Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05904

ELFUN MONEY MARKET FUND

(Exact name of registrant as specified in charter)

1600 SUMMER STREET, STAMFORD, CONNECTICUT 06905

(Address of principal executive offices) (Zip code)

GE ASSET MANAGEMENT, INC.

1600 SUMMER STREET, STAMFORD, CONNECTICUT 06905

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-242-0134

Date of fiscal year end: 12/31

Date of reporting period: 12/31/11

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Table of Contents

Elfun Funds

Annual Report

December 31, 2011

Table of Contents

| 1 | ||||

Manager Reviews and Schedules of Investments | ||||

| 2 | ||||

| 10 | ||||

| 16 | ||||

| 42 | ||||

| 55 | ||||

| 72 | ||||

| 78 | ||||

| 80 | ||||

| 84 | ||||

| 86 | ||||

| 88 | ||||

| 90 | ||||

| 104 | ||||

| 105 | ||||

| 106 | ||||

| 109 | ||||

| 113 | ||||

| 116 | ||||

This report has been prepared for shareholders and may be distributed to others only if preceded or accompanied by a current summary prospectus or prospectus.

Table of Contents

Information on the following performance pages relates to the Elfun Funds.

Total returns take into account changes in share price and assume reinvestment of all dividends and capital gains distributions, if any. Total returns shown are net of Fund expenses.

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Periods less than one year are not annualized. Please call toll-free 800-242-0134 or visit the Funds’ website at http://www.geam.com for the most recent month-end performance data.

A portion of the Elfun Tax-Exempt Income Fund’s income may be subject to state, federal and/or alternative minimum tax. Capital gains, if any, are subject to capital gains tax.

An investment in a Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. An investment in a Fund is subject to risk, including possible loss of principal invested.

The Standard & Poor’s (“S&P”) 500® Composite Price Index of stocks (S&P 500 Index), Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE® Index), Barclays Capital U.S. Aggregate Bond Index, the Barclays Capital U.S. Municipal Bond Index, and the 90 Day U.S. T-Bill are unmanaged indices and do not reflect the actual cost of investing in the instruments that comprise each index. The results shown for the foregoing indices assume the reinvestment of net dividends or interest and do not reflect the fees, expenses or taxes.

S&P 500 Index is an unmanaged, market capitalization-weighted index of stocks of 500 large U.S. companies, which is widely used as a measure of large-cap stock market performance. MSCI® EAFE® Index is a market capitalization-weighted index of equity securities of companies domiciled in various countries. The index is designed to represent the performance of developed stock markets outside the U.S. and Canada and excludes certain market segments unavailable to U.S. based

investors. Barclays Capital U.S. Aggregate Bond Index is a market value-weighted index of taxable investment-grade debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of one year or more. This index is designed to represent the performance of the U.S. investment-grade first-rate bond market. Barclays Capital U.S. Municipal Bond Index is an unmanaged index comprised of investment-grade, fixed rate securities with maturities of at least eight years and less than twelve years.

The 90 Day U.S. T-Bill is an unmanaged measure/index of the performance of the most recently auctioned 90 Day U.S. Treasury bills (i.e. having a total maturity of 90 days) currently available in the marketplace.

The peer universe of underlying funds used for the peer group average annual total return calculation is based on the blend of Morningstar peer categories, as shown. Morningstar is an independent mutual fund rating service. A Fund’s performance may be compared to or ranked within a universe of mutual funds with investment objectives and policies similar but not necessarily identical to the Fund.

©2012 Morningstar, Inc. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damage or losses relating from any use of this information. Past performance is no guarantee of future results.

The views, expressed in this document reflect our judgment as of the publication date and are subject to change at any time without notice.

GE Investment Distributors, Inc., member of FINRA, is the principal underwriter and distributor of the Elfun Funds and a wholly owned subsidiary of GE Asset Management Incorporated, the investment adviser of the Funds.

1

Table of Contents

(Unaudited)

Ralph R. Layman

President and

Chief Investment Officer – Public Equities

The Elfun International Equity Fund is managed by a team of portfolio managers that includes Brian Hopkinson, Ralph R. Layman (pictured to the left), Paul Nestro, Jonathan L. Passmore, and Michael J. Solecki. As lead portfolio manager for the Fund, Mr. Layman oversees the entire team and assigns a portion of the Fund to each manager, including himself. Each portfolio manager is limited to the management of his or her portion of the Fund, the size of the portion which Mr. Layman determines on an annual basis. The portfolio managers do not operate independently of each other, rather, the team operates collaboratively, communicating purchases or sales of securities on behalf of the Fund. See portfolio managers’ biographical information beginning on page 113.

| Q. | How did the Elfun International Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended December 31, 2011? |

| A. | For the twelve-month period ended December 31, 2011, the Elfun International Equity Fund returned -16.02%. The MSCI EAFE Index, the Fund’s benchmark, returned -12.14% and the Fund’s Morningstar peer group of 817 Foreign Large Blend Funds returned an average of -13.90% over the same period. |

| Q. | What factors affected the Fund’s performance? |

| A. | Macro-economic and geopolitical issues dominated sentiment for much of the year. The European sovereign debt crisis was a constant influence but had a harsher, |

| negative impact during the third quarter when the crisis moved from Greece to concerns that Italy, a much more indebted country, might struggle to roll over its debt. In addition, aggressive austerity measures introduced by European countries, while fiscally responsible, increased the risk of recession. Meanwhile, accelerating fears that China may experience an economic “hard-landing” added to the negative market sentiment. For much of the year, strong corporate results acted as a counter to the negative news, but in the third quarter, the weight of that news took stocks sharply lower before recovering slightly toward the end of the year. |

| Q. | What were the primary drivers of Fund performance? |

| A. | Despite being underweight, even modest positions in BNP Paribas (France), Lloyds Banking Group (UK) and Unicredit (Italy) had a disproportionately negative impact on the Fund’s performance due to the European debt crisis. In the energy sector, the Fund’s holding in Paladin, an Australian uranium miner, fell sharply after the Japanese earthquake/tsunami destroyed several nuclear reactors. From an allocation perspective, the underweight in healthcare and the Pacific Rim region were negative while the Fund’s underweight in Japan and overweight in the U.K. were positive. The Fund’s overweight in emerging markets had a negative impact. Stocks in the information technology sector were the |

2

Table of Contents

(Unaudited)

| top positive contributors, including Samsung Electronics, Taiwan Semiconductor and UK-based Autonomy, which was bought out by Hewlett Packard in an all-cash transaction. |

| Q. | Were there any significant changes to the Fund during the period? |

| A. | The Fund’s underweight in consumer discretionary stocks was reduced with the addition of WPP (advertising), LVMH (luxury goods) and autos. The Fund’s underweight in healthcare was increased with the elimination of Roche Holdings. The Fund’s overweights in industrials and materials were reduced as more cyclical stocks screened less well in a deteriorating economic environment; but IT holdings were increased selectively through the addition of Hexagon (measuring software) and SAP (enterprise software). Cash increased by year-end to approximately 2.5%. |

3

Table of Contents

(Unaudited)

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in units of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended December 31, 2011.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value

divided by $1,000 = 8.6), then multiply the result by the number given for your class under the heading “Expenses Paid During Period.”

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect any transaction costs, such as sales charges or redemption fees, if any.

July 1, 2011 – December 31, 2011

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($)* | ||||||||||

Actual Fund Return** | 1,000.00 | 806.60 | 1.37 | |||||||||

Hypothetical 5% Return | 1,000.00 | 1,023.69 | 1.53 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.30% (for the period July 1, 2011 - December 31, 2011), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | Actual Fund Return for the six-month period ended December 31, 2011 was: -19.34%. Past performance does not guarantee future results. |

4

Table of Contents

(Unaudited)

Investment Profile

A mutual fund designed for investors who seek long-term growth of capital and future income. The Fund seeks its objective by investing principally in foreign securities consistent with prudent investment management and the preservation of capital. The Fund invests at least 80% of its net assets under normal circumstances in equity securities, such as common stock and preferred stocks and invests primarily (meaning at least 65%) in companies in both developed and emerging market countries outside the United States.

Top Ten Largest Holdings

as of December 31, 2011 as a % of Fair Value(b)(c)

Royal Dutch Shell PLC | 3.66% | |||

Nestle S.A. | 2.86% | |||

HSBC Holdings PLC | 2.39% | |||

Samsung Electronics Company Ltd. | 2.31% | |||

Linde AG | 2.29% | |||

Novartis AG | 2.18% | |||

Diageo PLC | 2.14% | |||

Vodafone Group PLC | 2.10% | |||

Suzuki Motor Corp. | 2.01% | |||

BHP Billiton PLC | 1.99% |

Sector Allocation

as a % of the Fair Value of $239,314 (in thousands) as of December 31, 2011.(b)(c)

Morningstar Performance Comparison

Based on average annual returns for periods ended 12/31/11

One | Five | Ten | ||||||||||

Number of funds in peer group | 817 | 567 | 317 | |||||||||

Peer group average annual total return | -13.90 | % | -4.75 | % | 3.91 | % | ||||||

Morningstar category in peer group: Foreign Large Blend |

| |||||||||||

Change in Value of a $10,000 Investment(a)

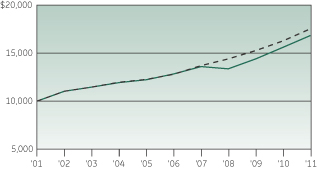

Average Annual Total Return

for the periods ended December 31, 2011

| (Inception date: 01/01/88) | ||||||||||||||||

One | Five | Ten | Ending value of a | |||||||||||||

Elfun International Equity Fund | -16.02% | -4.75% | 4.54% | $15,594 | ||||||||||||

MSCI® EAFE® Index | -12.14% | -4.72% | 4.67% | $15,780 | ||||||||||||

| (a) | Ending value of a $10,000 investment for the ten-year period or since inception, whichever is less. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

| (c) | Fair Value basis is inclusive of short-term investment in GE Institutional Money Market Fund Investment Class. |

See Notes to Performance on page 1 for further information.

Past performance does not predict future performance. The performance shown on the graph and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

5

Table of Contents

| Elfun International Equity Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

Common Stock — 95.0%† |

| |||||||||

| Australia — 1.8% | ||||||||||

Brambles Ltd. | 377,759 | $ | 2,773 | |||||||

Lynas Corporation Ltd. | 1,488,156 | 1,594 | (a) | |||||||

| 4,367 | ||||||||||

| Brazil — 1.6% | ||||||||||

Petroleo Brasileiro S.A. ADR | 109,123 | 2,563 | ||||||||

Vale S.A. ADR | 60,806 | 1,253 | ||||||||

| 3,816 | ||||||||||

| Canada — 4.1% | ||||||||||

Canadian Natural Resources Ltd. | 48,800 | 1,828 | ||||||||

Kinross Gold Corp. | 195,783 | 2,236 | ||||||||

Potash Corporation of Saskatchewan Inc. | 84,517 | 3,495 | ||||||||

Suncor Energy Inc. | 82,936 | 2,393 | ||||||||

| 9,952 | ||||||||||

| China — 1.7% | ||||||||||

Baidu Inc. ADR | 25,232 | 2,939 | (a) | |||||||

Bank of China Ltd. | 3,320,976 | 1,227 | ||||||||

| 4,166 | ||||||||||

| Denmark — 0.3% | ||||||||||

Carlsberg A/S | 11,097 | 785 | ||||||||

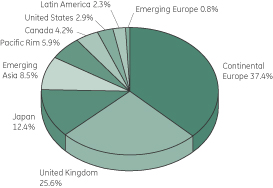

| France — 10.0% | ||||||||||

Accor S.A. | 6,225 | 158 | ||||||||

AXA S.A. | 162,152 | 2,114 | ||||||||

BNP Paribas S.A. | 84,510 | 3,330 | ||||||||

Cap Gemini S.A. | 53,058 | 1,663 | ||||||||

Cie Generale d’Optique Essilor International S.A. | 53,656 | 3,800 | ||||||||

European Aeronautic Defence and Space Company N.V. | 36,736 | 1,152 | ||||||||

LVMH Moet Hennessy Louis Vuitton S.A. | 14,182 | 2,014 | ||||||||

Safran S.A. | 125,887 | 3,792 | ||||||||

Schneider Electric S.A. | 14,852 | 784 | ||||||||

Total S.A. | 24,882 | 1,276 | ||||||||

Vallourec S.A. | 35,389 | 2,304 | ||||||||

| Number of Shares | Fair Value | |||||||||

VInci S.A. | 39,909 | $ | 1,749 | |||||||

| 24,136 | ||||||||||

| Germany — 9.9% | ||||||||||

Adidas AG | 32,919 | 2,148 | ||||||||

Bayer AG | 36,292 | 2,327 | (a) | |||||||

Daimler AG | 12,154 | 535 | ||||||||

Deutsche Boerse AG | 23,759 | 1,249 | (a) | |||||||

Fresenius SE & Company KGAA | 34,977 | 3,246 | ||||||||

Linde AG | 36,705 | 5,477 | ||||||||

Metro AG | 25,090 | 918 | ||||||||

SAP AG | 59,399 | 3,150 | ||||||||

Siemens AG | 35,724 | 3,429 | ||||||||

ThyssenKrupp AG | 56,454 | 1,299 | ||||||||

| 23,778 | ||||||||||

| Hong Kong — 2.9% | ||||||||||

AIA Group Ltd. | 1,075,843 | 3,359 | ||||||||

Hutchison Whampoa Ltd. | 264,147 | 2,221 | ||||||||

Wharf Holdings Ltd. | 324,043 | 1,469 | ||||||||

| 7,049 | ||||||||||

| India — 1.1% | ||||||||||

ICICI Bank Ltd. | 85,025 | 1,095 | ||||||||

Larsen & Toubro Ltd. | 48,435 | 908 | ||||||||

Power Grid Corporation of India Ltd. | 376,651 | 710 | ||||||||

| 2,713 | ||||||||||

| Ireland — 1.0% | ||||||||||

WPP PLC | 219,447 | 2,304 | ||||||||

| Italy — 0.4% | ||||||||||

ENI S.p.A | 41,856 | 870 | ||||||||

| Japan — 12.3% | ||||||||||

Daikin Industries Ltd. | 68,200 | 1,869 | ||||||||

FANUC Corp. | 21,300 | 3,261 | ||||||||

Mitsubishi Corp. | 129,000 | 2,607 | ||||||||

Mitsubishi Heavy Industries Ltd. | 205,000 | 874 | ||||||||

SMC Corp. | 12,400 | 2,002 | ||||||||

Softbank Corp. | 105,299 | 3,103 | ||||||||

Sony Financial Holdings Inc. | 147,100 | 2,168 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

6

Table of Contents

| Elfun International Equity Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

Sumitomo Realty & Development Company Ltd. (REIT) | 104,000 | $ | 1,822 | |||||||

Suzuki Motor Corp. | 232,631 | 4,813 | ||||||||

The Bank of Yokohama Ltd. | 465,990 | 2,205 | ||||||||

Toyota Motor Corp. | 32,282 | 1,076 | ||||||||

Unicharm Corp. | 77,300 | 3,813 | ||||||||

| 29,613 | ||||||||||

| Mexico — 0.8% | ||||||||||

America Movil SAB de C.V. ADR | 81,538 | 1,843 | ||||||||

| Netherlands — 2.9% | ||||||||||

ING Groep N.V. | 279,974 | 2,021 | (a) | |||||||

Koninklijke Ahold N.V. | 46,298 | 625 | ||||||||

Koninklijke Philips Electronics N.V. | 74,133 | 1,567 | ||||||||

Unilever N.V. | 81,110 | 2,798 | ||||||||

| 7,011 | ||||||||||

| Russian Federation — 0.3% | ||||||||||

Mobile Telesystems OJSC ADR | 46,082 | 676 | ||||||||

| Singapore — 1.1% | ||||||||||

United Overseas Bank Ltd. | 233,525 | 2,750 | ||||||||

| South Africa — 0.5% | ||||||||||

MTN Group Ltd. | 64,017 | 1,140 | ||||||||

| South Korea — 3.3% | ||||||||||

Hyundai Motor Co. | 12,923 | 2,389 | (a) | |||||||

Samsung Electronics Company Ltd. | 6,016 | 5,525 | ||||||||

| 7,914 | ||||||||||

| Spain — 1.5% | ||||||||||

Banco Santander S.A. | 243,365 | 1,854 | (h) | |||||||

Telefonica S.A. | 98,637 | 1,714 | ||||||||

| 3,568 | ||||||||||

| Sweden — 1.8% | ||||||||||

Hexagon AB | 117,707 | 1,767 | ||||||||

Telefonaktiebolaget LM Ericsson | 254,724 | 2,616 | ||||||||

| 4,383 | ||||||||||

| Number of Shares | Fair Value | |||||||||

| Switzerland — 7.9% | ||||||||||

Credit Suisse Group AG | 61,602 | $ | 1,454 | |||||||

Nestle S.A. | 118,477 | 6,842 | ||||||||

Novartis AG | 90,810 | 5,215 | ||||||||

Syngenta AG | 11,860 | 3,488 | ||||||||

Zurich Financial Services AG | 8,526 | 1,938 | ||||||||

| 18,937 | ||||||||||

| Taiwan — 2.3% | ||||||||||

Delta Electronics Inc. | 433,000 | 1,030 | ||||||||

Taiwan Semiconductor Manufacturing Company Ltd. | 1,693,400 | 4,239 | ||||||||

Taiwan Semiconductor Manufacturing Company Ltd. ADR | 16,397 | 212 | ||||||||

| 5,481 | ||||||||||

| United Kingdom — 25.5% | ||||||||||

Aggreko PLC | 56,065 | 1,757 | ||||||||

BG Group PLC | 155,191 | 3,320 | (a) | |||||||

BHP Billiton PLC | 163,368 | 4,767 | (h) | |||||||

Diageo PLC | 234,181 | 5,119 | ||||||||

G4S PLC†† | 286,397 | 1,210 | ||||||||

G4S PLC†† | 61,323 | 257 | ||||||||

HSBC Holdings PLC | 749,460 | 5,719 | ||||||||

Lloyds Banking Group PLC | 5,050,539 | 2,033 | (a) | |||||||

National Grid PLC | 433,675 | 4,212 | ||||||||

Prudential PLC | 446,858 | 4,434 | ||||||||

Reckitt Benckiser Group PLC | 79,766 | 3,942 | ||||||||

Rio Tinto PLC | 87,505 | 4,250 | ||||||||

Royal Dutch Shell PLC | 237,704 | 8,758 | ||||||||

Standard Chartered PLC | 146,926 | 3,217 | ||||||||

Tesco PLC | 365,959 | 2,295 | ||||||||

The Capita Group PLC | 108,399 | 1,059 | ||||||||

Vodafone Group PLC | 1,807,828 | 5,026 | ||||||||

| 61,375 | ||||||||||

Total Common Stock | 228,627 | |||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

7

Table of Contents

| Elfun International Equity Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| ||||||||||

Preferred Stock — 1.6% |

| |||||||||

Volkswagen AG | 25,374 | $ | 3,813 | |||||||

Other Investments — 0.1% |

| |||||||||

GEI Investment Fund | 77 | (k) | ||||||||

Total Investments in Securities (Cost $242,414) | 232,517 | |||||||||

Short-Term Investments — 2.8% |

| |||||||||

GE Institutional Money Market Fund — Investment |

| |||||||||

Class 0.06% | ||||||||||

(Cost $6,797) | 6,797 | (d,k) | ||||||||

Total Investments | 239,314 | |||||||||

Other Assets and Liabilities | 1,258 | |||||||||

|

| |||||||||

NET ASSETS — 100.0% | $ | 240,572 | ||||||||

|

| |||||||||

Other Information

The Fund had the following long futures contracts open at December 31, 2011:

| Description | Expiration date | Number of Contracts | Current Notional Value | Unrealized Appreciation/ (Depreciation) | ||||||||||

EURO Stoxx 50 Index Futures | March 2012 | 75 | $ | 2,247 | $ | 69 | ||||||||

FTSE 100 Index Futures | March 2012 | 27 | 2,323 | 41 | ||||||||||

Topix Index Futures | March 2012 | 11 | 1,041 | (28) | ||||||||||

|

| |||||||||||||

| $ | 82 | |||||||||||||

|

| |||||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

8

Table of Contents

| Elfun International Equity Fund | December 31, 2011 |

(Unaudited)

The Fund was invested in the following categories at December 31, 2011:

| Industry | | Percentage (based on Fair Value) | | |

Diversified Financial Services | 9.71% | |||

Integrated Oil & Gas | 8.01% | |||

Automobile Manufacturers | 5.28% | |||

Wireless Telecommunication Services | 4.93% | |||

Diversified Metals & Mining | 4.43% | |||

Semiconductors | 4.17% | |||

Life & Health Insurance | 4.16% | |||

Packaged Foods & Meats | 4.03% | |||

Industrial Machinery | 3.53% | |||

Household Products | 3.24% | |||

Pharmaceuticals | 3.15% | |||

Industrial Conglomerates | 3.02% | |||

Fertilizers & Agricultural Chemicals | 2.92% | |||

Industrial Gases | 2.29% | |||

Distillers & Vintners | 2.14% | |||

Aerospace & Defense | 2.07% | |||

Diversified Support Services | 1.89% | |||

Multi-Utilities | 1.76% | |||

Apparel, Accessories & Luxury Goods | 1.74% | |||

Multi-Line Insurance | 1.69% | |||

Healthcare Supplies | 1.59% | |||

Diversified Real Estate Activities | 1.37% | |||

Healthcare Services | 1.36% | |||

Application Software | 1.32% | |||

Internet Software & Services | 1.23% | |||

Food Retail | 1.22% | |||

Construction & Engineering | 1.11% |

Communications Equipment | 1.09% | |||

Trading Companies & Distributors | 1.09% | |||

Steel | 1.07% | |||

Advertising | 0.96% | |||

Gold | 0.93% | |||

Regional Banks | 0.92% | |||

Building Products | 0.78% | |||

Oil & Gas Exploration & Production | 0.76% | |||

Electronic Equipment & Instruments | 0.74% | |||

Integrated Telecommunication Services | 0.72% | |||

IT Consulting & Other Services | 0.69% | |||

Diversified Capital Markets | 0.61% | |||

Security & Alarm Services | 0.61% | |||

Specialized Finance | 0.52% | |||

Human Resource & Employment Services | 0.44% | |||

Electronic Components | 0.43% | |||

Hypermarkets & Super Centers | 0.38% | |||

Brewers | 0.33% | |||

Electrical Components & Equipment | 0.33% | |||

Electric Utilities | 0.30% | |||

Hotels, Resorts & Cruise Lines | 0.07% | |||

|

| |||

| 97.13% | ||||

|

|

| Short-Term and Other Investments | ||||

Short-Term | 2.84% | |||

Other Investments | 0.03% | |||

|

| |||

| 2.87% | ||||

|

| |||

| 100.00% | ||||

|

|

See Notes to Schedules of Investments and Notes to Financial Statements.

9

Table of Contents

(Unaudited)

David B. Carlson

Chief Investment Officer – U.S. Equities

The Elfun Trusts is managed by David B. Carlson. See portfolio managers’ biographical information beginning on page 113.

| Q. | How did the Elfun Trusts Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended December 31, 2011? |

| A. | For the twelve-month period ended December 31, 2011, the Elfun Trusts Fund returned 1.33%. The S&P 500® Index (S&P 500 Index), the Fund’s benchmark, returned 2.11% and the Fund’s Morningstar peer group of 1,683 U.S. Large Cap Growth Funds returned an average of -2.56% over the same period. Elfun Trusts outperformed 81% of its Morningstar peer group in 2011. |

| Q. | What market factors affected the Fund’s performance? |

| A. | While the market closed the year virtually flat with the start of the year, there was tremendous volatility along the way. A host of macro events buffeted that market—earthquake/tsunami in Japan, political unrest in several Middle Eastern states, sovereign debt issues in Europe (again) and a downgrade of U.S. Government debt. The U.S. economy muddled along with slow growth, and corporate profit growth was strong, due in large part to strength in foreign sourced earnings. Operating profits for the S&P 500 Index grew an estimated 15% in 2011, an impressive performance given below-average GDP growth. |

Within the equity market there was significant risk aversion and a reach for yield. The utility sector was the strongest performer with a 20% return, followed by the consumer staples sector with a 14% return. Stocks with above-average dividend yields were strong performers, regardless of sector—a theme that makes sense when fixed income rates are so low. The financial sector was the worst performing sector with a decline of 17%. Large banks and brokers had the steepest declines. Sovereign debt fears in Europe weighed heavily on the European banks, and the interconnectedness of the financial markets brought the concern to the U.S.

Globally, the U.S. was a strong relative performer as stock markets in Europe, Japan and the emerging markets were all down in excess of 10%. Fears of recession weighed on Europe and fears of a hard landing in China weighed on emerging markets. We believe these macro concerns will be with us in 2012 as well.

| Q. | What were the primary drivers of Fund performance? |

| A. | Elfun Trusts’ performance, while modestly behind the S&P 500 Index return was strong relative to peer funds. The year saw an unusually high number of equity mutual fund managers trail benchmarks, due in large part to the narrow leadership of defensive stocks (e.g., utilities and staples). Technology was the strongest sector for Elfun Trusts. |

10

Table of Contents

(Unaudited)

| Tech holdings in the Fund were up 12%, with Visa leading the way with a 45% gain. Other notable tech holdings were Apple (+26%), Baidu (+21%) and Qualcomm (+12%). |

The consumer-discretionary sector was a positive contributor for the year. Outperformers include Bed, Bath & Beyond (+18%), Liberty Global (+17%) and Comcast (+16%).

The Fund’s holdings in health care and energy were detractors from performance, due to the fact that we did not own the higher yielding companies. In health care, the Fund was underweighted in pharmaceuticals, which were strong performers. In energy, we favor the oil service sector over the large integrated companies such as Exxon. We simply underestimated investors demand for dividend yield and the Fund did not own enough of the higher yielding stocks in the market.

| Q. | Were there any significant changes to the Fund during the period? |

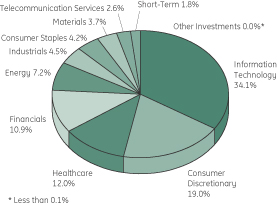

| A. | Changes to the Fund were modest during the year. Fund turnover remained low at 16%. We ended the year with 49 stocks in the Fund, down two names from the start of the year. Technology remains the largest sector in the Fund, comprising 34% of the total. This compares to a weight of 19% in the S&P 500 Index. We think tech has several things going for it: financial strength (large cash balances and free cash flow generation), global diversification (over 50% of the tech sector revenue is outside the U.S.), product cycle growth (e.g., wireless data), and attractive valuation. |

The Fund continues to have an underweight in utilities and consumer staples. We believe valuation looks full in these sectors, particularly after the strong performance last year.

We expect 2012 to be another year where global macro events will create volatility in the market. Further, it is an election year in the U.S., which creates additional uncertainty. We continue to focus on what we believe are financially strong companies with great management teams at attractive valuations. In a slow growth world, we believe the Fund’s collection of above-average growers will do well over the long term.

11

Table of Contents

(Unaudited)

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in units of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended December 31, 2011.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by

$1,000 = 8.6), then multiply the result by the number

given for your class under the heading “Expenses Paid During Period.”

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect any transaction costs, such as sales charges or redemption fees, if any.

July 1, 2011 – December 31, 2011

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($)* | ||||||||||

Actual Fund Return** | 1,000.00 | 939.90 | 1.03 | |||||||||

Hypothetical 5% Return | 1,000.00 | 1,024.15 | 1.07 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.21% (for the period July 1, 2011 - December 31, 2011), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | Actual Fund Return for the six-month period ended December 31, 2011 was: -6.01%. Past performance does not guarantee future results. |

12

Table of Contents

(Unaudited)

Investment Profile

A mutual fund designed for investors who seek long-term growth of capital and future income rather than current income. The Fund seeks its objective by investing in equity securities of U.S. companies, such as common and preferred stocks.

Top Ten Largest Holdings

as of December 31, 2011 as a % of Fair Value(b)(c)

Apple Inc. | 5.04% | |||

Qualcomm Inc. | 4.95% | |||

Visa Inc. | 4.41% | |||

Schlumberger Ltd. | 4.35% | |||

PepsiCo Inc. | 4.23% | |||

The Western Union Co. | 4.21% | |||

Liberty Global Inc. | 3.81% | |||

Express Scripts Inc. | 3.61% | |||

CME Group Inc. | 3.55% | |||

Dover Corp. | 3.49% |

Sector Allocation

as a % of the Fair Value of $1,647,279 (in thousands) as of December 31, 2011.(b)(c)

Morningstar Performance Comparison

Based on average annual returns for periods ended 12/31/11

| One Year | Five Year | Ten Year | ||||||||||

Number of funds in peer group | 1,683 | 1,279 | 804 | |||||||||

Peer group average annual total return | -2.56 | % | 0.34 | % | 1.52 | % | ||||||

Morningstar category in peer group: Large Growth

|

| |||||||||||

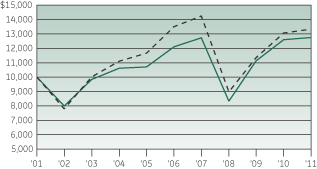

Change in Value of a $10,000 Investment(a)

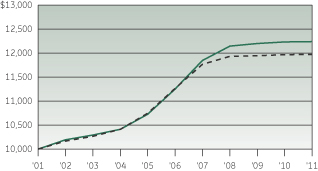

Average Annual Total Return

for the periods ended December 31, 2011

| (Inception date: 05/27/35) | ||||||||||||||||

| One Year | Five Year | Ten Year | Ending value of a $10,000 investment (a) | |||||||||||||

Elfun Trusts | 1.33% | 1.03% | 2.47% | $12,758 | ||||||||||||

S&P 500 Index | 2.11% | -0.25% | 2.92% | $13,340 | ||||||||||||

| (a) | Ending value of a $10,000 investment for the ten-year period or since inception, whichever is less. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

| (c) | Fair Value basis is inclusive of short-term investment in GE Institutional Money Market Fund Investment Class. |

See Notes to Performance on page 1 for further information.

Past performance does not predict future performance. The performance shown on the graph and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

13

Table of Contents

| Elfun Trusts | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

Common Stock — 98.2%† |

| |||||||||

| Air Freight & Logistics — 0.8% | ||||||||||

United Parcel Service Inc. | 170,000 | $ | 12,442 | |||||||

| Application Software — 1.6% | ||||||||||

Intuit Inc. | 430,000 | 22,614 | ||||||||

SuccessFactors Inc. | 100,000 | 3,987 | (a) | |||||||

| 26,601 | ||||||||||

| Asset Management & Custody Banks — 2.8% | ||||||||||

State Street Corp. | 1,140,000 | 45,953 | (e) | |||||||

| Automotive Retail — 0.5% | ||||||||||

O’Reilly Automotive Inc. | 100,000 | 7,995 | (a) | |||||||

| Biotechnology — 3.0% | ||||||||||

Amgen Inc. | 620,000 | 39,810 | ||||||||

Gilead Sciences Inc. | 250,000 | 10,232 | (a) | |||||||

| 50,042 | ||||||||||

| Broadcasting — 1.3% | ||||||||||

Discovery Communications Inc. | 570,000 | 21,489 | (a) | |||||||

| Cable & Satellite — 9.3% | ||||||||||

Comcast Corp. | 1,250,000 | 29,450 | ||||||||

DIRECTV | 1,300,000 | 55,588 | (a) | |||||||

Liberty Global Inc. | 1,590,000 | 62,837 | (a) | |||||||

Sirius XM Radio Inc. | 3,000,000 | 5,460 | (a) | |||||||

| 153,335 | ||||||||||

| Casinos & Gaming — 0.5% | ||||||||||

Las Vegas Sands Corp. | 200,000 | 8,546 | (a) | |||||||

| Communications Equipment — 6.3% | ||||||||||

Cisco Systems Inc. | 1,250,000 | 22,600 | ||||||||

Qualcomm Inc. | 1,490,000 | 81,503 | ||||||||

| 104,103 | ||||||||||

| Computer Hardware — 5.0% | ||||||||||

Apple Inc. | 205,000 | 83,025 | (a) | |||||||

| Number of Shares | Fair Value | |||||||||

| Data Processing & Outsourced Services — 12.2% | ||||||||||

Automatic Data Processing Inc. | 225,000 | $ | 12,152 | |||||||

Paychex Inc. | 1,550,000 | 46,671 | ||||||||

The Western Union Co. | 3,800,000 | 69,388 | ||||||||

Visa Inc. | 715,000 | 72,594 | ||||||||

| 200,805 | ||||||||||

| Diversified Financial Services — 1.4% | ||||||||||

JPMorgan Chase & Co. | 700,000 | 23,275 | ||||||||

| Electronic Manufacturing Services — 0.9% | ||||||||||

Molex Inc. | 760,000 | 15,033 | ||||||||

| Environmental & Facilities Services — 0.2% | ||||||||||

Stericycle Inc. | 45,000 | 3,506 | (a) | |||||||

| Fertilizers & Agricultural Chemicals — 2.8% | ||||||||||

Monsanto Co. | 650,000 | 45,546 | ||||||||

| Healthcare Equipment — 2.0% | ||||||||||

Covidien PLC | 750,000 | 33,758 | ||||||||

| Healthcare Services — 4.8% | ||||||||||

Express Scripts Inc. | 1,330,000 | 59,438 | (a) | |||||||

LIncare Holdings Inc. | 780,000 | 20,054 | ||||||||

| 79,492 | ||||||||||

| Healthcare Supplies — 0.1% | ||||||||||

DENTSPLY International Inc. | 60,000 | 2,099 | ||||||||

| Home Improvement Retail — 2.2% | ||||||||||

Lowe’s Companies Inc. | 1,400,000 | 35,532 | ||||||||

| Homefurnishing Retail — 2.1% | ||||||||||

Bed Bath & Beyond Inc. | 600,000 | 34,782 | (a) | |||||||

| Hotels, Resorts & Cruise Lines — 1.6% | ||||||||||

Carnival Corp. | 810,000 | 26,438 | ||||||||

| Industrial Gases — 1.0% | ||||||||||

Praxair Inc. | 150,000 | 16,035 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

14

Table of Contents

| Elfun Trusts | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| Industrial Machinery — 3.5% | ||||||||||

Dover Corp. | 990,000 | $ | 57,469 | |||||||

| Integrated Oil & Gas — 2.2% | ||||||||||

Chevron Corp. | 105,000 | 11,172 | ||||||||

Exxon Mobil Corp. | 300,000 | 25,428 | ||||||||

| 36,600 | ||||||||||

| Internet Retail — 1.1% | ||||||||||

Amazon.com Inc. | 100,000 | 17,310 | (a) | |||||||

| Internet Software & Services — 6.0% | ||||||||||

Baidu Inc. ADR | 400,000 | 46,588 | (a) | |||||||

eBay Inc. | 1,725,000 | 52,319 | (a) | |||||||

| 98,907 | ||||||||||

| Investment Banking & Brokerage — 1.8% | ||||||||||

The Goldman Sachs Group Inc. | 320,000 | 28,938 | ||||||||

| Oil & Gas Equipment & Services — 4.4% | ||||||||||

Schlumberger Ltd. | 1,050,000 | 71,726 | ||||||||

| Oil & Gas Exploration & Production — 0.6% | ||||||||||

Anadarko Petroleum Corp. | 140,000 | 10,686 | ||||||||

| Pharmaceuticals — 2.0% | ||||||||||

Johnson & Johnson | 500,000 | 32,790 | ||||||||

| Property & Casualty Insurance — 0.5% | ||||||||||

Alleghany Corp. | 30,000 | 8,559 | (a) | |||||||

| Real Estate Services — 0.9% | ||||||||||

CBRE Group Inc. | 925,000 | 14,078 | (a) | |||||||

| Soft Drinks — 4.2% | ||||||||||

PepsiCo Inc. | 1,050,000 | 69,667 | ||||||||

| Specialized Finance — 3.6% | ||||||||||

CME Group Inc. | 240,000 | 58,481 | ||||||||

| Number of Shares | Fair Value | |||||||||

| Specialty Stores — 0.5% | ||||||||||

Dick’s Sporting Goods Inc. | 220,000 | $ | 8,114 | |||||||

| Systems Software — 2.0% | ||||||||||

Microsoft Corp. | 1,250,000 | 32,450 | ||||||||

| Wireless Telecommunication Services — 2.5% | ||||||||||

American Tower Corp. | 700,000 | 42,007 | (a) | |||||||

Total Common Stock | 1,617,614 | |||||||||

Other Investments — 0.0%* |

| |||||||||

GEI Investment Fund | 356 | (k) | ||||||||

Total Investments in Securities | 1,617,970 | |||||||||

Short-Term Investments — 1.8% | ||||||||||

GE Institutional Money Market Fund — Investment | ||||||||||

Class 0.06% | ||||||||||

(Cost $29,309) | 29,309 | (d,k) | ||||||||

Total Investments | 1,647,279 | |||||||||

Other Assets and Liabilities, net — 0.0%* | 117 | |||||||||

|

| |||||||||

NET ASSETS — 100.0% | $ | 1,647,396 | ||||||||

|

| |||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

15

Table of Contents

(Unaudited)

Paul M. Colonna President and Chief Investment Officer – Fixed Income |

Greg Hartch Senior Vice President and Strategy and Business Development Leader | |

Ralph R. Layman President and Chief Investment Officer – Public Equities |

David Wiederecht President and Chief Investment Officer – Investment Strategies | |

The Elfun Diversified Fund is managed by a team of portfolio managers that includes Paul M. Colonna, Greg Hartch, Ralph R. Layman, and David Wiederecht. Mr. Hartch and Mr. Wiederecht are vested with oversight authority for determining asset allocations for the Fund, including the full discretion to allocate the Fund’s assets to sub-adviser(s) retained by GE Asset Management. Mr. Layman manages the equity portion of the Fund and Mr. Colonna manages the fixed income portion of the Fund, each with a team of portfolio managers and analysts. The sub-portfolios underlying the Fund are managed independently of each other, and the portfolio managers have full discretion over their particular sub-portfolio; however, the portfolio management team is collaborative to ensure strict adherence to seek the Fund’s objectives. In addition to oversight authority for asset allocation, Mr. Hartch and Mr. Wiederecht may at times adjust the Fund’s investment exposure through the use of various investment techniques such as investments in derivative instruments. . See portfolio managers’ biographical information beginning on page 113.

| Q. | How did the Elfun Diversified Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended December 31, 2011? |

| A. | For the twelve-month period ended December 31, 2011, the Elfun Diversified Fund returned -2.60%. The S&P 500 Index and the Barclays Capital U.S. Aggregate Bond Index, the Fund’s broad based benchmarks, returned 2.11% and 7.84%, respectively. The Fund’s Morningstar peer group of 963 U.S. Moderate Allocation funds returned an average of -0.40% over the same period. |

| Q. | What market factors affected the Funds performance? |

| A. | It was a very volatile year driven by several macro events both in the U.S. and abroad. In the first half of the year the markets were affected by the |

16

Table of Contents

(Unaudited)

| upheaval of governments in the Middle East and North Africa, a massive earthquake in Japan that affected global supply chains and the bailout of Greece due to their debt crisis. The turmoil intensified in the second half of the year as sovereign debt fears expanded beyond the periphery of Europe. S&P cut the U.S. AAA debt rating due to concerns about the ongoing budget deficit and the ECB had to start buying the sovereign debt of several nations in the secondary market due to the drastic widening of bond yields. High inflation in emerging markets was also a concern throughout most of the year, particularly in China as the government took several steps to stem rising prices in the real estate market. |

| Q. | What were the primary drivers of Fund performance? |

| A. | The primary drivers of the Fund’s performance were its asset allocation and the performance of the underlying strategies within the Fund. During the year the Fund’s average weight to fixed income was approximately 32%. This negatively impacted the Fund’s performance due to the strong performance of the fixed income markets compared to equities. Ongoing concerns throughout the year about Europe’s sovereign debt crisis led many investors to seek safety through investing in U.S. government securities, driving the Barclays Capital U.S. Aggregate Bond Index up 7.84% compared to only a slight rise in the S&P 500 Index of 2.11%, while the MSCI EAFE Index fell 12.14%. Stock selection also negatively impacted the Fund’s performance. The Fund’s large cap growth, mid cap and international equity strategy underperformed their respective benchmarks, offsetting the positive relative performance from the Fund’s fixed income strategy and equity yield strategy. |

| Q. | Were there any significant changes to the Fund during the period? |

| A. | During the year the biggest change in the Fund was the decision to reduce the Fund’s exposure to large cap growth in favor of an equity yield strategy that is focused on dividend yield and dividend growth. As a result, the Fund’s large cap growth exposure was reduced by 6% while its equity yield exposure was increased throughout the year by approximately 5%. This change positively impacted Fund performance. The Fund also reduced its international equity exposure throughout the year by 5% due to increased concerns about the European sovereign debt crisis and slowing economic growth. |

17

Table of Contents

(Unaudited)

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in units of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended December 31, 2011.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000

(for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your class under the heading “Expenses Paid During Period.”

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect any transaction costs, such as sales charges or redemption fees, if any.

July 1, 2011 – December 31, 2011

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($)* | ||||||||||

Actual Fund Return** | 1,000.00 | 938.50 | 1.95 | |||||||||

Hypothetical 5% Return (2.5% for the period) | 1,000.00 | 1,023.19 | 2.04 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.40% (for the period July 1, 2011 - December 31, 2011), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| ** | Actual Fund Return for the six-month period ended December 31, 2011 was: -6.15%. Past performance does not guarantee future results. |

18

Table of Contents

(Unaudited)

Investment Profile

A mutual fund designed for investors who seek the highest total return, composed of income and capital appreciation, as is consistent with prudent investment management and the preservation of capital. The Fund seeks its objective by investing primarily in a combination of U.S. and foreign (non-U.S.) equity and debt securities and cash. The Fund’s asset allocation process utilizes information from GE Asset Management’s Asset Allocation Committee to diversify holdings across these asset classes.

Top Ten Largest Holdings

as of December 31, 2011 as a % of Fair Value(b)(c)

Vangaurd MSCI Emerging Markets | 3.96% | |||

Federal National Mortgage Assoc. 4.50%, | 3.44% | |||

U.S. Treasury Bonds 3.75%, 08/15/41 | 2.20% | |||

U.S. Treasury Notes 0.81%, 11/30/16 | 1.31% | |||

Vangaurd REIT | 1.24% | |||

Federal National Mortgage Assoc. 5.00%, TBA | 1.15% | |||

U.S. Treasury Notes 0.80%, 10/30/16 | 1.10% | |||

Apple Inc. | 1.10% | |||

Cisco Systems Inc. | 0.83% | |||

Microsoft Corp. | 0.82% |

Sector Allocation

as a % of the Fair Value of $215,462 (in thousands) as of December 31, 2011.(b)(c)

Morningstar Performance Comparison

Based on average annual returns for periods ended 12/31/11

| One Year | Five Year | Ten Year | ||||||||||

Number of funds in peer group | 963 | 736 | 393 | |||||||||

Peer group average annual total return | -0.40 | % | 0.98 | % | 3.53 | % | ||||||

Morningstar category in peer group: Moderate Allocation |

| |||||||||||

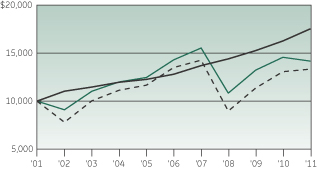

Change in Value of a $10,000 Investment(a)

Average Annual Total Return

for the periods ended December 31, 2011

| (Inception date: 01/01/88) | ||||||||||||||||

| One Year | Five Year | Ten Year | Ending value of a $10,000 investment (a) | |||||||||||||

Elfun Diversified Fund | -2.60% | -0.15% | 3.54% | $14,175 | ||||||||||||

S&P 500 Index | 2.11% | -0.25% | 2.92% | $13,340 | ||||||||||||

Barclays Capital U.S. Aggregate Bond Index | 7.84% | 6.50% | 5.78% | $17,535 | ||||||||||||

| (a) | Ending value of a $10,000 investment for the ten-year period or since inception, whichever is less. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

| (c) | Fair Value basis is inclusive of short-term investment in GE Institutional Money Market Fund Investment Class. |

See Notes to Performance on page 1 for further information.

Past performance does not predict future performance. The performance shown on the graph and tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

19

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

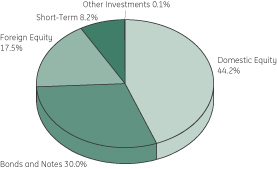

Domestic Equity – 39.9%† | ||||||||||

| Advertising — 0.5% | ||||||||||

Omnicom Group Inc. | 23,144 | $ | 1,032 | |||||||

| Aerospace & Defense — 0.9% | ||||||||||

Alliant Techsystems Inc. | 1,663 | 95 | ||||||||

Hexcel Corp. | 13,991 | 339 | (a) | |||||||

Honeywell International Inc. | 17,377 | 945 | ||||||||

Rockwell Collins Inc. | 5,891 | 326 | ||||||||

United Technologies Corp. | 2,718 | 199 | ||||||||

| 1,904 | ||||||||||

| Agricultural Products — 0.2% | ||||||||||

Archer-Daniels-Midland Co. | 14,000 | 400 | ||||||||

| Air Freight & Logistics — 0.5% | ||||||||||

FedEx Corp. | 3,862 | 323 | ||||||||

United Parcel Service Inc. | 8,809 | 645 | ||||||||

Uti Worldwide Inc. | 5,656 | 75 | ||||||||

| 1,043 | ||||||||||

| Apparel Retail — 0.1% | ||||||||||

Urban Outfitters Inc. | 6,004 | 165 | (a) | |||||||

| Apparel, Accessories & Luxury Goods — 0.2% | ||||||||||

Coach Inc. | 6,468 | 395 | ||||||||

Michael Kors Holdings Ltd. | 749 | 20 | (a) | |||||||

| 415 | ||||||||||

| Application Software — 0.3% | ||||||||||

Citrix Systems Inc. | 4,592 | 279 | (a) | |||||||

SuccessFactors Inc. | 8,472 | 338 | (a) | |||||||

| 617 | ||||||||||

| Asset Management & Custody Banks — 1.2% | ||||||||||

Affiliated Managers Group Inc. | 3,717 | 357 | (a) | |||||||

Ameriprise Financial Inc. | 13,538 | 672 | ||||||||

Invesco Ltd. | 35,989 | 723 | ||||||||

State Street Corp. | 19,465 | 785 | (e) | |||||||

| 2,537 | ||||||||||

| Number of Shares | Fair Value | |||||||||

| Auto Parts & Equipment — 0.1% | ||||||||||

Johnson Controls Inc. | 5,117 | $ | 160 | |||||||

| Automotive Retail — 0.2% | ||||||||||

O’Reilly Automotive Inc. | 4,325 | 346 | (a) | |||||||

| Biotechnology — 1.1% | ||||||||||

Alexion Pharmaceuticals Inc. | 4,923 | 352 | ||||||||

Amgen Inc. | 13,927 | 894 | ||||||||

Gilead Sciences Inc. | 17,321 | 709 | (a) | |||||||

Human Genome Sciences Inc. | 7,040 | 52 | (a) | |||||||

Incyte Corp Ltd | 7,087 | 106 | (a) | |||||||

Vertex Pharmaceuticals Inc. | 4,233 | 141 | (a) | |||||||

| 2,254 | ||||||||||

| Brewers — 0.1% | ||||||||||

Molson Coors Brewing Co. | 6,497 | 283 | ||||||||

| Broadcasting — 0.1% | ||||||||||

Discovery Communications | 1,814 | 74 | (a) | |||||||

Discovery Communications | 3,042 | 115 | (a) | |||||||

| 189 | ||||||||||

| Cable & Satellite — 0.4% | ||||||||||

DIRECTV | 8,531 | 365 | (a) | |||||||

Liberty Global Inc. | 8,712 | 345 | (a) | |||||||

Sirius XM Radio Inc. | 11,394 | 21 | (a) | |||||||

| 731 | ||||||||||

| Casinos & Gaming — 0.3% | ||||||||||

Las Vegas Sands Corp. | 7,619 | 326 | (a) | |||||||

Penn National Gaming Inc. | 7,146 | 272 | (a) | |||||||

| 598 | ||||||||||

| Coal & Consumable Fuels — 0.1% | ||||||||||

Alpha Natural Resources Inc. | 2,400 | 49 | (a) | |||||||

Peabody Energy Corp. | 3,826 | 127 | ||||||||

| 176 | ||||||||||

| Communications Equipment — 1.6% | ||||||||||

Cisco Systems Inc. | 98,519 | 1,781 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

20

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

Juniper Networks Inc. | 8,650 | $ | 177 | (a) | ||||||

Qualcomm Inc. | 26,672 | 1,459 | ||||||||

| 3,417 | ||||||||||

| Computer Hardware — 1.2% | ||||||||||

Apple Inc. | 5,856 | 2,371 | (a) | |||||||

Hewlett-Packard Co. | 5,793 | 149 | ||||||||

| 2,520 | ||||||||||

| Computer Storage & Peripherals — 0.1% | ||||||||||

Synaptics Inc. | 8,342 | 252 | (a) | |||||||

| Construction & Engineering — 0.1% | ||||||||||

Quanta Services Inc. | 10,593 | 228 | (a) | |||||||

| Construction & Farm Machinery & Heavy Trucks — 0.1% | ||||||||||

Cummins Inc. | 1,970 | 173 | ||||||||

Deere & Co. | 965 | 75 | ||||||||

| 248 | ||||||||||

| Consumer Finance — 0.3% | ||||||||||

American Express Co. | 12,960 | 612 | ||||||||

Discover Financial Services | 4,453 | 107 | ||||||||

| 719 | ||||||||||

| Data Processing & Outsourced Services — 0.6% | ||||||||||

Automatic Data Processing Inc. | 2,912 | 157 | ||||||||

The Western Union Co. | 21,243 | 388 | ||||||||

Visa Inc. | 6,856 | 696 | ||||||||

| 1,241 | ||||||||||

| Department Stores — 0.1% | ||||||||||

Macy’s Inc. | 8,104 | 261 | ||||||||

| Distributors — 0.1% | ||||||||||

Genuine Parts Co. | 3,151 | 193 | ||||||||

| Diversified Chemicals — 0.1% | ||||||||||

EI du Pont de Nemours & Co. | 3,636 | 166 | ||||||||

| Diversified Financial Services — 1.2% | ||||||||||

Bank of America Corp. | 44,194 | 245 | ||||||||

Comerica Inc. | 12,503 | 323 | ||||||||

| Number of Shares | Fair Value | |||||||||

JPMorgan Chase & Co. | 33,769 | $ | 1,123 | |||||||

US Bancorp | 3,689 | 100 | ||||||||

Wells Fargo & Co. | 25,931 | 715 | ||||||||

| 2,506 | ||||||||||

| Diversified Metals & Mining — 0.2% | ||||||||||

Freeport-McMoRan Copper & Gold Inc. | 9,404 | 346 | ||||||||

Molycorp Inc. | 2,081 | 50 | (a) | |||||||

| 396 | ||||||||||

| Drug Retail — 0.2% | ||||||||||

CVS Caremark Corp. | 10,428 | 425 | ||||||||

| Electric Utilities — 0.8% | ||||||||||

FirstEnergy Corp. | 5,445 | 241 | ||||||||

ITC Holdings Corp. | 8,026 | 609 | ||||||||

NextEra Energy Inc. | 5,986 | 364 | ||||||||

The Southern Co. | 7,875 | 365 | ||||||||

| 1,579 | ||||||||||

| Electrical Components & Equipment — 0.5% | ||||||||||

Cooper Industries PLC | 12,946 | 701 | ||||||||

Emerson Electric Co. | 6,309 | 294 | ||||||||

| 995 | ||||||||||

| Environmental & Facilities Services — 0.1% | ||||||||||

Stericycle Inc. | 2,296 | 179 | (a) | |||||||

| Fertilizers & Agricultural Chemicals — 0.4% | ||||||||||

Intrepid Potash Inc. | 3,984 | 90 | (a) | |||||||

Monsanto Co. | 10,795 | 757 | ||||||||

| 847 | ||||||||||

| General Merchandise Stores — 0.4% | ||||||||||

Target Corp. | 15,182 | 777 | ||||||||

| Healthcare Equipment — 0.8% | ||||||||||

Baxter International Inc. | 3,562 | 176 | ||||||||

Covidien PLC | 24,754 | 1,114 | ||||||||

Gen-Probe Inc. | 1,950 | 115 | (a) | |||||||

Masimo Corp. | 9,971 | 186 | (a) | |||||||

ResMed Inc. | 7,285 | 185 | (a) | |||||||

| 1,776 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

21

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| Healthcare Facilities — 0.2% | ||||||||||

HCA Holdings Inc. | 8,207 | $ | 181 | (a) | ||||||

Universal Health Services Inc. | 6,216 | 242 | ||||||||

| 423 | ||||||||||

| Healthcare Services — 0.8% | ||||||||||

Catalyst Health Solutions Inc. | 7,154 | 372 | (a) | |||||||

DaVita Inc. | 1,063 | 81 | (a) | |||||||

Express Scripts Inc. | 23,237 | 1,038 | (a) | |||||||

Omnicare Inc. | 2,897 | 100 | ||||||||

| 1,591 | ||||||||||

| Home Building — 0.1% | ||||||||||

MDC Holdings Inc. | 7,500 | 132 | ||||||||

| Home Entertainment Software — 0.1% | ||||||||||

Activision Blizzard Inc. | 23,912 | 295 | ||||||||

| Home Furnishing Retail — 0.2% | ||||||||||

Bed Bath & Beyond Inc. | 6,206 | 360 | (a) | |||||||

| Home Improvement Retail — 0.5% | ||||||||||

Lowe’s Companies Inc. | 15,685 | 398 | ||||||||

The Home Depot Inc. | 14,601 | 613 | ||||||||

| 1,011 | ||||||||||

| Hotels, Resorts & Cruise Lines — 0.1% | ||||||||||

Carnival Corp. | 4,654 | 152 | ||||||||

Royal Caribbean Cruises Ltd. | 6,089 | 151 | ||||||||

| 303 | ||||||||||

| Household Products — 0.7% | ||||||||||

Kimberly-Clark Corp. | 3,845 | 283 | ||||||||

The Clorox Co. | 5,629 | 375 | ||||||||

The Procter & Gamble Co. | 13,343 | 890 | ||||||||

| 1,548 | ||||||||||

| Independent Power Producers & Energy Traders — 0.5% | ||||||||||

Calpine Corp. | 22,440 | 366 | (a) | |||||||

The AES Corp. | 64,484 | 764 | ||||||||

| 1,130 | ||||||||||

| Number of Shares | Fair Value | |||||||||

| Industrial Gases — 0.5% | ||||||||||

Praxair Inc. | 9,519 | $ | 1,018 | |||||||

| Industrial Machinery — 0.3% | ||||||||||

Eaton Corp. | 7,373 | 321 | ||||||||

Harsco Corp. | 13,330 | 274 | ||||||||

| 595 | ||||||||||

| Insurance Brokers — 0.1% | ||||||||||

Marsh & McLennan Companies Inc. | 6,358 | 201 | ||||||||

| Integrated Oil & Gas — 1.7% | ||||||||||

Chevron Corp. | 14,680 | 1,562 | ||||||||

ConocoPhillips | 7,959 | 580 | ||||||||

Exxon Mobil Corp. | 6,290 | 533 | ||||||||

Hess Corp. | 5,506 | 312 | ||||||||

Occidental Petroleum Corp. | 7,153 | 670 | ||||||||

| 3,657 | ||||||||||

| Integrated Telecommunication Services — 0.6% | ||||||||||

AT&T Inc. | 22,183 | 671 | ||||||||

Verizon Communications Inc. | 12,589 | 505 | ||||||||

Windstream Corp. | 7,382 | 87 | ||||||||

| 1,263 | ||||||||||

| Internet Retail — 0.0%* | ||||||||||

Amazon.com Inc. | 485 | 84 | (a) | |||||||

HomeAway Inc. | 519 | 12 | (a) | |||||||

| 96 | ||||||||||

| Internet Software & Services — 0.9% | ||||||||||

Equinix Inc. | 6,170 | 626 | (a) | |||||||

Google Inc. | 1,426 | 921 | (a) | |||||||

MercadoLibre Inc. | 2,878 | 229 | ||||||||

Monster Worldwide Inc. | 16,978 | 135 | (a) | |||||||

| 1,911 | ||||||||||

| Investment Banking & Brokerage — 0.2% | ||||||||||

The Goldman Sachs Group Inc. | 4,692 | 424 | ||||||||

| IT Consulting & Other Services — 1.0% | ||||||||||

Cognizant Technology Solutions Corp. | 5,869 | 377 | (a) | |||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

22

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

International Business Machines Corp. | 8,985 | $ | 1,652 | (h) | ||||||

| 2,029 | ||||||||||

| Life & Health Insurance — 0.5% | ||||||||||

MetLife Inc. | 16,069 | 501 | ||||||||

Prudential Financial Inc. | 10,522 | 527 | ||||||||

| 1,028 | ||||||||||

| Life Sciences Tools & Services — 0.5% | ||||||||||

Covance Inc. | 3,857 | 176 | (a) | |||||||

Illumina Inc. | 5,427 | 165 | (a) | |||||||

Mettler-Toledo International Inc. | 1,441 | 213 | (a) | |||||||

PerkinElmer Inc. | 14,696 | 294 | ||||||||

Thermo Fisher Scientific Inc. | 5,642 | 254 | (a) | |||||||

| 1,102 | ||||||||||

| Managed Healthcare — 0.0%* | ||||||||||

UnitedHealth Group Inc. | 1,545 | 78 | ||||||||

| Movies & Entertainment — 0.8% | ||||||||||

Liberty Media Corporation — Capital | 1,834 | 143 | (a) | |||||||

The Walt Disney Co. | 14,483 | 543 | ||||||||

Time Warner Inc. | 26,066 | 942 | ||||||||

| 1,628 | ||||||||||

| Multi-Line Insurance — 0.2% | ||||||||||

Hartford Financial Services Group Inc. | 4,827 | 78 | ||||||||

HCC Insurance Holdings Inc. | 14,749 | 406 | ||||||||

| 484 | ||||||||||

| Multi-Utilities — 0.4% | ||||||||||

Dominion Resources Inc. | 10,900 | 579 | ||||||||

Public Service Enterprise Group Inc. | 2,494 | 82 | ||||||||

Xcel Energy Inc. | 4,603 | 127 | ||||||||

| 788 | ||||||||||

| Office REITs — 0.1% | ||||||||||

Douglas Emmett Inc. | 8,839 | 161 | ||||||||

SL Green Realty Corp. | 1,846 | 123 | ||||||||

| 284 | ||||||||||

| Number of Shares | Fair Value | |||||||||

| Oil & Gas Drilling — 0.1% | ||||||||||

Noble Corp. | 6,752 | $ | 204 | |||||||

| Oil & Gas Equipment & Services — 1.0% | ||||||||||

McDermott International Inc. | 13,768 | 158 | (a) | |||||||

National Oilwell Varco Inc. | 2,582 | 176 | ||||||||

Schlumberger Ltd. | 23,693 | 1,619 | ||||||||

Weatherford International Ltd. | 11,174 | 164 | (a) | |||||||

| 2,117 | ||||||||||

| Oil & Gas Exploration & Production — 0.9% | ||||||||||

Anadarko Petroleum Corp. | 11,900 | 909 | ||||||||

Apache Corp. | 1,821 | 165 | ||||||||

Forest Oil Corp. | 5,773 | 78 | (a) | |||||||

Pioneer Natural Resources Co. | 2,637 | 236 | ||||||||

Range Resources Corp. | 3,240 | 201 | ||||||||

Southwestern Energy Co. | 8,803 | 281 | (a) | |||||||

Ultra Petroleum Corp. | 2,360 | 70 | (a) | |||||||

| 1,940 | ||||||||||

| Oil & Gas Refining & Marketing — 0.1% | ||||||||||

Marathon Petroleum Corp. | 4,631 | 154 | ||||||||

| Oil & Gas Storage & Transportation — 0.4% | ||||||||||

El Paso Corp. | 11,945 | 317 | ||||||||

Spectra Energy Corp. | 15,030 | 462 | ||||||||

The Williams Companies Inc. | 4,827 | 159 | ||||||||

| 938 | ||||||||||

| Packaged Foods & Meats — 1.0% | ||||||||||

ConAgra Foods Inc. | 9,173 | 242 | ||||||||

General Mills Inc. | 4,852 | 196 | ||||||||

Kraft Foods Inc. | 33,670 | 1,258 | ||||||||

McCormick & Company Inc. | 4,017 | 203 | ||||||||

Mead Johnson Nutrition Co. | 2,809 | 193 | ||||||||

| 2,092 | ||||||||||

| Pharmaceuticals — 1.8% | ||||||||||

Bristol-Myers Squibb Co. | 20,066 | 707 | ||||||||

Johnson & Johnson | 18,337 | 1,203 | ||||||||

Merck & Company Inc. | 8,639 | 326 | ||||||||

Pfizer Inc. | 73,649 | 1,594 | ||||||||

| 3,830 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

23

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| Property & Casualty Insurance — 0.9% | ||||||||||

ACE Ltd. | 17,686 | $ | 1,241 | |||||||

The Chubb Corp. | 8,155 | 564 | ||||||||

| 1,805 | ||||||||||

| Railroads — 0.1% | ||||||||||

Union Pacific Corp. | 2,038 | 216 | ||||||||

| Real Estate Services — 0.1% | ||||||||||

CBRE Group Inc. (REIT) | 16,304 | 248 | (a,h) | |||||||

| Regional Banks — 0.0%* | ||||||||||

Zions Bancorporation | 6,189 | 101 | ||||||||

| Reinsurance — 0.2% | ||||||||||

PartnerRe Ltd. | 4,008 | 257 | ||||||||

RenaissanceRe Holdings Ltd. | 2,607 | 194 | ||||||||

| 451 | ||||||||||

| Research & Consulting Services — 0.3% | ||||||||||

FTI Consulting Inc. | 3,719 | 158 | (a) | |||||||

IHS Inc. | 3,655 | 315 | (a) | |||||||

Nielsen Holdings N.V. | 5,343 | 159 | (a) | |||||||

| 632 | ||||||||||

| Restaurants — 0.4% | ||||||||||

Darden Restaurants Inc. | 2,427 | 111 | ||||||||

McDonald’s Corp. | 6,406 | 643 | ||||||||

| 754 | ||||||||||

| Retail REITs — 0.1% | ||||||||||

Simon Property Group Inc. | 1,311 | 169 | ||||||||

| Security & Alarm Services — 0.2% | ||||||||||

Corrections Corporation of America | 20,327 | 414 | (a) | |||||||

| Semiconductor Equipment — 0.0%* | ||||||||||

KLA-Tencor Corp. | 2,135 | 103 | ||||||||

| Semiconductors — 1.1% | ||||||||||

Altera Corp. | 4,634 | 172 | ||||||||

Cree Inc. | 1,952 | 43 | (a) | |||||||

| Number of Shares | Fair Value | |||||||||

Hittite Microwave Corp. | 5,076 | $ | 251 | (a) | ||||||

Intel Corp. | 26,156 | 634 | (h) | |||||||

Marvell Technology Group Ltd. | 15,670 | 217 | (a) | |||||||

Microchip Technology Inc. | 6,872 | 251 | ||||||||

Texas Instruments Inc. | 22,269 | 648 | ||||||||

| 2,216 | ||||||||||

| Soft Drinks — 1.0% | ||||||||||

Coca-Cola Enterprises Inc. | 19,723 | 509 | ||||||||

PepsiCo Inc. | 22,793 | 1,512 | ||||||||

| 2,021 | ||||||||||

| Specialized Finance — 0.4% | ||||||||||

CBOE Holdings Inc. | 5,727 | 148 | ||||||||

CME Group Inc. | 2,239 | 545 | ||||||||

MSCI Inc. | 3,828 | 126 | (a) | |||||||

| 819 | ||||||||||

| Specialized REITs — 0.1% | ||||||||||

Public Storage | 1,456 | 196 | ||||||||

Rayonier Inc. | 2,266 | 101 | ||||||||

| 297 | ||||||||||

| Specialty Chemicals — 0.2% | ||||||||||

Albemarle Corp. | 976 | 50 | ||||||||

Celanese Corp. | 1,841 | 82 | ||||||||

Cytec Industries Inc. | 2,560 | 114 | ||||||||

Ecolab Inc. | 3,762 | 217 | ||||||||

| 463 | ||||||||||

| Specialty Stores — 0.1% | ||||||||||

Dick’s Sporting Goods Inc. | 4,556 | 168 | ||||||||

| Steel — 0.5% | ||||||||||

Allegheny Technologies Inc. | 21,587 | 1,032 | ||||||||

Steel Dynamics Inc. | 6,126 | 81 | ||||||||

| 1,113 | ||||||||||

| Systems Software — 1.4% | ||||||||||

Microsoft Corp. | 68,420 | 1,777 | (h) | |||||||

Oracle Corp. | 32,859 | 842 | ||||||||

Rovi Corp. | 9,712 | 239 | (a) | |||||||

| 2,858 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

24

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| Thrifts & Mortgage Finance — 0.3% | ||||||||||

BankUnited Inc. | 6,043 | $ | 133 | |||||||

People’s United Financial Inc. | 38,023 | 488 | ||||||||

| 621 | ||||||||||

| Tobacco — 0.2% | ||||||||||

Philip Morris International Inc. | 6,095 | 478 | ||||||||

| Trading Companies & Distributors — 0.1% | ||||||||||

MSC Industrial Direct Company Inc. | 3,960 | 283 | ||||||||

| Water Utilities — 0.1% | ||||||||||

American Water Works Company Inc. | 4,271 | 136 | ||||||||

| Wireless Telecommunication Services — 0.6% | ||||||||||

American Tower Corp. | 13,537 | 813 | (a) | |||||||

NII Holdings Inc. | 21,551 | 459 | (a) | |||||||

| 1,272 | ||||||||||

Total Domestic Equity | 83,867 | |||||||||

Foreign Equity — 17.9% |

| |||||||||

| Common Stock — 17.7% | ||||||||||

| Advertising — 0.1% | ||||||||||

WPP PLC | 30,245 | 317 | ||||||||

| Aerospace & Defense — 0.4% | ||||||||||

CAE Inc. | 17,264 | 168 | ||||||||

European Aeronautic Defence and Space Company N.V. | 5,063 | 159 | ||||||||

Safran S.A. | 17,351 | 523 | ||||||||

| 850 | ||||||||||

| Apparel, Accessories & Luxury Goods — 0.3% | ||||||||||

Adidas AG | 4,537 | 296 | ||||||||

LVMH Moet Hennessy Louis Vuitton S.A. | 1,955 | 278 | ||||||||

| 574 | ||||||||||

| Number of Shares | Fair Value | |||||||||

| Application Software — 0.2% | ||||||||||

SAP AG | 8,186 | $ | 434 | |||||||

| Automobile Manufacturers — 0.6% | ||||||||||

Daimler AG | 1,653 | 73 | ||||||||

Hyundai Motor Co. | 1,776 | 328 | (a) | |||||||

Suzuki Motor Corp. | 32,066 | 663 | ||||||||

Toyota Motor Corp. | 4,430 | 148 | ||||||||

| 1,212 | ||||||||||

| Brewers — 0.1% | ||||||||||

Carlsberg A/S | 1,529 | 108 | ||||||||

| Building Products — 0.1% | ||||||||||

Daikin Industries Ltd. | 9,400 | 258 | ||||||||

| Communications Equipment — 0.2% | ||||||||||

Telefonaktiebolaget LM Ericsson | 35,106 | 361 | ||||||||

| Construction & Engineering — 0.2% | ||||||||||

Larsen & Toubro Ltd. | 6,676 | 125 | ||||||||

VInci S.A. | 5,500 | 241 | ||||||||

| 366 | ||||||||||

| Distillers & Vintners — 0.4% | ||||||||||

Diageo PLC | 32,276 | 705 | ||||||||

Diageo PLC ADR | 1,986 | 174 | ||||||||

| 879 | ||||||||||

| Diversified Capital Markets — 0.1% | ||||||||||

Credit Suisse Group AG | 8,490 | 200 | ||||||||

| Diversified Financial Services — 1.5% | ||||||||||

Banco Santander S.A. | 33,543 | 256 | ||||||||

Bank of China Ltd. | 457,669 | 169 | ||||||||

BNP Paribas S.A. | 11,648 | 459 | ||||||||

HSBC Holdings PLC | 103,294 | 788 | ||||||||

ICICI Bank Ltd. | 11,718 | 151 | ||||||||

ING Groep N.V. | 38,587 | 279 | (a) | |||||||

Lloyds Banking Group PLC | 696,054 | 280 | (a) | |||||||

Standard Chartered PLC | 20,249 | 443 | ||||||||

United Overseas Bank Ltd. | 31,694 | 373 | ||||||||

| 3,198 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

25

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

| Diversified Metals & Mining — 0.9% | ||||||||||

Antofagasta PLC | 4,841 | $ | 91 | |||||||

BHP Billiton PLC | 22,516 | 657 | ||||||||

First Quantum Minerals Ltd. | 3,471 | 68 | ||||||||

Lynas Corporation Ltd. | 263,916 | 283 | (a) | |||||||

Rio Tinto PLC | 13,689 | 665 | ||||||||

Xstrata PLC | 7,029 | 107 | ||||||||

| 1,871 | ||||||||||

| Diversified Real Estate Activities — 0.2% | ||||||||||

Sumitomo Realty & Development Company Ltd. (REIT) | 14,000 | 245 | ||||||||

Wharf Holdings Ltd. | 44,625 | 202 | ||||||||

| 447 | ||||||||||

| Diversified Support Services — 0.3% | ||||||||||

Aggreko PLC | 7,727 | 242 | ||||||||

Brambles Ltd. | 52,063 | 382 | ||||||||

| 624 | ||||||||||

| Electric Utilities — 0.1% | ||||||||||

Power Grid Corporation of India Ltd. | 90,819 | 171 | ||||||||

Reliance Infrastructure Ltd. | 4,712 | 30 | ||||||||

| 201 | ||||||||||

| Electrical Components & Equipment — 0.1% | ||||||||||

Schneider Electric S.A. | 2,047 | 108 | ||||||||

| Electronic Components — 0.1% | ||||||||||

Delta Electronics Inc. | 60,000 | 143 | ||||||||

| Electronic Equipment & Instruments — 0.1% | ||||||||||

Hexagon AB | 16,223 | 244 | ||||||||

| Fertilizers & Agricultural Chemicals — 0.7% | ||||||||||

Potash Corporation of Saskatchewan Inc. †† | 13,382 | 554 | ||||||||

Potash Corporation of Saskatchewan Inc. †† | 5,310 | 219 | ||||||||

Sociedad Quimica y Minera de Chile S.A. ADR | 1,017 | 55 | ||||||||

| Number of Shares | Fair Value | |||||||||

Syngenta AG | 1,866 | $ | 549 | |||||||

| 1,377 | ||||||||||

| Food Retail — 0.2% | ||||||||||

Koninklijke Ahold N.V. | 6,382 | 86 | ||||||||

Tesco PLC | 50,438 | 316 | ||||||||

| 402 | ||||||||||

| Gold — 0.2% | ||||||||||

Barrick Gold Corp. | 1,064 | 48 | ||||||||

Goldcorp Inc. | 1,447 | 64 | ||||||||

Kinross Gold Corp. | 33,911 | 387 | ||||||||

| 499 | ||||||||||

| Healthcare Services — 0.2% | ||||||||||

Fresenius SE & Company KGaA | 4,821 | 447 | ||||||||

| Healthcare Supplies — 0.2% | ||||||||||

Cie Generale d’Optique Essilor International S.A. | 7,395 | 524 | ||||||||

| Heavy Electrical Equipment — 0.1% | ||||||||||

ABB Ltd. ADR | 5,794 | 109 | ||||||||

| Hotels, Resorts & Cruise Lines — 0.0%* | ||||||||||

Accor S.A. | 858 | 22 | ||||||||

| Household Products — 0.5% | ||||||||||

Reckitt Benckiser Group PLC | 10,994 | 543 | ||||||||

Unicharm Corp. | 10,600 | 523 | ||||||||

| 1,066 | ||||||||||

| Human Resource & Employment Services — 0.1% | ||||||||||

The Capita Group PLC | 14,940 | 146 | ||||||||

| Hypermarkets & Super Centers — 0.1% | ||||||||||

Metro AG | 3,458 | 127 | ||||||||

| Industrial Conglomerates — 0.6% | ||||||||||

Hutchison Whampoa Ltd. | 36,356 | 306 | ||||||||

Koninklijke Philips Electronics N.V. | 10,218 | 216 | ||||||||

Siemens AG | 4,923 | 473 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

26

Table of Contents

| Elfun Diversified Fund | (in thousands) — December 31, 2011 |

| Number of Shares | Fair Value | |||||||||

Siemens AG ADR | 2,322 | $ | 222 | |||||||

| 1,217 | ||||||||||

| Industrial Gases — 0.4% | ||||||||||

Linde AG | 5,853 | 873 | ||||||||

OCI Materials Company Ltd. | 680 | 47 | (a) | |||||||

| 920 | ||||||||||

| Industrial Machinery — 0.5% | ||||||||||

FANUC Corp. | 3,000 | 459 | ||||||||

Mitsubishi Heavy Industries Ltd. | 29,000 | 124 | ||||||||

SMC Corp. | 1,700 | 274 | ||||||||

Vallourec S.A. | 4,877 | 318 | ||||||||

| 1,175 | ||||||||||

| Integrated Oil & Gas — 1.8% | ||||||||||

BG Group PLC | 21,389 | 458 | (a) | |||||||

Cenovus Energy Inc. | 2,063 | 69 | ||||||||

China Petroleum & Chemical Corp. | 134,167 | 141 | ||||||||