UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________

FORM 20-F

(Mark One)

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | OR | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | For the fiscal year ended December 31, 2014 | |

| | OR | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | OR | |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission file number: 001-10306

THE ROYAL BANK OF SCOTLAND GROUP plc

(Exact name of Registrant as specified in its charter)

United Kingdom

(Jurisdiction of incorporation)

RBS Gogarburn, PO Box 1000, Edinburgh EH12 1HQ, United Kingdom

(Address of principal executive offices)

Aileen Taylor, Chief Governance Officer and Board Counsel, Tel: +44 (0) 131 626 4099, Fax: +44 (0) 131 626 3081

PO Box 1000, Gogarburn, Edinburgh EH12 1HQ

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| | | |

| American Depositary Shares, each representing 2 ordinary shares, nominal value £1 per share | | New York Stock Exchange |

| Ordinary shares, nominal value £1 per share | | |

| American Depositary Shares Series F, H, L, M, N, P, Q, R, S, T and U each representing one Non-Cumulative Dollar Preference Share, Series F, H, L, M, N, P, Q, R, S, T and U respectively | | New York Stock Exchange* |

| Dollar Perpetual Regulatory Tier 1 Securities | | New York Stock Exchange |

| 3.950% Senior Notes due 2015 | | New York Stock Exchange |

| 2.550% Senior Notes due 2015 | | New York Stock Exchange |

| 4.375% Senior Notes due 2016 | | New York Stock Exchange |

| Floating Rate Senior Notes due 2017 | | New York Stock Exchange |

| 1.875% Senior Notes due 2017 | | New York Stock Exchange |

| 4.70% Subordinated Notes due 2018 | | New York Stock Exchange |

| 5.625% Senior Notes due 2020 | | New York Stock Exchange |

| 6.125% Senior Notes due 2021 | | New York Stock Exchange |

| 6.125% Subordinated Tier 2 Notes due 2022 | | New York Stock Exchange |

| 6.000% Subordinated Tier 2 Notes due 2023 | | New York Stock Exchange |

| 6.100% Subordinated Tier 2 Notes due 2023 | | New York Stock Exchange |

| 5.125% Subordinated Tier 2 Notes due 2024 | | New York Stock Exchange |

| Structured HybrId Equity Linked Securities (SHIELDS) due January 16 2014 linked to the S&P 500 Index | | NYSE MKT |

| Leveraged CPI Linked Securities due January 13, 2020 | | NYSE MKT |

| RBS US Large Cap TrendpilotTM Exchange Traded Notes due December 7, 2040 | | NYSE Arca |

| RBS US Mid Cap TrendpilotTM Exchange Traded Notes due January 25, 2041 | | NYSE Arca |

| RBS Gold TrendpilotTM Exchange Traded Notes due February 15, 2041 | | NYSE Arca |

| RBS Oil TrendpilotTM Exchange Traded Notes due September 13, 2041 | | NYSE Arca |

| RBS Global Big Pharma Exchange Traded Notes due October 25, 2041 | | NYSE Arca |

| RBS NASDAQ-100® TrendpilotTM Exchange Traded Notes due December 13, 2041 | | NYSE Arca |

| RBS China TrendpilotTM Exchange Traded Notes due April 18, 2042 | | NYSE Arca |

| RBS US Large Cap Alternator Exchange Traded NotesTM due September 5, 2042 | | NYSE Arca |

| RBS Rogers Enhanced Commodity Index Exchange Traded Notes due October 29, 2042 | | NYSE Arca |

| RBS Rogers Enhanced Agriculture Exchange Traded Notes due October 29, 2042 | | NYSE Arca |

| RBS Rogers Enhanced Energy Exchange Traded Notes due October 29, 2042 | | NYSE Arca |

| RBS Rogers Enhanced Precious Metals Exchange Traded Notes due October 29, 2042 | | NYSE Arca |

| RBS Rogers Enhanced Industrial Metals Exchange Traded Notes due October 29, 2042 | | NYSE Arca |

* Not for trading, but only in connection with the registration of American Depositary Shares representing such ordinary shares pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

_______________

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

_______________

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2014, the close of the period covered by the annual report:

| (Title of each class) | | (Number of outstanding shares) |

| Ordinary shares of £1 each | | 6,365,895,896 |

| B Shares | | 51,000,000,000 |

| Dividend Access Share | | 1 |

| 11% cumulative preference shares | | 500,000 |

| 5½% cumulative preference shares | | 400,000 |

| Non-cumulative dollar preference shares, Series F, H and L to U | | 209,609,154 |

| Non-cumulative convertible dollar preference shares, Series 1 | | 64,772 |

| Non-cumulative euro preference shares, Series 1 to 3 | | 2,044,418 |

| Non-cumulative convertible sterling preference shares, Series 1 | | 14,866 |

| Non-cumulative sterling preference shares, Series 1 | | 54,442 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | Non-Accelerated filer o |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

oU.S. GAAP

x International Financial Reporting Standards as issued by the International Accounting Standards Board

oOther

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

SEC Form 20-F cross reference guide

| Item | Item Caption | Pages |

| | | |

| PART I | |

| 1 | Identity of Directors, Senior Management, | Not applicable |

| | Advisers | |

| | | |

| 2 | Offer Statistics and Expected Timetable | Not applicable |

| | | |

| 3 | Key Information | |

| | Selected financial data | 113-114, 409-412, 450-451, 460, 490-492 |

| | Capitalisation and indebtedness | Not applicable |

| | Reasons for the offer and use of proceeds | Not applicable |

| | Risk factors | 110-112, 466-484 |

| | | |

| 4 | Information on the Company | 117-121, 161, 212-330, 384-387, 391-392, 397-398, 450-460, 518 |

| | History and development of the Company | 3, 99-104, 107, 399-401, 421,462, 504 |

| | Business overview | 13, 21, 99-100, 107-112, 127-160, 184-186, 188, 434-439, 461 |

| -464 | | |

| | Organisational structure | 99, 107-108, 434, 461, Exhibit 8.1 |

| | Property, plant and equipment | 397-398, 461 |

| | | |

4A | Unresolved Staff Comments | Not applicable |

| | | |

| 5 | Operating and Financial Review and Prospects | |

| | Operating results | 15-33, 109, 113-161,184-186,188, 389-390, 434-439, 460 |

| | Liquidity and capital resources | 160-161, 164-179, 191-226, 270-293, 339, 366-370, 389-392, 399-401, 406-408, 410-412, 418-421, 432-433, 450-451,460 |

| | Research and development, patents, licences etc | Not applicable |

| | Trend information | 9-24, 107-108, 466-485 |

| | Off balance sheet arrangements | 415-416, 420-421 |

| | Contractual obligations | 212-226, 231, 384-386, 413-414, 417, 420-421 |

| | | |

| | | |

| 6 | Directors, Senior Management and Employees | |

| | Directors and senior management | 47-52 |

| | Compensation | 74-95, 354-363, 440 |

| | Board practices | 46-50, 51-55, 58-62, 74-75, 102-103 |

| | Employees | 100, 123-124, 129, 355-357 |

| | Share ownership | 82-84, 87-89, 103, 355-357 |

| | | |

| 7 | Major Shareholders and Related Party Transactions | |

| | Major shareholders | 104, 462 |

| | Related party transactions | 440, 441 |

| | Interests of experts and counsel | Not applicable |

| | | |

| 8 | Financial Information | |

| | Consolidated statements and other financial information | 99, 331-449, 491 |

| | Significant changes | |

| | | |

| 9 | The Offer and Listing | |

| | Offer and listing details | 490 |

| | Plan of distribution | Not applicable |

| | Markets | 98, 489 |

| | Selling shareholders | Not applicable |

| | Dilution | Not applicable |

| | Expenses of the issue | Not applicable |

| | | |

| 10 | Additional Information | |

| | Share capital | Not applicable |

| | Memorandum and articles of association | 495-504 |

| | Material contracts | 462-464 |

| | Exchange controls | 495 |

| | Taxation | 492-495 |

| | Dividends and paying agents | Not applicable |

| | Statement of experts | Not applicable |

| | Documents on display | 504 |

| | Subsidiary information | Not applicable |

| | | |

| 11 | Quantitative and Qualitative Disclosure | 165-330, 297-298, 300-318, 366-387, 389-390 |

| | about Market Risk | |

| | | |

| 12 | Description of Securities other than Equity Securities | 465 |

| Item | Item Caption | Pages |

| | | |

| PART II | |

| 13 | Defaults, Dividend Arrearages and Delinquencies | Not applicable |

| | | |

| 14 | Material Modifications to the Rights of Security | |

| | Holders and Use of Proceeds | Not applicable |

| | | |

| 15 | Controls and Procedures | 60-62, 96-98, 332 |

| | | |

| 16 | [Reserved] | |

| 16 | A Audit Committee financial expert | 58-62, 98 |

| 16 | B Code of ethics | 101 |

| 16 | C Principal Accountant Fees and services | 58-62, 363 |

| 16 | D Exemptions from the Listing Standards | Not applicable |

| | for Audit Committees | |

| 16 | E Purchases of Equity Securities by the | Not applicable |

| | Issuer and Affiliated Purchasers | |

| 16 | F Change in Registrant’s Certifying Accountant | Not applicable |

| 16 | G Corporate Governance | 51-55 |

| 16 | H Mine Safety Disclosure | Not applicable |

| | | |

| | | |

| PART III | | |

| 17 | Financial Statements | Not applicable |

| | | |

| 18 | Financial Statements | 331-448 |

| | | |

| 19 | Exhibits (including certifications) | |

| | | |

| | Signature | |

| 1 | Strategic Report |

| 2 | Forward-looking statements |

| 2 | Presentation of information |

| 3 | Recent Developments |

| 4 | 2014 Performance |

| 7 | Our progress in 2014 |

| 8 | Chairman’s statement |

| 9 | Chief Executive’s review |

| 13 | Our business model and strategy |

| 13 | - Our Structure |

| 14 | - Our Strategy |

| 14 | - Our Plan |

| 18 | - Our Operating Model |

| 18 | - Our Values |

| 19 | - Our Customers |

| 21 | Key economic indicators |

| 24 | Business review |

| 25 | - Personal & Business Banking |

| 27 | - Commercial & Private Banking |

| 29 | - Corporate & Institutional Banking |

| 31 | - Citizens Financial Group |

| 32 | - RBS Capital Resolution |

| 33 | - Services |

| 35 | Governance at a glance |

| 37 | Risk overview |

| 39 | Sustainability |

| | Detailed information |

| 43 | Governance report |

| 106 | Business review |

| 164 | Capital and risk management |

| 331 | Financial statements |

| 449 | Additional information |

| 486 | Shareholder information |

| 506 | Abbreviations and acronyms |

| 507 | Glossary of terms |

| 515 | Index |

| 518 | Important addresses |

Forward-looking statements

Certain sections in this document contain ‘forward-looking statements’ as that term is defined in the United States Private Securities Litigation Reform Act of 1995, such as statements that include the words ‘expect’, ‘estimate’, ‘project’, ‘anticipate’, ‘believe’, ‘should’, ‘intend’, ‘plan’, ‘could’, ‘probability’, ‘risk’, ‘Value-at-Risk (VaR)’, ‘target’, ‘goal’, ‘objective’, ‘may’, ‘endeavour’, ‘outlook’, ‘optimistic’, ‘prospects’ and similar expressions or variations on these expressions.

In particular, this document includes forward-looking statements relating, but not limited to: The Royal Bank of Scotland Group’s (RBS) Transformation Plan (which includes RBS’s 2013/2014 strategic plan relating to the implementation of its new divisional and functional structure and the continuation of its balance sheet reduction programme including its proposed divestments of Williams & Glyn and CFG, RBS’s information technology and operational investment plan, the proposed restructuring of RBS’s CIB business and the restructuring of the Group as a result of the implementation of the regulatory ring-fencing regime), as well as restructuring, capital and strategic plans, divestments, capitalisation, portfolios, net interest margin, capital and leverage ratios, liquidity, risk-weighted assets (RWAs), RWA equivalents (RWAe), Pillar 2A, Maximum Distributable Amount (MDA), total loss absorbing capital (TLAC), minimum requirements for eligible liabilities (MREL) return on equity (ROE), profitability, cost:income ratios, loan:deposit ratios, funding and risk profile; litigation, government and regulatory investigations including investigations relating to the setting of interest rates and foreign exchange trading and rate setting activities; costs or exposures borne by RBS arising out of the origination or sale of mortgages or mortgage-backed securities in the US; RBS’s future financial performance; the level and extent of future impairments and write-downs; and RBS’s exposure to political risks, credit rating risk and to various types of market risks, such as interest rate risk, foreign exchange rate risk and commodity and equity price risk. These statements are based on current plans, estimates, targets and projections, and are subject to inherent risks, uncertainties and other factors which could cause actual results to differ materially from the future results expressed or implied by such forward-looking statements. For example, certain market risk disclosures are dependent on choices relying on key model characteristics and assumptions and are subject to various limitations. By their nature, certain of the market risk disclosures are only estimates and, as a result, actual future gains and losses could differ materially from those that have been estimated.

Other factors that could adversely affect our results and the accuracy of forward looking statements in this document include the risk factors and other uncertainties discussed in the risk factors on pages 110 to 112 and 466 to 484. These include the significant risks for the Group presented by the execution of the Transformation Plan; RBS’s ability to successfully implement the various initiatives that are comprised in the Transformation Plan, particularly the balance sheet reduction programme including the divestment of Williams & Glyn and its remaining stake in CFG, the proposed restructuring of its CIB business and the significant restructuring undertaken by the Group as a result of the implementation of the ring fence; whether RBS will emerge from implementing the Transformation Plan as a viable, competitive, customer focussed and profitable bank; RBS’ ability to achieve its capital targets which depend on RBS’ success in reducing the size of its business; the cost and complexity of the implementation of the ring-fence and the extent to which it will have a material adverse effect on RBS; the risk of failure to realise the benefit of RBS’s substantial investments in its information technology and operational infrastructure and systems, the significant changes, complexity and costs relating to the implementation of the Transformation Plan, the risks of lower revenues resulting from lower customer retention and revenue generation as the Group refocuses on the UK as well as increasing competition. In addition, there are other risks and uncertainties. These include RBS’s ability to attract and retain qualified personnel; uncertainties regarding the outcomes of legal, regulatory and governmental actions and investigations that the Group is subject to and any resulting material adverse effect on the Group of unfavourable outcomes;; heightened regulatory and governmental scrutiny and the increasingly regulated environment in which the Group operates; uncertainty relating to how policies of the new government elected in the May 2015 UK election may impact RBS including a possible referendum on the UK’s membership of the EU; operational risks that are inherent in RBS’s business and that could increase as RBS implements its Transformation Plan; the potential negative impact on RBS’s business of actual or perceived global economic and financial market conditions and other global risks; how RBS will be increasingly impacted by UK developments as its operations become gradually more focussed on the UK; uncertainties regarding RBS exposure to any weakening of economies within the EU and renewed threat of default by certain counties in the Eurozone; the risks resulting from RBS implementing the State Aid restructuring plan including with respect to the disposal of certain assets and businesses as announced or required as part of the State Aid restructuring plan; the achievement of capital and costs reduction targets; ineffective management of capital or changes to regulatory requirements relating to capital adequacy and liquidity; the ability to access sufficient sources of capital, liquidity and funding when required; deteriorations in borrower and counterparty credit quality; the extent of future write-downs and impairment charges caused by depressed asset valuations; the value and effectiveness of any credit protection purchased by RBS; the impact of unanticipated turbulence in interest rates, yield curves, foreign currency exchange rates, credit spreads, bond prices, commodity prices, equity prices; basis, volatility and correlation risks; changes in the credit ratings of RBS; changes to the valuation of financial instruments recorded at fair value; competition and consolidation in the banking sector; regulatory or legal changes (including those requiring any restructuring of RBS’s operations); changes to the monetary and interest rate policies of central banks and other governmental and regulatory bodies; changes in UK and foreign laws, regulations, accounting standards and taxes; impairments of goodwill; the high dependence of RBS’ operations on its information technology systems and its increasing exposure to cyber security threats; the reputational risks inherent in RBS’ operations; the risk that RBS may suffer losses due to employee misconduct; pension fund shortfalls; the recoverability of deferred tax assets by the Group; HM Treasury exercising influence over the operations of RBS; limitations on, or additional requirements imposed on, RBS’s activities as a result of HM Treasury’s investment in RBS; and the success of RBS in managing the risks involved in the foregoing.

The forward-looking statements contained in this document speak only as of the date of this announcement, and RBS does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

The information, statements and opinions contained in this document do not constitute a public offer under any applicable legislation or an offer to sell or solicitation of any offer to buy any securities or financial instruments or any advice or recommendation with respect to such securities or other financial instruments.

Presentation of information

In this document, and unless specified otherwise, the term ‘company’ or ‘RBSG’ means The Royal Bank of Scotland Group plc, ‘RBS’, ‘RBS Group’ or the ‘Group’ means the company and its subsidiaries, ‘the Royal Bank’ or ‘RBS plc’ means The Royal Bank of Scotland plc and ‘NatWest’ means National Westminster Bank Plc.

The company publishes its financial statements in pounds sterling (‘£’ or ‘sterling’). The abbreviations ‘£m’ and ‘£bn’ represent millions and thousands of millions of pounds sterling, respectively, and references to ‘pence’ represent pence in the United Kingdom (‘UK’). Reference to ‘dollars’ or ‘$’ are to United States of America (‘US’) dollars. The abbreviations ‘$m’ and ‘$bn’ represent millions and thousands of millions of dollars, respectively, and references to ‘cents’ represent cents in the US. The abbreviation ‘€’ represents the ‘euro’, the European single currency, and the abbreviations ‘€m’ and ‘€bn’ represent millions and thousands of millions of euros, respectively.

The geographic analysis in the Business Review, including the average balance sheet and interest rates, changes in net interest income and average interest rates, yields, spreads and margins in this report have generally been compiled on the basis of location of office - UK and overseas – unless indicated otherwise. ‘UK’ in this context includes transactions conducted through the offices in the UK which service international banking transactions.

The results, assets and liabilities of individual business units are classified as trading or non-trading based on their predominant activity. Although this method may result in some non-trading activity being classified as trading, and vice versa, any resulting misclassification is not expected to be material.

Non-GAAP financial information

The directors manage RBS’s performance by class of business, before certain reconciling items, as is presented in the segmental analysis in Note 38 (the “non-statutory basis”). In 2014, RBS made changes to the reconciling items and only the following will now be reported as reconciling items: own credit adjustments, gain/(loss) on redemption of own debt, write-down of goodwill, strategic disposals and RFS Holdings minority interest.

Further the results of Citizens are included in the appropriate caption in the financial results presented on a non-statutory basis and included in discontinued operations in the financial results presented on a statutory basis. Discussion of RBS’s performance in this report presents RBS's results on a non-statutory basis as management believes that such measures allow a more meaningful analysis of RBS’s financial condition and the results of its operations. These measures are non-GAAP financial measures. A body of generally accepted accounting principles such as IFRS is commonly referred to as ‘GAAP’. A non-GAAP financial measure is defined as one that measures historical or future financial performance, financial position or cash flows but which excludes or includes amounts that would not be so adjusted in the most comparable GAAP measure. Reconciliations of these non-GAAP measures to the closest equivalent GAAP measure are presented throughout this document and in the segmental analysis in Note 38. These non-GAAP financial measures are not a substitute for GAAP measures.

Furthermore, RBS has divided its operations into “RBS excluding RBS Capital Resolution (RCR)” for all periods in 2014 and for prior periods “RBS excluding Non-Core”. Certain measures disclosed in this document for RBS excluding RCR/Non-Core operations are non-GAAP financial measures used by management as they represent a combination of all reportable segments with the exception of RCR/Non-Core.

The presentation of the financial perforance of Personal & Business Banking (“PBB”) which combines the reportable segments of UK Personal & Business Banking and Ulster Bank and the presentation of the financial performance of Commercial & Private Banking (“CPB”) which combines the reportable segments of Commercial Banking and Private Banking are non GAAP financial measures. In addition the presentation of operating profit, operating expenses and other performance measures excluding the impact of restructuring costs and litigation and conduct costs is a non-GAAP financial measure and is not a substitute for the equivalent GAAP measure.

Lastly, the liquidity coverage ratio, stressed outflow coverage, net stable funding ratio and other capital and liquidity metrics included in the Capital and risk management section are non-GAAP financial measures and are being presented for informational purposes given they are metrics that are not yet required to be disclosed by a government, governmental authority or self-regulatory organisation.

International Financial Reporting Standards

As required by the Companies Act 2006 and Article 4 of the European Union IAS Regulation, the consolidated financial statements of RBS are prepared in accordance with International Financial Reporting Standards issued by the International Accounting Standards Board (IASB) and interpretations issued by the IFRS Interpretations Committee of the IASB as adopted by the European Union (together ‘IFRS’). They also comply with IFRS as issued by the IASB.

Recent developments

Sale of a North American loan portfolio to Mizuho

On 26 February 2015, RBS announced that it has entered into a definitive agreement with Mizuho Bank, Ltd. ("Mizuho"), a wholly-owned subsidiary of the Mizuho Financial Group, for the sale of a portfolio of US and Canadian loan commitments. As part of the transaction, the parties also continue to explore the transfer of certain associated derivatives, and the transition from RBS to Mizuho of certain coverage banking, debt capital markets, syndicate, and associated capabilities related to these commitments.

The transaction is aligned with the strategic direction RBS has announced for its Corporate & Institutional Banking business, which will focus mainly on UK and Western European customers, built on existing product and service strengths. RBS will remain engaged in the US, serving a select group of North American clients with strong links into the UK.

The portfolio sold to Mizuho comprises $36.5 billion of loan commitments, including $3.2 billion of drawn assets, as of 31 December 2014. The risk-weighted assets associated with the portfolio business were approximately $8 billion as of 31 December 2014, and it generated profit after tax of $0.1 billion in the year ended on that date. The cash consideration on that basis would be approximately $3.0 billion, generating a loss on disposal of $0.2 billion. Actual cash consideration and loss will depend upon settlement date portfolio balances. Sale proceeds will be used for general corporate purposes.

The transaction is expected to complete before the end of Q2 2015. RBS will work closely with Mizuho and our existing clients associated with these loan commitments to ensure an orderly and seamless transition at completion.

Moody’s

On 17 March 2015, Moody’s announced multiple rating reviews following the publication of its new bank rating methodology on 16 March 2015. The new methodology affects banking entities globally and reflects, among other things, Moody’s lowered expectations about the likelihood of government support for European banks in light of the introduction of the EU Bank Recovery and Resolution Directive ("BRRD"). Moody’s provided a preliminary indication of the outcome of its review which is to be completed later in 2015. Moody’s preliminary indication contemplates that RBS’s long-term senior unsecured and issuer credit ratings would be downgraded by two notches to Ba1 and that the credit ratings of certain of the Group subsidiaries may also be downgraded. If these downgrades occur, the credit ratings of RBSG and of certain of its subsidiaries would, therefore, be considered to be below-investment grade by that credit rating agency.

Partial sale of Citizens Financial Group, Inc. stake

On 23 March 2015, RBS announced that it intended to sell part of its shareholding in Citizens Financial Group, Inc. (Citizens), and on 26 March 2015 announced the pricing of the offer.

The offer comprised 155.25 million shares, or 28.4%, of Citizens common stock at a public offering price per share of $23.75.

Gross proceeds realised by RBS will be $3.7 billion with the cash proceeds being used for general business purposes.

Following the offering, RBS will continue to hold up to 41.9% of Citizens shares of common stock which are subject to a 90-day lock-up. During this period, the lock-up agreement is subject to modification, waiver or cancellation. RBS will continue to consolidate Citizens in its financial statements.

The partial sale is part of RBS's strategy to fully exit its holding in Citizens by the end of 2016 as part of its European Commission state aid commitments.

Disposal internationally managed Private Banking and Wealth Management business

On 27 March 2015, RBS announced it had reached an agreement to sell its internationally managed Private Banking and Wealth Management business to Union Bancaire Privée UBP SA (UBP). The sale comprises client relationships outside the British Isles and associated staff. RBS will continue to service UK Private Banking and Wealth Management client needs, together with those of international clients with a strong connection to the UK, from the British Isles through its Coutts and Adam & Company brands. The transaction is subject to regulatory approvals.

The sale includes relationships managed from Switzerland, Monaco, UAE, Qatar, Singapore and Hong Kong. As at 31 December 2014 assets under management were approximately CHF32bn and total risk-weighted assets were CHF2bn. The price paid will be determined in part by assets under management on closing. RBS anticipates receiving a premium. The resulting capital benefit to RBS is expected to be modest after writing off goodwill related to the business and taking into account anticipated exit and restructuring costs. Initial closing of the transaction is envisaged in Q4 2015, when a majority of the business is expected to transfer, with the remainder during the first part of 2016.

The transaction is subject to regulatory approvals.

Executive change

On 30 March 2015 RBS announced that Rory Cullinan, Executive Chairman of Corporate & Institutional Banking will be leaving the company. To ensure an effective transfer of responsibilities he will remain with the Bank until 30 April 2015.

Chris Marks, Chief Executive Officer of CIB, and Mark Bailie, Chief Executive Officer of Capital Resolution, will join the Bank’s Executive Committee as Co-CEOs of Corporate & Institutional Banking.

The above appointments are subject to regulatory approval.

Loss attributable to ordinary and B shareholders | (£3,470m) | | Operating profit on a non-statutory basis | £3,503m |

| Profit before tax | £2,643m | | Common Equity Tier 1 ratio (1) | 11.2% |

| RWAs | £356bn | | Loan:deposit ratio (2) | 95% |

Short-term wholesale funding (3) | £28bn | | Liquidity portfolio | £151bn |

Leverage ratio (4) | 4.2% | | Return on tangible equity (5) | (8.0%) |

| Cost:income ratio | 91% | | Net interest margin | 2.14% |

Cost:income ratio adjusted - on a non-statutory basis (6) | 68% | | Net interest margin on a non-statutory basis (7) | 2.23% |

| (2) | Includes disposal groups and excludes repos see page 162 |

| (3) | Excludes derivative collateral |

| (4) | Based on end-point CRR Tier 1 capital and revised 2014 Basel III leverage ratio framework |

| (5) | Tangible equity is equity attributable to ordinary and B shareholders less intangible assets |

| (6) | Excludes restructuring costs of £1,257 million and litigation and conduct costs of £2,194 million |

| (7) | Includes results of Citizens Financial Group, Inc. |

Financial results

RBS reported a loss attributable to ordinary and B shareholders of £3.5 billion, following a £4.0 billion write-down on Citizens.

Operating profit on a non-statutory basis was £3.5 billion. Significant progress was made towards building a bank that is stronger, simpler and better for both customers and shareholders.

RBS reported a loss attributable to ordinary and B shareholders of £3,470 million in 2014, compared with a loss of £8,995 million in 2013. The result included a loss from discontinued operations of £3,445 million, which reflected a £3,994 million fair value write-down in relation to the reclassification of Citizens to disposal groups, and a tax charge of £1.9 billion which included a £1.5 billion write-off of deferred tax assets.

Operating profit before tax, which excludes results from discontinued operations, was £2,643 million compared with an operating loss of £8,849 million in 2013.

Operating profit on a non-statutory basis totalled £3,503 million for 2014, compared with an operating loss of £7,500 million in 2013. This reflected improved operating results from the core domestic businesses together with significant impairment releases in Ulster Bank and RBS Capital Resolution (RCR). These results include £1,257 million of restructuring costs compared with £656 million in 2013, and £2,194 million of litigation and conduct costs compared with £3,844 million in the prior year.

UK Personal & Business Banking (UK PBB) delivered a good performance built on strong growth from a reinvigorated mortgage business. Commercial Banking’s efforts to stimulate demand resulted in a resumption of loan book growth; together with active management of cost and capital, this supported a significant improvement in profitability. Corporate & Institutional Banking (CIB) made good progress towards a lower risk model with a further £40 billion reduction in risk-weighted assets (RWAs) on an end- point CRR basis.

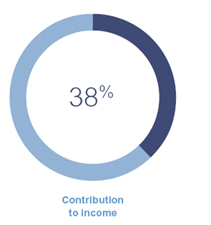

Personal & Business Banking - Share of non-statutory operating profit, 59%

| | 2014 | | 2013 |

| Performance highlights | UK PBB | Ulster Bank | PBB | | UK PBB | Ulster Bank | PBB |

| Return on equity (%) | 19.4 | 16.1 | 17.5 | | 9.8 | (33.2) | (5.7) |

| Net interest margin (%) | 3.68 | 2.27 | 3.42 | | 3.56 | 1.88 | 3.21 |

| Cost:income ratio (%) | 72 | 71 | 71 | | 77 | 81 | 78 |

| Loan:deposit ratio (%) | 86 | 107 | 88 | | 86 | 120 | 91 |

| Risk-weighted assets (£bn) | 42.8 | 23.8 | 66.6 | | 51.2 | 30.7 | 81.9 |

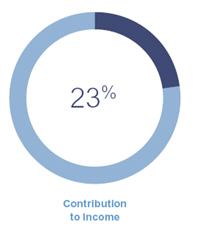

Commercial & Private Banking - Share of non-statutory operating profit, 41%

| | 2014 | | 2013 |

| Performance highlights | Commercial Banking | Private Banking | CPB | | Commercial Banking | Private Banking | CPB |

| Return on equity (%) | 12.6 | 7.8 | 11.9 | | 4.9 | (3.1) | 3.7 |

| Net interest margin (%) | 2.74 | 3.71 | 2.93 | | 2.64 | 3.74 | 2.81 |

| Cost:income ratio (%) | 57 | 87 | 65 | | 63 | 122 | 73 |

| Loan:deposit ratio (%) | 98 | 46 | 83 | | 92 | 45 | 78 |

| Risk-weighted assets (£bn) | 64 | 11.5 | 75.5 | | 65.8 | 12 | 77.8 |

Corporate & Institutional Banking - Share of non-statutory operating profit, (25%)

| Performance highlights | | | 2014 | | | | 2013 |

| Return on equity (%) | | | (4.2) | | | | (12.9) |

| Cost:income ratio (%) | | | 123 | | | | 144 |

| Risk-weighted assets (£bn) | | | 107.1 | | | | 120.4 |

Note: RWAs at 31 December 2013 are on Basel 2.5 basis and on an end-point CRR basis at 31 December 2014.

2014 was a year of significant progress for the bank, in which we delivered against all our commitments. In line with the new strategy it set out in 2014, RBS has:

| · | Implemented a new organisational design for a more UK-centred bank with focused international capabilities, built around its strongest customer franchises. |

| · | Exceeded its 2014 cost reduction targets with savings of £1.1 billion. |

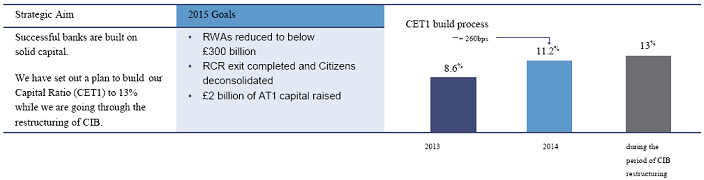

| · | Strengthened its Common Equity Tier 1 (CET1) ratio by 2.6 percentage points to 11.2% at the end of 2014, assisted by £4.8 billion of net capital release from RCR disposals and run-off. |

| · | Successfully listed Citizens as a step towards full divestment by the end of 2016. |

| · | Reached agreement with HM Treasury on the restructuring of the Dividend Access Share (DAS) and paid an initial dividend of £320 million. |

| · | Completed much of the orderly run-down and closure of the US asset-backed product business, removing £15 billion of RWAs from the balance sheet. |

| · | Completed a strategic review of Ulster Bank and the wealth businesses, launching a sales process for the international private banking activities(1). |

| · | Continued to rationalise, simplify and strengthen operating systems and processes, with a more secure mobile banking platform, faster overnight batch processing and key services available to customers 99.96% of the time. |

| · | Made our products simpler and fairer for customers, ending zero per cent balance transfers, halting teaser rates on savings accounts that penalise existing customers and explaining all charges for personal and business customers on one side of A4 paper. |

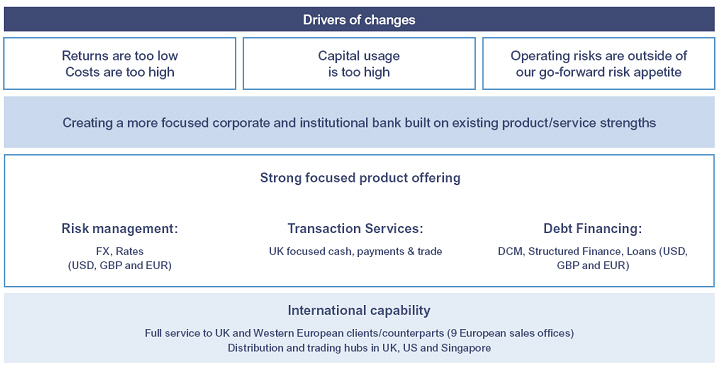

Within the overall strategic shape outlined for CIB in 2014, RBS is making further changes to improve its medium-term returns, building a stronger, safer and more sustainable business, focused mainly on UK and Western European customers, both corporates and financial institutions, supported by trading and distribution platforms in the UK, US and Singapore.

These changes will create a more focused corporate and institutional bank built on existing product and service strengths.

RBS will have a strong, client-focused product offering in sterling, US dollar and euro, including:

| · | Debt financing, with debt capital markets, structured finance and loans. |

| · | Risk management in currency, rates and inflation. |

| · | Transaction services, with UK-focused cash, payments and trade. |

| (1) | Private banking and wealth management activities where the primary relationship management is conducted outside the British Isles. |

CIB will reduce its geographical footprint to approximately 13 countries, compared with 38 at the end of 2014, though RBS will also retain its back office operations in Poland and India. In addition to its main distribution and trading hubs in the UK, US and Singapore, RBS will remain present in a number of Western European countries with coverage teams. A small sales team will be retained in Japan. US operations will shrink, while retaining the presence required to support the US dollar needs of RBS’s UK and Western European customers. Priority client sectors will be targeted in infrastructure, transportation, financial institutions, energy and resources.

CIB will continue to reduce its balance sheet and risk profile. RWAs will be reduced by 60% from £107 billion at 31 December 2014 to £35-£40 billion in 2019, with a reduction of more than £25 billion targeted in 2015. Third party assets will be reduced from £241 billion at the end of 2014 to £75- £80 billion in 2019.

This CIB strategy leaves RBS well-placed to meet the ring-fencing requirements of the Banking Reform Act 2013. As previously indicated, RBS intends to place most banking services inside the ring fence. CIB’s remaining “Markets” activities, the operations of RBS International and some corporate banking activity are expected to remain outside the ring-fenced bank in separate legal entities.

For 2015 RBS intends to:

| · | Move towards a capital target of 13% CET1(1), with risk-weighted assets below £300 billion and £2 billion Additional Tier 1 capital raised. |

| · | Deconsolidate Citizens and substantially complete RCR exit. |

| · | Improve customer net promoter scores in all UK franchises, in line with the long-term goal of becoming the number 1 bank for trust, service and advocacy. |

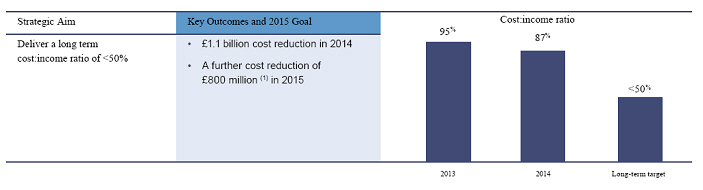

| · | Reduce costs by a further £800 million(2), taking RBS towards a long term cost:income ratio of under 50%. |

| · | Deliver lending growth in strategic segments equal to or higher than UK nominal GDP growth. |

| · | Raise employee engagement index to within 8% of the global benchmark so that staff are fully motivated to contribute to RBS’s long-term success. |

2014 performance

| · | Loss attributable to ordinary and B shareholders was £3,470 million, compared with a loss of £8,995 million in 2013. The result included a loss from discontinued operations net of tax of £3,445 million, which reflected an accounting write-down of £3,994 million taken in relation to Citizens, which has been written down to fair value less costs to sell as a consequence of it being reclassified as ‘held-for-sale’ in the statutory results. This write-down does not affect RBS’s capital position. |

| · | The tax charge included a net write-off of deferred tax assets of £1.5 billion relating to the UK (£850 million) and the US (£775 million), reflecting the impact of the decision to scale back the CIB operations. This was partially offset by write-backs relating to Ulster Bank. |

| · | Operating profit before tax was £2,643 million compared with an operating loss before tax of £8,849 million in 2013. Operating profit on a non-statutory basis improved to £3,503 million for 2014 compared with an operating loss of £7,500 million in 2013. Operating profit before tax benefitted from improved operating results in core businesses together with significant impairment releases in Ulster Bank and RCR. |

| · | Restructuring costs of £1,257 million (2013 - £656 million) were up 92% but conduct and litigation costs were 43% lower at £2,194 million (2013 - £3,844 million) and included charges relating to foreign exchange trading, Payment Protection Insurance (PPI), customer redress associated with interest rate hedging products, IT incident in 2012 and other costs including packaged accounts and investment products. Excluding restructuring, conduct and litigation costs, operating profit on a non-statutory basis was 6,954 million, compared with a loss of £3,000 million in 2013. |

| · | Total income was £15,150 million compared with £16,737 million in 2013. On a non-statutory basis total income totalled £18,197 million, down 6% from 2013. Improvements in net interest income in PBB and CPB were offset by lower income from trading activities in CIB, in line with its smaller balance sheet and reduced risk profile. Net interest margin on a statutory basis was 2.14%, up from 1.90% in 2013, with improved liability margins partially offset by pressure on mortgage and corporate lending margins and by the continuing shift in mix towards lower margin secured lending. |

| · | Operating expenses were £13,859 million compared with £17,466 million. On a non-statutory basis operating expenses of £15,849 million compared with £18,510 million, excluding restructuring, of £1,257 million (2013 - £656 million), conduct and litigation costs of £2,194 million (2013 - £3,844 million) , were down £1,612 million or 12%. Adjusting for currency movements of £0.3 billion and intangible assets write-offs of £0.2 billion, cost savings totalled £1.1 billion, in excess of the bank’s £1 billion target for the year. |

| · | Impairment releases of £1,352 million were recorded in 2014 compared with impairment losses of £8,120 million in 2013. On a non-statutory basis net impairment releases of £1,155 million were recorded in 2014 compared with impairment losses of £8,432 million in 2013, which included £4,490 million of charges recognised in connection with the creation of RCR. Provision releases arose principally in Ulster Bank and in the Irish portfolios managed by RCR, which benefited from improving Irish economic and property market conditions nd proactive debt management. |

Balance sheet and capital

| · | Funded assets which exclude derivatives of £354 billion (Q3 2014 - £314 billion, 2013 - £288 billion) totalled £697 billion at 31 December 2014, down £35 billion in the last quarter and £43 billion over the course of the year, principally reflecting continued risk and balance sheet reduction in CIB and disposals and run-off in RCR. |

| · | Net loans and advances to customers totalled £334 billion, down £57 billions from the end of 2013 which included balances relating to Citizens of £60 billion transferred to assets of disposal groups. Underlying net loans and advances to customers were up £3.0 billion from the end of 2013, despite a significant reduction in RCR. |

| | ° | UK PBB lending rose by £2 billion, with net new mortgage lending of £3.9 billion partially offset by reduced unsecured balances. |

| | ° | Commercial Banking balances rose by £1 billion, with a planned reduction in real estate finance offset by good growth in lending to other sectors. |

| | ° | Gross new lending to SMEs totalled £10.3 billion, exceeding RBS’s £9.3 billion target by 10%. |

| | ° | Total net lending flows reported within the scope of the Funding for Lending Scheme were minus £2.28 billion in Q4 2014, of which net lending to SMEs was minus £567 million. |

| · | Customer deposits totalled £354 billion at the end of 2014. Customer deposits including Citizens of £61 billion,, which has been reclassified to disposal groups, totalled £415 billion at the end of 2014, up £0.4 billion from the end of 2013. |

| · | RWAs declined to £356 billion from £429 billion at the end of 2013, primarily driven by risk and balance sheet reduction in CIB coupled with disposals and run-off in RCR. This contributed to the strengthening of the bank’s capital ratios, with the CET1 ratio strengthening by 260 basis points to 11.2% at the end of 2014 compared with 8.6% at the end of 2013. |

Our progress in 2014

We have a clear ambition to become No.1 for customer service, trust and advocacy. In 2014, our focus has been on Cost, Capital, Restructuring and Resilience. We have also begun the process of making RBS a simpler place to work and an easier bank to do business with.

Fairer banking

We’ve ended Credit Card teaser rates.

Account opening

We’ve reduced our current account opening times

for RBS and NatWest customers from

five days to one.

Launch of Citizens IPO

The biggest bank initial public offering in US history successfully delivered.

GPL system redesign

We simplified our Group Policy Learning system (GPL). As

a result we’ve seen a 62% reduction in the total hours required to complete modules, letting us spend more time

on customers.

SME funding

Gross new lending to SMEs totalled £10.3 billion, exceeding our 2014 target by 10%.

Simplified product range

Personal & Business Banking reduced the number of on sale products by 50%.

Project reduction

So far, we have reduced the number of change projects we are running

from 550 to 182.

Transparency

RBS scored top for corporate transparency in a study conducted by

Transparency International.

Small Business Fund

RBS and NatWest launch £1billion fund for both new and existing small business customers across the UK.

Online loans

We launched a new online loan application process for small businesses.

Faster processing

Our overnight batch processing is now twice as fast, processing 20 million transactions every day.

Resilience

We’ve created a mirror bank so customers still have access to our services during a system outage. Already we can process 90% of debit and credit card transactions if there is a system outage.

Mobile record

Our mobile app regularly supports around 4 million logins a day, with a record being set on ‘Black Friday’ 2014 of 4.86 million.

Living Our Values

We launched a recognition programme – Living Our Values, reducing over 200 local schemes into one and creating a bank-wide way of recognising a colleague.

Our 2015 targets

Capital target

Move towards a capital target of 13% CET1 ratio (1).

Improve NPS

Improve net promoter score in every UK franchise.

Reduce costs

Reduce costs by a further £800 million (2), taking RBS towards a long term cost:income ratio of under 50%.

Lending growth

Deliver lending growth in strategic segments equal to or higher than UK nominal GDP growth.

Our people

Raise employee engagement index to within 8% of GFS norm (3)

| (1) | During the period of CIB restructuring. |

| (2) | Excludes restructuring, conduct, litigation and intangible write-off charges as well as the operating costs of Citizens Financial Group and Williams & Glyn. |

| (3) | Global Financial Services (GFS) norm currently stands at 83%. |

2014 was a year of significant progress for RBS, with a much improved operating profit and major achievements in terms of business reorganisation, cost reduction, capital build and improved IT capability. As Ross McEwan has set out in his letter, the business continues to simplify and improve, focusing on putting its customers at the heart of its activities

The bank has delivered a good operating profit of £3.5 billion (1) for 2014, but the costs associated with completing the restructuring of RBS mean we are still reporting a bottom line attributable loss. Although the huge changes to the size, shape and risk profile of the business since the financial crisis are largely complete or in hand, the further substantial restructuring of our markets operations and international spread will require careful management in 2015.

Of course your Board is pleased to see the improved operating performance, which in our view reflects the underlying strength of the business. Looking back, however, we must acknowledge that we did not fully recognise the scale of the challenge that awaited us in 2009. At the time, we assumed that a Core Tier 1 capital ratio of more than 8% by 2013 would be sufficient to constitute undoubted financial strength in the minds of markets and regulators; today we have increased our capital target to 13%. We must also acknowledge that we did not anticipate the more than £9 billion of regulatory fines and customer redress we have borne so far as we paid, and will continue to pay, the price for our past conduct failings. These conduct issues have delayed the re-build of our capital and directly reduced shareholder value. They have also caused continuing reputational damage. I hope as we move beyond these issues we can fully rebuild the trust of our customers, and by doing so win more of their business.

The need to continue to rebuild capital strength means it has taken longer than we had expected to reach a point at which the Government could be in a position to start selling down its stake in RBS. The decision on timing rests with the Government, through UK Financial Investments, which manages its shareholding, but our task is to create the conditions in which it can do so. In working towards that end we are also furthering the interests of RBS’s other shareholders, as we believe that the beginning of the sell-down will be welcomed by investors.

As announced previously I will be leaving RBS in 2015. The Board is pleased to announce that Howard Davies will succeed me as Chairman, and we welcome him to RBS. He will join the Board at the end of June and take over from me on 1 September. On the day I joined the Board in January 2009, the shares traded at 9p, equivalent to 90p today, and the implications of the bank’s financial distress were unknowable. RBS has transformed itself over the last several years and continues to do so. The renewed focus on customer and customer service will make this a better organisation for all stakeholders, most especially customers, staff and shareholders.

I would like to thank my colleagues on the RBS Board for their support and dedication in dealing with the unusual challenges of being a majority government-owned listed company.

In particular, I would like to thank Nathan Bostock, Tony Di Iorio and Philip Scott, who all stepped down from the Board in 2014 after providing valuable service, and to welcome Morten Friis and Ewen Stevenson, who have joined the Board.

It has been a privilege to serve as Chairman of RBS and I am confident that the Board and the many outstanding people in the bank will continue to work with dedication to restore the bank’s standing.

Philip Hampton

Chairman

| (1) | On a non-statutory basis |

This is my first letter to you since we launched a new strategy for RBS last year. It is a strategy that sets out to deliver one very simple aim. To make this a great bank for our customers; a bank that will earn back their trust, and in turn win more of their business.

It’s a strategy that provides the fundamental building blocks to make RBS an attractive investment, a great place to work for our people, and a UK focused bank that the country can be proud of.

Last year we identified the areas we needed to improve in order to deliver our strategy - cost, complexity, capital, and trust from our customers. The energy and resolve of our people has resulted in significant progress on these, and we have delivered on the goals we set for 2014.

| · | We said we would reduce waste and inefficiency and reorganise ourselves around the needs of our customers, moving from seven operating divisions to three customer businesses. This reorganisation is complete and we have removed £1.1 billion of cost from the business. |

| · | We outlined a programme to rationalise, simplify and bolster our operating systems and processes to make them less complex, more resilient and easier to use. Significant progress has been made in this area with our key services available to customers 99.96% of the time during 2014. |

| · | We set out a plan to place the bank on a sure capital footing targeting a CET1 ratio of 11% by the end of 2015, and 12% or greater by the end of 2016, so as to remove any doubts about our fundamental strength and stability. This capital plan is on track and we have reached our 2015 target one year ahead of schedule. This improvement was driven by a 52% reduction in risk- weighted assets in RCR. |

| · | We said we would undertake the biggest bank initial public offering in US history. Citizens Financial Group was successfully floated on the New York Stock Exchange. At the same time we substantially completed the orderly run-down and closure of our US asset-backed product business, removing £15 billion of risk- weighted assets from our balance sheet. |

| · | We made a commitment to fairness with our customers. We said that RBS would no longer compete with other banks in a number of areas and we would use less technical language that our customers find easier to understand. We stopped offering zero per cent balance transfers on credit cards that trap customers in spirals of ever increasing debt, we ended teaser rates that penalise existing customers, and we now explain all of our fees and charges on one side of A4 paper for both our personal and business customer |

As well as being a stronger, simpler and fairer bank, I said that we would also be a very different bank. No longer chasing global market share, but instead focusing squarely on our core strength, namely our home market places in the UK and the Republic of Ireland (RoI).

Our 2014 performance shows a strategy that is working. It demonstrates the forensic approach we have taken to evaluate our businesses against the returns they provide to shareholders. The strong execution against the targets we set now gives us a platform to go further, faster.

As well as a review of our current performance I will set out exactly what this bank will become, what we will do and what we will not do as we seek to improve shareholder value and secure our market leading positions. It involves an acceleration of our strategy to build on our domestic strengths and a further reshaping of our CIB business as we seek to address its unacceptable returns.

We have five ambitious new goals for the second year of our plan and new financial targets so that you, our shareholders, can hold us to account for our performance.

2014 financial performance

The earning power of our key customer businesses lies at the heart of the strong financial progress RBS made during 2014. What you can see from these results is that underneath all the noise of conduct, litigation and restructuring charges, we have strong performing customer businesses that are geared towards delivering sustainable returns for investors.

We made an operating profit of £3.5 billion(1) in 2014, the highest since 2010 and a vast improvement on 2013. Great progress on cost reduction countered a fall in total income - which primarily reflected a smaller risk profile and lower income from trading activities in CIB - and led to an overall improvement in operating efficiency.

Our attributable loss of £3.5 billion(2), includes £1.3 billion of restructuring charges, £2.2 billion in litigation and conduct provisions, a £1.5 billion net deferred tax asset write-off, the initial £320 million dividend for the Dividend Access Share and a write-down of £4 billion anticipating the disposal of Citizens.

| (1) | On a non-statutory basis |

| (2) | Loss attributable to ordinary and B shareholders |

It is increasingly clear what is driving underlying performance at RBS - PBB and CPB. PBB and CPB are now more important to RBS’s performance than at any time in the past decade. This year they generated 61% of our income, compared with c.37% for equivalent businesses in 2009. And they have been at the forefront of progress towards our goal of increased operating efficiency, reducing adjusted operating expense(3) by 2.6% over the year whilst income was up 2.3%. ROEs of 17.5% and 11.9% respectively demonstrate their value to RBS today.

These franchises are also the custodians of our core strengths - serving the everyday banking needs of over 18 million personal and business customers in the UK and RoI, and helping these customers meet their ambitions. We’re investing in these franchises with a view to exceeding customers’ expectations and generating sustainable returns.

The performance of CIB reflects the big changes this business is going through, and the tough macro-economic conditions and increasingly high costs of regulation it faces. Income decreased alongside lower adjusted operating expenses as we reduced CIB’s risk profile in accordance with our strategy, with restructuring, litigation and conduct costs pushing the business to an operating loss. But CIB has a strong customer franchise serving our leading UK and Western European clients; increasingly it is these clients we intend to focus on. I will set out later in this letter the steps we will take to do this.

An overarching part of delivering sustainable returns is controlling operating costs. When I announced our cost target last year it was described by some as the most ambitious cost target in Europe. Well, through our drive across the bank for greater simplicity we have over-delivered, and surpassed our target of £1 billion of operating cost savings for the bank. With a cost:income ratio for the year of 68% on an adjusted basis(3) , we are still behind our peers on cost efficiency; and there is work to do to fulfil our desire to take it below 50%. But we have a strong track record on delivery, and there is resolve across this bank to get this done.

I am very pleased with the progress we have made in 2014 against our stated objectives. While that progress is evident in the operating profit line of the results announced we are still posting an attributable loss to our shareholders. This is an accounting consequence of one of our 2014 achievements - the successful flotation of Citizens on the New York Stock Exchange.

Now the deconsolidation of Citizens is finally within sight, accounting rules require us to write it down to its estimated disposal value. This write-down substantially represents the goodwill previously attached to Citizens. While I realise that the headlines this generates are disappointing it is important to emphasise that this particular accounting loss does not change our regulatory capital or tangible net asset value.

Safety remains a cornerstone of our strategy

A core question for any bank seeking the trust of its customers is whether it’s safe and strong and focused and able to support customers and the economy. The progress we have made should mean that it is no longer in any doubt. The CET1 ratio has improved by 260 basis points to 11.2% over the course of the year, up from 8.6% as at 31 December 2013. We reached our full year 2015 CET1 target of 11% one year ahead of schedule, and we are on track to achieve a revised CET1 target of 13%, which we have set in place for the period of the CIB restructuring.

We now have considerably more high quality capital than we had when the financial crisis hit and this bank was bailed out by the taxpayer. But we need to meet and exceed the expectations of the Prudential Regulation Authority (PRA) and of our shareholders and bondholders. Stress test results show it’s not just how much capital you have, but how your balance sheet behaves under extreme economic scenarios.

This year our team in RBS Capital Resolution has managed to accelerate the removal of some of our most capital intensive assets, and we are on track to complete our 2014- 2016 RCR run-down targets by the end of 2015, one year ahead of the original target we set for ourselves. Our capital strength will be bolstered further when Citizens Financial Group in the USA is deconsolidated from our balance sheet. This is also expected in 2015.

In 2015, we also plan to start a programme of issuing Basel III compliant Additional Tier 1 capital instruments.

Conduct

It has taken far longer than anyone realised to root out all the past problems, practices and related fines, and we still have challenges on the horizon. We are changing the culture of this bank; our aim is that shareholders are not exposed to this scale of conduct risk again.

What you will have seen from me over the last year is the way I will be open and honest with you and our customers when dealing with these issues; the way we continue to approach FX is a good example of this. I will not hide. I will talk openly about the hurt this wrongdoing causes me and the many thousands of people within this bank. I will detail the things we are doing to put things right for our customers, and the challenge and change we are driving through the culture and conduct of our staff.

We are determined to learn the lessons from the wrongdoings of the past and ensure that those responsible are held to account.

Notes:

| (3) | Excluding restructuring costs and litigation and conduct costs, see segmental analysis in Note 38 |

Building on our strengths

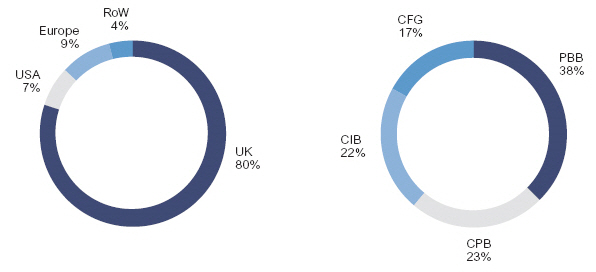

I said this time last year that the days when global domination mattered more to RBS than great customer service are well and truly over. Well, we are not just talking about being a UK-centred bank; we are a UK-centred bank. 80% of our revenues are generated in the UK. At the time of the 2008 financial crisis this number was 48%. Seven years after the crisis we still have top 3 market positions in the following UK segments:

| · | large corporates and financial institutions (FIs); |

| · | Sterling provider in wholesale banking; |

| · | Financing for UK infrastructure projects; and |

We are building on this strength to manage value for shareholders and deliver the most resilient future returns.

In last year’s letter, I told you that where a business can’t deliver value to our shareholders in a reasonable time period we will take decisive action. We have put international private banking activities(1) up for sale and we are now going further, faster in reshaping parts of our CIB business.

The investment bank was over-stretched both in range of product and geography. There was too much risk for too little return. Given the increasing regulatory requirements on this business, it was a strategy that now has little hope of delivering acceptable returns to shareholders.

To be a number 1 bank means providing a full service offering to UK and Western European corporate and financial institution clients. It means providing a first class platform to process payments in the UK and Europe. And it means having the expertise to help customers raise finance on the debt capital markets and manage the high level risks they face. Serving customers in these areas is an undisputed area of strength for us - they are our core capabilities, and are essential to us providing a first class service. In addition, trading and distribution hubs in Singapore and the US will ensure the corridors of commerce remain open to allow our customers access to investors in those regions.

We plan to fully exit our Markets businesses in Central and Eastern Europe, the Middle East and Africa, and substantially reduce our presence in Asia Pacific and the US. We will exit our cash management services outside the UK and RoI. These businesses are not essential to our go-forward client franchise, and their standalone returns are not sufficient to justify an exception.

In doing so we will be free to grow and improve the services our customers value most. And by serving customers better this franchise can reinforce its competitive position and deliver sustainable returns above the cost of equity for our shareholders.

This is a plan for a smaller, more focused, but ultimately more valuable bank with the vast majority of its assets in the UK, and for RBS marks the end of the standalone global investment bank model.

What I have just outlined will require an enormous amount of effort from our people. And I do not for one second take that for granted. We have a proven track record of delivering change in our business.

A better bank for customers

Much has been written and discussed about the root causes of the financial crisis. For me it came down to one big problem - a failure to put the customers’ interest at the heart of our business and its culture. For too long market share mattered more than customer care.

It is why over the last year our people have worked hard to embed this ‘customer first’ mentality into everything we do as a bank.

There are some concrete achievements we can call out for 2014 including: faster account opening times, a simplified product range and a clearer pricing structure. And we went against the rest of the industry and took a calculated risk by ending teaser rates, and we now offer our best rates to new and existing customers across our product range. We may have lost customers and income as a result, but we still believe that this was the right thing to do and will deliver long term value for shareholders.

I want to assure our customers that the positive changes we made in 2014 are not one-off. We strive to do better for our customers every day, and when we spot an opportunity to serve customers better, we will act. For example, customers shouldn’t be penalised because they lose track of the date and are hit with an unexpected overdraft charge for the first time. And if we can do more to help customers through both the ups and downs in their finances, it is absolutely our responsibility to do so.

But we recognise that these are chipping away at the edges, and more radical change is needed if we are to establish real upward momentum and achieve our targets. We have to be constantly asking ourselves what a really good bank for customers would look like, and to be constantly improving what we do to take us towards that goal. In our financial reporting we will include full details of the progress we have made as well as providing clear, independent measures of the bank’s customer trust and advocacy scores.

We may have started from further back than some, but we are determined to reach our aspiration of being number 1 for customer service, trust and advocacy. It won’t be easy, but I firmly believe it is doable.

A better bank for shareholders

Critical though it is that we build a bank that is safe, in capital strength, in structure and on behaviour, it must also be profitable.

There are good businesses within RBS that are capable of delivering real value to their customers. If we do that, our customers will be happy for us to make a fair and sustainable profit.

Without sustainable profitability we cannot ensure our future safety; profit is the best form of self-replenishing capital.

We remain acutely conscious of how much was invested to ensure our continued survival by our private shareholders and, critically, by the Government. As we reduce the tail risks our bank is exposed to, repair our overall profitability and reshape CIB we are creating the potential to build up excess capital, paving the way for distributions to the Government and other shareholders.

| (1) | Private banking and wealth management activities where the primary relationship management is conducted outside the British Isles. |

Our strategy envisages a capital benefit net of restructuring costs from 2016. We intend to return all capital to shareholders above a CET1 ratio of 13%. This capital return, which remains subject to regulatory approval at the time, will only be made once the significant legacy conduct hurdles are behind us. We see this as another important step towards repaying the support of our shareholders, including the UK tax payer.

2015 Goals and revised targets

I have set out in the table below five new ambitious business goals for the second year of our strategic plan to simplify and restructure this bank, achieving them will stand us in good stead to reach our goals. We have also published a revised set of financial and business targets. These are consistent with the other changes set out in this letter, and will enable you, our shareholders, to continue to track our progress and hold us to account.

By 2019 RBS intends to be a low cost business focused on effective, efficient delivery for our customers. It will be a bank based in the UK and RoI, with a presence in Western Europe, the US and Singapore. It intends to be a bank with leading market positions in each of our chosen business areas, and a bank that can generate attractive returns for shareholders on a sustainable basis.

Conclusion

I would like to take this opportunity to thank our Chairman, Sir Philip Hampton, as he takes part in his final Annual Results with the bank. Philip joined in 2009 amid the global financial crisis and immediately brought a clear sense of purpose and direction for the bank at a time of incredible uncertainty, both for the UK and RBS. His dedication to making this a great bank for the country served him well through the tremendous, but positive, change that RBS has undergone during his tenure. I want to express my personal gratitude to Philip for guiding me during my first year as CEO, and playing a key role in implementing the strategy that will take us forward. There is still work to do, but Philip will leave on a positive note, with RBS firmly focussed on serving its customers, and shareholders.

What you see today is a bank on track and delivering on its plan. A bank that is determined to earn the trust of its customers every day. A bank that helps the smallest enterprises through to the largest companies grow and prosper. A bank that is determined to reward its shareholders for their support. And a bank that is able to deliver on our ambition to be number one for customer service and advocacy in the UK and RoI.

Ross McEwan

Chief Executive

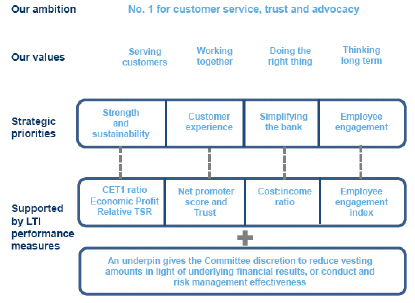

| | Our long-term targets | Our 2015 goals |

| Strength and sustainability | CET1 ratio = 13% during the period of CIB restructuring | Reduce RWAs to <£300bn |

| Customer experience | No.1 for service, trust and advocacy | Improve NPS in every UK franchise |

| Simplifying the bank | Cost:income ratio <50% | Reduce costs by £800m(1) |

| Supporting growth | Leading market positions in every franchise | Lending growth in strategic segments ³ nominal UK GDP growth |

| Employee engagement | Employee engagement index ³ GFS norm(2) | Raise employee engagement index to within 8% of GFS norm(2) |

| (1) | Excludes restructuring, conduct and litigation costs, intangible write-off charges as well as the operating costs of Citizens Financial Group and Williams & Glyn. |

| (2) | Global Financial Services (GFS) norm currently stands at 83%. |

Business model and strategy

Business model and strategy

Our major source of income in our retail and commercial banking businesses is net interest income. This is the difference between the income we earn from the loans and advances we have made to our personal, corporate and institutional customers and on our surplus funds and the interest we pay on deposits placed with us by our customers and our debt securities we have issued. We also earn fees from financial services and other products we provide to our customers as well as rental income from assets we lease to our customers.

Our Corporate & Institutional Banking business earns income from client driven trading activities particularly Rates, Currencies and Credit.

We do business in competitive markets but we have strong franchises and good growth opportunities, and we aim to target our investment to maximise these opportunities.

Our Personal & Business Banking and Commercial & Private Banking franchises provide services to over 17 million personal and business customers in the UK and to over 1 million personal and business customers in the Republic of Ireland. Our Corporate & Institutional Banking business serves our corporate and institutional clients primarily in the UK and Western Europe, as well as those US and Asian multinationals with substantial trade and investment links in the region. This business’s strategy has been further refined in 2015 (see page 15 for Reshaping our CIB business).

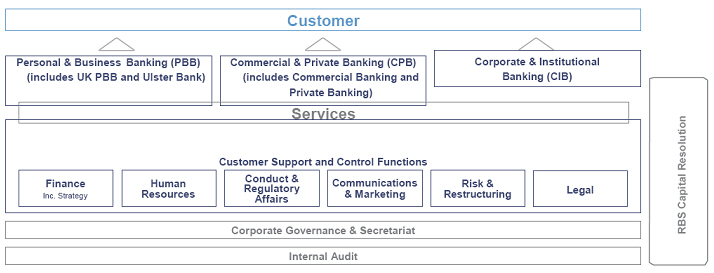

Our Structure

We are organised to provide products and services to personal, commercial and large corporate and institutional customers. Our principal customer-facing businesses are supported by a central Services function and other Support and Control Functions.

Customer Businesses

Our three customer-facing businesses are primarily responsible for defining the strategy and financial plan of their business and ensuring it is aligned with the wider RBS strategy. Teams define and deliver the customer proposition and are accountable for end-to-end customer processes and products. The teams partner with functions to specify functional requirements that deliver on customer needs.

Services

Services, led by the Chief Administrative Officer, provides business aligned technology, operations and property services across the bank. It is also accountable for technology risk, payments, data, change and the bank’s fraud and security functions.

Functions

These teams define functional strategy and the financial plan to support the Customer Businesses and other functions.

Most functions are a mix of control, expertise, advisory and transaction services. All common activities across the organisation are included and nothing else.

Business model and strategy

Our Strategy

After five years spent restoring fundamental soundness to the bank, we have created a strategy and a structure that provides us with an exciting opportunity. Over the next few years, we are going to focus all of our energy on earning back the trust we lost in 2008. And in doing so, RBS is going to change the UK banking sector for the better.

Our Priorities

We have a long way to go to be the bank that our customers deserve. But we are in a period of very significant, positive change. We have millions of great customers, tens of thousands of outstanding employees, and a home economy that is getting stronger. By building on this foundation, we can achieve our ambition to be number one for customer service, trust and advocacy in all our chosen markets.

Our Plan

Our overarching ambition is to become the number one bank for customer service, trust and advocacy. We have set out how we track our progress towards this goal on page 16.

We also track a number of other performance measures and have set long-term targets for these to keep us on track.

Business model and strategy

Reshaping our CIB business

We have announced our plans to go further and faster in reshaping parts of our CIB business. The investment bank was overstretched both in range of product and geography. We are building a stronger, safer and more sustainable business, focused mainly on UK and Western European customers, both corporates and financial institutions, supported by trading and distribution platforms in the UK, US and Singapore.

Our go-forward business is focused predominantly on UK and EMEA. Based on 2014 numbers, around 74% of CIB’s RWAs and 81% of income(4) is generated in these regions.