July 14, 2014 Allergan Further Thoughts On Potential Business Risks And Issues With Valeant Pharmaceuticals International, Inc. Exhibit 99.1 |

Important Information Information contained in this presentation regarding Valeant Pharmaceuticals International, Inc. (“Valeant”) is taken directly from the information publicly disclosed by Valeant and we do not make any representations or warranties, either express or implied, with respect to such information’s accuracy or completeness. In addition, certain other information contained in this presentation is based on publicly available sources as of the date of this presentation, and while we have no reason to believe that such information is not accurate, we can provide no such assurances with respect thereto. IMS data used in this presentation has been purchased from IMS Health, a provider of healthcare information. This presentation was prepared with the assistance of Allergan’s independent financial consultants and forensic accountants, Alvarez & Marsal and FTI Consulting. The information in this presentation represents the opinions of Allergan and investors and stockholders should make their own independent investigations of the matters referenced in this presentation and draw their own conclusions. 2 |

Review of Valeant’s Insufficient Disclosures and Unsupported Assertions 3 Valeant claims to have refuted numerous concerns about its business model, “organic” sales growth and financial reporting by providing responses on June 17, 2014 and June 23, 2014. Moreover, Valeant has recognized that its current disclosures lack transparency and has committed to improving its disclosures. Allergan believes such improved disclosures are important, and we expect those additional disclosures will confirm the concerns we have raised with respect to Valeant’s business model. The following slides highlight — In reviewing Valeant’s responses, there are many assertions, but limited underlying facts and supporting data. — Valeant’s commitments on improved financial disclosures on its Q2 2014 earnings call / press release — Valeant’s responses to several assertions are not based in fact nor supported by data — Valeant’s inconsistencies in prior statements — Valeant’s stated “organic” sales growth as compared to its actual business performance — Given Valeant’s opaque disclosures, our analysis is based on highly reputable and reliable publicly available information, which is commonly accepted and used in the healthcare industry |

“I think the one thing we'll probably start doing is disclosing our top 10 products, our top 15 products and how we're doing. ” “I think the other thing we will probably start doing again is price volume… we will report…the volume and price parts of our organic growth.” “Our financial statements will actually begin to really demonstrate that our one-time costs are really one-time costs. And that you'll begin to see that [reflected in] GAAP and non-GAAP, EPS and organic growth.” “I think what we will continue to do, at least throughout this year, is continue to report the organic growth in terms of how [B&L is] doing. And — which has been double digit, continues to be double digit and my guess is may actually increase as the year goes through given how well that business is doing. And then we'll decide in 2015 whether we continue that or not. ” Valeant has Promised More Transparency in Financial Disclosures 4 Statements Made by Valeant’s Management (Michael Pearson, June 17, 2014) Expected Additional Disclosures on Valeant’s Q2 Earnings Call/Press Release Full list and respective performance of the top 15 products (both $ and % growth) Organic growth by segment bifurcated into contribution from both the price and volume components Convergence in GAAP and Non-GAAP EPS and organic growth as acquisition activity scales down on a relative basis (to past history) Organic growth metrics for Bausch & Lomb business (both $ and % growth) Segment reporting that provides detail by business lines, not merely “developed markets” and “emerging markets” Define products that are included in each business line For categories such as ‘Bausch & Lomb performance’, Valeant should define products included and confirm that there have been no changes in the definition of the category and that no products have been added or excluded from the category from quarter to quarter All business units should be listed and defined and there should be consistency in reporting quarter over quarter — Include current and historic periods for comparison — For example, in the Q1 2014 earnings presentation, Valeant highlighted selected ‘top performing business units’, such as U.S. Dermatology, U.S. Contact Lens, U.S. Ophthalmology Rx, U.S. Neuro & Other, U.S. Consumer, Asia (ex. Japan), Western Europe and Brazil/Argentina. Valeant should disclose all business units, not only the ‘top performing’ — Previous quarterly presentations cherry-picked other completely different ‘top performing business units’ (such as Aesthetics, Russia, Canada, Poland and Oral Health) |

Valeant’s Responses to Many of Allergan’s Concerns Were Not Substantiated with Transparent Supporting Data 5 Allergan Statement (June 10, 2014) Corresponding Valeant Response (June 23, 2014 except as noted) Substantiated by Supporting Data? “Subscale Valeant products losing their market share” “Many products are category leaders in terms of market share or growth, both in the U.S. and abroad (e.g., Ocuvite, Elidel, Preservision, Duromine, Solodyn, Acanya, Renu, Biotrue Solutions, Bioscard, CeraVe, Difflam, Duro-Tuss, Probiotica), (products in bold growing market share)” NO “Decline in market share, competitiveness and product viability” “Our key products in dermatology, ophthalmology Rx, contact lenses, surgical, consumer, oral health, and generics in the U.S. are growing and gaining market share” NO “Lower tax regime with questionable sustainability” “Given we are an established Canadian company, with an established corporate structure we consider our tax regime sustainable and believe that we have a substantial tax advantage over Allergan” NO “Valeant has experienced volume decreases in 11 of its top 15 worldwide pharmaceutical products” “13 of Valeant’s top 15 products are growing overall, with 9 of the top 15 products growing by volume” NO “Lack of investment will put Allergan’s core business at risk under Valeant ownership” “R&D expenditure will be sufficient to maintain existing products, advance promising late stage programs, extend the Botox franchise, and support other line extensions” NO “Allergan’s Performance Enhancement Plan has also reduced Valeant’s originally stated synergies” “We have a detailed bottoms-up understanding of Allergan synergies. Actually in the interest of time and I know we have run over, each of our presenters today had their bottoms-up plan in terms of how they would achieve the synergies in their geographies and therapeutic areas. So again, we didn't treat it like one top-down analysis, it is 50 bottoms-up analysis of what we would do if we got Allergan and we feel very, very comfortable that we will achieve the synergies that we have set out.” - May 28, 2014 NO |

Valeant’s Statements are Inconsistent & Demonstrate a Lack of Ability to Forecast its Business 6 Inability to forecast branded drug sales – Solodyn® (one of Valeant’s Top 5 Products): Inability to forecast generic deterioration: — 9/4/2012 – Chairman, CEO Michael Pearson on Valeant conference call to discuss acquisition of Medicis: “In terms of our assumptions around Solodyn, we were actually very, very conservative in our model” — 1/4/2013 – CFO Howard Schiller on Valeant 2013 Financial Guidance conference call: “We are also projecting Solodyn sales of $250 million to $275 million in 2013, and we believe this is a conservative assumption” — 1/4/2013 – Chairman, CEO Michael Pearson on Valeant 2013 Financial Guidance conference call: “In terms of Solodyn... As Howard mentioned, we would hope to beat those numbers” — 8/7/2013 – Chairman, CEO Michael Pearson on Valeant 2Q13 Earnings conference call: “Solodyn is an important product for us… it’s a lot of money for us. It’s [probably our largest] product, so we're not going to be backing off on Solodyn, and in fact, the recent trends are positive.” — 10/31/2013 – Chairman, CEO Michael Pearson on Valeant 3Q13 Earnings conference call: “Solodyn, while seeing some erosion this year, appears to have stabilized at roughly $200 million on an annualized level…as Howard mentioned, the aesthetics business was the piece of [Medicis] that we were most excited about” — 8/7/2013 – CFO Howard Schiller on Valeant 2Q13 Earnings conference call: “In addition to the benefits of diversification, we have a very small percentage of our sales exposed to patent loss…” — 10/31/2013 – Chairman, CEO Michael Pearson on Valeant 3Q13 Earnings conference call: “…we were impacted by generic competition for Zovirax, Retin-A Micro and a number of other brands” — 10/31/2013 – CFO Howard Schiller on Valeant 3Q13 Earnings conference call: “Yes. In terms of the organic growth, obviously if you include those generics it's negative and your calculations are roughly correct” |

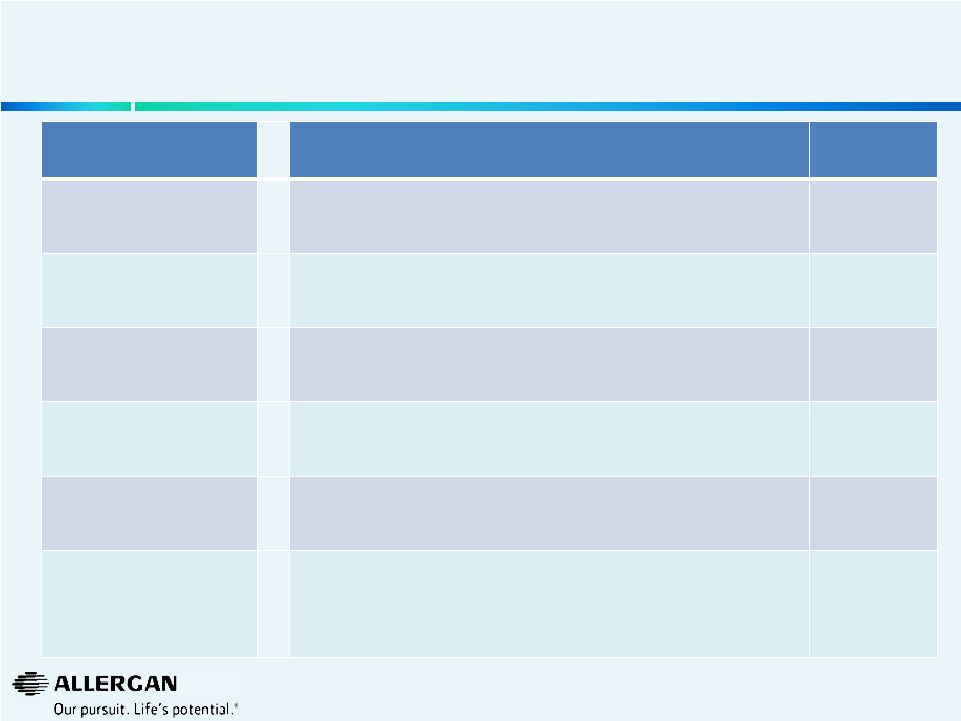

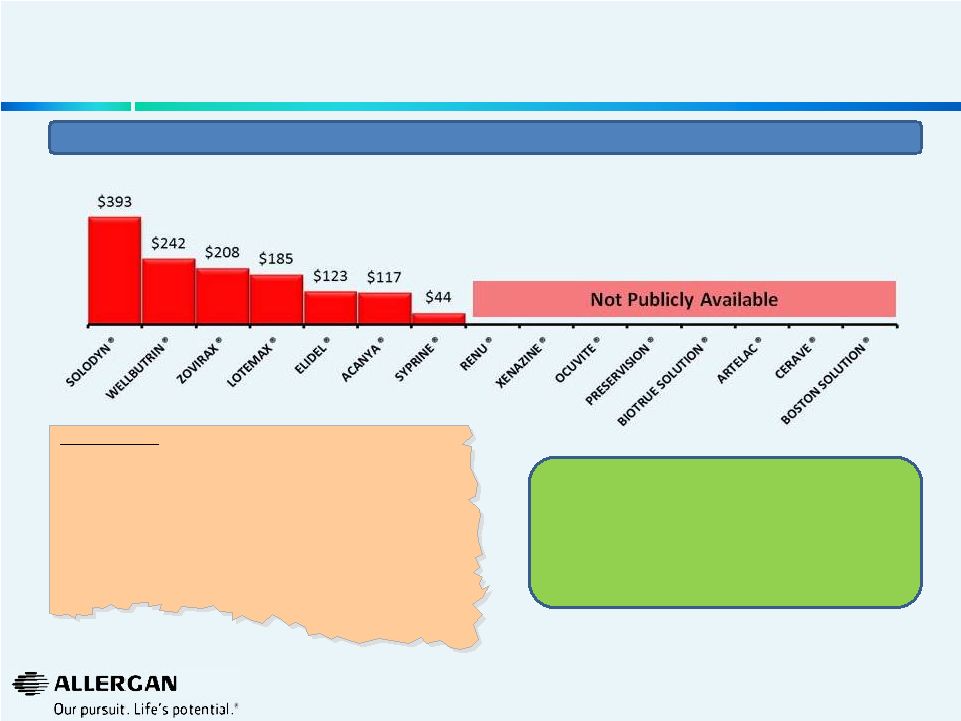

Valeant has Promised More Transparency in Financial Disclosures 7 Valeant “Fact” : “13 of the top 15 Valeant products are growing: Wellbutrin XL, Renu, Solodyn, Xenazine, Ocuvite, Preservision, Lotemax Gel, Elidel, BioTrue Solution, Artelac, CeraVe, Syprine, and Acanya Valeant “Fact Sheet” – 06/23/14 Allergan welcomes Valeant’s promise to disclose sales for their Top 15 products and related product performance (volume and price increases) during the upcoming Q2 2014 earnings release and thereafter. Valeant’s Stated Top 15 Products Q1 2014 MAT IMS Sales $’s (MM) for Top 15 products based on publicly available data* * Data represents global values triangulated based on various IMS data sources - IMS Knowledge Link & IMS FIRST. MAT is moving annual total. • 9 of the 15 are growing by volume: Renu, Xenazine, Ocuvite, Preservision, Lotemax Gel, Elidel, BioTrue Solutions, Artelac, CeraVe • Two products that are not growing are Zovirax (impacted by generic competition) and Boston Solution (~-2% growth)” |

Valeant’s View of “Fast Growing” Therapeutic Areas For Bausch & Lomb Is Inconsistent With Reality 8 (1) Per Valeant Investor Presentation triangulated with IMS First. (2) Per IMS First 2013 Eye Care including Retina at actual rates. (3) Per IMS First CLCP (S1L) and industry experts. “We pick markets, geographies and therapeutic areas that are growing faster than average. That way if we are just averaging those, we will grow above average.” — Michael Pearson, 05/28/14 Valeant Investor Meeting Losing share in IOL’s Losing share in Lenses Losing share in Pharmaceuticals (4) Weighted average of J&J Vision Care Growth, Alcon /Novartis & Cooper Contact Lens growth all per respective companies SEC filings / industry experts. (5) Per industry experts. (6) Per IMS First EyeCare Surgical and industry experts. Estimated How can Valeant claim that the Bausch & Lomb business is growing double-digits? Allergan looks forward to Valeant disclosing Bausch & Lomb’s true business performance (sales by segment, market share, price & volume). “I think what we will continue to do, at least throughout this year, is continue to report the organic growth in terms of how [B&L is] doing. And — which has been double digit, continues to be double digit and my guess is may actually increase as the year goes through given how well that business is doing.” — Michael Pearson, 06/17/14 B&L Product Mix (2013) (1) Market Growth Weighted Average Pharmaceuticals 42.0% 9.0% 4% Contact Lens Care 16.0% (2.0%) (0%) Contact Lenses 24.0% 1.8% 0% Refractive 3.0% (4.0%) (0%) Cataract & Vitreoretinal 15.0% 5.0% 1% B&L Estimated Growth At Constant Share 5% (2) (3) (4) (5) (6) Appears to be: |

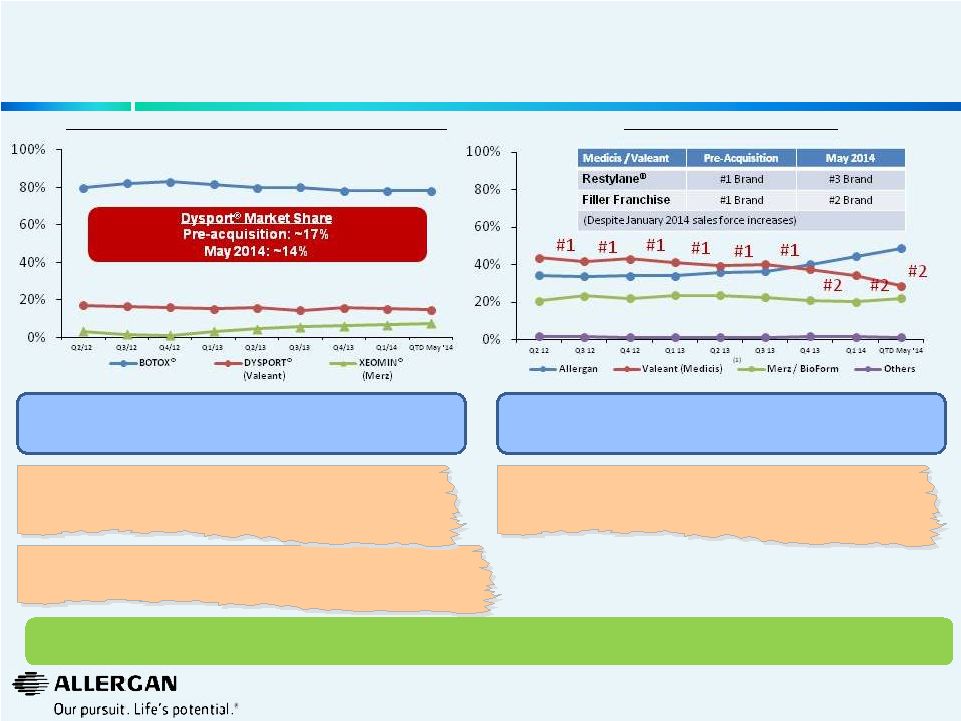

9 Medicis Performance Has Deteriorated Post Valeant Acquisition U.S. Aesthetic Neuromodulator Unit Market Share U.S. Filler Unit Market Share Source: Guidepoint Global (historical figures Q1’14 and prior based upon the March 2014 panel). QTD May 2014 figures based on May 2014 panel. Filler Unit share based on core injectors (dermatologists and plastic surgeons). (1) Includes all Valeant (Medicis) fillers, including the Restylane® brand. Permission to use quotes was neither sought nor received. Rapid erosion of purported “durable” Medicis’ business following acquisition & implementation of Valeant business model. Allergan’s franchises significantly at risk if under Valeant’s ownership. “I sincerely believe that the merger of Allergan and Valeant will significantly impair thecompetitive landscape in both medicaland aesthetic dermatology…” - Amy Forman Taub, M.D., Medical Director, Founder; Advanced Dermatology/skinfo; Assistant Clinical Professor, Northwestern University; Medical School, Department of Dermatology “Shock and dismay where the emotions that I felt when I heard the possibility of your company being acquired... This action would clearly result in a decrease in quality of your company. Please do not let this happen! …We trust Allergan. What would be the state of our medical disciplines had it not been for the innovations of your company?” - Carlos Burnett, M.D., FACS, Burnett Plastic Surgery, PC “Aesthetics, it's been a very nice business in the United States for us over – since we bought it from Medicis and we've continued to add products and grow that out. We grew that business over 30% organically this year” - Michael Pearson, Jan 7, 2014 Allergan’s customers (physicians) believe the proposed transaction by Valeant will destroy Allergan’s competitiveness Valeant’s growth assertions on its aesthetics franchise are not reflected in true results. If the business was performing so well, why did Valeant need to sell it? |

Conclusion 10 Allergan Board of Directors has unanimously rejected Valeant’s unsolicited exchange offer Allergan Board of Directors has determined Valeant’s offer is grossly inadequate, substantially undervalues Allergan and creates significant risks and uncertainties for Allergan stockholders Allergan stockholders have nothing to “gain” by merging with Valeant Allergan management and Board of Directors are committed to delivering the highest value for Allergan stockholders |

Important Information Allergan, its directors and certain of its officers and employees are participants in solicitations of Allergan stockholders. Information regarding the names of Allergan's directors and executive officers and their respective interests in Allergan by security holdings or otherwise is set forth in Allergan's proxy statement for its 2014 annual meeting of stockholders, filed with the SEC on March 26, 2014, as supplemented by the proxy information filed with the SEC on April 22, 2014. Additional information can be found in Allergan's Annual Report on Form 10-K for the year ended December 31, 2013, filed with the SEC on February 25, 2014 and its Quarterly Report on Form 10-Q for the quarter ended March 31, 2014, filed with the SEC on May 7, 2014. To the extent holdings of Allergan's securities have changed since the amounts printed in the proxy statement for the 2014 annual meeting of stockholders, such changes have been reflected on Initial Statements of Beneficial Ownership on Form 3 or Statements of Change in Ownership on Form 4 filed with the SEC. These documents are available free of charge at the SEC’s website at www.sec.gov. STOCKHOLDERS ARE ENCOURAGED TO READ ANY ALLERGAN SOLICITATION STATEMENT (INCLUDING ANY SUPPLEMENTS THERETO) AND ANY OTHER RELEVANT DOCUMENTS THAT ALLERGAN MAY FILE WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Stockholders will be able to obtain, free of charge, copies of any solicitation statement and any other documents filed by Allergan with the SEC at the SEC's website at www.sec.gov. In addition, copies will also be available at no charge at the Investors section of Allergan's website at www.allergan.com. 11 |

July 14, 2014 Allergan Further Thoughts On Potential Business Risks And Issues With Valeant Pharmaceuticals International, Inc. |