UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark one)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: June 30, 2010

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________to ________________

Commission File Number: 333-126654

BIRCH BRANCH, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Colorado | | 84-1124170 |

| (State or Other jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | | |

c/o Henan Shuncheng Group Coal Coke Co., Ltd. Henan Province, Anyang County, Cai Cun Road Intersection, Henan Shuncheng Group Coal Coke Co., Ltd. (New Building), China | | 455141 |

| (Address of Principal Executive Offices) | | (Zip Code) |

+86 372 323 7890

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

32,047,222 shares of common stock are issued and outstanding as of August 20, 2010.

Table of Contents

| | Page |

| | |

| PART I – FINANCIAL INFORMATION | 1 |

| | |

| Item 1. Financial Statements (Unaudited) | 1 |

| | |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| | |

| PART II - OTHER INFORMATION | 44 |

| | |

| Item 6. Exhibits. | 44 |

EXPLANATORY NOTE

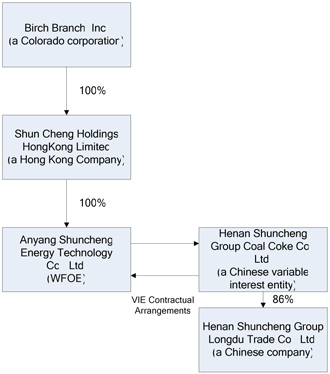

As used in this Quarterly Report, unless the context requires or is otherwise indicated, the terms “we,” “us,” “our,” the “Registrant,” the “Company,” “our company” and similar expressions include the following entities, after giving effect to the Share Exchange (as defined below):

(i) Birch Branch, Inc., a Colorado corporation (“BRBH”), which is a publicly traded company;

(ii) Shun Cheng Holdings HongKong Limited, a company organized under the laws of Hong Kong and a wholly-owned subsidiary of BRBH (“Shun Cheng HK”);

(iii) Anyang Shuncheng Energy Technology Co., Ltd., a Chinese wholly-foreign owned enterprise subsidiary of Shun Cheng HK (“Anyang WFOE”);

(iv) Henan Shuncheng Group Coal Coke Co., Ltd., a Chinese variable interest entity that Anyang WFOE controls through certain contractual arrangements (“SC Coke”); and

(v) Henan Shuncheng Group Longdu Trade Co., Ltd., a Chinese company which is 86% owned by SC Coke (“Longdu”). Wang Xinshun, our Chairman of the Board of Directors and the sole director and holder of a 60% interest in SC Coke, also owns a 5% interest in Longdu.

“China” or “PRC” refers to the People’s Republic of China, excluding Hong Kong, Macau and Taiwan. “RMB” or “Renminbi” refers to the legal currency of China and “$” or “U.S. Dollars” refers to the legal currency of the United States. The Company maintains its books and accounting records in Renminbi. Unless otherwise stated, the translations of RMB into U.S. Dollars have been made at the rate of exchange of $1.00 to RMB 6.8348, the approximate average exchange rate for the six months ended June 30, 2010. We make no representation that the RMB or U.S. Dollar amounts referred to in this Quarterly Report could have been or could be converted into U.S. Dollars or RMB, as the case may be, at any particular rate or at all. “GAAP” unless otherwise indicated refers to United States generally accepted accounting principles.

When used herein to describe SC Coke’s current products, “coke” refers to metallurgical coke unless otherwise indicated.

PART I – FINANCIAL INFORMATION

| Financial Statements (Unaudited) |

Birch Branch, Inc.

Consolidated Balance Sheets

As of June 30, 2010 and December 31, 2009

(Stated in US Dollars)

(unaudited)

| | | Note | | | 6/30/2010 | | | 12/31/2009 | |

| | | | | | | | | | |

Assets | | | | | | | | | |

| Current assets: | | | | | | | | | |

| Cash | | | 2D | | | $ | 6,295,178 | | | $ | 5,749,945 | |

| Restricted cash | | | 2E | | | | 64,771,024 | | | | 52,404,530 | |

| Bank notes receivable | | | 2F | | | | 7,408,689 | | | | 4,658,384 | |

| Trade receivables | | | 2G, 3 | | | | 25,238,022 | | | | 11,342,082 | |

| Other receivables | | | | | | | 14,405,374 | | | | - | |

| Related party receivable | | | 13 | | | | 36,278 | | | | - | |

| Inventories | | | 2H,4 | | | | 34,704,642 | | | | 32,426,320 | |

| Advances to Suppliers and Prepayments | | | 5 | | | | 60,051,807 | | | | 67,797,396 | |

| Total current assets | | | | | | | 212,911,014 | | | | 174,378,657 | |

| | | | | | | | | | | | | |

| Deposits for construction projects | | | | | | | 19,063,718 | | | | 9,578,896 | |

| Plant and equipment, net | | | 2I,6 | | | | 78,250,164 | | | | 65,386,090 | |

| Long-term investments | | | 2J, 7 | | | | 19,715,369 | | | | 15,420,649 | |

| Total non-current assets | | | | | | | 117,029,251 | | | | 90,385,635 | |

| | | | | | | | | | | | | |

| Total assets | | | | | | $ | 329,940,265 | | | $ | 264,764,292 | |

| | | | | | | | | | | | | |

| Liabilities and Stockholders’ Equity | | | | | | | | | | | | |

| | | | | | | | | | | | | |

Liabilities | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Current liabilities: | | | | | | | | | | | | |

| Bank notes payable | | | 8 | | | $ | 79,458,332 | | | $ | 59,234,774 | |

| Accounts payable | | | | | | | 47,962,168 | | | | 23,211,187 | |

| Accrued liabilities | | | | | | | 89,085 | | | | 438,928 | |

| Taxes payable | | | | | | | 10,481,603 | | | | 8,390,646 | |

| Loans | | | 9 | | | | 33,193,314 | | | | 67,299,038 | |

| Other payable | | | 10 | | | | 18,097,774 | | | | 10,254,272 | |

| Capital lease obligation, current portion | | | 15 | | | | 1,362,427 | | | | 989,829 | |

| Customer deposits | | | | | | | 13,772,337 | | | | 7,829,089 | |

| Total current liabilities | | | | | | | 204,417,040 | | | | 177,647,763 | |

| | | | | | | | | | | | | |

| Notes payable to related parties | | | 11 | | | | 71,308,488 | | | | 35,635,066 | |

| Forgivable loans | | | 12 | | | | 5,192,184 | | | | 5,192,184 | |

| Capital lease obligation, non-current portion | | | 15 | | | | 4,491,254 | | | | 5,163,274 | |

| Total non-current liabilities | | | | | | | 80,991,926 | | | | 45,990,524 | |

| | | | | | | | | | | | | |

| Total liabilities | | | | | | $ | 285,408,966 | | | $ | 223,638,287 | |

| | | | | | | | | | | | | |

Stockholders’ Equity | | | | | | | | | | | | |

| Preferred stock, 50,000,000 shares authorized, no par value, 0 shares issued and outstanding | | | | | | $ | - | | | $ | - | |

| Common stock, 500,000,000 shares authorized, no par value, 32,047,222 shares issued and outstanding | | | | | | | - | | | | - | |

| Additional paid in capital | | | | | | | 8,127,560 | | | | 6,395,907 | |

| Statutory reserve | | | | | | | 234,683 | | | | 234,683 | |

| Retained earnings | | | | | | | 33,945,520 | | | | 31,426,894 | |

| Accumulated other comprehensive income | | | | | | | 1,798,051 | | | | 2,595,677 | |

| Non-controlling interest | | | | | | | 425,485 | | | | 472,844 | |

| Total stockholders’ equity | | | | | | | 44,531,299 | | | | 41,126,005 | |

| | | | | | | | | | | | | |

| Total liabilities and equity | | | | | | $ | 329,940,265 | | | $ | 264,764,292 | |

The accompanying notes are an integral part of these consolidated financial statements

Birch Branch, Inc.

Consolidated Statements of Operations

For the three and six months ended June 30, 2010 and 2009

(unaudited)

| | | | | | Three months ended | | | Six months ended | |

| | | Note | | | 6/30/2010 | | | 6/30/2009 | | | 6/30/2010 | | | 6/30/2009 | |

| Revenues | | 2P | | | $ | 74,640,647 | | | $ | 50,974,475 | | | $ | 139,057,967 | | | $ | 77,370,512 | |

| Cost of revenues | | | | | | | 69,310,348 | | | | 46,058,684 | | | | 128,753,949 | | | | 70,900,979 | |

| Gross profit | | | | | | | 5,330,299 | | | | 4,915,791 | | | | 10,304,018 | | | | 6,469,533 | |

| | | | | | | | | | | | | | | | | | | | | |

| Operating expenses: | | | | | | | | | | | | | | | | | | | | |

| Sales and marketing | | 2R | | | | 952,614 | | | | 1,189,336 | | | | 1,815,988 | | | | 1,986,254 | |

| General and administrative | | | | | | | 1,383,150 | | | | 914,540 | | | | 3,111,609 | | | | 2,192,868 | |

| Total operating expenses | | | | | | | 2,335,764 | | | | 2,103,876 | | | | 4,927,597 | | | | 4,179,122 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income from operations | | | | | | | 2,994,535 | | | | 2,811,915 | | | | 5,376,421 | | | | 2,290,411 | |

| | | | | | | | | | | | | | | | | | | | | |

| Other income (expense): | | | | | | | | | | | | | | | | | | | | |

| Interest income | | | | | | | 189,671 | | | | 222,941 | | | | 501,406 | | | | 449,307 | |

| Interest expense | | | | | | | (1,397,706 | ) | | | (374,309 | ) | | | (2,633,454 | ) | | | (957,273 | ) |

| Other income | | | | | | | 142,691 | | | | 113,741 | | | | 246,685 | | | | 95,457 | |

| Other expense | | | | | | | - | | | | - | | | | - | | | | (50,693 | ) |

| Gain on investment | | | | | | | - | | | | 2,600,270 | | | | - | | | | 2,600,270 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total other income (expense) | | | | | | | (1,065,344 | ) | | | 2,562,643 | | | | (1,885,363 | ) | | | 2,137,068 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income before provision for income taxes | | | 2S, 14 | | | | 1,929,191 | | | | 5,374,558 | | | | 3,491,058 | | | | 4,427,479 | |

| | | | | | | | | | | | | | | | | | | | | |

| Provision for income taxes | | | | | | | 517,652 | | | | 1,438,106 | | | | 1,019,791 | | | | 1,201,336 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net income | | | | | | $ | 1,411,539 | | | $ | 3,936,452 | | | $ | 2,471,267 | | | $ | 3,226,143 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net income attributable to: | | | | | | | | | | | | | | | | | | | | |

| - Common stockholders | | | | | | $ | 1,396,362 | | | $ | 3,903,378 | | | $ | 2,518,626 | | | $ | 3,210,143 | |

| - Non-controlling interest | | | | | | $ | 15,172 | | | $ | 33,074 | | | $ | (47,359 | ) | | $ | 16,000 | |

| | | | | | | | | | | | | | | | | | | | | |

| Earnings per share | | | | | | | | | | | | | | | | | | | | |

| - Basic | | | | | | $ | 0.04 | | | $ | 0.12 | | | $ | 0.08 | | | $ | 0.10 | |

| - Diluted | | | | | | $ | 0.04 | | | $ | 0.12 | | | $ | 0.08 | | | $ | 0.10 | |

| | | | | | | | | | | | | | | | | | | | | |

| Weighted average shares outstanding | | | | | | | | | | | | | | | | | | | | |

| - Basic | | | | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

| - Diluted | | | | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

The accompanying notes are an integral part of these consolidated financial statements

Birch Branch, Inc.

Consolidated Statements of Equity

As of June 30, 2010 and December 31, 2009

And for the six months ended June 30, 2010 and 2009

(unaudited)

| | | | | | | | | | | | | | | | | | | | | Accumulated | | | | |

| | | | | | | | | Additional | | | | | | | | | Non- | | | Other | | | | |

| | | Shares | | | | | | Paid-in | | | Statutory | | | Retained | | | controlling | | | Comprehensive | | | Total | |

| | | Outstanding | | | Amount | | | Capital | | | Reserve | | | Earnings | | | Interest | | | Income | | | Equity | |

| Balance at January 1, 2009 | | | 1,708,123 | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | |

| Share Exchange | | | 30,233,750 | | | | - | | | | 6,395,907 | | | | 234,683 | | | | 15,681,231 | | | | 368,832 | | | | 2,429,705 | | | | 25,110,358 | |

| Cancellation of Shares | | | (435,123 | ) | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

| Net income | | | - | | | | - | | | | - | | | | - | | | | 15,849,675 | | | | - | | | | - | | | | 15,849,675 | |

| Apportionment of net income to non-controlling interest | | | - | | | | - | | | | - | | | | - | | | | (104,012 | ) | | | 104,012 | | | | - | | | | - | |

| Currency translation adjustment | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | 165,972 | | | | 165,972 | |

| Balance at December 31, 2009 | | | 31,506,750 | | | $ | - | | | $ | 6,395,907 | | | $ | 234,683 | | | $ | 31,426,894 | | | $ | 472,844 | | | $ | 2,595,677 | | | $ | 41,126,005 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance at January 1, 2010 | | | 31,506,750 | | | $ | - | | | $ | 6,395,907 | | | $ | 234,683 | | | $ | 31,426,894 | | | $ | 472,844 | | | $ | 2,595,677 | | | $ | 41,126,005 | |

| Share Compensation (see Note 17) | | | 540,472 | | | | - | | | | 567,496 | | | | - | | | | - | | | | - | | | | - | | | | 567,496 | |

| Capital Contribution | | | - | | | | - | | | | 1,164,157 | | | | - | | | | - | | | | - | | | | - | | | | 1,164,157 | |

| Apportionment of loss to non-controlling interest | | | - | | | | - | | | | - | | | | - | | | | 47,359 | | | | (47,359 | ) | | | - | | | | - | |

| Net income | | | - | | | | - | | | | - | | | | - | | | | 2,471,267 | | | | - | | | | - | | | | 2,471,267 | |

| Currency translation adjustment | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | (797,627 | ) | | | (797,627 | ) |

| Balance at June 30, 2010 | | | 32,047,222 | | | $ | - | | | $ | 8,127,560 | | | $ | 234,683 | | | $ | 33,945,520 | | | $ | 425,485 | | | $ | 1,798,050 | | | $ | 44,531,298 | |

| | | Six Months Ended | |

| | | 6/30/2010 | | | 6/30/2009 | |

| Comprehensive Income | | | | | | |

| Net Income | | $ | 2,471,267 | | | $ | 3,226,143 | |

| Other Comprehensive Income | | | | | | | | |

| Foreign Currency Translation Adjustment | | | (797,627 | ) | | | 130,004 | |

| Total Comprehensive Income | | $ | 1,673,640 | | | $ | 3,356,147 | |

The accompanying notes are an integral part of these consolidated financial statements

Birch Branch, Inc.

Consolidated Statements of Cash Flows

For the six months ended June 30, 2010 and 2009

(unaudited)

| | | 6/30/2010 | | | 6/30/2009 | |

| Cash flows from operating activities: | | | | | | |

| Net income | | $ | 2,471,267 | | | $ | 3,226,143 | |

| Adjustments to reconcile net income to net cash (used in) | | | | | | | | |

| provided by operating activities: | | | | | | | | |

| Share based compensation | | | 567,496 | | | | - | |

| Depreciation and amortization | | | 2,903,528 | | | | 2,056,335 | |

| Change in assets and liabilities: | | | | | | | | |

| Notes and trade receivables and customer deposits | | | (10,702,997 | ) | | | 5,588 | |

| Inventories | | | (2,278,322 | ) | | | (2,680,752 | ) |

| Prepayments and other current assets | | | (6,696,063 | ) | | | (1,906,714 | ) |

| Notes and accounts payable | | | 44,974,539 | | | | (9,370,881 | ) |

| Other payables and current liabilities | | | 9,584,616 | | | | (1,531,726 | ) |

| Net cash provided by (used in) operating activities | | | 40,824,064 | | | | (10,202,007 | ) |

| | | | | | | | | |

| Cash flows from investing activities: | | | | | | | | |

| Deposits in bank accounts as restricted cash | | | (12,366,494 | ) | | | - | |

| Purchase of long-term investment in equities | | | (4,294,720 | ) | | | (15,959 | ) |

| Acquisitions of property, plant and equipment | | | (15,767,602 | ) | | | (1,211,393 | ) |

| Deposits for capital expenditures | | | (9,484,822 | ) | | | (4,712,741 | ) |

| Net cash used in investing activities | | | (41,913,638 | ) | | | (5,940,093 | ) |

| | | | | | | | | |

| Cash flows from financing activities: | | | | | | | | |

| Owners’ capital contribution | | | 1,164,157 | | | | - | |

| Proceeds from borrowings from bank and others | | | 27,318,458 | | | | 76,009,842 | |

| Repayment of borrowings of bank and others | | | (25,750,759 | ) | | | (26,685,325 | ) |

| Repayment of capital lease obligation | | | (299,422 | ) | | | - | |

| Net cash provided by (used in) financing activities | | | 2,432,434 | | | | 49,324,517 | |

| | | | | | | | | |

| Net increase in cash | | | 1,342,860 | | | | 33,182,417 | |

| | | | | | | | | |

| Effect of exchange rate changes | | | (797,627 | ) | | | 130,004 | |

| | | | | | | | | |

| Cash at beginning of the period | | | 5,749,945 | | | | 26,873,633 | |

| | | | | | | | | |

| Cash at end of the period | | $ | 6,295,178 | | | $ | 60,186,054 | |

| | | | | | | | | |

| Supplemental disclosure of cash flow information: | | | | | | | | |

| Interest received | | $ | 501,406 | | | $ | 449,307 | |

| Interest paid | | | 2,633,454 | | | | 957,273 | |

| Income taxes paid | | | 2,855,836 | | | | 1,287,863 | |

The accompanying notes are an integral part of these consolidated financial statements

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

1. The Company and its Principal Business Activities

A. Organizational History

I. Ultimate Holding Company

a.) Birch Branch, Inc. (“BRBH”) was incorporated in the State of Colorado on September 29, 1989. BRBH was originally formed to pursue real estate development projects. Effective December 6, 2006, BRBH ceased pursuit of real estate development projects and any business operations. Unless the context requires or is otherwise indicated, the term the “Company” includes BRBH and the following entities, after giving effect to the Share Exchange (as defined herein):

II. Intermediary Holding Companies

a.) Shun Cheng Holdings HongKong Limited (“Shun Cheng HK”) is an investment holding company that was incorporated in Hong Kong on December 18, 2009.

Shun Cheng HK does not have any operations. Its sole purpose is to act as an intermediary holding company.

b.) On March 17, 2010, under the laws of the Henan Province, in the People’s Republic of China (“PRC”), Anyang Shuncheng Energy Technology Co., Ltd. (“Anyang WFOE”) was incorporated as a wholly-foreign owned entity. Anyang WFOE is wholly-owned by Shun Cheng HK.

Anyang WFOE does not conduct operations. All operations are conducted through the operating entities described below via a variable interest entity agreement detailed below.

III. Operating Entities

Pursuant to the VIE agreement described below, the Company's operations are conducted through the operating entities described below (the "operating entities") in the PRC:

a.) Henan Shuncheng Group Coal Coke Co., Ltd. (“SC Coke”) is a limited liability company organized in the PRC on August 27, 1997 as Anyang ShunCheng Washing Co., Ltd. In February 2005, the name was changed to Coal Coking Co., Ltd. In August 2007, the name was changed to the current name of Henan Shuncheng Group Coal Coke Co., Ltd. SC Coke has three shareholders: Wang Xinshun, Wang Xinming and Cheng Junsheng (collectively, the “SC Coke Shareholders”) owning 60%, 20% and 20% interests, respectively.

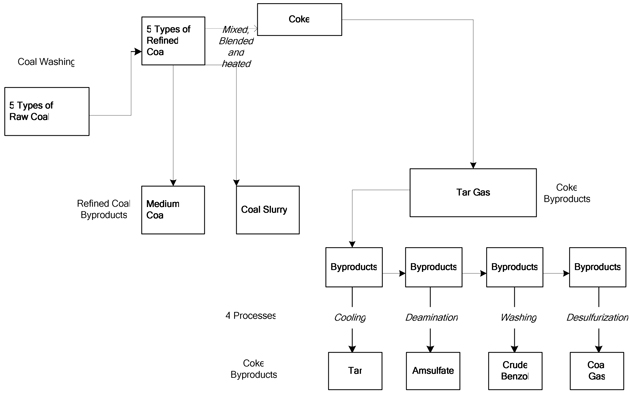

SC Coke is located in the Henan Province coal chemical industry cluster area in Anyang County, about 40 kilometers (approximately 25 miles) to the northwest of Anyang City. SC Coke is principally engaged in the processing of coal into coke, and related byproducts of cleaned coal, tar, crude benzene, and ammonium sulfate.

b.) Henan Shuncheng Group Longdu Trade Co., Ltd. (“Longdu”) is a limited liability company organized in the PRC on May 25, 2004. SC Coke holds an 86% interest in Longdu. The Company’s Chairman, Mr. Wang Xinshun, owns a 5% interest in Longdu.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

Longdu is principally engaged in coal-washing and the production of refined coal, medium coal and coal slurry. The majority of Longdu’s coal is sent to the Company for further processing, while the remainder is sold to outside customers.

The Company does not own any equity interest in the operating entities.

B. Variable Interest Entity Agreement

On March 19, 2010, Anyang WFOE entered into four contractual arrangements that for accounting purposes will be collectively known as the variable interest entity (“VIE”) agreement with the SC Coke Shareholders. The VIE agreement entitles Anyang WFOE to 100% of the future earnings and losses of both SC Coke, and its proportional 86% share of the earnings of Longdu. The Company filed with the Securities and Exchange Commission (“SEC”) a Current Report on Form 8-K on July 2, 2010 that included the documents comprising the VIE agreement as exhibits. The Company accounted for the VIE agreement, in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification™ (“ASC”) 810-10, by consolidating SC Coke and Longdu as subsidiaries of both Anyang WFOE and the Company because the Company: (1) has the authority to direct the operations of SC Coke and Longdu, (2) has the authority to provide financial support for SC Coke and Longdu, and (3) is primary beneficiary of the results of operations of SC Coke and Longdu. The significant terms of the VIE agreement are detailed for each of the contractual arrangements below:

I. Entrusted Management Agreement

Anyang WFOE has full and exclusive rights to manage SC Coke. These rights include, but are not limited to: appointment and dismissal of the members of the board of directors, hiring and termination of managerial and administrative personnel, and control over assets, which includes deployment and disposition thereof, and related cash flows generated by these assets.

Anyang WFOE is entitled to receive a quarterly management fee paid 45 days in arrears from the end of the quarter equivalent to SC Coke’s earnings before taxes for the quarter, subject to quarterly and annual adjustments.

Anyang WFOE is subject to operational risk and is obligated to settle debts on behalf of SC Coke, if SC Coke does not have sufficient funds to pays its debts itself.

II. Exclusive Option Agreement

Anyang WFOE, or parties designated by Anyang WFOE, has been granted the irrevocable right to purchase all or part of the ownership interest of SC Coke from the SC Coke Shareholders for the minimum possible price permissible by PRC law. The option is exercisable only to the extent that such purchase does not violate any PRC law then in effect. The purchase right is exclusively granted to Anyang WFOE and is not transferable without the express written consent of the SC Coke Shareholders.

The SC Coke Shareholders cannot dispose, assign or mortgage SC Coke assets or operations without the express written consent of Anyang WFOE.

Unless unanimously terminated by all parties, the Exclusive Option Agreement remains in effect for SC Coke, the SC Coke Shareholders, and Anyang WFOE and their successors.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

III. Shareholders’ Voting Proxy Agreement

The SC Coke Shareholders have irrevocably appointed the board of directors of Anyang WFOE as their proxy to vote on all matters that require the approval of the SC Coke Shareholders. These voting rights include, but are not limited to, the election of directors and the chairman of the board.

In the event that PRC regulations change (which regulations presently prohibit the transfer of SC Coke to Anyang WFOE), the SC Coke Shareholders may be exclusively permitted to transfer their ownership in SC Coke to Anyang WFOE; however, they are strictly prohibited from transferring their ownership in SC Coke to any other individuals or entities.

The SC Coke Shareholders have agreed to irrevocably and unconditionally indemnify the board of directors of Anyang WFOE from claims arising from the exercise of any of the powers conferred upon Anyang WFOE under the agreement.

IV. Shares Pledge Agreement

The SC Coke Shareholders have pledged all of their ownership interests in SC Coke, including rights to PRC registered capital and dividends related to ownership in SC Coke, to guarantee their obligations under the Entrusted Management Agreement, the Exclusive Option Agreement and the Shareholders’ Voting Proxy Agreement.

C. Share Exchange Agreement

On June 28, 2010, BRBH closed a share exchange transaction (the “Share Exchange”) in which BRBH issued 30,233,750 common shares to the former shareholders of Shun Cheng HK in exchange for all of the issued and outstanding shares of Shun Cheng HK. In connection with the Share Exchange, certain shareholders of BRBH agreed to cancel 435,123 common shares and BRBH issued 540,472 common shares to financial consultants. Immediately prior to the closing of the Share Exchange there were 1,708,123 common shares outstanding. Upon completion of the Share Exchange and transactions contemplated by the Share Exchange agreement, there were 32,047,222 common shares outstanding. Immediately following the closing of the Share Exchange, the former shareholders of Shun Cheng HK and the original shareholders of BRBH own approximately 95% and approximately 5% of BRBH’s issued and outstanding common shares, respectively.

The Share Exchange has been accounted for as a recapitalization of Shun Cheng HK in which BRBH (the legal acquirer) is considered the accounting acquiree and Shun Cheng HK (the legal acquiree) is considered the accounting acquirer. As a result of the Share Exchange, BRBH is deemed to be a continuation of the business of Shun Cheng HK. Accordingly, the financial data included in the accompanying consolidated financial statements for all periods prior to June 28, 2010 is that of the accounting acquirer Shun Cheng HK. The historical stockholders’ equity of the accounting acquirer prior to the Share Exchange has been retroactively restated as if the Share Exchange occurred as of the beginning of the first period presented.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

2. Summary of Significant Accounting Policies

A. Financial Statement Presentation

The financial statements are prepared in accordance with the accounting principles generally accepted in the United States of America (“US GAAP”). The consolidated financial statements include the accounts of BRBH, Shun Cheng HK, Anyang WFOE, SC Coke, and Longdu. All intercompany transactions, such as sales, cost of sales, and balances due to/due from, investment in subsidiaries, and the operating entities and the capitalization thereof have been eliminated.

The Company regrouped certain accounts in the December 31, 2009 consolidated balance sheet to improve comparability with June 30, 2010 balance sheet line items. There was no impact on earnings as a result of the regrouping.

B. Non-Controlling Interest

14% of the registered capital of Longdu is owned by parties other than SC Coke. The Company’s Chairman, Mr. Wang Xinshun, owns a 5% interest in Longdu, while other investors own the remaining 9% interest. Mr. Wang’s and the other investors’ share of capital, retained earnings, and income are separately disclosed on the Company’s balance sheet and statement of operations.

C. Use of Estimates

The preparation of consolidated financial statements in conformity with US GAAP requires the Company to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, and expenses and the related disclosure of contingent assets and liabilities. Significant estimates and assumptions are used for, but not limited to: (1) allowance for trade receivables, (2) economic lives of property, plant and equipment, (3) asset impairments, and (4) contingency reserves. The Company bases its estimates on historical experience and on various other assumptions that the Company believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates. In addition, any change in these estimates or their related assumptions could have an adverse effect on the Company’s operating results.

D. Cash

Cash consists primarily of cash on hand or cash deposits in banks that are available for withdrawal without restriction.

E. Restricted Cash

Restricted cash represents cash that is held by banks as collateral for bank notes payable. The banks have collateral requirements ranging from 50% to 100% of the outstanding bank notes.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

F. Bank Notes Receivable

Bank notes receivable are highly liquid negotiable instruments issued by banks in the PRC on behalf of SC Coke’s customers, which are collateralized by deposits made by such customers at the subject banks. These notes typically have maturities between one to six months. SC Coke can: (a) redeem the notes for face value at maturity, (b) endorse the notes to SC Coke’s vendors as a form of payment instrument, or (c) factor the notes to a bank. In the event that SC Coke factors these notes to a bank, it will record as interest expense the difference between cash received and the face value of the note.

G. Trade Receivables

Trade receivables are reported at net realizable value. SC Coke has established an allowance for doubtful accounts based upon factors pertaining to the credit risks of specific customers, historical trends, age of the receivable and other information. Delinquent accounts are written off when it is determined that the amounts are uncollectible.

H. Inventories

Inventories are stated at the lower of cost or market. Cost is determined on a standard cost basis, which approximates actual cost on a first-in, first-out (“FIFO”) method. Lower of cost or market is evaluated by considering obsolescence, excessive levels of inventory, deterioration, and other factors. Adjustments to reduce the cost of inventory to its net realizable value, if required, are made for estimated excess or obsolescence and are charged to cost of revenues. Currently, SC Coke does not allocate costs to the byproducts. However, due to rapid inventory turnover, differences to the financial statements are considered immaterial.

I. Plant and Equipment

Plant and equipment are stated at cost less accumulated depreciation. Depreciation is computed using the straight-line method over the estimated useful lives of the related assets as follows:

| Machinery and equipment | | 10 years |

| Building and improvements | | 20 years |

| Company vehicles | | 5 years |

| Furniture and office equipment | | 5 years |

| Miscellaneous | | 5 years |

Repairs and maintenance costs are expensed as incurred. Gains or losses on disposals are included in cost of revenues.

SC Coke capitalizes interest attributable to capital construction projects in accordance with ASC subtopic 835-20, Capitalization of Interest, which requires interest to be capitalized for assets that are constructed or otherwise produced for an entity’s own use, including assets constructed or produced for the entity by others for which deposits or progress payments have been made.

Construction in progress represents direct costs of construction or acquisition and design fees incurred. Capitalization of these costs ceases and the construction in progress is transferred to plant and equipment when substantially all the activities necessary to prepare the assets for their intended use are completed. No depreciation is recorded on construction in progress until construction has been completed and the related asset is ready for intended use and has been transferred to plant and equipment.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

J. Long-Term Investments

Long-term investments represent investments that SC Coke has in private companies within China other than Longdu. SC Coke does not hold any interest greater than 20% and it has determined that it did not have significant control or influence over any of the private companies in which it has investment holdings. As a result of the investments being private companies, there is a lack of readily determinable market value for these investments; as such, SC Coke recorded these investments at cost.

K. Impairment of Long-Lived Assets

The Company has adopted Statement of Financial Accounting Standards No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets”, ASC 360-10-35. The Company evaluates its long lived assets for impairment when indicators of impairment are present or annually, whichever occurs sooner. In the event that there are indications of impairment, the Company will record a loss to the statement of operations equal to the difference between the carrying value and the fair value of the long lived asset. The Company typically, but not exclusively, employs the expected future discounted cash flows method to determine fair value of long lived assets subject to impairment. The fair value of long lived assets that are held for disposition will include the cost of disposal.

SC Coke’s long-lived assets are grouped by their presentation on the consolidated balance sheets, and further segregated by their operating and asset type. Long-lived assets subject to impairment include buildings, equipment, vehicles, software licenses, and land-use-rights. The Company makes its determinations based on various factors that impact those assets.

At June 30, 2010 and 2009, SC Coke assessed its buildings, equipment, vehicles, software licenses, and land-use-rights for production and has concluded its long-lived assets have not experienced any impairment losses because SC Coke’s long lived assets have enabled SC Coke to experience significant profit growth during the six months ended June 30, 2010 and 2009.

L. Fair Value of Financial Instruments

The Company has adopted ASC 820-10, Fair Value Measurements and Disclosures, which defines fair value, establishes a framework for using fair value to measure assets and liabilities, and expands disclosures about fair value measurements. ASC 820-10 applies whenever other statements require or permit assets or liabilities to be measured at fair value.

ASC 820-10 includes a fair value hierarchy that is intended to increase the consistency and comparability in fair value measurements and related disclosures. The fair value hierarchy is based on inputs to valuation techniques that are used to measure fair value that are either observable or unobservable. Observable inputs reflect assumptions market participants would use in pricing an asset or liability based on market data obtained from independent sources while unobservable inputs reflect a reporting entity’s pricing an asset or liability based upon their own market assumptions. The fair value hierarchy consists of the following three levels:

Level 1–inputs are unadjusted quoted prices in active markets for identical assets or liabilities that the Company has the ability to access at the measurement date.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

Level 2–observable inputs other than level 1 prices, such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities.

Level 3–instrument valuations are obtained without observable market values and require a high-level of judgment to determine the fair value.

SC Coke’s financial instruments consist mainly of cash, restricted cash, bank notes receivable, and debt obligations. Bank notes receivable are reflected in the accompanying financial statements at historical cost, which approximates fair value due to the short-term nature of these instruments. Based on the borrowing rates currently available to the Company for loans with similar terms and average maturities, the fair value of debt obligations also approximates its carrying value due to the short-term nature of the instruments. While the Company believes its valuation methodologies are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of certain financial instruments could result in a different estimate of fair value at the reporting date.

The following table presents SC Coke’s financial assets and liabilities in accordance with the hierarchy set forth in ASC 820-10:

| | | June 30, 2010 | |

| | | Quoted | | | | | | | | | | |

| | | in Active | | | Significant | | | | | | | |

| | | Markets | | | Other | | | Significant | | | | |

| | | for Identical | | | Observable | | | Unobservable | | | | |

| | | Assets | | | Inputs | | | Inputs | | | | |

| | | (Level 1) | | | (Level 2) | | | (Level 3) | | | Total | |

| | | | | | | | | | | | | |

| Financial assets: | | | | | | | | | | | | |

| Cash | | | 6,295,178 | | | | - | | | | - | | | | 6,295,178 | |

| Restricted cash | | | 64,771,024 | | | | - | | | | - | | | | 64,771,024 | |

| Bank notes receivable | | | - | | | | 7,408,689 | | | | - | | | | 7,408,689 | |

| | | | | | | | | | | | | | | | | |

| Total financial assets | | | 71,066,202 | | | | 7,408,689 | | | | - | | | | 78,474,891 | |

| | | | | | | | | | | | | | | | | |

| Financial liabilities: | | | | | | | | | | | | | | | | |

| Bank notes payable | | | - | | | | 79,458,332 | | | | - | | | | 79,458,332 | |

| | | | | | | | | | | | | | | | | |

| Total financial liabilities | | | - | | | | 79,458,332 | | | | - | | | | 79,458,332 | |

In January 2008, the Company adopted ASC 825-10, Fair Value Option for Financial Assets and Financial Liabilities, and has elected not to measure any of SC Coke’s current eligible financial assets or liabilities at fair value. ASC 825-10 was issued to allow entities to voluntarily choose to measure certain financial assets and liabilities at fair value (fair value option). The fair value option may be elected on an instrument-by-instrument basis and is irrevocable, unless a new election date occurs. If the fair value option is elected for an instrument, ASC 825-10 specifies that unrealized gains and losses for that instrument shall be reported in earnings at each subsequent reporting date. ASC 825-10 became effective January 1, 2008. The Company did not elect the fair value option for its financial assets and liabilities existing on January 1, 2008, and did not elect the fair value option for any financial assets or liabilities transacted during the six months ended June 30, 2010.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

M. Statutory Reserve

In accordance with PRC laws, statutory reserve refers to the appropriation from net income, to the account “statutory reserve,” to be used for future company development, recovery of losses, and increase of capital, as approved, to expand production or operations. PRC laws prescribe that an enterprise operating at a profit must appropriate, on an annual basis, an amount equal to 10% of its profit. Such an appropriation is necessary until the reserve reaches a maximum that is equal to 50% of the enterprise’s PRC registered capital. SC Coke cannot pay dividends out of statutory reserves or paid in capital registered in PRC.

N. Foreign Currency Translation

The accompanying consolidated financial statements are presented in U.S. Dollars. The functional currency of the Company’s subsidiaries and the operating entities described herein is the RMB, the official currency of the PRC. Capital accounts of the consolidated financial statements are translated into U.S. Dollars from RMB at their historical exchange rates when the capital transactions occurred. Assets and liabilities are translated at the exchange rates as of the balance sheet date. Income and expenditures are translated at the average exchange rates for the six months ended June 30, 2010 and 2009. Currency translation adjustment results from translation to U.S. Dollar for financial reporting purposes are recorded in other comprehensive income as a component of owners’ equity. A summary of the conversion rates for the periods presented is as follows:

| | 6/30/2010 | | 12/31/2009 |

| Period/year end RMB: U.S. Dollar exchange rate | 6.8086 | | 6.8372 |

| Average RMB: U.S. Dollar exchange rate | 6.8348 | | 6.8408 |

RMB is not freely convertible into foreign currency and all foreign exchange transactions must take place through authorized institutions. No representation is made that the RMB amounts could have been, or could be, converted into U.S. Dollars at the rates used in translation.

O. Comprehensive Income

The Company accounts for comprehensive income in accordance with the provisions of ASC topic 220, Comprehensive Income, which establishes standards for reporting comprehensive income or loss and its components in the financial statements. The accumulated other comprehensive income represents foreign currency translation adjustments.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

P. Revenue Recognition

In accordance with ASC 605-10, SC Coke recognizes revenue upon receipt of an acceptance of goods document issued by its customers. Each customer enters into an annual master sales agreement with SC Coke which will indicate a total volume for the year, and an acceptable range of prices, given market fluctuations on a short term basis, for SC Coke’s coke and coal byproducts. Final determination of the price for coke is determined on individual purchase orders which lie in the aforementioned price range. SC Coke’s coke and coal byproducts are fully usable at the point of shipment. From a revenue recognition perspective, the Company believes that collectibility of the revenue is reasonably assured at the time that customers acknowledge receipt and accept SC Coke’s product. SC Coke has not experienced any material return of products, and as such, it has not prepared allowances for returns.

Customer payments received prior to completion of the above criteria are recorded as a liability on the Company’s balance sheet as unearned revenue.

Q. Shipping and Handling Costs

Shipping and handling costs billed to customers are recorded net of the amount collected. Shipping and handling expenses are included in sales and marketing expenses.

R. Advertising

Advertising and promotion costs are expensed as they are incurred; such costs were immaterial for 2010 and 2009 and are included in sales and marketing expenses.

S. Income Taxes

The Company has implemented ASC 740, Accounting for Income Taxes. Income tax liabilities computed according to the United States and PRC tax laws are provided for the tax effects of transactions reported in the financial statements and consist of taxes currently due plus deferred taxes related primarily to differences between the basis of fixed assets and intangible assets for financial and tax reporting. The deferred tax assets and liabilities represent the future tax consequences of those differences, which will be either taxable or deductible when the assets and liabilities are recovered or settled. Deferred taxes also are recognized for operating losses that are available to offset future income taxes. A valuation allowance is created to evaluate deferred tax assets if it is more likely than not that these items will either expire before the Company is able to realize the associated tax benefit, or that future realization is uncertain. The Company assesses its future tax assets and liabilities for any uncertainty on an annual basis. Upon completion of its annual review of its tax position for the years ended December 31, 2009 and 2008, the Company concluded that there was no uncertainty regarding its tax position. Any changes in the Company’s position on a going forward basis will be charged to tax expense or deferred tax benefit in its statement of operations.

T. Recent Accounting Pronouncements

In June 2009, FASB issued ASC 860, Transfers and Servicing, and ASC 810, Consolidation, a revision to FASB Interpretation No. 46 (Revised December 2003), Consolidation of Variable Interest Entities (FASB ASC 810 Consolidation). The Company has adopted the new accounting policies and has determined that there is no material impact to the financial statements presented herein.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

On June 30, 2009, FASB issued ASC 105, Accounting Standards Codification (FASB ASC 105 Generally Accepted Accounting Principles) a replacement of FASB Statement No. 162 the Hierarchy of Generally Accepted Accounting Principles. On the effective date of this standard, ASC became the source of authoritative U.S. accounting and reporting standards for nongovernmental entities, in addition to guidance issued by the SEC. This statement is effective for financial statements issued for interim and annual periods ending after September 15, 2009. If an accounting change results from the application of this guidance, an entity should disclose the nature and reason for the change in accounting principle in their financial statements. This new standard categorizes the US GAAP hierarchy to two levels: one that is authoritative (in ASC) and one that is non-authoritative (not in ASC). Exceptions include all rules and interpretive releases of the SEC under the authority of federal securities laws, which are sources of authoritative US GAAP for SEC registrants, and certain grandfathered guidance having an effective date before March 15, 1992. Statement No. 168 is the final standard that will be issued by FASB in that form. There will no longer be, for example, accounting standards in the form of statements, staff positions, Emerging Issues Task Force (“EITF”) abstracts, or AICPA Accounting Statements of Position. The Company has adopted and implemented the new accounting policy.

3. Trade Receivables

SC Coke’s trade receivables as of June 30, 2010 and December 31, 2009, as well as the activity in SC Coke’s allowance for bad debts for the six months ended June 30, 2010 and the year ended December 31, 2009 are set forth below:

| | | 6/30/2010 | | | 12/31/2009 | |

| Trade Receivables | | $ | 28,871,849 | | | $ | 14,960,708 | |

Less: Allowance for Bad Debt | | | 3,633,827 | | | | 3,618,626 | |

| Trade Receivables, net | | $ | 25,238,022 | | | $ | 11,342,082 | |

| | | | | | | | | |

| Allowance for Bad Debts | | | | | | | | |

| Beginning Balance | | $ | 3,618,626 | | | $ | 317,787 | |

| Provision for bad debts | | | 15,201 | | | | 3,300,839 | |

Less: Bad Debt Written Off | | | - | | | | - | |

| Ending Balance | | $ | 3,633,827 | | | $ | 3,618,626 | |

4. Inventories

The components of SC Coke’s inventories as of June 30, 2010 and December 31, 2009 are as follows:

| | | 6/30/2010 | | | 12/31/2009 | |

| Raw materials | | $ | 3,543,864 | | | $ | 6,580,843 | |

| Work in process and semi-finished goods | | | 24,504,501 | | | | 22,118,983 | |

| Finished goods | | | 6,656,277 | | | | 3,726,494 | |

| Total inventories | | $ | 34,704,642 | | | $ | 32,426,320 | |

5. Advances to Suppliers and Prepayments

The components of SC Coke’s advances to suppliers and prepayments as of June 30, 2010 and December 31, 2009 are as follows:

| | | 6/30/2010 | | | 12/31/2009 | |

| Construction projects prepayments | | $ | - | | | $ | 14,957,919 | |

| Prepayments for raw materials in operations | | | 55,838,629 | | | | 52,839,477 | |

| Prepaid expenses | | | 1,357,342 | | | | | |

| Prepaid taxes | | | 2,855,836 | | | | - | |

| | | $ | 60,051,807 | | | $ | 67,797,396 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

| 6. | Plant and Equipment, net |

The components of SC Coke’s plant and equipment are as follows:

| | | 6/30/2010 | |

| | | | | | Accumulated | | | | |

| | | At Cost | | | Depreciation | | | Net | |

| Buildings and plant | | $ | 21,041,719 | | | $ | 2,120,941 | | | $ | 18,920,778 | |

| Machinery and equipment | | | 35,204,488 | | | | 11,658,570 | | | | 23,545,918 | |

| Electronic equipment | | | 599,205 | | | | 199,206 | | | | 399,999 | |

| Vehicles | | | 2,461,911 | | | | 1,408,955 | | | | 1,052,956 | |

| Others | | | 697,849 | | | | 258,840 | | | | 439,009 | |

| Construction in progress | | | 33,891,504 | | | | - | | | | 33,891,504 | |

| Total plant and equipment | | $ | 93,896,676 | | | $ | 15,646,512 | | | $ | 78,250,164 | |

| | | 12/31/2009 | |

| | | | | | Accumulated | | | | |

| | | At Cost | | | Depreciation | | | Net | |

| Buildings and plant | | $ | 21,160,158 | | | $ | 1,211,661 | | | $ | 19,948,497 | |

| Machinery and equipment | | | 34,645,669 | | | | 9,967,947 | | | | 24,677,722 | |

| Electronic equipment | | | 429,188 | | | | 161,650 | | | | 267,538 | |

| Vehicles | | | 2,411,955 | | | | 1,209,313 | | | | 1,202,642 | |

| Others | | | 675,178 | | | | 192,411 | | | | 482,767 | |

| Construction in progress | | | 18,806,924 | | | | - | | | | 18,806,924 | |

| Total plant and equipment | | $ | 78,129,072 | | | $ | 12,742,982 | | | $ | 65,386,090 | |

Depreciation expense related to plant and equipment was $2,903,528 and $4,140,370 for the six months and twelve months ended June 30, 2010 and December 31, 2009, respectively.

The construction in progress sub-account is detailed below:

| Description | | 6/30/2010 | | | 12/31/2009 | |

| Coking furnace | | $ | 7,160,377 | | | $ | 151,665 | |

| Office buildings | | | 4,479,864 | | | | 2,438,888 | |

| Plant and facilities | | | 13,585,207 | | | | 11,687,086 | |

| Sewage system | | | 559,007 | | | | 511,223 | |

| Equipment peripherals | | | 8,107,049 | | | | 4,018,061 | |

| | | $ | 33,891,504 | | | $ | 18,806,924 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

The following tabulation presents SC Coke’s investment in noncontrolled entities, which are not included in the consolidation.

| Investment | | Ownership | | Type | | 6/30/2010 | |

| Anyang Rural Credit Cooperative - Tongye Branch | | | 11.26 | % | Equity | | $ | 4,315,543 | |

| Anyang Urban Credit Cooperative - Meiyuanzhuan Branch | | | 11.26 | % | Equity | | | 5,989,337 | |

| | | | | | | | | | |

| Ansteel Group Metallurgy Stove Co., Ltd. | | | 19 | % | Equity | | | 2,288,282 | |

| | | | | | | | | | |

| Anyang Xinlong Coal Industry Co., Ltd. - Hongling Branch | | | 16 | % | Equity | | | 7,092,207 | |

| | | | | | | | $ | 19,715,369 | |

The following table provides the name of the financial institution, due date, and amounts outstanding at June 30, 2010 for SC Coke’s bank notes payable.

| Financial Institution | | Due Date | | 6/30/2010 | |

| China Citic Bank | | 12/01/2011 | | $ | 5,874,923 | |

| China Citic Bank | | 10/15/2010 | | | 2,937,461 | |

| China Citic Bank | | 07/12/2010 | | | 2,937,461 | |

| China Citic Bank | | 07/13/2010 | | | 558,118 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | 09/10/2010 | | | 5,874,923 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | 12/29/2010 | | | 4,406,192 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | 12/29/2010 | | | 5,140,558 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | 10/08/2010 | | | 1,468,731 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | 10/08/2010 | | | 1,468,731 | |

| Agricultural Bank of China - Anyang Branch | | 09/17/2010 | | | 2,937,461 | |

| Guangdong Development Bank - Anyang Branch | | 12/09/2010 | | | 5,581,177 | |

| Guangdong Development Bank - Anyang Branch | | 12/10/2010 | | | 4,993,684 | |

| Guangdong Development Bank - Anyang Branch | | 08/08/2010 | | | 734,365 | |

| Henan Rural Credit Cooperative - Tongye Branch | | 09/23/2010 | | | 7,343,654 | |

| Henan Rural Credit Cooperative - Tongye Branch | | 09/25/2010 | | | 7,343,654 | |

| China Commercial Bank - Anyang Branch | | 08/02/2010 | | | 3,965,573 | |

| China Commercial Bank - Anyang Branch | | 08/02/2010 | | | 440,619 | |

| Bank of Luoyang | | 08/04/2010 | | | 5,874,923 | |

| The Industrial and Commercial Bank of China - Shuiye Branch | | 09/29/2010 | | | 763,740 | |

| The Industrial and Commercial Bank of China - Shuiye Branch | | 10/26/2010 | | | 1,468,731 | |

| China Everbright Bank | | 12/22/2010 | | | 2,937,461 | |

| China Everbright Bank | | 12/23/2010 | | | 4,406,192 | |

| | | | | $ | 79,458,332 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

The bank notes payable do not carry a stated interest rate, but do carry a specific due date. These notes are negotiable documents issued by financial institutions on SC Coke’s behalf to vendors. These notes can either be endorsed by the vendor to other third parties as payment, or prior to coming due, they can factor these notes to other financial institutions. These notes are short term in nature and, as such, SC Coke does not calculate imputed interest with respect to them. These notes are collateralized by SC Coke’s deposits as described in Note 2E - Restricted Cash.

The components of SC Coke’s loans payable are as follows:

| Name of Creditors | | Note | | Due Date | | Interest Rate | | | 6/30/2010 | |

| Henan Rural Credit Cooperatives - Anyang Branch | | A | | 03/22/2011 | | | 8.8500 | % | | $ | 4,406,193 | |

| Shanghai Pudong Development Bank - Zhengzhou Branch | | B | | 12/24/2010 | | | 5.3460 | % | | | 5,874,923 | |

| Bank of China - Anyang Hejiacun Branch | | C | | 07/01/2010 | | | 5.8410 | % | | | 2,937,461 | |

| Industrial and Commercial Bank of China - Shuiye Branch | | D | | 10/14/2010 | | | 5.3460 | % | | | 5,287,431 | |

| Guangdong Development Bank - Anyang Branch | | E | | 07/22/2010 | | | 5.3100 | % | | | 1,468,731 | |

| Guangdong Development Bank - Anyang Branch | | F | | 08/31/2010 | | | 5.3100 | % | | | 2,937,461 | |

| Guangdong Development Bank - Anyang Branch | | G | | 01/18/2011 | | | 5.3100 | % | | | 2,937,461 | |

| Guangdong Development Bank - Anyang Branch | | H | | 06/07/2011 | | | 5.3100 | % | | | 1,468,731 | |

| Henan Urban Credit Cooperative - Anyang Branch | | I | | 04/13/2011 | | | 6.6375 | % | | | 2,937,461 | |

| Bank of Luoyang - Zhengzhou Branch | | J | | 01/27/2011 | | | 5.3100 | % | | | 2,937,461 | |

| | | | | | | | | | | $ | 33,193,314 | |

SC Coke has collateralized its debt obligations above. Refer to notes below for collateral corresponding to each obligation.

| | A. | Guaranteed by Linzhou City Hongqiqu Electrical Carbon Co., Ltd and Henan Hubo Cement Co., Ltd |

| | B. | Guaranteed by Anyang City New Tianhe Cement Co., LLC |

| | C. | Guaranteed by Xinlei Group Cheng Chen Coking |

| | D. | Guaranteed by Anyang Top Coal Co., Ltd. |

| | E. | Guaranteed by Henan Hubo Cement Co., Ltd and Anyang Liyuan Coking Co., Ltd |

| | F. | Guaranteed by Henan Hubo Cement Co., Ltd and Xinlei Group Cheng Chen Coking |

| | G. | Guaranteed by Henan Hubo Cement Co., Ltd and Liyuan Coking Co., Ltd |

| | H. | Guaranteed by Henan Hubo Cement Co., Ltd and Anyang Liyuan Coking Co., Ltd |

| | I. | Guaranteed by Xinpu Steel Co., Ltd |

| | J. | Guaranteed by Anyang Liyuan Coking Co., Ltd |

Other payable at June 30, 2010 and December 31, 2009 is detailed in the table below.

| | | 6/30/2010 | | | 12/31/2009 | |

| Project safety deposit | | $ | 209,827 | | | $ | 167,836 | |

| Unbilled purchase payable | | | 13,981,726 | | | | 3,785,000 | |

| Payable for raw materials in operation | | | 1,611,347 | | | | 566,602 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

| | | 6/30/2010 | | | 12/31/2009 | |

| Non-collateralized, non-interest bearing loans from individuals payable on demand | | | 2,173,933 | | | | 5,159,865 | |

| Others | | | 120,941 | | | | 574,969 | |

| | | $ | 18,097,774 | | | $ | 10,254,272 | |

| 11. | Notes Payable to Related Parties |

| Creditor | | Note | | | 6/30/2010 | |

| Chairman, Wang Xinshun | | A | | | $ | 35,789,956 | |

| SC Coke Shareholders | | B | | | | 35,518,532 | |

| | | | | | $ | 71,308,488 | |

| | A. | Note Payable to Wang Xinshun |

On May 23, 2010, SC Coke entered into a formal loan agreement with the Company’s Chairman, Mr. Wang Xinshun, for amounts owed to him in the amount of approximately $35.6 million at December 31, 2009. The significant terms of the loan are: (a) 12 year term, beginning as of December 31, 2009 to December 31, 2021, (b) 3% fixed simple annual interest, (c) SC Coke has the option, but not the obligation, to pay interest for the first two years, (d) after the first two years, the balance of the loan will be amortized over the remaining 10 years of the term and SC Coke is required to make monthly interest and principal payments, and (e) Mr. Wang Xinshun is prohibited from declaring default against SC Coke.

The Company has neither accrued nor paid any interest for the note payable to Mr. Wang Xinshun during the six months ended June 30, 2010. The outstanding balance owed to Mr. Wang Xinshun for financial reporting purposes has increased slightly as result of a change in the foreign currency exchange rate.

| | B. | Note Payable to SC Coke Shareholders |

On March 31, 2010, the SC Coke Shareholders, and Anyang Xinlong Coal (Group) Hongling Coal Co., Ltd., Anyang Huichang Coal Washing Co., Ltd. and Anyang Jindu Coal Co., Ltd (collectively, the “third party lenders”) formalized the terms for approximately $35.5 million of loans previously extended to SC Coke by the three lenders.

On June 21, 2010, the SC Coke Shareholders entered into an agreement with the third party lenders to assume the obligations of the third party lenders, and concurrently the third party lenders released SC Coke from any liability.

Also, on June 21, 2010, SC Coke and the SC Coke Shareholders entered into a debt agreement for the original principal amount of the loans due to the third party lenders (approximately $35.5 million), the significant terms of which are: (a) 15 year term, commencing on June 21, 2010, (b) 2% fixed simple annual interest, (c) SC Coke has the option, but not the obligation, to pay interest when accrued, and (d) the SC Coke Shareholders do not have the ability to declare a default.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

SC Coke is currently the beneficiary of two government grants that are generally intended to be used towards capital technology improvement with the end goal of increased production and energy efficiency. The grants were awarded during 2008 and 2009, respectively. These grants have been recorded as forgivable loans in the liability section of the balance sheet. SC Coke has received payment of the grants, but has not yet met all the criteria set forth under the grant. Upon receiving government approval of fulfilling all of the criteria set forth under the grant, SC Coke will credit the balance to other income on the consolidated statement of operations. SC Coke will also appropriate that same amount from retained earnings to statutory reserves indicating that the assets associated with these grants are not available for dividend distribution.

| 13. | Related Party Transactions |

SC Coke has specified the following transactions with related parties with ending balances as of June 30, 2010 and December 31, 2009:

| | A. | Trade Receivables and Revenue |

Angang Steel Group Metallurgy Furnace Co., Ltd (Angang), in which SC Coke owns a 19% stake, is one of the customers of SC Coke.

There is an ending balance in accounts receivable from Angang of approximately $36,278 and $906,000 as of June 30, 2010 and December 31, 2009, respectively.

Revenue recorded in the consolidated financial statements from Angang amounts to approximately $2,766,000 and $1,841,000 for the six months ended June 30, 2010 and 2009, respectively.

| | B. | Deposits and Cost of Revenues |

The Chairman and majority owner, Mr. Wang Xinshun, owns a 43.86% interest in Anyang Bailianpo Coal Co., Ltd. (Bailianpo) which provides raw coal to SC Coke.

SC Coke had outstanding prepayments with Bailianpo of approximately $0 and $7,102,000 as of June 30, 2010 and December 31, 2009, respectively. Cost of revenues related to purchases from Bailianpo included in the consolidated financial statements amounts to approximately $8,142,000 and $1,104,000 for the six months ended June 30, 2010 and 2009, respectively.

SC Coke holds a 16% interest in Anyang Xinlong Coal (Group) Hongling Coal Co., Ltd. (Anyang Xinlong), which is a coal mine located in Anyang County providing SC Coke with a substantial portion of its coking coal requirements.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

SC Coke did not have any prepayments with Anyang Xinlong outstanding at June 30, 2010 and December 31, 2009, respectively. Cost of revenues related to purchases from Anyang Xinlong included in the consolidated financial statements amounts to approximately $4,192,000, and $3,488,000 for the six months ended June 30, 2010 and 2009, respectively.

The Company, its subsidiaries and the operating entities are subject to income tax under the jurisdictions where they operate. The following table details the Company, its subsidiaries and the operating entities, and the statutory tax rates to which they are subject:

| Entity | | Country of Domicile | | Income Tax Rate | |

| Birch Branch, Inc. | | USA | | 15.00% - 35.00% | |

| Shuncheng Holdings HongKong Ltd. | | BVI | | 0.00% | |

| Anyang Shuncheng Energy Technology Co., Ltd. | | PRC | | 25.00% | |

| Henan Shuncheng Group Coal Coke Co., Ltd. | | PRC | | 25.00% | |

| Henan Shuncheng Group Longdu Trade Co., Ltd. | | PRC | | 25.00% | |

Although the Company is subject to United States income taxes, it is a holding company with no operations or profits within the U.S. borders. The Company currently only incurs expenses in the United States that are associated with being a public company.

Income (loss) before taxes and provision for taxes consisted of the following for the six months ended June 30, 2010 and 2009, respectively:

| | | 6/30/2010 | | | 6/30/2009 | |

| Income (loss) before tax: | | | | | | |

| USA | | $ | (656,581 | ) | | $ | - | |

| BVI | | | (326 | ) | | | - | |

| PRC | | | 4,147,965 | | | | 4,427,479 | |

| Total | | $ | 3,491,058 | | | $ | 4,427,479 | |

| | | | | | | | | |

| Provision for income taxes: | | | | | | | | |

| US Federal | | $ | - | | | $ | - | |

| State | | | - | | | | - | |

| PRC | | | 1,019,791 | | | | 1,201,336 | |

| Total provision for taxes | | $ | 1,019,791 | | | $ | 1,201,336 | |

| | | | | | | | | |

| Effective tax rate | | | 29.22 | % | | | 27.13 | % |

The differences between the U.S. federal statutory income tax rates and the Company’s effective tax rate for the six months ended June 30, 2010 and 2009 are shown in the following table:

| | | 6/30/2010 | | | 6/30/2009 | |

| US statutory tax rate | | | 34.00 | % | | | 34.00 | % |

| Lower rates in the PRC | | | -9.00 | % | | | -9.00 | % |

| Tax holiday | | | - | % | | | - | % |

| Accrual and reconciling items | | | 4.22 | % | | | 2.13 | % |

| Effective tax rate | | | 29.22 | % | | | 27.13 | % |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

| 15. | Commitments and Contingencies |

Third Party Guarantees

SC Coke entered into agreements as a guarantor of debt for twelve companies (the “guarantees”) in the amount of approximately $46.0 million at June 30, 2010. Of the aforementioned guarantees, six of the twelve companies have, in turn, guaranteed debts of approximately $27.9 million on behalf of SC Coke at June 30, 2010. SC Coke has not historically incurred any losses due to such debt guarantees. Additionally, the Company has determined that the fair value of the guarantees is immaterial. For more details of the outstanding guarantees, see the table below:

| | | | | Guarantee | | | |

| Guarantee | | Creditor | | End | | 6/30/2010 | |

| Anshan Minshan Metal Co., Ltd. | | Avic International | | 03/31/2012 | | $ | 3,671,827 | |

| Anyang City New Tianhe Cement Co., Ltd | | Guangdong Development Bank - Anyang Branch | | 07/07/2011 | | | 5,874,923 | |

| Anyang Hengxiang Coal Co., Ltd. | | Agricultural Bank of China - Anyang Branch | | 04/13/2012 | | | 660,929 | |

| Anyang Public Transportation Department | | China Commercial Bank - Anyang Branch | | 11/25/2010 | | | 2,937,461 | |

| Anyang Xingya Xidi Product Co., Ltd. | | Guangdong Development Bank - Anyang Branch | | 07/22/2011 | | | 2,937,461 | |

| Anyang Yujin Ash Co., Ltd. | | China Construction Bank | | 01/05/2012 | | | 1,468,731 | |

| Anyang Yulong Coking Co., Ltd. | | Henan Rural Credit Cooperative - Tongye Branch | | 04/23/2011 | | | 2,937,461 | |

| Henan Hubo Cement Co., Ltd. | | Bank of China - Anyang Branch | | 11/11/2011 | | | 2,937,461 | |

| Henan Hubo Cement Co., Ltd. | | Bank of China - Anyang Branch | | 05/19/2012 | | | 1,468,731 | |

| Henan Hubo Cement Co., Ltd. | | Guangdong Development Bank - Anyang Branch | | 07/06/2011 | | | 1,615,604 | |

| Henan Hubo Cement Co., Ltd. | | Guangdong Development Bank - Anyang Branch | | 07/06/2011 | | | 1,909,350 | |

| Linzhou City Hongqiqu Electrical Carbon Co., Ltd | | Agricultural Bank of China - Linzhou Branch | | 12/15/2011 | | | 1,468,731 | |

| Linzhou City Hongqiqu Electrical Carbon Co., Ltd | | Agricultural Bank of China - Linzhou Branch | | 01/29/2012 | | | 1,468,731 | |

| Linzhou City Hongqiqu Electrical Carbon Co., Ltd | | Agricultural Bank of China - Linzhou Branch | | 02/10/2012 | | | 4,406,192 | |

| Xinlei Group Cheng Chen Coking | | Henan Rural Credit Cooperative - Tongye Branch | | 04/04/2011 | | | 2,937,461 | |

| Xinpu Steel Co., Ltd | | Henan Rural Credit Cooperative - Anyang Branch | | 01/04/2012 | | | 7,343,654 | |

| | | | | | | $ | 46,044,708 | |

Capital Lease Obligations

SC Coke has entered into a non-cancellable lease agreement for certain machinery and equipment. The following table details SC Coke’s commitments for minimum lease payments and the related principal outstanding at June 30, 2010:

| Year ending December 31: | | Principal | | | Payments | |

| 2011 | | $ | 668,718 | | | $ | 916,209 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

| Year ending December 31: | | Principal | | | Payments | |

| 2012 | | | 1,413,345 | | | | 1,832,418 | |

| 2013 | | | 1,520,962 | | | | 1,832,418 | |

| 2014 | | | 1,636,773 | | | | 1,832,418 | |

| 2015 | | | 613,883 | | | | 659,148 | |

| Total future minimum lease payments | | $ | 5,853,681 | | | $ | 7,072,611 | |

Past Due Payment of Enterprise Income Taxes

At December 31, 2009, SC Coke had approximately $3.0 million of overdue enterprise income taxes. As a result, SC Coke is subject to an overdue fine at the rate of 0.05% per day of the amount of taxes in arrears, commencing from the day the tax payment is overdue. The tax authority may also impose an additional fine of 50% to five times the underpaid taxes. SC Coke has recorded an accrued liability for the estimated taxes due and has determined that there is no uncertain tax position to record relating to the potential penalties and interest related to the overdue tax balance at this time.

SC Coke has available funds to cover the underpaid tax and overdue fine, but may not have sufficient funds available to pay the additional fine. The Chairman entered into a tax indemnity agreement on May 23, 2010, pursuant to which he agreed to indemnify SC Coke for any interest, penalties or other related extra costs resulting from the prior and any future tax underpayments in tax years in which he managed and operated SC Coke. The indemnification is capped at $35.6 million.

Concentration of Credit and Other Risks

Cash, bank notes receivable, and trade receivables subject SC Coke to concentrations of credit risk. SC Coke holds all its deposits and bank notes receivable with banks in China. In China, there is no insurance equivalent to the federal deposit insurance in the United States; as such these amounts held in banks in China are not insured. SC Coke has not experienced any losses in such bank accounts through June 30, 2010.

SC Coke offers unsecured credit to its customers in the normal course of business; therefore, SC Coke’s accounts receivable are subject to credit risks.

Economic and Political Risks

The operations of SC Coke are located in the PRC. Accordingly, the Company’s business, financial condition, and results of operations may be influenced by the political, economic, and legal environment in the PRC.

The Chinese Government controls its foreign currency reserves through restrictions on imports and conversion of Renminbi into foreign currency. In July 2005, the Chinese Government adjusted its exchange rate policy from “Fixed Rate” to “Floating Rate”. From December 31, 2009 to June 30, 2010, the exchange rate between RMB and US Dollars fluctuated between $1.00 to RMB 6.8372 and $1.00 to RMB 6.8086. There can be no assurance that the exchange rate will remain stable. The Renminbi could appreciate or depreciate against the US Dollar. The Company’s financial condition and results of operations may also be affected by changes in the value of certain currencies other than the Renminbi in which its earnings and obligations are denominated.

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

17. | Share Based Compensation |

For the six months ended June 30, 2010, the Company recorded an expense of $567,496 under the general and administrative account for the issuance of 540,472 common shares at $1.05 per share. The shares were issued to financial consultants for services rendered in connection with the Share Exchange and expected future financing transactions. For the purposes of calculating earnings per share, the Company has assumed that these shares were issued on January 1, 2010.

On June 28, 2010, the Company issued to SCM Capital, LLC two warrants. The first warrant entitles the holder to purchase 1,922,833 common shares, at an exercise price of $4.50 per share. The second warrant entitles the holder to purchase 6% of the number of common shares issued and outstanding immediately following the closing of a private financing resulting in gross proceeds of $25 million or more, less 1,922,833 common shares. Neither warrant is exercisable until the closing of such private financing, and each warrant is subject to forfeiture in the event such private financing is not closed on or prior to August 31, 2010. Accordingly, the Company believes that the contingently issuable shares are related to a capital transaction and are not compensatory in nature but are potentially dilutive for purposes of calculating earnings per share.

| | | 3 months | | | 3 months | | | 6 months | | | 6 months | |

| | | ended | | | ended | | | ended | | | ended | |

| | | 6/30/2010 | | | 6/30/2009 | | | 6/30/2010 | | | 6/30/2009 | |

| | | | | | | | | | | | | |

| Basic earnings per share numerator: | | | | | | | | | | | | |

| Net income attributable to common shareholders | | $ | 1,396,362 | | | $ | 3,903,378 | | | $ | 2,518,626 | | | $ | 3,210,143 | |

| | | | | | | | | | | | | | | | | |

| Basic weighted average shares outstanding: | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

| Additions from potentially dilutive events | | | | | | | | | | | | | | | | |

| Warrants issued to consultant | | | - | | | | - | | | | - | | | | - | |

| Diluted weighted average shares outstanding: | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

| | | | | | | | | | | | | | | | | |

| Earnings per share | | | | | | | | | | | | | | | | |

| - Basic | | $ | 0.04 | | | $ | 0.12 | | | $ | 0.08 | | | $ | 0.10 | |

| - Diluted | | $ | 0.04 | | | $ | 0.12 | | | $ | 0.08 | | | $ | 0.10 | |

| | | | | | | | | | | | | | | | | |

| Weighted average shares outstanding: | | | | | | | | | | | | | | | | |

| - Basic | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

| - Diluted | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | | | | 32,047,222 | |

Birch Branch, Inc.

Notes to Unaudited Interim Consolidated Financial Statements

(Unaudited)

(A) Loan from Bank of China, Anyang Branch

On July 20, 2010, SC Coke entered into a loan agreement with Bank of China, Anyang Branch. The principal amount of the secured loan is approximately $2,937,461. The secured loan carries an interest rate of 5.841% per annum, is due on July 20, 2011, and is personally guaranteed by the SC Coke Shareholders, one of whom is the chairman of the Board of the Company, and a third party guarantor.

(B) Loan from China Construction Bank, Anyang Branch

On July 28, 2010, SC Coke entered into a loan agreement with China Construction Bank, Anyang Branch. The principal amount of the loan is approximately $2,937,461. The loan carries an interest rate of the PRC prime rate, which was 5.310% per annum on July 28, 2010, and is due on July 28, 2011.

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis, as well as other sections in this Quarterly Report on Form 10-Q, should be read in conjunction with the unaudited interim consolidated financial statements and related notes to the unaudited interim consolidated financial statements included elsewhere herein.

The information contained in this Quarterly Report includes some statements that are not purely historical and that are “forward-looking statements” as defined by the Private Securities Litigation Reform Act of 1995. Such forward-looking statements include, but are not limited to, statements regarding our and our management’s expectations, hopes, beliefs, intentions or strategies regarding the future, including our financial condition and results of operations. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continues,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would” and similar expressions, or the negatives of such terms, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.