Table of Contents

As Filed with the Securities and Exchange Commission on August 2, 2006

Securities Act File No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933 x

Pre-Effective Amendment No. ¨

Post-Effective Amendment No. ¨

CASH ACCOUNT TRUST

(Exact Name of Registrant as Specified in Charter)

222 South Riverside Plaza

Chicago, Illinois 60606

(Address of Principal Executive Offices) (Zip Code)

617-295-2572

(Registrant’s Area Code and Telephone Number)

John Millette, Secretary

Cash Account Trust

Two International Place

Boston, Massachusetts 02110

(Name and Address of Agent for Service)

With copies to:

David A. Sturms, Esq.

Vedder, Price, Kaufman & Kammholz, P.C.

222 North LaSalle Street

Chicago, Illinois 60601

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

TITLE OF SECURITIES BEING REGISTERED: Shares of Beneficial Interest (no par value) of the Registrant.

No filing fee is required because an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Questions & Answers

DWS Government & Agency Money Fund

DWS Money Funds

Government & Agency Securities Portfolio

Investors Cash Trust

Q&A

Q What is happening?

A Deutsche Asset Management (or “DeAM” as defined on page [14] in the enclosed Prospectus/Proxy Statement) has initiated a program to reorganize and restructure the money market funds within the DWS fund family.

Q What issue am I being asked to vote on?

A You are being asked to vote on the merger of your fund into the Government & Agency Securities Portfolio series of Cash Account Trust (“CAT Government Fund”). Your fund and CAT Government Fund have substantially similar investment objectives and policies.

After carefully reviewing the proposal, your fund’s Board has determined that this action is in the best interest of your fund. The Board unanimously recommends that you vote for the proposal.

Q Why has this proposal been made for my fund?

A The proposal to merge your fund into CAT Government Fund is part of a program initiated by DeAM to provide a more streamlined selection of money market investment options. The program seeks to eliminate redundancies within the DWS money market funds and to focus DeAM’s investment resources on a core set of money market funds that best meet investor needs. DeAM believes that the merger will eliminate product

Table of Contents

Q&A continued

redundancies, maximize portfolio size wherever possible, and create the possibility for higher yielding funds with potentially lower expenses.

Q Will I have to pay taxes as a result of the merger?

A The merger is expected to be a tax-free reorganization for federal income tax purposes, and will not take place unless special tax counsel provides an opinion to that effect. Because each fund seeks to maintain a net asset value of $1.00 per share, you are unlikely to have a capital gain or loss if you redeem or exchange your shares before or after the merger. Nevertheless, you may wish to consult a tax advisor for more information on your own tax situation.

Q Will I own the same number of shares after the merger?

A Yes. You will receive shares equal in number to the shares owned as of the merger date.

Q Will my fund pay for the proxy solicitation and legal costs associated with this solicitation?

A No. DeAM will bear these costs.

Q When would the merger take place?

A If approved, the merger would occur on or about [October 30], 2006 or as soon as reasonably practicable after shareholder approval is obtained. Shortly after completion of the merger, shareholders whose accounts are affected by the merger will receive a confirmation statement reflecting their new account number and the number of shares owned.

Q How can I vote?

A You can vote in any one of four ways:

| n | Through the Internet by going to the website listed on your proxy card(s); |

| n | By telephone, with a toll-free call to the number listed on your proxy card(s); |

Table of Contents

Q&A continued

| n | By mail, by sending the enclosed proxy card(s), signed and dated, to us in the enclosed envelope; or |

| n | In person, by attending the special meeting. |

We encourage you to vote over the Internet or by telephone, following the instructions that appear on your proxy card(s). Whichever method you choose, please take the time to read the full text of the Prospectus/Proxy Statement before you vote.

Q If I send my proxy in now as requested, can I change my vote later?

A You may revoke your proxy at any time before it is voted by: (1) sending a written revocation to the Secretary of your Fund as explained in the proxy statement; or (2) forwarding a later-dated proxy that is received by your Fund at or prior to the special meeting; or (3) attending the special meeting and voting in person. Even if you plan to attend the special meeting, we ask that you return the enclosed proxy card. This will help us ensure that an adequate number of shares are present for the special meeting of your Fund to be held.

Q Will I be able to continue to track my fund’s performance on the Internet or through the voice response system (InvestorACCESS)?

A Yes. You will be able to continue to track your fund’s performance before the merger through both these means.

Q Whom should I call for additional information about this Prospectus/Proxy Statement?

A Please call Computershare Fund Services, Inc. your fund’s proxy solicitor, at (866) 774-4940.

Table of Contents

DWS GOVERNMENT & AGENCY MONEY FUND

DWS MONEY FUNDS

GOVERNMENT & AGENCY SECURITIES PORTFOLIO

INVESTORS CASH TRUST

A Message from the Funds’ President

[mailing date], 2006

Dear Shareholders:

I am writing to you to ask for your vote on an important matter that affects your investment in the DWS Government & Agency Money Fund series of DWS Money Funds (“DWS Government Fund”) and the Government & Agency Securities Portfolio series of Investors Cash Trust (“ICT Government Fund”), as applicable. While you are, of course, welcome to join us at the joint special shareholders’ meeting, most shareholders cast their vote by filling out and signing the enclosed proxy card, or by voting by telephone or through the Internet.

We are asking for your vote on the following matters, as applicable:

| Proposal for DWS Government Fund: | Approval of a proposed merger of DWS Government Fund into the Government & Agency Securities Portfolio series of Cash Account Trust (“CAT Government Fund”). In this merger, your shares of DWS Government Fund would be exchanged, on a tax-free basis for federal income tax purposes, for shares of a newly-created class of CAT Government Fund equal in number to the DWS Government Fund shares held by you. | |

| Proposal for ICT Government Fund: | Approval of a proposed merger of ICT Government Fund into CAT Government Fund. In this merger, your shares of ICT Government Fund would be exchanged, on a tax-free basis for federal income tax purposes, for shares of a newly-created class of CAT Government Fund equal in number to the ICT Government Fund shares held by you. | |

Each proposed merger is part of a program initiated by Deutsche Asset Management (or “DeAM” as defined on page [14] of the enclosed Prospectus/Proxy Statement) to reorganize and restructure the money market funds in the DWS family of funds. The program is designed to enable DeAM to: (1) eliminate redundancies within the DWS money market funds by reorganizing and combining certain funds; and (2) focus its investment resources on a core set of money market funds that best meet investor needs.

DeAM believes that the mergers offer shareholders:

| • | A similar investment opportunity in a larger fund with the opportunity to achieve greater economies of scale and a lower expense ratio; and |

| • | A portfolio with the possibility of higher yields generated through more efficient execution and greater stability of assets. |

Table of Contents

The Trustees of your Fund have determined that the proposed merger of your Fund into CAT Government Fund is in the best interests of the Fund. If approved by shareholders, the Board expects that the merger of your Fund will take effect during the [fourth] calendar quarter of 2006.

Included in this booklet is information about the upcoming joint special shareholders’ meeting:

| • | A Notice of a Joint Special Meeting of Shareholders, which summarizes the matter for which you are being asked to provide voting instructions; and |

| • | A Prospectus/Proxy Statement, which provides detailed information on CAT Government Fund and the specific proposals being considered at the joint special shareholders’ meeting and why the proposals are being made. |

Although we would like very much to have each shareholder attend the meeting, we realize this may not be possible. Whether or not you plan to be present, we need your vote. We urge you to review the enclosed materials thoroughly. Once you’ve determined how you would like your interests to be represented, please promptly complete, sign, date and return the enclosed proxy card, vote by telephone or record your voting instructions on the Internet. A postage-paid envelope is enclosed for mailing, and telephone and Internet voting instructions are listed at the top of your proxy card. You may receive more than one proxy card. If so, please vote each one.

I’m sure that you, like most people, lead a busy life and are tempted to put this proxy aside for another day. Please don’t. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

Your vote is important to us. We appreciate the time and consideration I am sure you will give to this important matter. If you have questions about the proposal, please call Computershare Fund Services, Inc., your fund’s proxy solicitor, at (866) 774-4940 or contact your financial advisor. Thank you for your continued support of DWS Scudder Investments.

Sincerely yours,

Michael Clark

President

DWS Money Funds

Investors Cash Trust

Table of Contents

DWS GOVERNMENT & AGENCY MONEY FUND DWS MONEY FUNDS

GOVERNMENT & AGENCY SECURITIES PORTFOLIO INVESTORS CASH TRUST

NOTICE OF A JOINT SPECIAL MEETING OF SHAREHOLDERS

This is the formal agenda for your Fund’s special shareholder meeting. It tells you what matter will be voted on and the time and place of the special meeting, in the event you choose to attend in person.

To the Shareholders of the DWS Government & Agency Money Fund series of DWS Money Funds (“DWS Government Fund”) and the Government & Agency Securities Portfolio series of Investors Cash Trust (“ICT Government Fund”):

A Joint Special Meeting of Shareholders of DWS Government Fund and ICT Government Fund will be held October 12, 2006 at [9:00 a.m.] Eastern time, at the offices of Deutsche Investment Management Americas Inc., 345 Park Avenue, 27th Floor, New York, New York 10154 (the “Meeting”), to consider the following (the “Proposals”):

| Proposal for DWS Government Fund: | Approving an Agreement and Plan of Reorganization and the transactions it contemplates, including the transfer of all of the assets of DWS Government Fund to the Government & Agency Securities Portfolio series of Cash Account Trust (“CAT Government Fund”), in exchange for shares of CAT Government Fund and the assumption by CAT Government Fund of all liabilities of DWS Government Fund, and the distribution of such shares, on a tax-free basis for federal income tax purposes, to the shareholders of DWS Government Fund in complete liquidation and termination of DWS Government Fund. | |

| Proposal for ICT Government Fund: | Approving an Agreement and Plan of Reorganization and the transactions it contemplates, including the transfer of all of the assets of ICT Government Fund to the Government & Agency Securities Portfolio series of Cash Account Trust (“CAT Government Fund”), in exchange for shares of CAT Government Fund and the assumption by CAT Government Fund of all liabilities of ICT Government Fund, and the distribution of such shares, on a tax-free basis for federal income tax purposes, to the shareholders of ICT Government Fund in complete liquidation and termination of ICT Government Fund. | |

The persons named as proxies will vote in their discretion on any other business that may properly come before the Meeting or any adjournments or postponements thereof.

Holders of record of shares of DWS Government Fund and ICT Government Fund at the close of business on August 14, 2006 and August 3, 2006, respectively, are entitled to vote with respect to the Proposal for their Fund at the Meeting and at any adjournments or postponements thereof.

In the event that the necessary quorum to transact business or the vote required to approve the merger of your Fund is not obtained at the Meeting, the persons named as

Table of Contents

proxies may propose one or more adjournments of the Meeting with respect to your Fund in accordance with applicable law to permit such further solicitation of proxies as may be deemed necessary or advisable.

By order of the Trustees

John Millette

Secretary

[mailing date], 2006

WE URGE YOU TO MARK, SIGN, DATE AND MAIL THE ENCLOSED PROXY CARD(S) IN THE POSTAGE-PAID ENVELOPE PROVIDED OR TO RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR THROUGH THE INTERNET SO THAT YOU WILL BE REPRESENTED AT THE MEETING.

Table of Contents

INSTRUCTIONS FOR SIGNING PROXY CARDS

The following general rules for signing proxy cards may be of assistance to you and avoid the time and expense involved in validating your vote if you fail to sign your proxy card properly.

1. Individual Accounts: Sign your name exactly as it appears in the registration on the proxy card.

2. Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to the name shown in the registration on the proxy card.

3. All Other Accounts: The capacity of the individual signing the proxy card should be indicated unless it is reflected in the form of registration. For example:

Registration | Valid Signature | |

Corporate Accounts: | ||

(1) ABC Corp. | ABC Corp. John Doe, Treasurer | |

(2) ABC Corp. | John Doe, Treasurer | |

(3) ABC Corp. c/o John Doe, Treasurer | John Doe | |

(4) ABC Corp. Profit Sharing Plan | John Doe, Trustee | |

Partnership Accounts | ||

(1) The XYZ Partnership | Jane B. Smith, Partner | |

(2) Smith and Jones, Limited Partnership | Jane B. Smith, General Partner | |

Trust Accounts | ||

(1) ABC Trust Account | Jane B. Doe, Trustee | |

(2) Jane B. Doe, Trustee u/t/d 12/28/78 | Jane B. Doe | |

Custodial or Estate Accounts | ||

(1) John B. Smith, Cust. f/b/o John B. Smith Jr. UGMA/UTMA | John B. Smith | |

(2) Estate of John B. Smith | John B. Smith, Jr., Executor | |

Table of Contents

IMPORTANT INFORMATION

FOR SHAREHOLDERS OF

DWS MONEY FUNDS—DWS GOVERNMENT & AGENCY MONEY FUND AND INVESTORS CASH TRUST—GOVERNMENT & AGENCY SECURITIES PORTFOLIO

This document contains a combined Prospectus/Proxy Statement and a proxy card. A proxy card is, in essence, a ballot. When you vote your proxy, it tells us how to vote on your behalf on an important issue relating to your fund. If you complete and sign the proxy card (or tell us how you want to vote by voting by telephone or through the Internet), we’ll vote it exactly as you tell us. If you simply sign the proxy card, we’ll vote it in accordance with the Trustees’ recommendation on the proposal applicable to your Fund.

We urge you to review the Prospectus/Proxy Statement carefully, and either fill out your proxy card and return it to us by mail, vote by telephone or record your voting instructions through the Internet. You may receive more than one proxy card since several shareholder meetings are being held as part of the broader restructuring program of the DWS fund family. If so, please vote each one. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

We want to know how you would like to vote and welcome your comments. Please take a few minutes to read these materials and return your proxy card to us. If you have any questions, please call Computershare Fund Services, Inc., your fund’s proxy solicitor, at the special toll-free number we have set up for you (866-774-4940) or contact your financial advisor.

Table of Contents

PROSPECTUS/PROXY STATEMENT

[effective date], 2006

Acquisition of the assets of: | By and in exchange for shares of: | |

| DWS Government & Agency Money Fund a series of DWS Money Funds | Government & Agency Securities Portfolio a series of Cash Account Trust | |

222 S. Riverside Plaza | 222 S. Riverside Plaza | |

Chicago, IL 60606 | Chicago, IL 60606 | |

(312)537-7000 | (312)537-7000 | |

Acquisition of the assets of: | By and in exchange for shares of: | |

| Government & Agency Securities Portfolio a series of Investors Cash Trust | Government & Agency Securities Portfolio a series of Cash Account Trust | |

222 S. Riverside Plaza | 222 S. Riverside Plaza | |

Chicago, IL 60606 | Chicago, IL 60606 | |

(312)537-7000 | (312)537-7000 | |

This Prospectus/Proxy Statement is being furnished in connection with the proposed merger of (a) the DWS Government & Agency Money Fund series of DWS Money Funds (“DWS Government Fund”) into the Government & Agency Securities Portfolio series of Cash Account Trust (“CAT Government Fund”), and (b) the Government & Agency Securities Portfolio series of Investors Cash Trust (“ICT Government Fund”) into CAT Government Fund. DWS Government Fund, ICT Government Fund and CAT Government Fund are referred to herein collectively as the “Funds,” and each is referred to herein individually as a “Fund.” DWS Government Fund and ICT Government Fund are also referred to herein collectively as the “Acquired Funds,” and each is referred to herein individually as an “Acquired Fund.”

The Trustees of each Acquired Fund are recommending that shareholders approve the transactions contemplated by the Agreements and Plans of Reorganization (as described below in Part IV and the form of which is attached hereto as Exhibit A), which we refer to as the merger of your Fund into CAT Government Fund.

As a result of the mergers, each shareholder of the Acquired Funds will receive shares of CAT Government Fund equal in number to such shareholder’s Acquired Fund shares as of the Valuation Time (as defined below on page [19]). Shareholders of each Acquired Fund will vote separately on the merger of their Fund into CAT Government Fund, with each merger being separate and distinct from the other. Neither merger is contingent upon the completion of the merger of the other Fund into CAT Government Fund.

1

Table of Contents

CAT Government Fund is comprised of eight classes of shares, including three new share classes, which were created to facilitate the mergers. Shareholders of the Acquired Funds will hold shares with a net asset value of $1.00 per share of the following newly created classes of CAT Government Fund after the mergers:

Acquired Fund/Class | CAT Government Fund Class | |

DWS Government Fund | DWS Government & Agency Money Fund shares | |

ICT Government Fund—DWS Government Cash Institutional Shares | DWS Government Cash Institutional Shares | |

ICT Government Fund—Service Shares | DWS Government Cash Institutional Shares | |

ICT Government Fund—Government Cash Managed Shares | Government Cash Managed Shares | |

Proposal | ||||

Fund | Approval of Proposed Merger | Approval of Proposed Merger | ||

DWS Government Fund | ü | |||

ICT Government Fund | ü | |||

This Prospectus/Proxy Statement is being mailed on or about [ ], 2006. It explains concisely what you should know before voting on the matters described herein or investing in CAT Government Fund, a diversified series of Cash Account Trust, an open-end management investment company. Please read it carefully and keep it for future reference.

The securities offered by this Prospectus/Proxy Statement have not been approved or disapproved by the Securities and Exchange Commission (the “SEC”), nor has the SEC passed upon the accuracy or adequacy of this Prospectus/Proxy Statement. Any representation to the contrary is a criminal offense.

The following documents have been filed with SEC and are incorporated into this Prospectus/Proxy Statement by reference:

| (i) | the prospectuses of CAT Government Fund dated [August 1], 2006, as supplemented from time to time, for DWS Government & Agency Money Fund shares, DWS Government Cash Institutional Shares and Government Cash Managed Shares (each a “CAT Government Fund Prospectus”), copies of which are included with this Prospectus/Proxy Statement; |

| (ii) | the prospectus of DWS Government Fund dated December 1, 2005, as supplemented from time to time; |

| (iii) | the prospectuses of ICT Government Fund dated [August 1], 2006, as supplemented from time to time, for Service Shares, DWS Government Cash Institutional Shares and Government Cash Managed Shares; |

| (iv) | the statement of additional information of DWS Government Fund dated December 1, 2005, as supplemented from time to time; |

| (v) | the statement of additional information of ICT Government Fund dated [August 1], 2006, as supplemented from time to time, for Service Shares and |

2

Table of Contents

the combined statement of additional information of ICT Government Fund dated [August 1], 2006, as supplemented from time to time, for DWS Government Cash Institutional Shares and Government Cash Managed Shares; |

| (vi) | the statement of additional information relating to the proposed mergers, dated [ ], 2006 (the “Merger SAI”); and |

| (vii) | the audited financial statements and related report of the Independent Registered Public Accounting Firm for DWS Government Fund contained in the Annual Report for the fiscal year ended July 31, 2005, and the unaudited financial statements contained in the Semi-annual Report for the six-month period ended January 31, 2006. |

| (viii) | the audited financial statements and related report of the Independent Registered Public Accounting Firm for ICT Government Fund contained in the Annual Reports for Service Shares, DWS Government Cash Institutional Shares and Government Cash Managed Shares for the fiscal year ended March 31, 2006. |

There is no financial information available for the three classes of CAT Government Fund created to facilitate the mergers as of the date of this Prospectus/Proxy Statement. Such classes will commence operation as of the effective date of the mergers.

Shareholders may obtain free copies of the foregoing documents for a Fund, request other information about a Fund, or make shareholder inquiries, by contacting their financial advisor or by calling the corresponding Fund at 1-800-621-1048 (for DWS Government & Agency Money Fund shares); 1-800-231-8568 (for Service Shares) and 1-800-537-3177 (for DWS Government Cash Institutional Shares and Government Cash Managed Shares).

Shares of CAT Government Fund are not bank deposits nor are they guaranteed or insured by the Federal Deposit Insurance Corporation, or any other government agency, and involve risk, including the possible loss of the principal amount invested. There can be no assurance that the Fund will be able to maintain a stable net asset value of $1.00 per share.

This document is designed to give you the information you need to vote on the merger of your Fund. Much of the information is required disclosure under rules of the SEC; some of it is technical. If there is anything you don’t understand, please contact Computershare Fund Services, your Fund’s proxy solicitor, at (866) 774-4940, or contact your financial advisor.

The Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and in accordance therewith file reports and other information with the SEC. You may review and copy information about the Funds, including each Fund’s prospectus(es) and statement(s) of additional information, at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C. 20549. You may call the SEC at 1-800-SEC-0330 for information about the operation of the public reference room. You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549-0102. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

3

Table of Contents

The responses to the questions that follow provide an overview of key points typically of concern to shareholders considering a proposed merger between mutual funds. These responses are qualified in their entirety by the remainder of this Prospectus/Proxy Statement, which you should read carefully because it contains additional information and further details regarding the proposed merger of your Fund.

| 1. | What is being proposed? |

The Trustees of each Acquired Fund are recommending that shareholders approve the transactions contemplated by the Agreements and Plans of Reorganization (as described below in Part IV and the form of which is attached hereto as Exhibit A), which we refer to as the “merger” of your Fund into CAT Government Fund.

If the merger is approved by shareholders of an Acquired Fund, all of the assets of the Acquired Fund will be transferred to CAT Government Fund solely in exchange for the issuance and delivery to the Acquired Fund of the class or classes of shares of CAT Government Fund identified in the Agreement and Plan of Reorganization (“Merger Shares”) equal in number to the outstanding shares of the Acquired Fund and for the assumption by CAT Government Fund of all liabilities of the Acquired Fund. Immediately following the transfer, the Merger Shares received by the Acquired Funds will be distributed pro rata, on a tax-free basis for federal income tax purposes, to shareholders of record.

| 2. | What will happen to my shares as a result of the merger? |

CAT Government Fund is comprised of eight classes of shares, including three new share classes, which were created to facilitate the mergers. Acquired Fund shareholders will hold shares of the following newly-created classes of CAT Government Fund after the mergers:

Acquired Fund/Class | CAT Government Fund Class | |

DWS Government Fund | DWS Government & Agency Money Fund shares (“CAT Money Fund Shares”) | |

ICT Government Fund—DWS Government Cash Institutional Shares (“ICT Institutional Shares”) | DWS Government Cash Institutional Shares (“CAT Institutional Shares”) | |

ICT Government Fund—Service Shares (“ICT Service Shares”) | CAT Institutional Shares | |

ICT Government Fund—Government Cash Managed Shares (“ICT Managed Shares”) | Government Cash Managed Shares (“CAT Managed Shares”) | |

| 3. | Why is the merger being proposed and why have the Trustees of my Fund recommended that I approve the merger? |

The proposed mergers are part of a program initiated by Deutsche Asset Management (or “DeAM” as defined below on p. [14]) to reorganize and restructure the money market funds in the DWS family of funds. The program is designed to enable

4

Table of Contents

DeAM to: (1) eliminate redundancies within the DWS money market funds by reorganizing and combining certain funds; and (2) focus its investment resources on a core set of money market funds that best meet investor needs.

DeAM believes that the mergers offer shareholders:

| • | A similar investment opportunity in a larger fund with the opportunity to achieve greater economies of scale and a lower expense ratio; and |

| • | A portfolio with the possibility of higher yields generated through more efficient execution and greater stability of assets. |

In determining whether to recommend that shareholders of the Acquired Funds approve the merger of their Fund into CAT Government Fund, the Trustees of each Fund considered, among others, the following factors:

| • | That the investment objectives, policies, restrictions and strategies of the Acquired Funds are similar to the investment objective, policies, restrictions and strategies of CAT Government Fund; |

| • | That shareholders of the Acquired Funds may benefit from a lower total fund operating expense ratio; |

| • | That Deutsche Investment Management Americas Inc. (“DeIM”), the investment adviser to CAT Government Fund, has agreed to cap the total operating expense ratios of each class of Merger Shares for at least three years following the mergers at levels equal to or lower than the current total operating expense ratios or current expense cap of the class of Acquired Fund shares for which they will be exchanged; and |

| • | That DeAM agreed to pay all costs associated with the mergers. |

The Trustees of your Fund concluded with respect to the proposed merger of your Fund into CAT Government Fund that: (1) the merger is in the best interests of the Fund, and (2) the interests of the existing shareholders of the Fund will not be diluted as a result of the merger. Accordingly, the Trustees of your Fund unanimously recommend that shareholders approve the Agreement and Plan of Reorganization (as defined below) and the merger as contemplated thereby.

| 4. | How do the investment goals, policies and restrictions of the Funds compare? |

The investment objective, policies and restrictions for each Acquired Fund and CAT Government Fund are substantially similar. DWS Government Fund seeks maximum current income to the extent consistent with stability of principal. ICT Government Fund and CAT Government Fund seek to provide maximum current income consistent with stability of capital. Each Fund seeks to maintain a stable net asset value of $1.00 per share pursuant to Rule 2a-7. Each Fund pursues its objective by investing exclusively in securities of the U.S. government and its agencies and instrumentalities.

As of April 30, 2006, the weighted average maturity for DWS Government Fund, ICT Government Fund and CAT Government Fund was days, days and days, respectively.

A complete list of each Fund’s portfolio holdings is posted on www.dws-scudder.com as of the month-end on or after the last day of the following month. This posted information generally remains accessible at least until the date on which a Fund files its

5

Table of Contents

Form N-CSR or N-Q with the SEC for the period that includes the date as of which the posted information is current. In addition, each Fund’s top ten holdings and other information about the Fund is posted on www.dws-scudder.com as of the calendar quarter-end on or after the 15th day following quarter-end. Each Fund’s statement of additional information includes a description of the Fund’s policies and procedures with respect to the disclosure of the Fund’s portfolio holdings.

| 5. | How do the management fees and expense ratios of the Funds compare, and what are they estimated to be following the mergers? |

The following table compares the annual management fee schedules of the Funds. Because DeIM has agreed to reduce its management fee for CAT Government Fund if the merger with ICT Government Fund is approved, the table reflects the management fee that shareholders of CAT Government Fund will pay assuming the merger with ICT Government Fund is consummated. The management fee for CAT Government Fund may be higher than shown if only the merger with DWS Government Fund is consummated; however, DWS Government Fund shareholders will still benefit from a lower management fee.

DWS Government Fund(1) | ICT Government Fund | CAT Government Fund | ||||||||

Combined Average Daily | Management Fee | Average Daily | Management Fee | Average Daily | Management Fee | |||||

| First $215 million | 0.500% | All | 0.150% | All | 0.150% | |||||

| Next $335 million | 0.375% | |||||||||

| Next $250 million | 0.300% | |||||||||

| Next $800 million | 0.250% | |||||||||

| Next $800 million | 0.240% | |||||||||

| Next $800 million | 0.230% | |||||||||

| Amount over $3.2 billion | 0.220% | |||||||||

| (1) | The management fee for each series of DWS Money Funds, including DWS Government Fund, is computed based on the combined average daily net assets of all series of DWS Money Funds and allocated to such series based upon the relative net assets of each series. |

| (2) | If the merger with ICT Government Fund is approved, DeIM has agreed to reduce its management fee such that after allocation of the fee to each series of Cash Account Trust the amount payable by CAT Government Fund is limited to 0.150% of the average daily net assets of CAT Government Fund. If the merger with ICT Government Fund is not approved, the annual management fee schedule for CAT Government Fund will be 0.22% of the first $500 million of combined average daily net assets of each series of Cash Account Trust, 0.20% of the next $500 million of combined assets, 0.175% of the next $1 billion of combined assets, 0.16% of the next $1 billion of combined assets and 0.15% of combined assets over $3 billion. The management fee will be allocated to CAT Government Fund based upon the relative net assets of CAT Government Fund. |

The following table summarizes the expenses that each Fund incurred during the year ended January 31, 2006, and the estimated annual expense ratios of the newly created classes of CAT Government Fund. The Funds are no-load funds, meaning no sales charges or other shareholder fees are paid directly from your investment. However, the Funds do have annual operating expenses, and as a shareholder you pay them indirectly. See the Annual Fund Operating Expenses table below for more information on these expenses.

6

Table of Contents

As shown below, the mergers are expected to result in the same or lower management fee ratio and a lower total expense ratio for shareholders of each Acquired Fund. However, there can be no assurance that the merger of your Fund will result in expense savings.

Annual Fund Operating Expenses

(expenses that are deducted from Fund assets)

| Management Fee | Distribution/ Service (12b-1) Fee | Other Expenses(1) | Total Annual Fund Operating Expenses | Less Expense Waiver/ Reimbursements | Net Annual Fund Operating Expenses | |||||||||||||

DWS Government Fund | 0.26% | None | 0.11% | 0.44% | — | (2) | 0.44% | |||||||||||

ICT Government Fund | ||||||||||||||||||

ICT Service Shares | 0.15 | % | None | 0.11 | % | 0.26 | % | 0.01 | %(3) | 0.25 | % | |||||||

ICT Institutional Shares | 0.15 | % | None | 0.08 | % | 0.23 | % | — | 0.23 | % | ||||||||

ICT Managed Shares | 0.15 | % | 0.15 | % | 0.18 | % | 0.43 | % | — | 0.46 | % | |||||||

CAT Government Fund | ||||||||||||||||||

CAT Money Fund Shares(4) | 0.15 | %(5) | None | 0.13 | % | 0.28 | % | — | (6) | 0.28 | % | |||||||

CAT Institutional Shares(4) | 0.15 | %(5) | None | 0.05 | % | 0.20 | % | — | (6) | 0.20 | % | |||||||

CAT Managed Shares(4) | 0.15 | %(5) | 0.15 | % | 0.13 | % | 0.43 | % | — | (6) | 0.43 | % |

| (1) | Includes costs of shareholder services, custody and similar expenses, which may vary with Fund size and other factors. |

| (2) | Through November 30, 2008, DeIM has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of DWS Government Fund to the extent necessary to maintain DWS Government Fund’s total operating expenses at 0.45%, excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest, and trustee and trustee counsel fees. |

| (3) | Through July 31, 2007, DeIM has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of ICT Service Shares to the extent necessary to maintain ICT Service Shares’ total operating expenses at 0.25%, excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest, and trustee and trustee counsel fees. |

| (4) | The Annual Fund Operating Expenses are estimated since no CAT Money Fund Shares, CAT Institutional Shares and CAT Managed Shares were issued as of CAT Government Fund’s fiscal year end. |

| (5) | Reflects the management fee reduction that will be effective upon consummation of the merger of ICT Government Fund into CAT Government Fund. If the merger with ICT Government Fund is approved, DeIM has agreed to reduce its management fee such that after allocation of the fee to each series of Cash Account Trust the amount payable by CAT Government Fund is limited to 0.150% of the average daily net assets of CAT Government Fund. If the merger with ICT Government Fund is not approved, the annual management fee schedule for CAT Government Fund will be 0.22% of the first $500 million of combined average daily net assets of each series of Cash Account Trust, 0.20% of the next $500 million of combined assets, 0.175% of the next $1 billion of combined assets, 0.16% of the next $1 billion of combined assets and 0.15% of combined assets over $3 billion. The management fee will be allocated to CAT Government Fund based upon the relative net assets of CAT Government Fund. If only the merger with DWS Government Fund is approved, based on pro forma asset size, the management fee for CAT Government Fund is expected to be [0.16%] of the average daily net assets of the combined fund. |

7

Table of Contents

| (6) | Contingent upon effectuation of the merger, through , 2009, DeIM has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of the combined fund to the extent necessary to maintain the combined fund’s total operating expenses at an annual rate of 0.45%, 0.24% and 0.46% for CAT Money Fund Shares, CAT Institutional Shares and CAT Managed Shares, respectively, excluding certain expenses such as extraordinary expenses, taxes, brokerage and interest. |

The tables are provided to help you understand your share of the operating expenses that each Fund incurs and that DeAM expects the combined fund to incur in the first year following the mergers.

Examples

The following examples translate the expenses shown in the preceding table into dollar amounts. By doing this, you can more easily compare the costs of investing in the Funds. The examples make certain assumptions. They assume that you invest $10,000 in a Fund for the time periods shown and reinvest all dividends and distributions. They also assume a 5% return on your investment each year, that a Fund’s operating expenses remain the same. The examples are hypothetical; your actual costs and returns may be higher or lower.

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

DWS Government Fund | $ | $ | $ | $ | ||||||||

ICT Government Fund | ||||||||||||

ICT Service Shares | $ | $ | $ | $ | ||||||||

ICT Institutional Shares | $ | $ | $ | $ | ||||||||

ICT Managed Shares | $ | $ | $ | $ | ||||||||

CAT Government Fund | ||||||||||||

CAT Money Fund Shares | $ | $ | $ | $ | ||||||||

CAT Institutional Shares | $ | $ | $ | $ | ||||||||

CAT Managed Shares | $ | $ | $ | $ | ||||||||

| (1) | [Includes one year of capped expenses in the “1 Year” period and three years of capped expenses in the “3 Years,” “5 Years,” and “10 Years” periods.] |

| 6. | What are the federal income tax consequences of the proposed merger? |

For federal income tax purposes, no gain or loss is expected to be recognized by an Acquired Fund or its shareholders as a direct result of the merger into CAT Government Fund. For a discussion of taxes that you may incur indirectly as a result of the merger of your Fund (e.g., due to differences in net investment income), please see “Information about the Proposed Mergers—Federal Income Tax Consequences” below.

| 7. | Are the dividend policies of the Funds the same? |

Each Fund declares dividends representing substantially all net income daily and pays distributions monthly. The cutoff time for wire transfer purchases to receive that day’s dividend is 4:00 p.m. Eastern time for CAT Government Fund and ICT

8

Table of Contents

Government Fund. DWS Government Fund has a 2:00 p.m. cutoff time to receive same day dividends. The cut-off time for CAT Government Fund will apply following the mergers.

| 8. | Do the procedures for purchasing, redeeming and exchanging shares of the Funds differ? |

No. The procedures for purchasing and redeeming shares of a particular class of each Fund, and for exchanging shares, if applicable, of a particular class of each Fund for shares of other DWS funds, are substantially similar.

Orders received by the Funds are effected only on days when the New York Stock Exchange (“NYSE”) is open for trading. Purchases and redemptions of shares of each Fund are made at the Fund’s net asset value (“NAV”) per share. DWS Government Fund calculates its share price three times every business day, first at 12 p.m. Eastern time, then at 2 p.m. Eastern time and again as of the close of regular trading on the NYSE (typically 4 p.m. Eastern time, but sometimes earlier, as in the case of scheduled half-day trading or unscheduled suspensions of trading). ICT Government Fund and CAT Government Fund calculate their share price three times every business day, first at 2 p.m. Eastern time then at 4 p.m. Eastern time and again at 5 p.m. Eastern time. The NAV calculation times for CAT Government Fund will apply following the mergers. You can place an order to buy or sell shares at any time. The NAV of each Fund is calculated by dividing the value of total assets of the Fund, minus all liabilities, by the total number of the outstanding shares. Each Fund seeks to maintain a stable $1.00 share price.

For more information on each Fund’s purchase, redemption and exchange policies, see the Fund’s applicable prospectus(es).

| 9. | How will I be notified of the outcome of the merger of my Fund? |

If the proposed merger involving your Fund is approved by shareholders, you will receive confirmation after the merger is completed, indicating your new account number and the number of shares you are receiving, which will be equal to the number of shares you own. Otherwise, you will be notified in the next shareholder report of your Fund.

| 10. | Will the number of shares I own change? |

No. You will receive shares equal in number to the shares owned as of the merger date.

| 11. | What percentage of shareholders’ votes is required to approve each merger? |

Approval of each merger will require the affirmative vote of shareholders of the applicable Acquired Fund entitled to vote more than fifty percent (50%) of the votes entitled to be cast on the matter at the Meeting.

The Trustees of your Fund believe that the proposed merger of your Fund is in the best interests of the Fund. Accordingly, the Trustees unanimously recommend that shareholders vote FOR approval of the proposed merger of their Fund.

9

Table of Contents

II. INVESTMENT STRATEGIES AND RISK FACTORS

What are the main investment strategies and related risks of CAT Government Fund, and how do they compare with those of my Fund?

Investment Strategies. The investment objective, policies and restrictions for DWS Government Fund, ICT Government Fund and CAT Government Fund are substantially similar. DWS Government Fund seeks maximum current income to the extent consistent with stability of principal. ICT Government Fund and CAT Government Fund seek to provide maximum current income consistent with stability of capital. Each Fund seeks to maintain a stable net asset value of $1.00 per share pursuant to Rule 2a-7.

Each Fund pursues its goal by investing exclusively in short-term securities that are issued or guaranteed by the U.S. Government or its agencies or instrumentalities, and repurchase agreements backed by obligations of such securities.

While the Funds’ advisor gives priority to earning income and maintaining the value of each Fund’s principal at $1.00 per share, all money market instruments, including U.S. Government obligations, can change in value when interest rates change or an issuer’s creditworthiness changes.

Each Fund may invest in floating and variable rate instruments (obligations that do not bear interest at fixed rates). Each Fund maintains a dollar-weighted average maturity of 90 days or less. Each Fund’s securities are denominated in U.S. dollars. DWS Government Fund and ICT Government Fund’s securities have remaining maturities of 397 days (about 13 months) or less at the time of purchase while CAT Government Fund’s securities have remaining maturities of 12 months or less at the time of purchase. Each Fund also may invest in securities that have features that reduce their maturities to 397 days or less or 12 months or less, respectively, at the time of purchase. Each Fund is managed in accordance with Rule 2a-7 under the 1940 Act.

Each Fund may invest up to 10% of its total assets in other money market mutual funds in accordance with applicable regulations.

Working in consultation with a credit team, the portfolio screens potential securities and develop a list of those that the Funds may buy. The managers, looking for attractive yield and weighing considerations such as credit quality, economic outlooks and possible interest rate movements, then decide which securities on this list to buy. The managers may adjust each Fund’s exposure to interest rate risk, typically seeking to take advantage of possible rises in interest rates and to preserve yield when interest rates appear likely to fall.

DeAM believes that CAT Government Fund should provide a comparable investment opportunity for shareholders of each Acquired Fund.

For a more detailed description of the investment techniques used by each Fund, please see the applicable Fund’s prospectus(es) and SAI(s).

Primary Risks. As with any investment, you may lose money by investing in CAT Government Fund. There are several risk factors summarized below that could reduce

10

Table of Contents

the yield from CAT Government Fund or make it perform less well than other investments. The risks of an investment in CAT Government Fund are the same as the risks of an investment in your current Fund. More detailed descriptions of the risks associated with an investment in CAT Government Fund can be found in the current prospectuses and statements of additional information of CAT Government Fund.

Interest Rate Risk. Money market instruments, like all debt securities, face the risk that the securities will decline in value because of changes in interest rates. Generally, investments subject to interest rate risk will decrease in value when interest rates rise and increase in value when interest rates decline. To minimize such price fluctuations, CAT Government Fund limits the dollar-weighted average maturity of the securities held by CAT Government Fund to 90 days or less. Generally, the price of short-term investments fluctuates less than longer-term bonds. Income earned on floating or variable rate securities may vary as interest rates decrease or increase. Because of CAT Government Fund’s high credit standards, its yield may be lower than the yields of money funds that do not invest primarily in U.S. Government and agency securities.

Credit Risk. If a portfolio security declines in credit quality or goes into default, it could hurt CAT Government Fund’s performance. Additionally, some securities issued by U.S. Government agencies or instrumentalities are supported only by the credit of that agency or instrumentality. There is no guarantee that the U.S. Government will provide support to such agencies or instrumentalities and such securities may involve risk of loss of principal and interest. Other securities are backed by the full faith and credit of the U.S. Government.

Market Risk. Although individual securities may outperform their market, the entire market may decline as a result of rising interest rates, regulatory developments or deteriorating economic conditions.

Security Selection Risk. While CAT Government Fund invests in short-term securities, which by their nature are relatively stable investments, the risk remains that the securities in which CAT Government Fund invests will not perform as expected. This could cause CAT Government Fund’s returns to lag behind those of similar money market funds.

Repurchase Agreement Risk. A repurchase agreement exposes the CAT Government Fund to the risk that the party that sells the securities may default on its obligation to repurchase them. In this circumstance, CAT Government Fund can lose money because:

| • | it cannot sell the securities at the agreed-upon time and price; or |

| • | the securities lose value before they can be sold. |

CAT Government Fund seeks to reduce this risk by monitoring the creditworthiness of the sellers with whom it enters into repurchase agreements. CAT Government Fund also monitors the value of the securities to ensure that they are at least equal to the total amount of the repurchase obligations, including interest and accrued interest.

An investment in CAT Government Fund is not insured or guaranteed by the FDIC or any other government agency. Although CAT Government Fund seeks to preserve the value of an investment at $1.00 per share, this share price isn’t guaranteed and you could lose money by investing in CAT Government Fund.

11

Table of Contents

Performance Information. The following information provides some indication of the risks of investing in the Funds. The bar charts show year-to-year changes in the performance of CAT Premier Money Market Shares, DWS Government Fund shares and ICT Service Shares. The table following the charts compares each Fund’s performance. Because the newly created classes of CAT Government Fund will not commence operations until the effective date of the mergers, the performance figures shown for CAT Government Fund reflect the historical performance of CAT Government Fund’s Premier Money Market Shares. The newly created classes of CAT Government Fund would be expected to have substantially similar gross annual returns (before the effect of expenses) as CAT Premier Money Market Shares, as the shares will be invested in the same portfolio of securities, and the returns of the classes net of expenses would be expected to differ primarily due to the different expenses of the classes.

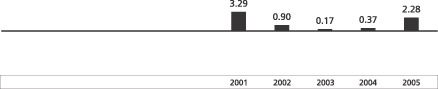

Calendar Year Total Returns (%)

CAT Government Fund—CAT Premier Money Market Shares

Annual Total Returns (%) as of 12/31 each year

2006 total return as of June 30: 1.84%

For the periods included in the bar chart:

Best Quarter: 1.24%, Q1 2001 Worst Quarter: 0.02%, Q4 2003

DWS Government Fund

Annual Total Returns (%) as of 12/31 each year

2006 total return as of June 30: 2.14%

For the periods included in the bar chart:

Best Quarter: 1.58%, Q3 2000 Worst Quarter: 0.16%, Q1 2004

12

Table of Contents

ICT Government Fund—ICT Service Shares

Annual Total Returns (%) as of 12/31 each year

2006 total return as of June 30: 2.24%

For the periods included in the bar chart:

Best Quarter: 1.62%, Q4 2000 Worst Quarter: 0.21%, Q1 2004

Average Annual Total Returns

(for periods ended December 31, 2005)

| Past 1 year | Past 5 years | Past 10 years/ Since Inception | |||||||

CAT Government Fund | |||||||||

CAT Premier Money Market Shares | 2.28 | % | 1.39 | % | 1.99 | %(1) | |||

DWS Government Fund | 2.85 | % | 1.96 | % | 3.63 | % | |||

ICT Government Fund | |||||||||

ICT Service Shares | 3.06 | % | 2.15 | % | 3.80 | % | |||

ICT Institutional Shares | 3.09 | % | 2.20 | % | 2.93 | %(2) | |||

ICT Managed Shares | 2.85 | % | 1.95 | % | 2.67 | %(2) | |||

| (1) | Inception date for CAT Premier Money Market Shares was March 1, 2000. |

| (2) | Inception date for ICT Institutional Shares and ICT Managed Shares was November 17, 1999. |

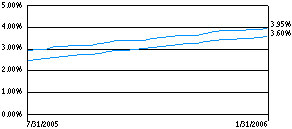

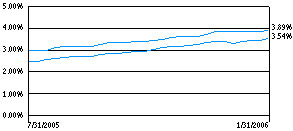

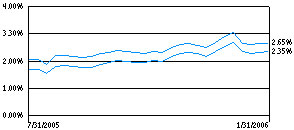

As of December 31, 2005, DWS Government Fund’s 7-day yield was 3.87%, ICT Government Fund’s 7-day yield was 3.32% for ICT Service Shares, 4.07% for ICT Institutional Shares and 4.06% for ICT Managed Shares and CAT Government Fund’s 7-day yield was 3.32% for CAT Premier Money Market Shares. The 7-day yield, which is often referred to as the “current yield,” is the income generated by a fund over a seven-day period. This amount is then annualized, which means that we assume a fund generates the same income every week for a year. The “total return” of a fund is the change in the value of an investment in the fund over a given period. Average annual returns are calculated by averaging the year-by-year returns of a fund over a given period.

Current performance information may be higher or lower than the performance data quoted above. For more recent performance information or to learn the current 7-day yield of the Funds, call your financial advisor or 1-800-621-1048 or visit the Funds’ website at www.dws-scudder.com.

13

Table of Contents

III. OTHER COMPARISONS BETWEEN THE FUNDS

Advisor and Portfolio Managers. DeIM is the investment advisor for each Fund. Under the supervision of the Board of Trustees of each trust, DeIM, with headquarters at 345 Park Avenue, New York, New York 10154, makes each Fund’s investment decisions, buys and sells securities for each Fund and conducts research that leads to these purchase and sale decisions. DeIM is also responsible for selecting brokers and dealers and for negotiating brokerage commissions and dealer charges. DeIM is part of DeAM and an indirect wholly-owned subsidiary of Deutsche Bank AG. DeAM, or Deutsche Asset Management, is the marketing name in the United States for the asset management activities of, among others, Deutsche Bank AG, DeIM, Deutsche Asset Management, Inc., Deutsche Bank Trust Company Americas and DWS Trust Company. Deutsche Bank AG is a major global banking institution that is engaged in a wide range of financial services, including investment management, mutual fund, retail, private and commercial banking, investment banking and insurance.

A group of investment professionals is responsible for the day-to-day management of each Fund. These investment professionals have a broad range of experience in managing money market funds.

Distribution and Service Fees. Pursuant to separate but substantially identical underwriting agreements, DWS Scudder Distributors, Inc. (“DWS-SDI”), 222 South Riverside Plaza, Chicago, Illinois 60606, an affiliate of the DeIM, is the principal underwriter, distributor and administrator for shares of each Fund and acts as agent of the Funds in the continuous sale of their shares.

CAT Government Fund has adopted a service plan on behalf of the CAT Managed Shares in accordance with Rule 12b-1 under the 1940 Act that is substantially the same as the Rule 12b-1 service plan currently in effect for ICT Managed Shares. Plans under Rule 12b-1 allow a fund to pay distribution and/or service fees for the sale and distribution of its shares. Because these fees are paid out of a fund’s assets on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than other types of investments.

Pursuant to a Shareholder Services Agreement with CAT Government Fund, which is substantially the same as the Shareholder Services Agreement with ICT Government Fund, DWS-SDI will receive a service fee of up to 0.15% of average daily net assets per year with respect to CAT Managed Shares. DWS-SDI will use the fee to compensate financial services firms for providing personal services and maintaining accounts for their customers that hold CAT Managed Shares, and may retain any portion of the fee not paid to such firms to compensate itself for administrative functions performed for such shares. All amounts are payable monthly and are based on the average daily net assets of the Fund attributable to CAT Government Fund.

Trustees and Officers. The Trustees overseeing DWS Government Fund, a series of DWS Money Funds, and ICT Government Fund, a series of Investors Cash Trust, are the same as those who oversee CAT Government Fund, a series of Cash Account Trust. The Trustees are Shirley D. Peterson (Chair), John W. Ballantine, Donald L. Dunaway, James R. Edgar, Paul K. Freeman, Robert B. Hoffman, William McClayton and Robert H. Wadsworth.

14

Table of Contents

The officers of DWS Government Fund and ICT Government Fund are the same as those of CAT Government Fund. The Officers are Michael Clark, President, Philip J. Collora, Vice President and Assistant Secretary, Paul H. Schubert, Chief Financial Officer and Treasurer, John Millette, Secretary, Patricia DeFilippis, Assistant Secretary, Elisa D. Metzger, Assistant Secretary, Caroline Pearson, Assistant Secretary, Scott M. McHugh, Assistant Treasurer, Kathleen Sullivan D’Eramo, Assistant Treasurer, John Robbins, Anti-Money Laundering Compliance Officer and Philip Gallo, Chief Compliance Officer.

Independent Registered Public Accounting Firm. Each Fund’s independent registered public accounting firm is Ernst & Young LLP.

Charter Documents. DWS Government Fund is a series of DWS Money Funds, a Massachusetts business trust governed by Massachusetts law. ICT Government Fund is a series of Investors Cash Trust, a Massachusetts business trust governed by Massachusetts law. CAT Government Fund is a series of Cash Account Trust, a Massachusetts business trust governed by Massachusetts law. DWS Government Fund is governed by an Amended and Restated Agreement and Declaration of Trust dated January 20, 1998, as amended from time to time. ICT Government Fund is governed by an Amended and Restated Agreement and Declaration of Trust dated March 9, 1990, as amended from time to time. CAT Government Fund is governed by an Amended and Restated Agreement and Declaration of Trust dated March 17, 1990, as amended from time to time. Each Declaration of Trust is referred to herein as a “Charter Document”. The Charter Documents are substantially identical to one another. Additional information about each Charter Document is provided below.

Shares. Under each Fund’s Charter Document, shares of the Fund do not entitle the holder thereof to any conversion, exchange, preemption or appraisal rights. Shares of each Fund do entitle the holder to any dividends or distributions declared by the Board Members of the Fund, and if a Fund were liquidated, shareholders of that Fund would receive a proportionate share of the net assets of the Fund. Each Fund has the right to redeem, at the then current net asset value, the shares of any shareholder whose account does not exceed a minimum balance.

Shareholder Meetings and Voting Rights. The Charter Document of each Fund does not require that annual meetings of shareholders be held, but meetings of the shareholders shall be called for the purpose of electing Board Members when required by the Charter Document or to comply with the 1940 Act. The Board Members or such other person or persons as may be specified in the By-Laws of each Fund may call a shareholder meeting if requested in writing by the holders of at least 25% (or at least 10%, if the purpose of the meeting is to vote to remove a Trustee) of the outstanding shares entitled to vote at such meeting. Shares of each Fund entitle their holders to one vote per share, with fractional shares voting proportionally; however, a separate vote will be taken by each Fund or class thereof on matters affecting the Fund or class only, as determined by the Board Members, or when the 1940 Act so requires. For example, a change in a fundamental investment policy for a Fund would be voted upon only by shareholders of that Fund, and adoption of a distribution plan relating to a particular class and requiring shareholder approval would be voted upon only by shareholders of that class. Any Trustee of the Funds may be removed by vote or written consent of fifty percent (50%) of the votes entitled to be cast on the matter. Trustee vacancies may be filled by a majority of the Board Members then in office through written appointment, unless a shareholder vote is required by the 1940 Act. Shares of both Funds have

15

Table of Contents

noncumulative voting rights with respect to the election of Board Members. Each Fund (or any class) may be terminated by a written instrument signed by a majority of its Board Members, or by the affirmative vote of the holders of fifty percent (50%) of the shares of the Fund (or class) outstanding and entitled to vote. Sale, conveyance, or transfer of any assets of the Funds to another trust, partnership, association or corporation organized under the laws of any state of the United States requires the affirmative vote of the shareholders entitled to vote more than fifty percent (50%) of the votes entitled to be cast on the matter. Quorum for a shareholder meeting of any Fund is the presence in person or by proxy of 30% of the shares entitled to vote.

Shareholder Liability. Under Massachusetts law, shareholders of a Massachusetts business trust could, under certain circumstances, be held personally liable for the acts or obligations of a fund. The Charter Document governing each Fund, however, disclaims shareholder liability in connection with the Fund’s property or the acts and obligations of the Fund. Moreover, each Fund’s Charter Document provides for indemnification out of the property of the Fund for all loss and expense of any shareholder held personally liable by reason of being a shareholder of the Fund, and, provides that the Fund may be covered by insurance that the Board Members consider necessary or appropriate.

Amendment of Charter Document. The Charter Document of each Fund may be amended at any time by an instrument in writing signed by a majority of the then Board Members when authorized to do so by vote of shareholders holding more than fifty percent (50%) of the shares of each series entitled to vote. Each Charter Document may also be amended by the Board Members without shareholder consent if the purpose of the amendment is to change the name of the Trust or to supply any omission, cure any ambiguity, or cure, correct or supplement any provision which is deficient or inconsistent with the 1940 Act or the requirements of the Internal Revenue Code of 1986, as amended.

The foregoing a general summary of certain provisions of the Charter Documents governing DWS Money Funds, Investors Cash Trust and Cash Account Trust and is not a complete description of provisions contained in those sources. Shareholders should refer to the provisions of those documents and state law directly for a more thorough description.

IV. INFORMATION ABOUT THE PROPOSED MERGERS

General. The shareholders of each Acquired Fund are being asked to approve a merger between their Fund and CAT Government Fund pursuant to separate Agreements and Plans of Reorganization between each Acquired Fund and CAT Government Fund (the “Agreements”). The form of the Agreements is attached to this Prospectus/Proxy Statement as Exhibit A.

Each merger is structured as a transfer of all of the assets of the Acquired Fund to CAT Government Fund in exchange for the assumption by CAT Government Fund of all liabilities of the Acquired Fund and for the issuance and delivery to the Acquired Fund of Merger Shares equal in number to the outstanding shares of the Acquired Fund as of the Valuation Time.

16

Table of Contents

After receipt of the Merger Shares, each Acquired Fund will distribute the Merger Shares to its shareholders, in proportion to their existing shareholdings, in complete liquidation of such Acquired Fund, and the legal existence of each Acquired Fund will be terminated. Each shareholder of each Acquired Fund will receive Merger Shares equal in number to the shareholder’s Acquired Fund shares at the Valuation Time.

Each Acquired Fund and CAT Government Fund have substantially similar investment objectives, policies, restrictions and strategies. Because of the similarities in the portfolios of each Fund and the short-term characteristics of the portfolio securities, the Acquired Funds do not expect to dispose of securities prior to the merger, except in the ordinary course.

The Trustees of your Fund have voted unanimously to approve the Agreement for your Fund and the proposed merger and to recommend that shareholders also approve the merger. With respect to each merger, the actions contemplated by the Agreements and the related matters described therein will be consummated only if approved by the affirmative vote of shareholders of the Acquired Fund entitled to vote more than fifty percent (50%) of the votes entitled to be cast on the matter.

In the event that a merger does not receive the required shareholder approval, that Fund will continue to be managed as a separate Fund in accordance with its current investment objective and policies, and the Trustees of the Fund may consider such alternatives as may be in the best interests of the Fund. Each merger is separate and distinct from the other and is not contingent upon completion of the other merger.

Background and Trustees’ Considerations Relating to the Proposed Mergers. DeAM first discussed the mergers with the Trustees in December 2005 as a part of an ongoing program initiated by DeAM to restructure its mutual fund lineup. The proposed mergers are designed to enable DeAM to: (1) eliminate redundancies within the DWS money market funds by reorganizing and combining certain funds; and (2) focus its investment resources on a core set of money market funds that best meet investor needs.

DeAM believes that the mergers offer shareholders:

| • | A similar investment opportunity in a larger fund with the opportunity to achieve greater economies of scale and a lower expense ratio; and |

| • | A portfolio with the possibility of higher yields generated through more efficient execution and greater stability of assets. |

The Trustees conducted a thorough review of the potential implications of each merger. They were assisted in this review by their independent legal counsel. The Trustees met on several occasions to review and discuss the mergers, both among themselves and with representatives of DeAM. In the course of their review, the Trustees requested and received substantial information.

On May 10, 2006, the Trustees of each Acquired Fund, all of whom are not “interested persons” (as defined by the 1940 Act) (“Disinterested Trustees”), approved the terms of each merger and recommend that each merger be approved by shareholders.

17

Table of Contents

In determining to recommend that the shareholders of each Acquired Fund approve its merger, the Trustees considered, among others, the factors described below:

| • | The Trustees noted that the estimated operating expense ratios of CAT Money Fund Shares, CAT Institutional Shares and CAT Managed Shares of the combined fund are lower than the expense ratios of shares of DWS Government Fund, ICT Service Shares, ICT Institutional Shares and ICT Managed Shares. The Trustees also considered DeIM’s commitment to cap the operating expenses of the combined fund’s CAT Money Fund Shares, CAT Institutional Shares and CAT Managed Shares for at least three years at a level equal to the current operating expenses or current expense cap of shares of DWS Government Fund, ICT Institutional Shares and ICT Managed Shares, respectively. The Trustees noted the possible economies of scale that might be realized by DeAM in connection with the mergers. |

| • | The Trustees considered that the mergers would not result in the dilution of shareholder interests and that the terms and conditions of the Agreements were fair and reasonable. |

| • | The Trustees noted that the investment objective, policies, restrictions and strategies of each Acquired Fund are similar to the investment objective, policies, restrictions and strategies of CAT Government Fund and that the securities in each Acquired Fund’s portfolio were compatible with the securities in CAT Government Fund’s portfolio. The Trustees also considered that the mergers would permit the shareholders of the Acquired Funds to pursue similar investment goals in a larger fund. |

| • | The Trustees noted that the services available to shareholders of CAT Government Fund were substantially similar to those available to shareholders of the Acquired Funds. |

| • | The Trustees noted that DeAM would bear all expenses associated with the mergers. |

| • | The Trustees noted that DeAM believes the combined fund would be more likely to attract additional assets than the Acquired Funds and enjoy any related economies of scale. |

| • | The Trustees noted that DeIM has agreed to indemnify CAT Government Fund against certain liabilities Cash Account Trust may incur in connection with any litigation or regulatory action related to possible improper market timing or possible improper marketing and sales activity in Cash Account Trust (see Section VI) so that the likelihood that the combined fund would suffer any loss is considered by fund management to be remote. |

| • | The Trustees noted that DeIM has agreed to indemnify the Disinterested Trustees of each Acquired Fund against certain liabilities that such Disinterested Trustees may incur by reason of having served as a Trustee of an Acquired Fund. |

Based on all of the foregoing, the Trustees of each Acquired Fund concluded that the participation of the Fund in the proposed merger with CAT Government Fund would be in the best interests of the Fund and would not dilute the interests of existing shareholders. The Trustees of each Acquired Fund unanimously recommend that shareholders of each Acquired Fund approve the merger of their Fund.

18

Table of Contents

Agreements and Plans of Reorganization. The proposed mergers will be governed by the Agreements, the form of which is attached as Exhibit A. Each Agreement provides that CAT Government Fund will acquire all of the assets of the Acquired Fund solely in exchange for the assumption by CAT Government Fund of all liabilities of the Acquired Fund and for the issuance of Merger Shares equal in number to the shares of the Acquired Fund outstanding as of the Valuation Time. The Merger Shares will be issued on the next full business day (the “Exchange Date”) following the time as of which the Funds’ assets and liabilities are valued for the merger (4:00 p.m. Eastern time, on [October 27], 2006, or such other date and time as may be agreed upon by the parties (the “Valuation Time”)). The following discussion of the Agreements is qualified in its entirety by the full text of each Agreement.

Each Acquired Fund will transfer all of its assets to CAT Government Fund, and in exchange, CAT Government Fund will assume all liabilities of the Acquired Funds and deliver to each Acquired Fund Merger Shares equal in number to the shares of the Acquired Fund outstanding as of the Valuation Time. Immediately following the transfer of assets on the Exchange Date, each Acquired Fund will distribute pro rata to its shareholders of record as of the Valuation Time the Merger Shares received by the Acquired Fund, as follows: (1) shareholders of DWS Government Fund will receive CAT Money Fund Shares; (2) shareholders of ICT Service Shares will receive CAT Institutional Shares; (3) shareholders of ICT Institutional Shares will receive CAT Institutional Shares; and (4) shareholders of ICT Managed Shares will receive CAT Managed Shares. As a result of each proposed merger, each shareholder of the Acquired Funds will receive Merger Shares of the class indicated above equal in number to the Acquired Fund shares surrendered by the shareholder. This distribution will be accomplished by the establishment of accounts on the share records of CAT Government Fund in the name of such Acquired Fund shareholders, each account representing the respective number of Merger Shares of each class due to the respective shareholder. New certificates for Merger Shares will not be issued.

The Trustees of each Fund have determined that the interests of their respective Fund’s shareholders will not be diluted as a result of the transactions contemplated by the Agreements, and the Trustees of each Fund have determined that the proposed merger of their Fund is in the Fund’s best interests.

The consummation of each merger is subject to the conditions set forth in the Agreements. An Agreement may be terminated and a merger abandoned (i) by mutual consent of the parties, (ii) by any party to the Agreement if the merger shall not be consummated by [December 29], 2006, (iii) if any condition set forth in the Agreement has not been fulfilled and has not been waived by the party entitled to its benefits, or (iv) if the net asset value per share of either party to the Agreement calculated using market values deviates by more than 0.3 of 1% from its net asset value per share calculated using amortized cost.

If shareholders of each Acquired Fund approve the merger of their Fund, CAT Government Fund has agreed to identify in writing prior to the Exchange Date any assets of the Acquired Fund that it does not wish to acquire because they are not consistent with the current investment strategy of CAT Government Fund, and the Acquired Fund agrees to dispose of such assets prior to the Exchange Date. CAT Government Fund also agrees to identify in writing prior to the Exchange Date any assets that it would like the Acquired Fund to purchase, consistent with CAT Government Fund’s investment

19

Table of Contents

objective, policies, restrictions and strategies, and the Acquired Fund agrees to purchase such assets with the cash proceeds from the disposition of assets identified by CAT Government Fund. DeIM has represented that it does not expect CAT Government Fund to identify any such assets in either Acquired Fund.

The fees and expenses for each merger and related transactions are estimated to be [$ ] and [$ ] in connection with DWS Government Fund and ICT Government Fund, respectively. All fees and expenses, including legal and accounting expenses, portfolio transfer taxes (if any) and any other expenses incurred in connection with the consummation of each merger and related transactions contemplated by the Agreements, will be borne by DeAM.

Description of the Merger Shares. Merger Shares will be issued to shareholders of each Acquired Fund in accordance with the Agreements as described above. The Merger Shares represent new share classes, which are being created to facilitate the mergers. Each new share class has substantially the same characteristics as its predecessor class. Your Merger Shares will be treated as having been purchased on the date you purchased your Acquired Fund shares and for the price you originally paid. For more information on the characteristics of each class of Merger Shares, please see the CAT Government Fund Prospectuses, copies of which were mailed with this Prospectus/Proxy Statement.

Federal Income Tax Consequences. As a condition to each Fund’s obligation to consummate the reorganization, each Fund will receive a tax opinion from Willkie Farr & Gallagher LLP (which opinion would be based on certain factual representations and certain customary assumptions), to the effect that, on the basis of the existing provisions of the U.S. Internal Revenue Code of 1986, as amended (the “Code”), current administrative rules and court decisions, for federal income tax purposes:

| • | The acquisition by CAT Government Fund of all of the assets of each Acquired Fund solely in exchange for Merger Shares and the assumption by CAT Government Fund of all of the liabilities of each Acquired Fund, followed by the distribution by such Acquired Fund to its shareholders of Merger Shares in complete liquidation of such Acquired Fund, all pursuant to the Agreements, constitutes a reorganization within the meaning of Section 368(a) of the Code, and the Acquired Funds and CAT Government Fund will each be a “party to a reorganization” within the meaning of Section 368(b) of the Code. |

| • | Under Section 361 of the Code, each Acquired Fund will not recognize gain or loss upon the transfer of its assets to CAT Government Fund in exchange for Merger Shares and the assumption of each Acquired Fund’s liabilities by CAT Government Fund, and such Acquired Fund will not recognize gain or loss upon the distribution to its shareholders of the Merger Shares in liquidation of such Acquired Fund. |

| • | Under Section 354 of the Code, shareholders of each Acquired Fund will not recognize gain or loss on the receipt of Merger Shares solely in exchange for such Acquired Fund shares. |

| • | Under Section 358 of the Code, the aggregate basis of the Merger Shares received by each shareholder of the Acquired Funds will be the same as the aggregate basis of the Acquired Fund shares exchanged therefore. |

20

Table of Contents