UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of The Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under Rule 14a-12 |

THE CHINA FUND, INC. |

(Name of Registrant as Specified in Its Charter) |

| |

CITY OF LONDON INVESTMENT GROUP PLC CITY OF LONDON INVESTMENT MANAGEMENT COMPANY LIMITED BARRY M. OLLIFF JULIAN REID RICHARD A. SILVER |

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| ☐ | Fee paid previously with preliminary materials: |

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

City of London Investment Management Company Limited, together with the other participants named herein (collectively, “City of London”), has filed a definitive proxy statement and accompanyingBLUE proxy card with the Securities and Exchange Commission to be used to solicit votes for the election of a slate of director nominees and certain business proposals at the upcoming 2018 annual meeting of stockholders of The China Fund, Inc., a Maryland corporation (the “Company”).

Please contact Saratoga Proxy Consulting LLC, which is assisting us, if you have any questions, require assistance in voting yourBLUE proxy card, or need additional copies of our proxy materials. Saratoga can be reached toll-free at (888) 368-0379.

City of London issued the following investor presentation:

CITY OF LONDON Investment Management Company Limited Additional Materials for ISS 0

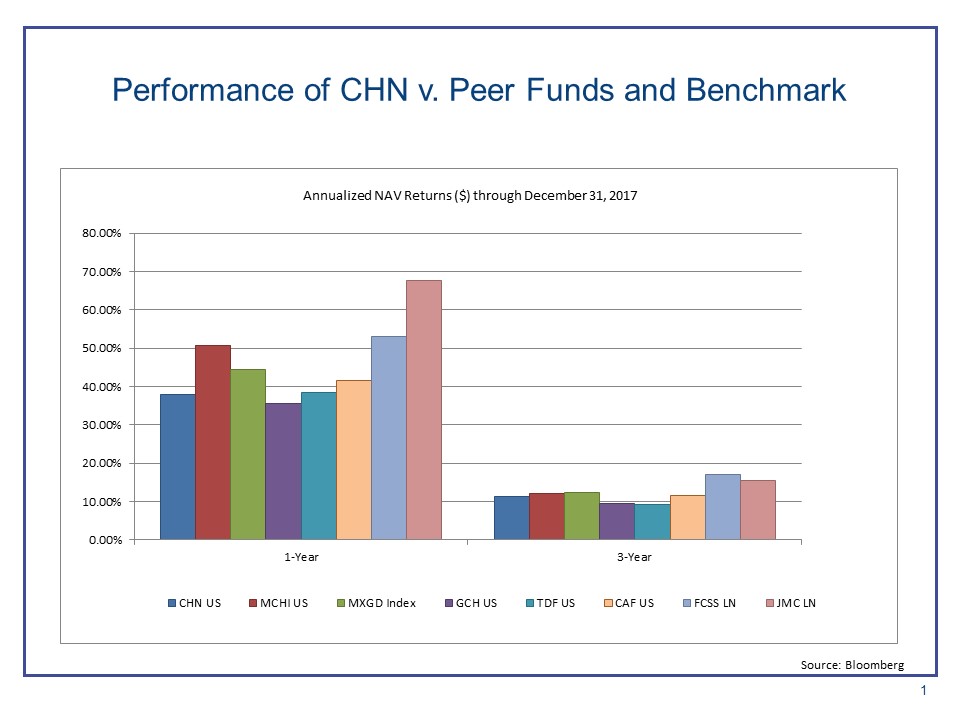

Performance of CHN v. Peer Funds and Benchmark 1 Source: Bloomberg 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00% 80.00% 1-Year 3-Year CHN US MCHI US MXGD Index GCH US TDF US CAF US FCSS LN JMC LN Annualized NAV Returns ($) through December 31, 2017

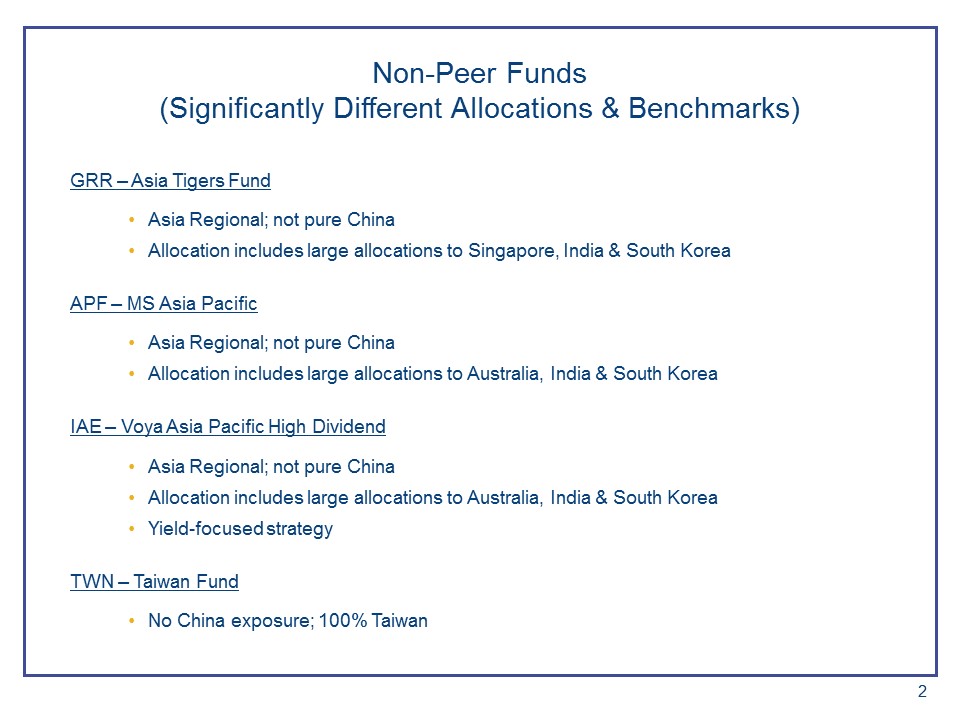

Non - Peer Funds (Significantly Different Allocations & Benchmarks) GRR – Asia Tigers Fund • Asia Regional; not pure China • Allocation includes large allocations to Singapore, India & South Korea APF – MS Asia Pacific • Asia Regional; not pure China • Allocation includes large allocations to Australia, India & South Korea IAE – Voya Asia Pacific High Dividend • Asia Regional; not pure China • Allocation includes large allocations to Australia, India & South Korea • Yield - focused strategy TWN – Taiwan Fund • No China exposure; 100% Taiwan 2

Nominees’ Experience & Credentials » Our Nominees are highly qualified and have relevant experience in overseeing closed - end fund portfolio manager transitions » As Directors of The Korea Fund, Inc. (KF), a NYSE Listed Investment Company, in 2006 Julian Reid (Chairman) and Richard Silver instigated and oversaw the transition from Deutsche Asset Management to the current manager » The KF Board has worked with the current manager to ensure the best individuals are responsible for investment decisions on KF, and has changed portfolio managers multiple times Our Nominees are confident that the selection of a new manager could be achieved in a timely manner 3

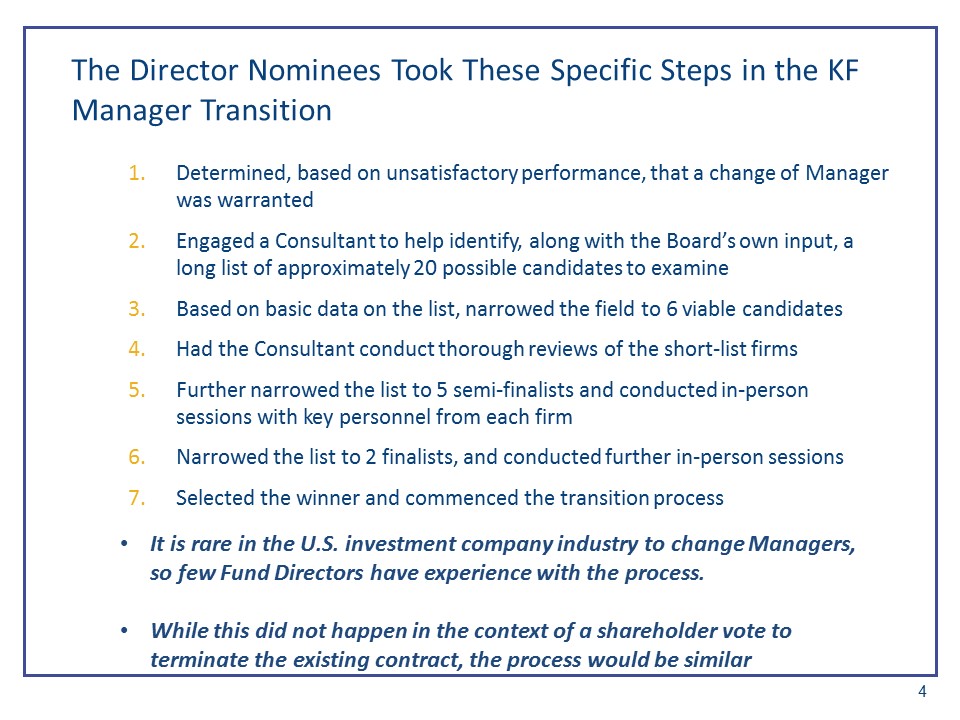

The Director Nominees Took These Specific Steps in the KF Manager Transition 1. Determined, based on unsatisfactory performance, that a change of Manager was warranted 2. Engaged a Consultant to help identify, along with the Board’s own input, a long list of approximately 20 possible candidates to examine 3. Based on basic data on the list, narrowed the field to 6 viable candidates 4. Had the Consultant conduct thorough reviews of the short - list firms 5. Further narrowed the list to 5 semi - finalists and conducted in - person sessions with key personnel from each firm 6. Narrowed the list to 2 finalists, and conducted further in - person sessions 7. Selected the winner and commenced the transition process 4 • It is rare in the U.S. investment company industry to change Managers, so few Fund Directors have experience with the process. • While this did not happen in the context of a shareholder vote to terminate the existing contract, the process would be similar

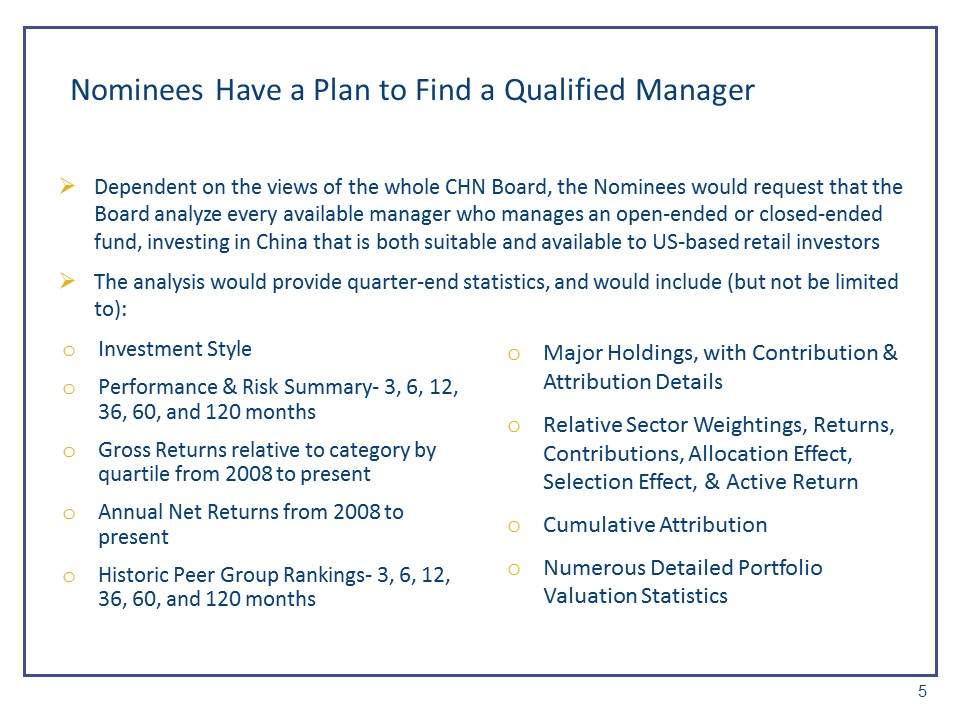

Nominees Have a Plan to Find a Qualified Manager » Dependent on the views of the whole CHN Board, the Nominees would request that the Board analyze every available manager who manages an open - ended or closed - ended fund, investing in China that is both suitable and available to US - based retail investors » The analysis would provide quarter - end statistics, and would include (but not be limited to): o Investment Style o Performance & Risk Summary - 3, 6, 12, 36, 60, and 120 months o Gross Returns relative to category by quartile from 2008 to present o Annual Net Returns from 2008 to present o Historic Peer Group Rankings - 3, 6, 12, 36, 60, and 120 months 5 o Major Holdings, with Contribution & Attribution Details o Relative Sector Weightings, Returns, Contributions, Allocation Effect, Selection Effect, & Active Return o Cumulative Attribution o Numerous Detailed Portfolio Valuation Statistics

Nominees Have a Track Record of Representing Shareholders’ Best Interests Julian Reid » Background in portfolio management » Considerable savings in legal fees at KF » Developed Board travel and expense guidelines 6 Richard Silver » Worked with regulators on the SEC Yield Rule, which provides fair and consistent advertising of yields by income - oriented funds » Worked with regulators to strengthen rules on 12b - 1 fees » As Treasurer, enacted procedures to protect shareholders As Directors, our Nominees possess expertise and have consistently worked to manage funds for the benefit of shareholders, not the Manager, as shown by the Discount Management Program at KF

IMPORTANT INFORMATION City of London Investment Management Company Limited is authorised and regulated by the Financial Conduct Authority, registered as an investment advisor with the Securities and Exchange Commission and regulated by the Dubai Financial Services Authority. This presentati on is for discussion and general informational purposes only. This presentation is not an offer to sell or the solicitation of an offer to buy interes ts in a fund or investment vehicle managed by City of London Investment Management Company Limited or any other participant in its solicitation (collect ive ly, “COL”) and is being provided to you for informational purposes only. The views expressed herein represent the opinions of COL, and are base d o n publicly available information with respect to The China Fund, Inc. (the “Fund"). Certain financial information and data used herein have been d eri ved or obtained from public filings, including filings made by the Fund with the Securities and Exchange Commission and other sources. All reasona ble care has been taken in the preparation of this information. No responsibility can be accepted under any circumstances for errors of fact or omission . Some of the information in this document may contain projections or other forward looking statements regarding future events or future financial performance of countries, markets or companies. These statements are only predictions and actual events or results may differ ma terially. Emerging market securities carry special risks, such as less developed or less efficient trading markets, a lack of company informatio n, and differing auditing and legal standards. The securities markets of emerging market countries can be extremely volatile; performance can also be influ enc ed by political, social, and economic factors affecting companies in these countries. Values may fall as well as rise and you may not get back the am oun t invested. Past performance is no guarantee of future results. 7