Presentation to Investors

June 15, 2005

Agenda

Welcome

Compac Overview & Plant Tour

TriMas Overview

Rieke Presentation

Fastening Systems & Industrial Specialties Presentation

Cequent Presentation

Lunch – Q&A

2

Company Overview

Grant Beard

President & Chief Executive Officer

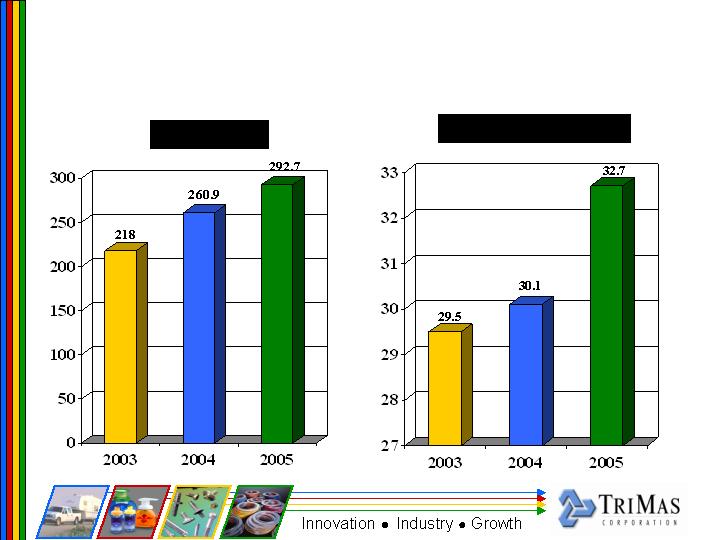

Q1 2005 Financial Highlights

First quarter sales $292.8 million, increase of 12.2% over

Q1 2004

Adjusted EBITDA* within quarter was $32.7 million, an

increase of $2.6 million compared to Q1 2004

Q1 2005 operating income was $23.3 million, an

increase of $3.1 million compared to Q1 2004

Net income within the quarter was $2.5 million or $0.13

per share vs. Q1 2004 net income of $2.2 million or

$0.11 per share

*The Company defines “Adjusted EBITDA” as net income before interest, taxes, depreciation, amortization, non-cash asset and goodwill impairment write-

offs, non-cash losses on sale-leaseback of property and equipment, legacy restricted stock award expense, and write-off of equity offering costs.

4

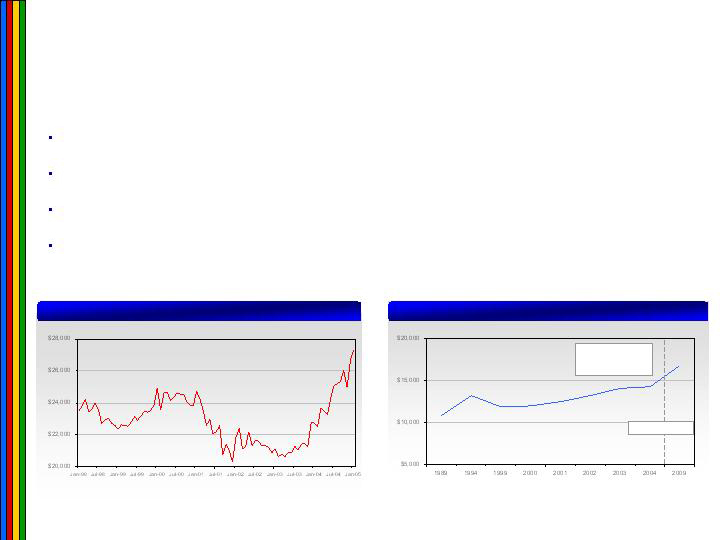

Q1 2005 Financial Highlights

($ in millions)

Q1 Revenue

Q1 Adjusted EBITDA

5

Q1 2005 Financial Highlights

Steel costs continued to challenge operating margins in

the quarter – most direct impact on Cequent and

Fastening Systems

Recovering approximately 85% of steel cost increases from

customers via pricing

TriMas ended quarter with $813.4 million of combined

debt and receivables securitization compared to $786.0

million at 12/31/04 and $792.0 million at 3/31/04

Approximate $27 million increase in leverage due to higher

accounts receivable balances at 3/31/05 as a result of increased

sales in Q1 2005

6

Q1 2005 Operating Highlights

Q1 2005 sales increased $11.1 million to

$140.6 million

Unit volume essentially flat when

adjusted for steel

Softer than expected demand for

towing products in wholesale

distributor and installer markets after

strong E.O.P. in Q4 2004

Competitive pricing pressures across

all channels, especially retail

Adjusted EBITDA in Q1 2005 decreased

$1.4 million to $16.9 million

Q1 2005 operating profit was $12.3

million (8.7% of sales)

Order fill performance is excellent

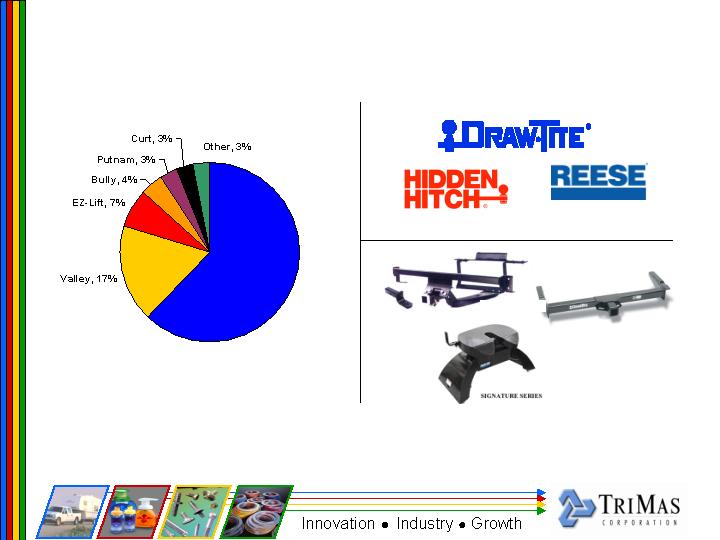

Cequent Transportation Accessories

7

Q1 2005 Operating Highlights

Net sales for the quarter were $34.1

million, up 12.2% compared to Q1

2004

Core product sales volume increased

approximately $4.0% while new

specialty dispensing product revenues

increased $4.3 million in the quarter

Rieke launched 8 new pump

dispensing products within Q1 2005

Operating income for Q1 2005

increased $1.3 million to $7.3 million

(21.3% of sales)

Order intake during Q1 2005

increased almost 20% compared to

the same period a year ago

Rieke Packaging Systems

8

Q1 2005 Operating Highlights

Q1 2005 sales increased 14.2% or

$5.5 million to $44.2 million

Sales of industrial fastener products

remained strong in the quarter

Sales of aerospace fasteners in the

quarter increased 8.9% compared to

prior year

Operating income for Q1 2005 was

$0.8 million, a $2.4 million

improvement from Q1 2004

Adjusted EBITDA in Q1 2005 was

$2.3 million compared to $0.1 million

in Q1 2004

Manufacturing activity levels

reached targeted production levels

at Frankfort and Wood Dale

Fastening Systems Group

9

Q1 2005 Operating Highlights

Net sales for Q1 2005 were $73.8

million, increase of 18.4%

Operating income for the quarter

increased 10.7% to $8.5 million

Adjusted EBITDA for the quarter

was $10.4 million compared to

$9.5 million in Q1 2004

Incremental costs associated with

facility consolidation and

restructuring activities decreased

$0.6 million

Industrial Specialties companies

expect continued momentum

across 2005

Industrial Specialties Group

10

Q1 2005 New Sales

Product

Customer

Run Rate

Gaskets

National Oilwell

2.6

$

Gaskets

Total Petroleum

0.2

Gaskets

Imperial Oil

0.2

Gaskets

Tat Lee

0.3

Engine Parts

Weatherford

TBD

SSL Tape

John Manville

1.00

Cartridge Cases

Dept. of Defense & Other

1.60

Total ISG

5.9

$

Industrial Specialties Group

11

($ millions)

Product

Customer

Run Rate

Tie Downs

Canadian Tire

3.0

$

Towing Accessories

Home Depot

1.0

Cargo Management

Costco

TBD

Tie Downs & Electrical

Sears

TBD

Trailer Hitches

Honda

TBD

Misc. Products

Toyota

TBD

Misc. Products

Land Rover

TBD

Total Cequent

4.0

$

Cequent Transportation Accessories

Product

Customer

Run Rate

Aerospace Fasteners

Airbus & Satair

2.7

$

Aerospace Fasteners

Northrop

TBD

Bolts

Caterpillar

0.4

Fasteners

Hendrickson

0.8

Fasteners

Other

TBD

Total FSG

3.9

$

Fastening Systems Group

Product

Customer

Run Rate

Dispenser

Ecolab

1.2

$

Dispenser

Starbucks

0.2

Dispenser

Hershey's

0.1

Dispenser

Colgate

TBD

Dispenser

Others

0.4

Total Rieke

2.7

$

Rieke Packaging Systems

2005 Focus & Priorities

Working capital reductions and free cash flow, positively

impacted by lower capex and non-recurring activity, will

drive substantial debt reduction by year end

SG&A costs will be flexed across all of TriMas consistent

with demand in end customer markets – especially within

the Cequent SBU’s

Discretionary spending on hold – capex approvals by

CEO & CFO

Measured actions in managing earnings volatility:

TriMas has positive year-over-year momentum in 12 of 14

businesses

Lean vs. Disable

12

Financial Overview

Skip Autry

Chief Financial Officer

(unaudited - in millions)

Mar. 31,

Dec. 31,

2005

2004

Assets

Current Assets

Cash & Cash Equivalents

3.9

$

3.1

$

Receivables

127.4

93.4

Inventories

176.6

180.0

Deferred Income Taxes

17.5

17.5

Prepaid Expenses and Other Current Assets

7.3

8.5

Total Current Assets

332.7

302.5

Property & Equipment, Net

193.3

198.6

Goodwill

655.7

658.0

Other Intangibles, Net

300.9

304.9

Other Assets

57.3

58.2

Total Assets

1,539.9

$

1,522.2

$

Liabilities and Shareholders' Equity

Current Liabilities:

Current Maturities, Long-Term Debt

2.9

$

3.0

$

Accounts Payable

132.9

135.2

Accrued Liabilities

74.6

68.2

Due to Metaldyne

2.7

2.6

Total Current Liabilities

213.1

209.0

Long-Term Debt

751.0

735.0

Deferred Income Taxes

133.4

133.5

Other Long-Term Liabilities

34.1

35.2

Due to Metaldyne

4.3

4.3

Total Liabilities

1,135.9

1,117.0

Total Shareholders' Equity

404.0

405.2

Total Liabilities and Shareholders' Equity

1,539.9

$

1,522.2

$

14

Condensed Balance Sheet

(unaudited - in millions, except per share amounts)

Q1 2005

Q1 2004

Net sales

292.7

$

260.9

$

Cost of sales

(227.2)

(196.8)

Gross profit

65.5

64.1

Selling, general and administrative expenses

(42.5)

(43.7)

Gain (loss) on dispositions of property & equipment

0.2

(0.3)

Operating profit

23.2

20.1

Other expense, net

(19.3)

(16.6)

Income before income taxes

3.9

3.5

Income tax expense

(1.4)

(1.3)

Net income

2.5

$

2.2

$

Basic earnings per share

0.13

$

0.11

$

Diluted earnings per share

0.13

$

0.11

$

Weighted average common shares - basic

20.0

20.0

Weighted average common shares - diluted

20.0

20.4

15

Condensed Statement of Operations

Cash Flow Highlights

(unaudited - in millions)

2005

2004

Cash provided by (used for) operating activities

(11.4)

$

21.6

$

Capital expenditures

(4.5)

(14.8)

Proceeds from sales of fixed assets

0.9

0.2

Acquisition of businesses, net of cash acquired

-

(5.5)

Cash used for investing activities

(3.6)

(20.1)

Proceeds from senior credit facility, net

15.9

6.3

Payments on notes payable and other

(0.1)

(7.7)

Cash provided by (used for) financing activites

15.8

(1.4)

Net increase in cash and cash equivalents

0.8

$

0.1

$

16

For the Three Months Ended March 31,

Cost Reduction/Profit Improvement

Initiatives

Represents a continuation of our

game plan

Mentioned a $10 million run rate

target in Cequent in the earnings

call

Goal has now expanded to

approximately $13 million

Are now ready to expand the

program across TriMas:

Improve earnings and cash flow

performance

Make the company more IPO

ready

Inventory reduction plan in place –

focus on Cequent & FSG

Stated goal is to improve profits

on a $25 million run rate basis

Actions are being formally rolled

out in Q2 with implementation

underway and continuing

throughout Q3

No cost area will be exempted

Roughly ½ people and ½ other

costs

Will focus on G&A/Selling/Indirect

Headcount

Investigating an SBU liquidation to

drive balance sheet strength

Utilization of NOL

17

Q2 Bank Compliance

Leverage covenant is 5.5x in Q2, 5.25x in Q3 and 5.0x in

Q4

Have been close in each of the last two quarters – no

way to live!

Steel increases in 2005 cost the Company $75 to $100

million in liquidity (e.g. higher inventory and receivable

levels, lower payables levels and lower EBITDA)

Actively managing working capital

Expect to meet our Q2 leverage covenant

18

Guidance

Have not given guidance historically

Aftermarket business is not precisely predictable

(receive orders on day “1” and ship on day “2”) – no

backlog

ISG businesses are all on positive trends

Rieke continues to see market expansion

FSG has stabilized but now needs higher sales levels as

we work through the backlog at Lake Erie. Monogram

continues to redefine itself with new products and a

record backlog.

19

Rieke Packaging Systems

Lynn Brooks

Group President

Rieke Packaging Systems

Consumer Products

Core Products

"Razor-blade" model with strong operating leverage

Promising growth prospects

21

Rieke Packaging Systems

50% of products IP-protected

Diverse end markets

Leading market shares

Benefiting from industrial

recovery

Strong growth drivers:

New product launches

Bundling and cross selling

International business

New plastic injection molding

facility in China to supply

specialty dispensing products

Pass-through on material

economics – metal and plastic

resins

Accelerating growth rate

22

Rieke New Products

Target market size is estimated at

$300 million and is growing at 9%

annually

36 new products introduced from

late 2002 through Q1 2005

Average concept to launch: 15

months

Margins are similar to core

products

Capacity in place

New markets in food, beverage,

personal care and pharmaceutical

Highly engineered products

23

Revenue Opportunity & Awarded Business ($mm)

Major Business Awards

Rieke Customer Forecast – Remainder of 2005

Petroleum – 5-10% growth in

2005

Chemical – Overall, double

digit growth

Ag Chem – Overall, double

digit growth

Paints – Overall, flat to 5%

Steel Drums – Flat to down

Medical – Flat

Ag Chem – Flat

Steel Drums – Flat to down

Plastic Drum – 5% increase

Petroleum – Flat to 2% growth

Paints – Flat to down

North America

Europe

24

Fastening Systems & Industrial

Specialties

Grant Beard

Interim Group President

Production very good at

Frankfort and Wood Dale in Q1

– Combined daily average of

281,000 lbs.

Reduced past due orders from

over $7 million in January to

under $2 million at end of March

Reduced spending in all major

categories

Inventory grew through first

quarter, will be adjusted during

Q2

Notification of steel price

reduction in Q1, no customer

effect until Q3

Frankfort Bolt-Making Comparison

26

Sales up from budgeted levels despite challenging production

environment at GM and Ford

Significant market share gains at Mark IV Automotive

Contribution margins exceeded budget due to favorable customer

recoveries relative to premium steel costs

Inventory levels increased in Q1 due to steel move to Republic and

strategic build of finished goods for new business growth

2004

Actual

2005

Impact

2006

Impact

2007

Impact

2008

Impact

Status

Legacy

15.52

15.52

15.52

15.52

15.52

Bud Inc.

0.82

0.82

0.82

0.82

Partially awarded

Steel Recoveries

0.73

1.15

1.15

1.15

1.15

B&E Closure

0.33

0.5

0.5

0.5

Awarded

AGS Standards

0.22

0.8

0.8

0.8

Awarded

TI, ITT, Other

0.15

0.35

0.45

0.55

Partially awarded

Curtis Maruyasu

0.4

0.5

0.65

Partially awarded

AMI

0.05

0.25

0.35

0.4

Highly likely

AZ Spacers, Net

0.6

2.25

3.1

Highly likely

MartinRea GMT900

0.15

0.45

0.53

Highly likely

Total Revenue

16.25

18.24

20.54

22.8

24.02

27

($ in millions)

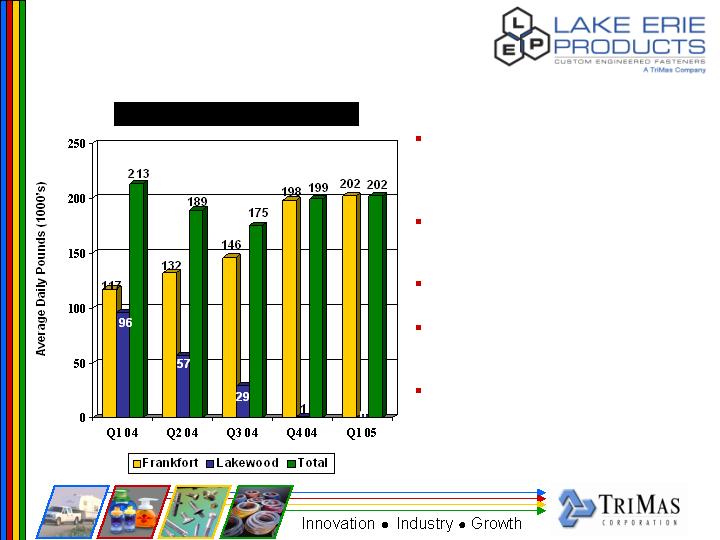

New Business Update

Record incoming orders of $15.8 million

March 2005 record production month of 42.4k pieces per day

Production for Q1 up 32% over 2004 average

Improved productivity of 6.5% for the quarter over 2004

Incoming business and total backlog reached record levels in Q1

Bookings and Backlog

28

Drilling activity at 4/8/05 shows 1,329 active rigs, represents 10%

improvement over prior 12 months

Good indication of future production

Engine sales expected to remain strong especially on Climax engine

line

Projecting engine sales in 2005 to be approximately 70% ahead of

2004

Continue to push product

development in Waukesha

market for VHP and

Intermediate parts

29

During Q1 experienced weak sales in

January combined with depressed material

margins, resulting in shortfalls in both

revenue and EBITDA

Sales in Q2 expected to improve due to

further selling price increases and

business growth from export and new

business opportunities

Purchasing initiatives implemented saving

$400K per year

Netcong, NJ facility sold March 31, 2005.

Will reduce majority of non-recurring

expenses beginning in May.

Fiberglass manufacturers enjoy sold-out

situation – production at an all time high

level

Finishing Department

Laminator

30

Q1 2005 largest revenue

quarter in Lamons’ history

Major turnarounds with: Exxon,

Premcor, BP, Citgo, Dow and

Bayer

Canadian operations expanding

into refining industry – new

contracts with Imperial Oil and

North Atlantic Refining

Latin America/Europe sales on plan in Q1 2005 - $647K vs. $418K in Q1

2004

Plan to grow business in UK through Novus Sealing and Mexico through

Auge

Signed Tat Lee (former Flexitallic licensee) as our distributor for spiral

wound and RTJ gaskets in Far East Asia

31

Revenue strong for Q1 2005 with

order strength continuing into Q2

Steel more available but prices

continued to rise in Q1. Indication

of prices being flat or giving back

for Q2 deliveries

March was record

production/shipping month over last

five years with over 30,000 units

produced

Secured first order for EU acetylene

products and DOT/ISO LHP

cylinders in Europe

32

FMS shipped record number of launchers in

Q1 2005 -7,310

LAW next generation – Nammo version in

prototype stages, Talley version in design

stage and should be available for review in

Q3

LAW relocation to Pennsylvania – complete

2005 assembly requirements in August at

Amarillo, move equipment and residual

inventory to Johnstown in Q3, first

production order scheduled in December

Flexible projectile line on track, requesting

$7 million for 2006

33

Orders continued strong for both Keo and

Richards Micro-Tool in Q1 2005

Sales into medical market exceeded budget

(>$250K)

Cost of steel continues to increase

Implemented second price increase in last six

months

New product sales for Keo brand (ZErO Flute

Countersinks, Kounterbores) were 12%

above budget

ZErO Flute Countersinks

KEO Kounterbores

34

Cequent Transportation Accessories

Ed Schwartz

Group President

Plymouth, Michigan

Plymouth, Michigan

Cequent

Towing Products

Cequent

Towing Products

Cequent

Trailer Products

Cequent

Trailer Products

Cequent

Australia

Cequent

Australia

Cequent

Consumer Products

Cequent

Consumer Products

Cequent

Electrical Products

Cequent

Electrical Products

Plymouth, Michigan

Plymouth, Michigan

Mosinee, Wisconsin

Mosinee, Wisconsin

Melbourne, Australia

Melbourne, Australia

Solon, Ohio

Solon, Ohio

Tekonsha, Michigan

Tekonsha, Michigan

Plymouth, Michigan

Plymouth, Michigan

Cequent

Towing Products

Cequent

Towing Products

Cequent

Trailer Products

Cequent

Trailer Products

Cequent

Australia

Cequent

Electrical Products

Cequent

Consumer Products

Cequent

Consumer Products

Cequent

Electrical Products

Cequent

Australia

Plymouth, Michigan

Plymouth, Michigan

Mosinee, Wisconsin

Mosinee, Wisconsin

Melbourne, Australia

Tekonsha, Michigan

Solon, Ohio

Solon, Ohio

Tekonsha, Michigan

Melbourne, Australia

Manufacturing – Goshen, IN;

Huntsville, ON; Elkhart, IN

Products – Towing Products,

Functional Vehicle Accessories

and Cargo Management

Solutions

Distribution – Installers,

Distributors, Automotive OEM,

and retail segments

Manufacturing –Sheffield, PA

Products – Towing Products,

Functional Vehicle Accessories

and Cargo Management

Solutions

Distribution –Mass

Merchants, Auto Specialty,

Program/Buying Groups

Manufacturing – Wakerley,

Brisbane, Sydney, Australia

Products – Towing, Trailering,

vehicle accessory, and cargo

management solutions

Distribution –Automotive OE

andAftermarket

Products – Brake Controls,

Breakaway Systems, Brake

Accessories, Electrical

Converters

Distribution –Automotive

OEM, Trailer OEM, Marine,

RV, Agricultural/Utility, and

Retail segments

Manufacturing – Tekonsha,

MI; Albion, IN; Reynosa, MX

Manufacturing – Mosinee, WI;

Juarez, MX

Products – Trailer Products

and Accessories

Distribution –Trailer OEM,

Wholesale-distributor, and

retail segments

LTM Ended Mar. 31

2005

2004

Net Sales .

$522.5

$458.0

Segment Adjusted EBITDA

69

64

% margin

13.2%

13.9%

37

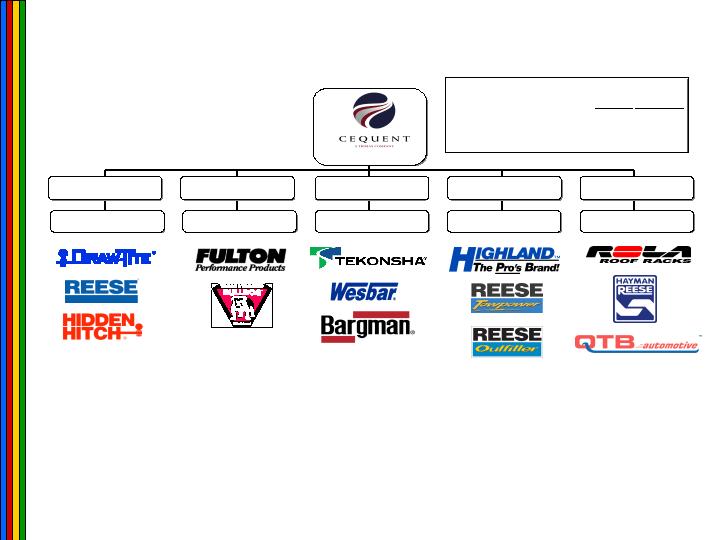

Cequent Operating Units

Cequent Major Facilities

Goshen, IN

South Bend, IN

Mosinee, WI

Juarez, Mexico

Tekonsha, MI

Plymouth, MI

38

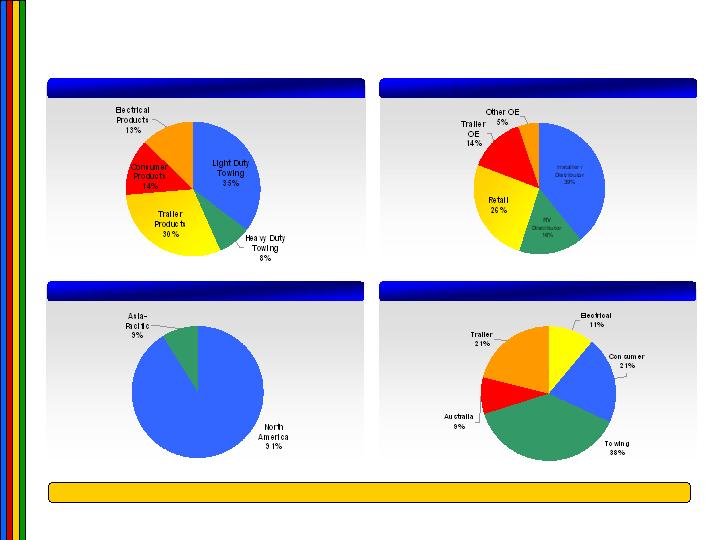

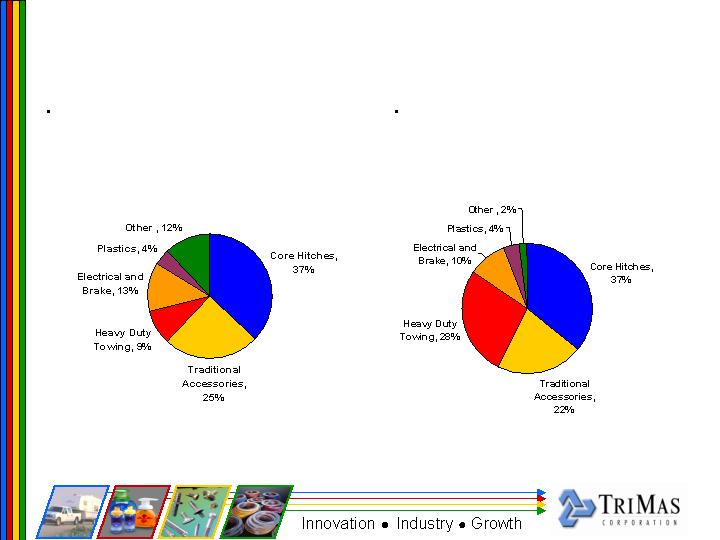

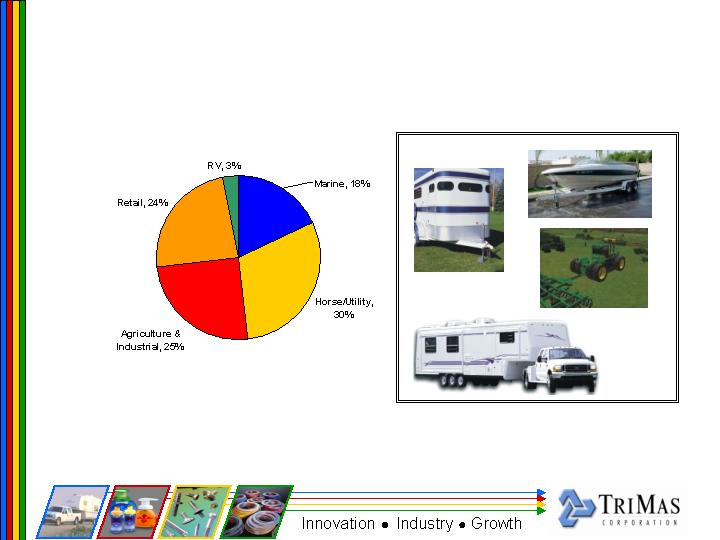

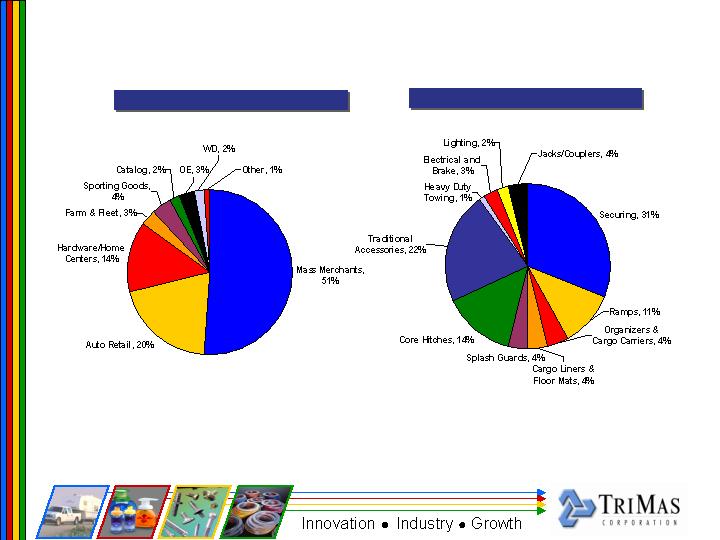

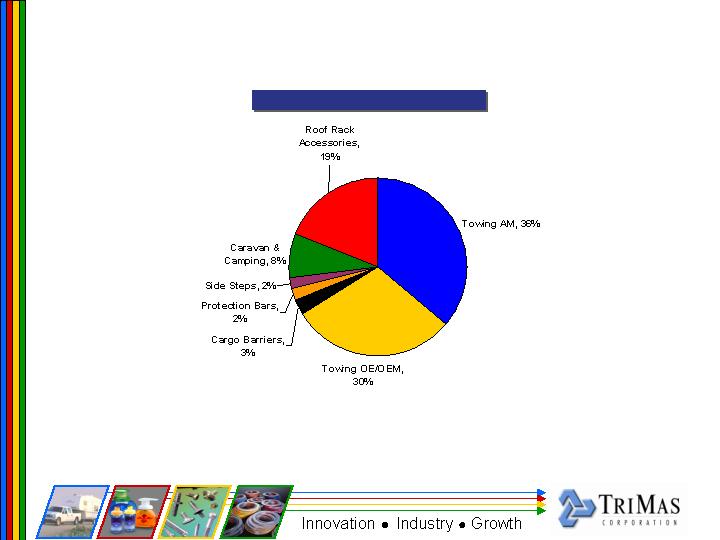

Cequent’s Sales Mix

Cequent Sales by Region

2005 (March 31, LTM) Total Cequent Net Sales . $522.5 Million

Cequent Sales by Business Unit

Cequent Sales by Product Group

Cequent Sales by Distribution Channel

39

Channel Strategic Plan - INSTALLER/WD

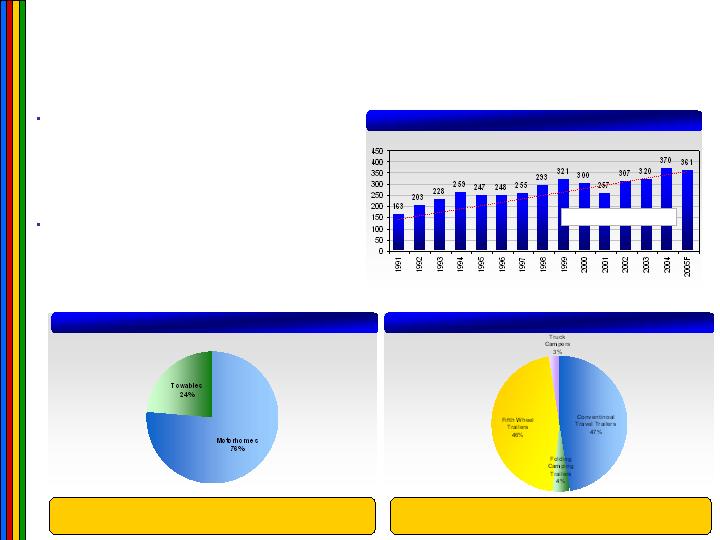

Market Overview - Recreational Vehicle Segment

U.S. RV Segment by Product Group

SOURCE: RVIA

2004 U.S. RV Market ...... $14.0 billion

(Retail Value)

Total U.S. Towable RV Trailer Market

SOURCE: RVIA

2004 U.S. Towable Trailer Market ... $5.8 billion

(Retail Value)

SOURCE: Recreation Vehicle Industry Association, Crove Capital Markets Research

NOTE: Does not include conversion vehicle shipments; dotted line represents a normalized

shipment trend, which was calculated using regression analysis.

RV Shipment Historical Volume Growth

1991-2005 CAGR . 5.8%

While the U.S. economy was on a roller coaster throughout

much of 2003, the RV industry performed solidly. Shipments to

retailers of all RVs rose 3.2% to 320,800 units in 2003—the

second best year in a quarter century. Towable RVs grew 3.3%

to 258,900 units, the best total for these products in 27 years.

Motor home shipments also increased, rising 2.5% over

the prior year on shipments to retailers of 61,900 units.

Perhaps the best news of all for the RV industry was the

increase in dollar values of shipments. Total retail value of all

RV shipments in 2003 rose an impressive 9.8% to set an all-

time re c o rd high of $12 billion dollars. The continued strength

in RV shipments as demonstrated by these growth trends

reflects the strong appeal of the RV lifestyle to a broadening

consumer base.

Total Shipments

(in thousands)

40

Channel Strategic Plan - COMMERCIAL

Market Overview – RV Segment Demand Drivers

SOURCE: Econstats.com

SOURCE: Energy Information Administration, conventional regular gasoline prices, U.S. Gulf Coast delivered.

The U.S prime lending rate is the

lowest it has been in the past six

years providing low financing rates

for major capital purchases such as

recreational vehicles.

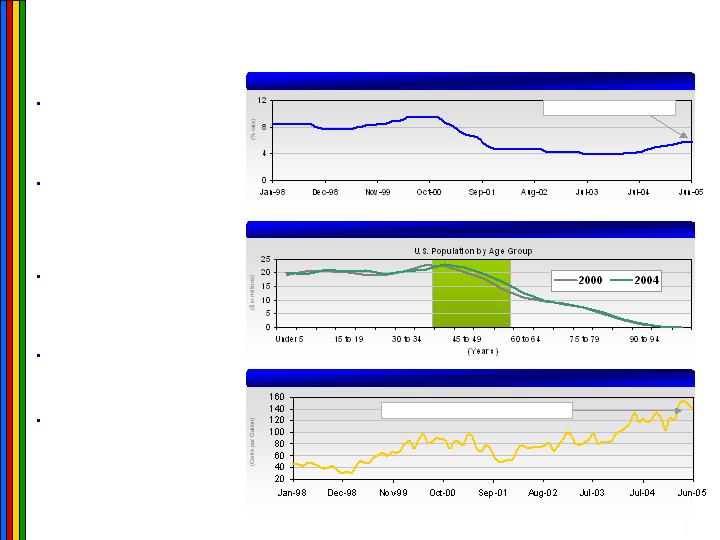

The U.S. population by age group

statistics indicate that the high

income age groups from 40 years

old to 60 years olds, baby boomers,

have increased by over 7.6 million

since 1998.

Growth in the high income age

group is a positive factor in

supporting recreational vehicle and

aftermarket accessory product

consumer demand.

Regular unleaded gasoline prices

have remained high through most

of 2004, somewhat, offsetting the

positive effects of low interest rates.

Gasoline prices are not perceived

to be a major deterrent in buying a

new recreational vehicle due to the

expectation for gasoline prices to

once again stabilize to a lower price

due to the cyclicality of oil prices.

SOURCE: U.S. Census Bureau.

Driving Age Population Growth is Driving Fleet Growth and Increased Consumer spending

Regular Unleaded Gasoline Prices Have Been on the Rise

U.S. Prime Lending Rate

(U.S. population)

U.S. Prime Lending Rate Feb 2004 . 6.0%

U.S. Wholesale Price of Unleaded Regular Gas Jan-05 . $1.41

41

Channel Strategic Plan - COMMERCIAL

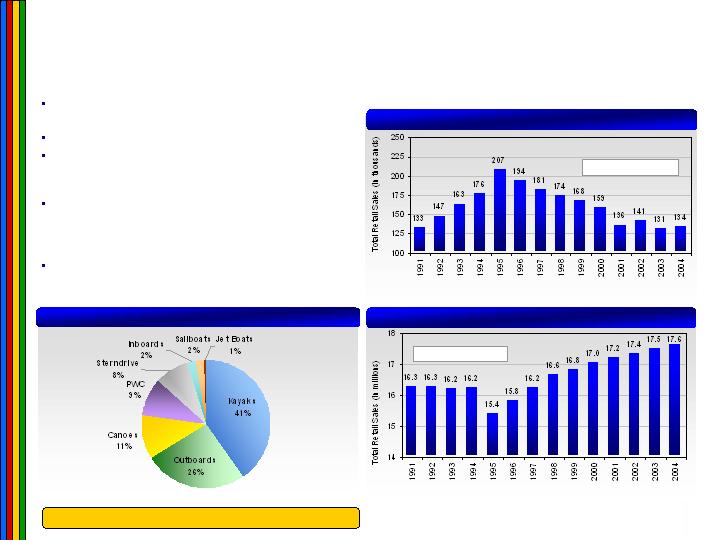

Market Overview - Marine Segment

U.S. Marine Segment by Type of Product

2004 Total Unit Sales ....... 838,500

Total Recreational Boats Owned in the U.S.

SOURCE: NMMA

Boat Trailer Unit Sales

SOURCE: NMMA

SOURCE: NMMA

Boat trailer sales peaked in 1995 and have declined

steadily until 2001, growing slightly in 2002.

2002 showed signs of a cyclical rebound in trailer sales.

The total estimated number of boats owned has

increased over the past eleven years at slow rate of 0.6%

annually.

The type of watercraft owned in the U.S is broad,

including kayaks, outboard power boats, canoes,

personal watercrafts, stern drive boats, inboard boats,

sailboats and jet boats.

All of the marine product segments require a towing,

trailer or accessory product to transport, providing

additional demand for towing and trailer products.

1991-2004 CAGR ........ 0.6%

1991-2004 CAGR ........ 0.1%

42

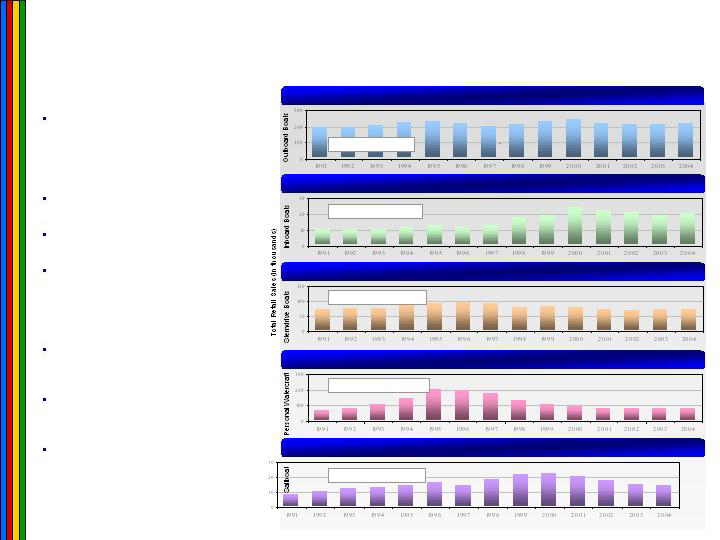

Channel Strategic Plan - COMMERCIAL

Market Overview - Marine Segment Volume Drivers

SOURCE: NMMA, 1991-2002 Annual Sailing Business Review.

Outboard Boats Sales

Inboard Boat Sales

Stern Drive Boat Sales

1991-2004 CAGR ........ 0.8%

1991-2004 CAGR ........ 5.7%

1991-2004 CAGR ........ –0.2%

The marine segment consists of a

mixture of different boat types such as

outboard engine boats, inboard

engine boats, stern drive boats,

personal watercraft and sail boats.

Most all of these boats require the use

of towing and trailer products.

The demand trend is mixed due to

varying trends with boats sales.

In general, inboard boat sales and

sailboat sales have been the strongest

among all boats types with a 7.1%

annual growth rate and a 6.8% annual

growth rate, respectively.

Outboard boat sales and stern drive

boats sales have basically been flat

over the past twelve years.

Personal watercraft sales peaked in

1995 and have dropped more than

50% below the peak volume by 2002.

The marine segment trend generally

moves with the economy due to luxury

product status of the product.

Personal Watercraft Sales

1991-2004 CAGR ........ 1.2%

Sailboat Sales

1991-2004 CAGR ........ 3.9%

43

Channel Strategic Plan - COMMERCIAL

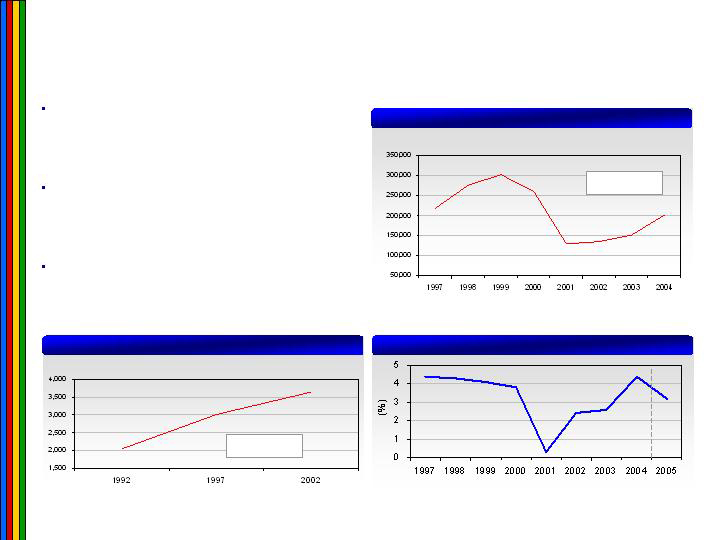

Market Overview - Cequent’s Other Market Segments

U.S. Equestrian(1) Population

SOURCE: Census of Agriculture 1992 and 2002

(1) Horses and ponies and farms reporting horses and ponies.

(horses in

thousands)

CAGR

1992-2002... 12.2%

U.S. Industrial Trailer Production

SOURCE: Trailer Body Builders

(Industrial

trailers in units)

CAGR

1997-2002... - 1.7%

Equestrian trailer industry has very few published

statistics to track demand, however, the U.S. farm

population of horses has increased at an annual rate of

1.7% over the past ten years providing an indicator of

corresponding growth in the equestrian trailer market.

The U.S. trailer production cycle over the past six years

has followed GDP growth, which bodes well for trailer

production and suppliers and should lead to strong

growth from a depressed production low in 2001 and

2002.

The light industrial and utility trailer segments generally

follow the same trends as light vehicle aftermarket

macro demand as most of these consumers are using

these trailers for personal use hobbies.

U.S. Gross Domestic Product YOY % Change

SOURCE: U.S. Census Bureau

44

Channel Strategic Plan - COMMERCIAL

Market Overview - Agricultural Equipment Segment

North American Agricultural Equipment Demand

SOURCE: Freedonia

SOURCE: U.S. Census Bureau

U.S. Farm Machinery and Equipment Shipments

($ millions)

The three largest agricultural equipment buying regions of the World are Western Europe, Asia-Pacific and North

America accounting for 88% of total World demand.

Fredonia predicts demand in North America for agricultural equipment will grow at an average annual rate of 3.5% over

the next five years.

Historically, agricultural equipment demand in North America has grown more slowly at 1.0%, however, this

measurement in growth does not account for peak demand in the mid-1990’s.

A recent positive indicator, U.S. farm machinery and equipment shipments are on the rise, 10% higher in January over a

seasonally adjusted low in April 2003.

CAGR

1989-2004... 1.9%

2004-2009... 3.3%

Forecast

($ millions)

45

Cequent Market Share - Towing

Cequent

Towing

Products

63%

Cequent

Towing

Products

49%

Source: Internal company estimates

46

Cequent Market Share - Trailer

Cequent

Trailer

Products

61%

Cequent

Trailer

Products

49%

Jacks

Couplers

Source: Internal company estimates

47

Cequent Market Share - Electrical

Cequent

Electrical

Products

63%

Cequent

Towing

Products

49%

Source: Internal company estimates

48

Cequent Market Share - Consumer

Cequent

Consumer

Products

37%

Cequent

Consumer

Products

31%

Loading Ramps

Tie Downs & Stretch Cords

Source: Internal company estimates

49

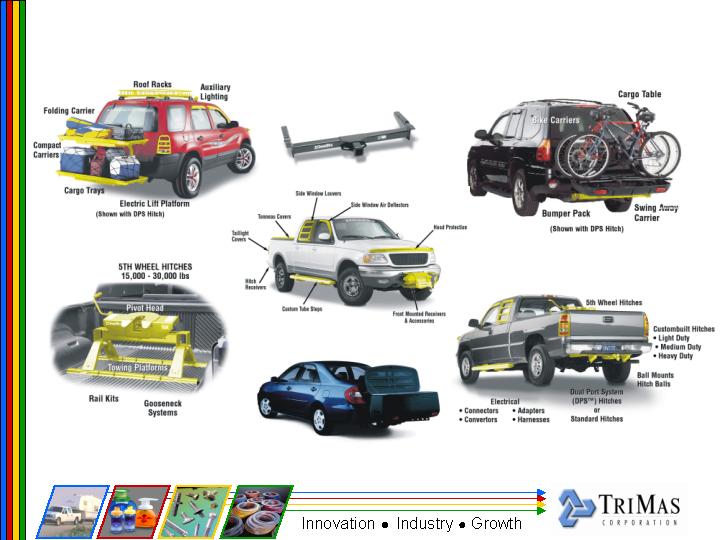

Cequent Towing: Extensive Product Portfolio

Standard Hitch

Storage Box

50

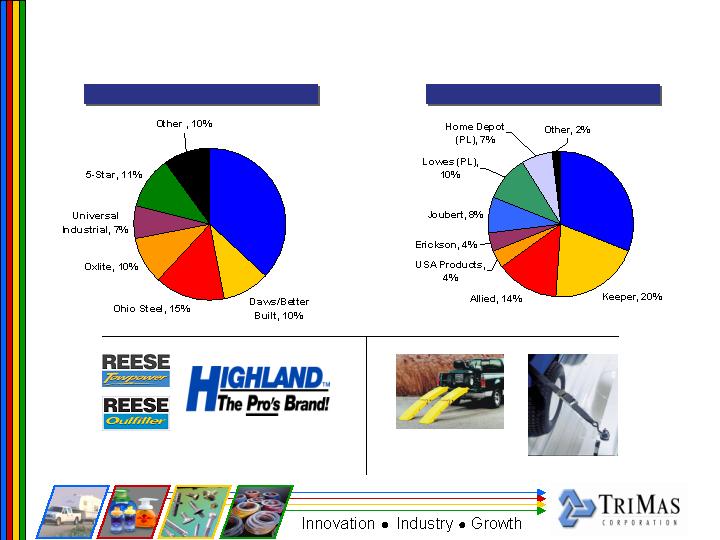

Cequent Towing: Channels of Distribution

RV Distributors

The Reese brand is more important in this channel. The

product mix is oriented towards heavy duty hitches (i.e., fifth

wheel), core-line hitches, and traditional accessories. Product

line sales generated through this channel are estimated as

follows:

Auto Aftermarket Installer/Distribution Channel

The Draw-Tite and Hidden Hitch brands operate through a

network of 60 two-step distributors and over 450 independent

installer shops (“Hitch Pros”) which carry the Draw-tite and

Hidden Hitch brands as an exclusive, or at least preferred,

brand. A sales breakdown to the auto aftermarket channel by

product type include:

51

Cequent Towing: Sales by Channel

Estimated Sales by Channel

Auto Installer/

Distributor,

46%

52

Cequent Trailer: Extensive Product Portfolio

Ramps

Bull Dog Couplers

Bull Dog Jacks

Swing Away

Tongue

53

Cequent Trailer: Sales Breakdown

54

Cequent Consumer: Product Portfolio

Load: Champ ramps and Ramparts ramp kits provide sturdy,

safe loading of motorcycles, ATVs, lawn tractors and

other equipment.

Anchor: A full line of anchor systems and hardware to anchor

heavy loads, attach tie downs, truck caps, toolboxes,

camper shells, over-the-rail bedliners, tonneau covers, CB

antenna mounts, cab extenders and more.

Secure: A complete line of tie downs, tarp straps, stretch cords

and bungee cords to meet all securing needs. Products are

available in a wide number of styles to match specific use.

Carry: Highland products which expand carrying capacity

include rooftop, rear and hitch mount carriers for

luggage, bikes and construction.

Organize: A wide range of products to organize vehicle and garage,

including the new award winning Space Master cargo

organizer, truck and storage nets, cargo bars, and a

complete line of garage organization products.

Protect: Keeps vehicles looking SHOWROOM NEW with Cargo

Liners, Floor Guards, All Weather Floor Mats, Hump

Liners, and Splash Guards. Custom fit vehicle protection

for trucks, cars, vans, and SUV’s.

55

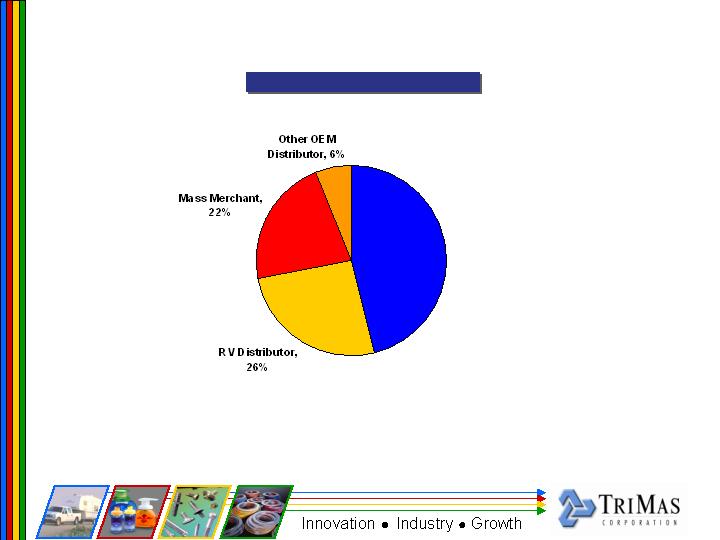

Cequent Consumer: Channels of Distribution

Estimated Sales by Channel

Estimated Sales by Product

56

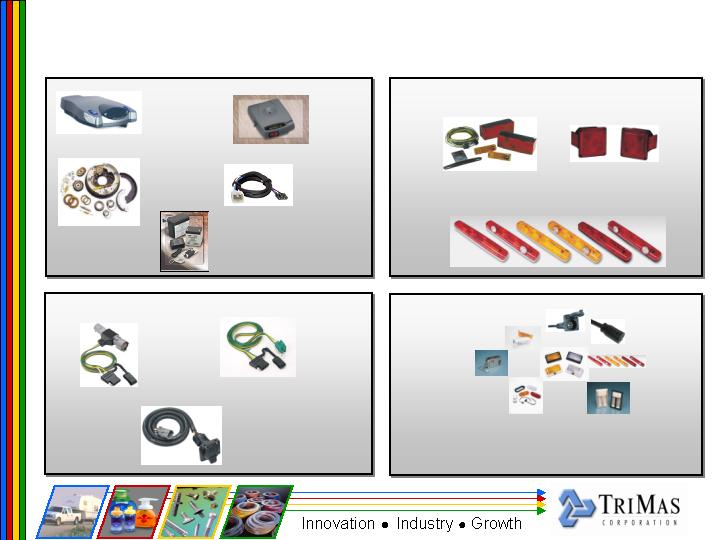

Cequent Electrical: Product Portfolio

Inertial

Brake

Control

Breakaway

Kits

Brake Control

Harness

Proportional

Brake Control

Brake

Hardware

T-One

Connector

Wiring

Harness

5, 6, 7

Way Connectors

Trailer

Lighting

Tail-light

Wiring Kits

Interior and Exterior Illumination Products

Electrical Accessories

Locks and Latches

57

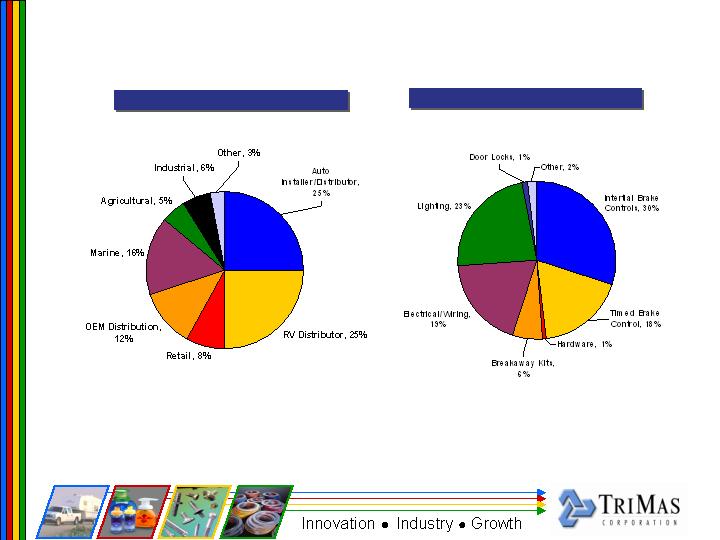

Cequent Electrical: Channels of Distribution

Estimated Sales by Channel

Estimated Sales by Product

58

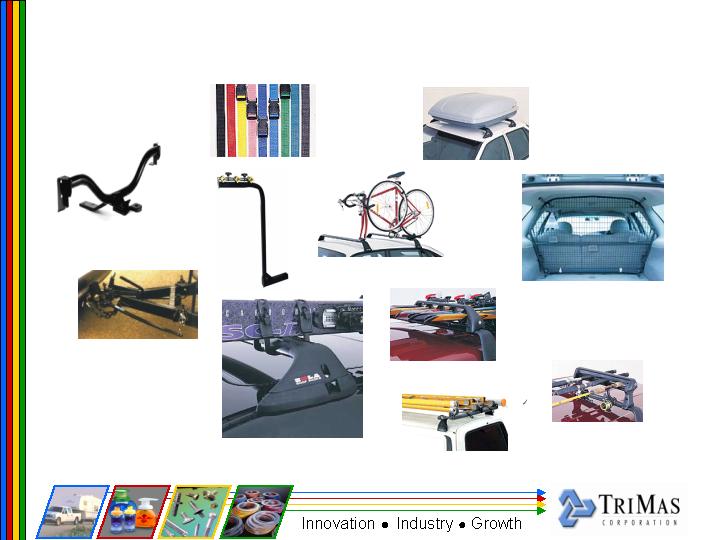

Cequent Australia: Product Portfolio

Ladder Rack System

Fishing Rod

Locking Arms

Snow Ski Diagonal

Locking Arms

Bike Carrier

Tie Downs

Luggage Pods

Luggage Pods

Cargo Barriers

Hitch-Mounted

Bike Rack

Tow Bar

Weight Distribution

59

Cequent Australia: Sales by Product

Estimated Gross Sales by Product

60

Wrap-Up

Events beyond our control are impacting the Company

Steel

End market demand – Cequent

We are dealing with these events on a number of fronts

Cost reductions – continuing the journey

Price increases

Customer/market tough decisions

We appreciate your support and thank you for attending

Q&A?

61