| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-257991-05 | ||

|  |  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,089,749,733

(Approximate Initial Pool Balance)

BANK 2022-BNK43

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Wells Fargo Bank, National Association

Morgan Stanley Mortgage Capital Holdings LLC

Bank of America, National Association

National Cooperative Bank, N.A.

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2022-BNK43

July 27, 2022

| WELLS FARGO SECURITIES | BofA SECURITIES | MORGAN STANLEY |

Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

Academy Securities, Inc. Co-Manager | Drexel Hamilton Co-Manager | Siebert Williams Shank Co-Manager |

| BANK 2022-BNK43 | Certificate Structure |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-257991) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of (i) Regulation (EU) 2017/1129 (as amended), (ii) such Regulation as it forms part of UK domestic law, or (iii) Part VI of the UK Financial Services and Markets Act 2000, as amended; and does not constitute an offering document for any other purpose.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Morgan Stanley & Co. LLC, BofA Securities, Inc., Academy Securities, Inc., Drexel Hamilton, LLC, Siebert Williams Shank & Co., LLC or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

“BofA Securities” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation, including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and member of FINRA and SIPC, and, in other jurisdictions, locally registered entities.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

I. Transaction Highlights

Mortgage Loan Sellers:

Mortgage Loan Seller | Number of | Number of | Aggregate Cut-off Date Balance | Approx. % of Initial Pool | |||||

| Wells Fargo Bank, National Association | 21 | 21 | $533,314,594 | 48.9% | |||||

| Morgan Stanley Mortgage Capital Holdings LLC | 18 | 60 | 372,124,318 | 34.2 | |||||

| Bank of America, National Association | 7 | 7 | 147,146,651 | 13.5 | |||||

| National Cooperative Bank, N.A. | 15 | 15 | 37,164,170 | 3.4 | |||||

Total | 61 | 103 | $1,089,749,733 | 100.0% |

Loan Pool:

| Initial Pool Balance: | $1,089,749,733 |

| Number of Mortgage Loans: | 61 |

| Average Cut-off Date Balance per Mortgage Loan: | $17,864,750 |

| Number of Mortgaged Properties: | 103 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $10,580,095 |

| Weighted Average Interest Rate: | 5.2506% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 59.2% |

| Weighted Average Original Term to Maturity (months): | 117 |

| Weighted Average Remaining Term to Maturity (months): | 116 |

| Weighted Average Original Amortization Term (months)(2): | 360 |

| Weighted Average Remaining Amortization Term (months)(2): | 360 |

| Weighted Average Seasoning (months): | 1 |

(1) Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. (2) Excludes any mortgage loan that does not amortize.

| |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 2.48x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 14.6% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 50.6% |

| Weighted Average Balloon Loan-to-Value Ratio(1): | 48.9% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 6.7% |

| % of Mortgage Loans with Single Tenants(3): | 12.1% |

(1) With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with one or more other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio, and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property are calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date, and the loan-to-value ratio is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. (2) Thirteen (13) of the mortgage loans, each of which is secured by a residential cooperative property sold to the depositor by National Cooperative Bank, N.A., currently have in place subordinate secured lines of credit to the related mortgage borrowers that permit future advances (such loans, collectively, the “Subordinate Coop LOCs”). The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” and “Description of the Mortgage Pool—Additional Indebtedness—Other Secured Indebtedness—Additional Debt Financing for Mortgage Loans Secured by Residential Cooperatives Sold to the Depositor by National Cooperative Bank, N.A.” in the Preliminary Prospectus. (3) Excludes mortgage loans that are secured by multiple single tenant properties.

| |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| BANK 2022-BNK43 | Characteristics of the Mortgage Pool |

II. Summary of the Whole Loans

| No. | Property Name | Mortgage Loan Seller in BANK 2022-BNK43 | Trust Cut-off Date Balance | Aggregate Pari- Passu Companion Loan Cut-off Date Balance(1) | Controlling Pooling / Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Companion Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 1 | High Street | WFB | $100,000,000 | $138,395,000 | BANK 2022-BNK43 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitizations | $38,395,000 |

| 2 | Katy Mills | BANA | $91,000,000 | $130,000,000 | BANK 2022-BNK43 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitizations | $39,000,000 |

| 3 | Constitution Center | MSMCH | $84,000,000 | $398,000,000 | MSC 2022-L8(2) | Midland Loan Services, a Division of PNC Bank National Association | LNR Partners, LLC | MSC 2022-L8 | $314,000,000 |

| 4 | The Boulders Resort | WFB | $74,930,466 | $99,907,288 | BANK 2022-BNK43 | Wells Fargo Bank, National Association | Greystone Servicing Company LLC | Future Securitizations | $25,000,000 |

| 8 | One Campus Martius | MSMCH | $46,200,000 | $218,000,000 | BANK 2022-43(3) | Wells Fargo Bank, National Association(3) | Greystone Servicing Company LLC(3) | Future Securitizations | $171,800,000 |

| 9 | Hilton Sandestin Beach Resort | WFB | $44,000,000 | $120,000,000 | BANK 2022-BNK42 | Wells Fargo Bank, National Association | LNR Partners, LLC | BANK 2022-BNK42 | $76,000,000 |

| 15 | 79 Fifth Avenue | WFB | $25,000,000 | $240,000,000 | CGCMT 2022-GC48 | Midland Loan Services, a Division of PNC Bank National Association | Greystone Servicing Company LLC | BANK 2022-BNK42, CGCMT 2022-GC48, BMO 2022-C2, Future Securitizations | $215,000,000 |

| 19 | 2355 and 2383 Utah Ave | MSMCH | $14,000,000 | $85,000,000 | BANK 2022-BNK42 | Wells Fargo Bank, National Association | LNR Partners, LLC | BANK 2022-BNK42 | $71,000,000 |

| (1) | The Aggregate Pari Passu Companion Loan Cut-off Date Balance excludes the related Subordinate Companion Loans. |

| (2) | Control rights are currently exercised by the holder of the related Subordinate Companion Loans until the occurrence and during the continuation of a control appraisal period for the related whole loan, as described under “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loan—The Constitution Center Whole Loan” in the Preliminary Prospectus. |

| (3) | The related whole loan is expected to initially be serviced under the BANK 2022-43 securitization pooling and servicing agreement until the securitization of the related “lead” pari passu note, after which the related whole loan will be serviced under the pooling and servicing agreement governing such securitization of the related “lead” pari passu note. The master servicer and special servicer for such securitization will be identified in a notice, report or statement to holders of the BANK 2022-BNK43 certificates after the closing of such securitization. Control rights with respect to the related whole loan will be exercised by the holder of the “lead” pari passu note. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| BANK 2022-BNK43 | Characteristics of the Mortgage Pool |

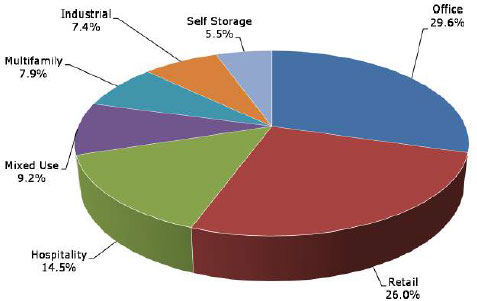

III. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted | Weighted Average Interest Rate (%) |

| Office | 11 | $322,073,830 | 29.6% | 53% | 51.7% | 2.53x | 12.1% | 11.4% | 4.7042% |

| Suburban | 7 | 162,580,123 | 14.9 | 55.1 | 52.6 | 1.99 | 11.8 | 11.0 | 5.1369 |

| CBD | 3 | 155,200,000 | 14.2 | 51.2 | 51.2 | 3.10 | 12.4 | 11.7 | 4.2350 |

| Medical | 1 | 4,293,707 | 0.4 | 39.4 | 33.3 | 2.04 | 17.2 | 14.7 | 5.2800 |

| Retail | 41 | 283,573,750 | 26.0 | 46.5 | 44.6 | 2.18 | 14.4 | 13.6 | 5.5720 |

| Anchored | 3 | 108,000,000 | 9.9 | 55.3 | 55.3 | 1.85 | 10.8 | 10.3 | 5.5421 |

| Super Regional Mall | 1 | 91,000,000 | 8.4 | 33.0 | 27.8 | 2.91 | 21.8 | 20.4 | 5.7670 |

| Single Tenant | 34 | 66,763,750 | 6.1 | 47.8 | 47.4 | 1.85 | 11.0 | 10.5 | 5.3824 |

| Unanchored | 3 | 17,810,000 | 1.6 | 56.6 | 55.3 | 1.75 | 10.8 | 10.2 | 5.4690 |

| Hospitality | 5 | 157,633,410 | 14.5 | 44.4 | 40.5 | 2.88 | 19.2 | 17.2 | 5.3987 |

| Full Service | 2 | 118,930,466 | 10.9 | 40.5 | 36.1 | 3.03 | 20.1 | 17.8 | 5.2141 |

| Extended Stay | 1 | 27,850,000 | 2.6 | 55.3 | 55.3 | 2.61 | 16.7 | 15.5 | 5.8400 |

| Limited Service | 2 | 10,852,944 | 1.0 | 60.3 | 51.1 | 1.88 | 16.2 | 14.4 | 6.2896 |

| Mixed Use | 1 | 100,000,000 | 9.2 | 71.5 | 71.5 | 1.61 | 8.8 | 8.7 | 5.3520 |

| Office/Retail/Multifamily | 1 | 100,000,000 | 9.2 | 71.5 | 71.5 | 1.61 | 8.8 | 8.7 | 5.3520 |

| Multifamily | 20 | 85,999,238 | 7.9 | 34.4 | 32.8 | 4.61 | 28.8 | 28.2 | 5.4917 |

| Cooperative | 16 | 43,149,238 | 4.0 | 13.0 | 11.5 | 7.55 | 45.9 | 45.2 | 4.9451 |

| Low Rise | 3 | 37,250,000 | 3.4 | 55.5 | 53.7 | 1.64 | 11.7 | 11.3 | 6.0966 |

| Garden | 1 | 5,600,000 | 0.5 | 58.3 | 58.3 | 1.76 | 11.0 | 10.2 | 5.6810 |

| Industrial | 5 | 80,675,000 | 7.4 | 56.6 | 56.6 | 1.86 | 10.7 | 10.2 | 5.4115 |

| Warehouse | 3 | 34,925,000 | 3.2 | 62.7 | 62.7 | 1.75 | 10.3 | 9.9 | 5.6045 |

| Light Manufacturing | 1 | 33,000,000 | 3.0 | 55.4 | 55.4 | 1.84 | 10.7 | 10.1 | 5.3900 |

| Flex | 1 | 12,750,000 | 1.2 | 42.6 | 42.6 | 2.23 | 11.9 | 11.2 | 4.9390 |

| Self Storage | 20 | 59,794,505 | 5.5 | 52.9 | 51.4 | 1.89 | 11.4 | 11.2 | 5.5440 |

| Self Storage | 20 | 59,794,505 | 5.5 | 52.9 | 51.4 | 1.89 | 11.4 | 11.2 | 5.5440 |

| Total | 103 | 1,089,749,733 | 100.0% | 50.6% | 48.9% | 2.48x | 14.6% | 13.8% | 5.2510% |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated loan amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate) and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. For mortgaged properties securing residential cooperative mortgage loans, the debt service coverage ratio and debt yield for each such mortgaged property is calculated using U/W Net Operating Income or U/W Net Cash Flow, as applicable, for the related residential cooperative property which is the projected net operating income or net cash flow, as applicable, reflected in the most recent appraisal obtained by or otherwise in the possession of the related mortgage loan seller as of the cut-off date and the loan-to-value ratio, is calculated based upon the appraised value of the residential cooperative property determined as if such residential cooperative property is operated as a residential cooperative, inclusive of the amount of the underlying debt encumbering such residential cooperative property. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

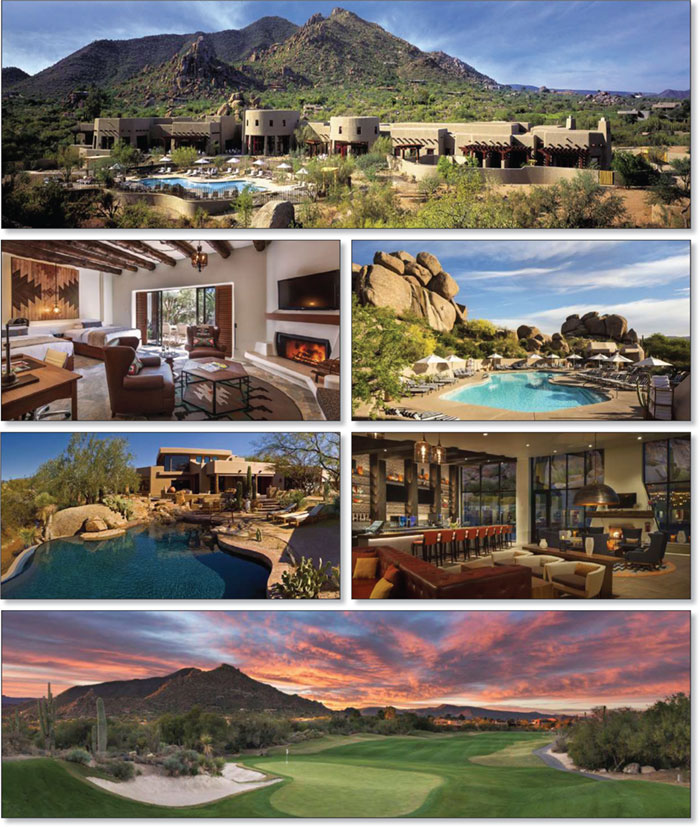

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| No. 1 – High Street |

| Mortgage Loan Information | Mortgaged Property Information | |||||

| Mortgage Loan Sellers: | Wells Fargo Bank, National Association | Single Asset/Portfolio: | Single Asset | |||

Credit Assessment (Fitch/KBRA/Moody’s): | NR/NR/NR | Property Type – Subtype: | Mixed Use – Office/Retail/Multifamily | |||

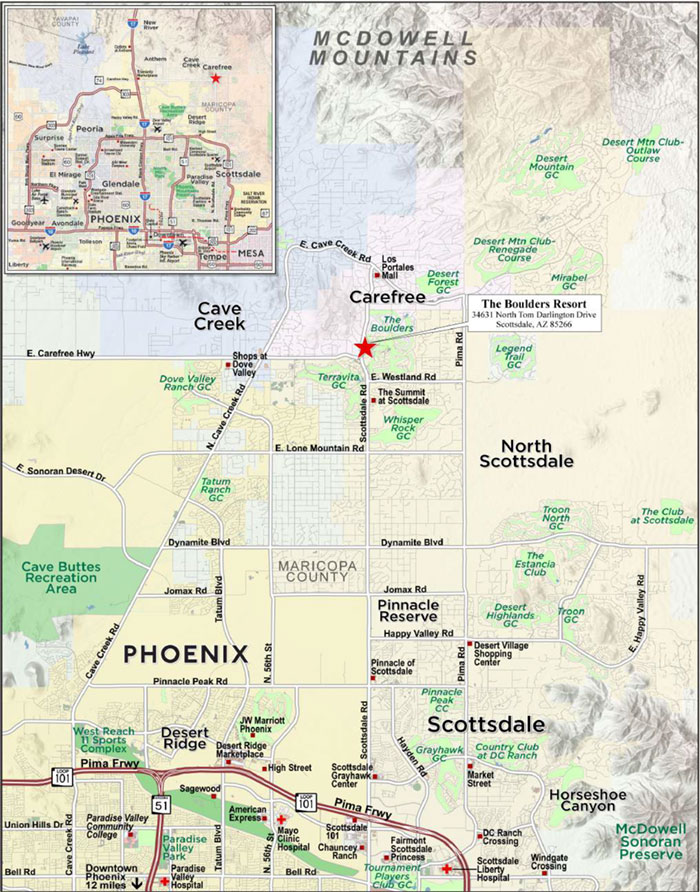

| Original Principal Balance(1): | $100,000,000 | Location: | Phoenix, AZ | |||

| Cut-off Date Balance(1): | $100,000,000 | Size: | 630,083 SF | |||

| % of Initial Pool Balance: | 9.2% | Cut-off Date Balance Per SF(1): | $219.65 | |||

| Loan Purpose: | Acquisition | Maturity Date Balance Per SF(1): | $219.65 | |||

| Borrower Sponsors: | (2) | Year Built/Renovated: | 2008/NAP | |||

| Guarantors: | (2) | Title Vesting: | Leasehold | |||

| Mortgage Rate: | 5.3520% | Property Manager: | SKB PM I, LLC and GREP Southwest, LLC | |||

| Note Date: | June 17, 2022 | Current Occupancy (As of)(5): | 90.4% (6/8/2022) | |||

| Seasoning: | 1 month | 3/31/2022 TTM Occupancy(5): | 86.1% | |||

| Maturity Date: | July 11, 2032 | YE 2021 Occupancy(5): | 85.1% | |||

| IO Period: | 120 months | YE 2020 Occupancy(5): | 85.3% | |||

| Loan Term (Original): | 120 months | YE 2019 Occupancy(5): | 84.1% | |||

| Amortization Term (Original): | 0 months | As-Is/As Stabilized Appraised Value(6): | $193,600,000 / $210,000,000 | |||

| Loan Amortization Type: | Interest Only | As-Is/As Stabilized Appraised Value Per SF(6): | $307.26 / $333.29 | |||

| Call Protection(3): | L(25),D(91),O(4) | As-Is/As Stabilized Appraisal Valuation Date: | May 10, 2022 / June 1, 2023 | |||

| Lockbox Type: | Hard/In-Place Cash Management | Underwriting and Financial Information(7) | ||||

| Additional Debt: | Yes | TTM NOI (5/31/2022)(8): | $9,301,715 | |||

| Additional Debt Type (Balance)(1): | Pari Passu ($38,395,000) | YE 2021 NOI(9): | $9,224,773 | |||

| YE 2020 NOI(9): | $7,760,559 | |||||

| Escrows and Reserves(4) | YE 2019 NOI(9): | $6,788,355 | ||||

| Initial | Monthly | Cap | U/W Revenues: | $19,932,833 | ||

| Taxes | $436,773 | $145,591 | NAP | U/W Expenses: | $7,716,208 | |

| Insurance | $0 | Springing | NAP | U/W NOI(8): | $12,216,625 | |

| Replacement Reserve | $5,905,000 | Springing | $302,262 | U/W NCF: | $12,094,342 | |

| TI/LC Reserve | $8,992,000 | Springing | $1,520,073 | U/W DSCR based on NOI/NCF(1): | 1.63x / 1.61x | |

| Ground Rent Reserve | $30,583 | $30,583 | NAP | U/W Debt Yield based on NOI/NCF(1): | 8.8% / 8.7% | |

| Rent Concession Reserve | $708,593 | $0 | NAP | U/W Debt Yield at Maturity based on NOI/NCF(1): | 8.8% / 8.7% | |

| Existing TI/LC Reserve | $1,873,516 | $0 | NAP | Cut-off Date LTV Ratio(1)(6): | 71.5% / 65.9% | |

| Prepaid Rent Reserve | $73,762 | $0 | NAP | LTV Ratio at Maturity(1)(6): | 71.5% / 65.9% | |

| Sources and Uses | ||||||||

| Sources | Uses | |||||||

| Whole loan amount | $138,395,000 | 65.4% | Purchase Price(10) | $192,103,940 | 90.7% | |||

| Sponsor Equity | $73,306,459 | 34.6% | Upfront Reserves | $18,020,228 | 8.5% | |||

| Closing Costs | $1,577,292 | 0.7% | ||||||

| Total Sources | $211,701,459 | 100.0% | Total Uses | $211,701,459 | 100.0% | |||

| (1) | The High Street Mortgage Loan (as defined below) is part of the High Street Whole Loan (as defined below) with an original aggregate principal balance of $138,395,000. The Cut-off Date Balance per SF, Maturity Date Balance per SF, U/W NOI Debt Yield, U/W NOI Debt Yield at Maturity, U/W NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV Ratio numbers presented above are based on the High Street Whole Loan. |

| (2) | The Borrower Sponsors and Guarantors are Scanlankemperbard Companies, LLC, Todd M. Gooding, James V. Paul, Gary J. Rood, and Gary J. Rood and Christine C. Rood as co-trustees of the Rood Family Trust U/T/A dated September 8, 2005 |

| (3) | Defeasance of the High Street Whole Loan is permitted at any time after the earlier to occur of (a) the end of the two-year period commencing on the closing date of the securitization of the last promissory note representing a portion of the High Street Whole Loan to be securitized and (b) August 11, 2025. The assumed defeasance lockout period of 25 payments is based on the closing date of this transaction in August 2022. |

| (4) | See “Escrows” below for further discussion of reserve requirements. |

| (5) | Occupancy is based on the total NRSF of 630,083 comprising both the Commercial Component and Multifamily Component of the High Street Property (as defined below). |

| (6) | The appraiser also concluded to an “As stabilized” appraised value of $210,000,000 ($333.29 per SF, 65.9% Cut-off Date LTV Ratio and 65.9% LTV Ratio at Maturity), which assumes the retail space is 90.0% occupied and an approximately 20.7% increase in multifamily market rents, as of June 1, 2023. At origination, the lender reserved $8,992,000 for TI/LCs and $5,905,000 for replacements. |

| (7) | The novel coronavirus pandemic is an evolving situation and could impact the High Street Whole Loan more severely than assumed in the underwriting of the High Street Whole Loan and could adversely affect the NOI, NCF and occupancy information, as well as the appraised value and the DSCR, LTV and Debt Yield metrics presented above and herein. See “Risk Factors—Risks Related to Market Conditions and Other External Factors—The Coronavirus Pandemic Has Adversely Affected the Global Economy and Will Likely Adversely Affect the Performance of the Mortgage Loans” in the prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

| (8) | The increase in Net Operating Income between TTM 5/31/2022 and U/W is primarily due to (i) 15 new and renewal leases (23.5% of Commercial Component NRA and 30.2% of Commercial Component underwritten base rent) commencing between January 2022 and June 2023 and (ii) Commercial Base Rent includes contractual rent steps through August 2023 totaling $290,878. |

| (9) | The increase in Net Operating Income between 2019 and 2020 and 2020 and 2021 was primarily due to 35 new and renewal leases (28.7% of Commercial Component NRA and 33.7% of Commercial Component underwritten base rent) commencing between January 2019 and December 2021. |

| (10) | SKB previously owned 15% of the High Street Property and, at origination, retained 10% ownership in the High Street Property. |

The Mortgage Loan. The mortgage loan (the “High Street Mortgage Loan”) is part of a whole loan (the “High Street Whole Loan”) secured by the leasehold interests in a 630,083 square foot mixed use property comprising office, retail, and multifamily components located in Phoenix, Arizona (the “High Street Property”). The High Street Whole Loan has an original aggregate principal balance of $138,395,000 and is comprised of two pari passu notes. The High Street Mortgage Loan, with an aggregate original principal balance of $100,000,000 is evidenced by the controlling Note A-1. The non-controlling Note A-2, with an aggregate original principal balance of $38,395,000, is currently held by WFB. The High Street Whole Loan will be serviced under the pooling and servicing agreement for the BANK 2022-BNK43 securitization trust. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced Pari Passu Whole Loans” and “Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loans” in the prospectus.

Whole Loan Note Summary

| Notes | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $100,000,000 | $100,000,000 | BANK 2022-BNK43 | Yes |

| A-2 | $38,395,000 | $38,395,000 | WFB | No |

| Total (Whole Loan) | $138,395,000 | $138,395,000 |

The Borrower and Borrower Sponsors. The borrowers comprise four tenants in common, RI East County HS Owner, LLC, RI Glenwood Lofts HS Owner, LLC, RI Glenwood Place HS Owner, LLC, and SKB-HS Owner LLC, each a Delaware limited liability company and single-purpose entity with one independent director. The borrower sponsors and non-recourse carveout guarantors are ScanlanKemperBard Companies, LLC, Todd M. Gooding, James V. Paul, Gary J. Rood, and Gary J. Rood and Christine C. Rood as co-trustees of the Rood Family Trust UTA Dated September 8, 2005.

ScanlanKemperBard Companies, LLC (“SKB”) is a real estate investor, operator, and developer specializing in urban industrial and suburban mixed use commercial properties. SKB has over 25 years of experience and currently has a team of over 80 professionals. Headquartered in Portland, Oregon, SKB’s portfolio comprises 5.5 million square feet valued at approximately $1.4 billion. For additional information on the borrower sponsor and guarantors please see “Description of the Mortgage Pool - Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings”.

Gary Rood and Christine Rood are CEO and President, respectively, and co-owners of Rood Investments. Founded in 2007, Rood Investments is a privately held asset management and real estate investment company located in Vancouver, Washington. Today, Rood Investments oversees the management of a 25 property portfolio of senior housing, retail, industrial, and multifamily holdings located across nine states valued at approximately $640 million.

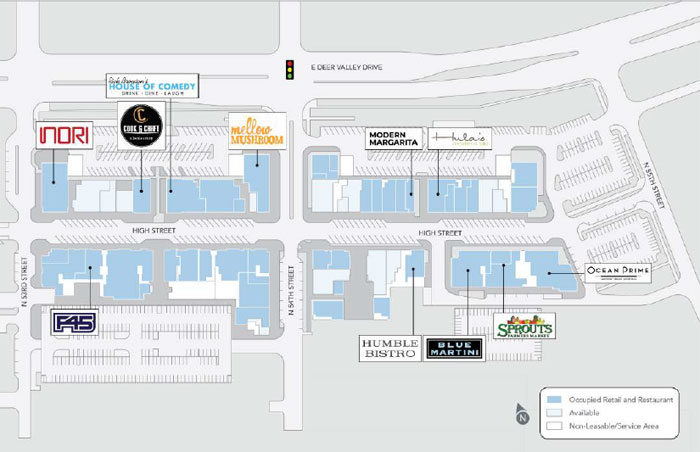

The Property. The High Street Property is comprised of the borrowers’ leasehold interests in a 630,038 square foot mixed use office, retail and multifamily development as well as a six- and a three-level parking garage located in Phoenix, Arizona. Built in 2008 and situated on a 20.0-acre site, the property includes nine, three- and four-story buildings. The property features 506,691 square feet of commercial space (333,128 square feet of office and 173,563 square feet of retail) and 99 multifamily units (123,392 square feet). The property contains 2,090 garage and surface parking spaces, resulting in a parking ratio of 3.32 spaces per 1,000 SF of rentable area. As of June 8, 2022, the property was 90.4% leased.

Office

The High Street Property includes 333,128 square feet of office space (the “Office Component”) comprising 52.9% of net rentable area and 62.9% of underwritten base rent. Tenant suites range in size from 225 square feet to 23,970 square feet. As of June 8, 2022, the Office Component is 93.2% leased to 35 tenants and has averaged 86.6% occupancy since 2016. Since January 2020, there have been 19 new and renewal leases comprising 28.5% of commercial net rentable area and 38.2% of underwritten commercial base rent.

Retail

The High Street Property includes 173,563 square feet of retail space (the “Retail Component” and, together with the Office Component, the “Commercial Component”) comprising 27.5% of net rentable area and 19.7% of underwritten base rent. The largest tenants include Desert Ridge Pediatric Dentist, Ocean Prime, Nori Sushi, Mellow Mushroom, and Sprouts Farmers Market (“Sprouts”). As of June 8, 2022, the Retail Component is 80.1% leased to 39 tenants and has averaged 71.5% occupancy since 2016. The as-stabilized appraised value as of June 1, 2023 assumes the retail space is 90.0% occupied. At origination, the lender reserved $8,992,000 for TI/LCs.

Multifamily

The High Street Property includes 99 multifamily units totaling 123,392 square feet (the “Multifamily Component”) comprising 19.6% of net rentable area and 17.4% of underwritten base rent. The Multifamily Component amenities include a courtyard with a heated pool, two areas with gas BBQs with adjacent granite countertops, outdoor gas fireplace, pet area, fitness center, and EV charging stations. Units feature a private patio or balcony, granite countertops, stainless steel appliances, inclusive of GE refrigerator, range,

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

microwave and dishwasher. In total, there are 24 one-bedrooms, 66 two-bedrooms and 9 three-bedrooms, with unit sizes ranging from 753 square feet to 1,855 square feet. There are 188 parking spaces designated to the Multifamily Component (this equates to a parking ratio of 1.90 per unit). As of June 8, 2022, the Multifamily Component was 97.0% leased (by units) and has averaged 96.1% occupancy since 2014.

According to the appraisal, the owner plans to renovate certain portions of the Multifamily Component, including unit interiors and portions on the common areas, between 2022 and 2023 (as units turn) for an approximate cost of $2,500,000. At origination, the lender reserved $5,905,000 for replacements.

Major Tenants.

Sprouts (95,832 square feet, 18.9% commercial net rentable area, 19.6% underwritten commercial base rent, April 30, 2029 expiration). Sprouts, which currently has more than 370 stores, was founded in 2002 and focuses on farm fresh produce and other healthy, affordable items. Sprouts occupies 89,220 square feet of office space and 6,612 square feet of retail space at the property, which serves as its headquarters. Sprouts has been a tenant at the property since 2015 and has a lease expiring in April 2029 with two, 5-year renewal options remaining. Sprouts has the option to terminate its lease on April 30, 2024 and April 30, 2027 with 12 months’ notice and by paying a termination fee (for the first option only) equal to unamortized TI/LCs and free rent plus two months’ of rent and CAM reimbursements. Sprouts is not required to report sales.

Life Insurance Company of North America (23,562 square feet, 4.7% of commercial net rentable area; 6.4% of underwritten commercial base rent, July 31, 2023 expiration). Life Insurance Company of North America was acquired by New York Life in December 2020. New York Life is a top five insurer across group life, accident and disability insurance. Life Insurance Company of North America has been an office tenant at the property since 2012 and is on a lease expiring on July 31, 2023 with one, 5-year renewal option and no termination options.

Navitus Health Solutions, LLC (22,405 square feet; 4.4% of commercial net rentable area; 6.0% of underwritten commercial base rent, October 31, 2023 expiration). Navitus Health Solutions, LLC (“Navitus”), which is a subsidiary of SSM Health and Costco Wholesale Corporation (Fitch/Moody’s/S&P: NR/Aa3/NR), is a pass-through pharmacy benefit manager and industry alternative to traditional models. Navitus is focused on making prescriptions more affordable for plan sponsors and members. Navitus has been an office tenant at the property since 2015 and is on a lease expiring on October 31, 2023 with one, 5-year renewal option and no termination options.

The following table presents certain information relating to the tenancy at the High Street Property:

Major Tenants

| Tenant Name (Property) | Credit Rating Moody’s/ | Tenant NRSF | % of NRSF(2) | Annual U/W Base Rent PSF(3) | Annual U/W Base Rent(3) | % of Total Annual U/W Base Rent(2) | Lease Expiration Date | Extension Options | Termination Option (Y/N) |

| Major Tenants | |||||||||

| Sprouts | NR/NR/NR | 95,832 | 18.9% | $28.65(4) | $2,746,026 | 19.6% | 4/30/2029 | 2, 5 year | Y(5) |

| Life Insurance Company of North America | AAA/Aaa/NR | 23,562 | 4.7% | $38.00 | $895,356 | 6.4% | 7/31/2023 | 1, 5 year | N |

| Navitus | NR/Aa3/NR | 22,405 | 4.4% | $37.25 | $834,586 | 6.0% | 10/31/2023 | 1, 5 year | N |

| RT Specialty | NR/NR/NR | 20,946 | 4.1% | $36.75 | $769,766 | 5.5% | 10/31/2027 | 2, 5 year | N |

| Healthiest You Teledoc | NR/NR/NR | 19,179 | 3.8% | $34.35 | $658,799 | 4.7% | 9/30/2023 | 1, 5 year | N |

| Total Major Tenants | 181,924 | 35.9% | $32.46 | $5,904,532 | 42.2% | ||||

| Non-Major Tenant | 267,533 | 52.8% | $30.24 | $8,090,008 | 57.8% | ||||

| Occupied Collateral Total | 449,457 | 88.7% | $31.14 | $13,994,540 | 100.0% | ||||

| Vacant Space | 57,234 | 11.3% | |||||||

| Collateral Total | 506,691(2) | 100.0% | |||||||

| (1) | Certain ratings are those of the parent company whether or not the parent company guarantees the lease. |

| (2) | Represents the % of NRSF based on the total net rental area for the Commercial Component of 506,691 and the % of Total Annual U/W Base Rent for the Commercial Component of $13,994,540. |

| (3) | Annual U/W Base Rent PSF and Annual U/W Base Rent include contractual rent steps through August 2023 totaling $290,878 |

| (4) | Sprouts pays $27.50 PSF on 77,391 SF of space and $33.50 PSF on 18,441 SF of space. |

| (5) | Sprouts may terminate its lease on April 30, 2024 and April 30, 2027 with 12 months’ notice and by paying a termination fee (for the first option only) equal to unamortized TI/LCs and free rent plus two months’ of rent and CAM reimbursements. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

The following table presents certain information relating to the lease rollover schedule at the High Street Property:

Lease Expiration Schedule(1)(2)(3)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent | % of Total Annual U/W Base Rent | Annual U/W Base Rent PSF(4) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2022 | 1 | 829 | 0.2% | 829 | 0.2% | $21,140 | 0.2% | $25.50 |

| 2023 | 11 | 107,736 | 21.3% | 108,565 | 21.4% | $3,536,117 | 25.3% | $32.82 |

| 2024 | 9 | 28,682 | 5.7% | 137,247 | 27.1% | $972,855 | 7.0% | $33.92 |

| 2025 | 9 | 30,116 | 5.9% | 167,363 | 33.0% | $938,926 | 6.7% | $31.18 |

| 2026 | 10 | 45,817 | 9.0% | 213,180 | 42.1% | $1,627,033 | 11.6% | $35.51 |

| 2027 | 5 | 41,551 | 8.2% | 254,731 | 50.3% | $1,471,173 | 10.5% | $35.41 |

| 2028 | 4 | 26,028 | 5.1% | 280,759 | 55.4% | $819,956 | 5.9% | $31.50 |

| 2029 | 7 | 98,813 | 19.5% | 379,572 | 74.9% | $2,842,189 | 20.3% | $28.76 |

| 2030 | 5 | 24,290 | 4.8% | 403,862 | 79.7% | $768,471 | 5.5% | $31.64 |

| 2031 | 4 | 15,338 | 3.0% | 419,200 | 82.7% | $402,238 | 2.9% | $26.22 |

| 2032 | 5 | 17,593 | 3.5% | 436,793 | 86.2% | $468,507 | 3.3% | $26.63 |

| Thereafter | 4 | 12,664(5) | 2.5%(5) | 449,457 | 88.7% | $125,936 | 0.9% | $9.94 |

| Vacant | 0 | 57,234 | 11.3% | 506,691 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 74 | 506,691 | 100.0% | $13,994,540 | 100.0% | $31.14 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the Lease Expiration Schedule. |

| (3) | Represents lease expiration information related to the Commercial Component at the High Street Property and excludes the Multifamily Component, which comprises 123,392 square feet and $2,952,497 of Annual U/W Base Rent |

| (4) | Total/Weighted Average Annual U/W Base Rent PSF excludes vacant space. |

| (5) | Includes 7,339 square feet of space occupied by management with no rent attributed to the space. |

The following table presents certain information relating to the unit mix of the Multifamily Component at the High Street Property:

Unit Mix Summary(1)

| Unit Type | Total No. of Units | Occupied Units | % of Total Units | Occupancy | Average Unit Size (SF) | Average per Unit |

| 1 Bedroom, 1 Bathroom | 24 | 23 | 24.2% | 95.8% | 876 | $1,951 |

| 2 Bedrooms, 2 Bathrooms | 60 | 58 | 60.6% | 96.7% | 1,263 | $2,570 |

| 2 Bedrooms, 2.5 Bathrooms | 6 | 6 | 6.1% | 100.0% | 1,696 | $3,374 |

| 3 Bedrooms, 2.5 Bathrooms | 9 | 9 | 9.1% | 100.0% | 1,822 | $3,540 |

| Total/Weighted Average | 99 | 96 | 100.0% | 97.0% | 1,246 | $2,563 |

The following table presents historical occupancy percentages at the High Street Property:

Combined Historical Occupancy

12/31/2019(1) | 12/31/2020(1) | 12/31/2021(1) | TTM 3/31/2021(1) | 6/8/2022(2) |

| 84.1% | 85.3% | 85.1% | 86.1% | 90.4% |

| (1) | Information obtained from the borrower. |

| (2) | Information obtained from the underwritten rent roll. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

Underwritten Net Cash Flow. The following table presents certain information relating to the underwritten net cash flow at the High Street Property:

Cash Flow Analysis

| 2019 | 2020 | 2021 | TTM 5/31/2022 | U/W | %(1) | U/W $ per SF(2) | |

| Commercial Base Rent | $10,313,704 | $10,866,962 | $11,799,778 | $12,346,127 | $13,994,540(3) | 64.5% | $27.62 |

| Percentage Rent | $455,003 | $335,077 | $673,113 | $750,934 | $518,745 | 2.4 | $1.02 |

| Grossed Up Vacant Space | $0 | $0 | $0 | $0 | $1,698,796 | 7.8 | $3.35 |

| Commercial Gross Potential Rent | $10,768,707 | $11,202,039 | $12,472,891 | $13,097,061 | $16,212,081 | 74.7% | $32.00 |

| Multifamily Base Rent | $2,355,590 | $2,344,540 | $2,616,933 | $2,800,614 | $2,952,497 | 13.6 | $23.93 |

| Grossed Up Vacant Space | $283,584 | $371,976 | $215,444 | $26,327 | $78,396 | 0.4 | $0.64 |

| Multifamily Gross Potential Rent | $2,639,174 | $2,716,516 | $2,832,376 | $2,826,941 | $3,030,893 | 14.0% | $24.56 |

| Gross Potential Rent | $13,407,881 | $13,918,554 | $15,305,268 | $15,924,002 | $19,242,974 | 88.6% | $30.54 |

| Other Income | $592,043 | $486,163 | $521,636 | $499,675 | $499,675 | 2.3 | $0.79 |

| Parking Income | $590,017 | $579,291 | $616,455 | $626,442 | $626,442 | 2.9 | $0.99 |

| Expense Reimbursements | $915,410 | $954,847 | $1,031,677 | $1,006,902 | $1,340,934 | 6.2 | $2.13 |

| Net Rental Income | $15,505,351 | $15,938,856 | $17,475,035 | $18,057,021 | $21,710,025 | 100.0% | $34.46 |

| (Commercial Vacancy) | $0 | $0 | $0 | $0 | ($1,698,796) | (10.8)(4) | ($3.35) |

| (Multifamily Vacancy) | ($283,584) | ($371,976) | ($215,444) | ($26,327) | ($78,396) | (2.6)(5) | ($0.64) |

| (Concessions & Collection Loss) | ($1,586,084) | ($1,016,644) | ($949,605) | ($1,344,475) | $0 | 0.0 | ($0.00) |

| Effective Gross Income | $13,635,683 | $14,550,236 | $16,309,986 | $16,686,219 | $19,932,833 | 91.8% | $31.64 |

| Real Estate Taxes | $1,617,241 | $1,613,128 | $1,664,368 | $1,695,466 | $1,762,950 | 8.8 | $2.80 |

| Insurance | $128,281 | $161,446 | $179,204 | $194,752 | $250,444 | 1.3 | $0.40 |

| Ground Rent | $297,976 | $330,728 | $346,383 | $348,418 | $439,267 | 2.2 | $0.70 |

| Management Fee | $521,734 | $532,425 | $606,601 | $637,870 | $755,550 | 3.8 | $1.20 |

| Other Operating Expenses | $4,282,096 | $4,151,949 | $4,288,658 | $4,507,998 | $4,507,998 | 22.6 | $7.15 |

| Total Operating Expenses | $6,847,328 | $6,789,677 | $7,085,214 | $7,384,504 | $7,716,208 | 38.7% | $12.25 |

| Net Operating Income | $6,788,355(6) | $7,760,559(6) | $9,224,773(6) | $9,301,715(7) | $12,216,625(7) | 61.3% | $19.39 |

| Replacement Reserves | $0 | $0 | $0 | $0 | $100,754 | 0.5 | $0.16 |

| TI/LC | $0 | $0 | $0 | $0 | $21,529(8) | 0.1 | $0.03 |

| Net Cash Flow | $6,788,355 | $7,760,559 | $9,224,773 | $9,301,715 | $12,094,342 | 60.7% | $19.19 |

| NOI DSCR(9) | 0.90x | 1.03x | 1.23x | 1.24x | 1.63x | ||

| NCF DSCR(9) | 0.90x | 1.03x | 1.23x | 1.24x | 1.61x | ||

| NOI Debt Yield(9) | 4.9% | 5.6% | 6.7% | 6.7% | 8.8% | ||

| NCF Debt Yield(9) | 4.9% | 5.6% | 6.7% | 6.7% | 8.7% |

| (1) | Represents (i) percent of Net Rental Income for all revenue fields, (ii) percent of Commercial Gross Potential Rent for Commercial Vacancy, (iii) percent of Multifamily Gross Potential Rent for Multifamily Vacancy, and (iv) percent of Effective Gross Income for all other fields. |

| (2) | Represents (i) U/W $ PSF based on the commercial NRSF for commercial revenue and vacancy fields, (ii) U/W $ PSF based on the multifamily NRSF for multifamily revenue and vacancy fields, and (iii) U/W $ PSF based on the total NRSF for all other fields. |

| (3) | Includes contractual rent steps through August 2023 totaling $290,878. |

| (4) | The underwritten economic vacancy is 10.8%. The Commercial Component of the High Street Property was 88.7% leased as of June 8, 2022. |

| (5) | The underwritten economic vacancy is 2.6%. The Multifamily Component of the High Street Property was 97.0% leased as of June 8, 2022. |

| (6) | The increase in Net Operating Income between 2019 and 2020 and 2020 and 2021 was primarily due to 35 new and renewal leases (28.7% of Commercial Component NRA and 33.7% of Commercial Component underwritten base rent) commencing between January 2019 and December 2021. |

| (7) | The increase in Net Operating Income between TTM 5/31/2022 and U/W is primarily due to (i) 15 new and renewal leases (23.5% of Commercial Component NRA and 30.2% of Commercial Component underwritten base rent) commencing between January 2022 and June 2023, (ii) TTM 5/31/2022 includes rent concessions totaling $1,086,530, and (iii) U/W Commercial Base Rent includes contractual rent steps through August 2023 totaling $290,878. |

| (8) | Includes a credit totaling $899,200, which represents 10% of the upfront TI/LC reserve. |

| (9) | The NOI and NCF DSCR and NOI and NCF Debt Yield are based on the High Street Whole Loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

Appraisal. According to the appraisal, the High Street Property had an “As Is” appraised value of $193,600,000 as of May 10, 2022. The appraisal concluded to an “As stabilized” appraised value of $210,000,000 ($333.29 per SF, 65.9% cut-off date LTV), which assumes the Retail Component is 90.0% occupied (80.1% occupied as of June 8, 2022) and an approximately 20.7% increase in multifamily market rents, as of June 1, 2023. According to the appraisal, the owner plans to renovate certain portions of the Multifamily Component, including unit interiors and portions on the common areas, between 2022 and 2023 (as units turn) for an approximate cost of $2,500,000. At origination, the lender reserved $8,992,000 for TI/LCs and $5,905,000 for replacements.

Environmental Matters. According to the Phase I environmental site assessment dated March 25, 2022, there was no evidence of any recognized environmental conditions at the High Street Property.

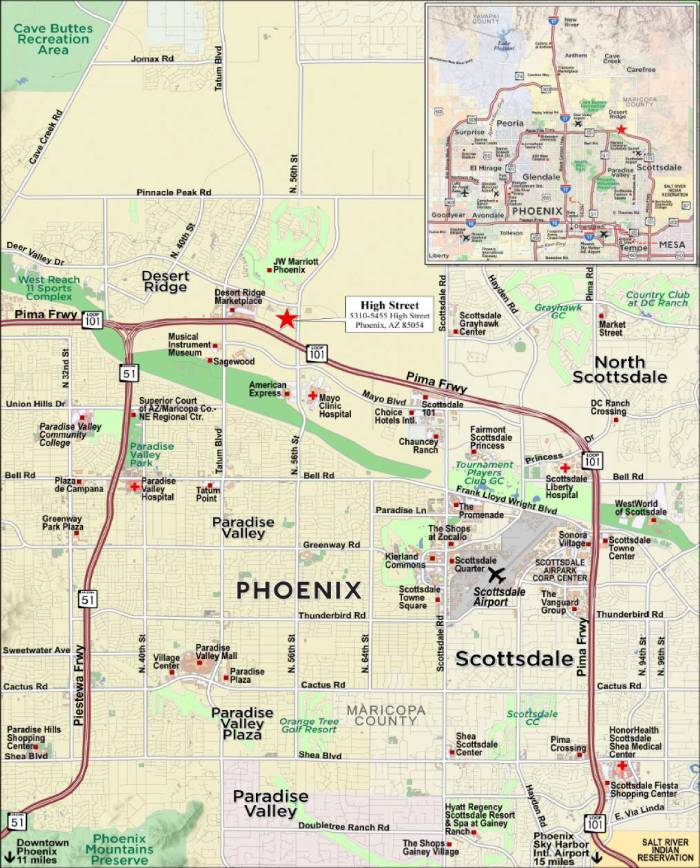

Market Overview and Competition. The High Street Property is located in the Desert Ridge master-planned community in northeast Phoenix, approximately 17 miles from the central business district. Desert Ridge is a 5,700 acre master-planned community located to both the north and south of the Loop 101. Development of Desert Ridge began in 1997 and now includes the 1.1 million square foot Desert Ridge Marketplace power retail center, the 950-room JW Marriott Desert Ridge Resort and Spa, two 18-hole golf courses, and three schools. Desert Ridge is home to Mayo Clinic Hospital and an American Express regional office. According to the appraisal, the population’s average annual growth rate between 2010 and 2022 within a one-, three, and five-mile radius was 6.2%, 2.7%, and 2.0%, respectively. According to the appraisal, the estimated 2022 population within a one-, three- and five-mile radius was approximately 5,882, 65,634, and 199,129, respectively, and the average household income within the same radii was $120,361, $126,319 and $115,545, respectively.

According to a third party market research report, the Office Component is situated within the Paradise Valley submarket of the Phoenix office market. As of July 2022, the Paradise Valley submarket reported inventory of approximately 5.4 million SF with an 11.0% vacancy rate (and a 12.2% availability rate) and average asking rents of $27.75 PSF. The appraisal concluded to market rents ranging from $36.00 to $37.00 per square foot, modified gross, for the various floors of office space at the High Street Property (see table below).

According to a third party market research report, the Retail Component is located within the North Scottsdale submarket of the Phoenix retail market. As of July 2022, the North Scottsdale submarket reported total inventory of approximately 13.9 million SF with a 4.6% vacancy rate and average asking rent of $26.22 PSF. The appraisal concluded to market rents ranging from $21.00 to $29.00 per square foot, triple net, for the retail spaces at the High Street Property (see table below).

According to a third party market research report, the Multifamily Component is located within the North Phoenix submarket of the Phoenix multifamily market. As of July 2022, the North Phoenix multifamily submarket reported total inventory of 41,441 units with a 5.6% vacancy rate and average asking rents of $1,404 per unit (per month). The appraisal concluded to market rents ranging from $1,941 per unit (per month) to $3,625 per unit (per month) for various multifamily unit types at the High Street Property (see table below).

The following table presents certain information relating to the appraisal’s market rent conclusion for the Office Component at the High Street Property:

Office Component Market Rent Summary(1)

| >5,000 square feet | <5,000 square feet | Sprouts | |

| Market Rent (PSF) | $36.50 | $37.00 | $36.00 |

| Lease Term (Years) | 5.4 | 5.4 | 5.4 |

| Lease Type (Reimbursements) | BY Stop | BY Stop | BY Stop |

| Rent Increase Projection | $0.75 PSF annually | $0.75 PSF annually | $0.75 PSF annually |

| Tenant Improvements (New/Renewal) | $50/$20 | $50/$20 | $50/$20 |

| Leasing Commissions (New/Renewal) | 8.5%/5.5% | 8.5%/5.5% | 8.5%/5.5% |

| (1) | Information obtained from the appraisal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

The following table presents certain information relating to the appraisal’s market rent conclusion for the Retail Component at the High Street Property:

Retail Component Market Rent Summary(1)

| Large Restaurants | Small Restaurants | Other | |

| Market Rent (PSF)(2) | $25.00 | $25.00 | $25.00 |

| Lease Term (Years) | 10 | 5 | 5 |

| Lease Type (Reimbursements) | NNN | NNN | NNN |

| Rent Increase Projection | 3.0% annually | 3.0% annually | 3.0% annually |

| Tenant Improvements (New/Renewal) | $60/$20 | $60/$20 | $40/$10 |

| Leasing Commissions (New/Renewal) | 8.5%/5.5% | 8.5%/5.5% | 8.5%/5.5% |

| (1) | Information obtained from the appraisal. |

| (2) | The appraiser did not include market rents for the market rent categories above but concluded to market rents ranging from $21.00 to $29.00 for the individual tenant suites at the property with an average of $25.00 PSF. |

The following table presents certain information relating to the appraisal’s market rent conclusion for the Multifamily Component at the High Street Property:

Multifamily Component Market Rent Summary

| Market Rent Summary | ||||||||

| Unit Mix / Type | Units(1 | Average Unit Size (square feet)(1) | Avg. Monthly Rent per Unit(1) | Avg. Monthly Rent PSF (1) | Avg. Monthly Market Rent per Unit(2) | Avg. Monthly Market Rent PSF(2) | Avg. Monthly Market Rent per Unit (Renovated)(2) | Avg. Monthly Market Rent PSF(Renovated)(2) |

| 1 Bedroom, 1 Bathroom | 24 | 876 | $1,951 | $2.23 | $1,941 | $2.22 | $2,410 | $2.75 |

| 2 Bedrooms, 2 Bathrooms | 60 | 1,263 | $2,570 | $2.03 | $2,462 | $1.95 | $2,987 | $2.36 |

| 2 Bedrooms, 2.5 Bathrooms | 6 | 1,696 | $3,374 | $1.99 | $3,555 | $2.10 | $4,131 | $2.44 |

| 3 Bedrooms, 2.5 Bathrooms | 9 | 1,822 | $3,540 | $1.94 | $3,625 | $1.99 | $4,207 | $2.31 |

| (1) | Based on the borrower rent roll dated June 8, 2022. |

| (2) | Based on the appraisal. |

The table below presents certain information relating to comparable office sales pertaining to the Office Component of the High Street Property identified by the appraiser:

Comparable Office Sales(1)

| Property Name | Location | Year Built/Renovated | Rentable Area (SF) | Occupancy | Sale Date | Sale Price | Sale Price (PSF) |

| Office Component | Phoenix, AZ | 2008/NAP | 333,128(2) | 93.2%(2) | |||

| Camelback Esplanade | Phoenix, AZ | 1989-2002/NAP | 980,041 | 86.0% | Mar-2022 | $385,000,000 | $392.84 |

| Block 23 at Cityscape | Phoenix, AZ | 2019/NAP | 307,030 | 94.0% | Dec-2021 | $150,000,000 | $488.55 |

| Kierland Corporate Center | Scottsdale, AZ | 2000/NAP | 109,811 | 93.0% | Dec-2021 | $37,750,000 | $343.77 |

| Allred Park Place (1650 & 1700) | Chandler, AZ | 2020/NAP | 271,359 | 100.0% | Dec-2021 | $106,000,000 | $390.63 |

| CASA | Phoenix, AZ | 1990/2019 | 181,142 | 92.0% | Aug-2021 | $56,500,000 | $311.91 |

| Anchor Centre | Phoenix, AZ | 1984-1986/NAP | 333,014 | 95.0% | Jan-2021 | $103,500,000 | $310.80 |

| (1) | Information obtained from the appraisal. |

| (2) | Information obtained from the underwritten rent roll. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

The table below presents certain information relating to comparable retail sales pertaining to the Retail Component at the High Street Property identified by the appraiser:

Comparable Retail Sales(1)

| Property Name | Location | Year Built/Renovated | Rentable Area (SF) | Occupancy | Sale Date | Sale Price | Sale Price (PSF) |

| Retail Component | Phoenix, AZ | 2008/NAP | 173,563(2) | 80.1%(2) | |||

| Mountain Vista Marketplace | Mesa, AZ | 2019/NAP | 52,807 | 93.0% | Feb-2022 | $19,867,169 | $376.22 |

| Arcadia Crossing | Phoenix, AZ | 1995/NAP | 454,389 | 85.0% | Nov-2021 | $65,800,000 | $144.81 |

| Gilbert Gateway Towne Center | Gilbert, AZ | 2005/NAP | 265,878 | 85.0% | Nov-2021 | $50,200,000 | $188.81 |

| Camelback Colonnade | Phoenix, AZ | 1993-2005/NAP | 643,000 | 99.0% | Jun-2021 | $165,816,327 | $257.88 |

| Longbow Marketplace | Mesa, AZ | 2017-2020/NAP | 58,507 | 100.0% | May-2021 | $26,000,000 | $444.39 |

| (1) | Information obtained from the appraisal. |

| (2) | Information obtained from the underwritten rent roll. |

The table below presents certain information relating to comparable multifamily sales pertaining to the Multifamily Component at the High Street Property identified by the appraiser:

Comparable Multifamily Sales(1)

| Property Name | Location | Year Built/Renovated | Rentable Area (SF) | Occupancy | Sale Date | Sale Price | Sale Price (PSF) |

| Multifamily Component | Phoenix, AZ | 2008/NAP | 123,392(2) | 97.0%(2) | |||

| Ascent at Papago | Phoenix, AZ | 2007/NAP | 247,052 | 95.0% | Mar-2022 | $107,500,000 | $435.13 |

| Roadrunner on McDowell | Scottsdale, AZ | 2021/NAP | 296,904 | 95.0% | Feb-2022 | $193,500,000 | $651.73 |

| Slate Scottsdale | Scottsdale, AZ | 2016/NAP | 256,016 | 96.0% | Dec-2021 | $114,000,000 | $445.28 |

| Scottsdale Grand | Scottsdale, AZ | 2021/NAP | 251,737 | NAV | Dec-2021 | $130,000,000 | $516.41 |

| District at Scottsdale | Scottsdale, AZ | 2018/NAP | 307,123 | 94.0% | Jul-2021 | $150,500,000 | $490.03 |

| (1) | Information obtained from the appraisal. |

| (2) | Information obtained from the underwritten rent roll. |

Escrows.

Real Estate Taxes – The loan documents require an upfront deposit of $436,773 and ongoing monthly deposits of $145,591 for real estate taxes.

Insurance - The loan documents require ongoing monthly insurance reserves in an amount equal to 1/12th of the insurance premiums that the lender estimates will be payable for the renewal of the coverage afforded by the policies upon the expiration thereof. Notwithstanding the above, the borrower’s obligation to make insurance reserve payments will be waived so long as (i) no event of default is continuing, (ii) the insurance policies maintained by borrower are part of a blanket or umbrella policy approved by the lender in its reasonable discretion, (iii) the lender is provided with evidence of renewal of the insurance policies, and (iv) the lender is provided with paid receipts for the payment of the insurance premiums no later than ten business days prior to the expiration dates of said policies.

Replacement Reserve - The loan documents require an upfront deposit of $5,905,000. The loan documents require springing monthly deposits of $8,396 for replacements if the balance in the reserve falls below the cap of $302,262.

TI/LC Reserve - The loan documents require an upfront deposit of $8,992,000. The loan documents require springing monthly deposits of $21,112 for tenant improvements and leasing commissions if the balance in the reserve falls below the cap of $1,520,073.

Ground Rent Reserve – The loan documents require an upfront deposit of $30,583, and ongoing monthly reserves in an amount equal to 1/12th of the ground rent that lender reasonably estimates to be payable during the next twelve months in order to accumulate sufficient funds to pay the annual ground rent at least 30 days prior to the annual due date, initially estimated at $30,583.

Tenant Specific TI/LC Reserve – The loan documents require an upfront deposit of $1,873,516 for outstanding tenant improvements and leasing commissions related to Humble Bistro ($59,730), Cook & Craft ($26,853), Desert Ridge Veterinary Clinic ($238,877), Gallery Bar ($64,052), RT Specialty ($696,313), Blue Martini Lounge ($225,000), Patio 54 ($3,470), KeHe Distributors ($21,338), Transtar Insurance Brokers ($425,813), M3V Nail Bar ($4,026), State Farm ($6,374), and United Surgical Partners ($101,670).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| Mixed Use – Office/Retail/ Multifamily | Loan #1 | Cut-off Date Balance: | $100,000,000 | |

| 5310-5455 High Street | High Street | Cut-off Date LTV: | 71.5% | |

| Phoenix, AZ 85054 | U/W NCF DSCR: | 1.61x | ||

| U/W NOI Debt Yield: | 8.8% |

Free Rent Reserve – The loan documents require an upfront deposit of $708,593 for certain future rent credits or abatements related to Transtar Insurance Brokers ($306,880), RT Specialty ($223,493), Desert Ridge Veterinary Clinic ($50,213), Gallery Bar ($41,012), United Surgical Partners ($39,655), Blue Martini Lounge ($25,219), Cook & Craft ($16,104), and State Farm ($6,016).

Prepaid Rent Reserve – The loan documents require an upfront deposit of $73,762 for one month of prepaid rent related to each of the following tenants: Cook & Craft ($3,523), Desert Ridge Veterinary Clinic ($7,402), and RT Specialty ($62,838).

Lockbox and Cash Management. The High Street Whole Loan requires a hard lockbox and in-place cash management. The borrowers are required to cause all rents to be deposited directly into the lockbox account, and all rents received by the borrowers or property manager be deposited into the lockbox account within two business days of receipt. Funds in the deposit account will be swept periodically into a cash management account and, prior to a Cash Trap Event Period, any funds remaining in the cash management account after the cash flow waterfall will be transferred to the borrowers. During a Cash Trap Event Period, any excess cash flow remaining after satisfaction of the waterfall items outlined in the High Street Whole Loan documents is required to be swept to an excess cash flow subaccount to be held as additional collateral for the High Street Whole Loan.

A “Cash Trap Event Period” will commence upon the earliest of the following:

| (i) | the occurrence and continuance of an event of default; or |

| (ii) | the net cash flow debt service coverage ratio (“NCF DSCR”) for the High Street Whole Loan falling below 1.10x at the end of any calendar quarter (based on a hypothetical 30 year amortization schedule). |

A Cash Trap Event Period will end upon the occurrence of the following:

| ● | with regard to clause (i) above, the cure of such event of default; or |

| ● | with regard to clause (ii) above: |

(a) the NCF DSCR for the High Street Whole Loan being greater than or equal to 1.15x for two consecutive calendar quarters; or

(b) the borrowers delivering to the lender as additional collateral and security for the payment of the debt, (x) cash to be held as an additional reserve fund that, if applied as a prepayment of the outstanding principal balance of the High Street Whole Loan, would cause the NCF DSCR to be at least 1.15x (the “Cash Management Sweep Cure Amount”), or (y) a letter of credit having an aggregate notional amount in the amount of the Cash Management Sweep Cure Amount.

Property Management. The High Street Property is self-managed by SKB PM I, LLC and GREP Southwest, LLC, each an affiliate of the borrowers.

Partial Release. Not permitted.

Real Estate Substitution. Not permitted.

Subordinate and Mezzanine Indebtedness. Not permitted.

Ground Lease. The High Street Property is subject to two long-term ground leases with the State of Arizona. The ground leases have 70 years remaining and both expire in July 2092 with one, 10-year renewal option. The ground lease payment is equal to the greater of: (i) the stipulated base rent per acre (currently $156,573 ($8,100 per acre)) increasing at an average rate of 7.4% every five years as outlined in the ground lease documents and (ii) 0.35% of the full cash value of the improvements as assessed annually by the Maricopa County Assessor (the “Alternative Rent”). For the lease period beginning in July 2022 and ending in July 2023, the Alternative Rent is $344,682, which is higher than the base rent per acre and used for underwriting purposes.

Letter of Credit. None; however, a letter of credit may be provided to avoid or terminate a Cash Trap Event Period due to clause (ii) as described above under “Lockbox and Cash Management” provided the aggregate amount of any letters of credit do not at any time exceed 10.0% of the outstanding principal balance of the High Street Whole Loan.

Terrorism Insurance. The loan documents require that the “all risk” insurance policy required to be maintained by the borrower, in an amount equal to the full replacement cost of the High Street Property contain no exclusion for damage or destruction caused by acts of terrorism, as well as business interruption insurance covering a period of restoration of 18 months and a 6-month extended period of indemnity.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

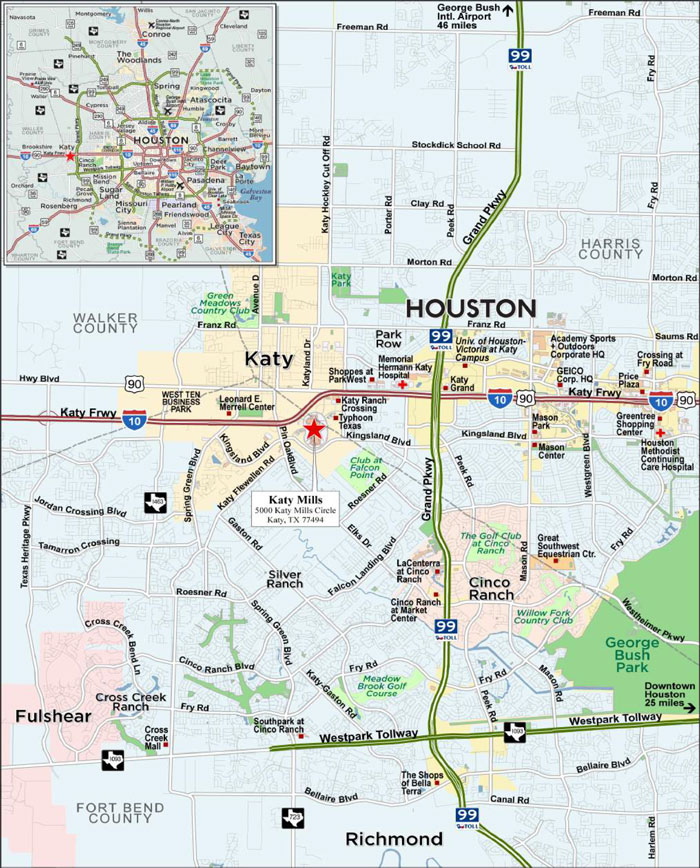

| Retail – Super Regional Mall | Loan # 2 | Cut-off Date Balance: | $91,000,000 | |

| 5000 Katy Mills Circle | Katy Mills | Cut-off Date LTV: | 33.0% | |

| Katy, TX 77494 | U/W NCF DSCR: | 2.91x | ||

| U/W NOI Debt Yield: | 21.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| Retail – Super Regional Mall | Loan # 2 | Cut-off Date Balance: | $91,000,000 | |

| 5000 Katy Mills Circle | Katy Mills | Cut-off Date LTV: | 33.0% | |

| Katy, TX 77494 | U/W NCF DSCR: | 2.91x | ||

| U/W NOI Debt Yield: | 21.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

19

| Retail – Super Regional Mall | Loan # 2 | Cut-off Date Balance: | $91,000,000 | |

| 5000 Katy Mills Circle | Katy Mills | Cut-off Date LTV: | 33.0% | |

| Katy, TX 77494 | U/W NCF DSCR: | 2.91x | ||

| U/W NOI Debt Yield: | 21.8% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

20

| No. 2 – Katy Mills | ||||||

| Mortgage Loan Information | Mortgaged Property Information | |||||

| Mortgage Loan Seller: | BANA | Single Asset/Portfolio: | Single Asset | |||

Credit Assessment (Fitch/KBRA/Moody’s): | NR/NR/Aa1 | Property Type – Subtype: | Retail – Super Regional Mall | |||

| Original Principal Balance(1): | $91,000,000 | Location: | Katy, TX | |||

| Cut-off Date Balance(1): | $91,000,000 | Size: | 1,181,987 SF | |||

| % of Initial Pool Balance: | 8.4% | Cut-off Date Balance Per SF(1): | $109.98 | |||

| Loan Purpose: | Refinance | Maturity Date Balance Per SF(1): | $64.98 | |||

| Borrower Sponsors: | Simon Property Group, L.P. and The KanAm Group | Year Built/Renovated: | 1999/2019 | |||

| Guarantor: | Simon Property Group, L.P. | Title Vesting: | Fee | |||

| Mortgage Rate: | 5.7670% | Property Manager: | Simon Management Associates II, LLC (borrower-related) | |||

| Note Date: | July 21, 2022 | Current Occupancy (As of)(4): | 86.3% (5/3/2022) | |||

| Seasoning: | 0 months | 12/31/2021 Occupancy(4): | 92.3% | |||

| Maturity Date: | August 1, 2032 | 12/31/2020 Occupancy(4): | 91.9% | |||

| IO Period: | 0 months | 12/31/2019 Occupancy(4): | 94.7% | |||

| Loan Term (Original): | 120 months | 12/31/2018 Occupancy(4): | 97.3% | |||

| Amortization Term (Original): | 360 months | As-Is Appraised Value(6): | $394,000,000 | |||

| Loan Amortization Type: | Amortizing Balloon | As-Is Appraised Value Per SF(6): | $333.34 | |||

| Call Protection(2): | L(24),D(90),O(6) | As-Is Appraisal Valuation Date: | May 17, 2022 | |||

| Lockbox Type: | Hard/Springing Cash Management | Underwriting and Financial Information(6) | ||||

| Additional Debt(1): | Yes | TTM 3/31/2022 NOI: | $27,420,178 | |||

| Additional Debt Type (Balance)(1): | Pari Passu ($39,000,000) | 12/31/2021 NOI: | $26,912,547 | |||

| 12/31/2020 NOI(5): | $24,343,858 | |||||

| 12/31/2019 NOI: | $29,158,868 | |||||

| U/W Revenues: | $42,515,577 | |||||

| U/W Expenses: | $14,235,384 | |||||

| Escrows and Reserves(3) | U/W NOI: | $28,280,193 | ||||

| Initial | Monthly | Cap | U/W NCF: | $26,546,115 | ||

| Taxes | $0 | Springing | NAP | U/W DSCR based on NOI/NCF(1): | 3.10x / 2.91x | |

| Insurance | $0 | Springing | NAP | U/W Debt Yield based on NOI/NCF(1): | 21.8% / 20.4% | |

| Replacement Reserve | $0 | $46,008 | $1,104,183(3) | U/W Debt Yield at Maturity based on NOI/NCF(1): | 25.8% / 24.2% | |

| TI/LC Reserve | $0 | $98,487 | $2,363,678(3) | Cut-off Date LTV Ratio(1): | 33.0% | |

| Outstanding TI/LC Reserve | $1,013,945 | $0 | NAP | LTV Ratio at Maturity(1): | 27.8% | |

| Sources and Uses | ||||||||

| Sources | Uses | |||||||

| Whole Loan Amount(1) | $130,000,000 | 91.2% | Loan Payoff(7) | $140,430,426 | 98.5% | |||

| Sponsor Equity | 12,562,007 | 8.8 | Closing Costs | 1,117,635 | 0.8 | |||

| Reserves | 1,013,945 | 0.7 | ||||||

| Total Sources | $142,562,007 | 100.0% | Total Uses | $142,562,007 | 100.0% | |||

| (1) | The Cut-off Date Balance Per SF, Maturity Date Balance Per SF, U/W DSCR based on NOI/NCF, U/W Debt Yield based on NOI/NCF, U/W Debt Yield at Maturity based on NOI/NCF, Cut-off Date LTV Ratio and LTV Ratio at Maturity numbers presented above are based on the Katy Mills Whole Loan (as defined below). |

| (2) | Defeasance of the Katy Mills Whole Loan is permitted at any time after the earlier to occur of (a) the end of the two-year period commencing on the closing date of the securitization of the last portion of the Katy Mills Whole Loan to be securitized and (b) February 1, 2026. The assumed prepayment lockout period of 24 payments is based on the closing date of this transaction in August 2022. |

| (3) | See “Escrows and Reserves” below for further discussion of reserve information. |