UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

¨ | Preliminary Proxy Statement | |

¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

¨ | Definitive Proxy Statement | |

x | Definitive Additional Materials | |

¨ | Soliciting Material Pursuant to §240.14a-12 | |

SILICON STORAGE TECHNOLOGY, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Explanatory Note

Attached is a presentation given by Silicon Storage Technology, Inc. to RiskMetrics Group on March 16, 2010.

S i l i c o n S t o r a g e T e c h n o l o g y, I n c. S i l i c o n S t o r a g e T e c h n o l o g y, I n c. www.SuperFlash.com Overview of SST Proposed Sale to Microchip March 16, 2010 |

SST Proprietary & Confidential 2 Forward-Looking Information Is Subject to Risk & Uncertainty Statements about the expected timing, completion and effects of the proposed merger, and all other statements in this presentation other than historical facts, constitute forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The audience is cautioned not to place undue reliance on these forward-looking statements, each of which is qualified in its entirety by reference to the following cautionary statements. Forward-looking statements speak only as of the date hereof and are based on current expectations and involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially from those projected in the forward-looking statements. A number of the matters discussed herein that are not historical or current facts deal with potential future circumstances and developments, in particular, whether and when the transactions contemplated by the merger agreement will be consummated. The discussion of such matters is qualified by the inherent risks and uncertainties surrounding future expectations generally, and also may materially differ from actual future experience involving any one or more of such matters. Such risks and uncertainties include: any conditions imposed on the parties in connection with consummation of the transaction described herein; approval of the merger by our shareholders; satisfaction of various other conditions to the closing of the transactions described herein; and the risks that are described from time to time in our reports filed with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2008 and our Quarterly Report on Form 10-Q for the quarter ended September 30, 2009. |

SST Proprietary & Confidential 3 Additional Information and Where To Find It In connection with the proposed merger with Microchip, Silicon Storage Technology, Inc. filed a definitive proxy statement with the Securities and Exchange Commission (the “SEC”) on March 1, 2010. INVESTORS AND SHAREHOLDERS ARE ADVISED TO READ THE DEFINITIVE PROXY STATEMENT AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT SST AND THE PROPOSED TRANSACTION WITH MICROCHIP. The definitive proxy statement was mailed to Silicon Storage Technology, Inc. shareholders on March 3, 2010. Investors and shareholders may obtain a free copy of these documents and other documents filed by Silicon Storage Technology, Inc. at the SEC’s web site at www.sec.gov and at the Investor section of our website at www.SST.com. The proxy statement and such other documents may also be obtained for free from Silicon Storage Technology, Inc. by directing such request to Silicon Storage Technology, Inc., Attention: Ricky Gradwohl, 1020 Kifer Road, Sunnyvale, California 94086, Telephone: 408/735-9110. Silicon Storage Technology, Inc. and its directors and executive officers may be deemed to be participants in the solicitation of proxies from its shareholders in connection with the proposed merger with Microchip. Information about Silicon Storage Technology, Inc.’s directors and executive officers is set forth in Silicon Storage Technology, Inc.’s proxy statement on Schedule 14A filed with the SEC on April 30, 2009. Additional information regarding the interests of participants in the solicitation of proxies in connection with the proposed merger with Microchip in included in the definitive proxy statement with respect to the proposed merger with Microchip that Silicon Storage Technology, Inc. filed with the SEC on March 1, 2010. |

SST Proprietary & Confidential 4 Microchip Transaction Provides Superior Shareholder Value Per-Share Consideration: Total Value (1) : Valuation Premium: Strategic Buyer: Transaction Timing: Merger Agreement Terms: Estimated Closing Date: • $3.05 Per Share Cash Offer – No Financing Contingency • $300.9 Million • 64.0% to $1.86 (Nov. 12, Prior to Prophet Equity Offer) • 45.2% to $2.10 (Nov. 13, Prophet Equity Bid) • 134.6% to $1.30 (52-Week Low, Prior to Prophet Equity Bid) • Microchip Technology, Inc. • Market Capitalization: $5.2 Billion; Net Cash: $1.2 Billion • SST Shareholder Vote: April 8, 2010 • 25.5% of Shareholders Committed to Vote for Highest-Priced Deal • Specific Performance • Straightforward Strategic Cash Merger • No further regulatory or HSR approvals required (1) Based on Diluted Shares Outstanding as of 2/28/2010: 98,655,330 and excluding additional 19,148,150 shares issued to Microchip on March 8, 2010. The Microchip transaction is the culmination of a 1½ years-long strategic review process and extensive go-shop period involving outreach to 145 prospective acquirers SST’s Board believes that Microchip’s increased $3.05 per-share cash offer provides shareholders with greater and more certain value than any other alternative the Board considered SST’s Board of Directors recommends shareholders vote FOR the $3.05 Microchip Offer • April 8, 2010 |

SST Proprietary & Confidential 5 Involved Parties Business Description: Exchange & Ticker Symbol: Market Capitalization (1) : Date of IPO: Employees: NOR and NAND flash memory provider NASDAQ: SSTI $303.9 Million November 21, 1995 576 Supplier of microcontroller, analog and memory products NASDAQ: MCHP $5.2 Billion March 19, 1993 4,895 (1) Based on Diluted Shares Outstanding as of 2/28/2010: 98,655,330 and excluding additional 19,148,150 shares issued to Microchip on March 8, 2010. |

SST Proprietary & Confidential 6 Company Overview Company Overview Small/Micro-Cap company ($165M NOR Revenue) #5 Player in NOR Memory Market with 4% Market Share Continued R&D investment necessary to refresh or diversify outdated product portfolio, and to support both memory and licensing businesses Historic product diversification efforts: All-in-One Memory, FlashMate, and Melody Wing product lines (all ended) Historically struggles with profitability; GM ~30% makes R&D difficult to subsidize Illiquid stock with low trading volume and no research coverage Public company costs No manufacturing facilities as opposed to larger competitors As part of the strategic review process, the Board determined a sale would provide greater and more certain value to shareholders than a liquidation or buyback |

SST Proprietary & Confidential 7 Highly Competitive Market Large-scale competitors all with fab capabilities Steadily declining ASP; SST experienced ASP CAGR of (20.1%) over the last 3 years Intel and STMicroelectronics exited NOR Flash product line in Mar. ’09 with sale of Numonyx (#1 Player, $1.5B Revenue) to Micron AMD and Fujitsu also divested NOR Flash product line with formation of Spansion (#2 Player, $1.3B Revenue), which filed for Chapter 11 Mar. ’09 Vulnerability to macro trends and volatility NAND encroaching on high densities (Samsung, SanDisk); intense competition on low densities from Taiwanese players (Macronix, Winbond) Market Overview |

SST Proprietary & Confidential 8 Process Designed to Maximize Shareholder Value Provides Significant Premium to Public Market Valuation (1) : 64.0% - Premium to Prophet Equity Bid of $2.10: 45.2% - Premium to 52-week low market price of $1.30: $134.6% Thorough Review of Alternatives to Maximize Value: 2008-2010 - Extensive private sale process (18 financial & 15 strategic potential buyers; Jun. ’08 – Nov. ‘09) followed by exhaustive public go-shop process (86 financial & 59 strategic potential buyers) - Considered alternative transactions including buyside, stock repurchase/Dutch Auction, divestiture, dividend & liquidation - Considered memory space consolidations: Intel-ST spin-off Numonyx, sold to Micron; AMD-Fujitsu spin-off Spansion, filed for Bankruptcy Mar. ‘09 Extensive Auction & Go-Shop Process: Contacted 145 Potential Acquirers - 59 Strategic & 86 Financial Potential Acquirers Contacted - NDAs and extensive discussion with 35 Potential Acquirers - 5 Excluded Parties Deemed and 5 Indications of Interest received for final negotiations - 4 Final Bids Received, and full contract negotiations commenced Microchip Deal Provides Superior Value and Terms to SST Shareholders - Unanimously approved by Independent Strategic Committee - All-cash offer, no financing contingency, 3.5% break-up fee, no 13e-3 filing - 3-week path to delivering $3.05 per share in cash to SST shareholders as compared to 2-step, multi-month process for $3.00 per share in cash with Cerberus/Dialectic alternative - Eliminates shareholder exposure to a micro-cap company with no research coverage and a weak product portfolio in a competitive market - Product portfolio requires an overhaul that would be extremely expensive from an R&D perspective alone - Voting agreement establishes a level playing field by neutralizing one bidder’s ability to prevent a significant percentage of shareholders form supporting any alternative transaction regardless of whether it provided superior value (1) Based on Stock Price of $1.86 Prior to Announcement of Prophet Equity Bid on November 12, 2009 |

SST Proprietary & Confidential 9 Board Process Overview Well-advised, independent, thorough process Established Strategic Committee of independent directors who investigated all reasonable alternative transactions to maximize shareholder value, including buyside, stock repurchase/Dutch auction, divestiture, dividend, and liquidation. Strategic Committee retained independent financial and legal advisors (Houlihan Lokey and Shearman & Sterling LLP) Conducted thorough strategic alternatives review process commenced May 12, 2008 with 70+ meetings over 1½ years Why this approach? Arm’s length auction process and negotiation to allow for best price to come forward Transparency of auction process allows shareholders to make the best and most informed decision Public nature of Go-Shop process increased interest from both strategic and financial buyers Number of bids and number of bid rounds validates auction structure and the Board of Directors’ precision in negotiating the highest price and best terms for its shareholders Original $2.10 offer increased to $3.05 over the course of three months with a carefully managed Go-Shop process Strategic Buyer (Microchip, $5 Billion Market Cap, $1.2 Billion Net Cash) 19.9% Share Issuance levels playing field with bidder who precluded shareholders from voting for the highest bid. The Board of Directors and Strategic Committee fully negotiated voting arrangements and limitations on Microchip’s profit on the block of shares Specific performance, no financing contingency, no regulatory approvals required, and fast closing schedule (Shareholder Meeting April 8, 2010) |

SST Proprietary & Confidential 10 Flash Memory Market Decline (1) 10 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00 NOR Flash Units ASP 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 $2.0 $3.0 $4.0 $5.0 $6.0 NAND Flash Units ASP $230 $316 $259 $343 $496 $614 $545 $851 $1,095 $0 $200 $400 $600 $800 $1,000 $1,200 2007 2008 2009 2010 2011 2012 2013 2014 2015 Low/ Medium Density (256KB - 64MB) Forecast Unit Sales & ASP NOR Flash Market Decline ($ MM) (1) Source: Web Feet Research. |

SST Proprietary & Confidential 11 Highly Competitive NOR Flash Industry (1) Other 6% Samsung 21% Macronix 8% SST 4% Spansion 29% Numonyx 32% 2009 NOR Flash Market Share 2009 NOR Flash Memory Revenue by Company $150.9 Spun-Off of Intel & ST (exiting NOR market) Acquired by Micron (Mkt. Cap: $8.3B) as of Feb. ‘10 Spun-Off of AMD & Fujitsu (exiting NOR market) Filed for Chapter 11 Protection on Mar. 1, 2009 (1) Source: Web Feet Research. $165 $1,340 $981 $1,473 $394 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 |

SST Proprietary & Confidential 12 Competitive Landscape 4/8/16 Mb 32 Mb 64 Mb 128 Mb 256 Mb > 512 Mb Spansion Numonyx Samsung SST Macronix Winbond Atmel AMIC EON ESI KH PMC Spansion Numonyx Samsung SST Macronix Winbond Atmel Spansion Numonyx Samsung SST Macronix Winbond Atmel Spansion Numonyx Samsung Macronix Spansion Numonyx Samsung Spansion Numonyx Higher density competitive landscape faces encroachment from NAND technologies Heavy price pressure caused by competition between Spansion and Numonyx Lower density products quickly become commodities High competition and rapid ASP declines NAND Encroachment |

SST Proprietary & Confidential 13 Products Overview NANDrive ™ • Based on NAND Controller Product • Small ATA solid-state drive serves embedded applications • Shipped in a wide range of product applications Low-Density Flash Memory • Parallel and serial product lines • Small, thin packaging SuperFlash ® Technology • Embedded flash technology • Shipped in a wide range of product applications • Reliable flash memory WiFi Power Amplifiers • High-volume WiFi Power Amplifier Supplier • Adopted by a number of leading chipset providers |

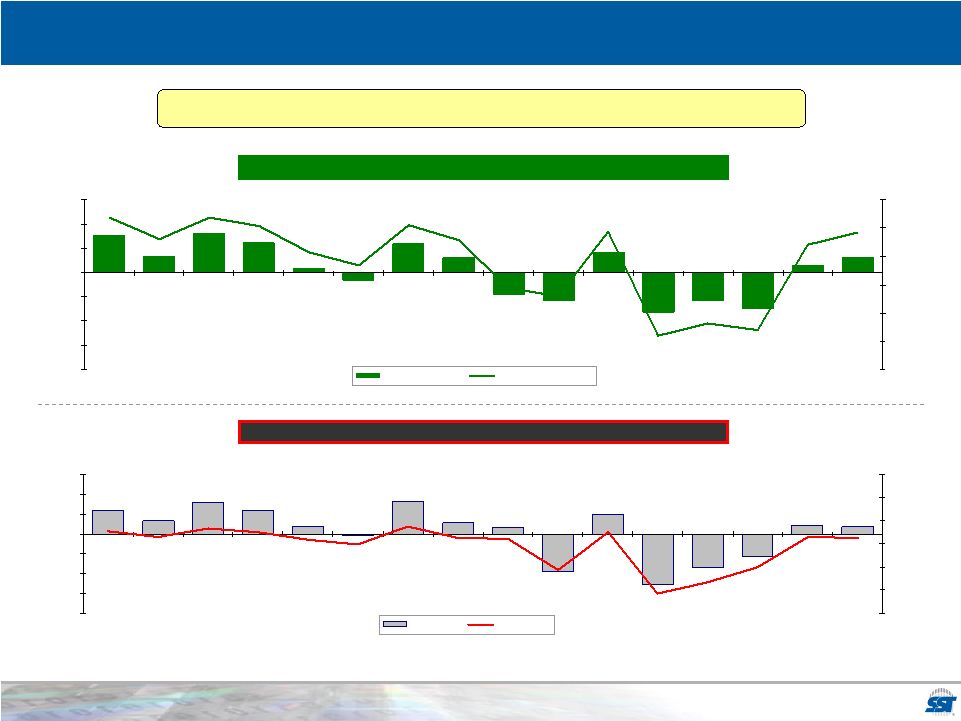

SST Proprietary & Confidential 14 Operating and Net Income – Trend Analysis (1) $1.5 ($7.5) $3.3 ($5.9) $4.1 ($8.3) ($4.6) $3.1 $6.0 ($1.6) $0.8 $6.2 $8.0 $7.6 $3.0 ($5.9) (14.1%) 4.2% 2.1% (11.8%) (13.0%) 4.4% (7.1%) (5.6%) 2.9% 5.6% (1.6%) 0.8% 5.3% 6.9% 6.9% 3.1% ($20.0) ($15.0) ($10.0) ($5.0) - $5 $10 $15 Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'07 Q4'07 Q1'08 Q2'08 Q3'08 Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 -20% -15% -10% -5% 0% 5% 10% Operating Income Operating Income % Operating Income vs. Operating Margin (Q1’06 – Q4’09A) ($8.3) $1.9 $5.9 $8.0 $6.0 $1.8 ($0.3) $8.3 $2.8 $1.7 ($12.5) $4.9 ($9.6) $3.4 ($5.7) $2.1 5.4% 3.2% 6.9% 5.1% 1.8% (0.3%) (11.4%) 5.3% (16.5%) 2.7% 2.1% 7.7% 2.6% (21.5%) (9.9%) 3.0% ($20.0) ($15.0) ($10.0) ($5.0) - $5 $10 $15 Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'07 Q4'07 Q1'08 Q2'08 Q3'08 Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 -30% -20% -10% 0% 10% 20% 30% Net Income Net Margin Net Income vs. Net Margin (Q1’06 – Q4’09A) (1) $ in Millions Operating/Net Margins Consistently Struggle with Profitability |

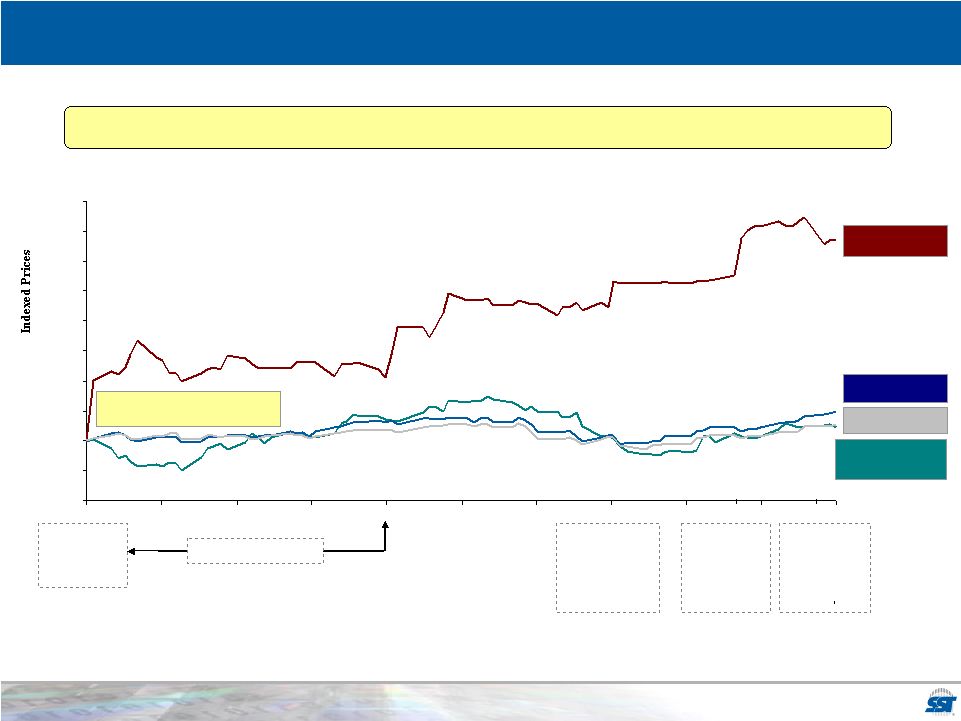

SST Proprietary & Confidential 15 Stock Performance Since Original Transaction (1)(2) SUN: 66.7% (1) Selected companies include: Infineon Technologies, Elpida Memory Inc., SanDisk Corp., Integrated Silicon Solutions Inc., Toshiba Corp., Imation Corp, Entorian Technologies Inc., and Netlist Inc. (2) Source: Bloomberg. S&P 500: 5.4% NASDAQ: 9.8% Nov. 13, 2009: Original Transaction Announced Before Market Open Full Auction & Go-Shop Process have achieved a significant increase in value 11/13/09 2/3/10 2/23/10 3/8/10 $2.10 Prophet Equity agrees to acquire SST $3.05 In response to Cerberus’ competing bid, MCHP raises its bid price Go-Shop Period $3.00 In response to a competing bidder, MCHP raises its bid price $2.85 After the Go-Shop period and assessment of final bids, MCHP announces its bid 80% 90% 100% 110% 120% 130% 140% 150% 160% 170% 180% 11/23/09 12/5/09 12/17/09 12/28/09 1/10/10 1/21/10 2/14/10 Index of Selected Companies: 4.4% |

SST Proprietary & Confidential 16 Comparative Trading Volume (1) 0 5,000,000 10,000,000 15,000,000 20,000,000 25,000,000 30,000,000 SST IFX ATML SNDK TOSHIBA (1) Source: Bloomberg. Micro-Cap Stock Without Research Coverage Average Daily Trading Volume CY'06 CY'07 CY'08 CY'09 906,420 903,910 460,790 304,790 XTRA:IFX 8,776,700 4,049,540 2,872,450 2,712,060 ATML 9,347,460 7,977,710 4,801,570 4,496,480 SNDK 11,296,520 9,895,590 10,425,200 7,861,760 25,216,000 28,511,330 24,902,730 62,869,330 |

SST Proprietary & Confidential 17 Transaction Key Events Timeline (1) Based on Diluted Shares Outstanding as of 2/28/2010: 98,655,330 and excluding additional 19,148,150 shares issued to Microchip on March 8, 2010. Date Event May 12, 2008 SST's Board of Directors establishes the Strategic Committee to review and evaluate a range of strategic transactions. June 6, 2008 The Strategic Committee selects Houlihan Lokey to serve as strategic and financial advisor. October 30, 2008 The Strategic Committee retains Shearman & Sterling LLP as legal advisor to the Strategic Committee. May 4, 2009 The Strategic Committee does not recommend Prophet Equity's $1.82 per share bid to the Board of Directors due to value considerations. November 13, 2009 Prophet Equity agrees to acquire SST for $2.10 per share, with a go-shop provision and 2.0% Break-Up Fee during the Go-Shop (3.5% afterwards) January 20, 2010 After reaching out to 145 potential partners with the help of Houlihan Lokey, the Board of Directors considered preliminary bids and deemed five excluded parties, from which three final bids were received. February 3, 2010 The Board of Directors votes to approve Microchip's $2.85 per share offer at a transaction value of $284.0 Million. February 23, 2010 In response to a competing bid entertained by the Board of Directors, Microchip raises its offer to $3.00 per share and amends the merger agreement. The Board approves the change, resulting in a transaction value of $295.0 Million. March 8, 2010 In response to a competing bid from a Cerberus Capital, Microchip raises its offer to $3.05 per share and purchases SST newly issued shares equal to 19.9% of outstanding common shares for a total transaction value of $300.9 Million (1) . |

SST Proprietary & Confidential 18 Roadmap to Completion Strategic Committee Established Merger Discussions Held with 33 Parties Prophet Equity Merger Agreement 45-Day Go-Shop Period & 145 Parties Contacted Five Excluded Parties Designated Diligence and Discussion with Five Excluded Parties Microchip Merger Agreement Executed Preliminary Microchip Proxy Filed Definitive Microchip Proxy Filed Proxy Supplement Filed Shareholder Meeting Estimated Closing May 12, 2008 June 2008 – November 2009 November 13, 2009 November 13, 2009 – December 28, 2009 December 29, 2009 December 29, 2009 – February 2, 2010 February 3, 2010 February 17, 2010 March 1, 2010 March 16, 2010 April 8, 2010 April 8, 2010 |

SST Proprietary & Confidential 19 Microchip Agreement Maximizes Shareholder Value The SST Board of Directors recommends that shareholders vote FOR the proposed transaction today. The Microchip agreement was unanimously approved by the Independent Strategic Committee and is the culmination of a 1½ years-long strategic review process and extensive go-shop period Attractive valuation at premium to historical trading range and peer group multiples Potential operational challenges as a standalone public company present execution and valuation risks relative to significantly larger competitors Microchip was the highest bidder after the Go-Shop period in a competitive auction situation Favorable terms achieved: Specific performance, all Cash, no financing contingency, fast closing time and 25.5% of shareholders committed to vote for the highest bidder 3-week path to $3.05 cash instead of 2-step, multi-month path to $3.00 cash, no 13e-3 filing and no pink sheet or stub stock as compared with Cerberus/Dialectic alternative transaction Immediate and certain cash value to shareholders with full guarantee and specific performance provided by Microchip ($5.2 Billion Market Cap & $1.2 Billion Net Cash) Three Weeks to Closing – April 8, 2010 |

S i l i c o n S t o r a g e T e c h n o l o g y, I n c. S i l i c o n S t o r a g e T e c h n o l o g y, I n c. www.SuperFlash.com Thank You! |