| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-18 | ||

|  |  |

Free Writing Prospectus

Collateral Term Sheet

$1,213,814,926

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

BANK 2017-BNK7

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Wells Fargo Bank, National Association

Morgan Stanley Mortgage Capital Holdings LLC

Bank of America, National Association

National Cooperative Bank, N.A.

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2017-BNK7

September 8, 2017

WELLS FARGO

Co-Lead Manager and Joint Bookrunner | BofA MERRILL

Co-Lead Manager and Joint Bookrunner | MORGAN

Co-Lead Manager and Joint Bookrunner |

Academy Securities Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (’’SEC’’) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Morgan Stanley & Co. LLC, Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

GENERAL MOTORS BUILDING

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

GENERAL MOTORS BUILDING

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

GENERAL MOTORS BUILDING

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

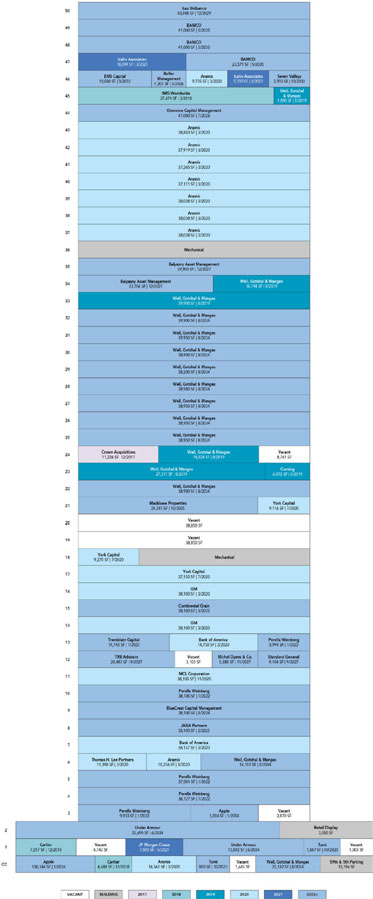

| No. 1 – General Motors Building | |||||||

| Loan Information | Property Information | ||||||

| Mortgage Loan Seller: | Morgan Stanley Mortgage Capital Holdings LLC | Single Asset/Portfolio: | Single Asset | ||||

Credit Assessment (DBRS/Fitch/Moody’s): | AAA/AAAsf /Aaa(sf) | Property Type: | Mixed Use | ||||

| Original Principal Balance(1): | $111,900,000 | Specific Property Type: | Office/Retail | ||||

| Cut-off Date Balance(1): | $111,900,000 | Location: | New York, NY | ||||

| % of Initial Pool Balance: | 9.2% | Size: | 1,989,983 SF | ||||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF(1): | $738.70 | ||||

| Borrower Name: | 767 Fifth Partners LLC | Year Built/Renovated: | 1968/2017 | ||||

| Borrower Sponsors: | Boston Properties Limited Partnership; 767 LLC; Sungate Fifth Avenue LLC | Title Vesting: | Fee | ||||

| Mortgage Rate: | 3.430% | Property Manager: | Self-managed | ||||

| Note Date: | June 7, 2017 | 4th Most Recent Occupancy (As of): | 96.9% (12/31/2013) | ||||

| Anticipated Repayment Date: | NAP | 3rd Most Recent Occupancy (As of): | 98.5% (12/31/2014) | ||||

| Maturity Date: | June 9, 2027 | 2nd Most Recent Occupancy (As of): | 96.7% (12/31/2015) | ||||

| IO Period: | 120 months | Most Recent Occupancy (As of): | 96.3% (12/31/2016) | ||||

| Loan Term (Original): | 120 months | Current Occupancy (As of)(4): | 95.0% (6/1/2017) | ||||

| Seasoning: | 3 months | ||||||

| Amortization Term (Original): | NAP | Underwriting and Financial Information: | |||||

| Loan Amortization Type: | Interest-only, Balloon | ||||||

| Interest Accrual Method: | Actual/360 | 4th Most Recent NOI (As of)(5): | $168,011,596 (12/31/2013) | ||||

| Call Protection: | L(27),D(86),O(7) | 3rd Most Recent NOI (As of)(5): | $165,315,617 (12/31/2014) | ||||

| Lockbox Type: | Hard/Springing Cash Management | 2nd Most Recent NOI (As of)(5): | $150,511,664 (12/31/2015) | ||||

| Additional Debt(1): | Yes | Most Recent NOI (As of)(5): | $151,425,346 (12/31/2016) | ||||

| Additional Debt Type(1): | Pari Passu; Subordinate Secured Debt | ||||||

| U/W Revenues: | $334,764,418 | ||||||

| U/W Expenses: | $107,458,009 | ||||||

| U/W NOI: | $227,306,409 | ||||||

| Escrows and Reserves(2): | U/W NCF: | $221,544,794 | |||||

| U/W NOI DSCR(1): | 4.45x | ||||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NCF DSCR(1): | 4.33x | ||

| Taxes | $0 | Springing | NAP | U/W NOI Debt Yield(1): | 15.5% | ||

| Insurance | $0 | Springing | NAP | U/W NCF Debt Yield(1): | 15.1% | ||

| TI/LC Reserve | $0 | $0 | NAP | As-Is Appraised Value: | $4,800,000,000 | ||

| Replacement Reserve | $0 | $0 | NAP | As-Is Appraisal Valuation Date: | May 8, 2017 | ||

| Tenant Specific TI/LC Reserve(3) | $0 | $0 | NAP | Cut-off Date LTV Ratio(1): | 30.6% | ||

| Free Rent Reserve(3) | $0 | $0 | NAP | LTV Ratio at Maturity(1): | 30.6% | ||

| (1) | The General Motors Building Whole Loan (as defined below), totaling $2,300,000,000, is comprised of the General Motors Building Senior Whole Loan (as defined below) totaling $1,470,000,000 and the General Motors Building Junior Notes (as defined below) totaling $830,000,000. The non-controlling General Motors Building Mortgage Loan (as defined below) had an original principal balance of $111,900,000, has an outstanding principal balance of $111,900,000 as of the Cut-off Date and will be contributed to the BANK 2017-BNK7 Trust. All statistical financial information related to balances PSF, loan-to-value ratios, debt service coverage ratios and debt yields are based on the General Motors Building Senior Whole Loan. The Cut-off Date LTV Ratio, U/W NCF DSCR, U/W NCF DY and Cut-off Date Balance Per SF based on the General Motors Building Whole Loan are 47.9%, 2.77x, 9.6% and $1,156, respectively. |

| (2) | See “Escrows” section. |

| (3) | At closing, Boston Properties Limited Partnership (“BPLP”) provided a guaranty in lieu of depositing (i) $107,946,183 for existing tenant improvement and leasing commission costs and (ii) $161,161,013 in existing gap rent and free rent obligations. |

| (4) | Current Occupancy includes Under Armour, which has an executed lease but is not expected to be in occupancy at the General Motors Building Property (as defined below) until on or after January 1, 2019. |

| (5) | See “Cash Flow Analysis” section. |

The Mortgage Loan. The mortgage loan (the “General Motors Building Mortgage Loan”) is part of a whole loan (the “General Motors Building Whole Loan”) evidenced by (i) a senior loan tranche (the “General Motors Building Senior Whole Loan”), and (ii) a subordinate loan tranche (the “General Motors Building Junior Notes”), secured by the fee interest in a mixed use office building located in New York, New York (the “General Motors Building Property”). The General Motors Building Whole Loan was co-originated on June 7, 2017 by Morgan Stanley Bank, N.A., Citigroup Global Markets Realty Corp., Deutsche Bank AG, New York Branch and Wells Fargo Bank, National Association (the “General Motors Building Whole Loan Origination Syndicate”). The General Motors Building Whole Loan had an original principal balance of $2,300,000,000, has an outstanding principal balance as of the Cut-off Date of $2,300,000,000 and accrues interest at an interest rate of 3.430%per annum. The General Motors Building Whole Loan had an initial term of 120 months, has a remaining term of 117 months as of the Cut-off Date and requires payments of interest only through the term of the General Motors Building Whole Loan. The General Motors Building Whole Loan matures on June 9, 2027.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

GENERAL MOTORS BUILDING

The General Motors Building Mortgage Loan, evidenced by certain notes of the General Motors Building Senior Whole Loan, which will be contributed to the BANK 2017-BNK7 Trust, had an original aggregate principal balance of $111,900,000, has an outstanding aggregate principal balance as of the Cut-off Date of $111,900,000 and represents a seniorpari passu non-controlling interest in the General Motors Building Whole Loan. Certain notes of the General Motors Building Senior Whole Loan (totaling $725,000,000) and the General Motors Building Junior Notes (totaling $830,000,000) were contributed to the BXP Trust 2017-GM Trust and represent the controlling interest in the General Motors Building Whole Loan. The remaining notes from the General Motors Building Senior Whole Loan, which had an aggregate original principal balance of $633,100,000 (the “General Motors Building Non-Serviced Pari Passu Companion Loans”), have either been contributed to securitization trusts or are expected to be contributed to future securitization trusts. After origination of the General Motors Building Whole Loan, the General Motors Building Whole Loan Origination Syndicate sold $85,000,000 of the General Motors Building Non-Serviced Pari Passu Companion Loans to Cantor Commercial Real Estate Lending, L.P. (“CCRE”). The lender provides no assurances that any non-securitized notes will not be split further or otherwise sold outside of the General Motors Building Whole Loan Origination Syndicate. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—General Motors Building Whole Loan” in the Preliminary Prospectus.

| General Motors Building Senior Whole Loan | ||

$725,000,000 BXP Trust 2017-GM | $111,900,000 BANK 2017-BNK7 | $633,100,000 General Motors Building Non- |

| General Motors Building Junior Notes | ||

$830,000,000 BXP Trust 2017-GM(2)

| ||

| (1) | After origination of the General Motors Building Whole Loan, the General Motors Building Whole Loan Origination Syndicate sold $85,000,000 of the General Motors Building Non-ServicedPari Passu Companion Loans to CCRE. |

| (2) | The holder of the controlling class of the BXP Trust 2017-GM is the controlling noteholder. |

Following the lockout period, on any date before December 9, 2026, the borrower has the right to defease the General Motors Building Whole Loan in whole, but not in part. In addition, the General Motors Building Whole Loan is prepayable without penalty on or after the due date in December 2026. The lockout period will expire on the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) June 7, 2020.

Sources and Uses

| Sources | Uses | |||||||

| Original whole loan amount | $2,300,000,000 | 100.0% | Loan payoff | $1,606,000,000 | 69.8% | |||

| Closing costs | 41,107,676 | 1.8 | ||||||

| Return of equity | 652,892,324 | 28.4 | ||||||

| Total Sources | $2,300,000,000 | 100.0% | Total Uses | $2,300,000,000 | 100.0% | |||

The Property. The General Motors Building Property is a 50-story mixed use office building comprised of approximately 1,989,983 total square feet, including approximately 187,954 square feet of retail space in the two-story retail base that wraps around the building and the below grade concourse. Originally developed in 1968 for the General Motors Corporation to serve as its headquarters, the General Motors Building Property occupies the entire city block bound by 58th Street, 59th Street, Madison Avenue and Fifth Avenue on the southeast corner of Central Park. The Fifth Avenue frontage of the General Motors Building Property features an open plaza with seating and is topped by the glass Apple cube, which serves as the entrance to Apple’s store in the below grade concourse (the “Apple Cube Space”). Because of its location, the General Motors Building Property features unobstructed views of Central Park from every office floor.

The General Motors Building Property is 95.0% leased as of June 1, 2017 by a diverse roster of office and retail tenants. Approximately 54.0% of the General Motors Building Property net rentable area (“NRA”) is leased by investment grade or large law firm tenants, which contribute approximately 49.0% of the General Motors Building Property’s underwritten gross rent. The General Motors Building Property serves as the global headquarters for Weil, Gotshal & Manges LLP (24.6% of NRA, 19.3% of underwritten base rent), which has been in occupancy since the building was constructed in 1968, headquarters for Aramis, an Estée Lauder company and another original tenant at the General Motors Building, (15.1% of NRA, 10.3% of underwritten base rent), is expected to serve as a flagship retail location for Under Armour (2.5% of NRA, 11.3% of underwritten base rent), and serves as headquarters for BAMCO (5.3% of NRA, 8.0% of underwritten base rent) and Apple’s flagship retail store (5.3% of NRA, 6.8% of underwritten base rent). The top five tenants by underwritten base rent at the General Motors Building Property lease 52.8% of NRA and comprise 55.6% of the underwritten base rent. The weighted average remaining lease term for the top five tenants is approximately 11.7 years, and the weighted average remaining lease term for the entire General Motors Building Property is approximately 9.4 years. The General Motors Building Property has a nine year average historical occupancy of 97.4% dating back to 2008.

According to the borrower sponsor, since acquiring the General Motors Building Property in 2008 and through 2016, the borrower has invested approximately $98.0 million in capital expenditures for tenant improvements and other capital projects at the General Motors Building Property.The Apple Cube Space is under renovation to expand such space by approximately 34,000 square feet, increasing ceiling heights by lowering the floor approximately five feet and adding storage space and back of house capacity by expanding into formerly dark space located below grade. Under Armour’s space is currently occupied by Apple while the Apple Cube Space and expansion is under construction. Under Armour is not currently in occupancy or paying rent. Apple is obligated to vacate

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

GENERAL MOTORS BUILDING

its temporary space by December 31, 2018 and has the right to terminate its entire lease if its expanded Apple Cube Space is not delivered by February 3, 2020, subject to force majeure. Under Armour has the right to terminate its lease if its space is not delivered by July 1, 2019 and if such failure to deliver the space is not due to tenant-caused delays or force majeure.

The majority of the General Motors Building Property’s annual underwritten base rent comes from office tenants (73.2%), with the remaining underwritten rent coming from retail tenants (26.3%) and storage space (0.4%).

The following table presents certain information relating to the tenancies at the General Motors Building Property:

Major Tenants

| Tenant Name | Credit Rating (Fitch/Moody’s/ S&P)(1) | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF(2) | Annual Rent(2) | % of Total Annual U/W Base Rent | Lease Expiration Date |

| Major Tenants | |||||||

| Weil, Gotshal & Manges LLP(3) | NR/NR/NR | 489,867 | 24.6% | $104.68 | $51,278,352 | 19.3% | Various |

| Under Armour(4) | NR/Baa2/BB+ | 49,582 | 2.5% | $605.06 | $29,999,945 | 11.3% | 6/30/2034 |

| Aramis(5) | NR/A2/A+ | 299,895 | 15.1% | $91.80 | $27,530,236 | 10.3% | 3/31/2020 |

| BAMCO(6) | NR/NR/NR | 105,579 | 5.3% | $201.65 | $21,290,010 | 8.0% | 5/31/2035 |

| Apple(7) | NR/Aa1/AA+ | 105,748 | 5.3% | $170.76 | $18,057,615 | 6.8% | Various |

| Perella Weinberg | NR/NR/NR | 130,155 | 6.5% | $95.21 | $12,392,687 | 4.7% | 1/31/2022 |

| JP Morgan Chase | A+/A3/A- | 7,500 | 0.4% | $1,464.10 | $10,980,750 | 4.1% | 5/31/2021 |

| Cartier | NR/NR/NR | 11,745 | 0.6% | $757.05 | $8,891,545 | 3.3% | 12/31/2018 |

| Balyasny Asset Management(8) | NR/NR/NR | 63,606 | 3.2% | $128.14 | $8,150,250 | 3.1% | 12/31/2027 |

| GM(9) | BBB/Baa3/BBB | 76,200 | 3.8% | $92.00 | $7,010,400 | 2.6% | 3/31/2020 |

| Total Major Tenants | 1,339,877 | 67.3% | $145.97 | $195,581,790 | 73.4% | ||

| Non-Major Tenants | 550,242 | 27.7% | $128.55 | $70,735,275 | 26.6% | ||

| Occupied Collateral Total | 1,890,119 | 95.0% | $140.90 | $266,317,065 | 100.0% | ||

| Vacant Space | 99,864 | 5.0% | |||||

| Collateral Total | 1,989,983 | 100.0% | |||||

| (1) | Certain ratings provided are for the parent company of the tenant whether or not the parent company guarantees the lease. |

| (2) | Annual U/W Base Rent PSF and Annual U/W Base Rent excludes $11,269,632 ($5.66 PSF) of total underwritten straight line rents through the tenants’ respective lease terms associated with Weil, Gotshal & Manges LLP ($6,010,916) and Apple ($4,107,800), as well as other tenants, which straight line rents are included in the “Cash Flow Analysis” table below. |

| (3) | Weil, Gotshal & Manges LLP leases 100,024 square feet of space through August 31, 2019 and 389,843 square feet through August 31, 2034. Weil, Gotshal & Manges LLP has the right to terminate (a) its 20,791 square feet of below grade storage space, at any time, and (b) either (i) its 38,900 square feet of space on the 22nd floor or (ii) its 39,900 square feet space on the 32nd floor, on or after August 31, 2022. Weil, Gotshal & Manges LLP most recently extended its lease for 389,843 square feet of its space through August 2034 at an initial base rent of $114.00 PSF, above its current in place weighted average gross rent of $92.37 PSF. BPLP, one of the borrower sponsors, provided a payment guaranty for the gap rent between Weil, Gotshal & Manges LLP current rent and Weil, Gotshal & Manges LLP underwritten rent which commences in September 2019. |

| (4) | Under Armour’s lease commences on the substantial completion of landlord’s work, which is projected to be January 1, 2019. Under Armour has the right to terminate its lease if its space is not delivered by July 1, 2019 and the failure to deliver the space is not due to tenant-caused delays or force majeure. Under Armour’s space is currently occupied by Apple while the Apple Cube Space and expansion is under construction. Under Armour is not currently in occupancy or paying rent. BPLP provided a payment guaranty with respect to Under Armour’s gap rent (for the difference between the rent being paid by Apple for the space anticipated to be occupied by Under Armour and the rent that will be due upon commencement of Under Armour’s lease), as well as for Under Armour’s free rent. Under Armour has 12 months of free rent, equal to $30,000,000, beginning after its lease commencement date. |

| (5) | Aramis subleases 9,725 square feet of its space on the 46th floor to GF Capital Management & Advisors, LLC at $107.00 PSF. |

| (6) | BAMCO has executed a renewal to extend its lease to May 2035, commencing in January 2024 for a weighted average base rent of approximately $201.65 PSF. BAMCO’s in place weighted average base rent is approximately $147.77 PSF. BPLP provided a payment guaranty with respect to BAMCO’s gap rent between closing and the renewal rent commencing in January 2024. After the expiration of the guaranty by BPLP, the lower of market or in place rent has been underwritten. |

| (7) | Apple is temporarily occupying the space expected to be occupied by Under Armour once its lease commences while the Apple Cube Space and expansion is under construction. Apple is obligated to vacate its temporary space by December 31, 2018 and has the right to terminate its entire lease if its space is not delivered by February 3, 2020, subject to force majeure. Apple leases 2,754 square feet through December 31, 2018 and 102,994 square feet through January 31, 2034. Apple has 17 months of free rent, equal to $9,562,500, on its 21,907 square feet of expansion space commencing in August 2017. BPLP provided a guaranty with respect to Apple’s free rent. Annual U/W Base Rent for Apple has been underwritten to Apple’s base rent as of January 2019 in conjunction with the Under Armour lease commencement date. |

| (8) | Balyasny Asset Management may terminate its lease effective December 31, 2022 with a minimum of one year’s notice and payment of a termination fee. Balyasny Asset Management has six months of free rent on its 34th floor space, totaling $1,481,625. |

| (9) | GM subleases 38,100 square feet on the 14th floor to Grosvenor Capital Management Holdings, LLLP at $80.00 PSF and 38,100 square feet on the 16th floor to Reservoir Operations, L.P. at $85.00 PSF. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

GENERAL MOTORS BUILDING

The following table presents certain information relating to the lease rollover schedule at the General Motors Building Property:

Lease Expiration Schedule(1)(2)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(3) | % of Total Annual U/W Base Rent | Annual U/W Base Rent PSF(4) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2017 | 1 | 11,226 | 0.6% | 11,226 | 0.6% | $993,600 | 0.4% | $88.51 |

| 2018 | 6 | 52,373 | 2.6% | 63,599 | 3.2% | $15,456,871 | 5.8% | $295.13 |

| 2019 | 9 | 106,096 | 5.3% | 169,695 | 8.5% | $9,123,113 | 3.4% | $85.99 |

| 2020 | 22 | 532,016 | 26.7% | 701,711 | 35.3% | $50,741,831 | 19.1% | $95.38 |

| 2021 | 4 | 35,486 | 1.8% | 737,197 | 37.0% | $16,570,250 | 6.2% | $466.95 |

| 2022 | 8 | 144,898 | 7.3% | 882,095 | 44.3% | $14,412,478 | 5.4% | $99.47 |

| 2023 | 2 | 2,747 | 0.1% | 884,842 | 44.5% | $1,870,937 | 0.7% | $681.08 |

| 2024 | 1 | 38,100 | 1.9% | 922,942 | 46.4% | $3,429,000 | 1.3% | $90.00 |

| 2025 | 3 | 66,347 | 3.3% | 989,289 | 49.7% | $6,783,128 | 2.5% | $102.24 |

| 2026 | 6 | 48,201 | 2.4% | 1,037,490 | 52.1% | $9,096,994 | 3.4% | $188.73 |

| 2027 | 6 | 99,324 | 5.0% | 1,136,814 | 57.1% | $12,273,236 | 4.6% | $123.57 |

| Thereafter | 38 | 753,305 | 37.9% | 1,890,119 | 95.0% | $125,565,627 | 47.1% | $166.69 |

| Vacant | 0 | 99,864 | 5.0% | 1,989,983 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 106 | 1,989,983 | 100.0% | $266,317,065 | 100.0% | $140.90 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the stated expiration date of the subject lease and that are not considered in the Lease Expiration Schedule. |

| (3) | Annual U/W Base Rent excludes $11,269,632 ($5.66 PSF) of total underwritten straight line rents through the tenants’ respective lease terms associated with Weil, Gotshal & Manges LLP ($6,010,916) and Apple ($4,107,800), as well as other tenants. |

| (4) | Weighted Average Annual U/W Base Rent PSF excludes vacant space. |

The following table presents historical occupancy percentages at the General Motors Building Property:

Historical Occupancy

2010(1) | 2011(1) | 2012(1) | 2013(1) | 2014(1) | 2015(1) | 2016(1) | 6/1/2017(2) | |||||||

| 98.5% | 98.2% | 95.5% | 96.9% | 98.5% | 96.7% | 96.3% | 95.0% |

| (1) | Information obtained from the borrower and represents average occupancy for the indicated year unless otherwise specified. |

| (2) | Information obtained from the underwritten rent roll. Underwritten occupancy includes Under Armour, which has an executed lease but is not expected to be in occupancy at the General Motors Building Property until on or after January 1, 2019. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

GENERAL MOTORS BUILDING

Operating History and Underwritten Net Cash Flow.The following table presents certain information relating to the historical operating performance and the underwritten net cash flow at the General Motors Building Property:

Cash Flow Analysis

2013 | 2014 | 2015 | 2016 | U/W | % of U/W Effective Gross Income | U/W $ per SF | |||||||

| Base Rent | $188,477,818 | $197,172,437 | $193,759,747 | $206,851,492 | $266,317,065(1) | 79.6% | $133.83 | ||||||

| Straight Line Rent | 0 | 0 | 0 | 0 | 11,269,632(2) | 3.4 | 5.66 | ||||||

| Grossed Up Vacant Space | 0 | 0 | 0 | 0 | 16,547,756(3) | 4.9 | 8.32 | ||||||

| Percentage Rent | 13,435,678 | 11,075,213 | 9,266,920 | 5,301,583 | 4,921,916(4) | 1.5 | 2.47 | ||||||

| Mark to Market(5) | 0 | 0 | 0 | 0 | 17,100,676 | 5.1 | 8.59 | ||||||

| Total Reimbursables | 29,544,790 | 35,800,858 | 38,501,366 | 39,027,298 | 27,629,542 | 8.3 | 13.88 | ||||||

| Other Income(6) | 20,814,262 | 13,270,276 | 8,240,130 | 5,169,082 | 7,525,587 | 2.2 | 3.78 | ||||||

| Less Vacancy & Credit Loss | 0 | 0 | 0 | 0 | (16,547,756)(3) | (4.9) | (8.32) | ||||||

| Effective Gross Income | $252,272,548 | $257,318,784 | $249,768,162 | $256,349,455 | $334,764,418 | 100.0% | $168.22 | ||||||

| Total Operating Expenses | $84,260,952 | $92,003,166 | $99,256,499 | $104,924,109 | $107,458,009(7) | 32.1% | $54.00 | ||||||

| Net Operating Income(8) | $168,011,596 | $165,315,617 | $150,511,664 | $151,425,346 | $227,306,409 | 67.9% | $114.23 | ||||||

| TI/LC | 0 | 0 | 0 | 0 | 5,363,618 | 1.6 | 2.70 | ||||||

| Capital Expenditures | 0 | 0 | 0 | 0 | 397,997 | 0.1 | 0.20 | ||||||

| Net Cash Flow | $168,011,596 | $165,315,617 | $150,511,664 | $151,425,346 | $221,544,794 | 66.2% | $111.33 | ||||||

| NOI DSCR(9) | 3.29x | 3.23x | 2.94x | 2.96x | 4.45x | ||||||||

| NCF DSCR(9) | 3.29x | 3.23x | 2.94x | 2.96x | 4.33x | ||||||||

| NOI DY(9) | 11.4% | 11.2% | 10.2% | 10.3% | 15.5% | ||||||||

| NCF DY(9) | 11.4% | 11.2% | 10.2% | 10.3% | 15.1% |

| (1) | U/W Base Rent is based on the rent roll as of June 1, 2017, and includes rent steps through June 2018. Lenders have made various adjustments to the in place rents which are detailed below. |

| i. | Apple is currently undergoing a major renovation to their Apple Cube Space. During the renovations, Apple is occupying the former FAO Schwarz space as temporary space until the earlier of the completion of their renovations or the outside kick out date of December 31, 2018. Base rent for Apple has been underwritten to Apple’s base rent as of January 2019 in conjunction with the Under Armour lease commencement date. Apple is currently paying annual contractual rent of $12,500,004 on the temporary space, which steps up to $24,000,000 annually in August 2018 in addition to their existing lease for the Apple Cube Space. Lenders are underwriting $18,057,615 in base rent and $19,429,881 in gross rent (base rent plus recoveries) for Apple. |

| ii. | Under Armour has executed a lease commencing in January 2019 for the space that is currently occupied by Apple as temporary space. Contractual rent has been underwritten for Under Armour based on the rent due as of January 2019 when the lease commences. BPLP provided a payment guaranty for the gap rent between the rent Apple is currently paying to occupy its temporary space and the rent that will be due under Under Armour’s lease once such lease commences. |

| iii. | Weil, Gotshal & Manges LLP has executed a renewal for 389,843 square feet of its space through August 2034, commencing in September 2019. For these spaces Underwritten base rent for Weil, Gotshal & Manges LLP uses rents effective as of September 2019. For the space not extended, contractual in-place rent inclusive of 12 months’ rent steps and existing recoveries has been underwritten. BPLP provided a payment guaranty for the gap rent between Weil, Gotshal & Manges LLP’ current rent and their underwritten rent which commences in September 2019. |

| iv. | BAMCO has executed a renewal to extend its lease to May 2035, commencing in January 2024 for a weighted average base rent of approximately $201.65 PSF. BAMCO’s in place weighted average base rent is approximately $147.77 PSF. The gap rent between closing and the renewal rent commencing in January 2024 is guaranteed by BPLP. After the expiration of the BPLP guaranty, the lower of market or in place rent has been underwritten. |

| v. | Continental Grain is currently subleasing from GM and has executed a direct lease commencing in April 2020 on the expiration of their existing sublease. GM is currently paying $92.00 PSF in base rent. Continental Grain’s direct rent in 2020 of $110.00 PSF has been underwritten. BPLP provided a guaranty for the gap rent until 2020. |

| (2) | U/W Straight Line Rent is based on net present value of future contractual rent steps after June 1, 2018 for investment grade and law firm tenants included in a listing of the largest 100 Untied States law firms through the tenants’ lease expirations (which in the case of certain tenants, expire beyond the loan term). Tenants with U/W straight line rents include $11,269,632 ($5.66 PSF) of total underwritten straight line rents through the tenants’ respective lease terms associated with Weil, Gotshal & Manges LLP ($6,010,916) and Apple ($4,107,800), as well as other tenants. |

| (3) | Vacancy is underwritten to current physical vacancy of 5.0%. |

| (4) | Apple has an abatement period for its percentage rent component that commences in October 2017. Once Apple has moved back into its expanded and redeveloped space, it will be required to pay 2.25% in percentage rent above $200,000,000 a year in sales. BPLP provided a guaranty for the estimated gap percentage rent. U/W Percentage Rent is equal to the average Apple sales from 2013 through 2016 over the new $200,000,000 breakpoint and the 2.25% percentage rent. |

| (5) | Rents have been marked up or down, as applicable, based on the appraiser’s conclusion of market rents. |

| (6) | Other income consists of primarily antenna income, direct utilities income and service income. |

| (7) | Contractual management fee is equal to 2.0% of Effective Gross Income. Underwritten management fee included in U/W Total Operating Expenses is capped at $1,000,000. |

| (8) | The Net Operating Income for the period beginning on January 1, 2017 and ending on March 31, 2017 was $49,643,832. |

| (9) | The debt service coverage ratios and debt yields are based on the outstanding principal balance of the General Motors Building Senior Whole Loan and exclude the outstanding principal balance of the General Motors Building Junior Notes. |

Appraisal.As of the appraisal valuation date of May 8, 2017, the General Motors Building Property had an “as-is” appraised value of $4,800,000,000.

Environmental Matters. According to the Phase I environmental site assessment dated May 9, 2017, there are no recognized environmental conditions at the General Motors Building Property. However, the General Motors Building Property is covered against certain environmental matters by a pollution legal liability-type environmental insurance policy issued by Chartis Specialty Insurance Company (a member company of American International Group Inc.) with limits of $20 million per incident and $40 million in the aggregate, subject to a $50,000 deductible. American International Group Inc. has an S&P rating of “BBB+”. The policy period ends September 15, 2018. Upon expiration of the existing policy, the General Motors Building Whole Loan documents require the borrower to provide a replacement policy, issued by an insurer having a minimum A.M. Best’s rating of “A-/VIII” that is maintained and renewed annually with a combined single limit of $5 million and a deductible no greater that $100,000.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

GENERAL MOTORS BUILDING

Market Overview and Competition. The General Motors Building Property is located on the entire city block bounded by Fifth Avenue and Madison Avenue between East 58th Street and East 59th Street. This area of Midtown Manhattan is known as the Madison/Fifth Avenue subdistrict, according to the appraisal. The Property is surrounded by many of New York’s landmarks, restaurants, hotels, shops and tourist attractions, made accessible by the presence of several major transportation hubs. The General Motors Building Property is located within the boundaries of the Plaza District, which is generally bound by 47th Street to the south and 65th Street to the north, and from Avenue of the Americas to the East River.

As of the first quarter 2017, the three office statistical areas that comprise the Plaza District contain 81.1 million square feet of Class A office space, 6.4 million square feet of Class B office space and 481,485 square feet of Class C office space. Historically, the Plaza District has evidenced the highest rents in Midtown Manhattan due to the demand generated by its location and quality space, according to the appraisal. As of the first quarter of 2017, the Class A office space in the Plaza District had a direct vacancy rate of 9.4% and average asking rents of $99.69 PSF, above the direct primary Midtown Manhattan average of $88.93 PSF. According to the appraisal, as of first quarter 2017, the Madison/Fifth Avenue subdistrict consisted of approximately 19.8 million square feet of Class A office space and had a direct vacancy rate of 11.0% and overall direct weighted average asking rents of $110.15 PSF.

The appraisal identified 29 comparable office properties totaling approximately 20.0 million square feet that exhibited a gross rental range of $75.00 PSF to $200.00 PSF and a weighted average occupancy rate of approximately 90.5% for direct space. Of the 29 buildings surveyed, seven are considered directly competitive with the General Motors Building Property in terms of building classification, asking rents, rentable office area and current occupancy. The directly competitive properties exhibited a gross rental range of $85.00 PSF to $200.00 PSF and a weighted average direct occupancy of approximately 86.0%, and excluding 9 West 57th Street, the average direct occupancy rate for these buildings is 94.0%, compared to 90.5% for all the competitive buildings compared with the General Motors Building Property, and 91.3% for Class A space within Midtown as a whole.

The following tables present certain information relating to comparable leases for the General Motors Building Property:

Comparable Office Leases(1)

| Property Location | Year Built | Stories | Total Office GLA (SF) | Tenant Name | Lease Date/Term | Lease Area (SF) | Annual Base Rent PSF | Lease Type |

590 Madison Avenue New York, New York | 1982 | 43 | 1,016,413 | Cemex | February 2017 / 15.0 Yrs. | 5,903 | $145.00 | Gross |

520 Madison Avenue New York, New York | 1982 | 43 | 849,600 | CIC Union | January 2017 / 10.0 Yrs. | 46,822 | $127.00 | Gross |

375 Park Avenue New York, New York | 1958 | 38 | 830,009 | Servcorp NYC | January 2017 / 10.0 Yrs. | 9,572 | $173.00 | Gross |

9 West 57th Street New York, New York | 1971 | 50 | 1,500,000 | Qatar Investment Authority | January 2017 / 10.0 Yrs | 14,000 | $180.00 | Gross |

650 Madison Avenue New York, New York | 1987 | 27 | 521,544 | Carson Family Trust | January 2017 / 10.0 Yrs | 4,002 | $120.00 | Gross |

450 Park Avenue New York, New York | 1972/2003 | 33 | 247,242 | Banco Bradesco | December 2016 / 13.0 Yrs | 21,822 | $149.00 | Gross |

399 Park Avenue New York, New York | 1961 | 39 | 1,250,000 | Morgan Stanley | July 2016 / 15.0 Yrs | 110,025 | $108.50 | Gross |

9 West 57th Street New York, New York | 1971 | 50 | 1,500,000 | Zimmer Partners | July 2016 / 10.0 Yrs | 20,100 | $155.00 | Gross |

375 Park Avenue New York, New York | 1958 | 38 | 830,009 | Fried Frank | June 2016 / 6.0 Yrs | 11,703 | $167.00 | Gross |

375 Park Avenue New York, New York | 1958 | 38 | 830,009 | Strategic Asset Services | May 2016 / 7.0 Yrs | 16,000 | $165.00 | Gross |

| (1) | Information obtained from the appraisal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

GENERAL MOTORS BUILDING

Comparable Retail Leases(1)

| Property Location | Tenant Name | Lease Date/Term | Lease Area (SF) | Level | Annual Base Rent PSF | Lease Type |

723 Madison Avenue New York, New York | Paule Ka | December 2016 / 10.0 Yrs | 1,661 | Lower, Ground, Second | (2) | Gross |

650 Fifth Avenue New York, New York | Nike | December 2016 / 15.5 Yrs | 69,214 | Lower – Sixth | (3) | Gross |

680 Madison Avenue New York, New York | Tom Ford | August 2016 / 10.0 Yrs | 8,470 | Ground, Second | (4) | Gross |

683 Fifth Avenue New York, New York | Stuart Weitzman | June 2016 / 10.0 Yrs | 1,281 | Ground | $3,903.20 | Gross |

685 Fifth Avenue New York, New York | Coach | February 2016 / 10.0 Yrs | 24,149 | Lower, Ground, Mezz, Second, Third | (5) | Gross |

683 Madison Avenue New York, New York | Bally’s | January 2016 / 10.0 Yrs | 3,013 | Ground | $1,660.00 | Gross |

730 Fifth Avenue New York, New York | Zegna | February 2016 / 15.0 Yrs | 11,580 | Lower, Ground, Mezz, Second | (6) | Gross |

650 Madison Avenue New York, New York | Moncler | September 2015 / 10.0 Yrs | 3,000 | Ground | $1,500.00 | Gross |

| (1) | Information obtained from the appraisal and a third party market report. |

| (2) | Paule Ka has a blended Annual Base Rent PSF of $874.31, which represents $50.00 PSF on its lower level space (415 square feet), $1,600 PSF on its ground floor space (867 square feet) and $125.00 PSF on its second floor space (379 square feet). |

| (3) | Nike has a blended Annual Base Rent PSF of $479.53, which represents $50.00 PSF on its lower level space (4,706 square feet), $3,500.00 PSF on its ground floor space (7,008 square feet), $350.00 PSF on its second floor space (9,500 square feet), $200.00 PSF on its third floor space (12,000 square feet), $75.00 PSF on its fourth floor space (12,000 square feet), $75.00 PSF on its fifth floor space (12,000 square feet), and $75.00 PSF on its sixth floor space (12,000 square feet). |

| (4) | Tom Ford has a blended Annual Base Rent PSF of $743.80, which represents $1,650.00 PSF on its ground floor space (3,470 square feet), $115.00 PSF on its second floor space (5,000 square feet). |

| (5) | Coach has a blended Annual Base Rent PSF of $869.60, which represents $150.00 PSF on its lower level space (5,247 square feet), $3,550.00 PSF on its ground floor space (4,627 square feet), $200.00 PSF on its mezzanine level space (1,601 square feet), $400.00 PSF on its second floor space (6,337 square feet) and $150.00 PSF on its third floor space (6,337 square feet). |

| (6) | Zegna has a blended Annual Base Rent PSF of $621.76, which represents $150.00 PSF on its lower level space (850 square feet), $3,515 PSF on its ground floor space (1,600 square feet), $200.00 PSF on its mezzanine level space (1,600 square feet) and $150.00 PSF on its second floor space (7,530 square feet). |

The Borrower.The borrower is 767 Fifth Partners LLC, a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the General Motors Building Whole Loan. Other than the borrower, no person or entity guarantees the nonrecourse carveouts or provides environmental indemnities with respect to the General Motors Building Whole Loan.

The Borrower Sponsor.The borrower sponsors are Boston Properties Limited Partnership, 767 LLC and Sungate Fifth Avenue LLC. BPLP is one of the largest owners, managers and developers of Class A office properties in the United States, with significant presence in five markets: Boston, Los Angeles, New York, San Francisco and Washington, D.C. As of May 31, 2017, BPLP owned or had interests in 175 commercial real estate properties, aggregating approximately 48.2 million net rentable square feet. New York is BPLP’s largest market by net operating income, generating annualized net operating income of approximately $452 million as of the first quarter 2017. For the same time period, its New York CBD portfolio was 94.3% leased at an average rental rate of $102.50 PSF.

Escrows.The General Motors Building Whole Loan documents provide for upfront escrows at origination in the amount of $107,946,183 for existing tenant improvement and leasing commissions costs (TI/LCs) and $161,161,013 for in existing gap rent and free rent obligations. At origination, BPLP provided a BPLP Guaranty (as defined below) in lieu of depositing $107,946,183 for existing TI/LCs and $161,161,013 in existing gap rent and free rent obligations. The loan documents do not require ongoing monthly reserve deposits for TI/LCs and replacement reserves. The General Motors Building Whole Loan documents do not require ongoing monthly deposits for real estate taxes and insurance premiums so long as there is no Cash Management Sweep Period (as defined below). During a Cash Management Sweep Period, monthly reserves are required to be collected in an amount equal to 1/12 of the real estate taxes that the lender reasonably estimates will be payable during the ensuing 12 months and 1/12 of the insurance premiums that the lender reasonably estimates will be payable for renewal of the coverage afforded by the insurance policies upon their expiration (unless the General Motors Building Property is insured as part of a “blanket” policy reasonably acceptable to the lenders) equal to one-twelfth of the amount.

The borrower has the right to deliver to the lender a guaranty (a “BPLP Guaranty”) from BPLP (in the context of the BPLP Guaranty, the “BPLP Guarantor”), in lieu of making the payments to any of the reserve accounts, so long as BPLP’s senior unsecured credit rating is BBB or higher by S&P and Baa3 or higher by Moody’s. The aggregate amount guaranteed under any such BPLP Guaranty (together with any cash delivered by the borrower to the lender in lieu of making the deposits to any reserve accounts and/or any letter of credit delivered by the borrower to the lender) related to any such purpose, must at all times be at least equal to the aggregate amount which the borrower is required to have on deposit for such purpose. The aggregate amount guaranteed under any such BPLP Guaranty will be reduced as the borrower expends funds for the purposes which such funds would have otherwise been deposited in the reserve account. The aggregate amount of any BPLP Guaranty may not at any time exceed 11.8% of the outstanding principal balance of the General Motors Building Whole Loan.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

GENERAL MOTORS BUILDING

Lockbox and Cash Management.The General Motors Building Whole Loan requires a lender-controlled lockbox account, which is already in place, and that the borrower direct all tenants to pay their rents directly into such lockbox account. The loan documents also require that all rents received by the borrower or the property manager be deposited into the lockbox account within five business days after receipt thereof. Prior to the occurrence of Cash Management Sweep Period, all funds in the lockbox account are required to be distributed to the borrower. During a Cash Management Sweep Period, all rents are required to be swept to a lender-controlled cash management account and applied to payment of debt service and funding of required reserves, with the remainder (i) to the extent a Cash Management Sweep Period is continuing, first applied to pay monthly operating expenses and then deposited into an excess cash flow reserve and held by the lender as additional collateral for the General Motors Building Whole Loan; provided, however, if no event of default is continuing, such funds are required to be disbursed to the borrower within ten days after the lender’s receipt of a written request from the borrower (at its election) (a) to pay shortfalls on debt service on the General Motors Building Whole Loan, (b) to disburse monthly operating expenses (including payments to any affiliate of the borrower if set forth in the approved annual budget or otherwise approved by the lender) as set forth in the approved annual budget and extraordinary expenses reasonably approved by the lender, (c) to pay capital expenditures (other than payments to any affiliate of the borrower unless set forth in the approved annual budget or otherwise approved by the lender) subject to the satisfaction of certain capital expenditure release conditions and (d) to pay tenant improvement costs, tenant improvement allowances or leasing expenses as set forth in the approved annual budget or incurred on commercially reasonable terms in connection with leases which do not require the lender’s approval, subject to satisfaction of certain tenant improvement release conditions or leasing commission/allowance release conditions, and (ii) to the extent no Cash Management Sweep Period is continuing, to be distributed to the borrower.

A “Cash Management Sweep Period” will commence upon the occurrence of (i) an event of default under the General Motors Building Whole Loan documents or (ii) debt service coverage ratio (“DSCR”) being less than 1.20x at the end of any calendar quarter. A Cash Management Sweep Period will end, with respect to clause (i) upon the cure of such event of default; or, with respect to clause (ii), upon (a) the DSCR being 1.20x or greater for one calendar quarter or (b) the borrower’s delivery of (x) cash to be held as an additional reserve fund, (y) a letter of credit satisfying the requirements of the General Motors Building Whole Loan documents or (z) so long as BPLP’s senior unsecured credit rating is “BBB” or higher by S&P and “Baa3” or higher by Moody’s, a guaranty by BPLP, in each case in an amount that would be required to be prepaid in order for the DSCR to equal at least 1.20x for one calendar quarter.

Property Management.The General Motors Building Property is managed by BPLP, an affiliate of the borrower.

Assumption.The borrower has the right to transfer the General Motors Building Property, provided that certain other conditions are satisfied, including, but not limited to: (i) no event of default has occurred and is continuing; (ii) the transferee is a “permitted transferee” as defined in the General Motors Building Whole Loan documents; and (iii) if requested by the lender, rating agency confirmation from each rating agency rating the Series 2017-BNK7 Certificates that the transfer will not result in a downgrade, withdrawal or qualification of the respective ratings assigned to the Series 2017-BNK7 Certificates and similar confirmations from each rating agency rating any securities backed by any portion of the General Motors Building Whole Loan with respect to the ratings of such securities. A “permitted transferee” includes (a) various types of institutional investors that own or control a specified dollar amount of real estate assets, (b) entities at least 20% owned by one or more of the types of entities in clause (a) and controlled by such entities or by a nationally recognized manager of investment funds investing in debt or equity relating to commercial real estate, and (c) entities at least 20% directly or indirectly owned by BPLP or Boston Properties, Inc.

Partial Release.Not permitted.

Real Estate Substitution.Not permitted.

Subordinate and Mezzanine Indebtedness.The General Motors Building Whole Loan includes the General Motors Building Junior Notes with an aggregate original principal balance of $830,000,000 that have been contributed to the BXP Trust 2017-GM transaction. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—General Motors Building Whole Loan” in the Preliminary Prospectus.

Ground Lease.None.

Terrorism Insurance.The General Motors Building Whole Loan documents require that the “all risk” insurance policy required to be maintained by the borrower provide coverage for terrorism in an amount equal to the full replacement cost of the General Motors Building Property, as well as 18 months of business interruption insurance and subject to a cap equal to two times the premium for the casualty (excluding any terrorism, earthquake or flood component thereof) and business interruption coverage on a stand-alone basis.

Windstorm Insurance.The General Motors Building Whole Loan documents require windstorm insurance covering the full replacement cost of the General Motors Building Property (subject to a deductible per loss that may not exceed 5% of the total insurable value of the General Motors Building Property) during the General Motors Building Whole Loan term.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

222 SECOND STREET

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

222 SECOND STREET

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| No. 2– 222 Second Street | |||||||

| Loan Information | Property Information | ||||||

| Mortgage Loan Seller: | Bank of America, N.A. | Single Asset/Portfolio: | Single Asset | ||||

Credit Assessment (Fitch/DBRS/Moody’s): | NR/NR/NR | Property Type: | Office | ||||

| Original Principal Balance(1): | $110,000,000 | Specific Property Type: | CBD | ||||

| Cut-off Date Balance(1): | $110,000,000 | Location: | San Francisco, CA | ||||

| % of Initial Pool Balance: | 9.1% | Size: | 452,418 SF | ||||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF(1): | $644.32 | ||||

| Borrower Name: | 222 Second Street Owner, L.P. | Year Built/Renovated: | 2015/NAP | ||||

| Sponsor: | TSCE Real Estate, L.P. | Title Vesting: | Fee | ||||

| Mortgage Rate: | 3.926% | Property Manager: | Tishman Speyer Properties, L.P. | ||||

| Note Date: | August 30, 2017 | 4thMost Recent Occupancy (As of)(4): | NAV | ||||

| Anticipated Repayment Date: | September 10, 2027 | 3rdMost Recent Occupancy (As of)(4): | NAV | ||||

| Maturity Date: | September 10, 2029 | 2ndMost Recent Occupancy (As of)(4): | NAV | ||||

| IO Period: | 120 months | Most Recent Occupancy (As of)(4): | 100.0% (12/31/2016) | ||||

| Loan Term (Original): | 120 months | Current Occupancy (As of)(4): | 100.0% (9/1/2017) | ||||

| Seasoning: | 0 months | ||||||

| Amortization Term (Original): | NAP | Underwriting and Financial Information: | |||||

| Loan Amortization Type: | Interest-only, ARD | ||||||

| Interest Accrual Method: | Actual/360 | 4thMost Recent NOI (As of)(4): | NAV | ||||

| Call Protection(2): | L(24),D(89),O(7) | 3rdMost Recent NOI (As of)(4): | NAV | ||||

| Lockbox Type: | Hard/Springing Cash Management | 2ndMost Recent NOI (As of)(4): | NAV | ||||

| Additional Debt(1): | Yes | Most Recent NOI (As of)(4): | NAV | ||||

| Additional Debt Type(1): | Pari Passu | ||||||

| U/W Revenues: | $35,316,832 | ||||||

| U/W Expenses: | $12,580,939 | ||||||

| U/W NOI: | $22,735,893 | ||||||

| U/W NCF: | $21,310,776 | ||||||

| U/W NOI DSCR(1): | 1.96x | ||||||

| Escrows and Reserves(3): | U/W NCF DSCR(1): | 1.84x | |||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NOI Debt Yield(1): | 7.8% | ||

| Taxes | $0 | Springing | NAP | U/W NCF Debt Yield(1): | 7.3% | ||

| Insurance | $0 | Springing | NAP | As-Is Appraised Value(5): | $516,000,000 | ||

| Replacement Reserves | $0 | Springing | $180,967 | As-Is Appraisal Valuation Date: | July 26, 2017 | ||

| TI/LC Reserve | $0 | Springing | $22,620,900 | Cut-off Date LTV Ratio(1)(5): | 56.5% | ||

| Other Reserve | $11,158,354 | $0 | NAP | LTV Ratio at Maturity or ARD(1)(5): | 56.5% | ||

| (1) | The 222 Second Street Whole Loan (as defined below) is comprised of threepari passu promissory notes with an aggregate original principal balance of $291,500,000. The controlling 222 Second Street Mortgage Loan (as defined below) had an original principal balance of $110,000,000, has an outstanding principal balance of $110,000,000 as of the Cut-off Date and will be contributed to the BANK 2017-BNK7 securitization trust. All statistical financial information related to balances per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based on the 222 Second Street Whole Loan balance of $291,500,000. |

| (2) | The defeasance lockout period will be at least 24 payment dates beginning with and including the first payment date of October 10, 2017. Defeasance of the 222 Second Street Whole Loan is permitted after the date that is the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized, and (ii) October 10, 2020. The assumed lockout period of 24 payments is based on the expected BANK 2017-BNK7 securitization trust closing date in September 2017. |

| (3) | See “Escrows” section. |

| (4) | The 222 Second Street Property is entirely leased to LinkedIn. The lease provides for four phases of occupancy: Phase I (34.6% of NRA) began on January 1, 2016, Phase II (32.9% of NRA) began on January 1, 2017, Phase III (15.7% of NRA) began on July 1, 2017 and Phase IV (16.8% of NRA) will begin on January 1, 2018. Historical occupancy and NOI information is not available. |

| (5) | The appraiser provided a hypothetical dark value for the 222 Second Street Property of $445.0 million, which would result in a Cut-off Date LTV Ratio and a LTV Ratio at Maturity of 65.5% and 65.5%, respectively. |

The Mortgage Loan. The mortgage loan (“222 Second Street Mortgage Loan”) is part of a whole loan (“222 Second Street Whole Loan”) evidenced by threepari passu promissory notes, secured by the fee interest in a 452,418 square foot Class A office tower in San Francisco, California (the “222 Second Street Property”). The 222 Second Street Whole Loan was originated on August 30, 2017 by Bank of America, N.A. The 222 Second Street Whole Loan had an original principal balance of $291,500,000, has an outstanding principal balance as of the Cut-off Date of $291,500,000 and accrues interest at an interest rate of 3.926%per annum (the “Initial Interest Rate”) through the anticipated repayment date of September 10, 2027. The 222 Second Street Whole Loan had an initial term to the anticipated repayment date of 120 months, has a remaining term to the anticipated repayment date of 120 months as of the Cut-off Date and requires payments of interest-only through the anticipated repayment date. After the anticipated repayment date, if the 222 Second Street Whole Loan remains outstanding, (a) all excess cash flow with respect to the 222 Second Street Property is required to be applied to prepay the 222 Second Street Whole Loan and (b) the 222 Second Street Whole loan will accrue interest an at interest rate equal to the sum of (x) the Initial Interest Rate plus (y) 3.000% through the final maturity date of

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

222 SECOND STREET |

September 10, 2029, with all interest accrued over the Initial Interest Rate deferred and due and payable with the repayment of the 222 Second Street Whole Loan in full at the maturity date.

The 222 Second Street Whole Loan was funded on August 30, 2017 in the amount of $280,341,646 and the 222 Second Street Whole Loan documents require that either (i) so long as no event of default has occurred and is continuing, before September 14, 2017, the 222 Second Street Borrower may request the lender to fund an amount up to $11,158,354 (resulting in the total whole loan amount of $291,500,000) to fund the required LinkedIn Reserve, Downtime Rent Reserve and Proposition 13 Reserve (collectively the “Tenant Reserves” as described below under “Escrows”), or (ii) by September 21, 2017 the 222 Second Street Borrower may deposit with lender up to $11,158,354 to fund the Tenant Reserves. In the event the 222 Second Street Borrower fails to make such funding request or deposit by September 21, 2017, the lender in its discretion may fund up to $11,158,354 to fund the Tenant Reserves. In any event, such funding will be completed prior to the Closing Date. The related Mortgage Loan seller expects, and all calculations and other information presented with respect to the 222 Second Street Mortgage Loan and the 222 Second Street Whole Loan (including the principal balances of the 222 Second Street companion loans) assume, that the Tenant Reserves will be funded by the lender.

The 222 Second Street Mortgage Loan, evidenced by Note A-1 will be contributed to the BANK 2017-BNK7 securitization trust, had an original principal balance of $110,000,000, has an outstanding principal balance as of the Cut-off Date of $110,000,000 and represents apari passu controlling interest in the 222 Second Street Whole Loan. The non-controlling notes and noteholders are shown in the note summary table below. The lender provides no assurances that any non-securitized notes will not be split further. See “Description of the Mortgage Pool—The Whole Loans” in the Preliminary Prospectus.

Note Summary

| Notes | Original Balance | Note Holder | Controlling Interest |

| A-1 | $110,000,000 | BANK 2017-BNK7 | Yes |

| A-2 | $100,000,000 | Bank of America, N.A. | No |

| A-3 | $81,500,000 | Bank of America, N.A. | No |

| Total | $291,500,000 |

Following the lockout period, the borrower has the right to defease the 222 Second Street Whole Loan in whole, but not in part. In addition, the 222 Second Street Whole Loan is prepayable without penalty on or after March 10, 2027. The lockout period will expire on the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) October 10, 2020.

Sources and Uses

| Sources | Uses(1) | |||||||

| Original whole loan amount | $291,500,000 | 100.0% | Loan Payoff | $213,720,346 | 73.3% | |||

| Closing costs | 2,080,863 | 0.7 | ||||||

| Reserves(2) | 11,158,354 | 3.8 | ||||||

| Return of equity(3) | 64,540,437 | 22.1 | ||||||

| Total Sources | $291,500,000 | 100.0% | Total Uses | $291,500,000 | 100.0% | |||

| (1) | The 222 Second Street Property was developed by the 222 Second Street Whole Loan sponsor in a joint venture partnership for a construction cost of approximately $304.5 million. |

| (2) | See “The Mortgage Loan” and “Escrows”. |

| (3) | Return of equity was used to pay off the previous joint venture partner. |

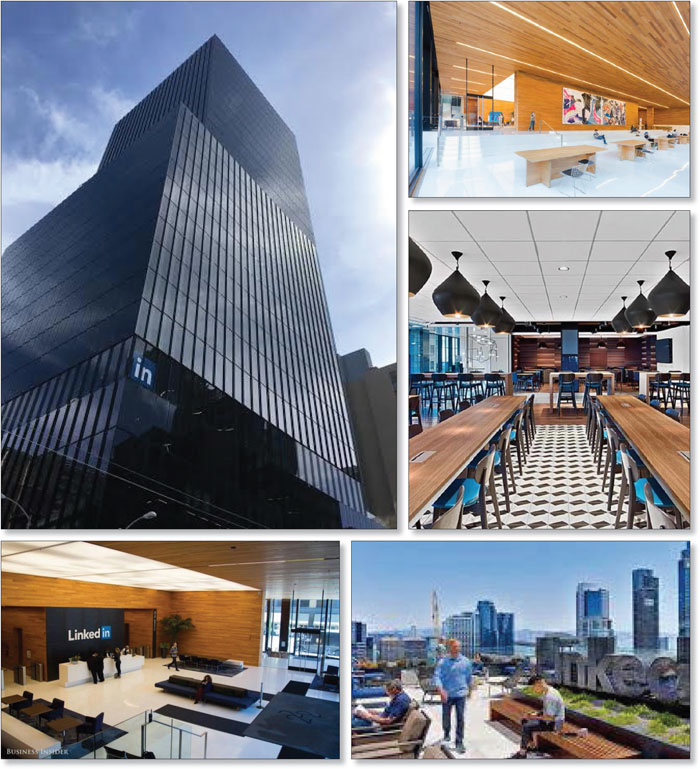

The Property. The 222 Second Street Property is a 452,418 square foot, 26-story high-rise, LEED-Gold certified, Class A office building that was constructed in 2015 and is entirely leased to LinkedIn. Approximately $103 million ($228 per square foot) in tenant improvements was invested to build out LinkedIn’s space, inclusive of approximately $60 million reportedly invested by LinkedIn directly, as it consolidated its San Francisco workforce previously housed in various buildings in San Francisco’s Financial District and SOMA district to the 222 Second Street Property. The LinkedIn lease provides for phased-in occupancy that began January 2016, with the last phase (16.8% of NRA, floors 21-26) expected to commence on January 1, 2018. On the ground floor of the building there is the LinkedIn lobby with a coffee kiosk, 2,209 square feet of retail space and a landscaped public open space. The 222 Second Street Property also features a fitness center offering fitness classes and a massage room and a café with a full-service kitchen on the 2nd floor, outdoor terraces on floors 5 and 17, and a two level sub-grade parking garage with 90 valet spots. The column-free floorplans provide for flexible layouts with floor-to-ceiling windows that allow for 360-degree bay and city views. LinkedIn has customized its space with art installations, creative interactive wall spaces, conference rooms, quiet areas, business centers and kitchenettes on every floor, a band room, pool hall, lending library, music library, and secure bicycle parking.

The Tenant.The 222 Second Street Property is entirely leased to LinkedIn Corporation (“LinkedIn”) under a lease dated April 21, 2014 with four phases of occupancy (Phase I (34.6% of NRA) began on January 1, 2016, Phase II (32.9% of NRA) began on January 1, 2017, Phase III (15.7% of NRA) began on July 1, 2017 and Phase IV (16.8% of NRA) is expected to begin on January 2018) and with staggered expirations in 2025, 2026 and 2027. The LinkedIn lease provides for an initial weighted average rent per square foot of $69.70 with annual rent increases of $1.50 per square foot on the office space and 3.0% on the retail space. The LinkedIn lease does not have any contraction or termination options. The LinkedIn lease contains two five-year renewal options for all or a portion of its space at 95% of fair market rent with 15 months’ notice, which if exercised consecutively and on the entire space, allows for a third five-year renewal option at 95% of fair market rent with 15 months’ notice. If the 222 Second Street Property is ever marketed for sale, LinkedIn has a one-time right of first offer to purchase the 222 Second Street Property provided that it continues to directly lease more than 400,000 square feet and there is no default under the lease.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

222 SECOND STREET |

LinkedIn is the world’s largest professional social network company with over 400 million members globally and more than 10,000 full time employees. LinkedIn has users in over 200 countries and provides services in 23 languages and earns revenue through three main sources: talent solutions, marketing solutions and premium subscriptions. LinkedIn launched in 2003, went public in 2011 and was acquired by Microsoft Corporation (NasdaqGS: MSFT) in December 2016 for $26.2 billion, the largest acquisition in Microsoft history. Microsoft Corporation fully guarantees the lease.

The following table presents certain information relating to the lease phases at the 222 Second Street Property:

Lease Phase Summary

| Tenant Name | Credit Rating (Fitch/Moody’s/ S&P)(1) | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF(2) | Annual U/W Base Rent(2) | % of Total Annual U/W Base Rent | Lease Expiration Date | |||

| LinkedIn Phase I | Floors 2-8 | AA+/Aaa/AAA | 154,450 | 34.1% | $70.98 | $10,962,862 | 32.2% | 12/1/2025 | ||

| LinkedIn Phase II | Floors 9-15 | AA+/Aaa/AAA | 148,664 | 32.9% | $74.23 | $11,035,648 | 32.4% | 12/1/2026 | ||

| LinkedIn Phase III | Floors 16-20 | AA+/Aaa/AAA | 70,883 | 15.7% | $78.86 | $5,590,148 | 16.4% | 6/1/2027 | ||

| LinkedIn Phase IV | Floors 21-26 | AA+/Aaa/AAA | 76,212 | 16.8% | $82.52 | $6,288,804 | 18.5% | 12/1/2027 | ||

| LinkedIn Retail Space | Lobby | AA+/Aaa/AAA | 2,209 | 0.5% | $76.26 | $168,463 | 0.5% | 12/1/2025 | ||

| Total | 452,418 | 100.0% | $75.25 | $34,045,925 | 100.0% | |||||

| Vacant Space | 0 | 0.0% | ||||||||

| Collateral Total | 452,418 | 100.0% | ||||||||

| (1) | The LinkedIn lease is guaranteed by Microsoft Corporation, whose ratings are shown. |

| (2) | Annual U/W Base Rent includes contractual rent increases through August 2018 and straightlined rent through the lease term. |

The following table presents certain information relating to the lease rollover schedule at the 222 Second Street Property:

Lease Phase Expiration Schedule(1)

| Year Ending December 31, | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(2) | % of Total Annual U/W Base Rent(2) | Annual U/W Base Rent PSF(2) |

| 2017 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2018 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2019 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2020 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2021 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2022 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2023 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2024 | 0 | 0.0% | 0 | 0.0% | 0 | 0.0% | $0.00 |

| 2025 | 156,659 | 34.6% | 156,659 | 34.6% | 11,131,325 | 32.7% | $71.05 |

| 2026 | 148,664 | 32.9% | 305,323 | 67.5% | 11,035,648 | 32.4% | $74.23 |

| 2027 | 147,095 | 32.5% | 452,418 | 100.0% | 11,878,952 | 34.9% | $80.76 |

| Thereafter | 0 | 0.0% | 452,418 | 100.0% | 0 | 0.0% | $0.00 |

| Vacant | 0 | 0.0% | 452,418 | 100.0% | 0 | 0.0% | $0.00 |

| Total/Wtd. Avg. | 452,418 | 100.0% | $34,045,925 | 100.0% | $75.25 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Annual U/W Base Rent includes contractual rent increases through August 2018 and straightlined rent through the lease term. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

222 SECOND STREET |

Underwritten Net Cash Flow. The following table presents certain information relating to the underwritten net cash flow at the 222 Second Street Property:

Cash Flow Analysis(1)

| U/W | % of U/W Effective Gross Income | U/W $ per SF | |||

| Base Rent(2) | $ 34,045,925 | 96.4% | $75.25 | ||

| Expense Reimbursements | 2,035,199 | 5.8 | 4.50 | ||

| Other Income & Parking Income(3) | 1,039,764 | 2.9 | 2.30 | ||

| Less Vacancy & Credit Loss | (1,804,056) | (5.1) | (3.99) | ||

| Effective Gross Income | $ 35,316,832 | 100.0% | $78.06 | ||

| Total Operating Expenses | 12,580,939 | 35.6 | 27.81 | ||

| Net Operating Income | $22,735,893 | 64.4% | $50.25 | ||

| TI/LC | 1,357,254 | 3.8 | 3.00 | ||

| Capital Expenditures | 67,863 | 0.2 | 0.15 | ||

| Net Cash Flow | $21,310,776 | 60.3% | $47.10 | ||

| NOI DSCR(4) | 1.96x | ||||

| NCF DSCR(4) | 1.84x | ||||

| NOI DY(4) | 7.8% | ||||

| NCF DY(4) | 7.3% |

| (1) | The 222 Second Street Property is entirely leased to LinkedIn. The lease provides for four phases of occupancy: Phase I (34.6% of NRA) began on January 1, 2016, Phase II (32.9% of NRA) began on January 1, 2017, Phase III (15.7% of NRA) began on July 1, 2017 and Phase IV (16.8% of NRA) is expected to begin on January 1, 2018. Historical information is not available. |

| (2) | U/W Base Rent includes contractual rent increases through August 2018 and straightlined rent through the lease term. |

| (3) | Other Income includes work order income, overtime HVAC, sub-metered electric and cleaning income. Parking Income includes the contractual rent step effective April 16, 2018. |

| (4) | Based on the 222 Second Street Whole Loan balance of $291,500,000. |

Appraisal.As of the appraisal valuation date of July 26, 2017, the 222 Second Street Property had an “as-is” appraised value of $516,000,000.

Environmental Matters.According to the Phase I environmental report dated July 31, 2017, there was no evidence of any recognized environmental conditions at the 222 Second Street Property.

Market Overview and Competition. The 222 Second Street Property is located in the South Financial District of downtown San Francisco, California, on the southwest corner of Howard and Second Streets with additional frontage on Tehama Street. To the north, the North Financial District contains most of the older development and prestigious buildings of San Francisco. To the south is the Rincon Hill/South Beach/SOMA District, which has seen a resurgence in leasing activity particularly with respect to the technology sector. To the west is the Yerba Buena District, which is home to several major redevelopment projects that have enhanced the economic utility of the area, including the Yerba Buena complex, the Moscone convention center, and Westfield Shopping Center.