Southwest Oil & Gas Income Fund X-B Inactive

Filed: 2 Nov 11, 12:00am

Use these links to rapidly review the document

TABLE OF CONTENTS

Table of Contents

Item 8. Financial Statements and Supplementary Data

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. 1)

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

ý | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

o | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material under §240.14a-12 | |

| Southwest Oil & Gas Income Fund X-B, L.P. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

Payment of Filing Fee (Check the appropriate box): | ||||

o | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: Units representing limited partnership interests | |||

| (2) | Aggregate number of securities to which transaction applies: 10,004.67 Units representing limited partnership interests | |||

(3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): The maximum aggregate value of the transaction was calculated by multiplying the 10,004.67 units representing limited partnership interests held by the investors unaffiliated with Southwest Royalties, Inc. by the merger consideration of $252.08 per unit. The filing fee was determined by multiplying 0.0001146 by the maximum aggregate value of the transaction as determined in accordance with the preceding sentence. | |||

| (4) | Proposed maximum aggregate value of transaction: $2,521,977 | |||

| (5) | Total fee paid: $292 ($290 was paid on September 9, 2011. The balance of $2 is being offset against the excess fee paid in connection with the filing referenced below.) | |||

ý | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: $303 | |||

| (2) | Form, Schedule or Registration Statement No.: Schedule 14A—Preliminary Proxy Statement | |||

| (3) | Filing Party: Southwest Royalties Institutional Income Fund VII-B L.P. | |||

| (4) | Date Filed: September 9, 2011 | |||

SOUTHWEST OIL & GAS INCOME FUND X-B, L.P.

6 DESTA DRIVE, SUITE 6500, MIDLAND, TEXAS 79705

NOTICE OF SPECIAL MEETING OF LIMITED PARTNERS

TO BE HELD ON , 2011

To the Limited Partners of Southwest Oil & Gas Income Fund X-B, L.P.:

This is notice that a special meeting of the limited partners of Southwest Oil & Gas Income Fund X-B, L.P., which we refer to as the partnership, will be held on , 2011, at , at the ClayDesta Conference Center, Six Desta Drive, Suite 6550, Midland, Texas 79705. The purpose of the special meeting is for you to consider and vote on the following matters:

The accompanying proxy statement contains information about the merger and a description of the merger agreement. The proxy statement also contains a copy of the merger agreement. We urge you to read the proxy statement and the documents included with the proxy statement, including the merger agreement, in their entirety.

SWR has set the close of business on , 2011 as the record date for the limited partners who are entitled to notice of, and to vote at, the special meeting or any adjournments or postponements of the special meeting. During the 10 days before the special meeting, you may examine the list of the limited partners of the partnership at its offices during normal business hours for any purpose relevant to the special meeting.

On October 27, 2011, a committee of the board of directors of SWR, which we refer to as the transaction committee and the board of directors, respectively, by a unanimous vote, (1) considering, among other factors, the written opinion of Energy Capital Solutions, LLC described in the accompanying proxy statement, determined that the consideration to be received by the limited partners of the partnership, other than SWR, which we refer to as the unaffiliated investors, in the merger pursuant to the merger agreement is fair to the unaffiliated investors from a financial point of view, (2) determined that the merger agreement and the merger are advisable and in the best interests of the unaffiliated investors and the partnership and (3) recommended that the board of directors (a) approve the merger agreement, the merger and the other transactions contemplated by the merger agreement and (b) recommend that the unaffiliated investors vote to approve the merger agreement.

On October 27, 2011, the board of directors, relying in part on the recommendation of the transaction committee, unanimously determined that the merger is advisable and substantively and

procedurally fair to the unaffiliated investors and is in their best interests.The board of directors has approved the merger agreement, the merger and the other transactions contemplated by the merger agreement, and recommends that you vote FOR the merger proposal and FOR any proposal to adjourn or postpone the special meeting to a later date if necessary or appropriate, including an adjournment or postponement to solicit additional proxies if, at the special meeting, the number of units present or represented by proxy and voting in favor of the approval of the merger proposal is insufficient to approve the merger proposal. Although the board of directors believes that it has fulfilled its fiduciary duties to you, the members of the board of directors had conflicting interests in evaluating the merger as described in more detail in the accompanying proxy statement.

The merger will be completed only if (1) the limited partners of the partnership who own more than 50 percent of the units owned by all limited partners approve the merger agreement, the merger and the transactions contemplated by the merger agreement and (2) the unaffiliated investors who own more than 50 percent of the units owned by all unaffiliated investors present in person or by proxy at the special meeting vote their units to approve the merger agreement, the merger and the transactions contemplated by the merger agreement.

Your vote is important regardless of the number of units you own. You are requested to sign, vote and date the enclosed proxy card and return it promptly in the enclosed envelope, even if you expect to be present at the special meeting. You may also vote by telephone or over the Internet by following the instructions provided on the proxy card. If you give a proxy, you can revoke it at any time before the special meeting. If you are present at the special meeting, you may withdraw your proxy and vote in person.

If you have any questions concerning the merger or the accompanying proxy statement, would like additional copies or need help voting, please contact SWR at its principal place of business at 6 Desta Drive, Suite 6500, Midland, Texas 79705, attention McRae M. Biggar, or by telephone at (432) 682-6324.

| Southwest Oil & Gas Income Fund X-B, L.P. | ||

/s/ MICHAEL L. POLLARD Michael L. Pollard Senior Vice President Southwest Royalties, Inc. General Partner | ||

, 2011 |

Preliminary Proxy Statement, Subject to Completion

SOUTHWEST OIL & GAS INCOME FUND X-B, L.P.

6 DESTA DRIVE, SUITE 6500, MIDLAND, TEXAS 79705

, 2011

Dear Limited Partners of Southwest Oil & Gas Income Fund X-B, L.P.:

We invite you to attend a special meeting of the limited partners of Southwest Oil & Gas Income Fund X-B, L.P., which we refer to as the partnership. The special meeting will be held on , 2011, at , at the ClayDesta Conference Center, Six Desta Drive, Suite 6550, Midland, Texas 79705. The purpose of the special meeting is for you to vote on the merger of the partnership that, if completed, will result in you receiving cash for your units representing limited partnership interests of the partnership, which we refer to as the units. Clayton Williams Energy, Inc., a Delaware corporation, which we refer to as CWEI, is the sole stockholder of Southwest Royalties, Inc., a Delaware corporation and the general partner of the partnership, which we refer to as SWR, and is the beneficial owner of the general and limited partnership interests in the partnership that are owned by SWR. CWEI desires to acquire all of the units not held by SWR through the merger of the partnership into SWR. The merger will be completed only if (1) the limited partners of the partnership who own more than 50 percent of the units owned by all limited partners approve the merger agreement, the merger and the transactions contemplated by the merger agreement and (2) the limited partners of the partnership, other than SWR, who we refer to as the unaffiliated investors, who own more than 50 percent of the units owned by all unaffiliated investors present in person or by proxy at the special meeting vote their units to approve the merger agreement, the merger and the transactions contemplated by the merger agreement. Upon completion of the merger, all units, other than those held by SWR, will be converted into the right to receive cash in an amount equal to $252.08 per unit, less the amount of per unit cash distributions made after September 30, 2011, if any. SWR will not receive any cash payment for its partnership interests in the partnership. However, as a result of the merger, SWR will acquire 100% of the assets and liabilities of the partnership.

On October 27, 2011, a committee of the board of directors of SWR, which we refer to as the transaction committee and the board of directors, respectively, by a unanimous vote, (1) considering, among other factors, the written opinion of Energy Capital Solutions, LLC, which we refer to as ECS, described in this proxy statement, determined that the consideration to be received by the unaffiliated investors in the merger pursuant to the merger agreement is fair to the unaffiliated investors from a financial point of view, (2) determined that the merger agreement and the merger are advisable and in the best interests of the unaffiliated investors and the partnership and (3) recommended that the board of directors (a) approve the merger agreement, the merger and the other transactions contemplated by the merger agreement and (b) recommend that the unaffiliated investors vote to approve the merger agreement.

On October 27, 2011, the board of directors, relying in part on the recommendation of the transaction committee, unanimously determined that the merger is advisable and substantively and procedurally fair to the unaffiliated investors and is in their best interests.The board of directors has approved the merger agreement, the merger and the other transactions contemplated by the merger agreement, and recommends that you vote FOR the merger proposal and FOR any proposal to adjourn or postpone the special meeting to a later date if necessary or appropriate, including an adjournment or postponement to solicit additional proxies if, at the special meeting, the number of units present or represented by proxy and voting in favor of the approval of the merger proposal is insufficient to approve the merger proposal. Although the board of directors believes that it has fulfilled its fiduciary duties to you, members of the board of directors had conflicting interests in evaluating the merger as described in more detail in this proxy statement.

The transaction committee retained ECS to issue a fairness opinion in connection with the merger. The ECS opinion is dated as of October 27, 2011 and, subject to the qualifications expressed in such opinion, states that the merger consideration to be paid with respect to the units is fair to the

unaffiliated investors from a financial point of view. The form of the written opinion of ECS is included with this proxy statement. We urge you to read the opinion of ECS in its entirety.

Your vote is important. Whether or not you plan to attend the special meeting, please take the time to vote by completing and mailing to us the enclosed proxy card. You may also vote by telephone or over the Internet by following the instructions provided on the proxy card. This will not prevent you from revoking your proxy at any time prior to the special meeting or from voting your units in person if you later choose to attend the special meeting.

If the merger is approved, checks will be mailed to the record holders of units, other than SWR, promptly after the effective time of the merger. Checks will be mailed to the same address to which monthly distribution checks are mailed.

| Sincerely, | ||

/s/ MICHAEL L. POLLARD Michael L. Pollard Senior Vice President Southwest Royalties, Inc. General Partner |

YOU SHOULD CAREFULLY CONSIDER THE RISKS RELATING TO THE MERGER DESCRIBED IN "RISK FACTORS" ON PAGE 16. THESE INCLUDE:

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE TRANSACTION, PASSED UPON THE MERITS OR FAIRNESS OF THE TRANSACTION OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This proxy statement is dated , 2011 and is first being mailed to the limited partners on or about , 2011.

WHERE YOU CAN FIND MORE INFORMATION

The partnership files annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission, which we refer to as the SEC, under the Securities Exchange Act of 1934, which we refer to as the Exchange Act. You may read and copy any of this information at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room. The SEC also maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers, including the partnership, who file electronically with the SEC. The address of that site is www.sec.gov.

The supplement to this proxy statement contains financial and other information for the partnership. The supplement constitutes an integral part of this proxy statement. We urge you to read the supplement in its entirety.

PROXY STATEMENT

TABLE OF CONTENTS

| | Page | ||||

|---|---|---|---|---|---|

ABOUT THIS PROXY STATEMENT | 1 | ||||

SUMMARY TERM SHEET | 2 | ||||

Special Meeting | 2 | ||||

Parties to the Merger | 2 | ||||

About Clayton Williams Energy, Inc. | 3 | ||||

The Merger | 3 | ||||

Merger Consideration | 3 | ||||

Calculation of Merger Consideration | 4 | ||||

Benefits to the Unaffiliated Investors | 6 | ||||

Recommendation to Unaffiliated Investors | 7 | ||||

Conflicts | 8 | ||||

Fairness | 9 | ||||

Fairness Opinion of Financial Advisor | 9 | ||||

Material U.S. Federal Income Tax Consequences | 9 | ||||

Record Date; Voting Power | 10 | ||||

Partner Vote Required to Approve the Merger | 10 | ||||

Conditions to the Merger | 10 | ||||

Termination of the Merger | 11 | ||||

Effects of Merger on Limited Partners Who Do Not Vote In Favor of the Merger | 11 | ||||

Future of the Partnership If the Merger Is Not Completed | 11 | ||||

Expenses and Fees | 12 | ||||

Regulatory Requirements | 12 | ||||

Similar Transactions | 12 | ||||

Third Party Offers | 13 | ||||

QUESTIONS AND ANSWERS ABOUT THE MERGER | 14 | ||||

RISK FACTORS | 16 | ||||

The merger consideration involves reserve estimates that may vary materially from the quantities of oil and gas actually recovered, and consequently future net cash flows may be materially different from the estimates used in calculating the merger consideration. | 16 | ||||

The merger consideration might not reflect the current market value of the partnership's assets. | 17 | ||||

The merger consideration involves estimates that will not be adjusted. | 17 | ||||

Unaffiliated investors were not independently represented in establishing the terms of the merger. | 17 | ||||

The interests of CWEI, SWR and their officers and directors may differ from the interests of the unaffiliated investors. | 18 | ||||

The merger is conditioned on CWEI's acquisition of other limited partnerships. | 18 | ||||

The merger consideration may be less than the value potentially attainable in an alternative transaction. | 19 | ||||

Third parties may not be willing to make an offer to acquire the partnership if they cannot become operator of the partnership's properties, or a third party may discount its offer to account for the lack of operating control. | 19 | ||||

Potential litigation challenging the merger may seek to delay or block the merger. | 19 | ||||

Your units could be bound by the merger even if you do not vote in favor of the merger. | 19 | ||||

i

| | Page | ||||

|---|---|---|---|---|---|

SPECIAL FACTORS | 20 | ||||

Background of the Merger | 20 | ||||

Reasons for the Merger | 29 | ||||

Position of the Partnership Affiliates as to the Fairness of the Merger to the Unaffiliated Investors | 31 | ||||

Recommendation of the Board of Directors | 35 | ||||

Opinion of the Transaction Committee's Financial Advisor | 36 | ||||

Summary Reserve Report | 45 | ||||

Alternative Transactions to the Merger | 46 | ||||

Third Party Offers | 49 | ||||

Effects of the Merger | 49 | ||||

Effect on Net Book Value and Net Earnings of CWEI and SWR | 49 | ||||

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING INFORMATION | 50 | ||||

METHOD OF DETERMINING THE MERGER CONSIDERATION AND AMOUNT OF CASH OFFERED | 52 | ||||

Calculation of Merger Consideration | 52 | ||||

Comparison of Merger Consideration to Historical Cash Distributions | 55 | ||||

Allocation of Merger Consideration Among Partners | 55 | ||||

Other Methods of Determining Merger Consideration | 55 | ||||

THE MERGER | 57 | ||||

General | 57 | ||||

Distribution of Cash Payments | 57 | ||||

Material U.S. Federal Income Tax Consequences | 57 | ||||

Accounting Treatment | 58 | ||||

Effect of the Merger on Limited Partners Who Do Not Vote in Favor of the Merger; No Appraisal or Dissenter Rights | 58 | ||||

Future of the Partnership if the Merger Is Not Completed | 59 | ||||

Termination of Registration and Reporting Requirements | 59 | ||||

Source of Funds | 59 | ||||

Payment of Expenses and Fees | 60 | ||||

THE MERGER AGREEMENT | 61 | ||||

Structure; Effective Time | 61 | ||||

Conduct of Business Prior to the Merger | 61 | ||||

Other Agreements | 61 | ||||

Vote of Units at the Special Meeting | 62 | ||||

Representations and Warranties of SWR and the Partnership | 62 | ||||

Conditions to the Merger | 62 | ||||

Termination of the Merger and the Merger Agreement | 63 | ||||

Amendments; Waivers | 64 | ||||

Authority of the Transaction Committee | 65 | ||||

Withholding | 65 | ||||

THE SPECIAL MEETING | 66 | ||||

General Background | 66 | ||||

Record Date; Voting Rights and Proxies | 66 | ||||

Revocation of Proxies | 67 | ||||

Solicitation of Proxies | 67 | ||||

Quorum | 68 | ||||

Required Vote; Broker Non-Votes | 68 | ||||

Participation by Assignees | 68 | ||||

Special Requirements for Certain Limited Partners | 69 | ||||

Validity of Proxy Cards | 69 | ||||

Local Laws | 69 | ||||

ii

| | Page | ||||

|---|---|---|---|---|---|

INTERESTS OF CWEI, SWR AND THEIR DIRECTORS AND OFFICERS | 70 | ||||

Conflicting Duties of SWR, Individually and as General Partner; Financial Interests of Officers and Directors | 70 | ||||

Employees of CWEI Provide Services to the Partnership | 71 | ||||

Operation of Oil and Gas Properties | 71 | ||||

Farm-Out Arrangements with SWR | 71 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT OF PARTNERSHIP INTERESTS | 72 | ||||

TRANSACTIONS AMONG THE PARTNERSHIP, CWEI, SWR AND THEIR DIRECTORS AND OFFICERS | 73 | ||||

MANAGEMENT | 74 | ||||

Clayton Williams Energy, Inc. | 74 | ||||

Southwest Royalties, Inc. | 75 | ||||

INDEPENDENT AUDITORS | 77 | ||||

INDEPENDENT PETROLEUM ENGINEERING CONSULTANTS | 77 | ||||

COMMONLY USED OIL AND GAS TERMS | 78 | ||||

LIST OF APPENDICES

| | | Appendix | |||||

|---|---|---|---|---|---|---|---|

General Information | A-1 | ||||||

Table 1 | Historical Cash Distributions to Limited Partners | A-2 | |||||

Table 2 | Quarterly Repurchase Prices and Aggregate Payments | A-3 | |||||

Table 3 | Production, Average Prices and Production Costs | A-4 | |||||

Table 4 | Proved Reserves Attributable to the General Partner and Limited Partners | A-5 | |||||

Table 5 | Summary Proposals from Prospective Equity Partners | A-6 | |||||

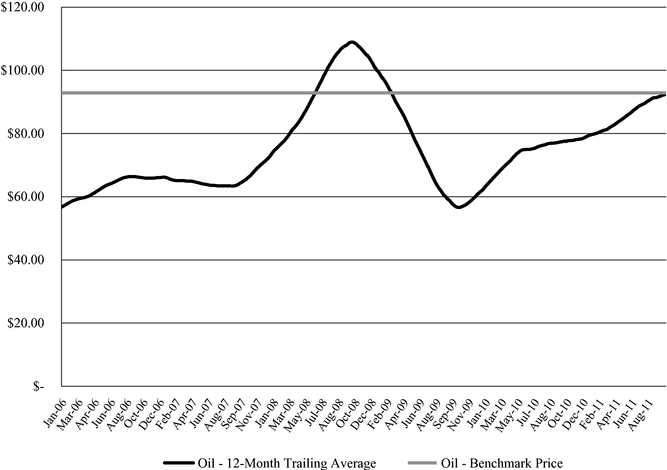

Table 6 | 12-Month Trailing Average of Closing NYMEX Futures Prices for Oil Compared to Benchmark Price of $92.84 per Bbl | A-7 | |||||

Reserve Audit Report of Ryder Scott Company, L.P. for the Partnership as of July 1, 2011 | B-1 | ||||||

Summary Reserve Report of Ryder Scott Company, L.P. for the Partnership as of December 31, 2010 | C-1 | ||||||

Fairness Opinion of Energy Capital Solutions, LLC | D-1 | ||||||

Agreement and Plan of Merger | E-1 | ||||||

WE HAVE PREPARED A SUPPLEMENT TO THIS PROXY STATEMENT, WHICH INCLUDES:

THE SUPPLEMENT CONSTITUTES AN INTEGRAL PART OF THIS PROXY STATEMENT. WE URGE YOU TO READ THE SUPPLEMENT IN ITS ENTIRETY.

iii

The definitions set forth below shall apply to the indicated terms as used in this proxy statement.

"board of directors" means the board of directors of SWR.

"CWEI" means Clayton Williams Energy, Inc., the sole stockholder of SWR.

"ECS" means Energy Capital Solutions, LLC, the independent financial advisory firm engaged by the transaction committee.

"Exchange Act" means the Securities Exchange Act of 1934.

"limited partners" means the limited partners of the partnership.

"merger" means the merger of the partnership into SWR.

"merger agreement" means the merger agreement between SWR and the partnership pursuant to which the merger will occur.

"merger proposal" means the proposal to approve the merger agreement.

"partnership" means Southwest Oil & Gas Income Fund X-B, L.P.

"partnership agreement" means our agreement of limited partnership as amended or modified.

"partnership affiliates" means CWEI and SWR.

"Ryder Scott" means Ryder Scott Company, L.P., independent engineering consulting firm.

"SEC" means the Securities and Exchange Commission.

"stated valuation date" means October 7, 2011, the latest practicable date through which historical oil and gas pricing information was available for calculating the merger consideration.

"SWR," "we," "our" and "us" mean Southwest Royalties, Inc., the general partner of the partnership and a wholly owned subsidiary of CWEI, unless the context otherwise requires.

"SWR partnerships" means the partnership and each of the 23 other oil and gas drilling and income partnerships in which SWR is the general partner.

"transaction committee" means the transaction committee of the board of directors. The members of the transaction committee are Ted Gray, Jr. and Davis L. Ford. Mr. Gray and Dr. Ford are also members of the board of directors of CWEI.

"trading day" means any day on which barrels of oil are traded on the NYMEX.

"unaffiliated investors" means the limited partners of the partnership, other than SWR.

"units" means units representing limited partnership interests in the partnership.

For definitions of oil and gas terms used in this proxy statement, see "Commonly Used Oil and Gas Terms" on page 78.

You should rely only on the information contained in this proxy statement to vote on the merger proposal. We have not authorized anyone to give any information that is different from that contained in this proxy statement. This proxy statement is dated , 2011. You should not assume that the information contained in this proxy statement is accurate as of any date other than that date and the mailing of this proxy statement to you shall not create an implication to the contrary.

1

This summary term sheet highlights selected information from this proxy statement and may not contain all of the information that is important to you. To understand the merger and the merger agreement and to obtain a description of the legal terms and conditions of the merger, you should carefully review this entire proxy statement, including the tables and appendices, which include a copy of the merger agreement and the fairness opinion of the independent financial advisory firm engaged by the transaction committee.

Southwest Royalties, Inc.

Southwest Oil & Gas Income Fund X-B, L.P.

2

The principal place of business for each of the parties to the merger is 6 Desta Drive, Suite 6500, Midland, Texas 79705, and the telephone number is (432) 682-6324. For additional information, see "Interests of CWEI, SWR and Their Directors and Officers" on page 70, "Transactions Among the Partnership, CWEI, SWR, and Their Directors and Officers" on page 73 and "Management" on page 74.

About Clayton Williams Energy, Inc.

The principal place of business for CWEI is 6 Desta Drive, Suite 6500, Midland, Texas 79705, and the telephone number is (432) 682-6324. For additional information about CWEI, see "Interests of CWEI, SWR and Their Directors and Officers," on page 70, "Transactions Among the Partnership, CWEI, SWR and Their Directors and Officers" on page 73 and "Management" on page 74.

3

| | Sharing Percentage | Amount | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Allocation of Merger Consideration: | ||||||||||

SWR as general partner | 10 | % | $ | 304,991 | ||||||

All limited partners as a group | 90 | % | 2,744,922 | |||||||

Total merger consideration | 100 | % | $ | 3,049,913 | ||||||

Allocation among limited partners: | ||||||||||

SWR | 8.121 | % | $ | 222,924 | ||||||

Unaffiliated investors as a group | 91.879 | % | 2,521,998 | |||||||

Total limited partners as a group | 100.000 | % | $ | 2,744,922 | ||||||

Summary of merger consideration by group: | ||||||||||

SWR as general and limited partner | 17.309 | % | $ | 527,915 | ||||||

Unaffiliated investors as a group | 82.691 | % | 2,521,998 | |||||||

Total merger consideration | 100.000 | % | $ | 3,049,913 | ||||||

Selected data applicable to unaffiliated investors: | ||||||||||

Total number of limited partnership units | 10,889.00 | |||||||||

Units held by unaffiliated investors as a group | 10,004.67 | |||||||||

Percentage of units held by unaffiliated investors as a group | 91.879 | % | ||||||||

Merger consideration allocated to unaffiliated investors as a group | $ | 2,521,998 | ||||||||

Merger consideration per unit | $ | 252.08 | ||||||||

Initial investment per unit | $ | 500.00 | ||||||||

Summary of cash return per unit: | ||||||||||

Cumulative cash distributions since inception | $ | 760.95 | ||||||||

Merger consideration | 252.08 | |||||||||

Total cash return, assuming consummation of merger | $ | 1,013.03 | ||||||||

Total cash return as a percentage of initial investment | 203 | % | ||||||||

Calculation of Merger Consideration

4

data maintained by SWR in conjunction with its responsibilities as operator of the properties and as general partner of the partnership.

Estimated fair value of oil and gas reserves | $ | 3,127,785 | |||

Net working capital | 260,567 | ||||

Net asset retirement obligations | (263,439 | ) | |||

Total enterprise value as of June 30, 2011 | 3,124,913 | ||||

Cash distributions after June 30, 2011 | (75,000 | ) | |||

Total merger consideration | $ | 3,049,913 | |||

5

Benefits to the Unaffiliated Investors

We believe the merger provides the following benefits to the unaffiliated investors:

6

levels generally decline and operating costs, particularly repair and maintenance costs, generally increase. To reverse this trend, the partnership would need to acquire additional properties to replace the reserves being produced. However, the partnership is a single purpose entity formed to own and operate certain properties. The partnership agreement does not permit the partnership to borrow money, assess its partners for additional capital contributions or reinvest operating cash flow in new property acquisitions. As a result, the partnership's production is expected to continue to decline. Declining production and increasing costs create adverse pressures on cash flow and make it difficult for the partnership to pay its fixed administrative costs and still be able to accumulate meaningful levels of distributable cash. We believe that unaffiliated investors will benefit by liquidating their holdings in the partnership's assets through the merger.

Recommendation to Unaffiliated Investors

7

8

In deciding to approve the merger, the board of directors determined that the merger is advisable and fair to the unaffiliated investors and is in their best interests based on a variety of factors. These factors include:

For additional information, see "Special Factors—Position of the Partnership Affiliates as to the Fairness of the Merger to the Unaffiliated Investors" on page 31 and "Special Factors—Recommendation of the Board of Directors" on page 35.

Fairness Opinion of Financial Advisor

Material U.S. Federal Income Tax Consequences

9

ordinary depending on the nature of the assets held by the partnership and the amount of any depletion, depreciation and intangible drilling and development costs that is subject to recapture.

Partner Vote Required to Approve the Merger

10

partnerships as described under "—Similar Transactions." If the limited partners of at least a majority of the other SWR partnerships do not approve the merger of their respective partnerships into SWR, or if the mergers of the other SWR partnerships into SWR are not completed for any reason, this condition to the merger will not be satisfied, and SWR may elect to abandon the merger.

Effects of Merger on Limited Partners Who Do Not Vote In Favor of the Merger

Future of the Partnership If the Merger Is Not Completed

11

or the unaffiliated investors are not obtained, (2) a condition to the merger agreement is not satisfied or (3) SWR or the partnership exercises a termination right with respect to the merger.

12

13

QUESTIONS AND ANSWERS ABOUT THE MERGER

When and where is the special meeting of the limited partners?

The special meeting will be held on , 2011, at , at the ClayDesta Conference Center, Six Desta Drive, Suite 6550, Midland, Texas 79705.

What is the structure of the merger?

CWEI proposes to acquire all of the units not held by SWR by merging the partnership into SWR. SWR will be the surviving entity in the merger.

What will approval of the merger mean for me?

Upon consummation of the merger, all of the outstanding units, other than those held by SWR, will be converted into the right to receive cash in an amount equal to $252.08 per unit, less the sum of per unit cash distributions made after September 30, 2011, if any. SWR will not receive any cash payment for its partnership interests in the partnership. However, as a result of the merger, SWR will acquire 100% of the assets and liabilities of the partnership.

How do I vote my units?

You may grant a proxy by dating, signing and mailing your proxy card or by voting by telephone or over the Internet. You may also attend the special meeting and cast your vote in person at the meeting.

What happens if I do not return a proxy card?

The merger will be completed only if (1) the limited partners of the partnership who own more than 50 percent of the units owned by all limited partners approve the merger agreement, the merger and the transactions contemplated by the merger agreement and (2) the unaffiliated investors who own more than 50 percent of the units owned by all unaffiliated investors present in person or by proxy at the special meeting vote their units to approve the merger agreement, the merger and the transactions contemplated by the merger agreement. For purposes of the limited partner vote described in clause (1) above, the failure to return your proxy card will have the same effect as voting against the merger. If, however, the limited partner vote is obtained, the failure to return your proxy card will not have any effect on the investor vote described in clause (2) above. Only units owned by unaffiliated investors present in person or by proxy at the special meeting will be considered in determining whether the vote of the unaffiliated investors has been obtained. SWR is entitled to vote the units it holds as a limited partner at the special meeting and has agreed in the merger agreement to vote all of its units in favor of the merger proposal.

What does the general partner recommend that I do?

The board of directors, relying in part on the recommendation of the transaction committee, recommends that you voteFOR the merger proposal andFOR any proposal to adjourn or postpone the special meeting to a later date if necessary or appropriate, including an adjournment or

14

postponement to solicit additional proxies if, at the special meeting, the number of units present or represented by proxy and voting in favor of the approval of the merger proposal is insufficient to approve the merger proposal.

May I change my vote after I have returned my signed proxy?

Yes. You may change your vote at any time before your proxy is voted at the special meeting by following the instructions on page 67. You then may either change your vote by sending in a new proxy card, changing your vote by telephone or over the Internet or by attending the special meeting.

Am I entitled to appraisal or dissenters' rights?

No. You will not have any appraisal, dissenters' or similar rights in connection with the merger.

What happens to my future cash distributions?

You will continue to receive distributions made by the partnership until the merger is completed. The merger consideration will be reduced by the sum of the per unit cash distributions made subsequent to September 30, 2011, if any. If the merger is completed, your units will be cancelled upon completion of the merger, and you will not receive future distributions on those units.

What are the tax implications of the transaction?

You will generally recognize gain or loss equal to the difference between your amount realized in the merger and your adjusted tax basis in your units. Your gain or loss will be capital or ordinary depending on the nature of the assets held by the partnership and the amount of depletion, depreciation and intangible drilling and development costs that is subject to recapture.

What effect will the merger have on my Schedule K-1 tax report?

In 2012, you will receive your 2011 Schedule K-1 tax report reflecting 2011 taxable income. If the merger is approved and completed in 2011, your 2011 Schedule K-1 tax report will be your final Schedule K-1 tax report. After the merger is completed, you will have no continuing interest in the partnership and you will not receive Schedule K-1 tax reports for the partnership for tax years after the year in which the merger occurs. We believe the merger will simplify your individual tax return preparation and reduce your tax preparation costs.

When is the proposed transaction expected to be completed?

We intend to complete the proposed transaction as soon as practicable following limited partner and unaffiliated investor approval. If the merger is approved, we estimate that the closing of the merger will occur on or before , 2011.

Who can help answer my questions?

If you have any questions concerning the merger or this proxy statement, would like additional copies or need help voting, please contact SWR at its principal place of business at 6 Desta Drive, Suite 6500, Midland, Texas 79705, attention McRae M. Biggar, or by telephone at (432) 682-6324.

15

You should carefully consider the following risk factors in determining whether to vote to approve the merger proposal.

The merger consideration involves reserve estimates that may vary materially from the quantities of oil and gas actually recovered, and consequently future net cash flows may be materially different from the estimates used in calculating the merger consideration.

The calculations of the partnership's estimated reserves of crude oil, natural gas liquids and natural gas and calculations of future net cash flows from those reserves included in this proxy statement are only estimates. The accuracy of any estimate of proved reserves is a function of:

Actual prices, production, operating expenses and quantities of recoverable oil and natural gas reserves may vary from those assumed in the estimates. Any significant variance from the assumptions used could result in the actual quantity of the partnership's reserves and future net cash flows being materially different from the estimates used in the calculation of the merger consideration. If a significant variance occurs, the merger consideration you will receive may not be a reflection of the actual value of the partnership's reserves.

SWR estimated the partnership's proved reserves based on production curves used in the December 31, 2010 evaluation made by Ryder Scott, with additional adjustments to the production curves made to reflect changes in well performance based on updated production information through March 2011. The recoverable reserves volumes and the related future net cash flows from those reserves were based on benchmark prices of $92.84 per Bbl of oil and NGL and $4.15 per MMBtu of natural gas. These benchmark prices, which were computed based on the 12-month historical average of the NYMEX closing prices for oil and gas through the stated valuation date, were further adjusted for quality, energy content, transportation fees and other price differentials specific to the partnership's properties, resulting in an average price of $84.88 per Bbl of oil and $5.56 per Mcf of natural gas. Estimated future operating costs were deducted in arriving at the estimated fair value of oil and gas reserves and include direct operating expenses, field overhead costs, and ad valorem taxes. Costs of workovers, well stimulations, and other significant non-recurring maintenance costs are not included in estimated future operating costs. Operating costs were held constant for the life of the properties.

The discount rates that were applied to the estimated future net cash flows from the partnership's proved reserves to determine the merger consideration were determined by CWEI and SWR. Lower discount rates would result in higher merger consideration and lower potential return to CWEI on its investment in the partnership's underlying assets. Conversely, higher discount rates would result in lower merger consideration and greater potential return on CWEI's investment in those assets. Furthermore, higher discount rates may disfavor longer-lived properties when compared to shorter-lived properties. In establishing these discount rates, CWEI considered various factors, including (1) its

16

desire and commitment to offer merger consideration that is fair to both the unaffiliated investors and the CWEI stockholders, (2) its cost of capital for the merger and (3) a reasonable profit incentive relative to the production, pricing and timing risks associated with the future cash flows from the partnership's assets. Although CWEI believes these discount rates are within the range of discount rates commonly used in the oil and gas industry in property acquisition transactions, the discount rates applied in the calculation of the merger consideration may not reflect the actual cost of capital in effect from time to time, the specific risks associated with the partnership's properties or the general risks of ownership of oil and gas properties in general.

The merger consideration might not reflect the current market value of the partnership's assets.

Since the merger consideration is based on assumptions about reserves, production, commodity prices and costs that may prove to be inaccurate, the merger consideration could vary materially from the current market value of, or the price that a third party might offer for, the partnership's estimated oil and gas reserves and from the value given to the partnership's actual future net revenues. The assumptions used to determine the merger consideration might not properly reflect the value of the partnership's assets. In that case, you could receive merger consideration that is less than a fair market price for your units.

The merger consideration involves estimates that will not be adjusted.

Actual prices, production, operating expenses and quantities of recoverable oil and natural gas reserves may vary from those assumed in the estimates considered for purposes of calculating the merger consideration. The variances could be significant. Any significant variance from the assumptions used could result in the actual quantity of the partnership's reserves and future net revenues being materially different from the estimates in the partnership's reserve reports and in the calculation of the merger consideration. In addition, changes in production levels and changes in crude oil, natural gas liquids and natural gas prices after the date of the estimate could result in substantial upward or downward revisions to estimated reserves. We do not expect to adjust the merger consideration for any such changes.

Unaffiliated investors were not independently represented in establishing the terms of the merger.

CWEI and SWR established the merger consideration and the transaction committee negotiated the merger agreement and the transactions contemplated by the merger agreement on behalf of the partnership and the unaffiliated investors. The board of directors, relying in part on the recommendation of the transaction committee, unanimously determined that the merger consideration is substantively and procedurally fair to the unaffiliated investors and is in their best interests. Members of the board of directors, including members of the transaction committee, had conflicting interests in evaluating the merger. Moreover, although the transaction committee was formed to negotiate the terms of the merger on behalf of the partnership and the unaffiliated investors, no committee or other entity independent of SWR or CWEI was formed or engaged to negotiate on your or the partnership's behalf. The transaction committee was authorized to review, evaluate and negotiate the terms of the merger on behalf of the unaffiliated investors; however, the transaction committee is not authorized to develop, solicit, initiate or pursue any potential alternatives to the merger. No representative group of unaffiliated investors and no outside experts or consultants, such as investment bankers, legal counsel, accountants or financial experts, were engaged solely to represent the interests of the unaffiliated investors in structuring and negotiating the terms of the merger. If the unaffiliated investors had been separately represented, the terms of the merger might have been different and possibly more favorable to the unaffiliated investors.

17

The interests of CWEI, SWR and their officers and directors may differ from the interests of the unaffiliated investors.

The interests of CWEI, SWR and their officers and directors may differ from interests of the unaffiliated investors. SWR, as the general partner of the partnership, has a duty to manage the partnership in the best interests of the limited partners. However, SWR also has a duty to operate its business for the benefit of CWEI, its sole stockholder. Consequently, SWR's duties to CWEI may conflict with its duties to the unaffiliated investors.

Members of the board of directors have a duty to cause SWR to manage the partnership in the best interests of the limited partners. However, members of the board of directors also have a duty to operate SWR's business for the benefit of CWEI, its sole stockholder, and board members who are also officers of SWR have a duty to operate SWR's business in SWR's best interests. Each member of the board of directors is also a member of the board of directors of CWEI. Members of the board of directors of CWEI have a duty to operate CWEI's business for the benefit of its stockholders. Two members of the board of directors are also officers of CWEI, and therefore have a duty to operate CWEI's business in the best interests of CWEI and its stockholders. In addition, one member of the board of directors, Clayton W. Williams, Jr., beneficially owns approximately 26% of the outstanding common stock of CWEI, and a partnership in which his adult children are limited partners owns approximately 25% of the outstanding common stock of CWEI. Members of the board of directors may have an indirect financial interest in the merger, as stockholders of CWEI or as officers of CWEI and SWR, and such interest may conflict with the interests of the unaffiliated investors. Consequently, the duties of members of the board of directors to the unaffiliated investors may conflict with the duties of those members to SWR and CWEI. The board of directors was aware of these interests and considered them in approving the merger proposal. See "Special Factors—Position of the Partnership Affiliates as to the Fairness of the Merger to the Unaffiliated Investors" and "Interests of CWEI, SWR and Their Directors and Officers."

Because both members of the transaction committee are also members of the boards of directors of SWR and CWEI, an inherent conflict may continue to exist with respect to each member's duties to the unaffiliated investors in his capacity as a member of the transaction committee, on the one hand, and such member's duties to SWR, CWEI and the stockholders of CWEI in his capacity as a member of the boards of directors of SWR and CWEI, on the other hand. The creation of the transaction committee did not eliminate these inherent conflicts of interests. In addition, members of the transaction committee are stockholders of CWEI and may have an indirect financial interest in the merger as stockholders of CWEI, which varies from the interests of the unaffiliated investors.

The merger is conditioned on CWEI's acquisition of other limited partnerships.

CWEI is also proposing to acquire each of the other SWR partnerships. Concurrently with the execution of the merger agreement, SWR and each other SWR partnership entered into a merger agreement pursuant to which such SWR partnership will merge into SWR. The terms and conditions of the other merger agreements are substantially similar to the terms and conditions of the merger agreement (other than financial terms) set forth in this proxy statement for the merger. The merger is conditioned on the fulfillment (or waiver in whole or in part by SWR in its sole discretion) of each of the conditions to our obligation to effect the mergers of at least a majority of the other SWR partnerships. If the limited partners of at least a majority of the other SWR partnerships do not approve the merger of their respective partnerships into SWR, or if the mergers of the other SWR partnerships into SWR are not completed for any reason, this condition to the merger will not be satisfied, and we may elect to abandon the merger.

18

The merger consideration may be less than the value potentially attainable in an alternative transaction.

CWEI is not offering to sell its beneficial interests in the partnership or the partnership's properties. CWEI did not consider the value that could be obtained in an alternative transaction, including the sale of all of the partnership properties and operational control of the properties to a third party. The transaction committee was authorized to review, evaluate and negotiate the terms of the merger on behalf of the unaffiliated investors; however, the transaction committee is not authorized to develop, solicit, initiate or pursue any potential alternatives to the merger. As a result, the merger consideration may be less than the value potentially attainable in an alternative transaction.

Third parties may not be willing to make an offer to acquire the partnership if they cannot become operator of the partnership's properties, or a third party may discount its offer to account for the lack of operating control.

SWR operates many of the partnership's wells on behalf of the partnership and others who own interests in those wells, including SWR. Since CWEI is not offering to sell or otherwise dispose of its beneficial interests in the partnership or the partnership's properties, SWR will retain its right to operate the partnership's properties. Consequently, potential buyers may not be interested in making an offer to acquire the partnership if they cannot also acquire operating rights to the partnership's properties, or if they do make an offer, they may discount the offer to give effect to the lack of operating control.

Potential litigation challenging the merger may seek to delay or block the merger.

One or more unaffiliated investors opposed to the merger may initiate legal action to seek to prevent the merger or to seek damages for alleged violations of federal and state laws. Litigation challenging the merger may delay or prevent the closing of the merger. In addition, if any lawsuits are filed, the partnership or SWR may decide to terminate the merger.

Your units could be bound by the merger even if you do not vote in favor of the merger.

Your units will be bound by the merger if (1) the limited partners of the partnership who own more than 50 percent of the units owned by all limited partners approve the merger agreement, the merger and the transactions contemplated by the merger agreement and (2) the unaffiliated investors who own more than 50 percent of the units owned by all unaffiliated investors present in person or by proxy at the special meeting vote their units to approve the merger agreement, the merger and the transactions contemplated by the merger agreement, even if you vote against the merger or do not vote. If the merger occurs, you will be entitled to receive only the per unit cash merger consideration described in this proxy statement. You will not have appraisal, dissenters' or similar rights in connection with the merger, even if you vote against the merger.

19

The partnership was formed in 1990 under the sponsorship of SWR. In 1995, SWR stopped sponsoring any new oil and gas development drilling and income partnerships to focus on acquiring and developing oil and gas properties for its own account. CWEI acquired SWR in 2004.

From time to time since 2004, CWEI has had general, internal discussions about whether to consolidate or liquidate the SWR partnerships. On occasion, CWEI has discussed various aspects of the consolidation or liquidation of the SWR partnerships with legal and financial advisors. The contemplated structure of possible transactions has varied significantly in these internal discussions and has included asset sales, mergers, tender offers and combinations of those types of transactions. See "—Reasons for the Merger" for a discussion of why CWEI and SWR selected the merger. In general, the transaction structures considered by CWEI, including the merger, would have been taxable to the limited partners of each SWR partnership because of the difficulties involved in structuring tax-free transactions for the SWR partnerships. Until 2010, each time CWEI considered such a transaction, it decided not to proceed with the transaction. The reasons CWEI did not previously proceed with a transaction varied and included volatility in oil and gas prices, the availability of financial resources, and other operating, financial and resource priorities.

In July 2010, CWEI assigned a higher priority to pursuing a possible consolidation of the SWR partnerships. The following factors were considered in making this decision:

In September 2010, CWEI had various internal discussions, as well as discussions with outside legal counsel, regarding a possible transaction involving an auction or negotiated sale of fractional interests in the oil and gas properties owned by the SWR partnerships, followed by a liquidation and dissolution of the SWR partnerships. CWEI contemplated that the limited partners of the SWR partnerships, other than SWR, would receive cash liquidating distributions and SWR would receive a liquidating distribution of the fractional interests in oil and gas properties not acquired by the third party purchasers. CWEI was concerned, however, that the transaction costs required to sell fractional interests in the properties in an auction or in a negotiated transaction would be significant and would have to be absorbed by the SWR partnerships even if the auction or negotiated transaction was not successful. CWEI believed that a sale of the partnership's properties on a direct basis would involve

20

substantial periods of time for title, technical and environmental due diligence, negotiation and execution of agreements and closings.

CWEI was also concerned that, since third party purchasers would be purchasing many oil and gas interests that they would neither control nor operate, SWR's control of such properties could negatively affect the amount that a third party would be willing to pay and the overall interest of third parties in buying such properties.

Based on all of these concerns, CWEI determined that an auction or negotiated sale of a portion of the SWR partnerships was not the best alternative for liquidating or consolidating the SWR partnerships. Because CWEI did not proceed with an auction or negotiated sale of a portion of the SWR partnerships, the value that could be obtained in such a transaction was not considered in establishing, or in determining the fairness of, the merger consideration.

Following CWEI's determination that an auction or negotiated sale of a portion of the SWR partnerships' properties was not the best alternative for liquidation or consolidation of the SWR partnerships, CWEI began to pursue the possibility of consolidating the SWR partnerships by merging the SWR partnerships into an acquisition entity to be formed for that purpose. As a result of such merger, the acquisition entity would have acquired for cash all the limited partnership interests of the SWR partnerships, other than those held by SWR. In connection with that possible consolidation transaction, CWEI would contribute SWR's general and limited partnership interests in each of the SWR partnerships to the acquisition entity in exchange for an equity interest in the acquisition entity. Furthermore, CWEI would seek a third party equity partner to contribute cash to the acquisition entity in exchange for the remaining equity interest in the acquisition entity. The proceeds from the equity financing transaction would be utilized by the acquisition entity to fund the consideration payable to the holders of limited partnership interests of the SWR partnerships, other than SWR. Following the consolidation, SWR would continue to own an interest in the SWR partnership properties through a minority ownership interest in the acquisition entity, and the equity partner would own a majority ownership interest in the acquisition entity. SWR would continue to operate the SWR partnerships properties. The acquisition entity would succeed to all of the SWR partnerships assets and liabilities by merger, which is a more efficient way to transfer title than effecting individual assignments of specified property interests.

CWEI believed that a consolidation of the SWR partnerships structured in this manner would achieve the following desired results:

In October 2010, CWEI began identifying and qualifying prospective equity partners to fund the acquisition by the acquisition entity of the units not owned by SWR. Since under the proposed structure, SWR would not receive any portion of the merger consideration and was not affected in any way by the value placed on such units in any third party valuation, CWEI's primary objective was to manage the valuation process fairly and to solicit the highest and best offer on behalf of the unaffiliated investors. To meet CWEI's qualifications, any prospective equity partner would need to demonstrate that it could consummate the merger, that it was financially sound, that it would adhere to high ethical standards in the conduct of business and that its expectations for the future activities of the

21

acquisition entity were compatible with those of CWEI. Finally, because CWEI was not willing to sell its beneficial interests in the SWR partnerships or their assets, or to relinquish operational control of the SWR partnerships' properties, any prospective equity partner would have to agree that it would not have control over the properties of the SWR partnerships.

Beginning in November 2010, CWEI discussed the possible consolidation of the SWR partnerships with five prospective equity partners. CWEI provided the prospective equity partners with information about the SWR partnerships, including reserve reports, historical operating information, financial statements, acreage tables and maps of major fields. CWEI asked the prospective equity partners to submit proposals in which an enterprise value as of December 31, 2010 was assigned to each SWR partnership. In January 2011, CWEI received preliminary, non-binding proposals from four of the prospective equity partners. In early February 2011, CWEI terminated discussions with the two prospective equity partners that had assigned the lowest aggregate enterprise values to the SWR partnerships. Because neither of the two remaining prospective equity partners had assigned the highest enterprise value to all of the SWR partnerships, CWEI asked that they reevaluate their proposals. CWEI informed the two remaining prospective equity partners that it would require one of them to have assigned the highest enterprise to all of the SWR partnerships. CWEI advised them that, based on the next round of proposals, the prospective equity partners assigning the aggregate high enterprise value to the SWR partnerships would be given an opportunity to match the enterprise value assigned by the other prospective equity partner.

In February 2011, CWEI received revised preliminary, non-binding proposals from the two remaining prospective equity partners. Neither of the prospective equity partners assigned the highest enterprise value to all of the SWR partnerships. However, the prospective equity partner that assigned the highest enterprise value to the SWR partnerships in the aggregate agreed to match the high enterprise values assigned to each SWR partnership individually by the other prospective equity partner and submitted a preliminary, non-binding proposal. The preliminary, non-binding proposal was subject to numerous conditions, including completion of due diligence and negotiation of definitive equity financing documents on terms mutually acceptable to the prospective equity partner and CWEI, and was subject to withdrawal at any time in the sole discretion of the prospective equity partner.

Table 5 of Appendix A includes information on the various proposals, including the high, low and average December 31, 2010 enterprise values assigned by the prospective equity partners and the corresponding high, low and average implied per unit values, on an actual basis and on an adjusted basis deducting cash distributions during the nine months ended September 30, 2011. Under the preliminary and non-binding terms of the equity financing proposals described above, the amount of per unit cash distributions would have been deducted from the consideration payable in connection with the possible consolidation of the SWR partnerships. Therefore, we believe that the adjusted enterprise values and implied per unit values facilitate the comparison of the enterprise values assigned by the prospective equity partners and the corresponding implied per unit values to the merger consideration.

From late February 2011 through mid-April 2011, CWEI had various discussions with the prospective equity partner regarding proposed terms of the consolidation transaction and the operating agreement for the acquisition entity. CWEI provided additional due diligence information to the prospective equity partner. During this period of time, CWEI began having concerns that the proposals it had received from the prospective equity partner were too low, in the aggregate, based on improvements in oil prices that had occurred subsequent to October 2010. Additionally, CWEI had concerns that the prospective equity partner would require control over the acquisition entity and the assets of the SWR partnerships. CWEI's willingness to effect a consolidation of the SWR partnerships had consistently been conditioned on SWR's retention of control over the assets of the SWR partnerships.

22

In April 2011, CWEI concluded that the aggregate, final enterprise values for the SWR partnerships submitted by the prospective equity partner may not have accurately reflected the enterprise value of the SWR partnerships because they did not give effect to increases in oil prices. CWEI was concerned that the fairness process could be compromised if CWEI negotiated increases in the merger values exclusively with the remaining prospective equity partner. CWEI also determined that it was not willing to solicit new proposals from other prospective equity partners.

CWEI believed that soliciting new proposals from other prospective equity partners would have required significant time to disseminate data to such prospective equity partners, plus the time needed to deal directly with multiple prospective equity partners. In addition, based on discussions with the remaining prospective equity partner, CWEI concluded that it was unlikely that CWEI would be able to negotiate an acceptable agreement with the remaining prospective equity partner regarding future operations and business objectives of the acquisition entity.

In April 2011, CWEI initiated preliminary discussions with an affiliate of JPMorgan Chase & Co. regarding various production-based financing alternatives available to CWEI to fund the merger consideration payable in connection with the merger of the SWR partnerships. CWEI believed that these financing alternatives could allow CWEI to achieve two of its desired results for the consolidation transaction: (1) a third party would provide funds for the merger consideration without CWEI being required to incur indebtedness or raise equity to fund the acquisition of the units owned by the unaffiliated investors; and (2) CWEI would retain operational control over the acquisition entity and the assets of the SWR partnerships. As a result, CWEI terminated discussions with the prospective equity partners and began pursuing a direct merger between the SWR partnerships and an affiliate of CWEI or SWR.

In an attempt to formally address the potential conflicts of interest inherent in the relationships among CWEI, SWR, the SWR limited partnerships and the officers and directors of CWEI and SWR, CWEI, as the sole stockholder of SWR, elected Dr. Ford and Mr. Gray to the board of directors on May 23, 2011. Dr. Ford and Mr. Gray are also members of the board of directors of CWEI. Because Dr. Ford and Mr. Gray are members of both the board of directors of SWR and the board of directors of CWEI, an inherent conflict may continue to exist with respect to each of their duties to the unaffiliated investors and their duties to SWR, CWEI and the stockholders of CWEI. See "Interests of CWEI, SWR and their Directors and Officers."

On June 14, 2011, representatives of Vinson & Elkins L.L.P., which we refer to as Vinson & Elkins, counsel to CWEI, met with representatives of Jackson Walker L.L.P., which we refer to as Jackson Walker, to discuss the proposed mergers of the SWR partnerships into SWR and the potential appointment of Dr. Ford and Mr. Gray to the transaction committee. Following the meeting on June 14, 2011, representatives of Vinson & Elkins and Jackson Walker, on behalf of CWEI and the transaction committee, respectively, regularly discussed the terms of the mergers of the SWR partnerships into SWR and the timeline for completing the mergers. On June 29, 2011, the board of directors, by a unanimous vote, appointed Dr. Ford and Mr. Gray to the transaction committee. The transaction committee is authorized to review, evaluate and negotiate the terms of the merger on behalf of the unaffiliated investors; however, the transaction committee is not authorized to develop, solicit, initiate or pursue any potential alternatives to the merger. Transaction committee members receive a fee of $10,000 per calendar month (beginning June 1, 2011) for serving on the transaction committee (with a minimum fee for each member of the transaction committee of $30,000). The transaction committee engaged Jackson Walker as counsel to the transaction committee for the purpose of advising the transaction committee on legal issues associated with the committee and the merger proposal. In addition, the transaction committee identified and interviewed several financial advisors to consider them as advisors to the committee for providing advice on the fairness from a financial perspective of the merger consideration.

23

On June 30, 2011, Michael L. Pollard, the Senior Vice President—Finance and Chief Financial Officer of CWEI, provided the transaction committee a summary of the valuation methodology utilized by CWEI and SWR in calculating the merger consideration. CWEI and SWR proposed that the merger consideration for each SWR partnership be calculated as of December 31, 2010 based on (1) estimated fair value of reserves, with proved reserves being evaluated using the 12-month average of the daily NYMEX futures prices of oil and natural gas as of a date reasonably close to the mailing of the proxy statements to unaffiliated investors, (2) net working capital and (3) net asset retirement obligations. The proposed valuation methodology also provided that merger consideration would be reduced by the amount of any cash distributions subsequent to December 31, 2010.

Since both CWEI and the unaffiliated investors would be subject to the risk that oil prices will fluctuate between the stated valuation date until the date the merger is completed, the valuation methodology initially proposed by CWEI included a mechanism that would adjust the merger consideration in the event that the 12-month average of the daily closing NYMEX futures price for oil as of the fifth trading day prior to the closing date of the merger was 3% higher or lower than the 12-month average of the daily closing NYMEX futures prices for oil used in determining the merger consideration. As originally proposed (1) on the fifth trading day prior to the closing date, which we referred to as the adjustment date, SWR and the partnership would recompute the 12-month average of the daily closing NYMEX futures prices for oil as of the adjustment date. Only the price of oil would be recomputed since a significant portion of the partnership's estimated future revenues are expected to be derived from oil production and since the impact of a change in natural gas price was not expected to be material; (2) if the recomputed average oil price changed by 3% or less as compared to the 12-month average of the daily closing NYMEX futures prices for oil as of the stated valuation date, no adjustment to the merger consideration would be made; and (3) if the recomputed average oil price changed by more than 3% as compared to the 12-month average of the daily closing NYMEX futures price as of the stated valuation date, SWR would prepare an amended reserve report using an oil price equal to the average of (a) the 12-month average of the daily closing NYMEX futures prices as of the stated valuation date and (b) the recomputed average. The aggregate merger consideration would be recalculated utilizing the resulting estimated fair value of oil and gas reserves and the per unit merger consideration would be increased or decreased, as applicable, as a result of such recalculation.

In June 2011, CWEI decided to pursue a volumetric production payment transaction with an affiliate of JPMorgan Chase & Co. to provide proceeds to finance the merger consideration payable pursuant to the merger and the mergers of each of the other SWR partnerships into SWR. CWEI believed that this transaction would provide CWEI with a self-funding, low cost capital resource to finance the merger consideration, and allow CWEI to continue using its available financial resources to achieve its strategic objectives.

Also in June 2011, SWR engaged Ryder Scott to conduct an audit of the SWR partnerships' reserve estimates as of July 1, 2011 and to issue an audit report for inclusion in this proxy statement. SWR regularly provided Ryder Scott with information necessary for Ryder Scott to conduct its audit of the SWR partnerships' reserve estimates. See "—Summary Reserve Report."

On July 8, 2011, the transaction committee engaged ECS to assist the transaction committee as financial advisor. Following ECS' engagement by the transaction committee, and at the direction of the transaction committee, management of CWEI and SWR, including Mr. Pollard, discussed with ECS the financial terms of the mergers. Management of CWEI and SWR, including Mr. Pollard, regularly made themselves available to representatives of ECS and provided information concerning the SWR partnerships to ECS as requested by ECS, the transaction committee, Vinson & Elkins and Jackson Walker from time to time. In addition, SWR maintained a secure website on which SWR posted valuation, reserve and other due diligence information. Members of the transaction committee, ECS, Vinson & Elkins and Jackson Walker had continuous access to the secure website.

24

Also on July 8, 2011, Vinson & Elkins provided the transaction committee and Jackson Walker a draft of the form of merger agreement. The initial draft of the merger agreement contemplated the merger of the partnership into a newly formed wholly owned subsidiary of CWEI, which we refer to as a merger subsidiary, with the merger subsidiary surviving the merger as a wholly owned subsidiary of CWEI. As a result of the merger, the holders of units, including SWR, would receive a cash payment for each unit they held. The initial draft of the merger agreement also included the following: (1) customary representations, warranties and covenants for each of the partnership, the merger subsidiary and SWR; (2) conditions to completion of the merger, including (a) limited partners who own more than 50 percent of the units owned by all limited partners approving, at the special meeting, the merger agreement, the merger and the transactions contemplated by the merger agreement; (b) unaffiliated investors who own more than 50 percent of the units owned by all unaffiliated investors present in person or by proxy at the special meeting approving the merger agreement, the merger, and the transactions contemplated by the merger agreement; (c) the written opinion of ECS not having been withdrawn prior to the effective time of the merger, unless a replacement opinion or opinions of an investment banking firm or firms satisfactory to SWR (including the transaction committee) to a similar effect has been received by the transaction committee and not been withdrawn; (d) no provision of any applicable law or regulation and no judgment, injunction, order or decree prohibits the consummation of the merger and the transactions related to the merger; (e) the merger subsidiary having received sufficient funds through one or more debt and/or equity financing transactions to pay all of the merger consideration, which we refer to as the financing condition; and (f) other customary conditions; and (3) the ability of the parties to terminate the merger agreement in certain circumstances, including the ability of (a) the partnership to terminate the merger agreement if the partnership, after considering the written advice of outside legal counsel, determines in good faith that termination of the merger agreement is required for the board of directors to comply with its fiduciary duties to the partnership and to the unaffiliated investors imposed by applicable law and (b) the merger subsidiary to terminate if any event, circumstance, condition, development, or occurrence occurs causing, resulting in, or having a material adverse effect on (i) the partnership's business, operations, properties (taken as a whole), condition (financial or otherwise), results of operations, assets (taken as a whole), liabilities or cash flows of the partnership or (ii) market prices for oil and gas prevailing generally in the oil and gas industry since the date of determination of the oil and gas commodity prices used in the determination of the consideration payable in accordance with the merger agreement. We refer to the provisions in (b) above as the initial draft MAE.

Between July 8, 2011 and July 26, 2011, the transaction committee and Jackson Walker reviewed the terms of the draft merger agreement, the proposed valuation methodology, the preliminary valuation material and related analysis. On July 26, 2011, Jackson Walker, on behalf of the transaction committee, provided the transaction committee's comments to the draft merger agreement to CWEI and Vinson & Elkins. Among other changes, the transaction committee requested (1) modifications to the representations and warranties of the partnership; (2) that CWEI be added as a party to the merger agreement for the purpose of making representations and warranties as to the merger subsidiary; and (3) the removal of certain provisions of the initial draft MAE that would have allowed the merger subsidiary to terminate the merger agreement as a result of events, circumstances, conditions, developments or occurrences causing, resulting in, or having a material adverse effect on market prices for oil and gas prevailing generally in the oil and gas industry since the date of determination of the oil and gas commodity prices used in the determination of the consideration payable in accordance with the merger agreement.

On July 28, 2011, representatives of Vinson & Elkins and Jackson Walker discussed the transaction committee's comments to the merger agreement. Vinson & Elkins advised Jackson Walker that for administrative efficiency, CWEI desired to modify the structure of the merger to provide for the mergers of the SWR partnerships into SWR, rather than merging the SWR partnerships into the merger subsidiary. Vinson & Elkins also discussed the initial draft MAE, the financing condition and

25

other terms and provisions of the draft merger agreement. On July 29, 2011, representatives of CWEI, the transaction committee, Vinson & Elkins and Jackson Walker further discussed the draft merger agreement and the preliminary valuation material and analysis.

On August 2, 2011, Mr. Pollard provided the transaction committee a revised summary of the valuation methodology utilized by CWEI and SWR in calculating the merger consideration. The revised summary proposed that the merger consideration be calculated as of June 30, 2011 instead of December 31, 2010. CWEI proposed the change in order to shorten the time period between the calculation date and the signing date of the merger agreement.