Southern Timberland Joint Venture Supporting Materials August 27, 2008 1 Exihibit 99.2 |

Safe Harbor This presentation contains forward-looking statements. Some of the forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates,” “projects,” “strategy” or “anticipates” or the negative of those words or other comparable terminology. Forward-looking statements involve inherent risks and uncertainties. A number of important factors could cause actual results to differ materially from those described in the forward-looking statements. Some of these factors include, but are not limited to: changes in governmental, legislative and environmental restrictions; catastrophic losses from fires, floods, conditions and competition in our domestic and export markets; our failure to qualify as a REIT or a reduction in the demand for timber products and/or an unanticipated increase in the supply of timber products; our failure to make strategic acquisitions or to integrate any such acquisitions effectively; the market for and our ability to sell or exchange non-strategic timberlands and timberland properties that have higher and better uses; and other factors described from time to time in our filings with the Securities and Exchange Commission under the Securities Exchange Act of 1934, as amended, and the Securities Act of 1933, as amended. Forward-looking statements are not guarantees of performance, and speak only as of the date made, and neither Plum Creek nor its management undertakes any obligation to update or revise any forward looking statements. 2 |

Transaction Highlights Highlights the value of Plum Creek Southern timberlands Captures substantially all the value of these timberlands today Transaction economics are largely fixed through our preferred equity position Receive $783 million of cash today through a loan from the joint venture Plum Creek maintains a 9% common equity position in the assets Expected to be both earnings and cash-flow accretive when coupled with planned permanent debt reduction No gain recognized for book or tax purposes No current distribution requirements 3 • • • • ($1,725/acre) |

Southern Timberlands Description 4 • Approximately 11% of Plum Creek’s Southern timberland portfolio • Lands are SFI certified, intensively managed, well diversified, productive core timberlands • Stocking levels are ~7% lower than Plum Creek’s Southern average due to slightly younger age class profile • Currently, 1% of lands are classified by Plum Creek as HBU/Recreation compared to 15% for Plum Creek’s remaining Southern acres 454,000 acres 6 states (SC, NC, GA, MS, AR, OK) |

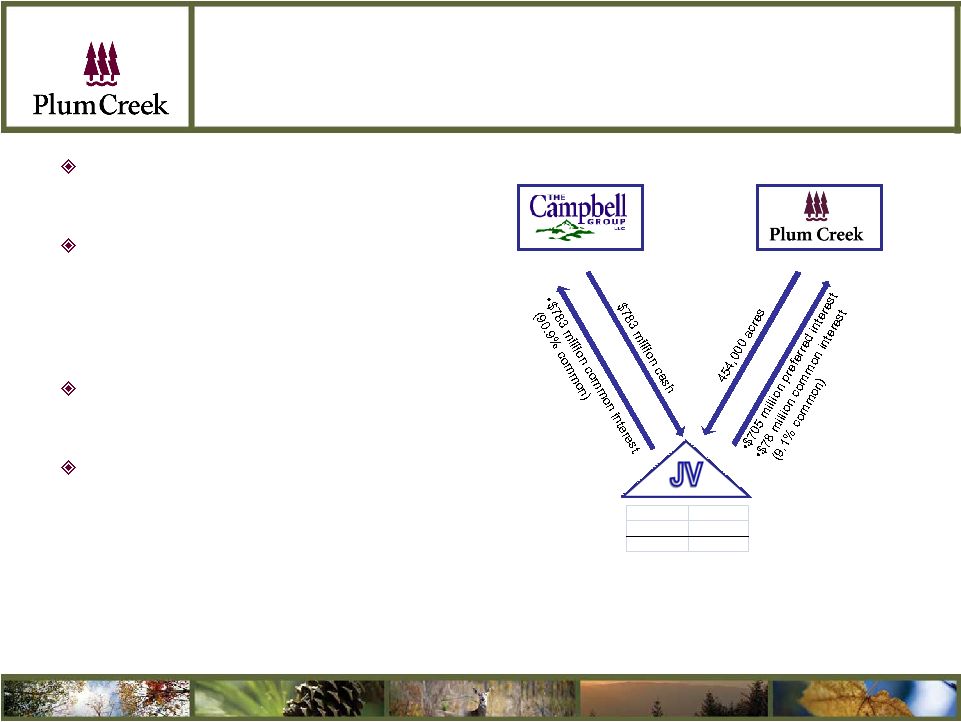

Joint Venture Formation The Campbell Group Contribution $783 million cash The Campbell Group Ownership $783 million common interest (90.9% of common equity) ---------------------------------------------- Plum Creek Contribution 454,000 acres Plum Creek Ownership $705 million preferred interest ($56 million annual preferred distribution yielding 7.875% ) $78 million common interest (9.1% of common equity) 5 Cash 783 $ Timberland 783 $ Assets 1,566 $ • • • • • |

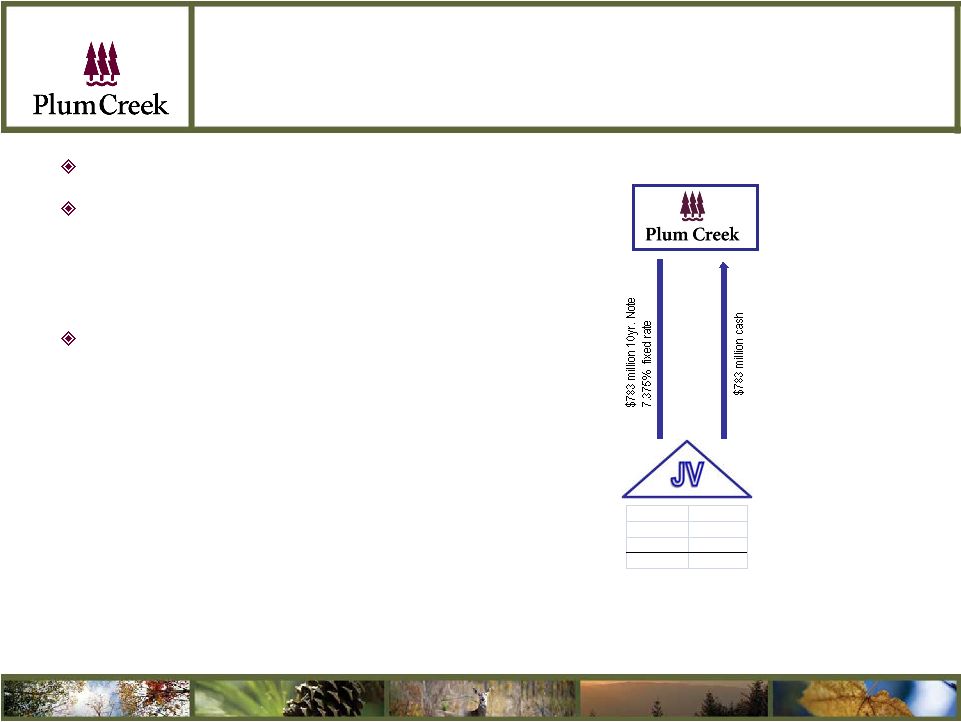

Joint Venture Loan* to Plum Creek $783 million loan amount 7.375% fixed interest rate $58 million annual interest expense, paid quarterly from Plum Creek to the JV 10 year term with 2 year extension 6 Cash - $ Loan 783 $ Timberland 783 $ Assets 1,566 $ * The loan is an obligation of Plum Creek Timber Co, Inc., the REIT’s holding company. Existing bank, private and public debt is an obligation of Plum Creek Timberlands L.P., an operating partnership which owns the REIT’s timberlands. The joint venture will have no claim or rights against the assets of the operating partnership. • |

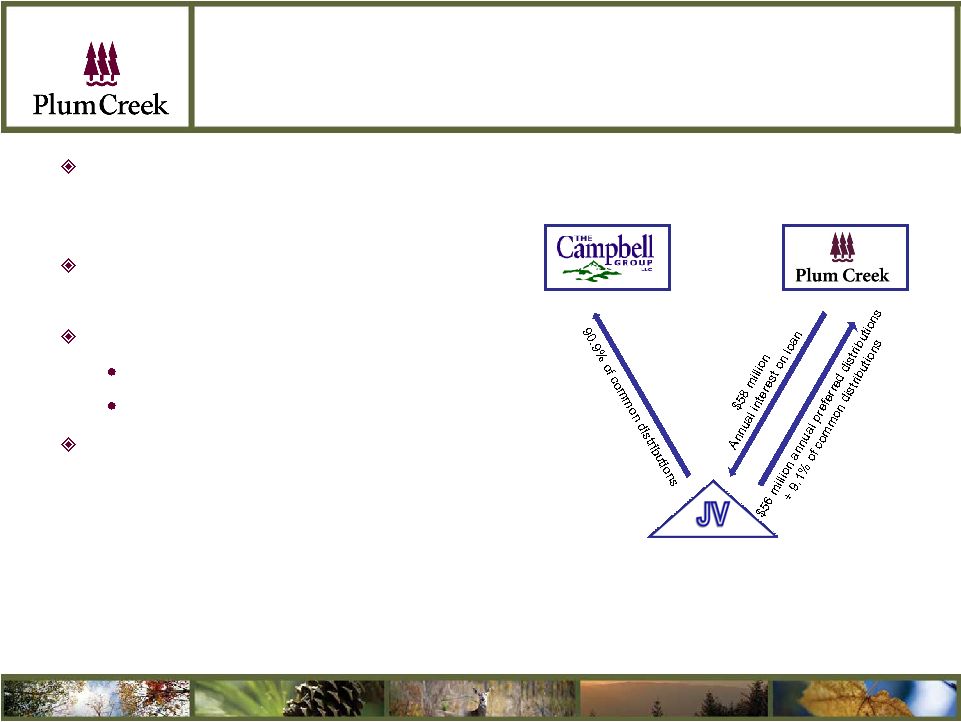

Joint Venture Operation JV earnings and cash flow generated by timber operations and interest income Preferred distributions have priority over common distributions Plum Creek distributions consist of $56 million annual preferred distributions 9.1% of common distributions The Campbell Group distributions consist of 90.9% of common distributions 7 Sources of earnings and cash flow for the JV: Timber operations + Interest income |

Plum Creek Capital Allocation Plans Repayment of existing debt with 50% of proceeds reduces interest expense on existing debt by approximately $27 million/year Retire $300 million private placement debt over the next 12 months, average interest rate of 8.1% – $100 million Q4 2008 – $ 50 million Q1 2009 – $150 million Q3 2009 $92 million paydown of bank debt, interest rate of 3.25% Continued opportunistic share repurchase 8 |

Key Financial Model Items No gain recognized upon contribution of timberlands. The book basis of contributed timberlands = book basis of Plum Creek’s investment in the unconsolidated partnership. Equity method of accounting for preferred and common interests. Plum Creek records its share of earnings as the JV earns them. 9 |

Summary Guidance Transaction and Initial Capital Allocation INCOME STATEMENT ITEMS Operating Income $ (23) Estimated reduction annual operating income directly attributed to the timberlands contributed to the JV. Based on 2007 results. The estimate assumes no reduction in allocated costs and expenses. Interest Expense $ (58) Increased interest expense due to loan from the JV. Interest Expense $ 27 Reduced interest expense from debt retirement Interest Income $ 10 Interest Income from cash awaiting deployment – assumes 50% of proceeds ($391 million) held as cash awaiting deployment, earnings 2.65% interest. Equity Earnings from unconsolidated JV $ 56 Preferred distributions from JV. Equity Earnings from unconsolidated JV $ 2 Estimated Common income from JV. 10 $ 23 Timber operations income of JV $ 58 Interest income of JV $ 81 Total JV income $ 56 Preferred distributions to Plum Creek $ 25 JV income available to common interests 9.1% Plum Creek common interest $ 2 Common income to Plum Creek ($ in millions) X |

Summary Guidance Transaction and Initial Capital Allocation BALANCE SHEET ITEMS Cash $ 783 Loan proceeds from JV. Cash $ (392) Debt retirement. Long-Term Debt $ 783 Loan from JV. Long-Term Debt $ (392) Retirement of debt. Timber and Timberlands, net $ (190) Book value of timberlands contributed to JV. Equity Investment in Unconsolidated JV $ 190 Book basis of equity investment in JV*. CASH FLOW STATEMENT ITEMS DD&A $ 6 Annual Depreciation and Depletion associated with timberlands contributed to the JV. Capital Investment $ 6 Annual Capital Investment associated with timberlands contributed to the JV. 11 *Market Value of equity investment in JV $705 Preferred interest in JV $ 78 9.1% common interest in JV ($ in millions) ($ in millions) |

Misc. Questions Q: Why did Plum Creek elect to go this route rather than simply continue to manage these assets? A: The transaction highlights the value of Plum Creek’s Southern timberlands and captures substantially all of the value of these particular lands today. This transaction is expected to be both cash and earnings accretive. Q: Why will The Campbell Group manage the timberlands? A: Plum Creek has largely secured its economics through its preferred interest. With our economics largely fixed, it’s appropriate for The Campbell Group, the party with over 90% of the common equity, to manage the property. Q: Does Plum Creek have a say in how the JV will be managed? A: Certain major decisions will require Plum Creek consent. For instance if the JV wanted to buy or sell timberlands, Plum Creek consent would generally be required. Q: Will the transaction have any impact on the company’s debt ratings? A: We do not expect any impact on our debt ratings. We have reviewed the transaction with the rating agencies. Q: Does Plum Creek’s ownership interest in the JV qualify as a good REIT asset? A: Yes, because the assets of the JV are considered good REIT assets. Q: Is the income Plum Creek receives from the JV considered good REIT income? A: Yes, because all the JV’s income is considered good REIT income. Q: What happens if the timberlands gain/lose value over the life of the JV? A: Plum Creek would recognize the appropriate capital gain/loss on its common interest at the time of redemption. Q: Does this agreement require any regulatory approvals? A: No. Q: Will this transaction have any effect on the tax characterization of Plum Creek’s dividends? A: No. 12 |

If you have further questions, please contact : John B. Hobbs Director-Investor Relations (206) 467-3628 13 |