UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05812

Legg Mason Partners Premium Money Market Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue,

47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-877-721-1926

Date of fiscal year end: August 31

Date of reporting period: August 31, 2020

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

| | |

| Annual Report | | August 31, 2020 |

WESTERN ASSET

PREMIUM LIQUID RESERVES

Beginning in or after February 2021, as permitted by regulations adopted by the Securities and Exchange Commission, the Fund intends to no longer mail paper copies of the Fund’s shareholder reports like this one, unless you specifically request paper copies of the reports from the Fund or from your Service Agent or financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically (“e-delivery”), you will not be affected by this change and you need not take any action. If you have not already elected e-delivery, you may elect to receive shareholder reports and other communications from the Fund electronically by contacting your Service Agent or, if you are a direct shareholder with the Fund, by calling 1-877-721-1926.

You may elect to receive all future reports in paper free of charge. If you invest through a Service Agent, you can contact your Service Agent to request that you continue to receive paper copies of your shareholder reports. That election will apply to all Legg Mason Funds held in your account at that Service Agent. If you are a direct shareholder with the Fund, you can call the Fund at 1-877-721-1926, or write to the Fund by regular mail at Legg Mason Funds, P.O. Box 9699, Providence, RI 02940-9699 or by express, certified or registered mail to Legg Mason Funds, 4400 Computer Drive, Westborough, MA 01581 to let the Fund know you wish to continue receiving paper copies of your shareholder reports. That election will apply to all Legg Mason Funds held in your account held directly with the fund complex.

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Fund objective

The Fund’s investment objective is to provide shareholders with liquidity and as high a level of current income as is consistent with preservation of capital.

| | |

| II | | Western Asset Premium Liquid Reserves |

Letter from the president

Dear Shareholder,

We are pleased to provide the annual report of Western Asset Premium Liquid Reserves for the twelve-month reporting period ended August 31, 2020. Please read on for a detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

Special shareholder notice

On July 31, 2020, Franklin Resources, Inc. (“Franklin Resources”) acquired Legg Mason, Inc. (“Legg Mason”) in an all-cash transaction. As a result of the transaction, Legg Mason Partners Fund Advisor, LLC (“LMPFA”) and the subadviser(s) became indirect, wholly-owned subsidiaries of Franklin Resources. Under the Investment Company Act of 1940, as amended, consummation of the transaction automatically terminated the management and subadvisory agreements that were in place for the Fund prior to the transaction. The Fund’s manager and subadviser(s) continue to provide uninterrupted services with respect to the Fund pursuant to either new management and subadvisory agreements that were approved by Fund shareholders or interim management and subadvisory agreements that were approved by the Fund’s board for use while the Fund continues to seek shareholder approval of the new agreements.

Franklin Resources, whose principal executive offices are at One Franklin Parkway, San Mateo, California 94403, is a global investment management organization operating, together with its subsidiaries, as Franklin Templeton. As of August 31, 2020, after giving effect to the transaction described above, Franklin Templeton’s asset management operations had aggregate assets under management of approximately $1.4 trillion.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.leggmason.com. Here you can gain immediate access to market and investment information, including:

| • | | Fund prices and performance, |

| • | | Market insights and commentaries from our portfolio managers, and |

| • | | A host of educational resources. |

| | |

| Western Asset Premium Liquid Reserves | | III |

Letter from the president

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

September 30, 2020

| | |

| IV | | Western Asset Premium Liquid Reserves |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund seeks to provide shareholders with liquidity and as high a level of current income as is consistent with preservation of capital. The Fund is a money market fund that invests in securities through an underlying mutual fund, Liquid Reserves Portfolio (the “Portfolio”), which has the same investment objective and strategies as the Fund. The Portfolio invests in high-quality, U.S. dollar-denominated short-term debt securities that, at the time of purchase, are rated by one or more rating agencies in the highest short-term rating category or, if not rated, that we determined to be of equivalent quality.

The Portfolio may invest in all types of money market instruments, including bank obligations, commercial paper and asset-backed securities, structured investments, repurchase agreements and other short-term debt securities. These instruments may be issued or guaranteed by all types of issuers, including U.S. and foreign banks and other private issuers, the U.S. government or any of its agencies or instrumentalities, U.S. states and municipalities, or foreign governments. These securities may pay interest at fixed, floating or adjustable rates, or may be issued at a discount.

The Portfolio may invest without limit in bank obligations, such as certificates of deposit, fixed time deposits and bankers’ acceptances. The Portfolio generally limits its investments in foreign securities to U.S. dollar denominated obligations of issuers, including banks and foreign governments, located in the major industrialized countries, although with respect to bank obligations, the branches of the banks issuing the obligations may be located in The Bahamas or the Cayman Islands.

As a money market fund, the Fund must follow strict rules as to the credit quality, liquidity, diversification and maturity of its investments. Where required by these rules, the Fund’s and the Portfolio’s subadviser, Western Asset Management Company, LLC (“Western Asset”), or Board of Trustees will decide whether a security should be held or sold in the event of credit downgrades or certain other events occurring after purchase. The Fund sells and redeems its shares at prices based on the current market value of the securities it holds. Therefore, the share price of the Fund will fluctuate along with changes in the market-based value of fund assets. Because the share price of the Fund fluctuates, it has what is called a “floating net asset value” or “floating NAV”.

At Western Asset, we utilize a fixed income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio management personnel, research analysts and an in-house economist. Under this team approach, management of client fixed income portfolios will reflect a consensus of interdisciplinary views within the Western Asset organization.

Q. What were the overall market conditions during the Fund’s reporting period?

A. Both short- and long-term Treasury yields moved sharply lower during the twelve-month reporting period ended August 31, 2020. The yield for the two-year Treasury note began the

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 1 |

Fund overview (cont’d)

reporting period at 1.50% and rose as high as 1.79% on September 13, 2019. The low for the period of 0.11% occurred several times toward the end of July and the beginning of August 2020, and ended the period at 0.14%. The yield for the ten-year Treasury began the reporting period at 1.50% and moved as high as 1.94% on November 8, 2019. The low for the period of 0.52% occurred on August 4, 2020, and ended the period at 0.72%.

The Federal Reserve Board (the “Fed”)i took a number of actions to support the economy during the reporting period. At its meeting that concluded on July 31, 2019, prior to the beginning of the reporting period, the Fed reduced the federal funds rateii from a range between 2.25% and 2.50% to a range between 2.00% and 2.25%. This represented the Fed’s first rate cut since 2008. The Fed then again lowered rates in September and October 2019 and ended calendar year 2019 with rates between 1.50% and 1.75%. After several months on hold, the Fed aggressively responded to the repercussions from the COVID-19 pandemic by cutting rates to a range between 1.00% and 1.25% on March 3, 2020, and then to a range between 0.00% and 0.25% on March 15, 2020. Finally, on August 27, 2020, the Fed announced a revision to its “Statement on Longer-Run Goals and Monetary Policy Strategy”. Fed Chair Jerome Powell said, “Our revised statement reflects our appreciation for the benefits of a strong labor market...and that a robust job market can be sustained without causing an unwelcome increase in inflation”, as he explained the changes. As such, the Fed’s new approach to setting U.S. monetary policy will entail letting inflation and employment run higher, which could mean interest rates remain lower for longer than previously anticipated.

Q. How did we respond to these changing market conditions?

A. During the early part of the reporting period, the Fund’s portfolio maintained an extended average maturity, as the Fed shifted to an easing bias. This was done in response to inflation remaining well below the targeted level of 2.0%, along with a relatively modest pace of economic growth. The Portfolio maintained a neutral maturity stance towards year-end 2019 and into early 2020. In early March 2020, the COVID-19 crisis required a shift towards maintaining higher liquidity levels and investors flocked towards the larger cash positions available in money market funds. After the Fed lowered rates to a range between 0.0% to 0.25% and put in place several programs to support market liquidity conditions, we sought to extend the average maturity of the portfolio, as it was clear that the low policy rate would remain in place for an extended period.

| | |

| 2 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

Performance review

As of August 31, 2020, the seven-day current yield for Western Asset Premium Liquid Reserves was 0.01% and the seven-day effective yield, which reflects compounding, was 0.01%.1

The Fund does not invest directly in securities but instead invests all of its investable assets in an underlying mutual fund, the Portfolio, which has the same investment objective and strategies, and substantially the same policies as the Fund. Unless otherwise indicated, references to the Fund include the underlying mutual fund, the Portfolio.

| | | | |

Western Asset Premium Liquid Reserves Yields as of August 31, 2020 (unaudited) | |

| Seven-Day Current Yield1 | | | 0.01 | % |

| Seven-Day Effective Yield1 | | | 0.01 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Yields will fluctuate. To obtain performance data current to the most recent month-end, please visit our website at www.leggmason.com/moneymarketfunds.

Absent fee waivers and/or expense reimbursements, the seven-day current yield and the seven-day effective yield would have been-0.90%.

The manager has voluntarily undertaken to limit Fund expenses. Such expense limitations may fluctuate daily and are voluntary and temporary and may be terminated by the manager at any time without notice.

You could lose money by investing in the Fund. Because the share price of the Fund fluctuates, when you sell your shares they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

| 1 | The seven-day current yield reflects the amount of income generated by the investment during that seven-day period and assumes that the income is generated each week over a 365-day period. The yield is shown as a percentage of the investment. The seven-day effective yield is calculated similarly to the seven-day current yield but, when annualized, the income earned by an investment in the Fund is assumed to be reinvested. The effective yield typically will be slightly higher than the current yield because of the compounding effect of the assumed reinvestment. |

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 3 |

Fund overview (cont’d)

Q. What were the most significant factors affecting Fund performance?

A. The maturity positioning of the Portfolio and its holdings of higher-yielding floating-rate securities positively impacted performance over the reporting period as yields declined. There were no meaningful detractors from performance during the period.

Thank you for your investment in Western Asset Premium Liquid Reserves. As always, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the Fund’s investment goals.

Sincerely,

Western Asset Management Company, LLC

September 30, 2020

RISKS: You could lose money by investing in the Fund. Because the share price of the Fund fluctuates, when you sell your shares they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time. The Fund will be more susceptible to negative events affecting the worldwide financial services sector as a significant portion of its assets may be invested in obligations that are issued or backed by U.S. and non- U.S. banks and other financial services companies. Please see the Fund’s prospectus for a more complete discussion of these and other risks and the Fund’s investment strategies.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| i | The Federal Reserve Board (the “Fed”) is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| ii | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| | |

| 4 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

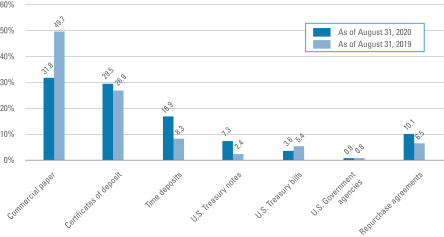

Portfolio at a glance† (unaudited)

Liquid Reserves Portfolio

The Fund invests all of its investable assets in Liquid Reserves Portfolio, the investment breakdown of which is shown below.

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of August 31, 2020 and August 31, 2019. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 5 |

Fund expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on March 1, 2020 and held for the six months ended August 31, 2020.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Based on actual total return1 | | | | Based on hypothetical total return1 |

Actual

Total

Return2 | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio3 | | Expenses

Paid During

the Period4 | | | | Hypothetical

Annualized

Total Return | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio3 | | Expenses

Paid During

the Period4 |

| | | 0.17% | | | | $ | 1,000.00 | | | | $ | 1,001.70 | | | | | 0.44 | % | | | $ | 2.21 | | | | | | | 5.00 | % | | | | $1,000.00 | | | | $ | 1,022.92 | | | | | 0.44 | % | | | $ | 2.24 | |

| 1 | For the six months ended August 31, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Includes the Fund’s share of Liquid Reserves Portfolio’s allocated expenses. |

| 4 | Expenses (net of fee waivers and/or expense reimbursements) are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 366. |

| | |

| 6 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

Statement of assets and liabilities

August 31, 2020

| | | | |

| |

| Assets: | | | | |

Investment in Liquid Reserves Portfolio, at value | | $ | 13,875,104 | |

Receivable from investment manager | | | 4,567 | |

Prepaid expenses | | | 13,073 | |

Total Assets | | | 13,892,744 | |

| |

| Liabilities: | | | | |

Audit fees payable | | | 17,164 | |

Transfer agent fees payable | | | 11,785 | |

Shareholder reports payable | | | 2,896 | |

Service and/or distribution fees payable | | | 586 | |

Trustees’ fees payable | | | 54 | |

Distributions payable | | | 2 | |

Accrued expenses | | | 3,250 | |

Total Liabilities | | | 35,737 | |

| Total Net Assets | | $ | 13,857,007 | |

| |

| Net Assets: | | | | |

Par value (Note 3) Paid-in capital in excess of par value | | $

| 138

13,885,504 |

|

Total distributable earnings (loss) | | | (28,635) | |

| Total Net Assets | | $ | 13,857,007 | |

| |

| Shares Outstanding | | | 13,847,974 | |

| |

| Net Asset Value | | $ | 1.0007 | |

See Notes to Financial Statements.

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 7 |

Statement of Operations

For the Year Ended August 31, 2020

| | | | |

| |

| Investment Income: | | | | |

Income from Liquid Reserves Portfolio | | $ | 211,083 | |

Allocated expenses from Liquid Reserves Portfolio | | | (15,841) | |

Allocated waiver and/or expense reimbursements from Liquid Reserves Portfolio | | | 14,901 | |

Total Investment Income | | | 210,143 | |

| |

| Expenses: | | | | |

Transfer agent fees | | | 56,548 | |

Investment management fee (Note 2) | | | 51,596 | |

Registration fees | | | 26,614 | |

Audit and tax fees | | | 21,212 | |

Service and/or distribution fees (Note 2) | | | 14,742 | |

Fund accounting fees | | | 9,000 | |

Legal fees | | | 5,790 | |

Shareholder reports | | | 5,289 | |

Trustees’ fees | | | 821 | |

Insurance | | | 651 | |

Miscellaneous expenses | | | 1,156 | |

Total Expenses | | | 193,419 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (128,889) | |

Net Expenses | | | 64,530 | |

| Net Investment Income | | | 145,613 | |

| |

| Realized and Unrealized Gain (Loss) on Investments: | | | | |

Net Realized Loss on Investments From Liquid Reserves Portfolio | | | (157) | |

Change in Net Unrealized Appreciation (Depreciation) From Investments in Liquid Reserves Portfolio | | | 4,404 | |

| Net Gain on Investments | | | 4,247 | |

| Increase in Net Assets From Operations | | $ | 149,860 | |

See Notes to Financial Statements.

| | |

| 8 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

Statements of changes in net assets

| | | | | | | | |

| For the Years Ended August 31, | | 2020 | | | 2019 | |

| | |

| Operations: | | | | | | | | |

Net investment income | | $ | 145,613 | | | $ | 336,149 | |

Net realized loss | | | (157) | | | | (736) | |

Change in net unrealized appreciation (depreciation) | | | 4,404 | | | | 783 | |

Increase in Net Assets From Operations | | | 149,860 | | | | 336,196 | |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | | | |

Total distributable earnings | | | (145,428) | | | | (336,508) | |

Decrease in Net Assets From Distributions to Shareholders | | | (145,428) | | | | (336,508) | |

| | |

| Fund Share Transactions (Note 3): | | | | | | | | |

Net proceeds from sale of shares | | | 6,977,208 | | | | 4,374,918 | |

Reinvestment of distributions | | | 142,291 | | | | 330,333 | |

Cost of shares repurchased | | | (8,656,172) | | | | (7,601,530) | |

Decrease in Net Assets From Fund Share Transactions | | | (1,536,673) | | | | (2,896,279) | |

| Decrease in Net Assets | | | (1,532,241) | | | | (2,896,591) | |

| | |

| Net Assets: | | | | | | | | |

Beginning of year | | | 15,389,248 | | | | 18,285,839 | |

End of year | | $ | 13,857,007 | | | $ | 15,389,248 | |

See Notes to Financial Statements.

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 9 |

Financial highlights

| | | | | | | | | | | | | | | | | | | | |

| For a share of each class of beneficial interest outstanding throughout each year ended August 31: | |

| | | 20201 | | | 20191 | | | 20181 | | | 20171,2 | | | 20161 | |

| | | | | |

| Net asset value, beginning of year | | $ | 1.0004 | | | $ | 1.0005 | | | $ | 1.0005 | | | $ | 1.0001 | | | $ | 1.000 | |

| | | | | |

Income (loss) from operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.0099 | | | | 0.0206 | | | | 0.0126 | | | | 0.0051 | | | | 0.001 | |

Net realized and unrealized gain (loss) | | | (0.0001) | 3 | | | 0.0000 | 4 | | | 0.0004 | 3 | | | 0.001 | 2 | | | (0.000) | 4 |

Total income from operations | | | 0.0098 | | | | 0.0206 | | | | 0.0130 | | | | 0.0063 | | | | 0.001 | |

| | | | | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.0095) | | | | (0.0207) | | | | (0.0130) | | | | (0.0059) | | | | (0.001) | |

Total distributions | | | (0.0095) | | | | (0.0207) | | | | (0.0130) | | | | (0.0059) | | | | (0.001) | |

| | | | | |

| Net asset value, end of year | | $ | 1.0007 | | | $ | 1.0004 | | | $ | 1.0005 | | | $ | 1.0005 | | | $ | 1.000 | |

Total return5 | | | 0.98 | % | | | 2.08 | % | | | 1.30 | % | | | 0.64 | % | | | 0.13 | % |

| | | | | |

| Net assets, end of year (000s) | | $ | 13,857 | | | $ | 15,389 | | | $ | 18,286 | | | $ | 24,291 | | | $ | 89,084 | |

| | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses6,7 | | | 1.42 | % | | | 1.69 | % | | | 1.56 | % | | | 1.22 | % | | | 0.66 | % |

Net expenses6,8,9 | | | 0.44 | | | | 0.45 | | | | 0.45 | | | | 0.44 | | | | 0.36 | |

Net investment income | | | 0.99 | | | | 2.06 | | | | 1.26 | | | | 0.51 | | | | 0.09 | |

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | Effective October 11, 2016, the share price of the Fund fluctuates along with changes in the market-based value of fund assets. |

| 3 | Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized loss presented in the Statement of Operations due to the timing of sales and repurchases of Fund Shares. |

| 4 | Amount represents less than $0.0005 per share. |

| 5 | Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 6 | Includes the Fund’s share of Liquid Reserves Portfolio’s allocated expenses. |

| 7 | The gross expenses do not reflect the reduction in the Fund’s management fee, pursuant to the Fund’s investment management agreement, by the amount paid by the Fund for its allocable share of the management fee paid by Liquid Reserves Portfolio. |

| 8 | As a result of an expense limitation arrangement, the ratio of total annual fund operating expenses, other than interest, brokerage, taxes, extraordinary expenses and acquired fund fees and expenses, to average net assets of the Fund did not exceed 0.45%. This expense limitation arrangement cannot be terminated prior to December 31, 2020 without the Board of Trustees’ consent. Additional amounts may be voluntarily waived and/or reimbursed from time to time. |

| 9 | Reflects fee waivers and/or expense reimbursements. |

See Notes to Financial Statements.

| | |

| 10 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

Notes to financial statements

1. Organization and significant accounting policies

Western Asset Premium Liquid Reserves (the “Fund”) is a separate diversified investment series of Legg Mason Partners Premium Money Market Trust (the “Trust”). The Trust, a Maryland statutory trust, is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund invests all of its investable assets in Liquid Reserves Portfolio (the “Portfolio”), a separate investment series of Master Portfolio Trust, that has the same investment objective as the Fund.

The financial statements of the Portfolio, including the schedule of investments, are contained elsewhere in this report and should be read in conjunction with the Fund’s financial statements.

The share price of the Fund fluctuates along with changes in the market-based value of fund assets. Because the share price of the Fund fluctuates, it has what is called a “floating net asset value” or “floating NAV”. Under Rule 2a-7 of the 1940 Act, the Fund must follow strict rules as to the credit quality, liquidity, diversification and maturity of its investments. The Fund may impose fees upon the sale of shares or temporarily suspend the ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation. The Fund records its investment in the Portfolio at value. The value of such investment in the Portfolio reflects the Fund’s proportionate interest (0.1% at August 31, 2020) in the net assets of the Portfolio.

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. The disclosure and valuation of securities held by the Portfolio are discussed in Note 1(a) of the Portfolio’s Notes to Financial Statements, which are included elsewhere in this report.

(b) Investment transactions and investment income. Net investment income and net realized/unrealized gains and losses of the Portfolio is allocated pro rata, based on respective ownership interests, among the Fund and other investors in the Portfolio (the “Holders”) at the time of such determination. The Fund also pays certain other expenses which can be directly attributed to the Fund.

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 11 |

Notes to financial statements (cont’d)

(c) Distributions to shareholders. Distributions from net investment income on the shares of the Fund are declared each business day and are paid monthly. Distributions of net realized gains, if any, are declared at least annually. Distributions to shareholders of the Fund are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from GAAP.

(d) Federal and other taxes. It is the Fund’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986 (the “Code”), as amended, applicable to regulated investment companies. Accordingly, the Fund intends to distribute its taxable income and net realized gains, if any, to shareholders in accordance with timing requirements imposed by the Code. Therefore, no federal or state income tax provision is required in the Fund’s financial statements.

Management has analyzed the Fund’s tax positions taken on income tax returns for all open tax years and has concluded that as of August 31, 2020, no provision for income tax is required in the Fund’s financial statements. The Fund’s federal and state income and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

(e) Reclassification. GAAP requires that certain components of net assets be reclassified to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. During the current year, the following reclassifications have been made:

| | | | | | | | |

| | | Total Distributable

Earnings (Loss) | | | Paid-in

Capital | |

| (a) | | $ | 1,664 | | | $ | (1,664) | |

| (a) | Reclassifications are due to a taxable overdistribution. |

2. Investment management agreement and other transactions with affiliates

Legg Mason Partners Fund Advisor, LLC (“LMPFA”) is the Fund’s and the Portfolio’s investment manager and Western Asset Management Company, LLC (“Western Asset”) is the Fund’s and the Portfolio’s subadviser. As of July 31, 2020, LMPFA and Western Asset are indirect, wholly-owned subsidiaries of Franklin Resources, Inc. (“Franklin Resources”). Prior to July 31, 2020, LMPFA and Western Asset were wholly-owned subsidiaries of Legg Mason, Inc. (“Legg Mason”). As of July 31, 2020, Legg Mason is a subsidiary of Franklin Resources.

Under the investment management agreement, the Fund pays an investment management fee, calculated daily and paid monthly, at an annual rate of 0.35% of the Fund’s average daily net assets.

Since the Fund invests all of its investable assets in Liquid Reserves Portfolio, the investment management fee of the Fund will be reduced by the investment management fee allocated to the Fund by Liquid Reserves Portfolio.

| | |

| 12 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

LMPFA provides administrative and certain oversight services to the Fund. LMPFA delegates to the subadviser the day-to-day portfolio management of the Fund. For its services, LMPFA pays Western Asset monthly 70% of the net management fee it receives from the Fund.

As a result of an expense limitation arrangement between the Fund and LMPFA, the ratio of total annual fund operating expenses, other than interest, brokerage, taxes, extraordinary expenses and acquired fund fees and expenses, to average net assets of the Fund did not exceed 0.45%. This expense limitation arrangement cannot be terminated prior to December 31, 2020 without the Board of Trustees’ consent. Additional amounts may be voluntarily waived and/or reimbursed from time to time.

During the year ended August 31, 2020, fees waived and/or expenses reimbursed amounted to $128,889.

LMPFA is permitted to recapture amounts waived and/or reimbursed to the Fund during the same fiscal year if the Fund’s total annual fund operating expenses have fallen to a level below the expense limitation (“expense cap”) in effect at the time the fees were earned or the expenses incurred. In no case will LMPFA recapture any amount that would result, on any particular business day of the Fund, in the class’ total annual fund operating expenses exceeding the expense cap or any other lower limit then in effect.

As of July 31, 2020, Legg Mason Investor Services, LLC (“LMIS”) is an indirect, wholly-owned broker-dealer subsidiary of Franklin Resources and serves as the Fund’s sole and exclusive distributor. Prior to July 31, 2020, LMIS was a wholly-owned broker-dealer subsidiary of Legg Mason.

The Fund has adopted a Rule 12b-1 shareholder services and distribution plan and under that plan the Fund pays service and/or distribution fees at an annual rate not to exceed 0.10% of the Fund’s average daily net assets. Service and/or distribution fees are accrued daily and paid monthly. For the year ended August 31, 2020, the service and/or distribution fees paid amounted to $14,742. For the year ended August 31, 2020, the service and/or distribution fees waived amounted to $7,371. Such waiver is voluntary and may be reduced or terminated at any time.

As of July 31, 2020, all officers and one Trustee of the Trust are employees of Franklin Resources or its affiliates and do not receive compensation from the Trust. Prior to July 31, 2020, all officers and one Trustee of the Trust were employees of Legg Mason and did not receive compensation from the Trust.

3. Shares of beneficial interest

At August 31, 2020, the Trust had an unlimited number of shares of beneficial interest authorized with a par value of $0.00001 per share.

| | |

| Western Asset Premium Liquid Reserves 2020 Annual Report | | 13 |

Notes to financial statements (cont’d)

Transactions in shares of the Fund were as follows:

| | | | | | | | |

| | | Year Ended

August 31, 2020 | | | Year Ended

August 31, 2019 | |

| Shares sold | | | 6,973,255 | | | | 4,373,276 | |

| Shares issued on reinvestment | | | 142,220 | | | | 330,200 | |

| Shares repurchased | | | (8,649,881) | | | | (7,598,433) | |

| Net decrease | | | (1,534,406) | | | | (2,894,957) | |

4. Income tax information and distributions to shareholders

The tax character of distributions paid during the fiscal years ended August 31, was as follows:

| | | | | | | | |

| | | 2020 | | | 2019 | |

| Distributions paid from: | | | | | | | | |

| Ordinary income | | $ | 145,428 | | | $ | 336,508 | |

As of August 31, 2020, there were no significant differences between the book and tax components of net assets.

Additionally, the Fund had deferred capital losses of $26,497. The losses will be deemed to occur on the first day of the next taxable year in the same character as they were originally deferred and will be available to offset future taxable capital gains.

5. Other matter

The outbreak of the respiratory illness COVID-19 (commonly referred to as “coronavirus”) has continued to rapidly spread around the world, causing considerable uncertainty for the global economy and financial markets. The ultimate economic fallout from the pandemic, and the long-term impact on economies, markets, industries and individual issuers, are not known. The COVID-19 pandemic could adversely affect the value and liquidity of the Fund’s investments through the Portfolio, impair the Fund’s ability to satisfy redemption requests, and negatively impact the Fund’s performance. In addition, the outbreak of COVID-19, and measures taken to mitigate its effects, could result in disruptions to the services provided to the Fund by its service providers.

| | |

| 14 | | Western Asset Premium Liquid Reserves 2020 Annual Report |

Report of independent registered public accounting firm

To the Board of Trustees of Legg Mason Partners Premium Money Market Trust and Shareholders of Western Asset Premium Liquid Reserves

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Western Asset Premium Liquid Reserves (one of the funds constituting Legg Mason Partners Premium Money Market Trust, referred to hereafter as the “Fund”) as of August 31, 2020, the related statement of operations for the year ended August 31, 2020, the statement of changes in net assets for each of the two years in the period ended August 31, 2020, including the related notes, and the financial highlights for each of the three years in the period ended August 31, 2020 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of August 31, 2020, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended August 31, 2020 and the financial highlights for each of the three years in the period ended August 31, 2020 in conformity with accounting principles generally accepted in the United States of America.

The financial statements of the Fund as of and for the year ended August 31, 2017 and the financial highlights for each of the periods ended on or prior to August 31, 2017 (not presented herein, other than the financial highlights) were audited by other auditors whose report dated October 16, 2017 expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of the security owned as of August 31, 2020 by correspondence with the accounting agent for the Liquid Reserves Portfolio. We believe that our audits provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Baltimore, Maryland

October 16, 2020

We have served as the auditor of one or more investment companies in the Franklin Templeton Group of Funds since 1948.

| | |

Western Asset Premium Liquid Reserves 2020 Annual Report | | 15 |

Board approval of new management and new subadvisory agreements (unaudited)

On February 18, 2020, Franklin Resources, Inc., a global investment management organization operating, together with its subsidiaries, as Franklin Templeton (“Franklin Templeton”), and Legg Mason, Inc. (“Legg Mason”) announced that they entered into a definitive agreement (the “Transaction Agreement”) for Franklin Templeton to acquire Legg Mason in an all-cash transaction (the “Transaction”). The Transaction closed on July 31, 2020. As part of this transaction, the Fund’s manager, Legg Mason Partners Fund Advisor, LLC (the “Manager”), and the Fund’s subadviser, Western Asset Management Company, LLC (the “Subadviser,” and collectively with the Manager, the “Advisers”), each a wholly owned subsidiary of Legg Mason, became wholly owned subsidiaries of Franklin Templeton. Under the Investment Company Act of 1940, as amended (the “1940 Act”), the Transaction resulted in the automatic termination of the Fund’s management agreement with the Manager that was in place prior to the closing of the Transaction (the “Existing Management Agreement”) and the sub-advisory agreement between the Manager and the Subadviser that was in place prior to the closing of the Transaction (the “Existing Sub-advisory Agreement,” and, collectively, the “Existing Agreements”).

At a meeting of the Board of Trustees of Legg Mason Partners Premium Money Market Trust (the “Trust”) held on April 14, 2020,1 the Board, including the Trustees who are not considered to be “interested persons” of the Trust (the “Independent Trustees”) under the 1940 Act, approved a new management agreement (the “New Management Agreement”) between the Trust and the Manager with respect to Western Asset Premium Liquid Reserves (the “Fund”), a series of the Trust, and the new sub-advisory agreement (the “New Sub-Advisory Agreement,” and collectively, the “New Agreements”) between the Manager and the Subadviser with respect to the Fund. The Board also authorized the Fund’s officers to submit the New Agreements to Fund shareholders for their approval. Fund shareholders were sent notice of the shareholder meeting and a proxy statement in April, 2020. Shareholders of the Fund have approved the New Agreements.

Background

On March 9, 2020, during a telephonic meeting, members of the Board discussed with Legg Mason management and certain Franklin Templeton representatives the Transaction and Franklin Templeton’s plans and intentions regarding the Legg Mason funds and Legg Mason’s asset management business, including the preservation and continued investment autonomy of the investment advisory businesses conducted by the Subadviser and the combination of Legg Mason’s and Franklin Templeton’s distribution resources.

| 1 | This meeting was held telephonically in reliance on an exemptive order issued by the Securities and Exchange Commission on March 25, 2020. Reliance on the exemptive order is necessary and appropriate due to circumstances related to current or potential effects of COVID-19. All Trustees participating in the telephonic meeting were able to hear each other simultaneously during the meeting. Reliance on the exemptive order requires Trustees, including a majority of the Independent Trustees, to ratify actions taken pursuant to the exemptive order by vote cast at the next in-person meeting. |

| | |

| 16 | | Western Asset Premium Liquid Reserves |

On April 8, 2020, the Independent Trustees met with representatives of Legg Mason to discuss the Transaction and the New Agreements. In addition, the Independent Trustees met separately, with the assistance of their independent legal counsel, to discuss and evaluate the information provided and to consider what additional information was desired.

The Independent Trustees considered, among other things, whether it would be in the best interests of the Fund and its respective shareholders to approve the New Agreements, and the anticipated impacts of the Transaction on the Fund and its shareholders. To assist the Board in its consideration of the New Agreements, Franklin Templeton provided materials and information about Franklin Templeton, including its financial condition and asset management capabilities and organization, and Franklin Templeton and Legg Mason provided materials and information about the Transaction.

Before or during the April 14, 2020 meeting, the Board sought additional information as it deemed necessary and appropriate. In connection with the Board’s consideration of the New Agreements, the Independent Trustees worked with their independent legal counsel to prepare requests for information that were submitted to Franklin Templeton and Legg Mason. The Board requested information relevant to the consideration of the New Agreements, distribution arrangements, and other anticipated impacts of the Transaction on the Fund and its shareholders. Franklin Templeton and Legg Mason provided documents and information in response to the request for information. Following their review of this information, the Independent Trustees submitted supplemental due diligence requests for additional information to Franklin Templeton and Legg Mason. Franklin Templeton and Legg Mason provided further information in response to this supplemental diligence request, which the Board reviewed. Senior management representatives from Franklin Templeton and Legg Mason participated in a portion of the meeting and addressed various questions raised by the Board.

At the April 14, 2020 meeting, representatives of Legg Mason (including representatives of the Advisers) and Franklin Templeton made presentations to, and responded to questions from, the Board. After the presentations and after reviewing the written materials provided, the Independent Trustees met in executive session with their counsel to consider the New Agreements.

The Board’s evaluation of the New Agreements reflected the information provided specifically in connection with its review of the New Agreements, as well as, where relevant, information that was previously furnished to the Board in connection with the most recent renewal of the Existing Agreements at in-person meetings held in November 2019 and at other prior Board meetings.

Among other things, the Board considered:

| | |

Western Asset Premium Liquid Reserves | | 17 |

Board approval of new management and new subadvisory agreements (unaudited) (cont’d)

| (i) | the reputation, experience, financial strength and resources of Franklin Templeton and its investment advisory subsidiaries; |

| (ii) | that Franklin Templeton informed the Board of its intent to maintain the investment autonomy of the Legg Mason investment advisory subsidiaries; |

| (iii) | that Franklin Templeton and Legg Mason informed the Board that, following the Transaction, there would not be any expected diminution in the nature, quality and extent of services provided to the Fund and its shareholders by the Advisers, including compliance and other non-advisory services, and represented that there were not expected to be any changes in the portfolio management personnel managing the Fund as a result of the Transaction; |

| (iv) | that Franklin Templeton and Legg Mason informed the Board regarding transition plans, including Legg Mason’s provision of retention incentives for certain Legg Mason corporate personnel prior to the closing of the Transaction, and Franklin Templeton’s provision of long-term retention mechanisms for certain personnel following the closing; |

| (v) | that no changes to the Fund’s custodian or other service providers were expected as a result of the Transaction; |

| (vi) | that Franklin Templeton informed the Board that it had no present intention to alter currently effective expense waivers and reimbursements after their expiration, and, while it reserves the right to do so in the future, it would consult with the Board before making any changes; |

| (vii) | that Franklin Templeton did not expect to propose any changes to the investment objective of the Fund or any changes to the principal investment strategies of the Fund as a result of the Transaction; |

| (viii) | the potential benefits to Fund shareholders from being part of a combined fund family with Franklin Templeton-sponsored funds and access to a broader array of investment opportunities; |

| (ix) | that Franklin Templeton’s distribution capabilities, particularly with respect to retail investors, and significant network of intermediary relationships may provide additional opportunities for the Fund to grow assets and lower expense ratios by spreading expenses over a larger asset base; |

| (x) | that Franklin Templeton and Legg Mason would each derive benefits from the Transaction and that, as a result, they had financial interests in the matters that were being considered; |

| (xi) | the fact that the Fund’s contractual management fee rates would remain the same and would not be increased by virtue of the New Agreements; |

| | |

| 18 | | Western Asset Premium Liquid Reserves |

| (xii) | the terms and conditions of the New Agreements, including that each New Agreement is identical to its corresponding Existing Agreement except for their respective dates of execution, effectiveness and termination; |

| (xiii) | the support expressed by the current senior management team at Legg Mason for the Transaction and Legg Mason’s recommendation that the Board approve the New Agreements; |

| (xiv) | that the Existing Agreements were the product of multiple years of review and negotiation and information received and considered by the Board in the exercise of its business judgment during those years, and that within the past year the Board had performed a full review of and approved the Existing Agreements as required by the 1940 Act and had determined in the exercise of the Board’s business judgment that each Adviser had the capabilities, resources and personnel necessary to provide the services provided to the Fund, and that the management and subadvisory fees paid by or in respect of the Fund represented reasonable compensation to the applicable Adviser in light of the services provided, the costs to the Adviser of providing those services, the fees and other expenses paid by similar funds, and such other matters as the Trustees considered relevant in the exercise of their business judgment, and represented an appropriate sharing between Fund shareholders and the Advisers of any economies of scale in the management of the Fund at current and anticipated asset levels; |

| (xv) | that the Existing Agreements were considered and approved in November 2019; |

| (xvi) | that the Fund would not bear the costs of obtaining shareholder approval of the New Agreements, including proxy solicitation costs, legal fees and the costs of printing and mailing the proxy statement; and |

| (xvii) | that under the Transaction Agreement Franklin Templeton acknowledged that Legg Mason had entered into the Transaction Agreement in reliance upon the benefits and protections provided by Section 15(f) of the 1940 Act, and that, in furtherance of the foregoing, Franklin Templeton represented to the Trustees that it would conduct its business such that (a) for a period of not less than three years after the closing of the Transaction no more than 25% of the members of the Board shall be “interested persons” (as defined in the 1940 Act) of any investment adviser for a Fund, and (b) for a period of not less than two years after the closing, neither Franklin Templeton nor any of its affiliates shall impose an “unfair burden” (within the meaning of the 1940 Act, including any interpretations or no-action letters of the Securities and Exchange Commission) on the Fund as a result of the transactions contemplated by the Transaction Agreement or any express or implied terms, conditions or understandings applicable thereto. |

| | |

Western Asset Premium Liquid Reserves | | 19 |

Board approval of new management and new subadvisory agreements (unaudited) (cont’d)

Certain of these considerations are discussed in more detail below.

The Board noted that the Fund is a “feeder fund” in a “master-feeder” structure, whereby, as a feeder fund, the Fund has the same investment objective and policies as the master fund, Liquid Reserves Portfolio (the “Master Fund”), a series of Master Portfolio Trust, and the Fund invests substantially all of its assets in the Master Fund.

The information provided and presentations made to the Board encompassed the Fund and all other funds for which the Board has responsibility. The discussion below covers both the advisory and the administrative functions rendered by the Manager, both of which functions are encompassed by the New Management Agreement, as well as the advisory functions rendered by the Subadviser pursuant to the New Sub-Advisory Agreement.

Board approval of the New Agreements

The Independent Trustees were advised by separate independent legal counsel throughout the process. Prior to voting, the Independent Trustees received a memorandum from their independent legal counsel discussing the legal standards for their consideration of the proposed approval of the New Management Agreement and the New Sub-Advisory Agreement. The Independent Trustees also reviewed the proposed approval of the New Management Agreement and the New Sub-Advisory Agreement in private sessions with their independent legal counsel at which no representatives of the Manager and Subadviser were present. The Independent Trustees considered the New Management Agreement and the New Sub-Advisory Agreement separately in the course of their review. In doing so, they noted the respective roles of the Manager and the Subadviser in providing services to the Fund.

In their deliberations, the Trustees considered information received in connection with the most recent Board approval/continuation of each Existing Agreement in addition to information provided by Franklin Templeton and Legg Mason in connection with their evaluation of the terms and conditions of the New Agreements. In connection with the most recent approval/continuation of each Existing Agreement, and in connection with their review of each New Agreement, the Trustees did not identify any particular information that was all-important or controlling, and each Trustee may have attributed different weights to the various factors.

After considering all of the factors and information, and in the exercise of its business judgment, the Board, including the Independent Trustees, concluded that the New Agreements, including the fees payable thereunder, were fair and reasonable and that entering into the New Agreements for the Fund was in the best interests of the Fund’s shareholders and approved the New Agreements and recommended that shareholders approve the New Agreements.

| | |

| 20 | | Western Asset Premium Liquid Reserves |

Nature, extent and quality of the services under the New Agreements

The Board received and considered information regarding the nature, extent and quality of services provided to the Fund by the Manager and the Subadviser under the Existing Agreements. In evaluating the nature, quality and extent of the services to be provided by the Advisers under the New Agreements, the Trustees considered, among other things, the expected impact, if any, of the Transaction on the operations, facilities, organization and personnel of each Adviser, and that Franklin Templeton and Legg Mason advised the Boards that, following the Transaction, no diminution in the nature, quality and extent of services provided to the Fund and its shareholders by the Advisers, including compliance and other non-advisory services, were expected, and that no changes in portfolio management personnel as a result of the Transaction were expected. The Board has received information at regular meetings throughout the past year related to the services rendered by the Manager in its management of the Fund’s affairs and the Manager’s role in coordinating the activities of the Fund’s other service providers. The Board’s evaluation of the services provided by the Manager and the Subadviser took into account the Board’s knowledge gained as Trustees of funds in the Legg Mason fund complex, including knowledge gained regarding the scope and quality of the investment management and other capabilities of the Manager and the Subadviser, and the quality of the Manager’s administrative and other services. The Board observed that the scope of services provided by the Manager and the Subadviser, and the undertakings required of the Manager and Subadviser in connection with those services, including maintaining and monitoring their own and the Fund’s compliance programs, liquidity management programs and cybersecurity programs, had expanded over time as a result of regulatory, market and other developments. The Board also noted that on a regular basis it received and reviewed information from the Manager and the Subadviser regarding the Fund’s compliance policies and procedures established pursuant to Rule 38a-1 under the 1940 Act, and took that information into account in its evaluation of the New Agreements. The Board also considered the risks associated with the Fund borne by the Manager and its affiliates (such as entrepreneurial, operational, reputational, litigation and regulatory risk), as well as the Manager’s and the Subadviser’s risk management processes.

The Board considered information provided by Franklin Templeton regarding its business and operating structure, scale of operation, leadership and reputation, distribution capabilities, and financial condition.

The Board also reviewed the qualifications, backgrounds and responsibilities of the Manager’s and the Subadviser’s senior personnel and the team of investment professionals primarily responsible for the day-to-day portfolio management of the Fund. The Board also considered the financial resources of Legg Mason and Franklin Templeton and the importance of having a Fund manager with, or with access to, significant organizational and financial resources. The Board considered the benefits to the Fund of being part of a larger

| | |

| Western Asset Premium Liquid Reserves | | 21 |

Board approval of new management and new subadvisory agreements (unaudited) (cont’d)

combined organization with greater financial resources following the Transaction, particularly during periods of market disruptions and volatility.

The Board also considered the policies and practices of the Manager and the Subadviser regarding the selection of brokers and dealers and the execution of portfolio transactions at the Master Fund level. In addition, the Board considered management’s periodic reports to the Board on, among other things, its business plans and any organizational changes.

The Board received and considered performance information for the Fund as well as for a group of funds (the “Performance Universe”) selected by Broadridge Financial Solutions, Inc. (“Broadridge”), an independent provider of investment company data, based on classifications provided by Thomson Reuters Lipper (“Lipper”). The Board was provided with a description of the methodology used to determine the similarity of the Fund with the funds included in the Performance Universe. It was noted that while the Board found the Broadridge data generally useful they recognized its limitations, including that the data may vary depending on the end date selected and that the results of the performance comparisons may vary depending on the selection of the peer group and its composition over time. The Board also noted that it had received and discussed with management information throughout the year at periodic intervals comparing the Fund’s performance against its benchmark and against the Fund’s peers. In addition, the Board considered the Fund’s performance in light of overall financial market conditions.

The information comparing the Fund’s performance to that of its Performance Universe, consisting of all funds (including the Fund) classified as institutional money market funds by Lipper, showed, among other data, that the Fund’s performance for the 1-, 3-, 5- and 10-year periods ended December 31, 2019 was below the median.

Based on their review of the materials provided and the assurances received from Franklin Templeton and Legg Mason, the Trustees determined that the Transaction was not expected to affect adversely the nature, extent and quality of services provided by each Adviser and that the Transaction was not expected to have an adverse effect on the ability of the Manager and Subadviser to provide those services, and the Board concluded that, overall, the nature, extent and quality of services expected to be provided, including performance, under the New Agreements were sufficient for approval.

Management fees and expense ratios

The Board considered that it had reviewed the Fund’s management fee and total expense ratio at the 2019 contract renewal meetings. The Board considered that the New Agreements would not change the Fund’s management fee rate or the computation method for calculating such fees, and that there is no present intention to alter expense waiver and reimbursement arrangements that are currently in effect.

| | |

| 22 | | Western Asset Premium Liquid Reserves |

The Board reviewed and considered the contractual management fee (the “Contractual Management Fee”) and the actual management fees paid by the Fund to the Manager (the “Actual Management Fee”) in light of the nature, extent and quality of the management and sub-advisory services to be provided by the Manager and the Subadviser. The Board noted that the Fund’s expense information reflected both management fees and total expenses payable by the Fund as well as management fees and total expenses payable by the Master Fund. The Board also considered that fee waiver and/or expense reimbursement arrangements are currently in place for the Fund. The Board also noted that the compensation paid to the Subadviser is the responsibility and expense of the Manager, not the Fund.

In addition, the Board received and considered information provided by Broadridge comparing the Contractual Management Fee and the Actual Management Fee and the Fund’s total actual expenses with those of funds in both the relevant expense group and a broader group of funds, each selected by Broadridge based on classifications provided by Lipper. It was noted that while the Board found the Broadridge data generally useful they recognized its limitations, including that the data may vary depending on the selection of the peer group. The Board also reviewed information regarding fees charged by the Manager and/or the Subadviser to other U.S. clients investing primarily in an asset class similar to that of the Fund, including, where applicable, separate accounts.

The Manager reviewed with the Board the differences in services provided to these different types of accounts, noting that the Fund is provided with certain administrative services, office facilities, and Fund officers (including the Fund’s chief executive, chief financial and chief compliance officers), and that the Manager coordinates and oversees the provision of services to the Fund by other Fund service providers. The Board considered the fee comparisons in light of the differences in management of these different types of accounts and the differences in associated risks borne by the Advisers.

The Board considered the management fee, the fees of the Subadviser and the amount of the management fee retained by the Manager after payment of the subadvisory fee in each case in light of the services rendered for those amounts. The Board also received an analysis of Legg Mason complex-wide management fees for funds with a similar strategy provided by the Manager, which, among other things, set out a framework of fees based on asset classes.

The information comparing the Fund’s Contractual and Actual Management Fees as well as its actual total expense ratio to its expense group, consisting of a group of money market funds (including the Fund) chosen by Broadridge to be comparable to the Fund, showed that the Fund’s Contractual Management Fee was higher than the median and Actual Management Fee was lower than the median. The Board noted that the Fund’s actual total

| | |

Western Asset Premium Liquid Reserves | | 23 |

Board approval of new management and new subadvisory agreements (unaudited) (cont’d)

expense ratio was equal to the median. The Board also considered that the current limitation on the Fund’s expenses is expected to continue through December 2020.

In evaluating the costs of the services to be provided by the Manager and Subadviser under the New Agreements, the Board considered, among other things, whether management fees or other expenses would change as a result of the Transaction. Based on their review of the materials provided and the assurances they had received from Franklin Templeton and Legg Mason, the Trustees determined that the Transaction would not increase the total fees payable by the Fund for management services.

Taking all of the above into consideration, as well as the factors identified below, the Board determined that the management fee and the subadvisory fee for the Fund were reasonable in light of the nature, extent and quality of the services to be provided to the Fund under the New Agreements.

Profitability and economies of scale

The Board received and considered an analysis of the profitability of the Manager and its affiliates in providing services to the Fund and in providing services to the Master Fund in which the Fund invests. The Board also received profitability information with respect to the Legg Mason fund complex as a whole. In addition, the Board received information with respect to the Manager’s allocation methodologies used in preparing this profitability data. It was noted that the allocation methodologies had been previously reviewed by an outside consultant. The profitability of the Manager and its affiliates was considered by the Board not excessive in light of the nature, extent and quality of the services provided to the Fund and the type of fund it represented.

The Board received and considered information concerning whether the Advisers realize economies of scale as the Fund’s assets grow. In conjunction with their most recent or prior deliberations concerning the Existing Agreements, the Board noted that contractual expense limitations had been implemented for the Fund, and that after taking those expense limitations into account, the Board had determined that the total fees for management services, and administrative services for the Fund, were reasonable in light of the services provided, and that any economies of scale were being shared appropriately.

The Board noted that Franklin Templeton and Legg Mason are expected to realize cost savings from the Transaction based on synergies of operations, as well as to benefit from possible growth of the Fund resulting from enhanced distribution capabilities. However, they noted that other factors could also affect profitability and potential economies of scale, and that it was not possible to predict with any degree of certainty how the Transaction would affect the Advisers’ profitability from their relationship with the Fund, nor to quantify at this time any possible future economies of scale. The Trustees noted they will

| | |

| 24 | | Western Asset Premium Liquid Reserves |

have the opportunity to periodically re-examine such profitability and any economies of scale going forward.

The Board determined that the management fee structure for the Fund was reasonable.

Other benefits to the Manager and the Subadviser

The Board considered other benefits received by the Manager, the Subadviser and their affiliates as a result of their relationship with the Fund, including the opportunity to offer additional products and services to Fund shareholders.

In light of the costs of providing investment management and other services to the Fund and the ongoing commitment of the Manager and the Subadviser to the Fund, the Board considered that the ancillary benefits that the Manager and its affiliates received are reasonable. In evaluating the fall-out benefits to be received by the Manager and Subadviser under the New Agreements, the Board considered whether the Transaction would have an impact on the fall-out benefits received by virtue of the Existing Agreements.

The Board considered that Franklin Templeton may derive reputational and other benefits from its ability to use the Legg Mason investment affiliates’ names in connection with operating and marketing the Fund. The Board also considered that the Transaction would significantly increase Franklin Templeton’s assets under management and expand Franklin Templeton’s investment capabilities.

| | |

| Western Asset Premium Liquid Reserves | | 25 |

Additional information (unaudited)

Information about Trustees and Officers

The business and affairs of Western Asset Premium Liquid Reserves (the “Fund”) are conducted by management under the supervision and subject to the direction of its Board of Trustees. The business address of each Trustee is c/o Jane Trust, Legg Mason, 100 International Drive, 11th Floor, Baltimore, Maryland 21202.

Previously, two different boards, the Legg Mason Partners Fixed Income Funds Board and the Western Asset Funds Board, oversaw substantially all the mutual funds within the Legg Mason fund complex that are advised by Western Asset Management Company, LLC†.A joint proxy statement was mailed to solicit shareholder approval for the election of a unified board. On December 3, 2019, a joint special meeting of shareholders of the funds was held to elect the unified board members. During this meeting, shareholders approved these nominees for Board membership — resulting in one Board overseeing these funds effective January 1, 2020.

Information pertaining to the Trustees and officers of the Board is set forth below. The Statement of Additional Information includes additional information about Trustees and is available, without charge, upon request by calling the Fund at 1-877-721-1926 or 1-203-703-6002.

| | |

| Independent Trustees†† |

|

| Robert Abeles, Jr. |

| |

| Year of birth | | 1945 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 2013 |

| Principal occupation(s) during the past five years | | Board Member, Great Public Schools Now (since 2018); Senior Vice President Emeritus (since 2016) and formerly, Senior Vice President, Finance and Chief Financial Officer (2009 to 2016) at University of Southern California; Board Member, Excellent Education Development (since 2012) |

| Number of funds in fund complex overseen by Trustee3 | | 57 |

| Other Trusteeships held by Trustee during the past five years | | None |

|

| Jane F. Dasher |

| |

| Year of birth | | 1949 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 1999 |

| Principal occupation(s) during the past five years | | Chief Financial Officer, Long Light Capital, LLC, formerly known as Korsant Partners, LLC (a family investment company) (since 1997) |

| Number of funds in fund complex overseen by Trustee3 | | 57 |

| Other Trusteeships held by Trustee during the past five years | | Director, Visual Kinematics, Inc. (since 2018) |

| | |

| 26 | | Western Asset Premium Liquid Reserves |

| | |

| Independent Trustees†† (cont’d) |

|

| Anita L. DeFrantz |

| |

| Year of birth | | 1952 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 1998 |

| Principal occupation(s) during the past five years | | President of Tubman Truth Corp. (since 2015); President Emeritus (since 2015) and formerly, President (1987 to 2015) and Director (1990 to 2015) of LA84 (formerly Amateur Athletic Foundation of Los Angeles); Member (since 1986), Member of the Executive Board (since 2013) and Vice President (since 2017) of the International Olympic Committee |

| Number of funds in fund complex overseen by Trustee3 | | 57 |

| Other Trusteeships held by Trustee during the past five years | | None |

|

| Susan B. Kerley |

| |

| Year of birth | | 1951 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 1992 |

| Principal occupation(s) during the past five years | | Investment Consulting Partner, Strategic Management Advisors, LLC (investment consulting) (since 1990) |

| Number of funds in fund complex overseen by Trustee3 | | 57 |

| Other Trusteeships held by Trustee during the past five years | | Director and Trustee (since 1990) and Chairman (since 2017 and 2005 to 2012) of various series of MainStay Family of Funds (66 funds); formerly, Investment Company Institute (ICI) Board of Governors (2006 to 2014); ICI Executive Committee (2011 to 2014); Chairman of the Independent Directors Council (2012 to 2014) |

|

| Michael Larson* |

| |

| Year of birth | | 1959 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 2004 |

| Principal occupation(s) during the past five years | | Chief Investment Officer for William H. Gates III (since 1994)4 |

| Number of funds in fund complex overseen by Trustee3 | | 57 |

| Other Trusteeships held by Trustee during the past five years | | Republic Services, Inc. (since 2009); Fomento Economico Mexicano, SAB (since 2011); Ecolab Inc. (since 2012); formerly, AutoNation, Inc. (2010 to 2018) |

| | |

| Western Asset Premium Liquid Reserves | | 27 |

Additional information (unaudited) (cont’d)

Information about Trustees and Officers

| | |

| Independent Trustees†† (cont’d) |

|

| Avedick B. Poladian |

| |

| Year of birth | | 1951 |

| Position(s) with Fund | | Trustee |

| Term of office1 and length of time served2 | | Since 2007 |