Exhibit 13

POTASHCORP 2004 ANNUAL REPORT

Several factors are driving a wave of demand for

fertilizer nutrients, especially potash.

| o | An expanding world population wants more and better food that must be grown on less land. |

| |

| o | Farmers recognize that replenishing potash, phosphate and nitrogen in their soils helps produce larger crops. |

| |

| o | Asian and Latin American nations with growing economies have more purchasing power and are increasing the ratio of potash, “the quality nutrient”, in their fertilizer applications. |

This represents the beginning of a period of substantial growth for the potash industry.

...and the

Pieces Are

Aligned

The growth in demand has pushed other producers close to their maximum output. Meaningful new production would require the development of additional reserves, as well as significant time and money.

With demand growing, supply tightening and prices rising, we are ready to show our unique strength – responding to the need for potash when others cannot.

This offers triple leverage: greater volumes, lower costs and better prices.

Our benefit from the upside in potash will be amplified by our investments in other potash companies.

| | | |

With

86 percent

of the world’s

excess capacity | | | PotashCorp has

the unique ability

to capitalize

on growing

demand for

potash. |

2

POTASHCORP 2004 ANNUAL REPORT | WHO WE ARE

A Global Company

for a Global

Industry

At PotashCorp, our goal is to be the global low-cost supplier of potash into all key world markets,

enhanced by a focused nitrogen and phosphate business that leverages our strengths of lower-cost gas in Trinidad and specialty phosphate products in North Carolina.

To achieve this, we have built an extended enterprise that includes facilities and investments in seven countries on three continents. This allows us optimal participation in a growing business.

We strive for transparency and open dialogue with our stakeholders, including investors, customers, employees and the communities where we work and live. Each year, we report on our financial, social and environmental performance, with the goal of continuous improvement.

Size and Market Prominence

| PotashCorp is not only the world’s largest fertilizer company by market capitalization, it has the greatest production capacity. We can produce more potash, the most desirable business of the three nutrients, than any other company or any country. | |

3

POTASHCORP 2004 ANNUAL REPORT | BUSINESS & FINANCIAL HIGHLIGHTS

2004 Business Highlights

| o | Produced and sold record potash volumes |

| |

| o | Achieved record potash prices |

| |

| o | Increased potash market share |

| |

| o | Generated record gross margin |

| |

| o | Reached record gross margin in potash and nitrogen |

| |

| o | Sold record purified acid volumes |

| |

| o | More than tripled 2003 adjusted earnings* |

| |

| o | Implemented a two-for-one stock split and increased dividend by 20 percent |

| |

| o | Outperformed sector in total shareholder return, with stock price almost doubling |

| |

| o | Reduced recordable injury frequency rate to record low for third consecutive year |

| |

| o | Received the Overall Award of Excellence for Corporate Reporting in Canada |

Financial Highlights

All financial data in this report are stated in US dollars

$ millions except per-share amounts

| | | | | | | | | | | | | |

| | | 2004 | | | 2003 | | | 2002 | |

Financial Results | | | | | | | | | | | | |

| Sales | | $ | 3,244.4 | | | $ | 2,799.0 | | | $ | 2,224.4 | |

| |

Net sales* | | $ | 2,901.4 | | | $ | 2,465.8 | | | $ | 1,928.7 | |

| |

| Gross margin | | $ | 681.4 | | | $ | 380.4 | | | $ | 307.3 | |

| |

| Net income (loss) | | $ | 298.6 | | | $ | (126.3 | ) | | $ | 53.6 | |

| |

Adjusted net income* | | $ | 267.8 | | | $ | 76.9 | | | $ | 53.6 | |

| |

| Net income (loss) per diluted share | | $ | 2.70 | | | $ | (1.21 | ) | | $ | 0.51 | |

| |

Adjusted net income per diluted share* | | $ | 2.42 | | | $ | 0.73 | | | $ | 0.51 | |

| |

EBITDA* | | $ | 754.3 | | | $ | 171.8 | | | $ | 386.0 | |

| |

Adjusted EBITDA* | | $ | 723.5 | | | $ | 417.7 | | | $ | 386.0 | |

| |

| Additions to property, plant and equipment | | $ | 220.5 | | | $ | 150.7 | | | $ | 212.2 | |

| |

| | | | | | | | | | | | | |

Financial Position | | | | | | | | | | | | |

| Total assets | | $ | 5,126.8 | | | $ | 4,567.3 | | | $ | 4,685.6 | |

| |

Net debt* | | $ | 903.5 | | | $ | 1,441.4 | | | $ | 1,471.8 | |

| |

Cash flow prior to working capital changes* | | $ | 529.6 | | | $ | 364.5 | | | $ | 289.2 | |

| |

| Cash provided by operating activities | | $ | 649.6 | | | $ | 381.5 | | | $ | 316.4 | |

| |

* See reconciliation and description of certain non-GAAP measures in Financial Performance Indicators on Pages 52 to 54.

4

POTASHCORP 2004 ANNUAL REPORT | LETTER TO SHAREHOLDERS

William J. Doyle

President and Chief Executive Officer

By any measure, 2004 was a rewarding year for your company.

PotashCorp sold 8.3 million tonnes of potash, setting North American and offshore sales records. Demand continued to grow and prices reached new highs by the end of the year, driving gross margin to an unprecedented level.

Our success was also reflected in areas beyond the income statement. We achieved growth while reducing our recordable injury frequency rate to the lowest ever. We earned recognition and awards for governance and corporate reporting. Our share price nearly doubled as our investors enjoyed the benefits of a stock split and a higher dividend.

It was an amazing year filled with remarkable successes. But for those who know our company and the determination of our people, it was not surprising. We have a talented, well-trained and committed team that has been building toward this time for almost two decades. We have assembled tremendous assets and managed them with a long-term view.

Now, the factors that impact our business – and our potential – are falling into place like dominos, each one triggering the next for PotashCorp.

Rewarding Investors

Our company holds a distinct advantage in potash. This was demonstrated in 2004 as higher volumes and prices resulted in a considerable increase in earnings. Our potash gross margin of $422.8 million was more than twice that of 2003 and represented 47 percent of potash net sales.

This was supplemented by a strong year in nitrogen as tight supply/demand fundamentals kept prices up and pushed our nitrogen gross margin to a record high of $242.8 million, 26 percent more than the previous year. The significance of this improvement should not be overlooked, as our 2003 nitrogen margin was aided by the sale of our natural gas hedges at the peak of the market.

Phosphate remained a challenging business, with continued excess supply in DAP, one of our four main product lines. Although higher input costs negatively impacted results,

5

POTASHCORP 2004 ANNUAL REPORT | LETTER TO SHAREHOLDERS

gross margin in this nutrient did recover from a loss of $16.5 million in 2003 to contribute $15.8 million in 2004. More importantly, our fourth-quarter gross margin of $10.4 million bodes well for 2005.

As a result, PotashCorp’s total gross margin grew to $681.4 million, operating income to $514.3 million and net income to $298.6 million. This led to earnings of $2.70 per diluted share. We generated $649.6 million in cash from operating activities, showing that strong cash flow remains a hallmark of PotashCorp.

This was accomplished despite the continued strengthening of the Canadian dollar, which began 2004 at 1.29 against the US dollar and closed at 1.20. Record potash production reduced our cost per tonne by 5 percent on a real basis, but the higher value of the Canadian dollar against its US counterpart hurt translated costs. While this had a negative effect on gross margin, the biggest earnings impact was primarily non-cash, due to the translation of certain items on our balance sheet. In total, the strong Canadian dollar reduced annual earnings by $0.16 per share.

In July, our Board of Directors approved a two-for-one stock split and raised our dividend by 20 percent. Our shares increased by 92.1 percent on the New York Stock Exchange in 2004. This compares to an increase of 10.5 percent for the Dow Jones Basic Materials Index and an average of 66.5 percent for other companies in our sector. Once again we achieved our goal of outperforming our industry peers and other basic materials companies.

Potash Triggers Growth

This was the third consecutive year of above-average growth for potash in offshore markets. We have emerged from a period of significant oversupply that began in the early 1980s and was exacerbated by the collapse of the Soviet Union. For nearly two decades, PotashCorp stuck to a strategy of matching production to demand, confident that the continued need for our products would drive world growth and eventually absorb the capacity overhang. Our patience was rewarded as we sold 17 percent more potash at prices 29 percent higher than in 2003.

A key driver is the rapid GDP growth in many Asian and Latin American nations. Among our major customers, China’s economy grew 9 percent in 2004, India’s 6 percent and Brazil’s 4 percent. Several foreign currencies rose against the US dollar, giving customers in those countries greater buying power and the ability to purchase more potash.

In the past, farmers in many agricultural economies applied nitrogen and phosphate at higher levels than potash. Now those countries are trying to catch up, especially in Southeast Asia where Indonesia, India, Malaysia, Vietnam, Thailand and Taiwan are becoming bigger customers.

This accelerating demand has pushed the rest of our industry to its production limits. Excluding PotashCorp, producers operated at approximately 98 percent of capacity in 2004. We operated at 65 percent of our maximum production rate. With 86 percent of the world’s unused capacity, we are in the enviable position of being the only producer able to bring on significant additional capacity in a timely manner.

In the second half of 2004, we took steps to utilize this strength. We added fourth shifts at Lanigan and Allan, which enables them to operate around the clock and will increase annual production by 1.2 million tonnes. We continued work on an $80-million expansion

6

POTASHCORP 2004 ANNUAL REPORT | LETTER TO SHAREHOLDERS

at Rocanville, which began producing in the first quarter of 2005. This raises our annual production capacity by 400,000 tonnes. Further projects in Saskatchewan and New Brunswick are being assessed with a view to being able to operate at full capacity – now 12.5 million tonnes – within three years.

Playing to Our Strengths

We also worked to leverage our unique strengths in nitrogen and phosphate, focusing on areas that offer the greatest returns.

North American gas costs continued to rise in 2004, leading to further reductions in domestic nitrogen production and more imports to the United States. Fertilizer and industrial demand remained strong and capacity additions did not keep pace with consumption growth. The resulting tight supply/demand drove our ammonia prices up by 23 percent, urea 18 percent and nitrogen solutions 29 percent.

These conditions demonstrated the value of our facility in Trinidad, where we have long-term, advantageous gas contracts that give PotashCorp a significant edge. We are building on that advantage with expansions at our four plants that together will add

270,000 tonnes of ammonia capacity for $71 million, less than half the cost of new capacity. This will give us the most low-cost offshore production capability of any producer in the Western Hemisphere. All expansions will be completed by the third quarter of 2006.

In phosphate, we are focused on specialty products to offset the cyclicality of the fertilizer business. However, start-up problems at our new DFP (poultry feed) plant at Aurora cost $9 million. We have worked to resolve them, and the facility should operate at capacity in 2005. We did demonstrate our unique strength in purified acid, a high-margin industrial product. PotashCorp is the only company with local access to the quality rock preferred for low-cost purified acid production. The lack of high-quality ore is a barrier for other phosphate producers.

We have increased our focus on industrial production, the area of phosphate furthest removed from commodity cycles. Industrial volumes rose 13 percent and prices 4 percent. We are pursuing a greater share of this high-margin market, investing $73 million at Aurora to add 82,000 tonnes of purified acid production per year. This expansion should be operational by 2006.

7

POTASHCORP 2004 ANNUAL REPORT | LETTER TO SHAREHOLDERS

The Chain Continues

As we look forward to 2005, it is clear that potash will be the value driver in the fertilizer industry as offshore markets continue to grow. With our global position, we expect to be the main beneficiary. That was certainly the case in 2004, when we brought on an additional 0.8 million tonnes of production. We plan to do more in 2005.

Our anticipation of further volume growth at higher prices was validated when Sinochem in China signed a 2005 contract with Canpotex. This agreement is expected to increase China’s Canadian potash imports from 1.8 million tonnes to 2.3 million tonnes at prices at least $40 per tonne higher than in 2004. China’s total consumption in 2005 will rival that of the United States, historically the world’s largest potash consumer.

In nitrogen, anticipated high natural gas prices in the United States and Europe are expected to keep some production shuttered. Limited new capacity is projected and this, combined with strong demand, should maintain high prices for nitrogen products and enhance the value of our Trinidad asset.

In phosphate, better supply/demand fundamentals in feed and purified acid should translate into higher prices and better returns. Still, the phosphate fertilizer industry suffers from oversupply, although a mid-term DAP recovery is possible with industry consolidation.

Over the longer term, all three nutrients – but especially potash – will benefit from the chain of events unfolding in Asia and Latin America. Brazil, an agricultural powerhouse and our largest offshore potash customer, continues to bring acres into production in the cerrado region, where soils are naturally low in potassium and the climate is ideal for growing soybeans.

That is important given China’s rapidly increasing demand for soybeans – a crop that provides an important protein source for livestock as well as oil for cooking. China’s population now expects a healthier, protein-rich diet and will not return to starch as its food staple. More soybeans and other grains will be needed for animal consumption.

This happens as world grain stocks are precariously low. Farmers around the world produced a huge crop in 2004, but it did little to raise grain inventories since consumption rose as well. The need for increased crop production is kickstarting the fertilizer industry.

Of the three nutrients, potash has the greatest growth potential as farmers have not applied enough of it compared to nitrogen and phosphate. For example, China would need to double its ratio of potash to other nutrients just to catch up to the US and could go even further to meet its scientifically recommended needs. India would need to more than triple potash applications to meet its recommended ratio, which translates to an additional 7.5 million tonnes. Brazil could increase consumption by as much as 50 percent. These regions have little or no indigenous production and must rely on imports from an industry that, exclusive of PotashCorp, is running full out.

Tight fundamentals and our historical practice of matching supply to demand have enabled potash to decouple from the grain cycle and position it best among the three nutrients. While we expect continuing vigorous competition as other producers strive to generate additional capacity by debottlenecking, we don’t anticipate any significant new greenfield production in the short- to mid-term.

8

POTASHCORP 2004 ANNUAL REPORT | LETTER TO SHAREHOLDERS

Available reserves are restricted to a few locations and the high cost and long lead time for a new mine prevent the volatile swings of a typical commodity cycle. We know there will be some fluctuations in our outward growth line, with either temporarily reduced consumption or competitive debottlenecking. However, we believe demand will continue to rise, taking our earnings with it. We will remain faithful to our strategy of matching production to demand, which served us well in the past and will do so in the future.

PotashCorp spent years preparing for today’s conditions. We have added to our Saskatchewan base with strategic investments in New Brunswick, Chile, Jordan and Israel that expand our global potash presence. Late in 2004, we increased our ownership in SQM in Chile from 20 percent to 25 percent. We are well placed to capitalize on our own potash position as well as on these investments. They have performed well and their value will become more evident in the years to come.

Now, more than ever, the world is looking to PotashCorp. We have the people, production facilities and excess capacity to answer the call.

Excellence in All Areas

One of our core values is to seek continuous improvement and in 2004 we pursued that in all areas of our business, with the objective of becoming a stronger company for our stakeholders.

The first priority is safety, as our people are at the heart of our success. We have a goal of no harm to people, no accidents and no damage to the environment. PotashCorp’s employees have embraced this and moved us closer to our goal by reducing our recordable injury frequency rate for the third year in a row. In addition, our potash operations in New Brunswick earned the John T. Ryan trophy, the Canadian mining industry’s most prestigious safety honor. Our environmental efforts were also recognized, as Aurora was honored with North Carolina’s Mining Stewardship Award for reclamation.

Cognizant of our company’s global responsibilities, we quickly donated $1 million to the relief effort after a tsunami struck Southeast Asia in December. Of that total, $250,000 was set aside to match donations

from our employees – yet another example of how our people rise to a challenge and step forward whenever and wherever they are needed.

Those values drive the ongoing advancement of our business. In 2004, we issued our second annual sustainability report, detailing our economic, social and environmental performance. This is part of a corporate reporting program designed to increase transparency and ensure we are responsible and accountable. These efforts led the Canadian Institute of Chartered Accountants to recognize PotashCorp as having the best corporate reporting program in Canada. The CICA selected our 2003 annual report as the best in Canada’s mining industry and one of the top two in all sectors. It also presented us with top honors for sustainability reporting and for our website, www.potashcorp.com.

All of these accomplishments are made possible by a Board of Directors focused on making PotashCorp not only the best company in our industry but a shining example for the corporate world. We have a dynamic board that sets high standards, demonstrates its stated commitment to best practices and leads with a vision of greater success for PotashCorp. In January 2005, it approved a plan to repurchase up to 5 percent of our outstanding common shares, which will allow us to reinvest in our potash business.

Our approach is opening new doors, such as increased opportunities for our people who have assumed management responsibilities with APC in Jordan. We are extending our reach and knowledge around the world – and that will bring benefits to all our stakeholders.

We continue to put in place more pieces that will lead to ongoing success for our company. In 2004, we enjoyed a tremendous year, but we believe it was only the beginning. At PotashCorp, our time has come.

William J. Doyle

President and Chief Executive Officer

February 28, 2005

9

POTASHCORP 2004 ANNUAL REPORT | GOALS AND TARGETS

| | | | | | | | |

| | | | | | |

| |

To continue to outperform our sector and other basic materials companies in total shareholder return.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Exceed total shareholder return performance of the companies on the Dow Jones Basic Materials Index (DJBMI). | |  PotashCorp provided total shareholder return of 93.4 percent, compared to 13.1 percent for the DJBMI. | | | 1Exceed total shareholder return performance for our sector and companies on the DJBMI for 2005 and three-year average. | |

| |

| | | | |

| | Be at the top of our earnings guidance range. | | Achieved adjusted earnings per diluted share* of $2.42, exceeding initial guidance of $1.35 to $1.75 (adjusted for stock split). | | | 2Be the preferred fertilizer investment as measured by surveys. | |

| |

| | | | |

| | Work with the management and board of APC to improve its shareholder return. | | APC increased its shareholder return by 137 percent. | | | 3Non-cash operating working capital to be less than 10 percent of net sales.

4Total cash flow return to exceed cost of capital by 500 basis points. | |

| |

| | | | |

| | Maintain non-cash operating working capital* at year-end rates. | | More than achieved as non-cash operating working capital declined by 47 percent to $185 million. | | | 5Carry higher multiple than average of other fertilizer companies on both earnings and cash flow. | |

| |

| | | | |

| | Total cash flow return* to exceed cost of capital by 200 basis points. | | Cash flow return exceeded cost of capital by 400 basis points. | | | 6Exceed five-year average of historical gross margin as a percentage of net sales. | |

| |

| | | | |

| | Exceed five-year average of historical gross margin as a percentage of net sales*.

| | Achieved 23.5 percent compared to five-year average of 18.6 percent. | | | 7Be at the top of our earnings guidance range. | |

| | | | | | |

| | | | | | | | |

| | | | | | |

| |

To remain the leader and preferred supplier of potash, phosphate and nitrogen products worldwide.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Continue to be the preferred supplier, as measured by customer surveys. | | Customers evaluated PotashCorp as No. 1 on a series of sales criteria, and we outperformed the competition. | | | 1Increase potash sales volumes by 5 percent at 25 percent higher realized prices. | |

| |

| | | | |

| | Reduce the number of customer complaints by 5 percent. | | PotashCorp reduced customer complaints by 10 percent. | | | 2Industrial nitrogen net sales from US plants to comprise 70 percent of the total from those plants. | |

| |

| | | | |

| | Increase total potash sales volumes by 5 percent at 5 percent higher realized prices. | | Sales volumes increased by 17 percent and realized prices by 29 percent. | | | 3Increase North American feed realized prices by 15 percent.

4Increase purified acid price realizations by 5 percent. | |

| |

| | | | |

| | Increase purified acid sales by 12 percent. | | Purified acid sales volumes increased 25 percent; net sales* up 24 percent. | | | 5Implement enterprise-wide customer complaint system to facilitate tracking and resolution. | |

| |

| | | | |

| | Increase North American industrial nitrogen sales volumes to 60 percent of total nitrogen sales. | | North American industrial nitrogen sales represented 67 percent of total North American nitrogen sales volumes. | | | 6Outperform competitors on quality and service as measured by customer surveys.

7Expand computer applications’ e-mail capabilities to improve communications with customers and vendors. |

| |

| | | | |

| | Increase DFP volumes by 18 percent at 16 percent higher realized prices. | | DFP volumes increased 31 percent at 16 percent higher realized prices. | | | | |

| | | | | | |

* See reconciliation and description of certain non-GAAP measures on Pages 52 to 54.

10

POTASHCORP 2004 ANNUAL REPORT | GOALS AND TARGETS

| | | | | | | | |

| | | | | | |

| |

To be the low-cost supplier in our industry.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Reduce per-tonne conversion costs in each of our three nutrients by 5 percent. | |  Costs were reduced in potash by 3 percent (on a Canadian dollar basis); in nitrogen by 3 percent; and in phosphate by 1 percent. | | | 1Achieve rock costs at Aurora and White Springs 5 percent below 2004. | |

| |

| | | | |

| | Reduce phosphate rock costs by 5 percent. | |  Phosphate rock costs were reduced by 1 percent. | | | 2Achieve conversion costs for P2O5 production 4 percent better than 2004. | |

| |

| | | | |

| | Achieve average natural gas input costs in North America 10 percent below the average NYMEX spot price. | | Achieved savings of 13 percent relative to NYMEX. | | | 3Achieve 5-percent reduction in per-tonne potash conversion costs on a Canadian dollar basis.

4Achieve energy efficiency in nitrogen 2 percent better than 2004. | |

| |

| | | | |

| | Implement supply-chain management process. | | Nitrogen implementation was completed in 2004; potash and phosphate implementations are scheduled for 2005. | | | 5Operate the Aurora DFP plant at design capacity. | |

| |

| | | | |

| | Reduce North American transportation and distribution expenses by 5 percent. | | Reduced North American transportation and distribution expenses by 4.2 percent. | | | 6Yield a 3-percent saving in transportation and distribution from industry benchmark. | |

| |

| | | | |

| | Realize expected saving from negotiated medical plan design. | | Changes in the medical plan were implemented, resulting in savings that exceeded expectations. Annual savings are projected to be $800,000. | | | | |

| | | | | | |

| | | | | | | | |

| | | | | | |

| |

To move closer to our goal of no harm to people, no accidents, no damage to the environment.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Reduce recordable and lost-time injury frequency rates by 10 percent. | | PotashCorp’s recordable injury frequency rate dropped by more than 13 percent and the lost-time injury rate fell 21 percent. | | | 1Reduce recordable and lost-time injury rates by 10 percent. | |

| |

| | | | |

| | Reduce the number of environmental releases and permit excursions by 10 percent. | | Total environmental releases (18) and permit excursions (31) were 25 percent higher due to issues at our Lima nitrogen plant. | | | 2Reduce reported releases and permit excursions by 25 percent. | |

| |

| | | | |

| | Implement proactive facility security plans addressing current and anticipated security regulations. | | All high-risk facilities (US and Trinidad nitrogen) have security plans in place. | | | 3Achieve 100-percent compliance on all environmental and safety audit action items. | |

| |

| | | | |

| | Through the use of effective management processes, continue to avoid major adverse incidents.

| | By designing, implementing and auditing safety processes and action plans, PotashCorp avoided major adverse incidents. | | | | |

| | | | | | |

11

POTASHCORP 2004 ANNUAL REPORT | GOALS AND TARGETS

| | | | | | | | |

| | | | | | |

| |

To have motivated and productive employees committed to our long-term goals.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Implement key corporate performance metrics. | | Senior management utilized a balanced scorecard approach to develop a system for tracking and reporting on key performance indicators in operations, sales, finance, investor relations and human resources. This system will be rolled out in 2005. | | | 1Integrate key corporate performance metrics into regular employee reviews, providing managers with greater discretion to reward individual achievement. | |

| |

| | | | |

| | Implement employee incentives that tie compensation more directly to the achievement of key corporate financial performance measures. | | A performance-related contribution to savings plans for non-union employees was introduced, based on cash flow return* exceeding weighted average cost of capital*. A redesigned stock-option program focusing on long-term achievement will be presented to shareholders for approval. | | | 2Proactively improve orientation programs for new employees and career development processes for existing employees. | |

| |

| | | | |

| | Complete implementation of succession management and employee development processes to improve focus on key talent and critical shortages. | | Succession management continued at the board level. Identification of key talent, critical positions and development is now an ongoing component of senior management discussions. | | | 3Complete implementation of a human resources administration system enabled by information technology. | |

| |

| | | | |

| | Complete implementation of a human resources administration system enabled by information technology. | | By January 2005, half of US payrolls had been shifted to the new system and all other components were in place for US administration. Implementation of the remaining components for Canada will be completed in 2005. | | | 4Maintain personnel turnover improvements achieved in 2004 in Trinidad. | |

| |

| | | | |

| | Reduce employee turnover in the Trinidad segment. | | Turnover at Trinidad was successfully reduced by 40 percent. | | | | |

| | | | | | |

| | | | | | | | |

| | | | | | |

| |

To have a positive impact on the communities in which we operate.

| |

| | | | | | |

| | 2004 Targets | | 2004 Results | | | 2005 Targets | |

| |

| | | | |

| | Be engaged with community support projects at each of our plants and offices. | | Each of our plants and offices completed many community support volunteer projects. | | | 1Be in the top quartile of responses in a survey of community leaders. | |

| |

| | | | |

| | Develop emergency management and crisis communication plans for Saskatoon and Northbrook offices. | | The emergency management plans for Saskatoon and Northbrook offices are in draft form. The crisis communication plan is complete. Emergency management and crisis communication plans are in place at all plant facilities. | | | 2Be engaged with community support projects at each of our plants and offices.

3Achieve a 10-percent increase in individual participation in the matching gift program and a 20-percent increase in total donations. | |

| |

| | | | |

| | Conduct a review of governance policies and principles to identify and implement most recent best practices. | | PotashCorp’s governance policies and practices were recognized as among the top 7 percent of companies by Governance Metrics International. | | | 4Remain in the top quartile of governance practices as measured by external reviews. | |

| | | | | | | | |

| | | | | | |

* See reconciliation and description of certain non-GAAP measures on Pages 52 to 54.

| | | |

| In January 2005, PotashCorp’s phosphate operation at Aurora won the North Carolina Mining Stewardship Award for its reclamation efforts at Whitehurst Creek. The restoration included enhancements to the aquatic culture and stream system, and the area is once again home to fish, birds and wildlife. | | achieved

partially achieved

did not achieve

|

12

POTASHCORP 2004 ANNUAL REPORT | SUSTAINABILITY

Sustainability

and

Success

At PotashCorp, we recognize that business success and sustainability are intertwined. We are building sustainable business practices into our management systems as we weave the policies and principles of sustainability into our company culture. This requires well-defined expectations that take into account the concerns of our stakeholders, and goals that move us forward as a sustainable enterprise.

Governance

To be sustainable, a company must clearly define the roles and responsibilities of its board and management as well as its relationships with stakeholders. Our Board of Directors follows a charter that sets out its responsibilities and the limits to management’s responsibilities, and adheres to a comprehensive statement of governance principles that addresses key issues, including: board independence and integrity; functions of the board; selection and composition of the board; and board committees. PotashCorp’s board is specifically charged with:

| |

| o | oversight and approval on an ongoing basis of the corporation’s business strategy; |

| |

| o | appointment of the Chief Executive Officer and monitoring his or her performance; |

| |

| o | approving the appointment of all corporate officers; |

| |

| o | establishing standards for management and monitoring performance; and |

| |

| o | approving procedures for strategy implementation, for identifying and managing risks and for ensuring the integrity of internal control and management information systems. |

Management Systems

At the management level, we continue to advance management systems designed to support continuous improvement. Our corporate disclosure policy, which was adopted before it was required, ensures

all shareholders have equal access to information. We have a comprehensive purchasing policy that links procurement, in part, to considerations of community development. Our Safety, Health and Environment Management System outlines our requirements and expectations in areas such as safety and accident prevention, pollution, energy conservation and product stewardship. This has contributed to improved safety performance and a reduction in the recordable injury frequency rate for three consecutive years.

Code of Conduct

Our statement of core values and code of business conduct make clear that honesty, transparency, integrity and respect for the law are fundamental to the way our company and our people operate. This has been communicated to all employees through meetings and ongoing dialogue. Employees sign off on having a thorough understanding of how PotashCorp’s values and code of conduct affect the way they do their jobs, fostering a culture of responsibility and accountability.

13

POTASHCORP 2004 ANNUAL REPORT | SUSTAINABILITY

| | | | | | |

| | | | | | |

| |

CONNECTING WITH STAKEHOLDERS: Sustainability does not live inside a company; it acknowledges the needs and interests of all stakeholders. PotashCorp maintains a dialogue with people affected by our operations, providing forums to share our strategies and the resulting benefits. This is also an important risk-management tool that can identify areas of concern before problems arise. We rely on independent research to gather feedback and insight into stakeholder perceptions and interests.

| |

| | | | | | |

| | | | | | |

| | | | | | |

| | Customers | | | Employees | |

| | | | | | |

| | o say product quality is the key factor in buying decisions, after price

o those surveyed ranked PotashCorp No. 1 in product quality in each of our four major product areas | | | o list PotashCorp’s integrity as an important factor in their continuous improvement efforts and positive view of the company

o those surveyed reported a high level of overall engagement | |

| | | | | | |

| | | | | | |

| | | | | | |

| | Investors | | | Communities | |

| | | | | | |

| | o believe PotashCorp has the attributes of a growth company

o those surveyed valued our Potash First strategy, which is well-matched to these attributes | | | o respect our long-term approach to business, strong safety and environmental performance and the work we do in the community

o those surveyed supported the expansion of our business | |

| | | | | | |

| | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| |

LEADING BY EXAMPLE: Actions speak louder than words – and PotashCorp demonstrates social responsibility in areas that are important to our stakeholders. Through financial support, volunteerism and corporate leadership, we are actively involved in the communities where we live and work.

| |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | Financial

Less than one week after a tsunami devastated regions of Southeast Asia in December 2004, PotashCorp announced a $1-million donation to the relief effort, including $250,000 to match donations from our employees.

The practice of matching donations brings a sense of partnership to our giving practices, as our financial support goes to causes our stakeholders consider important. For example, in Saskatchewan we pledged $1.5 million to match community donations to a health-care initiative. | | | Volunteerism

Volunteerism connects PotashCorp to our communities. At Aurora, our people answered telephones and recorded pledges at the Children’s Miracle Network telethon, contributing to a record-breaking effort that raised more than $1.25 million.

At Joplin, PotashCorp employees read to elementary school students on a regular basis, while Saskatoon and Northbrook employees teamed up on the construction of a house as part of Habitat for Humanity’s “Women Build” day. | | | Leadership

Our people rise to the occasion when assistance is needed. After Hurricane Ivan destroyed more than 90 percent of the homes in Grenada, employees in Trinidad gathered food, clothing and water, and collected money to purchase tarps for temporary shelters.

PotashCorp sponsored a series of anti-drug talks by D.D. Lewis, an employee and former NFL star, that reached more than 17,000 students in 2004. Our people also led the creation of a Saskatchewan chapter of the Institute of Corporate Directors to enhance governance. | |

| | | | | | | | | |

| | | | | | | | | |

| | | | |  | | |  | |

| | | | | | | | | |

14

POTASHCORP 2004 ANNUAL REPORT | MD&A

Management’s

Discussion &

Analysis

of Financial Condition and Results of Operations (in US Dollars)

The following discussion and analysis is the responsibility of management and is as of February 28, 2005. The Board of Directors carries out its responsibility for review of this disclosure principally through its audit committee, comprised exclusively of independent directors. The audit committee reviews this disclosure and recommends its approval by the Board of Directors. Additional information relating to us (which is not incorporated by reference herein) can be found on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

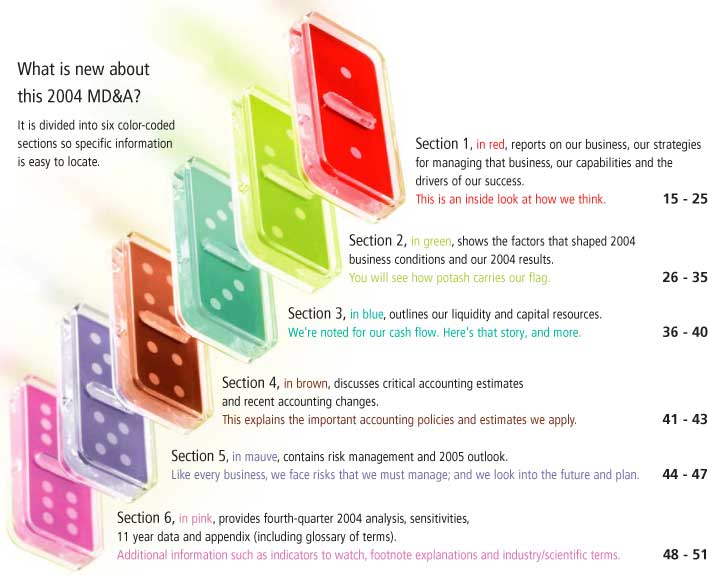

| Special things to watch for: |

| |

| 26 | Factors that shaped 2004 business conditions |

| |

| | World economic growth and specific conditions that affected the entire fertilizer industry last year. |

| |

| 28 | Earnings review |

| |

| | Our 2004 earnings exceeded our guidance and 2003 results. This section explains the variances in detail on a per-share basis. |

| |

| 44 | Risk management |

| |

| | A more integrated risk-management framework was introduced, and here are the details. |

| |

| 50 | Key earnings sensitivities |

| |

| | Key factors and their effect on earnings per share. |

| |

| 50 | Indicators to watch in 2005 |

| |

| | These are our best estimates of factors that could affect our industry and our performance in the year to come. |

15

POTASHCORP 2004 ANNUAL REPORT | MD&A•N, P & K and PotashCorp Facts

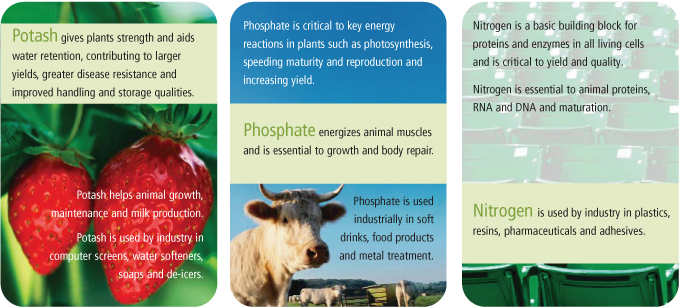

BUSINESS

Different nutrients, different attributes

Different nutrients, different business environments

| | | | | | | |

| | Potash(K) | | Phosphate(P) | | Nitrogen(N) |

| | | |

| Base Product | | Potassium chloride | | Phosphate rock

– phosphoric acid | | Ammonia |

| | | |

Geographic Availability

of Raw Materials1 | | Very limited | | Limited | | Readily available in numerous

locations (natural gas) |

| | | |

Cost of New Capacity2 | | Approximately $500 million

for 1 million tonnes KCl | | Approximately $1 billion

for 1 million tonnes P2O5 | | Approximately $500 million

for 1 million tonnes ammonia |

| | | |

Greenfield3

Development Time4 | | 5 years | | 3 years | | 2 years |

| | | |

Producing Countries5 | | 12 | | 41 (based on phosphoric acid) | | Approximately 60 |

| | | |

State- or Subsidy-

Controlled Production6 | | 14% | | 44% | | 50% |

| | | |

Industry Operating Rate7 | | 91% | | 74% | | 82% |

| | | |

PotashCorp Capacity8 | | 12.5 million tonnes potash*

23% of world capacity | | 2.5 million tonnes

phosphoric acid | | 3.9 million tonnes ammonia

2% of world capacity |

| | | | | 6% of world capacity | | |

| | | |

PotashCorp World Position

by Capacity9 | | # 1 | | # 3 | | # 4 |

| | | |

| | |

| * Increased from 12.1 million tonnes by expansion completed in first quarter of 2005. | | 1-9, See Appendix Page 51 |

16

POTASHCORP 2004 ANNUAL REPORT | MD&A•Our Business Environment

BUSINESS

Our Business Environment

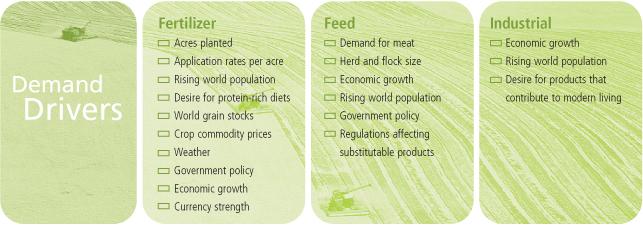

As the world’s largest producer, by capacity, of the three primary plant nutrients – potash, phosphate and nitrogen – PotashCorp has built a global business on these natural nutrients. Our products serve three different markets: fertilizer, feed and industrial. All three nutrients are important in fertilizer, with phosphate the biggest player in the feed market. In the industrial market, phosphate and nitrogen products play the major role.

We sell fertilizer to North American retailers, cooperatives and distributors that provide storage and application services to farmers, the end users. Our offshore customers are governments and private importers that tend to buy under contract, while spot sales are more prevalent in North America. Key offshore customers include Brazil, China, Japan, Malaysia and Indonesia. Fertilizers are sold primarily for spring and fall application in both northern and southern hemispheres. In North America, all three nutrients are used on

corn, wheat, cotton and rice, while nitrogen-producing soybeans require potash and phosphate. This is also true offshore, although potash is used extensively on a broader range of crops there, including oil palm, sugarcane and coffee.

Transportation is an important part of the final purchase price for fertilizer so producers usually sell to the closest customers. In North America, we sell mainly on a delivered basis via rail, barge, truck and pipeline. Offshore customers purchase product either at the port where it is loaded or with freight included. Approximately 60 percent of our potash customers buy it freight included (CFR) and the remainder are responsible for ocean freight (FOB). In phosphate, the majority of offshore sales are FOB. Our nitrogen is sold primarily in North America.

Our feed customers are mainly US bulk feed producers, with Brazil and Mexico the biggest offshore customers. Our industrial customers are primarily based in the US, and include industrial intermediate and product manufacturers such as Astaris and Innophos in phosphate and BASF and DSM in nitrogen. Most feed and industrial sales are by contract and are more evenly distributed throughout the year than fertilizer sales.

In all product categories (fertilizer, feed and industrial products), price is the most important variable in the buying decision. North American customer surveys indicate that product quality is the next most important factor when a supplier is being chosen. Customers’ specific needs also affect their buying decisions. For example, in Japan, where our potash products are commonly used in industrial applications, quality is a significant factor. In Brazil, granular potash to blend with the other nutrients is key.

17

POTASHCORP 2004 ANNUAL REPORT | MD&A•Vision/ Strategy

BUSINESS

Vision

We envision PotashCorp as a long-term business enterprise providing superior value to all our stakeholders. To achieve this, we believe we need to be the sustainable gross margin leader in the products we sell and the markets we serve.

Through our strategy, we attempt to minimize the natural volatility of our business. Risk rises with volatility and we believe the capital markets will assign a better earnings multiple to a growth company with lower risk. We also strive for increased earnings, and to outperform our peer group and other basic materials companies in total shareholder return, a key measure of any company’s value.

We link our financial performance with areas of extended responsibility: the environment, our social and economic stakeholders. We focus on increased transparency to improve our relationships with all our stakeholders, believing this gives us a competitive advantage.

Strategy

Our strategy is based on our commitment to seek earnings growth and quality. We strive to build value with reduced volatility and we reduce volatility by doing all we can to strengthen our potash business, hence our Potash First strategy. Our goal is to be the low-cost global potash supplier on a delivered basis into all key world markets. We supplement this potash strategy by leveraging our strengths in nitrogen with our lower-cost gas in Trinidad, and our specialty phosphate products, particularly the industrial product, purified acid, produced in North Carolina.

In our day-to-day actions, we seek to maximize gross margin by focusing on the right blend of price, volumes and asset utilization. Our highest-margin products – potash, purified phosphoric acid and Trinidad nitrogen products – drive our strategy, and we strive to grow the business by enhancing our position as supplier of choice. We aim to build on our strengths by acquiring and maintaining low-cost, high-quality capacity that complements our existing assets and adds strategic value. Our decisions are based on our cash flow return materially exceeding cost of capital.

18

POTASHCORP 2004 ANNUAL REPORT | MD&A•Potash

BUSINESS

PotashCorp in the World Potash Scene

Around the world, potash deposits that can be mined economically are limited to a few countries. There are only 12 producing countries, more than 150 consuming countries, and over 80 percent of the product crosses borders. The primary producing areas – Canada, Russia and Belarus – account for two-thirds of world production. The US, a mature market, is the largest potash importer. The greatest growth markets are nations with limited or no indigenous production, such as Brazil, China and India. PotashCorp is a prominent supplier to these markets.

Our major competitors in North America are Agrium and Mosaic, which have more exposure to North American sales than we do. Globally, we compete with producers in Belarus, Russia, Germany and Israel in the key growing markets of Asia and Latin America.

STRATEGY:

Using excess capacity to build on global leadership

Our strategy in potash is designed to capture the benefits of our excess capacity. We match supply to demand to minimize inventory overhang and we believe price and margin are more important than volumes. We focus on maintaining our low-cost position both in production and on a delivered basis. We expect to use our excess capacity and make capital investments as necessary to seamlessly provide the world with the appropriate amount of potash as consumption grows.

Growth in demand over the last three years (4.0 percent in 2002, 7.6 percent in 2003 and 9.9 percent in 2004) has absorbed nearly all of

the world’s excess capacity exclusive of PotashCorp. The threat of major new capacity in the form of a new mine is somewhat constrained, as we believe there are few geographic opportunities. According to industry consultants, a 2-million tonne greenfield operation would require approximately $1 billion in capital and a five-year lead time. We believe current potash margins do not support such investments.

Our competitors are debottlenecking and doing incremental expansions where possible, but none can bring up significant capacity as quickly and economically as we can. What’s more, their announced

| | STRENGTHS: |

| |

| o | 86 percent of world excess capacity to respond to growing world consumption |

| |

| o | Excess capacity can be brought on stream quickly with modest capital outlay |

| |

| o | Low-cost, flexible production with smaller percentage of fixed costs |

| |

| o | Long-term reserves from existing shafts |

| |

| o | Greater sales exposure in growing offshore market |

| |

| o | Few world producers, reduced government control |

| |

| o | Stable pricing historically with current upward trend |

| |

| o | High cost and long lead time to build greenfield capacity |

| |

| o | No greenfield operations initiated, providing us with a multi-year window |

| |

| o | No substitutable products for potash |

| |

| | WEAKNESSES: |

| |

| o | Competitors will continue with low-cost incremental expansions |

| |

| o | High provincial resource taxes (Saskatchewan) and federal income taxes relative to global competitors |

| |

| o | High freight costs to ship Saskatchewan potash to port |

| |

| o | Exposure to Canadian dollar volatility |

| |

| o | Currently high ocean freight costs |

| |

| o | Water inflow continues to hurt New Brunswick margins |

| |

| o | Potential for rail transportation bottlenecks |

| |

| | OPPORTUNITIES: |

| |

| o | Ability to optimize excess capacity quickly and competitively |

| |

| o | Our competitors are operating at capacity, which should allow us to benefit from a significant portion of accelerated growth |

| |

| o | New deposit found in New Brunswick could resolve water inflow problem and allow expansion in a lower-tax environment |

| |

| o | Strategic acquisitions of other low-cost production in the world, including adding to our existing investments in APC, SQM and ICL |

| |

| | THREATS: |

| |

| o | Current upward trend in pricing could encourage new greenfield operations

|

| |

| o | Competitors’ debottlenecking of existing plants with a simultaneous drop in demand could offset potential market growth for us |

19

POTASHCORP 2004 ANNUAL REPORT | MD&A•Potash

BUSINESS

debottlenecking plans amount to approximately 2 million tonnes in the next six years, while the historical growth rate of 2 percent suggests 7 million tonnes will be required. We expect customers to turn to us to meet the majority of continuing growth in world consumption. As we increase our operating rate, we expect to be able to capitalize on our three leverage points of increased sales volumes, lower per-unit costs and higher sales prices. This leverage is further enhanced by our investments in other potassium-based companies: SQM, APC and ICL.

Transportation costs are increasingly important and our sales strategy is built with customer proximity in mind. We are advantaged supplying Asia and the US from our Saskatchewan operations and South and Central America from New Brunswick. This allows for quicker and more cost-efficient delivery to some key markets – an important factor as ocean freight rates climbed to unprecedented levels in 2003 and stayed high throughout 2004.

Offshore sales of our Saskatchewan potash are handled through our membership in Canpotex, which minimizes transportation and marketing costs. Approximately 60 percent of Canpotex sales are made on a delivered basis, meaning it pays the freight. Domestically, our strategy relies on a distribution network in the US and Canada that allows timely delivery to high-demand spring and fall markets. We optimize these systems, attempting to get the lowest freight rates possible.

Shifts in foreign currencies can affect our margins. As currencies, including the Canadian dollar, strengthen against the US dollar, translated production costs rise. With higher freight rates, this could

impact margins. Investments in companies such as APC have the advantage of providing a natural hedge against rising freight costs and currency fluctuations, as the Jordanian dinar is pegged to the US dollar.

PotashCorp will continue to review investment opportunities that offer freight advantages, provide economic hedges and expand our enterprise. We will also explore opportunities in upgraded potash (which offers higher returns and less volatility), consistent with our investment in SQM, the world’s largest producer of specialty upgraded potash products. We believe the strategic positioning of our existing potash operations and investments places us in the targeted top right quadrant.

CAPABILITY TO DELIVER

In potash, the ability to bring on excess capacity in a timely manner is key to our growing profitability. Tight global supply is increasing the need for potash production. In 2004, we went to four shifts at our Lanigan and Allan mines and reduced inventory shutdown weeks by nearly one-third, to 28 weeks. This increased our production to almost 8 million tonnes from 7.1 million tonnes in 2003. In 2005, we will have the capability to produce 9.6 million tonnes. This would reflect a full year of four shifts at Lanigan and Allan and, if demand warrants, further reduction in inventory shutdown weeks and vacation/maintenance shutdowns. It also reflects the 400,000-tonne, $80-million expansion at Rocanville. Our ability to bring this capacity on quickly is unmatched in our industry – especially with virtually no capital costs other than the Rocanville expansion.

As markets continue to grow, we can add another 2.9 million tonnes of capacity at a current estimated cost of $300 million. This represents one-fifth of the cost of developing the same amount of new greenfield capacity. Engineering design work is being conducted to evaluate a number of projects in Saskatchewan and New Brunswick to determine the optimum mix, with a view to being able to operate at full stated capacity of 12.5 million tonnes within three years, if the market requires.

We have also recognized the growing demand for granular product by customers in areas such as Brazil. With the expansion at Rocanville on stream, we are able to produce 1.5 million tonnes of granular product there to help meet the needs of these key customers. A further expansion to the compaction capability at Rocanville is currently under way. It will facilitate the production of an additional 0.5 million tonnes per year and is scheduled for completion in August 2005.

20

POTASHCORP 2004 ANNUAL REPORT | MD&A•Phosphate

BUSINESS

PotashCorp in the World Phosphate Scene

Phosphate is produced in 41 countries, with the United States the biggest producer, followed by China, Morocco and Russia. World capacity of the major phosphate fertilizer product, diammonium phosphate (DAP), has surged in recent years, and approximately 42 percent is traded across borders. US DAP production was built predicated on exports and historically much of it went to India and China, which are now developing their domestic production behind protective trade barriers. The current excess capacity for DAP production relative to consumption is depressing prices. Governments influence a significant proportion of world capacity through subsidy control or ownership, or by overproducing and accepting negligible to negative returns to support employment.

In North America, our major competitor for both fertilizer and feed products is Mosaic (formerly IMC Global and Cargill Crop Nutrition, which merged in October 2004), while imports from Morocco and Israel compete for industrial sales. In offshore markets, competition for fertilizer sales comes from indigenous producers in India and China and from other global producers. In China, indigenous producers compete for feed sales.

STRATEGY:Strength through diversification

In phosphate, we work to maximize the benefits of our long-term rock position, multi-year mining permits and high-quality rock that enables low-cost production and product diversity. The quality of our rock at Aurora and its integrated production facility place that plant in a more desirable position on our strategic profile than

| | STRENGTHS: |

| |

| o | Most diversified producer, making the entire range of phosphate products – solid and liquid fertilizers, feed and industrial

|

| |

| o | High-quality rock makes it possible to upgrade economically to more stable, higher-margin products |

| |

| o | Strong competitive cost position and tight global supply in purified acid |

| |

| o | Long-term deposits close to low-cost processing facilities |

| |

| o | Approximately 75 years of reserves in North Carolina at current operating rates |

| |

| o | Existing mining permits at Aurora for seven years and covering estimated life of mine at White Springs (17 years) |

| |

| | WEAKNESSES: |

| |

| o | US producer dependency on declining world DAP trade has led to lower sales volumes and operating rates |

| |

| o | High percentage of fixed costs means plants do not perform profitably at lower operating rates |

| |

| o | Current high raw material input costs for ammonia and sulfur |

| |

| o | Product diversity creates production requirements that increase costs |

| |

| o | Too much government intervention globally, either in constructing capacity or in restricting imports

|

| |

| o | Offshore sales heavily exposed to China and India, which seek self-sufficiency |

| |

| | OPPORTUNITIES: |

| |

| o | Our high-quality rock and proven technology allow us to expand production of the industrial product purified acid |

| |

| o | Production flexibility will allow us to streamline production at three operations to reduce costs |

| |

| o | Our strong competitive cost position in purified acid makes us less susceptible to offshore competition |

| |

| o | Resolution of DFP start-up problems should improve feed profitability |

| |

| o | Potential for industry shutdowns |

| |

| | THREATS: |

| |

| o | Excess world DAP capacity in many hands can easily be brought back on stream |

| |

| o | Depressed fertilizer prices could encourage others to expand into the feed business, hurting margins |

| |

| o | Competitors with liquidity issues are selling at lower prices to accelerate cash flow |

| |

| o | Higher barriers to exit because environmental costs force some companies to continue production at uneconomic levels, impacting supply/demand fundamentals |

21

POTASHCORP 2004 ANNUAL REPORT | MD&A•Phosphate

BUSINESS

White Springs. One of Aurora’s upgraded products is purified acid, which has higher, more stable margins and lessens the impact of the volatility of phosphate fertilizer.

Industry demand for purified acid continues to grow globally in response to demand for products that require it. Our position strengthened in 2004 when imports from China to the US were down 10 percent from 2003 and there was consolidation among US competitors. Barriers to entry – the need for high-quality rock as well as capital considerations – keep this product in our most desirable strategic positioning quadrant.

We continue to expand the purified acid business at Aurora, where we have proven technology and a strong, competitive cost position. Prices are favorable, and we will continue to look for opportunities to further diversify in purified acid.

Feed phosphates, our other diversification effort in phosphate, have suffered recently. Declining demand due to increased use of substitutes, and the fallout from DAP as competitors switched their phosphoric acid into feed, hurt supply/demand fundamentals. However, recent consolidation in the US feed industry may improve its strategic positioning.

CAPABILITY TO DELIVER

Keys to profitability in phosphate include diversification away from fertilizer products, high operating rates and minimizing the impact of high costs for inputs such as ammonia, sulfur and rock. Therefore, we are reallocating P2O5 away from the more competitive fertilizers to higher-margin products. In March 2003, we increased our

purified acid capacity at Aurora to 251,000 tonnes P2O5, and that production capacity is sold out. We are now installing an additional 82,000 tonnes of P2O5 capacity, to be complete in June 2006, and all output is already in demand by various companies. Together, these expansions have allowed us to divert 165,000 tonnes P2O5 away from fertilizer production.

We have announced three projects that will allow us to run at higher operating rates, decreasing costs without increasing solid fertilizer production tonnes: At Aurora’s DAP/acid facility, we will debottleneck the #2 plant and close the less efficient #1 plant; also at Aurora, the gypsum blend process will be streamlined to use more gypsum from direct blend filters; and, at White Springs, we will convert production of all phosphoric acid to the superior hemihydrate process, which will lower energy costs, increase production flexibility and produce a higher quality P2O5.

At approximately 30 percent of total production costs, rock is the largest controllable cost of producing P2O5. Rock inventory was allowed to build in two previous years as a safety cushion during the transition to another mining area at Aurora, and reduction of that inventory last year increased rock costs by 10 percent. Constant inventory levels of wet phosphate rock concentrate year over year and higher operating rates should reduce costs moving forward.

The new design of the DFP plant brought on stream at Aurora in 2003 created complications, which have prevented it from achieving full operating rates. We are working at resolving the problems with the anticipation of operating it at design capacity in 2005.

22

POTASHCORP 2004 ANNUAL REPORT | MD&A•Nitrogen

BUSINESS

PotashCorp in the World Nitrogen Scene

Nitrogen, the most widely produced nutrient, is a regional business. Ammonia, the feedstock for all downstream nitrogen products, can be manufactured in any country with adequate natural gas supplies, and approximately 60 countries do so. Ownership is widely dispersed around the globe, so only 13 percent of ammonia is traded. Several developing countries with large gas reserves and low production costs use little of their gas domestically, and monetize it by producing ammonia cheaply for the export market. China is the largest producer, followed by India, Russia and the US. Half of the industry is under government ownership so decisions are not necessarily based on economic considerations.

Rising natural gas costs in North America and Europe have led to plant closures, since gas is at least 70 percent of the cost of producing ammonia. The resulting tight supply has increased prices, attracting imports from areas of low-cost gas such as Trinidad, Venezuela, Russia and the Middle East. Increasingly, the US is supplied from offshore. Since 1999, approximately 4.5 million tonnes of US ammonia capacity has been permanently shut down, with a corresponding increase in imports of 55 percent.

Nitrogen is an input in industrial production of a wide range of products that enhance modern living. Manufacturers want consistent quality and just-in-time delivery to keep their plants running efficiently. Many are attached to their suppliers by pipeline.

GDP improvements in developing nations have historically supported growth in demand for these lifestyle products.

Within North America, sales are regionalized due to transportation costs. This limits competition from Agrium and other Canadian sources which serve a different geographic market. CF Industries, a cooperative, Koch, a private company, and Terra, a publicly traded company, are our main competitors, along with imports.

STRATEGY: Trinidad is key

Our nitrogen strategy is designed to benefit from favorable gas contracts in Trinidad. In North America, we employ natural gas hedges with the goal of minimizing risk from gas price swings and protecting US margins. We believe our nitrogen position is spread along the bottom two quadrants of our strategic positioning profile, with our Trinidad operations in the superior right corner.

In nitrogen, North America is our primary market. We supply it through a combination of tonnes produced in Trinidad, US production and purchased tonnes which we re-sell, always seeking to source the highest-margin method of supply. Our multiple port facilities, warehouse and distribution network, dedicated sales and customer service teams and associated infrastructure make it possible to supply customers from this flexible production base.

Trinidad is home to more than 60 percent of our ammonia production. It has a stable government and is ideally situated to service the sizeable US market. Thus we are expanding this lower-cost facility.

23

POTASHCORP 2004 ANNUAL REPORT | MD&A•Nitrogen

BUSINESS

| | STRENGTHS: |

| |

| o | Long-term, lower-cost gas contracts in Trinidad |

| |

| o | Our gas hedging program in the US helps stabilize costs there |

| |

| o | Serve both fertilizer and industrial customers |

| |

| o | Some of our US plants are linked by pipeline to industrial customers willing to pay a premium for secure, high-quality supply |

| |

| o | We own/operate deepwater import terminals |

| |

| | WEAKNESSES: |

| |

| o | US plants depend on high-cost natural gas |

| |

| o | Plant ownership spread over many companies |

| |

| o | Contractual commitments to industrial customers may force us to operate unprofitably in a high-cost gas environment |

| |

| o | Small volume changes can significantly impact prices |

| |

| | OPPORTUNITIES: |

| |

| o | High volume demand in the US |

| |

| o | Plants in Trinidad being expanded to provide more cost-advantageous production |

| |

| o | Our US distribution system allows us to import and sell purchased tonnes |

| |

| o | Consolidation of US industry |

| |

| o | High cost of construction materials such as steel could delay new capacity, extending the current cycle |

| |

| | THREATS: |

| |

| o | Abundance of lower-cost natural gas in developing countries leads to new ammonia capacity as they attempt to monetize their gas resources

|

| |

| o | Competitors need only a short lead time to bring on new capacity when the supply/demand ratio is tight |

Our US plants, located in different regions, focus on industrial sales in which quality and security of supply are key. With varied production rates at these operations, we plan to maximize sales to industrial customers, supplemented by fertilizer sales, to run our plants at the highest possible operating rate to help control costs.

We currently operate three plants in the US: Augusta and Lima, producing a range of nitrogen products, and Geismar, the world’s largest nitric acid producer. Augusta is a highly competitive, economical plant with a strong industrial customer base. Lima is also a strong industrial supplier with a good inland location that is insulated from imports. We curtailed all production at Memphis and ammonia and nitrogen solutions production at Geismar in June 2003.

Our strategy moving forward also considers leveraging our marketing and operations expertise without significant capital

outlay through asset-light/fee-heavy arrangements. Our goal is to find investments where we provide the operating, management and marketing knowledge along with distribution resources, while our partner provides the assets. This has the potential to deliver stable returns for minimum investment.

CAPABILITY TO DELIVER

We have announced four debottlenecking expansions in Trinidad to capitalize on our lower-cost gas position there. The first two expansions are for approximately 138,000 tonnes of ammonia for $30 million; 69,000 tonnes will be available in the first quarter of 2005 and the rest in the third quarter. Subsequent expansions will increase capacity by a further 132,000 tonnes for $41 million. Half is expected to be available in the first quarter of 2006 and the remainder in the third quarter. US natural gas is expected to remain above $4.50 per MMBtu, which sets the floor price for US ammonia above $195 per tonne. Ammonia prices would have to fall below $140 per tonne before these expansions would provide a return of less than 15 percent.

In the US, we continue to utilize our gas hedging program to mitigate the risk of price volatility. Natural gas prices will determine the profitability of our hedging program and our ability to buy more cheaply, on average, than the market going forward. By using our distribution system for purchased tonnes, we can source product with the best margins.

24

POTASHCORP 2004 ANNUAL REPORT | MD&A•Sales

BUSINESS

PotashCorp Sales

STRATEGY: Be the supplier of choice

In our business, where products are similar and price is the most important influence on buying decisions, our goal is to move our customer base to the top right strategic position of highest volumes and highest margins. We want to be the supplier of choice to our customers, always getting the final opportunity to win their business. We seek to become the preferred supplier to high-volume, high-margin customers with the lowest credit risk.

CAPABILITY TO DELIVER

Customers’ perceptions of our ability to create value for them based on the price they pay for our products are fundamental to our ability to maintain and grow their business. Our dedicated sales teams for each product (fertilizer, feed and industrial) focus on increasing their specific knowledge to provide maximum value for customers. We follow up our sales with customer service that is available 24/7, and have strong technical support. We also do annual customer surveys. In our most recent survey, price was listed as the top purchasing criterion. However, beyond price, customers named “product quality” as the single most important factor influencing their buying decisions. The same research indicates that PotashCorp is rated by survey respondents from each customer group as having the highest product quality. In addition, at least three-quarters of those surveyed indicated that sustainability performance affected buying decisions, especially as it related to economic and safety, health and environmental performance. Recognizing its importance, PotashCorp focuses on this in customer communications and sets targets for improvement in these areas.

In North America, continued engagement with our customers, along with strategic alliances with dealers who warehouse our products, will influence our success in maintaining fertilizer market share. For feed, the proximity of our plants to customers is an advantage, as are our long-term relationships with purified acid customers. Additionally, our extensive North American distribution network gives us a logistical advantage in supplying the growing needs of all customers.

Our participation in the fertilizer sales organizations Canpotex and PhosChem, where we share marketing costs and volumes with other producers, is important to our offshore margins. These organizations maintain a network of agents in offshore markets, aimed at ensuring our products benefit from market growth.

As a producer of large volumes which are sold around the world, our success requires an efficient transportation system. This is achieved by operating our own transportation department, with a distribution

network of approximately 175 terminal and warehouse facilities and a fleet of approximately 6,600 railcars.

Rising sales of North American grain and other commodities have affected the availability of railcars for potash. CN Rail handles our North American rail shipments. In response to the growing demand and potential increase in rates, we signed a long-term agreement with CN through 2010, which will deliver annual savings. CN has committed to meeting our North American growth and has therefore added 60 locomotives and 500 covered hopper cars.

Rail from Saskatchewan to west coast ports is handled by CP Rail, Canpotex’s primary carrier. CP has committed to meet Canpotex’s offshore growth by investing approximately $1 billion in improvements that will include 24 more locomotives and 600 more covered hopper cars, for a total of 1,500. Canpotex’s private hopper car fleet will increase from 1,960 cars to 3,260 by mid-2005 to meet the growing demand.

The relationship between costs and return on our investment in the system is key. Recent increases in ocean freight rates are raising our cost to deliver to offshore customers that purchase potash on contracts with freight included. In response to the volatile and rising ocean freight rates, Canpotex plans to increase its fixed freight agreements from 15 percent in 2003 to a target of over 50 percent in 2005. For our sales out of New Brunswick, we negotiated a three-year freight contract for 60 percent of sales from there to Brazil.

25

POTASHCORP 2004 ANNUAL REPORT | MD&A•Key Performance Drivers

BUSINESS

Key Performance Drivers

Each year we set targets to advance our goals and drive results. In 2004 we further developed key performance indicators to monitor our progress and measure success. As we drill down the organization with these metrics, we believe:

| • | management will focus on the most important things, which will be reinforced by having the relevant results readily accessible; |

| |

| • | employees will understand and be able to effectively monitor their contribution to the achievement of corporate goals; and |

| |

| • | we will be even more effective in meeting our targets. |

Recognizing that this is an evolving process, we began by examining the company’s long-term goals and developing metrics to measure progress.

We achieve our goal of outperforming comparable companies by maximizing shareholder wealth through increasing sales of our products with more stable and higher margins. At the corporate level, the key performance metric for maximizing shareholder wealth is total shareholder return, on both an annual basis and a sustaining basis. Supporting metrics which contribute to this are cash flow return versus our weighted average cost of capital, EBITDA multiple relative to our peers, and sales and gross margin growth.

In our sales and production divisions, the metrics are cash flow return at the divisional gross margin level and associated working capital. We measure our success at increasing sales of products with stable, desirable margins by analyzing volumes, revenue and gross margin for all sales within each nutrient. The question we ask ourselves is, “Have we optimized our gross margin on a product and customer mix basis?”

The metrics for achieving our goal of being the preferred supplier are the number of complaints we receive and order fill rate categories. We also do annual customer surveys to measure our effectiveness at every stage of the sales transaction and how we compare with our competitors. Our goal is to outperform and be in the top quartile. We are establishing monthly surveys to monitor customer attitudes about our quality and service.

We recognize that being a low-cost supplier is essential to sustaining profitability. We achieve this goal by reducing cash costs and spending appropriate sustaining capital to maintain low costs and productivity. The metrics for success at the corporate level are total cost per tonne of each nutrient or primary product and supporting selling and administrative expense. In sales, we measure percentage of customer shipments by preferred carrier and route, associated transportation and distribution expense, freight cost, sales expense and number of tonnes per sales representative. For all nutrients, performance reliability relative to maintenance cost is measured.

Reducing injury rates and environmental impact will help us achieve our goal of no harm to people, no accidents and no damage to the environment. Lost-time and recordable injury rates and environmental events such as reportable releases and permit excursions measure the components of this goal.