-rate movements, increased activity in emerging countries and the United States, and the lower level of deleveraging in Spain as a result of the growth in the production of new loans. |

| • | These two factors, combined with the other factors impacting the capital base (organic growth, variation due to exchange rates and increase in some deductions), have resulted in an increase in the phased-incore capital ratio to 12.0% (10.4% fully-loaded). |

| • | There were no significant changes in the last quarter in theTier II ratio (also phased-in), which stands at 3.2% as of 31-Dec-2014, exactly the same level as in the previous quarter. |

| • | Lastly, as a result of what has been mentioned above, the phased-inBIS III ratio closed the year at 15.1% and the fully-loaded ratio at 14.2%, both well above current regulatory requirements (8.0%). |

In short, BBVA Group continues to manage its solvency ratios appropriately and has a strong capital position that is clearly above regulatory requirements.

Ratings

Following the announcement of the acquisition of the additional 14.89% in Garanti Bank, in November 2014 the main agencies verified BBVA’s rating. The upgrades in the Bank’s ratings in the first half of 2014 have thus been confirmed.

Ratings

Long term | Short term | Outlook | ||||

DBRS | A | R-1 (low) | Negative | |||

Fitch | A– | F-2 | Stable | |||

Moody’s | Baa2 | P-2 | Positive | |||

Scope Ratings | A | S-1 | Stable | |||

Standard & Poor’s | BBB | A-2 | Stable |

Capital base

(Million euros)

| BIS III phased-in | BIS II | |||||||||||||||||||

| 31-12-14 | 30-09-14 | 30-06-14 | 31-03-14 | 31-12-13 | ||||||||||||||||

Core capital | 41,937 | 40,422 | 38,978 | 38,700 | 37,492 | |||||||||||||||

Capital (Tier I) | 41,937 | 40,422 | 38,978 | 38,700 | 39,611 | |||||||||||||||

Other eligible capital (Tier II) | 11,046 | 10,893 | 10,421 | 9,170 | 8,695 | |||||||||||||||

Capital base | 52,983 | 51,316 | 49,399 | 47,870 | 48,306 | |||||||||||||||

Risk-weighted assets | 350,588 | 345,381 | 336,584 | 335,276 | 323,605 | |||||||||||||||

BIS ratio (%) | 15.1 | 14.9 | 14.7 | 14.3 | 14.9 | |||||||||||||||

Core capital (%) | 12.0 | 11.7 | 11.6 | 11.5 | 11.6 | |||||||||||||||

Tier I (%) | 12.0 | 11.7 | 11.6 | 11.5 | 12.2 | |||||||||||||||

Tier II (%) | 3.2 | 3.2 | 3.1 | 2.7 | 2.7 | |||||||||||||||

| 12 | Group information |

Table of Contents

Credit risk

In thelast quarter of 2014 the main variables related to the Group’s credit risk management have been positive, in line with the trend of previous quarters:

| • | The Group’sNPA ratio continued to decline, closing December at 5.8% (including real-estate activity), down from 6.1% in September 2014. This favorable performance cuts across all geographical areas and is due to the declining trend in non-performing assets, combined with an increase in the balance of the loan book. |

| • | The totalcoverage ratio has increased by 142 basis points over the quarter to 64%, also across all the geographical areas. |

Credit risks(1)

(Million euros)

| 31-12-14 | 30-09-14 | 30-06-14 | 31-03-14 | 31-12-13 | ||||||||||||||||

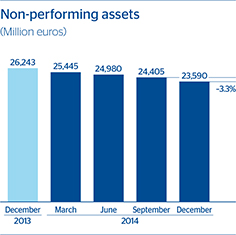

Non-performing assets(2) | 23,590 | 24,405 | 24,980 | 25,445 | 26,243 | |||||||||||||||

Credit risks | 403,633 | 397,952 | 389,355 | 384,577 | 386,401 | |||||||||||||||

Provisions | 15,157 | 15,335 | 15,515 | 15,372 | 15,715 | |||||||||||||||

Specific | 12,169 | 12,436 | 12,750 | 12,752 | 13,030 | |||||||||||||||

Generic and country-risk | 2,988 | 2,899 | 2,765 | 2,620 | 2,684 | |||||||||||||||

NPA ratio (%) | 5.8 | 6.1 | 6.4 | 6.6 | 6.8 | |||||||||||||||

NPA coverage ratio (%) | 64 | 63 | 62 | 60 | 60 | |||||||||||||||

NPA ratio (%) (excluding real-estate activity in Spain) | 4.1 | 4.3 | 4.5 | 4.6 | 4.6 | |||||||||||||||

NPA coverage ratio (%) (excluding real-estate activity in Spain) | 65 | 64 | 63 | 59 | 59 | |||||||||||||||

| (1) | Include gross customer lending plus contingent exposures. |

| (2) | Include non-performing assets originating from lending to customers and contingent liabilities. |

Non-performing assets evolution(1)

(Million euros)

| 4Q14 | 3Q14 | 2Q14 | 1Q14 | 4Q13 | ||||||||||||||||

Beginning balance | 24,405 | 24,980 | 25,445 | 26,243 | 26,508 | |||||||||||||||

Entries | 2,363 | 2,429 | 2,092 | 2,190 | 3,255 | |||||||||||||||

Recoveries | (1,935 | ) | (1,840 | ) | (1,781 | ) | (1,708 | ) | (2,261 | ) | ||||||||||

Net variation | 427 | 589 | 311 | 482 | 993 | |||||||||||||||

Write-offs | (1,248 | ) | (1,297 | ) | (961 | ) | (1,248 | ) | (1,102 | ) | ||||||||||

Exchange rate differences and other | 5 | 133 | 185 | (32 | ) | (155 | ) | |||||||||||||

Period-end balance | 23,590 | 24,405 | 24,980 | 25,445 | 26,243 | |||||||||||||||

Memorandum item: | ||||||||||||||||||||

Non-performing loans | 23,164 | 23,983 | 24,554 | 25,032 | 25,826 | |||||||||||||||

Non-performing contingent liabilities | 426 | 422 | 426 | 413 | 418 | |||||||||||||||

| (1) | Includes non-performing assets originating from lending to customers and contingent liabilities. |

| Risk management | 13 |

Table of Contents

As of 31-Dec-2014, the Group’scredit risk has once more shown an upward movement over the quarter of 1.4% since the end of September. This change has been influenced by strong activity in the Americas and Turkey, as well as the recovery in new production in Spain. Although this recovery is still insufficient to offset the maturities of the current stock of credit, the lending trend is stabilizing.

Non-performing assets once again declined in the quarter, influenced by the reduction in net additions to NPA, due both to the control of gross entries and to increased recoveries with respect to the previous quarter (the ratio of recoveries to gross entries in the quarter has been 81.9% in the fourth quarter).

The Group’sNPA ratio closed 2014 at 5.8% (4.1% excluding real-estate activity in Spain), once again falling 29 basis points over the last three months of the year. The decline was due to the aforementioned reduction in the volume of the non-performing portfolio and the increase in the Group’s credit risk. By area, the ratio in the banking business in Spain stands at 6.0%, with a fall of 20 basis points since September; in real-estate activity in Spain is stable at 55.4%; in Mexico and Eurasia this ratio has improved to 2.9% and to 3.3%, respectively (3.2% for Mexico and 3.4% for Eurasia, with data as of the close of the previous quarter); in South America and in the United States is stable at 2.1% and 0.9% respectively.

Lastly,coverage provisions for customer risk amounted to €15,157m as of 31-Dec-2014, a decline of 1.2% over the quarter. Despite this, and given the aforementioned reduction in the non-performing balances, the Group’s coverage ratio has increased by 142 basis points to 64%. By business area, there has been an increase in the coverage ratio in all the geographical areas: in Spain from 51% to 52% (45% in banking activity and 63% in real-estate activity); in the United States it closed the quarter at 167% (164% in September); in Eurasia it has increased from 91% to 92%; in Mexico to 114% (112% at the close of the third quarter); and in South America it stands at 138% (up from 137% as of 30-Sep-2014).

Structural risks

The Assets and Liabilities Management unit in BBVA’s Strategy and Finance area is responsible for managing the Group’s overall liquidity and structural interest-rate and foreign-exchange positions.

Liquidity and finance management aims to finance the recurring growth of the banking business at suitable maturities and costs, using a wide range of instruments that provide access to a large number of alternative sources of finance. A core principle in BBVA Group’s liquidity and finance management is the financial independence of its banking subsidiaries abroad. This principle prevents the propagation of a liquidity crisis among the Group’s different areas and guarantees correct transmission of the cost of liquidity to the price formation process.

In the fourth quarter of 2014, the liquidity conditions remained comfortable in the euro area. The unconventional measures announced by the ECB at its meeting on June 5, 2014 were followed by a second round in the form of the TLTRO auction of December 2014, at which BBVA borrowed €2.6 billion. The ECB has also launched covered bond purchase programs (CBPP) and asset-backed securities purchase programs (ABSPP). The long-term wholesale funding market in Europe has been stable, thanks to the improvement in sovereign risk premiums and the banking system’s better profile, following the results of the stress tests published this quarter. Short-term funding in Europe has also continued to perform extremely well, in a context marked by a high level of market liquidity. In addition to the above, BBVA’s retail franchise in Spain performed well as a result of its customer-centric strategy and the Entity’s financial soundness.

| 14 | Group information |

Table of Contents

With respect to the Group’s international subsidiaries, the financial soundness of the banks in other jurisdictions is supported by the funding of lending activity basically through the use of customer funds. Of note in this respect is the extraordinary performance of new deposits in Mexico over the year, which has continued into the last quarter. In the case of BBVA Compass, excess liquidity has been the dominant trend over the fourth quarter, despite the demands of lending activity. In both Mexico and the United States, in 2014 BBVA has adapted to the local liquidity coverage ratio (LCR) regulations, which will be binding starting in 2015 for BBVA Bancomer, and in January 2016 in the case of BBVA Compass. With respect to the balance sheets in South America, the liquidity situation has once more been strengthened this quarter by the growth in customer funds and also by bond issues on the respective local markets in Chile, Colombia, Argentina and Paraguay. All these issues have enjoyed an excellent uptake by investors. They have allowed the banks to diversify their sources of finance and demonstrated BBVA’s soundness in the region, as well as the good operation of local markets.

To sum up, BBVA’s proactive policy in its liquidity management, the outstanding performance of customer funds in all geographical areas, its proven ability to access the market, even in difficult environments, its retail business model and the lower volume of maturities compared with its competitors, all give it a comparative advantage against its peers. Moreover, the increased proportion of retail deposits continues to strengthen the Group’s liquidity position and to improve its financing structure.

Foreign-exchange risk management of BBVA’s long-term investments, basically stemming from its franchises abroad, aims to preserve the Group’s capital adequacy ratios and ensure the stability of its income statement.

The fourth quarter of the year saw gains in the dollar against the euro and greater volatility in those emerging currencies affected by the major fall in the oil price. In this context, BBVA has maintained a policy of actively hedging its investments in Mexico, Chile, Colombia, Turkey and the dollar area. In addition to this corporate-level hedging, dollar positions are held at a local level by some of the subsidiary banks. The foreign-exchange risk of the earnings expected from abroad for 2014 is also managed.

The unit also actively manages thestructural interest-rate exposure on the Group’s balance sheet. This aims to maintain a steady growth in net interest income in the short and medium term, regardless of interest-rate fluctuations.

In the fourth quarter of 2014, the results of this management have been very satisfactory, with strategies limiting risk in Europe, the United States and Mexico. These strategies are managed both with hedging derivatives (caps, floors, swaps and FRAs) and with balance-sheet instruments (mainly government bonds with the highest credit ratings and liquidity). The amount of NTI generated in Spain, Mexico and the United States is the result of prudent portfolio management strategies, particularly in terms of sovereign debt, in a context marked by low interest rates.

Economic capital

Attributableeconomic risk capital (ERC) consumption at the end of 2014 stood at €31,569m, up 3.5% with respect to the close of the previous quarter.

As is to be expected from BBVA’s profile, the largest allocation to ERC (52.3%) relates tocredit risk on portfolios originated in the Group’s branch network from its own customer base. Over the last 3 months, ERC from credit risk has increased by 4.2%, due mainly to rises in the United States and South America.

Equity risk, in other words, from the portfolio of holdings in industrial and financial companies, the stake in the CNCB group and consumption of economic capital from goodwill, has increased slightly as a proportion of total risks to 18.1%.

Structural balance-sheet risk, which originates from the management of both, structural interest-rate risk and exchange-rate risk, accounts for 7.2% of all ERC. It has increased by 6.7% during the period.

Operational risk remains stable and accounts for 6.7% of the total, whilefixed-asset risk has reduced its share to 11.7%.

Lastly,trading risk which is of less importance given the nature of the business and BBVA’s policy of minimal proprietary trading, remains at 2.9%.

| Risk management | 15 |

Table of Contents

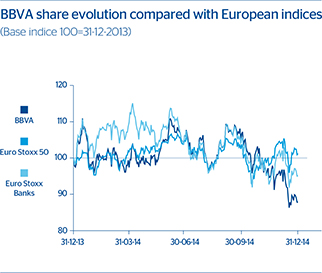

Theglobal economy continued to grow in the second half of 2014, and at a slightly faster pace than at the beginning of the year (+3.0%), but performance varied from one geographical area to another: sustained improvement in the United States, reduced growth in Europe and Japan, and moderation in China and in other large emerging economies. The impact of the sharp slump in oil prices, which is positive for overall economic activity and exerts a downward pressure on prices, is a new factor that will widen the gap between exporting and importing economies, in a scenario marked by geopolitical tension and diverging monetary policies. Financial assets, interest rates and exchange rates reflect this scenario.

In this context, the mainstock market indices have performed unevenly over the quarter. In Europe, the Euro Stoxx 50 fell by 2.5% and the Ibex 35 by 5.0%, while in the United States the S&P 500 gained 4.4%. The Eurozone’s banking sector index, Euro Stoxx Banks, fell by 9.9%, partly reflecting the uncertainty surrounding growth and monetary policy measures. In contrast, in the United States, the S&P Regional Banks index gained 5.2%.

The BBVA share and share performance ratios

| 31-12-14 | 30-09-14 | |||||||

Number of shareholders | 960,397 | 947,901 | ||||||

Number of shares issued | 6,171,338,995 | 5,887,168,710 | ||||||

Daily average number of shares traded | 59,856,509 | 60,252,342 | ||||||

Daily average trading | 508 | 561 | ||||||

Maximum price (euros) | 9.66 | 9.91 | ||||||

Minimum price (euros) | 7.45 | 8.51 | ||||||

Closing price (euros) | 7.85 | 9.55 | ||||||

Book value per share (euros) | 8.01 | 7.99 | ||||||

Market capitalization (million euros) | 48,470 | 56,228 | ||||||

Price/book value (times) | 1.0 | 1.2 | ||||||

PER (Price/earnings; times) | 17.3 | 18.4 | ||||||

Yield (Dividend/price; %)(1) | 4.5 | 3.8 | ||||||

| (1) | Calculated by dividing the median of the forecast dividend per share of a consensus of analysts by the BBVA share price at the end of each quarter. |

BBVA’searnings for the third quarter of 2014 coincided with the publication of the results of the comprehensive assessment of European banks conducted by the European Central Bank (ECB). For the Group, the results for the period confirm its sound solvency position and its capacity to generate earnings under different scenarios, placing BBVA among the leaders in the ranking of the main European banks.

As of December 31, 2014, theBBVA share closed at €7.85, down 17.8% in the quarter and 12.2% in the year, after a very positive performance in 2013. As of 31-Dec-2014, BBVA weight on the Ibex 35 was 10.11% (2.44% on the Euro Stoxx 50). At year-end 2014, BBVA’s market capitalization amounted to €48,470m, down 13.8% on the figure as of 30-Sep-2014.

With respect toshareholder remuneration, the Board of Directors agreed on December 17 to once again perform a capital increase against reserves for the implementation of a new “dividend option”. Each shareholder had one free allocation right for every BBVA share held on December 19, with 99 rights entitling the holder to receive one new BBVA share. Alternatively, shareholders who wish to receive their remuneration in cash are entitled to sell their rights to BBVA at a gross fixed price of €0.08 per right during the first ten calendar days of their trading period, or on the market during the complete trading period. On this occasion, owners of 86.0% of these rights chose to receive new shares. This once more confirms the excellent response to this system of remuneration and the confidence felt by shareholders in the future performance of the share.

| 16 | Group information |

Table of Contents

Environmental and Social Governance

At BBVA we are convinced that the return adjusted to principles is, in itself, a source of competitive advantage that can ensure the Group’s long-term sustainability.

The most relevant highlights in environmental and social governance in thefourth quarter of 2014 are summarized below:

Transparent, Clear and Responsible (TCR) Communication

BBVA has continued to make progress in its TCR communication strategy. In this regard, a Commercial TCR Communication Code, which began to be implemented on January 1, 2015, has been developed that guarantees the use of simple, clear and precise language in all Group commercial communication and advertising, which will help our customers make the right decisions.

Education

The4th Pensions Event organized by BBVA Pensiones on the theme of financial literacy for retirement was held in October 2014. During the event, it was announced the launch of a new tool that has been designed to facilitate decision-making in matters related to retirement. It is a public pensions simulator adapted to the latest Social Security reforms in Spain that enables the expected pension to be calculated under different scenarios.

The 5th edition of theMomentum Project has also been launched in Spain. For the first time in this program’s history, 5 of the 15 participating social enterprises will come from the organizations recognized in BBVA’s 7th Integra Awards.

Lastly, the Group has received the “Premio Latinoamericano a la Responsabilidad de Empresas” (Latin American Award for Responsibility in Business). The award has highlighted the commitment to education and the integration scholarship program that promotes access to quality education for children and young people from the most underprivileged areas in Latin America.

Products with a high social impact

BBVA has received the Award for Innovation and Social Engagement from the SERES Foundation for promoting job creation through the “Yo Soy Empleo” (I am Employment) initiative. This program has helped 4,614 businesses and self-employed workers create 7,427 jobs in Spain, nearly 70% with permanent employment contracts. On average, those hired had been unemployed for 14 months and 40% were under the age of 30. Of these new jobs, 1,000 correspond to €1,500 non-repayable self-employment aid packages for each new self-employed person starting work in Spain. In addition, in November, BBVA reached an agreement with the ONCE Foundation whereby they will allocate €750,000 in aid packages to create 500 new jobs for disabled people.

Other lines

In partnership with Deusto University, BBVA has organized the series of conferences “Empresa y Banca Responsable” (Business and Responsible Banking), which discussed the link between banking and social innovation processes.

Aware of its responsibility to society, BBVA will donate up to €3 million tocharity projects (Cáritas, Spanish Red Cross and Food Bank).

Team

In Spain, the 6thIntegra Prize was awarded to the AMIAB group, an organization that promotes the labor and social integration of disabled people in Albacete. The prize is worth €200,000. Moreover, a special mention worth €100,000 and another four additional recognitions for €50,000 each were also granted. The 7th edition of the Integra Prize was launched in December 2014. On this occasion there will be two categories: one, for €150,000, that recognizes an organization’s track record, and one for innovative projects, with a €25,000 prize. In addition, all the winners will become participants in Momentum Project, an initiative that aims to promote and extend the activity and impact of social ventures.

Lastly, the “8th Carrera Solidaria” BBVA (Charity Run) brought together nearly 8,000 runners. A total of €140,000 has been raised from registrations of those taking part, the matching contribution made by BBVA and “zero vest number” donations. The funds will go to the Cáritas Madrid charity store.

BBVA in the sustainability indices

BBVA has a notable position on the main international sustainability indices, with a weight as of 31-Dec-2014 as follows:

For more information and contact details, see the chapter on Business areas and www.bbvaresponsiblebanking.com

| Environmental and Social Governance | 17 |

Table of Contents

This section presents and analyzes the most relevant aspects of the Group’s different areas. Specifically, it shows the income statement, the balance sheet, the business activity and the most significant ratios in each of them: loan book, customer deposits under management, mutual funds and pension funds, efficiency ratio, NPA ratio, coverage ratio and risk premium.

In 2014, thereporting structure of the BBVA Group’s business areas is basically the same as that reported in 2013:

| • | Banking activity in Spain, which as in previous years includes: The Retail network, with the segments of individual customers, private banking and small businesses; Corporate and Business Banking (CBB), which handles the SMEs, corporations and institutions in the country; Corporate & Investment Banking (CIB), which includes business with large corporations and multinational groups and the trading floor and distribution business in the same geographical area; and other units, among them BBVA Seguros and Asset Management (management of mutual and pension funds in Spain). It also includes the portfolios, finance and structural interest-rate positions of the euro balance sheet. |

| • | Real-estate activity in Spain. This area basically covers lending to real-estate developers and foreclosed real-estate assets in the country. |

| • | The United States encompasses the Group’s businesses in the United States. |

| • | Eurasia, which includes the business carried out in the rest of Europe and Asia, i.e. the Group’s retail and wholesale businesses in the area. It also includes BBVA’s stakes in the Turkish bank Garanti and the Chinese banks CNCB and CIFH (a sell agreement on the later stake was signed in December 2014 and its execution is subject to the pertinent authorizations). However, the equity-accounted income of CNCB (excluding the dividends) from its acquisition until the conclusion of the new agreement with the CITIC Group in the fourth quarter of 2013 (which included the sale of 5.1% of the stake in CNCB) has been reclassified in the Corporate Center under the heading “Results from corporate operations”. |

| • | Mexico includes the banking and insurance businesses in the country. |

| • | South America includes the banking and insurance businesses that BBVA carries out in the region. In the first quarter of 2014, the historical series in this area has been reconstructed to exclude the business in Panama, which was sold in the fourth quarter of 2013, and include it in the Corporate Center. |

In addition to the above, all the areas include a remainder made up of other businesses and of a supplement that includes deletions and allocations not assigned to the units making up the above areas.

Lastly, theCorporate Center is an aggregate that contains the rest of the items that have not been allocated to the business areas, as it basically corresponds to the Group’s holding function. It groups together the costs of the head offices that have a corporate function; management of structural exchange-rate positions, carried out by BBVA’s Strategy and Finance area; specific issues of capital instruments to ensure adequate management of the Group’s global solvency; portfolios and their corresponding results, whose management is not linked to customer relations, such as industrial holdings; certain tax assets and liabilities; funds due to commitments with pensioners; goodwill and other intangibles. It also comprises the result from certain corporate operations carried out in 2013, such as the earnings and capital gains from the pension business disposals in Latin America during 2013; those from BBVA Panama taking into consideration the capital gain from its disposal (in the fourth quarter); and the effect of the repricing of the stake in CNCB to market value following the signing in the fourth quarter of 2013 of the agreement with the CITIC group, which included the sale of 5.1% of the stake in CNCB. It also includes the equity-accounted earnings from CNCB (excluding the dividends).

In addition to this geographical breakdown,supplementary information is provided for all the wholesale businesses carried out by BBVA, i.e. Corporate & Investment Banking (CIB). This aggregate business is considered relevant to better understand the BBVA Group because of the characteristics of the customers served, the type of products offered and the risks assumed.

Lastly, as usual, in the case of the Americas and Eurasia (basically Garanti), the results of applying constant exchange rates are given in addition to the year-on-year variations at currentexchange rates.

The Group compilesinformation by areas based on units at the same level, and all the accounting data related to the business they manage are recorded in full. These basic units are then aggregated in accordance with the organizational structure established by the Group for higher-level units and, finally, the business areas themselves. Similarly, all the companies making up the Group are also assigned to the different units according to the geographical area of their activity.

Once the composition of each business area has been defined, certainmanagement criteria are applied, of which the following are particularly important:

| 18 | Business areas |

Table of Contents

| • | Capital. Capital is allocated to each business according to economic risk capital (ERC) criteria. This is based on the concept of unexpected loss at a specific confidence level, depending on the Group’s capital adequacy targets. The calculation of the ERC combines credit risk, market risk, structural balance-sheet risk, equity positions, operational risk, fixed-asset risk and technical risks in the case of insurance companies. These calculations are carried out using internal models that have been defined following the guidelines and requirements established under the Basel III capital accord, with economic criteria taking precedence over regulatory ones. |

ERC is risk-sensitive and thus linked to the management policies of the businesses themselves. It standardizes capital allocation between them in accordance with the risks incurred. In other words, it is calculated in a way that is standard and integrated for all kinds of risks and for each operation, balance or risk position, allowing its risk-adjusted return to be assessed and an aggregate to be calculated for profitability by client, product, segment, unit or business area.

| • | Internal transfer prices. Within each geographical area, internal transfer rates are applied to calculate the net interest income of its businesses, under both the asset and liability headings. These rates are composed of a market rate that depends on the operation’s revision period, and a liquidity premium that aims to reflect the conditions and outlook for the financial markets in each area. Earnings are distributed across revenue-generating and distribution units (e.g., in asset management products) at market prices. |

| • | Allocation of operating expenses. Both direct and indirect costs are allocated to the business areas, except where there is no clearly defined relationship with the businesses, i.e. when they are of a clearly corporate or institutional nature for the Group as a whole. |

| • | Cross-selling. In some cases, consolidation adjustments are required to eliminate shadow accounting entries in the earnings of two or more units as a result of cross-selling incentives. |

Mayor income statement items by business area

(Million euros)

| Business areas | ||||||||||||||||||||||||||||||||||||

| BBVA Group (1) | Banking activity in Spain | Real-estate activity in Spain | The United States | Eurasia (1) | Mexico | South America | S Business areas | Corporate Center | ||||||||||||||||||||||||||||

2014 | ||||||||||||||||||||||||||||||||||||

Net interest income | 15,116 | 3,830 | (38 | ) | 1,443 | 924 | 4,910 | 4,699 | 15,767 | (651 | ) | |||||||||||||||||||||||||

Gross income | 21,357 | 6,622 | (132 | ) | 2,137 | 1,680 | 6,522 | 5,191 | 22,020 | (664 | ) | |||||||||||||||||||||||||

Operating income | 10,406 | 3,777 | (291 | ) | 640 | 942 | 4,115 | 2,875 | 12,058 | (1,653 | ) | |||||||||||||||||||||||||

Income before tax | 4,063 | 1,463 | (1,225 | ) | 561 | 713 | 2,519 | 1,951 | 5,983 | (1,920 | ) | |||||||||||||||||||||||||

Net attributable profit | 2,618 | 1,028 | (876 | ) | 428 | 565 | 1,915 | 1,001 | 4,062 | (1,444 | ) | |||||||||||||||||||||||||

2013 | ||||||||||||||||||||||||||||||||||||

Net interest income | 14,613 | 3,838 | (3 | ) | 1,402 | 909 | 4,478 | 4,660 | 15,284 | (671 | ) | |||||||||||||||||||||||||

Gross income | 21,397 | 6,103 | (38 | ) | 2,047 | 1,717 | 6,194 | 5,583 | 21,607 | (210 | ) | |||||||||||||||||||||||||

Operating income | 10,196 | 3,088 | (188 | ) | 618 | 981 | 3,865 | 3,208 | 11,573 | (1,378 | ) | |||||||||||||||||||||||||

Income before tax | 2,750 | 230 | (1,838 | ) | 534 | 586 | 2,358 | 2,354 | 4,225 | (1,474 | ) | |||||||||||||||||||||||||

Net attributable profit | 2,228 | 589 | (1,252 | ) | 390 | 449 | 1,802 | 1,224 | 3,201 | (973 | ) | |||||||||||||||||||||||||

| (1) | Pro forma financial statements with the revenues and expenses of the Garanti Group consolidated in proportion to the percentage of the Group’s stake. |

Breakdown of gross income, operating income and net attributable profit by geography(1)

(2014)

| Banking activity in Spain | Spain (2) | The United States | Eurasia | Mexico | South America | |||||||||||||||||||

Gross income | 30.1 | % | 29.5 | % | 9.7 | % | 7.6 | % | 29.6 | % | 23.6 | % | ||||||||||||

Operating income | 31.3 | % | 28.9 | % | 5.3 | % | 7.8 | % | 34.1 | % | 23.8 | % | ||||||||||||

Net attributable profit | 25.3 | % | 3.7 | % | 10.5 | % | 13.9 | % | 47.1 | % | 24.6 | % | ||||||||||||

| (1) | Excludes the Corporate Center. |

| (2) | Including real-estate activity in Spain. |

| Business areas | 19 |

Table of Contents

| 20 | Business areas |

Table of Contents

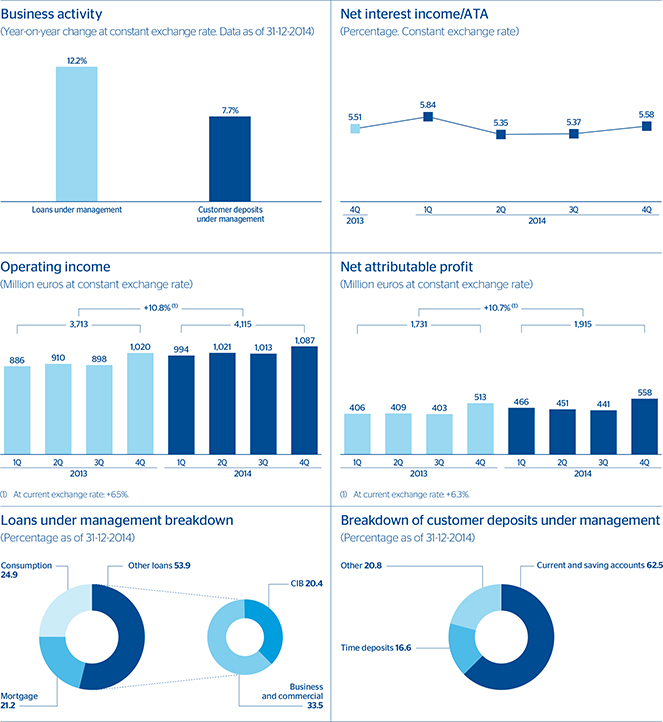

Highlights

In thefourth quarter of 2014 earnings continued to rise, as they had in previous quarters. The main reason has been the falling cost of deposits and the recovery of production of new loans, above all mortgage loans, consumer finance and finance for SMEs.

Macro and industry trends

The Spanisheconomy continued to improve in the second half of 2014. The rate of growth in the third quarter of 0.5% is expected to be slightly exceeded in the fourth quarter. This improvement can be seen both in consumption and in investment and exports, boosted by the depreciation of the euro, the rise in the index of household and business confidence, reduced financial tension and a looser fiscal policy. In addition, the reforms carried out over recent years, such as those affecting the labor market, have had a positive impact.

The highlight in thebanking sector in the quarter has been the publication of the results of the comprehensive assessment of the European banking system, which were in general positive for Spanish banks. Thus, the asset quality review identified a limited volume of adjustments required, even under the most extreme stress scenario.

According to the latest information available as of November 2014, the decline in the volume of loans in the Spanish banking system amounts to 5.8% year-on-year, although the flow of new lending to the retail segment (loans to companies for less than one million euros and to individuals) continues to improve. Moreover, the total figure for non-performing loans has fallen for the tenth month in a row, and the NPA ratio stood at 12.75% at the close of November.

Activity

The increase in new loan production is the result of increased demand for finance, although the higher production still does not offset the maturities of the current stock. Thus, the volume ofloans under management by the area continues to decline, although at a much slower pace than in previous quarters (down 1.3% year-on-year) in practically all the portfolios. Consumer finance has grown quarter-on-quarter (up 1.4%, including credit cards). This improvement in demand for finance is expected to consolidate further over the coming quarters, underpinned by stronger economic activity in the country.

Financial statements and relevant business indicators

(Million euros and percentage)

Income statement | 2014 | D% | 2013 | |||||||||

Net interest income | 3,830 | (0.2 | ) | 3,838 | ||||||||

Net fees and commissions | 1,454 | 5.7 | 1,376 | |||||||||

Net trading income | 1,149 | 42.4 | 807 | |||||||||

Other income/expenses | 189 | 129.6 | 82 | |||||||||

Gross income | 6,622 | 8.5 | 6,103 | |||||||||

Operating expenses | (2,845 | ) | (5.6 | ) | (3,014 | ) | ||||||

Personnel expenses | (1,707 | ) | (7.8 | ) | (1,851 | ) | ||||||

General and administrative expenses | (1,034 | ) | (1.8 | ) | (1,052 | ) | ||||||

Depreciation and amortization | (105 | ) | (5.3 | ) | (111 | ) | ||||||

Operating income | 3,777 | 22.3 | 3,088 | |||||||||

Impairment on financial assets (net) | (1,690 | ) | (34.4 | ) | (2,577 | ) | ||||||

Provisions (net) and other gains (losses) | (623 | ) | 121.3 | (282 | ) | |||||||

Income before tax | 1,463 | n.m. | 230 | |||||||||

Income tax | (432 | ) | n.m. | (62 | ) | |||||||

Net income from ongoing operations | 1,032 | n.m. | 168 | |||||||||

Results from corporate operations | — | — | 440 | |||||||||

Net income | 1,032 | 69.7 | 608 | |||||||||

Non-controlling interests | (4 | ) | (81.8 | ) | (20 | ) | ||||||

Net attributable profit | 1,028 | 74.7 | 589 | |||||||||

Net attributable profit (excluding results from corporate operations) | 1,028 | n.m. | 149 | |||||||||

Balance sheet | 31-12-14 | D% | 31-12-13 | |||||||||

Cash and balances with central banks | 7,876 | (30.8 | ) | 11,389 | ||||||||

Financial assets | 116,016 | 16.4 | 99,712 | |||||||||

Loans and receivables | 191,273 | 0.8 | 189,734 | |||||||||

Loans and advances to customers | 169,211 | (2.3 | ) | 173,249 | ||||||||

Loans and advances to credit institutions and other | 22,062 | 33.8 | 16,484 | |||||||||

Inter-area positions | 173 | (98.6 | ) | 12,699 | ||||||||

Tangible assets | 700 | (10.4 | ) | 781 | ||||||||

Other assets | 2,315 | 293.3 | 589 | |||||||||

Total assets/liabilities and equity | 318,353 | 1.1 | 314,902 | |||||||||

Deposits from central banks and credit institutions | 64,765 | 12.5 | 57,562 | |||||||||

Deposits from customers | 154,261 | (1.8 | ) | 157,124 | ||||||||

Debt certificates | 41,689 | (15.1 | ) | 49,105 | ||||||||

Subordinated liabilities | 2,077 | (13.9 | ) | 2,411 | ||||||||

Inter-area positions | — | — | — | |||||||||

Financial liabilities held for trading | 43,977 | 14.4 | 38,435 | |||||||||

Other liabilities | 3,426 | n.m. | 673 | |||||||||

Economic capital allocated | 8,158 | (14.9 | ) | 9,592 | ||||||||

Relevant business indicators | 31-12-14 | 30-09-14 | 31-12-13 | |||||||||

Loans under management(1) | 166,446 | 166,065 | 168,594 | |||||||||

Customer deposits under management(2) | 138,647 | 139,838 | 136,295 | |||||||||

Mutual funds | 28,695 | 27,552 | 22,298 | |||||||||

Pension funds | 21,880 | 21,677 | 20,428 | |||||||||

Efficiency ratio (%) | 43.0 | 43.8 | 49.4 | |||||||||

NPA ratio (%) | 6.0 | 6.2 | 6.4 | |||||||||

NPA coverage ratio (%) | 45 | 44 | 41 | |||||||||

Cost of risk (%) | 0.95 | 0.93 | 1.36 | |||||||||

| (1) | Includes funding for segments managed by CBB through fixed-income. |

| (2) | Excluding repos. |

| Banking activity in Spain | 21 |

Table of Contents