Table of Contents

As filed with the Securities and Exchange Commission on February 28, 2006

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F/A

Amendment No. 1

¨ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF

THE SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2005

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period to

OR

¨ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

Commission file number 333-11072

KABUSHIKI KAISHA MITSUBISHI TOKYO UFJ GINKO

(Exact name of Registrant as specified in its charter)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

(Translation of Registrant’s name into English)

Japan

(Jurisdiction of incorporation or organization)

7-1, Marunouchi 2-chome

Chiyoda-ku, Tokyo 100-8388

Japan

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

$2,000,000,000 aggregate principal amount of 8.40% Global Senior Subordinated Notes due April 15, 2010

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

At July 31, 2005, (1) 5,100,869,546 shares of common stock and (2) 100,000,000 shares of preferred stock were issued.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such short period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Yes x No ¨

Indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

Table of Contents

| Page | ||||

| 3 | ||||

Operating and Financial Review and Prospects | 6 | |||

Financial Statements | 59 | |||

Exhibits | 59 | |||

| A-1 | ||||

| F-1 | ||||

2

Table of Contents

We are filing this Form 20-F/A to correct the following inadvertent errors found in our Form 20-F for the fiscal year ended March 31, 2005 previously filed on August 25, 2005:

| 1. | In Note 5 to the consolidated financial statements, the details of loans by domicile and type of industry of borrower at March 31, 2004 and 2005 have been corrected from the amounts previously reported as follows: |

| 2004 | 2005 | |||||||||||

| As previously reported | As restated | As previously reported | As restated | |||||||||

| (in millions) | ||||||||||||

Domestic: | ||||||||||||

Banks and other financial institutions | ¥ | 1,765,377 | ¥ | 1,676,785 | ¥ | 2,447,443 | ¥ | 2,364,504 | ||||

Other industries | 4,750,575 | 4,750,575 | 5,261,648 | 5,344,587 | ||||||||

Consumer | 7,473,998 | 7,562,590 | 7,662,809 | 7,662,809 | ||||||||

Foreign: | ||||||||||||

Banks and other financial institutions | 904,841 | 904,841 | 1,075,339 | 780,666 | ||||||||

Commercial and industrial | 7,063,034 | 7,063,034 | 8,259,006 | 8,553,679 | ||||||||

| 2. | In Note 10 to the consolidated financial statements, the following items at March 31, 2005 have been corrected from the amounts previously reported as follows: |

| (1) | Assets mortgaged, pledged, or otherwise subject to lien: |

| 2005 | ||||||

| As previously reported | As restated | |||||

| (in millions) | ||||||

Trading account securities | ¥ | 2,658,751 | ¥ | 2,301,452 | ||

Investment securities | 4,858,397 | 4,991,587 | ||||

Loans | 4,731,949 | 4,598,759 | ||||

| (2) | Type of liabilities the above pledged assets relate to: |

| 2005 | ||||||

| As previously reported | As restated | |||||

| (in millions) | ||||||

Payables under repurchase agreements and securities lending transactions | ¥ | 3,906,993 | ¥ | 3,549,694 | ||

| (3) | Pledged assets that may not be sold or repledged by the secured parties: |

| 2005 | ||||||

| As previously reported | As restated | |||||

| (in billions) | ||||||

Pledged assets that may not be sold or repledged by the secured parties | ¥ | 12,835 | ¥ | 12,816 | ||

| (4) | Fair value of collateral accepted by the Group which was sold or repledged: |

| 2005 | ||||||

| As previously reported | As restated | |||||

| (in billions) | ||||||

Fair value of collateral accepted by the Group which was sold or repledged | ¥ | 4,937 | ¥ | 5,072 | ||

3

Table of Contents

| 3. | In the parenthetic note to the consolidated balance sheet, the following items at March 31, 2005 have been corrected from the amounts previously reported as follows: |

| 2005 | ||||||

| As previously reported | As restated | |||||

| (in millions) | ||||||

Trading account assets pledged that secured parties are permitted to sell or repledge ………….. | ¥ | 2,626,534 | ¥ | 2,269,235 | ||

Securities available for sale pledged that secured parties are permitted to sell or repledge ……… | 1,557,907 | 1,571,463 | ||||

| 4. | In Note 23 to the consolidated financial statements, the following items at March 31, 2004 and 2005 have been corrected from the amounts previously reported as follows: |

| (1) | Contractual amounts of obligations under guarantees: |

Maximum potential/Contractual | Amount by expiration period | |||||||||||||||||||||||||||||||||||

| Less than 1 year | 1-2 years | 2-3 years | 3-5 years | Over 5 years | ||||||||||||||||||||||||||||||||

| As previously reported | As restated | As previously reported | As restated | As previously reported | As restated | As previously reported | As restated | As previously reported | As restated | As previously reported | As restated | |||||||||||||||||||||||||

| (in billions) | ||||||||||||||||||||||||||||||||||||

March 31, 2004: | ||||||||||||||||||||||||||||||||||||

Standby letters of credit and financial guarantees | ¥ | 2,561 | ¥ | 2,561 | ¥ | 1,043 | ¥ | 1,340 | ¥ | 198 | ¥ | 120 | ¥ | 159 | ¥ | 75 | ¥ | 252 | ¥ | 127 | ¥ | 909 | ¥ | 899 | ||||||||||||

Performance guarantees | 1,192 | 1,192 | 654 | 669 | 199 | 191 | 128 | 125 | 126 | 122 | 85 | 85 | ||||||||||||||||||||||||

March 31, 2005: | ||||||||||||||||||||||||||||||||||||

Standby letters of credit and financial guarantees | ¥ | 3,754 | ¥ | 2,482 | ¥ | 928 | ¥ | 1,247 | ¥ | 659 | ¥ | 124 | ¥ | 257 | ¥ | 97 | ¥ | 686 | ¥ | 244 | ¥ | 1,224 | ¥ | 770 | ||||||||||||

Performance guarantees | 1,353 | 1,353 | 264 | 773 | 564 | 214 | 191 | 113 | 203 | 175 | 131 | 78 | ||||||||||||||||||||||||

| (2) | Commitment amounts of resale and repurchase agreements: |

| 2004 | 2005 | |||||||||||

| As previously reported | As restated | As previously reported | As restated | |||||||||

| (in billions) | ||||||||||||

Resale and repurchase agreements | ¥ | 206 | ¥ | 186 | ¥ | 372 | ¥ | — | ||||

| (3) | Approximate remaining terms of these commitments: |

| 2005 | ||||||||||||||||||

| Within one year | From one year to five years | After five years | ||||||||||||||||

| As previously reported | As restated | As previously reported | As restated | As previously reported | As restated | |||||||||||||

Approximate remaining terms of these commitments | 65 | % | 75 | % | 29 | % | 23 | % | 6 | % | 2 | % | ||||||

In addition, certain reclassifications have been made in the consolidated balance sheets, Notes 3 and 29 to the consolidated financial statements.

4

Table of Contents

As a result of the corrections and reclassifications described above, the relevant figures in Item 5 and Selected Statistical Data have also been corrected or reclassified.

With the exceptions of the foregoing corrections and reclassifications, no other changes have been made to the Form 20-F for the fiscal year ended March 31, 2005.

5

Table of Contents

| Item 5. | Operating and Financial Review and Prospects. |

The following discussion and analysis should be read in conjunction with “Item 3.A. Key Information—Selected Financial Data,” “Selected Statistical Data” and our consolidated financial statements and related notes included elsewhere in this Annual Report.

| Page | ||

Roadmap to Reading the Discussion of Our Operating and Financial Review and Prospects | ||

| 6 | ||

| 6 | ||

| 9 | ||

| 12 | ||

| 14 | ||

| 18 | ||

| 20 | ||

| 21 | ||

| 31 | ||

| 36 | ||

Effect of the Change in Exchange Rates on Foreign Currency Translation | 37 | |

| 38 | ||

| 38 | ||

| 51 | ||

| 54 | ||

| 57 | ||

| 57 | ||

| 58 | ||

| 58 | ||

| 58 | ||

| 58 | ||

G. Safe Harbor | 58 | |

| A. | Operating Results |

We are a wholly owned subsidiary of Mitsubishi Tokyo Financial Group, Inc. We engage in a broad range of financial operations, including commercial banking, investment banking and asset management services, and provide related services to individual and corporate customers.

6

Table of Contents

Key Financial Figures

The following are some key figures in accordance with US GAAP relating to our business:

| Fiscal year ended March 31, | ||||||||||

| 2003 | 2004 | 2005 | ||||||||

| (in billions) | ||||||||||

Net interest income | ¥ | 825.6 | ¥ | 781.3 | ¥ | 808.7 | ||||

Provision (credit) for credit losses | 287.3 | (142.4 | ) | 125.1 | ||||||

Non-interest income | 724.6 | 983.1 | 804.0 | |||||||

Non-interest expense | 973.3 | 1,035.0 | 960.7 | |||||||

Net income | 249.0 | 537.6 | 287.1 | |||||||

Total assets (at end of period) | 77,680.4 | 85,058.6 | 92,050.3 | |||||||

Our revenues consist of net interest income and non-interest income.

Net interest income is a function of:

| • | the amount of interest-earning assets, |

| • | the general level of interest rates, |

| • | the so-called “spread,” or the difference between the rate of interest earned on interest-earning assets and the rate of interest paid on interest-bearing liabilities, and |

| • | the proportion of interest-earning assets financed by non-interest-bearing liabilities and equity. |

Non-interest income consists of:

| • | fees and commissions, including |

| • | trust fees, |

| • | fees on funds transfer and service charges for collections, |

| • | fees and commissions on international business, |

| • | fees and commissions on credit card business, |

| • | service charges on deposits, |

| • | fees and commissions on securities business, and |

| • | other fees and commissions; |

| • | foreign exchange gains (losses)—net, which primarily include net gains (losses) on currency derivative instruments entered into for trading purposes and transaction gains (losses) on the translation into Japanese yen of monetary assets and liabilities denominated in foreign currencies; |

| • | trading account profits—net, which primarily include net gains (losses) on trading securities and interest rate derivative instruments entered into for trading purposes; |

| • | investment securities gains (losses)—net, which primarily include net gains on sales of marketable securities, particularly marketable equity securities; |

| • | equity in earnings (losses) of equity method investees; and |

| • | other non-interest income. |

Provision (credit) for credit losses are charged to operations to maintain the allowance for credit losses at a level deemed appropriate by management. Although in recent periods, we generally recorded a provision for credit losses, we recorded a reversal of allowance for credit losses in the fiscal year ended March 31, 2004.

7

Table of Contents

Business Trends and Challenges

Reduction of nonperforming loans. We have been actively working on disposing nonperforming loans. We met the guideline for the disposal of nonperforming loans, which was based on a Japanese regulation established under the program for financial revival announced by the Japanese government in October 2002. Under the program, the Financial Services Agency stated that it would strive to normalize the problems with nonperforming loans by March 31, 2005, by reducing major Japanese banks’ ratio of nonperforming loans to total loans by about half. The following table sets forth a summary of our nonaccrual and restructured loans, and accruing loans that are contractually past due 90 days or more as to principal or interest payments, and allowance for credit losses at March 31, 2003, 2004 and 2005:

| At March 31, | |||||||||

| 2003 | 2004 | 2005 | |||||||

| (in billions, except percentages) | |||||||||

Nonaccrual loans | ¥1,069.1 | ¥790.5 | ¥631.1 | ||||||

Restructured loans | 1,028.5 | 426.8 | 365.3 | ||||||

Accruing loans contractually past due 90 days or more | 18.1 | 12.0 | 10.1 | ||||||

Nonaccrual and restructured loans, and accruing loans contractually past due 90 days or more as a percentage of loans | 5.29 | % | 3.08 | % | 2.32 | % | |||

Allowance for credit losses | ¥1,058.6 | ¥649.3 | ¥568.5 | ||||||

Allowance for credit losses as a percentage of loans | 2.65 | % | 1.63 | % | 1.31 | % | |||

Allowance for credit losses as a percentage of nonaccrual and restructured loans and accruing loans contractually past due 90 days or more | 50.04 | % | 52.82 | % | 56.48 | % | |||

In the future, we may suffer additional losses due to new nonperforming loans, and our allowance for credit losses may be insufficient to cover future loan losses.

Broader range of products. The reduction of barriers since the late 1990s among the banking, securities and insurance businesses has enabled us to engage in businesses such as sales of annuity and investment trusts to retail banking customers, which we were not permitted to conduct before. We have been seeking, and will continue to seek, to increase our fees and commissions by taking advantage of the reduction of barriers and other deregulatory trends.

Greater competition. We face strong competition in all of our principal areas of operation as a result of the relaxation of regulations relating to Japanese financial institutions. Deregulation has eliminated barriers between different types of Japanese financial institutions, which are now able to compete directly against one another. Deregulation and market factors have also facilitated the entry of various large foreign financial institutions into the Japanese domestic market. Greater competition may prevent us from increasing our level of fee income in the future.

External economic conditions. The financial services industry and the global financial markets are influenced by many unpredictable factors, including economic conditions, monetary policy, international political events, liquidity in global markets and regulatory developments. Our operations are significantly affected by external factors, such as the level and volatility of interest rates, currency exchange rates, stock and real estate markets and other economic and market conditions. In addition, we hold a significant number of shares in some of our customers for strategic purposes, in particular to maintain long-term relationships. These shareholdings expose us to risk of losses resulting from a decline in market prices of the shares. Accordingly, our results of operations may vary significantly from period to period because of unpredictable events, including unexpected failures of large corporate borrowers, defaults in emerging markets and market volatility.

8

Table of Contents

Management Integration of Mitsubishi Tokyo Financial Group and the UFJ Group

Signing of Basic Agreement. On August 12, 2004, Mitsubishi Tokyo Financial Group, Inc., UFJ Holdings, we, UFJ Bank, Mitsubishi Trust Bank, UFJ Trust Bank, Mitsubishi Securities and UFJ Tsubasa Securities concluded a basic agreement with regard to the management integration of the holding companies, banks, trust banks and securities companies of the two groups.

Preferred Stock Investment into UFJ Bank. On September 17, 2004, Mitsubishi Tokyo Financial Group, Inc. purchased 3.5 billion non-voting class E preferred shares issued by UFJ Bank for ¥700 billion. This capital injection to UFJ Bank is part of the proposed management integration with the UFJ group. The investment is based on the assumption that the management integration of the two groups will proceed, and is intended to maximize the benefits of the management integration.

Signing of Integration Agreement. On February 18, 2005, Mitsubishi Tokyo Financial Group, Inc., UFJ Holdings, we, UFJ Bank, Mitsubishi Trust Bank, UFJ Trust Bank, Mitsubishi Securities and UFJ Tsubasa Securities entered into an integration agreement, which sets forth various terms of the management integration, including the merger ratios, company names and other material terms. The merger ratios with respect to the common stock set forth in the integration agreement are as follows:

| • | Holding companies: 0.62 shares of Mitsubishi Tokyo Financial Group, Inc. common stock for each share of UFJ Holdings common stock; |

| • | Banks: 0.62 shares of our common stock for each share of UFJ Bank common stock; |

| • | Trust banks: 0.62 shares of Mitsubishi Trust Bank common stock for each share of UFJ Trust Bank common stock; and |

| • | Securities companies: 0.42 shares of Mitsubishi Securities common stock for each share of UFJ Tsubasa Securities common stock. |

On April 20, 2005, the parties to the integration agreement amended several technical provisions in the integration agreement to make the terms consistent with the merger agreements entered into on April 20, 2005 between the holding companies, banks, trust banks and securities companies.

Announcement of Integration Strategy. On February 18, 2005, Mitsubishi Tokyo Financial Group, Inc. and UFJ Holdings also announced some details about implementing the combined group’s integration strategy. In particular, Mitsubishi Tokyo Financial Group, Inc. and UFJ Holdings announced the following cost saving measures:

| • | A group-wide reduction and reassignment of roughly 10,000 employees by streamlining back office operations mainly in the head office, including a reduction of staff by approximately 6,000 and a reassignment of approximately 4,000 to strategic business areas and marketing sections by the end of the fiscal year ending March 31, 2009. |

| • | Integration of systems relating to treasury activities and overseas activities by the closing of the merger, and integration of the domestic settlement and information systems by the end of the fiscal year ending March 31, 2008. |

| • | Consolidation of approximately 170 retail branches and 100 corporate branches in Japan, and approximately 30 overseas branches by the end of the fiscal year ending March 31, 2009. |

| • | Integration of head office functions and overlapping subsidiaries. |

In implementing the integration strategy, Mitsubishi Tokyo Financial Group, Inc. expects that the combined group’s integration-related costs will exceed cost synergies for the first one to two years following the merger

9

Table of Contents

until the cost saving effects begin to materialize. In addition, Mitsubishi Tokyo Financial Group, Inc. expects that the combined group’s revenues will decrease for the first one to two years after the merger as the combined group adjusts loan exposures to certain borrowers.

Signing of Merger Agreement. On April 20, 2005, we and UFJ Bank entered into a merger agreement setting forth the final terms of the merger, including the detailed terms of our shares to be issued to UFJ Bank’s shareholder and other proposed amendments to our articles of incorporation upon the merger, as well as the details of the shareholders meetings at which the merger agreement and related matters necessary to complete the merger were to be approved.

Approval of Merger Agreement at General Shareholders Meeting. On June 29, 2005, the merger agreement between Mitsubishi Tokyo Financial Group, Inc. and UFJ Holdings, Inc. was approved at the general shareholders meetings of Mitsubishi Tokyo Financial Group, Inc. and UFJ Holdings. The merger agreement between us and UFJ Bank was also approved at the general shareholders meeting of UFJ Bank and at our general shareholders meeting. The general shareholders meetings of Mitsubishi Trust Bank, UFJ Trust Bank, Mitsubishi Securities and UFJ Tsubasa Securities, which were also held in late June 2005, also approved the merger agreements of the respective trust banks and securities companies.

Effect of the Merger. Pursuant to the merger agreement, we will combine our business with that of UFJ Bank by consummating a statutory merger under the Commercial Code of Japan, with The Bank of Tokyo-Mitsubishi, Ltd. being the surviving entity. As a result of the merger, UFJ Bank shareholders of record as of the date one day prior to the date of the merger will become entitled to receive 0.62 shares of our common stock in exchange for each share of UFJ Bank common stock. Concurrently, the surviving entity will be renamed “The Bank of Tokyo-Mitsubishi UFJ, Ltd.”

Postponement of the Merger. Although we originally planned to complete our merger with UFJ Bank on October 1, 2005, we postponed the merger to January 1, 2006 in order to enable additional testing of the two banks’ systems intended to minimize risks arising from the merger. Our merger agreement with UFJ Bank was amended to reflect the postponement, and the amendment is subject to shareholder approval. However, the merger between the parent companies, Mitsubishi Tokyo Financial Group, Inc. and UFJ Holdings, the merger between Mitsubishi Trust Bank and UFJ Trust Bank and the merger between Mitsubishi Securities and UFJ Tsubasa Securities are still expected to occur on October 1, 2005. Additional delays or other difficulties in integrating the systems with UFJ Bank may result in additional costs or cause delays in achieving targeted cost savings and other merger synergies.

Introduction of Integrated Business Groups

Effective April 1, 2004, Mitsubishi Tokyo Financial Group implemented a new integrated business group system, which currently integrates our operations together with the operations of Mitsubishi Trust Bank and Mitsubishi Securities in the following three areas—Retail, Corporate, and Trust Assets.

Issuance of“Non-dilutive” Preferred Securities by a Funding Vehicle of Mitsubishi Tokyo Financial Group, Inc.

On August 24, 2005, MTFG Capital Finance Limited, a special purpose company of Mitsubishi Tokyo Financial Group, Inc. established in the Cayman Islands, issued ¥165 billion in non-cumulative perpetual preferred securities in a private placement to institutional investors. The proceeds will be provided to us through BTM Preferred Capital Limited, our wholly-owned vehicle, to strengthen our capital base under the BIS capital adequacy requirements, and thus the flexibility of our capital management.

Mitsubishi Securities Becomes a Directly-Held Subsidiary of Mitsubishi Tokyo Financial Group, Inc.

On July 1, 2005, Mitsubishi Tokyo Financial Group, Inc. made Mitsubishi Securities a directly-held subsidiary by acquiring all of the shares of Mitsubishi Securities common stock held by us and Mitsubishi Trust Bank. As a result of the transaction, Mitsubishi Tokyo Financial Group holds Mitsubishi Securities common stock representing 57.43% of the voting rights as of July 1, 2005, and we no longer hold any shares of Mitsubishi Securities common stock. For the fiscal year ended March 31, 2005, however, Mitsubishi Securities is reported as one of our consolidated subsidiaries.

10

Table of Contents

Strategic Business and Capital Alliance between Mitsubishi Tokyo Financial Group, Inc. and ACOM

In March 2004, Mitsubishi Tokyo Financial Group, Inc. reached an agreement with ACOM, a consumer finance company in Japan, with respect to a strategic business alliance in retail financial services and a capital alliance. The main elements of the business alliance are undertaken by ACOM and us. As part of the capital alliance, in April 2004, Mitsubishi Tokyo Financial Group, Inc. acquired an additional 12.9% of the common shares of ACOM, resulting in an aggregate ownership interest of 15.1% in ACOM.

Basic Agreement Regarding the Combination of Operations and Reorganization to Strengthen the Consumer Finance Business

On October 29, 2004, Mitsubishi Tokyo Financial Group, Inc., we, DC Card Co., Ltd. and Tokyo-Mitsubishi Cash One Ltd., or Cash One, reached a basic agreement with ACOM to integrate and reorganize the business operations of our consumer finance business. Cash One will integrate its business operations with DC Card’s processing centers, call centers and guarantee divisions during the first half of the fiscal year ending March 31, 2006. On January 31, 2005, ACOM acquired shares in DC Card and Cash One. After the acquisition of the shares, ACOM owns approximately 55% and Mitsubishi Tokyo Financial Group owns approximately 45% of the common shares of Cash One, which has changed its name to DC Cash One Ltd.

Transfer of Shareholdings in Diamond Computer Service

During the fiscal year ended March 31, 2005, Mitsubishi Tokyo Financial Group, Inc. acquired 100% of Diamond Computer Service Co., Ltd., or DCS, which provides data processing and IT development services, through a share exchange. 26,205 shares of Mitsubishi Tokyo Financial Group Inc. common stock were issued in exchange for all of the outstanding shares of DCS’s common stock based on the exchange ratio of 0.00135 shares of Mitsubishi Tokyo Financial Group Inc. common stock for each share of DCS’s common stock. Following the completion of the exchange offer, in accordance with a business alliance between DCS and Mitsubishi Research Institute, Inc., or MRI, a research and consulting company headquartered in Tokyo, Japan, Mitsubishi Tokyo Financial Group Inc. sold 60% of its shares of DCS to MRI.

Planned Merger of Mitsubishi Asset Management and UFJ Partners Asset Management

On July 1, 2005, Mitsubishi Asset Management Co., Ltd. and UFJ Partners Asset Management Co., Ltd. signed a merger agreement, which was subsequently approved at the general meeting of shareholders of the respective companies on July 25, 2005.

Mitsubishi Asset Management was created on October 1, 2004 by the merger of Tokyo-Mitsubishi Asset Management Ltd. and Mitsubishi Trust Asset Management Co., Ltd., and we own 15% of Mitsubishi Asset Management. The merger of Mitsubishi Asset Management and UFJ Partners Asset Management is scheduled to be completed on October 1, 2005. The name of the new asset management company will be Mitsubishi UFJ Asset Management Co., Ltd.

Business Revitalization Plan of Mitsubishi Motors

On January 28, 2005, Mitsubishi Motors Corporation announced a new business revitalization plan through the fiscal year ending March 31, 2008. The new revitalization plan includes measures for stabilizing Mitsubishi Motors’ operations and improving its financial position over the medium- and long-term. In connection with the revitalization plan, and at the request of Mitsubishi Motors, we, Mitsubishi Heavy Industries, Ltd. and Mitsubishi Corporation participated in a capital enhancement of ¥274 billion by purchasing newly issued common and preferred shares of Mitsubishi Motors on March 10, 2005. As a result, we subscribed to common and preferred shares of Mitsubishi Motors for an aggregate amount of ¥154 billion, of which ¥54 billion consisted of a debt-for-equity swap. In addition, on March 22, 2005, Mitsubishi Trust Bank purchased, in a debt-for-equity swap, newly issued preferred shares of Mitsubishi Motors for an aggregate amount of ¥10.2 billion.

11

Table of Contents

Suspension of Consolidated Corporate-Tax System

In February 2005, Mitsubishi Tokyo Financial Group, Inc.’s application to suspend the consolidated corporate-tax system, which has been adopted since the fiscal year ended March 31, 2003, was approved by the Japanese tax authorities. Mitsubishi Tokyo Financial Group, Inc. filed for the fiscal year ended March 31, 2005, its tax returns under the consolidated corporate-tax system, which allows companies to base tax payments on the combined profits or losses of a parent company and its wholly-owned domestic subsidiaries. Due to the suspension of the consolidated corporate-tax system, deferred income taxes have been calculated separately based on temporary differences as of March 31, 2005 and future taxable income at each company.

Transfer to the Japanese Government of the Substitutional Portion of Employee Pension Fund Liabilities

As discussed under “Accounting Changes” below, the substitutional portion of our employee pension fund liabilities was transferred to the Japanese government in March 2005. Since the transfer was completed after the measurement date in the fiscal year ended March 31, 2005, the impact of the transfer, an increase in pre-tax income of ¥36.1 billion, will be reflected to our consolidated financial statements for the fiscal year ending March 31, 2006.

Strengthening of Corporate Governance in the United States

Mitsubishi Tokyo Financial Group, Inc. has decided to strengthen its corporate governance function in the United States by appointing a managing officer with responsibility for corporate governance in the United States as of June 29, 2005. This managing officer will be resident in the United States and will oversee governance-related matters with respect to Mitsubishi Tokyo Financial Group’s U.S. consolidated subsidiaries, including risk management, and legal and other compliance issues. In conjunction with this appointment, Mitsubishi Tokyo Financial Group, Inc. has also established a Corporate Governance Division for the United States to carry out support functions for the managing officer.

Purchase of 50% of Our Head Office and Nihonbashi Annex

On July 21, 2005, we announced that we reached an agreement to purchase from Mitsubishi Estate Co., Ltd., or Mitsubishi Estate, the equivalent of 50% of the land and building of each of our head office and Nihonbashi annex. These assets are currently jointly owned by us and Mitsubishi Estate. The purchase is scheduled to take place on August 31, 2005 and the total purchase price will be ¥111.3 billion. For further information, see note 7 to our consolidated financial statements.

We engage in a wide range of financial operations, including commercial banking, investment banking, asset management and securities-related businesses, and provide related services to individual and corporate customers around the world. Our results of operations and financial condition are exposed to changes in various external economic factors, including:

| • | General economic conditions; |

| • | Interest rates; |

| • | Currency exchange rates; and |

| • | Stock and real estate prices. |

12

Table of Contents

Economic Environment in Japan

In the Japanese economy, exports and capital expenditures rose due to increased overseas demand in the early part of the current period. Private consumption also steadily increased as consumer confidence improved. Nevertheless, a certain degree of uncertainty prevailed over the Japanese economy from the latter part of the fiscal year ended March 31, 2005 and deflation continued.

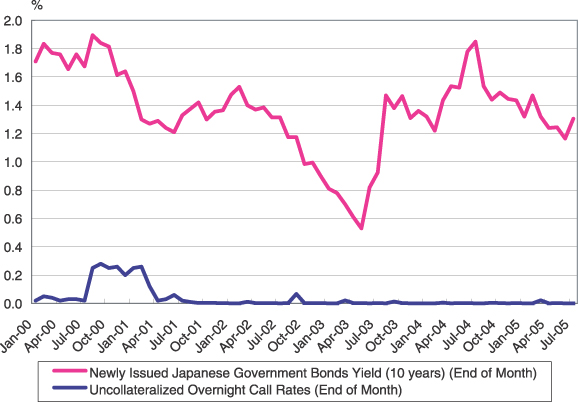

With respect to interest rates, the Bank of Japan continued its current easy monetary policy and kept short-term interest rates at near zero percent. On the other hand, the yield on ten-year Japanese government bonds which was approximately 1.4% in April 2004, rose temporarily to approximately 1.9% in June and July 2004, before declining to approximately 1.3% in March 2005. As of mid-August 2005, the yield was around 1.4%. The following chart shows the interest rate trends in Japan since January 2000:

The Japanese stock markets were relatively stable during the fiscal year ended March 31 2005. The Nikkei Stock Average, which is an average of 225 blue chip stocks listed on the Tokyo Stock Exchange, declined from ¥11,715.39 at March 31, 2004 to ¥11,668.95 at March 31, 2005. Conversely, the Tokyo Stock Price Index, or TOPIX, a composite index of all stocks listed on the First Section of the Tokyo Stock Exchange, rose from 1,179.23 at March 31, 2004 to 1,182.18 at March 31, 2005. As of mid-August 2005, the Nikkei Stock Average was around ¥12,000, and TOPIX was around 1,200.

In the foreign exchange markets, although the yen initially depreciated against the U.S. dollar mainly due to the rise in the U.S. federal funds rate, the exchange rate subsequently stabilized and remained within a narrow range. See “Item 3. A. Key Information—Selected Financial Data—Exchange Rate Information” for the historical noon buying rates of the Federal Reserve Bank of New York.

Land prices in Japan continued to decline during the fiscal year ended March 31, 2005, but the extent of the decline was smaller than the previous fiscal year. Based on the average government-set official land prices as of

13

Table of Contents

January 1, 2005, nationwide residential land prices declined 4.6%, compared to a 5.7% decline in the previous fiscal year, and nationwide land prices for commercial properties declined 5.6%, compared to a 7.4% decline in the previous fiscal year.

The number of corporate bankruptcy filings in Japan during the fiscal year ended March 31, 2005 was approximately 13,000 representing a 16% decline compared with the previous fiscal year.

International Financial Markets

With respect to the financial and economic environment for the fiscal year ended March 31, 2005, overseas economies moved toward recovery in the early part of this period, particularly in the United States where the recovery was driven by large-scale tax cuts, and in China where domestic demand continued to expand. In the latter part of the fiscal year, however, a certain degree of uncertainty prevailed in overseas economies as the positive effects of the tax cuts in the United States began to wane, as China began to restrain investments and as crude oil prices rose sharply.

In the United States, the 10-year U.S. treasury note, a benchmark for long-term interest rates, started at around 3.8% in April 2004 and rose to around 4.5% in March 2005. As of mid-July 2005, the yield was around 4.2%. The target for the federal funds rate has been steadily increased since the end of the previous fiscal year, rising from 1.0% in April 2004 to 3.5% as of August 2005.

In the EU, the European Central Bank’s policy rate remained at 2% during the fiscal year ended March 31, 2005 and has remained unchanged as of July 2005.

Our financial statements are prepared in accordance with US GAAP. Many of the accounting policies require management to make difficult, complex or subjective judgments regarding the valuation of assets and liabilities. The accounting policies are fundamental to understanding our operating and financial review and prospects. The notes to our consolidated financial statements provide a summary of our significant accounting policies. The following is a summary of the critical accounting estimates.

Allowance for Credit Losses

The allowance for credit losses represents management’s estimate of probable losses in our loan portfolio. The evaluation process involves a number of estimates and judgments. The allowance is based on two principles of accounting: (1) Statement of Financial Accounting Standards, or SFAS, No. 5, “Accounting for Contingencies,” which requires that losses be accrued when they are probable of occurring and can be estimated; and (2) SFAS No. 114, “Accounting by Creditors for Impairment of a Loan” and SFAS No. 118, “Accounting by Creditors for Impairment of a Loan—Income Recognition and Disclosures,” which require that losses be accrued based on the difference between the present value of expected future cash flows discounted at the loan’s effective interest rate, the fair value of collateral or the loan’s value that is observable in the secondary market and the loan balance.

Our allowance for credit losses consists of an allocated allowance and an unallocated allowance. The allocated allowance comprises (a) the allowance for specifically identified problem loans, (b) the allowance for large groups of smaller balance homogeneous loans, (c) the allowance for loans exposed to specific country risk and (d) the formula allowance. Both the allowance for loans exposed to specific country risk and formula allowance are provided to performing loans, that are not subject to either the allowance for specifically identified problem loans or the allowance for large groups of smaller balance homogeneous loans. The allowance for loans exposed to specific country risk covers transfer risk which is not specifically covered by other types of allowance. Each of these components is determined based upon estimates that can and do change when actual events occur.

The allowance for specifically identified problem loans, which represent large-balance, non-homogeneous loans that have been individually determined to be impaired, uses various techniques to arrive at an estimate of loss. Historical loss information, discounted cash flows, fair value of collateral and secondary market information are all used to estimate those losses.

14

Table of Contents

Large groups of smaller balance homogeneous loans are collectively evaluated for impairment, and the allowance for such loans is established through a process that begins with estimates of probable losses inherent in the portfolio, based upon various analyses, including historical delinquency and credit loss experience.

The allowance for loans exposed to specific country risk is based on an estimate of probable losses relating to our exposure to countries that we identify as having a high degree of transfer risk. We use a country risk grading system that assigns risk ratings to individual countries. To determine the risk rating, we consider the instability of foreign currency and difficulties regarding our borrowers’ ability to service their debt.

The formula allowance uses a model based on historical losses as an indicator of future probable losses. However, the use of historical losses is inherently uncertain and as a result could differ from losses incurred in the future. However, since this history is updated with the most recent loss information, the differences that might otherwise occur are mitigated.

Our actual losses could be more or less than the estimates. The unallocated allowance captures losses that are attributable to various economic events, industry or geographic sectors whose impact on the portfolio have occurred but have yet to be recognized in the allocated allowance. For further information regarding our allowance for credit losses, see “Item 5.B. Liquidity and Capital Resources—Financial Condition—Allowance for Credit Losses, Nonperforming and Past Due Loans.”

In addition to the allowance for credit losses on our loan portfolio, we maintain an allowance for credit losses on off-balance-sheet credit instruments, including commitments to extend credit, a variety of guarantees and standby letters of credit. Such allowance is included in other liabilities. With regard to the allocated allowance for specifically identified credit exposure and the allocated formula allowance, we apply the same methodology that we use in determining the allowance for loan credit losses.

To the extent that actual losses differ from management’s estimates, additional provisions for credit losses may be required that would adversely impact our operating results and financial condition in future periods.

Impairment of Investment Securities

US GAAP requires the recognition in earnings of an impairment loss on investment securities for a decline in fair value that is other than temporary. Determinations of whether a decline is other than temporary often involves estimating the outcome of future events. Management judgment is required in determining whether factors exist that indicate that an impairment loss has been incurred at the balance sheet date. These judgments are based on subjective as well as objective factors. We conduct a review semi-annually to identify and evaluate investment securities that have indications of possible impairment.

Debt and marketable equity securities. In determining whether a decline in fair value is other than temporary for a particular security, indicators of an other-than-temporary decline for both debt and marketable equity securities include the extent of decline in fair value below cost and the length of time that the decline has continued. If a decline in fair value is 20% or more or a decline in fair value has continued for six months or more, we generally deem such decline as an indicator of other-than-temporary decline. We also consider the financial condition and near-term prospects of issuers primarily based on the credit standing of the issuers as determined by our credit rating system.

Prior to the fiscal year ended March 31, 2004, we did not take the lengths of time that a decline continued into consideration with respect to debt securities because a substantial majority of our investments in debt securities are in high-grade fixed-rate bonds, including sovereign bonds such as U.S. treasury bonds and we generally had the intent to hold such investments for a period longer than that inherent in cyclical short-term market price fluctuations due to market interest rate and foreign exchange rate changes. However, in light of the recent decline in the bond market, which made it difficult for us to hold debt securities for a period longer than that necessary for recovery, during the fiscal year ended March 31, 2004, we determined that the length of period that a decline

15

Table of Contents

in fair value continued should be considered in identifying other-than temporary decline in fair value of debt securities. The aggregate amount of unrealized losses at March 31, 2005 that we determined to be temporary was ¥34,884 million.

The determination of other-than-temporary impairment for certain securities held by UnionBanCal Corporation, our U.S. subsidiary, which primarily consists of securities backed by the full faith and credit of the U.S. government and corporate asset-backed and debt securities, are made on the basis of a cash flow analysis of securities and/or the ability of UnionBanCal Corporation to hold such securities to maturity.

Non-marketable equity securities. We consider the credit standing of issuers and the extent of decline in net assets of issuers to determine whether the decline is other than temporary. When we determine that the decline is other than temporary, non-marketable equity securities are written down to our share of the amount of the issuer’s net assets, which approximates fair value.

The markets for equity securities and debt securities are inherently volatile, and the values of both types of securities have fluctuated significantly in recent years. Accordingly, our assessment of potential impairment involves risks and uncertainties depending on the market condition. If we later conclude that a decline is other than temporary, the impairment loss may significantly affect our operating results and financial condition in future periods.

Valuation of Deferred Tax Assets

A valuation allowance for deferred tax assets is recognized if, based on the weight of available evidence, it is more likely than not that some portion or all of the deferred tax assets will not be realized. All available evidence, both positive and negative, is considered to determine whether, based on the weight of that evidence, a valuation allowance is needed. Future realization of the tax benefit of existing deductible temporary differences or carryforwards ultimately depends on the existence of sufficient taxable income in future periods.

In determining a valuation allowance, we perform a review of future taxable income (exclusive of reversing temporary differences and carryforwards) and future reversals of existing taxable temporary differences. Due to losses in recent years and continuing weak economic conditions, the determination of the valuation allowance involves difficult judgments to estimate future taxable income.

At March 31, 2005, we had operating loss carryforwards of ¥982.2 billion. Based on our estimates of future taxable income, we recognized a valuation allowance for a portion of the operating loss carryforwards.

Because the establishment of the valuation allowance is an inherently uncertain process involving estimates, currently established allowance may not be sufficient. If the estimated allowance is not sufficient, we will incur additional deferred tax expenses, which could materially affect our operating results and financial condition in future periods.

Accounting for Goodwill

US GAAP requires us to test goodwill for impairment at least annually using a two-step process that begins with an estimation of the fair value of a reporting unit of our business, which is to be compared with the carrying amount of the unit, to identify potential impairment of goodwill. The fair value of a reporting unit is defined as the amount at which the unit as a whole could be bought or sold in a current transaction between willing parties. Since an observable quoted market price for units is not always available, the estimate of fair value is based on the best information available, including prices for comparable units and the results of using other valuation techniques including the present value technique, which requires an estimate of future cash flows and other assumptions. If the carrying amount of a reporting unit exceeds its estimated fair value, the second step of the goodwill impairment test is performed to measure the amount of impairment loss. This test requires comparison

16

Table of Contents

of the implied fair value of the unit’s goodwill with the carrying amount of that goodwill. The estimate of the implied fair value of the reporting unit’s goodwill requires us to allocate the fair value of a reporting unit to all of the assets and liabilities of that unit, including unrecognized intangible assets, if any, since the implied fair value is determined as the excess of the fair value of a reporting unit over the net amounts assigned to its assets and liabilities in the allocation. Accordingly, the second step of the impairment test also requires an estimate of the fair value of individual assets and liabilities, including any unrecognized intangible assets that belong to that unit.

At March 31, 2005, we had goodwill of ¥56.1 billion. In connection with our merger with UFJ Bank, we expect to record a significant amount of additional goodwill.

Accrued Severance Indemnities and Pension Liabilities

We have defined benefit retirement plans, including lump-sum severance indemnities and pension plans, which cover substantially all of our employees. Severance indemnities and pension costs are calculated based upon a number of actuarial assumptions, including discount rates, expected long-term rates of return on our plan assets and rates of increase in future compensation levels. In accordance with US GAAP, actual results that differ from the assumptions are accumulated and amortized over future periods, and affect our recognized net periodic pension costs and accrued severance indemnities and pension obligations in future periods. We had an unrecognized net actuarial loss for domestic severance indemnities and pension plans of ¥281.8 billion at March 31, 2005. Differences in actual experience or changes in assumptions may affect our financial condition and operating results in future periods.

The discount rates for the domestic plans are set to reflect the interest rates of high-quality fixed-rate instruments with maturities that correspond to the timing of future benefit payments.

In developing our assumptions for expected long-term rates of return, we refer to the historical average returns earned by the plan assets and the rates of return expected to be available for reinvestment of existing plan assets, which reflect recent changes in trends and economic conditions, including market price. We also evaluate input from our actuaries, including their reviews of asset class return expectations.

Valuation of Financial Instruments with No Available Market Prices

Some assets and liabilities, including available-for-sale securities, trading accounts and derivatives, are reflected at their estimated fair values in our financial statements. Fair values for the substantial majority of our portfolio of financial instruments with no available market prices are determined based upon externally verifiable model inputs and quoted prices. All financial models, which are used for independent risk monitoring, must be validated and periodically reviewed by qualified personnel independent of the area that created the model. The fair value of derivatives is determined based upon liquid market prices evidenced by exchange-traded prices, broker-dealer quotations or prices of other transactions with similarly rated counterparties. If available, quoted market prices provide the best indication of value. If quoted market prices are not available for fixed maturity securities and derivatives, we discount expected cash flows using market interest rates commensurate with the credit quality and maturity of the investment. Alternatively, we may use matrix or model pricing to determine an appropriate fair value. In determining fair values, we consider various factors, including time value, volatility factors and underlying options, warrants and derivatives.

The estimated fair values of financial instruments without quoted market prices are as follows:

| At March 31, | ||||||

| 2004 | 2005 | |||||

| (in billions) | ||||||

Financial assets: | ||||||

Trading account assets, excluding derivatives | ¥ | 5,544 | ¥ | 5,006 | ||

Investment securities | 18,568 | 20,909 | ||||

Derivative financial instruments, net | 108 | 49 | ||||

Financial liabilities: | ||||||

Trading account liabilities, excluding derivatives | 153 | 5 | ||||

Obligations to return securities received as collateral | 2,317 | 3,015 | ||||

17

Table of Contents

A significant portion of trading account assets and liabilities, excluding derivatives, investment securities and obligations to return securities received as collateral consists of Japanese national government and agency bonds, and foreign government and official institutions bonds, for which prices are actively quoted among brokers and are readily available but are not publicly reported and therefore are not considered quoted market prices. Additionally, a substantial portion of derivative financial instruments are comprised of over-the-counter interest rate and currency swaps and options. Estimates of fair value of these derivative transactions are determined using quantitative models with multiple market inputs, which can be validated through external sources, including brokers and market transactions with third parties.

Variable Interest Entities—In January 2003, the Financial Accounting Standards Board, or FASB, issued FASB Interpretation, or FIN, No. 46, “Consolidation of Variable Interest Entities, an interpretation of ARB No. 51.” FIN No. 46 addresses consolidation by business enterprises of variable interest entities, or VIEs. The consolidation requirements of FIN No. 46 apply immediately to VIEs created after January 31, 2003. We have applied, as required, FIN No. 46 to all VIEs created after January 31, 2003. The consolidation requirements apply to older entities in the first fiscal year or interim period beginning after June 15, 2003, which has been amended by the FASB as described below.

In December 2003, the FASB issued FIN No. 46 (revised December 2003), “Consolidation of Variable Interest Entities, an interpretation of ARB No. 51,” or FIN No. 46R. FIN No. 46R modifies FIN No. 46 in certain respects including the scope exception, the definition of VIEs, and other factors that would affect the determination of VIEs and primary beneficiaries that must consolidate VIEs. FIN No. 46R, as written, applies to VIEs created before February 1, 2003 no later than the end of the first reporting period that ends after March 15, 2004, and to all special purpose entities no later than the first reporting period that ends after December 15, 2003. Subsequent to the issuance of FIN No. 46R, the Chief Accountant of the U.S. Securities and Exchange Commission, or SEC, stated the SEC staff’s position in a letter to the American Institute of Certified Public Accountants, or AICPA, dated March 3, 2004, that the SEC staff does not object to the conclusion that FIN No. 46R should not be required to be applied at a date earlier than the original FIN No. 46 and that foreign private issuers would be required to apply FIN No. 46R at various dates depending on the entity’s year-end and the frequency of interim reporting. In accordance with the letter, we adopted FIN No. 46R on April 1, 2004, except for its variable interest in certain investment companies, for which the effective date of FIN No. 46R is deferred. Under FIN No. 46R, any difference between the net amount added to the balance sheet and the amount of any previously recognized interest in the VIE is to be recognized as a cumulative effect of a change in accounting principle. The cumulative effect of the change in accounting principle was to decrease net income by ¥977 million. See note 24 to our consolidated financial statements for further discussion of VIEs in which we hold variable interests.

Certain Financial Instruments with Characteristics of both Liabilities and Equity—In May 2003, the FASB issued SFAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity.” SFAS No. 150 establishes standards for how an issuer classifies and measures certain financial instruments with characteristics of both liabilities and equity. SFAS No. 150 is effective at the beginning of the first interim period beginning after June 15, 2003, which is our fiscal year ended March 31, 2005. On November 7, 2003, FASB Staff Position No. 150-3, “Effective Date, Disclosures, and Transition for Mandatorily Redeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests under FASB Statement No. 150, Accounting for Certain Financial Instruments with Characteristics of Both Liabilities and Equity,” delayed the effective date of certain provisions of SFAS No. 150 for certain mandatorily redeemable noncontrolling interests. The adoption of SFAS No. 150 did not have a material impact on our financial position and results of operations.

Disclosure about Pension and Other Postretirement Benefit—In December 2003, the FASB issued SFAS No. 132 (revised 2003), “Employers’ Disclosures about Pensions and Other Postretirement Benefits, an amendment of FASB Statements No. 87, 88, and 106,” or SFAS No. 132R, which replaces existing FASB disclosure requirements for pensions. SFAS No. 132R requires disclosure of more details about plan assets,

18

Table of Contents

benefit obligations, cash flows, benefit costs and other relevant information. SFAS No. 132R is generally effective for the fiscal years ending after December 15, 2003, and for interim periods beginning after December 15, 2003. See note 15 to our consolidated financial statements for the required disclosure.

Impairment of securities investments—In November 2003, the FASB Emerging Issues Task Force, or the EITF, reached a consensus on Issue No. 03-1, “The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments,” or EITF 03-1. EITF 03-1 requires certain additional quantitative and qualitative disclosures in addition to the disclosures already required by SFAS No. 115, “Accounting for Certain Investments in Debt and Equity Securities.” The new disclosure requirements are applied to financial statements for the fiscal years ending after December 15, 2003. See note 4 to our consolidated financial statements for the required disclosure. In March 2004, the EITF also reached a consensus on additional accounting guidance for other-than-temporary impairments, which requires an evaluation and recognition of other-than-temporary impairment by a three-step impairment test. The guidance should be applied for reporting periods beginning after June 15, 2004. On September 30, 2004, FASB Staff Position EITF Issue 03-1-1, “The Meaning of Other-Than-Temporary Impairment and its Application to Certain Investments” delayed the effective date for the measurement and recognition guidance contained in paragraphs 10 through 20 of EITF 03-1. The FASB will be issuing implementation guidance related to this topic. Once issued, we will evaluate the effect of the measurement and recognition provision of EITF 03-1.

Goodwill and Other Intangible Assets—Effective April 1, 2002, we adopted SFAS No. 142, “Goodwill and Other Intangible Assets.” SFAS No. 142 requires that goodwill, formerly amortized over its useful life, no longer be amortized but rather tested for impairment at least annually. Further, SFAS No. 142 requires that intangible assets that have finite useful lives will continue to be amortized over their useful lives while intangible assets with indefinite lives will no longer be amortized and are subject to impairment testing at least annually.

We performed the required transitional impairment tests of goodwill and intangible assets with indefinite lives upon adoption of SFAS No. 142. The initial adoption resulted in a cumulative adjustment charge to earnings of ¥532 million for the fiscal year ended March 31, 2003.

Derivative Instruments and Hedging Activities— In April 2003, the FASB issued SFAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging Activities.” SFAS No. 149 amends and clarifies accounting for derivative instruments, including certain derivative instruments embedded in other contracts, and for hedging activities under SFAS No. 133. In particular, SFAS No. 149 (1) clarifies under what circumstances a contract with an initial net investment meets the characteristics of a derivative, (2) clarifies when a derivative contains a financing component that warrants special reporting in the statement of cash flows, (3) amends the definition of underlyings, one of the components of the three characteristics of a derivative instrument, to include the occurrence or non-occurrence of a specified event such as a scheduled payment under a contract, and (4) amends certain other existing pronouncements, in particular, those related to the scope of instruments that are subject to the requirements of SFAS No. 133. SFAS No. 149 is generally effective for contracts entered into or modified after June 30, 2003. The adoption of SFAS No. 149 did not have a material impact on our financial position or results of operations.

Transfer to the Japanese Government of the Substitutional Portion of Employee Pension Fund Liabilities—In January 2003, the EITF reached a consensus on Issue No. 03-2, “Accounting for the Transfer to the Japanese Government of the Substitutional Portion of Employee Pension Fund Liabilities,” or EITF 03-2, which was ratified by the FASB in February 2003. EITF 03-2 addresses accounting for a transfer to the Japanese government of a substitutional portion of an employee pension fund and requires employers to account for the entire separation process of the substitutional portion from an entire plan upon completion of the transfer to the government of the substitutional portion of the benefit obligation and related plan assets as the culmination of a series of steps in a single settlement transaction. It also requires that the difference between the fair value of the obligation and the assets required to be transferred to the government, if any, should be accounted for as a subsidy from the government, separately from gain or loss on settlement of the substitutional portion of the obligation, upon completion of the transfer.

19

Table of Contents

In June 2003, we submitted to the government an application to transfer the obligation to pay benefits for future employee service related to the substitutional portion and the application was approved in August 2003. In August 2004, we made another application for transfer to the government of the remaining substitutional portion and the application was approved in November 2004. Substitutional obligation and related plan assets were transferred to a government agency in March 2005 and we were released from paying the substitutional portion of the benefits to our employees. The completion of the transfer to the Japanese Government of the substitutional portion of the employee pension plan constituted a settlement of such plan. However, since there remains a defined benefit plan and the settlement occurred subsequent to December 31, 2004 (the measurement date of such plan), the impact of the transfer / settlement of a pre-tax income of ¥36.1 billion will be recognized in the fiscal year ending March 31, 2006. See note 15 to our consolidated financial statements for the required disclosure.

Recently Issued Accounting Pronouncements

Accounting for Certain Loans and Debt Securities Acquired in a Transfer—In December 2003, the AICPA issued Statement of Position 03-3, “Accounting for Certain Loans or Debt Securities Acquired in a Transfer,” or SOP 03-3, which supersedes AICPA Practice Bulletin 6, “Amortization of Discounts on Certain Acquired Loans” and addresses accounting for differences between contractual cash flows and cash flows expected to be collected from an investor’s initial investment in loans or debt securities acquired in a transfer if those differences are attributable, at least, in part, to credit quality. SOP 03-3 requires acquired impaired loans for which it is probable that the investor will be unable to collect all contractually required payments receivable to be recorded at the present value of amounts expected to be received and prohibits carrying over or creation of valuation allowances in the initial accounting for these loans. SOP 03-3 also limits accretable yield to the excess of the investor’s estimate of undiscounted cash flows over the investor’s initial investment in the loan and prohibits the recognition of the non-accretable difference. Subsequent increases in cash flows expected to be collected generally should be recognized prospectively through adjustment of the loan’s yield over its remaining life while any decreases in cash flows expected to be collected should be recognized as impairments. SOP 03-3 also provides guidance with regard to presentation and disclosures. SOP 03-3 is effective for loans acquired in the fiscal years beginning after December 15, 2004. We have not completed the study of what effect SOP 03-3 will have on our financial position and results of operations.

Share-Based Payment—In December 2004, the FASB issued SFAS No. 123 (revised 2004), “Share-Based Payment,” or SFAS No. 123R. SFAS No. 123R replaces SFAS No. 123, “Accounting for Stock-Based Compensation,” and supersedes Accounting Principles Board Opinion, or APB, No. 25, “Accounting for Stock Issued to Employees.” SFAS No. 123 preferred a fair-value-based method of accounting for share-based payment transactions with employees, but it permitted the option of continuing to apply the guidance of using intrinsic-value-based measurement method in APB No. 25, as long as the footnotes to the financial statements disclosed what net income would have been had the preferable fair-value-based method been used. SFAS No. 123R establishes fair value as the measurement objective in accounting for share-based payment arrangements and requires a fair-value-based measurement method in accounting for share-based payment transactions with employees. As a result, the cost resulting from all share-based payment transactions shall be recognized in the financial statements. SFAS No. 123R is effective as of the beginning of the interim or annual reporting periods beginning after June 15, 2005. Seenote 1 to our consolidated financial statements for the pro forma information as if the fair value based method had been applied to all awards in accordance with SFAS No. 123.

Exchanges of Nonmonetary Assets—In December 2004, the FASB issued SFAS No. 153, “Exchanges of Nonmonetary Assets, an amendment of APB Opinion No. 29.” The guidance in APB No. 29, “Accounting for Nonmonetary Transactions,” is based on the principle that exchanges of nonmonetary assets should be measured based on the fair value of the assets exchanged. The guidance in APB No. 29, however, included certain exceptions to that principle. SFAS No. 153 amends APB No. 29 to eliminate the exception for nonmonetary exchanges of similar productive assets and replaces it with a general exception for exchanges of nonmonetary assets that do not have commercial substance. A nonmonetary exchange has commercial substance if the future cash flows of the entity are expected to change significantly as a result of the exchange. SFAS No. 153 is

20

Table of Contents

effective for nonmonetary asset exchanges occurring in fiscal periods beginning after June 15, 2005, with earlier adoption permitted. We have not completed the study of what effect SFAS No. 153 will have on our financial position and results of operations.

Accounting Changes and Error Corrections—In May 2005, the FASB issued SFAS No. 154, “Accounting Changes and Error Corrections—a replacement of APB Opinion No. 20 and FASB Statement No. 3.” SFAS No. 154 replaces APB No. 20, “Accounting Changes,” and SFAS No. 3, “Reporting Accounting Changes in Interim Financial Statements,” and changes the requirements for the accounting for and reporting of a change in accounting principle. This Statement applies to all voluntary changes in accounting principle. It also applies to changes required by an accounting pronouncement in the unusual instance that the pronouncement does not include specific transition provisions. SFAS No. 154 is effective for accounting changes and corrections of errors made in fiscal years beginning after December 15, 2005, with earlier adoption permitted. Accordingly, we can not reasonably estimate the ultimate impact of SFAS No. 154.

Accounting for Conditional Asset Retirement Obligations—In March 2005, the FASB issued FIN No. 47, “Accounting for Conditional Asset Retirement Obligations—an interpretation of FASB Statement No. 143.” This Interpretation clarifies that the term “conditional asset retirement obligation” as used in SFAS No. 143, “Accounting for Asset Retirement Obligations,” refers to a legal obligation to perform an asset retirement activity in which the timing and (or) method of settlement are conditional on a future event that may or may not be within the control of the entity. The obligation to perform the asset retirement activity is unconditional even though uncertainty exists about the timing and (or) method of settlement. SFAS No. 143 acknowledges that in some cases, sufficient information may not be available to reasonably estimate the fair value of an asset retirement obligation. This Interpretation also clarifies when an entity would have sufficient information to reasonably estimate the fair value of an asset retirement obligation. This Interpretation is effective no later than the end of fiscal years ending after December 15, 2005. We have not completed the study of what effect FIN No. 47 will have on our financial position and results of operations.

The following table sets forth a summary of our results of operations for the fiscal years ended March 31, 2003, 2004 and 2005:

| Fiscal years ended March 31, | ||||||||||||

| 2003 | 2004 | 2005 | ||||||||||

| (in billions) | ||||||||||||

Interest income | ¥ | 1,260.7 | ¥ | 1,120.2 | ¥ | 1,198.4 | ||||||

Interest expense | 435.1 | 338.9 | 389.7 | |||||||||

Net interest income | 825.6 | 781.3 | 808.7 | |||||||||

Provision (credit) for credit losses | 287.3 | (142.4 | ) | 125.1 | ||||||||

Non-interest income | 724.6 | 983.1 | 804.0 | |||||||||

Non-interest expense | 973.3 | 1,035.0 | 960.7 | |||||||||

Income from continuing operations before income tax expense and cumulative effect of a change in accounting principle | 289.6 | 871.8 | 526.9 | |||||||||

Income tax expense | 50.5 | 333.6 | 238.8 | |||||||||

Income from continuing operations before cumulative effect of a change in accounting principle | 239.1 | 538.2 | 288.1 | |||||||||

Income (loss) from discontinued operations—net | 10.4 | (0.6 | ) | — | ||||||||

Cumulative effect of a change in accounting principle, net of tax | (0.5 | ) | — | (1.0 | ) | |||||||

Net income | ¥ | 249.0 | ¥ | 537.6 | ¥ | 287.1 | ||||||

21

Table of Contents

We reported net income of ¥287.1 billion for the fiscal year ended March 31, 2005, compared to net income of ¥537.6 billion for the fiscal year ended March 31, 2004. Our basic earnings per common share (net income available to common shareholders) for the fiscal year ended March 31, 2005 was ¥55.87 compared to an earnings per share of ¥105.10 for the fiscal year ended March 31, 2004. Income from continuing operations before income tax expense and cumulative effect of a change in accounting principle for the fiscal year ended March 31, 2005 was ¥526.9 billion, compared with ¥871.8 billion for the fiscal year ended March 31, 2004. The changes in our operating results were primarily attributable to the following:

| • | Non-interest income decreased ¥179.1 billion from ¥983.1 billion for the fiscal year ended March 31, 2004 to ¥804.0 billion for the fiscal year ended March 31, 2005. This decrease was primarily attributable to a decrease of ¥246.2 billion in net foreign exchange gains, from a gain of ¥247.4 billion for the fiscal year ended March 31, 2004 to a gain of ¥1.2 billion for the fiscal year ended March 31, 2005. This decrease in foreign exchange gains was due to the depreciation of the yen against foreign currencies in the fiscal year ended March 31, 2005, compared to an appreciation of the yen in the fiscal year ended March 31, 2004. All transaction gains or losses on translation of monetary liabilities denominated in foreign currencies are included in current earnings. However, the transaction gains or losses on translation of securities available for sale, such as bonds denominated in foreign currencies, are not included in current earnings but are reflected in other changes in equity from nonowner sources. As we maintain monetary liabilities denominated in foreign currencies for our asset liability management, net foreign exchange gains (losses) fluctuate with the appreciation (depreciation) of the yen. This decrease in foreign exchange gains was partially offset by the increase in fees and commissions of ¥40.7 billion and an increase in net investment securities gains of ¥92.7 billion compared to the fiscal year ended March 31, 2004. |

| • | For the fiscal year ended March 31, 2005, provision for credit losses of ¥125.1 billion was recorded. In contrast, for the fiscal year ended March 31, 2004, a reversal of allowance for credit losses of ¥142.4 billion was recorded. Although the reversals of allowance for credit losses were recorded for both March 31, 2004 and 2005 due to improvements in our loan portfolio as evidenced by the reduction in our nonperforming loans, for the fiscal year ended March 31, 2005, additional provisions were recognized as downgrades of several borrowers to which we extended relatively large amounts of loans were greater than the reversals recognized. |

Net Interest Income

Net interest income is a function of:

| • | the amount of interest-earning assets; |

| • | the general level of interest rates; |

| • | the so-called “spread,” or the difference between the rate of interest earned on interest-earning assets and the rate of interest paid on interest-bearing liabilities; and |

| • | the proportion of interest-earning assets financed by non-interest-bearing liabilities and equity. |

Our net interest income for the fiscal years ended March 31, 2003, 2004 and 2005 were not materially affected by gains or losses resulting from derivative financial instruments used for hedging purposes.

22

Table of Contents

The following is a summary of the interest rate spread for the fiscal years ended March 31, 2003, 2004 and 2005:

| Fiscal years ended March 31, | ||||||||||||||||||

| 2003 | 2004 | 2005 | ||||||||||||||||

| Average balance | Average rate | Average balance | Average rate | Average balance | Average rate | |||||||||||||

| (in billions, except percentages) | ||||||||||||||||||

Interest-earning assets: | ||||||||||||||||||

Domestic | ¥ | 49,643.3 | 1.21 | % | ¥ | 54,930.7 | 1.07 | % | ¥ | 63,582.4 | 0.97 | % | ||||||

Foreign | 18,686.8 | 3.53 | 17,660.7 | 3.02 | 18,841.2 | 3.07 | ||||||||||||

Total | ¥ | 68,330.1 | 1.84 | % | ¥ | 72,591.4 | 1.54 | % | ¥ | 82,423.6 | 1.45 | % | ||||||

Financed by: | ||||||||||||||||||

Interest-bearing funds: | ||||||||||||||||||

Domestic | ¥ | 50,100.6 | 0.34 | % | ¥ | 55,267.0 | 0.30 | % | ¥ | 62,838.8 | 0.30 | % | ||||||

Foreign | 12,286.4 | 2.17 | 11,874.3 | 1.45 | 12,933.2 | 1.56 | ||||||||||||

Total | 62,387.0 | 0.70 | 67,141.3 | 0.50 | 75,772.0 | 0.51 | ||||||||||||

Non-interest-bearing funds | 5,943.1 | — | 5,450.1 | — | 6,651.6 | — | ||||||||||||

Total | ¥ | 68,330.1 | 0.63 | % | ¥ | 72,591.4 | 0.46 | % | ¥ | 82,423.6 | 0.47 | % | ||||||

Spread on: | ||||||||||||||||||

Interest-bearing funds | 1.14 | % | 1.04 | % | 0.94 | % | ||||||||||||

Total funds | 1.21 | % | 1.08 | % | 0.98 | % | ||||||||||||

Fiscal Year Ended March 31, 2005 Compared to Fiscal Year Ended March 31, 2004

Net interest income for the fiscal year ended March 31, 2005 was ¥808.7 billion, an increase of ¥27.4 billion, or 3.5%, from ¥781.3 billion for the fiscal year ended March 31, 2004. This increase was due primarily to an increase in the average balance of interest-earning assets.

The average interest rate spread decreased 10 basis points from 1.04% for the fiscal year ended March 31, 2004 to 0.94% for the fiscal year ended March 31, 2005. This decrease was due primarily to the increase in average rate of foreign interest-bearing funds, reflecting the rise in interest rates on foreign deposits as interest rates in foreign markets such as the United States rose, and also due to the decline in average rate of domestic investment securities and domestic loans. The decline in average rate of domestic investment securities was mainly due to the increase in our holdings of Japanese government bonds, as the interest rates on Japanese government bonds are generally lower compared to other domestic investment securities reflecting the low risk. The decline in average rate of domestic loans was mainly due to the reduction of loans with relatively high interest rates and due to increased competition in lending to large corporations and in retail housing loans, which negatively affected the interest rate spread of our loans.

Net interest income as a percentage of average total funds decreased 10 basis points from 1.08% for the fiscal year ended March 31, 2004 to 0.98% for the fiscal year ended March 31, 2005.

Average interest-earning assets for the fiscal year ended March 31, 2005 were ¥82,423.6 billion, an increase of ¥9,832.2 billion, or 13.5%, from ¥72,591.4 billion for the fiscal year ended March 31, 2004. The increase was primarily attributable to an increase of ¥6,290.1 billion in domestic investment securities, which reflected an increase in our holdings of Japanese government bonds, and an increase of ¥2,108.3 billion in domestic loans. The increase in domestic loans was primarily due to an increase in loans to industries such as manufacturing, real estate, wholesale and retail, other industries, reflecting the consolidation of certain VIEs in accordance with FIN No. 46R. An increase of ¥730.5 billion in foreign investment securities, which reflected an increase in our holdings of mortgage-backed securities, also contributed to the increase in interest-earning assets.

Average interest-bearing liabilities for the fiscal year ended March 31, 2005 were ¥75,772.0 billion, an increase of ¥8,630.7 billion, or 12.9%, from ¥67,141.3 billion for the fiscal year ended March 31, 2004. The increase in average interest-bearing liabilities primarily reflected an increase of ¥5,540.6 billion in domestic other short-term borrowings and trading account liabilities, reflecting an increase of funding from the Bank of Japan in connection with our daily money market operations, and an increase in commercial paper issued by VIEs consolidated in accordance with FIN No. 46R.

23

Table of Contents

Fiscal Year Ended March 31, 2004 Compared to Fiscal Year Ended March 31, 2003

Net interest income for the fiscal year ended March 31, 2004 was ¥781.3 billion, a decrease of ¥44.3 billion, or 5.4%, from ¥825.6 billion for the fiscal year ended March 31, 2003. This decrease was due primarily to a decline in the average interest rate spread. In addition, a decrease in average foreign loans, which earn relatively higher yields, contributed to the decrease in net interest income.