UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of March, 2021

Commission file number: 1-10110

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

(Exact name of Registrant as specified in its charter)

BANK BILBAO VIZCAYA ARGENTARIA, S.A.

(Translation of Registrant’s name into English)

Calle Azul 4,

28050 Madrid

Spain

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

| BBVA. PILLAR III 2020 | P. 1 |

The English language version of this report is a free translation from the original, which was prepared in Spanish. All possible care has been taken, to ensure that the translation is an accurate presentation of the original. However, in all matters of interpretation, views or opinion expressed in the original language version of the document in Spanish take precedence over the translation.

| BBVA. PILLAR III 2020 | INDEX | P. 2 |

Index

| 4 | ||||||

| 7 | ||||||

| 11 | ||||||

| 12 | ||||||

| 13 | ||||||

| 14 | ||||||

| 16 | ||||||

| 18 | ||||||

1. | 22 | |||||

| 1.1. | Corporate name and differences between the consolidated group for the purposes of solvency regulations and accounting criteria | 23 | ||||

1.2. | 27 | |||||

1.3. | Exemptions from capital requirements at the individual or sub-consolidated level | 27 | ||||

2. | 28 | |||||

2.1. | 29 | |||||

2.2. | 30 | |||||

2.3. | 33 | |||||

2.4. | 34 | |||||

2.5. | 36 | |||||

2.6. | 38 | |||||

3. | 40 | |||||

3.1. | 41 | |||||

3.2. | 41 | |||||

3.3. | 103 | |||||

3.4. | 114 | |||||

3.5. | 117 | |||||

3.6. | 124 | |||||

| BBVA. PILLAR III 2020 | INDEX | P. 3 |

| BBVA. PILLAR III 2020 | GLOSSARY OF TERMS | P. 4 |

ACRONYM | DESCRIPTION | |

| ALM (Asset - Liability Management) | Mechanism for managing structural balance-sheet risk due to potential imbalances between assets and liabilities due to different types of factors (interest rate, exchange rate, liquidity, etc.) | |

| AMA | Advanced method for calculating the own funds requirements for operational risk | |

| AT1 (Additional Tier 1) | Additional Tier 1 capital consisting of hybrid instruments, mainly CoCos and preferred shares | |

| Basel III | Package of proposals for reform of banking regulation, published as of December 16, 2010 and with a period of gradual implementation | |

| BCBS (Basel Committee on Banking Supervision) | Basel Committee on Banking Supervision. International cooperation forum on banking supervision to increase the quality of banking supervision worldwide | |

| CCyB (Countercyclical Buffer) | Countercyclical buffer, the part of a set of macroprudential instruments designed to help counteract the procyclicality of the financial system | |

| CCF (Credit Conversion Factor) | Credit conversion factor. The ratio between the current available amount of a commitment that could be used and would therefore be outstanding at the time of default, and the current available amount of the commitment | |

| CCP (Central Counterparty Clearing House) | An entity that liaises between counterparties, acting as a buyer when dealing with sellers and as a seller when dealing with buyers | |

| CDS (Credit Default Swap) | Financial derivative between a beneficiary and a guarantor through which the beneficiary pays the guarantor a premium in exchange for receiving protection from possible credit events over a period of time | |

| CET1 (Common Equity Tier 1) | Common Equity Tier 1: the entity’s capital of the highest quality (see paragraph 2.1) | |

| Counterparty Credit Risk | The credit risk corresponding to derivative instruments, repurchase and reverse repurchase transactions, securities or commodities lending or borrowing transactions and deferred settlement transactions | |

| CoCo (Contingent Convertible) | Convertible contingent bond. Hybrid issues with debt and equity elements convertible | |

| Credit Risk | into shares Credit risk is based on the possibility that one party to the financial instrument’s contract will fail to meet its contractual obligations on the grounds of insolvency or inability to pay and will cause a financial loss for the other party | |

| CRM (Credit Risk Mitigation) | Credit Risk Mitigation: a technique used by the institution to reduce the credit risk associated with one or more exposures that the institution still maintains | |

| CRR / CrD IV | Solvency regulation on prudential requirements of credit institutions and investment firms (EU Regulation 575/2013) | |

| CVA (Credit Valuation Adjustment) | Valuation adjustments for counterparty credit risk | |

| DlGD (Downturn loss Given Default) | Severity in a period of stress in the economic cycle | |

| D-SIB (Domestic Systemically Important Bank) | Domestic Systemically Important Bank | |

| EAD (Exposure at default) | Maximum loss at the time of the counterparty entering into default | |

| EBA (European Banking authority) | European Banking Authority. Independent institution responsible for promoting the stability of the financial system, the transparency of financial markets and products and the protection of depositors and investors | |

| EC (Economic Capital) | The amount of capital considered necessary to cover unexpected losses if actual losses are greater than expected losses | |

| ECB (European Central Bank) | Central bank of the countries of the European Union that have the euro as their currency | |

| ECAI (External Credit assessment Institutions) | External Credit Assessment Agency designated by the entity | |

| El (Expected Loss) | The ratio between the amount expected to be lost in an exposure, due to potential non-payment by a counterparty or dilution over a period of one year, and the amount due at the time of non-payment | |

| ERBA (External Rating Base Aproach) | Methodology for estimating RWAs of securitisations from external ratings | |

| Environmental, social and governance (ESG) | Environmental, social and good corporate governance criteria, the main objective of which is to contribute to sustainable development | |

| FRTB (Fundamental Review of the Trading Book) | A set of reforms proposed by the BCBS on the market risk framework, with the aim of improving the design and consistency of market risk capital standards | |

| FsB (financial Stability Board) | Financial Stability Board. An international body that pursues the effectiveness and stability of the international financial system, monitoring it and publishing recommendations | |

| FTD (First to default) | Derivative by which both parties negotiate protection against the first default by any of the entities that form part of the basket | |

| GRM (Global Risk Management) | Global Risk Management | |

| GRMC (Global Risk Management Committee) | Global Risk Management Committee | |

| G-SIBS (Global Systemically Important Banks) | Financial institutions that, because of their large size, market importance and interconnectedness, could cause a serious crisis in the international financial system in the event of economic problems | |

| IAA (Internal Assessment Approach) | Internal evaluation method for the calculation of securitisation exposures in the banking book | |

| BBVA. PILLAR III 2020 | GLOSSARY OF TERMS | P. 5 |

| ICAAP (Internal Capital Adequacy Assessment Process) | Internal Capital Adequacy Assessment Process | |

| IFRS 9 (International Financial Reporting Standards – Financial Instruments) | International Financial Reporting Standards for Financial Instruments which entered into force on January 1, 2018, replacing IAS 39 in relation to the classification and valuation of financial assets and liabilities, the impairment of financial assets and the accounting of hedges | |

| ILAAP (Internal Liquidity Adequacy Assessment Process) | Internal Liquidity Adequacy Assessment Process | |

| IMA (Internal Model Approach) | Internal model approach for calculating exposure due to market risk | |

| IMM (Internal Model Method) | Internal model method for calculating exposure due to counterparty risk | |

| IRB (Internal Rating-based approach) | Internal model method for calculating exposure due to credit risk, based on internal ratings. This method can be broken down into two types, depending on the estimations set by the Supervisor or the own ones: FIRB (Foundation IRB) and AIRB (Advanced IRB) | |

| IRBA (Internal Risk Base Approach) | Methodology for estimating RWAs of securitisations from internal ratings | |

| IRC (Incremental Risk Capital) | Charge applied to the market risk exposure calculated by the internal method that quantifies the risk not captured by the VaR model, specifically in migration and default events | |

| LCR (Liquidity Coverage Ratio) | Liquidity coverage ratio | |

| LDP (Low Default Portfolios) | Low default portfolios | |

| LGD (Loss Given Default) | Severity or amount to be lost in the event of non-payment | |

| LGD BE (Loss Given Default Best Estimate) | “Actual” loss from default portfolio | |

| Liquidity Risk | Risk of an entity having difficulties in duly meeting its payment commitments, or where, to meet them, it has to resort to funding under burdensome terms which may harm the entity’s image or reputation | |

| LMUS (Liquidity Management Units) | Group entities with financial self-sufficiency created with the aim of preventing and limiting liquidity risk, preventing it from spreading in a crisis that could affect only one or more of these Entities | |

| LR (Leverage Ratio) | Leverage ratio: a measure that relates a company’s indebtedness and assets, calculated as level 1 capital divided by the entity’s total exposure | |

| LRLGD (Long Run Loss Given Default) | Long-term severity (loss given default) | |

| LtSCD (Loan to Stable Customer Deposits) | Ratio that measures the relationship between net credit investment and stable customer resources | |

| Market Risk | Risk due to the possibility that there may be losses in the value of positions held due to movements in the market variables that affect the valuation of financial products and assets in trading activity | |

| MDA (Maximum Distributable Amount) | Trigger by which the ECB restricts the capacity to pay out dividends | |

| MREL (Minimum Required Eligible Liabilities) | Minimum requirement of own funds and eligible liabilities. New requirement faced by European banks, which aims to create a buffer of solvency that absorbs the losses of a financial entity in the event of resolution without jeopardizing taxpayers’ money. The level of this buffer is determined individually for each banking group based on their level of risk and other particular characteristics | |

| MTN (Medium Term Note) | Notes accounted as Issuances designated at fair value through P&L considered equivalent to senior issuances for liquidity | |

| NCAHS | Non-Current Assets Held for Sale | |

| NClHS | Non-Current Liabilities Held for Sale | |

| NSFR | Net Stable Funding Ratio | |

| OE (Original Exposure) | Gross amount that the entity may lose in the event that the counterparty cannot meet its contractual payment obligations, regardless of the effect of guarantees or credit improvements or credit risk mitigation operations | |

| Operational Risk (OR) | BBVA defines operational risk (OR) as risk that may cause losses as a result of human error; inadequate or defective internal processes; inadequate conduct towards customers, in the markets or against the company; failures, interruptions or deficiencies in systems or communications; theft, loss or misuse of information, as well as deterioration of its quality; internal or external fraud including, in all cases, fraud resulting from cyber-attacks; theft or physical damage to assets or persons; legal risks; risks resulting from workforce and occupational health management; and inadequate service provided by suppliers | |

| PD (Probability of Default) | Probability of non-payment by a counterparty over a period of one year | |

| PD-TTC (PD Through the Cycle) | Probability of Default throughout the business cycle | |

| PIT (Point-In-Time) | Approach for calculating provisions under which PD and LGD parameters must be adapted at each moment in time | |

| P2G | Pillar 2 Capital Guidance | |

| P2R | Pillar 2 Capital Requirement | |

| RW (Risk Weight) | Degree of risk applied to exposures (%) | |

| RWAs (Risk-Weighted assets) | Risk exposure of the entity weighted by a percentage derived from the applicable standard (standardised approach) or internal models | |

| SFTs | Securities financing transactions | |

| SREP (Supervisory Review and Evaluation Process) | Supervisory Review and Evaluation Process | |

| Structural Risk | This risk is divided into Structural Interest-Rate Risk (movements in market interest rates that cause changes in an entity’s net interest income and book value) and Structural Exchange-Rate Risk (exposure to variations in exchange rates originating in the Group’s foreign companies and in the provision of funds to foreign branches financed in a different currency from that of the investment) | |

| BBVA. PILLAR III 2020 | GLOSSARY OF TERMS | P. 6 |

| Synthetic Securitisation | A type of operation where the loan portfolio is not typically transferred to a fund; on the contrary, the credit remains in the balance sheet of the corresponding entity, but this transfers the default risk to a third party. The objective of this type of instrument is the transmission of balance risk and capital release. Normally, the assignment of risk is usually made through a derivative (CDS) or through a financial guarantee | |

| TIER I (Tier One Capital) | Capital built by instruments that are able to absorb losses when the entity is in operation. It consists of CET1 and AT1 | |

| TIER II (Tier Two Capital) | Supplementary capital consisting of instruments, mainly subordinated debt, revaluation reserves and hybrid instruments, which will absorb losses when the entity is not viable | |

| TLAC (Total Loss Absorbing Capacity) | Total loss absorption capacity: Regulatory framework approved by the FSB with the aim of ensuring that global systemically important entities (G-SIB) maintain a minimum level of eligible instruments and liabilities to ensure that in resolution procedures, and immediately thereafter, the essential functions of the entity can be maintained without jeopardizing taxpayers’ money or financial stability | |

| Traditional Securitisation | Operation through which an entity is capable of transforming a series of heterogeneous and illiquid financial assets into liquid homogeneous instruments (usually guarantees or bonds) and marketable securities, managing to transfer the risk of the assets in most cases while liquidity is preserved | |

| TRIM (Targeted Review of Internal Models) | Control model implemented by the ECB aimed at reducing inconsistencies and the variability in banks’ internal models used to calculate their risk-weighted assets | |

| Var (Value at Risk) | A risk measurement model that provides a prediction of the maximum loss that the entity’s trading portfolios might experience as a result of market price variations over a given time horizon and for a specific confidence interval | |

| BBVA. PILLAR III 2020 | INDEX OF TABLES | P. 7 |

| BBVA. PILLAR III 2020 | INDEX OF TABLES | P. 8 |

| BBVA. PILLAR III 2020 | INDEX OF TABLES | P. 9 |

| BBVA. PILLAR III 2020 | INDEX OF TABLES | P. 10 |

| BBVA. PILLAR III 2020 | INDEX OF CHARTS | P. 11 |

| BBVA. PILLAR III 2020 | EXECUTIVE SUMMARY | P. 12 |

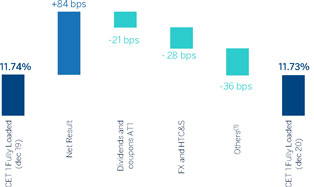

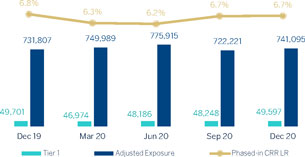

BBVA’s consolidated phased-in CET1 ratio stood at 12.15% at the close of December 2020, which increased by +17 basis points compared to 2019, mainly due to:

| • | The positive generation of organic results for the Group, which has enabled it to cover the growth of risk-weighted assets (RWAs), and the relative stabilisation of the financial markets that began during the second quarter. This was largely the result of the economic stimulus measures and guarantee programmes announced by various national and supranational authorities, as well as the approval by the European Parliament and the Council of Capital Requirements Regulation 2020/873 (known as the CRR Quick Fix). Here, the positive impact of +19 basis points due to the regulatory change in the deduction of intangible (software) assets stands out. |

| • | The effect of transitional adjustments of IFRS9 impact on the solvency indicators, and subsequent changes in response to the COVID-19 pandemic. |

| • | A positive impact of +7 basis points at the CET1 level due to the execution of the agreement reached with Allianz to jointly boost the non-life insurance business in Spain. |

Additionally, the CET1 capital as of December 2020 includes the effect of the Shareholders’ remuneration of €0.059 gross per share, which amounts to a maximum value of approximately €393m (equivalent to 11 CET1 basis points), calculated based on the ECB’s recommendation.

In fully loaded terms, the CET1 ratio stood at 11.73%, similar to the level recorded by the Group in December 2019 (11.74%).

This ratio does not include the positive impact of the sale of BBVA USA and other companies in the United States, which, according to the current estimate and taking the capital level of December 2020 as a reference, would place the fully-loaded CET1 ratio at 14.58%. This also does not include the effect of the completion of the sale of BBVA Paraguay, which would have an approximate impact of +6 basis points and will be recorded in the first quarter of 2021.

The Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) in the Group has remained well above 100% throughout 2020. At December 31, 2020, these ratios stood at 149% (185% considering the excess liquidity of the subsidiaries) and 127%, respectively. Although these requirements are only established at Group level, this minimum is comfortably exceeded in all subsidiaries.

As for the leverage ratio, as of December 31, 2020, the fully loaded ratio was 6.49%, above the minimum required ratio of 3%, still comparing very favorably with the rest of the Peer Group1. This ratio does not include the impact of the sale of BBVA USA, which, according to the current estimate and taking December 2020 as a reference, would place the leverage ratio at 7.74%

The following sections detail matters relating to the Group’s solvency. These are supplemented by information included in the Group’s Consolidated Financial Statements and Management Report, which also contain the Group’s main activity and profitability indicators.

| 1. | The peer group of the Group consists of the following entities: Barclays, BNP Paribas, Crédit Agricole, Commerzbank, Deutsche Bank, HSBC, Intesa Sanpaolo, Lloyds Bank, RBS, Santander, Société Générale, UBS and UniCredit. |

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 13 |

| 14 | ||||

| 16 | ||||

| 18 | ||||

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 14 |

Regulatory framework and regulatory developments in 2020

As a Spanish credit institution, BBVA is subject to Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013, on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms (the “CRD IV Directive”) amended by Directive 2019/878/EU (the “CRD V Directive).

The major regulation governing the solvency of credit institutions is (EU) Regulation No. 575/2013 of the European Parliament and of the Council of June 26, 2013, on the prudential requirements for credit institutions and investment firms amending (EU) Regulation No 648/2012 (“CRR” and in conjunction with Directive CRD IV and any implementing measures of CRD IV, “CRD IV”), which is complemented by several binding Regulatory Technical Standards that are directly applicable to all EU member states, without the need to implement national measures. This Regulation has been amended by Regulation 2019/876/EU (“CRR2”) and Regulation 2020/873/EU (“Quick Fix”).

The CRD IV Directive was transposed to Spanish national law by means of the Royal Decree-Law 14/2013, of November 29 (“RD-L 14/2013”), Law 10/2014 of June 26, Royal Decree 84/2015, of February 13 (“RD 84/2015”), Bank of Spain Circular 2/2014 of January 31 and Circular 2/2016 of February 2 (“Bank of Spain Circular 2/2016”). During 2020, the adoption of the amendments proposed by Directive (EU) 2019/878 to the Spanish legal system began through the publication on September 4, 2020 of the proposed amendments to Law 10/2014 as well as RD 84/2015. As of the date of publication of this report, they had not yet been published in the BOE (Boletín Oficial del Estado — Spanish Official Journal).

In the Macroprudential field, Royal Decree 102/2019 was published in March 2019, establishing the Macroprudential Authority of the Financial Stability Board, establishing its legal regime. The aforementioned Royal Decree also develops certain aspects related to the macroprudential tools contained in Royal Decree-Law 22/2018. The draft Bank of Spain Circular on macroprudential tools was open for consultation during February 2021 (this was the Bank of Spain Circular amending Bank of Spain Circular 2/2016, of 2 February, to credit institutions, on supervision and solvency, which completes the adaptation of the Spanish legal system to Directive 2013/36/EU and Regulation (EU) No 575/2013.) This Circular develops measures that the Bank of Spain may decide to put in place, such as a countercyclical buffer for a particular sector, industry limits on exposure concentration, or the establishment of limits and conditions on the granting of loans and other transactions. As of the date of publication of this report, the Circular had not yet been published in the BOE (Boletín Oficial del Estado — Spanish Official Journal).

Regulatory developments in 2020

Major economic disruption caused by the COVID-19 pandemic and the exceptional containment measures have significantly impacted the economy. Businesses have faced disruptions in the supply chain, temporary closures, and reduced demand, while households have faced unemployment and declining incomes. Public authorities at the Union and Member State level have acted proactively to help households and solvent businesses to weather the intense-but-temporary slowdown in economic activity and the consequent shortage of liquidity.

With the aim of mitigating the impact of COVID-19, various bodies have made pronouncements aimed at allowing greater flexibility in terms of implementing accounting and prudential frameworks. Generally speaking, the following initiatives are notable due to their relevance:

| • | In its press release on 12 March in response to COVID-19, the ECB allowed banks to bring forward the use of Additional Tier 1 or Tier 2 capital instruments to partially meet Pillar II requirements (P2R). This measure has been bolstered by the relaxation of the countercyclical capital buffer (CCyB) that has been announced by various national macroprudential authorities, and by other additional measures published by the ECB that have provided institutions with flexibility by allowing them to operate below established P2G levels as well as to use capital and liquidity buffers. |

With regard to dividends, 15 December 2020 saw the ban on paying out dividends (in force since 27 March 2020) lifted, albeit under the recommendation of exercising extreme caution and limiting the maximum amount to be distributed. The ECB expects dividends and share buy-backs to remain below 15% of the adjusted cumulated 2019-2020 profit attributable to the parent company, provided that they do not exceed 20 basis points of Common Equity Tier I in the fourth quarter of 2020. This recommendation is effective until 30 September 2021.

| • | The European Banking Authority (EBA) published guidelines on legislative and non-legislative payment moratoria in April 2020. These guidelines set out the criteria that both public and private legislative and non-legislative payment moratoria must meet in order to avoid the exposures subject to these payment deferrals being automatically reclassified as forbearance or defaulted exposures. According to the EBA’s latest communication on 2 December 2020, these guidelines remain applicable until 31 March 2021. |

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 15 |

Regarding relevant EBA publications on prudential aspects, the guidelines on structural FX (Guidelines on the treatment of structural foreign exchange under Article 352 (2) of the CRR) that were issued on July 1, 2020, stand out. They apply as of January 1, 2022.

| • | The European Parliament and Council adopted Regulation 2020/873 applicable from 27 June 2020 (known as the “CRR Quick Fix”), which amends both Regulation (EU) 575/2013 (CRR) and Regulation 2019/876 (CRR2). The main amendments included in this Regulation are: the extension of the IFRS 9 transitional treatment (affects phased-in ratios only); the non-deductibility of software from CET1 capital (this entered into force on 23 December 2020 following the publication of Delegated Regulation 2020/2176 in the OJEU); the bringing forward of the application of the SME and infrastructure support factor; the possibility of applying a prudential filter that temporarily neutralises the impact on CET1 capital of variation in the value of sovereign debt instruments classified as fair value through other comprehensive income (FVOCI); the flexibilization of aspects associated with market risk (supplemented by related communications from the EBA); and the temporary exclusion of certain exposures to central banks for leverage ratio purposes (ECB Decision 2020/1306, allowing the exclusion of exposures to central banks from the Eurosystem, entered into force on 26 September 2020). With regard to ongoing regulatory changes also concerning prudential matters, the European Commission’s proposal of 24 July 2020 (pending approval by the European Parliament and Council) on amendments to the securitisation framework (known as the “Securitisation Quick Fix”) is noteworthy. |

| • | On 27 March, the Basel Committee announced the deferral by one year (until 1 January 2023) to the implementation date of the Basel III reform (known as Basel IV). |

The EBA published two Calls for Advice in 2020 to support the European Commission in its task of releasing a European proposal to implement this Basel III reform:

| • | Submission of additional analysis for the Call for Advice for the purposes of revising the own fund requirements for credit, operational, market and credit valuation adjustment risk: published on 5 March 2020. |

| • | Basel III Reforms: Updated Impact Study: published on 15 December 2020. |

With regard to public disclosure and supervisory reporting, the main new development is the publication by the EBA on

2 June 2020 of the guidelines setting out the templates to be used to perform the supervisory reporting and disclosure to the market of exposures subject to payment moratoria and public guarantees introduced by Member States in response to the COVID-19 crisis (“Guidelines on reporting and disclosure of exposures subject to measures applied in response to the COVID-19 crisis”). With regard to the measures contained in the “CRR Quick Fix,” the EBA published guidelines on 11 August setting out how to report and disclose said measures (“Guidelines on supervisory reporting and disclosure requirements in compliance with the CRR quick fix”

and “Guidelines amending Guidelines EBA/GL/2018/01 on uniform disclosures under Article 473a of Regulation (EU) No 575/2013 (CRR) on the transitional period for mitigating the impact of the introduction of IFRS 9 on own funds to ensure compliance with the CRR quick fix”). Finally, on November 4, 2020, the EBA published the guidelines on the specification and disclosure of systemic importance indicators, which apply from December 16, 2020 and repeal the previous revised guidelines. of February 29, 2016 (EBA/GL/2016/01). These guidelines apply to entities whose leverage ratio exposure measure exceeds €200 billion.

Since approved regulatory developments (e.g. CRR2) are in place but apply further down the line, the EBA is in the process of reviewing current implementing technical standards (ITS) related to supervisory reporting and public disclosure to reflect changes derived from these regulations. In this sense, the EBA made the following pronouncements throughout 2020:

| 1. | DPM 2.10 Framework: |

| • | On 4 May 2020, the final document on the benchmarking of internal models for the 2021 exercise (“ITS amending Commission Implementing Regulation (EU) 2016/2070 with regard to benchmarking of internal models”) was published. This document is part of the DPM 2.10 framework and to date its publication in the Official Journal of the European Union (OJEU) is pending. |

| 2. | DPM 3.0 Framework: |

| • | On 24 June 2020, the final documents in terms of both reporting (“ITS on supervisory reporting requirements for institutions”) and disclosure (“TS on public disclosures by institutions”) were published. These documents implement the changes introduced by both the CRR2 (Regulation 2019/876) and the Regulation on the minimum loss coverage for non-performing exposures (Regulation 2019/630). Their application date is 28 June 2021, although they are yet to be published in the OJEU. |

| • | On 3 August 2020, the final document on the reporting and disclosure of MREL and TLAC (“ITS on disclosure and reporting of MREL and TLAC”) was published, which implements the changes introduced by BRRD 2 (Regulation 2019/879). Although it is yet to be published in the OJEU, the application date of the reporting requirements is 30 June 2021, while the application date for disclosure requirements varies between those for the TLAC (once the ITS entries into force) and those for the MREL (1 January 2024 at the earliest). |

| 3. | DPM 3.1 Framework: |

| • | ITS on specific supervisory reporting requirements for market risk: on 4 May 2020, the final document on reporting requirements for the new alternative standardised approach for market risk (“FRTB-SA”) was published. It proposes delaying its application date by six months until 1 September 2021. This document is yet to be published in the OJEU. |

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 16 |

The EBA will gradually publish the documents containing the new reporting templates for the new market risk framework, this being the first publication.

| • | ITS amending Commission Implementing Regulation (EU) 2016/2070 with regard to benchmarking of internal models: published on 17 December 2020 and open for consultation until 15 February 2020, it introduces changes for the 2022 exercise on the benchmarking of internal models. |

With regard to the Minimum Requirement for Own Funds and Eligible Liabilities (MREL), on 20 May 2020, the Single Resolution Board (SRB) issued its MREL policy for the 2020 resolution planning cycle, which incorporates the criteria set out in BRRD 2/CRR 2 and establishes new transition periods (intermediate target in 2022 and final target in 2024). With regard to the existing binding targets (set out in the 2018 and 2019 resolution cycles), the SRB has clarified that it will adopt a forward-looking approach for banks that may face difficulties meeting those targets.

Sustainable finance: Towards integration in regulation and prudential supervision

Throughout 2020, progress continued towards ensuring that ESG criteria are integrated into the policies of companies—specifically their financial and risk departments—so that these criteria can fully permeate their actions and corporate culture. The pandemic seems to have been an accelerator in this area as well. At the global level, the Financial Stability Board (FSB) published its assessment of financial authorities’ experience in including physical and transitional climate risks as part of their financial stability monitoring. The Task Force on

Climate-related Financial Disclosures (TCFD), created by the FSB, has published a consultation paper to gather feedback on climate-related forward-looking metrics that are useful for financial sector decision-making. The TCFD has also published important documents on sustainability. These include its third status report, which highlights an increase in disclosures by companies in line with TCFD recommendations; guidance on the analysis of climate-related scenarios and on the integration of climate-related risks into existing risk management processes; and guidance on the analysis of climate-related scenarios for non-financial firms.

The EU continues to integrate sustainability into the financial system and to make progress on developing regulations for this purpose. To this end, the European Commission consulted on its renewed sustainable finance strategy, which is expected to be published in early 2021. It has also consulted on a possible initiative on sustainable corporate governance principles. For their part, the Commission, Council and Parliament agreed on a sustainable finance taxonomy using a common classification system applicable from the close of 2021 for adaptation and mitigation objectives. The European supervisory authorities (ESAs) published a consultation paper with a set of standards covering the disclosure of ESG information. The survey is part of EBA’s work to develop a draft Implementing Technical Standard (ITS) on the disclosure of prudential information regarding ESG risks. It will also be used to monitor the short-term expectations specified in the EBA Action Plan on Sustainable Finance. The EBA has also published for consultation a document on the management and supervision of ESG risks, which covers a wide range of topics (definition of ESG risks and factors, quantitative and qualitative indicators). Lastly, the ECB published its final guidelines on its supervisory expectations regarding climate change and environmental risks at the end of the year.

Contents of the 2020 Prudential Relevance Report

Article 13 of the CRR establishes that the parent entities of the European Union are subject, based on their consolidated situation, to the disclosure requirements set by Part Eight of CRR.

This report provides the prudential information of BBVA Consolidated Group as of December 31, 2020 which has been prepared in accordance with the precepts contained in Part Eight of the CRR, complying with the guidelines published by EBA and the applicable technical implementation standards.

In addition, the main EBA guidelines that apply as of December 31, 2020 are highlighted below:

| • | Guidelines on materiality, proprietary information, and confidentiality, and on the frequency of disclosure of information according to Article 432, sections 1 and 2, and Article 433 of Regulation (EU) No. 575/2013 (EBA/ GL/2014/14). These guidelines detail the process and the criteria to be followed regarding the principles of materiality, proprietary information, confidentiality and the right to omit information, and provide guidance for entities to assess the need to publish information more frequently than the annual one. These guidelines were adopted by the Executive Commission of the Bank of Spain in February 2015. |

| • | Guidelines on disclosure requirements under Part Eight of Regulation (EU) No. 575/2013 (EBA/GL/2016/11). These guidelines provide guidance in relation to the information that entities must disclose in application of the corresponding articles of the Part Eight and with the presentation of said information. These guidelines were adopted by the Executive Commission of the Bank of Spain in October 2017. |

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 17 |

| • | Guidelines on appropriate remuneration policies under Articles 74, Paragraph 3 and 75, Paragraph 2, of Directive 2013/36/EU and disclosure of information under Article 450 of Regulation (EU) No 575/2013 (EBA/GL/2015/22). These guidelines were adopted by the Executive Commission of the Bank of Spain in July 2016. |

| • | Guidelines amending the EBA/GL/2018/01 guidelines regarding the uniform disclosure of information in accordance with article 473 bis of Regulation (EU) No. 575/2013 (CRR) in relation to transitional provisions to mitigate the impact on capital of the introduction of IFRS 9, to ensure compliance with the quick fix carried out in the CRR in response to the COVID-19 pandemic (EBA/ GL/2020/12). These guidelines are applicable from August 11, 2020 until the end of the transitional periods set by articles 468 and 473 bis of the CRR (December 31, 2024 and December 31, 2022, respectively). |

Furthermore, with the goal of promoting transparency and as a transition towards the new DPM 3.0 framework defined by the EBA (see 2020 Regulatory Developments), the BBVA Group has decided to bring forward the adaptation of certain templates with standard formats, taking into account the

Implementing Technical Standards published in June 2020 concerning reporting and disclosure of public information (EBA/ITS/2020/04). These Implementing Technical Standards entry into force on 28 June 2021 and to date its publication in the Official Journal of the European Union (OJEU) is pending.

In those Implementing Technical Standards, the EBA, as mandated by the European Commission in Article 434a of the CRR2, implements the changes introduced by this regulation, integrating most of the public disclosure requirements that were issued in various guidelines and ITS published to date into a single document. In addition, these guidelines also aim to unify, as far as possible, the public information with the information reported to the Supervisor through integration in regulatory reporting and, in some cases, have involved simplifying standard templates that may contain similar information, maintaining only those templates that contain more complete and relevant information, such as those referring to the asset quality of exposures. Together with the aforementioned ITS, the EBA has also published a mapping tool for informational purposes. This document maps the quantitative data in most of the standard templates required in Pillar 3 with supervisory reporting, which has been taken into account when preparing the data in those templates that apply as of the date of the report. The table below sets out the principal changes and the legislative provisions on which they are based.

Table 2019 | Description | ITS applicable on 2019 report | Modificación | Table 2020 | ITS applicable | |||||

| NPL1 | Credit quality of forborne exposures | EBA/GL/2018/10 | Renamed | EU CQ1 | EBA/ITS/2020/04 | |||||

| NPL3 | Credit quality of performing and non-performing exposures by past due days | EBA/GL/2018/10 | Renamed | EU CQ3 | EBA/ITS/2020/04 | |||||

| NPL4 | Performing and non-performing exposures and related provisions | EBA/GL/2018/10 | Renamed | EU CR1 | EBA/ITS/2020/04 | |||||

| NPL9 | Collateral obtainedd obtained by taking possesion and execution processes | EBA/GL/2018/10 | Renamed | EU CQ7 | EBA/ITS/2020/04 | |||||

| Credit quality of exposures by geographic region | New template | EU CQ4 | ||||||||

| Credit quality of loans and advances to non-financial corporations by sector of activity | New template | EU CQ5 | ||||||||

| EU CR1-A | Credit quality of exposures by exposure class and instrument | EBA/GL/2016/11 | Dropped. Requirement covered by EU CR1 | EU CR1 | Art. 442 g), h) CRR | |||||

| EU CR1-B | Credit quality of exposures by industry or counterparty type | EBA/GL/2016/11 | Dropped. Requirement covered by EU CQ5 | EU CQ5 | EBA/GL/2018/10 | |||||

| EU CR1-C | Credit quality of exposures by geographic | EBA/GL/2016/11 | Dropped. Requirement covered by EU CQ4 | EU CQ4 | EBA/GL/2018/10 | |||||

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 18 |

Annex VI to this report contains the correspondence to the articles of Part Eight of the CRR, which apply on the date of the report, with the different headings of the document (or other public documents) where the required information can be found.

The aforementioned annex, together with the other annexes and the tables of this Report, are included in an editable document in order to facilitate its analysis, following the recommendations of the EBA Guidelines. This document is called “Pillar III 2020 – Tables & Annexes”, which is available in the section of financial reports on the Group’s Shareholders and Investors website.

It must be pointed out that the data published in the Prudential Relevance Report (Pillar 3) was prepared in accordance with internal control processes described in the “Standard for the preparation of periodic public information of Banco Bilbao Vizcaya Argentaria, S.A. and BBVA Group”. These policies ensure that the information disclosed in Pillar 3 is subject to the internal control framework defined by the Group, as well as adequate internal and external revision (by an independent expert), in compliance with the aforementioned Implementing Technical Standards.

Regulatory capital requirements

In this regard, Article 92 of the CRR establishes that credit institutions must maintain the following own funds requirements at all times:

| a. | Common Equity Tier 1 capital ratio of 4.5%, calculated as Common Equity Tier 1 capital expressed as a percentage on the total amount of risk-weighted assets. |

| b. | Tier 1 capital ratio of 6%, calculated as the level of tier capital 1 expressed as a percentage of the total amount of risk-weighted assets. |

| c. | Total capital ratio of 8%, calculated as the total own funds expressed as a percentage of the total amount of risk-weighted assets |

Notwithstanding the application of the Pillar 1 requirement, CRD IV allows competent authorities to require credit institutions to maintain a level of own funds higher than the requirements of Pillar 1 to cover types of risk other than those already covered by the Pillar 1 requirement (this power of the competent authority is commonly referred to as “Pillar 2”).

Furthermore, from 2016 and in accordance with CRD IV, credit institutions must comply with the following combined requirement of capital buffers at all times: (i) the capital conservation buffer, (ii) the buffer for global systemically important banks (the “G-SIB” buffer), (iii) the entity-specific countercyclical capital buffer, (iv) the buffer for other systemically important banks (“D-SIB” buffer) and (v) the systemic risk capital buffer. The “combined capital buffer requirement” must be met with Common Equity Tier 1 capital (“CET1”) to cover both minimum capital required by “Pillar 1” and “Pillar 2”.

Both the capital conservation buffer and the G-SIB buffer (where appropriate) will apply to credit institutions as it establishes a percentage greater than 0%.

The buffer for global systemically important banks applies to those institutions on the list of global systemically important banks, which is updated annually by the Financial Stability Board (“FSB”). Considering the fact that BBVA has not appeared on the said list since November 2015 (effective January 1, 2017), the G-SIB buffer does not apply to BBVA.

For more details on the quantitative indicators for assessing global systemically important entities, see “Annex V – G-SIB indicators”.

The Bank of Spain has extensive discretionary powers as regards the countercyclical capital buffer specific to each bank, the buffer for other systemically important financial institutions (which are those institutions considered to be systemically important domestic financial institutions “D-SIB”) and the buffer against systemic risk (to prevent or avoid systemic or macroprudential risk). The European Central Bank (ECB) has the powers to issue recommendations in this respect following the entry into force on November 4, 2014 of the Single Supervisory Mechanism (SSM).

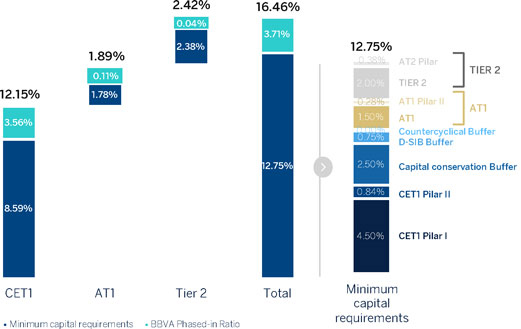

With regard to minimum capital requirements, the ECB, in its announcement on 12 March 2020, has allowed banks to use Additional Tier 1 and Tier 2 capital instruments to comply with the Pillar II (P2R) requirements, which is known as “Pillar 2 tiering.” This measure is reinforced by the relaxation of the Countercyclical Capital Buffer (CCyB) announced by various national macroprudential authorities and by other complementary measures published by the ECB. Furthermore, the BBVA Group received its SREP (Supervisory Review and Evaluation Process) results in December 2020. Through this letter, the ECB informed the Group that, as from 1 January 2021, the Pillar 2 requirement would be maintained at 1.5%, to be distributed according to the aforementioned Pillar 2 tiering. All this has resulted in a lower fully-loaded CET1 requirement of 66 basis points for BBVA, whereby said requirement stands at 8.59% and the requirement at the total ratio level stands at 12.75%.

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 19 |

Then, the consolidated overall capital requirement includes: i) the minimum capital requirement of Common Equity Tier 1 (CET1) of Pillar 1 (4.5%); ii) the capital requirement of Additional Tier 1 (AT1) of Pillar 1 (1.5%); iii) the capital requirement of Tier 2 of Pillar 1 (2%); iv) the CET1 requirement of Pillar 2 (0.84%), v) the capital requirement of Additional Tier 1 (AT1) of Pillar 2 (0.28%); vi) the capital requirement of Tier 2 of Pillar 2 (0.38%); vii) the capital conservation buffer (2.5% of CET1); and viii) the capital buffer for Other Systemically Important Institutions (O-SIIs) (0.75% of CET1).

As of 2021, the BBVA Group has set an objective to maintain a fully-loaded CET1 ratio of between 11.5% and 12.0%, increasing the target distance from the minimum requirement (currently 8.59%) to 291–341 basis points. At the end of financial year 2020, the fully-loaded CET1 ratio falls within this target management range (+314 basis points).

CET1 phased-in ratio reach 12.15% which represents +315 basis points over the mínimum requirement of 8.59%.

Chart 1. Capital Requirements and capital ratios (phased-in)

The following table shows the CET1 ratio that would trigger restrictions on capital distribution and the capital ratios as of December 2020:

Table 1. Capital distribution contrains (12-31-2020)

| CET1 capital ratio that would trigger capital distribution constraints (%) | Current CET 1 capital ratio (%) | |||||||

CET1 Pillar 1 | 4.50 | % | ||||||

CET1 Pillar 2 (P2R) | 0.84 | % | ||||||

Capital conservation buffer | 2.50 | % | ||||||

D-SIB buffer | 0.75 | % | ||||||

Countercyclical buffer | 0.00 | % | ||||||

CET1 phased-in minimum plus Basel III buffers (excluding capital used to meet other minimum regulatory capital) | 8.59 | % | 12.15 | % | ||||

|

|

|

| |||||

CET1 phased-in minimum plus Basel III buffers (including capital used to meet other minimum regulatory capital) | N/A | N/A | ||||||

|

|

|

| |||||

The Group has not made use of CET1 phased-in capital to meet other minimum capital requirements other than the minimum CET1 capital requirement plus combined capital buffer requirements.

The following table shows the distribution by geographic areas of the credit exposure for calculation of the countercyclical capital buffer:

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 20 |

Table 2. Geographical breakdown of relevant credit exposures for the calculation of the countercyclical capital buffer (Million Euros. 12-31-2020)

| General credit exposures(1) | Trading book exposure | Securitisation exposure | Own funds requirements | |||||||||||||||||||||||||||||||||||||||||||||||||

| Exposure value for SA | Exposure value for IRB | Sum of long and short position of trading book | Trading book exposure value for internal models | Exposure value for SA | Total exposure value | Of which: General credit exposures | Of which: Trading book exposures | Of which: Securitisation exposures | Total | Risk weighted exposures | Own funds requirements weights | Countercyclical capital buffer rate | ||||||||||||||||||||||||||||||||||||||||

Geographical breakdown | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Bulgary | 34 | 3 | — | — | — | 37 | 3 | — | — | 3 | 35 | 0.01 | % | 0.50 | % | |||||||||||||||||||||||||||||||||||||

Slovakia | 7 | 187 | — | — | — | 194 | 18 | — | — | 18 | 219 | 0.09 | % | 1.00 | % | |||||||||||||||||||||||||||||||||||||

Hong Kong | 21 | 1,694 | 0 | 9 | — | 1,724 | 24 | 0 | — | 24 | 303 | 0.13 | % | 1.00 | % | |||||||||||||||||||||||||||||||||||||

Luxemburg | 148 | 1,810 | 21 | 3 | — | 1,982 | 59 | 0 | — | 59 | 743 | 0.31 | % | 0.25 | % | |||||||||||||||||||||||||||||||||||||

Norway | 3 | 48 | 0 | 0 | — | 51 | 2 | 0 | — | 2 | 19 | 0.01 | % | 1.00 | % | |||||||||||||||||||||||||||||||||||||

Czech Republic | 14 | 9 | — | — | — | 23 | 1 | — | — | 1 | 15 | 0.01 | % | 0.50 | % | |||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Total countries with countercyclical capital buffer stablished | 227 | 3,750 | 21 | 12 | — | 4,011 | 106 | 1 | — | 107 | 1,334 | 0.55 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Argentina | 5,617 | 396 | 490 | — | — | 6,502 | 289 | 0 | — | 289 | 3,613 | 1.50 | % | — | ||||||||||||||||||||||||||||||||||||||

Colombia | 13,934 | 680 | 737 | 5 | — | 15,355 | 730 | 7 | — | 738 | 9,220 | 3.82 | % | — | ||||||||||||||||||||||||||||||||||||||

Spain | 29,723 | 175,782 | 145 | 105 | 1,585 | 207,339 | 5,197 | 5 | 24 | 5,226 | 65,325 | 27.10 | % | — | ||||||||||||||||||||||||||||||||||||||

United States | 74,786 | 18,691 | 393 | 163 | 64 | 94,097 | 4,138 | 9 | 4 | 4,151 | 51,885 | 21.53 | % | — | ||||||||||||||||||||||||||||||||||||||

France | 341 | 8,544 | 39 | 23 | — | 8,947 | 206 | 1 | — | 207 | 2,589 | 1.07 | % | — | ||||||||||||||||||||||||||||||||||||||

Mexico | 34,802 | 37,954 | 368 | 299 | — | 73,423 | 3,121 | 30 | — | 3,152 | 39,394 | 16.34 | % | — | ||||||||||||||||||||||||||||||||||||||

Peru | 21,648 | 699 | 1,103 | — | — | 23,450 | 902 | 17 | — | 919 | 11,485 | 4.76 | % | — | ||||||||||||||||||||||||||||||||||||||

Portugal | 4,475 | 574 | 18 | 18 | — | 5,085 | 270 | 1 | — | 271 | 3,382 | 1.40 | % | — | ||||||||||||||||||||||||||||||||||||||

United Kingdom | 700 | 6,726 | 101 | 85 | — | 7,612 | 219 | 1 | — | 220 | 2,751 | 1.14 | % | — | ||||||||||||||||||||||||||||||||||||||

Turkey | 51,104 | 556 | 1,887 | — | — | 53,547 | 2,725 | 3 | — | 2,728 | 34,096 | 14.14 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Total countries with a 0% countercyclical buffer or without countercyclical capital buffer (with own funds requirements greater than 1%) | 237,129 | 250,601 | 5,281 | 697 | 1,649 | 495,357 | 17,798 | 74 | 27 | 17,899 | 223,739 | 92.82 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Other areas | 10,865 | 29,630 | 428 | 360 | 74 | 41,356 | 1,264 | 14 | 1 | 1,278 | 15,972 | 6.63 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Total countries without countercyclical capital buffer (with own funds requirements less than 1%) | 10,865 | 29,630 | 428 | 360 | 74 | 41,356 | 1,264 | 14 | 1 | 1,278 | 15,972 | 6.63 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Total | 248,221 | 283,982 | 5,730 | 1,069 | 1,723 | 540,724 | 19,167 | 88 | 28 | 19,284 | 241,044 | 100.00 | % | — | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

| (*) | Table format adapted to the EBA/ITS/2020/04 version of the standards. |

| (1) | Credit exposure excludes exposures to Central Governments or Central Banks, Regional Governments or Local Authorities, Public sector entities, Multilateral Development Banks, International Organisations and Institutions in accordance with art. 140.4 of Directive 2013/36/EU. |

| Amount | ||||

Total risk exposure amount | 353,273 | |||

Institution specific countercyclical buffer rate(2) | 0.31 | % | ||

Institution specific countercyclical buffer requirement | 11 | |||

| (2) | Countercyclical capital buffer calculated as of December 2020 in accordance with Commission Delegated Regulation (EU) 2015/1555. |

| BBVA. PILLAR III 2020 | INTRODUCTION | P. 21 |

The countercyclical capital buffer requirement applicable to the BBVA Group has been reduced by approximately €60 million as compared to December 2019. This is due to the relaxation of the countercyclical capital buffer announced by various national macroprudential authorities, principally in France and the United Kingdom, which went from 0.25% and 1% respectively in December 2019 to 0% in December 2020.

Leverage ratio

In order to provide the financial system with a metric that serves as a backstop to capital levels, irrespective of the credit risk, a measure complementing all the other capital indicators has been incorporated into Basel III and transposed to the solvency regulations. This measure, the leverage ratio, can be used to estimate the percentage of assets and off-balance sheet items financed with Tier 1 capital.

Although the book value of the assets used in this ratio is adjusted to reflect the bank’s current or potential leverage with a given balance sheet position, the leverage ratio is intended to be an objective measure that may be reconciled with the Financial Statements.

As of December 31, 2020, the Group had a leverage fully loaded ratio of 6.49% and a phased-in ratio of 6.69%, above the minimum required ratio of 3% and continuing to compare very favorably with the rest of the peer group. This ratio does not include the impact of the sale of BBVA USA, which, according to the current estimate and taking December 2020 as a reference, would place the leverage ratio at 7.74%.

| BBVA. PILLAR III 2020 | 1. GENERAL INFORMATION REQUIREMENTS | P. 22 |

1. General information requirements

| BBVA. PILLAR III 2020 | 1. GENERAL INFORMATION REQUIREMENTS | P. 23 |

1.1. Corporate name and differences between the consolidated group for the purposes of solvency regulations and accounting criteria

1.1.1. Corporate name and scope of application

Banco Bilbao Vizcaya Argentaria, S.A. (hereinafter the “Bank” or “BBVA”) is a private law entity subject to the rules and regulations of the banking entities operating in Spain and carries out its activity through branches and agencies throughout the country and abroad.

The bylaws and other public information are available for consultation at the Bank’s registered office (Plaza San Nicolás, 4, Bilbao) and on its website (www.bbva.com).

Solvency regulations are applicable at a consolidated level for the whole Group.

1.1.2. Differences between the Consolidated Group for the purposes of solvency regulations and accounting criteria

The Consolidated Financial Statements of BBVA Group are presented in accordance with the International Financial Reporting Standards adopted by the European Union (hereinafter referred to as ‘IFRS-EU’) applicable as of December 31, 2020, considering the Bank of Spain Circular

4/2017, and its successive modifications and the other provisions of the financial reporting framework which are applicable and the marking and format requirements stablished by Regulation EU 2019/815 of European Commision.

On the basis of accounting criteria, companies are considered to form part of a consolidated group when the parent entity holds or can hold, directly or indirectly, control of them. An institution is understood to control a subsidiary when it is exposed, or is entitled to, variable returns as a result of its involvement in the subsidiary and has the capacity to influence those returns through the power it exercises over the subsidiary. For control to exist, the following aspects must be fulfilled:

| a. | Power: An investor has power over a subsidiary when it has current rights that provide it with the capacity to direct its relevant activities, i.e. those that significantly affect the returns of the subsidiary. |

| b. | Returns: An investor is exposed, or is entitled to variable returns, as a result of its involvement in the subsidiary when the returns obtained by the investor for such involvement may vary based on the economic performance of the subsidiary. Investor returns can be positive only, negative only, or positive and negative at the same time. |

| c. | Relationship between power and returns: An investor has control over a subsidiary when it not only has power over the subsidiary and is exposed, or is entitled to, variable returns for its involvement in the subsidiary, but it also has the capacity to use its power to influence the returns it obtains due to its involvement in the subsidiary. |

Therefore, in drawing up the Consolidated Financial Statements of BBVA Group, all dependent companies and consolidating structured entities have been consolidated by applying the full consolidation method.

Associated companies, as well as joint ventures (those over which joint control arrangements are in place), are valued using the equity method.

The list of all the companies forming part of the Group is included in the appendices to the Consolidated Financial Statements of BBVA Group.

For the purposes of solvency regulations, the following subsidiaries form part of the consolidated group, as defined in Article 18 of the CRR:

| • | Credit institutions |

| • | Investment firms |

| • | Financial Institutions |

A financial institution is a company, separate from other institutions (credit institution or investment firm), whose main activity may consist of acquiring holdings or performing one or more of the following activities:

| • | Loans, including in particular consumer finance, credit agreements relating to immovable property, recourse and non-recourse factoring, and financing of commercial transactions (including forfaiting) |

| • | Financial leasing |

| • | Payment services |

| • | Issuing and managing other payment channels (e.g. traveler’s checks and bank checks) |

| • | Granting of guarantees and commitments |

| BBVA. PILLAR III 2020 | 1. GENERAL INFORMATION REQUIREMENTS | P. 24 |

| • | Trading on their own account or on behalf of customers on any of the following instruments: |

| • | Money market instruments (checks, bills, certificates of deposit etc.) |

| • | Foreign currency |

| • | Financial futures and options |

| • | Foreign-exchange or interest-rate instruments |

| • | Marketable securities |

| • | Participating in the issuance of securities and the provision of corresponding services |

| • | Advising companies with regard to capital structure, industrial strategy and related matters, as well as advice and services for mergers and acquisitions of companies |

| • | Brokerage in the interbank markets |

| • | Managing or advising on equity management |

| • | Custody and administration of marketable securities |

| • | Issuance of electronic money |

This definition includes financial holding companies, mixed financial holding companies, payment institutions and asset management firms, but excludes pure industrial holding companies, insurance companies, insurance holding companies and mixed insurance holding companies.

| • | Auxiliary services companies: A company whose main activity is holding or management of property, management of computing services or any other similar activity of an auxiliary nature with regard to the main activity of one or more institutions (credit institution or investment firm). |

Therefore, for the purposes of calculating solvency requirements, and hence the drawing up of this Prudential

Relevance Report, the scope of consolidating entities is different from the scope defined for the purposes of drawing up the Consolidated Financial Statements of BBVA Group.

The effect of the difference between the two regulations is mainly due to:

| • | Withdrawals from the balance made by entities (largely insurance companies regulated by the Solvency II regulatory framework) that are consolidated in the Consolidated Financial Statements of BBVA Group by the full consolidation method and consolidated for the purposes of solvency by applying the equity method. |

| • | Entries to the balance contributed mainly by financial entities, consolidated by applying the equity method at the accounting level, but for the purposes of solvency, are proportionally integrated. |

The list of entities that use different consolidation methods in their public and regulatory balance sheets is included in table LI3 in Appendix 1 to the file titled, “Excel Tables and Pillar III 2020 Appendices”, which is included with this report and is available in the Shareholders and Investors/Financial Information section of the Group’s website.

1.1.3. Main changes in the Group in the 2020 financial year

In 2020, the BBVA Group underwent two significant divestment operations, which are detailed in Note 3 to the Consolidated Financial Statements. These operations involved the agreement reached with Allianz to jointly boost the non-life insurance business in Spain, which was finalised in December 2020, and the agreement to sell BBVA USA and other subsidiaries in the United States with activities related to the banking business. The closing of this agreement is subject to the receipt of regulatory authorisations from the relevant authorities.

Furthermore, on 22 January 2021, once all required authorisations had been obtained, BBVA completed the sale of its direct and indirect holdings of 100% of the share capital of Banco Bilbao Vizcaya Argentaria Paraguay, S.A. (“BBVA Paraguay”) to Banco GNB Paraguay S.A., part of the Gilinski Group. This sale will have a positive impact on the Group’s fully loaded CET1 ratio of approximately +6 basis points, which will be reflected in the BBVA Group’s capital base for the first quarter of 2021 (see Note 56 to the Group’s Consolidated Financial Statements).

As result of the agreement to sale BBVA USA, as of 31 December 2020 in the Group’s consolidated public balance sheet, all the items on the balance sheet of BBVA USA, have been reclassified to the category of “Non-current assets (liabilities) and disposal groups classified as held for sale”. The same treatment applied in this report for those breakdowns that, in compliance with the respective RTS/ITS of the EBA, are made based on information from the FINREP Statements (indicated in the respective breakdowns).

On the contrary, for the purposes of prudential consolidation and in compliance with article 18 of the CRR, both in the Corep Statements submitted to the Supervisor, and in the disclosures of this report other than those mentioned above, BBVA USA’s assets and liabilities are presented in their respective balance sheet headings.

This also applies to BBVA Paraguay, whose balance sheet items have been reclassified as “Non-current assets (liabilities) and disposal groups held for sale” since 2019, when the sale agreement was reached with Banco GNB Paraguay, S.A.

For more information on the main transactions during the year, see Note 3 of the Consolidated Financial Statements of BBVA Group.

| BBVA. PILLAR III 2020 | 1. GENERAL INFORMATION REQUIREMENTS | P. 25 |

1.1.4. Reconciliation of the Public Balance Sheet from the accounting perimeter to the regulatory perimeter

This section includes an exercise in transparency to show the reconciliation process between the book balances reported in the public balance sheet (attached to the Consolidated Financial Statements of BBVA Group) and the book balances

this report uses (regulatory perimeter), revealing the main differences between both perimeters. This comparison is affected by the classification of BBVA USA’s and BBVA Paraguay’s assets and liabilities as “Non-current assets (liabilities) and disposal groups held for sale” in the public balance sheet, while they are classified on the prudential balance sheet under their respective balance sheet headings in accordance with the prudential method of consolidation established by the CRR (see Chapter 1.3).

Table 3. CC2 - Reconciliation of regulatory capital to balance sheet (Million Euros. 12-31-2020)

Public Balance Sheet Headings(1) | Public Balance Sheet | Regulatory balance sheet | Referece to template CC1 | |||||||||

Cash, cash balances at central banks and other demand deposits | 65,520 | 77,557 | ||||||||||

Financial assets held for trading | 108,257 | 109,759 | ||||||||||

Non-trading financial assets mandatorily at fair value through profit or loss | 5,198 | 1,619 | ||||||||||

Financial assets designated at fair value through profit or loss | 1,117 | — | ||||||||||

Financial assets at fair value through accumulated other comprehensive income | 69,440 | 59,379 | ||||||||||

Financial assets at amortised cost | 367,668 | 424,956 | ||||||||||

Derivatives - Hedge accounting | 1,991 | 1,863 | ||||||||||

Fair value changes of the hedged items in portfolio hedges of interest rate risk | 51 | 51 | ||||||||||

Joint ventures and associates | 1,437 | 4,382 | ||||||||||

Insurance and reinsurance assets | — | — | ||||||||||

Tangible assets | 7,823 | 8,326 | ||||||||||

Intangible assets | 2,345 | 4,246 | g) | |||||||||

Tax assets | 16,526 | 16,557 | ||||||||||

Of which: deferred tax assets | 15,327 | 15,353 | h) | |||||||||

Other assets | 2,819 | 5,932 | ||||||||||

Non-current assets and disposal groups classified as held for sale | 85,987 | 1,223 | ||||||||||

|

|

|

|

|

| |||||||

Total Assets | 736,176 | 715,850 | — | |||||||||

|

|

|

|

|

| |||||||

Financial liabilities held for trading | 86,488 | 86,933 | ||||||||||

Financial liabilities designated at fair value through profit or loss | 10,050 | 4,531 | ||||||||||

Financial liabilities at amortised cost | 490,606 | 561,576 | o) p) r) | |||||||||

Derivatives - Hedge accounting | 2,318 | 2,157 | ||||||||||

Fair value changes of the hedged items in portfolio hedges of interest rate risk | — | — | ||||||||||

Liabilities under insurance and reinsurance contracts | — | 67 | ||||||||||

Provisions | 6,141 | 5,816 | ||||||||||

Tax liabilities | 2,355 | 1,668 | ||||||||||

Of which: deferred tax liabilities | 1,809 | 1,142 | ||||||||||

Other liabilities | 12,753 | 3,267 | ||||||||||

Liabilities included in disposal groups classified as held for sale | 75,446 | — | ||||||||||

|

|

|

|

|

| |||||||

Total liabilities | 686,156 | 666,015 | — | |||||||||

|

|

|

|

|

| |||||||

Capital | 3,267 | 3,267 | a) | |||||||||

Share premium | 23,992 | 23,992 | a) | |||||||||

Equity instruments issued other than capital | — | — | b) | |||||||||

Other equity | 42 | 42 | b) | |||||||||

Retained earnings | 30,508 | 29,974 | b) | |||||||||

Revaluation reserves | — | — | b) | |||||||||

Other reserves | (164 | ) | 275 | b) | ||||||||

Less: treasury shares | (46 | ) | (46 | ) | l) | |||||||

Profit or loss atributable to owners of the parent | 1,305 | 1,253 | e) | |||||||||

Less: interim dividend | — | — | e) | |||||||||

Accumulated other comprehensive income (loss) | (14,356 | ) | (14,341 | ) | c) i) k) | |||||||

Minority interests | 5,471 | 5,417 | ||||||||||

|

|

|

|

|

| |||||||

Total equity | 50,020 | 49,834 | — | |||||||||

|

|

|

|

|

| |||||||

Total equity and total liabilities | 736,176 | 715,850 | — | |||||||||

|

|

|

|

|

| |||||||

| (1) | In the public balance sheet the assets and liabilities of BBVA USA and BBVA Paraguay are classified as “Non current assets held for sale” and “Non current liabilities held for sale”, while in the regulatory balance sheet they are classified under their respective balance sheet headings in accordance with the prudential consolidation established by the CRR (see section 1.1.3). |

The main differences between the public balance sheet and the regulatory balance sheet, apart from the sales of BBVA USA and BBVA Paraguay, are due to withdrawals from the balance generated by insurance, real estate and financial entities that are consolidated through the application of the equity method for the amount of -21,312 million euros; and balance entries generated by entities that are consolidated using the proportional integration method for an amount of +986 million euros.

The following table also shows the risk to which each of the items on the regulatory balance sheet is exposed:

| BBVA. PILLAR III 2020 | GENERAL INFORMATION REQUIREMENTS | P. 26 |

Table 4. EU LI1 - Differences between the accounting and regulatory scopes of consolidation and the mapping of the financial statements categories with regulatory risk categories (Million Euros. 12-31-2020)

| Carrying values of items (1) | ||||||||||||||||||||||||||||||||||||

| Carrying values as reported in published financial statements(2) | Proforma consolidated accounting values including the United States and Paraguay(3) | From which summarised consolidated balance sheet of US companies for sale(4) | Carrying Values under scope of regulatory consolidation(5) | Subject to credit risk framework | Subject to counterparty credit risk framework | Subject to the Securitisation framework | Subject to the market risk framework | Not subject to capital requirements or subject to deduction from capital | ||||||||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||||||||||

Cash, cash balances at central banks and other demand deposits | 65,520 | 77,303 | 11,368 | 77,557 | 77,557 | — | — | — | — | |||||||||||||||||||||||||||

Financial assets held for trading | 108,257 | 109,078 | 821 | 109,759 | 12,325 | 74,610 | — | 109,759 | — | |||||||||||||||||||||||||||

Non-trading financial assets mandatorily at fair value through profit or loss | 5,198 | 5,211 | 13 | 1,619 | 1,567 | — | 52 | — | — | |||||||||||||||||||||||||||

Financial assets designated at fair value through profit or loss | 1,117 | 1,117 | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Financial assets at fair value through accumulated other comprehensive income | 69,440 | 74,416 | 4,974 | 59,379 | 58,987 | — | 364 | 29 | — | |||||||||||||||||||||||||||

Financial assets at amortised cost | 367,668 | 430,260 | 61,558 | 424,956 | 418,357 | 2,120 | 3,917 | — | 562 | |||||||||||||||||||||||||||

Derivatives - Hedge accounting | 1,991 | 2,000 | 9 | 1,863 | — | 1,863 | — | — | — | |||||||||||||||||||||||||||

Fair value changes of the hedged items in portfolio hedges of interest rate risk | 51 | 51 | — | 51 | — | — | — | — | 51 | |||||||||||||||||||||||||||

Joint ventures and associates | 1,436 | 1,437 | — | 4,382 | 4,350 | — | — | — | 32 | |||||||||||||||||||||||||||

Insurance and reinsurance assets | 306 | 306 | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Tangible assets | 7,823 | 8,629 | 799 | 8,326 | 8,326 | — | — | — | — | |||||||||||||||||||||||||||

Intangible assets | 2,345 | 4,297 | 1,949 | 4,246 | 753 | — | — | — | 3,493 | |||||||||||||||||||||||||||

Tax assets(6) | 16,526 | 16,888 | 360 | 16,557 | 15,079 | — | — | — | 1,478 | |||||||||||||||||||||||||||

Other assets(7) | 2,512 | 3,912 | 1,390 | 5,932 | 3,858 | — | — | — | 2,074 | |||||||||||||||||||||||||||

Non-current assets and disposal groups classified as held for sale(4) | 85,986 | 1,271 | 16 | 1,223 | 1,223 | — | — | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total assets | 736,176 | 736,176 | 83,257 | 715,850 | 602,382 | 78,593 | 4,333 | 109,788 | 7,690 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Liabilities | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Financial liabilities held for trading | 86,487 | 86,587 | 98 | 86,933 | — | 74,128 | — | 86,933 | — | |||||||||||||||||||||||||||

Financial liabilities designated at fair value through profit or loss | 10,050 | 10,050 | — | 4,531 | — | — | — | — | 4,531 | |||||||||||||||||||||||||||

Financial liabilities at amortised cost | 490,606 | 565,085 | 73,132 | 561,576 | — | 11,840 | — | — | 549,736 | |||||||||||||||||||||||||||

Derivatives - Hedge accounting | 2,318 | 2,320 | 2 | 2,157 | — | 2,157 | — | — | — | |||||||||||||||||||||||||||

Fair value changes of the hedged items in portfolio hedges of interest rate risk | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Liabilities under insurance and reinsurance contracts | 9,951 | 9,951 | — | 67 | — | — | — | — | 67 | |||||||||||||||||||||||||||

Provisions | 6,141 | 6,304 | 157 | 5,816 | 830 | — | — | — | 4,986 | |||||||||||||||||||||||||||

Tax liabilities(3) | 2,355 | 2,558 | 201 | 1,668 | 1,142 | — | — | — | 526 | |||||||||||||||||||||||||||

Other liabilities | 2,802 | 3,300 | 493 | 3,267 | — | — | — | — | 3,267 | |||||||||||||||||||||||||||

Liabilities included in disposal groups classified as held for sale(4) | 75,446 | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Liabilities | 686,156 | 686,156 | 74,083 | 666,015 | 1,973 | 88,125 | — | 86,933 | 563,112 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| (1) | For the purpose of the template, when a single item is associated with the capital requirements according to more than one risk framework, it is shown in all the columns corresponding to the capital requirements to which it is associated. As a result, the sum of the values of the columns by type of risk may be greater than the carrying value according to the scope of regulatory consolidation. |

| (2) | These headings include BBVA Paraguay’s and USA’s assets and liabilities, reclassified in the epigraphs of Non Current Assets Held For Sale” and “Non Current Liabilities Held For Sale” (see section 1.1.3.). |

| (3) | For comparative purposes, this column presents in proforma the Consolidated Balance Sheet of the Group including the companies for sale of the United States and Paraguay (see section 1.1.3.). |

| (4) | These headings present the summarised consolidated balance sheet of companies for sale in the United States (see section 1.1.3) and footnote 21 of the Group’s Consolidated Annual Statements. |

| (5) | These headings include BBVA USA and BBVA Paraguay’s assets and liabilities under their respective balance sheet headings according to the prudential consolidation established by the CRR (see section 1.1.3.). |

| (6) | Deferred tax assets that depend on future profitability, which deducted from deferred tax liabilities (Article 38 of CCR) amount to 3,441 million euros and have a risk weight of 250%, accordance to Article 48 of CCR. |

| (7) | The amount of other assets includes 2,074 million euros corresponding to insurance contracts linked to pensions, are not subject to capital requirements. |

| BBVA. PILLAR III 2020 | 1. GENERAL INFORMATION REQUIREMENTS | P. 27 |

A table summarizing the main sources of the differences between the amount of exposure in regulatory terms (EAD)

and the book balances according to the Financial Statements is presented below:

Table 5. EU LI2 - Main sources of the differences between regulatory original exposure amounts and carrying values in financial statements (Million Euros. 12-31-2020)

| Items subject to: | ||||||||||||||||||||