U.S. Securities and Exchange Commission

Washington, D.C. 20549

FORM 10-K

Annual Report pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934 (Fee required)

For the fiscal year ended December 31, 2007

Commission file number: 0-23090

| | | Carrollton Bancorp | | |

| | (Exact Name of Registrant as Specified in its Charter) | |

| | | | | Maryland | | | | | | 52 1660951 |

| (State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | | | | 344 N. Charles St. | | | | | | |

| | | | | Baltimore, MD | | | | | | 21201 |

| | | | | (Address of principal executive offices) | | | | | | (Zip Code) |

| | | | | (410) 536 4600 | | | | | | |

| | | | | (Registrant’s telephone number, including area code) | | | | | | |

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock,

par value $1.00 per share

(Title of class)

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained in this form, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K o.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer x

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the Common Stock, all of which has voting rights, held by non-affiliates of the registrant upon the closing price of such common equity as of the last business day of the most recently completed second fiscal quarter was approximately $39.0 million. For the purpose of this calculation, directors and executive officers of the registrant are considered affiliates.

At March 20, 2008, the Registrant had 2,635,377 shares of $1.00 par value common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for Annual Meeting of Shareholders to be held on May 13, 2008, are incorporated by reference in Part III of this Form 10-K.

| Part I | | | | | |

| Item 1 — | | Business | | 4 | |

| Item 1A — | | Risk Factors | | 11 | |

| Item 2 — | | Properties | | 14 | |

| Item 3 — | | Legal Proceedings | | 15 | |

| Item 4 — | | Submission of Matters to a Vote of Security Holders | | 15 | |

Part II | | | | | |

| Item 5 — | | Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities | | 16 | |

| Item 6 — | | Selected Financial Data | | 19 | |

| Item 7 — | | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 20 | |

| Item 7A — | | Quantitative and Qualitative Disclosures About Market Risk | | 35 | |

| Item 8 — | | Financial Statements and Supplementary Data | | 36 | |

| Item 9— | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 68 | |

| Item 9A(T) — | | Controls and Procedures | | 68 | |

| Item 9B — | | Other Information | | 68 | |

Part III | | | | | |

| Item 10 — | | Directors, Executive Officers, and Corporate Governance | | 68 | |

| Item 11 — | | Executive Compensation | | 68 | |

| Item 12 — | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 69 | |

| Item 13 — | | Certain Relationships and Related Transactions and Director Independence | | 69 | |

| Item 14 — | | Principal Accountant Fees and Services | | 69 | |

Part IV | | | | | |

| Item 15 — | | Exhibits and Financial Statement Schedules | | 69 | |

| Signatures | | | | 71 | |

| | Forward-looking Statements |

This Annual Report on Form 10-K and certain information incorporated herein by reference contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements included or incorporated by reference in this Annual Report on Form 10-K, other than statements that are purely historical, are forward-looking statements. Statements that include the use of terminology such as “anticipates,” “expects,” “plans”, “believes,” “estimates” and similar expressions also identify forward-looking statements. The forward-looking statements are based on Carrollton Bancorp’s current intent, belief and expectations. Forward-looking statements in this Annual Report on Form 10-K include, but are not limited to:

Part I. Item 3. Legal Proceedings:

Statement regarding the impact on the Company of routine legal proceeding.

Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations:

Statements regarding loan growth in real estate development and construction and commercial loan portfolios in 2008.

Statement regarding 2008 certificate of deposit pricing strategy.

Statement regarding challenges facing management in terms of interest rates, growth in net interest income and overall management of the net interest margin.

Statements regarding volatility in mortgage refinancing activity.

Part III. Item 7A. Quantitative and Qualitative Disclosures About Market Risk:

Statements regarding the Company’s ability to limit exposure to interest rate risk.

Statements regarding factors that influence demand for real estate loans.

Statements regarding future revenue improvements.

Statements regarding the sufficiency of the Company’s allowance for loan losses.

Part IV. Item 8. Note 3. Investments:

Statement regarding anticipated changes in the fair value of securities in relation to market rates.

These statements are not guarantees of future performance and are subject to certain risks and uncertainties that are difficult to predict. Actual results may differ materially from these forward-looking statements because of interest rate fluctuations, a deterioration of economic conditions in the Baltimore/ Washington metropolitan area, a downturn in the real estate market, losses from impaired loans, an increase in nonperforming assets, potential exposure to environmental laws, changes in federal and state bank laws and regulations, the highly competitive nature of the banking industry, a loss of key personnel, changes in accounting standards and other risks described in the Company’s filings with the Securities and Exchange Commission. Existing and prospective investors are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. Carrollton Bancorp undertakes no obligation to update or revise the information contained in this Annual Report whether as a result of new information, future events or circumstances or otherwise. Past results of operations may not be indicative of future results.

General. – Carrollton Bancorp (the “Company”), a bank holding company registered under the Bank Holding Company Act of 1956, as amended, was organized on January 11, 1990, and is headquartered in Baltimore, Maryland. Carrollton Bank (the “Bank”) is a commercial bank and the principal subsidiary of the Company. The Bank was chartered by an act of the General Assembly of Maryland (Chapter 727) approved April 10, 1900. The Bank is engaged in a general commercial and retail banking business and, as of December 31, 2007, had a total of eleven branch locations in Maryland with two branch locations in Baltimore City; three branch locations in Anne Arundel County; five branches in Baltimore County and one branch in Harford County. The Bank’s wholly owned subsidiaries are Carrollton Mortgage Services, Inc. (“CMSI”), which is used primarily to originate and sell residential mortgage loans, Carrollton Financial Services, Inc. (“CFS”), which provides brokerage services, and Mulberry Street LLC (“MSLLC”) which is used to dispose of other real estate owned. Carrollton Community Development Corporation (“CCDC”) is a 96.4% owned subsidiary of the Bank which promotes, develops and improves the housing and economic conditions of people in Maryland, particularly the Metropolitan Baltimore area.

The Bank also operated a network of ATMs in Maryland, Virginia, and West Virginia and sponsors national retailers who accept ATM cards for purchases in various electronic networks. On September 22, 2005, Wal-Mart notified the Bank of its intention to terminate the agreement for the Bank to provide ATM’s at Wal-Mart, Sam’s Club, and Wal-Mart Supercenters in Maryland, Virginia, and West Virginia. The effective date of the termination was January 22, 2006.

The Bank is an independent, community bank that seeks to provide personal attention and professional financial services to its customers while offering virtually all of the banking services of larger competitors. Our customers are primarily individuals and small and medium-sized businesses. The Bank’s business philosophy includes offering informed and courteous service, local and timely decision-making, flexible and reasonable operating procedures and consistently applied credit policies.

The executive offices of the Company and the principal office of the Bank are located at 344 North Charles Street, Baltimore, Maryland 21201, telephone number (410) 536-4600. The Company files quarterly and annual reports with the Securities and Exchange Commission (“SEC”) on forms 10-Q and 10-K, respectively, proxy materials on Schedule 14A and current reports on Form 8-K. The Company makes available, free of charge, all of these reports, as well as any amendments, through the Company’s Internet site as soon as is reasonably practicable after they are filed electronically with the SEC. The address of that site is http://www.carrolltonbank.com. To access the SEC reports, click on “About Us” —“SEC Filings”. The SEC also maintains an internet site that contains reports, proxy materials and information statements at http://sec.gov. In addition, the Company will provide paper copies of filings free of charge upon written request.

Description of Services. – The Bank provides a broad range of consumer and commercial banking products and services to individuals, businesses, professionals and governments. The services and products have been designed in such a manner as to appeal to consumers and business principals.

The following is a partial listing of the types of services and products that the Bank offers:

| · | Commercial loans for businesses, including those for working capital purposes, equipment purchases and accounts receivable and inventory financing. |

| · | Commercial and residential real estate loans for acquisition, refinancing and construction. |

| · | Consumer loans including automobile loans, home equity loans and lines of credit. |

| · | Loans guaranteed by the United States Small Business Administration. |

| · | Money market deposits, demand deposits, NOW accounts, savings accounts and certificates of deposit. |

| · | Internet banking, including electronic bill payment |

| · | Letters of credit and remittance services. |

| · | Credit and debit card services. |

| · | Merchant credit card deposit servicing. |

| · | Brokerage services for stocks, bonds, mutual funds and annuities. |

| · | After-hours depository services. |

| · | Point of Sale (POS) services. |

| · | Other services, such as direct deposit, traveler’s checks and IRAs. |

Customer service hours for the Bank are competitive with other institutions in the market area. The Bank also acts as a reseller of services purchased from third party vendors for customers requiring services not offered directly by the Bank.

Lending Activities. – The Bank makes various types of loans to borrowers based on, among other things, an evaluation of the borrowers’ net asset value, cash flow, security and ability to repay. Loans to consumers include home mortgage loans, home equity lines of credit, home improvement loans, overdraft lines of credit, and installment loans for automobiles, boats and recreational vehicles. The Bank also makes loans secured by deposit accounts and common stocks. The Bank’s commercial loan product line includes commercial mortgage loans, time and demand loans, lines and letters of credit, and acquisition, development and construction financing. The Notes to the Consolidated Financial Statements contained in Part II, Item 8 report the classification by type of loan for the whole portfolio.

First and second residential mortgage loans, made principally through the Bank’s subsidiary, CMSI, enable customers to purchase or refinance residential properties. These loans are secured by liens on the residential property. All first mortgage loans with a loan to value ratio greater than 80% have private mortgage insurance coverage equal to or greater than the amount required under the Federal National Mortgage Association guidelines. Residential loans are considered low risk based on the type of collateral (residential property) and the underwriting standards used. The Bank experienced $76,426 of losses and $7,516 in recoveries on residential mortgage loans in 2007. The Bank experienced no losses and no recoveries on residential mortgage loans in 2006. The Bank experienced no losses and recoveries of $14,874 in 2005. There were approximately $1.7 million of residential mortgage loans delinquent more than 90 days at December 31, 2007.

Home equity lines of credit are typically second mortgage loans (sometimes first mortgages) secured by the borrower’s primary residence structured as a revolving borrowing line with a maximum loan amount. Customers write checks to access the line. Generally, the Bank has a second lien on the property behind the first mortgage lien holder. The Bank has a number of different equity loan products that it offers. Borrowers can choose between fixed rate loans or loans tied to the prime rate with margins ranging from 0% to 1.5%. The Bank will finance up to 90% of the value of the home in combination with the first mortgage loan balance, depending on the rate and program. Home equity loans carry a higher level of risk than first mortgage residential loans because of the second lien position on the property, and because a higher loan to value ratio is used in the underwriting of the loan. However, the overall risk of loss on home equity loans is also considered low due to the underlying values of the collateral. The Bank experienced losses on home equity loans of $100,455 during 2007 and none during 2006 and 2005. The Bank experienced no recoveries on home equity loans during 2007 and 2006 and $7,700 during 2005. There were approximately $249,000 of home equity loans delinquent more than 90 days at December 31, 2007.

Commercial and investment mortgage loans are first mortgage loans made to individuals or to businesses to finance acquisitions of plant or earning assets, such as rental property. These loans are secured by a first mortgage lien on the commercial property, and may be further secured by other property or other assets depending on the value of the mortgaged property. In most instances, these loans are guaranteed personally by the principals. The Bank typically looks for cash flow from the business at least equal to 115% coverage of the business debt service, and for income-producing property to be self-supporting, generally, with a minimum debt service coverage ratio of 120% to 125%. Commercial mortgage loans carry more risk than residential real estate loans. Commercial mortgage loans tend to be larger in size, and the properties tend to exhibit more fluctuation in value. The repayment of the loan is primarily dependent on the success of the business itself, or the tenants in the case of income producing property. Economic cycles can affect the success of a business. The Bank experienced losses on commercial mortgage loans of $220,640 during 2007, $59,120 during 2006 and $0 during 2005. There were no commercial mortgage loans past due more than 90 days at December 31, 2007.

Construction and land development loans are loans to finance the acquisition and development of parcels of land and to construct residential housing or commercial property. The Bank typically will finance 70% to 80% of the discounted future value of these projects, or 80% of value or 90% of cost, whichever is less, on a single-family detached home. The loan is collateralized by the project or real estate itself, and other assets or guarantees of the principals in most cases. Repayment to the Bank is anticipated from the proceeds of sale of the final units, or permanent mortgage financing on a residential construction loan for a single borrower. These types of loans carry a higher degree of risk than a commercial mortgage loan. Interest rates, buyer preferences, and desired locations are all subject to change during the period from the time of the loan commitment to final delivery of the final unit, all of which can change the economics of the project. In addition, real estate developers to whom these loans are typically made are subject to the business risk of operating a business in a competitive environment. The Bank did not experience any losses or recoveries on construction and land development loans during 2007, 2006 and 2005. There were no construction and land development loans past due more than 90 days at December 31, 2007.

Demand and time loans and lines of credit are loans to businesses for relatively short periods of time, usually not more than one year. These loans are made for any valid business purpose. These loans may be secured by assets of the borrower or guarantor, but may be unsecured based on the personal guarantee of the principal. If secured, loans may be made for up to 100% of the value of the collateral. The businesses to which these loans are made are subject to normal business risk, and cash flows of the business may be subject to economic cycles. In addition, the value of the collateral may fluctuate. If guaranteed by the principal, the net worth and assets of the principal may be dissipated by demands of the business, or due to other factors. The Bank had no losses or recoveries on demand and time loans in 2007 and 2006.The Bank had losses of $123,578 and recoveries of $130,904 on time demand and loans in 2005. There were $3.3 million of demand and time and line of credit loans delinquent more than 90 days at December 31, 2007.

Home improvement loans are loans made to borrowers to complete improvements to their homes including such projects as room additions, swimming pool installations or new roofs. The Bank makes unsecured home improvement loans to a maximum amount of $15,000. Any loan above that limit is secured by a deed of trust. Borrowers are required to own their home, and to meet certain income and debt ratio requirements. The Bank also reviews the credit history of all applicants. Because they are unsecured or secured by a deed of trust, these loans are more risky than first mortgage residential lending. This risk is mitigated somewhat based on the fact that the loans are used to improve the borrower’s home, typically a borrower’s most significant asset. In addition, the debt-to-income ratio requirement helps determine the borrower’s current ability to repay the loan. The Bank had charge-offs of home improvement loans of $249, $11,515 and $0, in 2007, 2006 and 2005, respectively. There were recoveries of $320, $608, and $0, in 2007, 2006, and 2005 respectively. There were no home improvement loans delinquent more than 90 days at December 31, 2007.

The remainder of the consumer loan portfolio is comprised of installment loans for automobiles, boats and recreational vehicles (“RV”), overdraft protection lines, and loans secured by deposit accounts or stocks. The largest portion of this group is installment loans for automobiles and other vehicles. The Bank will finance up to 90% of the cost of a new car purchase, or the maximum loan amount as determined by the National Automobile Dealers Association (NADA) publication for used cars. The Bank will finance up to 85% of the cost of a new boat or RV, or the maximum loan amount determined by the NADA Boat/RV Guide for used Boats and RVs. These loans are secured by the vehicle purchased. Borrowers must meet certain income and debt ratio requirements, and a credit review is performed on each applicant. These types of loans are subject to the risk that the value of the vehicle will decline faster than the amount due on the loan. However, the income-to-debt ratio requirement helps determine the borrower’s current ability to repay. The Bank had no losses on automobile loans in 2007 and $6,849 in 2006 and no losses in 2005 and recoveries of $5,598, $1,251, and $0, in 2007, 2006 and 2005, respectively. There were approximately $11,000 of automobile or other vehicle loans past due more than 90 days at December 31, 2007.

Overdraft lines and other personal loans are unsecured lending arrangements. These loans or lines of credit are made to allow customers to easily make purchases of consumer goods. If the lines are handled as agreed, they will typically be automatically renewed each year. Because they are unsecured, these loans carry a higher level of risk than secured lending transactions. The Bank attempts to mitigate significant risk by establishing fairly low credit limits. Net charge-offs in 2007, 2006, and 2005 were $2,916, $11,662, and $1,927, respectively. There were $1,000 overdraft loans and other personal loans past due more than 90 days at December 31, 2007.

Loans secured by savings accounts and stock and bond certificates are secured lending arrangements. The Bank will advance funds for up to 95% of balances in savings or certificate of deposit accounts. The Bank will advance funds up to 60% of the market value of actively traded stock certificates and bonds or 50% of the market value of listed but not actively traded stocks and bonds. Loans secured by stocks and bonds are subject to margin calls to maintain the loan to value ratio. Collateral is not released until the loan is repaid, and the borrower is generally required to pay interest monthly. There were no losses on loans secured by savings accounts or stock and bond certificates during 2007, 2006, or 2005. Recoveries on loans secured by stocks and bonds were $437, $0, and $0 in 2007, 2006, and 2005 respectively. There were no loans secured by savings accounts or stock and bond certificates past due more than 90 days at December 31, 2007.

The Bank is the principal originator of the loans it makes, at this time. In prior periods, residential mortgage loans and home equity loans and lines of credit were predominantly purchased from a network of brokers or other types of originators with whom the Bank did business. The Bank has sold some loans in the secondary market and therefore derives a small amount of noninterest income from serviced loans. These income amounts are not significant to the amounts of noninterest income derived from other sources.

CMSI originates adjustable and fixed-rate residential mortgage loans at terms and conditions and with documentation that permit their sale in the secondary mortgage market. CMSI’s practice is to immediately sell substantially all residential mortgage loans in the secondary market with servicing released.

CCDC was established in 1995 for the purpose of promoting, developing, and improving the housing and economic conditions of people in Maryland with particular emphasis in the Metropolitan Baltimore area. CCDC promotes through loans, investments, and other transactions, efforts to increase housing for low and moderate-income individuals.

MSLLC was established in 2004 for the purpose of disposing of real estate owned. There was no activity in MSLLC in 2007, 2006, and 2005.

Investment Activities. – The Company maintains a portfolio of investment securities to provide liquidity and income. The current portfolio amounts to about 15% of total assets, and is invested primarily in U.S. government agency securities, state and municipal bonds, corporate bonds, and mortgage-backed securities with maturities varying from 2008 to 2031, as well as equity securities.

Deposit Services. – The Bank offers a wide range of both personal and commercial types of deposit accounts and services as a means of gathering funds. Deposit accounts available include noninterest-bearing demand checking, interest-bearing checking (NOW accounts), savings, money market, certificates of deposit, and individual retirement accounts. Deposit accounts carry varying fee structures depending on the level of services desired by the customer. Interest rates vary depending on the balance in the account maintained by the customer. Commercial deposit customers may also choose an overnight investment account which automatically invests excess balances available in demand accounts on a daily basis in repurchase agreements. The Bank’s customer base for deposits is primarily retail in nature. The Bank also offers certificates of deposit over $100,000 to its retail and commercial customers. The Bank has used deposit brokers in the past and may do so in the future to meet liquidity needs.

The Company offers Certificate of Deposit Registry Service (“CDARS”) deposits to its customers. This is a program which allows customers to deposit more than would normally be covered by FDIC insurance. CDARS is a nationwide program that allows participating banks to “swap” customer deposits so that no customer has greater than the insurable maximum in one bank, but the customer only deals with his/her own bank.

In addition to traditional deposit services, the Bank offers telephone banking services, internet banking services and internet bill paying services to its customers. Also, the Bank offers remote deposit capture to its commercial customers.

Brokerage Activities. – CFS provides full service brokerage services for stocks, bonds, mutual funds and annuities. For 2007, commission income totaled $678,000 and net income was $158,000.

Market. – The Company considers its core markets to be the communities within the Baltimore Metropolitan Statistical Area (“Baltimore MSA”), particularly Baltimore City and the counties of Baltimore, Anne Arundel and Harford. Lending activities are broader and include areas outside of the Baltimore MSA. CMSI operates in Delaware, Pennsylvania, Virginia and West Virginia in addition to its core Maryland operations.

Competition. – The Bank faces strong competition in all areas of its operations. This competition comes from entities operating in Baltimore City, Baltimore County, Anne Arundel County, Harford County, and Carroll County, and includes branches of some of the largest banks in Maryland. Its most direct competition for deposits historically has come from other commercial banks, savings banks, savings and loan associations and credit unions. The Bank also competes for deposits with money market funds, mutual funds and corporate and government securities. The Bank competes with the same banking entities for loans, as well as mortgage banking companies and other institutional lenders. The competition for loans varies from time to time depending on certain factors, including, among others, the general availability of lendable funds and credit, general and local economic conditions, current interest rate levels, conditions in the mortgage market and other factors which are not readily predictable. Some of the Bank’s competitors have greater assets and operating capacity than the Bank.

Current federal law allows the acquisition of banks by bank holding companies nationwide. Further, federal and Maryland law permit interstate banking. Recent legislation has broadened the extent to which financial services companies, such as investment banks and insurance companies, may control commercial banks. As a consequence of these developments, competition in the Bank’s principal market may increase, and a further consolidation of financial institutions in Maryland may occur.

Asset Management. – The Bank makes available several types of loan services to its customers as described above, depending on customer needs. Recent emphasis has been made on originating short-term (one year or less), variable rate commercial loans and variable rate home equity lines of credit, with the balance of its funds invested in consumer/installment loans and real estate loans, both commercial and residential. In addition, a portion of the Bank’s assets is invested in high-grade securities and other investments in order to provide income, liquidity and safety. Such investments include U.S. government agency securities, corporate bonds, mortgage-backed securities and collateralized mortgage obligations, as well as advances of federal funds to other member banks of the Federal Reserve System. Subject to the effects of taxes, the Bank also invests in tax-exempt state and municipal securities with a minimum rating of “A” by a recognized ratings agency. The Bank’s primary source of funds is customer deposits. The risk of non-repayment (or deferred payment) of loans is inherent in the business of commercial banking, regardless of the type of loan or borrower. The Bank’s efforts to expand its loan portfolio to small and medium-sized businesses may result in the Bank undertaking certain lending risks which are somewhat different from those involved in loans made to larger businesses. The Bank’s management evaluates all loan applications and seeks to minimize the exposure to credit risks through the use of thorough loan application, approval and monitoring procedures. However, there can be no assurance that such procedures significantly reduce all risks.

Employees. – As of December 31, 2007, the Bank and its subsidiaries had 137 full time equivalent employees, 29 of whom were officers. Each officer generally has responsibility for one or more loan, banking, customer contact, operations, or subsidiary functions. Non-officer employees are employed in a variety of administrative capacities. Management believes that it has a favorable relationship with its employees.

Critical accounting policies

The Company’s financial condition and results of operations are sensitive to accounting measurements and estimates of matters that are inherently uncertain. When applying accounting policies in areas that are subjective in nature, management must use its best judgment to arrive at the carrying value of certain assets. One of the most critical accounting policies applied is related to the valuation of the loan portfolio.

A variety of estimates impact the carrying value of the loan portfolio including the calculation of the allowance for loan losses, valuation of underlying collateral and the timing of loan charge-offs.

The allowance for loan losses is one of the most difficult and subjective judgments. The allowance is established and maintained at a level that management believes is adequate to cover losses resulting from the inability of borrowers to make required payments on loans. Estimates for loan losses are arrived at by analyzing risks associated with specific loans and the loan portfolio. Current trends in delinquencies and charge-offs, the views of Bank regulators, changes in the size and composition of the loan portfolio and peer comparisons are also factors. The analysis also requires consideration of the economic climate and direction and change in the interest rate environment, which may impact a borrower’s ability to pay, legislation impacting the banking industry and economic conditions specific to the Bank’s service area. Because the calculation of the allowance for loan losses relies on estimates and judgments relating to inherently uncertain events, results may differ from our estimates.

Another critical accounting policy is related to securities. Securities are evaluated periodically to determine whether a decline in their value is other than temporary. The term “other than temporary” is not intended to indicate a permanent decline in value. Rather, it means that the prospects for near term recovery of value are not necessarily favorable, or that there is a lack of evidence to support fair values equal to, or greater than, the carrying value of the investment. Management reviews criteria such as the magnitude and duration of the decline, as well as the reasons for the decline, to predict whether the loss in value is other than temporary. Once a decline in value is determined to be other than temporary, the value of the security is reduced and a corresponding charge to earnings is recognized.

Supervision and Regulation

General. – The Company and Bank are extensively regulated under federal and state law. Generally, these laws and regulations are intended to protect depositors, not stockholders. The following is a summary description of certain provisions of certain laws, which affect the regulation of banks and holding companies. The discussion is qualified in its entirety by reference to applicable laws and regulations. Changes in these laws and regulations may have a material effect on the business and prospects of the Company and the Bank.

As a bank holding company, the Company is subject to the Bank Holding Company Act of 1956, as amended (the “BHCA”). The BHCA is administered by the Board of Governors of the Federal Reserve System (the “Board of Governors”), and the Company is required to file with the Board of Governors such reports and information as may be required pursuant to the BHCA. The Board of Governors also may examine the Company and any of its nonbank subsidiaries. The BCHA requires every bank holding company to obtain the prior approval of the Board of Governors before: (i) it or any of its subsidiaries (other than a bank) acquires substantially all of the assets of any bank; (ii) it acquires ownership or control of any voting shares of

any bank if after such acquisition it would own or control, directly or indirectly, more than five percent of the voting shares of such bank; or (iii) it merges or consolidates with any other bank holding company.

Under the BHCA, a bank holding company is generally prohibited from engaging in, or acquiring direct or indirect control of more than five percent (5%) of the voting shares of any company engaged in non-banking activities. A major exception to this prohibition is for activities the Board of Governors finds, by order or regulation, to be so closely related to banking or managing or controlling banks. Some of the activities that the Board of Governors has determined by regulation to be properly incident to the business of a bank holding company are: making or servicing loans and certain types of leases; engaging in certain investment advisory and discount brokerage activities; performing certain data processing services; acting in certain circumstances as a fiduciary or as an investment or financial advisor; ownership of certain types of savings associations; engaging in certain insurance activities; and making investments in certain corporations or projects designed primarily to promote community welfare.

Federal and State Bank Regulation. The Bank is a Maryland state-chartered bank, with all the powers of a commercial bank, regulated and examined by the Office of the Maryland Commissioner of Financial Regulation (the “Commissioner’) and the Federal Deposit Insurance Corporation (“FDIC”). The Commissioner and the FDIC have extensive enforcement authority over the institutions they regulate to prohibit or correct activities which violate law, regulations or written agreements with the regulator, or which are deemed to constitute unsafe or unsound practices. Enforcement actions may include the appointment of a conservator or receiver, the issuance of a cease and desist order, the termination of deposit insurance, the imposition of civil money penalties on the institution, its directors, officers, employees and institution-affiliated parties, and the enforcement of any such mechanisms through restraining orders or other court actions.

In its lending activities, the maximum legal rate of interest, fees and charges which a financial institution may charge on a particular loan depends on a variety of factors such as the type of borrower, the purpose of the loan, the amount of the loan and the date the loan is made. Other laws tie the maximum amount, which may be loaned to any one customer and its related interests to capital levels. The Bank is also subject to certain restrictions on extensions of credit to executive officers, directors, principal stockholders or any related interest of such persons which generally require that such credit extensions be made on substantially the same terms as are available to third persons dealing with the Bank and not involve more than the normal risk of repayment.

The Community Reinvestment Act (“CRA”) requires that in connection with the examination of financial institutions within their jurisdictions, the FDIC evaluate the record of the financial institutions in meeting the credit needs of their local communities, including low and moderate-income neighborhoods, consistent with the safe and sound operation of these banks. The factors are also considered by all regulatory agencies in evaluating mergers, acquisitions and applications to open a branch or facility. As of the date of its most recent examination report, the Bank has a CRA rating of “Satisfactory.”

Under the Federal Deposit Insurance Corporation Improvement Act of 1991(“FDICIA”), each federal banking agency is required to prescribe, by regulation, non-capital safety and soundness standards for institutions under its authority. The federal banking agencies, including the FDIC, have adopted standards covering internal controls, information systems, internal audit systems, loan documentation, credit underwriting, interest rate exposure, asset growth, and compensation, fees and benefits. An institution that fails to meet those standards may be required by the agency to develop a plan acceptable to the agency, which specifies the steps that the institution will take to meet the standards. Failure to submit or implement such a plan may subject the institution to regulatory sanctions. The Bank believes that it meets substantially all standards which have been adopted. FDICIA also imposed new capital standards on insured depository institutions described under the caption, “Capital Requirements.”

Before establishing new branch offices, the Bank must meet certain minimum capital stock and surplus requirements. Prior to establishment of the branch, the Bank must obtain Commissioner and FDIC approval.

Deposit Insurance. As an FDIC insured institution, deposits of the Bank are currently insured to a maximum of $100,000 per depositor through the Bank Insurance Fund (“BIF”). For traditional and ROTH IRA’s, the federal deposit insurance limit is $250,000. The FDIC is required to establish the semi-annual assessments for BIF-insured depository institutions at a rate determined to be appropriate to maintain or increase the reserve ratio of the respective deposit insurance funds at or above 1.25 percent of estimated insured deposits or at such higher percentage that the FDIC determines to be justified for that year by circumstances raising significant risk of substantial future losses to the fund. The Bank currently pays a de minimus semi-annual assessment.

Limits on Dividends and Other Payment. Both federal and state laws impose restrictions on the ability of the Bank to pay dividends. The Federal Reserve Board (“FRB”) has issued a policy statement, which provides that, as a general matter, insured banks may pay dividends only out of prior operating earnings. For a Maryland state-chartered bank, dividends may be paid out of undivided profits or, with the prior approval of the Commissioner, from surplus in excess of 100% of required capital stock. If, however, the surplus of a Maryland bank is less than 100% of its required capital stock, cash dividends may not be paid in excess of 90% of the net earnings. In addition to these specific restrictions, bank regulatory agencies, in general, also

have the ability to prohibit proposed dividends by a financial institution, which would otherwise be permitted under applicable regulations if the regulatory body determines that such distribution would constitute an unsafe or unsound practice.

Capital Requirements. The FDIC adopted certain risk-based capital guidelines to assist in the assessment of the capital adequacy of a banking organization’s operations for both transactions reported as assets on the balance sheet and transactions, such as letters of credit and recourse arrangements, which are recorded as off balance sheet items. Under these guidelines, nominal dollar amounts of assets and credit equivalent amounts of off balance sheet items are multiplied by one of several risk adjustment percentages, which range from 0% for assets with low credit risk, such as certain U.S. Treasury securities, to 100% for assets with relatively high credit risk, such as business loans.

A banking organization’s risk-based capital ratios are obtained by dividing its qualifying capital by its total risk adjusted assets. The regulators measure risk-adjusted assets, which include off balance sheet items, against both total qualifying capital (the sum of Tier 1 capital and limited amounts of Tier 2 capital) and Tier 1 capital. “Tier 1,” or core capital, includes common equity, perpetual preferred stock (excluding auction rate issues) and minority interest in equity accounts of consolidated subsidiaries, less goodwill and other intangibles, subject to certain exceptions. “Tier 2,” or supplementary capital, includes, among other things, limited-life preferred stock, hybrid capital instruments, mandatory convertible securities, qualifying subordinated debt, and the allowance for loan losses, subject to certain limitations and less required deductions. The inclusion of elements of Tier 2 capital is subject to certain other requirements and limitations of the federal banking agencies. Banks subject to the risk-based capital guidelines are required to maintain a ratio of Tier 1 capital to risk-weighted assets of at least 4% and a ratio to total capital to risk-weighted assets of at least 8%. The appropriate regulatory authority may set higher capital requirements when particular circumstances warrant.

In August 1995 and May 1996, the federal banking agencies adopted final regulations specifying that the agencies will include, in their evaluations of a bank’s capital adequacy, an assessment of the bank’s interest rate risk (“IRR”) exposure. The standards for measuring the adequacy and effectiveness of a banking organization’s interest rate risk management include a measurement of board of director and senior management oversight, and a determination of whether a banking organization’s procedures for comprehensive risk management are appropriate to the circumstances of the specific banking organization. The Bank has internal IRR models that are used to measure and monitor IRR. Additionally, the regulatory agencies have been assessing IRR on an informal basis for several years. For these reasons the addition of IRR evaluation to the agencies’ capital guidelines has not resulted in significant changes in capital requirements for the Bank.

Failure to meet applicable capital guidelines could subject a banking organization to a variety of enforcement actions, including limitations on its ability to pay dividends, the issuance by the applicable regulatory authority of a capital directive to increase capital and, in the case of depository institutions, the termination of deposit insurance by the FDIC, as well as to the measures described under the caption, “Federal Deposit Insurance Corporation Improvement Act of 1991” below, as applicable to undercapitalized institutions. In addition, future changes in regulations or practices could further reduce the amount of capital recognized for purposes of capital adequacy. Such a change could affect the ability of the Bank to grow and could restrict the amount of profits, if any, available for the payment of dividends to the stockholders.

Federal Deposit Insurance Corporation Improvement Act of 1991. In December 1991, Congress enacted FDICIA, which substantially revised the bank regulatory and funding provisions of the Federal Deposit Insurance Act and made significant revisions to several other federal banking statutes. FDICIA provides for, among other things, (i) publicly available annual financial condition and management reports for financial institutions, including audits by independent accountants, (ii) the establishment of uniform accounting standards by federal banking agencies, (iii) the establishment of a “prompt corrective action” system of regulatory supervision and intervention, based on capitalization levels, with more scrutiny and restrictions placed on depository institutions with lower levels of capital, (iv) additional grounds for the appointment of a conservator or receiver, and (v) restrictions or prohibitions on accepting brokered deposits, except for institutions which significantly exceed minimum capital requirements. FDICIA also provides for increased funding of the FDIC insurance funds and the implementation of risk-based premiums, described further under the caption “Deposit Insurance.”

A central feature of FDICIA is the requirement that the federal banking agencies take “prompt corrective action” with respect to depository institutions that do not meet minimum capital requirements. Pursuant to FDICIA, the federal bank regulatory authorities have adopted regulations setting forth a five-tiered system for measuring the capital adequacy of the depository institutions that they supervise. Under these regulations, a depository institution is classified in one of the following capital categories: “well capitalized,” “adequately capitalized,” “undercapitalized,” “significantly undercapitalized” and “critically undercapitalized.” An institution may be deemed by the regulators to be in a capitalization category that is lower than is indicated by its actual capital position if, among other things, it receives an unsatisfactory examination rating with respect to asset quality, management, earnings or liquidity. The Bank is currently “well capitalized.”

FDICIA generally prohibits a depository institution from making any capital distribution (including payment of a cash dividend) if the depository institution would thereafter be undercapitalized. Undercapitalized depository institutions are subject to growth limitations and are required to submit capital restoration plans. If a depository institution fails to submit an acceptable plan, it is treated as if it is significantly undercapitalized. Significantly undercapitalized depository institutions may be subject to a number

of other requirements and restrictions, including orders to sell sufficient voting stock to become adequately capitalized, requirements to reduce total assets and stop accepting deposits from correspondent banks. Critically undercapitalized institutions are subject to the appointment of a receiver or conservator; generally within 90 days of the date such institution is determined to be critically undercapitalized.

FDICIA provides the federal banking agencies with significantly expanded powers to take enforcement action against institutions, which fail to comply with capital or other standards. Such action may include the termination of deposit insurance by the FDIC or the appointment of a receiver or conservator for the institution. FDICIA also limits the circumstances under which the FDIC is permitted to provide financial assistance to an insured institution before appointment of a conservator or receiver.

Financial Modernization. In November 1999, the Gramm-Leach-Bliley Act (“GLBA”) was signed into law. Effective in part on March 11, 2000, GLBA revises the BHCA and repeals the affiliation provisions for the Glass-Steagall Act of 1933, which, taken together, limited the securities, insurance and other non-banking activities of any company that controls a FDIC insured institution. Under GLBA, bank holding companies can elect, subject to certain qualifications, to become a “financial holding company.” GLBA provides that a financial holding company may engage in a full range of financial activities, including, insurance and securities sales and underwriting activities, and real estate development, with the expedited notice procedures.

Maryland law generally permits Maryland state-chartered banks, including the Bank, to engage in the same activities, directly or through an affiliate, as national banks. GLBA permits certain qualified national banks to form financial subsidiaries, which have broad authority to engage in all financial activities except insurance underwriting, insurance investments, real estate investment or development, or merchant banking. Thus, GLBA has the effect of broadening the permitted activities of Maryland state-chartered banks.

The Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (the “PATRIOT Act”) requires financial institutions to develop a customer identification plan that includes procedures to:

| · | Collect identifying information about customers opening a deposit or loan account |

| · | Verify customer identity |

| · | Maintain records of the information used to verify the customer’s identity |

| · | Determine whether the customer appears on any list of suspected terrorists or terrorist organizations |

Under the provisions of the PATRIOT Act, the Bank is also required from time to time to search its customer data base for the names of known or suspected terrorists as provided by the government.

Due to the extensive regulation of the commercial banking business in the United States, the Company is particularly susceptible to changes in federal and state legislation and regulations.

Governmental monetary policies and economic controls

The Company is affected by monetary policies of regulatory agencies, including the FRB, which regulates the national money supply in order to mitigate recessionary and inflationary pressures. Among the techniques available to the FRB are: engaging in open market transactions in U.S. Government securities, changing the discount rate on bank borrowings, changing reserve requirements against bank deposits, prohibiting the payment of interest on demand deposits, and imposing conditions on time and savings deposits. These techniques are used in varying combinations to influence the overall growth of bank loans, investments and deposits. Their use may also affect interest rates charged on loans or paid on deposits. The effect of governmental policies on the earnings of the Company cannot be predicted. However, the Company’s earnings will be impacted by movement in interest rates, as discussed in Part II Item 7a. “Quantitative and Qualitative Disclosure About Market Risk.”

The risks and uncertainties described below are not the only ones that we face. Additional risks and uncertainties that we are unaware of, or that we currently deem immaterial, also may become important factors that affect us and our business. If any of these risks were to occur, our business, financial condition or results of operations could be materially and adversely affected. Also, consider the other information in this Annual Report on Form 10-K, as well as the documents incorporated by reference.

Competition may decrease our growth or profits.

We face significant competition for banking services in our primary market in which we operate. Competition in the local banking industries may limit our ability to attract and retain customers. We may face competition now and in the future from the

following: other local and regional banking institutions, including larger commercial banking organizations; savings banks; credit unions; other financial institutions; and non-bank financial services companies serving the area.

In particular, our competitors may possess greater resources that may afford them a marketplace advantage by enabling them to maintain numerous banking locations and mount extensive promotional and advertising campaigns. Additionally, banks and other financial institutions with larger capitalization and financial intermediaries not subject to bank regulatory restrictions have larger lending limits, which enable them to serve the credit needs of larger customers. We also face competition from out-of-state financial intermediaries that have opened low-end production offices or that solicit deposits in their respective market areas. If we are unable to attract and retain banking customers we may be unable to continue our loan growth and level of deposits and our results of operations and financial condition may otherwise be negatively affected.

In the past, we have expanded our operations into non-banking activities such as insurance-related products and brokerage services. We may have difficulty competing with more established providers of these products and services due to the intense competition in many of these industries. In addition, we may be unable to attract and retain non-banking customers due to a lack of market and product knowledge or other industry specific matters or an inability to attract and retain qualified, experienced employees. Our failure to attract and retain customers with respect to these non-banking activities could negatively impact our future earnings.

Changes in interest rates and other factors beyond our control may adversely affect our earnings and financial condition.

Our main source of income from operations is net interest income, which is equal to the difference between the interest income received on loans, investment securities and other interest-earning assets and the interest expense incurred in connection with deposits, borrowings and other interest-bearing liabilities. As a result, our net interest income can be affected by changes in market interest rates. These rates are highly sensitive to many factors beyond our control, including general economic conditions, both domestic and foreign, and the monetary and fiscal policies of various governmental and regulatory authorities. We have adopted asset and liability management policies to try to minimize the potential adverse effects of changes in interest rates on our net interest income, primarily by altering the mix and maturity of loans, investments and funding sources. However, even with these policies in place, we cannot provide assurance that changes in interest rates will not negatively impact our operating results.

An increase in interest rates also could have a negative impact on our business by reducing the ability of borrowers to repay their current loan obligations, which could not only result in increased loan defaults, foreclosures and write-offs, but also necessitate further increases to our allowance for loan losses. Increases in interest rates also may reduce the demand for loans and, as a result, the amount of loan and commitment fees. In addition, fluctuations in interest rates may result in disintermediation, which is the flow of funds away from depository institutions into direct investments that pay higher rates of return, and may affect the value of our investment securities and other interest-earning assets.

We originate and sell mortgage loans. Changes in interest rates affect demand for our loan products and the revenue realized on the sale of loans. A decrease in the volume of loans sold and lower gains on sales of mortgages can decrease our revenues and net income.

Our allowance for loan losses may not be adequate to cover our actual loan losses, which could adversely affect our earnings.

If our customers default on the repayment of their loans, our profitability could be adversely affected. A borrower’s default on its obligations under one or more of our loans may result in lost principal and interest income and increased operating expenses as a result of the allocation of management time and resources to the collection and work-out of the loans. If collection efforts are unsuccessful or acceptable workout arrangements cannot be reached, we may have to write-off the loans in whole or in part. Although we may acquire any real estate or other assets that secure the defaulted loans through foreclosure or other similar remedies, the amount owed under the defaulted loans may exceed the value of the assets acquired.

Our management periodically makes a determination of our allowance for loan losses based on available information, including the quality of our loan portfolio, economic conditions, and the value of the underlying collateral and the level of our non-accruing loans. If our assumptions prove to be incorrect, our allowance may not be sufficient and future additions to the allowance may be necessary which will result in an expense for the period. If, as a result of general economic conditions or an increase in nonperforming loans, management determines that an increase in our allowance for loan losses is necessary, we may incur additional expenses.

In addition, as an integral part of their examination process, bank regulatory agencies periodically review our allowance for loan losses and the value we attribute to real estate acquired through foreclosure or other similar remedies. These regulatory agencies may require us to adjust our determination of the value for these items based on their judgment. These adjustments could negatively impact our results of operations or financial condition.

In the course of our business, we may acquire, through foreclosure, properties securing loans that are in default. Particularly in commercial real estate lending, there is a risk that hazardous substances could be discovered on these properties. In this event, we might be required to remove these substances from the affected properties at our sole cost and expense. The cost of this removal could substantially exceed the value of the affected properties. We may not have adequate remedies against the prior owners or other responsible parties and could find it difficult or impossible to sell the affected properties. The occurrence of one or more of these events could adversely affect our financial condition or operating results.

Changes in local economic conditions could adversely affect our business.

Because we serve primarily individuals and smaller businesses, the ability of our customers to repay their loans is impacted by the economic conditions in these areas. As of December 31, 2007, approximately 74% of our loan portfolio consisted of commercial loans, defined as commercial and industrial, municipal, multi-family, commercial real estate and construction loans. Thus, our results of operations, both in terms of the origination of new loans and the potential default of existing loans, is heavily dependent upon the strength of local businesses.

We have traditionally obtained funds principally through deposits and borrowings. As a general matter, deposits are a cheaper source of funds than borrowings, because interest rates paid for deposits are typically less than interest rates charged for borrowings. If, as a result of competitive pressures, market interest rates, general economic conditions or other events, the balance of our deposits decrease relative to our overall banking operations, we may have to rely more heavily on borrowings as a source of funds in the future. Such an increased reliance on borrowings could have a negative impact on our results of operations or financial condition.

Government regulation significantly affects our business.

Bank holding companies and state and federally chartered banks operate in a highly regulated environment and are subject to supervision and examination by federal and state regulatory agencies. We are subject to the BHCA, as amended, and to regulation and supervision by the Federal Deposit Insurance Corporation, or FDIC, and the Office of the Maryland Commissioner. The cost of compliance with regulatory requirements may adversely affect our results of operations or financial condition. Federal and state laws and regulations govern numerous matters including: changes in the ownership or control of banks and bank holding companies; maintenance of adequate capital and the financial condition of a financial institution; permissible types, amounts and terms of extensions of credit and investments; permissible non-banking activities; the level of reserves against deposits; and restrictions on dividend payments. Regulations affecting banks and financial services companies undergo continuous change, and we cannot predict the ultimate effect of these changes, which could have a material adverse effect on our profitability or financial condition. Federal economic and monetary policy may also affect our ability to attract deposits and other funding sources, make loans and investments, and achieve satisfactory interest spreads.

The FDIC, and state banking authorities possess cease and desist powers to prevent or remedy unsafe or unsound practices or violations of law by banks subject to their regulation, and the FRB possesses similar powers with respect to bank holding companies. These and other restrictions limit the manner in which we may conduct our business and obtain financing.

Furthermore, our banking business is affected not only by general economic conditions, but also by the monetary policies of the FRB. Changes in monetary or legislative policies may affect the interest rates we must offer to attract deposits and the interest rates we can charge on our loans, as well as the manner in which we offer deposits and make loans. These monetary policies have had, and are expected to continue to have, significant effects on the operating results of depository institutions, including our Bank.

Under regulatory capital adequacy guidelines and other regulatory requirements, we must meet guidelines that include quantitative measures of assets, liabilities, and certain off-balance sheet items, subject to qualitative judgments by regulators about components, risk weightings and other factors. If we fail to meet these minimum capital guidelines and other regulatory requirements, our financial condition would be materially and adversely affected. Our failure to maintain the status of “well capitalized” under our regulatory framework could affect the confidence of our customers in us, thus compromising our competitive position. In addition, failure to maintain the status of “well capitalized” under our regulatory framework or “well managed” under regulatory examination procedures could compromise our status as a bank holding company and related eligibility for a streamlined review process for acquisition proposals.

Changes in the Federal and State tax laws may negatively impact the financial performance of the Company

The Company is subject to changes in tax law that could increase the effective tax rate payable to the state or federal government. These law changes may be retroactive to previous periods and as a result, could negatively affect the current and future performance of the Company.

Technology failure could adversely affect our operations and profits.

We rely heavily on communications and information systems to conduct our business. Any failure or interruptions or breach in security of these systems could result in failures or disruptions in our customer relationship management, general ledger, deposits, and servicing or loan origination systems. The occurrence of any failures or interruptions could result in a loss of customer business and have a material adverse effect on our results of operations and financial condition.

The Company is subject to litigation risk.

In the normal course of business, the Corporation may become involved in litigation, the outcome of which may have a direct material impact on our financial position and daily operations. Please see Note 16, “Contingencies” for the current status of existing and threatened litigation.

Changes in accounting standards or interpretation in new or existing standards could materially affect the results of the Company.

From time to time the Financial Accounting Standards Board (“FASB”) and the SEC change accounting regulations and reporting standards that govern the preparation of the Company’s financial statements. In addition, the FASB, SEC, bank regulators and the outside independent auditors may revise their previous interpretations regarding existing accounting and regulations and the application of these accounting standards. These revisions in their interpretations are out of the Company’s control and may have a material impact on the Company’s financial results of operations.

Our ability to pay dividends is limited by law and contract.

Our ability to pay dividends to our shareholders largely depends on the Company’s receipt of dividends from the Bank. The amount of dividends that the Bank may pay to the Company is limited by federal laws and regulations. We also may decide to limit the payment of dividends even when we have the legal ability to pay them in order to maintain earnings for use in our business.

The market price for our common stock may be volatile.

The market price for our common stock has fluctuated, ranging between $11.25 and $18.40 per share during the 12 months ended December 31, 2007. The overall market and the price of our common stock may continue to be volatile. There may be a significant impact on the market share of our common stock due to, among other things:

Variations in our anticipated or actual operating results or the results of our competitors;

Changes in investors’ or analysts’ perceptions of the risks and conditions of business;

The size of the public float of our common stock;

Regulatory developments;

The announcement of acquisitions or new branch locations by us or our competitors;

Market conditions; and

General economic conditions.

Additionally, the average daily trading volume for our common stock is low and on various days throughout the year, there is no activity on the stock. There can be no assurance that a more active or consistent trading market will develop. As a result, relatively small trades could have a significant impact on the price of our stock.

The Company owned the following properties, which had a book value of $2.7 million at December 31, 2007:

| Location | | Description |

1740 East Joppa Road Towson, MD 21234 | | Full service branch with drive thru, Electronic Banking offices and leased office space |

427 Crain Highway Glen Burnie, MD 21061 | | Full service branch with drive-thru |

531 South Conkling Street Baltimore, MD 21224 | | Full service branch with drive-thru |

344 N. Charles Street Baltimore, MD 21201 | | Full service branch with Executive offices, Lending offices and Finance offices |

The Company leased the following facilities at an aggregate annual rental of approximately $1.1 million as of December 31, 2007:

| Location | | Description | | Lease Expiration Date* |

1066-70 Maiden Choice Lane Arbutus, MD 21229 | | Full service branch | | April 30, 2031 |

4738 Shelbourne Road Baltimore, MD 21229 | | Detached drive-thru | | April 30, 2031 |

Suites 101-103 & 120-122 1589 Sulphur Spring Road Baltimore, MD 21227 | | Administrative and operational offices | | February 28, 2019 |

2637-A Old Annapolis Road Hanover, MD 21076 | | Full service branch | | October 1, 2014 |

Wilkens Beltway Plaza 4658 Wilkens Avenue Baltimore, MD 21229 | | Limited-service branch | | October 21, 2024 |

8157A Honeygo Boulevard White Marsh, MD 21236 | | Full service branch closed January 4, 2008. Relocated to Perry Hall, Maryland | | |

Northway Shopping Center 684 Old Mill Road Millersville, MD 21108 | | Full service branch | | August 31, 2014 |

602 Hoagie Drive Bel Air, MD 21014 | | Full service branch | | November 30, 2044 |

10301 York Road Cockeysville, MD 21030 | | Full service branch | | December 1, 2047 |

4040 Schroeder Avenue Perry Hall, MD 21128 | | Full service branch opened January 7, 2008. Relocated from White Marsh, Maryland | | August 13, 2047 |

2300 York Road Timonium, MD 21093 | | Mortgage subsidiary offices | | January 14, 2010 |

208 Hickory Avenue Bel Air, MD 21014 | | Mortgage subsidiary office closed | | March 31, 2010 |

8905 Harford Road Baltimore, MD 21234 | | Mortgage subsidiary offices | | June 30, 2008 |

1 Center Square, Suite 201 Hanover, PA 17331 | | Mortgage subsidiary offices | | June 29, 2008 |

*Expiration date, assuming the Company exercises all extension options.

| | Item 3: Legal Proceedings |

The Company is involved in various legal actions arising from normal business activities. In management’s opinion, the outcome of these matters, individually or in the aggregate, will not have a material adverse impact on the results of operation or financial position of the Company.

| | Item 4: Submission of Matters to a Vote of Security-Holders |

There were no matters submitted to a vote of the shareholders during the quarter ended December 31, 2007.

| | Item 5: Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

As of December 31, 2007, there were 380 shareholders of record of the Company. The Company’s Common Stock has traded on the National Association of Security Dealers’ Automated Quotation System (“NASDAQ”) National Market Tier of The NASDAQ Stock Market under the symbol “CRRB.” Currently, there are two broker-dealers who make a market in the Common Stock.

As a depository institution whose deposits are insured by the FDIC, the Bank may not pay dividends or distribute any of its capital assets while it remains in default on any assessment due to the FDIC. The Bank currently is not in default under any of its obligations to the FDIC. As a commercial bank under the Maryland Financial Institution Law, the Bank may declare cash dividends from undivided profits or, with the prior approval of the Commissioner of Financial Regulation, out of surplus in excess of 100% of its required capital stock, and after providing for due or accrued expenses, losses, interest and taxes.

The Company and the Bank, in declaring and paying dividends, are also limited insofar as minimum capital requirements of regulatory authorities must be maintained. The Company and the Bank currently comply with such capital requirements.

Dividends declared per share on the Company’s common stock were $0.48 in 2007, $0.45 in 2006, and $0.40 in 2005, representing a payout ratio of 63.88% in 2007, 48.98% in 2006, and 45.97% in 2005. The dividend payout ratio is the result of dividing the amount of dividends paid by net income.

The Company implemented a Dividend Reinvestment Plan that provides automatic reinvestment of dividends in additional shares of Company common stock.

During 2007, the Company repurchased and retired 16,015 shares of common stock at an average price of $16.50. In 2006, the Company repurchased and retired 7,518 shares of common stock at a price of $17.14 per share.

The following table sets forth the high and low sales price and dividends per share of the Company’s common stock for the periods indicated.

| Period | | Price Per Share | | | Cash Dividends Paid Per Share | |

| | | 2007 | | | 2006 | | | 2007 | | | 2006 | |

| | | Low | | | High | | | Low | | | High | | | | | | | |

| 4th Quarter | | $ | 11.25 | | | $ | 14.85 | | | $ | 16.99 | | | $ | 19.45 | | | $ | 0.12 | | | $ | 0.12 | |

| 3rd Quarter | | | 12.00 | | | | 16.73 | | | | 16.11 | | | | 18.00 | | | | 0.12 | | | | 0.11 | |

| 2nd Quarter | | | 15.55 | | | | 18.40 | | | | 15.64 | | | | 18.80 | | | | 0.12 | | | | 0.11 | |

| 1st Quarter | | | 16.40 | | | | 18.00 | | | | 14.40 | | | | 15.95 | | | | 0.12 | | | | 0.11 | |

| | | | | | | | | | | | | | | | | | | $ | 0.48 | | | $ | 0.45 | |

As of December 31, 2007, there were 380 common shareholders of record holding an aggregate of 2,834,975 shares. The Company believes there to be in excess of 561 beneficial owners of the Company’s Common Stock.

The ability of the Company to pay dividends in the future will be dependent on the earnings, if any, financial condition and business of the Company, as well as other relevant factors, such as regulatory requirements. No assurance can be given either that the Company’s future earnings, if any, will be sufficient to enable it to pay dividends, or that if such earnings are sufficient, that the Company will not decide to retain such earnings for general working capital and other funding needs. In addition, the Company is highly dependent on dividends received from the Bank to enable it to pay dividends to shareholders. No assurance can be given that the Bank will continue to generate sufficient earnings to enable it to pay dividends to the Company, or that it will continue to meet regulatory capital requirements which, if not met, could prohibit payment of dividends to the Company.

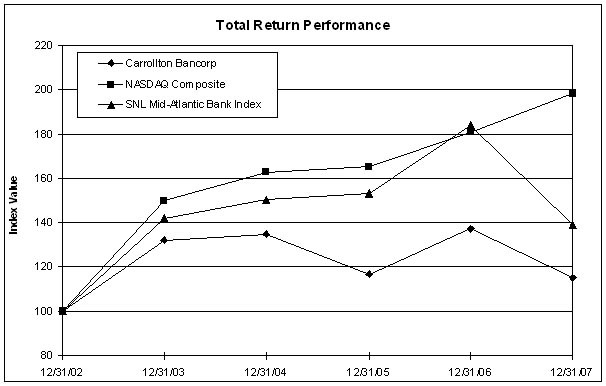

The Company is required by the SEC to provide a five-year comparison of the cumulative total shareholder return on our common stock compared with that of a broad equity market index, and either a published industry index or a constructed peer group index of the Company.

The following chart compares the cumulative Shareholder return on the Company’s common stock from December 31, 2002 to December 31, 2007 with the cumulative total of the NASDAQ Composite (U.S.), the NASDAQ Bank and SNL Mid-Atlantic Indices. The comparison assumes $100 was invested on December 31, 2002 in the Company’s common stock and in each of the foregoing indices. It also assumes reinvestment of any dividends.

The Company does not make, nor does it endorse, any predictions as to future stock performance.

Carrollton Bancorp

| | | Period Ending | |

| Index | | 12/31/02 | | 12/31/03 | | 12/31/04 | | 12/31/05 | | 12/31/06 | | 12/31/07 | |

| Carrollton Bancorp | | | 100.00 | | | | 131.90 | | | | 134.76 | | | | 116.78 | | | | 137.26 | | | | 115.23 | | |

| NASDAQ Composite | | | 100.00 | | | | 150.01 | | | | 162.89 | | | | 165.13 | | | | 180.85 | | | | 198.60 | | |

| SNL Mid-Atlantic Bank Index | | | 100.00 | | | | 142.18 | | | | 150.59 | | | | 153.26 | | | | 183.94 | | | | 139.10 | | |

The following table provides information about the Company’s equity securities that may be issued under all of the Company’s equity compensation plans as of the end of the most recently completed fiscal year:

| Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants and rights (a) | | Weighted-average exercise price of outstanding options, warrants and rights (b) | | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) | | |

| Equity compensation plans approved by security holders | | 184,555 | | | | $14.64 | | | | 496,400 | | |

| Equity compensation plans not approved by security holders | | N/A | | | | N/A | | | | N/A | | |

| Total | | 184,555 | | | | $14.64 | | | | 496,400 | | |

Item 6: Selected Financial Data

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Consolidated Income Statement Data: | | | | | | | | | | | | | | | |

| Interest income | | $ | 23,676,360 | | | $ | 23,127,504 | | | $ | 19,071,379 | | | $ | 15,500,323 | | | $ | 15,935,691 | |

| Interest expense | | | 9,762,324 | | | | 8,737,450 | | | | 7,375,083 | | | | 5,321,622 | | | | 6,639,734 | |

| Net interest income | | | 13,914,036 | | | | 14,390,054 | | | | 11,696,296 | | | | 10,178,701 | | | | 9,295,957 | |

| Provision for loan losses | | | 536,000 | | | | — | | | | — | | | | — | | | | 243,000 | |

| Net interest income after provision for loan losses | | | 13,378,036 | | | | 14,390,054 | | | | 11,696,296 | | | | 10,178,701 | | | | 9,052,957 | |

| Noninterest income | | | 6,274,142 | | | | 8,898,996 | | | | 10,718,636 | | | | 8,781,151 | | | | 8,268,612 | |

| Noninterest expenses | | | 16,475,141 | | | | 19,381,003 | | | | 18,634,124 | | | | 17,751,000 | | | | 16,058,355 | |

| Income before income taxes | | | 3,177,037 | | | | 3,908,047 | | | | 3,780,808 | | | | 1,208,852 | | | | 1,263,214 | |

| Income taxes | | | 1,050,774 | | | | 1,323,268 | | | | 1,322,371 | | | | 320,488 | | | | 338,500 | |

| Net income | | $ | 2,126,263 | | | $ | 2,584,779 | | | $ | 2,458,437 | | | $ | 888,364 | | | $ | 924,714 | |

Consolidated Balance Sheet Data, at year end | | | | | | | | | | | | | | | | | | | | |

| Assets | | $ | 352,848,570 | | | $ | 349,824,752 | | | $ | 360,467,146 | | | $ | 319,123,132 | | | $ | 302,409,975 | |

| Gross loans | | | 261,623,833 | | | | 260,001,314 | | | | 247,943,073 | | | | 219,726,294 | | | | 199,296,561 | |

| Deposits | | | 285,638,625 | | | | 277,903,801 | | | | 271,626,503 | | | | 225,846,145 | | | | 207,056,100 | |

| Shareholders’ equity | | | 35,931,300 | | | | 34,711,378 | | | | 34,640,165 | | | | 34,215,280 | | | | 34,124,882 | |

| Per Share Data: | | | | | | | | | | | | | | | | | | | | |

| Number of shares of Common Stock outstanding, at year-end | | | 2,834,975 | | | | 2,806,705 | | | | 2,809,698 | | | | 2,834,823 | | | | 2,828,078 | |

| Net income: | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 0.75 | | | $ | 0.92 | | | $ | 0.87 | | | $ | 0.31 | | | $ | 0.33 | |