Table of Contents

As filed with the Securities and Exchange Commission on January 29, 2024

Commission File No. 333-267180

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FIDELITY & GUARANTY LIFE INSURANCE COMPANY

(Exact Name of registrant as specified in its charter)

| Iowa | 6311 | 52-6033321 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

801 Grand Avenue, Suite 2600, Des Moines IA 50309

(515) 330-3340

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Christopher Blunt

Jodi Ahlman, Esq.

c/o Fidelity & Guaranty Life Insurance Company

801 Grand Avenue, Suite 2600, Des Moines IA 50309

(515) 330-3340

(Name and Address of Agent for Service)

Copy to:

Stephen E. Roth, Esq.

Eversheds Sutherland (US) LLP

700 Sixth Street, NW, Suite 700

Washington, DC 20001

(202) 383-0100

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell this Contract until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell this Contract and it is not soliciting an offer to buy this Contract in any state where the offer or sale is not permitted.

F&G CONFIDENCE BUILDER

Individual Single Premium Deferred Index-Linked Annuity Contract

Issued By:

FIDELITY & GUARANTY LIFE INSURANCE COMPANY

Prospectus Dated: May 1, 2024

This prospectus provides information you should know before you purchase the F&G Confidence Builder Contract (the “Contract”). The prospectus describes the Contract between the Owner (“you”) and Fidelity & Guaranty Life Insurance Company (“F&G,” the “Company,” “us,” “we” or “our”). The Contract is a single premium deferred index-linked annuity contract with a minimum Premium Payment of $25,000 that is designed to help you invest on a tax-deferred basis and meet long-term financial goals. The Company does not allow additional Premium Payments after the initial Premium Payment. Certain words and phrases used and capitalized throughout the prospectus are defined in the section titled “Defined Terms.”

Please read this prospectus before investing and keep it for future reference.

Under the Contract, you may allocate your Premium to the Fixed Interest Strategy, which guarantees principal and a rate of interest for a 1-year crediting period, and one or more of the Index-Linked Interest Strategies that are available under the Contract. The Contract is an insurance product and is not an investment in a mutual fund or exchange-traded fund (“ETF”) that tracks an index. Each Index-Linked Interest Strategy has an applicable Crediting Method and is tied to a market index that is a price return index and the performance of the Index does not reflect any dividends or distributions paid by the component companies included in the Index. At the end of a defined time period (a “Crediting Period”), we will credit to your Contract an amount of interest (which may be positive, negative, or equal to zero) based on the Index performance and Crediting Method of the Indexed-Linked Strategy in which you invested. Each Crediting Method includes a “Buffer,” which provides limited protection against a negative Index Change for a Crediting Period, and either has a “Cap Rate,” which is the maximum percentage change that can be credited under an Index-Linked Interest Strategy for a Crediting Period, a “Performance Trigger Rate,” which is the percentage that will be credited if the Index Change is positive or equal to zero for a Crediting Period, or a “Participation Rate,” which is a percentage by which any positive Index Change is multiplied to determine the Adjusted Index Change for a Crediting Period. The Cap Rate, the Performance Trigger Rate or the Participation Rate may limit the amount that will be credited to your Contract, and you may earn less than the Index return during the Crediting Period. When you invest in an Indexed-Linked Interest Strategy, if there is negative Index performance for the Crediting Period, you risk any losses that exceed the amount of the Buffer. In the case of Index-Linked Interest Strategies with a Buffer of 10%, on the Crediting Date you could lose up to 90% of your investment, and up 80% of your investment in the case of Index-Linked Interest Strategies with a Buffer of 20%. If you select an Index-Linked Interest Strategy with an Annual Lock Crediting Method, on the Crediting Date, you could lose significantly more than 90% of your investment in the case of an Index-Linked Interest Strategy with a Buffer of 10% or more than 80% of your investment in the case of an Index-Linked Interest Strategy with a Buffer of 20%. We may change Cap Rates, Performance Trigger Rates and Participation Rates for each Crediting Period, subject to the Guaranteed Minimum Cap Rate, Guaranteed Minimum Performance Trigger Rate and Guaranteed Minimum Participation Rate, respectively. We currently offer Index-Linked Interest Strategies with Buffers of 10% and 20%, but in the future may only offer Index-Linked Interest Strategies with Buffers as low as 10%. The Crediting Methods are described in more detail in the section titled “Crediting Methods.”

We reserve the right to stop offering all but one Index-Linked Interest Strategy (the S&P 500® Index with a 1-Year Crediting Period, (Buffer of 10% and a Cap Rate). At that time, you may choose to surrender your Contract, but you may be subject to surrender charges, asset adjustment charges, taxes, and tax penalties, and if you purchase another retirement vehicle, it may have different features, fees, and risks than this Contract.

Any interest credited to your Contract, as well as our obligations under the Contract, either as a result of investing in an Index-Linked Interest Strategy or the Fixed Interest Strategy, are subject to our creditworthiness and claims-paying ability.

You should not buy this Contract if you are not willing to assume its investment risks. See “Risk Factors” beginning on Page 14. The Contracts are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation, Federal Reserve Board, or any other government agency. You may lose money, including your entire principal investment and previously credited interest. Charges and adjustments under the Contract could cause your losses to be greater than the downside protection of the Index-Linked Interest Strategies. Your losses may be significant.

Withdrawals (including systematic withdrawals) and surrenders may be subject to a surrender charge during the first six years that you own your contract of up to 7% of the amount of the withdrawals. Before the end of a Crediting Period for an Index-Linked Interest Strategy, if you take a surrender or any withdrawal (including systematic withdrawals and required minimum distributions), or if you annuitize, or if the death benefit is paid, the transaction will be based on the Strategy Interim Value of your investment in that Index-Linked Interest Strategy, which is calculated by using a formula that takes into account the value of a specific set of hypothetical derivatives and changes in interest rates that impact the value of the fixed income assets supporting your Contract. Also, if you take a withdrawal or surrender from your Contract at the end of a Crediting Period during the first six Contract Years, your withdrawal or surrender will be subject to an adjustment for changes in interest rates that impact the value of the fixed income assets supporting your Contract (an “Asset Adjustment”). A withdrawal during a Crediting Period, or, during the first six Contract Years, on the Crediting Date will reduce your Account Value on a proportionate, rather than a dollar-for-dollar, basis.

Strategy Interim Values and Asset Adjustments fluctuate daily, positively or negatively, and can reflect significantly less gain or more loss than would be applied at the end of a Crediting Period. You could lose up to your entire principal investment in the Index-Linked Interest Strategies and previously credited interest. For as long as you have multiple ongoing Crediting Periods for Index-Linked Interest Strategies, there may be no time that any such transaction listed above can be performed without the application of at least one Strategy Interim Value and/or Asset Adjustment.

This Contract is not appropriate for investors who plan to take withdrawals or surrender the Contract during the first six Contract Years due to the imposition of surrender charges, Strategy Interim Values and Asset Adjustments. In addition, both the application of the Strategy Interim Value to partial withdrawals during the Crediting Period and the Asset Adjustment to partial withdrawals at the end of a Crediting Period and the proportional reduction in your Strategy Base Value, together with any surrender charges, could reduce the value of the Contract to less than the protection provided by the Buffers applicable to your Index-Linked Interest Strategies, perhaps significantly. In addition, an Index-Linked Strategy with an Annual Lock Crediting Method is not appropriate for investors who intend or need to take withdrawals during the Crediting Period, which is 6 years.

The Contract does not provide tax deferral benefits, beyond those already provided under the Internal Revenue Code, for a Contract purchased as a Qualified Contract, such as an Individual Retirement Annuity (“IRA”). Amounts withdrawn from the Contract prior to age 59 1/2 may also be subject to taxes and a 10% federal penalty. Investors should consult with their tax advisor for more information.

You may cancel the Contract without charge within 30 days after you receive it. If you cancel your Contract during this period, we will issue a refund including all charges that may have been deducted from your Contract and you will not be subject to a surrender charge. Your state’s law will determine the amount you will receive.

Fidelity & Guaranty Securities, LLC (“F&G Securities) is the principal underwriter of the Contracts. This prospectus does not constitute an offering in any jurisdiction in which the Contract may not be lawfully sold.

Index-linked annuity contracts are complex insurance and investment vehicles. Investors should speak with a financial professional about the Contract’s features, benefits, risks, and fees, and whether the Contract is appropriate for the investor based upon his or her financial situation and objectives.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Table of Contents

| Page | ||||

| 1 | ||||

| 5 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

Cap Rate, Performance Trigger Rate and Participation Rate Risk | 19 | |||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| Risk that We May Eliminate an Index-Linked Interest Strategy | 22 | |||

| 22 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 24 | ||||

| 24 | ||||

| 24 | ||||

| 25 | ||||

| 25 | ||||

| 26 | ||||

| 26 | ||||

| 26 | ||||

| 26 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

ADDITIONAL INFORMATION ABOUT THE INDEX-LINKED INTEREST STRATEGIES | 30 | |||

| 30 | ||||

| 32 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 42 | ||||

| 43 | ||||

| 43 | ||||

Automatic Transfer from an Index-Linked Interest Strategy to the Fixed Interest Strategy | 43 | |||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 45 | ||||

Table of Contents

TABLE OF CONTENTS | Page | |||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| 49 | ||||

| 49 | ||||

| 50 | ||||

| 51 | ||||

| 51 | ||||

| 51 | ||||

| 53 | ||||

| 53 | ||||

| 54 | ||||

| 54 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 63 | ||||

| 63 | ||||

| 63 | ||||

| 63 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 65 | ||||

| 65 | ||||

| 65 | ||||

| 66 | ||||

| 66 | ||||

| 66 | ||||

| 67 | ||||

| 67 | ||||

| 68 | ||||

| 68 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 72 | ||||

Security Ownership of Certain Beneficial Owners and Management | 72 | |||

Transactions with Related Persons, Promoters and Certain Control Persons | 72 | |||

| 74 | ||||

| 82 | ||||

| 98 | ||||

| 100 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 101 | |||

| 131 | ||||

Table of Contents

Table of Contents

We have used simple, clear language as much as possible in this prospectus. However, by the very nature of the Contracts certain technical words or terms are unavoidable. We have identified the following as some of these words or terms.

| Account Value | The total amount attributable to your Contract during the Accumulation Phase at any given time. Your Account Value is the sum of your Strategy Account Values and your Fixed Interest Strategy Value at any given time. Your Account Value may not necessarily equal your Cash Surrender Value. | |

| Accumulation Phase | The period beginning on the Effective Date and ending on the Maturity Date. | |

| Adjusted Index Change | The net change percentage in the Index Value of an Index from the start of a Crediting Period to the end of the Crediting Period, after any applicable adjustment for the Crediting Method applicable to an Index-Linked Interest Strategy. The Adjusted Index Change for an Index-Linked Interest Strategy represents the rate at which we credit interest at the end of a Crediting Period. The Adjusted Index Change may be positive, negative, or equal to zero. | |

| Annuitant | The natural person(s) on whose life (or lives) annuity payments under the Contract are based. | |

| Asset Adjustment | An adjustment to your Strategy Base Value used to determine the Strategy Interim Value based on the Bloomberg US Aggregate Yield to Worst Index to account for changes in interest rates that impact the value of the fixed income assets supporting your Contract since the Contract’s Effective Date. On a Crediting Date prior to the sixth Contract Anniversary, your Strategy Account Value also includes the Asset Adjustment. | |

| Beneficiary | The person or entity designated by the Owner to receive any Contract benefits upon the Owner’s death during the Accumulation Phase. | |

| Business Day | Any day that the New York Stock Exchange (“NYSE”) is open for regular trading. A Business Day ends at the same time that regular trading on the NYSE closes (typically, 4:00 PM Eastern Time). | |

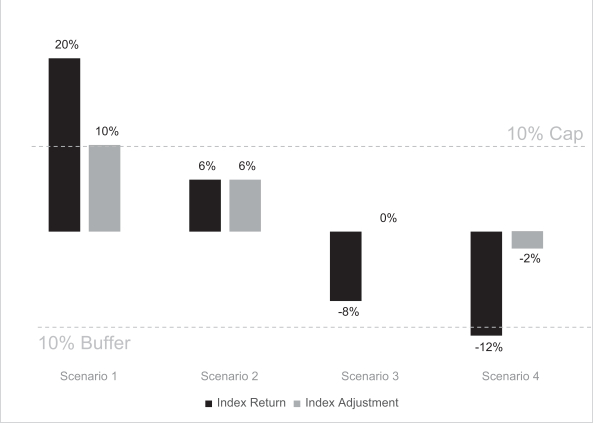

| Buffer | A Buffer protects against a negative Index Change until the protection level has been exceeded. The Buffer represents the maximum negative Index Change that will not result in a negative Adjusted Index Change for a given Crediting Period. If the Index Change for the Crediting Period is negative, and the negative Index Change is within the Buffer, then the Index-Linked Interest credited to the Strategy Account Value is zero. If the negative Index Change exceeds the Buffer, then negative Index-Linked Interest is credited to the extent that the Index Change extends beyond the Buffer. The Buffer provides limited protection against negative Index-Linked Interest being credited to your Contract for a Crediting Period. For example, if the Buffer is 20% and the Index Change for the Crediting Period is negative 35%, negative Index-Linked Interest of 15% would be credited to the Index-Linked Interest Strategy. | |

| Cap Rate | An element of certain Crediting Methods. The Cap Rate represents the maximum Adjusted Index Change that can be credited under an Index-Linked Interest Strategy for a Crediting Period. It limits the potential positive Index-Linked Interest that may be credited for a Crediting Period. Each Index-Linked Interest Strategy that is subject to a Cap Rate has its own Cap Rate. | |

| Cash Surrender Value | The amount that you will receive if you surrender your Contract (i.e., take a full withdrawal) during the Accumulation Phase. The Cash Surrender Value equals your Account Value minus any surrender charge. | |

1

Table of Contents

| Code | Internal Revenue Code of 1986, as amended. | |

| Commuted Value | The commuted value of remaining guaranteed annuity payments is determined by discounting the remaining guaranteed annuity payments at an annually compounded interest rate which is one percent more than the rate we use to determine those payments. The commuted value will always be less than the sum of the remaining guaranteed annuity payments. The commuted value is calculated as of the date a lump sum payment will be made. | |

| Contract | The F&G Confidence Builder Contract, which is a single premium deferred index-linked annuity contract between F&G and you, as the Owner. | |

| Contract Anniversary | The annual anniversary of the Effective Date of your Contract. | |

| Contract Year | The 12-month period starting on the Effective Date and each anniversary of your Effective Date while the Contract remains in force. | |

| Crediting Date | The last day of a Crediting Period. | |

| Crediting Method | The Cap Rate, Performance Trigger Rate or Participation Rate, the Buffer and the calculating methodology (Point to Point or Annual Lock) that determines the applicable Index-Linked Interest credited for a Strategy at the end of a Crediting Period. | |

| Crediting Period | The investment period over which performance of an Index is measured to determine the amount of Index-Linked Interest credited for an Index-Linked Interest Strategy, or, for the Fixed Interest Strategy, the one-year period over which interest is credited at a specified declared rate. A Crediting Period is designated for each Index-Linked Interest Strategy and may be one, three, or six years. You may only reallocate your Strategy Account Value or Fixed Interest Strategy Value among the Fixed Interest Strategy and/or one or more Index-Linked Interest Strategies at the end of a Crediting Period. You may not reallocate your Strategy Account Value or Fixed Interest Strategy Value until the end of a Crediting Period. | |

| Effective Date | The date when the Contract is issued and the Premium is allocated to the Fixed Interest Strategy and/or one or more of the Index-Linked Interest Strategies for the initial Crediting Period. | |

| Equity Adjustment | An adjustment to your Strategy Base Value used to determine the Strategy Interim Value based on the value of a specific set of hypothetical derivatives. | |

| F&G (or the “Company,” “we,” “us,” or “our”) | Fidelity & Guaranty Life Insurance Company. | |

| Fixed Interest Strategy | The investment option under the Contract that provides for guaranteed interest, and is subject to a guaranteed minimum interest rate. The Fixed Interest Strategy is part of the Separate Account. | |

| Fixed Interest Strategy Value | The amount of your Account Value allocated to the Fixed Interest Strategy at any given time. | |

| General Account | The account that holds all of F&G’s assets, including all assets held in the Separate Account. | |

| Guaranteed Minimum Cap Rate | The Guaranteed Minimum Cap Rate is 2% for a point to point Index-Linked Interest Strategy with a one-year Crediting Period; 6% for a point to point Index-Linked Interest Strategy with a three-year Crediting Period; 3% for a point to point Index-Linked Interest Strategy with a six-year Crediting Period where the Index is Hindsight 20/20; 12% for a point to point Index-Linked Interest Strategy with a six-year Crediting Period with any other Index; and 2% for each year of an Annual Lock Index-Linked Interest Strategy with a six-year Crediting Period. | |

2

Table of Contents

| Guaranteed Minimum Participation Rate | The Guaranteed Minimum Participation Rate is [XX%] for a point to point Index-Linked Interest Strategy with a six-year Crediting Period. | |

| Guaranteed Minimum Performance Trigger Rate | The Guaranteed Minimum Performance Trigger Rate is 0.50% for a point to point Index-Linked Interest Strategy with a one-year Crediting Period. | |

| Income Phase | The period beginning on the Maturity Date during which we make annuity payments to the Payee(s). | |

| Income Phase Death Benefit Recipient | The person entitled during the Income Phase to any payments to be made under an annuity option after the death of the Annuitant(s). The Income Phase Death Benefit Recipient is the first person(s) living on the date of such death in the following order: (i) Owner(s) or a surviving joint Owner; (ii) the Beneficiary(ies); or (iii) the estate of the last owner to die. | |

| Index | The market index used to determine the Index Change for a Strategy. Each Index is comprised of or defined by certain securities or by a combination of certain securities and other instruments. | |

| Index Change | The net change percentage in the Index Value of an Index from the start of a Crediting Period to the end of the Crediting Period, before any applicable adjustment for the Crediting Method applicable to an Index-Linked Interest Strategy. If the start or end of a Crediting Period is not on a Business Day, we will use the Index Value on the next Business Day to calculate the Index Change. | |

| Index Value | The closing value of an Index on any Business Day. If an Index Value is not published for a Business Day, we will use the closing Index Value from the next Business Day. | |

| Index-Linked Interest Strategy | An investment option under the Contract that provides for credited interest (either positive, negative, or equal to zero) based on the performance of a particular Index and the applicable Crediting Method. | |

| Index-Linked Interest | The dollar amount of interest credited under an Index-Linked Interest Strategy at the end of a Crediting Period. Index-Linked Interest can be positive, negative or equal to zero. | |

| IRS | The Internal Revenue Service. | |

| Maturity Date | The date the Income Phase begins. The Maturity Date is the Contract Anniversary on or first following the Annuitant’s (or oldest Annuitant’s if a Joint Annuitant is named) 100th birthday. You may change the Maturity Date to an earlier date following the first Contract Anniversary. | |

| Owner | The person(s) or legal entity entitled to exercise all rights and privileges under the Contract. Any reference to Owner in this prospectus includes any joint Owner. References to “you” in this prospectus refer to the Owner or a prospective Owner. In the case of a Qualified Contract, the Owner must be a natural person and joint Owners are not allowed. | |

| Participation Rate | An element of certain Crediting Methods. The Participation Rate, which can be more than, less than or equal to 100%, is a percentage specific to certain Index-Linked Interest Strategies by which the positive Index Change is multiplied to determine the Adjusted Index Change for a Crediting Period. Each Index-Linked Interest Strategy that is subject to a Participation Rate has its own Participation Rate. | |

| Payee | The person(s) or entity (or entities) designated by you to receive annuity payments during the Income Phase. You are the Payee unless you designate another person or entity as the Payee. | |

3

Table of Contents

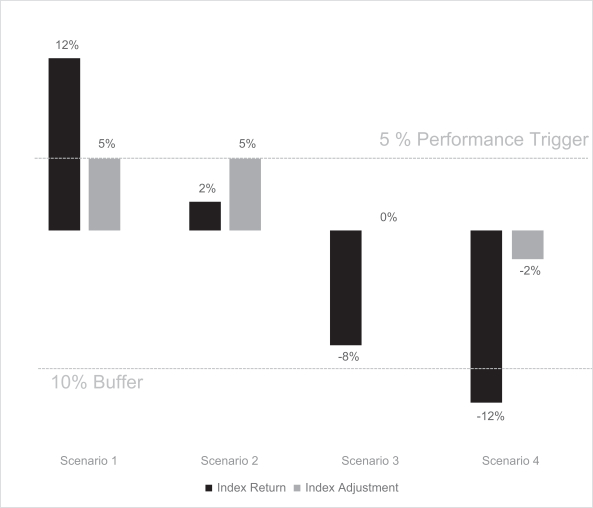

| Performance Trigger Rate | The Performance Trigger Rate is the percentage that will be credited if the Index Change is positive or equal to zero for a Crediting Period. For an Index-Linked Interest Strategy with a Performance Trigger Rate, if the Index Change is equal to zero or greater for a Crediting Period, the Adjusted Index Change will be equal to the Performance Trigger Rate for that Crediting Period. The Performance Trigger Rate limits the potential positive Index-Linked Interest that will be credited for a Crediting Period if the Index Change exceeds the Performance Trigger Rate. Each Index-Linked Interest Strategy that is subject to a Performance Trigger Rate has its own Performance Trigger Rate. | |

| Premium | The single premium paid to us under the Contract, less any applicable taxes due at the time the payment is made. | |

| Qualified/Non-Qualified Contract | A Qualified Contract is purchased as part of an individual retirement plan or an employer-sponsored plan. Currently, we offer two types of Qualified Contracts: (1) a traditional IRA, and (2) a Roth IRA. The Contract is not available for purchase by qualified retirement plans, as a “section 403(b) contract,” or in the form of a Simplified Employee Pension or SIMPLE Retirement Account. A Non-Qualified Contract is a Contract that is not a Qualified Contract. | |

| Rollover Contribution | A transfer of “eligible” funds between a qualified retirement plan and a traditional or Roth IRA that takes one of these forms: (1) direct transfer— funds are paid directly from one qualified retirement plan or IRA to another; (2) trustee-to-trustee transfer—funds held in a traditional IRA are transferred directly to another traditional IRA or funds held in a Roth IRA are transferred directly to another Roth IRA; or (3) a 60-Day Rollover—funds held in a qualified retirement plan or IRA are distributed directly to you and within 60 days you deposit all or a portion of them in an IRA or qualified retirement plan. You should consult with your tax advisor about the applicable requirements for making a rollover contribution and about what funds are “eligible” for such a transfer. | |

| Separate Account | F&G’s Separate Account ILA-1. We hold certain investments supporting the assets allocated to the Index-Linked Interest Strategies and the Fixed Interest Strategy in F&G Separate Account ILA-1, which we established under the laws of Iowa. Separate Account ILA-1 is a non-insulated separate account. Assets in Separate Account ILA-1 are part of F&G’s General Account and are chargeable with the claims of any of our contract owners as well as our creditors and are subject to the liabilities arising from any of our other business. Separate Account ILA-1 is not registered under the Investment Company Act of 1940, as amended. | |

| Strategy Account Value | During a Crediting Period, you have a Strategy Account Value for each Index-Linked Interest Strategy in which you invest. On the Effective Date, your Strategy Account Value equals the Premium you allocate the Index-Linked Interest Strategy. On each Business Day other than the Effective Date or a Crediting Date during the first six Contract Years, your Strategy Account Value equals your Strategy Interim Value. On a Crediting Date during the first six Contract Years, your Strategy Account Value includes the Asset Adjustment. Your Strategy Account Value is the amount available for withdrawals, surrenders, annuitization and death benefits. | |

| Strategy Base Value | For each Index-Linked Interest Strategy in which you invest, your Strategy Base Value is an amount used to calculate (i) your Strategy Account Value on the first Business Day of the Crediting Period; (ii) your Strategy Interim Value on each other Business Day; and (iii) your Index-Linked Interest credited on the last Business Day of the Crediting Period. Your Strategy Base Value is not a cash value under the Contract. Your Strategy Base Value will be adjusted for any withdrawals you make during the Crediting Period. | |

| Strategy Interim Value | For each Index-Linked Interest Strategy in which you invest, your Strategy Account Value equals your Strategy Interim Value on any Business Day except for the Effective Date and a Crediting Date. The Strategy Interim Value is calculated by using a formula that takes into account the Equity Adjustment and the Asset Adjustment to your Strategy Base Value. | |

| Surrender Charge Period | The first six Contract Years. | |

4

Table of Contents

This summary provides a brief overview of the F&G Confidence Builder Contract. You should carefully read the entire prospectus before you decide whether to purchase the Contract. The Contract may not be currently available in all states, may vary in your state, or may not be available from all selling firms or from all financial professionals.

Who is F&G? The Contract would be an agreement between you, the Owner, and Fidelity & Guaranty Life Insurance Company. F&G is an Iowa stock life insurance company and a wholly-owned subsidiary of Fidelity and Guaranty Life Holdings, Inc., a Delaware corporation that is an indirect, wholly owned subsidiary of F&G Annuities & Life, Inc., a Delaware corporation (“FGAL”), which is listed on the New York Stock Exchange. FGAL is a direct, majority owned subsidiary of Fidelity National Financial, Inc. (“FNF”), a New York Stock Exchange listed company with its headquarters in Jacksonville, Florida. We offer annuities, life insurance products, pension risk transfer solutions and funding agreements and are licensed to do business in the District of Columbia, Puerto Rico and all states except New York. The Contract is not available in Puerto Rico or any state in which we are licensed that has not approved the Contract for issuance.

What is the purpose of the Contract? The Contract is designed to help you invest on a tax-deferred basis and meet your long-term financial goals, such as funding your retirement. During the Accumulation Phase, you can access your funds by taking withdrawals of your Account Value (which may be subject to a surrender charge of up to 7% and other adjustments based on Strategy Interim Values and Asset Adjustments). During the Income Phase, we pay guaranteed income in the form of annuity payments. The Contract also will pay a death benefit to your Beneficiaries in the event of death of the Owner or the Annuitant during the Accumulation Phase. All payments under the Contract are subject to the terms and conditions described in this prospectus. You should not buy the Contract as a short-term investment, if you plan on taking withdrawals before the end of the Surrender Charge Period (which is the first six Contract Years), or if you anticipate taking significant withdrawals from your Strategy Account Values. You should understand that while the Contract provides some protection against loss, you can lose money under the Contract. It is possible to lose your entire principal investment and previously credited Index-Linked Interest You should not buy the Contract if you are not willing to assume the risks associated with the Contract. See the section titled “Risk Factors.”

Are the Contracts Non-Qualified Contracts or Qualified Contracts? The Contract is available in both forms. A Non-Qualified Contract will provide you with certain tax deferral features under the Code. If you purchase a Qualified Contract, the Contract will not provide you tax deferral benefits in addition to those already provided by your IRA or Roth IRA, and you should only buy the Contract for its other features.

How do I purchase the Contract? You may purchase the Contract by completing an application and submitting Premium of at least $25,000. We reserve the right to reject any Premium payment that exceeds $1.5 million. You may only make one Premium payment under the Contract.

What are the investment options during the Accumulation Phase? The Contract currently offers 29 Index-Linked Interest Strategies and the Fixed Interest Strategy. The Contract is an insurance product and is not an investment in a mutual fund or ETF that tracks an index. For each Crediting Period, which is one, three or six years for the Index-Linked Interest Strategies, you may allocate Account Value to one or more Index-Linked Interest Strategies and/or you may allocate Account Value for one year Crediting Periods to the Fixed Interest Strategy. Each Index-Linked Interest Strategy credits Index-Linked Interest (either positive, negative, or equal to zero) at the end of a Crediting Period based on the performance of a particular Index and the applicable Crediting Method. The Fixed Interest Strategy credits interest during each Crediting Period based on a guaranteed rate set by us. The guaranteed minimum interest rate (for the Fixed Interest Strategy) will never be less than 0.15%.

5

Table of Contents

What are the Indexes for the Index-Linked Interest Strategies? Currently, the Contract offers Index-Linked Interest Strategies that credit interest based on the performance of the following Indexes:

| • | S&P 500® Index; |

| • | Russell 2000® Index; |

| • | NASDAQ-100® Index; |

| • | MSCI EAFE Index; or |

| • | Hindsight 20/20, which is based on the best performance during a Crediting Period of the BofA MP Growth Index, the BofA MP Balanced Index or the BofA Defensive Index. |

Each Index is a price return index and the performance of the Index does not reflect any dividends or distributions paid by the component companies included in the Index. Each Index is described in more detail under the section titled “Indexes.”

We reserve the right to add, remove or replace any Index in the future, subject to necessary regulatory approvals. We may remove or replace an Index if it is discontinued, if there is a substantial change in the calculation of the Index, if the fees to use an Index substantially increase, or if hedging instruments become difficult to acquire or the cost of hedging becomes excessive. If we replace an Index during a Crediting Period, we will calculate the Index Change using the old Index as of the replacement date. After the replacement date, we will calculate the Index Change using the new index, but with a modified starting Crediting Period value for the new index. The modified starting Crediting Period value for the new index will reflect the Index Change for the old Index from the start of the Crediting Period to the replacement date. For an example of how the Index Change is calculated under these circumstances, see the section titled “Indexes.” If we replace an Index during a Crediting Period, this does not cause a change in the Cap Rate, Performance Trigger Rate, Participation Rate or Buffer.

If we add or remove an Index (as opposed to replacing an index as described in the previous paragraph), the changes will not be effective for your Contract until the start of the next Crediting Period. Adding, removing or replacing an Index does not cause a change in the Buffer. The Buffer will not change while we continue to offer that Index-Linked Interest Strategy. Any Index-Linked Interest Strategies based on the performance of a newly added Index will have a new Cap Rate, Performance Trigger Rate or Participation Rate, provided that a Cap Rate will never be lower than the Guaranteed Minimum Cap Rate, a Performance Trigger Rate will never be lower than the Guaranteed Minimum Performance Trigger Rate, a Participation Rate will never be lower than the Guaranteed Minimum Participation Rate and the Buffer will never be lower than 10%. Changes to the Cap Rates, Performance Trigger Rates or Participation Rates, if any, occur at the start of the next Crediting Period. See the sections titled “Index Risk,” “Risk that We May Eliminate or Substitute an Index,” “Risk that We May Eliminate an Index-Linked Interest Strategy”, and “Additional Information about the Index-Linked Interest Strategies” for more information.

6

Table of Contents

What Index-Linked Interest Strategies are offered in the Contract? Currently, the Contract offers Index-Linked Interest Strategies with the following Crediting Methods:

| 1 Year Crediting Period | ||||||||||||

| Crediting Method | Buffer | S&P 500® Index | Russell 2000® Index | Nasdaq- 100® Index | MSCI EAFE Index | Hindsight 20/20 | ||||||

Point to Point Cap | 10% Buffer | ✓ | ✓ | ✓ | ✓ | N/A | ||||||

| 20% Buffer | ✓ | ✓ | N/A | ✓ | N/A | |||||||

Point to Point Performance Trigger | 10% Buffer | ✓ | ✓ | ✓ | ✓ | N/A | ||||||

| 3 Year Crediting Period | ||||||||||||

Point to Point Cap | 10% Buffer | ✓ | ✓ | N/A | ✓ | N/A | ||||||

| 20% Buffer | ✓ | ✓ | N/A | ✓ | N/A | |||||||

| 6 Year Crediting Period | ||||||||||||

Point to Point Cap | 10% Buffer | ✓ | ✓ | N/A | ✓ | ✓ | ||||||

| 20% Buffer | ✓ | ✓ | N/A | ✓ | N/A | |||||||

Point to Point Participation Rate* | 10% Buffer | ✓ | N/A | N/A | N/A | ✓ | ||||||

Annual Lock Cap | 10% Buffer | ✓ | ✓ | N/A | ✓ | N/A | ||||||

| * | The Index-Linked Investment Strategies with a Point to Point Participation Rate Crediting Method will be available for Crediting Periods beginning on or about June 1, 2024. |

Not all Crediting Methods and/or Crediting Periods are available with all Indexes. We expect to add and remove Index-Linked Interest Strategies from time to time. We reserve the right to stop offering all but one of 29 Index-Linked Interest Strategies offered under this Contract. If we stop offering these strategies, you will be limited to investing in one Index-Linked Interest Strategy (the S&P 500® Index with a 1-Year Crediting Period, (Buffer Rate of 10% and a Cap). At that time, you may choose to surrender your Contract, but you may be subject to surrender charges, asset adjustment charges, taxes, and tax penalties, and if you purchase another retirement vehicle, it may have different features, fees, and risks than this Contract. For additional information, see “Indexed-Linked Interest Strategies.”

How do the Crediting Methods for the Index-Linked Interest Strategies work? The Crediting Methods are used to calculate Index-Linked Interest for the Index-Linked Interest Strategies at the end of each Crediting Period. The Index-Linked Interest may be positive, negative, or equal to zero. Each Index-Linked Interest Strategy uses either a “Point to Point” or “Annual Lock” Crediting Method.

Point to Point Crediting Method

A Point to Point Crediting Method compares the Index Value at the beginning of the first day of the Crediting Period with the Index Value on the Crediting Date to calculate the Index Change and then takes into account the following elements to calculate the Adjusted Index Change:

| • | Either the Cap Rate, the Performance Trigger Rate or the Participation Rate; and |

| • | The Buffer. |

7

Table of Contents

To calculate the Adjusted Index Change for an Index-Linked Interest Strategy with a Point to Point Crediting Method, we use a three step process at the end of the Crediting Period:

| • | First, we calculate the Index Change. The Index Change for an Index-Linked Interest Strategy is the net change percentage in the Index Value from the beginning of the first day of a Crediting Period to the Crediting Date. |

| • | Second, if the Index Change is positive or zero, we determine whether it must be adjusted for the Cap Rate, the Performance Trigger Rate or the Participation Rate. |

If the Crediting Method for the Index-Linked Interest Strategy includes a Cap Rate, the Cap Rate is the maximum positive Adjusted Index Change for a given Crediting Period. The Cap Rate may vary for different Index-Linked Interest Strategies, and we set the Cap Rates prior to the beginning of a Crediting Period. A Cap Rate for a particular Crediting Period may be higher or lower than the Cap Rates for previous or future Crediting Periods. In no event will we set a Cap Rate for any Index-Linked Interest Strategy at less than the Guaranteed Minimum Cap Rate.

If the Crediting Method for the Index-Linked Interest Strategy includes a Performance Trigger Rate, if the Index Change is at least zero, the Adjusted Index Change is the Performance Trigger Rate is for a given Crediting Period. The Performance Trigger Rate may vary for different Index-Linked Interest Strategies, and we set the Performance Trigger Rates prior to the beginning of a Crediting Period. A Performance Trigger Rate for a particular Crediting Period may be higher or lower than the Performance Trigger Rates for previous or future Crediting Periods. In no event will we set a Performance Trigger Rate for any Index-Linked Interest Strategy at less than the Guaranteed Minimum Performance Trigger Rate.

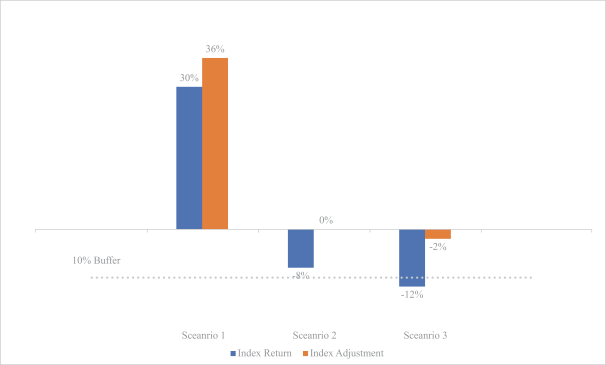

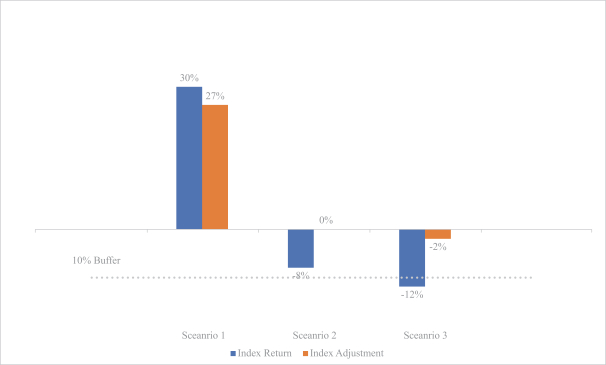

If the Crediting Method for the Index-Linked Interest Strategy includes a Participation Rate, the Index Change is multiplied by the Participation Rate to calculate the Adjusted Index Change for a given Crediting Period. The Participation Rate may vary for different Index-Linked Interest Strategies, and we set the Participation Rates prior to the beginning of a Crediting Period. A Participation Rate for a particular Crediting Period may be higher or lower than the Participation Rates for previous or future Crediting Periods. In no event will we set a Participation Rate for any Index-Linked Interest Strategy at less than the Guaranteed Minimum Participation Rate.

The Cap Rate, the Performance Trigger Rate or the Participation Rate may limit the amount that will be credited to your Contract, and you may earn less than the Index return during the Crediting Period.

| • | Third, if the Index Change is negative, we determine whether the Index Change must be adjusted for the Buffer that applies to the Crediting Method being used. |

The Buffer is the maximum negative Index Change that will not result in a negative Adjusted Index Change for a given Crediting Period. The Buffer for an Index-Linked Interest Strategy may provide protection from a negative Index Change of up to 10% or up to 20%. The Buffer for any Index-Linked Interest Strategy will not change while we continue to offer that Index-Linked Interest Strategy.

Once the Adjusted Index Change is determined, the Adjusted Index Change is applied to the Strategy Base Value to calculate the Index-Linked Interest credited for the Crediting Period. See the section titled “Crediting Methods” for additional information.

Annual Lock Crediting Method

The Annual Lock Crediting Method is a multi-year Index-Linked Interest Strategy that applies the Buffer and Cap separately for each Contract Year during the Crediting Period. If the Crediting Method for an Index-Linked Interest Strategy has an Annual Lock, the Adjusted Index Change will be calculated in the same manner as for a Point to

8

Table of Contents

Point Index-Linked Interest Strategy, except it will be calculated on each Contract Anniversary. However, no Index-Linked Interest will be credited to the Index-Linked Interest Strategy until the Crediting Date at the end of the Crediting Period. If you take a withdrawal from an Index-Linked Interest Strategy with an Annual Lock Crediting Method prior to the end of the Crediting Period, your withdrawal will be based on the Strategy Interim Value on the date of the withdrawal, and not the gains or losses locked in for the completed Contract Years during the Crediting Period. An Index-Linked Interest Strategy with an Annual Lock Crediting Method is not appropriate for investors who intend or need to take withdrawals during the Crediting Period.

The Adjusted Index Change for the full Crediting Period will equal the cumulative result of each successive Adjusted Index Change for each Contract Year during the Crediting Period. On the first Contract Anniversary during the Crediting Period, the performance equals the Adjusted Index Change for that Contract Year multiplied by Strategy Base Value for the Index-Linked Interest Strategy. This performance amount is added to or deducted from the Strategy Base Value to form the Annual Lock Amount. The Annual Lock Amount is used to calculate the performance for the next Contract Year during the Crediting Period. On each Contract Anniversary during the Crediting Period thereafter, the return for the year is equal to the Adjusted Index Change for that Contract Year multiplied by Annual Lock Amount. This amount is credited to or deducted from the Annual Lock Amount, which becomes the new Annual Lock Amount for the next Contract Year. On the Crediting Date, Interest-Linked Interest is credited to the Strategy Base Value in the amount of the difference between the Annual Lock Amount for the Contract Anniversary that is the Crediting Date and the Strategy Base Value. Because of the cumulative impact of the Annual Lock, if you incur a loss in one Contract Year during the Crediting Period, it will reduce the amount on which performance will be calculated for the next Contract year during the Crediting Period. In a continuing down market, you could lose in excess of the percentage remaining after the Buffer. For example, if the Buffer is 10%, in a continuing down market, you could lose more than 90% of your investment. On the other hand, if you incur a gain in one Contract Year during the Crediting Period, it will increase the Annual Lock Amount for the next Contract Year, upon which future gains (if any) will be calculated. See the section titled “Crediting Methods” for additional information.

When does F&G set the Cap Rate, Performance Trigger Rate, Participation Rate and Buffer and can they be adjusted? We set the Cap Rate, Performance Trigger Rate or Participation Rate, as applicable, for each Index-Linked Interest Strategy prior to the beginning of each Crediting Period and those rates will not change during the Crediting Period. The Cap Rates, Performance Trigger Rates and Participation Rates for the initial Crediting Period will be disclosed to you at the time you apply for a Contract and will be no lower for 30 days thereafter. The Cap Rates, Performance Trigger Rates and Participation Rates for the initial Crediting Period will be shown in your Contract. If your Contract is issued after that 30 day period, the Cap Rate, Performance Trigger Rate or Participation Rate for any Index-Linked Interest Strategy to which you have allocated Premium will be based on our then-current rates, which you will not know until the Effective Date of your Contract. If those rates are lower on the Effective Date of your Contract than at the time of your application and you are dissatisfied with those rates, you may cancel your Contract within 30 days and have the amount of your Premium, or your Account Value (based on your Strategy Interim Values), if greater, returned to you without any surrender charges. There may be tax consequences when you cancel your Contract. Please consult with your tax advisor.

We can change the Cap Rates, Performance Trigger Rates and Participation Rates for each Crediting Period, subject to the Guaranteed Minimum Cap Rate, the Guaranteed Minimum Performance Trigger Rate and the Guaranteed Minimum Participation Rate, respectively. At least 30 days prior to the end of a Crediting Period, we will send written notice with instructions for how you can obtain the Cap Rates, Performance Trigger Rates and Participation Rates that we have established by that time for the next Crediting Period. You do not have the right to reject the Cap Rates, Performance Trigger Rates and Participation Rates for the next Crediting Period, but you can select a new allocation from among the Index-Linked Interest Strategies and the Fixed Interest Strategy for the next Crediting Period. See the section titled “Risk that We May Eliminate or Substitute an Index” “Risk that We May Eliminate an Index-Linked Interest Strategy” for more information.

9

Table of Contents

The Buffer for each of the Index-Linked Interest Strategies is shown in your Contract and cannot be changed while we offer that Index-Linked Interest Strategy. If we add an Index-Linked Interest Strategy available under your Contract, the Buffer is guaranteed to be at least 10%. We currently offer Index-Linked Interest Strategies with Buffers of 10% and 20%, but in the future may only offer Index-Linked Interest Strategies with Buffers as low as 10%.

How is my Account Value calculated while I own the Contract? Your Account Value is the sum of your Strategy Account Values and your Fixed Interest Strategy Value at any given time.

How are my Strategy Account Values calculated while I own the Contract? You will have a separate Strategy Account Value for each Index-Linked Interest Strategy in which you invest. On the Effective Date, your Strategy Account Value equals the Premium you have allocated to the Index-Linked Interest Strategy, which is your Strategy Base Value at the inception of your Contract. On the last Business Day of the Crediting Period, your Strategy Base Value is recalculated to equal your Strategy Base Value (including any adjustments due to withdrawals) plus the amount of Index-Linked Interest applied for the Crediting Period, which may be positive, negative or equal to zero.

On each Business Day other than the Effective Date or a Crediting Date, your Strategy Account Value equals your Strategy Interim Value. Your Strategy Interim Value on a given Business Day is intended to reflect the value of your investment in an Index-Linked Interest Strategy on that particular day. Changes to your Strategy Interim Value are not directly tied to the performance of the relevant Index (although Index performance impacts your Strategy Interim Value). Instead, your Strategy Interim Value for an Index-Linked Interest Strategy is calculated on any day other than a Crediting Date using a formula that takes into account (i) an Equity Adjustment to your Strategy Base Value based on the value of a specific set of hypothetical derivatives; and (ii) an Asset Adjustment to your Strategy Base Value based on the Bloomberg US Aggregate Yield to Worst Index to account for changes in interest rates that impact the value of the fixed income assets supporting your Contract.

On a Crediting Date prior to the sixth Contract Anniversary, your Strategy Account Value will include the Asset Adjustment. Accordingly, if you surrender your Contract, take a withdrawal, annuitize or if a death benefit is paid on a Crediting Date prior to the sixth Contract Anniversary, those transactions will be based on the Strategy Account Value including the Asset Adjustment, and your Strategy Base Value for the following Crediting Period will be adjusted proportionally.

For example, if you take a $20,000 withdrawal on a Crediting Date prior to the sixth Contract Anniversary and your Strategy Account Value, inclusive of the Asset Adjustment, is $95,000, you will receive $20,000 (less the amount of any applicable surrender charge of up to 7%) and your Strategy Account Value will be reduced to $75,000. If your Strategy Base Value immediately prior to the withdrawal was $100,000, it will be reduced in proportion to the reduction in the Strategy Account Value. This withdrawal will reduce your Strategy Account Value by $20,000 divided by $95,000, or approximately 21.1%, and your new Strategy Base Value would be $78,947.

Please see Appendix B for a detailed description of how we calculate Strategy Interim Values and the Strategy Account Value when it is subject to the Asset Adjustment on a Crediting Date. It is important to understand that even if an Index performs positively, it is possible that your Strategy Interim Value will decrease. On any day, if you wish to obtain your Strategy Interim Value or the Strategy Account Value available to you, you may contact our Home Office. Your Strategy Interim Value is calculated at the end of each Business Day and may be more or less than the value quoted.

Also, if you take a withdrawal during the first six years that you own your contract, you may be assessed a surrender charge of up to 7%. If you take a withdrawal from an Index-Linked Interest Strategy, your Strategy Account Value on the date of the withdrawal will be reduced by the withdrawal amount, including any applicable surrender charges. In addition, any such withdrawal will also reduce your Strategy Base Value proportionally, which in turn will negatively impact your Strategy Account Value. See “How do withdrawals affect my Fixed Interest Strategy Value and Index-Linked Interest Strategy Account Values?” below.

10

Table of Contents

Can I make transfers between Index-Linked Interest Strategies and the Fixed Interest Strategy? During the Accumulation Phase, you can transfer Account Value (without imposition of an Asset Adjustment) among the Index-Linked Interest Strategies, and between the Index-Linked Interest Strategies and the Fixed Interest Strategy, free of charge, at the end of an Index-Linked Interest Strategy’s or Fixed Interest Strategy’s Crediting Period. You may not make transfers at any other time. We must receive your transfer request at our Service Center at least two Business Days prior to the end of a Crediting Period. If we do not receive a transfer request, no transfers will occur and your then existing allocation will remain in place for the next Crediting Period. See the section titled “General Liquidity Risk” for more information. Transfers are discussed in detail in the section titled “Transfers.”

Can I make withdrawals? You may take withdrawals from your Contract at any time during the Accumulation Phase. If you take a partial withdrawal or surrender your Contract (i.e., a full withdrawal), your withdrawal may be subject to a surrender charge, and withdrawals from your Strategy Account Values during a Crediting period will be based on respective Strategy Interim Values. Surrenders and withdrawals on a Crediting Date during the first six Contract Years will be based on Strategy Account Values that includes the Asset Adjustment. Repetitive withdrawals (a form of systematic partial withdrawals) are also available during the Accumulation Phase. If you are under age 591⁄2, amounts you withdraw from the Contract may also be subject to a 10% additional federal tax. Please consult with your Tax Advisor for additional information.

See the section titled “Access to your Money During the Accumulation Phase” for additional information.

How do withdrawals affect my Fixed Interest Strategy Value and Strategy Account Values? When you take a withdrawal from your Fixed Interest Strategy, your Fixed Interest Strategy Value is reduced by the dollar amount of the withdrawal, including any applicable surrender charges. When you take a withdrawal from an Index-Linked Interest Strategy, the applicable Strategy Account Value is reduced in the same manner. However, if you take a withdrawal from an Index-Linked Interest Strategy, the withdrawal will also cause a proportional reduction (perhaps significant reduction) to your Strategy Base Value. A reduction in your Strategy Base Value negatively impacts your Strategy Account Value because the Strategy Base Value is what is used to calculate the Index-Linked Interest to be credited at the end of the Crediting Period. Overall, withdrawals may result in a loss of principal and previously-credited interest due to adjustments and charges that may be imposed even if Index Performance has been positive.

You should fully understand how withdrawals affect the value of your Contract, particularly your Strategy Account Values, prior to purchasing the Contract. See “Strategy Base Value Risk” and “Impact of Withdrawals from Index-Linked Interest Strategies” for additional information about how withdrawals affect your Strategy Account Values.

What charges are deducted under the Contract? During the first six years that you own the Contract, if you take a withdrawal (including systematic withdrawals) more than the free withdrawal amount allowed under your Contract, you may be assessed a surrender charge. The amount of the surrender charge, if any, will depend on the Contract Year during which the withdrawal is taken. The schedule below sets forth the surrender charges under the Contract. The surrender charge schedule starts at 7% and declines until the seventh Contract Year when it reaches 0%.

Contract Year | 1 | 2 | 3 | 4 | 5 | 6 | 7+ | |||||||||||||||||||||

Surrender Charge (as a percentage of the amount withdrawn in excess of the free withdrawal amount) | 7% | 7% | 6% | 5% | 4% | 3% | 0 | % | ||||||||||||||||||||

For the first six Contract Years, you may take withdrawals during each Contract Year, in the aggregate, up to your free withdrawal amount without the imposition of surrender charges. Such withdrawals are subject to calculation using Strategy Interim Values if made during a Crediting Period or adjustment for the Asset Adjustment if made on a Crediting Date during the first six Contract Years. Surrender charges will be imposed

11

Table of Contents

only on the amounts withdrawn in excess of your free withdrawal amount. Your free withdrawal amount during the first Contract Year is 10% of Premium. Your free withdrawal amount during each subsequent Contract Years is 10% of your Account Value as of the preceding Contract Anniversary.

Surrender charges are discussed in detail in the section titled “Surrender Charge.”

Additionally, if you take a withdrawal (including a withdrawal of the free withdrawal amount) from an Index-Linked Interest Strategy prior to the end of the Crediting Period, the amount of your withdrawal will be based on the Strategy Interim Value, which may be less than the Strategy Account Value at the end of the Crediting Period. If you take a withdrawal on a Crediting Date during the first six Contract Years, that transaction will be based on your Strategy Account Value that includes the Asset Adjustment. You may lose up to your entire Strategy Account Value in any or all Index-Linked Interest Strategies by taking withdrawals prior to the end of the Crediting Period or, during the first six Contract Years, on a Crediting Date. It is possible to lose your entire principal investment and any previously credited Index-Linked Interest over the life of your Contract.

What annuity options are available during the Income Phase? You may select from three annuity options under the Contract. The available annuity options are:

| • | Income for Fixed Period; |

| • | Life Income with Guaranteed Period; or |

| • | Joint and Survivor Income with Guaranteed Period. |

All annuity payments will be made on a fixed basis. Your annuity payments will be based on the Surrender Value of your Contract on the Maturity Date. This means that if your Maturity Date is (i) during a Crediting Period, your payments will be based on the Strategy Interim Values of the Index-Linked Interest Strategies in which you are invested; (ii) on a Crediting Date during the first six Contract Years, your payments will be based on Strategy Account Values that include the Asset Adjustment; and (iii) during the Surrender Charge Period, your payments will be based on your Account Value less surrender charges. The annuity options are discussed in more detail in the section titled “Annuity Payments.”

Does the Contract provide a death benefit? If you die during the Accumulation Phase, your Contract provides for a death benefit equal to the greater of:

| (a) | Your Account Value (subject to Strategy Interim Values during a Crediting Period or including the Asset Adjustment on a Crediting Date during the first six Contract Years); or |

| (b) | Your Premium, reduced proportionately by the percentage reduction in the Account Value for each partial withdrawal, including any surrender charge deduction. |

The death benefit is not payable during the Income Phase and will terminate without value as of the Maturity Date. The death benefit is discussed in more detail in the section titled “Death Benefit.”

How do I contact Fidelity & Guaranty Life Insurance Company? F&G’s principal place of business is located at 801 Grand Ave., Suite 2600, Des Moines, IA 50309. If you need more information, or you wish to submit a request, you should contact us at the following:

Service Center: For all written communications, general correspondence and other transactional requests, please contact us at:

F&G Service Center

P.O. Box 81497

Lincoln, NE 68501-1497

12

Table of Contents

For Overnight Mail:

F&G Service Center

777 Research Drive

Lincoln, NE 68521

We will not deem correspondence, including transactional requests including applications and Premium payments to be received by us until picked up at our Service Center.

Customer Service by Phone: 1-888-513-8797

Online Service: www.fglife.com

13

Table of Contents

The purchase of the Contract involves certain risks. You should carefully consider the following factors, in addition to the matters set forth elsewhere in this prospectus, prior to purchasing the Contract.

The Contract is intended to be a long-term investment that you may use to help save for retirement. The Contract is not designed to be a short-term investment. If you take withdrawals from your Contract during the Surrender Charge Period, surrender charges may apply. In addition, if you make withdrawals from the Contract before you attain age 591⁄2, the amounts you withdraw may also be subject to a 10% additional federal tax. This Contract may not be appropriate for you if you expect to take withdrawals that will be subject to surrender charges or additional federal taxes.

You can transfer Account Value among the Index-Linked Interest Strategies and the Fixed Interest Strategy only at the end of a Crediting Period, which may be as long as six years. This restricts your ability to react to changes in market conditions during Crediting Period. You should consider whether the inability to reallocate Account Value during a Crediting Period meets your financial needs. We must receive your transfer request at least two Business Days prior to the end of a Crediting Period. If we do not receive a transfer request, no transfers will occur and your then existing allocation will remain in place for the next Crediting Period. This will occur even if the Index, Cap Rate, Performance Trigger Rate or Participation Rate associated with the Index-Linked Interest Strategy has changed since you last selected the Index-Linked Interest Strategy. Under such circumstances, the Index-Linked Interest Strategy may no longer be appropriate for your investment goals. If you fail to transfer Strategy Account Value at the beginning of a Crediting Period and do not wish to remain invested in a particular Index-Linked Interest Strategy for the remainder of the Crediting Period, your only option will be to surrender the related Strategy Account Value.

Surrendering all or withdrawing a portion of your Account Value may cause you to incur surrender charges, negative adjustments to certain values under your Contract based on the Strategy Interim Value of the Index-Linked Interest Strategy or imposition of the Asset Adjustment, and negative tax consequences. If you withdraw Account Value allocated to an Index-Linked Interest Strategy prior to the end of a Crediting Period (including through a repetitive withdrawal) or, during the first six Contract Years, on a Crediting Date, the withdrawal will cause a reduction to your Strategy Base Value.

When you take such a withdrawal, your Strategy Base Value will be immediately reduced in a proportion equal to the reduction in your Strategy Account Value. A proportional reduction could be larger than the dollar amount of your withdrawal. Reductions to your Strategy Base Value will negatively impact your Strategy Account Value for the remainder of the Crediting Period and may result in a lower amount of Index-Linked Interest being credited, if any, at the end of the Crediting Period.

Once your Strategy Base Value is reduced due to a withdrawal, there is no way under the Contract to increase your Strategy Base Value during the remainder of the Crediting Period. See “Impact of Withdrawals from Index-Linked Interest Strategies” for additional information about how withdrawals affect your Strategy Account Values.

See “Interim Value Risk” below for information on how liquidity risks relate to our Interim Value calculation.

We may defer payments made under this Contract for up to six months if the applicable insurance regulatory authority approves such deferral.

RISK OF LOSS RELATED TO SURRENDER CHARGES

There is a risk of loss of principal and previously-credited Index-Linked Interest if you take a withdrawal from your Contract or surrender it during the first six Contract Years when we will deduct a surrender charge. This risk exists even if you are invested in an Index-Linked Interest Strategy with an Index that is performing positively as of the date of your withdrawal.

14

Table of Contents

If you allocate money to an Index-Linked Interest Strategy for a Crediting Period, the value of your investment will depend in part on the performance of the applicable Index or Indexes. The performance of an Index is based on changes in the values of the securities or other instruments that comprise or define the Index. The securities and instruments comprising or defining the Indexes are subject to a variety of investment risks, many of which are complicated and interrelated. These risks may affect capital markets generally, specific market segments, or specific issuers. The performance of the Indexes may fluctuate, sometimes rapidly and unpredictably. Negative Index performance may cause you to lose money on your investment in the Contract. The historical performance of an Index or an Index-Linked Interest Strategy does not guarantee future results. It is impossible to predict whether an Index will perform positively or negatively over the course of a Crediting Period.

While it is not possible to invest directly in an Index, if you choose to allocate amounts to an Index-Linked Interest Strategy, you are indirectly exposed to the investment risks associated with the applicable Index. Because each Index is comprised or defined by a collection of securities, each Index is largely exposed to market risk and issuer risk.

You may earn less than the positive return of an Index due to the Cap Rate, Performance Trigger Rate or Participation Rate applicable to an Index-Linked Interest Strategy, because a positive return of the Index is subject to a maximum in the form of the Cap Rate or Performance Trigger Rate and a positive return of the Index may be subject to a Participation Rate below 100%. Your returns may be lower than those earned by a shareholder of a mutual fund or exchange-traded fund (“ETF”) designed to track the same Index.

Market risk is the risk that market fluctuations may cause the value of a security to fluctuate, sometimes rapidly and unpredictably. Issuer risk is the risk that the value of an issuer’s securities may decline for reasons directly related to the issuer, as opposed to the market generally.

Provided below is a summary of other important investment risks to which the Indexes are exposed. For more information on the Indexes, see the section titled “Indexes.”

| • | S&P 500® Index. The S&P 500® Index is comprised of equity securities issued by large-capitalization U.S. companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges, and may not be able to attain the high growth rate of successful smaller companies. |

| • | Russell 2000® Index. The Russell 2000® Index is comprised of equity securities of small-capitalization U.S. companies. In general, the securities of small-capitalization companies may be more volatile and may involve more risk than the securities of larger companies. Small-capitalization companies are more likely to fail than larger companies. |

| • | Nasdaq-100® Index. The Nasdaq-100® Index is comprised of equity securities of the largest U.S. and non-U.S. companies listed on the Nasdaq Stock Market, including companies across all major industry groups except financial companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges, and may not be able to attain the high growth rate of successful smaller companies. To the extent that the Nasdaq-100® Index is comprised of securities issued by companies in a particular sector, those securities may not perform as well as the securities of companies in other sectors or the market as a whole. Also, any securities issued by non-U.S. companies (including related depositary receipts) are subject to the risks related to investments in foreign markets (e.g., increased volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty). |

| • | MSCI EAFE Index. The MSCI EAFE Index is an equity index that captures large and mid-cap representation across developed markets around the world. The securities comprising the MSCI EAFE Price Return Index are subject to the risks related to investments in foreign markets (e.g. increased |

15

Table of Contents

price volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty). In general, foreign markets may be less liquid, more volatile, and subject to less government supervision than domestic markets. |

| • | Hindsight 20/20 Index-Linked Interest Strategy. The Index-Linked Interest Strategy is linked to the performance of the BofA MP Growth Index, the BofA MP Balanced Index or the BofA Defensive Index (together, the “BofA MP Indices”). The Company determines the performance of the Hindsight 20/20 Index-Linked Interest Strategy based on whichever of the BofA MP Indices has performed best during the applicable Crediting Period. |

Each of the BofA MP Indices follows a rules-based methodology designed to provide exposure to four markets: U.S. large-capitalization companies, U.S. Treasury bonds, U.S. high yield corporate bonds, and gold. To provide such exposure, each BofA MP Index is comprised of four ETFs providing exposure to those four markets, respectively: SPDR S&P 500 ETF Trust (SPY); iShares 7-10 Year Treasury Bond ETF (IEF); iShares iBoxx High Yield Corporate Bond ETF (HYG); and SPDR Gold Shares (GLD). The target weightings for the ETFs differ among the BofA MP Indices based on their respective “growth,” “balanced,” and “defensive” methodologies. Notwithstanding the names of the BofA MP Indices, there is no assurance that any of their methodologies will achieve “growth,” “balance,” or “defensiveness,” enhance performance or reduce risk. Moreover, the Indices may underperform a direct investment in the underlying ETFs.

Risks relating to the BofA MP Indices

| • | The BofA MP Indices may not be successful or outperform any alternative strategy. Each BofA MP Index follow a rules-based strategy that operates on the basis of pre-determined rules. No assurance can be given that the strategy will be successful or that any BofA MP Index will outperform any alternative strategy that might be employed. Each BofA MP Index strategy may have objectives, features and/or constituents that are similar to those of other indices or for which other underlying components may be better suited to achieve the stated objective. Each BofA MP Index operates independently and does not necessarily enhance, modify or seek to outperform any other BofA MP Index. Each BofA MP Index is not itself an investment or instrument and does not give any person any entitlement to, or ownership interest in, any underlying asset referenced (directly or indirectly) by such index. |

| • | Limited Operating History. The BofA MP Indices were established on February 7, 2023 and therefore each has a limited operating history. Past performance should not be considered indicative of future performance. No assurance, representation or warranty is given with respect to the future performance of any BofA MP Index or that it will achieve its objective. |

| • | Interactions between underlying ETFs. Changes in the values of the underlying ETFs may not result in a comparable change in the value of each BofA MP Index. Because the underlying ETF weights are set at each rebalancing date in accordance with the pre-determined allocation for the applicable strategy, movements in the value of the underlying ETF will not affect each Index equally. Also, although the weights are rebalanced on a quarterly basis, in between rebalancings the value of each underlying ETF may fluctuate significantly and as a result the weights will vary. Performance of the underlying ETFs may become highly correlated from time to time, including periods in which there is a substantial decline in the assets represented by one or more underlying ETFs. High correlation between underlying ETFs during periods of negative returns could have a materially adverse effect on the performance of each BofA MP Index. Price movements between the underlying ETFs may not correlate with each other. At a time when the value of an underlying ETF increases, the value of other underlying ETFs may not increase as much or may decline. Therefore, increases in the values of some of the underlying ETFs may be moderated, or more than offset, by lesser increases or declines in the values of other Underlying ETFs. |

16

Table of Contents

When you select a Hindsight 20/20 Index-Linked Interest Strategy for investment, you are exposed to the investment risks of the four ETFs that comprise the BofA MP Indexes, such as the following:

Primary Market Exposures

| • | Equity Risk. Equity securities (e.g., common stocks) are subject to changes in value. The values of equity securities may be volatile and can be influenced by a number of factors, such as changes in (or perceived changes in) general capital markets, specific market segments, or specific issuers, and factors such as economic and political developments, changes in interest rates, perceived trends in securities prices, war, acts of terrorism, the spread of infectious disease or other public health issues. |

| • | Fixed Income Risk. Fixed income instruments (e.g., bonds) are subject to investment risks such as interest rate risk (i.e., negative fluctuations in market value due to changes in interest rates) and credit risk (i.e., the risk of default by the obligors). The market price of a fixed income instrument can be volatile and influenced by a number of factors, particularly its duration, yield as compared to current market interest rates, and the actual or perceived credit quality of the issuer. |

| • | Commodity Related Risk. The price of gold has fluctuated widely over the past several years. Several factors may affect the price of gold, including global gold supply and demand; global or regional political, economic or financial events and situations; investors’ expectations with respect to the rate of inflation; interest rates; investment and trading activities of hedge funds and commodity funds; and other economic variables. The possibility of large-scale distress sales of gold in times of crisis may have a negative impact on the price of gold. There is a risk that some or all of the gold bars held by the Custodian or any subcustodian on behalf of the GLD ETF could be lost, damaged or stolen and the value of the GLD ETF could diminish materially. |

| • | Government Bond Risk. The prices of government bonds are significantly influenced by the creditworthiness of the governments that issue them. Any decline or perceived decline in a government’s creditworthiness, as a result of a credit rating downgrade or otherwise, may cause the prices of that government’s bonds to fall, perhaps significantly, and may cause increased volatility in local or global credit markets. In recent years, U.S. rating agencies have downgraded the creditworthiness and/or assigned negative outlooks to the U.S. and may do so again in the future. |