UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2007

Commission File Number 0-21656

UNITED COMMUNITY BANKS, INC.

(Exact name of registrant as specified in its charter)

| | |

| (State or other jurisdiction of incorporation) | | (I.R.S. Employer Identification No.) |

| | | |

63 Highway 515, Blairsville, Georgia | | 30512 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (706) 781-2265

Securities registered pursuant to Section 12(b) of the Act: None

Name of exchange on which registered: Nasdaq Global Select

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $1.00 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Sections 13 or 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (check one):

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).Yes o No x

State the aggregate market value of the voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $1,088,226,189 based on shares held by non-affiliates at $25.89 per share, the closing stock price on the Nasdaq stock market on June 29, 2007).

As of January 31, 2008, 49,965,766 shares of common stock were issued and outstanding, including presently exercisable options to acquire 1,694,064 shares and 84,627 shares issuable under United Community Banks, Inc.’s deferred compensation plan.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the Annual Meeting of Shareholders to be held on April 30, 2008 are incorporated herein into Part III by reference.

INDEX

| PART I | | |

| | | | |

| | Item 1. | Business | 3 |

| | Item 1A. | Risk Factors | 12 |

| | Item 1B. | Unresolved Staff Comments | 13 |

| | Item 2. | Properties | 13 |

| | Item 3. | Legal Proceedings | 13 |

| | Item 4. | Submission of Matters to a Vote of Security Holders | 14 |

| | | | |

| PART II | | |

| | | | |

| | Item 5. | Market for United’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 |

| | Item 6. | Selected Financial Data | 17 |

| | Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 |

| | Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 37 |

| | Item 8. | Financial Statements and Supplementary Data | 41 |

| | Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 72 |

| | Item 9A. | Controls and Procedures | 72 |

| | Item 9B. | Other Information | 72 |

| | | | |

| PART III | | |

| | | | |

| | Item 10. | Directors, Executive Officers and Corporate Governance | 73 |

| | Item 11. | Executive Compensation | 73 |

| | Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 73 |

| | Item 13. | Certain Relationships and Related Transactions, and Director Independence | 73 |

| | Item 14. | Principal Accounting Fees and Services | 73 |

| | | | |

| PART IV | | |

| | | | |

| | Item 15. | Exhibits, Financial Statement Schedules | 73 |

| | Signatures | | 77 |

PART I

ITEM 1. BUSINESS.

United Community Banks, Inc. (“United”), a bank holding company registered under the Bank Holding Company Act of 1956, was incorporated under the laws of Georgia in 1987 and commenced operations in 1988 by acquiring 100% of the outstanding shares of Union County Bank, Blairsville, Georgia, now known as United Community Bank, Blairsville, Georgia

United acquired United Community Bank, Brevard, North Carolina in 1990 and merged the bank into United Community Bank, Blairsville, Georgia effective February 1, 2008. Although United operated both the Georgia bank and north Carolina bank for the past five years, we will refer to the consolidated Georgia bank (“the Bank”) only through this report. Substantially all of United’s activities were conducted by the Bank.

Since the early 1990’s, United has actively expanded its market coverage through organic growth complemented by selective acquisitions, primarily of banks whose managements share United’s community banking and customer service philosophies. Although those acquisitions have directly contributed to United’s growth over the last ten years, their contribution has primarily been to provide United access to new markets with attractive growth potential. Organic growth in assets includes growth through existing offices as well as growth at de novo locations and post-acquisition growth at acquired banking offices. Organic growth will continue to be the principal focus of United’s balanced growth strategy to extend its reach in both new and existing markets.

To emphasize its commitment to community banking, United conducts substantially all of its operations through a community-focused operating model of 27 separate “community banks”, which as of December 31, 2007, operated at 111 locations in north Georgia, metro Atlanta and Gainesville (“Atlanta Region”), coastal Georgia, western North Carolina and east Tennessee. The community banks offer a full range of retail and corporate banking services, including checking, savings, and time deposit accounts, secured and unsecured loans, wire transfers, brokerage services, and other financial services, and are led by local bank presidents (referred to herein as the “Presidents”) and management with significant experience in, and ties to, their communities. Each of the community bank Presidents has authority, alone or with other local officers, to make most credit decisions.

In June 2007, United completed the acquisition of Gwinnett Commercial Group, Inc. and its wholly-owned subsidiary First Bank of the South. The acquisition of Gwinnett Commercial Group added assets and deposits of $809 million and $568 million, respectively, and five banking offices in Atlanta Region.

In December 2006, United completed the acquisition of Southern Bancorp, Inc. a Georgia bank holding company and its wholly-owned subsidiary Southern National Bank. Southern National Bank has two banking offices in Atlanta Region. United also acquired two branch locations in western North Carolina. Both transactions collectively added $430 million in assets and $360 million in deposits. In addition, United opened five de novo locations in 2007 and eight in 2006.

The Bank, through its full-service retail mortgage lending division, United Community Mortgage Services (“UCMS”), is approved as a seller/servicer for Federal National Mortgage Association and Federal Home Loan Mortgage Corporation and provides fixed and adjustable-rate home mortgages. During 2007, the Bank originated $410 million of residential mortgage loans throughout Georgia, North Carolina and Tennessee for the purchase of homes and to refinance existing mortgage debt. Substantially all of these mortgages were sold into the secondary market with no recourse to the Bank other than for breach of warranties.

Acquired in 2000, Brintech, Inc. (“Brintech”), a subsidiary of the Bank, is a consulting firm for the financial services industry. Brintech provides consulting, advisory, and implementation services in the areas of strategic planning, profitability improvement, technology, efficiency, security, risk management, network, Internet banking, marketing, core processing, and telecommunications.

United owns an insurance agency, United Community Insurance Services, Inc. (“UCIS”), known as United Community Advisory Services, that is a subsidiary of the Bank.

United provides retail brokerage services through an affiliation with a third party broker/dealer.

Forward-Looking Statements

This Form 10-K contains forward-looking statements regarding United, including, without limitation, statements relating to United’s expectations with respect to revenue, credit losses, levels of nonperforming assets, expenses, earnings and other measures of financial performance. Words such as “may”, “could”, “would”, “should”, “believes”, “expects”, “anticipates”, “estimates”, “intends”, “plans”, “targets” or similar expressions are intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties that are subject to change based on various factors (many of which are beyond United’s control). The following factors, among others, could cause United’s financial performance to differ materially from the expectations expressed in such forward-looking statements:

| | ● | our past operating results may not be indicative of future operating results; |

| | | our business is subject to the success of the local economies in which we operate; |

| | ● | our concentration of construction and land development loans is subject to unique risks that could adversely affect our earnings; |

| | ● | we may face risks with respect to future expansion and acquisitions or mergers; |

| | ● | changes in prevailing interest rates may negatively affect our net income and the value of our assets; |

| | ● | if our allowance for loan losses is not sufficient to cover actual loan losses, earnings would decrease; |

| | ● | competition from financial institutions and other financial service providers may adversely affect our profitability; |

| | ● | business increases, productivity gains and other investments are lower than expected or do not occur as quickly as anticipated; |

| | ● | competitive pressures among financial services companies increase significantly; |

| | ● | the success of our business strategy; |

| | ● | the strength of the United States economy in general changes; |

| | ● | trade, monetary and fiscal policies and laws, including interest rate policies of the Board of Governors of the Federal Reserve System, change; |

| | ● | inflation or market conditions fluctuate; |

| | ● | conditions in the stock market, the public debt market and other capital markets deteriorate; |

| | ● | financial services laws and regulations change; |

| | ● | technology changes and United fails to adapt to those changes; |

| | ● | consumer spending and saving habits change; |

| | ● | unanticipated regulatory or judicial proceedings occur; and |

| | ● | United is unsuccessful at managing the risks involved in the foregoing. |

Additional information with respect to factors that may cause actual results to differ materially from those contemplated by such forward-looking statements may also be included in other reports that United files with the Securities and Exchange Commission. United cautions that the foregoing list of factors is not exclusive and not to place undue reliance on forward-looking statements. United does not intend to update any forward-looking statement, whether written or oral, relating to the matters discussed in this Form 10-K.

Monetary Policy And Economic Conditions

United’s profitability depends to a substantial extent on the difference between interest revenue received from loans, investments, and other earning assets, and the interest paid on deposits and other liabilities. These rates are highly sensitive to many factors that are beyond the control of United, including national and international economic conditions and the monetary policies of various governmental and regulatory authorities, particularly the Federal Reserve. The instruments of monetary policy employed by the Federal Reserve include open market operations in U.S. government securities, changes in the discount rate on bank borrowings and changes in reserve requirements against bank deposits.

Competition

The market for banking and bank-related services is highly competitive. United actively competes in their respective market areas, which include north Georgia, the Atlanta Region, coastal Georgia, western North Carolina and east Tennessee, with other providers of deposit and credit services. These competitors include other commercial banks, savings banks, savings and loan associations, credit unions, mortgage companies, and brokerage firms.

The following table displays the respective percentage of total bank and thrift deposits in each county where the Bank has operations. The table also indicates the ranking by deposit size in each county. All information in the table was obtained from the Federal Deposit Insurance Corporation Summary of Deposits as of June 30, 2007. The following information only shows market share in deposit gathering, which may not be indicative of market presence in other areas.

| Share of Local Deposit Markets by County - Banks and Savings Institutions | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | Market | | | Rank in | | | | Market | | | Rank in | | | | Market | | | Rank in | |

| | | Share | | | Market | | | | Share | | | Market | | | | Share | | | Market | |

| | | | | | | | | | | | | | | | | | | | | |

| Atlanta Region | | | | | | | North Georgia | | | | | | | Coastal Georgia | | | | | | |

| Bartow | | 7% | | | 6 | | Chattooga | | 42% | | | 1 | | Chatham | | 1% | | | 12 | |

| Carroll | | 3 | | | 9 | | Fannin | | 50 | | | 1 | | Glynn | | 18 | | | 2 | |

| Cherokee | | 4 | | | 9 | | Floyd | | 15 | | | 3 | | Ware | | 7 | | | 5 | |

| Cobb | | 4 | | | 8 | | Gilmer | | 15 | | | 2 | | | | | | | | | |

| Coweta | | 1 | | | 12 | | Habersham | | 14 | | | 3 | | North Carolina | | | | | | | |

| Dawson | | 36 | | | 1 | | Jackson | | 2 | | | 11 | | Avery | | 13 | | | 4 | |

| DeKalb | | 1 | | | 18 | | Lumpkin | | 27 | | | 2 | | Cherokee | | 46 | | | 1 | |

| Douglas | | 2 | | | 11 | | Rabun | | 12 | | | 5 | | Clay | | 53 | | | 1 | |

| Fayette | | 1 | | | 12 | | Towns | | 32 | | | 2 | | Graham | | 75 | | | 1 | |

| Forsyth | | 3 | | | 11 | | Union | | 85 | | | 1 | | Haywood | | 11 | | | 5 | |

| Fulton | | 1 | | | 17 | | White | | 40 | | | 1 | | Henderson | | 3 | | | 11 | |

| Gwinnett | | 4 | | | 5 | | | | | | | | | | Jackson | | 23 | | | 2 | |

| Hall | | 9 | | | 5 | | Tennessee | | | | | | | | Macon | | 9 | | | 4 | |

| Henry | | 3 | | | 12 | | Blount | | 4 | | | 8 | | Mitchell | | 29 | | | 1 | |

| Newton | | 4 | | | 6 | | Bradley | | 4 | | | 7 | | Swain | | 31 | | | 2 | |

| Paulding | | 2 | | | 8 | | Knox | | 1 | | | 13 | | Transylvania | | 12 | | | 3 | |

| Pickens | | 2 | | | 7 | | Loudon | | 19 | | | 3 | | Watauga | | 1 | | | 13 | |

| Rockdale | | 12 | | | 4 | | McMinn | | 3 | | | 8 | | Yancey | | 12 | | | 5 | |

| Walton | | 1 | | | 13 | | Monroe | | 2 | | | 8 | | | | | | | | | |

| | | | | | | | | | Roane | | 9 | | | 4 | | | | | | | | | |

Loans

The Bank makes both secured and unsecured loans to individuals, firms, and corporations. Secured loans include first and second real estate mortgage loans. The Bank also makes direct installment loans to consumers on both a secured and unsecured basis. At December 31, 2007, commercial (commercial and industrial), commercial (secured by real estate), construction (residential and commercial), residential mortgage and consumer installment loans represented approximately 7%, 25%, 40%, 25% and 3%, respectively, of United’s total loan portfolio.

Specific risk elements associated with the Bank’s lending categories include, but are not limited to:

| Loan Type | Risk Elements |

| | |

| Commercial (commercial and industrial) | Industry concentrations; inability to monitor the condition of collateral (inventory, accounts receivable and vehicles); increased competition; use of specialized or obsolete equipment as collateral; insufficient cash flow from operations to service debt payments. |

| | |

| Commercial (secured by real estate) | Loan portfolio concentrations; declines in general economic conditions and occupancy rates; business failure and lack of a suitable alternative use for property; environmental contamination. |

| | |

| Construction (residential and commercial) | Loan portfolio concentrations; inadequate long-term financing arrangements; cost overruns, changes in market demand for property. |

| | |

| Residential mortgage | Changes in general economic conditions or in the local economy; loss of borrower’s employment; insufficient collateral value due to decline in property value. |

| | |

| Consumer installment | Loss of borrower’s employment; changes in local economy; the inability to monitor collateral (vehicles and boats). |

Lending Policy

The Bank makes loans primarily to persons or businesses that reside, work, own property, or operate in its primary market areas. Unsecured loans are generally made only to persons who qualify for such credit based on net worth and liquidity. Secured loans are made to persons who are well established and have net worth, collateral, and cash flow to support the loan. Exceptions to the Bank’s policies are permitted on a case-by-case basis and require the approving officer to document, in writing, the reason for the exception. Loans exceeding the approving officer’s credit limit must be approved through the credit approval process involving Regional Credit Managers. All loans to borrowers whose aggregate lending relationship exceeds $5 million must be reported to the Bank’s Board of Directors for ratification.

United’s Credit Administration department provides each lending officer with written guidelines for lending activities as approved by the Bank’s Board of Directors. Limited lending authority is delegated to lending officers by United’s Management Credit and Policy Committee as authorized by the Bank’s Board of Directors or the Committee’s designees in Credit Administration. Loans in excess of individual officer credit authority must be approved by a senior officer with sufficient approval authority delegated by the Management Credit and Policy Committee as authorized by the Bank’s Board of Directors. Loans to borrowers whose total aggregate loans exceed $15.0 million require the additional approval of two Bank directors.

Regional Credit Managers

United utilizes its Regional Credit Managers to provide credit administration support to the Bank as needed. The Regional Credit Managers have joint lending approval authority with the community bank Presidents within varying limits set by the Management Credit and Policy Committee based on characteristics of each market. The Regional Credit Managers also provide credit underwriting support as needed by the community banks they serve.

Loan Review and Non-performing Assets

The Loan Review Department of United reviews, or engages an independent third party to review, the Bank’s loan portfolio on an ongoing basis to identify any weaknesses in the portfolio and to assess the general quality of credit underwriting. The results of such reviews are presented to Executive Management, the community bank Presidents, Credit Administration management and the Audit Committee of the Board of Directors. If an individual loan or credit relationship has a material weakness identified during the review process, the risk rating of the loan, or all loans comprising that credit relationship, will be downgraded to the classification that most closely matches the current risk level. The review process also provides for the upgrade of loans that show improvement since the last review. Since each loan in a credit relationship may have a different credit structure, collateral, and other secondary source of repayment, different loans in a relationship can be assigned different risk ratings. Under United’s 10-tier loan grading system, grades 1 through 6 are considered “pass” (acceptable) credit risk, grade 7 is a “watch” rating, and grades 8 through 10 are “adversely classified” credits that require management’s attention. Both the pass and adversely classified ratings, and the entire 10-grade rating scale, provide for a higher numeric rating for increased risk. For example, a risk rating of 1 is the least risky of all credits and would be typical of a loan that is 100% secured by a deposit at the Bank. Risk ratings of 2 through 6 in the pass category each have incrementally more risk. The four watch list credit ratings and rating definitions are:

| | 7 (Watch) | Weaknesses exist that could cause future impairment, including the deterioration of financial ratios, past-due status and questionable management capabilities. Collateral values generally afford adequate coverage, but may not be immediately marketable. |

| | | |

| | 8 (Substandard) | Specific and well-defined weaknesses that may include poor liquidity and deterioration of financial ratios. Loan may be past-due and related deposit accounts experiencing overdrafts. Immediate corrective action is necessary. |

| | | |

| | 9 (Doubtful) | Specific weaknesses characterized as Substandard that are severe enough to make collection in full unlikely. No reliable secondary source of full repayment. |

| | | |

| | 10 (Loss) | Same characteristics as Doubtful, however, probability of loss is certain. Loans classified as such are generally charged-off. |

In addition, Credit Administration and Accounting jointly prepare a quarterly analysis to determine the adequacy of the Allowance for Loan Losses (“ALL”) for the Bank. The ALL analysis also provides the consolidated analysis for United. The ALL analysis starts with total loans and subtracting loans fully secured by deposit accounts at the Bank, which effectively have no risk of loss. Next, all loans with an adversely classified rating are subtracted, including loans considered impaired. The remaining loan balance for each major loan category is then multiplied by its respective loss factor that is derived from the average historical loss rate for the preceding two year period, adjusted to reflect current economic conditions, which provides a required minimum ALL for pass credits. Loss factors for these loans are determined based on historical loss experience by type of loan. Loans that are considered impaired are evaluated separately and are assigned specific reserves as necessary.

Asset/Liability Committees

United’s asset/liability committee (“ALCO”) is composed of executive officers and the Treasurer of United. The ALCO is charged with managing the assets and liabilities of United and the Bank. The ALCO attempts to manage asset growth, liquidity, and capital to maximize income and reduce interest rate risk, market risk and liquidity risk. The ALCO directs the Bank’s overall acquisition and allocation of funds. At periodic meetings, the committee reviews the monthly asset and liability funds budget in relation to the actual flow of funds; the ratio of the amount of rate sensitive assets to the amount of rate sensitive liabilities; the ratio of allowance for loan losses to outstanding and non-performing loans; and other variables, such as stress testing expected loan demand, investment opportunities, core deposit growth within specified categories, regulatory changes, monetary policy adjustments and the overall state of the economy. A more comprehensive discussion of United’s Asset/Liability Management and interest rate risk is contained in Management’s Discussion and Analysis (Part II, Item 7) and Quantitative and Qualitative Disclosures About Market Risk (Part II, Item 7A) sections of this report.

Investment Policy

United’s investment portfolio policy is to maximize income within liquidity, asset quality and regulatory constraints. The policy is reviewed from time to time by United’s ALCO and United’s Board of Directors. Individual transactions, portfolio composition, and performance are reviewed and approved periodically by United’s Board of Directors or a committee thereof. The Chief Financial Officer and Treasurer of United administer the policy and report information to the Board of Directors on a quarterly basis concerning sales, purchases, maturities and calls, resultant gains or losses, average maturity, federal taxable equivalent yields, and appreciation or depreciation by investment categories.

Employees

As of December 31, 2007, United and its subsidiaries had 1,944 full-time equivalent employees. Neither United nor any of its subsidiaries is a party to any collective bargaining agreement and management believes that employee relations are good.

Available Information

United’s Internet website address is ucbi.com. United makes available free of charge through its website Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after they are filed with, or furnished to, the Securities & Exchange Commission.

Supervision And Regulation

The following is an explanation of the supervision and regulation of United and the Bank as financial institutions. This explanation does not purport to describe state, federal or Nasdaq Stock Market supervision and regulation of general business corporations or Nasdaq listed companies.

General. United is a registered bank holding company subject to regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve”) under the Bank Holding Company Act of 1956, as amended (the “Act”). United is required to file annual and quarterly financial information with the Federal Reserve and is subject to periodic examination by the Federal Reserve.

The Act requires every bank holding company to obtain the Federal Reserve’s prior approval before (1) it may acquire direct or indirect ownership or control of more than 5% of the voting shares of any bank that it does not already control; (2) it or any of its non-bank subsidiaries may acquire all or substantially all of the assets of a bank; and (3) it may merge or consolidate with any other bank holding company. In addition, a bank holding company is generally prohibited from engaging in, or acquiring, direct or indirect control of the voting shares of any company engaged in non-banking activities. This prohibition does not apply to activities listed in the Act or found by the Federal Reserve, by order or regulation, to be closely related to banking or managing or controlling banks as to be a proper incident thereto. Some of the activities that the Federal Reserve has determined by regulation or order to be closely related to banking are:

| | ● | making or servicing loans and certain types of leases; |

| | ● | performing certain data processing services; |

| | ● | acting as fiduciary or investment or financial advisor; |

| | ● | providing brokerage services; |

| | ● | underwriting bank eligible securities; |

| | ● | underwriting debt and equity securities on a limited basis through separately capitalized subsidiaries; and |

| | ● | making investments in corporations or projects designed primarily to promote community welfare. |

Although the activities of bank holding companies have traditionally been limited to the business of banking and activities closely related or incidental to banking (as discussed above), the Gramm-Leach-Bliley Act (the “GLB Act”) relaxed the previous limitations and permitted bank holding companies to engage in a broader range of financial activities. Specifically, bank holding companies may elect to become financial holding companies which may affiliate with securities firms and insurance companies and engage in other activities that are financial in nature. Among the activities that are deemed “financial in nature” include:

| | ● | lending, exchanging, transferring, investing for others or safeguarding money or securities; |

| | ● | insuring, guaranteeing, or indemnifying against loss, harm, damage, illness, disability, or death, or providing and issuing annuities, and acting as principal, agent, or broker with respect thereto; |

| | ● | providing financial, investment, or economic advisory services, including advising an investment company; |

| | ● | issuing or selling instruments representing interests in pools of assets permissible for a bank to hold directly; and |

| | ● | underwriting, dealing in or making a market in securities |

.

A bank holding company may become a financial holding company under this statute only if each of its subsidiary banks is well-capitalized, is well managed and has at least a satisfactory rating under the Community Reinvestment Act. A bank holding company that falls out of compliance with such requirement may be required to cease engaging in certain activities. Any bank holding company that does not elect to become a financial holding company remains subject to the bank holding company restrictions of the Act.

Under this legislation, the Federal Reserve Board serves as the primary “umbrella” regulator of financial holding companies with supervisory authority over each parent company and limited authority over its subsidiaries. The primary regulator of each subsidiary of a financial holding company will depend on the type of activity conducted by the subsidiary. For example, broker-dealer subsidiaries will be regulated largely by securities regulators and insurance subsidiaries will be regulated largely by insurance authorities.

United has no current plans to register as a financial holding company.

United must also register with the Georgia Department of Banking and Finance (“DBF”) and file periodic information with the DBF. As part of such registration, the DBF requires information with respect to the financial condition, operations, management and intercompany relationship of United and the Bank and related matters. The DBF may also require such other information as is necessary to keep itself informed concerning compliance with Georgia law and the regulations and orders issued thereunder by the DBF, and the DBF may examine United and the Bank. Although the Bank operates branches in North Carolina and Tennessee, neither the North Carolina Banking Commission (“NCBC”), nor the Tennessee Department of Financial Institutions (“TDFI”) examines or directly regulates out-of-state holding companies.

United is an “affiliate” of the Bank under the Federal Reserve Act, which imposes certain restrictions on (1) loans by the Bank to United, (2) investments in the stock or securities of United by the Bank, (3) the Bank taking the stock or securities of an “affiliate” as collateral for loans by the Bank to a borrower, and (4) the purchase of assets from United by the Bank. Further, a bank holding company and its subsidiaries are prohibited from engaging in certain tie-in arrangements in connection with any extension of credit, lease or sale of property or furnishing of services.

The Bank and each of its subsidiaries are regularly examined by the Federal Deposit Insurance Corporation (the “FDIC”). The Bank, as a state banking association organized under Georgia law, is subject to the supervision of, and is regularly examined by, the DBF. The Bank’s North Carolina branches are subject to examination by the NCBC. The Bank’s Tennessee branches are subject to examination by the TDFI. Both the FDIC and the DBF must grant prior approval of any merger, consolidation or other corporation reorganization involving The Bank.

Payment of Dividends. United is a legal entity separate and distinct from the Bank. Most of the revenue of United results from dividends paid to it by the Bank. There are statutory and regulatory requirements applicable to the payment of dividends by the Bank, as well as by United to its shareholders.

Under the regulations of the DBF, dividends may not be declared out of the retained earnings of a state bank without first obtaining the written permission of the DBF, unless such bank meets all the following requirements:

| | (a) | total classified assets as of the most recent examination of the bank do not exceed 80% of equity capital (as defined by regulation); |

| | | |

| | (b) | the aggregate amount of dividends declared or anticipated to be declared in the calendar year does not exceed 50% of the net profits after taxes but before dividends for the previous calendar year; and |

| | | |

| | (c) | the ratio of equity capital to adjusted assets is not less than 6%. |

The payment of dividends by United and the Bank may also be affected or limited by other factors, such as the requirement to maintain adequate capital above regulatory guidelines. In addition, if, in the opinion of the applicable regulatory authority, a bank under its jurisdiction is engaged in or is about to engage in an unsafe or unsound practice (which, depending upon the financial condition of the bank, could include the payment of dividends), such authority may require, after notice and hearing, that such bank cease and desist from such practice. The FDIC has issued a policy statement providing that insured banks should generally only pay dividends out of current operating earnings. In addition to the formal statutes and regulations, regulatory authorities consider the adequacy of the Bank’s total capital in relation to its assets, deposits and other such items. Capital adequacy considerations could further limit the availability of dividends from the Bank. At February 1, 2008, net assets available from the Bank to pay dividends without prior approval from regulatory authorities totaled approximately $28 million. For 2007, United’s declared cash dividend payout to common stockholders was $16.8 million, or 28.57% of basic earnings per common share.

Capital Adequacy. The Federal Reserve and the FDIC have implemented substantially identical risk-based rules for assessing bank and bank holding company capital adequacy. These regulations establish minimum capital standards in relation to assets and off-balance sheet exposures as adjusted for credit risk. Banks and bank holding companies are required to have (1) a minimum level of Total Capital (as defined) to risk-weighted assets of eight percent (8%); and (2) a minimum Tier I Capital (as defined) to risk-weighted assets of four percent (4%). In addition, the Federal Reserve and the FDIC have established a minimum three percent (3%) leverage ratio of Tier I Capital to quarterly average total assets for the most highly-rated banks and bank holding companies. “Tier I Capital” generally consists of common equity excluding unrecognized gains and losses on available for sale securities, plus minority interests in equity accounts of consolidated subsidiaries and certain perpetual preferred stock less certain intangibles. The Federal Reserve and the FDIC will require a bank holding company and a bank, respectively, to maintain a leverage ratio greater than four percent (4%) if either is experiencing or anticipating significant growth or is operating with less than well-diversified risks in the opinion of the Federal Reserve. The Federal Reserve and the FDIC use the leverage ratio in tandem with the risk-based ratio to assess the capital adequacy of banks and bank holding companies. The FDIC, the Office of the Comptroller of the Currency (the “OCC”) and the Federal Reserve consider interest rate risk in the overall determination of a bank’s capital ratio, requiring banks with greater interest rate risk to maintain adequate capital for the risk.

In addition, Section 38 of the Federal Deposit Insurance Act implemented the prompt corrective action provisions that Congress enacted as a part of the Federal Deposit Insurance Corporation Improvement Act of 1991 (the “1991 Act”). The “prompt corrective action” provisions set forth five regulatory zones in which all banks are placed largely based on their capital positions. Regulators are permitted to take increasingly harsh action as a bank’s financial condition declines. Regulators are also empowered to place in receivership or require the sale of a bank to another depository institution when a bank’s capital leverage ratio reaches 2%. Better capitalized institutions are generally subject to less onerous regulation and supervision than banks with lesser amounts of capital.

The FDIC has adopted regulations implementing the prompt corrective action provisions of the 1991 Act, which place financial institutions in the following five categories based upon capitalization ratios: (1) a “well-capitalized” institution has a Total risk-based capital ratio of at least 10%, a Tier I risk-based ratio of at least 6% and a leverage ratio of at least 5%; (2) an “adequately capitalized” institution has a Total risk-based capital ratio of at least 8%, a Tier I risk-based ratio of at least 4% and a leverage ratio of at least 4%; (3) an “undercapitalized” institution has a Total risk-based capital ratio of under 8%, a Tier I risk-based ratio of under 4% or a leverage ratio of under 4%; (4) a “significantly undercapitalized” institution has a Total risk-based capital ratio of under 6%, a Tier I risk-based ratio of under 3% or a leverage ratio of under 3%; and (5) a “critically undercapitalized” institution has a leverage ratio of 2% or less. Institutions in any of the three undercapitalized categories would be prohibited from declaring dividends or making capital distributions. The FDIC regulations also establish procedures for “downgrading” an institution to a lower capital category based on supervisory factors other than capital.

To continue to conduct its business as currently conducted, United and the Bank will need to maintain capital well above the minimum levels. As of December 31, 2007 and 2006, the most recent notifications from the FDIC categorize the Bank as “well-capitalized” under current regulations.

Commercial Real Estate. In December, 2006 the federal banking agencies, including the FDIC, issued a final guidance on concentrations in commercial real estate lending, noting that recent increases in banks’ commercial real estate concentrations could create safety and soundness concerns in the event of a significant economic downturn. The guidance mandates certain minimal risk management practices and categorizes banks with defined levels of such concentrations as banks requiring elevated examiner scrutiny. The Bank has concentrations in commercial real estate loans in excess of those defined levels. Although management believes that United’s credit processes and procedures meet the risk management standards dictated by this guidance, regulatory outcomes could effectively limit increases in the real estate concentrations in the Bank’s loan portfolio and require additional credit administration and management costs associated with those portfolios.

Loans. Inter-agency guidelines adopted by federal bank regulators mandate that financial institutions establish real estate lending policies with maximum allowable real estate loan-to-value limits, subject to an allowable amount of non-conforming loans as a percentage of capital. The Bank adopted the federal guidelines in 2001.

Transactions with Affiliates. Under federal law, all transactions between and among a state nonmember bank and its affiliates, which include holding companies, are subject to Sections 23A and 23B of the Federal Reserve Act and Regulation W promulgated thereunder. Generally, these requirements limit these transactions to a percentage of the bank’s capital and require all of them to be on terms at least as favorable to the bank as transactions with non-affiliates. In addition, a bank may not lend to any affiliate engaged in non-banking activities not permissible for a bank holding company or acquire shares of any affiliate that is not a subsidiary. The FDIC is authorized to impose additional restrictions on transactions with affiliates if necessary to protect the safety and soundness of a bank. The regulations also set forth various reporting requirements relating to transactions with affiliates.

Financial Privacy. In accordance with the GLB Act, federal banking regulators adopted rules that limit the ability of banks and other financial institutions to disclose non-public information about consumers to nonaffiliated third parties. These limitations require disclosure of privacy policies to consumers and, in some circumstances, allow consumers to prevent disclosure of certain personal information to a nonaffiliated third party. The privacy provisions of the GLB Act affect how consumer information is transmitted through diversified financial companies and conveyed to outside vendors.

Anti-Money Laundering Initiatives and the USA Patriot Act. A major focus of governmental policy on financial institutions in recent years has been aimed at combating terrorist financing. This has generally been accomplished by amending existing anti-money laundering laws and regulations. The USA Patriot Act of 2001 (the “USA Patriot Act”) has imposed significant new compliance and due diligence obligations, creating new crimes and penalties. The United States Treasury Department has issued a number of implementing regulations which apply to various requirements of the USA Patriot Act to United and the Bank. These regulations impose obligations on financial institutions to maintain appropriate policies, procedures and controls to detect, prevent and report money laundering and terrorist financing and to verify the identity of their customers. Failure of a financial institution to maintain and implement adequate programs to combat terrorist financing, or to comply with all of the relevant laws or regulations, could have serious legal and reputational consequences for the institution.

Executive Officers Of United

Senior executives of United are elected by the Board of Directors annually and serve at the pleasure of the Board of Directors.

The senior executives officers of United, and their ages, positions with United, past five year employment history and terms of office as of February 1, 2008, are as follows:

| Name (age) | Position with United | Officer of United Since |

| | | |

Jimmy C. Tallent (55) | President, Chief Executive Officer and Director | 1988 |

| | | |

Guy W. Freeman (71) | Executive Vice President, Chief Operating Officer and Director | 1995 |

| | | |

Rex S. Schuette (58) | Executive Vice President and Chief Financial Officer | 2001 |

| | | |

David Shearrow (48) | Executive Vice President and Chief Risk Officer since April 2007; prior to joining United, he served as Executive Vice President and Senior Credit Officer of SunTrust Banks. | 2007 |

| | | |

Craig Metz (52) | Executive Vice President of Marketing | 2002 |

| | | |

Bill M. Gilbert (55) | Senior Vice President of Retail Banking since June 2003; previously, he was President of United Community Bank - Summerville | 2003 |

None of the above officers are related and there are no arrangements or understandings between them and any other person pursuant to which any of them was elected as an officer, other than arrangements or understandings with directors or officers of United acting solely in their capacities as such. Thomas C. Gilliland, former Executive Vice President, Secretary, and General Counsel, retired effective January 31, 2008.

ITEM 1A. RISK FACTORS.

An investment in United’s common stock involves risk. Investors should carefully consider the risks described below and all other information contained in this Annual Report on Form 10-K and the documents incorporated by reference before deciding to purchase common stock. It is possible that risks and uncertainties not listed below may arise or become material in the future and affect United’s business.

Past operating results may not be indicative of future operating results.

United may not be able to sustain its growth. Various factors, such as increased size, economic conditions, regulatory and legislative considerations, competition and the ability to find and retain people that can make United’s community-focused operating model successful, may impede its ability to expand its market presence. If United experiences a significant decrease in its growth rate, its results of operations and financial condition may be adversely affected.

United’s business is subject to the success of the local economies and real estate markets in which it operates.

United’s success significantly depends on the growth in population, income levels, loans and deposits and on the continued stability in real estate values in its markets. If the communities in which it operates do not grow or if prevailing economic conditions locally or nationally are unfavorable, United’s business may be adversely affected. Adverse economic conditions in United’s specific market areas, specifically decreases in real estate property values due to the nature of United’s loan portfolio, approximately 90% of which is secured by real estate, could reduce United’s growth rate, affect the ability of customers to repay their loans and generally affect United’s financial condition and results of operations. United is less able than a larger institution to spread the risks of unfavorable local economic conditions across a large number of more diverse economies.

United’s concentration of residential construction loans is subject to unique risks that could adversely affect earnings.

United’s residential construction loan portfolio was $1.8 billion at December 31, 2007, comprising 31% of total loans. Residential construction loans are often riskier than home equity loans or residential mortgage loans to individuals. In the event of a general economic slowdown like the one we are currently experiencing, these loans sometimes represent higher risk due to slower sales and reduced cash flow that could affect the borrowers’ ability to repay on a timely basis.

In addition, although regulations and regulatory policies affecting banks and financial services companies undergo continuous change and we cannot predict when changes will occur or the ultimate effect of any changes, there has been recent regulatory focus on construction, development and other commercial real estate lending. Recent changes in the federal policies applicable to construction, development or other commercial real estate loans make us subject us to substantial limitations with respect to making such loans, increase the costs of making such loans, and require us to have a greater amount of capital to support this kind of lending, all of which could have a material adverse effect on our profitability or financial condition.

United may face risks with respect to future expansion and acquisitions.

United regularly engages in de novo branch expansion. Also, when a business opportunity becomes available in the right market with the right management team, United may seek to acquire other financial institutions or parts of those institutions. These involve a number of risks, including:

| | · | the potential inaccuracy of the estimates and judgments used to evaluate credit, operations, management and market risks with respect to an acquired branch or institution,a new branch office or a new market; |

| | · | the time and costs of evaluating new markets, hiring or retaining experienced local management and opening new offices and the time lags between these activities and the generation of sufficient assets and deposits to support the costs of the expansion; |

| | · | the incurrence and possible impairment of goodwill associated with an acquisition and possible adverse effects on results of operations; and |

| | · | the risk of loss of key employees and customers of an acquired branch or institution. |

Changes in prevailing interest rates may negatively affect net income and the value of United’s assets.

Changes in prevailing interest rates may negatively affect the level of net interest revenue, the primary component of net income. In a period of changing interest rates, interest expense may increase at different rates than the interest earned on assets. Accordingly, changes in interest rates could decrease net interest revenue. At December 31, 2007, our simulation model indicated that a 200 basis point increase in rates over the next twelve months would cause an approximate 1.3% increase in net interest revenue and a 200 basis point decrease in rates over the next twelve months would cause an approximate 1.5% decrease in net interest revenue.

Changes in the level of interest rates may also negatively affect the value of United’s assets and its ability to realize gains or avoid losses from the sale of those assets, all of which ultimately affect earnings. In addition, an increase in interest rates may decrease the demand for loans.

If United’s allowance for loan losses is not sufficient to cover actual loan losses, earnings would decrease.

United’s loan customers may not repay their loans according to their terms and the collateral securing the payment of these loans may be insufficient to assure repayment. United may experience significant loan losses which would have a material adverse effect on operating results. Management makes various assumptions and judgments about the collectibility of the loan portfolio, including the creditworthiness of borrowers and the value of the real estate and other assets serving as collateral for the repayment of loans. United maintains an allowance for loan losses in an attempt to cover any loan losses inherent in the portfolio. In determining the size of the allowance, management relies on an analysis of the loan portfolio based on historical loss experience, volume and types of loans, trends in classification, volume and trends in delinquencies and non-accruals, national and local economic conditions and other pertinent information. If those assumptions are incorrect, the allowance may not be sufficient to cover future loan losses and adjustments may be necessary to allow for different economic conditions or adverse developments in the loan portfolio.

United may be subject to losses due to fraudulent and negligent conduct of our loan customers, third party service providers and employees.

When we make loans to individuals or entities, we rely upon information supplied by borrowers and other third parties, including information contained in the applicant’s loan application, property appraisal reports, title information and the borrower’s net worth, liquidity and cash flow information. While we attempt to verify information provided through available sources, we cannot be certain all such information is correct or complete. Our reliance on incorrect or incomplete information could have a material adverse effect on our profitability or financial condition.

Competition from financial institutions and other financial service providers may adversely affect United’s profitability.

The banking business is highly competitive, and United experiences competition in each of its markets from many other financial institutions. United competes with commercial banks, credit unions, savings and loan associations, mortgage banking firms, securities brokerage firms, insurance companies, money market funds and other mutual funds, as well as community, super-regional, national and international financial institutions that operate offices in its market areas and elsewhere. United competes with these institutions both in attracting deposits and in making loans. Many of United’s competitors are well-established, larger financial institutions that are able to operate profitably with a narrower net interest margin and have a more diverse revenue base. United may face a competitive disadvantage as a result of its smaller size, more limited geographic diversification and inability to spread costs across broader markets. Although United competes by concentrating marketing efforts in primary markets with local advertisements, personal contacts and greater flexibility and responsiveness in working with local customers, there can be no assurance that this strategy will continue to be successful.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

There are no unresolved comments from the Securities and Exchange Commission staff regarding United’s periodic or current reports under the Exchange Act.

ITEM 2. PROPERTIES.

The executive offices of United are located at 63 Highway 515, Blairsville, Georgia. United owns this property. The Bank conducts business from facilities primarily owned by the Bank, all of which are in a good state of repair and appropriately designed for use as banking facilities. The Bank, Brintech and UCIS provide services or perform operational functions at 130 locations, of which 99 are owned and 31 are leased under operating leases. Note 7 to United’s Consolidated Financial Statements includes additional information regarding amounts invested in premises and equipment.

ITEM 3. LEGAL PROCEEDINGS.

In the ordinary course of operations, United and the Bank are defendants in various legal proceedings incidental to its business. In the opinion of management, there is no pending or threatened proceeding in which an adverse decision will result in a material adverse change in the consolidated financial condition or results of operations of United. No material proceedings terminated in the fourth quarter of 2007.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

No matters were submitted to a vote of the security holders of United during the fourth quarter of 2007.

PART II

ITEM 5. MARKET FOR UNITED’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Stock. United’s common stock trades on the Nasdaq Global Select Market under the symbol “UCBI”. The closing price for the period ended December 31, 2007 was $15.80. Below is a schedule of high, low and closing stock prices and average daily volume for all quarters in 2007 and 2006.

Stock Price Information

| | | 2007 | | | 2006 | |

| | | High | | | Low | | | Close | | | Avg Daily Volume | | | High | | | Low | | | Close | | | Avg Daily Volume | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| First quarter | | $ | 34.98 | | | $ | 30.81 | | | $ | 32.79 | | | | 232,269 | | | $ | 29.64 | | | $ | 26.02 | | | $ | 28.15 | | | | 59,252 | |

| Second quarter | | | 33.03 | | | | 25.80 | | | | 25.89 | | | | 266,682 | | | | 31.26 | | | | 27.02 | | | | 30.44 | | | | 92,937 | |

| Third quarter | | | 27.50 | | | | 22.16 | | | | 24.52 | | | | 346,596 | | | | 33.10 | | | | 27.51 | | | | 30.05 | | | | 86,495 | |

| Fourth quarter | | | 25.73 | | | | 15.13 | | | | 15.80 | | | | 421,910 | | | | 33.37 | | | | 29.03 | | | | 32.32 | | | | 87,626 | |

At January 31, 2008, there were approximately 6,435 record shareholders and 15,200 beneficial shareholders of United’s common stock.

Dividends. United declared cash dividends of $.36, $.32 and $.28 per common share in 2007, 2006 and 2005, respectively. Federal and state laws and regulations impose restrictions on the ability of United and the Bank to pay dividends. Additional information regarding this item is included in Note 16 to the Consolidated Financial Statements and under the heading of “Supervision and Regulation” in Part I of this report.

Share Repurchases. United has in place a board approved repurchase authorization for up to 3,000,000 shares of United’s common stock. The share repurchase program was initially authorized for 1,000,000 shares expiring December 31, 2007 and was announced in our Form 10-Q for the period ended March 31, 2006, filed May 8, 2006. In July 2007, the authorization was increased by the Board of Directors to 2,000,000 shares as announced in our Form 10-Q for the period ended June 30, 2007, filed August 8, 2007. In October 2007, the Board of Directors further increased the authorization to 3,000,000 shares and extended the expiration date to December 31, 2008. This amendment was announced in our third quarter 2007 earnings announcement dated October 23, 2007. At December 31, 2007, 2,000,000 shares had been purchased under the authorization and 1,000,000 shares remain available under the authorization. Stock repurchases may be made in the open market or in private transactions at time and in amounts we deem appropriate. However, there is no guarantee as to the exact number of additional shares that may be repurchased and we may terminate or limit the stock repurchase program at any time. We will hold the repurchased shares as treasury shares.

Additionally, United’s Amended and Restated 2000 Key Employee Stock Option Plan allows option holders to exercise stock options by delivering previously acquired shares having a fair market value equal to the exercise price provided that the shares delivered must have been held by the option holder for at least six months. During 2007 and 2006, optionees delivered 1,755 and 17,576 shares, respectively, to exercise stock options.

The following table sets forth information regarding purchases of our common stock by us or any affiliated purchaser, by quarter, during 2007. There were no purchases of stock during the first and second quarters of 2007 and there were no purchases, other than shares delivered by optionees, during 2006.

| Period | | Total number of shares purchased | | | Average price paid per share | | | Total number of shares purchased as part of publicly announced plans or programs | | | Maximum number of shares that may yet be purchased under the publicly announced plans or programs | |

| | | | | | | | | | | | | |

| July 2007 | | | 62,000 | | | $ | 23.91 | | | | 62,000 | | | | 2,938,000 | |

| August 2007 | | | 602,775 | | | | 24.08 | | | | 602,775 | | | | 2,335,225 | |

| September 2007 | | | 640,000 | | | | 24.81 | | | | 640,000 | | | | 1,695,225 | |

| Total third quarter | | | 1,304,775 | | | | 24.43 | | | | 1,304,775 | | | | | |

| | | | | | | | | | | | | | | | | |

| October 2007 | | | 94,600 | | | $ | 22.02 | | | | 94,600 | | | | 1,600,625 | |

| November 2007 | | | 495,000 | | | | 20.42 | | | | 495,000 | | | | 1,105,625 | |

| December 2007 | | | 105,625 | | | | 18.85 | | | | 105,625 | | | | 1,000,000 | |

| Total fourth quarter | | | 695,225 | | | | 20.40 | | | | 695,225 | | | | | |

| | | | | | | | | | | | | | | | | |

Sales of Unregistered Securities. United has not sold any unregistered securities in the past three years other than 7,500 shares sold to one employee in one transaction for $15.37 per share on August 4, 2005 and 189 shares sold to one employee in one transaction for $7.55 on July 13, 2005. Both of these transactions were pursuant to the exercise of options granted by companies that were acquired by United, exempt under Section 4(2) of the Securities Act because of the small number of purchasers and shares involved, the knowledge and sophistication of the purchases and the nature of the transactions.

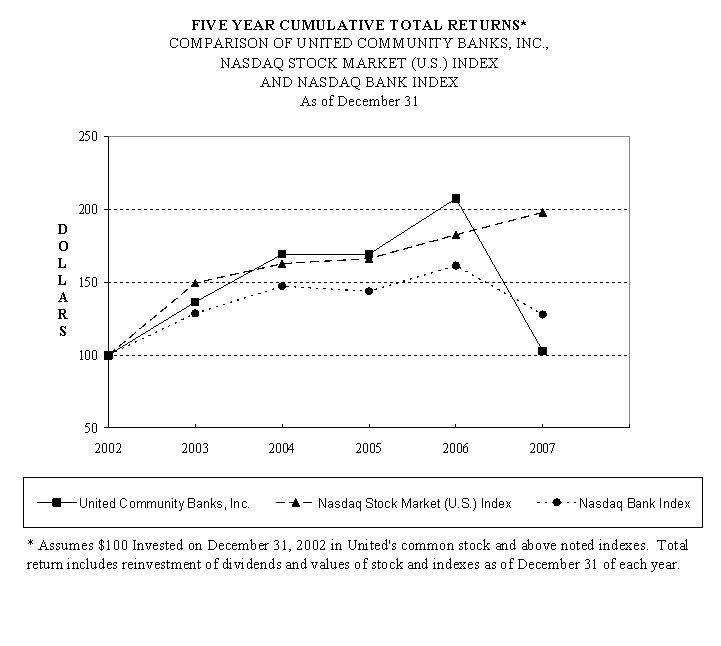

Performance Graph. Set forth below is a line graph comparing the yearly percentage change in the cumulative total shareholder return on United’s common stock against the cumulative total return on the Nasdaq Stock Market (U.S. Companies) Index and the Nasdaq Bank Stocks Index for the five-year period commencing December 31, 2002 and ending on December 31, 2007.

| | | Cumulative Total Return | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | |

| United Community Banks, Inc. | | $ | 100 | | | $ | 136 | | | $ | 169 | | | $ | 169 | | | $ | 207 | | | $ | 103 | |

| Nasdaq Stock Market (U.S.) Index | | | 100 | | | | 150 | | | | 163 | | | | 166 | | | | 183 | | | | 198 | |

| Nasdaq Bank Index | | | 100 | | | | 129 | | | | 147 | | | | 144 | | | | 161 | | | | 128 | |

| ITEM 6. SELECTED FINANCIAL DATA. | | | | | | | | | | | | | | | | | | |

| UNITED COMMUNITY BANKS, INC. | | | | | | | | | | | | | | | | | | |

| Selected Financial Information | | | | | | | | | | | | | | | | | | |

| For the Years Ended December 31, | | | | | | | | | | | | | | | | | | |

| | |

| (in thousands, except per share data; | | | | | | | | | | | | | | | | | | 5 Year | |

| taxable equivalent) | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | CAGR (4) | |

| INCOME SUMMARY | | | | | | | | | | | | | | | | | | | | | |

| Interest revenue | | $ | 550,917 | | | $ | 446,695 | | | $ | 324,225 | | | $ | 227,792 | | | $ | 198,689 | | | $ | 185,498 | | | | |

| Interest expense | | | 276,434 | | | | 208,815 | | | | 127,426 | | | | 74,794 | | | | 70,600 | | | | 76,357 | | | | |

| Net interest revenue | | | 274,483 | | | | 237,880 | | | | 196,799 | | | | 152,998 | | | | 128,089 | | | | 109,141 | | | 20% | |

Provision for loan losses (1) | | | 37,600 | | | | 14,600 | | | | 12,100 | | | | 7,600 | | | | 6,300 | | | | 6,900 | | | | |

| Fee revenue | | | 62,651 | | | | 49,095 | | | | 46,148 | | | | 39,539 | | | | 38,184 | | | | 30,734 | | | 15 | |

| Total revenue | | | 299,534 | | | | 272,375 | | | | 230,847 | | | | 184,937 | | | | 159,973 | | | | 132,975 | | | 18 | |

Operating expenses (1) | | | 190,061 | | | | 162,070 | | | | 140,808 | | | | 110,974 | | | | 97,251 | | | | 80,690 | | | 19 | |

| Income before taxes | | | 109,473 | | | | 110,305 | | | | 90,039 | | | | 73,963 | | | | 62,722 | | | | 52,285 | | | 16 | |

| Income taxes | | | 40,482 | | | | 41,490 | | | | 33,297 | | | | 26,807 | | | | 23,247 | | | | 19,505 | | | | |

| Net operating income | | | 68,991 | | | | 68,815 | | | | 56,742 | | | | 47,156 | | | | 39,475 | | | | 32,780 | | | 16 | |

| Fraud loss provision, net of tax | | | 10,998 | | | | - | | | | - | | | | - | | | | - | | | | - | | | | |

| Merger-related charges, net of tax | | | - | | | | - | | | | - | | | | 565 | | | | 1,357 | | | | - | | | | |

| Net income | | $ | 57,993 | | | $ | 68,815 | | | $ | 56,742 | | | $ | 46,591 | | | $ | 38,118 | | | $ | 32,780 | | | 12 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

OPERATING PERFORMANCE (1) | | | | | | | | | | | | | | | | | | | | | | | | |

| Earnings per common share: | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 1.50 | | | $ | 1.70 | | | $ | 1.47 | | | $ | 1.31 | | | $ | 1.15 | | | $ | 1.02 | | | 8 | |

| Diluted | | | 1.48 | | | | 1.66 | | | | 1.43 | | | | 1.27 | | | | 1.12 | | | | .99 | | | 8 | |

Return on tangible equity (2)(3) | | | 14.23 | % | | | 17.52 | % | | | 18.99 | % | | | 19.74 | % | | | 19.24 | % | | | 17.88 | % | | | |

| Return on assets | | | .89 | | | | 1.09 | | | | 1.04 | | | | 1.07 | | | | 1.06 | | | | 1.11 | | | | |

| Efficiency ratio | | | 56.53 | | | | 56.35 | | | | 57.77 | | | | 57.65 | | | | 58.39 | | | | 57.72 | | | | |

| Dividend payout ratio | | | 24.00 | | | | 18.82 | | | | 19.05 | | | | 18.32 | | | | 17.39 | | | | 16.34 | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| GAAP PERFORMANCE | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Per common share: | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic earnings | | $ | 1.26 | | | $ | 1.70 | | | $ | 1.47 | | | $ | 1.29 | | | $ | 1.11 | | | $ | 1.02 | | | 4 | |

| Diluted earnings | | | 1.24 | | | | 1.66 | | | | 1.43 | | | | 1.25 | | | | 1.08 | | | | .99 | | | 5 | |

| Cash dividends declared (rounded) | .36 | | | | .32 | | | | .28 | | | | .24 | | | | .20 | | | | .17 | | | 17 | |

| Book value | | | 17.73 | | | | 14.37 | | | | 11.80 | | | | 10.39 | | | | 8.47 | | | | 6.89 | | | 21 | |

Tangible book value (3) | | | 10.94 | | | | 10.57 | | | | 8.94 | | | | 7.34 | | | | 6.52 | | | | 6.49 | | | 11 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Key performance ratios: | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Return on equity (2) | | | 7.79 | % | | | 13.28 | % | | | 13.46 | % | | | 14.39 | % | | | 14.79 | % | | | 16.54 | % | | | |

| Return on assets | | | .75 | | | | 1.09 | | | | 1.04 | | | | 1.05 | | | | 1.02 | | | | 1.11 | | | | |

| Net interest margin | | | 3.88 | | | | 4.05 | | | | 3.85 | | | | 3.71 | | | | 3.68 | | | | 3.95 | | | | |

| Dividend payout ratio | | | 28.57 | | | | 18.82 | | | | 19.05 | | | | 18.60 | | | | 18.02 | | | | 16.34 | | | | |

| Equity to assets | | | 9.61 | | | | 8.06 | | | | 7.63 | | | | 7.45 | | | | 7.21 | | | | 7.01 | | | | |

Tangible equity to assets (3) | | | 6.63 | | | | 6.32 | | | | 5.64 | | | | 5.78 | | | | 6.02 | | | | 6.60 | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ASSET QUALITY | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | $ | 89,423 | | | $ | 66,566 | | | $ | 53,595 | | | $ | 47,196 | | | $ | 38,655 | | | $ | 30,914 | | | | |

| Non-performing assets | | | 46,258 | | | | 13,654 | | | | 12,995 | | | | 8,725 | | | | 7,589 | | | | 8,019 | | | | |

| Net charge-offs | | | 39,834 | | | | 5,524 | | | | 5,701 | | | | 3,617 | | | | 4,097 | | | | 3,111 | | | | |

| Allowance for loan losses to loans | | | 1.51 | % | | | 1.24 | % | | | 1.22 | % | | | 1.26 | % | | | 1.28 | % | | | 1.30 | % | | | |

| Non-performing assets to total assets | | | .56 | | | | .19 | | | | .22 | | | | .17 | | | | .19 | | | | .25 | | | | |

| Net charge-offs to average loans | | | .69 | | | | .12 | | | | .14 | | | | .11 | | | | .15 | | | | .14 | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AVERAGE BALANCES | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 5,734,608 | | | $ | 4,800,981 | | | $ | 4,061,091 | | | $ | 3,322,916 | | | $ | 2,753,451 | | | $ | 2,239,875 | | | 21 | |

| Investment securities | | | 1,277,935 | | | | 1,041,897 | | | | 989,201 | | | | 734,577 | | | | 667,211 | | | | 464,468 | | | 22 | |

| Earning assets | | | 7,070,900 | | | | 5,877,483 | | | | 5,109,053 | | | | 4,119,327 | | | | 3,476,030 | | | | 2,761,265 | | | 21 | |

| Total assets | | | 7,730,530 | | | | 6,287,148 | | | | 5,472,200 | | | | 4,416,835 | | | | 3,721,284 | | | | 2,959,295 | | | 21 | |

| Deposits | | | 6,028,625 | | | | 5,017,435 | | | | 4,003,084 | | | | 3,247,612 | | | | 2,743,087 | | | | 2,311,717 | | | 21 | |

| Shareholders’ equity | | | 742,771 | | | | 506,946 | | | | 417,309 | | | | 329,225 | | | | 268,446 | | | | 207,312 | | | 29 | |

| Common shares - Basic | | | 45,893 | | | | 40,393 | | | | 38,477 | | | | 36,071 | | | | 34,132 | | | | 32,062 | | | | |

| Common shares - Diluted | | | 46,593 | | | | 41,575 | | | | 39,721 | | | | 37,273 | | | | 35,252 | | | | 33,241 | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AT YEAR END | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 5,929,263 | | | $ | 5,376,538 | | | $ | 4,398,286 | | | $ | 3,734,905 | | | $ | 3,015,997 | | | $ | 2,381,798 | | | 20 | |

| Investment securities | | | 1,356,846 | | | | 1,107,153 | | | | 990,687 | | | | 879,978 | | | | 659,891 | | | | 559,390 | | | 19 | |

| Total assets | | | 8,207,302 | | | | 7,101,249 | | | | 5,865,756 | | | | 5,087,702 | | | | 4,068,834 | | | | 3,211,344 | | | 21 | |

| Deposits | | | 6,075,951 | | | | 5,772,886 | | | | 4,477,600 | | | | 3,680,516 | | | | 2,857,449 | | | | 2,385,239 | | | 21 | |

| Shareholders’ equity | | | 831,902 | | | | 616,767 | | | | 472,686 | | | | 397,088 | | | | 299,373 | | | | 221,579 | | | 30 | |

| Common shares outstanding | | | 46,903 | | | | 42,891 | | | | 40,020 | | | | 38,168 | | | | 35,289 | | | | 31,895 | | | 8 | |

| (1) | | Excludes pre-tax provision for fraud losses of $18 million, or $.24 per diluted common share, recorded in 2007 and pre-tax merger-related charges totaling $.9 million, or $.02 per diluted common share, recorded in 2004 and $2.1 million, or $.04 per diluted share, recorded in 2003. |

| (2) | | Net income available to common shareholders, which excludes preferred stock dividends, divided by average realized common equity which excludes accumulated other comprehensive income (loss). |

| (3) | | Excludes effect of acquisition related intangibles and associated amortization. | | | | | | | | | |

| (4) | | Compound annual growth rate. | | | | | | | | | | | | | | |

| UNITED COMMUNITY BANKS, INC. | | | | | | | | | | | | | | | | | | | | | |

| Selected Financial Information (continued) | | | | | | | | | | | | | | | | | | | | | |

| | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2007 | | | 2006 | |

| (in thousands, except per share | | Fourth | | | Third | | | Second | | | First | | | Fourth | | | Third | | | Second | | | First | |

| data; taxable equivalent) | | Quarter | | | Quarter | | | Quarter | | | Quarter | | | Quarter | | | Quarter | | | Quarter | | | Quarter | |

| INCOME SUMMARY | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest revenue | | $ | 140,768 | | | $ | 144,884 | | | $ | 136,237 | | | $ | 129,028 | | | $ | 123,463 | | | $ | 116,304 | | | $ | 107,890 | | | $ | 99,038 | |

| Interest expense | | | 71,038 | | | | 73,203 | | | | 68,270 | | | | 63,923 | | | | 60,912 | | | | 55,431 | | | | 49,407 | | | | 43,065 | |

| Net interest revenue | | | 69,730 | | | | 71,681 | | | | 67,967 | | | | 65,105 | | | | 62,551 | | | | 60,873 | | | | 58,483 | | | | 55,973 | |

Provision for loan losses (1) | | | 26,500 | | | | 3,700 | | | | 3,700 | | | | 3,700 | | | | 3,700 | | | | 3,700 | | | | 3,700 | | | | 3,500 | |

| Fee revenue | | | 16,100 | | | | 15,615 | | | | 16,554 | | | | 14,382 | | | | 13,215 | | | | 12,146 | | | | 11,976 | | | | 11,758 | |

| Total revenue | | | 59,330 | | | | 83,596 | | | | 80,821 | | | | 75,787 | | | | 72,066 | | | | 69,319 | | | | 66,759 | | | | 64,231 | |

| Operating expenses | | | 49,336 | | | | 48,182 | | | | 47,702 | | | | 44,841 | | | | 42,521 | | | | 41,441 | | | | 39,645 | | | | 38,463 | |

| Income before taxes | | | 9,994 | | | | 35,414 | | | | 33,119 | | | | 30,946 | | | | 29,545 | | | | 27,878 | | | | 27,114 | | | | 25,768 | |

| Income taxes | | | 3,960 | | | | 12,878 | | | | 12,043 | | | | 11,601 | | | | 11,111 | | | | 10,465 | | | | 10,185 | | | | 9,729 | |

| Net operating income | | | 6,034 | | | | 22,536 | | | | 21,076 | | | | 19,345 | | | | 18,434 | | | | 17,413 | | | | 16,929 | | | | 16,039 | |

| Fraud loss provision, net of tax | | | 1,833 | | | | - | | | | 9,165 | | | | - | | | | - | | | | - | | | | - | | | | - | |

| Net income | | $ | 4,201 | | | $ | 22,536 | | | $ | 11,911 | | | $ | 19,345 | | | $ | 18,434 | | | $ | 17,413 | | | $ | 16,929 | | | $ | 16,039 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

OPERATING PERFORMANCE (1) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Per common share: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic earnings | | $ | .13 | | | $ | .47 | | | $ | .47 | | | $ | .45 | | | $ | .45 | | | $ | .43 | | | $ | .42 | | | $ | .40 | |

| Diluted earnings | | | .13 | | | | .46 | | | | .46 | | | | .44 | | | | .44 | | | | .42 | | | | .41 | | | | .39 | |

Return on tangible equity (2)(3)(4) | | | 5.06 | % | | | 17.54 | % | | | 17.52 | % | | | 17.18 | % | | | 17.49 | % | | | 17.29 | % | | | 17.68 | % | | | 17.66 | % |

Return on assets (4) | | | .29 | | | | 1.11 | | | | 1.12 | | | | 1.11 | | | | 1.10 | | | | 1.09 | | | | 1.10 | | | | 1.09 | |

| Dividend payout ratio | | | 69.23 | | | | 19.15 | | | | 19.15 | | | | 20.00 | | | | 17.78 | | | | 18.60 | | | | 19.05 | | | | 20.00 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| GAAP PERFORMANCE MEASURES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Per common share: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic earnings | | $ | .09 | | | $ | .47 | | | $ | .26 | | | $ | .45 | | | $ | .45 | | | $ | .43 | | | $ | .42 | | | $ | .40 | |

| Diluted earnings | | | .09 | | | | .46 | | | | .26 | | | | .44 | | | | .44 | | | | .42 | | | | .41 | | | | .39 | |

| Cash dividends declared | | | .09 | | | | .09 | | | | .09 | | | | .09 | | | | .08 | | | | .08 | | | | .08 | | | | .08 | |

| Book value | | | 17.73 | | | | 17.53 | | | | 16.98 | | | | 14.83 | | | | 14.37 | | | | 13.07 | | | | 12.34 | | | | 12.09 | |

Tangible book value (3) | | | 10.94 | | | | 10.82 | | | | 10.44 | | | | 11.06 | | | | 10.57 | | | | 10.16 | | | | 9.50 | | | | 9.25 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Key performance ratios: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Return on equity (2)(4) | | | 2.01 | % | | | 10.66 | % | | | 7.05 | % | | | 12.47 | % | | | 13.26 | % | | | 13.22 | % | | | 13.41 | % | | | 13.25 | % |

Return on assets (4) | | | .20 | | | | 1.11 | | | | .64 | | | | 1.11 | | | | 1.10 | | | | 1.09 | | | | 1.10 | | | | 1.09 | |

Net interest margin (4) | | | 3.73 | | | | 3.89 | | | | 3.94 | | | | 3.99 | | | | 3.99 | | | | 4.07 | | | | 4.07 | | | | 4.06 | |

| Efficiency ratio | | | 57.67 | | | | 55.34 | | | | 56.59 | | | | 56.56 | | | | 55.93 | | | | 56.46 | | | | 56.27 | | | | 56.79 | |

| Dividend payout ratio | | | 100.00 | | | | 19.15 | | | | 34.62 | | | | 20.00 | | | | 17.78 | | | | 18.60 | | | | 19.05 | | | | 20.00 | |

| Equity to assets | | | 10.20 | | | | 10.32 | | | | 8.94 | | | | 8.80 | | | | 8.21 | | | | 8.04 | | | | 7.95 | | | | 8.04 | |

Tangible equity to assets (3) | | | 6.58 | | | | 6.65 | | | | 6.65 | | | | 6.66 | | | | 6.46 | | | | 6.35 | | | | 6.22 | | | | 6.24 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ASSET QUALITY | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | $ | 89,423 | | | $ | 90,935 | | | $ | 92,471 | | | $ | 68,804 | | | $ | 66,566 | | | $ | 60,901 | | | $ | 58,508 | | | $ | 55,850 | |

| Non-performing assets | | | 46,258 | | | | 63,337 | | | | 43,601 | | | | 14,290 | | | | 13,654 | | | | 9,347 | | | | 8,805 | | | | 8,367 | |

| Net charge-offs | | | 31,012 | | | | 5,236 | | | | 2,124 | | | | 1,462 | | | | 1,930 | | | | 1,307 | | | | 1,042 | | | | 1,245 | |

| Allowance for loan losses to loans | | | 1.51 | % | | | 1.53 | % | | | 1.54 | % | | | 1.27 | % | | | 1.24 | % | | | 1.23 | % | | | 1.22 | % | | | 1.22 | % |

| Non-performing assets to total assets | | | .56 | | | | .77 | | | | .54 | | | | .20 | | | | .19 | | | | .14 | | | | .14 | | | | .14 | |

Net charge-offs to average loans (4) | | | 2.07 | | | | .35 | | | | .15 | | | | .11 | | | | .15 | | | | .11 | | | | .09 | | | | .11 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AVERAGE BALANCES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 5,940,230 | | | $ | 5,966,933 | | | $ | 5,619,950 | | | $ | 5,402,860 | | | $ | 5,134,721 | | | $ | 4,865,886 | | | $ | 4,690,196 | | | $ | 4,505,494 | |

| Investment securities | | | 1,404,796 | | | | 1,308,192 | | | | 1,242,448 | | | | 1,153,208 | | | | 1,059,125 | | | | 1,029,981 | | | | 1,039,707 | | | | 1,038,683 | |

| Earning assets | | | 7,424,992 | | | | 7,332,492 | | | | 5,915,134 | | | | 6,599,035 | | | | 6,225,943 | | | | 5,942,710 | | | | 5,758,697 | | | | 5,574,712 | |

| Total assets | | | 8,210,120 | | | | 8,083,739 | | | | 7,519,392 | | | | 7,092,710 | | | | 6,669,950 | | | | 6,350,205 | | | | 6,159,152 | | | | 5,960,801 | |

| Deposits | | | 6,151,476 | | | | 6,246,319 | | | | 5,945,633 | | | | 5,764,426 | | | | 5,517,696 | | | | 5,085,168 | | | | 4,842,389 | | | | 4,613,810 | |

| Stockholders’ equity | | | 837,195 | | | | 834,094 | | | | 672,348 | | | | 624,100 | | | | 547,419 | | | | 510,791 | | | | 489,821 | | | | 478,960 | |

| Common Shares - Basic | | | 47,203 | | | | 48,348 | | | | 44,949 | | | | 43,000 | | | | 41,096 | | | | 40,223 | | | | 40,156 | | | | 40,088 | |

| Common Shares - Diluted | | | 47,652 | | | | 48,977 | | | | 45,761 | | | | 43,912 | | | | 42,311 | | | | 41,460 | | | | 41,328 | | | | 41,190 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AT PERIOD END | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 5,929,263 | | | $ | 5,952,749 | | | $ | 5,999,093 | | | $ | 5,402,198 | | | $ | 5,376,538 | | | $ | 4,965,365 | | | $ | 4,810,277 | | | $ | 4,584,155 | |

| Investment securities | | | 1,356,846 | | | | 1,296,826 | | | | 1,213,659 | | | | 1,150,424 | | | | 1,107,153 | | | | 980,273 | | | | 974,524 | | | | 983,846 | |

| Total assets | | | 8,207,302 | | | | 8,180,600 | | | | 8,087,667 | | | | 7,186,602 | | | | 7,101,249 | | | | 6,455,290 | | | | 6,331,136 | | | | 6,070,596 | |

| Deposits | | | 6,075,951 | | | | 6,154,308 | | | | 6,361,269 | | | | 5,841,687 | | | | 5,772,886 | | | | 5,309,219 | | | | 4,976,650 | | | | 4,748,438 | |

| Stockholders’ equity | | | 831,902 | | | | 833,761 | | | | 828,731 | | | | 638,456 | | | | 616,767 | | | | 526,734 | | | | 496,297 | | | | 485,414 | |