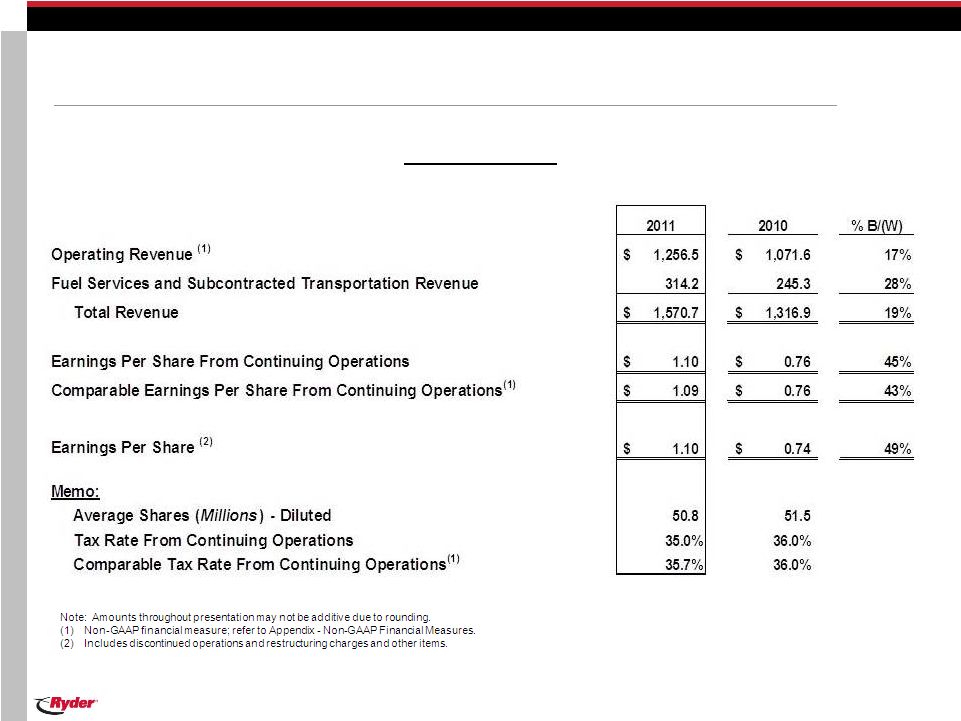

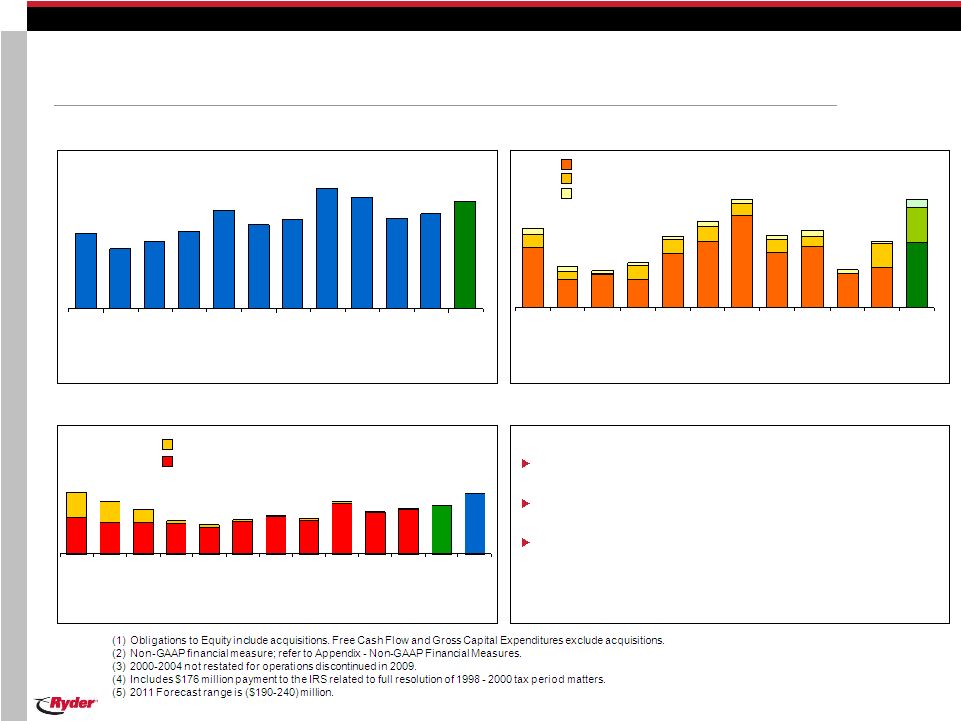

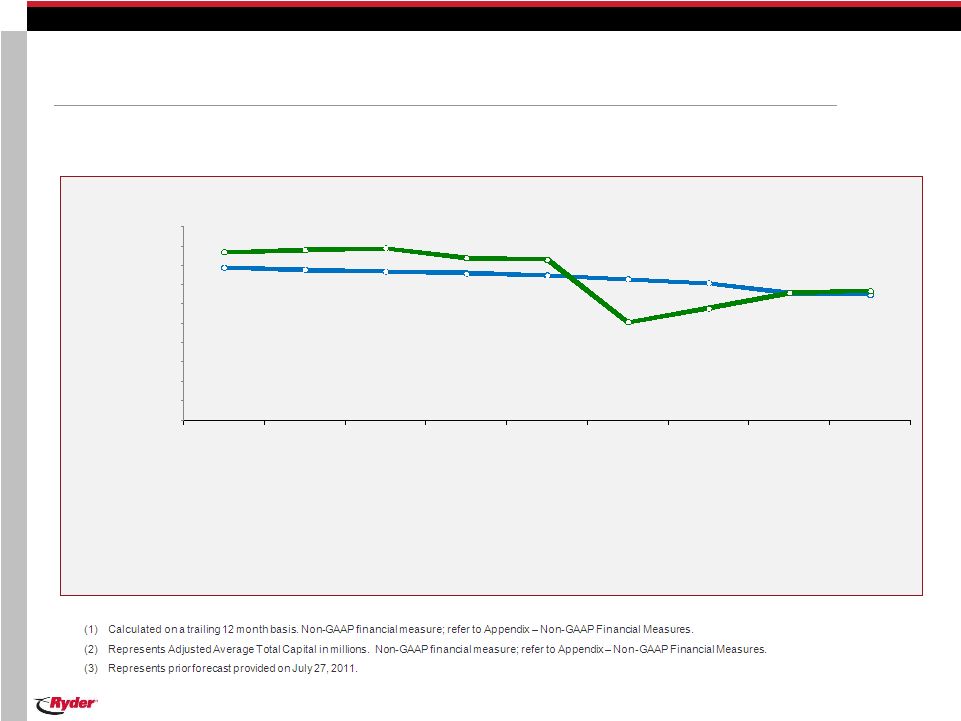

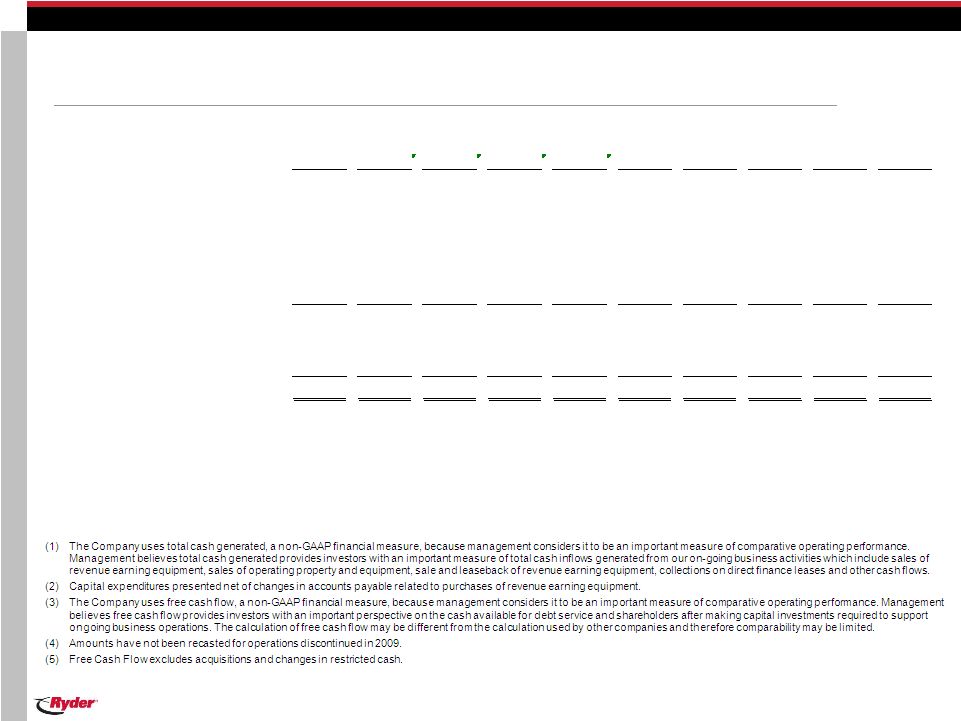

10/25/11 Proprietary and Confidential 38 Non-GAAP Financial Measures This presentation includes “non-GAAP financial measures” as defined by SEC rules. As required by SEC rules, we provide a reconciliation of each non-GAAP financial measure to the most comparable GAAP measure and an explanation why management believes that presentation of the non-GAAP financial measure provides useful information to investors. Non-GAAP financial measures should be considered in addition to, but not as a substitute for or superior to, other measures of financial performance prepared in accordance with GAAP. Specifically, the following non-GAAP financial measures are included in this presentation: Non-GAAP Financial Measure Comparable GAAP Measure Reconciliation & Additional Information Presented on Slide Titled Page Operating Revenue Total Revenue Key Financial Statistics 5-6 Earnings Before Restructuring and Income Taxes Earnings before Income Taxes from Continuing Operations Business Segments 9-10 Comparable Earnings / EPS from Continuing Operations Earnings / EPS from Continuing Operations Earnings and EPS from Continuing Operations Reconciliation 17 Comparable NBT / Tax Rate NBT / Tax Rate NBT and Tax Rate from Continuing Operations Reconciliation 40 Adjusted Return on Capital Net Earnings Adjusted Return on Capital Reconciliation 41-42 Total Cash Generated / Free Cash Flow Cash Provided by Operating Activities Cash Flow Reconciliation 45-46 Total Obligations / Total Obligations to Equity Balance Sheet Debt / Debt to Equity Debt to Equity Ratio Debt to Equity Reconciliation 13 43-44 FMS / SCS / DCC Operating Revenue and Segment NBT as % of Operating Revenue FMS / SCS / DCC Total Revenue and Segment NBT as % of Total Revenue Fleet Management Solutions / Supply Chain Solutions / Dedicated Contract Carriage 26-31 |