| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226486-20 | ||

|  |  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,033,345,645

(Approximate Initial Pool Balance)

BANK 2021-BNK34

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Wells Fargo Bank, National Association

Morgan Stanley Mortgage Capital Holdings LLC

Bank of America, National Association

National Cooperative Bank, N.A.

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2021-BNK34

June 3, 2021

| WELLS FARGO SECURITIES | BofA SECURITIES | MORGAN STANLEY |

Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

Academy Securities, Inc. Co-Manager | Drexel Hamilton Co-Manager | Siebert Williams Shank Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-226486) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, BofA Securities, Inc., Morgan Stanley & Co. LLC, Academy Securities, Inc., Drexel Hamilton, LLC, Siebert Williams Shank & Co., LLC or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| BANK 2021-BNK34 | Transaction Highlights |

| I. | Transaction Highlights |

Mortgage Loan Sellers:

| Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | Approx. % of Initial Pool Balance | ||||||||

| Wells Fargo Bank, National Association | 14 | 22 | $375,675,000 | 36.4 | % | |||||||

| Morgan Stanley Mortgage Capital Holdings LLC | 13 | 19 | 323,898,260 | 31.3 | ||||||||

| Bank of America, National Association | 9 | 10 | 265,433,900 | 25.7 | ||||||||

| National Cooperative Bank, N.A. | 20 | 20 | 68,338,485 | 6.6 | ||||||||

| Total | 56 | 71 | $1,033,345,645 | 100.0 | % | |||||||

Loan Pool:

| Initial Pool Balance: | $1,033,345,645 |

| Number of Mortgage Loans: | 56 |

| Average Cut-off Date Balance per Mortgage Loan: | $18,452,601 |

| Number of Mortgaged Properties: | 71 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $14,554,164 |

| Weighted Average Mortgage Interest Rate: | 3.298% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 64.6% |

| Weighted Average Original Term to Maturity or ARD (months): | 114 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 114 |

| Weighted Average Original Amortization Term (months)(2): | 375 |

| Weighted Average Remaining Amortization Term (months)(2): | 374 |

| Weighted Average Seasoning (months): | 0 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 3.43x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 11.9% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 51.4% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 51.0% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 12.6% |

| % of Mortgage Loans with Single Tenants(3): | 31.4% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property are calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the loan-to-value ratio is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | Twenty (20) of the mortgage loans, each of which is secured by a residential cooperative property sold to the depositor by National Cooperative Bank, N.A., currently have in place either (i) subordinate secured lines of credit to the related mortgage borrowers that permit future advances (such loans, collectively, the “Subordinate Coop LOCs”) or (ii) a subordinate wraparound mortgage to the related mortgage borrower that is currently held by the cooperative sponsor (such loan, the “Subordinate Wrap Mortgage”). The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” and “Description of the Mortgage Pool—Additional—Indebtedness—Other Secured Indebtedness—Additional Debt Financing for Mortgage Loans Secured by Residential Cooperatives Sold to the Depositor by National Cooperative Bank, N.A.” in the Preliminary Prospectus. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| BANK 2021-BNK34 | Transaction Highlights |

| II. | COVID-19 Update |

The following table contains information regarding the status of the Mortgage Loans and Mortgaged Properties provided by the respective borrowers as of the date set forth in the “Information As Of Date” column. The cumulative effects of the COVID-19 emergency on the global economy may cause tenants to be unable to pay their rent and borrowers to be unable to pay debt service under the Mortgage Loans. As a result, we cannot assure you that the information in the following table is indicative of future performance or that tenants or borrowers will not seek rent or debt service relief (including forbearance arrangements) or other lease or loan modifications in the future. Such actions may lead to shortfalls and losses on the certificates. Any information in the following table will be superseded by the information contained under the heading “Description of the Mortgage Pool—COVID-19 Considerations” in the Preliminary Prospectus.

Loan Number | Mortgage Loan Seller | Information As Of Date | Origination Date | Mortgage Loan Name | Mortgaged Property Type | April Debt Service Payment Received (Y/N) | May Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested (Y/N) | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Total SF or Unit Count Making Full April Rent Payment (%)(1) | UW April Base Rent Paid (%) | Total SF or Unit Count Making Full May Rent Payment (%)(1) | UW May Base Rent Paid (%) | ||||||||||||||

| 1 | WFB | 5/28/2021 | 6/1/2021 | 375 Pearl Street | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 2 | BANA | 5/11/2021 | 5/14/2021 | Four Constitution Square | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 3 | WFB | 5/28/2021 | 6/1/2021 | National Cancer Institute Center | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 4 | MSMCH | 5/20/2021 | 5/6/2021 | U.S. Steel Tower | Office | NAP(2) | NAP(2) | N | N | Y(3) | 99.9% | 99.9% | 99.9% | 99.9% | ||||||||||||||

| 5 | MSMCH | 5/24/2021 | 5/24/2021 | 160-08 Jamaica Avenue | Retail | NAP(2) | NAP(2) | N | N | N | 100.0%(4) | 100.0%(4) | 100.0%(4) | 100.0%(4) | ||||||||||||||

| 6 | WFB | 5/19/2021 | 4/1/2021 | Burlingame Point | Office | NAP(5) | Y | N | N | N | NAP(6) | NAP(6) | NAP(6) | NAP(6) | ||||||||||||||

| 7 | BANA | 5/11/2021 | 5/11/2021 | Summerhill Pointe Apartments | Multifamily | NAP(2) | NAP(2) | N | N | N | 97.0% | 97.4% | NAV | NAV | ||||||||||||||

| 8 | BANA | 5/11/2021 | 5/14/2021 | Three Constitution Square | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 9 | MSMCH | 5/13/2021 | 4/23/2021 | Fortune 7 Leased Campus | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 10 | MSMCH | 5/25/2021 | 4/27/2021 | 261-275 Amsterdam Avenue | Mixed Use | NAP(2) | NAP(2) | N(7) | N | Y(8) | 91.0% | 91.0% | 89.0% | 89.0% | ||||||||||||||

| 11 | WFB | 5/28/2021 | 5/21/2021 | Brookwood Self Storage Portfolio | Self-Storage | NAP(2) | NAP(2) | N | N | N | 83.2% | 97.3% | 82.8% | 95.8% | ||||||||||||||

| 12 | MSMCH | 5/24/2021 | 5/21/2021 | League City Town Center | Retail | NAP(2) | NAP(2) | N | N | Y(9) | 100.0% | 100.0% | NAV(10) | NAV(10) | ||||||||||||||

| 13 | BANA | 5/19/2021 | 5/19/2021 | Lowe’s - San Jose, CA | Leased Fee | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 14 | WFB | 5/18/2021 | 5/10/2021 | Securlock 12 Self-Storage Portfolio | Self-Storage | NAP(2) | NAP(2) | N | N | N | 99.8% | 99.6% | 99.2% | 98.6% | ||||||||||||||

| 15 | MSMCH | 6/2/2021 | 4/26/2021 | 57 Prince Street | Mixed Use | NAP(2) | NAP(2) | N | N | N(11) | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 16 | MSMCH | 5/21/2021 | 4/21/2021 | Euclid Plaza | Retail | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 17 | BANA | 6/2/2021 | 6/2/2021 | 200 South Virginia Street | Office | NAP(2) | NAP(2) | N | N | Y(12) | 100.0%(12) | 100.0%(12) | 100.0%(12) | 100.0%(12) | ||||||||||||||

| 18 | WFB | 5/17/2021 | 5/6/2021 | A Storage Place Portfolio | Self-Storage | NAP(2) | NAP(2) | N | N | N | NAV | 99.1% | NAV | 98.9% | ||||||||||||||

| 19 | NCB | 5/17/2021 | 5/21/2021 | 150 East Tenants Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 94.4%(13) | NAP(14) | 87.9%(13) | NAP(14) | ||||||||||||||

| 20 | WFB | 5/18/2021 | 5/6/2021 | Midtown Mobile | Retail | NAP(2) | NAP(2) | N | N | Y(15) | 94.9% | 100.0% | 90.1% | 93.4% | ||||||||||||||

| 21 | WFB | 5/24/2021 | 5/4/2021 | Sherman Oaks Plaza | Office | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 22 | BANA | 5/20/2021 | 5/7/2021 | Vista Park Self Storage | Self Storage | NAP(2) | NAP(2) | N | N | N | 99.0% | 98.4% | 99.8% | 99.2% | ||||||||||||||

| 23 | WFB | 5/19/2021 | 4/30/2021 | 3041 Sunrise Boulevard | Industrial | NAP(2) | NAP(2) | N | N | N | NAP(16) | NAP(16) | 100.0% | 100.0% | ||||||||||||||

| 24 | WFB | 5/17/2021 | 5/14/2021 | Riverdale Commerce Park | Industrial | NAP(2) | NAP(2) | N | N | Y(17) | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 25 | WFB | 5/19/2021 | 4/20/2021 | North Ridge Center | Retail | NAP(2) | NAP(2) | N | N | Y(18) | 74.1% | 97.3% | 100.0% | 100.0% | ||||||||||||||

| 26 | MSMCH | 6/2/2021 | 5/7/2021 | Adar New Haven Multifamily Portfolio | Multifamily | NAP(2) | NAP(2) | N | N | N | 93.0% | 93.0% | 95.0% | 95.0% | ||||||||||||||

| 27 | WFB | 5/14/2021 | 5/18/2021 | StorQuest Brentwood | Self-Storage | NAP(2) | NAP(2) | N | N | N | NAV | NAV | 92.6% | 89.4% | ||||||||||||||

| 28 | NCB | 5/20/2021 | 4/29/2021 | Eden Rock Owners, Inc. | Multifamily | NAP(2) | NAP(2) | N | N | N | 92.5%(13) | NAP(14) | 85.9%(13) | NAP(14) | ||||||||||||||

| 29 | MSMCH | 5/25/2021 | 4/19/2021 | Westwood Shopping Center | Retail | NAP(2) | NAP(2) | N | N | Y(19) | 99.0% | 99.0% | 98.0% | 98.0% | ||||||||||||||

| 30 | MSMCH | 5/18/2021 | 5/6/2021 | 31 Jane Street | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 31 | NCB | 5/19/2021 | 5/19/2021 | Briarwood Owners’ Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 92.7%(13) | NAP(14) | 87.2%(13) | NAP(14) | ||||||||||||||

| 32 | BANA | 5/28/2021 | 5/21/2021 | Eastgate & Estes Multifamily Portfolio | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 33 | NCB | 5/17/2021 | 4/23/2021 | Bon Aire Properties, Inc. | Multifamily | NAP(2) | NAP(2) | N | N | N | 90.8%(13) | NAP(14) | 86.2%(13) | NAP(14) | ||||||||||||||

| 34 | NCB | 5/27/2021 | 4/26/2021 | 215 W. 75th St. Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 98.1%(13) | NAP(14) | 98.1%(13) | NAP(14) | ||||||||||||||

| 35 | MSMCH | 5/13/2021 | 4/30/2021 | Burlington Merrillville IN | Retail | NAP(2) | NAP(2) | N | N | N | (20) | (20) | (20) | (20) | ||||||||||||||

| 36 | MSMCH | 5/20/2021 | 5/18/2021 | 928 North San Vicente | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 37 | WFB | 5/19/2021 | 5/18/2021 | WAG – Nashville | Retail | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 38 | NCB | 5/19/2021 | 4/29/2021 | 10 Bleecker Street Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 95.5%(13) | NAP(14) | 95.5%(13) | NAP(14) | ||||||||||||||

| 39 | WFB | 5/17/2021 | 4/28/2021 | New Albany Self Storage - OH | Self-Storage | NAP(2) | NAP(2) | N | N | N | 99.6% | 99.3% | NAV(10) | NAV(10) | ||||||||||||||

| 40 | NCB | 5/27/2021 | 5/20/2021 | 45 W. 10 Tenants’ Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 92.7%(13) | NAP(14) | 91.5%(13) | NAP(14) | ||||||||||||||

| 41 | NCB | 5/21/2021 | 5/10/2021 | Sterling Arms Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 95.9%(13) | NAP(14) | 90.5%(13) | NAP(14) | ||||||||||||||

| 42 | MSMCH | 6/1/2021 | 5/19/2021 | Discount Mini Storage & Retail | Mixed Use | NAP(2) | NAP(2) | N | N | N | 99.7% | 98.7% | 96.9% | 96.8% | ||||||||||||||

| 43 | BANA | 5/28/2021 | 4/26/2021 | Shamrock MHC | Manufactured Housing | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 44 | NCB | 5/19/2021 | 5/18/2021 | Orienta Owners, Inc. | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0%(13) | NAP(14) | 100.0%(13) | NAP(14) | ||||||||||||||

| 45 | BANA | 4/30/2021 | 4/30/2021 | CVS – Littleton, MA | Retail | NAP(2) | NAP(2) | N | N | N | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

| 46 | NCB | 5/19/2021 | 5/20/2021 | Chateaufort Place Cooperative, Inc. | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0%(13) | NAP(14) | 88.3%(13) | NAP(14) | ||||||||||||||

| 47 | NCB | 5/17/2021 | 5/12/2021 | North Broadway Estates Ltd. | Multifamily | NAP(2) | NAP(2) | N | N | N | 90.7%(13) | NAP(14) | 81.5%(13) | NAP(14) | ||||||||||||||

| 48 | NCB | 5/19/2021 | 5/21/2021 | 55-57 East 76th Street, Inc. A/K/A 55-57 East 76th Street Inc | Multifamily | NAP(2) | NAP(2) | N | N | N | 95.0%(13) | NAP(14) | 90.0%(13) | NAP(14) | ||||||||||||||

| 49 | NCB | 5/19/2021 | 5/21/2021 | Princeton Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 95.5%(13) | NAP(14) | 90.9%(13) | NAP(14) | ||||||||||||||

| 50 | NCB | 5/19/2021 | 5/19/2021 | Lincoln Park Manor Tenant Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0%(13) | NAP(14) | 90.0%(13) | NAP(14) | ||||||||||||||

| 51 | NCB | 5/15/2021 | 4/27/2021 | Crocheron Tenants Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 96.5%(13) | NAP(14) | 88.2%(13) | NAP(14) | ||||||||||||||

| 52 | NCB | 5/19/2021 | 4/28/2021 | 203 Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 96.7%(13) | NAP(14) | 66.7%(13) | NAP(14) | ||||||||||||||

| 53 | NCB | 5/19/2021 | 5/21/2021 | 107-109-111 North 9th St. Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 92.9%(13) | NAP(14) | 85.7%(13) | NAP(14) | ||||||||||||||

| 54 | NCB | 5/19/2021 | 5/20/2021 | Tiffany Towers Ltd. | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0%(13) | NAP(14) | 100.0%(13) | NAP(14) | ||||||||||||||

| 55 | NCB | 5/19/2021 | 5/19/2021 | Yorkville 87 Housing Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 100.0%(13) | NAP(14) | 94.4%(13) | NAP(14) | ||||||||||||||

| 56 | NCB | 5/19/2021 | 4/28/2021 | 177 Columbia Owners Corp. | Multifamily | NAP(2) | NAP(2) | N | N | N | 89.7%(13) | NAP(14) | 75.9%(13) | NAP(14) |

| (1) | Total SF or Unit Count Making Full April Rent Payment (%) and Total SF or Unit Count Making Full May Rent Payment (%) are presented as percentages of the total net rentable area. With respect to the mortgage loans secured by residential cooperative properties, Total SF or Unit Count Making Full Rent Payment and UW Base Rent Paid percentages are based on occupied units rather than total SF. |

| (2) | The related mortgage loan has its first due date in June or July 2021. |

| (3) | With respect to the U.S. Steel Tower mortgaged property, three tenants (0.8% of NRA and 6.4% of underwritten rent) were granted rent relief. Two of the three tenants have repaid their deferred rent in full and are current on their rent payments. One of the tenants received a 6 month rent deferral and a 3 month rent abatement in exchange for an additional five years on their term. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| BANK 2021-BNK34 | Transaction Highlights |

| (4) | With respect to the 160-08 Jamaica Avenue mortgaged property, Jollibee (2.3% of NRA and 7.4% of underwritten rent) has taken possession of its space and is currently in the process of building it out. No rent is expected from the tenant. |

| (5) | The related mortgage loan has its first due date in May 2021. |

| (6) | For the Burlingame Point mortgage loan, the sole tenant, Facebook, is currently in a free rent period for all of its leased space. |

| (7) | With respect to the 261-275 Amsterdam Avenue mortgaged property, there is no forbearance or modification on the current 261-275 Amsterdam Avenue mortgage loan. The borrower entered into a forbearance agreement with regard to the previous mortgage loan on the mortgaged property. The previous lender agreed to 6 months of forbearance of all interest payments and reserve fund payments due on the previous loan on the payment dates from April through September 2020, totaling approximately $1,345,367. Such amounts were repaid with the proceeds of the current mortgage loan. |

| (8) | With respect to the 261-275 Amsterdam Avenue mortgaged property, eight retail tenants and the building’s lobby tenant received rent relief in 2020 (17.3% of underwritten rent), of which eight tenants had a portion of unpaid rent paid back using their security deposit and the remaining portion forgiven, and 1 tenant received a rent credit. There are six retail tenants as well as the building’s lobby tenant that are receiving ongoing rent relief (14.5% of underwritten rent) from January 2021 through June 2021. The tenants have remained current on their amended rent obligations and are expected to commence their full contractual rent obligations in July 2021. |

| (9) | With respect to the League City Town Center mortgaged property, five tenants (33.2% of NRA and 23.6% of underwritten rent) were granted rent relief. Three of the tenants (31.1% of NRA and 19.8% of underwritten rent) received three months of deferred rent in 2020 and have repayment plans in place spanning three to twelve months throughout 2021. Two tenants (2.2% of NRA and 3.8% of underwritten rent) received three to four months of 50.0% abated rent in 2020 and both tenants began paying percentage rent in January 2021 in addition to all other rent. |

| (10) | Given the timing of collection and reporting, an accurate estimate of the base rent paid or the percentage of tenants paying rent in May is not available. |

| (11) | With respect to the 57 Prince Street mortgaged property, according to the borrower sponsor, (i) Scotch & Soda (32.5% of NRA and 35.5% of underwritten rent) did not pay rent in April through June of 2020, but repaid half of its missed rent in 2021, (ii) DITA (33.8% of NRA and 27.5% of underwritten rent) did not pay rent in July 2020, but repaid the missed rent over a six month period from September 2020 to February 2021 and (iii) Seen Outdoor Media, LLC (a signage tenant representing 5.4% of underwritten rent) did not pay rent in April and May of 2020; however, all tenants have paid their rent in full and on time since September 2020. No tenants have formally requested or received rent relief or lease modifications. |

| (12) | With respect to the 200 South Virginia Street mortgaged property, three tenants (21.5% of NRA and 20.5% of underwritten rent) received rent relief in relation to the COVID-19 pandemic. One tenant (13.7% of NRA and 12.5% of underwritten rent) has paid back its deferred rent relief. One tenant (5.8% of NRA and 5.8% of underwritten rent) is paying back the deferred rent in equal installments from March 2021 through December 2021. One tenant (1.9% of NRA and 2.1% of underwritten rent) is paying increased rent to account for past rent deferrals. All tenants are current on April and May rent payments. |

| (13) | For residential cooperative properties, the percentages reported were determined based on available cooperative maintenance receivables reports provided from the borrowers (although the borrowers were not required, pursuant to the loan documents, to furnish those reports). Generally, this information is not tracked for residential cooperative properties and the borrowers are not required, pursuant to the loan documents, to report this data on a monthly basis. In addition, for residential cooperative properties, the figures reported were determined based on revenue derived from maintenance charges payable by tenant-shareholders, and not based on rental income for commercial units as to which cooperative shares have not been allocated. Further, with respect to certain residential cooperative properties, the related cooperative borrower may have entered into a primary master lease with a third-party or the cooperative’s sponsor. Generally, however, information regarding subleases under such primary master leases are not tracked for residential cooperative properties. |

| (14) | This information is not presented for residential cooperative properties. The base rent represented in the underwritten cash flow for residential cooperative properties is the hypothetical income derived from the appraisal. Residential cooperative properties are structured to allow for an increase in unit owner maintenance charges or the assessment of additional charges to cover operating deficits, including deficits resulting from unpaid or delinquent rents or maintenance charges. |

| (15) | For the Midtown Mobile mortgage loan, two tenants (Charm Nail Lounge and Coffee Monster), totaling 5.8% of net rentable area and 7.8% of underwritten base rent, requested and received rent relief. |

| (16) | For the 3041 Sunrise Boulevard mortgage loan, an accurate estimate of the base rent paid or the percentage of tenants paying rent in April is not available as the subject transaction was an acquisition and the information was not made available by the seller. |

| (17) | For the Riverdale Commerce Park mortgage loan, one tenant, Battle Axe (6.9% of net rentable area; 6.4% underwritten base rent), became chronically delinquent and remained behind on its rent until May 2021, however, that tenant is now fully caught up on prior rent and is current in payments. A final check for approximately $10,000 to cure all remaining delinquencies for Battle Axe was delivered to the borrower sponsor on May 15, 2021. |

| (18) | For the North Ridge Center mortgage loan, two tenants totaling 22.1% of net rentable area and 32.3% of underwritten base rent received three and four months of abated rent, all of which has been repaid. |

| (19) | With respect to the Westwood Shopping Center mortgaged property, one tenant (10.2% of NRA and 33.1% of underwritten rent) was granted rent relief for its April and May 2020 base rent. The landlord executed a rent deferral agreement with the tenant to repay the base rent on or before December 31, 2024. |

| (20) | With respect to the Burlington Merrillville IN mortgaged property, the single tenant at the property received free rent through June 2021. Free Rent totaling $88,270 was reserved up front, which equates to the tenant’s free rent until it starts paying rent in July. |

See “Risk Factors—Risks Related to Market Conditions and Other External Factors—The Coronavirus Pandemic Has Adversely Affected the Global Economy and Will Likely Adversely Affect the Performance of the Mortgage Loans”.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| BANK 2021-BNK34 | Characteristics of the Mortgage Pool |

| III. | Summary of the Whole Loans |

| No. | Property Name | Mortgage Loan Seller in BANK 2021-BNK34 | Trust Cut-off Date Balance | Aggregate Pari-Passu Companion Loan Cut-off Date Balance(1) | Controlling Pooling / Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Companion Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 1 | 375 Pearl Street | WFB | $100,000,000 | $120,000,000 | BANK 2021-BNK34 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitization(s) | $120,000,000 |

| 2 | Four Constitution Square | BANA | $83,000,000 | $55,000,000 | BANK 2021-BNK34 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitization(s) | $55,000,000 |

| 4 | U.S. Steel Tower | MSMCH | $70,000,000 | $90,000,000 | BANK 2021-BNK34 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitization(s) | $90,000,000 |

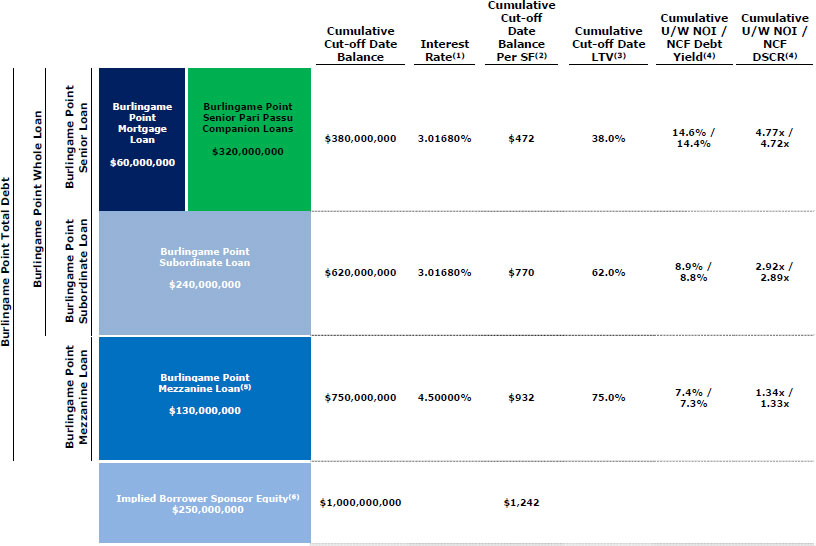

| 6 | Burlingame Point | $60,000,000 | $320,000,000 | KeyBank National Association | Situs Holdings, LLC | BGME 2021-VR | $20,000,000 | ||

| Benchmark 2021-B25 | $120,000,000 | ||||||||

| Benchmark 2021-B26 | $96,000,000 | ||||||||

| Future Securitization(s) | $84,000,000 | ||||||||

| 8 | Three Constitution Square | BANA | $58,000,000 | $38,000,000 | BANK 2021-BNK34 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitization(s) | $38,000,000 |

| 9 | Fortune 7 Leased Campus | $50,000,000 | $28,000,000 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitization(s) | $28,000,000 | ||

| 10 | 261-275 Amsterdam Avenue | MSMCH | $40,000,000 | $55,000,000 | BANK 2021-BNK33 | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | BANK 2021-BNK33 | $55,000,000 |

| (1) | The Aggregate Pari Passu Companion Loan Cut-off Date Balance excludes the related Subordinate Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| BANK 2021-BNK34 | Characteristics of the Mortgage Pool |

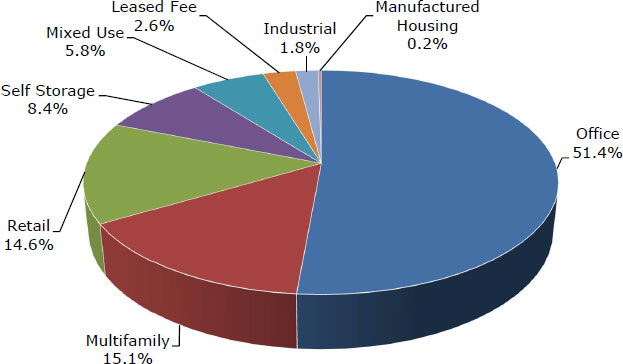

| IV. | Property Type Distribution(1) |

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | ||||||||||||||||||

| Office | 9 | $531,150,000 | 51.4 | % | 49.7 | % | 49.7 | % | 3.71 | x | 11.5 | % | 11.1 | % | 3.023 | % | |||||||||||

| CBD | 6 | 376,900,000 | 36.5 | 51.2 | 51.2 | 3.55 | 11.0 | 10.7 | 3.070 | ||||||||||||||||||

| Suburban | 3 | 154,250,000 | 14.9 | 46.1 | 46.1 | 4.09 | 12.5 | 12.1 | 2.906 | ||||||||||||||||||

| Multifamily | 32 | 155,783,485 | 15.1 | 34.8 | 33.2 | 4.76 | 19.3 | 18.8 | 3.502 | ||||||||||||||||||

| Garden | 11 | 80,445,000 | 7.8 | 55.4 | 53.9 | 2.16 | 8.8 | 8.5 | 3.697 | ||||||||||||||||||

| Cooperative | 21 | 75,338,485 | 7.3 | 12.8 | 11.2 | 7.55 | 30.6 | 29.9 | 3.294 | ||||||||||||||||||

| Retail | 9 | 151,128,260 | 14.6 | 64.6 | 63.5 | 2.28 | 9.5 | 8.9 | 3.799 | ||||||||||||||||||

| Anchored | 5 | 131,995,000 | 12.8 | 64.5 | 64.5 | 2.34 | 9.5 | 8.8 | 3.773 | ||||||||||||||||||

| Single Tenant | 3 | 11,693,422 | 1.1 | 62.8 | 57.2 | 1.81 | 8.8 | 8.5 | 4.044 | ||||||||||||||||||

| Shadow Anchored | 1 | 7,439,837 | 0.7 | 68.9 | 54.7 | 1.80 | 11.8 | 10.2 | 3.880 | ||||||||||||||||||

| Self Storage | 14 | 86,650,000 | 8.4 | 53.4 | 53.1 | 3.19 | 10.5 | 10.3 | 3.192 | ||||||||||||||||||

| Self Storage | 14 | 86,650,000 | 8.4 | 53.4 | 53.1 | 3.19 | 10.5 | 10.3 | 3.192 | ||||||||||||||||||

| Mixed Use | 3 | 60,275,000 | 5.8 | 63.2 | 63.2 | 1.94 | 7.6 | 7.4 | 3.769 | ||||||||||||||||||

| Multifamily/Retail | 1 | 40,000,000 | 3.9 | 63.3 | 63.3 | 1.97 | 7.3 | 7.1 | 3.550 | ||||||||||||||||||

| Retail/Multifamily | 1 | 17,600,000 | 1.7 | 64.5 | 64.5 | 1.73 | 7.7 | 7.4 | 4.215 | ||||||||||||||||||

| Self Storage/Retail | 1 | 2,675,000 | 0.3 | 52.5 | 52.5 | 2.82 | 12.2 | 11.7 | 4.100 | ||||||||||||||||||

| Leased Fee | 1 | 27,108,900 | 2.6 | 64.5 | 64.5 | 2.01 | 7.4 | 7.2 | 3.550 | ||||||||||||||||||

| Leased Fee | 1 | 27,108,900 | 2.6 | 64.5 | 64.5 | 2.01 | 7.4 | 7.2 | 3.550 | ||||||||||||||||||

| Industrial | 2 | 18,750,000 | 1.8 | 62.5 | 61.4 | 1.94 | 9.6 | 9.0 | 3.797 | ||||||||||||||||||

| Flex | 2 | 18,750,000 | 1.8 | 62.5 | 61.4 | 1.94 | 9.6 | 9.0 | 3.797 | ||||||||||||||||||

| Manufactured Housing | 1 | 2,500,000 | 0.2 | 64.9 | 64.9 | 1.87 | 9.1 | 8.9 | 4.695 | ||||||||||||||||||

| Manufactured Housing | 1 | 2,500,000 | 0.2 | 64.9 | 64.9 | 1.87 | 9.1 | 8.9 | 4.695 | ||||||||||||||||||

| Total | 71 | $1,033,345,645 | 100.0 | % | 51.4 | % | 51.0 | % | 3.43 | x | 11.9 | % | 11.5 | % | 3.298 | % | |||||||||||

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property is calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date and the loan-to-value ratio, is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| No. 1 – 375 Pearl Street | ||||||

| Mortgage Loan Information | Mortgaged Property Information(5) | |||||

| Mortgage Loan Seller: | Wells Fargo Bank, National Association | Single Asset/Portfolio: | Single Asset | |||

| Credit Assessment (Fitch/KBRA/S&P): | NR/NR/NR | Property Type – Subtype: | Office – CBD | |||

| Original Principal Balance(1): | $100,000,000 | Location: | New York, NY | |||

| Cut-off Date Balance(1): | $100,000,000 | Size: | 573,083 SF | |||

| % of Initial Pool Balance: | 9.7% | Cut-off Date Balance Per SF(1): | $384 | |||

| Loan Purpose: | Refinance | Maturity Date Balance Per SF(1): | $384 | |||

| Borrower Sponsor: | Sabey-National Properties LLC | Year Built/Renovated: | 1975/2018 | |||

| Guarantor: | Indure Build-To-Core Fund, LLC | Title Vesting: | Fee | |||

| Mortgage Rate: | 3.3682% | Property Manager: | CBRE, Inc. | |||

| Note Date: | June 1, 2021 | Current Occupancy (As of): | 100.0% (5/1/2021) | |||

| Seasoning: | 0 months | YE 2020 Occupancy: | 81.5% | |||

| Maturity Date: | June 11, 2031 | YE 2019 Occupancy: | 81.5% | |||

| IO Period: | 120 months | YE 2018 Occupancy(5): | NAV | |||

| Loan Term (Original): | 120 months | YE 2017 Occupancy(5): | NAV | |||

| Amortization Term (Original): | NAP | Appraised Value(6)(7): | $365,000,000 | |||

| Loan Amortization Type: | Interest-only, Balloon | Appraised Value Per SF(6)(7): | $637 | |||

| Call Protection(2): | L(24),D(89),O(7) | Appraisal Valuation Date: | May 1, 2021 | |||

| Lockbox Type: | Hard/Springing Cash Management | |||||

| Additional Debt(1): | Yes | Underwriting and Financial Information(7) | ||||

| Additional Debt Type (Balance)(1)(3): | Pari Passu ($120,000,000); Mezzanine ($30,000,000) | YE 2020 NOI(8): | $12,454,512 | |||

| YE 2019 NOI(8): | $3,202,972 | |||||

| YE 2018 NOI: | NAV | |||||

| YE 2017 NOI: | NAV | |||||

| Escrows and Reserves(4) | U/W Revenues: | $32,466,229 | ||||

| Initial | Monthly | Cap | U/W Expenses: | $12,264,849 | ||

| Taxes | $0 | Springing | NAP | U/W NOI(8): | $20,201,380 | |

| Insurance | $0 | Springing | NAP | U/W NCF: | $20,086,764 | |

| Landlord Work Reserve | $2,963,439 | $0 | NAP | U/W DSCR based on NOI/NCF(1): | 2.69x / 2.67x | |

| Replacement Reserves | $0 | Springing | NAP | U/W Debt Yield based on NOI/NCF(1): | 9.2% / 9.1% | |

| Termination Fee Reserve | $0 | Springing | (4) | U/W Debt Yield at Maturity based on NOI/NCF(1): | 9.2% / 9.1% | |

| Rent Concession Reserve | $2,882,231 | $0 | NAP | Cut-off Date LTV Ratio(1): | 60.3% | |

| LTV Ratio at Maturity(1): | 60.3% | |||||

| Sources and Uses | ||||||||

| Sources | Uses | |||||||

| Original whole loan amount(1) | $220,000,000 | 88.0% | Loan payoff | $234,451,625 | 93.8% | |||

| Mezzanine loan | 30,000,000 | 12.0 | Upfront reserves | 5,845,670 | 2.3 | |||

| Closing costs | 3,151,476 | 1 .3 | ||||||

| Return of equity | 6,551,229 | 2.6 | ||||||

| Total Sources | $250,000,000 | 100.0% | Total Uses | $250,000,000 | 100.0% | |||

| (1) | The 375 Pearl Street Mortgage Loan (as defined below) is part of the 375 Pearl Street Whole Loan (as defined below) with an original aggregate principal balance of $220,000,000. The Cut-off Date Balance Per SF, Maturity Date Balance Per SF, U/W Debt Yield based on NOI/NCF, U/W Debt Yield at Maturity based on NOI/NCF, U/W DSCR based on NOI/NCF, Cut-off Date LTV Ratio and LTV Ratio at Maturity numbers presented above are based on the 375 Pearl Street Whole Loan. |

| (2) | At any time after the earlier of (i) July 11, 2024 and (ii) two years from the closing date of the securitization that includes the last pari passu note of the 375 Pearl Street Whole Loan to be securitized, and prior to December 11, 2030, the borrower has the right to defease the 375 Pearl Street Whole Loan in whole, but not in part. |

| (3) | See “Subordinate and Mezzanine Indebtedness” section below. |

| (4) | See “Escrows” section below. |

| (5) | See “Historical Occupancy” section below. |

| (6) | Represents the appraiser’s “Hypothetical Market Value”. See “Appraisal” section below. |

| (7) | While the 375 Pearl Street Whole Loan was originated after the emergence of the novel coronavirus pandemic and the economic disruption resulting from measures to combat the pandemic, the pandemic is an evolving situation and could impact the 375 Pearl Street Whole Loan more severely than assumed in the underwriting of the 375 Pearl Street Whole Loan. The pandemic and resulting economic disruption could also adversely affect the NOI, NCF and occupancy information, as well as the appraised value and the DSCR, LTV and Debt Yield metrics presented above. See “Risk Factors—Risks Related to Market Conditions and Other External Factors—Coronavirus Pandemic Has Adversely Affected the Global Economy and Will Likely Adversely Affect the Performance of the Mortgage Loans” in the Preliminary Prospectus. |

| (8) | See “Operating History and Underwritten Net Cash Flow” section below for information regarding year-over-year increases in NOI and increase to U/W NOI from YE 2020 NOI. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

The Mortgage Loan. The largest mortgage loan (the “375 Pearl Street Mortgage Loan”) is part of a whole loan (the “375 Pearl Street Whole Loan”) that is evidenced by four pari passu promissory notes in the aggregate original principal amount of $220,000,000. The 375 Pearl Street Whole Loan is secured by a first priority fee mortgage encumbering a 573,083 square foot office condominium in New York, New York (the “375 Pearl Street Property”). The 375 Pearl Street Whole Loan was co-originated on June 1, 2021 by Wells Fargo Bank, National Association (“WFB”) and JPMorgan Chase Bank, National Association (“JPM”). The 375 Pearl Street Whole Loan will be serviced under the pooling and servicing agreement for the BANK 2021-BNK34 securitization trust. See “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus.

Note Summary

| Notes | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $80,000,000 | $80,000,000 | BANK 2021-BNK34 | Yes |

| A-2 | $66,000,000 | $66,000,000 | JPM | No |

| A-3 | $54,000,000 | $54,000,000 | WFB | No |

| A-4 | $20,000,000 | $20,000,000 | BANK 2021-BNK34 | No |

| Total | $220,000,000 | $220,000,000 |

The Borrower and Borrower Sponsor. The borrower is Intergate.Manhattan Office LLC, a Delaware limited liability company and single purpose entity with two independent directors. In connection with the origination of the 375 Pearl Street Whole Loan, legal counsel to the borrower delivered a non-consolidation opinion. The borrower sponsor under the 375 Pearl Street Whole Loan is Sabey-National Properties LLC, and the nonrecourse carveout guarantor is Indure Build-To-Core Fund, LLC.

The borrower is 51.5% owned by Sabey Corporation (“Sabey”) and 48.5% owned by The Indure Build-To-Core Fund, LLC (the guarantor of the 375 Pearl Street Whole Loan and an affiliate of National Real Estate Advisors, LLC (“NREA”)). Sabey is a privately held real estate development and investment company specializing in mission critical and other technical space for the data center, medical and life sciences, education, government and military sectors. Over the past 40 years, Sabey has designed, constructed, and operated more than 30 million square feet of space. NREA is a subsidiary of the National Electric Benefit Fund and specializes in developing and owning large-scale, urban commercial and multifamily projects for its institutional clients. NREA constructs various asset types including apartment, office, mixed-use, industrial, data center, and hotel.

The Property. The 375 Pearl Street Property consists of an office condominium totaling 573,083 square feet located on floors 15 through 30 of 375 Pearl Street, a 32-story class A office and data center property located in New York, New York, and built in 1975. The entire 375 Pearl Street building contains 806,001 square feet of gross building area situated on a 58,193 square foot parcel of land. The 375 Pearl Street Property was renovated from data center use to office space in 2016 to 2018, and limestone walls on the top 15 stories of the building were removed and replaced with plate glass panels to improve the aesthetics and attract office tenants. In total, the borrower sponsors spent approximately $159 million in capital improvements at the 375 Pearl Street building. The 375 Pearl Street Property features approximately 37,000 square foot floor plates and unobstructed 360-degree views due to the building’s location in a low-rise area.

The 375 Pearl Street Property is fully leased to four New York City agencies through leases with NYC Human Resources Administration, the Department of Finance, the New York City Police Department (“NYPD”), and the Department of Sanitation with all leases expiring between 2038 and 2042. The 375 Pearl Street building is located immediately adjacent to City Hall, One Police Plaza, and One Centre Street. According to the appraisal, NYC agencies own or occupy over 2.3 million square feet of office space in the area of the 375 Pearl Street building, and all tenants of the 375 Pearl Street Property occupy additional office space in the immediate surrounding area. Further, according to the appraisal, the tenants at the 375 Pearl Street Property have invested approximately $44.5 million of capital into the buildout of their respective spaces.

Condominium Regime. The 375 Pearl Street Property represents one unit (known as Office Unit 2, representing a 51.99% interest in the overall condominium) of a nine-unit condominium that governs the 375 Pearl Street building. Four of the nine condominium units are owned by Verizon, consisting of a telephone cable vault in the cellar and switching equipment and office space on floors 8, 9 and 10 (representing an aggregate 11.21% interest in the common elements of the condominium). One condo unit, known as Office Unit 3, representing the 31st floor of the 375 Pearl Street building, is owned by an affiliate of Rafael Viñoly Architects, P.C.. The additional three condominium units (representing ground floor retail space; data center space on floors 1 through 7, 11 through 13 and 32; and office space on floor 14) are owned by affiliates of the borrower sponsor.

COVID-19 Update. As of May 21, 2021, the 375 Pearl Street Property was open and operational. All tenants paid full rent for April and May 2021, and there have been no rent relief requests through the COVID-19 pandemic. The 375 Pearl Street Whole Loan is not subject to any modification or forbearance request.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

Major Tenants.

Largest Tenant: NYC Human Resources Administration (193,821 square feet, 33.8% of net rentable area; 34.3% of underwritten base rent; September 13, 2039 lease expiration) The NYC Human Resources Administration is a municipal agency serving more than three million people per year that fights poverty and provides New York City residents with tools and support to alleviate inequalities. Programs of the NYC Human Resources Administration include Child Support, Emergency Food Programs, Cash Assistance, Adult Protective Services, and a Job Center. According to the appraisal, the agency has a large footprint in Downtown Manhattan with six additional offices in Lower Manhattan and 10 offices directly across the Brooklyn Bridge. According to the appraisal, the NYC Human Resources Administration has invested approximately $11.0 million (approximately $57 per square foot) into its space. The NYC Human Resources Administration has a termination option in September 2029 with 12 months’ notice and payment of a termination fee of approximately $22.3 million (See “Termination Option Summary” below).

2nd Largest Tenant: Department of Finance (182,315 square feet, 31.8% of net rentable area; 32.7% of underwritten base rent; September 13, 2038 lease expiration) The New York City Department of Finance administers the tax and revenue laws of New York City. The Department of Finance is the taxation agency, recorder of deeds, and revenue service provider of New York City. The department’s responsibilities include administering parking violations and overseeing the sheriff’s office. According to the appraisal, the Department of Finance has invested approximately $12.0 million (approximately $66 per square foot) into its space. The Department of Finance has a termination option in September 2028 with 12 months’ notice and payment of a termination fee of approximately $21.1 million (See “Termination Option Summary” below).

3rd Largest Tenant: NYPD (124,767 square feet, 21.8% of net rentable area; 20.1% of underwritten base rent; Various lease expirations) The NYPD is the largest law enforcement agency in the world, providing security and safety to the residents, workers, and visitors throughout the five boroughs of New York City. There are currently over 34,000 uniformed members and over 15,000 civilian members employed by the NYPD. The NYPD has expanded its headquarters by moving its federal monitor and compliance units to the 20th floor of the 375 Pearl Street Property, and utilizing floors 15 through 17 to provide expansion space for the adjacent One Police Plaza. The NYPD has occupied its 20th floor space since 2018. The NYPD has a signed lease for its space on floors 15 through 17 but is not yet in occupancy and is expected to begin paying rent in January 2022. According to the appraisal, NYPD has invested approximately $14.7 million (approximately $118 per square foot) into its space. The NYPD has two termination options (one in April 2029 for its 20th floor space, and one in February 2032 for its space on floors 15 through 17) with 12 months’ notice and payment of a termination fee (approximately $915,014 for the Floor 20 space, and $11.8 million for the space on floors 15 through 17) (See “Termination Option Summary” below).

4th Largest Tenant: Department of Sanitation (72,180 square feet, 12.6% of net rentable area; 12.9% of underwritten base rent; September 23, 2039 lease expiration) The New York City Department of Sanitation is the world’s largest sanitation department and manages approximately 6,300 miles of streets throughout the five boroughs of New York City. The Department of Sanitation is responsible for garbage and recycling collecting, snow removal, and street cleaning. The Department of Sanitation’s headquarters are a 10-minute walk from the 375 Pearl Street Property. According to the appraisal, the Department of Sanitation has invested approximately $6.8 million (approximately $94 per square foot) into its space. The Department of Sanitation has a termination option in September 2029 with 12 months’ notice and payment of a termination fee of approximately $8.7 million (See “Termination Option Summary” below).

The following table presents certain information relating to the tenancy at the 375 Pearl Street Property:

Major Tenants

| Tenant Name | Credit Rating Moody’s/ | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF | Annual U/W Base Rent | % of Total Annual U/W Base Rent | Lease Expiration Date | Extension Options | Termination Option (Y/N)(2) |

| Major Tenants | |||||||||

| NYC Human Resources Administration | AA-/Aa2/AA | 193,821 | 33.8% | $46.25 | $8,964,223 | 34.3% | 9/13/2039 | 2, 5-year | Y |

| Department of Finance | AA-/Aa2/AA | 182,315 | 31.8% | $46.75 | $8,523,225 | 32.7% | 9/13/2038 | 2, 5-year | Y |

| NYPD (Floors 15-17)(3) | AA-/Aa2/AA | 106,000 | 18.5% | $42.50 | $4,505,000 | 17.3% | 1/21/2042 | 2, 5-year | Y |

| Department of Sanitation | AA-/Aa2/AA | 72,180 | 12.6% | $46.75 | $3,374,416 | 12.9% | 9/23/2039 | 2, 5-year | Y |

| NYPD (Floor 20)(3) | AA-/Aa2/AA | 18,767 | 3.3% | $39.00 | $731,913 | 2.8% | 4/10/2039 | 2, 5-year | Y |

| Occupied Collateral Total | 573,083 | 100.0% | $45.54 | $26,098,777 | 100.0% | ||||

| Vacant Space | 0 | 0.0% | |||||||

| Collateral Total | 573,083 | 100.0% | |||||||

| (1) | Ratings shown represent the City of New York, which is the entity on each tenant’s lease. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

| (2) | Each lease contains a one-time termination right effective on the 10th anniversary of the rent commencement date, provided that the tenant provides 12 months’ notice and pays a termination fee. See “Termination Option Summary” below for further details on the termination option effective dates and estimated termination fees for each tenant. |

| (3) | The NYPD has executed a lease for its space on floors 15 through 17 but has not yet taken occupancy. NYPD is expected to begin paying rent in January 2022. The tenant is currently in occupancy and paying full rent on its 20th floor space. |

Termination Option Summary(1)

| Tenant | Estimated Fee(2) | Estimated Fee PSF(2) | Termination Effective Date |

| NYC Human Resources Administration | $22,318,637 | $115.15 | 9/14/2029 |

| Department of Finance | $21,095,726 | $115.71 | 9/14/2028 |

| NYPD (Floors 15-17) | $11,752,356 | $110.87 | 2/16/2032 |

| Department of Sanitation | $8,746,206 | $121.17 | 9/24/2029 |

| NYPD (Floor 20) | $915,014 | $48.76 | 4/11/2029 |

| Total | $64,827,939 | $113.12 |

| (1) | Information obtained from the appraisal. |

| (2) | The termination fee for each tenant is equal to the sum of the unamortized portion of the landlord’s contribution, leasing commission and free rent amount, amortized on a straight-line basis over a 20-year period with interest at 6% per annum plus the total rent amount for the 6 months following the termination date (however, the NYPD 20th floor lease does not include interest in its amortization schedule as well as the total rent amount for the 6 months following the termination date). |

The following table presents certain information relating to the lease rollover schedule at the 375 Pearl Street Property:

Lease Expiration Schedule(1)(2)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(3) | % of Total Annual U/W Base Rent | Annual U/W Base Rent PSF(3) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2021 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2022 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2023 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2024 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2025 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2026 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2027 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2028 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2029 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2030 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2031 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| Thereafter | 5 | 573,083 | 100.0% | 573,083 | 100.0% | $26,098,777 | 100.0% | $45.54 |

| Vacant | 0 | 0 | 0% | 573,083 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 5 | 573,083 | 100.0% | $26,098,777 | 100.0% | $45.54 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | All tenants have termination options, which are not accounted for on this table. See “Termination Option Summary” above. |

The following table presents historical occupancy percentages at the 375 Pearl Street Property:

Historical Occupancy

12/31/2017(1) | 12/31/2018(1) | 12/31/2019(2) | 12/31/2020(2) | 5/1/2021(2) |

| NAV | NAV | 81.5% | 81.5% | 100.0% |

| (1) | Historical occupancy prior to 2019 is not available, as the 375 Pearl Street Property was renovated and converted from data center space to office space from 2016 to 2018. |

| (2) | Information obtained from the underwritten rent roll. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and underwritten net cash flow at the 375 Pearl Street Property:

Cash Flow Analysis(1)

| 2019 | 2020 | U/W | %(2) | U/W $ per SF | |

| Base Rent | $21,403,560 | $21,836,662 | $26,098,777 | 80.4% | $45.54 |

| Rent Average Benefit | 0 | 0 | 3,852,698(3) | 11.9 | 6.72 |

| Free Rent | (8,853,132) | 0 | 0 | 0.0 | 0.00 |

| Gross Potential Rent | $12,550,428 | $21,836,662 | $29,951,475 | 92.3% | $52.26 |

| Other Income | 714,779 | 736,581 | 756,242 | 2.3 | 1.32 |

| Expense Reimbursements | 133,660 | 719,425 | 1,758,512 | 5.4 | 3.07 |

| Net Rental Income | $13,398,867 | $23,292,668 | $32,466,229 | 100.0% | $56.65 |

| (Vacancy & Credit Loss)(4) | 0 | 0 | 0 | 0.0 | 0.00 |

| Effective Gross Income | $13,398,867 | $23,292,668 | $32,466,229 | 100.0% | $56.65 |

| Real Estate Taxes | 3,493,494 | 2,888,190 | 3,465,549(5) | 10.7 | 6.05 |

| Insurance | 366,563 | 375,095 | 415,260 | 1.3 | 0.72 |

| Management Fee | 213,444 | 120,479 | 965,886 | 3.0 | 1.69 |

| Other Operating Expenses | 6,122,394 | 7,454,392 | 7,418,154 | 22.8 | 12.94 |

| Total Operating Expenses | $10,195,895 | $10,838,156 | $12,264,849 | 37.8% | $21.40 |

| Net Operating Income(6) | $3,202,972 | $12,454,512 | $20,201,380 | 62.2% | $35.25 |

| Replacement Reserves | 0 | 0 | 114,617 | 0.4 | 0.20 |

| TI/LC | 0 | 0 | 0 | 0.0 | 0.00 |

| Net Cash Flow | $3,202,972 | $12,454,512 | $20,086,764 | 61.9% | $35.05 |

| NOI DSCR(7) | 0.43x | 1.66x | 2.69x | ||

| NCF DSCR(7) | 0.43x | 1.66x | 2.67x | ||

| NOI Debt Yield(7) | 1.5% | 5.7% | 9.2% | ||

| NCF Debt Yield(7) | 1.5% | 5.7% | 9.1% |

| (1) | Prior historical operating history is not available, as the 375 Pearl Street Property was renovated and converted from data center space to professional office space in 2016 through 2018. |

| (2) | Represents (i) percent of Net Rental Income for all revenue fields, (ii) percent of Gross Potential Rent for Vacancy & Credit Loss and (iii) percent of Effective Gross Income for all other fields. |

| (3) | Represents straight-line rent averaging through each tenant’s lease expiration due to investment-grade nature. |

| (4) | The underwritten economic vacancy is 0.0%. The 375 Pearl Street Property was 100.0% leased as of May 1, 2021. |

| (5) | The 375 Pearl Street Property is subject to a 10-year tax abatement via the Industrial & Commercial Incentive Program (ICAP) as a result of its recent renovation. The ICAP abatement commenced in the 2016/2017 tax year and will expire at the end of the 2025/2026 tax year. According to a third-party tax projection analysis provided by the borrower, the estimated taxes inclusive of ICAP benefit for the 2020/2021 and 2021/2022 tax years were $2,854,104 and $3,677,695, respectively; and the real estate taxes were underwritten based on a blend of these two numbers. According to the same analysis, the estimated full unabated taxes for the 2020/2021 and 2026/2027 (once the ICAP benefit expires) tax years are $3,603,985 and $5,912,415, respectively. |

| (6) | The increase in Net Operating Income from 2019 to 2020 and from 2020 to U/W was due to tenant lease commencements and free rent periods following the completion of renovations at the 375 Pearl Street Property in 2018. The Department of Finance’s lease commenced in September 2018; The NYPD’s lease for floor 20 commenced in October 2018; The Department of Sanitation and the NYC Human Resource Administration’s leases commenced in January 2019; and The NYPD’s lease for floors 15 through 17 commenced in April 2021. |

| (7) | The NOI DSCR, NCF DSCR, NOI Debt Yield and NCF Debt Yield are based on the 375 Pearl Street Whole Loan. |

Appraisal. The appraisal concluded to a “Hypothetical Market Value” of $365,000,000 as of May 1, 2021, which assumes contractually obligated free rent, tenant improvements, and capital improvements have been escrowed. The appraisal also concluded to an “As-Is” value of $360,000,000 as of the same date. The appraiser’s “Hypothetical Market Value” and “As-Is” value each include an estimated $1,600,000 of value for the ICAP tax benefits.

Environmental Matters. According to the Phase I environmental reports dated April 21, 2021, there was no evidence of any recognized environmental conditions at the 375 Pearl Street Property.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

Market Overview and Competition. The 375 Pearl Street Property is situated within the City Hall office submarket of Downtown Manhattan in New York, New York and is bordered by Pearl Street to the east and south, Avenue of the Finest to the west, and Madison Street to the north. The building is also adjacent to the Manhattan-side entrance of the Brooklyn Bridge. The 375 Pearl Street Property is situated immediately adjacent to City Hall, One Police Plaza, and One Centre Street. According to the appraisal, NYC agencies own or occupy over 2.3 million square feet of office space in the area of the 375 Pearl Street building, and all tenants of the 375 Pearl Street Property occupy additional office space in the immediate surrounding area.

According to the appraisal, as of the fourth quarter of 2020, the City Hall submarket reported total inventory of approximately 7.7 million square feet with a 7.0% direct vacancy rate (8.8% overall vacancy rate) and average asking rent of $60.25 per square foot. The appraiser concluded to a market rent for the 375 Pearl Street Property of $44.00 per square foot for floors 15 to 17, $49.00 per square foot for floors 18 to 22, and $52.00 per square foot for floors 23 to 30, all on a modified gross basis.

The following table presents certain information relating to the appraisal’s market rent conclusions for the 375 Pearl Street Property:

Market Rent Summary(1)

| Floors 15-17 | Floors 18-22 | Floors 23-30 | |

| Market Rent (PSF) | $44.00 | $49.00 | $52.00 |

| Lease Term (Years) | 10 | 10 | 10 |

| Lease Type | MG | MG | MG |

| Rent Increase Projection | 10%/5 years | 10%/5 years | 10%/5 years |

| (1) | Information obtained from the appraisal. |

Escrows.

Real Estate Taxes – During a Cash Trap Event Period (as defined below), ongoing monthly real estate tax reserves are required in an amount equal to one-twelfth of the real estate taxes that the lender estimates will be payable during the next 12 months.

Insurance – During a Cash Trap Event Period, ongoing monthly insurance reserves are required in an amount equal to one-twelfth of the insurance premiums that the lender estimates will be payable for the renewal of the coverage afforded by the policies upon the expiration thereof.

However, the borrower’s obligation to make insurance reserve payments will be waived so long as, (i) no event of default is continuing, (ii) the insurance policies maintained by the borrower are part of a blanket or umbrella policy approved by the lender in its reasonable discretion, (iii) the borrower provides the lender with paid receipts for the payment of the insurance premiums by no later than 10 business days prior to the expiration dates of said policies, and (iv) the borrower provides evidence of renewal of such policies.

Landlord Work Reserve – The loan documents require an upfront reserve of $2,963,439 for open contract payables with respect to certain ongoing construction work pursuant to contracts with contractors.

Replacement Reserve – During a Cash Trap Event Period, ongoing monthly replacement reserves are required in the amount of $4,776 ($0.10 per square foot annually).

Termination Fee Reserve– The borrower is required to deposit termination fees or payments into the termination fee reserve account if either (a) the termination fee or payment is equal to or greater than $50,000, (b) the related event has a material adverse effect on the 375 Pearl Street Property, the borrower or the guarantor (among other conditions outlined in the loan documents), and/or (c) an event of default or Cash Trap Event Period is continuing. As long as no Cash Trap Event Period is continuing, the termination fee reserve account is subject to a cap in an amount equal to $80 per square foot of the related premises (“Termination Fee Reserve Cap”). If a Cash Trap Event Period is ongoing, funds in excess of the Termination Fee Reserve Cap are required to deposited into the excess cash flow subaccount (see “Lockbox and Cash Management” section below). Funds in the Termination Fee Reserve account may only be used for qualified leasing expenses incurred in connection with the space related to the applicable termination fee or payment.

Rent Concession Reserve - The loan documents require an upfront reserve of $2,882,231 related to rent concessions through January 2022.

Lockbox and Cash Management. The 375 Pearl Street Whole Loan requires a hard lockbox and springing cash management, and the borrower is required to cause all rents to be deposited directly into the lockbox account. The 375 Pearl Street Whole Loan documents also require that all rents received by the borrower or property manager be deposited into the lockbox account within two business days of receipt. Prior to a Cash Trap Event Period (as defined below), all funds will be transferred to the borrower. During a Cash Trap Event Period, all funds in the lockbox account and excess cash flow remaining after satisfaction of the waterfall items outlined in the 375 Pearl Street Whole Loan documents, are required to be swept to an excess cash flow subaccount to be held as additional collateral for the 375 Pearl Street Whole Loan.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Office – CBD | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

375 Pearl Street New York, NY 10038 | 375 Pearl Street | Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | 60.3% 2.67x 9.2% |

A “Cash Trap Event Period” will commence upon the earlier of the following:

| (i) | the occurrence of an event of default under the 375 Pearl Street Whole Loan or 375 Pearl Street Mezzanine Loan; or |

| (ii) | the net cash flow debt yield falling below 5.25% (tested quarterly, or upon any termination, modification or amendment or settlement of any lease, or any release or discharge of any tenant under its lease obligation). |

A Cash Trap Event Period will end upon the occurrence of the following:

| • | with regard to clause (i), the cure of the applicable event of default; or |

| • | with regard to clause (ii), the net cash flow debt yield being equal to or greater than 5.25% for one calendar quarter; or the borrower delivering to the lender cash or a letter of credit in an amount such that the proceeds, if applied to prepay the 375 Pearl Street Whole Loan, would result in a net cash flow debt yield of at least 5.25%. |

Property Management. The 375 Pearl Street Property is managed by CBRE, Inc.

Partial Release. Not permitted.

Real Estate Substitution. Not permitted.

Subordinate and Mezzanine Indebtedness. Concurrently with the origination of the 375 Pearl Street Whole Loan, WFB made a $30,000,000 mezzanine loan (the “375 Pearl Street Mezzanine Loan”) to the sole member of the borrower, which is secured by the sole member’s ownership interest in the borrower. The 375 Pearl Street Mezzanine Loan is coterminous with the 375 Pearl Street Whole Loan. The 375 Pearl Street Mezzanine Loan accrues interest at a fixed per annum rate equal to 7.000% and is interest-only through the loan term.

The following table presents certain information relating to the 375 Pearl Street Mezzanine Loan:

Mezzanine Loan Original Principal Balance | Mezzanine Loan Interest Rate | Original Term (mos.) | Original Amort. Term (mos.) | Original IO Term (mos.) | Total Debt UW NCF DSCR | Total Debt UW NOI Debt Yield | Total Debt Cutoff Date LTV | ||

| 375 Pearl Street Mezzanine Loan | $30,000,000 | 7.000% | 120 | 0 | 120 | 2.08x | 8.1% | 68.5% | |

Ground Lease. None.

Terrorism Insurance. The loan documents require that the “all risk” insurance policy required to be maintained by the borrower provides coverage for terrorism in an amount equal to the full replacement cost of the 375 Pearl Street Property, as well as business interruption insurance covering no less than the 24-month period following the occurrence of a casualty event, together with a six-month extended period of indemnity (provided that if TRIPRA or a similar statute is not in effect, the 375 Pearl Street Borrower will not be obligated to pay terrorism insurance premiums in excess of two times the annual premium for a separate special form or all risks policy or equivalent policy insuring only the 375 Pearl Street Property on a stand-alone basis).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| No. 2 – Four Constitution Square | |||||||

| Mortgage Loan Information | Mortgaged Property Information | ||||||

| Mortgage Loan Seller: | Bank of America, National Association | Single Asset/Portfolio: | Single Asset | ||||

| Credit Assessment (Fitch/KBRA/S&P): | NR/NR/NR | Property Type – Subtype: | Office – CBD | ||||

| Original Principal Balance(1): | $83,000,000 | Location: | Washington, DC | ||||

| Cut-off Date Balance(1): | $83,000,000 | Size: | 493,620 SF | ||||

| % of Initial Pool Balance: | 8.0% | Cut-off Date Balance Per SF(1): | $279.57 | ||||

| Loan Purpose: | Recapitalization | Maturity Date Balance Per SF(1): | $279.57 | ||||

| Borrower Sponsors: | MetLife and Norges Investment Management | Year Built/Renovated: | 2018/NAP | ||||

| Guarantor(2): | ConSquare Office Four Owner, LLC | Title Vesting: | Fee | ||||

| Mortgage Rate: | 2.5365% | Property Manager: | StonebridgeCarras Management, LLC | ||||

| Note Date: | May 14, 2021 | Current Occupancy (As of)(8): | 100.0% (6/1/2021) | ||||

| Seasoning: | 0 months | YE 2020 Occupancy: | 100.0% | ||||