| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-172366-06 | ||

|  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,231,492,115

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

$1,018,342,000

(Approximate Aggregate Principal Balance of Offered Certificates)

WFRBS Commercial Mortgage Trust 2013-C12

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

The Royal Bank of Scotland

Wells Fargo Bank, National Association

Liberty Island Group I LLC

C-III Commercial Mortgage LLC

Basis Real Estate Capital II, LLC

NCB, FSB

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2013-C12

February 22, 2013

| WELLS FARGO SECURITIES | RBS | |||

| Co-Lead Manager and | Co-Lead Manager and | |||

| Co-Bookrunner | Co-Bookrunner | |||

Deutsche Bank Securities

Co-Manager

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-172366) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any other jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC (“WFS”), RBS Securities Inc. (“RBSSI”), Deutsche Bank Securities Inc. or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for certain capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including Wells Fargo Securities, LLC, member FINRA and SIPC, and Wells Fargo Bank, National Association.

RBS is a trade name for the investment banking business of RBSSI. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by RBSSI and their securities affiliates. Lending, derivatives and other commercial banking activities are performed by The Royal Bank of Scotland plc and their banking affiliates. RBSSI is a member of SIPC, FINRA and the NYSE.

IRS CIRCULAR 230 NOTICE

THIS TERM SHEET IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. THIS TERM SHEET IS WRITTEN AND PROVIDED BY THE DEPOSITOR IN CONNECTION WITH THE PROMOTION OR MARKETING BY THE DEPOSITOR AND THE CO-LEAD BOOKRUNNING MANAGERS OF THE TRANSACTION OR MATTERS ADDRESSED HEREIN. INVESTORS SHOULD SEEK ADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. Prospective investors should understand that, when considering the purchase of the Offered Certificates, a contract of sale will come into being no sooner than the date on which the relevant class of certificates has been priced and the underwriters have confirmed the allocation of certificates to be made to investors; any “indications of interest” expressed by any prospective investor, and any “soft circles” generated by the underwriters, will not create binding contractual obligations for such prospective investors, on the one hand, or the underwriters, the depositor or any of their respective agents or affiliates, on the other hand.

As a result of the foregoing, a prospective investor may commit to purchase certificates that have characteristics that may change, and each prospective investor is advised that all or a portion of the certificates referred to in these materials may be issued without all or certain of the characteristics described in these materials. The underwriters’ obligation to sell certificates to any prospective investor is conditioned on the certificates and the transaction having the characteristics described in these materials. If the underwriters determine that a condition is not satisfied in any material respect, such prospective investor will be notified, and neither the depositor nor the underwriters will have any obligation to such prospective investor to deliver any portion of the Offered Certificates which such prospective investor has committed to purchase, and there will be no liability between the underwriters, the depositor or any of their respective agents or affiliates, on the one hand, and such prospective investor, on the other hand, as a consequence of the non-delivery.

Each prospective investor has requested that the underwriters provide to such prospective investor information in connection with such prospective investor’s consideration of the purchase of the certificates described in these materials. These materials are being provided to each prospective investor for informative purposes only in response to such prospective investor’s specific request. The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| WFRBS Commercial Mortgage Trust 2013-C12 | Certificate Structure |

I. Certificate Structure

Expected Ratings (Fitch/KBRA/S&P)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approx. Initial Credit Support(3) | Pass- Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | |||

| Offered Certificates | ||||||||||

| A-1 | AAA(sf)/AAA(sf)/AAA(sf) | $63,911,000 | 30.000% | (7) | 2.67 | 04/13 – 01/18 | 35.0% | 17.7% | ||

| A-2 | AAA(sf)/AAA(sf)/AAA(sf) | $142,980,000 | 30.000% | (7) | 4.87 | 01/18 – 03/18 | 35.0% | 17.7% | ||

| A-3 | AAA(sf)/AAA(sf)/AAA(sf) | $165,000,000 | 30.000% | (7) | 9.55 | 04/21 – 01/23 | 35.0% | 17.7% | ||

| A-4 | AAA(sf)/AAA(sf)/AAA(sf) | $298,198,000 | 30.000% | (7) | 9.92 | 01/23 – 03/23 | 35.0% | 17.7% | ||

| A-SB | AAA(sf)/AAA(sf)/AAA(sf) | $101,955,000 | 30.000% | (7) | 7.40 | 03/18 – 12/22 | 35.0% | 17.7% | ||

| A-S | AAA(sf)/AAA(sf)/AAA(sf) | $120,070,000 | 20.250% | (7) | 9.99 | 03/23 – 03/23 | 39.9% | 15.5% | ||

| B | AA-(sf)/AA-(sf)/AA-(sf) | $75,429,000 | 14.125% | (7) | 9.99 | 03/23 – 03/23 | 43.0% | 14.4% | ||

| C | A-(sf)/A-(sf)/A-(sf) | $50,799,000 | 10.000% | (7) | 9.99 | 03/23 – 03/23 | 45.1% | 13.8% | ||

| Non-Offered Certificates | ||||||||||

| X-A | AAA(sf)/AAA(sf)/AAA(sf) | $982,114,000(8) | N/A | Variable(9) | N/A | N/A | N/A | N/A | ||

| X-B | A-(sf)/AAA(sf)/A-(sf) | $126,228,000(10) | N/A | Variable(11) | N/A | N/A | N/A | N/A | ||

| X-C | NR/NR/NR | $81,587,114(12) | N/A | Variable(13) | N/A | N/A | N/A | N/A | ||

A-3FL(14) | AAA(sf)/AAA(sf)/AAA(sf)(15) | $90,000,000(14) | 30.000% | Libor Plus(16) | 9.55 | 04/21 – 01/23 | 35.0% | 17.7% | ||

A-3FX(14) | AAA(sf)/AAA(sf)/AAA(sf) | $0 (14) | 30.000% | (7) | 9.55 | 04/21 – 01/23 | 35.0% | 17.7% | ||

| D | BBB-(sf)/BBB-(sf)/BBB-(sf) | $41,563,000 | 6.625% | (7) | 9.99 | 03/23 – 03/23 | 46.8% | 13.3% | ||

| E | BB(sf)/BB(sf)/BB(sf) | $27,709,000 | 4.375% | (7) | 9.99 | 03/23 – 03/23 | 47.9% | 12.9% | ||

| F | B(sf)/B(sf)/B+(sf) | $16,933,000 | 3.000% | (7) | 9.99 | 03/23 – 03/23 | 48.6% | 12.8% | ||

| G | NR/NR/NR | $36,945,114 | 0.000% | (7) | 9.99 | 03/23 – 03/23 | 50.1% | 12.4% | ||

Notes:

| (1) | The expected ratings presented are those of Fitch, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”) and Standard & Poor’s Ratings Services (“S&P”) which the depositor hired to rate the rated offered certificates. One or more other nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise, to rate or provide market reports and/or published commentary related to the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the offered certificates. See “Risk Factors—Risks Related to the Offered Certificates—Risks Related to the Offered Certificates – Ratings on the Certificates Have Substantial Limitations and Ratings” in the free writing prospectus, dated February 22, 2013 (the “Free Writing Prospectus”). |

| (2) | The principal balances and notional amounts set forth in the table are approximate. The actual initial principal balances and notional amounts may be larger or smaller depending on the aggregate cut-off date principal balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date principal balance may be as much as 5% larger or smaller than the amount presented in the Free Writing Prospectus. |

| (3) | The approximate initial credit support with respect to the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates in the aggregate. No class of Certificates will provide any credit support to the Class A-3FL Certificates for any failure by the swap counterparty to make the payment under the related swap contract. |

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described on Annex B to the Free Writing Prospectus. |

| (5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates) is calculated by dividing the aggregate principal balance of such class of certificates and all classes of certificates senior to such class by the aggregate appraised value of $2,459,509,212 (calculated as described in the Free Writing Prospectus) of the mortgaged properties securing the mortgage loans (excluding, with respect to the One South Wacker Drive loan combination, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). The Certificate Principal to Value Ratios for each of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates are calculated by dividing the aggregate principal balance of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates by such aggregate appraised value (excluding, with respect to the One South Wacker Drive loan combination, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). However, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). |

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates) is calculated by dividing the underwritten net operating income (which excludes, with respect to the One South Wacker Drive loan combination, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) for the mortgage pool of $152,398,895 (calculated as described in the Free Writing Prospectus) by the aggregate certificate balance of such class of certificates and all classes of certificates senior to such class of certificates. The Underwritten NOI Debt Yield for each of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates is calculated by dividing such mortgage pool underwritten net operating income (which excludes, with respect to the One South Wacker Drive loan combination, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) by the aggregate principal balance of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4 and A-SB Certificates. However, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). |

| (7) | The pass-through rates for the Class A-1, A-2, A-3, A-3FX, A-4, A-SB, A-S, B, C, D, E, F and G Certificates and the Class A-3FX Regular Interest in each case will be one of the following: (i) a fixed rate per annum, (ii) the WAC Rate (as defined in the Free Writing Prospectus) for the related distribution date, (iii) a variable rate per annum equal to the lesser of (a) a fixed rate and (b) the WAC Rate for the related distribution date or (iv) a variable rate per annum equal to the WAC Rate for the related distribution date minus a specified percentage. |

| (8) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate principal balance of the Class A-1, A-2, A-3, A-4, A-SB and A-S Certificates and the Class A-3FX Regular Interest outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. |

| (9) | The pass-through rate for the Class X-A Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2, A-3, A-4, A-SB and A-S Certificates and the Class A-3FX Regular Interest for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| WFRBS Commercial Mortgage Trust 2013-C12 | Certificate Structure |

| (10) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the aggregate principal balance of the Class B and C Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. |

| (11) | The pass-through rate for the Class X-B Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class B and C Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. |

| (12) | The Class X-C Certificates are notional amount certificates. The Notional Amount of the Class X-C Certificates will be equal to the aggregate principal balance of the Class E, F and G Certificates outstanding from time to time. The Class X-C Certificates will not be entitled to distributions of principal. |

| (13) | The pass-through rate for the Class X-C Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class E, F and G Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. |

| (14) | The Class A-3FL Certificates will evidence a beneficial interest in a grantor trust that includes the Class A-3FX Regular Interest and an interest rate swap contract. Under certain circumstances, holders of the Class A-3FL Certificates may exchange all or a portion of their certificates for a like principal amount of Class A-3FX Certificates having the same pass-through rate as the Class A-3FX Regular Interest. The aggregate principal balance of the Class A-3FL Certificates may be adjusted from time to time as a result of such an exchange. The aggregate principal balance of the Class A-3FX Certificates and Class A-3FL Certificates will at all times equal the principal balance of the Class A-3FX Regular Interest. The principal balance of the Class A-3FX Certificates will initially be $0. |

| (15) | The ratings assigned to the Class A-3FL Certificates reflect only the receipt of up to the fixed rate of interest at a rate equal to the applicable pass-through rate for the Class A-3FX Regular Interest. The ratings of Fitch, KBRA and S&P do not address any shortfalls or delays in payments that investors in the Class A-3FL Certificates may experience as a result of the conversion of the pass-through Certificates from a floating interest rate to a fixed rate. |

| (16) | The pass-through rate on the Class A-3FL Certificates will be a per annum rate equal to LIBOR plus a specified percentage; provided, however, that under certain circumstances, the pass-through rate on the Class A-3FL Certificates may convert to the pass-through rate applicable to the Class A-3FX Regular Interest. The initial LIBOR rate will be determined two LIBOR Business Days prior to the Closing Date, and subsequent LIBOR rates for the Class A-3FL Certificates will be determined two LIBOR Business Days before the start of the related interest accrual period. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| WFRBS Commercial Mortgage Trust 2013-C12 | Issue Characteristics |

II. Transaction Highlights

Mortgage Loan Sellers:

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Cut-off Date Pool Balance | ||||||

The Royal Bank of Scotland(1) | 18 | 38 | $551,861,106 | 44.8 | % | |||||

| Wells Fargo Bank, National Association | 28 | 34 | 392,593,464 | 31.9 | ||||||

| Liberty Island Group I LLC | 11 | 11 | 93,211,515 | 7.6 | ||||||

| C-III Commercial Mortgage LLC | 14 | 15 | 80,772,384 | 6.6 | ||||||

| Basis Real Estate Capital II, LLC | 6 | 17 | 57,645,471 | 4.7 | ||||||

NCB, FSB | 23 | 23 | 55,408,173 | 4.5 | ||||||

| Total | 100 | 138 | $1,231,492,115 | 100.0 | % | |||||

(1) The mortgage loan seller referred to herein as The Royal Bank of Scotland is comprised of two affiliated companies: The Royal Bank of Scotland plc and RBS Financial Products Inc. With respect to the mortgage loans being sold for the deposit into the trust by The Royal Bank of Scotland: (a) fifteen (15) of the mortgage loans, having an aggregate cut-off date principal balance of $510,282,589 and representing approximately 41.4% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, were originated by and are being sold to the trust only by The Royal Bank of Scotland plc and (b) three (3) of the mortgage loans, having a cut-off date principal balance of $41,578,518 and representing approximately 3.4% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date were originated by RBS Financial Products Inc. and are being sold to the trust by RBS Financial Products Inc.

Loan Pool:

| Cut-off Date Balance: | $1,231,492,115 |

| Number of Mortgage Loans: | 100 |

| Average Cut-off Date Balance per Mortgage Loan: | $12,314,921 |

| Number of Mortgaged Properties: | 138 |

Average Cut-off Date Balance per Mortgaged Property(1): | $8,923,856 |

| Weighted Average Mortgage Interest Rate: | 4.394% |

| Ten Largest Mortgage Loans as % of Cut-off Date Pool Balance: | 52.5% |

| Weighted Average Original Term to Maturity or ARD (months): | 113 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 111 |

Weighted Average Original Amortization Term (months)(2): | 344 |

Weighted Average Remaining Amortization Term (months)(2): | 342 |

| Weighted Average Seasoning (months): | 2 |

(1) Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. With respect to One South Wacker Drive, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan unless otherwise stated.

(2) Excludes any mortgage loan that does not amortize.

Credit Statistics:

Weighted Average U/W Net Cash Flow DSCR(1): | 2.05x |

Weighted Average U/W Net Operating Income Debt Yield Ratio(1): | 12.4% |

Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 61.8% |

Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 53.5% |

% of Mortgage Loans with Additional Subordinate Debt(2): | 2.8% |

% of Mortgage Loans with Single Tenants(3): | 22.8% |

(1) With respect to One South Wacker Drive, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan unless otherwise stated. The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. Information for residential cooperative mortgage loans is calculated using underwritten net cash flow for the related residential cooperative property which is the projected net cash flow reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the loan-to value ratio information for residential cooperative mortgage loans is based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative. See Annex A-1 to the Free Writing Prospectus. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan.

(2) Fifteen (15) of the mortgage loans, each of which are secured by residential cooperative properties, currently have in place subordinate secured lines of credit to the related mortgage borrowers that permit future advances (such loans, collectively, the “Subordinate Coop LOCs”). In addition, one (1) of the mortgage loans, secured by a residential cooperative property known as Plaza West Cooperative Association, Inc., has two (2) corresponding subordinate secured mortgages (collectively, the “Plaza West Subordinate Mortgages”, and, together with the Subordinate Coop LOCs, collectively, the “Subordinate Secured Coop Loans”), neither of which are lines of credit. The Subordinate Secured Coop Loans are not included in the trust. As of February 15, 2013 the aggregate outstanding principal balance of the Subordinate Coop LOCs is $2,772,500. As of December 12, 2012 the aggregate outstanding principal balance of the Plaza West Subordinate Mortgages is $130,347. If fully drawn, the maximum aggregate principal balance of the Subordinate Coop LOCs is $8,950,000. The maximum principal amount of indebtedness available under the Subordinate Coop LOCs ranges between $100,000 and $2,500,000, and the average of such maximum principal amounts is $596,667. The percentage figure expressed as “% of Mortgage loans with Additional Subordinate Debt” does not take into account future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the Pooling and Servicing Agreement. See “Description of the Mortgage Pool—Subordinate and/or Other Financing” and “—Additional Debt Financing for Mortgage Loans Secured by Residential Cooperatives” in the Free Writing Prospectus.

(3) Excludes mortgage loans that are secured by multiple single tenant properties.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| WFRBS Commercial Mortgage Trust 2013-C12 | Issue Characteristics |

Loan Structural Features:

Amortization: Based on the Cut-off Date Pool Balance, 73.1% of the mortgage pool (91 mortgage loans) has scheduled amortization, as follows:

44.4% (82 mortgage loans) requires amortization during the entire loan term

28.7% (9 mortgage loans) provides for an interest-only period followed by an amortization period

Interest-Only: Based on the Cut-off Date Pool Balance, 26.9% of the mortgage pool (9 mortgage loans) provides for interest-only payments during the entire loan term. The Weighted Average Cut-off Date Loan-to-Value Ratio and Weighted Average U/W Net Cash Flow DSCR for those mortgage loans is 60.0% and 2.65x, respectively.

Hard Lockboxes: Based on the Cut-off Date Pool Balance, 50.7% of the mortgage pool (25 mortgage loans) has hard lockboxes in place.

Reserves: The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 73.2% of the pool |

| Insurance Premiums: | 49.4% of the pool |

| Capital Replacements: | 48.7% of the pool |

| TI/LC: | 51.3% of the pool(1) |

(1) The percentage of Cut-off Date Balance for loans with TI/LC reserves is based on the aggregate principal balance allocable to office, retail, mixed use and industrial properties. | |

Call Protection/Defeasance: Based on the Cut-off Date Pool Balance, the mortgage pool has the following call protection and defeasance features:

65.2% of the mortgage pool (63 mortgage loans) features a lockout period, then defeasance only until an open period

30.3% of the mortgage pool (14 mortgage loans) features a lockout period, then the greater of a prepayment premium or yield maintenance until an open period

4.5% of the mortgage pool (23 mortgage loans) features a period of the greater of a prepayment premium or yield maintenance, then a prepayment premium until an open period

Please refer to Annex A-1 to the Free Writing Prospectus for further description of individual loan call protection.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| WFRBS Commercial Mortgage Trust 2013-C12 | Issue Characteristics |

III. Issue Characteristics

| Securities Offered: | $1,018,342,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of eight classes (Classes A-1, A-2, A-3, A-4, A-SB, A-S, B and C), which are offered pursuant to a registration statement filed with the SEC. | |

| Mortgage Loan Sellers: | The Royal Bank of Scotland (“RBS”); Wells Fargo Bank, National Association (“WFB”); Liberty Island Group I LLC (“LIG I”); C-III Commercial Mortgage LLC (“CIIICM”); Basis Real Estate Capital II, LLC (“Basis”); and NCB, FSB (“NCB”). | |

| Co-lead Bookrunning Managers: | Wells Fargo Securities, LLC and RBS Securities Inc. | |

| Co-Manager: | Deutsche Bank Securities Inc. | |

| Rating Agencies: | Fitch, Inc., Kroll Bond Rating Agency, Inc. and Standard & Poor’s Ratings Services | |

| Master Servicers: | Wells Fargo Bank, National Association and NCB, FSB | |

| Special Servicers: | Rialto Capital Advisors, LLC and NCB, FSB | |

| Certificate Administrator: | Wells Fargo Bank, National Association | |

| Trustee: | U.S. Bank National Association | |

| Trust Advisor: | Pentalpha Surveillance LLC | |

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in March 2013 (or, in the case of any mortgage loan that has its first due date in April 2013, the date that would have been its due date in March 2013 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | |

| Expected Closing Date: | On or about March 20, 2013. | |

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in April 2013. | |

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in April 2013. | |

| Rated Final Distribution Date: | The Distribution Date in March 2048. | |

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month preceding the month in which such Distribution Date occurs. | |

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. | |

| Minimum Denominations: | $10,000 for each Class of Offered Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. | |

| Clean-up Call: | 1% | |

| Delivery: | DTC, Euroclear and Clearstream Banking | |

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. | |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE FREE WRITING PROSPECTUS. | |

| Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date settlements, CREFC reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg Financial Markets L.P., Trepp LLC, Intex Solutions, Inc., Markit Group Limited, Interactive Data Corp. and BlackRock Financial Management Inc. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

IV. Characteristics of the Mortgage Pool(1)

A. Ten Largest Mortgage Loans

Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Pool Balance (%) | Property Type | Number of SF, Rooms, Pads or Beds | Cut-off Date Balance Per SF, Room, Pad or Bed ($) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) |

| RBS | Grand Beach Hotel | Miami Beach | FL | 1 / 1 | $125,000,000 | 10.2% | Hospitality | 424 | $294,811 | 59.5% | 50.8% | 1.94x | 12.9% |

| RBS | RHP Portfolio II | Various | Various | 1 / 18 | 116,137,000 | 9.4 | Manufactured Housing Community | 2,967 | 39,143 | 73.1 | 62.2 | 1.45 | 8.8 |

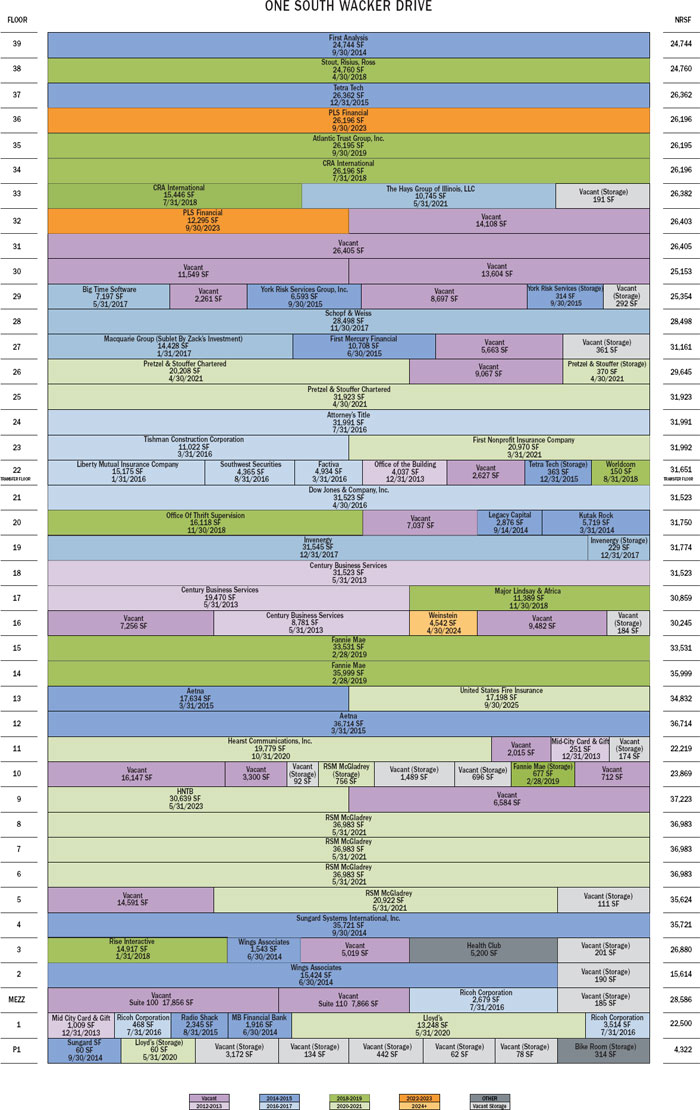

| WFB | One South Wacker Drive | Chicago | IL | 1 / 1 | 95,000,000 | 7.7 | Office | 1,193,448 | 138 | 73.0 | 73.0 | 2.40 | 10.0 |

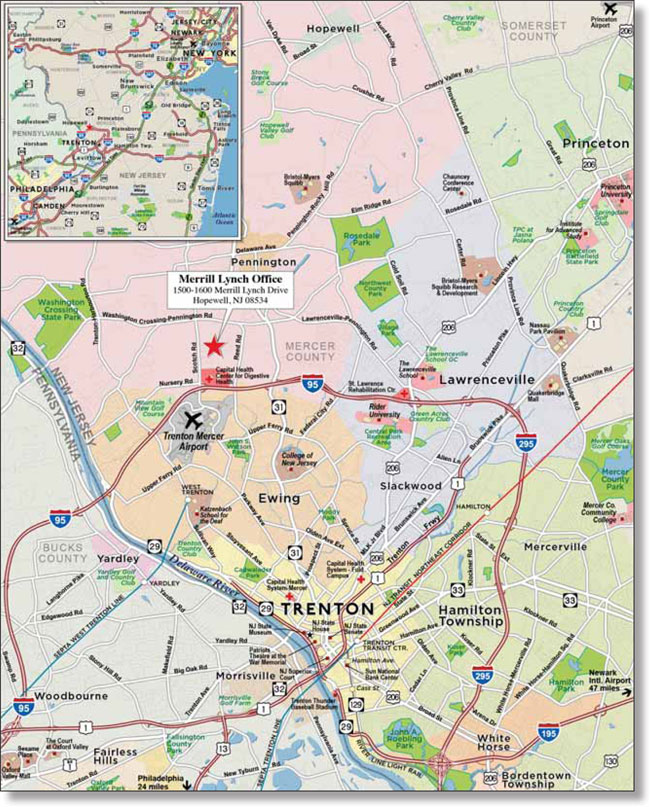

| RBS | Merrill Lynch Office | Hopewell | NJ | 1 / 1 | 74,250,000 | 6.0 | Office | 481,854 | 154 | 54.3 | 54.3 | 2.83 | 13.0 |

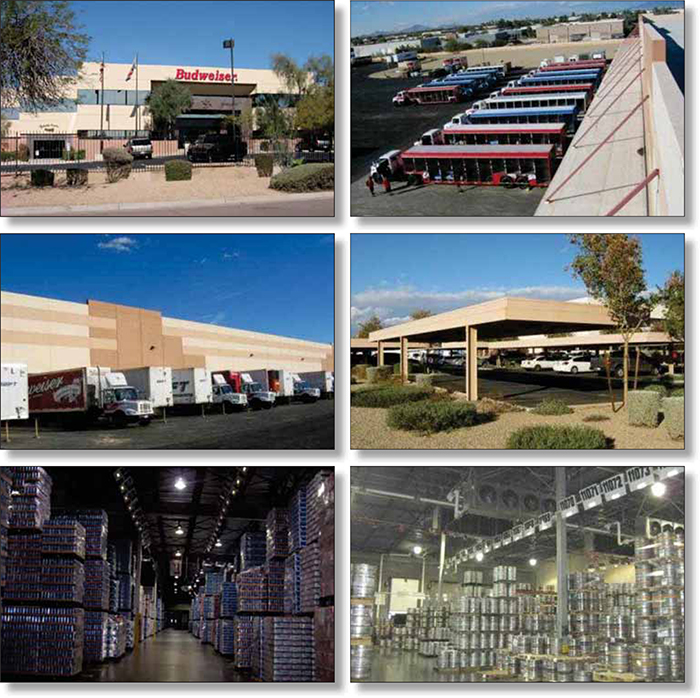

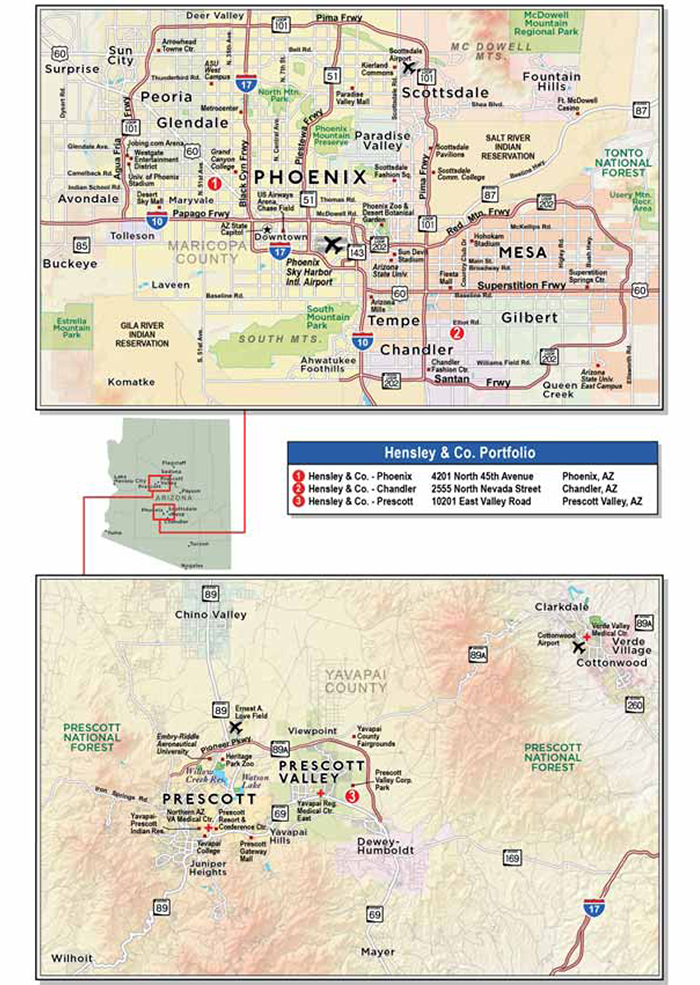

| RBS | Hensley & Co. Portfolio | Various | AZ | 1 / 3 | 49,750,000 | 4.0 | Industrial | 577,167 | 86 | 65.5 | 59.9 | 1.41 | 9.1 |

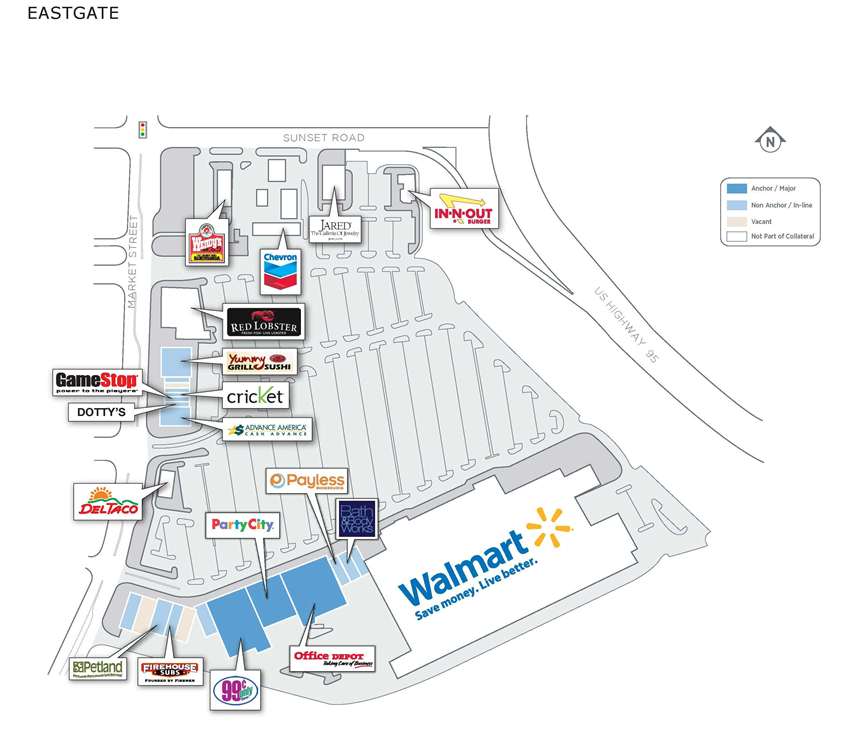

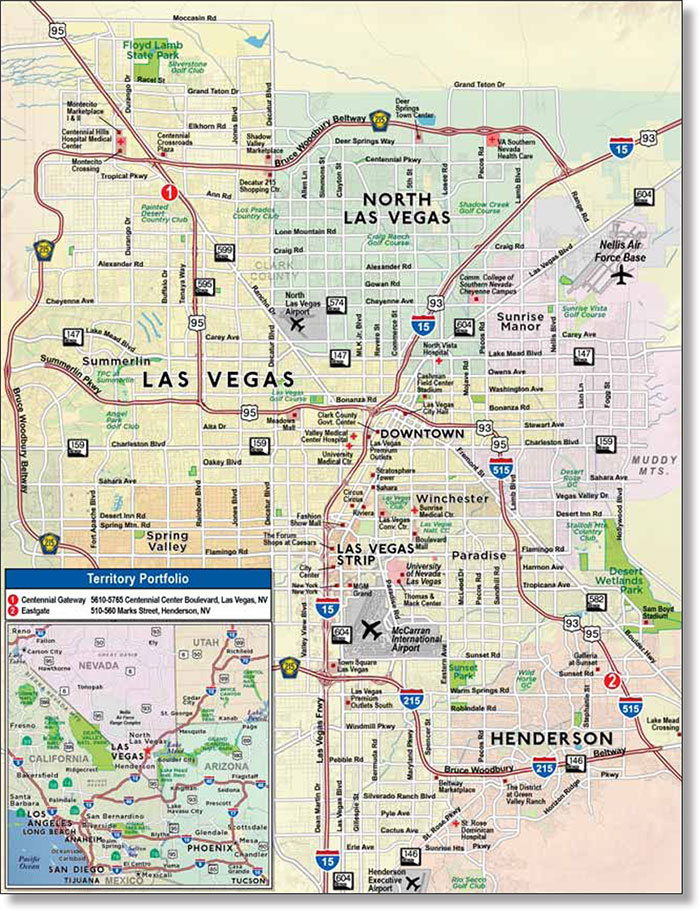

| RBS | Territory Portfolio | Various | NV | 1 / 2 | 44,385,000 | 3.6 | Retail | 289,572 | 153 | 56.2 | 56.2 | 3.10 | 12.7 |

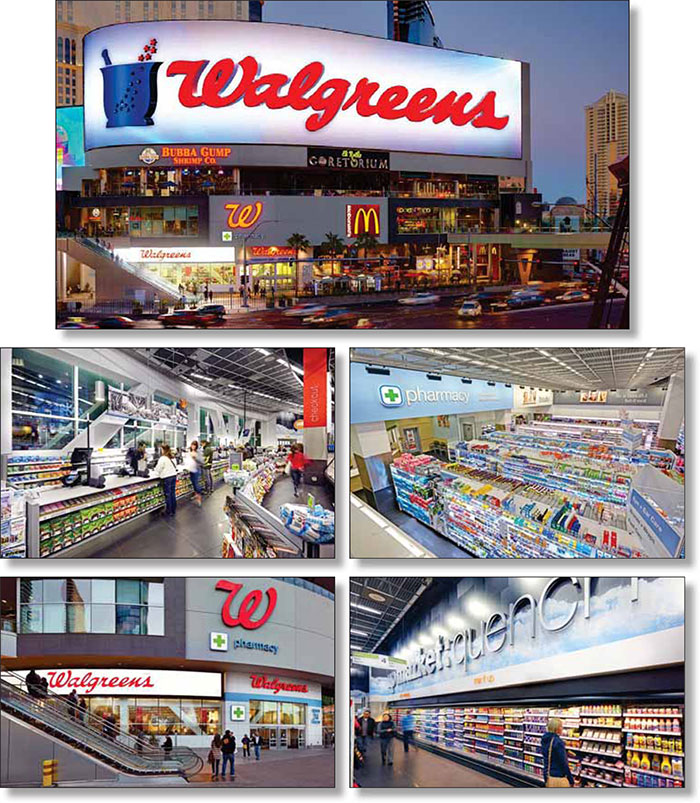

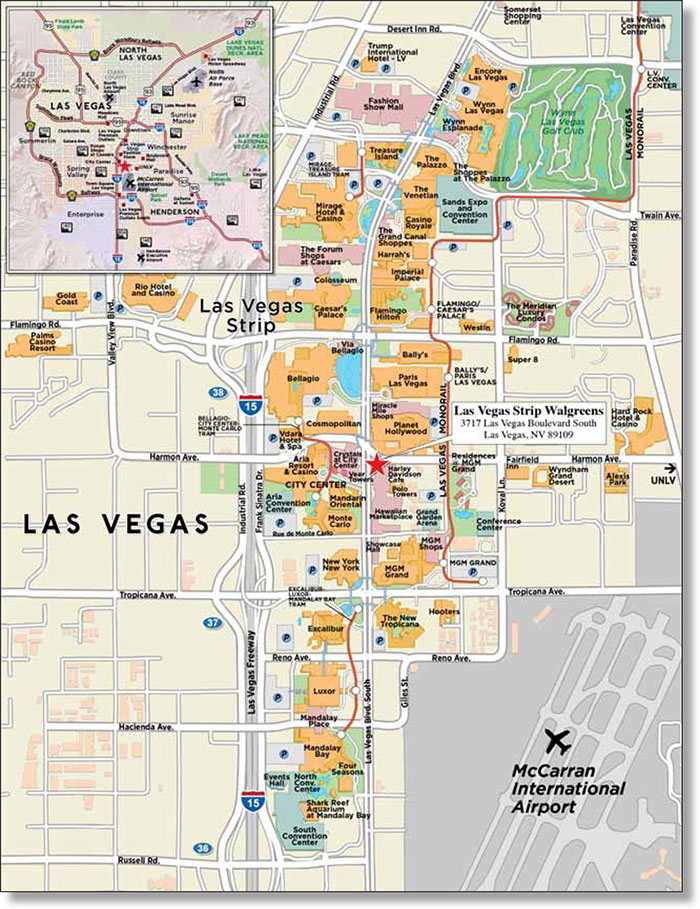

| WFB | Las Vegas Strip Walgreens | Las Vegas | NV | 1 / 1 | 40,000,000 | 3.2 | Retail | 24,721 | 1,618 | 60.6 | 60.6 | 2.11 | 8.5 |

| WFB | Kraft - Three Lakes Drive | Northfield | IL | 1 / 1 | 36,500,000 | 3.0 | Office | 679,109 | 54 | 49.3 | 49.3 | 2.69 | 13.2 |

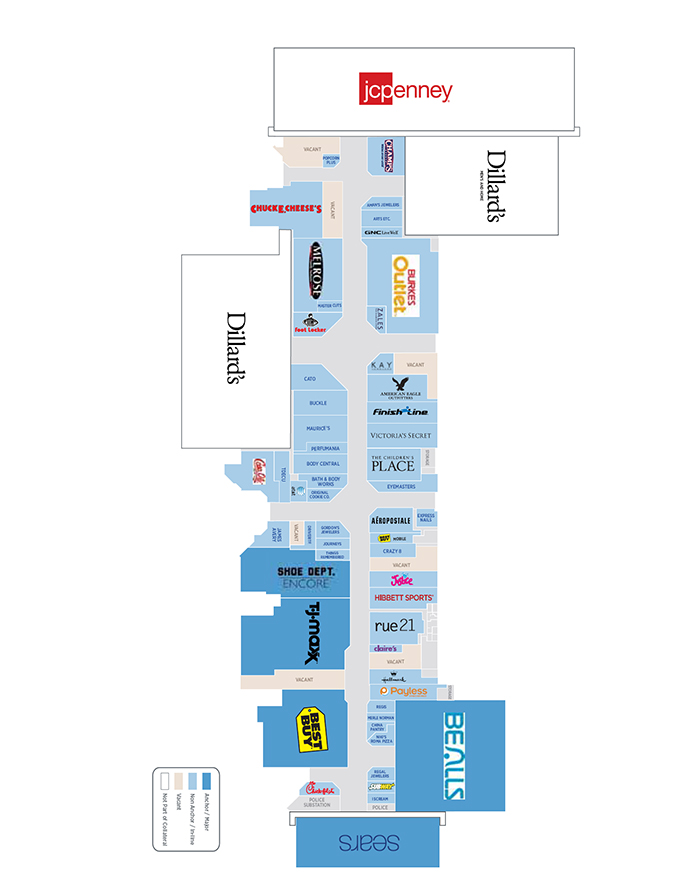

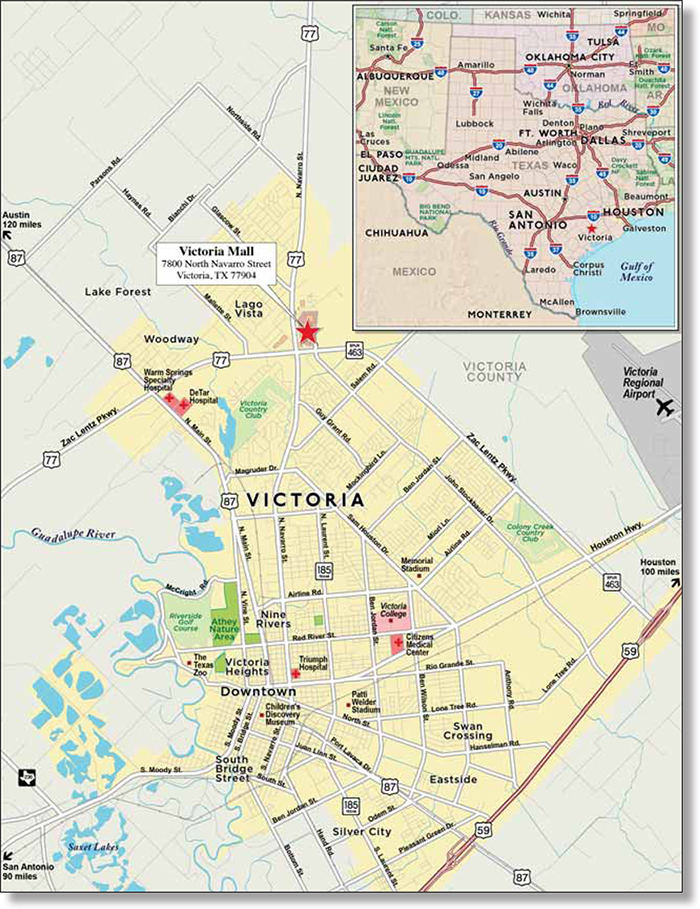

| WFB | Victoria Mall | Victoria | TX | 1 / 1 | 34,872,435 | 2.8 | Retail | 448,935 | 78 | 64.6 | 47.0 | 1.68 | 12.8 |

| CIIICM | Studio Green Apartments | Newark | DE | 1 / 1 | 30,250,000 | 2.5 | Multifamily | 1,074 | 28,166 | 56.1 | 41.8 | 1.39 | 10.3 |

| Top Three Total/Weighted Average | 3 / 20 | $336,137,000 | 27.3% | 68.0% | 61.0% | 1.90x | 10.7% | ||||||

| Top Five Total/Weighted Average | 5 / 24 | $460,137,000 | 37.4% | 65.5% | 59.8% | 2.00x | 10.9% | ||||||

| Top Ten Total/Weighted Average | 10 / 30 | $646,144,435 | 52.5% | 63.2% | 57.5% | 2.07x | 11.1% | ||||||

| (1) | With respect to One South Wacker Drive, Cut-off Date Balance per square foot, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. With respect to each Mortgage Loan, debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. |

B. Summary of Pari Passu Split Loan Structures

| Property Name | Mortgage Loan Seller | Related Notes in Loan Group (Original Balance) | Holder of Note | Whether Note is Lead Servicing for the Entire Loan Combination | Current Master Servicer Under Related Securitization PSA | Current Special Servicer Under Related Securitization PSA |

| One South Wacker Drive | WFB | $95,000,000 | WFRBS 2013-C12 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| WFB | $70,000,000 | WFRBS 2013-C11 | No | Wells Fargo Bank, National Association(1) | Midland Loan Services, a Division of PNC Bank, National Association |

| (1) | The One South Wacker Drive pari passu loan combination will be serviced under the WFRBS 2013-C11 pooling and servicing agreement until the closing date, after which such loan combination will be serviced under the pooling and servicing agreement for this transaction. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

C. Previous Securitization History(1)

Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Previous Securitization |

| 9 | WFB | Victoria Mall | Victoria | TX | Retail | $34,872,435 | 2.8% | CGCMT 2004-C1 |

| 10 | CIIICM | Studio Green Apartments | Newark | DE | Multifamily | 30,250,000 | 2.5 | Nomura CRE CDO 2007-2 |

| 14 | WFB | Old Oakland | Oakland | CA | Mixed Use | 18,000,000 | 1.5 | PCMT 2003-PWR1 |

| 21 | LIG I | Independence Park | Durham | NC | Industrial | 11,500,000 | 0.9 | WBCMT 2003-C6 |

| 23 | WFB | Santa Barbara Tech Center | Goleta | CA | Office | 10,982,437 | 0.9 | CSFB 2003-CK2 |

| 26 | WFB | Patricia Southway Manor | Houston | TX | Multifamily | 10,324,039 | 0.8 | BACM 2005-3 |

| 29 | LIG I | Travis Park Retail & Garage | San Antonio | TX | Mixed Use | 9,984,987 | 0.8 | GCCFC 2003-C1 |

| 30 | WFB | 3200 Liberty Avenue | North Bergen | NJ | Industrial | 9,984,386 | 0.8 | BSCMS 2005-T18 |

| 36 | WFB | Oak Creek Apartments | Vancouver | WA | Multifamily | 9,000,000 | 0.7 | JPMCC 2003-ML1A |

| 37 | WFB | Pacific Center | Tacoma | WA | Office | 8,974,227 | 0.7 | GCCFC 2003-C1 |

| 38 | WFB | Union Square – Manteca | Manteca | CA | Retail | 8,973,974 | 0.7 | JPMCC 2003-PM1A |

| 40 | LIG I | North Towne Plaza | San Antonio | TX | Retail | 8,800,000 | 0.7 | MSC 2004-IQ7 |

| 41 | NCB, FSB | Parkview Apartments Corp. | Ossining | NY | Multifamily | 8,310,278 | 0.7 | CSFB 2003-CPN1 |

| 42 | LIG I | Woodlands Plaza | Simi Valley | CA | Retail | 7,799,937 | 0.6 | GMACC 1998-C1 |

| 48 | Basis | Walgreens Portfolio | Various | Various | Retail | 6,000,000 | 0.5 | BSCMS 2006-T22 |

| 52 | WFB | SafKeep Self Storage – Del Rey Oaks | Del Rey Oaks | CA | Self Storage | 5,491,677 | 0.4 | MSC 2003-T11 |

| 54 | WFB | Mill Run Office Center | Allentown | PA | Office | 5,488,421 | 0.4 | JPMCC 2003-ML1A |

| 55 | WFB | Nellis Crossing Shopping Center | Las Vegas | NV | Retail | 5,400,000 | 0.4 | LBUBS 2003-C3 |

| 61 | NCB, FSB | Evergreen Owners, Inc. | Jackson Heights | NY | Multifamily | 4,160,482 | 0.3 | FNMA MBS 2002-2 |

| 63 | WFB | Yosemite Crossing | Greenwood Village | CO | Retail | 3,650,000 | 0.3 | BSCMS 2006-T24 |

| 64 | NCB, FSB | 515 East 7th Street Corporation | Brooklyn | NY | Multifamily | 3,490,023 | 0.3 | FNMA MBS 2001-6 |

| 66 | RBS | CVS Cypress | Cypress | CA | Retail | 3,095,168 | 0.3 | COMM 2003-LB1A |

| 67 | RBS | State Tower Building | Syracuse | NY | Office | 3,083,493 | 0.3 | BSCMS 1999-WF2 |

| 70 | NCB, FSB | Salisbury Point Cooperative, Inc. | South Nyack | NY | Multifamily | 2,938,550 | 0.2 | CSFB 2002-CKN2 |

| 76 | NCB, FSB | Maple Court Apartments, Inc. | Jackson Heights | NY | Multifamily | 2,256,778 | 0.2 | FNMA MBS 2002-2 |

| 80 | NCB, FSB | 415 Gramatan Avenue Corporation | Mount Vernon | NY | Multifamily | 2,124,561 | 0.2 | CSFB 2001-CKN5 |

| 82 | NCB, FSB | 417 Riverside Drive, Inc. | New York | NY | Multifamily | 2,002,083 | 0.2 | FNMA MBS 1999-1 |

| 83 | CIIICM | West Prairie MHC | Spokane | WA | Manufactured Housing Community | 1,994,637 | 0.2 | WBCMT 2003-C3 |

| 90 | CIIICM | Superstition MHC | Apache Junction | AZ | Manufactured Housing Community | 1,567,672 | 0.1 | BACM 2003-1 |

| 91 | NCB, FSB | Cherry Lane Owners Corp. | Flushing | NY | Multifamily | 1,566,824 | 0.1 | CSFB 2001-CKN5 |

| 92 | NCB, FSB | Castleton Gardens Owner’s Corp. | Staten Island | NY | Multifamily | 1,563,779 | 0.1 | CSFB 2003-CPN1 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

C. Previous Securitization History (continued)(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Previous Securitization |

| 93 | CIIICM | Acme Kent Plaza | Kent | OH | Retail | 1,500,000 | 0.1 | WBCMT 2003-C4 |

| 96 | NCB, FSB | Elizabeth Gardens Corp. | Farmingdale | NY | Multifamily | 1,317,223 | 0.1 | FNMA MBS 1999-1 |

| 97 | NCB, FSB | Broad Hollow Owners, Inc. | Amityville | NY | Multifamily | 1,275,905 | 0.1 | CSFB 2002-CKN2 |

| 98 | NCB, FSB | Bleecker & 11th Owners Corp. | New York | NY | Multifamily | 1,173,084 | 0.1 | CSFB 1998-PS2 |

| Total | $248,897,062 | 20.2% | ||||||

| (1) | The table above represents the recent commercial mortgage pass–through securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. The information has not otherwise been confirmed by the mortgage loan sellers. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

D. Mortgage Loans with Scheduled Balloon Payments and Related Classes

Class A-2(1) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-2 Certificate Principal Balance (%)(2) | SF/ Rooms/ Pads/ Units | Loan per SF/ Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 3 | WFB | One South Wacker Drive | IL | Office | $95,000,000 | 7.7% | $95,000,000 | 66.4% | 1,193,448 | $138 | 2.40x | 10.0% | 73.0% | 73.0% | 58 | 58 |

| 12 | WFB | Sportsman’s Warehouse Portfolio | Various | Retail | 24,800,000 | 2.0 | 24,800,000 | 17.3 | 296,778 | 84 | 2.95 | 12.8 | 54.9 | 54.9 | 60 | 60 |

| 16 | LIG I | Gander Mountain | FL | Retail | 15,250,000 | 1.2 | 13,768,446 | 9.6 | 120,000 | 127 | 2.37 | 15.1 | 47.7 | 43.0 | 0 | 60 |

| 56 | LIG I | Klee Plaza | IL | Mixed Use | 5,392,240 | 0.4 | 4,998,932 | 3.5 | 19,784 | 273 | 1.56 | 11.1 | 73.9 | 68.5 | 0 | 59 |

| Total/Weighted Average | $140,442,240 | 11.4% | $138,567,378 | 96.9% | 2.46x | 11.1% | 67.1% | 66.4% | 50 | 59 | ||||||

(1) The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. (2) Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-2 Certificate Principal Balance. | ||||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

Class A-3 and A-3FX Regular Interest(1)(2) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-3/ A-3FX RI Certificate Principal Balance (%)(3) | SF/ Rooms/ Pads/ Units | Loan per SF/Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 2 | RBS | RHP Portfolio II | Various | Manufactured Housing Community | $116,137,000 | 9.4% | $98,883,654 | 38.8% | 2,967 | $39,143 | 1.45x | 8.8% | 73.1% | 62.2% | 22 | 118 |

| 6 | RBS | Territory Portfolio | NV | Retail | 44,385,000 | 3.6 | 44,385,000 | 17.4 | 289,572 | 153 | 3.10 | 12.7 | 56.2 | 56.2 | 118 | 118 |

| 9 | WFB | Victoria Mall | TX | Retail | 34,872,435 | 2.8 | 25,394,512 | 10.0 | 448,935 | 78 | 1.68 | 12.8 | 64.6 | 47.0 | 0 | 118 |

| 22 | RBS | Independence Plaza | TX | Retail | 11,217,096 | 0.9 | 8,983,322 | 3.5 | 170,342 | 66 | 2.05 | 14.0 | 72.4 | 58.0 | 0 | 118 |

| 26 | WFB | Patricia Southway Manor | TX | Multifamily | 10,324,039 | 0.8 | 7,622,673 | 3.0 | 492 | 20,984 | 1.77 | 13.3 | 66.4 | 49.1 | 0 | 116 |

| 34 | WFB | Pineview Plaza | UT | Retail | 9,173,439 | 0.7 | 7,367,206 | 2.9 | 94,013 | 98 | 1.70 | 10.7 | 62.2 | 50.0 | 0 | 118 |

| 37 | WFB | Pacific Center | WA | Office | 8,974,227 | 0.7 | 7,219,739 | 2.8 | 94,960 | 95 | 1.78 | 12.6 | 66.0 | 53.1 | 0 | 118 |

| 38 | WFB | Union Square - Manteca | CA | Retail | 8,973,974 | 0.7 | 7,204,505 | 2.8 | 80,304 | 112 | 1.59 | 10.2 | 78.4 | 63.0 | 0 | 118 |

| 39 | WFB | Residence Inn - Waynesboro | VA | Hospitality | 8,838,517 | 0.7 | 6,616,549 | 2.6 | 90 | 98,206 | 1.61 | 12.4 | 67.0 | 50.1 | 0 | 116 |

| 41 | NCB, FSB | Parkview Apartments Corp. | NY | Multifamily | 8,310,278 | 0.7 | 7,057,865 | 2.8 | 202 | 41,140 | 3.44 | 23.4 | 25.5 | 21.6 | 0 | 100 |

| 59 | NCB, FSB | 950 Fifth Avenue Corporation | NY | Multifamily | 4,896,910 | 0.4 | 4,136,438 | 1.6 | 8 | 612,114 | 3.03 | 20.4 | 3.1 | 2.6 | 0 | 102 |

| 60 | LIG I | High Meadow Office | MI | Office | 4,582,854 | 0.4 | 3,380,436 | 1.3 | 58,906 | 78 | 1.41 | 11.8 | 65.5 | 48.3 | 0 | 118 |

| 61 | NCB, FSB | Evergreen Owners, Inc. | NY | Multifamily | 4,160,482 | 0.3 | 3,829,467 | 1.5 | 100 | 41,605 | 2.02 | 12.1 | 33.3 | 30.6 | 0 | 104 |

| 62 | WFB | EZ Storage | MI | Self Storage | 3,885,424 | 0.3 | 2,863,860 | 1.1 | 76,968 | 50 | 1.82 | 12.5 | 65.9 | 48.5 | 0 | 118 |

| 64 | NCB, FSB | 515 East 7th Street Corporation | NY | Multifamily | 3,490,023 | 0.3 | 2,986,526 | 1.2 | 122 | 28,607 | 3.63 | 25.2 | 14.5 | 12.4 | 0 | 97 |

| 67 | RBS | State Tower Building | NY | Office | 3,083,493 | 0.3 | 2,287,746 | 0.9 | 160,488 | 19 | 2.25 | 19.7 | 37.2 | 27.6 | 0 | 117 |

| 70 | NCB, FSB | Salisbury Point Cooperative, Inc. | NY | Multifamily | 2,938,550 | 0.2 | 2,504,928 | 1.0 | 120 | 24,488 | 7.42 | 51.5 | 9.4 | 8.0 | 0 | 101 |

| 73 | NCB, FSB | Sterling Arms Owners Corp. | NY | Multifamily | 2,593,277 | 0.2 | 2,178,869 | 0.9 | 74 | 35,044 | 3.3 | 21.7 | 17.4 | 14.6 | 0 | 102 |

| 75 | WFB | Pinelands Airport Center III | FL | Industrial | 2,291,937 | 0.2 | 1,901,137 | 0.7 | 52,000 | 44 | 1.67 | 12.4 | 67.4 | 55.9 | 0 | 117 |

| 76 | NCB, FSB | Maple Court Apartments, Inc. | NY | Multifamily | 2,256,778 | 0.2 | 1,894,147 | 0.7 | 63 | 35,822 | 3.15 | 20.8 | 16.7 | 14.0 | 0 | 104 |

| 77 | NCB, FSB | The Ridge Owners Corp. | NY | Multifamily | 2,159,628 | 0.2 | 1,866,680 | 0.7 | 42 | 51,420 | 4.08 | 29.9 | 13.1 | 11.3 | 0 | 101 |

| 78 | NCB, FSB | Plaza West Cooperative Association, Inc. | DC | Multifamily | 2,157,729 | 0.2 | 1,822,486 | 0.7 | 53 | 40,712 | 4.85 | 32.7 | 14.4 | 12.1 | 0 | 103 |

| 79 | NCB, FSB | Wellesley Gardens Owners Corp. | NY | Multifamily | 2,148,575 | 0.2 | 1,813,293 | 0.7 | 91 | 23,611 | 6.85 | 45.5 | 9.0 | 7.6 | 0 | 100 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

Class A-3 and A-3FX Regular Interest (continued)(1)(2) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-3/ A-3FX RI Certificate Principal Balance (%)(3) | SF/ Rooms/ Pads/ Units | Loan per SF/ Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 80 | NCB, FSB | 415 Gramatan Avenue Corporation | NY | Multifamily | 2,124,561 | 0.2 | 1,966,878 | 0.8 | 52 | 40,857 | 2.53 | 15.5 | 25.6 | 23.7 | 0 | 99 |

| 82 | NCB, FSB | 417 Riverside Drive, Inc. | NY | Multifamily | 2,002,083 | 0.2 | 1,704,230 | 0.7 | 64 | 31,283 | 7.58 | 52.0 | 4.6 | 3.9 | 0 | 99 |

| 84 | NCB, FSB | Capri Gardens Owners Corp. | NY | Multifamily | 1,955,517 | 0.2 | 1,648,315 | 0.6 | 72 | 27,160 | 4.98 | 33.0 | 11.3 | 9.5 | 0 | 101 |

| 86 | NCB, FSB | Waldo Gardens, Inc. | NY | Multifamily | 1,860,412 | 0.2 | 872,259 | 0.3 | 170 | 10,944 | 9.26 | 97.6 | 5.6 | 2.6 | 0 | 101 |

| 87 | NCB, FSB | 317 East 18th Street Owners Corp. | NY | Multifamily | 1,750,000 | 0.1 | 1,750,000 | 0.7 | 29 | 60,345 | 2.91 | 15.7 | 16.1 | 16.1 | 100 | 100 |

| 91 | NCB, FSB | Cherry Lane Owners Corp. | NY | Multifamily | 1,566,824 | 0.1 | 1,333,459 | 0.5 | 71 | 22,068 | 7.15 | 49.3 | 10.0 | 8.5 | 0 | 101 |

| 92 | NCB, FSB | Castleton Gardens Owner’s Corp. | NY | Multifamily | 1,563,779 | 0.1 | 1,325,579 | 0.5 | 52 | 30,073 | 3.7 | 25.0 | 19.8 | 16.8 | 0 | 100 |

| 95 | NCB, FSB | The Knolls Cooperative Section No. 2, Inc. | NY | Multifamily | 1,459,683 | 0.1 | 6,516 | 0.0 | 251 | 5,815 | 18 | 227.9 | 2.5 | 0.0 | 0 | 116 |

| 96 | NCB, FSB | Elizabeth Gardens Corp. | NY | Multifamily | 1,317,223 | 0.1 | 1,132,149 | 0.4 | 78 | 16,887 | 6.85 | 48.5 | 10.9 | 9.4 | 0 | 97 |

| 97 | NCB, FSB | Broad Hollow Owners, Inc. | NY | Multifamily | 1,275,905 | 0.1 | 1,073,036 | 0.4 | 53 | 24,074 | 4.39 | 29.2 | 20.4 | 17.2 | 0 | 104 |

| 98 | NCB, FSB | Bleecker & 11th Owners Corp. | NY | Multifamily | 1,173,084 | 0.1 | 1,010,739 | 0.4 | 35 | 33,517 | 7.59 | 54.4 | 7.6 | 6.6 | 0 | 98 |

| 99 | NCB, FSB | West 239th Owners, Inc. | NY | Multifamily | 1,172,998 | 0.1 | 995,137 | 0.4 | 42 | 27,929 | 3.90 | 26.4 | 11.3 | 9.6 | 0 | 100 |

| 100 | NCB, FSB | Work of Art Loft Corp. | NY | Multifamily | 1,073,872 | 0.1 | 912,146 | 0.4 | 9 | 119,319 | 6.74 | 45.8 | 8.2 | 6.9 | 0 | 99 |

| Total/Weighted Average | $322,147,608 | 26.2% | $269,931,483 | 105.9% | 2.35x | 15.4% | 58.6% | 49.1% | 25 | 115 | ||||||

(1) The table above presents the mortgage loans whose balloon payment would be applied to pay down the principal balance of the Class A-3 Certificates and Class A-3FX Regular Interest, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-3 and Class A-3FX Regular Interest Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. (2) Amounts allocated in respect of the Class A-3FX Regular Interest will be allocated between the Class A-3FX and Class A-3FL Certificates as described in the Free Writing Prospectus. (3) Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-3 Certificates and Class A-3FX Regular Interest Principal Balance. See Annex A-1 to the Free Writing Prospectus. | ||||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

Class A-SB(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-SB Certificate Principal Balance (%)(2) | SF/ Rooms/ Pads/ Units | Loan per SF/ Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 25 | WFB | Valley Farms Apartments | KY | Multifamily | $10,370,072 | 0.8% | $9,049,045 | 8.9% | 160 | $64,813 | 1.42x | 8.8% | 67.3% | 58.8% | 0 | 82 |

| Total/Weighted Average | $10,370,072 | 0.8% | $9,049,045 | 8.9% | 1.42x | 8.8% | 67.3% | 58.8% | 0 | 82 | ||||||

(1) The table above presents the mortgage loan whose balloon payment would be applied to pay down the principal balance of the Class A-SB Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-SB Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus.

(2) Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-SB Certificate Principal Balance.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

(THIS PAGE INTENTIONALLY LEFT BLANK)

15

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

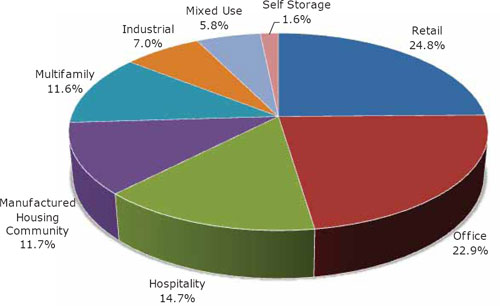

E. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate Cut- off Date Balance ($) | % of Cut- off Date Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||

| Retail | 40 | $304,972,411 | 24.8 | % | 63.2 | % | 54.3 | % | 2.06 | x | 11.5 | % | 10.6 | % | 4.220 | % |

| Anchored | 9 | 101,947,858 | 8.3 | 66.5 | 56.5 | 2.09 | 11.5 | 10.6 | 4.177 | |||||||

| Single Tenant | 21 | 101,865,639 | 8.3 | 58.2 | 54.4 | 2.24 | 11.1 | 10.4 | 4.100 | |||||||

| Shadow Anchored | 6 | 49,636,478 | 4.0 | 62.7 | 53.7 | 2.10 | 11.7 | 10.8 | 4.304 | |||||||

| Regional Mall | 1 | 34,872,435 | 2.8 | 64.6 | 47.0 | 1.68 | 12.8 | 11.2 | 4.460 | |||||||

| Unanchored | 3 | 16,650,000 | 1.4 | 71.7 | 57.9 | 1.47 | 9.5 | 8.8 | 4.455 | |||||||

| Office | 13 | 281,536,431 | 22.9 | 61.9 | 57.6 | 2.36 | 11.9 | 10.7 | 4.111 | |||||||

| Suburban | 8 | 156,028,711 | 12.7 | 55.0 | 50.3 | 2.47 | 12.9 | 11.7 | 4.264 | |||||||

| CBD | 5 | 125,507,720 | 10.2 | 70.5 | 66.8 | 2.22 | 10.6 | 9.5 | 3.921 | |||||||

| Hospitality | 7 | 181,038,517 | 14.7 | 61.7 | 50.4 | 1.85 | 12.8 | 11.7 | 4.564 | |||||||

| Full Service | 1 | 125,000,000 | 10.2 | 59.5 | 50.8 | 1.94 | 12.9 | 11.8 | 4.467 | |||||||

| Limited Service | 6 | 56,038,517 | 4.6 | 66.6 | 49.4 | 1.66 | 12.7 | 11.4 | 4.780 | |||||||

| Manufactured Housing Community | 27 | 144,078,454 | 11.7 | 72.4 | 60.8 | 1.45 | 9.1 | 9.0 | 4.542 | |||||||

| Manufactured Housing Community | 27 | 144,078,454 | 11.7 | 72.4 | 60.8 | 1.45 | 9.1 | 9.0 | 4.542 | |||||||

| Multifamily | 32 | 143,106,650 | 11.6 | 46.0 | 37.2 | 2.79 | 20.6 | 20.1 | 4.857 | |||||||

| Cooperative | 23 | 55,408,173 | 4.5 | 15.4 | 13.2 | 4.82 | 36.5 | 36.5 | 5.280 | |||||||

| Garden | 7 | 54,373,111 | 4.4 | 70.3 | 58.0 | 1.57 | 10.6 | 9.7 | 4.407 | |||||||

| Student Housing | 2 | 33,325,366 | 2.7 | 57.4 | 43.2 | 1.41 | 10.4 | 9.7 | 4.886 | |||||||

| Industrial | 8 | 86,001,324 | 7.0 | 65.4 | 57.0 | 1.51 | 10.1 | 9.1 | 4.473 | |||||||

| Warehouse | 4 | 59,734,386 | 4.9 | 66.1 | 59.2 | 1.45 | 9.4 | 8.8 | 4.477 | |||||||

| Flex | 4 | 26,266,937 | 2.1 | 63.8 | 51.9 | 1.65 | 11.5 | 10.0 | 4.466 | |||||||

| Mixed Use | 5 | 70,877,227 | 5.8 | 62.3 | 55.2 | 1.52 | 9.7 | 9.0 | 4.463 | |||||||

| Office/Retail | 2 | 46,500,000 | 3.8 | 63.4 | 55.3 | 1.38 | 9.3 | 8.5 | 4.320 | |||||||

| Parking Garage/Retail | 1 | 9,984,987 | 0.8 | 54.3 | 44.5 | 1.57 | 10.5 | 10.0 | 4.870 | |||||||

| Office/Multifamily | 1 | 9,000,000 | 0.7 | 58.4 | 58.4 | 2.21 | 10.2 | 9.6 | 4.273 | |||||||

| Multifamily/Retail | 1 | 5,392,240 | 0.4 | 73.9 | 68.5 | 1.56 | 11.1 | 10.4 | 5.260 | |||||||

| Self Storage | 6 | 19,881,101 | 1.6 | 62.0 | 51.9 | 2.34 | 12.9 | 12.5 | 4.535 | |||||||

| Self Storage | 6 | 19,881,101 | 1.6 | 62.0 | 51.9 | 2.34 | 12.9 | 12.5 | 4.535 | |||||||

| Total/Weighted Average | 138 | $1,231,492,115 | 100.0 | % | 61.8 | % | 53.5 | % | 2.05 | x | 12.4 | % | 11.5 | % | 4.394 | % |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. For mortgaged properties securing residential cooperative mortgage loans, the loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property are calculated using underwritten net cash flow for the related residential cooperative property which is the projected net cash flow reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative. With respect to One South Wacker Drive, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

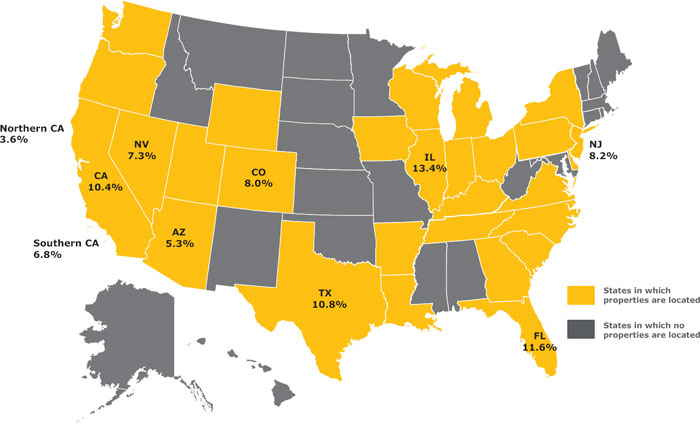

F. Geographic Distribution(1)

Location(2) | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($)(3) | % of Cut- off Date Balance | Weighted Average Cut- off Date LTV Ratio (%)(3) | Weighted Average Balloon or ARD LTV Ratio (%)(3) | Weighted Average U/W NCF DSCR (x)(3) | Weighted Average U/W NOI Debt Yield (%)(3) | Weighted Average U/W NCF Debt Yield (%)(3) | Weighted Average Mortgage Rate (%)(3) | ||||||||||

| Illinois | 8 | $165,085,240 | 13.4 | % | 67.6 | % | 65.0 | % | 2.28 | x | 10.7 | % | 9.6 | % | 4.003 | % | |||

| Florida | 3 | 142,541,937 | 11.6 | 58.4 | 50.0 | 1.98 | 13.1 | 11.9 | 4.396 | ||||||||||

| Texas | 18 | 133,229,820 | 10.8 | 67.6 | 52.9 | 1.68 | 11.8 | 10.6 | 4.528 | ||||||||||

| California | 13 | 128,071,542 | 10.4 | 62.3 | 51.1 | 1.67 | 10.9 | 10.1 | 4.358 | ||||||||||

| Southern | 8 | 83,305,891 | 6.8 | 63.0 | 51.4 | 1.75 | 10.8 | 10.3 | 4.315 | ||||||||||

| Northern | 5 | 44,765,651 | 3.6 | 61.1 | 50.5 | 1.53 | 11.0 | 9.8 | 4.440 | ||||||||||

| New Jersey | 3 | 101,234,386 | 8.2 | 58.0 | 53.6 | 2.52 | 12.7 | 11.9 | 4.302 | ||||||||||

| Colorado | 13 | 99,113,721 | 8.0 | 69.7 | 59.4 | 1.58 | 9.4 | 9.1 | 4.386 | ||||||||||

| Nevada | 4 | 89,785,000 | 7.3 | 58.6 | 57.9 | 2.58 | 10.8 | 10.4 | 3.917 | ||||||||||

| Arizona | 9 | 65,545,794 | 5.3 | 64.5 | 58.8 | 1.62 | 9.7 | 9.1 | 4.422 | ||||||||||

Other(4) | 67 | 306,884,674 | 24.9 | 56.7 | 45.6 | 2.20 | 15.7 | 14.9 | 4.726 | ||||||||||

| Total/Weighted Average | 138 | $1,231,492,115 | 100.0 | % | 61.8 | % | 53.5 | % | 2.05 | x | 12.4 | % | 11.5 | % | 4.394 | % | |||

| (1) | The Mortgaged Properties are located in 28 states and the District of Columbia. |

| (2) | For purposes of determining whether a mortgaged property is in Northern California or Southern California, Northern California includes areas with zip codes above 93600 and Southern California includes areas with zip codes of 93600 and below. |

| (3) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. For mortgaged properties securing residential cooperative mortgage loans, the loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property are calculated using underwritten net cash flow for the related residential cooperative property which is the projected net cash flow reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative. With respect to One South Wacker Drive, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan (unless otherwise stated) in total debt. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

| (4) | Includes 20 other states and the District of Columbia. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| WFRBS Commercial Mortgage Trust 2013-C12 | Characteristics of the Mortgage Pool |

G. Characteristics of the Mortgage Pool (1)

| CUT-OFF DATE BALANCE | LOAN PURPOSE | |||||||

Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Cut-off Date Balance | Loan Purpose | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Cut-off Date Balance | |

| 576,000 - 1,000,000 | 1 | $576,000 | 0.0% | Refinance | 81 | $654,889,242 | 53.2% | |

| 1,000,001 - 2,000,000 | 19 | 28,518,754 | 2.3 | Acquisition | 19 | 576,602,873 | 46.8 | |

| 2,000,001 - 3,000,000 | 12 | 28,273,118 | 2.3 | Total: | 100 | $1,231,492,115 | 100.0% | |

| 3,000,001 - 4,000,000 | 7 | 23,479,473 | 1.9 | |||||

| 4,000,001 - 5,000,000 | 4 | 18,640,246 | 1.5 | MORTGAGE RATE | ||||

| 5,000,001 - 6,000,000 | 10 | 55,783,879 | 4.5 | Number of | ||||

| 6,000,001 - 7,000,000 | 1 | 7,000,000 | 0.6 | Range of Mortgage Rates | Mortgage | Aggregate Cut- | % of Cut-off | |

| 7,000,001 - 8,000,000 | 5 | 37,645,408 | 3.1 | (%) | Loans | off Date Balance | Date Balance | |

| 8,000,001 - 9,000,000 | 7 | 61,896,997 | 5.0 | 3.700 - 4.500 | 38 | $932,190,109 | 75.7% | |

| 9,000,001 - 10,000,000 | 7 | 67,811,119 | 5.5 | 4.501 - 4.750 | 15 | 84,214,898 | 6.8 | |

| 10,000,001 - 15,000,000 | 9 | 100,943,644 | 8.2 | 4.751 - 5.000 | 13 | 115,796,967 | 9.4 | |

| 15,000,001 - 20,000,000 | 5 | 80,479,043 | 6.5 | 5.001 - 5.250 | 19 | 60,458,364 | 4.9 | |

| 20,000,001 - 30,000,000 | 3 | 74,300,000 | 6.0 | 5.251 - 5.500 | 11 | 31,681,842 | 2.6 | |

| 30,000,001 - 50,000,000 | 6 | 235,757,435 | 19.1 | 5.501 - 5.750 | 2 | 3,817,223 | 0.3 | |

| 70,000,001 - 80,000,000 | 1 | 74,250,000 | 6.0 | 5.751 - 6.000 | 1 | 1,173,084 | 0.1 | |

| 90,000,001 - 100,000,000 | 1 | 95,000,000 | 7.7 | 6.001 - 6.010 | 1 | 2,159,628 | 0.2 | |

| 100,000,001 - 125,000,000 | 2 | 241,137,000 | 19.6 | Total: | 100 | $1,231,492,115 | 100.0% | |

| Total: | 100 | $1,231,492,115 | 100.0% | Weighted Average: | 4.394% | |||

| Average: | $12,314,921 | |||||||

| UNDERWRITTEN NOI DEBT YIELD | ||||||||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | Number of | |||||||

| Number of | Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | ||||

| Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | Debt Yields (%) | Loans | off Date Balance | Date Balance | |

| DSCRs (x) | Loans | off Date Balance | Date Balance | 8.3 - 9.0 | 7 | $221,585,590 | 18.0% | |

| 1.34 - 1.40 | 2 | $42,000,000 | 3.4% | 9.1 - 10.0 | 7 | 180,850,000 | 14.7 | |

| 1.41 - 1.50 | 7 | 222,085,590 | 18.0 | 10.1 - 11.0 | 14 | 140,843,738 | 11.4 | |

| 1.51 - 1.60 | 6 | 38,367,672 | 3.1 | 11.1 - 12.0 | 21 | 132,125,287 | 10.7 | |

| 1.61 - 1.70 | 14 | 94,475,820 | 7.7 | 12.1 - 13.0 | 20 | 384,720,181 | 31.2 | |

| 1.71 - 1.80 | 14 | 83,282,840 | 6.8 | 13.1 - 14.0 | 5 | 86,041,135 | 7.0 | |

| 1.81 - 1.90 | 10 | 77,426,344 | 6.3 | 14.1 - 15.0 | 1 | 10,025,000 | 0.8 | |

| 1.91 - 2.00 | 7 | 97,390,923 | 7.9 | 15.1 - 16.0 | 3 | 19,124,561 | 1.6 | |

| 2.01 - 2.25 | 8 | 206,009,646 | 16.7 | 16.1 - 17.0 | 1 | 5,720,000 | 0.5 | |

| 2.26 - 2.50 | 2 | 20,217,096 | 1.6 | 19.1 - 20.0 | 1 | 3,083,493 | 0.3 | |

| 2.51 - 3.00 | 5 | 117,208,054 | 9.5 | 20.1 - 227.9 | 20 | 47,373,130 | 3.8 | |

| 3.01 - 3.50 | 8 | 197,992,243 | 16.1 | Total: | 100 | $1,231,492,115 | 100.0% | |

| 3.51 - 4.00 | 4 | 11,946,801 | 1.0 | Weighted Average: | 12.4% | |||

| 4.01 - 18.00 | 13 | 23,089,086 | 1.9 | |||||

| Total: | 100 | $1,231,492,115 | 100.0% | UNDERWRITTEN NCF DEBT YIELD | ||||

| Weighted Average: | 2.21x | Number of | ||||||

| Range of U/W NCF | Mortgage | Aggregate Cut - | % of Cut-off | |||||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | Debt Yields (%) | Loans | off Date Balance | Date Balance | ||||

| Number of | 8.2 - 9.0 | 13 | $320,135,590 | 26.0% | ||||

| Range of U/W NCF | Mortgage | Aggregate Cut- | % of Cut-off | 9.1 - 10.0 | 16 | 244,885,347 | 19.9 | |

| DSCRs (x) | Loans | off Date Balance | Date Balance | 10.1 - 11.0 | 20 | 125,140,842 | 10.2 | |

| 1.31 - 1.40 | 4 | $90,250,000 | 7.3% | 11.1 - 12.0 | 19 | 363,216,495 | 29.5 | |

| 1.41 - 1.50 | 15 | 255,656,864 | 20.8 | 12.1 - 13.0 | 6 | 92,787,657 | 7.5 | |

| 1.51 - 1.60 | 17 | 89,442,467 | 7.3 | 13.1 - 14.0 | 2 | 25,275,000 | 2.1 | |

| 1.61 - 1.70 | 13 | 136,738,342 | 11.1 | 15.1 - 16.0 | 4 | 12,678,054 | 1.0 | |

| 1.71 - 1.80 | 12 | 95,205,319 | 7.7 | 20.1 - 227.9 | 20 | 47,373,130 | 3.8 | |

| 1.81 - 1.90 | 3 | 16,785,424 | 1.4 | Total: | 100 | $1,231,492,115 | 100.0% | |

| 1.91 - 2.00 | 2 | 132,799,937 | 10.8 | Weighted Average: | 11.5% | |||

| 2.01 - 2.25 | 5 | 67,461,071 | 5.5 | |||||

| 2.26 - 2.50 | 2 | 110,250,000 | 9.0 | |||||

| 2.51 - 3.00 | 5 | 139,424,561 | 11.3 | |||||

| 3.01 - 3.50 | 5 | 62,442,243 | 5.1 | |||||

| 3.51 - 4.00 | 4 | 11,946,801 | 1.0 | |||||

| 4.01 - 18.00 | 13 | 23,089,086 | 1.9 | |||||

| Total: | 100 | $1,231,492,115 | 100.0% | |||||

| Weighted Average: | 2.05x | |||||||