October 19, 2005

Innovation

A Heartland Industrial Partners’ Company

Investor Communications Meeting

Growth

Industry

This document contains “forward-looking” statements, as that term is defined by the federal securities laws, about our financial condition, results of operations and business. Forward-looking statements include certain anticipated, believed, planned, forecasted, expected, targeted and estimated results along with TriMas’ outlook concerning future results. The words “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” “forecasts,” or future or conditional verbs, such as “will,” “should,” “could,” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. All forward-looking statements, including, without limitation, management’s examination of historical operating trends and data are based upon our current expectations and various assumptions. Our expectations, beliefs and projections are expressed in good faith and we believe there is a reasonable basis for them. However, there can be no assurance that management’s expectations, beliefs and projections will be achieved. These forward-looking statements are subject to numerous assumptions, risks and uncertainties and accordingly, actual results may differ materially from those expressed or implied by the forward-looking statements. We caution readers not to place undue reliance on the statements, which speak only as of the date of this document. The cautionary statements set forth above should be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue. We do not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events. Risks and uncertainties that could cause actual results to vary materially from those anticipated in the forward-looking statements included in this document include general economic conditions in the markets in which we operate and industry-based factors such as: technological developments that could competitively disadvantage us, increases in our raw material, energy, and healthcare costs, our dependence on key individuals and relationships, exposure to product liability, recall and warranty claims, compliance with environmental and other regulations, and competition within our industries. In addition, factors more specific to us could cause actual results to vary materially from those anticipated in the forward-looking statements included in this document such as our substantial leverage, limitations imposed by our debt instruments, our ability to successfully pursue our stated growth strategies and opportunities, including our ability to identify attractive and other strategic acquisition opportunities and to successfully integrate acquired businesses and complete actions we have identified as providing cost-saving opportunities.

Safe Harbor Statement

2

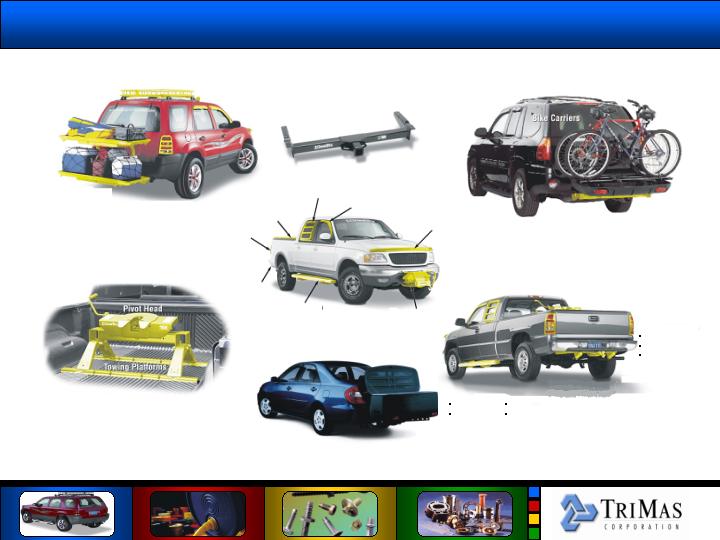

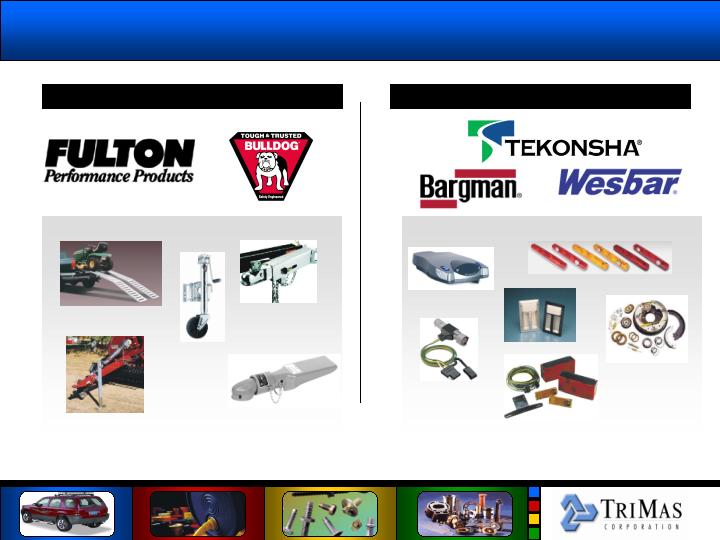

Manufacturing – Goshen, IN;

Huntsville, ON; Elkhart, IN

Products – Towing Products,

Functional Vehicle Accessories

and Cargo Management

Solutions

Distribution – Installers,

Distributors, Automotive OEM,

and retail segments

Manufacturing –Sheffield, PA

Products – Towing Products,

Functional Vehicle Accessories

and Cargo Management

Solutions

Distribution –Mass

Merchants, Auto Specialty,

Program/Buying Groups

Manufacturing – Wakerley,

Brisbane, Sydney, Australia;

Chonburi Province, Thailand

Products – Towing, Trailering,

vehicle accessory, and cargo

management solutions

Distribution –Automotive OE

andAftermarket

Products – Brake Controls,

Breakaway Systems, Brake

Accessories, Electrical

Converters

Distribution –Automotive

OEM, Trailer OEM, Marine,

RV, Agricultural/Utility

Manufacturing – Tekonsha,

MI; Albion, IN; Reynosa, MX

Manufacturing – Mosinee, WI;

Juarez, MX

Products – Trailer Products

and Accessories

Distribution –Trailer OEM,

Wholesale-distributor

Six Months Ended June 30

16.4%

11.2%

% margin ……………………

46.0

31.6

Segment Adjusted EBITDA …

$

280.0

$

283.0

Net Sales ….…….…….…..….

2004

2005

Plymouth, Michigan

Plymouth, Michigan

Melbourne, Australia

Solon, Ohio

Tekonsha, Michigan

Mosinee, Wisconsin

Cequent

Australia

Cequent

Consumer Products

Cequent

Electrical Products

Cequent

Trailer Products

Cequent

Towing Products

3

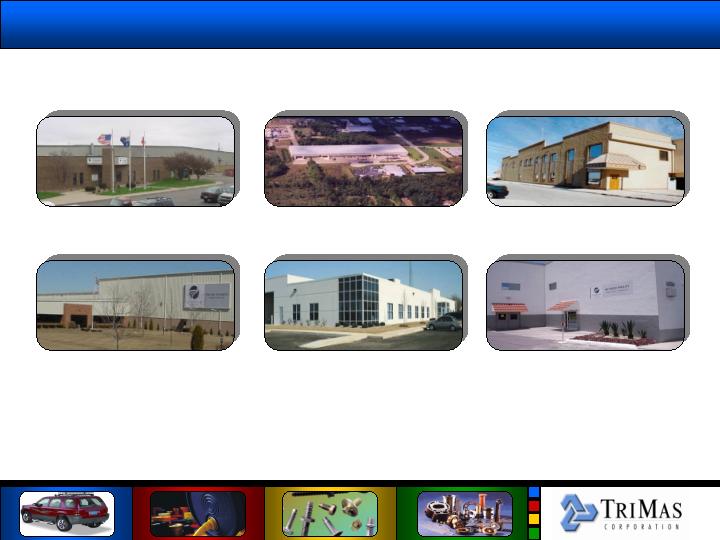

Cequent Transportation Accessories

Cequent Major Facilities

Goshen, IN

South Bend, IN

Mosinee, WI

Juarez, Mexico

Tekonsha, MI

Reynosa, Mexico

4

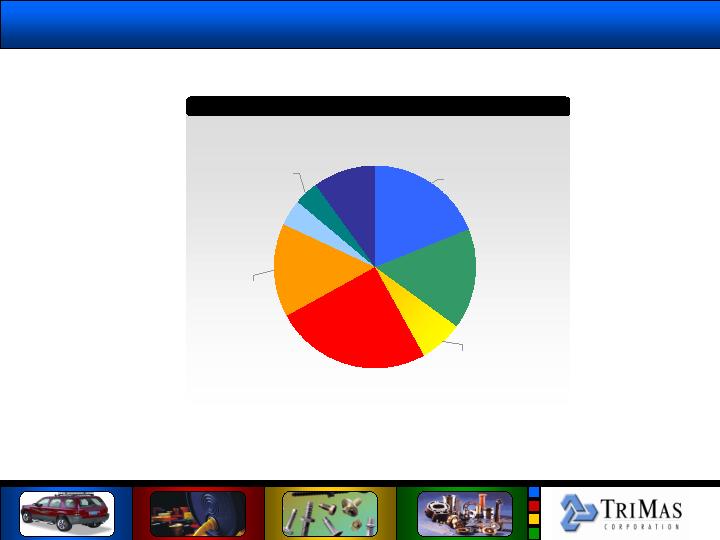

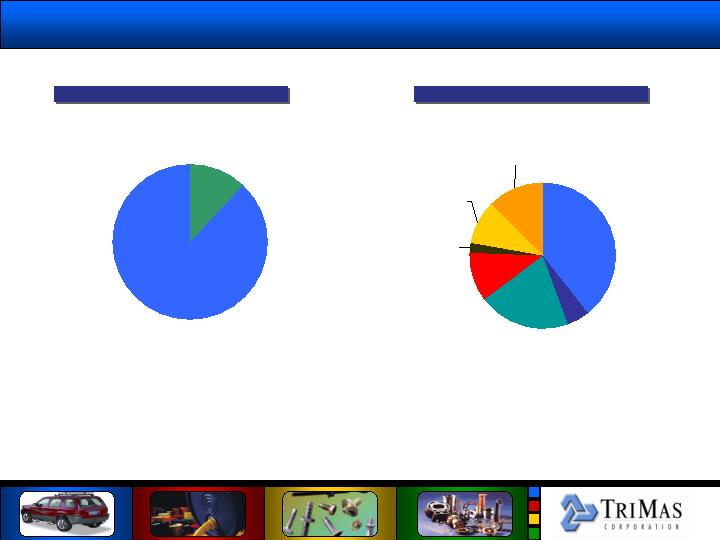

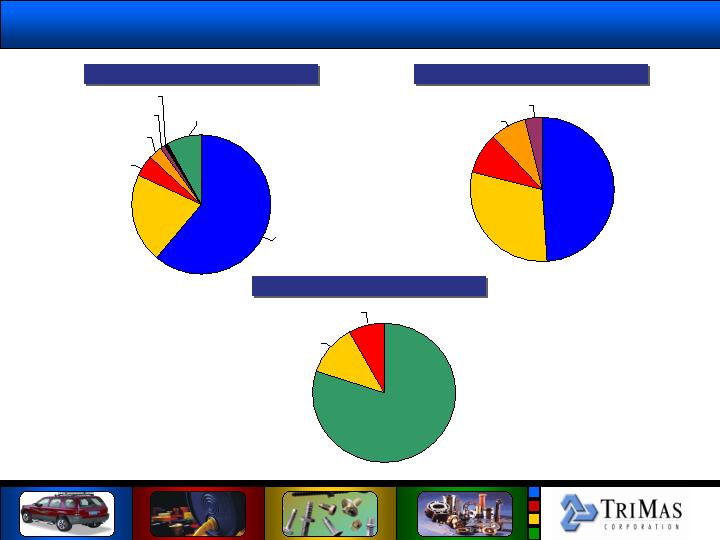

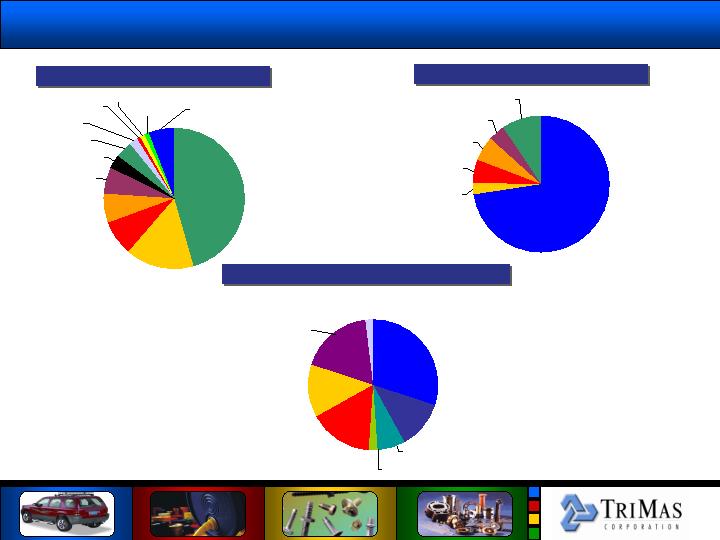

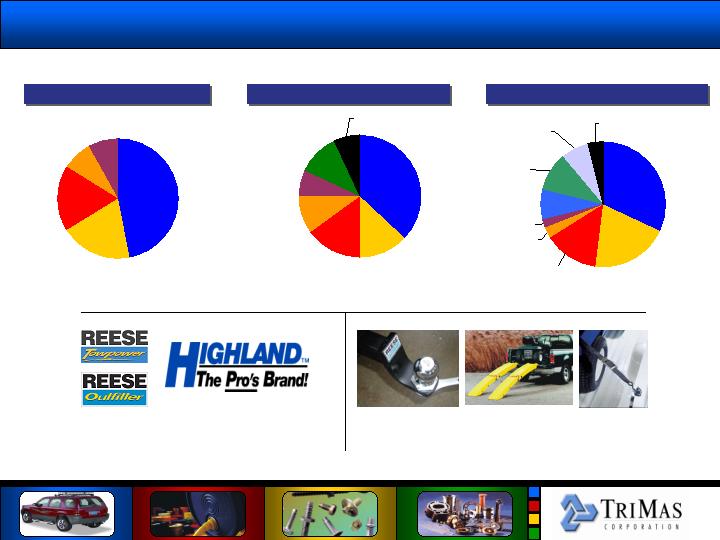

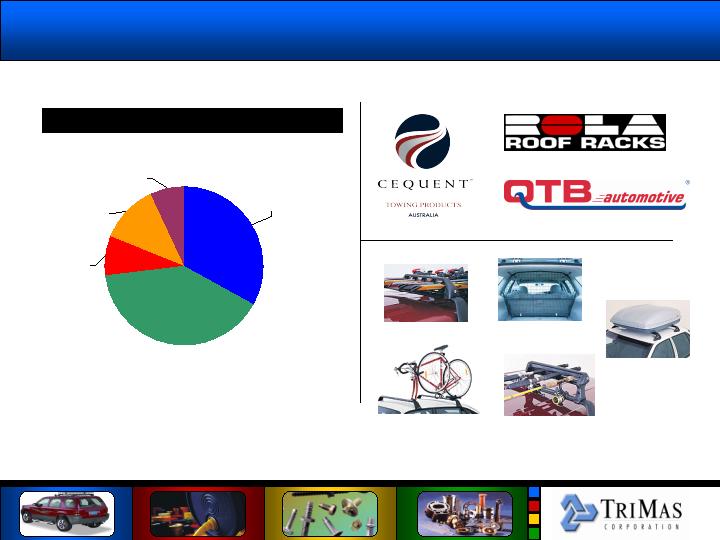

2005 (June 30, LTM) Total Cequent Net Sales …. $514.3 Million

Cequent Sales by Business Unit

Cequent Sales by Region

Cequent’s Sales Mix

Trailer

20%

Australia

11%

Towing

36%

Consumer

22%

Electrical

11%

Asia-

Pacific

11%

North

America

89%

5

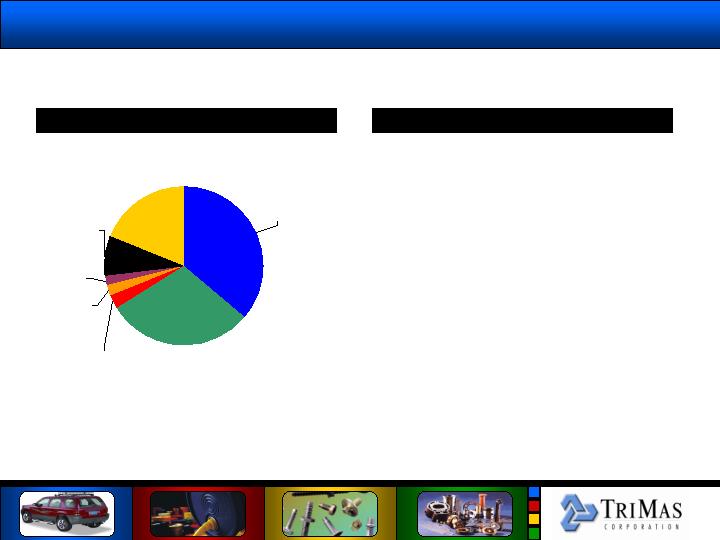

Cequent’s Sales Mix

Cequent Sales by Distribution Channel

Installer 19%

Big Box

Retail

16%

Spec. Retail

7%

RV

25%

Ag/Utility

15%

Auto OEM

4%

Marine

4%

Auto Dealer

10%

6

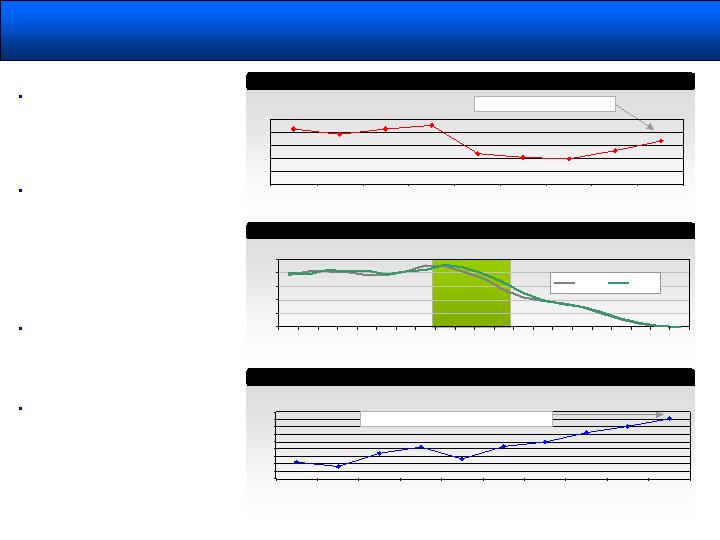

Market Overview - Recreational Vehicle Segment

U.S. RV Segment by Product Group

SOURCE: RVIA

2004 U.S. RV Market ……. $14.0 billion

(Retail Value)

Total U.S. Towable RV Trailer Market

SOURCE: RVIA

2004 U.S. Towable Trailer Market … $5.8 billion

(Retail Value)

RV Shipment Historical Volume Growth

Total Shipments

(in thousands)

*Pull ahead due to Katrina

0

50

100

150

200

250

300

350

400

450

163

203

228

259

247

248

255

293

321

300

257

307

320

370

370*

340

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005F

2006F

Towables

24%

Motorhomes

76%

Truck

Campers

3%

Folding

Camping

Trailers

4%

Conventional

Travel Trailers

47%

Fifth Wheel

Trailers

46%

1991-2005 CAGR ……. 5.8%

Total unit shipments will be down slightly in 2005.

Katrina caused a significant pull ahead into 2005,

normalized shipments expected to be flat 2005 to

2006. Industry expect volumes to reach 500,000 as

demographics continue to improve.

Perhaps the best news of all for the RV industry was

the increase in dollar values of shipments. Total

retail value of all RV shipments in 2004 rose an

impressive 15% to set an all time record high of over

$15 billion. The continued strength in RV shipments

as demonstrated by these growth trends reflects the

strong appeal of the RV lifestyle to a broadening

consumer base.

7

SOURCE:

Recreation Vehicle Industry Association, Crove Capital Markets Research

NOTE:

Does not include conversion vehicle shipments; dotted line represents a normalized

shipment trend, which was calculated using regression analysis.

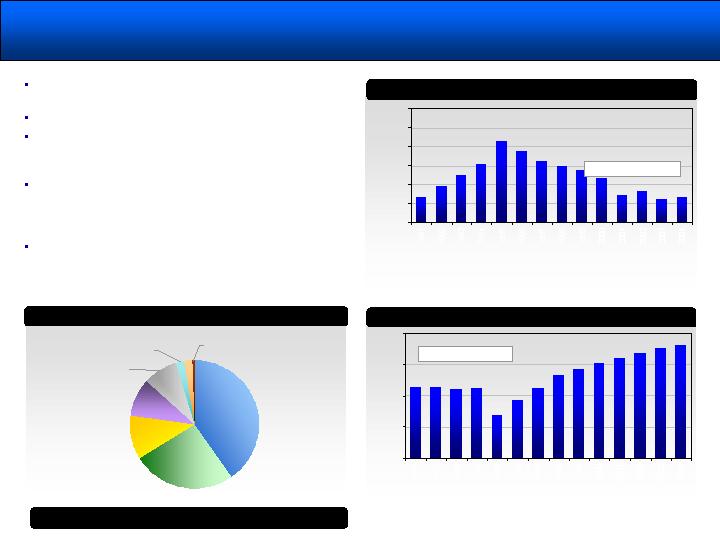

Market Overview – RV Segment Demand Drivers

SOURCE: Econstats.com

SOURCE: Energy Information Administration, conventional regular gasoline prices, U.S. Gulf Coast delivered.

(Cents per

Gallon)

(%

rate)

SOURCE: U.S. Census Bureau.

(U.S. population)

($ in

millions)

Jan- 98

Jan- 99

Jan- 00

Jan. 01

Jan. 02

Jan. 03

Jan. 04

Jan. 05

Sep. 05

0

2

4

6

8

10

2000

2004

Under 5

15 to 19

30 to 34

45 to 49

60 to 64

75 to 79

90 to 94

0

5

10

15

20

25

0

20

40

60

80

100

120

140

160

180

Jan-98

Jan-99

Jan-00

Jan. 01

Jan. 02

Jan. 03

Jan. 04

Jan. 05

June. 05

Sep. 05

( Years)

U.S. Population by Age Group

Regular Unleaded Gasoline Prices Have Been on the Rise

Driving Age Population Growth is Driving Fleet Growth and Increased Consumer Spending

U.S. Prime Lending Rate Sept. 2005 – 6.75%

U.S. Prime Lending Rate

U.S. Wholesale Price of Unleaded Regular Gas Sept. -05 ... $2.80

The U.S. prime lending rate has

been increasing. Industry experts

believe that increasing lending rates

have more impact on RV demand

than the price of gasoline. Length of

trip can always be reduced.

The U.S. population by age group

statistics indicate that the high

income age groups from 40 years old

to 60 years olds, baby boomers,

have increased by over 7.6 million

since 1998. By the end of the

decade, the number of consumers

aged 50 to 64 will total 57 million,

38% higher than in 2000.

Growth in the high income age group

is a positive factor in supporting

recreational vehicle and aftermarket

accessory product consumer

demand.

Regular unleaded gasoline prices,

while at all time highs, have less

impact on RV demand than interest

rates and disposable income which

rose 1.4% in Q2 of 2005 vs. the

2.9% decline in Q1.

8

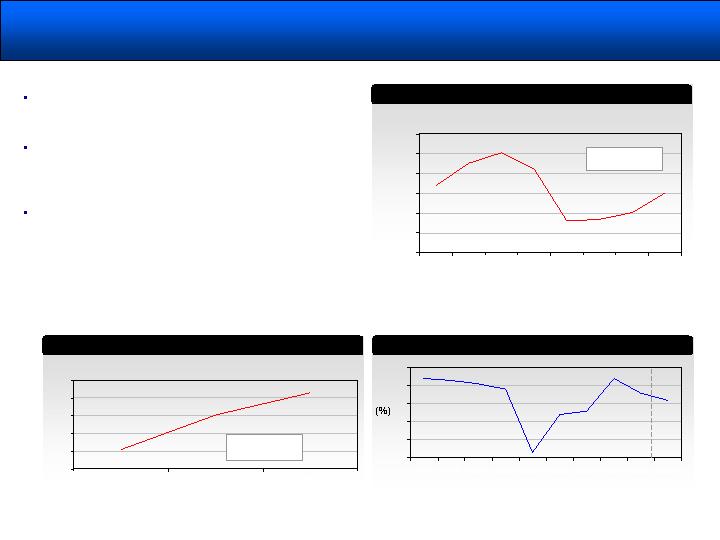

Market Overview - Marine Segment

SOURCE: NMMA

SOURCE: NMMA

SOURCE: NMMA

Total

Retail

Sales

(in

thou-

sands)

Total

Retail

Sales

(in mil-

lions)

100

125

150

175

200

225

250

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

133

147

163

176

207

194

181

174

168

136

141

131

134

14

15

16

17

18

16.3

16.3

16.2

16.2

15.4

15.8

16.2

16.6

16.8

17.0

17.2

17.4

17.5

17.6

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Canoes

11%

PWC

9%

Outboards

26%

Sterndrive

8%

Kayaks

41%

Sailboats

2%

Jet Boats

1%

Inboards

2%

Boat trailer sales peaked in 1995 and have declined

steadily until 2001, growing slightly in 2002.

2002 showed signs of a cyclical rebound in trailer sales.

The total estimated number of boats owned has

increased over the past eleven years at slow rate of 0.6%

annually.

The type of watercraft owned in the U.S is broad,

including kayaks, outboard power boats, canoes,

personal watercrafts, stern drive boats, inboard boats,

sailboats and jet boats.

All of the marine product segments require a towing,

trailer or accessory product to transport, providing

additional demand for towing and trailer products.

Boat Trailer Unit Sales

U.S. Marine Segment by Type of Product

Total Recreational Boats Owned in the U.S.

1991-2004 CAGR ……. 0.6%

2004 Total Unit Sales ……. 838,500

1991-2004 CAGR ……. 0.1%

9

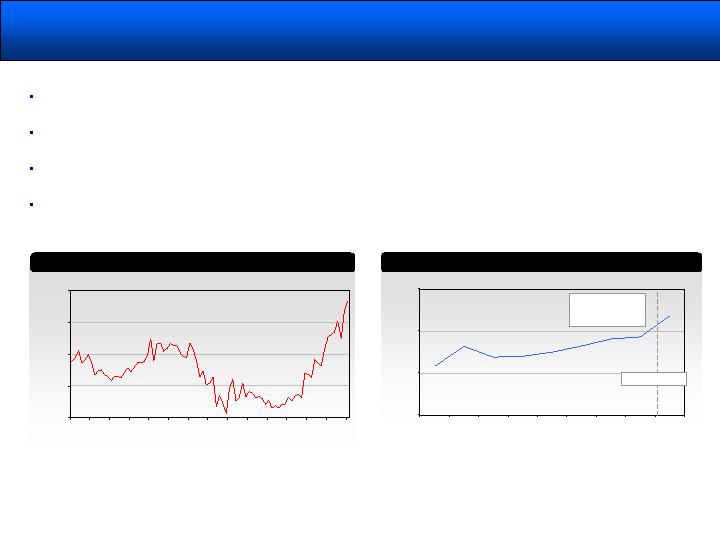

Market Overview - Other Market Segments

SOURCE: Census of Agriculture 1992 and 2002

(1) Horses and ponies and farms reporting horses and ponies.

(horses in

thousands)

SOURCE: Trailer Body Builders

(Industrial

trailers in units)

��

SOURCE: U.S. Census Bureau

1997

1998

1999

2000

2001

2002

2003

2004

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1,500

2,000

2,500

3,000

3,500

4,000

1992

1997

2002

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

0

1

2

3

4

5

The U.S. trailer production cycle typically follows GDP

growth. Current estimates of GDP growth in 2005 and

2006 are 3.6% and 3.2%, respectively.

The light industrial and utility trailer segments generally

follow the same trends as light vehicle aftermarket macro

demand as most of these consumers are using these

trailers for personal use hobbies.

Equestrian trailer industry has very few published

statistics to track demand, however, the U.S. farm

population of horses has increased at an annual rate of

1.7% over the past ten years providing an indicator of

corresponding growth in the equestrian trailer market.

CAGR

1997-2002… - 1.7%

CAGR

1992-2002 … 12.2%

U.S. Equestrian(1) Population

U.S. Gross Domestic Product YOY % Change

U.S. Industrial Trailer Production

10

Market Overview - Agricultural Equipment

North American Agricultural Equipment Demand

SOURCE: Freedonia

SOURCE: U.S. Census Bureau

U.S. Farm Machinery and Equipment Shipments

($ millions)

CAGR

1989-2004 … 1.9%

2004-2009 … 3.3%

Forecast

($ millions)

Jan-98

Jul-98

Jan-99

Jul-99

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

$20,000

$22,000

$24,000

$26,000

$28,000

$5,000

$10,000

$15,000

$20,000

1989

1994

1999

2000

2001

2002

2003

2004

2009

The three largest agricultural equipment buying regions of the World are Western Europe, Asia-Pacific and North America

accounting for 88% of total World demand.

Fredonia predicts demand in North America for agricultural equipment will grow at an average annual rate of 3.5% over the

next five years.

Historically, agricultural equipment demand in North America has grown more slowly at 1.0%, however, this measurement

in growth does not account for peak demand in the mid-1990’s.

A recent positive indicator, U.S. farm machinery and equipment shipments are on the rise, 10% higher in January over a

seasonally adjusted low in April 2003.

11

Cequent Road to Recovery(Profit Improvement)

Removed a layer of management

Elimination of 99 salaried positions

Initiated closure of four plants

Simplifying towing distribution systems

30% Towing SKU reduction project

Transfer Trailer products to Mexico

On Target to Exceed $15 Million Cost Structure Reduction

Aggressive stance with

retail/consumer customers

Offset operational cost (due to freight,

etc.) when possible

Reduce Cost Structure

Aggressive off-shore sourcing plan

Maximize leverage with steel supply

options

Raise Prices

Reduce Material Spending

12

Tom Benson, President

Industry

A Heartland Industrial Partners’ Company

Cequent Towing Products

Innovation

Growth

Cequent Towing Products – Market Share

Towing Products Market Share

Source: Internal company estimates

Cequent

Towing,

50%

Other, 2%

Curt, 9%

Putnam,

5%

EZ-Lift, 8%

Valley, 26%

14

Cequent Towing: Extensive Product Portfolio

Standard Hitch

Storage Box

Roof Racks

Auxiliary

Lighting

Electric Lift Platform

(Shown with DPS Hitch)

Cargo Trays

Compact

Carriers

Folding Carrier

5TH WHEEL HITCHES

15,000 - 30,000 lbs

Rail Kits

Gooseneck

Systems

Custom Tube Steps

Side Window Air Deflector

Side Window Louvers

Tonneau Covers

Taillight

Covers

Hitch

Receivers

Cargo Table

Swing Away

Carrier

Bumper Pack

(Shown with DPS Hitch)

5th Wheel Hitches

Custombuilt Hitches

Ball Mounts

Hitch Balls

Dual Port System

(DPSTM) Hitches

or

Standard Hitches

Connectors

Convertors

Adapters

Harnesses

Electrical

Hood Protection

Light Duty

Medium Duty

Heavy Duty

Front Mounted Receivers

& Accessories

15

Cequent Towing Trade Sales Breakdown

Source: Internal company estimates

Installer/WD,

88%

OE, 12%

Balls &

Mounts,

5.0%

Fifth Wheel,

20.3%

WDH, 10.7%

Sway

Controls,

2.3%

Brake

Controls,

9.7%

Other

(wiring, pins,

racks),

12.5%

Hitches,

39.5%

Installer Sales by Product Line

Sales by Channel

16

Cequent Towing Top Customers

Stag Parkway – Largest RV WD in

North America

Channel: RVWD

Toyota/Flex-N-Gate – TMMNA

635 Tacoma Project

Channel: Auto OE

U-Haul – Largest Purchaser of

Trailer Hitches of any Installer in

the US

Channel: Installer

17

Cequent Towing Top Customers

Rigid Hitch – Telemarketing-based

Business with no Field Sales

Force

Channel: Installer

E-Trailer – Leader in E-Commerce

Business in Towing Category

Channel: E-Commerce

Meyer Distribution – Third Largest

Truck Accessory Distributor in the

US

Channel: Truck Accessories

18

Cequent Towing - Market Update

19

Current Market Conditions

$3.00 gas has slowed the RV market and reduced disposable income (RV towables are down 7.9%

YTD)

Boat sales are off 1.8% YTD

End of automotive incentives have slowed vehicle sales

This is the slow time of the year

Opportunities

Expect a pick-up in Class I and II sales as more passenger cars are sold versus “already hitched”

SUV’s

Improved sales due to increased FTM (first to market) activity

Expect a slight increase in WDH (weight distributing hitch) sales as FEMA trailers hit the Gulf Coast

Threats

Concerns about interest rates and inflation have caused the RV trade to expect lower sales

Considerable talk in the marketplace about large distributors going offshore on a direct basis

Bob Lewis, President

Innovation

A Heartland Industrial Partners’ Company

Cequent Trailer & Electrical Products

Industry

Growth

Cequent Trailer & Electrical Products

Trailer Products

Electrical Products

21

Cequent Trailer & Electrical – Market Share

Trailer - Jacks

Trailer - Couplers

Source: Internal company estimates

Electrical Products

Atwood, 21%

Shelby, 5%

Dutton

Lainson, 3%

Stallion, 1%

Binkley, 1%

Other, 8%

Cequent, 80%

Other (Jordan,

Hopkins), 8%

Kelsey-Hayes,

12%

Cequent, 49%

Other, 4%

Lainson, 8%

Shelby, 9%

Atwood, 30%

Cequent, 61%

22

Cequent Trailer & Electrical Products

Trailer/Electrical Trade Sales by Channel

Electrical – Sales by Product Line

Source: Internal company estimates

Trailer – Sales by Product Line

Jacks, 46%

Lights, Kits &

Wiring, 6%

Locks, 3%

Accessories, 4%

Brakes, 2%

Fenders, 1%

Mounts, 1%

Service Kits, 1%

Winches, 8%

ATV Acc., 7%

Other, 6%

Couplers, 16%

Lighting

Products, 9.4%

Breakaway

Systems, 5.5%

Electrical &

Wiring, 5.8%

Other, 4.0%

Brake Controls,

72.6%

Brake

Hardware, 2.7%

Marine, 12%

OE Auto, 7%

OE RV, 2%

Retail, 16%

WD RV, 13%

Export/Misc.,

2%

AG & Indust.,

18%

Horse/Utility,

30%

23

Cequent Trailer & Electrical – Top Customers

24

Trailer/Electrical2005 Initiatives – Revenue Growth

Trailer & Electrical 2005 Initiatives

25

Target opportunities include additional trailer

brake control options, manufactured electrical

control modules and integrated connectivity

within automotive OEM

Target opportunities for expansion in RV and

Specialty OEM include LED taillights and

couplers and jacks where Cequent has not

pursued business in the past

Target opportunities for expansion in RV

distribution include an LED taillights

replacement program, enhanced lighting line,

new trailer brake control technology and

couplers/ jacks where Cequent is not a

market share leader

Target opportunities in Horse, Livestock &

Utility include the introduction of new

electric jack, the introduction of new

gooseneck couplers in a HD capacity, the

enhanced lighting program and an enhanced

line of connectivity

Target opportunities in Marine Trailer

Manufacturers, Marine Distribution & Marine

Retail include LED based illumination, our

import jack expansion and the introduction of

our pivot coupler and actuator

The launch of a Bargman branded electrical t-

connect line in Q4

Electrical harness opportunities within the

Agricultural and Industrial channel

New category growth of couplers and jacks

within the RV OEM channel

Cequent Trailer Products – Market Update

26

Current Market Conditions

Trailer OEM Feeders currently busy with FEMA orders (dump and construction

trailers in high demand)

Marine suffering from years of decreased demand, will be impacted by fuel costs

even more

Ag and Industrial has been steady, impacted by fuel prices that consume budgets in

lieu of capital purchases

Q4 will be stronger than previous estimates, could see some FEMA trailer build

impact, some peripheral RV support

Opportunities

RV manufacturer penetration with steel parts and electrical

Off-shore sourcing

More Mexico production

Threats

Fuel prices impact travel, capital budgets for equipment, the “blue collar” marine

purchases

Chinese imports and infringement of our patents, below market pricing

Cequent Electrical Products – Market Update

27

Trailer OEM Feeders currently busy with FEMA orders (dump and construction

trailers in high demand)

RV distributors working off inventories this year, should buy into the Q4 dating for

upcoming Q1 ’06 shows

RV OEM will add one month of sales of lighting products for FEMA in Q4

Auto OEM will remain constant in Q4

RV manufacturer penetration with steel parts and electrical with our consolidated

sales channel approach

Lighting line expansion, new catalog, new products (i.e. LED)

Q1 ’06 rebuild of RV inventories on dealer lots

Chinese imports, below market pricing

Fuel prices on RV buyers

Cequent Electrical Products – Market Update

Cequent Electrical Products – Market Update

Current Market Conditions

Opportunities

Threats

Craig Manchen, President

Innovation

A Heartland Industrial Partners’ Company

Cequent Consumer Products

Industry

Growth

Cequent Consumer – Market Share

Loading Ramps

Tie Downs & Stretch Cords

Source: Internal company estimates

Towing Accessories

Valley, 19%

MasterLock,

18%

Bully, 8%

Other, 8%

Cequent, 47%

Daws/Better

Built, 13%

Ohio Steel, 15%

Oxlite, 10%

Universal

Industrial, 7%

5-Star, 11%

Other , 7%

Cequent, 37%

Keeper, 20%

Allied, 14%

USA Products,

3%

Erickson, 2%

Joubert, 8%

Other, 4%

Home Depot

(PL), 7%

Lowes (PL),

10%

Cequent, 32%

29

Cequent Consumer Products

Load:

Anchor:

Secure:

Carry:

Organize:

Protect:

Cargo Management Products

LOAD

ANCHOR

SECURE

CARRY

ORGANIZE

PROTECT

A full line of aluminum, steel and plastic loading

ramps and ramp kits provide sturdy, safe loading of

motorcycles, ATVs, lawn tractors and other

equipment.

Anchor systems and hardware to anchor heavy

loads, attach tie downs, truck caps, toolboxes,

camper shells, over-the-rail bedliners, tonneau

covers, antenna mounts, cab extenders and more.

A complete line of tie downs, tarp straps, stretch

cords and bungee cords to meet all securing needs.

Products are available in a wide number of styles to

match specific use.

Products which expand vehicle carrying capacity,

which include roof top, rear and hitch mount carriers

for luggage, bikes and construction.

A wide range of products to organize vehicle and

garage, including the new award winning Space

Master cargo organizer, truck and storage nets,

cargo bars, and a complete line of garage

organization products.

Keeps vehicles looking SHOWROOM NEW with

Cargo Liners, Floor Guards, All Weather Floor Mats,

Hump Liners, and Splash Guards. Custom fit vehicle

protection for trucks, cars, vans, and SUVs.

30

Cequent Consumer Products

HITCHES

TOWING ACCESSORIES

TRAILER ACCESSORIES

ELECTRICAL & LIGHTING

Towing, Trailering and Electrical Products

31

Hitches:

Multi-fit and customer fit hitches for a wide range of

vehicles, from light duty to heavy duty applications.

Towing:

Complete range of towing accessories for any usage

application, including ball mounts, hitch balls, locking

accessories, heavy duty towing products, and safety

chains. Hitch Balls and ball mounts feature our

exclusive InterLock™ design.

Trailer:

Full line of trailer accessories to fit marine, utility and

agricultural trailers. Products include couplers, jacks,

winches, and wheel bearing kits.

Electrical:

Products that connect the towing vehicle to the

trailer, including, brake controls, adapters, universal

and custom electrical connectors, and wiring kits.

Lighting:

A broad line of trailer and towing lights for marine,

utility and agricultural trailers. Products provide

added safety and visibility, and include clearance

markers, reflectors, stop/turn/tail lights and

submersible light kits.

Cequent Consumer – Market Update

Retail sales of Towing/Tie Down/Trailer Products has been growing at a rate

of 3-5% over the last four years

Retail sales in 2005 started very strong earlier in the year: 10% sales growth

Now experiencing softness in sales due to high gas prices (less disposable

income and lower store traffic) – flat with last year

Retail market share growing on DIY (Do It Yourself) Towing Accessories

(e.g., non-application-specific hitches, balls, ball mounts, locks, etc.)

Retail market share also growing on DIY Tie Downs and Trailer Products

(easy to use products priced at a value)

Application-specific hitches buying through OE or Installer (hard to install,

substantial retailer inventory commitment)

Consumers are looking for value (quality, name brand products, at fair prices)

32

Cequent Consumer – Opportunities & Threats

Competition is more experienced in off-

shore sourcing – CCP now has major

initiatives underway

Competition has focused on innovation to

penetrate our shelves – increasing our focus

on innovation

Consolidation of retail customers has

created extremely large customers with high

leverage

Some of these customers are looking to

source our products directly from Asian

sources

Reese brand name stand for quality to both

the consumer and retailer

Retailers understand the importance of the

Reese brand – worked with us during our

integration hardships in 2004

Currently raising pricing/profits on towing

items as customer service improves

Extending the Reese brand into other

product categories (Tie Downs, Electrical,

Lighting, Marine)

Switching production to lower cost Asian

sources, while maintaining strict quality

specifications

Consolidating warehousing/shipping of all

retail products for cost savings and ease of

servicing customers

Expect profitability and sales to grow

substantially in 2006 and beyond

Threats

Opportunities

33

Cequent Consumer - Opportunities (cont’d)

Top accounts offer significant growth potential

Major retailers are committed to double-digit growth

Combined, these retailers open hundreds of new stores each year

Acquisitions by major retailers are common, e.g.,

Advance Auto recently acquired American International (65 stores)

and Lappens Auto Parts (18 stores)

O’Reilly recently purchased Midwest Auto (65 stores)

Wal-Mart expanding globally

34

Ed Schwartz, Group President

Cequent Transportation Accessories

A Heartland Industrial Partners’ Company

Cequent Australia

Industry

Innovation

Growth

Cequent Australia

Australia Sales by Channel

Other, 7%

Towing

Aftermarket,

33%

Roof Racks

OE, 12%

Roof Racks

Aftermarket,

8%

Towing OE,

40%

36

Cequent Australia

Estimated Sales by Product

Top Customers

Toyota

Ford

Nissan

GM Holden

Subaru

Towing OE,

30%

Side Steps,

2%

Caravan &

Camping,

8%

Protection

Bars, 2%

Cargo

Barriers, 3%

Roof Rack

Accessories,

19%

Towing

Aftermarket,

36%

37

2006 Imperatives - Business Partners

TriMotive enjoys tremendous relationships with OE vehicle manufacturers

Represented with every marquee in Australia

Relationships with parent overseas (Japan, Thailand, Korea)

Awarded supplier

Q1

Toyota President Award

Nomination yearly since 2000

Established Corporate Organizations

Trust

IP

Stringent standards

Long term relationship building

Recognize value add

Expect continued investment

Innovation

Japan

FHI - Subaru

Brisbane OLD

Planned

Current

Ford

Mitsubishi

Nissan

Toyota

Subaru

Audi

Daewoo

SsangYong

Hidden

BMW

Daimler Chrysler

Porsche

Honda

AdelaideSA

Sydney NSW

Melbourne Victoria

38

Mitsubishi

Suzuki - Mayfair

Hyundai / Mobis

GM Daewoo

Toyota

Ford

Nissan

Renault

Mazda

Suzuki

Toyota Engineering

Alfa

Citroen

Mobis / Hyundai

Cequent Wrap-Up

Events beyond our control are impacting the Cequent group of companies

Gas prices

Weather (Katrina/Rita)

Economy

We are dealing with these events on a number of fronts

Sales initiatives

Cost reductions – Road to Recovery

Price increases – Road to Recovery

Customer/market tough decisions

We appreciate your support and thank you for attending

Q&A?

39

Thank You!

Innovation

A Heartland Industrial Partners’ Company

Industry

Growth