| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-25 | ||

|  |

Free Writing Prospectus

Collateral Term Sheet

$658,765,419

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

Wells Fargo Commercial Mortgage Trust 2018-C45

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Wells Fargo Bank, National Association

Barclays Bank PLC

Rialto Mortgage Finance, LLC

C-III Commercial Mortgage LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2018-C45

June 15, 2018

WELLS FARGO SECURITIES

Co-Lead Manager and Joint Bookrunner | BARCLAYS

Co-Lead Manager and Joint Bookrunner | |

Academy Securities Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (’’SEC’’) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Barclays Capital Inc., Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

A. Transaction Highlights

Mortgage Loan Sellers:

Mortgage Loan Seller | Number | Number of | Aggregate Cut- | % of Initial |

| Wells Fargo Bank, National Association | 14 | 27 | $271,350,036 | 41.2% |

| Barclays Bank PLC | 11 | 31 | 172,882,585 | 26.2 |

| Rialto Mortgage Finance, LLC | 7 | 13 | 113,800,000 | 17.3 |

| C-III Commercial Mortgage LLC | 17 | 18 | 100,732,798 | 15.3 |

Total | 49 | 89 | $658,765,419 | 100.0% |

Loan Pool:

| Initial Pool Balance: | $658,765,419 |

| Number of Mortgage Loans: | 49 |

| Average Cut-off Date Balance per Mortgage Loan: | $13,444,192 |

| Number of Mortgaged Properties: | 89 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $7,401,859 |

| Weighted Average Mortgage Interest Rate: | 4.899% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 54.6% |

| Weighted Average Original Term to Maturity or ARD (months): | 120 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 118 |

| Weighted Average Original Amortization Term (months)(2): | 358 |

| Weighted Average Remaining Amortization Term (months)(2): | 358 |

| Weighted Average Seasoning (months): | 2 |

(1) Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. (2) Excludes any mortgage loan that does not amortize. | |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 1.66x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 10.3% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 61.2% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 55.8% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 17.2% |

| % of Mortgage Loans with Single Tenants(3): | 9.9% |

(1) With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) but exclude any related subordinate debt (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. (2) The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” in the Preliminary Prospectus. (3) Excludes mortgage loans that are secured by multiple single tenant properties. | |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| Wells Fargo Commercial Mortgage Trust 2018-C45 | Certain Loan Information |

B. Summary of the Whole Loans

| Property Name | Mortgage Loan Seller in | Note(s)(1) | Original Balance | Holder of Note(1) | Lead Servicer for Whole Loan | Master Servicer Under Lead Securitization Servicing Agreement | Special Servicer Under Lead Securitization Servicing Agreement |

| Village at Leesburg | WFB | A-1 | $66,000,000 | WFCM 2018-C44 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $65,250,000 | WFCM 2018-C45 | No | ||||

| CoolSprings Galleria | WFB | A-1 | $75,000,000 | BANK 2018-BNK12 | Yes | Wells Fargo Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association |

| A-2 | $15,000,000 | BANK 2018-BNK12 | No | ||||

| A-3 | $20,000,000 | WFCM 2018-C45 | No | ||||

| A-4 | $45,000,000 | WFB | No | ||||

| 181 Fremont Street(3) | Barclays | A-1 | $50,000,000 | Deutsche Bank AG, New York Branch | Yes | Wells Fargo Bank, National Association(2) | Rialto Capital Advisors, LLC(2) |

| A-2 | $58,000,000 | BANK 2018-BNK12 | No | ||||

| A-3 | $22,000,000 | WFB | No | ||||

| A-4 | $30,000,000 | Deutsche Bank AG, New York Branch | No | ||||

| A-5 | $40,000,000 | Deutsche Bank AG, New York Branch | No | ||||

| A-6-1 | $30,000,000 | WFCM 2018-C44 | No | ||||

| A-6-2 | $20,000,000 | WFCM 2018-C45 | No | ||||

| A-1 | $59,000,000 | CGCMT 2018-C5(3) | Yes | Midland Loan Services, a Division of PNC Bank, National Association | |||

| Flats at East Bank | RMF | A-2 | $13,000,000 | WFCM 2018-C45 | No | KeyBank National Association | |

| B | $21,000,000 | ACREFI Mortgage Lending, LLC | No |

| (1) | Unless otherwise indicated, each note not currently held by a securitization trust is expected to be contributed to a future securitization. No assurance can be provided that any such note will not be split further. |

| (2) | On and after the securitization of the related “lead” pari passu note (namely, the related pari passu note marked “Yes” in the column entitled “Lead Servicer for Whole Loan”), such whole loan will be serviced under the pooling and servicing agreement governing such securitization. The master servicer and special servicer for such securitization will be identified in a notice, report or statement to holders of the WFCM 2018-C45 certificates after the closing of such securitization. |

| (3) | The CGCMT 2018-C5 securitization is expected to close on or about June 21, 2018. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| Wells Fargo Commercial Mortgage Trust 2018-C45 | Certain Loan Information |

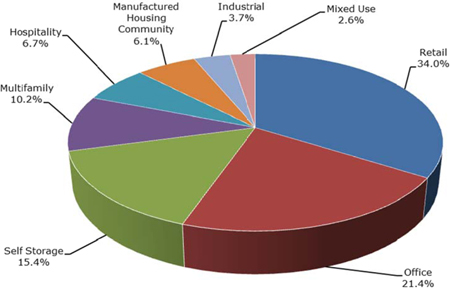

C. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut- off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) |

| Retail | 34 | $223,732,106 | 34.0% | 59.4% | 54.3% | 1.66% | 10.2% | 9.7% | 4.812% |

| Anchored | 7 | 131,605,357 | 20.0 | 58.3 | 53.1 | 1.55 | 10.0 | 9.4 | 4.821 |

| Single Tenant | 18 | 35,515,000 | 5.4 | 62.5 | 62.2 | 2.07 | 9.7 | 9.6 | 4.539 |

| Shadow Anchored | 5 | 19,974,600 | 3.0 | 68.8 | 61.1 | 1.45 | 9.9 | 9.3 | 5.035 |

| Super Regional Mall | 1 | 19,950,390 | 3.0 | 48.0 | 39.0 | 1.91 | 12.8 | 12.1 | 4.839 |

| Unanchored | 3 | 16,686,759 | 2.5 | 63.2 | 57.4 | 1.59 | 9.8 | 9.3 | 5.020 |

| Office | 10 | 140,937,221 | 21.4 | 61.4 | 56.0 | 1.85 | 11.2 | 10.1 | 4.678 |

| Suburban | 5 | 104,187,221 | 15.8 | 64.6 | 58.0 | 1.62 | 11.3 | 9.9 | 4.872 |

| CBD | 1 | 20,000,000 | 3.0 | 39.6 | 39.6 | 3.14 | 11.8 | 11.8 | 3.709 |

| Medical | 4 | 16,750,000 | 2.5 | 68.0 | 63.2 | 1.73 | 9.4 | 9.1 | 4.629 |

| Self Storage | 19 | 101,447,884 | 15.4 | 62.1 | 56.8 | 1.40 | 9.3 | 9.1 | 5.082 |

| Self Storage | 19 | 101,447,884 | 15.4 | 62.1 | 56.8 | 1.40 | 9.3 | 9.1 | 5.082 |

| Multifamily | 3 | 67,091,470 | 10.2 | 66.2 | 63.1 | 1.50 | 8.6 | 8.4 | 5.071 |

| Low Rise | 1 | 38,000,000 | 5.8 | 63.1 | 63.1 | 1.61 | 8.1 | 7.9 | 4.845 |

| Garden | 2 | 29,091,470 | 4.4 | 70.2 | 63.1 | 1.35 | 9.3 | 9.1 | 5.367 |

| Hospitality | 5 | 44,430,416 | 6.7 | 62.3 | 51.4 | 1.95 | 14.3 | 12.7 | 5.071 |

| Limited Service | 5 | 44,430,416 | 6.7 | 62.3 | 51.4 | 1.95 | 14.3 | 12.7 | 5.071 |

| Manufactured Housing Community | 13 | 39,992,909 | 6.1 | 60.6 | 55.3 | 1.58 | 9.8 | 9.6 | 5.208 |

| Manufactured Housing Community | 13 | 39,992,909 | 6.1 | 60.6 | 55.3 | 1.58 | 9.8 | 9.6 | 5.208 |

| Industrial | 2 | 24,137,006 | 3.7 | 62.7 | 54.9 | 1.57 | 10.1 | 9.8 | 4.709 |

| Warehouse | 2 | 24,137,006 | 3.7 | 62.7 | 54.9 | 1.57 | 10.1 | 9.8 | 4.709 |

| Mixed Use | 3 | 16,996,408 | 2.6 | 53.5 | 52.4 | 1.81 | 9.8 | 9.7 | 5.183 |

| Multifamily/Retail | 1 | 13,000,000 | 2.0 | 52.0 | 52.0 | 1.90 | 9.9 | 9.8 | 5.090 |

| Retail/Multifamily | 1 | 2,100,000 | 0.3 | 52.5 | 52.5 | 1.68 | 8.9 | 8.8 | 5.160 |

| Self Storage/Office | 1 | 1,896,408 | 0.3 | 64.7 | 54.8 | 1.37 | 10.5 | 9.7 | 5.850 |

| Total/Weighted Average: | 89 | $658,765,419 | 100.0% | 61.2% | 55.8% | 1.66% | 10.3% | 9.7% | 4.899% |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate debt (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Wells Fargo Commercial Mortgage Trust 2018-C45 | Certain Loan Information |

D. Large Loan Summaries

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| No. 1 – Village at Leesburg | |||||||

| Loan Information | Property Information | ||||||

| Mortgage Loan Seller: | Wells Fargo Bank, National Association | Single Asset/Portfolio: | Single Asset | ||||

Credit Assessment (DBRS/Fitch/Moody’s): | NR/NR/NR | Property Type: | Retail | ||||

| Original Principal Balance(1): | $65,250,000 | Specific Property Type: | Anchored | ||||

| Cut-off Date Balance(1): | $65,250,000 | Location: | Leesburg, VA | ||||

| % of Initial Pool Balance: | 9.9% | Size(4): | 546,107 SF | ||||

| Loan Purpose(2): | Recapitalization | Cut-off Date Balance Per SF(1)(4): | $240.34 | ||||

| Borrower Name: | CRP/TRC Leesburg Retail Owner, L.L.C. | Year Built/Renovated: | 2009/2018 | ||||

| Sponsor: | Gary D. Rappaport | Title Vesting: | Fee | ||||

| Mortgage Rate: | 4.7580% | Property Manager: | Self-managed | ||||

| Note Date: | March 9, 2018 | 4thMost Recent Occupancy (As of): | 78.7% (12/31/2014) | ||||

| Anticipated Repayment Date: | NAP | 3rdMost Recent Occupancy (As of): | 82.1% (12/31/2015) | ||||

| Maturity Date: | April 1, 2028 | 2ndMost Recent Occupancy (As of): | 88.4% (12/31/2016) | ||||

| IO Period: | 60 months | Most Recent Occupancy (As of): | 93.6% (12/31/2017) | ||||

| Loan Term (Original): | 120 months | Current Occupancy (As of)(4): | 91.6% (3/9/2018) | ||||

| Seasoning: | 3 month | ||||||

| Amortization Term (Original): | 360 months | Underwriting and Financial Information: | |||||

| Loan Amortization Type: | Interest-only, Amortizing Balloon | ||||||

| Interest Accrual Method: | Actual/360 | 4thMost Recent NOI (As of)(5): | $6,914,642 (12/31/2014) | ||||

| Call Protection: | L(27),D(89),O(4) | 3rdMost Recent NOI (As of)(5): | $6,200,743 (12/31/2015) | ||||

| Lockbox Type: | Hard/Upfront Cash Management | 2ndMost Recent NOI (As of)(5): | $7,766,054 (12/31/2016) | ||||

| Additional Debt(1): | Yes | Most Recent NOI (As of)(5): | $8,685,899 (12/31/2017) | ||||

| Additional Debt Type(1): | Pari Passu | ||||||

| U/W Revenues: | $14,588,909 | ||||||

| U/W Expenses: | $3,574,353 | ||||||

| Escrows and Reserves(3): | U/W NOI(4): | $11,014,555 | |||||

| U/W NCF: | $10,531,133 | ||||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NOI DSCR(1): | 1.34x | ||

| Taxes | $560,062 | $112,013 | NAP | U/W NCF DSCR(1): | 1.28x | ||

| Insurance | $0 | Springing | NAP | U/W NOI Debt Yield(1): | 8.4% | ||

| Immediate Repairs | $28,125 | $0 | NAP | U/W NCF Debt Yield(1): | 8.0% | ||

| Replacement Reserve | $0 | $6,801 | $244,818 | Appraised Value(6): | $226,000,000 | ||

| Leasing Reserve | $0 | $45,894 | $2,010,135(3) | Appraisal Valuation Date(6): | December 1, 2018 | ||

| Rent Concession Reserve | $842,933 | $0 | NAP | Cut-off Date LTV Ratio(1)(6): | 58.1% | ||

| Existing TI/LC Reserve | $7,649,629 | $0 | NAP | LTV Ratio at Maturity or ARD(1)(6): | 53.4% | ||

| (1) | See “The Mortgage Loan” section. All statistical financial information related to balance per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based on the funded outstanding principal balance of the Village at Leesburg Whole Loan (as defined below). |

| (2) | The Village at Leesburg Property (as defined below) was previously majority owned by an affiliate of the Carlyle Group, which originally developed the overall Village at Leesburg community in 2009. At the time of origination, an entity related to Rappaport (see “Borrower Sponsor” section) acquired a 60% equity ownership interest in the Village at Leesburg Property with the Carlyle Group maintaining a 40% equity ownership interest. |

| (3) | See “Escrows” section. |

| (4) | The Size, Cut-off Date Balance per SF and Current Occupancy assume the completion of the 12,297 square foot expansion related to Cobb Theatres (see “The Property” section). Excluding the expansion space, the Size, Cut-off Date Balance per SF and Current Occupancy are 533,810, $245.87 and 91.4%, respectively. |

| (5) | See “Cash Flow Analysis” section. |

| (6) | The Appraised Value and LTV Ratios shown are based on the appraiser’s Prospective Market Value Upon Completion, which assumes the completion of planned renovations and an expansion related to Cobb Theatres. Cobb Theatres is expected to renovate all existing auditoriums and add two new auditoriums with all work projected to be completed by November 2018 (see “The Property” section). Cobb Theatres is required to commence paying rent on its expanded premises once the tenant is open for business in such space. The underwritten base rent for Cobb Theatres is based on its expanded premises, and the difference between the tenant’s underwritten base rent and current base rent through December 31, 2018 was reserved upon origination of the Village at Leesburg Whole Loan (see “Major Tenants” section). In addition, outstanding tenant improvement obligations related to Cobb Theatres were reserved upon origination of the Village at Leesburg Whole Loan (see “Escrows” section). Based on the as-is appraised value of $205,000,000 (as of February 2, 2018), the Cut-off Date LTV Ratio and LTV Ratio at Maturity are 64.0% and 58.8%, respectively. |

The Mortgage Loan. The mortgage loan (the “Village at Leesburg Mortgage Loan”) is part of a whole loan (the “Village at Leesburg Whole Loan”) evidenced by twopari passu notes secured by a first mortgage encumbering the fee interest in an anchored retail shopping center located in Leesburg, Virginia (the “Village at Leesburg Property”). The Village at Leesburg Whole Loan was originated on March 9, 2018 by Wells Fargo Bank, National Association. The Village at Leesburg Whole Loan had an original principal balance of $131,250,000, has an outstanding principal balance as of the Cut-off Date of $131,250,000 and accrues interest at an interest rate of 4.7580%per annum. The Village at Leesburg Whole Loan had an initial term of 120 months, has a remaining term of 117 months as of the Cut-off Date and requires interest-only payments for the first 60 months following origination and, thereafter, requires payments of principal and interest based on a 30-year amortization schedule. The Village at Leesburg Whole Loan matures on April 1, 2028.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| VILLAGE AT LEESBURG |

The non-controlling Note A-2, which will be contributed to the WFCM 2018-C45 securitization trust, had an original principal balance of $65,250,000 and has an outstanding principal balance as of the Cut-off Date of $65,250,000. The controlling Note A-1, which has been contributed to the WFCM 2018-C44 securitization trust, had an original principal balance of $66,000,000 and has an outstanding principal balance as of the Cut-off Date of $66,000,000. The mortgage loan evidenced by Note A-1 is referred to herein as the “Village at Leesburg Companion Loan”. The lender provides no assurances that the non-securitizedpari passu note will not be split further. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced Pari Passu Whole Loans” and “Pooling and Servicing Agreement” in the Prospectus.

Note Summary

| Notes | Original Balance | Note Holder | Controlling Interest | |

| A-1 | $66,000,000 | WFCM 2018-C44 | Yes | |

| A-2 | $65,250,000 | WFCM 2018-C45 | No | |

| Total | $131,250,000 |

Following the lockout period, on any date before January 1, 2028, the borrower has the right to defease the Village at Leesburg Whole Loan in whole, but not in part. In addition, the Village at Leesburg Whole Loan is prepayable without penalty on or after January 1, 2028. The lockout period will expire on July 17, 2020.

Sources and Uses

| Sources | Uses | |||||||

| Original whole loan amount | $131,250,000 | 100.0% | Loan payoff(1): | $112,394,408 | 85.6% | |||

| Upfront reserves: | 9,080,749 | 6.9 | ||||||

| Closing costs: | 1,181,685 | 0.9 | ||||||

| Return of equity: | 8,593,158 | 6.5 | ||||||

| Total Sources | $131,250,000 | 100.0% | Total Uses | $131,250,000 | 100.0% |

| (1) | Prior to the origination of the Village at Leesburg Whole Loan, the Village at Leesburg Property was majority owned by an affiliate of the Carlyle Group, which originally developed the overall Village at Leesburg community in 2009. At the time of origination, an entity related to Rappaport (see “Borrower Sponsor” section) acquired a 60% equity ownership interest in the Village at Leesburg Property with the Carlyle Group maintaining a 40% equity ownership interest. The loan payoff shown represents a mortgage loan related to the Carlyle Group’s prior majority ownership of the Village at Leesburg Property. |

The Property.The Village at Leesburg Property consists of 546,107 square feet of retail, open-air lifestyle and entertainment space within the Village at Leesburg development in Leesburg, Virginia. The Village at Leesburg Property is situated on 55.0 acres of land and encompasses 16 one- and two-story buildings. In addition to the Village at Leesburg Property, the overall Village at Leesburg development contains office and multifamily components, which do not serve as collateral for the Village at Leesburg Whole Loan. The non-collateral office component comprises approximately 120,000 square feet of class A office space above the street level retail space and was 91.2% occupied as of April 2018, while the non-collateral multifamily component comprises 335 class A rental units with monthly rental rates for one-bedroom units starting at approximately $1,571. The Village at Leesburg Property was built in 2009, and in 2016, the Village at Leesburg development underwent a $6.6 million common area maintenance project that included upgrades to landscaping, patio seating, and the addition of a fountain and fire-pit. The Village at Leesburg Property hosts entertainment and cultural events throughout the year, including the Winter Ice Festival and ice carving in January, the Leesburg Fine Arts Festival in May, movie nights throughout the summer, Halloween activities and an annual holiday tree lighting in December. The Village at Leesburg Property has exclusive use of 3,128 surface and garage parking spaces, resulting in a parking ratio of 5.7 spaces per 1,000 square feet of rentable area (the overall Village at Leesburg development contains 3,732 surface and garage parking spaces, of which 604 spaces are for the exclusive use of the non-collateral multifamily units).

As of March 9, 2018, the Village at Leesburg Property was 91.6% leased to 65 tenants. In addition to the Wegmans grocery anchor, the tenant mix at the Village at Leesburg Property consists of entertainment options, including Cobb Theatres, Bowlero bowling alley, Atomic Trampoline and Luv2Play Indoor Playground; restaurant tenants, including Firebirds Wood Fire Grill, Travinia Italian Kitchen, Eggspectations, Noodles & Company, BurgerFi and Bon Chon Chicken; and national retail tenants including Ulta, Verizon Wireless, AT&T, European Wax Center, Massage Envy, Visionworks and GNC.

The Village at Leesburg Property is anchored by a Wegmans grocery store (Rated ‘BBB+’ by S&P, 142,692 square feet, 26.1% of net rentable area and 10.1% of underwritten base rent), which is subject to a ground lease with a lease expiration date in July 2034 with five, five-year renewal options. Wegmans is a regional supermarket chain with 96 stores in the northeastern United States. The company reported 2017 sales of approximately $8.7 billion and was ranked 31stof the top 75 supermarkets in the country based on sales volume by an industry news publication. The store provides customers with the convenience of an in-store pharmacy, a Market Café with take-out and in-store dining, a cheese shop, a sub shop, a fresh sushi shop, a salad bar, a pizza shop, a floral shop and a pastry shop.

The second largest tenant is Cobb Theatres (63,564 square feet, 11.6% of net rentable area and 15.0% of underwritten base rent), which currently features 12 screens with approximately 1,900 seats. Cobb Theatres is currently renovating its existing auditoriums with new, reclining seats and is expected to add two new auditoriums (for a total of 14 screens) with a total estimated renovation and construction cost of approximately $7.6 million. The existing auditorium renovations began in January 2018 and are expected to be completed by September 2018; while the expansion work is expected to begin by June 2018 and is expected to be completed by November 2018. With respect to Cobb Theatres, all outstanding tenant improvement costs and gap rent through December 31, 2018 were reserved upon origination of the Village at Leesburg Whole Loan. Cobb Theatres recently exercised a 10-year lease renewal and has a lease expiration date in December 2028 with three, five-year renewal options.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| VILLAGE AT LEESBURG |

The third largest tenant is LA Fitness (45,000 square feet, 8.2% of net rentable area and 9.1% of underwritten base rent). LA Fitness is a privately-owned American health club with headquarters in Irvine, California. LA Fitness has 675 locations across 27 states in the U.S. and Canada, serving over 3.8 million members. The LA Fitness at the Village at Leesburg Property features basketball courts, group fitness classes, indoor cycling, an indoor pool, a kids club, personal training, a racquetball court, a sauna, a whirlpool spa and a juice bar.

The fourth largest tenant is Bowlero (21,564 square feet, 3.9% net rentable area and 4.2% underwritten base rent). Bowlmor AMF, the owner of Bowlero, is the largest ten-pin bowling center operator in the world with over 300 locations. Bowlero leased the former King Pinz bowling alley space at the Village at Leesburg Property with a lease that commenced in March 2017.

The Village at Leesburg Property comprises two retail condominium units consisting of the Wegmans leased fee parcel (excluding the improvements), and the remaining retail space within the related project (having a 58.06% voting rights interest in each of (i) a condominium regime governing the common elements of the related mixed use buildings within the overall Village at Leesburg development and (ii) a master condominium regime governing the common areas within the overall Village of Leesburg development, including parking garages and structures and private streets). The loan documents provide for springing full recourse to the borrower and guarantors resulting from the condominium regime’s being withdrawn or terminated, or the master owners’ association regime being terminated. See“Description of the Mortgage Pool—Mortgage Pool Characteristics—Condominium Interests”in the Prospectus.

The following table presents certain information relating to the tenancy at the Village at Leesburg Property:

Major Tenants

| Tenant Name | Credit Rating (Fitch/Moody’s/ S&P)(1) | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF(2) | Annual U/W Base Rent(2) | % of Total Annual U/W Base Rent | Sales | Occupancy Cost | Lease Expiration Date |

| Anchor Tenant | |||||||||

| Wegmans (Ground Lease) | NR/NR/BBB+ | 142,692 | 26.1% | $8.30(3) | $1,184,921(3) | 10.1% | NAV | NAV | 7/31/2034(4) |

| Total Anchor Tenant | 142,692 | 26.1% | $8.30 | $1,184,921 | 100.0% | ||||

| Major Tenants | |||||||||

| Cobb Theatres | NR/NR/NR | 63,564(5) | 11.6% | $27.50(5) | $1,748,010(5) | 15.0% | $516,260(6) | 24.4%(6) | 12/31/2028(7) |

| LA Fitness | NR/NR/NR | 45,000 | 8.2% | $23.67 | $1,065,042 | 9.1% | NAV | NAV | 3/31/2026(8) |

| Bowlero | NR/B3/B | 21,564 | 3.9% | $22.49 | $485,000 | 4.2% | NAV | NAV | 3/31/2027(9) |

| Wells Fargo (Ground Lease) | AA-/Aa2/A+ | (10) | (10) | (10) | $430,532(11) | 3.7% | NAV | NAV | 11/14/2029(12) |

| Atomic Trampoline | NR/NR/NR | 16,653 | 3.0% | $19.26 | $320,736 | 2.7% | NAV | NAV | 8/31/2026(13) |

| Total Major Tenants | 289,473 | 53.0% | $16.59(14) | $5,234,241 | 44.8% | ||||

| Non-Major Tenants | 210,864 | 38.6% | $30.59(14) | $6,451,262 | 55.2% | ||||

| Occupied Collateral Total | 500,337 | 91.6% | $22.49(14) | $11,685,503 | 100.0% | ||||

| Vacant Space | 45,770 | 8.4% | |||||||

| Collateral Total | 546,107 | 100.0% | |||||||

| (1) | Certain ratings are those of the parent company whether or not the parent company guarantees the lease. |

| (2) | Annual U/W Base Rent PSF and Annual U/W Base Rent include contractual rent steps totaling $147,163 through January 2019 and straight-line rent averaging for investment grade tenants over the loan term for Wegmans and Wells Fargo (totaling $165,453) and over the remaining lease term for Charles Schwab (totaling $28,642). |

| (3) | Wegman’s Annual U/W Base Rent PSF and Annual U/W Base Rent are based on the tenant’s average rental rate over the loan term. Wegman’s current annual base rent is $1,065,000 ($7.46 per square foot). Commencing on August 1, 2019, Wegman’s annual base rent will increase to $1,164,367 ($8.16 per square foot) and commencing on August 1, 2024, Wegman’s annual base rent will increase to $1,265,678 ($8.87 per square foot). |

| (4) | Wegmans hasfive, five-year renewal options, with nine months’ notice, at rental rates as specified in the lease. |

| (5) | Cobb Theatres’ Tenant NRSF, Annual U/W Base Rent PSF and Annual U/W Base Rent assume the completion of the planned renovation and expansion, which are expected to be completed by November 2018 (see “The Property” section). The tenant’s current net rentable square footage, annual base rent per square foot and annual base rent are 51,267, $23.10 and $1,184,961, respectively. The tenant is required to begin paying rent on its expanded premises once it is open for business in such space, and the difference between the tenant’s underwritten base rent and current base rent through December 31, 2018 was reserved at origination of the Village at Leesburg Whole Loan. We cannot assure you that such renovation or expansion work will be completed or that the tenant will begin paying rent on such expansion space. |

| (6) | Sales and Occupancy Cost are for the trailing 12-month period ending December 31, 2017. Sales shown are per screen and based on the tenant’s current 12 screens; and occupancy cost shown is based on the tenant’s current annual base rent of $1,184,961 and underwritten reimbursements. |

| (7) | Cobb Theatres has three five-year renewal options, with nine months’ notice, at rental rates as specified in the lease. |

| (8) | LA Fitness has three five-year renewal options, with six months’ notice, at rental rates calculated in accordance with the Consumer Price Index or 12.0% greater than the minimum rent in effect immediately prior to the extension. |

| (9) | Bowlero has two five-year renewal options, with 180 days’ notice, at rental rates as specified in the lease. |

| (10) | Wells Fargo is subject to a ground lease and owns its improvements with no attributed square footage. |

| (11) | Wells Fargo’s Annual U/W Base Rent is based on the tenant’s average rental rate over the loan term. Wells Fargo’s current annual base rent is $385,000. Commencing on December 1, 2019, Wells Fargo’s annual base rent will increase to $423,519 and commencing on December 1, 2024, Wells Fargo’s annual base rent will increase to $465,838. |

| (12) | Wells Fargo has four five-year renewal options, with 270 days’ notice, at rental rates as specified in the lease. |

| (13) | Atomic Trampoline has one five-year renewal option, with 12 months’ notice, at rental rates as specified in the lease. |

| (14) | Annual U/W Base Rent PSF for Total Major Tenants, Non-Major Tenants and Occupied Collateral Total excludes Annual U/W Base Rent related to Wells Fargo, which is on a ground lease and owns its improvements with no attributed square footage. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| VILLAGE AT LEESBURG |

The following table presents certain information relating to the lease rollover schedule at the Village at Leesburg Property:

Lease Expiration Schedule(1)(2)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(3) | % of Total Annual U/W Base Rent(3) | Annual U/W Base Rent PSF(3)(4) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2018 | 2 | 5,819 | 1.1% | 5,819 | 1.1% | $171,678 | 1.5% | $29.50 |

| 2019 | 4 | 10,544 | 1.9% | 16,363 | 3.0% | $270,722 | 2.3% | $25.68 |

| 2020 | 13 | 35,568 | 6.5% | 51,931 | 9.5% | $1,566,326 | 13.4% | $44.04 |

| 2021 | 8 | 35,416 | 6.5% | 87,347 | 16.0% | $878,891 | 7.5% | $24.82 |

| 2022 | 4 | 16,161 | 3.0% | 103,508 | 19.0% | $455,520 | 3.9% | $28.19 |

| 2023 | 3 | 14,127 | 2.6% | 117,635 | 21.5% | $369,802 | 3.2% | $26.18 |

| 2024 | 4 | 17,290 | 3.2% | 134,925 | 24.7% | $402,174 | 3.4% | $23.26 |

| 2025 | 7 | 24,061 | 4.4% | 158,986 | 29.1% | $774,013 | 6.6% | $32.17 |

| 2026 | 6 | 76,309 | 14.0% | 235,295 | 43.1% | $1,955,297 | 16.7% | $25.62 |

| 2027 | 8 | 43,074 | 7.9% | 278,369 | 51.0% | $1,115,539 | 9.5% | $25.90 |

| 2028 | 4 | 79,276 | 14.5% | 357,645 | 65.5% | $2,110,088 | 18.1% | $26.62 |

| Thereafter | 2 | 142,692 | 26.1% | 500,337 | 91.6% | $1,615,453 | 13.8% | $11.32 |

| Vacant | 0 | 45,770 | 8.4% | 546,107 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 65 | 546,107 | 100.0% | $11,685,503 | 100.0% | $22.49 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the Lease Expiration Schedule. |

| (3) | Weighted Average Annual U/W Base Rent PSF and Total Annual U/W Base Rent exclude vacant space. |

| (4) | Annual U/W Base Rent PSF excludes Annual U/W Base Rent related to Wells Fargo, which is on a ground lease and owns its improvements. |

The following table presents historical occupancy percentages at the Village at Leesburg Mortgaged Property:

Historical Occupancy

12/31/2014(1) | 12/31/2015(1) | 12/31/2016(1) | 12/31/2017(1) | 3/9/2018(2) |

| 78.7% | 82.1% | 88.4% | 93.6% | 91.6% |

| (1) | Information obtained from the borrower. |

| (2) | Information obtained from the underwritten rent roll. Occupancy assumes the completion of the 12,297 square foot expansion related to Cobb Theatres (see “The Property” section). Excluding the expansion space, the physical occupancy as of March 9, 2018 was 91.4%. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| VILLAGE AT LEESBURG |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and the underwritten net cash flow at the Village at Leesburg Property:

Cash Flow Analysis

| 2014 | 2015(2) | 2016(3) | 2017(4) | U/W(5) | % of U/W Effective Gross Income | U/W $ per SF | |||||||||

| Base Rent | $8,506,614 | $7,561,648 | $8,431,880 | $9,277,247 | $11,685,503 | 80.1% | $21.40 | ||||||||

| Grossed Up Vacant Space | 0 | 0 | 0 | 0 | 1,532,967 | 10.5 | 2.81 | ||||||||

| Percentage Rent | 181,679 | 194,854 | 153,795 | 72,657 | 55,276 | 0.4 | 0.10 | ||||||||

| Total Reimbursables | 2,416,951 | 2,643,318 | 2,832,773 | 2,846,697 | 2,843,935 | 19.5 | 5.21 | ||||||||

| Other Income(1) | 89,005 | 49,684 | 129,044 | 179,020 | 4,195 | 0.0 | 0.01 | ||||||||

| Less Vacancy & Credit Loss | 0 | 0 | 0 | 0 | (1,532,967)(6) | (10.5) | (2.81) | ||||||||

| Effective Gross Income | $11,194,249 | $10,449,504 | $11,547,492 | $12,375,621 | $14,588,909 | 100.0% | $26.71 | ||||||||

| Total Operating Expenses | $4,279,607 | $4,248,761 | $3,781,438 | $3,689,722 | $3,574,353 | 24.5% | $6.55 | ||||||||

| Net Operating Income | $6,914,642 | $6,200,743 | $7,766,054 | $8,685,899 | $11,014,555 | 75.5% | $20.17 | ||||||||

| TI/LC | 0 | 0 | 0 | 0 | 403,415 | 2.8 | 0.74 | ||||||||

| Capital Expenditures | 0 | 0 | 0 | 0 | 80,007 | 0.5 | 0.15 | ||||||||

| Net Cash Flow | $6,914,642 | $6,200,743 | $7,766,054 | $8,685,899 | $10,531,133 | 72.2% | $19.28 | ||||||||

| NOI DSCR(7) | 0.84x | 0.75x | 0.94x | 1.06x | 1.34x | ||||||||||

| NCF DSCR(7) | 0.84x | 0.75x | 0.94x | 1.06x | 1.28x | ||||||||||

| NOI DY(7) | 5.3% | 4.7% | 5.9% | �� | 6.6% | 8.4% | |||||||||

| NCF DY(7) | 5.3% | 4.7% | 5.9% | 6.6% | 8.0% |

| (1) | Other income includes income from storage, stroller rentals, ATMs and other miscellaneous rental income. |

| (2) | The decline in Base Rent and Net Operating Income from 2014 to 2015 was driven partly by bad debt expense in 2015 from multiple tenants totaling $730,948. |

| (3) | The increase in Net Operating Income from 2015 to 2016 was primarily driven by an increase in Base Rent and decrease in Total Operating Expenses. The increase in Base Rent from 2015 to 2016 was driven by 13 new leases (10.6% of net rentable area, 12.6% of underwritten base rent) signed from March 2015 to December 2016 and three renewal leases (1.9% of net rentable area, 3.4% of underwritten base rent) signed from March 2015 to November 2015. The decrease in Total Operating Expenses from 2015 to 2016 was primarily driven by reduced expenses for snow removal, advertising and holiday decorating. |

| (4) | The increase in Base Rent and Net Operating Income from 2016 to 2017 was driven by eight new leases (7.2% of net rentable area, 10.1% of underwritten base rent) signed from January 2017 to July 2017 and two renewal leases (0.9% of net rentable area, 1.7% of underwritten base rent) signed from May 2017 to November 2017. |

| (5) | The increase in Net Operating Income from 2017 to U/W was driven by (i) three new leases(2.9% of net rentable area, 3.1% of underwritten base rent) and three renewal leases (1.8% of net rentable area, 2.4% of underwritten base rent) signed since January 2018; (ii) the inclusion of increased base rent for Cobb Theatres assuming the completion of the tenant’s planned renovation and expansion (annual base rent increase of $563,049; see “The Property” and “Major Tenants” sections); (iii) the inclusion ofcontractual rent steps totaling $147,163 through January 2019 and straight-line rent averaging for investment grade tenants over the lesser of the loan term and remaining lease term (totaling $194,095); and (iv) bad debt expenses in 2017 from multiple tenants totaling approximately $1.0 million. |

| (6) | The underwritten economic vacancy is 11.6%. The Village at Leesburg Property was 91.6% leased as of March 9, 2018. |

| (7) | The debt service coverage ratios and debt yields shown are based on the Village at Leesburg Whole Loan. |

Appraisal.The appraiser concluded to a Prospective Market Value Upon Completion for the Village at Leesburg Property of $226,000,000 as of December 1, 2018, which assumes the completion of the renovation and expansion related to Cobb Theatres.

Environmental Matters. According to a Phase I environmental site assessment dated February 23, 2018, there was no evidence of any recognized environmental conditions at the Village at Leesburg Property.

Market Overview and Competition.The Village at Leesburg Property is located in Leesburg, Loudoun County, Virginia, approximately 38.1 miles northwest of the Washington, D.C. central business district, 14.4 miles northwest of Washington Dulles International Airport and 1.7 miles southeast of U.S. Route 15. Per U.S. Census Bureau estimates, Loudoun County has the highest median household income of any county in the United States, and according to a third party market research report, the 2017 estimated average household income within a three- and five-mile radius of the Village at Leesburg Property was $144,117 and $151,624, respectively. According to the appraisal, Loudoun County has grown faster than any other Virginia jurisdiction since 1990, and the county’s population grew by approximately 3.7% annually from 2006 to 2016. According to a third party market research report, the estimated 2017 population within a three- and five-mile radius of the Village at Leesburg Property was 74,657 and 137,723, respectively.

The Metropolitan Washington Airports Authority is constructing a 23-mile extension of the existing Metrorail system, branching from the East Falls Church Station in Arlington, Virginia to the Washington Dulles International Airport and west to eastern Loudoun County. Phase 2 of the extension, expected to be completed in 2020, is expected to continue 11 miles from Wiehle Avenue to eastern Loudoun County. This phase will add six stations, including stops in Reston, Herndon, Dulles Airport, and Ashburn. The Ashburn Station is expected to be located approximately 9.7 miles southeast of the Village at Leesburg Property.

According to a third party market research report, the Village at Leesburg Property is situated within the Loudoun County submarket of the Suburban Virginia retail market. As of year-end 2017, the submarket reported total inventory of approximately 6.8 million square feet with a 3.0% vacancy rate and an average asking net rental rate of $29.13 per square foot. Submarket vacancy has decreased from 6.6% in 2012 and has averaged 4.4% in the last six years. The appraiser concluded to a weighted average net market rent for the Village at Leesburg Property of $22.89 per square foot.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| VILLAGE AT LEESBURG |

The table below presents certain information relating to five comparable properties to the Village at Leesburg Property identified by the appraiser:

Competitive Set(1)

Village at Leesburg (Subject) | Marketplace at Potomac Station | Fort Evan Plaza I | Fort Evans Plaza II | Battlefield Shopping Center | Leesburg Plaza | |

| Location | Leesburg, VA | Leesburg, VA | Leesburg, VA | Leesburg, VA | Leesburg, VA | Leesburg, VA |

| Distance from Subject | -- | 1.1 miles | 2.1 miles | 1.8 miles | 2.3 miles | 2.4 miles |

| Property Type | Lifestyle Center | Community Center | Community Center | Community Center | Power Center | Community Center |

| Year Built/Renovated | 2009/2018 | 2004/NAP | 1999/NAP | 2008/NAP | 1991/NAP | 1956/1992 |

| Anchors | Wegmans, Cobb Theatres, LA Fitness, Bowlero | Giant Food, Best Buy | Home Depot, Hobby Lobby | Marshall’s, Bed, Bath & Beyond, Walgreens, Jo-Ann Stores | Dick’s Sporting Goods, DSW, Ross Dress for Less, Staples, Stein Mart, Michael’s | Giant Food, Office Depot, PetSmart, Party City |

| Total GLA | 546,107 SF | 143,176 SF | 214,477 SF | 228,529 SF | 296,140 SF | 228,878 SF |

| Total Occupancy | 91.6%(2) | 92.0% | 97.0% | 100.0% | 97.0% | 96.0% |

| (1) | Information obtained from the appraisal. In total, the appraiser identified 10 comparable properties totaling approximately 2.7 million square feet with an average occupancy rate of approximately 96.0% and minimum occupancy rate of 90.0%. |

| (2) | Information obtained from underwritten rent roll. |

The Borrower.The borrower is CRP/TRC Leesburg Retail Owner, L.L.C., a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the Village at Leesburg Whole Loan. Gary D. Rappaport and the Gary D. Rappaport Revocable Trust, individually and/or collectively, are the guarantors of certain nonrecourse carveouts under the Village at Leesburg Whole Loan.

The Borrower Sponsor.The borrower sponsor is Gary D. Rappaport, the chief executive officer of Rappaport, a retail real estate company founded in 1984. Rappaport’s portfolio includes more than 50 shopping centers and ground floor retail spaces in approximately 125 mixed-use properties, both residential and office, located primarily throughout the mid-Atlantic region of the United States. Mr. Rappaport is the former chairman and trustee of the International Council of Shopping Centers and is the principal partner for approximately 4.3 million square feet of the shopping centers managed by Rappaport. At the time of origination of the Village at Leesburg Whole Loan, an entity related to Rappaport acquired a 60% equity interest in the Village at Leesburg Property. Gary D. Rappaport and affiliates owned an indirect and non-controlling 10% interest in an entity that defaulted on a loan that was the subject of a foreclosure in 2009. See“Description of the Mortgage Pool— Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings”in the Prospectus.

The remaining 40% equity interest in the Village at Leesburg Property is held by an affiliate of the Carlyle Group (“Carlyle”). Carlyle was the original developer of the overall Village at Leesburg community and was the majority owner of the Village at Leesburg Property prior to the origination of the Village at Leesburg Whole Loan. Founded in 1987 in Washington, D.C., Carlyle currently has approximately $195 billion of assets under management and more than 1,600 professionals operating in 31 offices in North America, South America, Europe, the Middle East, Africa, Asia and Australia. Carlyle’s real estate division has made more than 850 investments in 397 metropolitan statistical areas around the world. As of December 31, 2017, Carlyle’s real estate funds reported more than $18 billion in assets under management.

Escrows.The loan documents provide for upfront reserves of $560,062 for real estate taxes, $28,125 for immediate repairs, $842,933 for outstanding rent concessions and gap rent related to multiple tenants (including $520,190 related to the Cobb Theatres expansion) and $7,649,629 for existing tenant improvements and leasing commissions (“TI/LC”) related to multiple tenants (including $6,455,836 related to the Cobb Theatres renovation and expansion). The loan documents also provide for ongoing monthly reserves of $112,013 for real estate taxes, $6,801 for replacement reserves (subject to a cap of $244,818), and $45,894 for general TI/LCs (subject to a cap of $2,010,135 so long as no event of default exists and the net cash flow debt service coverage ratio is equal to or greater than 1.20x).

The loan documents do not require ongoing monthly escrows for insurance premiums as long as (i) no event of default has occurred and is continuing; (ii) the borrower provides the lender with evidence that the Village at Leesburg Property’s insurance coverage is included in a blanket policy and such policy is in full force and effect; and (iii) the borrower pays all applicable insurance premiums and provides the lender with evidence of renewals.

Lockbox and Cash Management.The Village at Leesburg Whole Loan requires a lender-controlled lockbox account, which is already in place, and that the borrower directs tenants to pay all rents directly into such lockbox account. The loan documents also require that all rents received by the borrower or the property manager be deposited into the lockbox account within one business day of receipt. All funds in the lockbox account are required to be swept each business day into the cash management account controlled by the lender and disbursed on each payment date in accordance with the loan documents. Prior to the occurrence of a Cash Trap Event Period (as defined below), all excess funds are required to be distributed to the borrower. During a Cash Trap Event Period, all excess funds are required to be swept to an excess cash flow subaccount.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| VILLAGE AT LEESBURG |

A “Cash Trap Event Period” will commence upon the earlier of the following:

| (i) | the occurrence of an event of default; |

| (ii) | the amortizing net cash flow debt service coverage ratio falling below 1.15x at the end of any calendar quarter; or |

| (iii) | the occurrence of a Lease Expiration Cash Trap Event Period (as defined below). |

A Cash Trap Event Period will end upon the occurrence of the following:

| ● | with regard to clause (i), the cure of such event of default; |

| ● | with regard to clause (ii), the amortizing net cash flow debt service coverage ratio being equal to or greater than 1.20x for two consecutive calendar quarters; or |

| ● | with regard to clause (iii), a Lease Expiration Cash Trap Event Period Cure (as defined below). |

A “Lease Expiration Cash Trap Event Period” will commence upon the earlier of the following:

| (i) | either Wegmans or Cobb Theatres giving notice of its intent to terminate its lease or vacate its space; |

| (ii) | either Wegmans or Cobb Theatres failing to be in actual, physical occupancy of its entire space, failing to be open to the public during customary hours or going dark; |

| (iii) | either Wegmans or Cobb Theatres becoming insolvent or filing for bankruptcy; or |

| (iv) | Cobb Theatres failing to extend its lease nine months prior to expiration upon terms and conditions reasonably satisfactory to the lender. |

A “Lease Expiration Cash Trap Event Period Cure” will occur upon the following:

| ● | with regard to clause (i), a Qualified Re-Leasing Event (as defined below); |

| ● | with regard to clause (ii), Wegmans or Cobb Theatres, as applicable, being in actual, physical possession of its entire space, being open to the public during customary hours and no longer being dark; |

| ● | with regard to clause (iii), Wegmans or Cobb Theatres, as applicable, being no longer insolvent or subject to any bankruptcy or insolvency proceedings and its lease having been affirmed or assigned pursuant to a final and non-appealable order of a court of competent jurisdiction; or |

| ● | with regard to clause (iv), Cobb Theatres extending its lease upon terms and conditions reasonably satisfactory to the lender. |

A “Qualified Re-Leasing Event” will occur upon one or more replacement tenants reasonably acceptable to the lender executing leases covering all of the space currently occupied by Wegmans or Cobb Theatres, as applicable, and delivering an estoppel certificate confirming such replacement tenants having taken physical occupancy of the entire space, commencing normal business operations and paying full unabated rent.

Property Management. The Village at Leesburg Property is managed by Rappaport Management Company, an affiliate of the borrower.

Assumption.The borrower has the two-time right to transfer the Village at Leesburg Property, provided that certain conditions are satisfied, including (i) no event of default has occurred and is continuing; (ii) the lender has reasonably determined that the proposed transferee and guarantor satisfy the lender’s credit review and underwriting standards, taking into consideration the transferee’s experience, financial strength and general business standing; and (iii) if required by the lender, rating agency confirmation from DBRS, Fitch and Moody’s that the transfer will not result in a downgrade, withdrawal or qualification of the respective ratings assigned to the Series WFCM 2018-C45 certificates and similar confirmations from each rating agency rating any securities backed by the Village at Leesburg Companion Loan with respect to the ratings of such securities.

Partial Release. Not permitted.

Real Estate Substitution.Not permitted.

Subordinate and Mezzanine Indebtedness.Not permitted.

Ground Lease. None.

Terrorism Insurance.The loan documents require that the “all risk” insurance policies required to be maintained by the borrower provide coverage for terrorism in an amount equal to the full replacement cost of the Village at Leesburg Property. The loan documents also require business interruption insurance covering no less than the 18-month period following the occurrence of a casualty event, together with a six-month extended period of indemnity.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| No. 2 – Westport Self Storage Portfolio | |||||||

| Loan Information | Property Information | ||||||

| Mortgage Loan Seller: | Wells Fargo Bank, National Association | Single Asset/Portfolio: | Portfolio | ||||

| Credit Assessment (DBRS/Fitch/Moody’s): | NR/NR/NR | Property Type: | Self Storage | ||||

| Original Principal Balance: | $48,300,000 | Specific Property Type: | Self Storage | ||||

| Cut-off Date Balance: | $48,300,000 | Location: | Various – See Table | ||||

| % of Initial Pool Balance: | 7.3% | Size: | 851,164 SF | ||||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF: | $56.75 | ||||

| Borrower Names(1): | Various | Year Built/Renovated: | Various – See Table | ||||

| Borrower Sponsor: | Westport Properties Inc. | Title Vesting: | Fee | ||||

| Mortgage Rate: | 4.680% | Property Manager: | Self-Managed | ||||

| Note Date: | June 8, 2018 | 4thMost Recent Occupancy(3): | NAV | ||||

| Anticipated Repayment Date: | NAP | 3rdMost Recent Occupancy(3): | NAV | ||||

| Maturity Date: | June 11, 2028 | 2ndMost Recent Occupancy (As of): | 80.3% (12/31/2016) | ||||

| IO Period: | 84 months | Most Recent Occupancy (As of): | 85.1% (12/31/2017) | ||||

| Loan Term (Original): | 120 months | Current Occupancy (As of): | 87.1% (5/21/2018) | ||||

| Seasoning: | 1 month | ||||||

| Amortization Term (Original): | 360 months | Underwriting and Financial Information: | |||||

| Loan Amortization Type: | Interest-only, Amortizing Balloon | 4thMost Recent NOI (As of)(4): | $4,113,114 (Annualized 10 or 11 12/31/2016) | ||||

| Interest Accrual Method: | Actual/360 | ||||||

| Call Protection: | L(25),D(91),O(4) | 3rdMost Recent NOI (As of)(4): | $4,767,136 (12/31/2017) | ||||

| Lockbox Type: | Springing | 2ndMost Recent NOI (As of): | $4,677,216 (TTM 5/31/2018) | ||||

| Additional Debt: | None | Most Recent NOI (As of): | $4,783,088 (Annualized 3 5/31/2018) | ||||

| Additional Debt Type: | NAP | ||||||

| U/W Revenues: | $8,105,950 | ||||||

| U/W Expenses: | $3,430,604 | ||||||

| U/W NOI: | $4,675,346 | ||||||

| U/W NCF: | $4,518,214 | ||||||

| U/W NOI DSCR: | 1.56x | ||||||

| U/W NCF DSCR: | 1.51x | ||||||

| Escrows and Reserves(2): | U/W NOI Debt Yield: | 9.7% | |||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NCF Debt Yield: | 9.4% | ||

| Taxes | $0 | Springing | NAP | As-Is Appraised Value(5): | $82,240,000 | ||

| Insurance | $0 | Springing | NAP | As-Is Appraisal Valuation Date(5) : | April 18, 2018 | ||

| Deferred Maintenance | $74,520 | $0 | NAP | Cut-off Date LTV Ratio(5) : | 58.7% | ||

| Replacement Reserves | $0 | Springing | NAP | LTV Ratio at Maturity(5) : | 56.0% | ||

| (1) | See “The Borrower” section. |

| (2) | See “Escrows” section. |

| (3) | The Westport Self Storage Portfolio Borrower (as defined below) acquired the Westport Self Storage Portfolio Properties (as defined below) on March 31, 2016 and historical occupancy prior to such date is not available. |

| (4) | See “Cash Flow Analysis” section. |

| (5) | The individual property level appraised values total $79,210,000, which would equate to a Cut-off Date LTV Ratio and LTV Ratio at Maturity of 61.0% and 58.1%, respectively; however, the appraiser concluded to a portfolio value of $82,240,000 based on the assumption that the entire portfolio is marketed to a single purchaser. |

The Mortgage Loan. The mortgage loan (the “Westport Self Storage Mortgage Loan”) is evidenced by a single promissory note secured by the fee interest in a 12-property self-storage portfolio located in Texas and Florida (the “Westport Self Storage Portfolio Properties”). The Westport Self Storage Mortgage Loan was originated on June 8, 2018 by Wells Fargo Bank, National Association. The Westport Self Storage Mortgage Loan had an original principal balance of $48,300,000, has an outstanding principal balance as of the Cut-off Date of $48,300,000 and accrues interest at an interest rate of 4.680%per annum. The Westport Self Storage Mortgage Loan had an initial term of 120 months, has a remaining term of 119 months as of the Cut-off Date and requires interest-only payments for the first 84 months following origination and, thereafter, requires payments of principal and interest based on a 30-year amortization schedule. The Westport Self Storage Mortgage Loan matures on June 11, 2028.

Following the lockout period, the borrower has the right to defease the Westport Self Storage Mortgage Loan in whole, or in part (see “Partial Release” section), on any date before March 11, 2028. In addition, the Westport Self Storage Mortgage Loan is prepayable without penalty on or after March 11, 2028.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| WESTPORT SELF STORAGE PORTFOLIO |

Sources and Uses

| Sources | Uses | |||||||

| Original loan amount | $48,300,000 | 100.0% | Loan payoff | $39,966,576 | 82.7% | |||

| Reserves | $74,520 | 0.2 | ||||||

| Closing costs | $667,552 | 1.4 | ||||||

| Return of equity | $7,591,352 | 15.7 | ||||||

| Total Sources | $48,300,000 | 100.0% | Total Uses | $48,300,000 | 100.0% |

The Properties. The Westport Self Storage Portfolio Properties comprise 12 self-storage properties totaling 851,164 square feet of rentable area, including 5,913 self storage units and 32,127 square feet of retail and commercial space, plus 406 RV parking spaces (see “Unit Mix” table below). The net rentable area of the Westport Self Storage Portfolio consists of approximately 96.2% self storage space and 3.8% retail and commercial space with no square footage attributed to the RV parking spaces. The Westport Self Storage Portfolio Properties range in size from 42,131 square feet to 176,939 square feet and were originally built between 1960 and 2002, with 10 properties having been renovated and/or expanded since 2004 (including eight since 2016).

The Westport Self Storage Portfolio Properties are located in Texas (10 properties; 748,537 square feet; 87.9% of net rentable area) and Florida (two properties; 102,627 square feet; 12.1% of net rentable area). Since acquiring the Westport Self Storage Portfolio Properties in 2016, the borrower sponsor has spent approximately $8.1 million in capital expenditures across the portfolio to rebrand the properties to US Storage Centers (“USSC”) and add CCTV security systems. As of May 21, 2018, the Westport Self Storage Portfolio Properties were 87.1% occupied with individual property occupancies ranging from 76.5% to 95.1% (see “Historical Occupancy” table below).

The following table presents certain information relating to the Westport Self Storage Portfolio Properties:

| Property Name – Location | Year Built/ Renovated | Allocated Cut-off Date Balance | % of ALA | Appraised Value(1) | Allocated LTV | UW NCF | % UW NCF |

| San Antonio/Boerne USSC – San Antonio/Boerne, TX | 1984/2004 | $9,437,217 | 19.5% | $15,640,000 | 60.3% | $868,811 | 19.2% |

| Fort Worth USSC – Fort Worth, TX | 2001/2016 | $5,407,616 | 11.2% | $8,920,000 | 60.6% | $483,788 | 10.7% |

| Grissom USSC – San Antonio, TX | 1987/2016 | $5,054,009 | 10.5% | $7,830,000 | 64.5% | $502,664 | 11.1% |

| Laredo USSC – San Antonio, TX | 2000/2016 | $4,662,017 | 9.7% | $7,870,000 | 59.2% | $435,928 | 9.6% |

| Austin USSC – Austin, TX | 1983/2016 | $4,291,045 | 8.9% | $7,790,000 | 55.1% | $418,084 | 9.3% |

| Tampa USSC – Tampa, FL | 1987/NAP | $3,454,403 | 7.2% | $5,300,000 | 65.2% | $315,043 | 7.0% |

| Harker Heights USSC – Harker Heights, TX | 2002/2016 | $3,450,344 | 7.1% | $5,320,000 | 64.9% | $317,966 | 7.0% |

| Denton USSC – Denton, TX | 1960/2016 | $3,356,378 | 6.9% | $5,600,000 | 59.9% | $352,264 | 7.8% |

| Floresville USSC – Floresville, TX | 1986/2006 | $3,306,223 | 6.8% | $5,070,000 | 65.2% | $314,230 | 7.0% |

| Blanco USSC – San Antonio, TX | 1986/2016 | $2,933,616 | 6.1% | $4,660,000 | 63.0% | $285,453 | 6.3% |

| Houston Hinman USSC – Houston, TX | 1975/2016 | $1,571,800 | 3.3% | $2,710,000 | 58.0% | $96,647 | 2.1% |

| Ocala USSC – Ocala, FL | 1989/NAP | $1,375,332 | 2.8% | $2,500,000 | 55.0% | $127,336 | 2.8% |

| Total/Weighted Average | $48,300,000 | 100.0% | $82,240,000 | 58.7% | $4,518,214 | 100.0% |

| (1) | The individual property level appraised values total $79,210,000, which would equate to a Cut-off Date LTV Ratio and LTV Ratio at Maturity of 61.0% and 58.1%, respectively; however, the appraiser concluded to a portfolio value of $82,240,000 based on the assumption that the entire portfolio is marketed to a single purchaser. |

The following table presents detailed information with respect to the unit mix of the Westport Self Storage Portfolio Properties:

Unit Mix

| Property Name | Net Rentable Area (SF)(1) | % GLA | Self Storage Units | Commercial Space (SF) | RV Parking Units |

| San Antonio/Boerne USSC | 176,939 | 20.8% | 741 | 11,055 | 45 |

| Fort Worth USSC | 65,140 | 7.7% | 453 | 0 | 60 |

| Grissom USSC | 100,320 | 11.8% | 330 | 0 | 276 |

| Laredo USSC | 56,706 | 6.7% | 577 | 0 | 8 |

| Austin USSC | 62,402 | 7.3% | 707 | 0 | 0 |

| Tampa USSC | 60,496 | 7.1% | 435 | 0 | 1 |

| Harker Heights USSC | 66,075 | 7.8% | 464 | 0 | 4 |

| Denton USSC | 61,533 | 7.2% | 524 | 18,000 | 0 |

| Floresville USSC | 56,197 | 6.6% | 369 | 3,072 | 0 |

| Blanco USSC | 51,205 | 6.0% | 490 | 0 | 0 |

| Houston Hinman USSC | 52,020 | 6.1% | 466 | 0 | 0 |

| Ocala USSC | 42,131 | 4.9% | 357 | 0 | 12 |

| Total/Weighted Average | 851,164 | 100% | 5,913 | 32,127 | 406 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| WESTPORT SELF STORAGE PORTFOLIO |

The following table presents historical occupancy percentages at the Westport Self Storage Portfolio Properties:

Historical Occupancy(1)

| Property Name | 12/31/2016(2) | 12/31/2017(2) | 5/21/2018(3) |

| San Antonio/Boerne USSC | 87.6% | 90.2% | 88.9% |

| Fort Worth USSC | 76.9% | 90.6% | 88.8% |

| Grissom USSC | 94.3% | 93.9% | 95.1% |

| Laredo USSC | 92.6% | 88.3% | 89.7% |

| Austin USSC | 72.8% | 78.8% | 80.3% |

| Tampa USSC | 82.5% | 91.6% | 83.6% |

| Harker Heights USSC | 81.3% | 87.3% | 89.2% |

| Denton USSC | 73.7% | 82.7% | 83.2% |

| Floresville USSC | 84.7% | 86.8% | 82.4% |

| Blanco USSC | 89.0% | 89.4% | 90.2% |

| Houston Hinman USSC | 68.8% | 34.8%(4) | 76.5% |

| Ocala USSC | 74.3% | 82.6% | 86.8% |

| Total/Weighted Average | 83.0% | 85.1% | 87.1% |

| (1) | The Westport Self Storage Portfolio Borrower acquired the Westport Self Storage Portfolio Properties on March 31, 2016, and historical occupancy is not available prior to such date. |

| (2) | Information obtained from the Westport Self Storage Portfolio Borrower. |

| (3) | Information obtained from the underwritten rent roll. |

| (4) | The decline in occupancy at the Houston Hinman USSC property from 2016 to 2017 was due to damage sustained from Hurricane Harvey. |

Operating History and Underwritten Net Cash Flow.The following table presents certain information relating to the historical operating performance and the underwritten net cash flow at the Westport Self Storage Portfolio Properties:

Cash Flow Analysis

| Annualized 10 or 11 12/31/2016(1) | 2017(2) | TTM 5/31/2018 | Annualized 3 5/31/2018 | U/W | % of U/W Effective Gross Income | U/W $ per SF | |||||||||

| Base Rent | $6,491,761 | $6,981,609 | $7,037,957 | $6,914,044 | $7,285,656(4) | 89.9% | $8.56 | ||||||||

| Grossed Up Vacant Space | 0 | 0 | 0 | 0 | 1,242,624 | 15.3 | 1.46 | ||||||||

| Other Income(3) | 953,817 | 997,930 | 936,219 | 988,076 | 988,076 | 12.2 | 1.16 | ||||||||

| Retail/Commercial | 144,781 | 348,052 | 372,326 | 387,336 | 323,114 | 4.0 | 0.38 | ||||||||

| Less Vacancy and Credit Loss | (340,639) | (443,133) | (349,086) | (182,320) | (1,733,520)(5) | (21.4) | (2.04) | ||||||||

| Effective Gross Income | $7,249,719 | $7,884,458 | $7,997,416 | $8,107,136 | $8,105,950 | 100.0% | $9.52 | ||||||||

| Total Operating Expenses | $3,136,605 | $3,117,322 | $3,320,200 | $3,324,048 | $3,430,604 | 42.3% | $4.03 | ||||||||

| Net Operating Income | $4,113,114 | $4,767,136 | $4,677,216 | $4,783,088 | $4,675,346 | 57.7% | $5.49 | ||||||||

| Capital Expenditures | 0 | 0 | 0 | 0 | 157,132 | 1.9 | 0.18 | ||||||||

| Net Cash Flow | $4,113,114 | $4,767,136 | $4,677,216 | $4,783,088 | $4,518,214 | 55.7% | $5.31 | ||||||||

| NOI DSCR | 1.37x | 1.59x | 1.56x | 1.59x | 1.56x | ||||||||||

| NCF DSCR | 1.37x | 1.59x | 1.56x | 1.59x | 1.51x | ||||||||||

| NOI DY | 8.5% | 9.9% | 9.7% | 9.9% | 9.7% | ||||||||||

| NCF DY | 8.5% | 9.9% | 9.7% | 9.9% | 9.4% |

| (1) | Of the 12 Westport Self Storage Portfolio properties, financials for four properties represent trailing 10-month annualized financials ending December 31, 2016, and financials for the remaining eight properties represent trailing 11-month annualized financials ending December 31, 2016. |

| (2) | 2017 NOI is higher than Annualized 10 or 11 2016 NOI due in part to a $247,384 increase in other income, primarily driven by retail and commercial tenant income, and an overall increase in occupancy from 80.3% as of December 31, 2016 to 85.1% as of December 31, 2017. |

| (3) | Other Income consists of late fees, administrative fees, retail merchandise sales, truck rental income, postal box income, income from two cell tower leases (at the San Antonio/Boerne USSC property and Blanco USSC property) and two billboard leases (at the San Antonio/Boerne USSC property and Ocala USSC property), and tenant insurance. |

| (4) | Underwritten Base Rent comprises approximately 95.3% of income from self storage units and 4.7% of income from RV parking income. |

| (5) | The underwritten economic vacancy is 20.3%. As of May 21, 2018, the Westport Self Storage Portfolio Properties were 87.1% physically occupied. |

Appraisal.The appraiser concluded to an “as is” appraised value for the Westport Self Storage Portfolio Properties of $82,240,000 as of April 18, 2018.

Environmental Matters. According to the Phase I environmental site assessments dated April 30, 2018, there are no recognized environmental conditions at the Westport Self Storage Portfolio Properties.

Market Overview and Competition. The Westport Self Storage Portfolio Properties are located in eight cities in Texas (87.9% of net rentable area) and two cities in Florida (12.1% of net rentable area). Within a five-mile radius of the Westport Self Storage Portfolio Properties, the average estimated population and median household income are 185,670 and $78,311, respectively (see table below).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| WESTPORT SELF STORAGE PORTFOLIO |

Four of the Westport Self Storage Portfolio Properties are located in San Antonio, Texas (45.7% of the allocated loan amount and 45.3% of net rentable area). According to the appraisal, the overall San Antonio self storage market reported an average vacancy rate of 13.4% from 2011 to 2017, with a 2017 vacancy rate of 14.4%.

The following table presents certain demographic information with respect to the Westport Self Storage Portfolio Properties:

Demographic Summary(1)

| Property | City | State | 2017/2018 Population (within 1- ,3- , 5-mile radius) | 2017/2018 Median Income (within 1- ,3- , 5-mile radius) |

| San Antonio/Boerne USSC | San Antonio/Boerne | TX | 4,552, 23,555, 36,905 | $115,357, $127,041, $126,484 |

| Fort Worth USSC | Fort Worth | TX | 11,873, 98,031, 216,520 | $89,197, $93,373, $89,624 |

| Grissom USSC | San Antonio | TX | 4,552, 23,555, 36,905 | $115,357, $127,041, $126,484 |

| Laredo USSC | San Antonio | TX | 4,552, 23,555, 36,905 | $115,357, $127,041, $126,484 |

| Austin USSC | Austin | TX | 19,953, 144,227, 308,009 | $46,068, $46,129, $53,641 |

| Tampa USSC | Tampa | FL | 106,870, 250,987, 757,077 | $32,915, $42,031, $49,471 |