| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-226486-16 |

| | | |

Free Writing Prospectus

Structural and Collateral Term Sheet

$720,172,953

(Approximate Initial Pool Balance)

BANK 2020-BNK28

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Morgan Stanley Mortgage Capital Holdings LLC

Bank of America, National Association

Wells Fargo Bank, National Association

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2020-BNK28

September 14, 2020

WELLS FARGO

SECURITIES | BofA SECURITIES | MORGAN STANLEY |

| | | |

Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

| | | |

Academy Securities, Inc. Co-Manager | | Drexel Hamilton Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-226486) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, BofA Securities, Inc., Morgan Stanley & Co. LLC, Academy Securities, Inc., Drexel Hamilton, LLC or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-2

| BANK 2020-BNK28 | Transaction Highlights |

I. Transaction Highlights

Mortgage Loan Sellers:

| Mortgage Loan Seller | | Number of

Mortgage Loans | | Number of

Mortgaged

Properties | | Aggregate Cut-off Date Balance | | Approx. % of Initial Pool

Balance |

| Morgan Stanley Mortgage Capital Holdings LLC | | 23 | | | 40 | | | $321,196,000 | | | 44.6 | % |

| Bank of America, National Association | | 8 | | | 29 | | | 295,885,000 | | | 41.1 | |

| Wells Fargo Bank, National Association | | 23 | | | 23 | | | 103,091,953 | | | 14.3 | |

| Total | | 54 | | | 92 | | | $720,172,953 | | | 100.0 | % |

Loan Pool:

| Initial Pool Balance: | $720,172,953 |

| Number of Mortgage Loans: | 54 |

| Average Cut-off Date Balance per Mortgage Loan: | $13,336,536 |

| Number of Mortgaged Properties: | 92 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $7,827,967 |

| Weighted Average Mortgage Interest Rate: | 3.505% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 64.7% |

| Weighted Average Original Term to Maturity (months): | 120 |

| Weighted Average Remaining Term to Maturity (months): | 118 |

| Weighted Average Original Amortization Term (months)(2): | 365 |

| Weighted Average Remaining Amortization Term (months)(2): | 363 |

| Weighted Average Seasoning (months): | 2 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 3.33x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 13.8% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 51.2% |

| Weighted Average Balloon Loan-to-Value Ratio(1): | 49.0% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 7.6% |

| % of Mortgage Loans with Single Tenants(3): | 13.6% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property are calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the loan-to-value ratio is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | Fifteen (15) of the mortgage loans, each of which is secured by a residential cooperative property originated by National Cooperative Bank, N.A. or National Consumer Cooperative Bank and sold to the depositor by Wells Fargo Bank, National Association, currently have in place subordinate secured lines of credit to the related mortgage borrowers that permit future advances (such loans, collectively, the “Subordinate Coop LOCs”). The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” and “Description of the Mortgage Pool—Additional Indebtedness—Other Secured Indebtedness—Additional Debt Financing for Mortgage Loans Secured by Residential Cooperatives Sold to the Depositor by Wells Fargo Bank, National Association.” in the Preliminary Prospectus. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-3

| BANK 2020-BNK28 | Transaction Highlights |

II. COVID-19 Update

The following table contains information regarding the status of the Mortgage Loans and Mortgaged Properties provided by the respective borrowers as of the date set forth in the “Information As Of Date” column. The cumulative effects of the COVID-19 emergency on the global economy may cause tenants to be unable to pay their rent and borrowers to be unable to pay debt service under the Mortgage Loans. As a result, we cannot assure you that the information in the following table is indicative of future performance or that tenants or borrowers will not seek rent or debt service relief (including forbearance arrangements) or other lease or loan modifications in the future. Such actions may lead to shortfalls and losses on the certificates. Any information in the following table will be superseded by the information contained under the heading “Description of the Mortgage Pool—COVID-19 Considerations” in the Preliminary Prospectus.

Mortgage Loan Seller | Information As Of Date | Origination Date | Property Name | Property Type | July Debt Service Payment Received (Y/N) | August Debt Service Payment Received (Y/N) | September Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested (Y/N) | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Total SF or Unit Count Making Full July Rent Payment (%) | UW July Base Rent Paid (%) | Total SF or Unit Count Making Full August Rent Payment (%) | UW August Base Rent Paid (%) |

| BANA | 9/8/2020 | 9/4/2020 | 9th & Thomas | Office | NAP(1) | NAP(1) | NAP(1) | N | N | Y(2) | 99.6% | 99.6% | 96.1% | 96.2% |

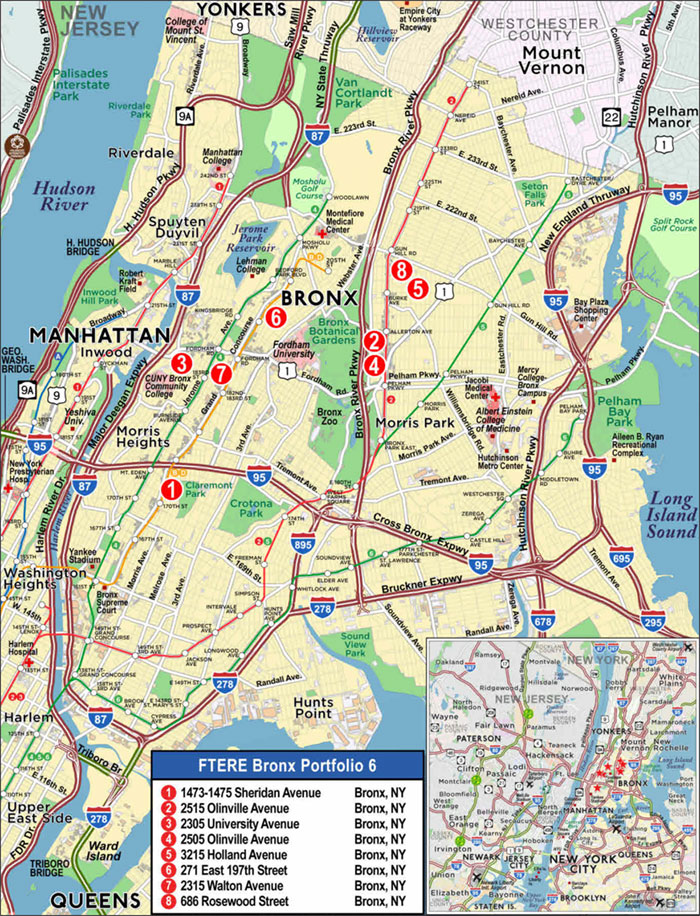

| MSMCH | 9/9/2020 | 3/17/2020 | FTERE Bronx Portfolio 6 | Multifamily | Y | Y | Y | Y(3) | N | N | 74.5% | 74.5% | 79.3% | 79.3% |

| BANA | 9/9/2020 | 3/6/2020 | 711 Fifth Avenue | Mixed Use | Y | Y | Y | N | N | Y(4) | 100.0% | 100.0% | 100.0% | 100.0% |

| BANA | 9/8/2020 | 9/2/2020 | ExchangeRight Net Leased Portfolio #39 | Various | NAP(1) | NAP(1) | NAP(1) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% |

| MSMCH | 8/21/2020 | 8/28/2020 | 329 Wyckoff Mills Road | Industrial | NAP(5) | NAP(5) | NAP(5) | N | N | N | NAP(6) | NAP(6) | NAP(6) | NAP(6) |

| MSMCH | 8/25/2020 | 7/31/2020 | Waterfront Clematis | Mixed Use | NAP(5) | NAP(5) | Y | N | N | Y(7) | 94.6% | 95.7% | 94.6% | 95.7% |

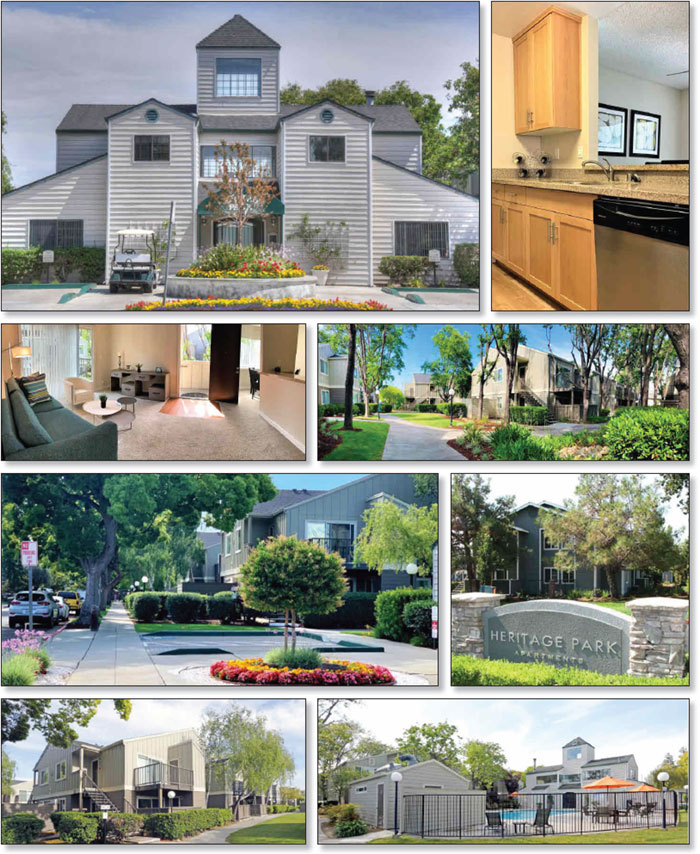

| BANA | 9/8/2020 | 9/4/2020 | Heritage Park Apartments | Multifamily | NAP(1) | NAP(1) | NAP(1) | N | N | N | 99.7% | 99.7% | 99.8% | 99.8% |

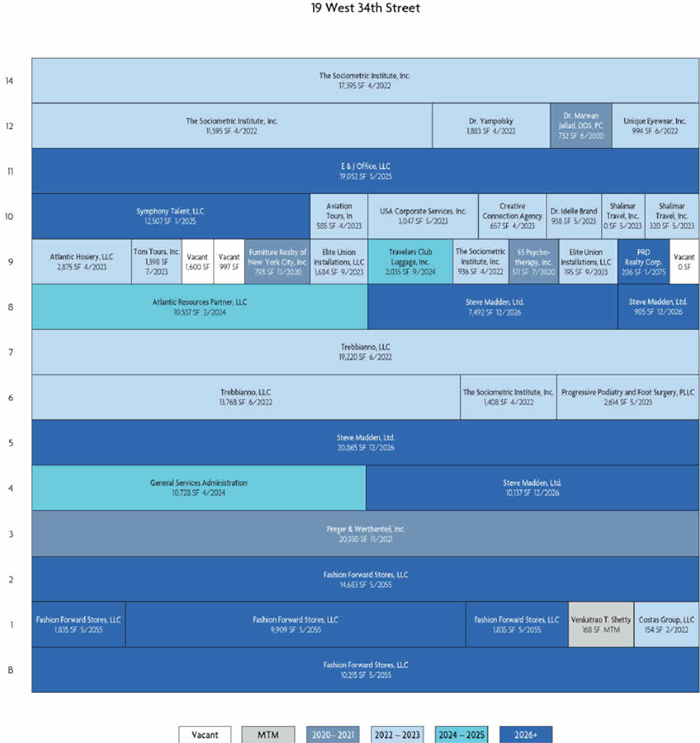

| BANA | 9/9/2020 | 6/30/2020 | 19 West 34th Street | Mixed Use | Y | Y | Y | N | N | Y(8) | 99.3% | 99.4% | 76.0% | 81.0% |

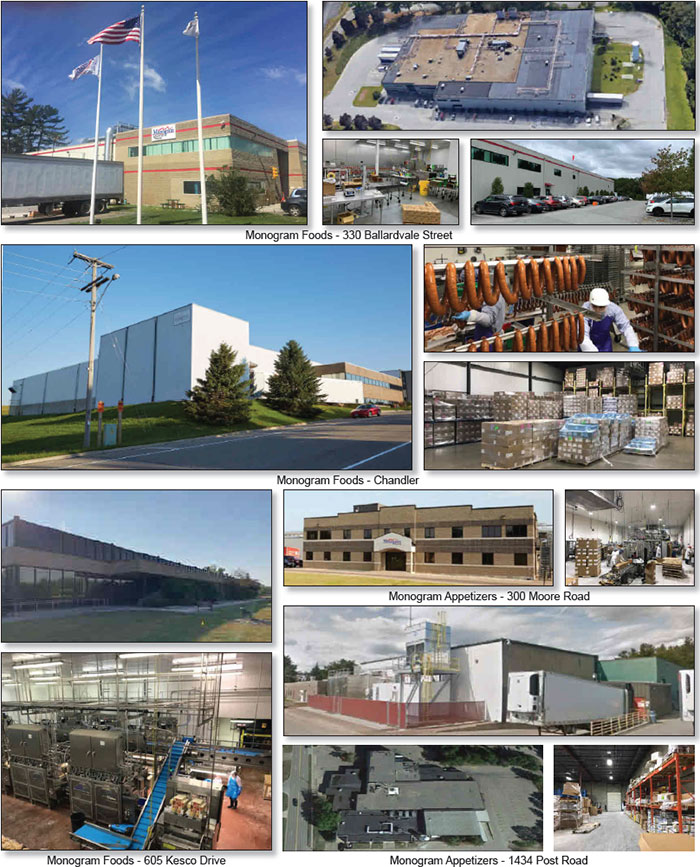

| BANA | 9/8/2020 | 2/7/2020 | Monogram Portfolio | Industrial | Y | Y | Y | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% |

| MSMCH | 9/1/2020 | 8/31/2020 | Chasewood Technology Park | Office | NAP(5) | NAP(5) | NAP(5) | N | N | Y(9) | 99.0% | 98.6% | 90.1% | 87.7% |

| MSMCH | 9/2/2020 | 7/31/2020 | 305 East 72nd Street | Retail | NAP(5) | NAP(5) | Y | N | N | Y(10) | 90.1% | 88.5% | 85.1% | 99.1%(11) |

| WFB | 9/10/2020 | 3/18/2020 | 754-768 Brady Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 95.9%(12) | NAP(13) | 93.4%(12) | NAP(13) |

| MSMCH | 9/10/2020 | 9/1/2020 | Austin Storage Portfolio | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 98.0% | 94.6% | 98.2% | 96.0% |

| WFB | 9/4/2020 | 9/9/2020 | Harbor Point Multifamily Leased Fee | Other | NAP(14) | NAP(14) | NAP(14) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% |

| BANA | 8/31/2020 | 7/31/2020 | Central Self Storage Corte Madera | Self Storage | NAP(15) | Y | Y | N | N | N | 97.8% | 99.8% | 98.5% | 99.9% |

| MSMCH | 9/1/2020 | 8/21/2020 | Cubesmart Portfolio Baton Rouge | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 97.7% | 97.7% | NAP(16) | NAP(16) |

| MSMCH | 8/25/2020 | 8/24/2020 | Rego Multifamily Portfolio II | Multifamily | NAP(5) | NAP(5) | NAP(5) | N | N | N | 98.4% | 98.4% | 97.3% | 97.3% |

| WFB | 9/10/2020 | 8/25/2020 | 4275 & 4283 El Cajon Boulevard | Office | NAP(14) | NAP(14) | NAP(14) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% |

| WFB | 9/1/2020 | 7/17/2020 | Sundance Self Storage | Self Storage | NAP(17) | NAP(17) | Y(18) | N | N | N | 98.8% | 97.1% | 98.4% | 96.9% |

| MSMCH | 8/31/2020 | 9/1/2020 | Villa Victoria Apartments | Multifamily | NAP(5) | NAP(5) | NAP(5) | N | N | N | 98.3% | 98.3% | 98.3% | 98.3% |

| MSMCH | 9/3/2020 | 7/29/2020 | JCG III Industrial Complex | Industrial | NAP(5) | NAP(5) | Y | N | N | Y(19) | 100.0% | 100.0% | 100.0% | 100.0% |

| WFB | 9/10/2020 | 2/28/2020 | Cherry Valley Apartments Inc. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 98.4%(12) | NAP(13) | 94.8%(12) | NAP(13) |

| MSMCH | 9/3/2020 | 3/6/2020 | 33 1 3 @ Thirtyfourth | Retail | Y | Y | Y | N | N | Y(20) | 78.1% | 75.2% | 84.4%(21) | 83.8%(21) |

| BANA | 9/9/2020 | 8/21/2020 | Palm Springs Airport Self Storage | Self Storage | NAP(17) | NAP(17) | Y | N | N | N | 97.2% | 99.7% | 97.5% | 99.8% |

| MSMCH | 9/2/2020 | 8/28/2020 | Lancaster Towne Center | Retail | NAP(5) | NAP(5) | NAP(5) | N | N | Y(22) | 86.9% | 79.5% | 95.8% | 93.1% |

| MSMCH | 9/1/2020 | 9/2/2020 | Storage Max Tyler | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 100.0% | 100.0% | 94.8% | 94.8% |

| MSMCH | 9/1/2020 | 9/1/2020 | Storage Depot Beaumont | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | NAP(16) | NAP(16) | NAP(16) | NAP(16) |

| MSMCH | 9/10/2020 | 3/4/2020 | 1602 Spruce Street & 238 South 20th Street | Mixed Use | Y | Y | Y | Y(23) | N | Y(24) | 76.1% | 76.1% | NAP(16) | NAP(16) |

| WFB | 9/8/2020 | 8/11/2020 | Hardin Station | Retail | NAP(17) | NAP(17) | (18) | N | N | Y(25) | 93.8%(26) | 100.0% | 93.8%(26) | 100.0% |

| WFB | 9/10/2020 | 2/25/2020 | 20 Plaza Housing Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 93.9%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/25/2020 | 121 W. 72nd St. Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 97.6%(12) | NAP(13) | NAP(27) | NAP(13) |

| MSMCH | 9/1/2020 | 8/18/2020 | AAA Self Storage - Kernersville NC | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 96.0% | 96.0% | 99.4% | 99.4% |

| MSMCH | 8/21/2020 | 8/10/2020 | Walgreens Pembroke Pines | Retail | NAP(5) | NAP(5) | NAP(5) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% |

| MSMCH | 9/2/2020 | 8/7/2020 | Spicewood Self Storage | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 99.8% | 99.8% | 100.0% | 100.0% |

| WFB | 9/10/2020 | 3/18/2020 | Larchmont Hills Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | 97.0%(12) | NAP(13) |

| WFB | 9/10/2020 | 2/13/2020 | 15455 Memorial Drive | Retail | Y | Y | (18) | Y(28) | N | Y(29) | 83.7%(29) | 85.7% | 93.8%(29) | 93.7% |

| MSMCH | 9/1/2020 | 9/2/2020 | Convenient Self Storage | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 93.2% | 93.2% | 93.1% | 93.1% |

| MSMCH | 8/31/2020 | 9/1/2020 | Execuplex Mini Storage Center | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 99.4% | 99.4% | 99.4% | 99.4% |

| WFB | 9/10/2020 | 2/26/2020 | 2187 Holland Avenue Apartment Corp. f/k/a Marbreff Syndicate, Inc. | Multifamily - Cooperative | Y | Y | Y | N | N | N | NAP(27) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/20/2020 | Kirby at Southfork | Retail | Y | Y | (18) | Y(28) | N | Y(30) | 72.7%(30) | 84.0% | 91.4%(30) | 100.0% |

| MSMCH | 9/2/2020 | 9/2/2020 | Store More Self Storage | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | NAP(16) | NAP(16) | NAP(16) | NAP(16) |

| MSMCH | 8/31/2020 | 8/5/2020 | Liberty Self Storage | Self Storage | NAP(5) | NAP(5) | NAP(5) | N | N | N | 98.7% | 95.9% | 99.7% | 98.9% |

| WFB | 9/10/2020 | 2/27/2020 | 657 Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | NAP(27) | NAP(13) | NAP(27) | NAP(13) |

| MSMCH | 8/27/2020 | 2/20/2020 | F-B Plaza | Retail | Y | Y | Y | N | N | Y(31) | 79.5% | 89.2% | 79.5% | 89.2% |

| WFB | 9/10/2020 | 3/18/2020 | 41-15 44th Street Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 84.1%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/27/2020 | 35 Eastern Parkway Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/27/2020 | 82 Horatio Owners Ltd. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 98.5%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/24/2020 | Ten West Eighty-Six Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 96.7%(12) | NAP(13) | 96.7%(12) | NAP(13) |

| WFB | 9/10/2020 | 2/28/2020 | 21 Chapel Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | 100.0%(12) | NAP(13) |

| WFB | 9/10/2020 | 3/3/2020 | Carlton Terrace Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 2/27/2020 | Annapurna Real Estate Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | 100.0%(12) | NAP(13) |

| WFB | 9/10/2020 | 3/17/2020 | Whitney Realty Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 88.9%(12) | NAP(13) | NAP(27) | NAP(13) |

| WFB | 9/10/2020 | 3/5/2020 | 175 PPSW Owners Corp. | Multifamily - Cooperative | Y | Y | Y | N | N | N | 100.0%(12) | NAP(13) | 100.0%(12) | NAP(13) |

| WFB | 9/10/2020 | 2/20/2020 | Crossroads Owners Corp. | Multifamily – Cooperative | Y | Y | Y | N | N | N | NAP(27) | NAP(13) | NAP(27) | NAP(13) |

| (1) | The related mortgage loan has its first due date in November 2020. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-4

| BANK 2020-BNK28 | Transaction Highlights |

| (2) | Thomas Street Warehouse Restaurant (2.5% of NRA and 2.4% of underwritten base rent), a full service restaurant and bar, was provided with a base rent abatement for April, August and September 2020 and is currently under negotiations for a rent deferral strategy that would allow the tenant flexibility and time to implement a menu that could be supported by delivery and to-go sales. Jack’s BBQ (1.0% of NRA and 1.0% of underwritten base rent) was provided with two months of base rent abatement for April and August 2020 and resumed full rental payments in September 2020. Elm Coffee (0.4% of NRA and 0.4% of underwritten base rent) was provided with five months of base rent abatement (May through September 2020). |

| (3) | With respect to the FTERE Bronx Portfolio 6 mortgage loan, the borrowers submitted a forbearance/loan modification request on April 2, 2020, which included (i) forbearance of debt service payments through July 31, 2020, with the deferred payments due on the maturity date, (ii) a 50% reduction of interest payments from August 1, 2020 through December 31, 2020, with the remainder due on the maturity date, (iii) waiver of escrow deposits through December 31, 2020, (iv) release of escrow funds to be utilized for operation of the FTERE Bronx Portfolio 6 Properties, and (v) suspension of financial covenants and cash management or other consequences which might arise from such covenants. The request was formally withdrawn by the FTERE Bronx Portfolio 6 borrowers on May 27, 2020. |

| (4) | As of May 18, 2020, the borrower has entered into a rent deferral agreement with the sixth largest tenant at the property, The Swatch Group (4.2% NRA, 37.3% UW rent). For the months of April, May and June 2020, The Swatch Group base rent has been reduced to 50.0%. The abated 50% of base rent is required to be repaid by December 31, 2020 (50.0%) and March 31, 2021 (50.0%). All tenants have paid rent for July and August. |

| (5) | The first debt service due date for the Mortgage Loan is in October 2020. |

| (6) | With respect to the 329 Wyckoff Mills Road mortgaged property, the sole tenant, Modway, Inc., which is an affiliate of the borrower, entered into a lease amendment in connection with the origination of the mortgage loan and the acquisition of the mortgaged property by the borrower. The first payment under the amended lease is in September 1, 2020. The sole tenant received a Paycheck Protection Act loan on April 10, 2020. The tenant has informed the lender that it was current under the unamended lease in July and August (prior to the borrower’s acquisition of the mortgaged property). |

| (7) | With respect to the Waterfront Clematis mortgaged property, two ground floor retail tenants were granted rent relief. Pistache French Bistro is paying rent equal to 10% of gross revenues with a minimum of $11,704 per month from April 2020 to November 2020. Phenix Salon Suites received one-month of free rent in April 2020 and has resumed paying its full rent since. Two office tenants (Andersen Tax, LLC and Cozen O' Connor, PC) requested relief, but were not granted relief. These tenants have continued to pay full rent on time. |

| (8) | The 19 West 34th Street Borrower has provided rent abatements to six tenants: A 20,350 square foot tenant (6.4% UW rent) received an abatement of August 2020 rent; a 1,398 square foot tenant (0.4% of UW rent) received an abatement of July 2020 rent and a reduction in monthly rent from approximately $4,824 to $4,500 from August 2020 through March 2021; a 585 square foot tenant (0.3% UW rent) received reduction in monthly rent from approximately $3,096 to $2,400 from August 2020 through December 2020; a 511 square foot tenant (0.2% UW rent) received an abatement of 50% of August and September 2020 rent; and a 154 square foot tenant (0.2% UW rent) received an abatement of July 2020 rent and 50% of August 2020 rent. Additionally, The Sociometric Institute, Inc. in Suites 1401 (33,926 sf) (11.5% UW rent) has received a deferral of August 2020 rent which is expected to be repaid within twelve months. (August 2020 rent was paid by the tenant on Suite 602 (1,408 sf) and Suite 916 (936 sf)). |

| (9) | With respect to the Chasewood Technology Park mortgaged property, one tenant, Scardello & Associates (0.5% of NRA / 0.7% of underwritten base rent) requested and received rent relief of approximately 50% rent from May through August 2020. In exchange, the tenant extended its lease one month. |

| (10) | With respect to the 305 East 72nd Street mortgaged property, as of September 2, 2020, CVS Center, Inc. (69.8% of NRA) has paid 100% of its contractual rent. Mission Ceviche (13.8% of NRA) did not pay rent from March through June 2020. In August 2020, the borrower executed a lease modification with Mission Ceviche, amending the ongoing rent obligation to 12% of gross sales, in lieu of the tenant’s contractual rent, until the tenant is legally able to resume operation with the same seating capacity (65 seats) as immediately prior to COVID-19 restrictions (under no circumstances beyond October 31, 2023). Mission Ceviche paid 50% of its outstanding rent for April through June 2020 concurrently with the signature of the amendment. La Esquina (9.2% of NRA) paid 50% rent from April through June 2020. In July 2020, the borrower executed a lease modification with La Esquina, which waived the tenant’s unpaid rent for April, May and June and provided the tenant with a 1.5 month rent credit, which is being applied to July and part of August. The full August rent payment for La Esquina was reserved at origination. |

| (11) | With respect to the 305 East 72nd Street mortgaged property, Mission Ceviche's rent obligation is 12% of gross sales starting in July 2020. August sales information is not yet available and the tenant has therefore not been billed. The UW August Base Rent Paid (%) equates to the percentage of billed rent that was collected. |

| (12) | For residential cooperatives, values were determined using the available cooperative maintenance receivables reports provided from the borrowers. Generally this information is not tracked for residential cooperative properties and the borrowers are not required, pursuant to the loan documents, to report this data on a monthly basis. |

| (13) | This information is not presented for residential cooperative properties. Residential cooperative properties are structured to allow for an increase in unit owner maintenance charges or the assessment of additional charges to cover operating deficits, including deficits resulting from unpaid or delinquent rents or maintenance charges. |

| (14) | The related mortgage loan has its first due date in October 2020. |

| (15) | The related mortgage loan had its first due date in August 2020. |

| (16) | Given the timing of collection and reporting, an accurate estimate of the percentage of tenants paying rent in August is not available. |

| (17) | The related mortgage loan had its first due date in September 2020. |

| (18) | The Sundance Self Storage, Hardin Station, 15455 Memorial Drive and Kirby at Southfork mortgage loans have scheduled debt service payments due on the 11th of each month. |

| (19) | With respect to the JCG III Industrial Complex mortgaged property, the borrower offered all tenants the option of paying 50% of rent for April, May and June 2020, with repayment due with July, August and September rent payments. Only one tenant, Champion Windows (6.3% of NRA), took advantage of the offer, and started to repay deferred rent with July and August payments. All tenants have paid July rent in full. |

| (20) | With respect to the 33 1 3 @ Thirtyfourth mortgaged property, the borrower offered tenants to pay CAM, Taxes, Insurance and 25% of base rent for April and May 2020, with deferred amount due in 2021. Five tenants (37.9% of NRA) accepted this offer. |

| (21) | With respect to the 33 1 3 @ Thirtyfourth mortgaged property, Les Ba'Get Vietnamese Café (15.6% of NRA) has been underwritten as vacant, but is in place and open. Without the tenant, Total SF or Unit Count Making Full August Rent Payment (%) and UW August Base Rent Paid (%) is 100%. |

| (22) | With respect to the Lancaster Towne Center mortgaged property, two tenants (12.1% of NRA) have been granted rent relief in the form of short term rent deferment. Dragon Hibachi & Sushi Buffet (8.2% of NRA / 12.6% of underwritten base rent) owes a portion of its rent for July and has been granted rent relief in the form of a short term rent deferment. The borrower has executed a payment plan with the tenant to repay the outstanding rent of $13,805 in two equal installments by October 2020. The tenant paid its August rent in full. Ichiban Japanese Steakhouse (3.9% of NRA / 6.3% of underwritten base rent) paid partial rent for July and August and has been granted rent relief in the form of a short term rent deferment. The borrower has executed a payment plan with the tenant to repay the outstanding rent of $15,020 in three equal installments by November 2020. One tenant, At Home (59.9% of NRA / 37.7% of underwritten base rent), was late on its April and May rent. The tenant requested a rent deferment, which was rejected, and subsequently paid all of its outstanding rent in June. The tenant is now fully paid and has been current since. |

| (23) | With respect to the 1602 Spruce Street & 238 South 20th Street mortgage loan, on or about May 29, 2020, the borrower requested the lender to grant a forbearance on debt service payments for the months of June, July and August 2020. On or about June 19, 2020, the lender refused such request. On or about July 23, 2020, the borrower again requested the lender to grant a forbearance on debt service payments for 90 days. On or about July 28, 2020, the borrower rescinded such request. |

| (24) | With respect to the 1602 Spruce Street & 238 South 20th Street mortgaged property, the one retail tenant at 238 South 20th Street, Ultimo Coffee, is open for business and paid its rent full through June 2020. The tenant requested rent relief in July and August of 2020 and is required to return to paying full rent in September. Four residential units at 238 South 20th Street paid in full through May 2020 and were granted 50% rent relief from June 2020 through September 2020. These four units are master leased by Abode LA, LLC (“Abode”) and rented out for short term rentals. Abode signed a three year lease renewal for these four units beginning in October 2020. The remaining four residential tenants at 238 South 20th Street paid in full through their May lease expirations and vacated the property. Abode is expanding into these four units and signed a new, three year lease beginning in October 2020. The one borrower-affiliated retail tenant, at 1602 Spruce Street, vacated in June and the space is currently dark. The lease is guaranteed by the borrower sponsor and the tenant is current on its rent. Two residential units at 1602 Spruce Street paid in full through their June lease expirations and vacated the property. Abode is expanding into these two units and signed a new, three year lease beginning in October 2020. |

| (25) | With respect to the Hardin Station mortgage loan, four tenants representing 35.1% of NRA and 37.5% of UW Rent received rent relief in prior months: (i) Don Gallo Mexican Grill, representing 12.8% of NRA and 15.2% of UW Rent, received a 3-month rent deferral (April-June), and ongoing rent starting 7/1/2020 was reduced from 32.22 PSF to 28.48 PSF. An amendment to the tenant’s lease extended its term by 3 months; (ii) Casual Pint, representing 9.9% of NRA and 10.2% of UW Rent, received free rent for May; (iii) Ross the Boss, Inc., |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-5

| BANK 2020-BNK28 | Transaction Highlights |

representing 7.5% of NRA and 6.3% of UW Rent, received a rent deferral for April. An amendment to the tenant’s lease extended its term by 1 month; and (iv) The UPS Store, representing 5.0% of NRA and 5.8% of UW Rent, received a 3-month rent deferral (April-June), and ongoing rent starting 7/1/2020 was reduced from 30.50 PSF to 27.84 PSF. An amendment to the tenant’s lease extended its term by 3 months. Tenants with rent reductions going forward were underwritten to the new reduced rent levels.

| (26) | With respect to the Hardin Station mortgage loan, all tenants in occupancy paid July and August rent. There is one vacant unit accounting for 6.2% of NRA. |

| (27) | This information is generally not tracked for residential cooperative properties; the borrowers are not required, pursuant to the loan documents, to report such data on a monthly basis. |

| (28) | The borrower for both mortgage loans made forbearance requests on April 28, 2020; however, the requests were withdrawn on June 24, 2020. |

| (29) | With respect to the 15455 Memorial Drive mortgage loan, six tenants, representing 79.5% of NRA and 75.8% of UW Rent, received rent relief in prior months: (i) 3602 Restaurant Group, LLC d/b/a Café Benedicte and Beckham Insurance, representing 38.3% of NRA and 31.8% of UW Rent, received rent deferrals for April; (ii) Jacqueline’s Day Spa and Edge Dental, representing 24.9% of NRA and 28.3% of UW Rent, received rent deferrals for April and May; (iii) A prior tenant, representing 10.1% of NRA and 9.3% of UW Rent, did not pay rent in June. The tenant vacated the suite and the new tenant began paying rent in August; and (iv) GQ Cleaners, representing 6.2% of NRA and 6.3% of UW Rent, made partial rent payments in June and July and did not pay rent in August. The deferred rent is required to be paid back over the period of each tenant's remaining lease term starting in September 2020. |

| (30) | With respect to the Kirby at Southfork mortgage loan, all tenants, representing 91.4% of NRA and 100.0% of UW Rent, at the mortgaged property received a rent deferral for April. In addition, Divine Nails, representing 10.0% of NRA and 11.5% of UW Rent, received a rent deferral for May and HC Tae Kwon Do, representing 13.3% of NRA and 13.0% of UW Rent, received a 50% rent deferral for May. The deferred rent is required to be paid back over the period of each tenant's remaining lease term starting in September 2020. |

| (31) | With respect to the F-B Plaza mortgaged property, Marcos Pizza (18.0% of NRA / 21.1% of underwritten base rent) has been granted deferral of 50% of its April and May rent, repayment of which is due by the end of 2020. MetroPCS (10.3% of NRA / 10.1% of underwritten base rent) has been granted deferral of 50% of its April, May and June rent, repayment of which is due by the end of 2020. Boost Mobile (10.3% of NRA / 10.1% of underwritten base rent) has been granted deferral of 100% of its April and May rent, repayment of which is due by the end of 2020. Wow 8 Spa & Nails (17.9% of NRA / 13.8% of underwritten base rent) has been granted deferral of 100% of its April, May and June rent, repayment of which is due by the end of 2020. L&L Chinese Restaurant (20.5% of NRA / 21.9% of underwritten base rent) has been granted deferral of 100% of its April, May and June rent and 50% of its July and August rent, repayment of which is due by the end of 2020. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-6

| BANK 2020-BNK28 | Characteristics of the Mortgage Pool |

III. Summary of the Whole Loans

| Property Name | Mortgage Loan Seller in BANK 2020-BNK28 | Trust Cut-off Date Balance | Aggregate Pari-Passu Companion Loan Cut-off Date Balance(1) | Controlling Pooling / Trust & Servicing Agreement | Master Servicer | Special Servicer Agreement | Related Pari Passu Companion Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 9th & Thomas | BANA | $70,000,000 | $96,000,000 | BANK 2020-BNK28 | Wells Fargo Bank, National Association | KeyBank National Association | Future Securitization(s) | $26,000,000 |

| 711 Fifth Avenue | BANA | $60,000,000 | $545,000,000 | GSMS 2020-GC47 | Wells Fargo Bank, National Association | KeyBank National Association | GSMS 2020-GC47 | $62,500,000 |

| | | | | | | | JPMDB 2020-COR7 | $40,000,000 |

| | | | | | | | Benchmark 2020-B18 | $45,000,000 |

| | | | | | | | BANK 2020-BNK27 | $43,000,000 |

| | | | | | | | DBJPM 2020-C9 | $25,000,000 |

| | | | | | | | Future Securitizations(s) | $269,500,000 |

| ExchangeRight Net Leased Portfolio #39 | BANA | $37,660,000 | $49,660,000 | BANK 2020-BNK28 | Wells Fargo Bank, National Association | KeyBank National Association | Future Securitization(s) | $12,000,000 |

| Chasewood Technology Park | MS | $30,000,000 | $46,000,000 | BANK 2020-BNK28 | Wells Fargo Bank, National Association | KeyBank National Association | Future Securitization(s) | $16,000,000 |

| | | | | | | | | |

| (1) | The Aggregate Pari Passu Companion Loan Cut-off Date Balance excludes the related Subordinate Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-7

| BANK 2020-BNK28 | Characteristics of the Mortgage Pool |

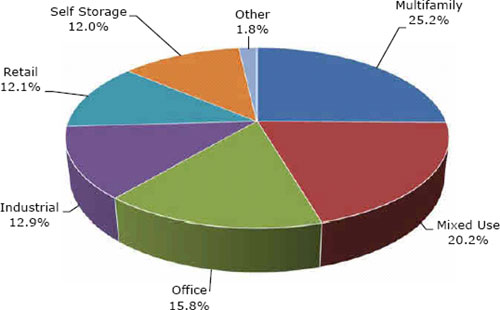

IV. Property Type Distribution(1)

| Property Type | Number of

Mortgaged

Properties | Aggregate Cut-off

Date Balance ($) | % of Cut-off

Date Balance

(%) | Weighted

Average Cut-

off Date LTV

Ratio (%) | Weighted

Average

Balloon LTV

Ratio (%) | Weighted

Average

U/W NCF

DSCR (x) | Weighted

Average

U/W NOI

Debt Yield

(%) | Weighted

Average

U/W NCF

Debt Yield

(%) | Weighted

Average

Mortgage

Rate (%) |

| Multifamily | 35 | $181,498,424 | 25.2% | 39.0% | 37.2% | 5.13x | 23.0% | 22.6% | 3.456% |

| Mid Rise | 11 | 68,925,407 | 9.6 | 67.0 | 66.6 | 1.84 | 7.9 | 7.7 | 3.991 |

| Cooperative | 17 | 59,387,424 | 8.2 | 14.8 | 13.5 | 9.37 | 40.6 | 40.0 | 3.177 |

| Garden | 2 | 48,500,000 | 6.7 | 26.6 | 22.7 | 4.93 | 24.3 | 23.8 | 2.997 |

| Low Rise | 5 | 4,685,593 | 0.7 | 63.3 | 57.3 | 1.71 | 10.1 | 9.7 | 3.880 |

| Mixed Use | 4 | 145,750,000 | 20.2 | 46.6 | 46.6 | 4.01 | 13.1 | 12.4 | 3.150 |

| Office/Retail | 3 | 140,000,000 | 19.4 | 45.9 | 45.9 | 4.11 | 13.4 | 12.7 | 3.112 |

| Multifamily/Retail | 1 | 5,750,000 | 0.8 | 62.5 | 62.5 | 1.64 | 7.0 | 6.8 | 4.070 |

| Office | 4 | 113,811,666 | 15.8 | 61.6 | 57.9 | 2.01 | 9.1 | 8.6 | 3.677 |

| CBD | 1 | 70,000,000 | 9.7 | 60.2 | 60.2 | 2.13 | 7.8 | 7.8 | 3.600 |

| Suburban | 2 | 39,425,000 | 5.5 | 64.5 | 53.8 | 1.76 | 11.3 | 9.8 | 3.774 |

| Medical | 1 | 4,386,666 | 0.6 | 58.1 | 58.1 | 2.35 | 9.8 | 9.6 | 4.025 |

| Industrial | 7 | 92,625,000 | 12.9 | 54.2 | 51.7 | 2.42 | 10.1 | 9.7 | 3.482 |

| Warehouse | 2 | 57,900,000 | 8.0 | 48.0 | 48.0 | 2.87 | 10.6 | 10.1 | 3.472 |

| Manufacturing | 4 | 28,212,047 | 3.9 | 64.5 | 58.0 | 1.67 | 9.3 | 9.0 | 3.498 |

| Warehouse Distribution | 1 | 6,512,953 | 0.9 | 64.5 | 58.0 | 1.67 | 9.3 | 9.0 | 3.498 |

| Retail | 25 | 87,062,863 | 12.1 | 57.9 | 54.6 | 2.33 | 10.6 | 10.2 | 3.822 |

| Unanchored | 6 | 42,689,529 | 5.9 | 62.8 | 58.2 | 2.16 | 9.7 | 9.3 | 3.764 |

| Single Tenant | 18 | 37,773,334 | 5.2 | 56.9 | 55.6 | 2.30 | 9.9 | 9.7 | 3.946 |

| Anchored | 1 | 6,600,000 | 0.9 | 31.9 | 24.9 | 3.50 | 20.9 | 18.9 | 3.490 |

| Self Storage | 16 | 86,625,000 | 12.0 | 58.2 | 54.4 | 2.34 | 10.0 | 9.8 | 3.737 |

| Self Storage | 16 | 86,625,000 | 12.0 | 58.2 | 54.4 | 2.34 | 10.0 | 9.8 | 3.737 |

| Other | 1 | 12,800,000 | 1.8 | 69.2 | 69.2 | 2.06 | 6.5 | 6.5 | 3.134 |

| Leased Fee | 1 | 12,800,000 | 1.8 | 69.2 | 69.2 | 2.06 | 6.5 | 6.5 | 3.134 |

| Total | 92 | $720,172,953 | 100.0% | 51.2% | 49.0% | 3.33x | 13.8% | 13.3% | 3.505% |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property is calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date and the loan-to-value ratio, is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-8

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-9

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-10

| No. 1 – 9th & Thomas |

| |

| Mortgage Loan Information | | Mortgaged Property Information |

| Mortgage Loan Seller: | Bank of America, National Association | | Single Asset/Portfolio: | Single Asset |

Credit Assessment (Fitch/KBRA/Moody’s): | [NR/NR/NR] | | Property Type – Subtype: | Office – CBD |

| Original Principal Balance(1): | $70,000,000 | | Location: | Seattle, WA |

| Cut-off Date Balance(1): | $70,000,000 | | Size: | 170,812 SF |

| % of Initial Pool Balance: | 9.7% | | Cut-off Date Balance Per SF(1): | $562.02 |

| Loan Purpose: | Refinance | | Maturity Date Balance Per SF(1): | $562.02 |

| Borrower Sponsors: | Scott B. Redman; Richard C. Redman | | Year Built/Renovated: | 2018/NAP |

| Guarantors: | Scott B. Redman; Richard C. Redman | | Title Vesting: | Fee |

| Mortgage Rate: | 3.6000% | | Property Manager: | B/T Washington, LLC |

| Note Date: | September 4, 2020 | | Current Occupancy (As of): | 98.6% (8/28/2020) |

| Seasoning: | 0 months | | YE 2019 Occupancy: | 100.0% |

| Maturity Date: | October 1, 2030 | | YE 2018 Occupancy: | 98.8% |

| IO Period(2): | 121 months | | YE 2017 Occupancy(4): | NAP |

| Loan Term (Original)(2): | 121 months | | YE 2016 Occupancy(4): | NAP |

| Amortization Term (Original): | NAP | | As-Is Appraised Value: | $159,400,000 |

| Loan Amortization Type: | Interest-only, Balloon | | As-Is Appraised Value Per SF: | $933.19 |

| Call Protection(2): | L(24); D(92); O(5) | | As-Is Appraisal Valuation Date: | July 16, 2020 |

| Lockbox Type: | Hard/Upfront Cash Management | | Underwriting and Financial Information |

| Additional Debt(1): | Yes | | YE 2019 NOI: | $6,835,379 |

| Additional Debt Type (Balance) (1): | Pari Passu ($26,000,000) | | YE 2018 NOI(4): | NAP |

| | | | YE 2017 NOI(4): | NAP |

| | | | YE 2016 NOI(4): | NAP |

| | | | U/W Revenues: | $10,490,555 |

| | | | U/W Expenses: | $2,966,141 |

| | | | U/W NOI: | $7,524,414 |

| | | | U/W NCF: | $7,464,791 |

| Escrows and Reserves(3) | | U/W DSCR based on NOI/NCF(1): | 2.15x / 2.13x |

| | Initial | Monthly | Cap | | U/W Debt Yield based on NOI/NCF(1): | 7.8% / 7.8% |

| Taxes | $406,459 | $81,292 | NAP | | U/W Debt Yield at Maturity based on NOI/NCF(1): | 7.8% / 7.8% |

| Insurance | $140,847 | Springing | NAP | | Cut-off Date LTV Ratio(1): | 60.2% |

| Replacement Reserve | $0 | $712 | NAP | | LTV Ratio at Maturity(1): | 60.2% |

| | | | | | | | | |

| Sources and Uses |

| Sources | | | | Uses | | |

| Original whole loan amount | $96,000,000 | 99.2% | | Loan Payoff | $95,067,682 | 98.2% |

| Borrower Equity | 810,006 | 0.8 | | Closing costs | 1,195,018 | 1.2 |

| | | | | Reserves | 547,306 | 0.6 |

| Total Sources | $96,810,006 | 100.0% | | Total Uses | $96,810,006 | 100.0% |

| (1) | The Cut-off Date Balance Per SF, Maturity Date Balance Per SF, U/W DSCR based on NOI/NCF, U/W Debt Yield based on NOI/NCF, U/W Debt Yield at Maturity based on NOI/NCF, Cut-off Date LTV Ratio and LTV Ratio at Maturity numbers presented above are based on the 9th & Thomas Whole Loan (as defined below). |

| (2) | The first payment date for the 9th & Thomas Whole Loan is November 1, 2020. On the Closing Date of the BANK 2020-BNK28 securitization transaction, Bank of America, National Association will deposit sufficient funds to pay the amount of interest that would be due with respect to an October 1, 2020 payment. IO Period, Loan Term (Original) and Call Protection are inclusive of the additional October 1, 2020 interest-only payment funded by Bank of America, National Association on the Closing Date. |

| (3) | See “Escrows” section. |

| (4) | Further historical occupancy and NOI is not available, as construction of the 9th & Thomas Property (as defined below) was completed in July 2018. |

| (5) | While the 9th & Thomas Whole Loan was originated after the emergence of the novel coronavirus pandemic and the economic disruption resulting from measures to combat the pandemic, the pandemic is an evolving situation and could impact the 9th & Thomas Whole Loan more severely than assumed in the underwriting of the 9th & Thomas Whole Loan and could adversely affect the NOI, NCF and occupancy information, as well as the appraised value and the DSCR, LTV and Debt Yield metrics presented above. See “Risk Factors-—Risks Related to Market Conditions and Other External Factors—The Coronavirus Pandemic Has Adversely Affected the Global Economy and Will Likely Adversely Affect the Performance of the Mortgage Loans” in the Preliminary Prospectus |

The Mortgage Loan. The mortgage loan (the “9th & Thomas Mortgage Loan”) is part of a whole loan (the “9th & Thomas Whole Loan”) that is evidenced by five pari passu promissory notes, with an aggregate original principal balance of $96,000,000, and secured by a first priority fee mortgage encumbering a Class A office property located in Seattle, Washington (the “9th & Thomas Property”). The controlling Note A-1, together with Notes A-3, A-4 and A-5, with an aggregate original principal balance of $70,000,000, represent the 9th & Thomas Mortgage Loan. The non-controlling Note A-2 is currently held by Bank of America, National Association, and is expected to be contributed to one or more future transactions. The 9th & Thomas Whole Loan will be serviced pursuant to the pooling

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-11

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

and servicing agreement for the BANK 2020-BNK28 securitization transaction. See “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus.

Note Summary

| Notes | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $30,000,000 | $30,000,000 | BANK 2020-BNK28 | Yes |

| A-2 | $26,000,000 | $26,000,000 | Bank of America, National Association | No |

| A-3 | $20,000,000 | $20,000,000 | BANK 2020-BNK28 | No |

| A-4 | $10,000,000 | $10,000,000 | BANK 2020-BNK28 | No |

| A-5 | $10,000,000 | $10,000,000 | BANK 2020-BNK28 | No |

| Total | $96,000,000 | $96,000,000 | | |

The Borrower and Borrower Sponsors. The borrower is 234 9th, LLC (the “9th & Thomas Borrower”), a single-purpose Delaware limited liability company, with one independent director. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the 9th & Thomas Whole Loan.

The borrower sponsors and non-recourse carveout guarantors are Scott B. Redman and Richard C. Redman (the “9th & Thomas Borrower Sponsors”). Scott B. Redman is the current CEO of Sellen Construction and the son of Richard C. Redman, the former CEO of Sellen Construction. Sellen Construction is a family-owned general contractor that has owned the 9th & Thomas Property site since 1944. In its 76-year history, Sellen Construction has completed over 700 projects in the Pacific Northwest, including over 50 LEED certified projects. Sellen Construction’s clients have included Microsoft, Amazon, AT&T, Vulcan and The Bill and Melinda Gates Foundation, and some of their most well-known Seattle developments include the WaMu Tower, Seattle Children’s Hospital, Watermark Tower and Fairmont Olympic Hotel. Sellen Construction has developed three Seattle office properties for Amazon, including the 9th & Thomas Property, and was recently engaged to build a fourth: the Bellevue 600 Tower.

The Property. The 9th & Thomas Property is a 12-story, Class A, LEED Gold certified office building that includes a total of 170,812 square feet above three levels of subterranean parking for 134 vehicles. The improvements were completed in 2018 and are comprised of 9,018 square feet of ground floor retail space (6,559 square feet of which is currently leased to three restaurant tenants: Thomas Street Warehouse Restaurant, Elm Coffee and Jack’s BBQ); 159,037 square feet of office space wholly leased to Amazon Fulfillment Services (“Amazon”); and a 2,757 square foot penthouse residential unit plus rooftop garden, which is leased to Scott B. Redman, one of the 9th & Thomas Borrower Sponsors, and his wife. The 9th & Thomas Property was 98.6% occupied as of August 28, 2020, with the only vacancy being 2,459 square feet of “pop up” short term retail space.

The 9th & Thomas Property features views of Seattle’s Space Needle, open floorplates, terraces on nearly every floor, a fourth floor roof garden, large operable windows and other environmentally sustainable features, locker rooms and secure storage for 60 bicycles. The 9th & Thomas Property also features a double-height “living room” lobby designed for public gathering and used for entertainment and art installations sponsored by the 9th & Thomas Borrower Sponsors, Amazon, and other local groups.

COVID-19 Update. As of September 12, 2020, the 9th & Thomas Property is open and operating. Amazon (93.1% of NRA and 92.8% of underwritten base rent) remains current on all rent and lease obligations. Rent relief was provided for the ground floor restaurant tenants due to operational limitations during the stay-at-home orders directed by Washington’s Governor. Thomas Street Warehouse (2.5% of NRA and 2.4% of underwritten base rent), a full service restaurant and bar, was provided with a base rent abatement for April, August and September 2020 and is currently under negotiations for a rent deferral strategy that would allow the tenant flexibility and time to implement a menu that could be supported by delivery and to-go sales. Jack’s BBQ (1.0% of NRA and 1.0% of underwritten base rent) was provided with two months of base rent abatement for April and August 2020 and resumed full rental payments in September 2020. Elm Coffee (0.4% of NRA and 0.4% of underwritten base rent) was provided with five months of base rent abatement (May through September 2020). The first debt service payment on the 9th & Thomas Mortgage Loan is due in November 2020 and, as of September 12, 2020, the 9th & Thomas Mortgage Loan is not subject to any forbearance, modification or debt service relief request.

Major Tenant.

Amazon Fulfillment Services (159,037 square feet, 93.1% of net rentable area, 92.8% of underwritten base rent). Amazon occupies floors two through eleven, plus 2,249 square feet of ground floor area adjacent to its elevator bays at the 9th & Thomas Property, for use by its Fulfillment by Amazon (“FBA”) division and its tax accounting division. Amazon’s FBA division provides merchants, businesses and individual clients with a product sales platform, handling product listings, inventory management, product shipments and customer support.

Amazon’s 15-year lease expires July 31, 2033, with two seven-year renewal options at fair market rent upon 15-21 months’ notice. Amazon was provided with $11,927,775 ($75 per square foot) as a tenant improvement allowance and also reportedly invested approximately $15.0 million of its own capital for additional build-out. Amazon’s initial rent was $6,043,406 ($38.00 per square foot), with 2.5% annual rent steps increasing base rent to $53.69 per square foot by the last year of the lease term. Additionally, pursuant to its lease, Amazon has the right to use 124 parking spaces for which it pays monthly rent equal to 120% of prevailing market rates. The lease does not provide any termination or contraction options.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-12

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

The Amazon lease is guaranteed by Amazon.com, Inc. (“Amazon.com”) (Nasdaq: AMZN) (S&P/Moody’s/Fitch: AA-/A2/A+) for all payment obligations under the lease, subject to an initial cap equal to $31,516,077, which reduces by $81,372 per month to a cap of $16,869,055 by the last month of the lease term.

Amazon has a 30-day right of first offer to purchase the 9th & Thomas Property should it be marketed for sale or if the 9th & Thomas Borrower receives a bona fide offer from a third party. Such right of first offer does not apply to a foreclosure or refinancing. For additional details regarding the right of first offer, see “Description of the Mortgage Pool—Tenant Issues—Purchase Options and Rights of First Refusal” in the preliminary prospectus. Amazon’s lease prohibits the 9th & Thomas Property from being sold (or for any other space at the property to be leased) to any of 13 entities that currently include: Apple, Barnes & Noble, Best Buy, Dell, eBay, Facebook, Google, HP, Microsoft, Samsung, Sony, Walmart and Snapchat (which list of entities may be updated by Amazon).

Amazon.com is one of the largest companies in the world in terms of market cap and provides e-commerce services and marketing and promotional services. Amazon.com’s global corporate headquarters is located within 0.5 miles of the 9th & Thomas Property and it currently occupies approximately 12.0 million square feet in the South Lake Union neighborhood of Seattle, Washington, employing approximately 50,000 people across the submarket. Amazon.com is now the region’s second largest employer, with Boeing as the largest and Microsoft as the third largest.

The following table presents certain information relating to the tenancy at the 9th & Thomas Property:

Tenant Summary(1)

| Tenant Name | Credit Rating (Fitch/ Moody’s/

S&P) | Tenant NRSF | % of

NRSF | Annual U/W Base Rent PSF | Annual

U/W Base Rent | % of Total Annual U/W Base Rent | Lease

Expiration

Date | Extension Options | Termination Option (Y/N) |

| Amazon | A+/A2/AA- | 159,037 | 93.1% | $45.01 | $7,157,882(2) | 94.1% | 7/31/2033 | 2 x 7 Yr | N |

| | | | | | | | | | |

| Retail Tenants | | 6,559 | 3.8% | $44.06 | $288,977 | 3.8% | | | |

| Residential Penthouse(3) | | 2,757 | 1.6% | $57.07 | $157,353 | 2.1% | 3/31/2030 | 5 x 5 Yr | N |

| | | | | | | | | | |

| Vacant Space (Retail) | 2,459 | 1.4% | $0.00 | $0 | 0.0% | | | |

| | | | | | | | | |

| Total/Wtd. Avg. | 170,812 | 100.0% | $45.17(4) | $7,604,212 | 100.0% | | | |

| | | | | | | | | | |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Annual U/W Base Rent for Amazon is the straight-lined average rent over the 9th & Thomas Whole Loan term. |

| (3) | The Residential Penthouse is leased by Scott B. Redman, one of the 9th & Thomas Borrower Sponsors, and his wife, on a twelve year lease that commenced in March 2018. The starting rental rate was $11,500/month, with 3.0% annual escalations. |

| (4) | Total/Wtd. Avg. Annual U/W Base Rent PSF excludes vacant space. |

The following table presents certain information relating to the lease rollover schedule at the 9th & Thomas Property:

Lease Expiration Schedule(1)

Year Ending

December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF Expiring | Cumulative Expiring NRSF | Cumulative % of Total NRSF Expiring | Annual

U/W

Base Rent Expiring | % of Total Annual U/W Base Rent Expiring | Annual

U/W

Base Rent

PSF Expiring |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2020 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2021 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2022 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2023 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2024 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2025 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2026 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2027 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2028 | 3 | 6,559 | 3.8% | 6,559 | 3.8% | $288,977 | 3.8% | $44.06 |

| 2029 | 0 | 0 | 0.0% | 6,559 | 3.8% | $0 | 0.0% | $0.00 |

| 2030 | 1 | 2,757 | 1.6% | 9,316 | 5.5% | $157,353 | 2.1% | $57.07 |

| Thereafter | 1 | 159,037 | 93.1% | 168,353 | 98.6% | $7,157,882 | 94.1% | $45.01 |

| Vacant | 0 | 2,459 | 1.4% | 170,812 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Wtd. Avg. | 5 | 170,812 | 100.0% | | | $7,604,212 | 100.0% | $45.17(2) |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Total/Wtd. Avg. Annual U/W Base Rent PSF Expiring excludes vacant space. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-13

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

The following table presents historical occupancy percentages at the 9th & Thomas Property:

Historical Occupancy

12/31/2016(1) | 12/31/2017(1) | 12/31/2018(2) | 12/31/2019(2) | 8/28/2020(3) |

| NAP | NAP | 98.8% | 100.0% | 98.6% |

| (1) | Historical occupancy is not available, as construction of the 9th & Thomas Property was completed in July 2018. |

| (2) | Information obtained from the borrower. |

| (3) | Information obtained from the underwritten rent roll. |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the operating history and the underwritten net cash flow at the 9th & Thomas Property:

Cash Flow Analysis(1)

| | | 2019 | | U/W | | %(2) | | U/W $ per SF | |

| Gross Potential Rent(3) | | $6,513,314 | | $7,709,949 | | 70.0% | | $45.14 | |

| Total Recoveries | | 2,217,675 | | 2,731,905 | | 24.8% | | $15.99 | |

| Parking Income(4) | | 561,858 | | 570,794 | | 5.2% | | $3.34 | |

| Other Income | | 2,879 | | 0 | | 0.0% | | $0.00 | |

| Net Rental Income | | $9,295,726 | | $11,012,648 | | 100.0% | | $64.47 | |

| (Vacancy & Credit Loss) | | 0 | | -522,093 | | -6.8% | | ($3.06) | |

| Effective Gross Income | | $9,295,726 | | $10,490,555 | | 95.3% | | $61.42 | |

| | | | | | | | | | |

| Real Estate Taxes | | 792,257 | | 946,324 | | 9.0% | | $5.54 | |

| Insurance | | 118,222 | | 152,205 | | 1.5% | | $0.89 | |

| Other Operating Expenses | | 1,549,868 | | 1,867,612 | | 17.8% | | $10.93 | |

| Total Operating Expenses | | $2,460,347 | | $2,966,141 | | 28.3% | | $17.36 | |

| | | | | | | | | | |

| Net Operating Income | | $6,835,379 | | $7,524,414 | | 71.7% | | $44.05 | |

| Replacement Reserves | | 0 | | 42,703 | | 0.4% | | $0.25 | |

| TI/LC(4) | | 0 | | 16,920 | | 0.2% | | $0.10 | |

| Net Cash Flow | | $6,835,379 | | $7,464,791 | | 71.2% | | $43.70 | |

| | | | | | | | | | |

| NOI DSCR(5) | | 1.95x | | 2.15x | | | | | |

| NCF DSCR(5) | | 1.95x | | 2.13x | | | | | |

| NOI Debt Yield(5) | | 7.1% | | 7.8% | | | | | |

| NCF Debt Yield(5) | | 7.1% | | 7.8% | | | | | |

| (1) | Further historical information is not available, as construction of the 9th & Thomas Property was completed in July 2018. |

| (2) | Represents (i) percent of Net Rental Income for all revenue fields, (ii) percent of Gross Potential Rent for Vacancy & Credit Loss and (iii) percent of Effective Gross Income for all other fields. |

| (3) | U/W Gross Potential Rent is based on the August 28, 2020 rent roll, with rent steps through September 2021 and vacant space underwritten at market rent. Rent for Amazon is the straight-lined average rent over the 9th & Thomas Whole Loan term. |

| (4) | U/W Parking Income is based on trailing twelve month actual income. |

| (5) | The debt service coverage ratios and debt yields are based on the 9th & Thomas Whole Loan. |

Appraisal. The appraiser concluded to an “as-is” Appraised Value for the 9th & Thomas Property of $159,400,000 as of July 16, 2020.

Environmental Matters. According to the Phase I environmental site assessment dated February 25, 2020, there was no evidence of any recognized environmental conditions at the 9th & Thomas Property.

Market Overview and Competition. The 9th & Thomas Property is located at 234 9th Avenue North, at the southeast corner of 9th Avenue and Thomas Street in the heart of the South Lake Union neighborhood of downtown Seattle, Washington. Seattle has seen its population increase 18.6% since 2010, the fastest growth rate among the 50 largest U.S. cities. Seattle benefits from its large port with connections to emerging Asian Markets, highly-trained and well-educated labor force, and a concentration of cloud computing and software development employers, particularly in the South Lake Union area. Notable technology tenants occupying Seattle central business district towers include Amazon, DocuSign, Zillow, F5, Qualtrics, and Dropbox. Other technology tenants with significant office space in the region include Microsoft, Google, Facebook, Oculus, and Tableau.

Access to the 9th & Thomas Property is via local roads to Interstate 5, which runs through the Seattle metropolitan area and across Highway 99. The local area is also served by King County Metro bus transit, Link Light Rail, Sounder Commuter Rail, and two streetcar lines (South Lake Union and First Hill).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-14

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

According to the appraisal, the 9th & Thomas Property is part of the Downtown Seattle office market and the Lake Union office submarket. For the trailing four quarters ended Q2 2020, with respect to Class A office space, the Downtown Seattle office market had total office inventory of approximately 52.9 million square feet, with a vacancy rate of 5.9%, an average asking rent of $45.99 per square foot, and net absorption of approximately 4.0 million square feet. The Lake Union office submarket had total office inventory of approximately 10.4 million square feet, with a vacancy rate of 1.8%, an average asking rent of $51.46 per square foot, and net absorption of approximately 1.0 million square feet.

The biggest lease of the second quarter 2020 in the Seattle market was Amazon.com’s lease of 111,368 square feet at a former Macy’s department store in Redmond Town Center. Amazon.com’s office footprint in the region now exceeds 18.0 million square feet, including future space commitments.

According to the appraisal, the estimated 2019 population within a one-, three- and five-mile radius of the 9th & Thomas Property was 76,692, 252,312, 478,675, respectively. The 2019 average household income within the same radii was $116,395, $126,893, and $132,777, respectively.

The following table presents certain information relating to the appraiser’s market rent conclusions for the 9th & Thomas Property:

Market Rent Summary

| | Office | Retail | Penthouse |

| Market Rent (PSF) | $43.00 | $42.00 | $12,000 |

| Lease Term (Years) | 10 | 10 | 1 |

| Rent Increase Projection | 2.5% per annum | 3.0% per annum | 0.0% per annum |

The following table presents recent office leasing data at comparable properties with respect to the 9th & Thomas Property:

Comparable Office Leases(1)

Property

Name/Address | Year

Built/

Renovated | Distance

from

Subject | Total GLA

(SF) / #

Stories | Tenant | Tenant

Size

(SF) | Lease

Start

Date | Lease

Term

(Mos) | Annual

Base

Rent

PSF

(NNN) | Rent

Escalation |

9th & Thomas

234 9th Avenue North Seattle, WA | 2018/NAP | N/A | 170,812 / 12 | Amazon | 159,037 | Jul-18 | 180 | $38.00 | 2.5%/yr |

2+U (Qualtrics Tower) 1201 2nd Avenue Seattle, WA | 2019/NAP | 1.1 miles | 686,908 / 38 | Dropbox, Inc. Spaces | 120,886 90,848 | Oct-20 Jul-19 | 147 150 | $45.50 $42.50 | 2.75%/yr 2.75%/yr |

8th + Olive 720 Olive Way Seattle, WA | 1981/2014 | 0.6 miles | 300,710 / 20 | AirBNB | 15,631 | Jul-20 | 61 | $39.00 | 3.0%/yr |

Watershed Building 900 N 34th St Seattle, WA | 2020/NAP | 2.3 miles | 66,542 / 7 | Schultz Family Foundation | 21,806 | Apr-20 | 144 | $52.00 | 2.5%/yr |

Rainier Square 1301 5th Ave, Seattle, WA | 2020/NAP | 0.9 miles | 994,567 / 58 | Amazon | 722,000 | Jan-20 | 180 | $39.00 | 2.5%/yr |

450 Alaskan 450 Alaskan Way S. Seattle, WA | 2017/NAP | 2.2 miles | 166,772 / 7 | Nestle | 57,610 | Jun-19 | 120 | $40.00 | 2.75%/yr |

503 Westlake 503 Westlake Seattle, WA | 1919/2017 | 0.3 miles | 38,640 / 6 | Compass Realty | 18,936 | Apr-19 | 132 | $40.00 | 2.75%/yr |

| (1) | Information obtained from the appraisal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

T-15

| Office – CBD | Loan #1 | Cut-off Date Balance: | | $70,000,000 |

| 234 9th Avenue North | 9th & Thomas | Cut-off Date LTV: | | 60.2% |

| Seattle, WA 98109 | | U/W NCF DSCR: | | 2.13x |

| | | U/W NOI Debt Yield: | | 7.8% |

The following table presents recent sales data at comparable office properties with respect to the 9th & Thomas Property:

Comparable Sales(1)

| Property Name/Location | Year

Built/ Renovated | Distance

from

Subject | Total

GLA

(SF) | Occupancy | Date of

Sale | Sale Price | Sale

Price PSF | NOI PSF | Cap Rate |

9th & Thomas(2)

234 9th Avenue North Seattle, WA | 2018/NAP | N/A | 170,812 | 98.6%(3) | NAP | NAP | NAP | $40.02(4) | 4.29%(5) |

Tower 333(2) 333 108th Avenue Bellevue, WA | 2008/2020 | 10.4 miles | 435,091 | 100% | Mar-20 | $401,460,000 | $922.70 | $38.75 | 4.20% |

Amazon Phase VIII(2) 325 9th Ave. N. Seattle, WA | 2015/NAP | 0.0 miles | 317,804 | 100% | Dec-19 | $270,100,000 | $849.89 | $38.25 | 4.50% |

Arbor Blocks(6) 300 8th Ave N Seattle, WA | 2019/NAP | 0.1 miles | 388,072 | 100% | Nov-19 | $415,000,000 | $1,069.39 | $45.45 | 4.25% |

Troy Block(2) 300 Boren Avenue N. Seattle, WA | 2017/NAP | 0.3 miles | 811,463 | 100% | Mar-19 | $740,000,000 | $911.93 | $40.58 | 4.45% |

400 Fairview 400 Fairview Ave. N. Seattle, WA | 2015/NAP | 0.3 miles | 349,152 | 99% | Jul-18 | $338,425,250 | $969.28 | $40.71 | 4.20% |

202 Westlake(2) 202 Westlake Ave. N. Seattle, WA | 2013/NAP | 0.1 miles | 130,710 | 100% | May-18 | $129,500,000 | $990.74 | $43.59 | 4.40% |

| (1) | Information obtained from the appraisal. |

| (2) | 100% of office space leased by Amazon. |

| (3) | Occupancy as of August 28, 2020. |

| (4) | NOI PSF based on 2019 financial information. |

| (5) | Cap Rate based on 2019 NOI and the appraised value. |

| (6) | 100% of office space leased by Facebook. |

Escrows.

Real Estate Taxes – The 9th & Thomas Borrower deposited $406,459 into a real estate tax reserve at origination and is required to deposit an ongoing monthly real estate tax reserve payment in an amount equal to 1/12 of the annual estimated real estate taxes, which currently equates to $81,292.

Insurance – The 9th & Thomas Borrower deposited $140,847 into an insurance reserve at origination and is required to deposit an ongoing monthly insurance reserve payment in an amount equal to 1/12 of the annual estimated insurance premiums unless the 9th & Thomas Property is covered by a blanket policy.

Replacement Reserve – The 9th & Thomas Borrower is required to deposit monthly $712 for replacement reserves.

Lockbox and Cash Management. The 9th & Thomas Whole Loan is structured with a hard lockbox and in-place cash management. Revenues from the 9th & Thomas Property are required to be deposited directly into the lockbox account and transferred on each business day into the cash management account controlled by the lender to be applied and disbursed in accordance with the 9th & Thomas Whole Loan documents. During the occurrence and continuance of a Cash Sweep Period (as defined below), all excess cash is required to be held by the lender as additional collateral for the 9th & Thomas Whole Loan. In the event a Cash Sweep Period occurs more than once during the 9th & Thomas Whole Loan term, the Cash Sweep Period will not be cured and all excess cash will continue to be collected and held by the lender until the full repayment of the 9th & Thomas Whole Loan.

A “Cash Sweep Period” means the earliest of the period:

| (i) | commencing when the amortizing debt service coverage ratio is less than 1.10x (tested quarterly) and ending when the amortizing debt service coverage ratio is at least 1.10x (tested quarterly for two consecutive quarters); |

| (ii) | during an Amazon Bankruptcy Event (as defined below) until cured; |

| (iii) | during an Amazon Credit Event (as defined below) until cured; |

| (iv) | during an Amazon Renewal Event (as defined below) until cured; and |