| Profit Announcement For the half year ended 31 December 2003 |

| Results have been subject to an independent review by the external auditors. Released 11 February 2004 |

This Profit Announcement is available on the Internet at:

www.commbank.com.au

Table of Contents

Highlights | 3 | ||||

| Key Performance Indicators | 3 | ||||

| Financial Performance and Business Review | 4 | ||||

| Market share | 4 | ||||

| Which new Bank initiative | 5 | ||||

| Outlook | 5 | ||||

| Balance Sheet Summary | 7 | ||||

| Shareholder Summary | 7 | ||||

| Productivity and Efficiency | 7 | ||||

Banking Analysis | 8 | ||||

| Key Performance Indicators | 8 | ||||

| Financial Performance and Business Review | 9 | ||||

| Profit Summary | 10 | ||||

| Major Balance Sheet Items | 12 | ||||

Funds Management Analysis | 15 | ||||

| Key Performance Indicators | 15 | ||||

| Financial Performance and Business Review | 15 | ||||

| Profit Summary | 16 | ||||

| Funds Under Management | 17 | ||||

Insurance Analysis | 19 | ||||

| Key Performance Indicators | 19 | ||||

| Financial Performance and Business Review | 19 | ||||

| Profit Summary | 20 | ||||

| Inforce Premiums | 21 | ||||

Shareholder Investment Returns | 23 | ||||

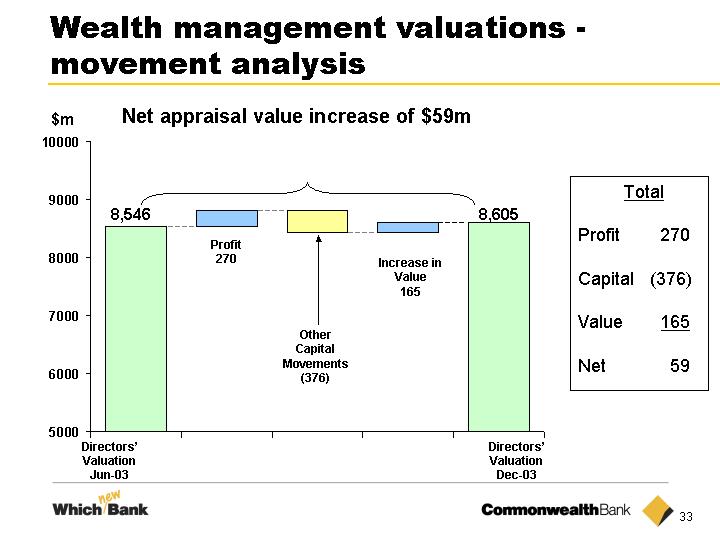

Life Company Valuations | 24 | ||||

Statutory Financial Report | 25 | ||||

| Directors Report | 25 | ||||

| Consolidated Statement of Financial Performance | 26 | ||||

| Consolidated Statement of Financial Position | 27 | ||||

| Consolidated Statement of Cash Flows | 28 | ||||

Notes to the Financial Statements | 29 | ||||

Directors’ Declaration | 39 | ||||

Independent Review Report | 40 | ||||

Appendices | |||||

| 1. Net Interest Income | 42 | ||||

| 2. Net Interest Margin | 42 | ||||

| 3. Average Balances and Related Interest | 43 | ||||

| 4. Interest Rate and Volume Analysis | 46 | ||||

| 5. Other Banking Operating Income | 48 | ||||

| 6. Operating Expenses | 48 | ||||

| 7. Integrated Risk Management | 49 | ||||

| 8. Capital Adequacy | 51 | ||||

| 9. Share Capital | 53 | ||||

| 10. Life Company Valuations | 54 | ||||

| 11. Intangible Assets | 58 | ||||

| 12. Amortisation Schedule | 58 | ||||

| 13. Definitions | 59 | ||||

Terms used in the Profit Announcement are defined in Appendix 13.

| For further information contact: | ||

| Carolyn Kerr | - | Investor Relations |

| Ph:02 | 9378 5130 | |

| Fax: | 02 9378 2344 | |

| E-mail address: | ir@cba.com.au | |

Except where otherwise stated, all figures relate to the half year ended 31 December 2003 and comparatives for the profit and loss are to the half year ended 31 December 2002. The term “prior comparative period” refers to the six months ended 31 December 2002. Comparisons on balance sheet are to 30 June 2003 unless otherwise stated.

Highlights

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v-31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

Profitability | ||||||||||||||||

| Underlying Segment Profit after Income Tax: | ||||||||||||||||

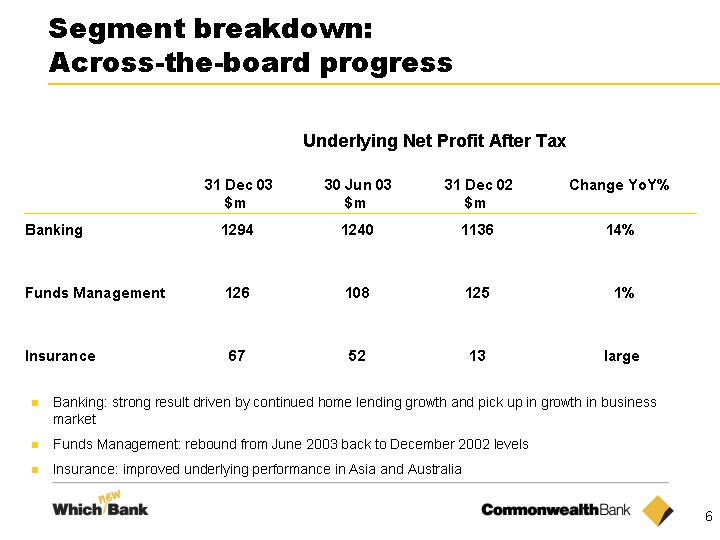

| Banking | 1,294 | 1,240 | 1,136 | 14 | ||||||||||||

| Funds Management | 126 | 108 | 125 | 1 | ||||||||||||

| Insurance | 67 | 52 | 13 | large | ||||||||||||

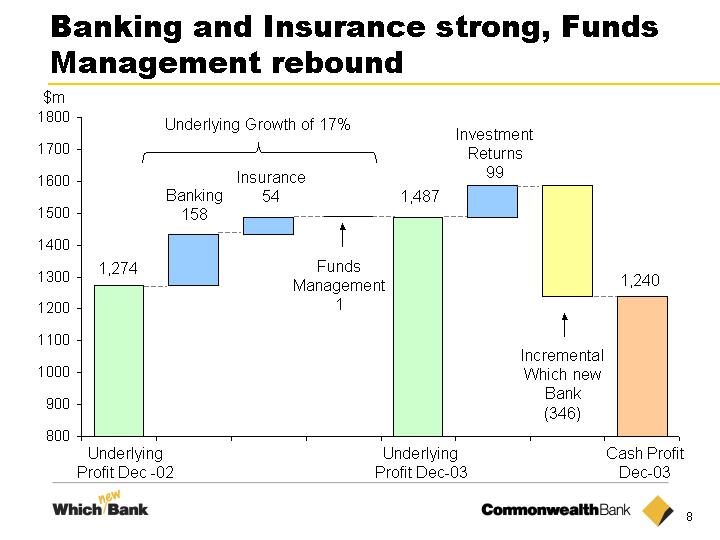

Underlying Profit after Income Tax | 1,487 | 1,400 | 1,274 | 17 | ||||||||||||

| Shareholder investment returns (after tax) | 99 | 81 | (8 | ) | large | |||||||||||

| Initiatives including Which new Bank (after tax) (1) | (346 | ) | (110 | ) | (58 | ) | large | |||||||||

Net Profit after Income Tax (“cash basis”) | 1,240 | 1,371 | 1,208 | 3 | ||||||||||||

| Goodwill amortisation | (162 | ) | (162 | ) | (160 | ) | 1 | |||||||||

| Appraisal value uplift/(reduction) | 165 | 181 | (426 | ) | large | |||||||||||

Net Profit after Income Tax (“statutory basis”) | 1,243 | 1,390 | 622 | 100 | ||||||||||||

Banking | ||||||||||||||||

| Net interest margin (%) | 2.60 | 2.69 | 2.65 | (2 | ) | |||||||||||

| Average interest earning assets | 204,323 | 192,942 | 183,675 | 11 | ||||||||||||

| Average interest bearing liabilities | 188,688 | 178,069 | 171,460 | 10 | ||||||||||||

Funds Management | ||||||||||||||||

| Funds under management | 100,383 | 94,207 | 95,266 | 5 | ||||||||||||

Insurance | ||||||||||||||||

| Inforce premiums | 1,102 | 1,076 | 1,040 | 6 | ||||||||||||

| Shareholder Investment Returns (before Tax) | 141 | 96 | (5 | ) | large | |||||||||||

Operating Expenses | ||||||||||||||||

| Operating expenses | 2,709 | 2,685 | 2,627 | 3 | ||||||||||||

| Initiatives including Which new Bank (1) | 494 | 156 | 83 | large | ||||||||||||

| Total | 3,203 | 2,841 | 2,710 | 18 | ||||||||||||

Underlying Productivity | ||||||||||||||||

| Banking expenses to income (%) | 50.7 | 51.9 | 52.2 | (3 | ) | |||||||||||

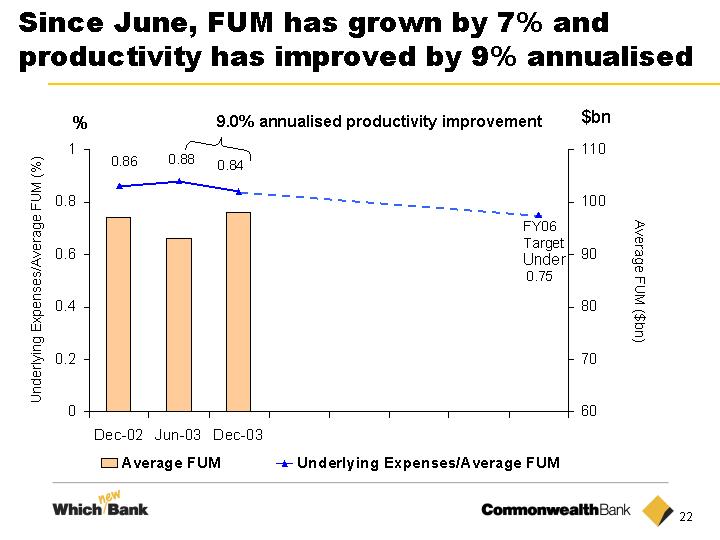

| Funds Management expenses to average funds under management (%) | 0.84 | 0.88 | 0.86 | (2 | ) | |||||||||||

| Insurance expenses to average inforce premiums (%) | 45.5 | 47.7 | 52.8 | (14 | ) | |||||||||||

Shareholder Measures | ||||||||||||||||

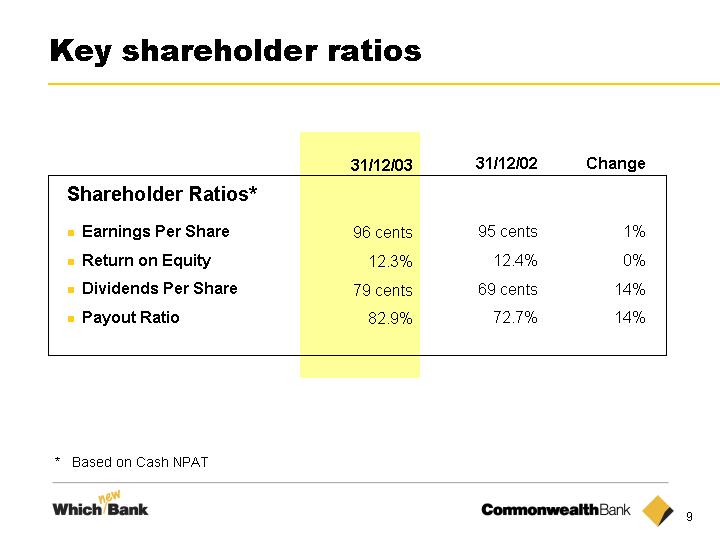

| Return on equity — cash basis | 12.33 | 13.95 | 12.39 | — | ||||||||||||

| EPS — cash basis — basic (cents) | 95.5 | 107.7 | 95.0 | 1 | ||||||||||||

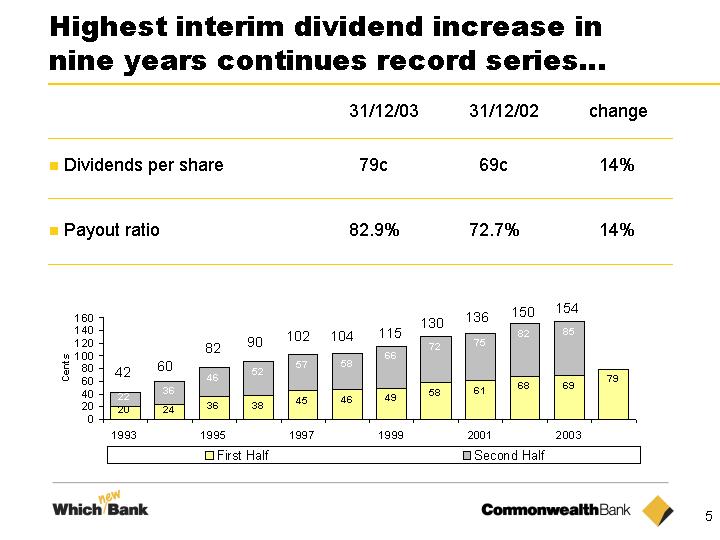

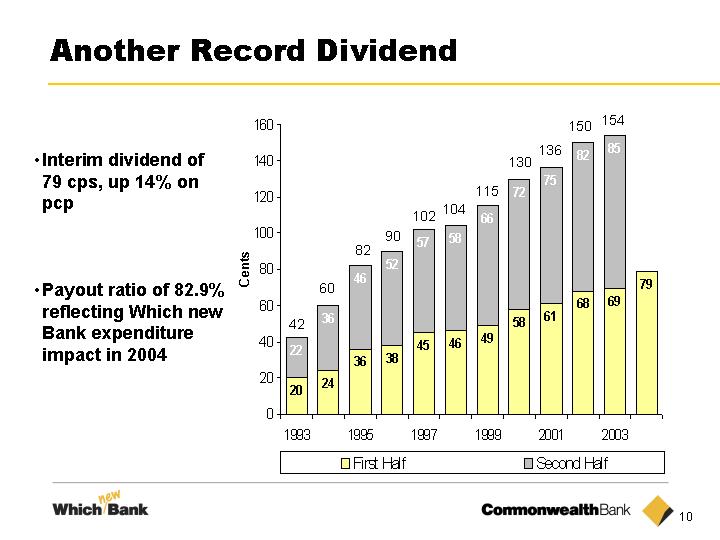

| Dividend per share (cents) | 79 | 85 | 69 | 14 | ||||||||||||

| Dividend payout ratio (%) | 82.9 | 79.0 | 72.7 | 14 | ||||||||||||

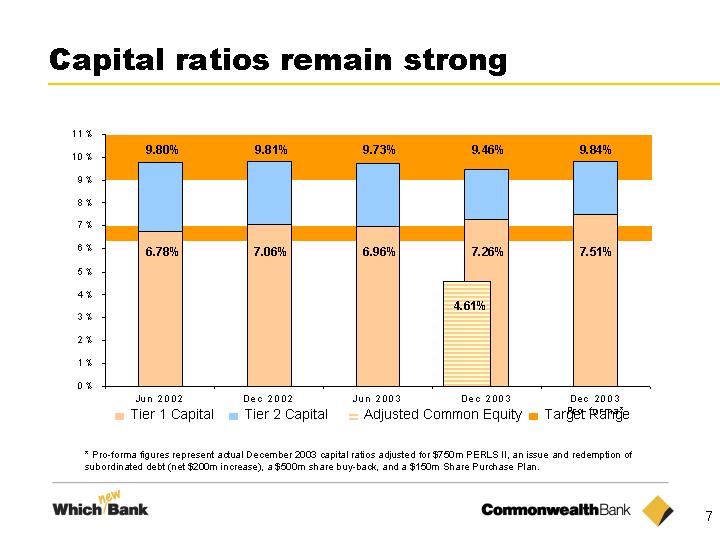

Capital Adequacy | ||||||||||||||||

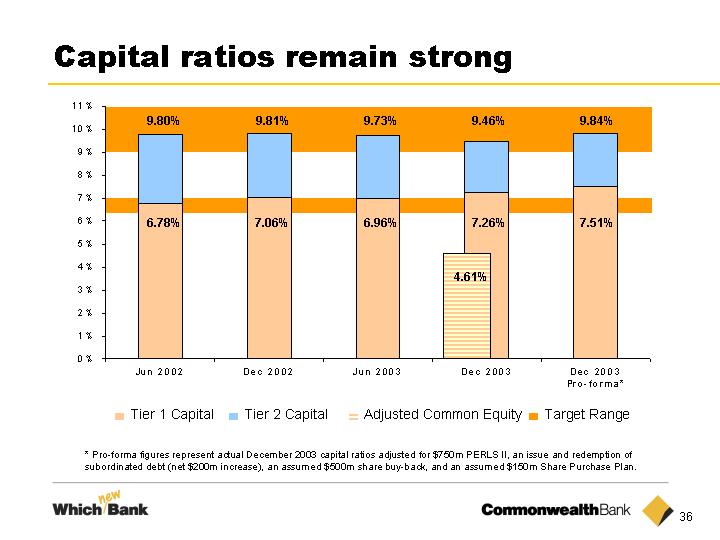

| Tier 1 (%) | 7.26 | 6.96 | 7.06 | 3 | ||||||||||||

| Total (%) | 9.46 | 9.73 | 9.81 | (4 | ) | |||||||||||

Full-time Staff Equivalent (FTE’s) | 34,956 | 35,845 | 36,421 | (4 | ) | |||||||||||

| (1) | December 2003 results include Which new Bank, while prior year includes strategic initiatives undertaken and June 2002 ESAP costs paid in October 2002. |

Underlying measures exclude shareholder investment returns and the cost of initiatives (including Which new Bank) along with their associated tax if relevant. This represents core operating performance, removing the volatility of shareholder earnings and the impact of strategic initiatives.

3

Highlights (cont’d)

Financial Performance and Business Review

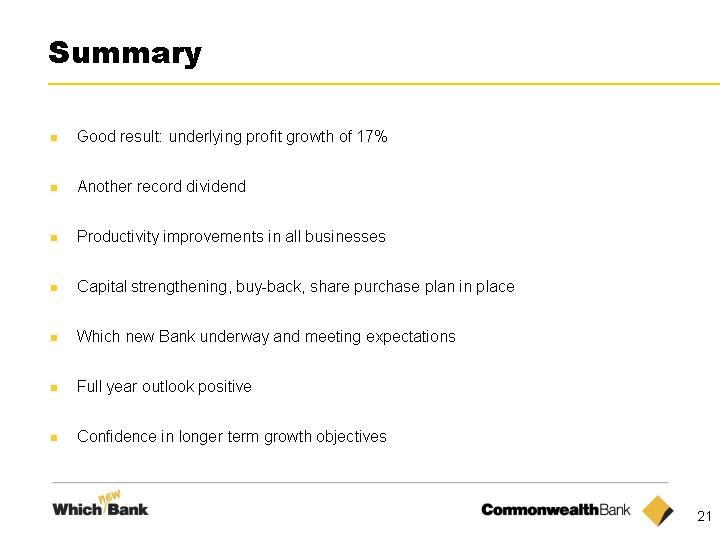

The Bank’s net profit after tax (“statutory basis”) for the six months ended 31 December 2003 was $1,243 million. This is against a net profit after tax of $622 million for the six months ended 31 December 2002, which included a reduction in the appraisal value of controlled entities of $426 million, compared with an increase of $165 million in the appraisal value in the current period.

The net profit after tax (“cash basis”) for the period was $1,240 million, an increase of 3% over the prior comparative period. This result was achieved inclusive of $346 million (after tax) of incremental expenses in relation to the Which new Bank strategic initiative.

The Bank posted a strong core operating result for the six months ended 31 December 2003, with net profit after tax (“underlying basis”) up 17% to $1,487 million from $1,274 million at 31 December 2002.

This result reflects a strong performance in the Australian and New Zealand retail banking operations, driven primarily by strong growth in the housing market. Housing assets increased by 12% over the six months ending 31 December 2003 to $112 billion up from $100 billion as at 30 June 2003. The New Zealand performance represents above market growth across the portfolio.

Results for the Institutional and Business Services business has shown modest growth over the six months, reflecting improved market conditions combined with the more customer focussed business model implemented through the IBS redesign program during the second half of the last financial year and continuing in this financial year.

In Funds Management, stronger equity markets contributed to a rise in funds under management, an improvement in investor confidence and the levels of funds flow. Underlying net profit after tax of $126 million was up 1% on the prior comparative period, while the underlying net profit on a pre-tax basis was up 7% to $173 million. Funds under management levels have recovered significantly since June 2003.

Insurance results were strong, with underlying net profit after tax of $67 million, compared with $13 million in the prior comparable period. The increase was across all regions, particularly Australia and Asia. The Insurance result was restated for prior periods to include the General Insurance operations.

Underlying productivity across all three segments has improved since June 2003. Underlying operating expenses increased by 3% on the prior comparative period. This reflects growth in banking volumes, the full year effect of the establishment of the Premium Financial Services business, general Enterprise Bargaining Agreement (EBA) wage increases partly offset by benefits from prior period initiatives and reduced Asian expenses as a result of business disposals and cost management.

Credit quality in the lending portfolio has continued to improve with very low levels of corporate defaults. The bad debt charge as a percentage of risk weighted assets remained largely unchanged at 0.10% at 31 December 2003 compared with 0.11% at 31 December 2002.

Dividends

The interim dividend declared for the half year is another record at 79 cents per share, an increase of 10 cents or 14.5% on the prior comparative period. For the current half year, the dividend takes into acount the expense in relation to the Which new Bank initiative. As a result, the dividend payout ratio for the half year is 82.9% compared with a payout ratio of 72.7% in the prior comparative period.

This dividend payment is fully franked and will be paid on 30 March 2004 to owners of ordinary shares at the close of business on 20 February 2004 (record date). Shares become ex-dividend on 16 February 2004.

The Bank issued $201 million of shares to satisfy shareholder participation in the Dividend Reinvestment Plan (DRP) in respect of the final dividend for 2002/03. It expects to issue around $189 million of shares in respect to the DRP for the interim dividend for 2003/04.

Dividends are based on net profit after tax (“cash basis”) per share, having regard to the following:

| • | Rate of business growth; |

| • | Capital adequacy; |

| • | Investment requirements; |

| • | The cyclical nature of investment returns and expectations of long term investment returns; and |

| • | A range of other factors. |

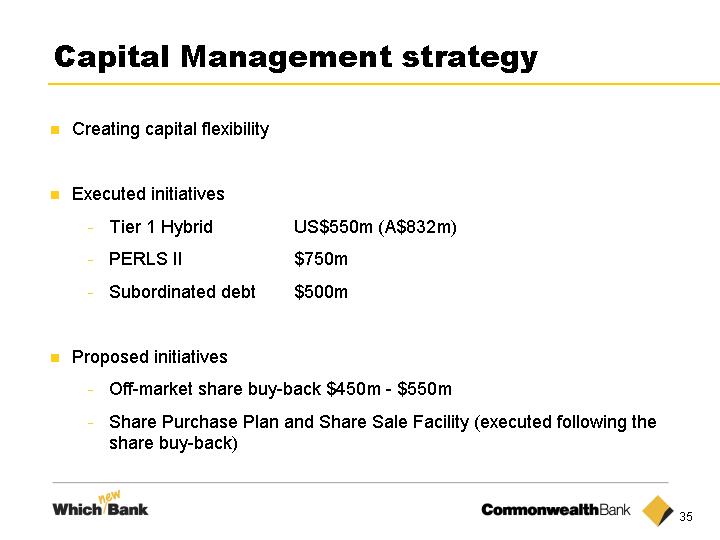

Capital Management

The Bank maintains a strong capital position. This is recognised in its credit ratings. The Bank’s credit ratings remained unchanged during the period.

| Long- | Short- | |||||||||||

| term | term | Affirmed | ||||||||||

| Fitch Ratings | AA | F1+ | Feb 03 | |||||||||

| Moody’s Investor Services | Aa3 | P-1 | Dec 03 | |||||||||

| Standard & Poor’s | AA- | A-1+ | Sep 03 | |||||||||

Risk Weighted Capital Ratios

| 31/12/03 | 30/06/03 | 31/12/02 | ||||||||||

| % | % | % | ||||||||||

| Tier one | 7.26 | 6.96 | 7.06 | |||||||||

| Tier two | 3.56 | 4.21 | 4.08 | |||||||||

| Less deductions | (1.36 | ) | (1.44 | ) | (1.33 | ) | ||||||

| Total capital | 9.46 | 9.73 | 9.81 | |||||||||

| Adjusted Common Equity (ACE) (1) | 4.61 | |||||||||||

| (1) | The ACE ratio has been calculated in accordance with the Standard & Poor’s methodology. As this is the first time the Bank has disclosed this ratio, no comparatives are published. |

The Bank’s capital position remains strong. A more detailed explanation of the movements in the capital ratios are set out on page 51.

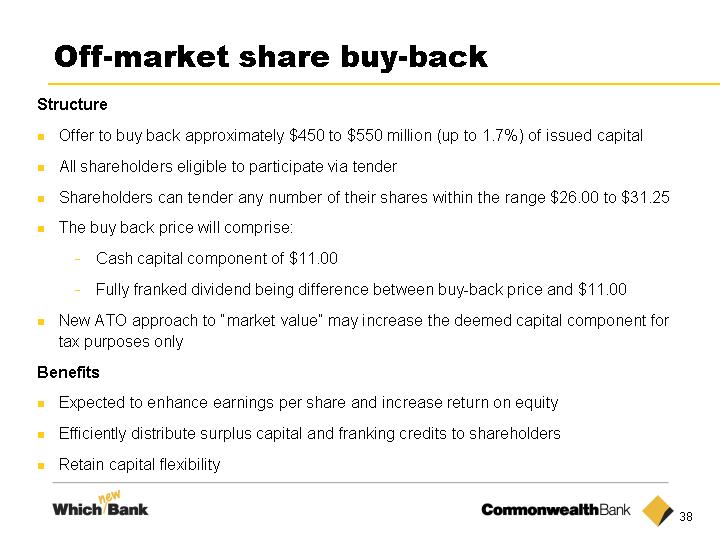

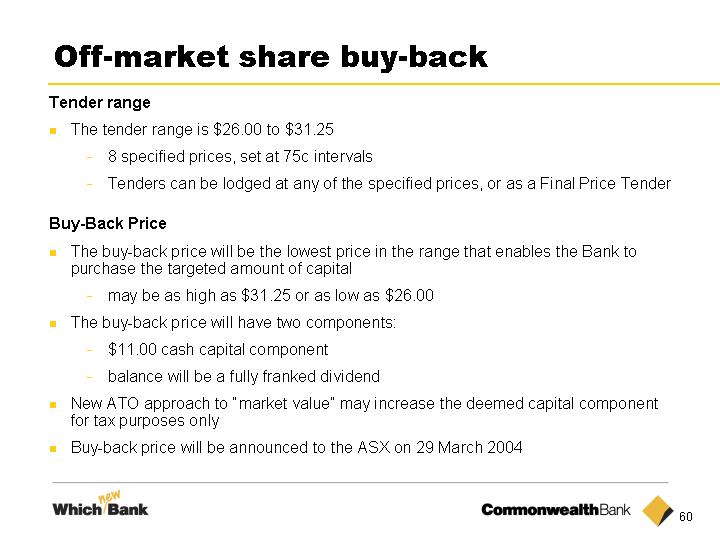

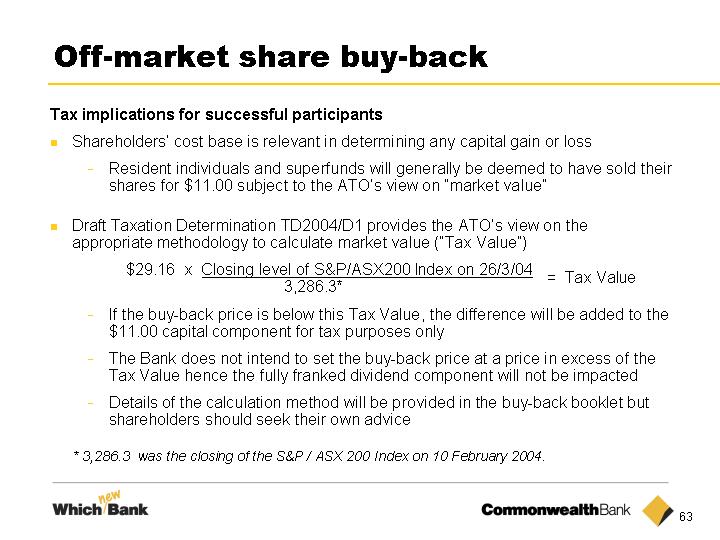

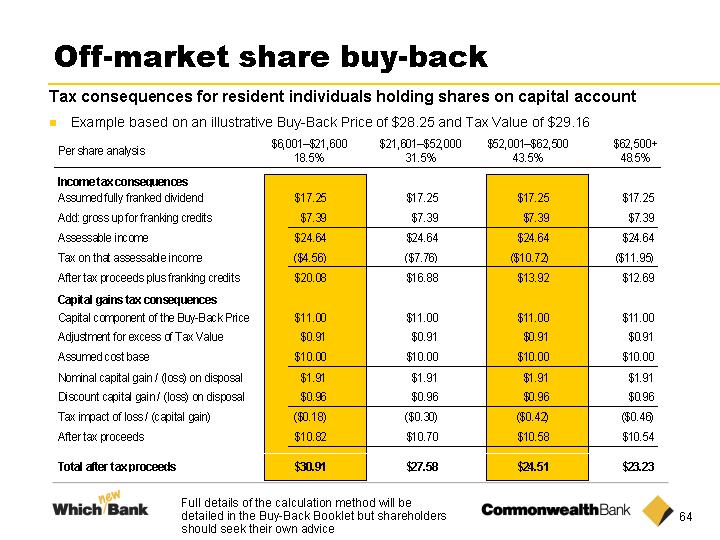

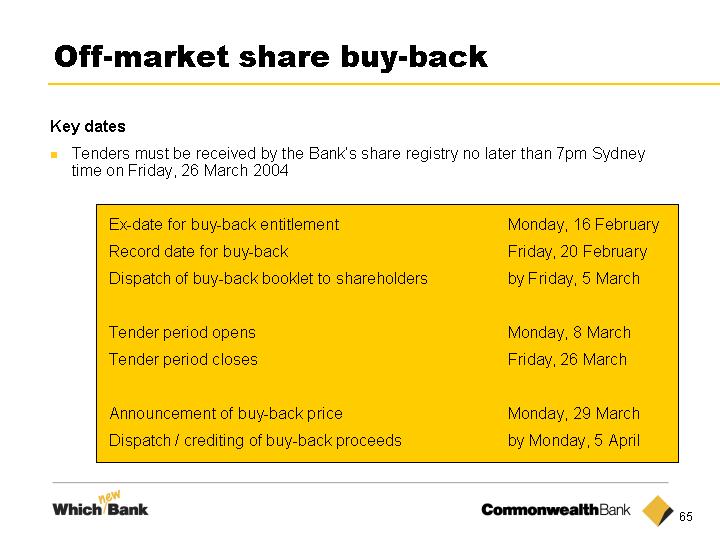

An off-market buy-back of $450 million to $550 million is planned for March 2004. This is expected to result in enhanced EPS and improved ROE. The ultimate size of the buy-back is at the discretion of Directors and will be dependent on market conditions at the time.

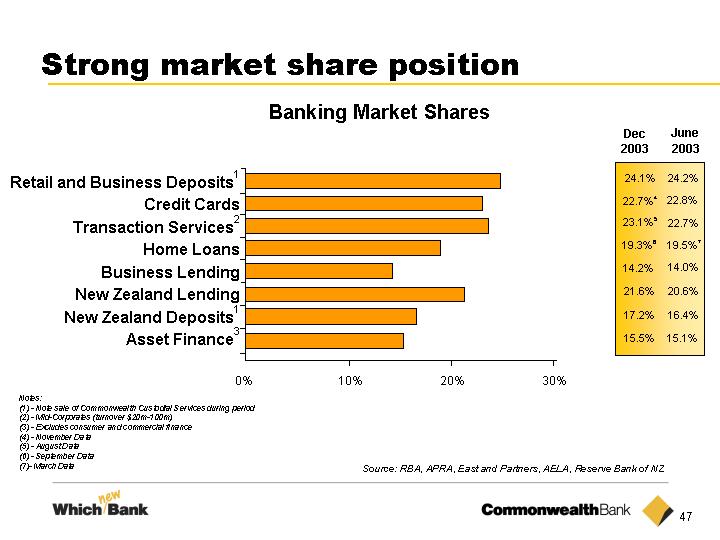

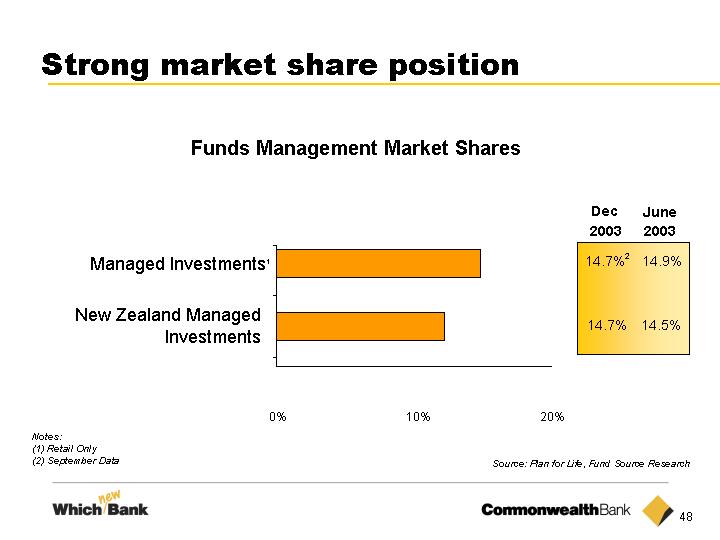

Market share

The table below sets out the latest available market shares for the current and prior period along key product lines.

| Line of Business | 31/12/03 | 30/06/03(1) | ||||||||||

Banking | ||||||||||||

| Retail and Business Deposits | 24.1 | %(2) | 24.2 | % | ||||||||

| Credit Cards | 22.7 | %(3) | 22.8 | % | ||||||||

| Home Loans | 19.3 | %(4) | 19.5 | %(6) | ||||||||

| New Zealand Lending | 21.6 | % | 20.6 | % | ||||||||

| New Zealand Retail Deposits | 17.2 | % | 16.4 | % | ||||||||

| Transaction Services | 23.1 | %(5) | 22.7 | % | ||||||||

| Business Lending | 14.2 | % | 14.0 | % | ||||||||

| Asset Finance | 15.5 | % | 15.1 | % | ||||||||

Funds Management | ||||||||||||

| Australia Retail | 14.7 | %(4) | 14.9 | % | ||||||||

| New Zealand | 14.7 | % | 14.5 | % | ||||||||

Insurance | ||||||||||||

| New Zealand | 28.1 | %(4) | 28.3 | % | ||||||||

| Australia | 15.1 | %(4) | 15.3 | % | ||||||||

| Hong Kong | 2.2 | %(4) | 2.2 | % | ||||||||

| (1) | Actual June 2003 Market Share number which was generally unavailable at the time of the previous profit announcement and includes an adjustment for any change in definitions on the part of regulatory authorities (2) reflects sale of Commonwealth Custodian Services in October 2003 (3) as at November 2003 (4) as at September 2003 (5) as at August 2003 (6) as at March 2003 |

4

Highlights (cont’d)

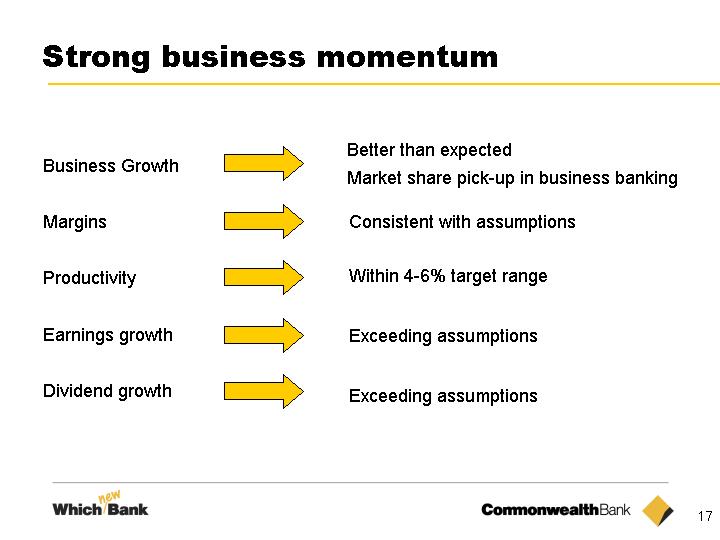

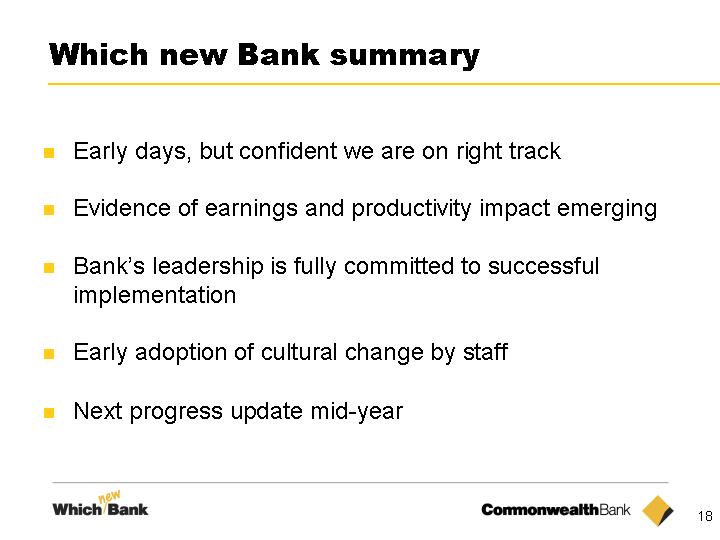

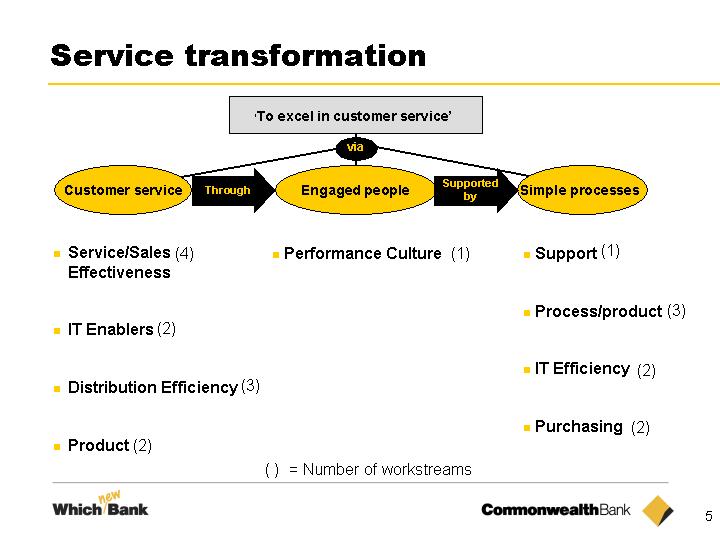

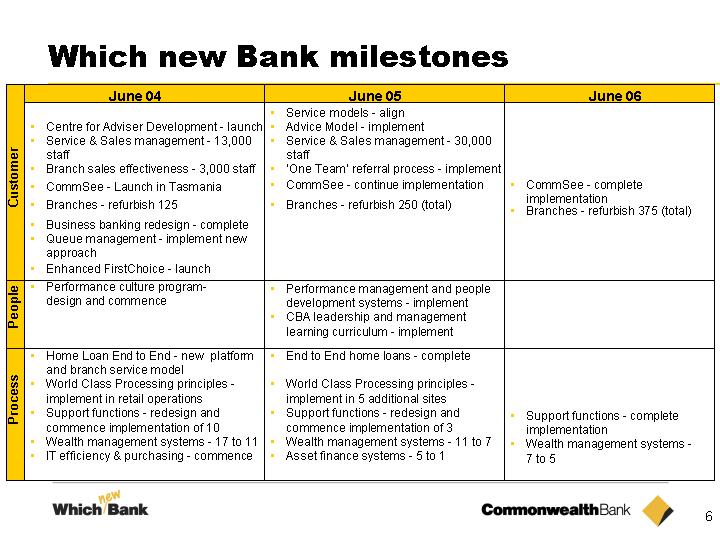

Which new Bank initiative

During September 2003, the Bank launched it’s Which new Bank initiative. The objective of this initiative is to excel in customer service through engaged people supported by simpler processes.

Outcomes will include faster service delivery and better quality advice, enhanced training for staff, simpler processes and less bureaucracy.

The Bank is pleased with the early stages of these initiatives where good progress has been made on several key workstreams. This has resulted in improved productivity across all businesses since June 2003. Over the life of the program, the improved customer service levels are expected to lead to growth in market share.

For the six months, total incremental spend on the Which new Bank initiative totalled $494 million pre-tax, ($346 million after-tax). The major categories of spend include the expensing of $210 million of previously capitalised software, $200 million of provisions for future spend and $134 million costs net of $45 million capitalisation. This incremental spend is after taking into consideration the normal level of project spend, which is $50 million pre-tax net of capitalisation. The $200 million provision covers expected retrenchment costs, consulting fees and other expenses.

The financial impact of Which new Bank for the half year is set out below:

| $m | Actual | |||

| 31/12/03 | ||||

| Initiative expenses incurred | 179 | |||

| Investment capitalised | (45 | ) | ||

| Provision for future costs | 200 | |||

| Expensing of previously capitalised software | 210 | |||

| Gross Which new Bank expense | 544 | |||

| Normal project spend (gross) | (70 | ) | ||

| Normal project spend capitalised | 20 | |||

Incremental Which new Bank expense | 494 | |||

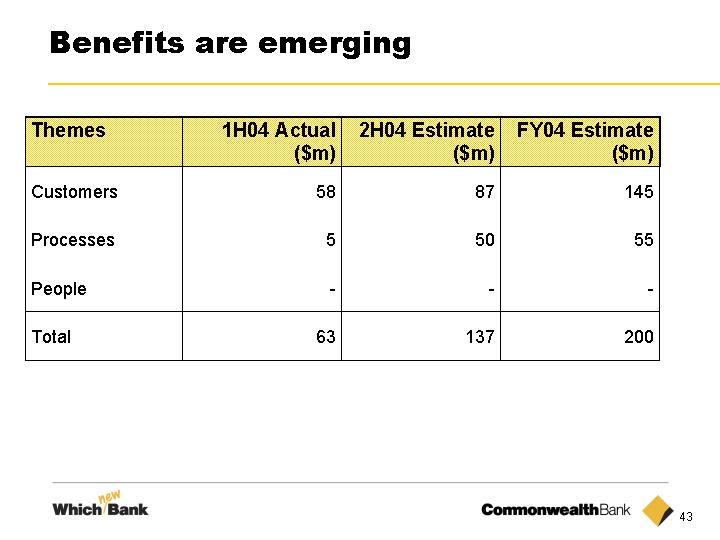

Net benefits realised during the six months ended 31 December 2003 total $63m pre-tax. These benefits are mainly ongoing cost savings, and were realised across the following areas:

| • | Redesign of Business and Corporate Banking and associated risk support. |

| • | Several initiatives in the Retail Banking Services and Premium Financial Services business. |

The Bank remains on track to meet the targets for the Which new Bank initiative that were announced in September 2003.

Further details on the specific initiatives are included in the business overview sections.

Outlook

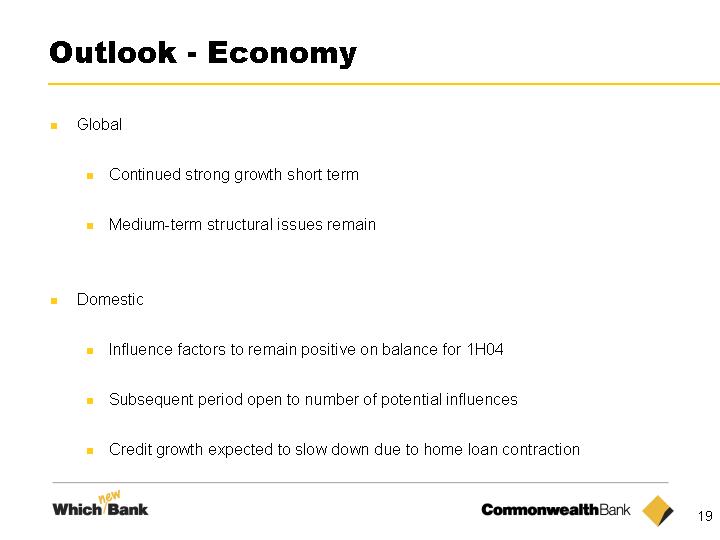

The global economy is expected to continue its strong growth in the short term. However, a number of medium-term structural issues remain, including the US current account deficit and the exchange rate re-alignment currently underway.

Factors influencing the Australian economy remain, on balance, positive and are expected to remain so for the first half of 2004. Beyond that, the interplay between household debt and interest rates, house prices and household wealth and the Australian Dollar could result in a slowing in credit growth.

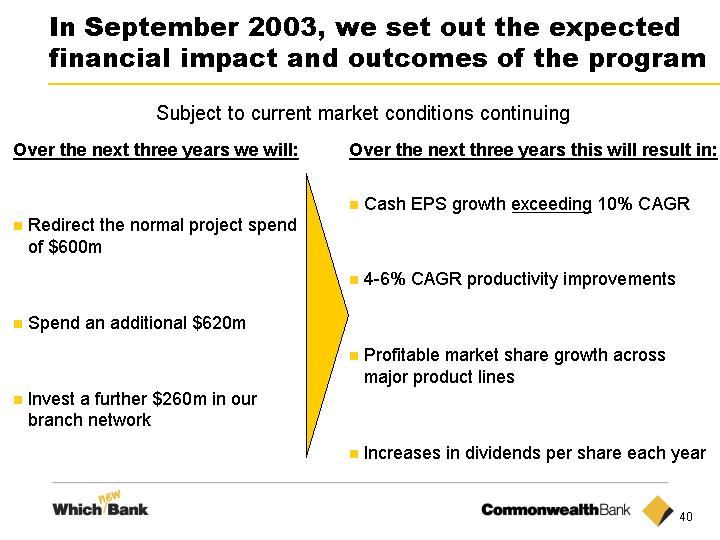

Subject to market conditions being maintained, the Bank is targetting growth in cash EPS exceeding 10% compound annual growth rate (CAGR) over the three years to 30 June 2006, which is expected to be ahead of the industry growth for the period. The Bank also expects to improve productivity by between 4-6% CAGR over this period and aims to grow profitable market share across major product lines and increase the dividend per share every year.

Growth in cash earnings was sufficient to offset Which new Bank expenses in the first half. The Bank reiterates the views expressed at the AGM that:

“At this stage, there appears to be sufficient momentum in the economy to support solid underlying earnings growth for the full year, although the rate of growth may moderate in the second half.

The Bank will add back the non-recurring transformation charges, in considering the amount to be distributed as dividends to shareholders. Consequently, as indicated in the Which new Bank announcement, we expect to be able to continue the uninterrupted pattern of increased dividends that we have been able to deliver since privatisation.”

In respect of Which new Bank, early signs of the positive impact of some of our initiatives on the Bank’s culture, processes and performance confirm that the course we are taking is the right way forward.

The Bank remains extremely well positioned to meet the challenges ahead and will benefit from scale, breadth of services and strength of its proprietary distribution systems.

5

Highlights (cont’d)

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| $M | $M | $M | % | |||||||||||||

Net Profit after Income Tax (“statutory basis”) | 1,243 | 1,390 | 622 | 100 | ||||||||||||

Net Profit after Income Tax (“cash basis”) | 1,240 | 1,371 | 1,208 | 3 | ||||||||||||

Net Profit after Income Tax (“underlying basis”) | 1,487 | 1,400 | 1,274 | 17 | ||||||||||||

| Net Interest Income | 2,671 | 2,572 | 2,454 | 9 | ||||||||||||

| Other banking income | 1,375 | 1,356 | 1,271 | 8 | ||||||||||||

| Funds management income | 582 | 540 | 575 | 1 | ||||||||||||

| Insurance income | 322 | 318 | 280 | 15 | ||||||||||||

Total Operating Income | 4,950 | 4,786 | 4,580 | 8 | ||||||||||||

| Shareholder investment returns | 141 | 96 | (5 | ) | large | |||||||||||

| Policyholder tax benefit/(expense) | 120 | 32 | (90 | ) | large | |||||||||||

Total Income | 5,211 | 4,914 | 4,485 | 16 | ||||||||||||

| Operating expenses | 2,709 | 2,685 | 2,627 | 3 | ||||||||||||

| Initiatives including Which new Bank(1) | 494 | 156 | 83 | large | ||||||||||||

Total Operating Expenses | 3,203 | 2,841 | 2,710 | 18 | ||||||||||||

| Charge for bad and doubtful debts | 150 | 154 | 151 | (1 | ) | |||||||||||

| Net Profit Before Income Tax | 1,858 | 1,919 | 1,624 | 14 | ||||||||||||

| Policyholder tax expense/(benefits) | 120 | 32 | (90 | ) | large | |||||||||||

| Corporate tax expense | 494 | 513 | 503 | (2 | ) | |||||||||||

| Outside equity interests | 4 | 3 | 3 | 33 | ||||||||||||

Net Profit after Income Tax (“cash basis”) | 1,240 | 1,371 | 1,208 | 3 | ||||||||||||

| Appraisal value uplift/(reduction) | 165 | 181 | (426 | ) | large | |||||||||||

| Goodwill amortisation | (162 | ) | (162 | ) | (160 | ) | 1 | |||||||||

Net Profit after Income Tax (“statutory basis”) | 1,243 | 1,390 | 622 | 100 | ||||||||||||

Contributions to Profit (after income tax) | ||||||||||||||||

| Banking | 1,294 | 1,240 | 1,136 | 14 | ||||||||||||

| Funds Management | 126 | 108 | 125 | 1 | ||||||||||||

| Insurance | 67 | 52 | 13 | large | ||||||||||||

Net Profit after Income Tax (“underlying basis”) | 1,487 | 1,400 | 1,274 | 17 | ||||||||||||

| Shareholder Investment Returns (after tax) | 99 | 81 | (8 | ) | large | |||||||||||

| Initiatives including Which new Bank (after tax)(1) | (346 | ) | (110 | ) | (58 | ) | large | |||||||||

Net Profit after Income Tax (“cash basis”) | 1,240 | 1,371 | 1,208 | 3 | ||||||||||||

| Appraisal value uplift/(reduction) | 165 | 181 | (426 | ) | large | |||||||||||

| Goodwill amortisation | (162 | ) | (162 | ) | (160 | ) | 1 | |||||||||

Net Profit after Income Tax (“statutory basis”) | 1,243 | 1,390 | 622 | 100 | ||||||||||||

| Half Year Ended | ||||||||||||||||

| Strategic Initiative Expenses and Shareholder | ||||||||||||||||

| Investment Returns(1) | Before Tax | After Tax | Before Tax | After Tax | ||||||||||||

| 31/12/03 | 31/12/03 | 31/12/02 | 31/12/02 | |||||||||||||

| "Underlying" measures exclude the following items: | $M | $M | $M | $M | ||||||||||||

Banking | ||||||||||||||||

| Initiatives | 463 | 324 | 56 | 39 | ||||||||||||

| ESAP | — | — | 27 | 19 | ||||||||||||

Funds Management | ||||||||||||||||

| Initiatives | 27 | 19 | — | — | ||||||||||||

| Investment returns | 14 | 10 | 5 | 4 | ||||||||||||

Insurance | ||||||||||||||||

| Initiatives | 4 | 3 | — | — | ||||||||||||

| Investment returns | 127 | 89 | (10 | ) | (12 | ) | ||||||||||

Total | ||||||||||||||||

| Initiatives | 494 | 346 | 56 | 39 | ||||||||||||

| ESAP | — | — | 27 | 19 | ||||||||||||

| Investment returns | 141 | 99 | (5 | ) | (8 | ) | ||||||||||

The current period benefits from initiatives of $63 million were reflected in operating expenses and operating income.

Throughout the report underlying measures exclude shareholder investment returns and incremental first time operating expenses, being strategic initiatives and the cost of the June 2002 ESAP paid in October 2002.

| (1) | December 2003 results reflects the Which new Bank initiative, while prior periods include strategic initiatives undertaken and the cost of the June 2002 ESAP paid in October 2002. |

6

Highlights (cont’d)

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Balance Sheet Summary | $M | $M | $M | % | ||||||||||||

| Total assets | 285,879 | 265,110 | 262,017 | 9 | ||||||||||||

| Total liabilities | 262,678 | 242,958 | 239,571 | 10 | ||||||||||||

| Shareholders’ equity | 23,201 | 22,152 | 22,446 | 3 | ||||||||||||

Assets held and Funds under Management | ||||||||||||||||

| On Balance Sheet Banking assets | 250,594 | 229,289 | 226,729 | 11 | ||||||||||||

| Insurance funds under management | 22,145 | 22,800 | 23,969 | (8 | ) | |||||||||||

| Other insurance and internal funds management assets | 13,140 | 13,021 | 11,319 | 16 | ||||||||||||

| 285,879 | 265,110 | 262,017 | 9 | |||||||||||||

| Off Balance Sheet | ||||||||||||||||

| Funds under management | 78,238 | 71,407 | 71,297 | 10 | ||||||||||||

| 364,117 | 336,517 | 333,314 | 9 | |||||||||||||

| Half Year Ended | |||||||||||||||||

| 31/12/03 | |||||||||||||||||

| -v- 31/12/02 | |||||||||||||||||

| Shareholder Summary | 31/12/03 | 30/06/03 | 31/12/02 | % | |||||||||||||

| Dividends per share — fully franked (cents) | 79 | 85 | 69 | 14 | |||||||||||||

| Dividend cover — cash (times) | 1.2 | 1.3 | 1.4 | (14 | ) | ||||||||||||

| Earnings per share (cents) | |||||||||||||||||

| Statutory — basic | 95.8 | 109.2 | 48.2 | 99 | |||||||||||||

| Statutory — fully diluted | 95.7 | 109.1 | 48.2 | 99 | |||||||||||||

| Cash basis — basic | 95.5 | 107.7 | 95.0 | 1 | |||||||||||||

| Cash basis — fully diluted | 95.5 | 107.6 | 94.9 | 1 | |||||||||||||

| Dividend payout ratio (%) | |||||||||||||||||

| Statutory | 82.7 | 77.9 | 143.2 | (42 | ) | ||||||||||||

| Cash basis | 82.9 | 79.0 | 72.7 | 14 | |||||||||||||

| Weighted average number of shares — basic (number) | 1,257 | 1,254 | 1,253 | 0 | |||||||||||||

| Weighted average number of shares — fully diluted (number) | 1,258 | 1,254 | 1,254 | 0 | |||||||||||||

| Half Year Ended | ||||||||||||||||||||

| 31/12/03 | ||||||||||||||||||||

| -v- 31/12/02 | ||||||||||||||||||||

| Productivity and Efficiency | 31/12/03 | 30/06/03 | 31/12/02 | % | ||||||||||||||||

Banking | ||||||||||||||||||||

| Expense to income (%) | 62.1 | 54.9 | 54.4 | 14 | ||||||||||||||||

| Underlying expense to income (%) | 50.7 | 51.9 | 52.2 | (3 | ) | |||||||||||||||

Funds Management | ||||||||||||||||||||

| Expense to average funds under management (%) | 0.90 | 0.96 | 0.86 | 5 | ||||||||||||||||

| Underlying expenses to average funds under management (%) | 0.84 | 0.88 | 0.86 | (2 | ) | |||||||||||||||

Insurance | ||||||||||||||||||||

| Expense to average inforce premiums (%) | 46.2 | 47.7 | 52.8 | (13 | ) | |||||||||||||||

| Underlying expense to average inforce premiums (%) | 45.5 | 47.7 | 52.8 | (14 | ) | |||||||||||||||

| Underlying staff expense/total operating income (%) | 25.86 | 26.43 | 26.46 | (2 | ) | |||||||||||||||

| Total operating income per FTE ($) | 141,607 | 133,519 | 125,752 | 13 | ||||||||||||||||

| Full time staff equivalent (FTE’s) | 34,956 | 35,845 | 36,421 | (4 | ) | |||||||||||||||

7

Banking Analysis

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

Profitability | ||||||||||||||||

Underlying Profit after Income Tax | 1,294 | 1,240 | 1,136 | 14 | ||||||||||||

| Initiatives including Which new Bank (after tax)(1) | (324 | ) | (84 | ) | (58 | ) | large | |||||||||

Net Profit after Income Tax (“cash basis”) | 970 | 1,156 | 1,078 | (10 | ) | |||||||||||

Operating Income | ||||||||||||||||

| Net interest income ($m) | 2,671 | 2,572 | 2,454 | 9 | ||||||||||||

| Net interest margin (%) | 2.60 | 2.69 | 2.65 | (2 | ) | |||||||||||

| Other banking income ($m) | 1,375 | 1,356 | 1,271 | 8 | ||||||||||||

| Total banking income ($m) | 4,046 | 3,928 | 3,725 | 9 | ||||||||||||

| Other banking income/Total banking income (%) | 34.0 | 34.5 | 34.1 | — | ||||||||||||

Operating Expenses | ||||||||||||||||

| Operating expenses ($m) | 2,051 | 2,037 | 1,945 | 5 | ||||||||||||

| Initiatives including Which new Bank(1)($m) | 463 | 118 | 83 | large | ||||||||||||

Productivity and Other Measures | ||||||||||||||||

| Expense to income (%) | 62.1 | 54.9 | 54.4 | 14 | ||||||||||||

| Expense to income — underlying (%) | 50.7 | 51.9 | 52.2 | (3 | ) | |||||||||||

| Effective corporate tax rate (%) | 29.8 | 28.6 | 30.3 | (2 | ) | |||||||||||

Balance Sheet | ||||||||||||||||

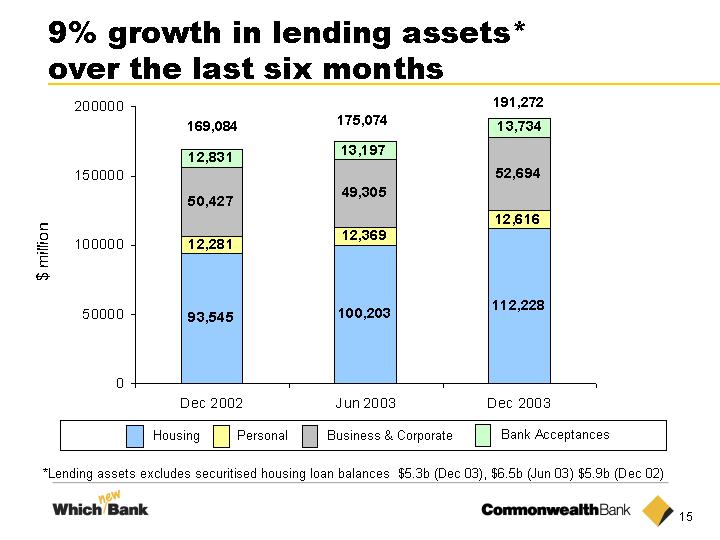

| Lending assets ($m) | 191,272 | 175,074 | 169,084 | 13 | ||||||||||||

| Average interest earning assets ($m) | 204,323 | 192,942 | 183,675 | 11 | ||||||||||||

| Average interest bearing liabilities ($m) | 188,688 | 178,069 | 171,460 | 10 | ||||||||||||

Asset Quality | ||||||||||||||||

| Charge for bad and doubtful debts ($m) | 150 | 154 | 151 | (1 | ) | |||||||||||

| Risk weighted assets ($m) | 157,471 | 146,808 | 143,771 | 10 | ||||||||||||

| Net impaired assets ($m) | 375 | 434 | 599 | (37 | ) | |||||||||||

| General provision/Risk weighted assets (%) | 0.86 | 0.90 | 0.92 | (7 | ) | |||||||||||

| Total provisions/Gross impaired assets (net of interest reserved) (%) | 271.6 | 239.4 | 184.1 | 48 | ||||||||||||

| Bad debt expense/Risk weighted assets (%) | 0.10 | 0.10 | 0.11 | (9 | ) | |||||||||||

| (1) | December 2003 results reflects the Which new Bank initiative, while prior periods include strategic initiatives undertaken and the cost of the June 2002 ESAP paid in October 2002. |

8

Banking Analysis (cont’d)

Financial Performance and Business Review

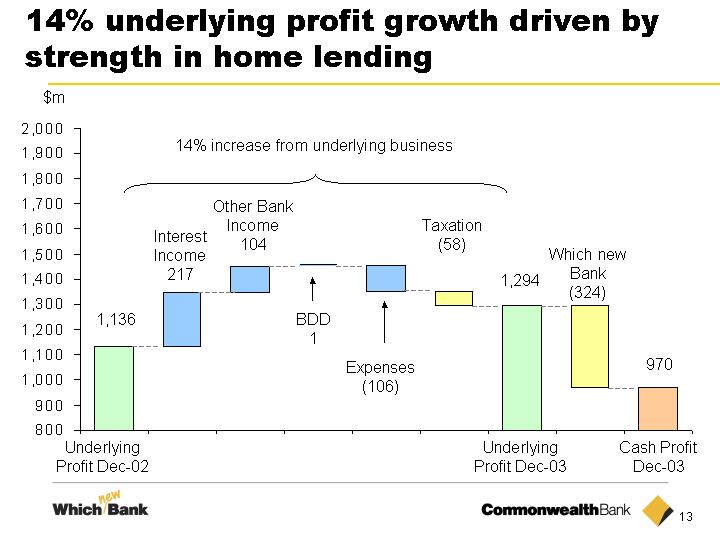

Banking operations continued to post strong results, with underlying net profit after tax up 14% or $158 million to $1,294 million from $1,136 million for the prior comparative period. On a cash basis, after reflecting incremental expenses on the Which new Bank initiative totaling $324 million (after tax), net profit was down $108 million or 10% to $970 million.

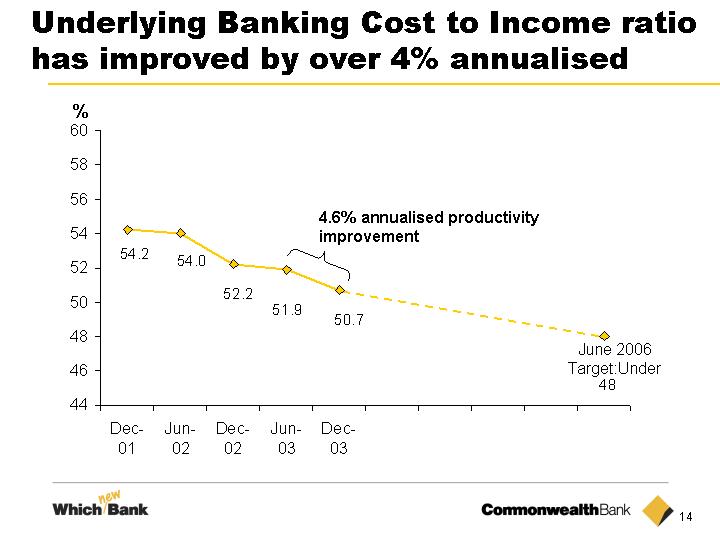

The strong underlying result was driven by higher home loan balances, higher credit card and ATM volumes and an improvement in trading and business activity. The underlying cost to income ratio continued to reduce from 52.2% for the prior comparative period to 50.7% for the half year ended 31 December 2003.

Retail

In retail banking operations, the performance for the half-year to December was driven by continued growth in the residential housing market, with record new approval volumes underpinning strong growth in net interest income, which was up 9% on the prior corresponding period. The strong revenue result was further supported by strong credit card sales and new deposit growth.

Going forward, opportunities for further market-driven revenue growth are expected to come under pressure from a slowing housing market and the impact of Reserve Bank credit card reforms. In an environment of heightened competitive pressures, the Bank is pursuing a service transformation program designed to ensure a better service outcome for our customers. Across the retail bank, highlights to-date have included:

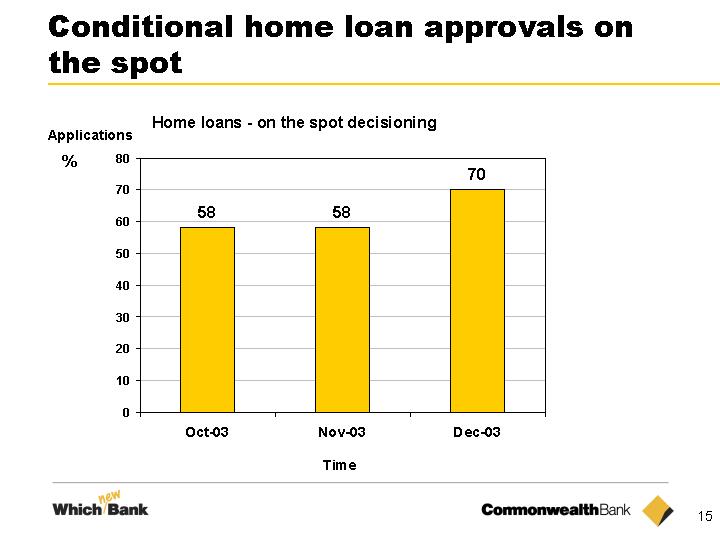

| • | Changes to our home loan process, which make applying for a new loan or changing details on an existing loan much simpler and easier. Through system and process improvements, the great majority of home loan applications are now either conditionally approved on the spot or within one business day. Around 70% of maintenance transactions (such as amending loan repayments) on existing loans can now be done immediately in the branch or over the telephone, compared with up to 10 days previously. |

| • | The refurbishment of 20 branches (at 31 December 2003) to a modern layout more conducive to effective customer service, with a further 105 branches to be completed by June 2004. This ongoing program will see more than 10% of branches modernised each year with a total investment of $260 million over the next three years. |

| • | A continued emphasis on reducing customer waiting times, with some branches showing up to a 50% improvement over the past six months. |

These actions represent the initial steps in a wide-ranging three year program that will transform the Bank’s service culture and results. Over the next twelve months, specific actions will include;

| • | Changes to frontline customer service roles from early 2004, designed to ensure a greater proportion of staff time is spent on servicing customers. Changes will be supported by additional skills training and new incentives for staff aligned to better customer service outcomes. Early trials of these changes in a selected number of branches have shown significant improvements in service and sales outcomes. |

| • | Changing the role of our branch managers so that up to 80% of their time is spent with their customers or coaching their staff. |

| • | Developing more efficient processes leading to faster approval times for credit cards and personal loans. |

| • | The introduction of a new, more efficient NetBank service with additional functionality by the end of 2004. |

Asia Pacific

Asia Pacific Banking incorporates the Bank’s retail and commercial banking operations in New Zealand, Fiji, and Indonesia. ASB Bank in New Zealand represents the majority of the Asia Pacific Banking business.

The New Zealand economy continued to grow strongly during the first half. Three successive interest rate reductions prior to August 2003 further boosted the housing sector. Total market lending as measured by Private Sector Credit (Residents only) grew by 8.2% in the year to November 2003. ASB Bank’s lending growth was 19.2%, more than double the market rate (source: Reserve Bank of New Zealand). The key drivers of the success were our first class sales and service performance, successful marketing campaigns and the continued momentum of the “One Team” referral program.

ASB Bank was recognised as the top major retail bank (for the sixth consecutive year) and business bank (for the fifth consecutive year) in the annual University of Auckland “Bank customer satisfaction survey”, resulting from the bank’s focus on customer service.

The banking operations in Indonesia and Fiji continued to achieve solid balance sheet growth.

Institutional & Business

The robust domestic economy, supported by improving global conditions, has sustained stronger momentum across all business segments. The environment has been conducive to maintaining good credit quality.

Significant transformation across all client segments and associated risk functions has improved client service standards, while achieving substantial productivity gains. While there was some slippage in lending market share during the implementation phase of this program, this has been recovered. Importantly, client satisfaction scores have continued to improve, providing positive feedback on the new service delivery models.

In Business Banking, we maintained our leading market share (source: Taylor Nelson Sofries). A range of successful marketing campaigns were conducted over the period. The support for regional and rural Australia, especially areas hard hit by the drought, was recognised at both State and Federal levels.

In Corporate Banking, we increased market share across a range of products while maintaining the leading market share for principal banker to mid-corporates and ranking first overall in client satisfaction for treasury services to mid-corporates (source: East & Partners).

A number of market leading transactions in commercial property and infrastructure finance were executed by the Institutional Banking teams. These included finance for the Chatswood Chase Shopping Centre acquisition, and acting as sponsor for the consortium that won the bid for the Sydney Basin airports.

The implementation for the Financial Services Reform Act (FSRA) has progressed well and our license is effective from 1 December 2003.

9

Banking Analysis (cont’d)

Profit Summary

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

| Net interest income | 2,671 | 2,572 | 2,454 | 9 | ||||||||||||

| Other operating income | 1,375 | 1,356 | 1,271 | 8 | ||||||||||||

Total Operating Income | 4,046 | 3,928 | 3,725 | 9 | ||||||||||||

| Operating expenses | 2,051 | 2,037 | 1,945 | 5 | ||||||||||||

| Initiatives including Which new Bank(1) | 463 | 118 | 83 | large | ||||||||||||

Total Operating Expenses | 2,514 | 2,155 | 2,028 | 24 | ||||||||||||

| Charge for bad and doubtful debts | 150 | 154 | 151 | (1 | ) | |||||||||||

Net Profit before Income Tax | 1,382 | 1,619 | 1,546 | (11 | ) | |||||||||||

| Income tax expense | 412 | 463 | 468 | (12 | ) | |||||||||||

Net Profit after Income Tax (“cash basis”) | 970 | 1,156 | 1,078 | (10 | ) | |||||||||||

| (1) | December 2003 results reflects the Which new Bank initiative, while prior periods include strategic initiatives undertaken and the cost of the June 2002 ESAP paid in October 2002. |

Net Interest Income

Net interest income increased by 9% or $217 million to $2,671 million for the six months ended 31 December 2003 while average interest earning assets increased by 11% or $20.6 billion to $204.3 billion over the same period. The average net interest margin (NIM) reduced by 5 basis points to 2.60%.

The increase in average interest earning assets comprises an increase of $16 billion in lending assets and $4 billion in investment and trading securities. The increase in average interest earning assets contributed $266 million to the increase in net interest income.

The largest contributor to the increase in average interest earning assets continued to be the strong residential lending market in Australia and New Zealand, with loan balances increasing by $12 billion or 12% since 30 June 2003, accounting for 75% of the total increase in lending assets.

The reduction of 5 basis points in the net interest margin from 2.65% for the six months to 31 December 2002 to 2.60% impacted net interest income by $49m. Factors impacting the margin reduction include:

| • | The strong growth in home loan balances was not matched by a similar increase in retail deposits, resulting in a higher reliance on wholesale funding. The net impact of the growth in home loans and higher reliance on wholesale funding reduced the net interest margin by 4 basis points. |

| • | Benefit from the two increases in the Australian cash rates contributed 1 basis point, although the impact of the second increase on 4 December was minimal for the period. |

| • | Margins in ASB Bank reduced as a result of three reductions in the cash rate in New Zealand prior to August and due to competitive pressures. This reduced the Bank’s overall net interest margin by 2 basis points. |

10

Banking Analysis (cont’d)

Other Banking Operating Income

Other Banking Operating Income

Other banking operating income increased by 8% or $104 million to $1,375 million for the half year compared with $1,271 million for the period ended 31 December 2002. Other banking operating income includes non-interest income earned on transaction accounts for the Bank’s personal, business and corporate customers.

The reasons for the increase in other operating income include:

| • | Fees and commissions increased by 12% or $80 million to $771 million. CommSec experienced record trading levels during the six months (exceeding 477,000 trades in October), resulting in an increase in commissions of $31 million or 84%. The acquisition and integration of TD Waterhouse effective 1 May 2003 also contributed to this increase. Credit card spend was up 15% while growth in transactional activity was also positive. Personal transaction fees are less than 5% of the Bank’s total income. |

| • | Lending fees increased by 9% or $28 million. Growth in retail lending fees was the result of the increased activity in home lending, margin lending and overdraft line fees, which was partly offset by increased mortgage brokerage and valuation fees. Institutional and Business fees increased, reflecting an improvement in market conditions relative to the prior comparative period. |

| • | Trading income was up 19% or $43 million, reflecting improved trading and market conditions in the reporting period compared with the half year ended 31 December 2002. |

| • | Other banking income decreased by $47 million to negative $7 million. The current period includes an equity accounted loss of an associate entity principally related to a change in its accounting policy. The prior period results included a loss on strategic investments. |

The income for General Insurance has been reallocated to the Insurance segment and prior period numbers and ratios have been restated. This reduced Banking other operating income by $24 million for the six months ended 31 December 2002 and $17 million for the year ended 30 June 2003, with a similar increase in the Insurance total operating income.

The income from tied financial planners was reallocated to Funds Management, reducing other banking operating income by $11 million for the six months ended 31 December 2002 and $18 million for the six months ended 30 June 2003.

Operating Expenses

Total operating expenses on a comparable business basis for the half year increased by 5% from $1,945 million in December 2002 to $2,051 million in December 2003. The increase was due to:

| • | Increases in volume related expenses including credit card loyalty. |

| • | The full year effect of establishing the Premium Financial Services business. |

| • | Salary increases of 4% awarded under the Enterprise Bargaining Agreement (EBA). |

| • | The net loss incurred as a result of a large fraud in Western Australia. |

These increases were partly offset by savings from prior period strategic initiatives.

Productivity Efficiency

The underlying banking expense to income ratio continued to improve from 51.9% for the six months ended 30 June 2003 to 50.7% at 31 December 2003, a productivity improvement of 4.6% annualised. The improvement is due to strong revenue growth in the Bank and the benefits from strategic initiatives implemented in current and prior years partially offset by the increase in costs.

Initiatives including Which new Bank

The key strategic activities carried out in the current period were the continued implementation of the IBS redesign program and process improvements relating to the home loan application process, as well as the branch refurbishment program in Retail Banking Services. More details on specific initiatives are outlined on page 9.

Bad and Doubtful Debts

The total charge of $150 million for bad and doubtful debts is at similar levels for the prior two six month periods ($151 million for the six months ended 31 December 2002 and $154 million for the six months ended 30 June 2003).

Low interest rates continued to contribute to a good credit environment, with personal and corporate arrears and default levels at historically low levels.

The Bank remains well provisioned, with total provisions for impairment as a percentage of gross impaired assets net of interest reserved of 271.6% (June 2003 : 239.4%) and a general provision as a percentage of risk weighted assets of 0.86%, compared against 0.90% at 30 June 2003.

Taxation Expense

The corporate tax charge of $412 million is 12% or $56 million lower than 31 December 2002 reflecting the lower profit inclusive of the incremental initiative expenses. The average effective tax rate has reduced slightly to 29.8%.

11

Banking Analysis (cont’d)

Major Balance Sheet Items

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Major Balance Sheet Items (gross of impairment) - by Product | $M | $M | $M | % | ||||||||||||

| Gross housing | 117,530 | 106,683 | 99,456 | 18 | ||||||||||||

| Securitisation | (5,302 | ) | (6,480 | ) | (5,911 | ) | (10 | ) | ||||||||

| Housing (net of securitisation) | 112,228 | 100,203 | 93,545 | 20 | ||||||||||||

| Personal | 12,616 | 12,369 | 12,281 | 3 | ||||||||||||

| Institutional and Business | 52,694 | 49,305 | 50,427 | 4 | ||||||||||||

| Bank acceptances | 13,734 | 13,197 | 12,831 | 7 | ||||||||||||

Total Lending Assets | 191,272 | 175,074 | 169,084 | 13 | ||||||||||||

Trading & Investment Securities | 23,945 | 21,471 | 26,053 | (8 | ) | |||||||||||

Deposits and Other Public Borrowings | 158,914 | 140,974 | 139,348 | 14 | ||||||||||||

Debt Issues | 33,157 | 30,629 | 29,025 | 14 | ||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Major Balance Sheet Items (gross of impairment) - by Business | $M | $M | $M | % | ||||||||||||

Retail: | ||||||||||||||||

| Lending assets | 110,604 | 100,134 | 94,094 | 18 | ||||||||||||

| Deposits | 71,932 | 68,702 | 68,024 | 6 | ||||||||||||

Asia Pacific: | ||||||||||||||||

| Lending assets | 22,685 | 19,880 | 19,468 | 17 | ||||||||||||

| Trading & investment securities | 3,008 | 2,953 | 2,983 | 1 | ||||||||||||

| Debt issues | 3,075 | 2,570 | 1,928 | 59 | ||||||||||||

| Deposits | 17,783 | 17,168 | 16,662 | 7 | ||||||||||||

Institutional and Business and Group Treasury: | ||||||||||||||||

| Lending assets | 57,983 | 55,060 | 55,522 | 4 | ||||||||||||

| Trading & investment securities | 20,937 | 18,518 | 23,070 | (9 | ) | |||||||||||

| Debt issues | 30,082 | 28,059 | 27,097 | 11 | ||||||||||||

| Deposits | 69,199 | 55,104 | 54,662 | 27 | ||||||||||||

|  |

12

Banking Analysis (cont’d)

Retail

Lending Assets

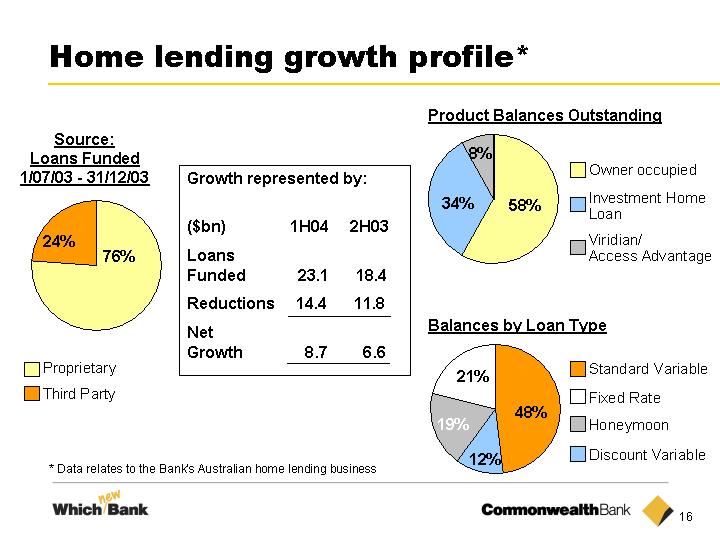

Australian retail banking lending assets at 31 December 2003 were $111 billion, an increase of 11% or $11 billion over 30 June 2003 and up 18% over the 12 months since 31 December 2002. Lending assets comprise Australian Home Lending and Personal Lending.

Home Lending

Home loan balances net of securitisation increased by 12% since 30 June 2003 and 20% since 31 December 2002. The increase in home loans accounts for approximately 75% of the increase in total lending assets during the last six months. This reflects continued strong demand in both owner occupied and investment loans. Market share as at 30 September 2003 was 19.3%, compared with 19.5% as reported at June 2003, relating to March 2003 (source: APRA). The market for “low document” home loans experienced strong growth during the period. As most of these borrowers fall outside the Bank’s lending criteria, the Bank did not benefit from this growth. The Bank maintained its position as Australia’s leading home loan provider and has increased its share of broker originated loans which now account for 13% of the total Australian book compared with 10% at June 2003, while 25% of new home loans funded are originated by third party brokers. The Bank’s share of broker originated loans as at 30 September 2003 was 20.3% (source: Market Intelligence Strategy Centre), achieving its objective of at least 20% share of that market.

Approval levels remained strong up to December. It is likely that growth will moderate in the forthcoming half due to the increase in interest rates from historically low levels, and investors’ changing views on the relative merits of direct property investment.

Personal Lending

Personal lending includes Personal Loans, Credit Cards and Margin Loans. Balances increased by 2% over six months to $12.6 billion as at December 2003 reflecting growth in Credit Card balances and margin lending.

Retail Deposits

Retail deposits showed good growth, with total balances increasing by $3 billion from 30 June 2003 to $71.9 billion. Competition has intensified within the market as the improved investment market performance has started to attract customers back to equity based products.

Asia Pacific

Lending Assets

The New Zealand lending volumes remained strong during the first half across all sectors, particularly in housing and business lending. Credit demand was the major contributor to the strong growth. Housing activity remained buoyant and this has driven growth in housing mortgage balances.

ASB Bank’s share of the lending market continued to grow, with market share increasing to 21.6% as at December 2003 from 20.6% in June 2003 (source: Reserve Bank of New Zealand). Focused marketing activity and ASB Bank’s sales and service performance underpinned this result.

Deposits

Retail funding within ASB Bank increased from $12.3 billion at 30 June 2003 to $13 billion at 31 December 2003, an increase of 6%.

Institutional and Business and Group Treasury

Lending Assets

Institutional and Business Lending has increased $2.8 billion or 5% over the six months since 30 June 2003 to $58 billion. This growth reflected good transaction activity in Institutional Banking, a stronger performance in Corporate Banking and steady growth in Business Banking. Market share at 14.2% as at December 2003 has increased relative to 30 June 2003 of 14% (source: APRA).

Trading and Investment Securities

Trading and investment securities increased by $2.4 billion to $20.9 billion at 31 December 2003 from $18.5 billion as at 30 June 2003. This increase is primarily due to short term deposits as a result of funding operations.

Debt Issues

Debt issues were $30 billion at 31 December 2003, an increase of $2 billion since 30 June 2003. The increase reflects offshore funding raised to fund the growth in the Bank’s assets.

Deposits

Deposits were $69 billion at 31 December 2003, an increase of $14 billion from $55 billion at 30 June 2003. This primarily reflects an increase in business deposit market share as well as increased use of wholesale funding to fund the growth in the Bank’s assets.

13

Banking Analysis (cont’d)

| 31/12/03 | 30/06/03 | 31/12/02 | ||||||||||

| Provisions for Impairment | $M | $M | $M | |||||||||

| General provisions | 1,358 | 1,325 | 1,327 | |||||||||

| Specific provisions | 198 | 205 | 264 | |||||||||

Total Provisions | 1,556 | 1,530 | 1,591 | |||||||||

| Total provisions for impairment as a % of gross impaired assets net of interest reserved | 271.6 | 239.4 | 184.1 | |||||||||

| Specific provisions for impairment as a % of gross impaired assets net of interest reserved | 34.55 | 32.08 | 30.56 | |||||||||

| General provisions as a % of risk weighted assets | 0.86 | 0.90 | 0.92 | |||||||||

| Bad debt expense/Risk weighted assets | 0.10 | 0.10 | 0.11 | |||||||||

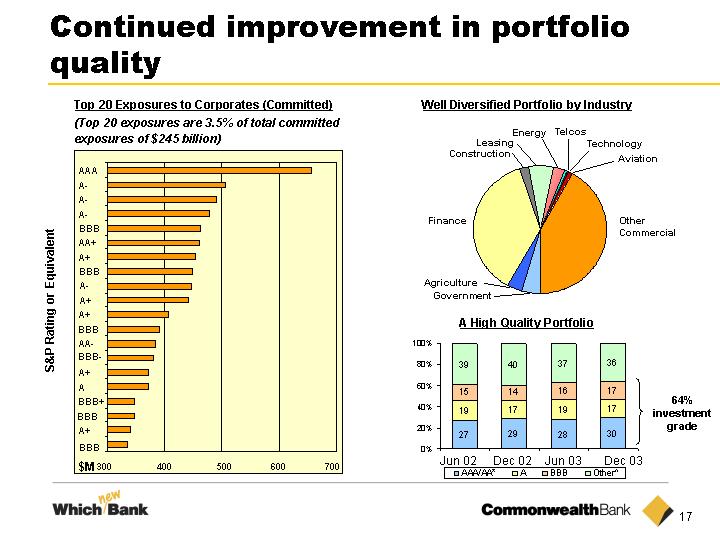

Total provisions for impairment for the Bank at 31 December 2003 were $1,556 million, up 1.7% from 30 June 2003. This level of provisioning is considered adequate to cover any bad debt write offs from the current lending portfolio having regard to the current outlook.

Specific provisions for impairment have decreased by 3.4% from $205 million at 30 June 2003 to $198 million at 31 December 2003, primarily as a result of continuing reductions in the level of impaired assets (Gross Impaired Assets net of interest reserved have reduced by $290 million since December 2002, a reduction of 34%).

The general provision for impairment has increased to $1,358 million at 31 December 2003 from $1,325 million at 30 June 2003, an increase of 2.5%. The general provision as a percentage of Risk Weighted Assets reduced to 0.86% from 0.90% in that period. This level is generally consistent with that of other major Australian banks. The general provision as a percentage of risk weighted assets has declined over the last 3 years reflecting the fact that the major growth in credit has been in home loans which have lower credit risk than other portfolios.

14

Funds Management Analysis

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

Profitability(2) | ||||||||||||||||

Underlying Profit after Income Tax | 126 | 108 | 125 | 1 | ||||||||||||

| Shareholder investment returns (after tax) | 10 | 6 | 4 | large | ||||||||||||

Initiatives including Which new Bank (after tax)(1) | (19 | ) | (27 | ) | — | — | ||||||||||

Net Profit after Income Tax (“cash basis”) | 117 | 87 | 129 | (9 | ) | |||||||||||

Operating Income | ||||||||||||||||

| Operating income | 589 | 548 | 580 | 2 | ||||||||||||

| Operating income to average funds under management (%) | 1.19 | 1.19 | 1.18 | 1 | ||||||||||||

Operating Expenses | ||||||||||||||||

| Operating expenses | 416 | 406 | 418 | — | ||||||||||||

Initiatives including Which new Bank(1) | 27 | 38 | — | — | ||||||||||||

Funds Under Management | ||||||||||||||||

| Funds under management — average | 98,357 | 93,202 | 97,465 | 1 | ||||||||||||

| Funds under management — spot | 100,383 | 94,207 | 95,266 | 5 | ||||||||||||

| Net flows | 1,080 | (1,493 | ) | (2,232 | ) | large | ||||||||||

Productivity and Other Measures | ||||||||||||||||

| Expenses to average funds under management — actual (%) | 0.90 | 0.96 | 0.86 | 5 | ||||||||||||

| Expenses to average funds under management — underlying (%) | 0.84 | 0.88 | 0.86 | (2 | ) | |||||||||||

| Effective corporate tax rate (%) | 24.4 | 19.6 | 21.4 | 14 | ||||||||||||

| (1) | December 2003 results reflects the Which new Bank initiative, while prior periods include strategic initiatives undertaken |

| (2) | Prior periods have been restated to include income from external advisors previously reported under Banking and some minor expense reallocations. |

Financial Performance and Business Review

Performance Highlights

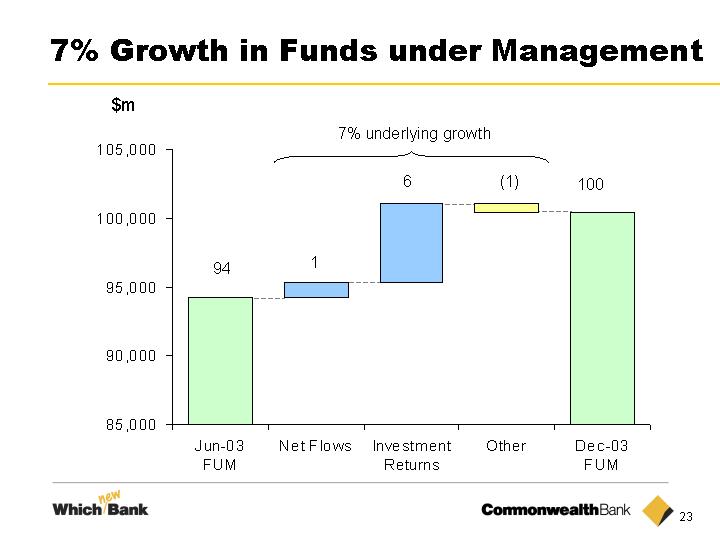

Underlying net profit after tax of $126 million was up 1% on the prior comparative period and up a strong 17% on the six months ended 30 June 2003. On a pre-tax basis the underlying net profit was up 7% to $173 million on the prior comparative period. Spot funds under management for the six months ended 31 December 2003 was $100 billion, which is up 7% on 30 June 2003 levels ($94 billion).

Business Review

The business benefited from a recovery in global share markets which boosted funds under management. The more favourable market conditions also contributed to an improvement in investor confidence and funds flows. However, after the sustained period of poor equity returns in previous years, funds flow for the industry remains well down on historic levels.

A very tight focus was maintained on costs with business as usual expenses down $2 million period on period. The business, however, continued to incur significant costs in respect of regulatory and compliance spend in addition to initiative spend associated with Which new Bank.

Underpinning the financial results, the business highlights included:

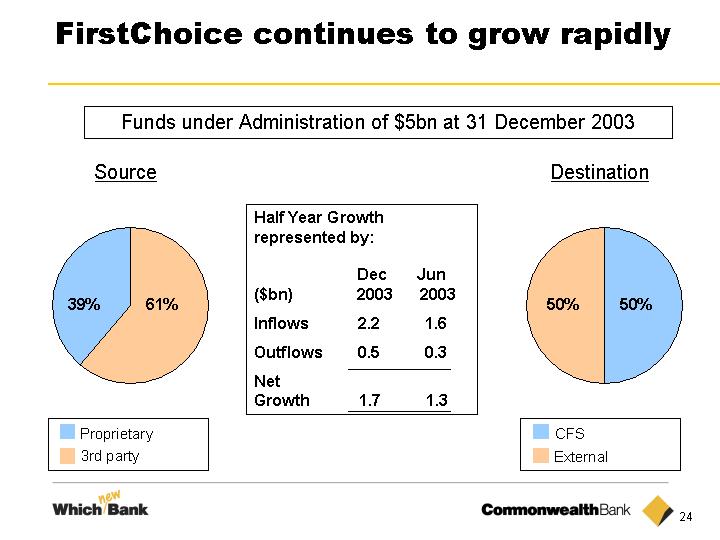

| • | The FirstChoice mastertrust product continued to achieve very strong flows in the latest reported quarter (September 2003). Funds in this product, launched only 18 months ago now total $5 billion. |

| • | Funds flow in our UK business has been extremely strong. Net flows of $2.4 billion for the six months represent a record for the UK business. |

| • | Investment performance on the flagship Colonial First State Australian Equities fund continues to improve and is now back in the second quartile on a 12 month basis. |

Strategic Initiatives

The major strategic initiatives undertaken were focussed on process and system simplification, as well as continuing to build our position in the platform market. These included:

| • | Further progress was made on the product migration program, aimed at reducing the number of products and systems especially on the older closed products. The number of product systems supporting the older products has already been reduced from 17 to 14, and is targeted to reach five by 2006. |

| • | Continued development of the FirstChoice mastertrust platform, with a focus on enhancing the platform to provide additional services and reporting for financial planners. |

| • | A reorganisation of the various support functions, designed to reduce costs and better leverage the resources through the creation of common support functions across the various businesses. |

| • | Following a strategic review of our UK operations, the business has been refocussed as a manufacturer of specialist product, rather than a more generalised operation in all asset classes. |

Comparative Figures

The December 2003 result has been impacted by a different expense allocation between funds management and insurance.

If the comparatives were adjusted to reflect the December 2003 basis, $11 million of pre-tax expenses would have been included in the insurance business rather than the funds management business.

If done, this adjustment would have resulted in a 8% increase in underlying cash NPAT compared to the previous comparative period.

15

Funds Management Analysis (cont’d)

Profit Summary

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

Funds Management | ||||||||||||||||

| Operating income — external | 582 | 540 | 575 | 1 | ||||||||||||

| Operating income — internal | 7 | 8 | 5 | 40 | ||||||||||||

Total Operating Income | 589 | 548 | 580 | 2 | ||||||||||||

| Shareholder investment returns | 14 | 8 | 5 | large | ||||||||||||

| Policyholder tax expense/(benefits) | 82 | 4 | (66 | ) | large | |||||||||||

Funds Management Income | 685 | 560 | 519 | 32 | ||||||||||||

| Volume based expenses | 82 | 77 | 81 | 1 | ||||||||||||

| Other operating expenses | 334 | 329 | 337 | (1 | ) | |||||||||||

Operating expenses | 416 | 406 | 418 | — | ||||||||||||

Initiatives including Which new Bank(1) | 27 | 38 | — | — | ||||||||||||

Total Operating Expenses | 443 | 444 | 418 | 6 | ||||||||||||

| Net Profit before Income Tax | 242 | 116 | 101 | large | ||||||||||||

| Policyholder tax expense/(benefits) | 82 | 4 | (66 | ) | large | |||||||||||

| Corporate tax expense | 39 | 22 | 35 | 11 | ||||||||||||

| Outside equity interests | 4 | 3 | 3 | 33 | ||||||||||||

Net Profit after Income Tax (“cash basis”) | 117 | 87 | 129 | (9 | ) | |||||||||||

| (1) | December 2003 results reflects the Which new Bank initiative, while prior periods include strategic initiatives undertaken including the one off cost relating to the sale of the custody business. |

Operating Income

Operating income increased by 2% or $9 million to $589 million for the six months to 31 December 2003, compared with $580 million for the prior comparative period.

Improved domestic and global equity markets and strong inflows into the UK business resulted in an increase in total funds under management (spot balance) from $94.2 billion at 30 June 2003 to $100.4 billion. Average funds under management for the six months was $98.4 billion, which is 1% higher than levels at 31 December 2002 of $97.5 billion, although the closing funds under management at 31 December 2003 is much higher.

The operating income to average funds under management ratio remained steady at 1.19% which is consistent with the prior two six month periods.

Shareholder Investment Returns

Shareholder investment returns of $14 million reflected the impact of improved local and global equity markets compared with prior periods.

Operating Expenses

Volume related expenses (consisting mainly of commissions) increased slightly from $81 million for the six months ended 31 December 2002 to $82 million in the current reporting period.

A strong focus on expense control and the benefits from prior year strategic initiatives led to other expenses reducing slightly compared with the comparable period last year, with expenses totalling $334 million for the six months ended 31 December 2003 against $337 million for the prior comparative period.

Productivity Efficiency

Operating expenses as a percentage of average funds under management of 0.84% was down 4basis points compared with June 2003.

Initiatives including Which new Bank

Costs of $27 million relating to Which new Bank initiatives include the expenses of continued rationalisation of systems, development of FirstChoice mastertrust platform, reorganisation of support functions and the strategic review of the UK operations. In addition to strategic initiatives, the prior period also includes the one-off cost relating to the sale of the custody business.

Taxation

The corporate taxation charge for the period ending 31 December 2003 was $39 million, an increase of 11% compared wtih 31 December 2002. The tax charge reflects an increased effective tax rate of 24% compared with 21% at 31 December 2002. The low effective tax rate in this business is due to transitional tax relief on investment style funds management products within life insurance legal entities. The benefits derived from this relief are being phased out over a five year period ending in 2005, thereby progressively increasing the effective tax rate.

16

Funds Management Analysis (cont’d)

Funds Under Management

| Half Year Ended 31 December 2003 | ||||||||||||||||||||||||||||

| Opening | Other | Closing | ||||||||||||||||||||||||||

| Balance | Investment | Acquisitions & | Movements | Balance | ||||||||||||||||||||||||

| 30/06/03 | Inflows | Outflows | Income | Disposals | & Transfers(1) | 31/12/03 | ||||||||||||||||||||||

| $M | $M | $M | $M | $M | $M | $M | ||||||||||||||||||||||

| FirstChoice | 3,211 | 2,177 | (517 | ) | 157 | — | — | 5,028 | ||||||||||||||||||||

| Cash Management | 4,963 | 1,635 | (2,027 | ) | 93 | — | — | 4,664 | ||||||||||||||||||||

| Other Retail | 36,417 | 3,506 | (4,940 | ) | 1,720 | — | — | 36,703 | ||||||||||||||||||||

| Wholesale | 23,966 | 6,788 | (7,978 | ) | 1,717 | — | — | 24,493 | ||||||||||||||||||||

| Property | 11,790 | 1,418 | (1,490 | ) | 411 | — | — | 12,129 | ||||||||||||||||||||

Domestically Sourced | 80,347 | 15,524 | (16,952 | ) | 4,098 | — | — | 83,017 | ||||||||||||||||||||

| Internationally Sourced | 13,860 | 6,502 | (3,994 | ) | 1,678 | — | (680 | ) | 17,366 | |||||||||||||||||||

Total | 94,207 | 22,026 | (20,946 | ) | 5,776 | — | (680 | ) | 100,383 | |||||||||||||||||||

| Half Year Ended 30 June 2003 | ||||||||||||||||||||||||||||

| Opening | Other | Closing | ||||||||||||||||||||||||||

| Balance | Investment | Acquisitions & | Movements | Balance | ||||||||||||||||||||||||

| 31/12/02 | Inflows | Outflows | Income | Disposals | & Transfers(1) | 30/06/03 | ||||||||||||||||||||||

| $M | $M | $M | $M | $M | $M | $M | ||||||||||||||||||||||

| FirstChoice | 1,846 | 1,648 | (323 | ) | 40 | — | — | 3,211 | ||||||||||||||||||||

| Cash Management | 5,244 | 525 | (879 | ) | 73 | — | — | 4,963 | ||||||||||||||||||||

| Other Retail | 38,487 | 4,340 | (6,738 | ) | 328 | — | — | 36,417 | ||||||||||||||||||||

| Wholesale | 24,878 | 5,137 | (6,761 | ) | 712 | — | — | 23,966 | ||||||||||||||||||||

| Property | 11,250 | — | 348 | 192 | — | — | 11,790 | |||||||||||||||||||||

Domestically Sourced | 81,705 | 11,650 | (14,353 | ) | 1,345 | — | — | 80,347 | ||||||||||||||||||||

| Internationally Sourced | 13,561 | 1,311 | (101 | ) | 838 | — | (1,749 | ) | 13,860 | |||||||||||||||||||

Total | 95,266 | 12,961 | (14,454 | ) | 2,183 | — | (1,749 | ) | 94,207 | |||||||||||||||||||

| Half Year Ended 31 December 2002 | ||||||||||||||||||||||||||||

| Opening | Other | Closing | ||||||||||||||||||||||||||

| Balance | Investment | Acquisitions & | Movements | Balance | ||||||||||||||||||||||||

| 30/06/02 | Inflows | Outflows | Income | Disposals | & Transfers(1) | 31/12/02 | ||||||||||||||||||||||

| $M | $M | $M | $M | $M | $M | $M | ||||||||||||||||||||||

| FirstChoice | 561 | 1,558 | (255 | ) | (18 | ) | — | — | 1,846 | |||||||||||||||||||

| Cash Management | 5,634 | 596 | (1,091 | ) | 105 | — | — | 5,244 | ||||||||||||||||||||

| Other Retail | 40,909 | 3,111 | (4,404 | ) | (1,129 | ) | — | — | 38,487 | |||||||||||||||||||

| Wholesale | 27,766 | 4,460 | (6,062 | ) | (1,286 | ) | — | — | 24,878 | |||||||||||||||||||

| Property | 8,895 | — | (348 | ) | 545 | 2,158 | — | 11,250 | ||||||||||||||||||||

Domestically Sourced | 83,765 | 9,725 | (12,160 | ) | (1,783 | ) | 2,158 | — | 81,705 | |||||||||||||||||||

| Internationally Sourced | 19,073 | 5,273 | (5,070 | ) | (1,263 | ) | (5,000 | ) | 548 | 13,561 | ||||||||||||||||||

Total | 102,838 | 14,998 | (17,230 | ) | (3,046 | ) | (2,842 | ) | 548 | 95,266 | ||||||||||||||||||

| (1) | Includes foreign exchange gains and losses from translation of internationally sourced business. |

17

Funds Management Analysis (cont’d)

Funds under management

Funds under management increased by $6 billion or 7% from $94 billion at 30 June 2003 to $100 billion at 31 December 2003. Strong local and global equity markets contributed $6 billion, net inflows were $1 billion while the impact of a stronger Australian dollar had a negative impact of $680 million. Average funds under management of $98 billion at 31 December 2003 were 1% higher than 31 December 2002.

FirstChoice

FirstChoice continued its strong performance, with net inflows totalling $1.7 billion for the six months ended 31 December 2003. This took the total funds under management to over $5 billion since its launch in May 2002. FirstChoice topped the industry flows into platforms for the September 2003 quarter.

Cash Management

Cash management trusts saw further net outflows totalling $0.4 billion during the reporting period. The majority of these funds have moved into similar cash deposit products in Banking.

Other Retail

Other retail funds under management grew a modest $0.3 billion or 1% to $36.7 billion. The net outflows (excluding investment returns) on Colonial First State retail products reflects an industry move away from single manager retail products to masterfund products (like FirstChoice).

Wholesale

Despite relatively high levels of outflows, wholesale FUM has increased by $0.5 billion or 2.2% to $24.5 billion. These outflows were predominantly in the Australian equities asset class.

The level of FUM in the institutional market increased substantially with the cash, fixed interest and other debt products performing strongly.

Property

Property FUM comprises both listed and unlisted (wholesale) funds. Total property FUM grew $0.3 billion or 2.8%, benefiting from both asset revaluations and acquisitions of new properties.

Internationally sourced

International funds inflow was particularly strong at $6.5 billion for the half year due to some large mandate wins into the Global Emerging Markets product.

Due to the exceptional funds flow, FUM growth was 25% (or 30% in local currency).

18

Insurance Analysis

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Key Performance Indicators | $M | $M | $M | % | ||||||||||||

Profitability | ||||||||||||||||

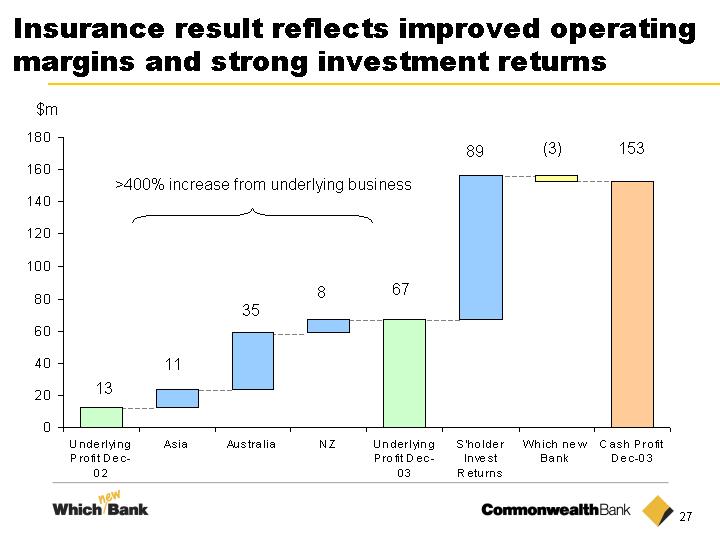

| Underlying Profit after Income Tax | 67 | 52 | 13 | large | ||||||||||||

| Shareholder investment returns (after tax) | 89 | 76 | (12 | ) | large | |||||||||||

| Initiatives including Which new Bank (after tax) | (3 | ) | — | — | — | |||||||||||

| Net Profit after Income Tax (“cash basis”) | 153 | 128 | 1 | large | ||||||||||||

Regional Net Profit after Income Tax — (“cash basis”) | ||||||||||||||||

| Australia | 96 | 75 | 3 | large | ||||||||||||

| New Zealand | 30 | 33 | 13 | large | ||||||||||||

| Asia | 27 | 20 | (15 | ) | large | |||||||||||

Operating Income | ||||||||||||||||

| Operating income | 322 | 318 | 280 | 15 | ||||||||||||

Operating Expenses | ||||||||||||||||

| Operating expenses | 249 | 250 | 269 | (7 | ) | |||||||||||

| Initiatives including Which new Bank | 4 | — | — | — | ||||||||||||

Annual Inforce Premiums | ||||||||||||||||

| Australia | 800 | 771 | 746 | 7 | ||||||||||||

| New Zealand | 226 | 221 | 203 | 11 | ||||||||||||

| Asia | 76 | 84 | 91 | (16 | ) | |||||||||||

Productivity and Other Measures | ||||||||||||||||

| Expenses to average inforce premiums (actual %) | 46.2 | 47.7 | 52.8 | 12 | ||||||||||||

| Expenses to average inforce premiums (underlying %) | 45.5 | 47.7 | 52.8 | 13 | ||||||||||||

| Effective corporate tax rate (%) | 21.9 | 17.9 | — | |||||||||||||

Financial Performance and Business Review

Performance Highlights

The profit from the Insurance business was $153 million compared with a profit of $1 million for the prior comparative period. Excluding investment returns and incremental Which new Bank expenses, the underlying operating performance was $67 million, an increase of $54 million over the prior comparative period. This improvement was across all regions. The insurance results have been restated from those reported at 30 June 2003 and 31 December 2002 to include the general insurance business, which were previously reported under Banking.

Business Review

Australia

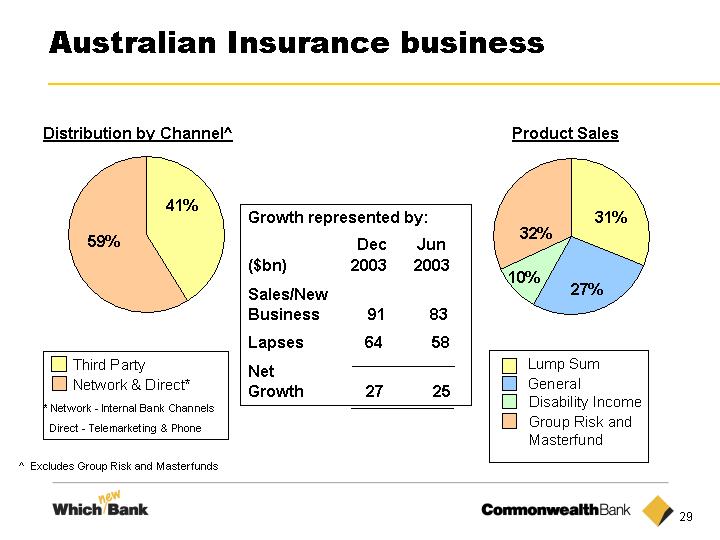

The profit in the Australian insurance business was up strongly on the prior comparative period, which was adversely impacted by a one off asset write down. Key drivers of the half year result were the positive investment returns, solid premium growth (4%) and tight expense control. General insurance claims were slightly above prior period mainly due to claims arising from the Melbourne and Sydney storms and flooding.

Other highlights for the period included:

| • | Maintained No. 1 market share (15.1%) of inforce life risk premiums. |

| • | Launch of a new Loan Protection product, designed to facilitate cross sell to bank customers taking out loans. |

A number of reengineering projects and technology investments were commenced, designed to streamline processes, improve customer service, improve productivity and reduce costs in servicing and administration areas.

New Zealand

The life insurance manufacturing operations in New Zealand trade predominantly under the Sovereign brand.

New business volumes across the market contracted by 3.4% in the year to September 2003. During the same period, Sovereign’s market share held steady at 25.4%. Sovereign had maintained its market leadership position with 28.1% share of the in-force premium income market in September 2003.

Repricing of products, new underwriting and claims management programmes produced significant profit margin expansion. In addition persistency experience showed continued improvement as the business maintained its focus on improving customer service. Product and system platform rationalisation continued to make substantial progress.

Asia

Asia includes life insurance and pension administration operations in Hong Kong, together with life businesses in China, Vietnam, Indonesia and Fiji. Hong Kong represents our largest operation in the region.

The relatively swift containment of the SARS epidemic, increasing economic co-operation with the Chinese mainland, and the rebound of international equity markets improved economic conditions and stabilised the life insurance industry in Hong Kong.

The Asian business continued to improve. Key initiatives during the period included:

| • | Alignment of policyholder dividends to investment returns in Hong Kong. |

| • | Launch of an innovative new multi-manager investment product in Hong Kong. |

| • | Expense reductions within Hong Kong operations. |

| • | Improvement in agent remuneration practice in China and Indonesia. |

19

Insurance Analysis (cont’d)

Profit Summary

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| Summary Financial Performance | 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | ||||||||||||

| (excluding appraisal value (reduction)/uplift) | $M | $M | $M | % | ||||||||||||

Insurance | ||||||||||||||||

| Insurance Operating Income | 303 | 297 | 254 | 19 | ||||||||||||

| General Insurance Operating Income | 19 | 21 | 26 | (27 | ) | |||||||||||

Total Operating Income | 322 | 318 | 280 | 15 | ||||||||||||

| Shareholder investment returns | 127 | 88 | (10 | ) | large | |||||||||||

| Policyholder tax | 38 | 28 | (24 | ) | large | |||||||||||

Total Insurance Income | 487 | 434 | 246 | 98 | ||||||||||||

| Volume based expenses | 105 | 114 | 114 | (8 | ) | |||||||||||

| Other operating expenses — external | 137 | 128 | 150 | (9 | ) | |||||||||||

| Other operating expenses — internal | 7 | 8 | 5 | 40 | ||||||||||||

Operating expenses | 249 | 250 | 269 | (7 | ) | |||||||||||

| Initiatives including Which new Bank | 4 | — | — | — | ||||||||||||

Total operating expenses | 253 | 250 | 269 | (6 | ) | |||||||||||

| Net Profit before Income Tax | 234 | 184 | (23 | ) | large | |||||||||||

| Income tax expense attributable to: | ||||||||||||||||

| Policyholder | 38 | 28 | (24 | ) | large | |||||||||||

| Corporate | 43 | 28 | — | — | ||||||||||||

| Net Profit after Income Tax (“cash basis”) | 153 | 128 | 1 | large | ||||||||||||

Operating Income

Operating income of $322 million was 15% or $42 million higher than in the prior comparative period. Operating income in the prior period included a write-down of an asset in the Australian annuity fund of $23 million. Taking this item into account, operating income was up 6% on 31 December 2002 with a growth in life insurance income being partly offset by a decline in general insurance income as a result of adverse weather claims in Melbourne and Sydney.

Shareholder Investment Returns

Shareholder investment returns of $127 million for the period represent an increase of $137 million on the prior comparative period, reflecting the rebound in domestic and overseas equity markets.

Operating Expenses

Operating expenses of $249 million represent a decline of $20 million on the prior comparative period. This reflects a decline in expenses particularly within the Asian business, due to cost control initiatives in the Hong Kong life and CommServe businesses.

Corporate Taxation

The corporate tax charge for the period was $43 million compared with a nil charge in the prior year. This reflects the growth in profit. The effective tax rate for the business was 22%.

| Half Year Ended | ||||||||||||||||

| 31/12/03 | ||||||||||||||||

| 31/12/03 | 30/06/03 | 31/12/02 | -v- 31/12/02 | |||||||||||||

| Sources of Profit from Insurance Activities | $M | $M | $M | % | ||||||||||||

| The Margin on Services profit from ordinary activities after income tax is represented by: | ||||||||||||||||

| Planned profit margins | 52 | 52 | 52 | — | ||||||||||||

| Experience variations | 11 | 4 | (46 | ) | large | |||||||||||

| New business losses / reversal of capitalised losses | 2 | (8 | ) | — | n/a | |||||||||||

| General insurance operating margin | (1 | ) | 4 | 7 | large | |||||||||||

| Operating margins | 64 | 52 | 13 | large | ||||||||||||

| After tax shareholder investment returns | 89 | 76 | (12 | ) | large | |||||||||||

| Net profit after Income Tax (“cash basis”) | 153 | 128 | 1 | large | ||||||||||||

20

Insurance Analysis (cont’d)

Geographical Analysis of Business Performance

| Half Year Ended | ||||||||||||||||||||||||||||||||

| Australia | New Zealand | Asia | Total | |||||||||||||||||||||||||||||

| 31/12/03 | 31/12/02 | 31/12/03 | 31/12/02 | 31/12/03 | 31/12/02 | 31/12/03 | 31/12/02 | |||||||||||||||||||||||||

| Underlying Profit after Income Tax | $M | $M | $M | $M | $M | $M | $M | $M | ||||||||||||||||||||||||

| Operating margins | 42 | 10 | 20 | 12 | 2 | (9 | ) | 64 | 13 | |||||||||||||||||||||||

| Investment earnings on assets in excess of policyholder liabilities | 54 | (7 | ) | 10 | 1 | 25 | (6 | ) | 89 | (12 | ) | |||||||||||||||||||||

Net Profit after Income Tax | 96 | 3 | 30 | 13 | 27 | (15 | ) | 153 | 1 | |||||||||||||||||||||||

Australia

The Australian business generated $96 million in cash profit after tax. This reflects an increase of $93 million on the prior comparative period. This is attributable to:

| • | An increase in shareholder investment returns of $61 million. |

| • | An improvement in operating margins of $32 million, reflecting the inclusion in the prior periods of the write-down of an investment asset, together with better claims experience and improved investment returns. |

New Zealand

The New Zealand business generated $30 million in profit after tax. This represents an increase of $17 million over the same period last year. This is attributable to:

| • | Improved underwriting and claims management. |

| • | Rate increases. |

| • | Improved persistency. |

| • | Positive investment earnings. |

| • | Expenses containment. |

Asia

The Asian business produced $27 million in profit, compared with a loss of $15 million in the prior period. Disposal of the Philippine life company had adversely impacted the prior result by $10 million. The favourable current period result reflected strong investment markets performance and improved operating margins.

Operating margins (including regional and business start-up/development expenses) improved to a profit of $2 million, compared with a prior year loss of $9 million due to:

| • | Continuing improvement in persistency rates within the Hong Kong business. |

| • | Expense reductions. |

| • | Consolidation of the pension administration business in the first half of 2003. |

| Half Year Ended 31 December 2003 | ||||||||||||||||||||

| Opening | Closing | |||||||||||||||||||

| Balance | Sales/New | Other | Balance | |||||||||||||||||

| 30/06/03 | Business | Lapses | Movements(1) | 31/12/03 | ||||||||||||||||

| Annual Inforce Premiums | $M | $M | $M | $M | $M | |||||||||||||||

| General Insurance | 196 | 24 | (19 | ) | — | 201 | ||||||||||||||

| Personal Life | 626 | 56 | (41 | ) | (6 | ) | 635 | |||||||||||||

| Group Life | 254 | 39 | (24 | ) | (3 | ) | 266 | |||||||||||||

Total | 1,076 | 119 | (84 | ) | (9 | ) | 1,102 | |||||||||||||

| Australia | 771 | 91 | (64 | ) | 2 | 800 | ||||||||||||||

| New Zealand | 221 | 18 | (13 | ) | — | 226 | ||||||||||||||

| Asia | 84 | 10 | (7 | ) | (11 | ) | 76 | |||||||||||||

Total | 1,076 | 119 | (84 | ) | (9 | ) | 1,102 | |||||||||||||

| (1) | Consists mainly of foreign exchange movements. |

21

Insurance Analysis (cont’d)

| Half Year Ended 30 June 2003 | ||||||||||||||||||||

| Opening | Closing | |||||||||||||||||||

| Balance | Sales/New | Other | Balance | |||||||||||||||||

| 31/12/02 | Business | Lapses | Movements(2) | 30/06/03 | ||||||||||||||||