UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of July, 2015

Commission file number: 1-10110

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

(Exact name of Registrant as specified in its charter)

BANK BILBAO VIZCAYA ARGENTARIA, S.A.

(Translation of Registrant’s name into English)

Paseo de la Castellana, 81

28046 Madrid

Spain

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ¨ No x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ¨ No x

2015 Second Quarter Results

Madrid, July 31st 2015

July 31st 2015

2015 Second Quarter Results 2

Disclaimer

This document is only provided for information purposes and does not constitute, nor must it be interpreted as, an offer to sell or exchange or acquire, or an invitation for offers to buy securities issued by any of the aforementioned companies. Any decision to buy or invest in securities in relation to a specific issue must be made solely and exclusively on the basis of the information set out in the pertinent prospectus filed by the company in relation to such specific issue. Nobody who becomes aware of the information contained in this report must regard it as definitive, because it is subject to changes and modifications.

This document contains or may contain forward looking statements (in the usual meaning and within the meaning of the US Private Securities Litigation Act of 1995) regarding intentions, expectations or projections of BBVA or of its management on the date thereof, that refer to miscellaneous aspects, including projections about the future earnings of the business. The statements contained herein are based on our current projections, although the said earnings may be substantially modified in the future by certain risks, uncertainty and other factors relevant that may cause the results or final decisions to differ from such intentions, projections or estimates. These factors include, without limitation, (1) the market situation, macroeconomic factors, regulatory, political or government guidelines, (2) domestic and international stock market movements, exchange rates and interest rates, (3) competitive pressures, (4) technological changes, (5) alterations in the financial situation, creditworthiness or solvency of our customers, debtors or counterparts. These factors could condition and result in actual events differing from the information and intentions stated, projected or forecast in this document and other past or future documents. BBVA does not undertake to publicly revise the contents of this or any other document, either if the events are not exactly as described herein, or if such events lead to changes in the information of this document.

This document may contain summarised information or information that has not been audited, and its recipients are invited to consult the documentation and public information filed by BBVA with stock market supervisory bodies, in particular, the prospectuses and periodical information filed with the Spanish Securities Exchange Commission (CNMV) and the Annual Report on form 20-F and information on form 6-K that are disclosed to the US Securities and Exchange Commission.

Distribution of this document in other jurisdictions may be prohibited, and recipients into whose possession this document comes shall be solely responsible for informing themselves about, and observing any such restrictions. By accepting this document you agree to be bound by the foregoing restrictions.

July 31st 2015

2015 Second Quarter Results 3

Garanti Bank Closing

(1) According to Bloomberg consensus

July 31st 2015

2015 Second Quarter Results 4

Priorities in a Changing Environment

1 2 3

New standard in Drive digital sales New business models

customer experience

4 5 6

Optimize capital Unrivaled efficiency A first class

allocation workforce

July 31st 2015

2015 Second Quarter Results 5

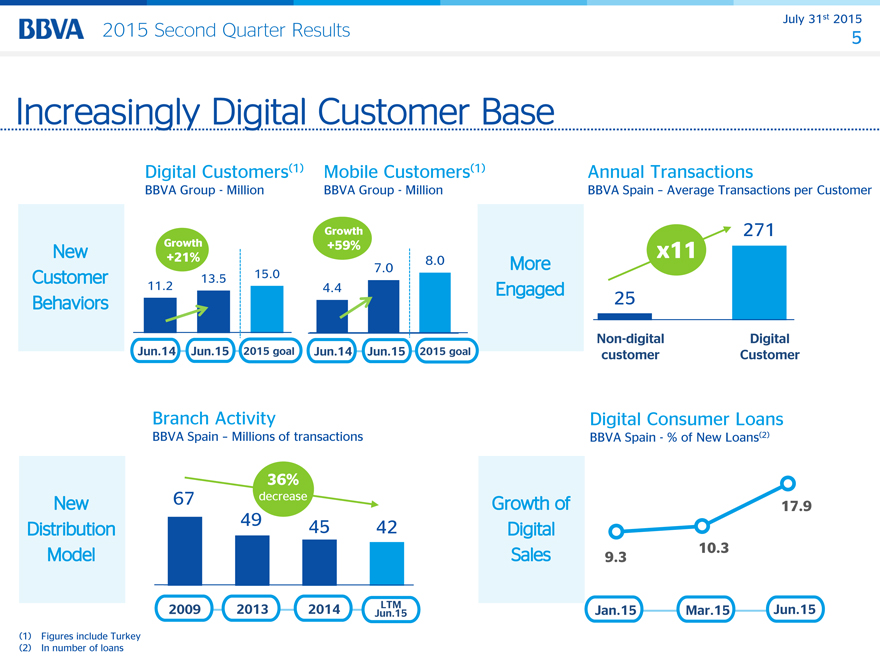

Digital Customers(1) Mobile Customers(1)

BBVA Group—Million BBVA Group—Million

Growth

Growth +59%

+21% 8.0

7.0

13.5 15.0

11.2 4.4

Jun.14 Jun.15 2015 goal Jun.14 Jun.15 2015 goal

Annual Transactions

BBVA Spain – Average Transactions per Customer

271

x11

25

Non-digital Digital

customer Customer

Branch Activity

BBVA Spain – Millions of transactions

36%

67 decrease

49 45 42

2009 2013 2014 Jun.LTM 15

Digital Consumer Loans

BBVA Spain—% of New Loans(2)

17.9

9.3 10.3

Jan.15 Mar.15 Jun.15

Figures include Turkey

In number of loans

July 31st 2015

2015 Second Quarter Results 6

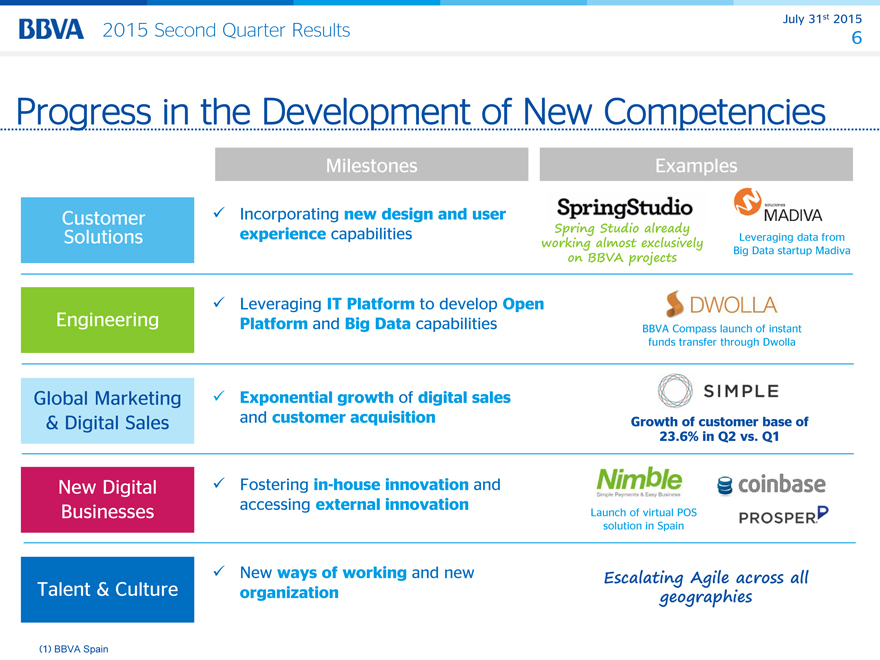

Progress in the Development of New Competencies

Milestones Examples

Customer Incorporating new design and user Spring Studio already

Solutions experience capabilities working almost exclusively Leveraging data from

on BBVA projects Big Data startup Madiva

Leveraging IT Platform to develop Open

Engineering Platform and Big Data capabilities BBVA Compass launch of instant

funds transfer through Dwolla

Global Marketing Exponential growth of digital sales

& Digital Sales and customer acquisition Growth of customer base of

23.6% in Q2 vs. Q1

New Digital Fostering in-house innovation and

Businesses accessing external innovation Launch of virtual POS

solution in Spain

New ways of working and new Escalating Agile across all

Talent & Culture organization geographies

(1) BBVA Spain

July 31st 2015

2015 Second Quarter Results 7

2Q Execution & Performance

Activity growth(1) (Jun15/Jun14) Lending +13.6% Cust.Funds +18.3%

Strong Activity

& Double digit income growth (2Q15/2Q14) Operating Income: +17.2%

P&L Dynamics

Net attributable profit (2Q15) € 1.2Bn

Improvement in NPL Ratio 6.1%

Risk Indicators

Coverage Ratio 72%

CET 1 ratio Leverage

Solid Capital

Ratios Catalunya Caixa impact 10.4% 12.3% 5.9%

(Fully-loaded) (Phased-in) (Fully-loaded)

Corporate Strategic Catalunya Caixa Closing (April 2015) +144 €m

Operations Sale of 0.8% of CNCB Attrib. profit

Note: All figures exclude Venezuela and include Catalunya Caixa

(1) Activity excludes repos; Gross loans and advances to customers; customer funds include promissory notes.

July 31st 2015

2015 Second Quarter Results 8

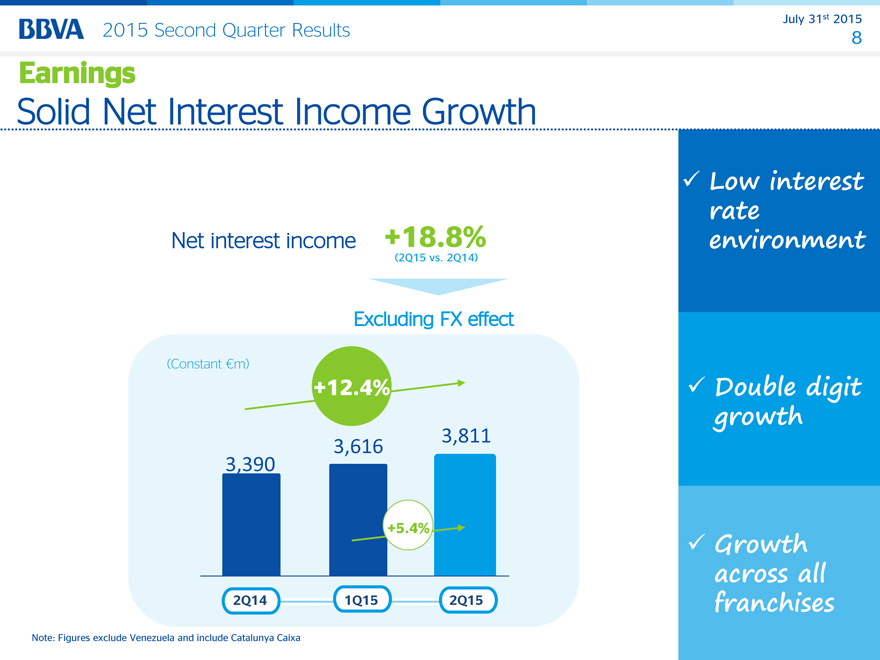

Earnings

Solid Net Interest Income Growth

Net interest income +18.8%

(2Q15 vs. 2Q14)

(Constant €m)

+12.4%

3,616 3,811

3,390

+5.4%

2Q14 1Q15 2Q15

Note: Figures exclude Venezuela and include Catalunya Caixa

Low interest

rate

environment

Double digit

growth

Growth

across all

franchises

July 31st 2015

2015 Second Quarter Results 9

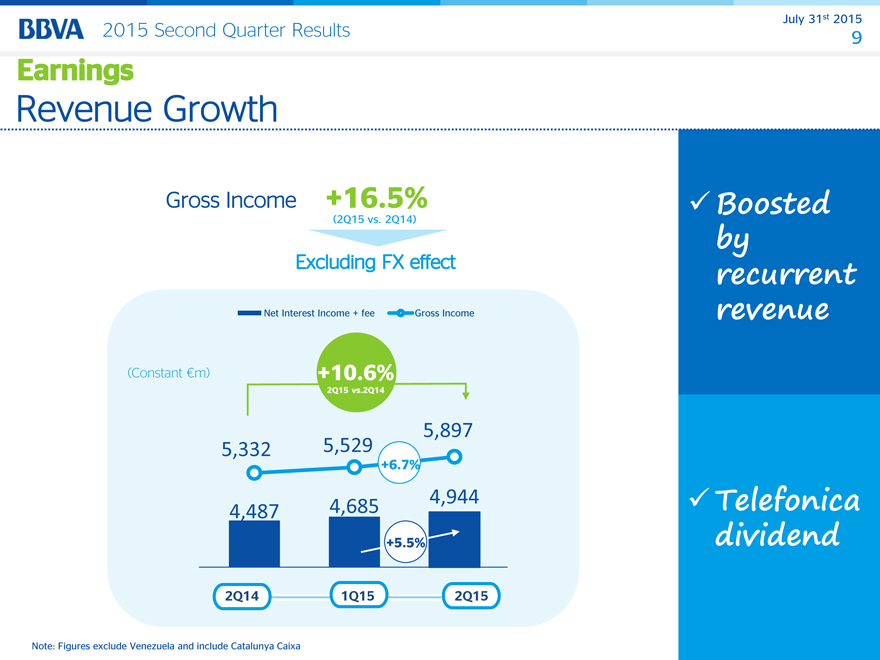

Earnings Revenue Growth

Gross Income +16.5%

(2Q15 vs. 2Q14)

Net Interest Income + fee Gross Income

(Constant €m) +10.6%

2Q15 vs.2Q14

5,897

5,332 5,529

+6.7%

4,487 4,685 4,944

+5.5%

2Q14 1Q15 2Q15

Boosted by recurrent revenue

Telefonica dividend

Note: Figures exclude Venezuela and include Catalunya Caixa

July 31st 2015

2015 Second Quarter Results 10

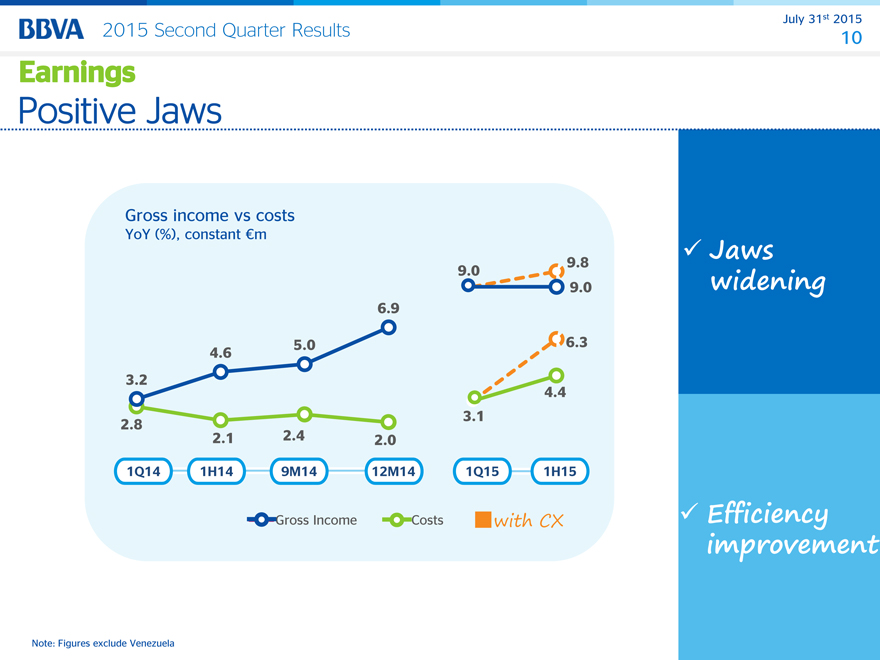

Earnings Positive Jaws

Gross income vs costs

YoY (%), constant €m

9.0 9.8

9.0

6.9

4.6 5.0 6.3

3.2

4.4

2.8 3.1

2.1 2.4 2.0

1Q14 1H14 9M14 12M14 1Q15 1H15

Gross Income Costs with CX

Jaws widening

Efficiency improvement

Note: Figures exclude Venezuela

July 31st 2015

2015 Second Quarter Results 11

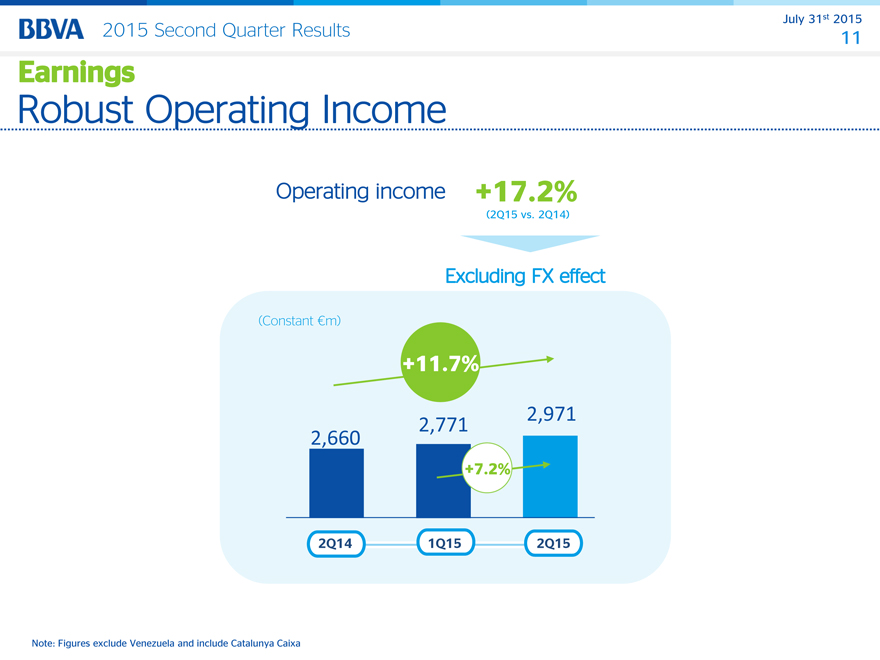

Earnings Robust Operating Income

Operating income +17.2%

(2Q15 vs. 2Q14)

(Constant €m)

+11.7%

2,771 2,971

2,660

+7.2%

2Q14 1Q15 2Q15

Note: Figures exclude Venezuela and include Catalunya Caixa

July 31st 2015

2015 Second Quarter Results 12

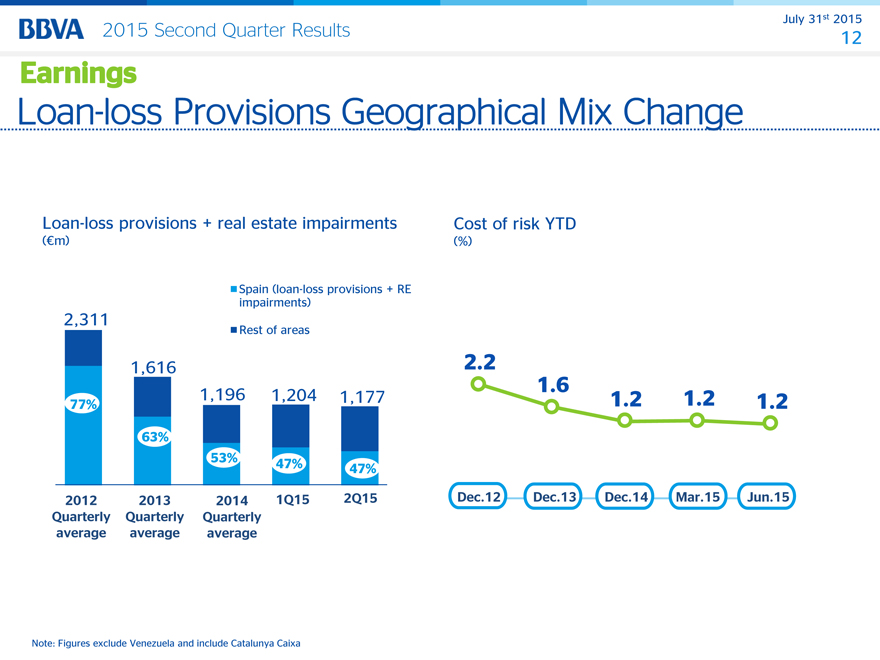

Earnings Loan-loss Provisions Geographical Mix Change

Loan-loss provisions + real estate impairments

(€m)

Spain (loan-loss provisions + RE

impairments)

2,311

Rest of areas

1,616

77% 1,196 1,204 1,177

63%

53%

47% 47%

2012 2013 2014 1Q15 2Q15

Quarterly Quarterly Quarterly

average average average

Cost of risk YTD

(%)

2.2

1.6 1.2 1.2 1.2

Dec.12 Dec.13 Dec.14 Mar.15 Jun.15

Note: Figures exclude Venezuela and include Catalunya Caixa

July 31st 2015

2015 Second Quarter Results 13

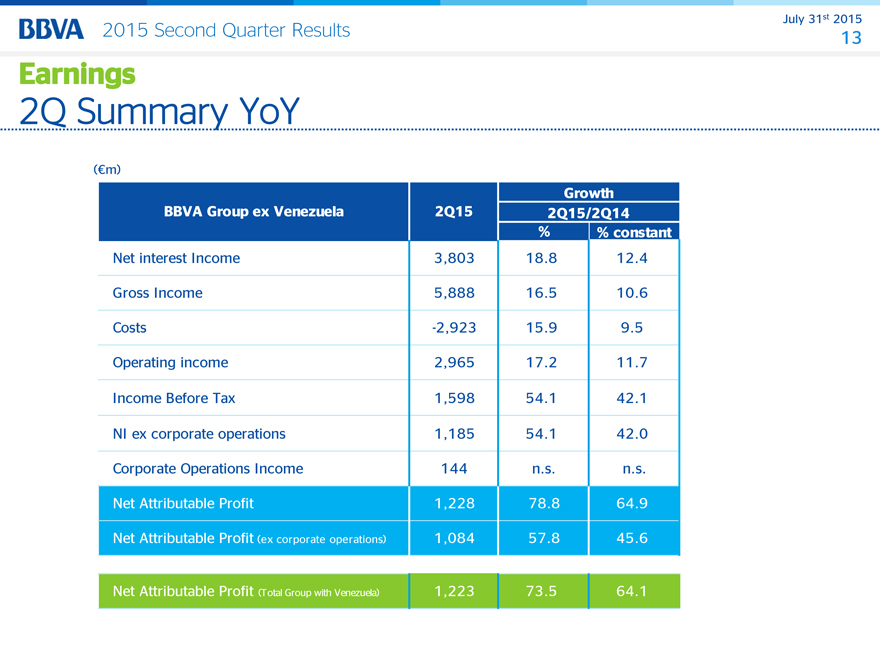

Earnings 2Q Summary YoY

(€m)

Growth

BBVA Group ex Venezuela 2Q15 2Q15/2Q14

% % constant

Net interest Income 3,803 18.8 12.4

Gross Income 5,888 16.5 10.6

Costs -2,923 15.9 9.5

Operating income 2,965 17.2 11.7

Income Before Tax 1,598 54.1 42.1

NI ex corporate operations 1,185 54.1 42.0

Corporate Operations Income 144 n.s. n.s.

Net Attributable Profit 1,228 78.8 64.9

Net Attributable Profit (ex corporate operations) 1,084 57.8 45.6

Net Attributable Profit (Total Group with Venezuela) 1,223 73.5 64.1

July 31st 2015

2015 Second Quarter Results 14

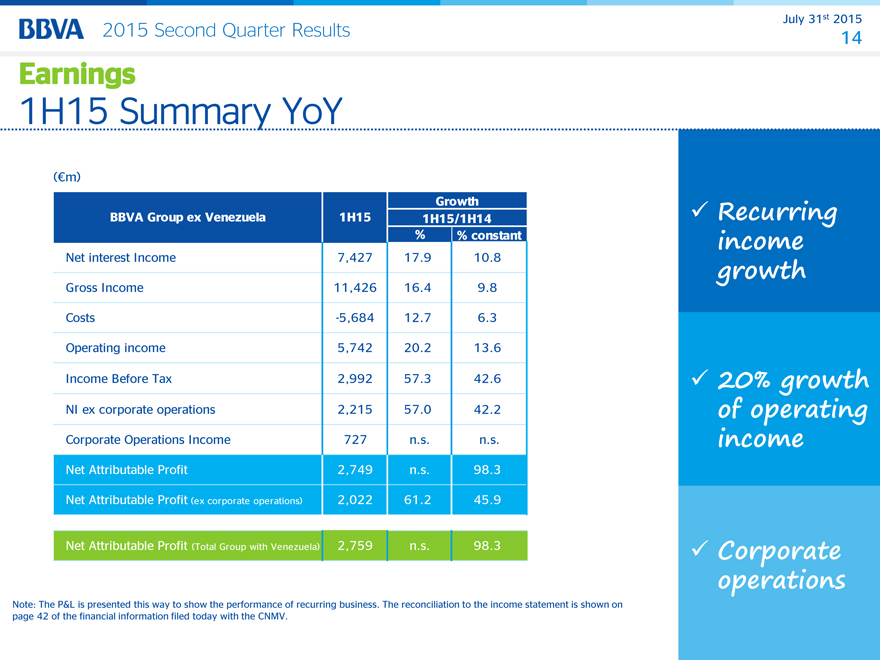

Earnings 1H15 Summary YoY

(€m)

Growth

BBVA Group ex Venezuela 1H15 1H15/1H14

% % constant

Net interest Income 7,427 17.9 10.8

Gross Income 11,426 16.4 9.8

Costs -5,684 12.7 6.3

Operating income 5,742 20.2 13.6

Income Before Tax 2,992 57.3 42.6

NI ex corporate operations 2,215 57.0 42.2

Corporate Operations Income 727 n.s. n.s.

Net Attributable Profit 2,749 n.s. 98.3

Net Attributable Profit (ex corporate operations) 2,022 61.2 45.9

Net Attributable Profit (Total Group with Venezuela) 2,759 n.s. 98.3

Note: The P&L is presented this way to show the performance of recurring business. The reconciliation to the income statement is shown on page 42 of the financial information filed today with the CNMV.

July 31st 2015

2015 Second Quarter Results 15

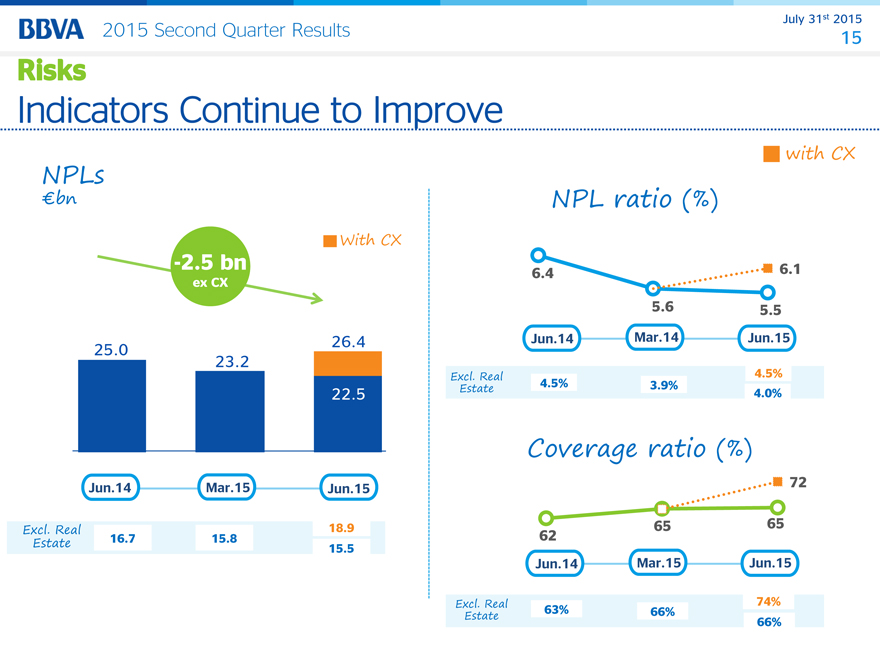

Risks

Indicators Continue to improve

NPLs

€bn

With CX

-2.5 bn

ex CX

25.0 26.4

23.2

22.5

Jun.14 Mar.15 Jun.15

Excl. Real 18.9

Estate 16.7 15.8 15.5

NPL ratio (%)

6.4 6.1

5.6 5.5

Jun.14 Mar.14 Jun.15

Excl. Real 4.5%

Estate 4.5% 3.9% 4.0%

Coverage ratio (%)

72

62 65 65

Jun.14 Mar.15 Jun.15

Excl. Real 74%

Estate 63% 66% 66%

with CX

July 31st 2015

2015 Second Quarter Results 16

Capital

Solid Capital Positition

Strong & Resilient

Regulatory Ratios

CET 1 ratio

12.3% 10.4%

(Phased-in) (Fully-loaded)

Pro-forma*

CET 1 ratio

10.0%e

(Fully-loaded)

High Quality Capital

The highest RWA density ratio of the European peer group (51%)

Leverage ratio

(%); Fully-loaded

5.9 4.1

BBVA European Peer

#1 Group Average

Pro-forma of corporate operations announced and pending to be closed at June 2015.

European Peer Group: BARC, BNPP, CASA, CS, CMZ, DB, HSBC, ISP, LBG, RBS, SAN, SG, UBS, UCG

July 31st 2015

2015 Second Quarter Results 17

Business Areas

July 31st 2015

2015 Second Quarter Results 18

Business Areas

1H15 Earnings Breakdown

Net Attributable Profit

(€m)

Growth

Business Areas 1H15 1H15/1H14

% % (constant)

Spain 509 n.s. n.s.

USA 286 45.9% 18.8%

Mexico 1,041 15.7% 8.6%

Turkey 174 12.9% 8.9%

Rest of Eurasia 43 -79.3% -79.4%

South America ex Venezuela 465 14.4% 8.4%

Corporate Center 230 n.s. n.s.

Total ex Venezuela 2,749 n.s. 98.3%

Note: Spain includes Real Estate activities

2015 Second Quarter Results July 31st 2015

19

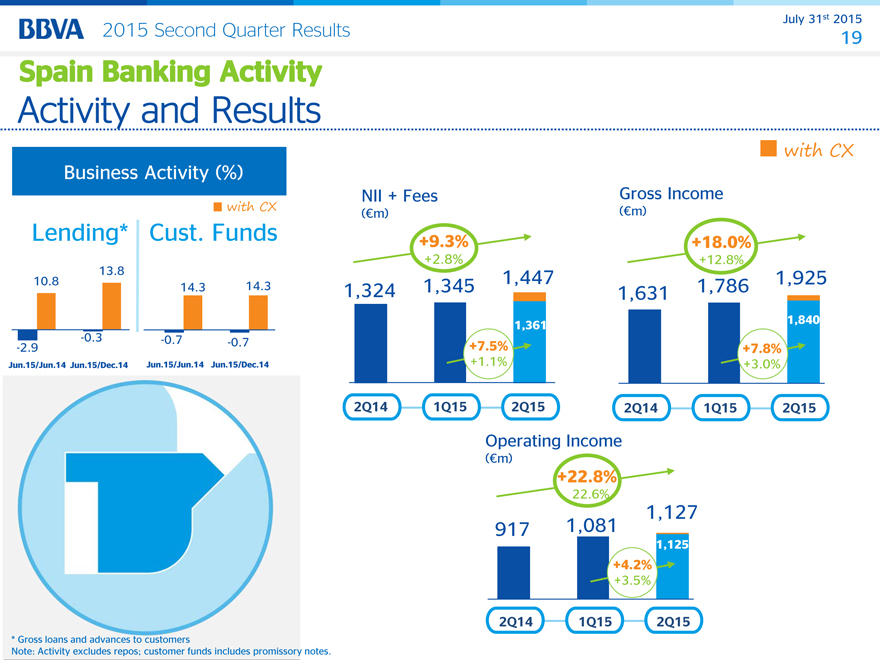

Spain Banking Activity

Activity and Results

Business Activity (%)

(%) with CX

Lending* Cust. Funds

13.8

10.8 14.3 14.3

-2.9 -0.3 -0.7 -0.7

with CX

NII + Fees Gross Income

(€m) (€m)

+9.3% +18.0%

+2.8% +12.8%

1,324 1,345 1,447 1,631 1,786 1,925

1,361 1,840

+7.5% +7.8%

+1.1% +3.0%

2Q14 1Q15 2Q15 2Q14 1Q15 2Q15

Operating Income

(€m)

+22.8%

+22.6%

1,127

917 1,081

1,125

+4.2%

+3.5%

2Q14 1Q15 2Q15

* Gross loans and advances to customers

Note: Activity excludes repos; customer funds includes promissory notes.

July 31st 2015

2015 Second Quarter Results 20

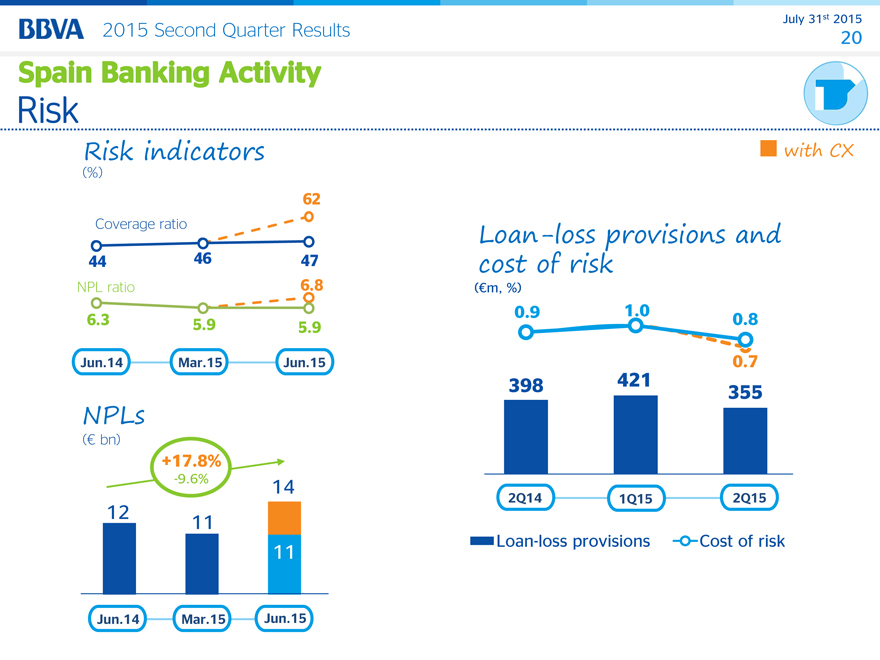

Spain Banking Activity

Risk

Risk indicators

(%)

62

Coverage ratio

44 46 47

NPL ratio 6.8

6.3 5.9 5.9

Jun.14 Mar.15 Jun.15

NPLs

(€ bn)

+17.8%

-9.6% 14

12 11

11

Jun.14 Mar.15 Jun.15

Loan-loss provisions and

cost of risk

(€m, %)

0.9 1.0 0.8

0.7

398 421 355

2Q14 1Q15 2Q15

Loan-loss provisions Cost of risk

July 31st 2015

2015 Second Quarter Results 21

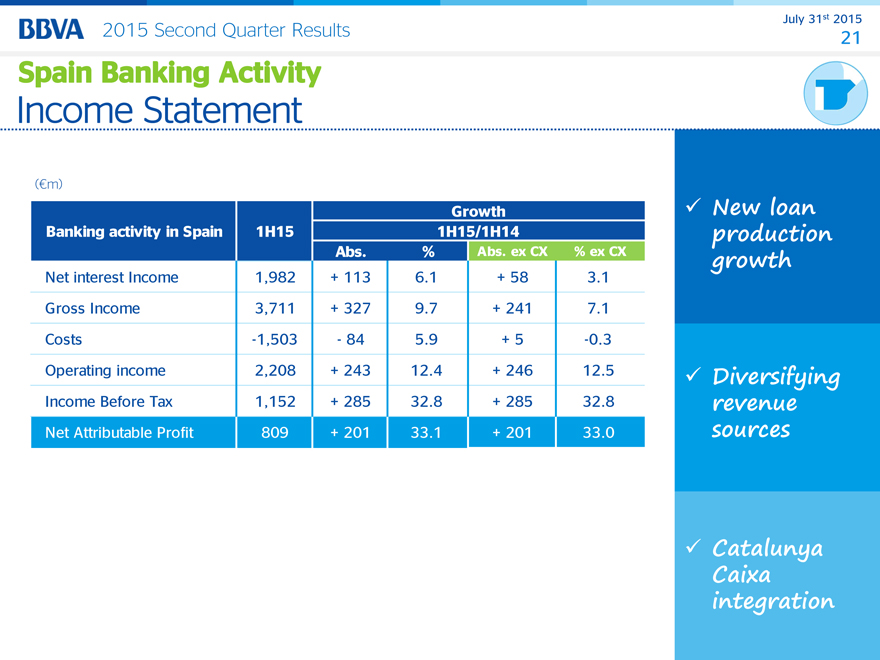

Spain Banking Activity

Income Statement

(€m)

Growth

Banking activity in Spain 1H15 1H15/1H14

Abs. % Abs. ex CX % ex CX

Net interest Income 1,982 + 113 6.1 + 58 3.1

Gross Income 3,711 + 327 9.7 + 241 7.1

Costs -1,503 —84 5.9 + 5 -0.3

Operating income 2,208 + 243 12.4 + 246 12.5

Income Before Tax 1,152 + 285 32.8 + 285 32.8

Net Attributable Profit 809 + 201 33.1 + 201 33.0

New loan production growth

Diversifying revenue sources

Catalunya Caixa integration

July 31 2015

2015 Second Quarter Results 22

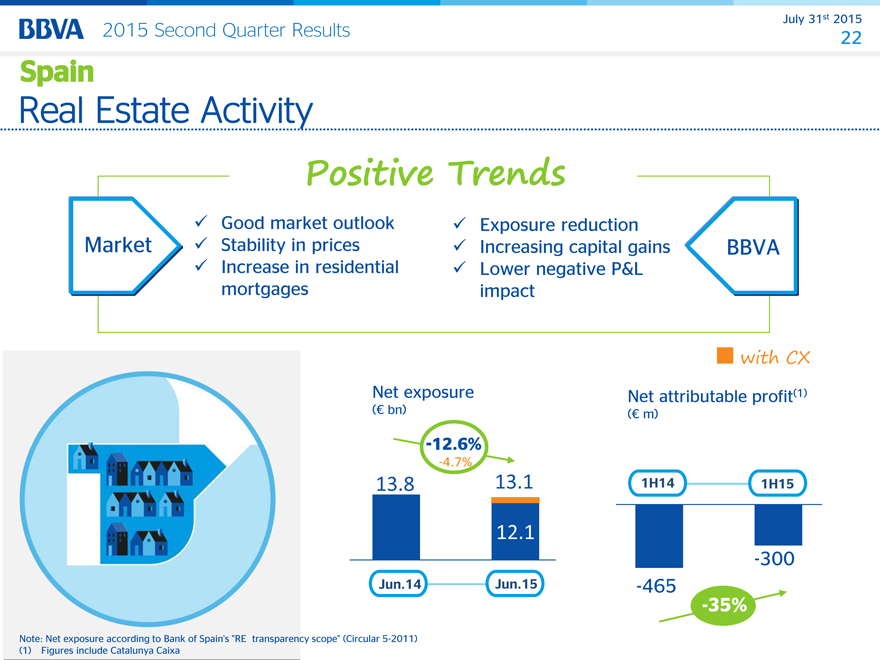

Spain Real Estate Activity

Positive Trends

Good market outlook Exposure reduction

Market Stability in prices Increasing capital gains BBVA

Increase in residential Lower negative P&L

mortgages impact

with CX

Net exposure Net attributable profit(1)

(€ bn) (€ m)

-12.6%

-4.7%

13.8 13.1 1H14 1H15

12.1

-300

Jun.14 Jun.15 -465

-35%

Note: Net exposure according to Bank of Spain’s “RE transparency scope” (Circular 5-2011) (1) Figures include Catalunya Caixa

July 31st 2015

2015 Second Quarter Results 23

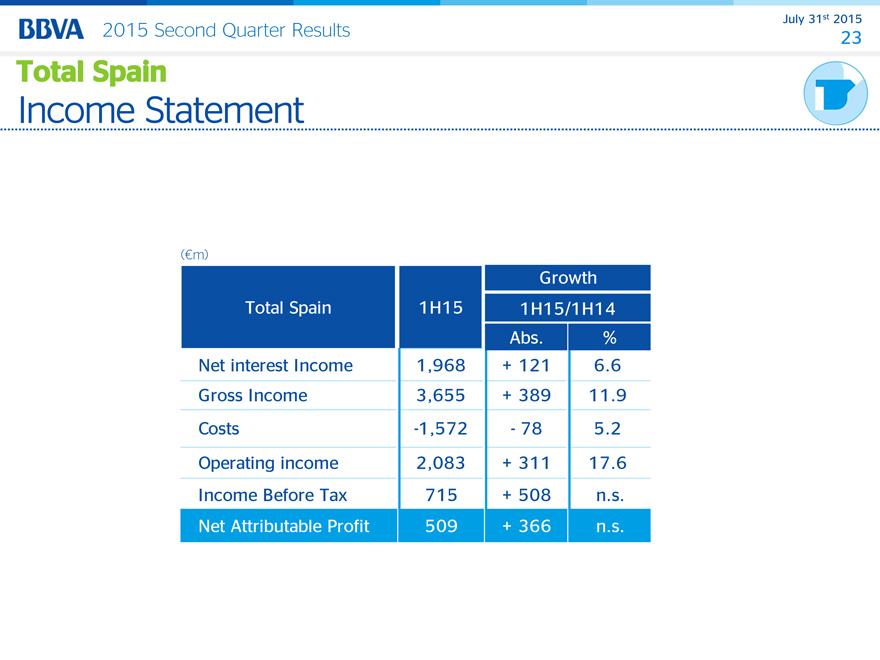

Total Spain

Income Statement

(€m)

Growth

Total Spain 1H15 1H15/1H14

Abs. %

Net interest Income 1,968 + 121 6.6

Gross Income 3,655 + 389 11.9

Costs -1,572 —78 5.2

Operating income 2,083 + 311 17.6

Income Before Tax 715 + 508 n.s.

Net Attributable Profit 509 + 366 n.s.

July 31st 2015

2015 Second Quarter Results 24

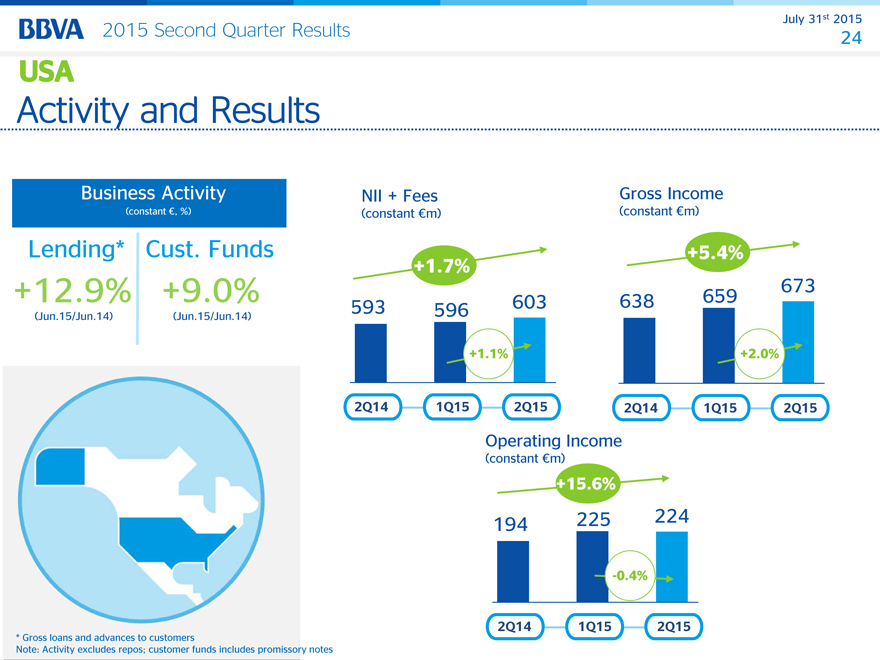

USA Total Spain Income Statement

Activity and Results

Business Activity

(constant €, %)

Lending* Cust. Funds

-2,2%

+12.9% +9.0%

(Jun.15/Jun.14) (Jun.15/Jun.14)

* Gross loans and advances to customers

Note: Activity excludes repos; customer funds includes promissory notes

NII + Fees Gross Income

(constant €m) (constant €m)

+1.7% +5.4%

673

593 596 603 638 659

+1.1% +2.0%

2Q14 1Q15 2Q15 2Q14 1Q15 2Q15

Operating Income

(constant €m)

+15.6%

194 225 224

-0.4%

2Q14 1Q15 2Q15

2015 Second Quarter Results July 31st 2015

25

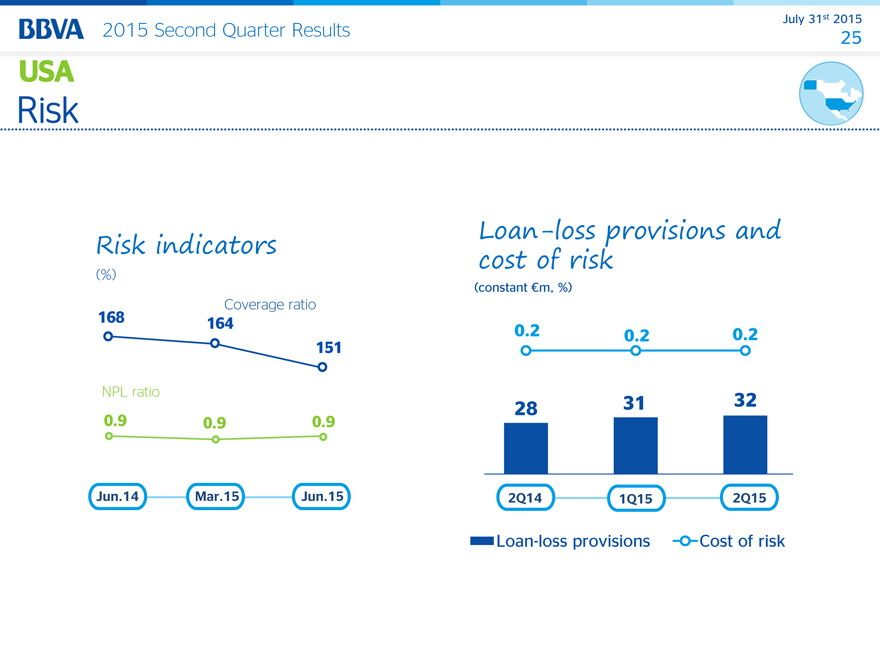

USA Activity and Results

Risk

Risk indicators

(%)

Coverage ratio

168 164

151

NPL ratio

0.9 0.9 0.9

Jun.14 Mar.15 Jun.15

Loan-loss provisions and

cost of risk

(constant €m, %)

0.2 0.2 0.2

28 31 32

2Q14 1Q15 2Q15

Loan-loss provisions Cost of risk

July 31st 2015

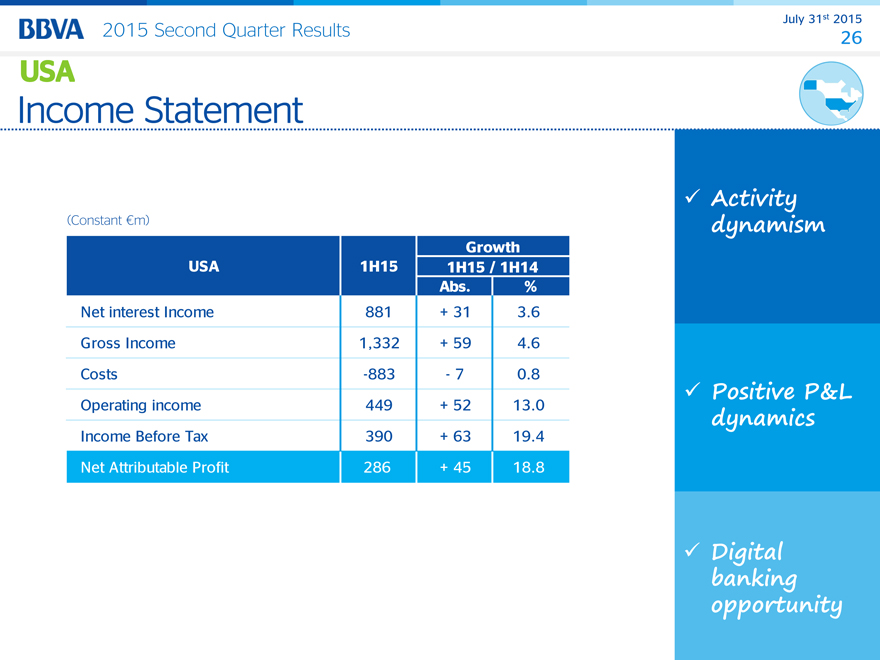

2015 Second Quarter Results 26

USA Risk

Income Statement

(Constant €m)

Growth

USA 1H15 1H15 / 1H14

Abs. %

Net interest Income 881 + 31 3.6

Gross Income 1,332 + 59 4.6

Costs -883 —7 0.8

Operating income 449 + 52 13.0

Income Before Tax 390 + 63 19.4

Net Attributable Profit 286 + 45 18.8

Activity dynamism

Positive P&L dynamics

Digital banking opportunity

July 31st 2015

income statement USA

2015 Second Quarter Results 27

Business Activity

(constant €, %)

Lending* Cust. Funds

-2,2%

+13.0% +9.7%

(Jun.15/Jun. -2,2% 14) (Jun.15/Jun.14)

* Gross loans and advances to customers

Note: Activity excludes repos; customer funds includes promissory notes

NII + Fees Gross Income

(constant €m) (constant €m)

+9.4% +7.4%

1,562 1,630 1,709 1,687 1,746 1,812

+4.8% +3.8%

2Q14 1Q15 2Q15 2Q14 1Q15 2Q15

Operating Income

(constant €m)

+7.5%

1,067 1,101 1,147

+4.2%

2Q14 1Q15 2Q15

July 31st 2015

2015 Second Quarter Results 28

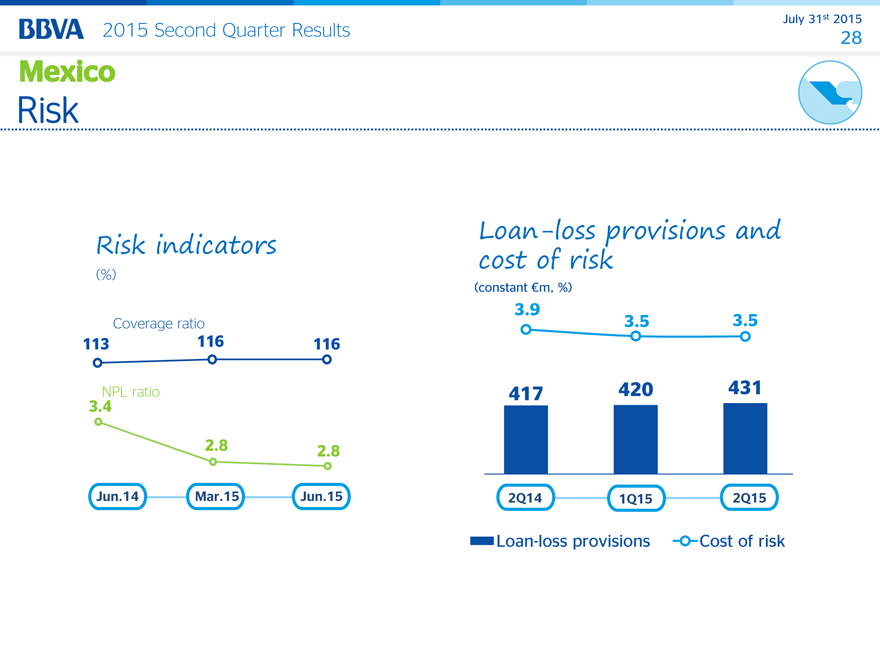

Risk indicators

(%) Mexico Activity and Results

Coverage ratio

113 116 116

NPL ratio

3.4

2.8 2.8

Jun.14 Mar.15 Jun.15

Loan-loss provisions and

cost of risk

(constant €m, %)

3.9 3.5 3.5

417 420 431

2Q14 1Q15 2Q15

Loan-loss provisions Cost of risk

July 31st 2015

2015 Second Quarter Results 29

(Constant m)

Growth

Mexico 1H15 1H15 / 1H14

Abs. %

Net interest Income 2,734 + 228 9.1

Gross Income 3,558 + 221 6.6

Costs -1,309 - 80 6.5

Operating income 2,248 + 141 6.7

Income Before Tax 1,380 + 116 9.2

Net Attributable Profit 1,041 + 83 8.6

Double-digit business activity

Portfolio mix change

Sound and improving risk indicators

July 31st 2015

2015 Second Quarter Results 30

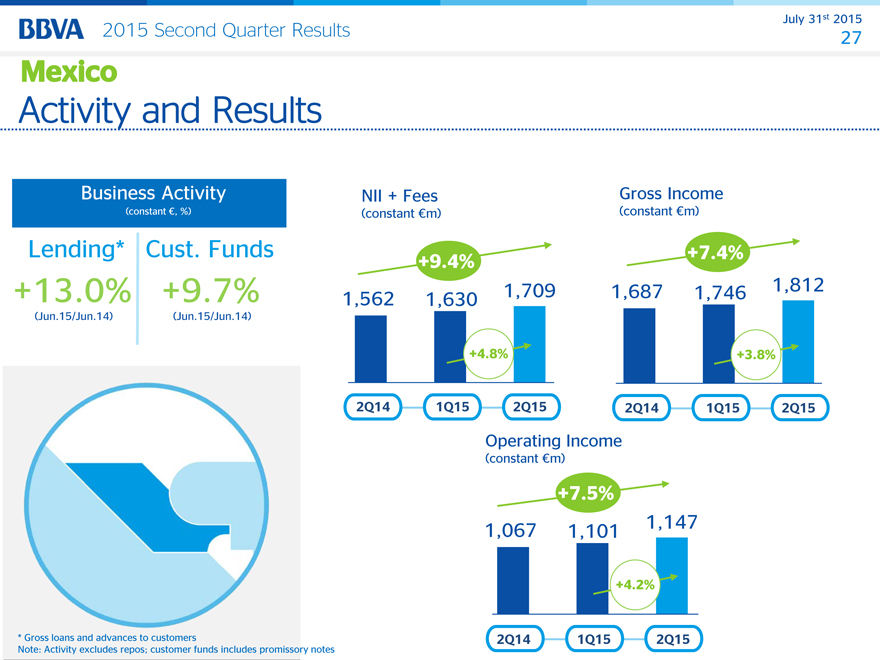

Business Activity

(constant €, %) Mexico income statement

Lending* Cust. Funds

-2,2%

+12.2% +14.5%

(Jun.15/Jun. -2,2% 14) (Jun.15/Jun.14)

*Gross loans and advances to customers

Note: activity excluding repos; customer funds includes promissory notes

NII + Fees Gross Income

(constant €m) (constant €m)

+10.0% +10.4%

886 930 974 1,001 1,064 1,105

+4.7% +3.9%

2Q14 1Q15 2Q15 2Q14 1Q15 2Q15

Operating Income

(constant €m)

+9.2%

613

561 576

+6.5%

2Q14 1Q15 2Q15

July 31st 2015

2015 Second Quarter Results 31

Risk indicators

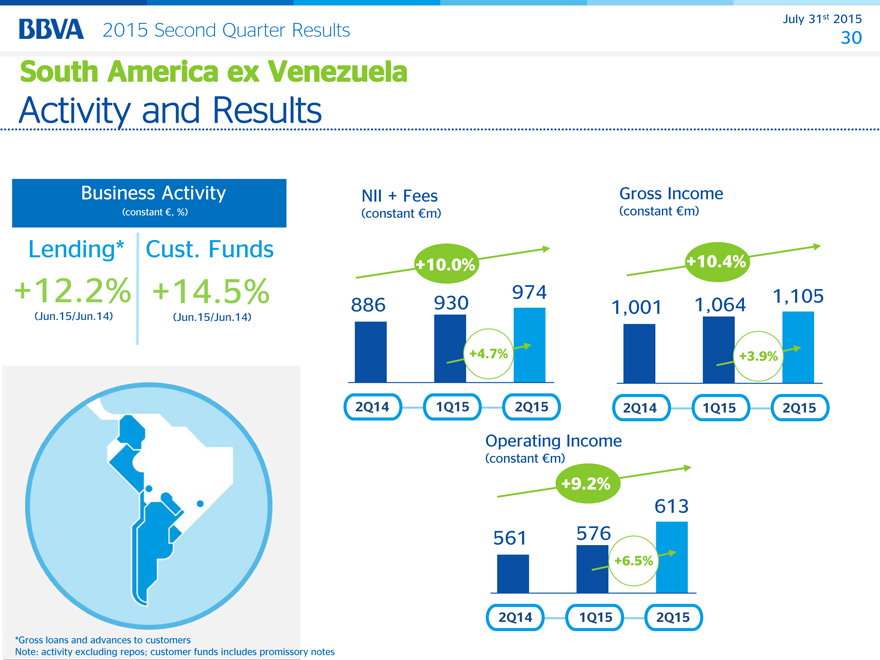

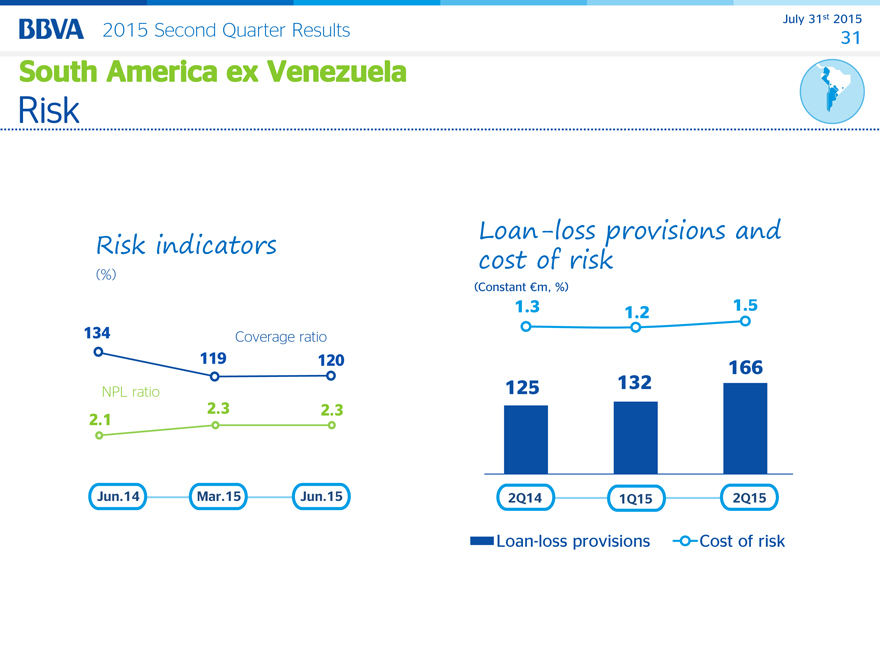

South America ex Venezuela

Activity and Results

(%)

134 Coverage ratio

119 120

NPL ratio

2.1 2.3 2.3

Jun.14 Mar.15 Jun.15

Loan-loss provisions and

cost of risk

(Constant €m, %)

1.3 1.2 1.5

166

125 132

2Q14 1Q15 2Q15

Loan-loss provisions Cost of risk

July 31st 2015

2015 Second Quarter Results 32

(Constant €m)

Growth

South America ex Venezuela 1H15 1H15 / 1H14

Abs. %

Net interest Income 1,558 + 158 11.3

Gross Income 2,169 + 236 12.2

Costs -981 —114 13.2

Operating income 1,189 + 122 11.4

Income Before Tax 874 + 75 9.4

Net Attributable Profit 465 + 36 8.4

Activity dynamism translated into the P&L

Transforming distribution network

July 31st 2015

2015 Second Quarter Results 33

South America ex Venezuela

income statement

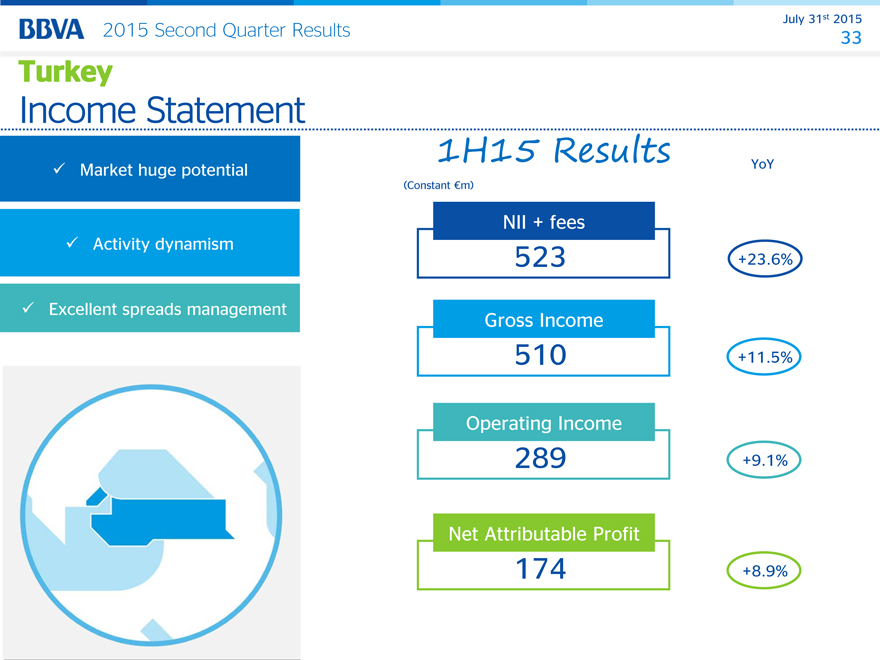

Market huge potential Activity dynamism

Excellent spreads management

YoY

(Constant €m)

NII + fees

523 +23.6%

Gross Income

510 +11.5%

Operating Income

289 +9.1%

Net Attributable Profit

174 +8.9%

July 31st 2015

2015 Second Quarter Results 34

Takeaways Turkey

income statement

July 31st 2015

2015 Second Quarter Results 35

Annex

July 31st 2015

2015 Second Quarter Results 36

Rest of Eurasia

265 €m

South America 2%

2,169 €m 19% 32% Spain

3,655 €m

Gross

Mexico Income USA

1H15

3,558 €m 1,332 €m

12%

31%

4% Turkey*

510 €m

Note: Figures excluding Corporate activities, Venezuela and including Catalunya Caixa.

* In a theoretical exercise of fully consolidation of Garanti Bank, the pro-forma weight of Turkey’s gross income would be 16%.

July 31st 2015

2015 Second Quarter Results 37

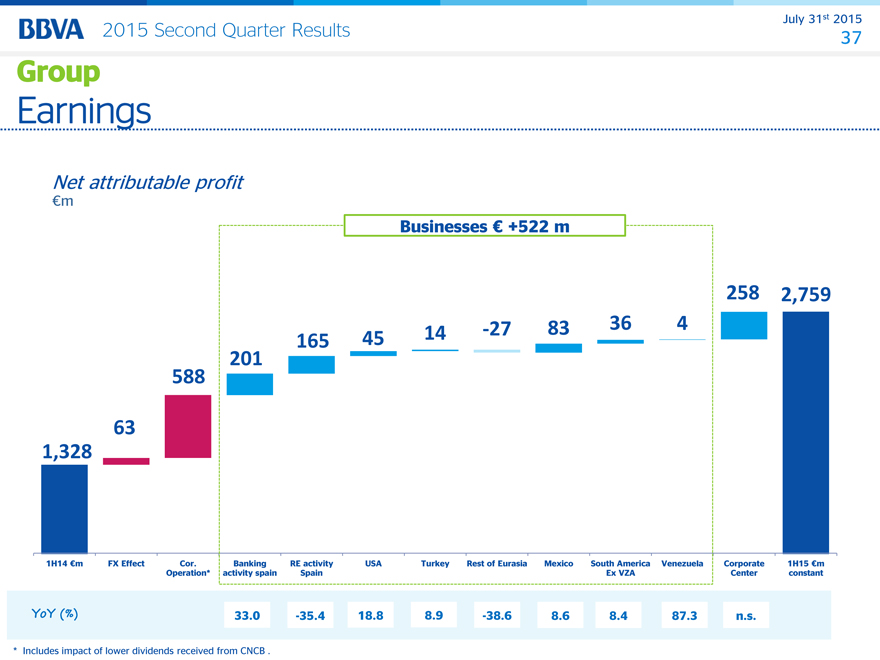

Net attributable profit

€m

Businesses € +522 m

258 2,759

165 45 14 -27 83 36 4

201

588

63

1,328

1H14 €m FX Effect Cor. Banking RE activity USA Turkey Rest of Eurasia Mexico South America Venezuela Corporate 1H15 €m

Operation* activity spain Spain Ex VZA Center constant

YoY (%) 33.0 -35.4 18.8 8.9 -38.6 8.6 8.4 87.3 n.s.

* Includes impact of lower dividends received from CNCB .

July 31st 2015

2015 Second Quarter Results 38

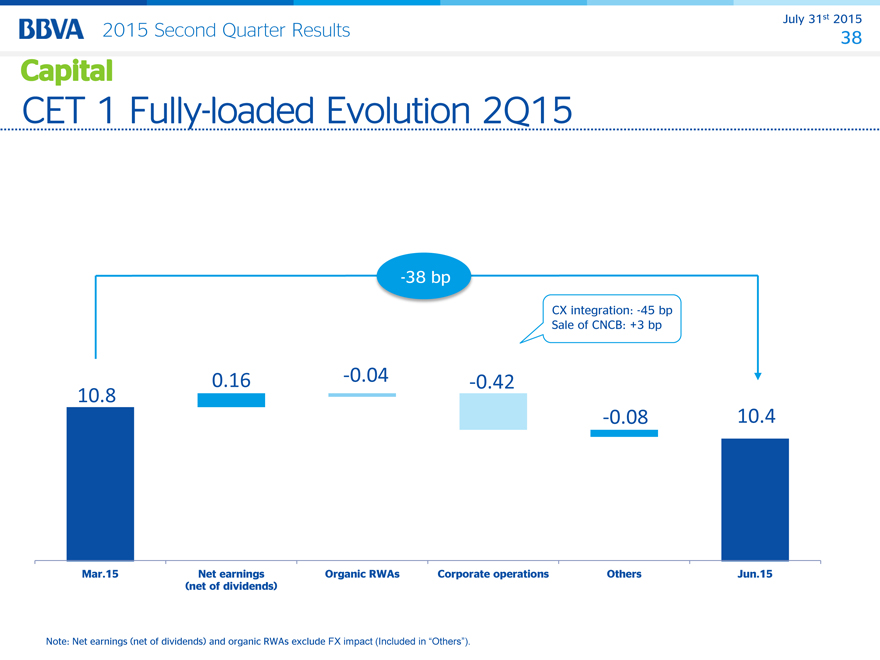

-38 bp

CX integration: -45 bp

Sale of CNCB: +3 bp

10.8 0.16 -0.04 -0.42

-0.08 10.4

Mar.15 Net earnings Organic RWAs Corporate operations Others Jun.15

(net of dividends)

July 31st 2015

2015 Second Quarter Results 39

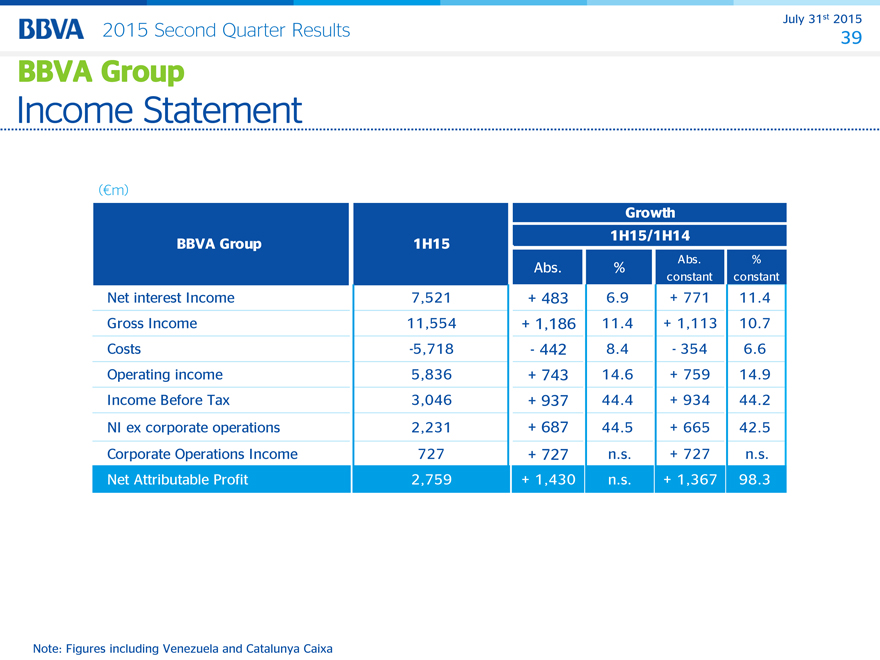

(€m)

Growth

BBVA Group 1H15 1H15/1H14

Abs. % Abs. %

constant constant

Net interest Income 7,521 + 483 6.9 + 771 11.4

Gross Income 11,554 + 1,186 11.4 + 1,113 10.7

Costs -5,718 —442 8.4 —354 6.6

Operating income 5,836 + 743 14.6 + 759 14.9

Income Before Tax 3,046 + 937 44.4 + 934 44.2

NI ex corporate operations 2,231 + 687 44.5 + 665 42.5

Corporate Operations Income 727 + 727 n.s. + 727 n.s.

Net Attributable Profit 2,759 + 1,430 n.s. + 1,367 98.3

Note: Figures including Venezuela and Catalunya Caixa

July 31st 2015

2015 Second Quarter Results 40

Coverage ratio (%)

61 61 63 63 65

NPL ratio (%)

54.8 55.3 55.4 54.0 54.3

Jun.14 Sep.14 Dec.14 Mar.15 Jun.15

July 31st 2015

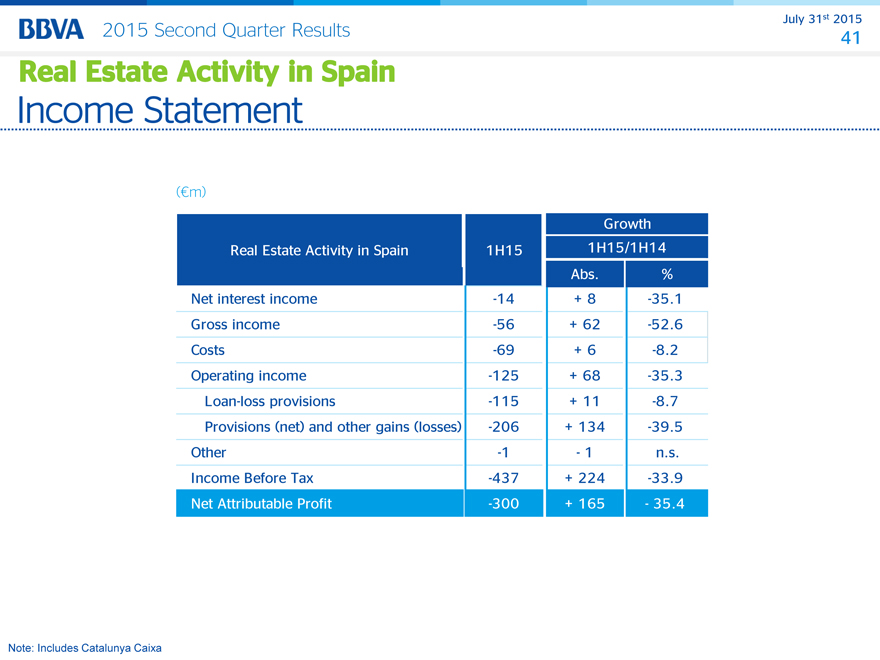

2015 Second Quarter Results 41

(€m)

Growth

Real Estate Activity in Spain 1H15 1H15/1H14

Abs. %

Net interest income -14 + 8 -35.1

Gross income -56 + 62 -52.6

Costs -69 + 6 -8.2

Operating income -125 + 68 -35.3

Loan-loss provisions -115 + 11 -8.7

Provisions (net) and other gains (losses) -206 + 134 -39.5

Other -1 —1 n.s.

Income Before Tax -437 + 224 -33.9

Net Attributable Profit -300 + 165 —35.4

Note: Includes Catalunya Caixa

July 31st 2015

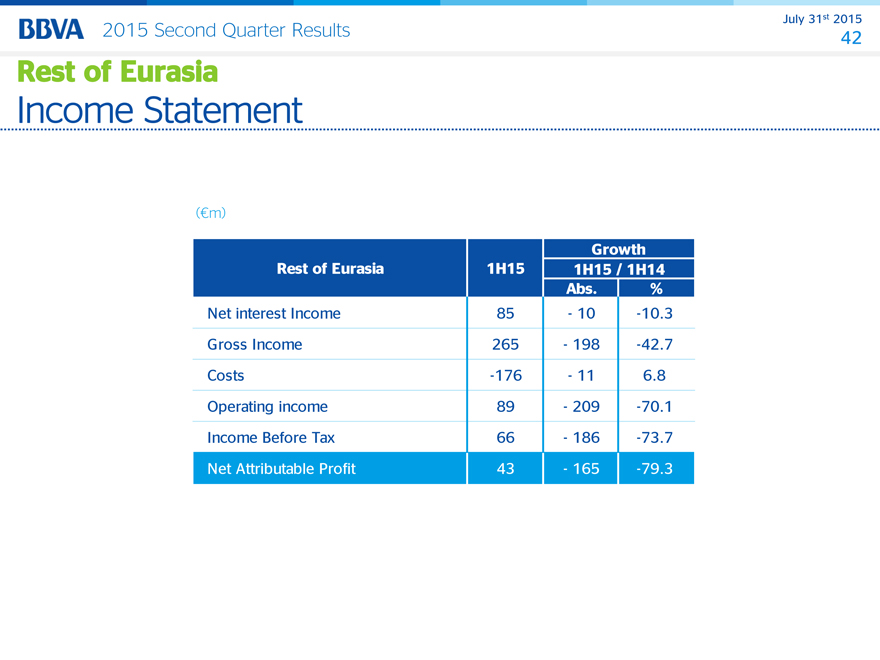

2015 Second Quarter Results 42

(€m)

Growth

Rest of Eurasia 1H15 1H15 / 1H14

Abs. %

Net interest Income 85 —10 -10.3

Gross Income 265 — 198 -42.7

Costs -176 —11 6.8

Operating income 89 — 209 -70.1

Income Before Tax 66 — 186 -73.7

Net Attributable Profit 43 — 165 -79.3

July 31st 2015

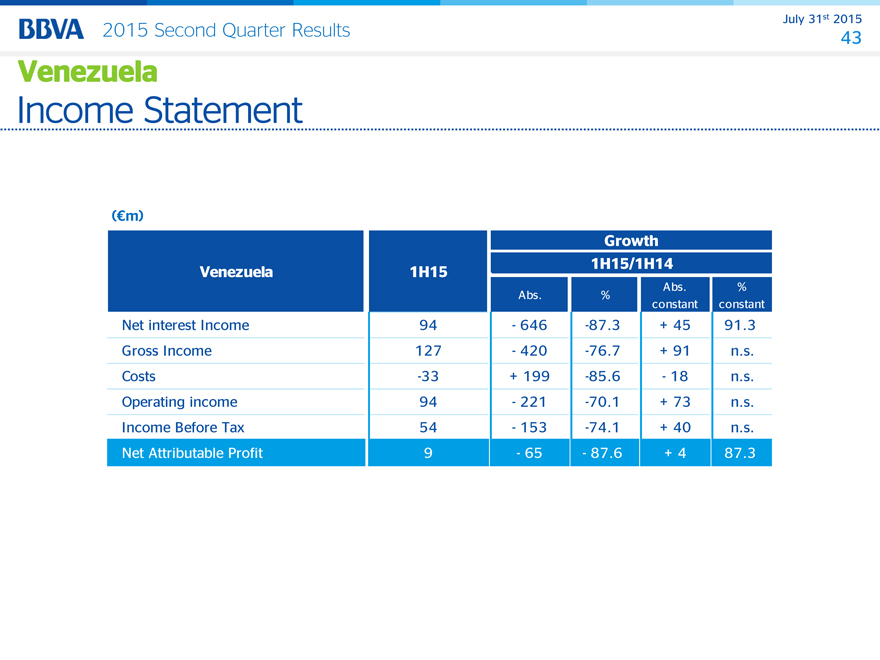

2015 Second Quarter Results 43

(€m)

Growth

Venezuela 1H15 1H15/1H14

Abs. %

Abs. %

constant constant

Net interest Income 94 — 646 -87.3 + 45 91.3

Gross Income N 127 — 420 -76.7 + 91 n.s.

Costs g -33 + 199 -85.6 —18 n.s.

Operating income 94 — 221 -70.1 + 73 n.s.

Income Before Tax 54 — 153 -74.1 + 40 n.s.

Net Attributable Profit B 9 —65 —87.6 + 4 87.3

July 31st 2015

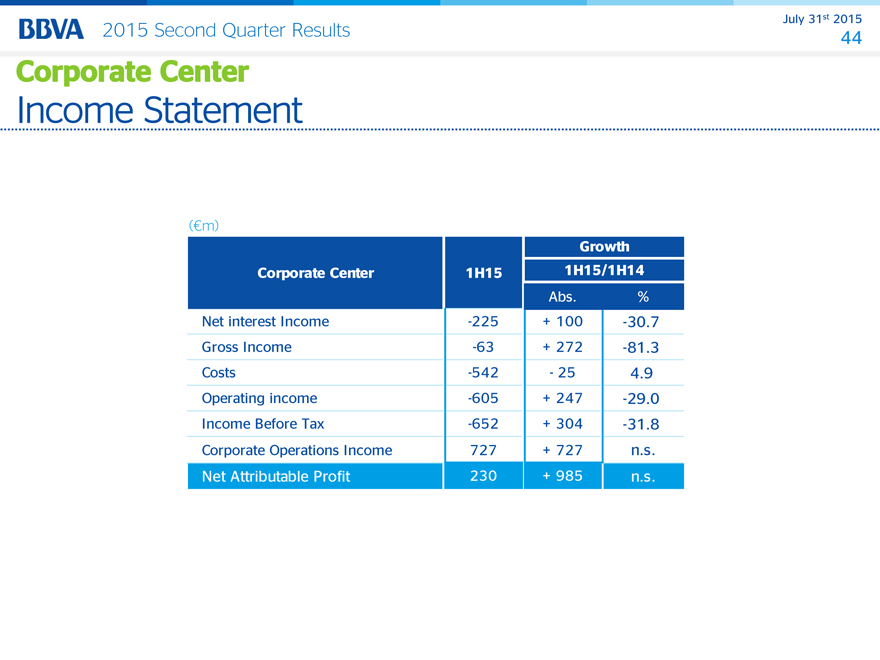

2015 Second Quarter Results 44

(€m)

Growth

Corporate Center 1H15 1H15/1H14

Abs. %

Net interest Income -225 + 100 -30.7

Gross Income -63 + 272 -81.3

Costs -542 —25 4.9

Operating income -605 + 247 -29.0

Income Before Tax -652 + 304 -31.8

Corporate Operations Income 727 + 727 n.s.

Net Attributable Profit 230 + 985 n.s.

July 31st 2015

2015 Second Quarter Results 45

Jun-15 vs. Jun-14

(constant €, %)

Gross Customer

loans * Funds *

Spain +10.8% +14.3%

USA +12.9% +9.0%

Turkey +21.0% +26.8%

Mexico +13.0% +9.7%

South America** +12.2% +14.5%

(*) Activity ex repos. Includes Catalunya Caixa. Customer Funds include promissory notes. (**) Figures exclude Venezuela

July 31st 2015

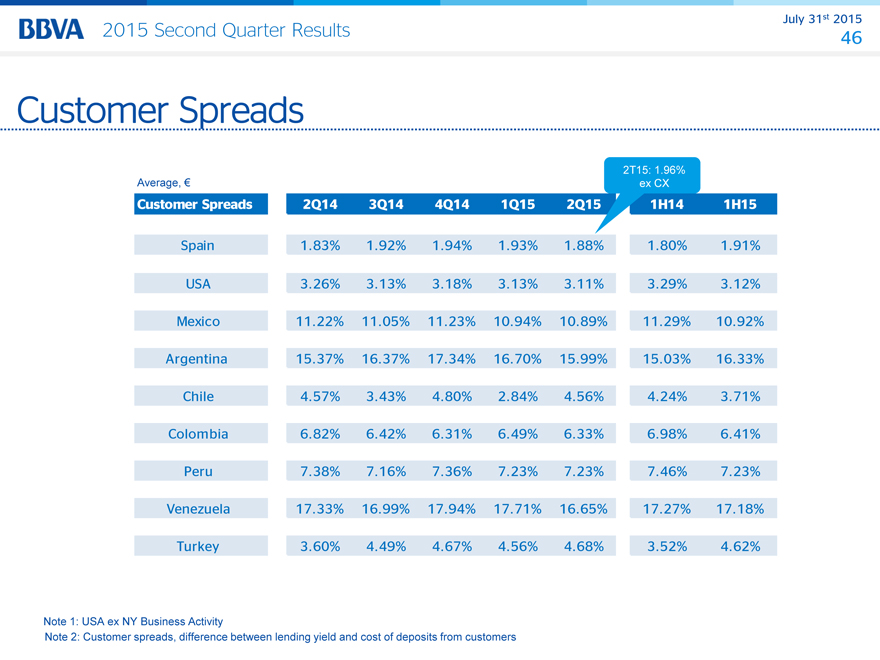

2015 Second Quarter Results 46

2T15: 1.96%

Average, € ex CX

Customer Spreads 2Q14 3Q14 4Q14 1Q15 2Q15 1H14 1H15

Spain 1.83% 1.92% 1.94% 1.93% 1.88% 1.80% 1.91%

USA 3.26% 3.13% 3.18% 3.13% 3.11% 3.29% 3.12%

Mexico 11.22% 11.05% 11.23% 10.94% 10.89% 11.29% 10.92%

Argentina 15.37% 16.37% 17.34% 16.70% 15.99% 15.03% 16.33%

Chile 4.57% 3.43% 4.80% 2.84% 4.56% 4.24% 3.71%

Colombia 6.82% 6.42% 6.31% 6.49% 6.33% 6.98% 6.41%

Peru 7.38% 7.16% 7.36% 7.23% 7.23% 7.46% 7.23%

Venezuela 17.33% 16.99% 17.94% 17.71% 16.65% 17.27% 17.18%

Turkey 3.60% 4.49% 4.67% 4.56% 4.68% 3.52% 4.62%

Note 1: USA ex NY Business Activity

Note 2: Customer spreads, difference between lending yield and cost of deposits from customers

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Banco Bilbao Vizcaya Argentaria, S.A. | ||||||

| Date: July 31 , 2015 | By: | /s/ María Ángeles Peláez | ||||

| Name: | María Ángeles Peláez | |||||

| Title: | Authorized Representative | |||||