South Hertfordshire United Kingdom Fund Inactive

Filed: 2 Mar 11, 12:00am

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX OF FINANCIAL STATEMENTS

TABLE OF CONTENTS 2

INDEX OF FINANCIAL STATEMENTS 2

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. 1)

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

ý | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

o | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material under §240.14a-12 | |

| South Hertfordshire United Kingdom Fund, Ltd. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

N/A | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

Payment of Filing Fee (Check the appropriate box): | ||||

o | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: N/A | |||

| (2) | Aggregate number of securities to which transaction applies: N/A | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): For purposes of calculating the filing fee only, the underlying value of transaction of $22,864,513 was determined by multiplying (i) the purchase price of £14,293,000 to be paid by ntl (B) Limited to acquire 299,390 A ordinary shares of ntl (South Hertfordshire) Limited from South Hertfordshire United Kingdom Fund, Ltd. by (ii) the exchange rate of $1.5997 per £1.00, the noon buying rate for cable transfers in pounds sterling as certified for custom purposes by the Federal Reserve Bank of New York as of January 21, 2011. | |||

| (4) | Proposed maximum aggregate value of transaction: $22,864,513 | |||

| (5) | Total fee paid: $2,654.57, determined by multiplying the proposed maximum aggregate value of transaction by 0.0001161 | |||

ý | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

PRELIMINARY COPY—SUBJECT TO COMPLETION, DATED [ • ], 2011

SOUTH HERTFORDSHIRE UNITED KINGDOM FUND, LTD.

SPECIAL MEETING OF UNITHOLDERS

[ • ], 2011

Dear Unitholder,

You are cordially invited to attend a special meeting of holders ("unitholders") of the limited partnership interests (the "Partnership units") of South Hertfordshire United Kingdom Fund, Ltd. (the "Partnership") on [ • ], 2011 at [ • ], local time, at [ • ].

At the special meeting, you will be asked to consider and vote upon a proposal to approve the sale (the "Asset Sale") of the Partnership's 66.7% ownership interest in ntl (South Hertfordshire) Limited ("ntl South Herts") to ntl (B) Limited for £14,293,000 ($22,864,513, assuming an exchange rate of $1.5997 per £1.00 as of January 21, 2011). ntl (B) Limited is an indirect wholly owned subsidiary of Virgin Media Inc. and an affiliate of ntl Fawnspring Limited, the general partner of the Partnership (the "General Partner").

The Partnership's 66.7% ownership interest in ntl South Herts, which consists of 299,390 A ordinary shares of ntl South Herts (the "Partnership Asset"), is the Partnership's sole asset.

The agreement governing the Partnership (the "Partnership Agreement") requires that the price to be paid in a sale of the Partnership Asset to an affiliate of the General Partner must be determined by the average of three separate independent appraisals of the fair market value of the Partnership Asset and that the sale must be approved by unitholders (other than the General Partner or its affiliates) holding a majority of the outstanding Partnership units. Accordingly, the purchase price to be paid by ntl (B) Limited for the Partnership Asset represents the average of three separate independent appraisals, as more fully described in the proxy statement accompanying this letter, and you and the other unitholders of the Partnership are being asked to consider and vote upon the proposal to approve the Asset Sale.

If the proposal to approve the Asset Sale is approved and the Asset Sale is completed, then, as required by the Partnership Agreement, the Partnership will be dissolved and the General Partner will commence the process of liquidating and winding up the Partnership. The General Partner will use the proceeds of the Asset Sale to pay and provide for the outstanding liabilities and other obligations of the Partnership (including indebtedness owed by the Partnership to Virgin Media Inc. and its affiliates) and establish cash reserves in an amount equal to $335,000 for the payment of contingent or unforeseen liabilities of the Partnership. The actual amount of reserves established by the General Partner may be increased at the discretion of the General Partner, as more fully described in the proxy statement accompanying this letter.

The General Partner will distribute the remaining proceeds to the unitholders of record as of the record date of the distribution in accordance with the terms of the Partnership Agreement. The General Partner estimates that unitholders will receive approximately $300 per unit upon the initial distribution of the proceeds of the Asset Sale, based on, among other things, the purchase price for the Partnership Asset and estimates of the Partnership's outstanding liabilities, expenses and required cash reserves described in the preceding paragraph, and assuming an exchange rate of $1.5997 per £1.00. To the extent that all or a portion of the Partnership's cash reserves are not used to settle any contingent or unforeseen liabilities of the Partnership after our dissolution, a further distribution of the unused portion of the cash reserves will be made to unitholders at a later date to be established by the General Partner. The actual amounts distributed to unitholders will depend on, among other things, the actual amount of liabilities and obligations of the Partnership upon its dissolution (including contingent liabilities paid out of the cash reserves following the dissolution), expenses incurred by the Partnership prior to or in connection with its dissolution and winding up, the amount of the General Partner's

capital account deficit, and the exchange rate at the time the proceeds of the Asset Sale are converted into U.S. Dollars, as further described in the proxy statement accompanying this letter.

Following the Asset Sale, the dissolution of the Partnership and the distributions of all remaining Partnership funds to unitholders of record, the Partnership will be terminated.

If the Asset Sale and the dissolution of the Partnership are not completed, there will be no distribution in connection with the Asset Sale and the Partnership's term will otherwise expire on December 31, 2016, at which time the Partnership will be dissolved and liquidated in accordance with the Partnership Agreement. There can be no assurance that, prior to or upon the expiration of the Partnership term, Virgin Media Inc., any of its affiliates or any other party will offer to acquire the Partnership Asset for an amount equal to or greater than the purchase price contemplated in the proposed Asset Sale or that unitholders will receive distributions equal to or greater than the distributions expected to be made in connection with the Asset Sale.

Whether or not you plan to attend the special meeting, please complete, date, sign and return, as promptly as possible, the enclosed proxy card in the accompanying prepaid reply envelope, or submit your proxy by telephone or the Internet. If you attend the special meeting and vote in person, your vote by ballot will revoke any proxy previously submitted.The failure to vote will have the same effect as a vote "AGAINST" the proposal to approve the Asset Sale.

The accompanying proxy statement provides you with detailed information about the special meeting and the items of business, the three separate independent appraisals, the Asset Sale and the dissolution of the Partnership.You are encouraged to read the entire proxy statement and its annexes carefully. You may also obtain additional information about the Partnership from documents it has filed with the Securities and Exchange Commission.

If you have any questions or need assistance voting your Partnership units, please call Georgeson Inc., the Partnership's proxy solicitor ("Georgeson"), toll-free, at 877-797-1153. If calling from outside the United States, please call collect: 212-440-9800. You can also email Georgeson at southherts@georgeson.com.

Thank you in advance for your cooperation.

Sincerely,

| Robert Mackenzie Director | Robert Gale Director |

For and on behalf of the General Partner, ntl Fawnspring Limited

The proxy statement is dated [ • ], 2011, and is first being mailed to the Partnership's unitholders on or about [ • ], 2011.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THE ASSET SALE, PASSED UPON THE MERITS OR FAIRNESS OF THE ASSET SALE, OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE INFORMATION CONTAINED IN THE ENCLOSED PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

PRELIMINARY COPY—SUBJECT TO COMPLETION, DATED [ • ], 2011

SOUTH HERTFORDSHIRE UNITED KINGDOM FUND, LTD.

7103 South Revere Parkway, Englewood Colorado 80112, United States

Address of principal executive office:

Media House, Bartley Wood Business Park, Hook, Hampshire, RG27 9UP, England

NOTICE OF SPECIAL MEETING OF UNITHOLDERS

TO BE HELD ON[ • ], 2011

To the Unitholders of South Hertfordshire United Kingdom Fund, Ltd.,

A special meeting of unitholders of the Partnership will be held on [ • ], 2011 at [ • ], local time, at [ • ], to consider and vote upon a proposal to approve the sale of the Partnership's 299,390 A ordinary shares of ntl South Herts (representing a 66.7% ownership interest) to ntl (B) Limited pursuant to a Share Purchase Agreement, dated as of January 31, 2011, by and between the Partnership and ntl (B) Limited, a copy of which is attached asAnnex A to the proxy statement accompanying this notice.

Holders of Partnership units as of the close of business on [ • ], 2011 will be entitled to notice of, and to vote at, the special meeting and at any adjournments or postponements of the meeting.

Whether or not you plan to attend the special meeting, please complete, date, sign and return, as promptly as possible, the enclosed proxy card in the accompanying prepaid reply envelope, or submit your proxy by telephone or the Internet. If you attend the special meeting and vote in person, your vote by ballot will revoke any proxy previously submitted.The failure to vote will have the same effect as a vote "AGAINST" the proposal to approve the Asset Sale.

By order of the General Partner, ntl Fawnspring Limited

| Robert Mackenzie Director | Robert Gale Director |

[ • ], 2011

The proxy statement is dated [ • ], 2011, and is first being mailed to the Partnership's unitholders on or about [ • ], 2011.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THE ASSET SALE, PASSED UPON THE MERITS OR FAIRNESS OF THE ASSET SALE, OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE INFORMATION CONTAINED IN THE ENCLOSED PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE

SUMMARY TERM SHEET | 1 | |||

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND THE ASSET SALE | 9 | |||

The Special Meeting | 9 | |||

The Asset Sale | 11 | |||

SPECIAL FACTORS | 15 | |||

The Parties to the Asset Sale | 15 | |||

The Partnership Asset | 15 | |||

Certain Relevant Provisions of the Partnership Agreement | 16 | |||

Dissolution of the Partnership Following the Asset Sale and Distributions to Unitholders | 18 | |||

Background of the Asset Sale | 19 | |||

The General Partner's Reasons for the Asset Sale and Factors Considered in Determining Fairness | 22 | |||

Reasons and Position of ntl (B) Limited and its Affiliates Regarding the Fairness of the Asset Sale | 26 | |||

Alternatives to the Asset Sale | 27 | |||

Certain Other Effects of the Asset Sale | 28 | |||

Plans for ntl South Herts After the Asset Sale | 29 | |||

Interests of Certain Persons in the Asset Sale | 29 | |||

Reports of the Appraisal Firms | 30 | |||

Material U.S. Federal Income Tax Consequences of the Asset Sale and the Dissolution of the Partnership | 43 | |||

Material United Kingdom Income Tax Consequences of the Asset Sale and Dissolution of the Partnership | 46 | |||

ntl (B) Limited's Financing of the Asset Sale | 46 | |||

Rights of Dissenting Unitholders | 47 | |||

Regulatory Approvals | 47 | |||

FORWARD-LOOKING STATEMENTS | 48 | |||

THE SHARE PURCHASE AGREEMENT | 50 | |||

The Asset Sale | 50 | |||

Effective Time of the Asset Sale | 50 | |||

Representations and Warranties | 50 | |||

Conditions to the Closing of the Asset Sale | 51 | |||

Termination | 51 | |||

PAST CONTACTS, TRANSACTIONS, NEGOTIATIONS AND AGREEMENTS | 52 | |||

Consulting and Management Fees | 52 | |||

General Partner Services and Interest Expense Reimbursement | 52 | |||

Arrangements between ntl South Herts and Affiliates of Virgin Media Inc. | 52 | |||

Outstanding Indebtedness | 53 | |||

THE SPECIAL MEETING | 54 | |||

Time, Place and Purpose of the Special Meeting | 54 | |||

Record Date | 54 | |||

Attendance | 54 | |||

Vote Required | 54 | |||

Solicitation of Proxies; Payment of Solicitation Expenses | 55 | |||

No Unitholder Proposals | 56 | |||

Dissenter's Rights | 56 | |||

Other Matters of Action at the Special Meeting | 56 | |||

OTHER IMPORTANT INFORMATION REGARDING THE PARTNERSHIP | 57 | |||

Description of Business | 57 | |||

i

Description of Property | 57 | |||

Legal Proceedings | 57 | |||

Financial Statements and Supplementary Financial Information | 57 | |||

Management's Discussion and Analysis of Financial Condition and Results of Operations | 57 | |||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 57 | |||

Historical Selected Financial Data | 57 | |||

Currencies and Exchange Rates | 60 | |||

Book Value Per Unit | 61 | |||

Quantitative and Qualitative Disclosures about Market Risk | 63 | |||

Officers and Directors | 63 | |||

Business Address | 63 | |||

OTHER IMPORTANT INFORMATION REGARDING THE GENERAL PARTNER, NTL (B) LIMITED AND THEIR AFFILIATES | 64 | |||

The General Partner | 64 | |||

ntl (B) Limited | 64 | |||

Virgin Media Inc. | 65 | |||

Virgin Media Limited | 69 | |||

INCORPORATION BY REFERENCE | 70 | |||

WHERE YOU CAN FIND MORE INFORMATION ABOUT US | 70 | |||

Annex A—Share Purchase Agreement, dated January 31, 2011, between South Hertfordshire United Kingdom Fund, Ltd. and ntl (B) Limited | ||||

Annex B—Annual Report on Form 10-K for the fiscal year ended December 31, 2009 | ||||

Annex C—Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2010 | ||||

ii

The following summary highlights selected information in this proxy statement and may not contain all the information that may be important to you. Accordingly, we encourage you to read carefully this entire proxy statement, its annexes and the documents referred to in this proxy statement. Each item in this summary includes a page reference directing you to a more complete description of that item. References to the "Partnership," "we", "our" or "us" in this proxy statement refer to South Hertfordshire United Kingdom Fund, Ltd. unless otherwise indicated by context.

This proxy statement is dated [ • ], 2011, and is first being mailed to unitholders on or about [ • ], 2011.

Overview: The Asset Sale Proposal

The Parties to the Asset Sale (page [ • ])

1

The Dissolution of the Partnership Following the Asset Sale (page [ • ])

Distributions to Unitholders in Connection with the Asset Sale and the Dissolution of the Partnership (page [ • ])

2

contingent or unforeseen liabilities paid for out of the Cash Reserves after the dissolution), expenses incurred by us prior to or in connection with our dissolution and winding up, the actual amount of the General Partner's capital account deficit, and the exchange rate at the time the proceeds of the Asset Sale are converted into U.S. Dollars.

Proceeds of the Asset Sale | £14,293,000 | ||||

Estimated outstanding Partnership liabilities (1) | £(3,100,000 | ) | |||

| £11,193,000 | |||||

Conversion into U.S. dollars, assuming the Current Exchange Ratio ($1.5997 per £1.00) | $ | 17,905,442 | |||

Estimated expenses | $ | (645,000 | ) | ||

Estimated Cash Reserves | $ | (335,000 | ) | ||

Estimated General Partner's capital account deficit contribution | $ | 400,000 | |||

Estimated aggregate amount of initial distribution to unitholders | $ | 17,325,442 | |||

Estimated per unit amount of initial distribution to unitholders (2)(3) | $ | 304.30 | |||

Certain Relevant Provisions of the Partnership Agreement (page [ • ])

The following are certain provisions of the Partnership Agreement relevant to the Asset Sale proposal:

3

determining capital accounts of the partners (i) 99% to the unitholders and 1% to the General Partner, and (ii) among the unitholders, so that each unitholder will have an equal capital account per Partnership interest.

The General Partner's Reasons for the Asset Sale and Factors Considered in Determining Fairness (page [ • ])

Reports of the Appraisals Firms (page [ • ])

Appraisal Report of BTG Mesirow Financial Consulting, LLC

4

Appraisal Report of BTG Mesirow Financial Consulting, LLC" beginning on page [ • ]. The General Partner agreed to pay BTG MFC a fee equal to £46,600, exclusive of expenses, for its services in connection with the appraisal. The fee paid to BTG MFC was not contingent upon the conclusion reached by BTG MFC in its report or whether or not the Asset Sale is successfully completed.

Appraisal Report of Duff & Phelps Ltd.

Appraisal Report of Grant Thornton LLP

Material Tax Consequences of the Asset Sale and the Dissolution of the Partnership (page [ • ])

5

Partnership should result in any unitholder of the Partnership who is non-U.K. resident and non-U.K. ordinarily resident being liable to U.K. taxation on any gain realized on such disposal, provided that the unitholder concerned is not carrying on a trade in the U.K. through a branch or agency in the U.K.

ntl (B) Limited's Financing of the Asset Sale (page [ • ])

Interests of Certain Persons in the Asset Sale (page [ • ])

You should be aware that the General Partner, its directors and management, and their affiliates have interests in the Asset Sale that are different from, or in addition to, the interests of the Partnership's unitholders generally as described in "Interests of Certain Persons in the Asset Sale" beginning on page [ • ], including the following:

Affiliations with Virgin Media Inc.

Payments to the General Partner and Affiliates of Virgin Media Inc. in Connection with the Asset Sale.

6

Rights of Dissenting Unitholders (page [ • ])

The Share Purchase Agreement (page [ • ])

7

The Special Meeting (page [ • ])

8

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND THE ASSET SALE

The following questions and answers are intended to address briefly some commonly asked questions regarding the special meeting, the proposed Asset Sale and, the subsequent dissolution of the Partnership. These questions and answers may not address all the questions that may be important to you as a Partnership unitholder. Please refer to the "Summary Term Sheet" and the more detailed information contained elsewhere in this proxy statement, the annexes to this proxy statement and the documents referred to in this proxy statement. For instructions on obtaining more information, see "Where You Can Find More Information" beginning on page [ • ].

Q: Why am I receiving this proxy statement and proxy card?

Q: When and where is the special meeting?

The special meeting may be adjourned, recessed or postponed by the General Partner at its discretion to another date for any proper purposes (including, without limitation, for the purpose of soliciting additional proxies), subject to applicable law.

Q: What am I being asked to vote on at the special meeting?

Q: Who is entitled to vote at the special meeting?

Q: What do I need to do to vote?

Internet. You may submit a proxy to vote on the Internet up until 11:59 p.m. Eastern Time on [ • ] by going to the website for Internet voting on your proxy card (www.georgeson.com) and

9

following the instructions on your screen. Have your proxy card available when you access the web page. If you vote by the Internet, you should not return your proxy card.

Telephone. You may submit a proxy to vote by telephone by calling the toll-free telephone number on your proxy card, 24 hours a day and up until 11:59 p.m. Eastern Time on [ • ], and following the prerecorded instructions. Have your proxy card available when you call. If you vote by telephone, you should not return your proxy card.

Mail. You may submit a proxy to vote by mail by marking the enclosed proxy card, dating and signing it, and returning it in the postage-paid envelope provided. If you own the Partnership units in various registered forms, such as jointly with your spouse, as trustee of a trust or as custodian for a minor, you will receive, and will need to sign and return, a separate proxy card for those units because they are held in a different form of record ownership. Partnership units held by a corporation or business entity must be voted by an authorized officer of the entity.

Televote™. You may submit a proxy by way of Televote™. Georgeson, our proxy solicitor, will call investors to solicit their voting instructions. The procedures for executing a vote via this method will be provided by telephone.

In Person. You may vote in person by attending the special meeting. If you plan to attend the special meeting and wish to vote in person, you will be given a ballot at the special meeting. Whether or not you plan to attend the special meeting, you should submit your proxy as described in this proxy statement.

Q: Can I change my vote after I return my proxy card?

Q: Can I vote in person at the special meeting rather than completing the proxy card?

Q: What is a proxy?

Q: If a unitholder gives a proxy, how are the Partnership units voted?

10

If you properly sign your proxy card but do not mark the boxes showing how your units should be voted on a matter, the units represented by your properly signed proxy will be voted "FOR" the proposal to approve the Asset Sale.

Q: What constitutes a quorum?

Q: What vote is required to approve the Asset Sale proposal?

Q: Will my vote really make a difference?

Q: What is the proposed Asset Sale?

Q: How were the purchase price to be paid for the Partnership Asset and the other terms of the Asset Sale determined?

11

negotiation. As the General Partner and the Partnership do not have any employees or management other than the employees and management of Virgin Media, Inc., none of the other terms of the Asset Sale or the Share Purchase Agreement were subject to arm's-length negotiation. Any transaction between the General Partner and an affiliate of Virgin Media Inc. should not be deemed to be free of conflicts of interest.

Q: What will happen if the vote to approve the sale of the Partnership Asset is passed?

Following the completion of the Asset Sale, the Partnership will be dissolved and the General Partner will commence the process of liquidating and winding up the Partnership in accordance with the Partnership Agreement and Colorado law.

In connection with the dissolution of the Partnership, the General Partner intends to first pay or provide for the outstanding liabilities and obligations of the Partnership (including indebtedness owed by the Partnership to Virgin Media Inc. and its affiliates). The General Partner intends to then convert the remaining proceeds of the Asset Sale from U.K. pounds sterling into U.S. dollars and pay or provide for expenses to be incurred by the Partnership prior to and in connection with its dissolution and winding up. The General Partner also intends to establish cash reserves (the "Cash Reserves") in an amount equal to $335,000 out of Partnership funds for the payment of contingent or unforeseen liabilities of the Partnership. The General Partner may increase the amount of the Cash Reserves if, prior to the initial distribution to unitholders, the General Partner becomes aware of circumstances or events that in its judgment would increase the amount of potential liabilities (or the likelihood of their realization) of the Partnership following its dissolution. Portions of the Cash Reserves may be used to pay any indemnification obligations of the Partnership in favor of the General Partner permitted under the terms of the Partnership Agreement.

Amounts of the Cash Reserves remaining after payment of any contingent or unforeseen liabilities will be distributed by the General Partner at a later date to be established by the General Partner in its discretion.

Subsequent to the Asset Sale, the Partnership may seek termination of its obligation to file reports under the Exchange Act. Following the Asset Sale, the dissolution of the Partnership and the distributions of all remaining Partnership funds to unitholders of record, the Partnership will be terminated and will cease to exist.

Q: What will I receive if the Asset Sale and the dissolution of the Partnership is completed?

Amounts reserved by the General Partner remaining after payment of any contingent or unforeseen liabilities will be distributed by the General Partner at a later date to be established by the General Partner in its discretion. The actual amounts distributed to unitholders will depend on, among other things, the actual amount of liabilities and obligations of the Partnership upon our dissolution (including contingent and unforeseen liabilities to be paid for out of the Cash

12

Reserves), expenses incurred by us prior to or in connection with our dissolution and winding up, the actual amount of the General Partner's capital account deficit, and the exchange rate at the time the proceeds of the Asset Sale are converted into U.S. Dollars.

Q: When is the Asset Sale and the dissolution of the Partnership expected to be completed if approved by the Partnership unitholders?

Q: What will happen if the Asset Sale is not approved?

Q: Why is the Partnership engaging in the Asset Sale at the present time?

Q: What are the material U.S. federal income tax consequences of the Asset Sale and the dissolution of the Partnership to me?

13

exceeds) the unitholder's adjusted tax basis in its Partnership units. You should consult your own tax advisor for a complete analysis of the effect of the Asset Sale and the dissolution of the Partnership on your federal, state and local and/or foreign taxes. See "Material U.S. Federal Income Tax Consequences of the Asset Sale and Dissolution of the Partnership" for more detail including information regarding limitations on the ability to claim certain losses realized by the Partnership.

Q: Who can help answer my other questions?

14

The Partnership

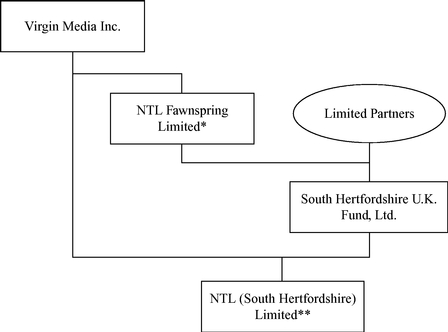

We are a Colorado limited partnership formed on December 31, 1991 in connection with the public offering of our Partnership units for the purpose of acquiring, constructing, developing, owning and operating cable television/telephone systems in the United Kingdom. Our sole asset consists of a 66.7% ownership interest in ntl South Herts.

Our business is managed by our General Partner and our only operations consist of those of ntl South Herts. We do not directly employ personnel of our own. The various personnel required to carry out our business and the operations of ntl South Herts are employed by affiliates of Virgin Media Inc., including Virgin Media Limited, an indirect wholly owned subsidiary of Virgin Media Inc. We rely on Virgin Media Inc.'s management, organization, financing and infrastructure to carry on our business and operations.

The General Partner

The General Partner is an English company incorporated on April 29, 1994 and is an indirect wholly owned subsidiary of Virgin Media Inc. The General Partner manages our business, properties and activities in accordance with the terms of the Partnership Agreement, although operating control is delegated to other affiliated companies of Virgin Media Inc. The General Partner holds a general partnership interest in the Partnership, but will not vote on the proposal to approve the Asset Sale. Neither Virgin Media Inc., ntl (B) Limited nor any of their affiliates hold any Partnership units.

ntl (B) Limited

ntl (B) Limited is an English company incorporated on July 30, 1992 and is an indirect wholly owned subsidiary of Virgin Media Inc. ntl (B) Limited holds the 33.3% of the shares of ntl South Herts not owned by the Partnership and has no other assets or operations. ntl (B) Limited relies on the employees and management of Virgin Media Inc. for its business and operations.

For further information regarding the parties to the Asset Sale, see "Past Contacts, Transactions, Negotiations and Agreements" beginning on page [ • ], "Other Important Information Regarding the Partnership" beginning on page [ • ] and "Other Important Information Regarding the General Partner, ntl (B) Limited and Their Affiliates" beginning on page [ • ]. In addition, see our Annual Report on Form 10-K for the fiscal year ended December 31, 2009, which is attached asAnnex B to this proxy statement and is referred to as the "Form 10-K", and our Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2010, which is attached to this proxy statement asAnnex C and is referred to as the "Third Quarter Form 10-Q". The Form 10-K attached to this proxy statement does not include the exhibits originally filed with that report.

The Partnership Asset consists of our 299,390 A ordinary shares of ntl South Herts, which represents a 66.7% ownership interest in ntl South Herts. ntl (B) Limited holds the remaining stake in ntl South Herts.

ntl South Herts is an English company principally engaged in the development, construction, management and operation of broadband communications networks for telephone, cable television and internet services in the United Kingdom.

15

The area covered by the ntl South Herts cable television/telephone system, which is referred to as the franchise area, comprises the administrative areas in South Hertfordshire: Three Rivers, Watford and Hertsmere. Construction in the franchise area is complete.

As of September 30, 2010, ntl South Herts serviced 28,103 digital television subscribers, 30,539 residential telephony subscribers and 29,163 broadband internet subscribers, representing a total of 34,829 residential customers.

ntl South Herts owns the local cable television/telephone network infrastructure, but it is not a stand-alone business as its network is totally integrated with that of Virgin Media Inc. and its affiliates. Virgin Media Limited performs a variety of management functions and procures services on behalf of ntl South Herts, including technology infrastructure, cable television content, marketing and billing services, customer and technical support, financing and back office services, and employs the various personnel required to operate the cable television/telephone network. ntl South Herts' customers procure services through Virgin Media Limited and its affiliates and under the Virgin Media name.

Management control of ntl South Herts is exercised by our General Partner, although operating control is delegated to Virgin Media Limited and other affiliated companies of Virgin Media Inc.

For further information regarding ntl South Herts, see "Past Contacts, Transactions, Negotiations and Agreements" beginning on page [ • ] and our Form 10-K and Third Quarter Form 10-Q, which are attached to this proxy statement asAnnex B andAnnex C, respectively.

Certain Relevant Provisions of the Partnership Agreement

Dissolution

Under the Partnership Agreement, the term of the Partnership will expire on December 31, 2016, at which time the Partnership will be dissolved. Prior to this date, however the Partnership shall also be dissolved upon the occurrence of certain other events, including the disposition of substantially all of the assets of the Partnership or upon a vote by the unitholders to dissolve the Partnership. The Asset Sale will constitute a disposition of substantially all of the assets of the Partnership.

The Partnership Agreement provides that upon the dissolution of the Partnership, the General Partner will wind up the affairs of the Partnership, sell all of the assets of the Partnership and pay or provide for all of its liabilities including the costs of dissolution and fees due to the General Partner. The General Partner will then distribute the remainder of the Partnership's funds to the unitholders and the General Partner in accordance with the distribution priorities specified in the Partnership Agreement. The General Partner will also be required to contribute funds equal to the amount of any accumulated deficit that may exist in the capital account of the General Partner. Upon completion of the dissolution, the Partnership will be terminated.

Certain Sales of Partnership Assets

The Partnership Agreement provides that the General Partner may sell cable television/telephony property, including shares of a company holding cable television/telephony property such as the Partnership Asset, to the General Partner or its affiliates if the sale price for the property is determined by the average of three separate independent appraisals of the fair market value of the property and if the sale is approved by unitholders (other than the General Partner and its affiliates) holding a majority of the outstanding Partnership units. The cost of the appraisals is borne by the General Partner or its affiliate and not by the Partnership.

16

Allocations of Book Loss

Pursuant to the Partnership Agreement, for purposes of determining the capital accounts of the partners, items of loss are generally required to be allocated 99% to the unitholders and 1% to the General Partner. Additionally, if a Partnership asset is sold at a loss as determined for book purposes pursuant to the Partnership Agreement after the admission of additional unitholders as limited partners, book loss is to be allocated as deemed appropriate by the General Partner on the advice of its counsel or its accountants to conform the allocations to the order of distributions described in Section 5.4(b) of the Partnership Agreement. Section 5.4(b) of the Partnership Agreement requires certain distributions to be made first to each unitholder in an amount that will equal the unitholder's adjusted capital contribution (generally, the amount of cash contributed by the unitholder to the Partnership taking into account certain adjustments thereto), and if the amount of the distribution is insufficient to satisfy that amount, in proportion to the amount which each unitholder would receive if the amount were sufficient. The General Partner will allocate the loss on the disposition of the Partnership Asset (i) 99% to the unitholders and 1% to the General Partner, and (ii) among the unitholders, so that each unitholder will have an equal capital account per unit, an allocation which would cause each unitholder to receive distributions in proportion to that unitholder's capital contribution.

Certain Distributions

Under the Partnership Agreement any distribution upon dissolution of the Partnership Agreement is made as follows: first, to each unitholder having a positive balance in its capital account after having income or gain allocated pursuant to the Partnership Agreement in an amount equal to such positive balance in proportion to such positive balance, but in an amount not to exceed each unitholder's capital contributions after taking into account certain adjustments thereto; second, to each unitholder having a positive balance in its capital account after having income or gain allocated pursuant to the Partnership Agreement in an amount equal to such positive balance in proportion to such positive balance, but in an amount not to exceed each unitholder's 12% per annum return; third to the General Partner to the extent it has a positive balance in its capital account after having income or gain allocated to it pursuant to the Partnership Agreement in an amount equal to such positive balances. Since the amounts that will be distributed in connection with the Asset Sale will not exceed each unitholder's capital contributions, distributions will be made only to the unitholders, in proportion to their positive capital account balances. The capital account balances, subsequent to the allocation of book losses described above under "—Allocations of Book Loss", will be equal for each Partnership unit, and, accordingly, distributions will be made equally with respect to each Partnership unit. No distributions will be made to the General Partner with respect to its general partnership interest.

Certain Restrictions on Transfers of Partnership Units

The Partnership Agreement contains certain restrictions on the assignment and transfer of Partnership units, including the following:

17

Notwithstanding the foregoing and the other applicable restrictions on assignments and transfers contained in the Partnership Agreement, the economic benefits of ownership of the Partnership units may be transferred without receiving the written consent of the General Partner or executing an amended Partnership Agreement.

Dissolution of the Partnership Following the Asset Sale and Distributions to Unitholders

The Asset Sale will constitute the sale of all of our assets, which will result in the dissolution and, ultimately, the termination of the Partnership. Immediately following the completion of the Asset Sale, the General Partner intends to begin to wind up our affairs in accordance with the terms of the Partnership Agreement and Colorado law.

The General Partner intends first to apply the proceeds received by us in the Asset Sale to pay or provide for our outstanding liabilities and obligations. As of September 30, 2010, our outstanding liabilities totalled approximately £3.1 million. These outstanding liabilities were comprised solely of debt obligations owed to Virgin Media Limited, an indirectly wholly owned subsidiary of Virgin Media Inc. and an affiliate of the General Partner and ntl (B) Limited, as more fully described under "Past Contacts, Transactions, Negotiations and Agreements" beginning on page [ • ].

After paying or providing for our outstanding liabilities and obligations, the General Partner intends to convert the remaining proceeds into U.S. Dollars at the spot exchange rate and pay or provide for expenses to be incurred by the Partnership prior to and in connection with its dissolution and winding up. We currently estimate that we will incur approximately $645,000 in additional transaction, operating and other expenses prior to or in connection with our dissolution and winding up, which will be paid or provided for out of Partnership funds. Other than costs and expenses attributable to the dissolution and winding up of the Partnership, including certain costs incurred in connection with this proxy solicitation, ntl (B) Limited will pay for any expenses in connection with the Asset Sale, including the fees associated with obtaining the three independent appraisals.

The General Partner will then contribute to the Partnership the amount of its capital account deficit, which we currently estimate will be approximately $400,000 if the Asset Sale is consummated. The General Partner also intends to establish the Cash Reserves in an amount equal to at least $335,000 for the payment of contingent or unforeseen liabilities of the Partnership. The General Partner may increase the amount of the Cash Reserves if, prior to the initial distribution to unitholders, the General Partner becomes aware of circumstances or events that in its judgment would increase the amount of potential liabilities (or the likelihood of their realization) of the Partnership following its dissolution. Portions of the Cash Reserves may be used to pay any indemnification obligations of the Partnership in favor of the General Partner permitted under the terms of the Partnership Agreement.

Based upon, among other things, the amount of our liabilities outstanding as of September 30, 2010 and estimated additional expenses, the General Partner estimates that unitholders will receive an initial distribution of approximately $17 million as a group and approximately $300 per Partnership unit (assuming the Current Exchange Rate). To the extent that all or a portion of the Cash Reserves are not used to settle any contingent or unforeseen liabilities of the Partnership after our dissolution, a further

18

distribution of remaining amounts will be made to unitholders at a later date established by the General Partner. The actual amounts distributed to unitholders will depend on, among other things, the actual amount of liabilities and obligations of the Partnership upon our dissolution (including contingent or unforeseen liabilities paid for out of the Cash Reserves after the dissolution), expenses incurred by us prior to and in connection with our dissolution and winding up, the actual amount of the General Partner's capital account deficit, and the exchange rate at the time the proceeds of the Asset Sale are converted into U.S. Dollars.

The Asset Sale and the dissolution constitute a "going private transaction" for purposes of U.S. federal securities laws. Subsequent to the Asset Sale, we may seek termination of our obligation to file reports under the Exchange Act. Following the Asset Sale, the Partnership will be dissolved and the General Partner will file a statement of dissolution with the Colorado Secretary of State on behalf of the Partnership and will complete the liquidation and winding up process of the Partnership, including the distribution of remaining Partnership funds to unitholders, following which the Partnership will be terminated and will cease to exist.

In accordance with the Partnership Agreement the dissolution of the Partnership will be triggered upon consummation of the Asset Sale and the General Partner expects to commence the liquidation and winding up process as soon as practicable following the Asset Sale and dissolution. The final distribution of amounts reserved by the General Partner remaining after payment of any contingent or unforeseen liabilities will be distributed by the General Partner at a later date established by the General Partner in its discretion. A dissolution and liquidation is a complex process that may depend on a number of factors, and some of these factors are beyond our control. For example, we may be pursuing claims against others or defending litigation, or there may be other contingencies to which we may become subject during the dissolution process. These factors may delay our ultimate liquidation and the distribution of the proceeds of the Asset Sale to unitholders. In addition, these factors may impact our financial condition and may negatively impact the amount of distributions received by unitholders upon our liquidation. Our current estimates of the expenses to be incurred by the Partnership prior to and in connection with its dissolution and winding up, the amount of the General Partner's capital account deficit if the Asset Sale is consummated, and other amounts and factors that will affect the amount of funds available for distribution to unitholders if the Asset Sale is completed, including the applicable exchange rate between the U.S. dollar and the U.K. pound sterling, are subject to inherent uncertainty and risks, as further described below under "Forward-Looking Statements" beginning on page [ • ].

Other than the purchase price for the Partnership Asset, which represents the average of three independent appraisals of the fair market value of the Partnership Asset, the terms and conditions of the proposed Asset Sale and the Share Purchase Agreement were determined by employees and management of Virgin Media Limited and Virgin Media Inc. (collectively, "Virgin Media"), some of whom are also directors of the General Partner (which manages the Partnership) and ntl (B) Limited. The directors of the General Partner and ntl (B) Limited are Robert Gale, the principal accounting officer of Virgin Media Inc., and Robert Mackenzie, the legal director of Virgin Media Limited. In their capacity as directors, they approved the Asset Sale and the Share Purchase Agreement on behalf of both the Partnership and ntl (B) Limited. Other Virgin Media Limited employees in the finance and legal functions have been involved on a day to day basis in preparing for the Asset Sale and setting the terms of the Share Purchase Agreement. The Chief Financial Officer of Virgin Media Inc., Eamonn O'Hare, has also overseen this process. As none of the foregoing directors or employees of Virgin Media Limited and Virgin Media Inc. acted as an independent representative of the General Partner or ntl (B) Limited, and neither the General Partner nor ntl (B) Limited has any independent directors, managers or employees, the terms and conditions of the Share Purchase Agreement and the proposed

19

Asset Sale were not subject to negotiation. Set forth below is a summary of the background of events that led to the decision to execute the Share Purchase Agreement.

The management of Virgin Media has, from time to time, discussed with its Audit Committee (which is also the audit committee of the Partnership) and its Board of Directors the possibility of an affiliate of Virgin Media acquiring the Partnership or the Partnership's interest in ntl South Herts and providing liquidity to the Partnership's unitholders. In part, the impetus for this consideration has been the burdens associated with the Partnership's status as an SEC registrant, including the preparation of its periodic reports.

In November 2006, funds associated with MacKenzie Patterson Fuller, LP ("MacKenzie Patterson") commenced a tender offer for units of the Partnership at a price of $65 per unit. The General Partner recommended that partners not accept the offer on the basis that it was inconsistent with the Partnership Agreement and, consequently, the General Partner did not intend to permit the transfers on the basis set out in the offer. The General Partner noted, among other reasons, that the purchase of Partnership units in accordance with the terms of the offer could have adverse tax consequences to the Partnership, including causing the Partnership to be treated as a "publicly traded partnership" under the Internal Revenue Code.

In connection with its adverse recommendation on the MacKenzie Patterson offer, the General Partner undertook to examine various means, consistent with the Partnership Agreement, by which unitholders could obtain increased liquidity. The General Partner warned, however, that it could give no assurance as to whether any such action would be undertaken, the timing of any such action or the value per unit that would be generated by any such action.

Shortly thereafter, Virgin Media retained the law firm Fried, Frank, Harris, Shriver & Jacobson LLP ("Fried Frank"), which regularly acted as counsel to Virgin Media and its affiliates and had advised it in connection with the MacKenzie Patterson offer, to undertake a review of alternative means by which unitholders could be provided with increased liquidity consistent with the requirements of the Partnership Agreement and the tax considerations described above. The means considered included both structures through which individual unitholders could be afforded liquidity, such as odd lot offers and other similar transactions, and various alternative transaction structures through which Virgin Media Inc. or its affiliates could acquire the Partnership or the Partnership's interest in ntl South Herts. Management made a presentation on this subject to the Virgin Media Audit Committee at its May 2007 meeting.

Commencing in May and June 2007, Virgin Media undertook a strategic review of its own status, including a potential sale of Virgin Media. This resulted in an auction process for Virgin Media, which was terminated in early August 2007 as a result of the collapse of the public debt markets that would have provided the financing for such an acquisition.

From August 2007 through early 2010, Virgin Media focused on other priorities, including its own substantial recapitalization through a series of financing transactions, as well as on the disposition of assets that were seen as non-strategic. During this period of time, the management of Virgin Media did not focus on issues associated with the Partnership.

At its meeting on April 27, 2010, the Audit Committee requested that management prepare a presentation on alternative proposals for the acquisition of the Partnership and/or its assets and dissolution of the Partnership. The discussion of this issue arose in the context of the Committee's consideration of the continuing burdens associated with the Partnership's status as an SEC registrant.

From May through July 2010, Virgin Media management and employees, with advice of counsel, carried out further work relating to alternative transaction structures. At its meeting on July 26, 2010, the Audit Committee received a presentation about alternative approaches to winding up the Partnership. The presentation reflected legal advice from Virgin Media's internal counsel and Fried

20

Frank. The presentation focused on the alternatives of acquisition of ntl South Herts, acquisition of the Partnership, and dissolution of the Partnership in 2016 in accordance with the terms of the Partnership Agreement. Mr. Gale indicated that management intended to proceed to explore the alternatives and next steps.

The presentation was also made to the Virgin Media Inc. Group Executive Committee ("GEC") on July 27, 2010. The GEC is comprised of the most senior U.K. executives of Virgin Media Inc. and is chaired by the chief executive officer, Mr. Neil Berkett. The GEC authorized management to proceed to explore the alternatives and next steps and delegated to Mr. Eamonn O'Hare the responsibility of overseeing the process and authorizing any transaction.

After the meetings on July 26 and 27, 2010, Virgin Media retained Davis Graham & Stubbs LLP ("Davis Graham") as Colorado counsel. Members of management and internal counsel, Fried Frank and Davis Graham held conference calls in August to explore alternative transaction structures. After due consideration of the risks and benefits associated with each alternative, and taking into account the fact that the directors of the General Partner of the Partnership were also officers of Virgin Media and there were no independent directors of, or other advisors to, the Partnership, the directors of the General Partner and Mr. O'Hare, concluded that the most sensible course of action was to follow the procedure contemplated by the Partnership Agreement for a sale of assets to affiliates of the General Partner, which involved the securing of three independent appraisals. This procedure is described above under "—Certain Relevant Provisions of the Partnership Agreement—Certain Sales of Partnership Assets" beginning on page [ • ]. They also determined that the acquiror of the Partnership Asset should be ntl (B) Limited, which held the other 33.3% interest in ntl South Herts.

In September 2010, Virgin Media employees, with oversight from one of the directors of the General Partner, drafted a request for proposal (the "RFP") that was addressed to independent valuation firms. The RFP process was initiated in late September 2010 by contacting eight valuation firms that management and counsel identified that seemed to have relevant industry expertise and where, insofar as management was aware, Virgin Media had no commercial relationships. Responses were received from six firms, five of which were interviewed. On or about October 18, 2010, Virgin Media Limited and the General Partner formally engaged BTG MFC, Duff & Phelps and Grant Thornton to render a conclusion as to the fair market value of the Partnership Asset as of September 30, 2010. The process by which the three independent appraisal firms were selected, the bases of the appraisal firms' analyses and the conclusions of their respective appraisal reports are described under—"Reports of the Appraisal Firms" beginning on page [ • ].

Virgin Media management and employees delivered separate presentations to BTG MFC, Duff & Phelps and Grant Thornton regarding the operations, financial conditions, and historic performance of ntl South Herts and on taxation and financing matters. During those presentations and thereafter, Virgin Media management and employees responded to questions from the appraisers. The appraisers were instructed to perform their own assessments of the future prospects of ntl South Herts in order that the independence of their valuations not be influenced by Virgin Media's views on valuation, but Virgin Media responded to factual questions about anticipated future developments.

On November 9, 2011, Virgin Media employees, with Virgin Media internal and outside counsel present, met at Fried Frank's offices in London with each appraisal firm to respond to questions and comment on any factual issues.

Draft appraisal reports were delivered to Virgin Media and the General Partner between November 11 and 13, 2011.

The independent appraisers then finalized their reports on or around November 24, 2010.

While the appraisal processes were underway, Virgin Media and the directors of the General Partner reviewed proposals from two proxy solicitation firms, and the General Partner determined to

21

retain Georgeson Inc. It was agreed that Georgeson Inc. would be paid a base fee, plus an additional incentive based on the percentage of unitholders that voted (without regard to whether the unitholders voted for, against or abstained in connection with the Asset Sale proposal). Georgeson's fee arrangements are further described under "The Special Meeting—Solicitation of Proxies; Payment of Solicitation Expenses" beginning on page [ • ]. Employees of Virgin Media, under supervision of the directors of the General Partner, together with Fried Frank, began to prepare this proxy statement soliciting the approval of the unitholders for the Asset Sale. Fried Frank, as counsel to Virgin Media, prepared the draft Share Purchase Agreement for the Asset Sale, and reviewed the terms with internal counsel and the management and employees of Virgin Media and the directors of the General Partner.

On January 31, 2011, for the reasons set forth under "—The General Partner's Reasons for the Asset Sale and Factors Considered in Determining Fairness" beginning on page [ • ], after carefully reviewing the reports of the three independent appraisers, the process that was followed in connection with the proposed Asset Sale, and the terms of the Share Purchase Agreement, the board of directors of the General Partner (i) determined that the Asset Sale is procedurally and substantively fair to the unitholders that are unaffiliated with ntl (B) Limited, Virgin Media Limited and Virgin Media Inc., (ii) approved the Share Purchase Agreement with ntl (B) Limited and authorized the General Partner to execute the Share Purchase Agreement on behalf of the Partnership, (iii) authorized the General Partner to submit the Asset Sale for the consideration and approval of the unitholders, and (iv) authorized the filing of the preliminary proxy statement. Similarly, the management of Virgin Media, including Mr. O'Hare, and the board of directors of ntl (B) Limited, for the reasons set forth under "—Reasons and Position of ntl (B) Limited and its Affiliates Regarding the Fairness of the Asset Sale," (i) determined that the Asset Sale is procedurally and substantively fair to the unitholders that are unaffiliated with ntl (B) Limited, Virgin Media Limited and Virgin Media Inc., (ii) approved the Share Purchase Agreement with the Partnership and authorized ntl (B) Limited to execute the Share Purchase Agreement and (iii) authorized the filing of the preliminary proxy statement.

The General Partner's Reasons for the Asset Sale and Factors Considered in Determining Fairness

This section describes the General Partner's purposes and reasons for the Asset Sale and factors considered in determining its fairness. It is important to bear in mind that the General Partner does not have any employees or management other than the employees and management of Virgin Media Limited and Virgin Media Inc. who represented both the General Partner and ntl (B) Limited in connection with the Asset Sale. Consequently, the purposes, reasons, and factors attributable to the General Partner represent those of employees and management of Virgin Media Limited and Virgin Media Inc. acting solely in their capacities as employees and management of the General Partner and should not be deemed to be free of conflicts of interest. Please see "Interests of Certain Persons in the Asset Sale" beginning on page [ • ] and "Past Contacts, Transactions, Negotiations and Agreements" beginning on page [ • ] for further information about the relationships among the parties to the Asset Sale and their affiliates.

The proposed Asset Sale will provide unitholders with an opportunity to liquidate their investment in the Partnership units at a price determined in accordance with the Partnership Agreement in advance of the scheduled expiration of the Partnership term.

Since the primary offering of the Partnership units in 1991, the Partnership units have been generally illiquid. Additionally, the Partnership is not required to pay and has never paid distributions to unitholders. Although the Partnership units are registered under the Exchange Act due to the number of individual unitholders, the Partnership units are not traded on a national securities exchange or any formal trading market and are subject to certain restrictions on transfers, including those described above under "—Certain Relevant Provisions of the Partnership Agreement—Certain Restrictions on Transfers of Partnership Units" beginning on page [ • ].

22

For the past several years, the General Partner has been aware that certain unitholders have desired increased liquidity with respect to their Partnership units. Some unitholders have expressed a desire to liquidate their investment in the Partnership prior to the scheduled expiration of the Partnership term on December 31, 2016 and eliminate the federal income tax complexities and other fees associated with holding the Partnership units.

At the time of the $65 per unit tender offer by funds associated with MacKenzie Patterson in 2006, the General Partner undertook to examine various means by which unitholders could obtain such increased liquidity consistent with the provisions of the Partnership Agreement. The General Partner believes that at the present time there is no reasonable likelihood that the Partnership units will become freely tradable prior to the scheduled expiration of the Partnership term. Under the Internal Revenue Code, transfers of Partnership units could cause the Partnership to be treated as a "publicly traded partnership". Among other things, treatment as a publicly traded partnership would cause the Partnership to be treated as a corporation for U.S. federal income tax purposes, and would cause the Partnership to be subject to entity level U.S. federal income tax upon all of its income. As a result, the General Partner intends to continue to enforce the transfer restrictions of the Partnership Agreement and to exercise its authority to prevent the public trading of the Partnership units.

However, the General Partner believes that, as an alternative to the public trading of the Partnership units, the proposed Asset Sale would allow unitholders the opportunity to determine whether to proceed with the sale of the Partnership Asset and liquidate their investment several years in advance of the scheduled expiration of the Partnership term through the subsequent dissolution of the Partnership. The General Partner determined to engage in the Asset Sale at this time because it believes that the recent improvement in the financial performance of the Partnership provides an opportune time for the unitholders to consider the proposed Asset Sale. After the General Partner undertook to examine potential transaction alternatives following the 2006 MacKenzie Patterson tender offer, the Partnership had net profit (loss) of $(3,316,921) and $619,521 in 2006 and 2007, respectively, which has since improved to $1,855,296 and $2,989,112 in 2008 and 2009, respectively, and $1,469,742 in the first nine months of 2010. In addition, while at the present time ntl (B) Limited is willing and able to engage in the Asset Sale subject to the terms and conditions of the Share Purchase Agreement, there can be no assurance that ntl (B) Limited or any other affiliate of Virgin Media Inc. will have the financial means or willingness to engage in a similar transaction in the future. In addition, there can be no assurance that, prior to or upon the expiration of the Partnership term, any other party would offer to acquire the Partnership Asset for an amount equal to or greater than the purchase price contemplated in the proposed Asset Sale or that unitholders would receive distributions equal to or greater than the distributions expected to be made in connection with the Asset Sale.

After carefully reviewing the reports of the three independent appraisers, the process that was followed in connection with the proposed Asset Sale, and the terms of the Share Purchase Agreement, the board of directors of the General Partner (i) determined, on behalf of itself, the General Partner and the Partnership, that the Asset Sale is procedurally and substantively fair to the unitholders that are unaffiliated with ntl (B) Limited, Virgin Media Limited and Virgin Media Inc., (ii) approved the Share Purchase Agreement with ntl (B) Limited and authorized the General Partner to execute the Share Purchase Agreement on behalf of the Partnership and (iii) authorized the General Partner to submit the Asset Sale for the consideration and approval of the unitholders.

In evaluating the Asset Sale and its fairness to the unaffiliated unitholders, the board of directors of the General Partner, acting on behalf of the General Partner and the Partnership, considered a number of potentially positive factors, including the following:

23

The board of directors of the General Partner also believes that the process by which the General Partner entered into the Share Purchase Agreement was fair, and in reaching that determination, the board of directors of the General Partner considered a number of potentially positive factors, including the following:

24

The board of directors of the General Partner also considered a number of additional potentially countervailing factors in its deliberations concerning the Asset Sale, including the following:

The board of directors of the General Partner did not give weight to the net book value of the Partnership, which is an accounting concept derived by deducting the total liabilities from the total assets as reported in the Partnership's consolidated financial statements, in determining the substantive fairness of the Asset Sale to the unitholders. The board of directors of the General Partner believes that the net book value of the Partnership of $4,961,386 as at September 30, 2010 is not a material

25

indicator of the value of the Partnership as a going concern but rather is indicative of historical costs and that, as discussed below, the value of the Partnership's interest in ntl South Herts is derived from the cash flows generated by ntl South Herts' continuing operations. For reference purposes only, as of September 30, 2010, the Partnership's net book value per Partnership unit is $87.14 as compared with the initial per unit distribution of $300 (assuming the Current Exchange Rate) that the General Partner estimates unitholders will receive after the Asset Sale and the dissolution of the Partnership.

For the same reason, the board of directors of the General Partner did not give weight to the consolidated value of the limited partners' interest in the Partnership in determining the substantive fairness of the Asset Sale to the unitholders. The limited partners' interest in the Partnership was $2,293,980 as at September 30, 2010 as compared with the $22,864,513 (assuming the Current Exchange Rate) purchase price for the Partnership Asset.

Additionally, the board of directors of the General Partner did not give weight to the liquidation value of ntl South Herts in determining the substantive fairness of the Asset Sale to the unitholders. The board of directors of the General Partner believes that liquidation value does not present a meaningful valuation for ntl South Herts and its business. It is the belief of the board of directors of the General Partner that the value of the Partnership's 66.7% interest in ntl South Herts is derived from the cash flows generated from ntl South Herts' continuing operations, rather than from the value of its assets that might be realized in a liquidation. Because the assets of ntl South Herts are not readily transferable in a liquidation scenario (other than to Virgin Media Inc. or its affiliates), the board of directors of the General Partner believes that ntl South Herts is not susceptible to a meaningful liquidation valuation.

The preceding discussion is not meant to be an exhaustive description of the information and factors considered by the board of directors of the General Partner, but is believed to address the material information and factors considered. In view of the wide variety of factors considered in connection with its evaluation of the Asset Sale and the complexity of these matters, the board of directors of the General Partner did not find it practicable to, and did not, quantify or otherwise attempt to assign relative weights to the various factors considered in reaching its determination. In considering the factors described above, the individual members of the board of directors of the General Partner may have given different weight to different factors. The board of directors of the General Partner has determined the Asset Sale is fair to unitholders based upon the totality of the information presented to and considered by it.

Reasons and Position of ntl (B) Limited and its Affiliates Regarding the Fairness of the Asset Sale

For ntl (B) Limited and its owners and management, including Virgin Media Inc., Virgin Media Limited and their affiliates, the purpose of the Asset Sale is to acquire the interests in ntl South Herts owned by the Partnership so that ntl (B) Limited can directly control 100% of the interests of ntl South Herts.

ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. and their affiliates believe that the Asset Sale will reduce Virgin Media Inc.'s organizational complexity and enhance the overall operational efficiency associated with managing the operations of ntl South Herts. Affiliates of Virgin Media Limited currently manage all aspects of the operations of ntl South Herts through the current Partnership structure via arrangements with the General Partner. These arrangements are more fully described below under "Past Contacts, Transactions, Negotiations and Agreements" beginning on page [ • ]. Affiliates of Virgin Media Inc. also devote significant time and resources to the management of the Partnership as a standalone public company. The Asset Sale, dissolution and the ultimate termination of the Partnership will eliminate the need for the business currently represented by the Partnership to comply with the federal securities laws and filing requirements applicable to a public company.

26

Virgin Media Inc. also desires to complete the Asset Sale in order to ensure the stability of Virgin Media Inc.'s reputation and brand, as ntl South Herts distributes its cable and telephone services to its customers under the Virgin Media brand.

In addition, the Asset Sale will allow Virgin Media Inc. to bear the full rewards and risks of ownership of ntl South Herts. Virgin Media Inc., as a corporation with perpetual existence, has a longer investment horizon as well as a more diversified business than the Partnership.

ntl (B) Limited and its affiliates also believe that the Asset Sale will provide unitholders with an opportunity to liquidate their investment in the Partnership at a price determined in accordance with the Partnership Agreement in advance of the scheduled expiration of the Partnership term. ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. believe that the Asset Sale is substantively and procedurally fair to the Partnership's unitholders that are unaffiliated with ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. each expressly adopt the analysis of the board of directors of the General Partner of the factors upon which its determination as to the fairness of the proposed Asset Sale is based and the conclusions of the board of directors of the General Partner with respect to the fairness of the proposed Asset Sale, as described under "The General Partner's Reasons for the Asset Sale and Factors Considered in Determining Fairness" beginning on page [ • ]

Alternatives to the Asset Sale

In connection with its consideration of the Asset Sale, the General Partner considered two primary alternatives to provide unitholders with an opportunity to liquidate their investment in the Partnership: (i) the continued ownership of the Partnership Asset by the Partnership until the liquidation of the Partnership upon the expiration of the Partnership's term and (ii) the sale of the Partnership Asset to a third party unaffiliated with Virgin Media Inc. and the distribution of the net proceeds to unitholders.

As the Asset Sale is subject to unitholder approval, the Asset Sale provides unitholders the opportunity to determine whether to proceed with the Asset Sale and the resulting dissolution of the Partnership. If the Asset Sale proposal is not approved, the General Partner believes the Partnership will continue its operations until the Partnership is dissolved upon the scheduled expiration of the Partnership's term on December 31, 2016.

The General Partner also considered a potential sale of the Partnership Asset to an unaffiliated third party, but determined that the fact that the operations of ntl South Herts are fully integrated with, and are dependent on, those of Virgin Media Inc. would preclude a viable, or in any case, a financially competitive, and timely third party offer for the Partnership Asset. In addition, the General Partner believes that a transaction effected in accordance with the explicit terms of the Partnership Agreement would provide the fairest treatment of the unitholders.

In determining to acquire the Partnership Asset, ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. considered various alternative transaction structures, such as a tender offer for Partnership units or a merger of the Partnership. ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. ultimately concluded that effecting an asset sale in accordance with the explicit terms of the Partnership Agreement by obtaining the three independent appraisals and conditioning the transaction on the approval of holders (other than the General Partner and its affiliates) of a majority of the outstanding Partnership units would eliminate issues relating to the determination of fairness to unitholders that would otherwise arise in connection with a transaction between affiliates. ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. believed that since the Partnership Agreement did not contain provisions for determining the fairness to unitholders of a tender offer or merger transaction between the Partnership and its affiliates, those transaction structures would create greater uncertainty than the Asset Sale as to the precise procedures required for ensuring that the transaction was fair to unitholders.

27

Certain Other Effects of the Asset Sale

If the Asset Sale is completed, ntl (B) Limited will own 100% of the shares of ntl South Herts (as compared to the 33.3% percent of the shares of ntl South Herts that it currently owns). Consequently, ntl (B) Limited, and indirectly, its direct and indirect parent companies Virgin Media Limited and Virgin Media Inc., will become the sole beneficiaries of the future earnings and growth, if any, of ntl South Herts and will acquire a 100% interest in the net book value and the net profits of ntl South Herts. Based upon the net book value of ntl South Herts as of September 30, 2010 and the net profit of ntl South Herts for the nine months ended September 30, 2010 as reflected in the unaudited books and records of ntl South Herts, ntl (B) Limited's 100% interest in the net book value of ntl South Herts would be equal to approximately £6.3 million (as compared to its 33.3% interest of the net book value of ntl South Herts of approximately £2.1 million), and its 100% interest in the net profit of ntl South Herts for the nine-month period ended September 30, 2010 would be equal to £1.8 million (as compared to its 33.3% interest in the net profit of ntl South Herts of approximately £0.6 million). In addition, following the Asset Sale ntl South Herts will retain the benefit of U.K. tax assets arising from previous expenditure on fixed assets, which will indirectly benefit ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. to the extent deductions are available to be applied to ntl South Herts' U.K. taxable income. The maximum deduction that can be claimed in any one year is 20% of the remaining balance of expenditure, after additions, disposals and prior claims, and is deductible in computing ntl South Herts' U.K. taxable income for a year. The maximum deduction is expected to fall to 18% beginning April 1, 2012. At December 31, 2010, ntl South Herts is estimated to have £47.3 million of future deductible expenditure. The decision to acquire the Partnership's interests in ntl South Herts through an asset sale structure was not based on these tax benefits.

Detriments of the Asset Sale to ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. include the fact that they will bear the full risks of ownership of ntl South Herts and that they will have incurred significant transaction expenses in connection with the Asset Sale. ntl (B) Limited, Virgin Media Limited and Virgin Media Inc. expect to elect to surrender tax losses of other affiliate companies to ntl South Herts to cover taxable income of ntl South Herts remaining after the deduction of ntl South Herts' own tax assets described above.

Following completion of the Asset Sale, the General Partner will continue to manage the liquidation and winding up of the Partnership, including managing any distributions to unitholders out of the Cash Reserve, until the Partnership's termination. Following the termination of the Partnership, the General Partner's general partnership interest in the Partnership will be extinguished and the General Partner will no longer have an interest in the Partnership's net book value, net profits or potential future profits or growth. In connection with the dissolution of the Partnership, the General Partner will be required to contribute to the Partnership the amount of its outstanding capital account deficit, which the General Partner estimates will be approximately $400,000.

The benefits of the Asset Sale to the Partnership include the fact that the Asset Sale constitutes the sale of all the assets of the Partnership for £14,293,000 in cash and that the Partnership will pay off all its outstanding liabilities. Detriments of the Asset Sale to the Partnership include the fact that it will no longer have an interest in ntl South Herts' net book value, net profits or potential future profits or growth of ntl South Herts and that the Asset Sale will result in the dissolution and, ultimately, the termination of the Partnership.

If the Asset Sale is completed and the Partnership is terminated, the Partnership's unaffiliated unitholders will no longer have any equity interests in the Partnership. Benefits of the Asset Sale to the Partnership's unaffiliated unitholders include the fact that they will receive distributions out of the proceeds of the Asset Sale as described above under "—Dissolution of the Partnership Following the Asset Sale and Distributions to Unitholders" and will cease to bear the risk of any decrease in the value of the Partnership. Detriments of the Asset Sale to the Partnership's unaffiliated unitholders

28