UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 0-21229

Stericycle, Inc.

(Exact name of Registrant as Specified in its Charter)

| | |

| Delaware | | 36-3640402 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification Number) |

28161 North Keith Drive

Lake Forest, Illinois 60045

(Address of Principal Executive Offices including Zip Code)

(847) 367-5910

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value

(title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is an accelerated filer (as defined in Exchange Act Rule 12b-2). Yes x No ¨

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates computed by reference to the price at which common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter (June 30, 2006) was: $2,771,381,279.

On February 22, 2007, there were 44,316,672 shares of the Registrant’s Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Information required by Items 10, 11, 12 and 13 of Part III of this Report is incorporated by reference from the Registrant’s definitive Proxy Statement for the 2007 Annual Meeting of Stockholders to be held on May 16, 2007.

Stericycle, Inc.

2006 ANNUAL REPORT ON FORM 10-K

INDEX

2

PART I

Item 1. Business

Unless the context requires otherwise, “we,” “us” or “our” refers to Stericycle, Inc. and its subsidiaries on a consolidated basis.

Overview

We are in the business of managing regulated waste and providing an array of related services. We operate in the United States, Canada, Mexico, the United Kingdom, Ireland and Argentina.

For large-quantity generators of regulated waste such as hospitals and for pharmaceutical companies and distributors, we offer:

| | • | | our institutional regulated waste management services |

| | • | | ourBio Systems® sharps management services to reduce the risk of needle sticks |

| | • | | a variety of products and services for infection control |

| | • | | our regulated returns management services for expired or recalled healthcare products |

For small-quantity generators of regulated waste such as doctors’ offices and for retail pharmacies, we offer:

| | • | | our regulated waste management services |

| | • | | ourSteri-Safe® Occupational Safety and Health Act and Health Insurance Portability and Accountability Act (HIPAA) compliance programs |

| | • | | a variety of products and services for infection control |

| | • | | our regulated returns management services for expired or recalled healthcare products |

We operate integrated national regulated waste management networks in the United States, Canada, Mexico, Argentina, the United Kingdom and Ireland. Our national networks include a total of 76 processing or combined processing and collection sites and 104 additional transfer, collection or combined transfer and collection sites.

Our regulated waste processing technologies include autoclaving, our proprietary electro-thermal-deactivation system (ETD), chemical treatment and incineration.

We serve approximately 351,700 customers worldwide, of which approximately 8,600 are large-quantity generators, such as hospitals, blood banks and pharmaceutical manufacturers, and approximately 343,100 are small-quantity generators, such as outpatient clinics, medical and dental offices, long-term and sub-acute care facilities and retail pharmacies.

We benefit from significant customer diversification. No one customer accounts for more than 2% of our total revenues, and our top 10 customers account for approximately 9% of total revenues.

Industry Overview

Governmental legislation and regulation increasingly requires the proper handling and disposal of regulated waste. Regulated medical waste is generally any medical waste that can cause an infectious disease, and includes: single-use disposable items, such as needles, syringes, gloves and other medical supplies; cultures and stocks of infectious agents; and blood and blood products. Regulated pharmaceutical waste consists of expired or recalled pharmaceuticals.

3

We believe that the United States market for regulated waste and compliance services of the type that we provide is approximately $3.5 billion and that the market is in excess of $10.0 billion worldwide. Industry growth is driven by a number of factors. These factors include:

| | • | | Aging of U.S. Population. The average age of the U.S. population is rising. As people age, they typically require more medical attention and a wider variety of tests, procedures and medications, leading to an increase in the quantity of regulated waste generated. |

| | • | | Pressure To Reduce Healthcare Costs. The healthcare industry is under pressure to reduce costs. We believe that our services can help healthcare providers to reduce their handling and compliance costs and to reduce their potential liability for employee exposure to blood-borne pathogens and other infectious agents. |

| | • | | Environmental and Safety Regulation. We believe that many businesses that are not currently using third party regulated waste services are unaware either of the need for proper training of employees or of the requirements of the Occupational Safety and Health Administration (OSHA) regarding the handling of regulated waste. These businesses include manufacturing facilities, schools, restaurants, hotels and other businesses where employees may come into contact with blood-borne pathogens. Similarly, the proper handling of expired or recalled pharmaceuticals requires an expertise that many retail pharmacies lack or find inefficient to provide. |

| | • | | Shift to Off-Site Treatment. We believe that patient care is continuing to shift from institutional higher-cost acute-care settings to less expensive, smaller, off-site treatment alternatives, with a resulting increase in the number of regulated waste generators that cannot treat their own regulated waste. |

| | • | | Control of Drug Diversion. The U.S. Drug Enforcement Administration (DEA) has recently emphasized improved control of the handling and shipment of controlled substances to prevent diversion and counterfeiting, thus increasing the utility to pharmaceutical manufacturers and distributors of a returns service for expired or recalled pharmaceuticals. |

Competitive Strengths

We believe that we benefit from the following competitive strengths, among others:

| | • | | Broad Range of Services. We offer our customers a broad range of services to help them develop systems and processes to manage their regulated waste safely and efficiently. For example, we have developed programs to help our customers ensure and maintain compliance with OSHA and HIPAA regulations. |

| | • | | Established National Network. We believe that a network like ours would be very expensive and time-consuming for a competitor to develop. |

| | • | | Diverse Customer Base and Revenue Stability. We have a very diverse customer base in all the markets in which we operate. We are also generally protected from the cost of regulatory changes and increases in fuel, insurance and other operating costs because our regulated waste contracts typically allow us to adjust our prices to reflect these cost increases. |

| | • | | Strong Sales Network and Proprietary Database. We use both telemarketing and direct sales efforts to obtain new regulated waste customers. In addition, we have a large database of potential new small-quantity customers, which we believe gives us a competitive advantage in identifying and reaching this higher-margin sector. |

| | • | | Experienced Senior Management Team. We have experienced leadership. Our six most senior executives collectively have over 150 years of management experience in the health care, consumer and waste management industries. |

| | • | | Ability To Integrate Acquisitions. We have completed 116 acquisitions since 1993 and have demonstrated a consistent ability to integrate our acquisitions into our operations successfully. |

4

Business Strategy

Our goals are to strengthen our position as a leading provider of regulated waste and compliance services and to continue to improve our profitability. Components of our strategy to achieve these goals include:

| | • | | Expand Range of Services and Products. We believe that we continue to have opportunities to expand our business by increasing the range of products and services that we offer our existing regulated waste customers. For example, through ourSteri-Safe® program, we now offer OSHA compliance services to small-quantity customers, and an acquisition in 2003 enabled us to market theBio Systems® sharps management program to large-quantity customers in new geographic areas. We have expanded our regulated waste services to pharmaceutical companies and other large-quantity generators through a series of acquisitions in 2005 and 2006 of five businesses engaged in regulated returns management services. |

| | • | | Improve Margins. We intend to continue working to improve our margins by increasing our base of small-quantity customers and focusing on service strategies that more efficiently meet the needs of our large-quantity customers. We have succeeded in raising the percentage of our revenues from small-quantity customers from 33% of domestic revenues in the fourth quarter of 1996 to 62% in the fourth quarter of 2006. |

| | • | | Seek Complementary Acquisitions. We intend to continue to seek opportunities to acquire businesses that expand our national networks in the United States and internationally and increase our customer base. We believe that selective acquisitions can enable us to improve our operating efficiencies through increased utilization of our service infrastructure. |

Acquisitions

We have substantial experience in evaluating potential acquisitions and determining whether a particular waste business can be integrated into our operations with minimal disruption. Once a business is acquired, we implement programs and procedures to improve customer service, sales, marketing, routing, equipment utilization, employee productivity, operating efficiency and overall profitability.

We completed 116 acquisitions from 1993 through 2006, with 89 in the United States and 27 internationally.

During 2006, we completed 16 acquisitions, with seven in the United States, one in Canada, six in Mexico, one in Ireland, and one in Argentina.

Services and Operations

Collection and Transportation. In many respects, our regulated waste business is one of logistics. Efficiency of collection and transportation of regulated waste is a critical element of our operations because it represents the largest component of our operating costs.

For regulated waste, we supply specially designed reusable leak-and puncture-resistant plastic containers to most of our large-quantity customers and many of our larger small-quantity customers. To assure regulatory compliance, we will not accept regulated waste from customers unless it is properly packaged in containers that we have either supplied or approved.

We collect containers or corrugated boxes of regulated waste from our customers at intervals depending upon customer requirements, contract terms and volume of waste generated. The waste is then transported directly to one of our processing facilities or to one of our transfer stations where it is combined with other regulated waste and transported to a processing facility.

5

Transfer stations allow us to temporarily hold small loads of waste until they can be consolidated into full truckloads and transported to a processing facility. Our use of transfer stations in a “hub and spoke” configuration improves the efficiency of our collection and transportation operations by expanding the geographic area that a particular processing facility can serve and thereby increasing utilization of the facility by increasing the volume of waste that it processes.

We collect some expired or recalled pharmaceuticals from pharmacy shelves but more typically, pharmacies ship them directly to our processing facilities.

Processing and Disposal. Upon arrival at a processing facility, containers or boxes of regulated waste are typically scanned to verify that they do not contain any unacceptable substances like radioactive material. Any container or box that is discovered to contain unacceptable waste is returned to the customer and the appropriate regulatory authorities are informed.

The regulated waste is then processed using one of our various treatment technologies. Upon completion of the particular process, the resulting waste or incinerator ash is transported for resource recovery, recycling or disposal in a landfill operated by an unaffiliated third party. We do not own any landfills. After plastic containers such as ourSteri-Tub® orBio Systems® containers have been emptied, they are washed, sanitized and returned to customers for re-use.

Upon receipt at a processing facility, expired or recalled pharmaceuticals are counted and logged, and controlled substances are stored securely. In accordance with the manufacturer’s instructions, expired or recalled pharmaceuticals are then returned to the manufacturer or destroyed in compliance with applicable regulations.

Documentation. We provide complete documentation to our customers for all regulated waste that we collect in accordance with applicable regulations and customer requirements.

Marketing and Sales

Marketing Strategy. We use both telemarketing and direct sales efforts to obtain new customers. In addition, our drivers may also participate in our regulated waste marketing efforts by actively soliciting small-quantity customers they service.

Small-Quantity Customers. We target small-quantity customers as a growth area of our regulated waste business. We believe that small-quantity regulated waste customers view the potential risks of failing to comply with applicable state and federal regulated waste regulations as disproportionate to the cost of the services that we provide. We believe that this factor has been the basis for the significantly higher gross margins that we have achieved with our small-quantity customers relative to our large-quantity customers. We believe that the same potential exists in processing returns of expired pharmaceuticals for smaller retail pharmacies.

Steri-Safe®. OurSteri-Safe® OSHA compliance program provides an integrated regulated waste management and compliance-assistance service for small-quantity customers who typically lack the internal personnel and systems to comply with OSHA blood-borne regulations. Customers for ourSteri-Safe® service pay a predetermined subscription fee in advance for regulated waste collection and processing services and can also choose from available packages of training and education services and products designed to help them to comply with OSHA regulations. Approximately 105,000 small-quantity customers are enrolled in this program. We believe that the implementation of ourSteri-Safe® service provides us with an enhanced opportunity to leverage our existing customer base through the program’s prepayment structure and diversified product and service offerings.

Mail-Back Program. We also operate a “mail-back” program by which we can reach small-quantity regulated waste customers located in outlying areas that would be inefficient to serve using our regular route structure. Mail-back programs are also used in home care patient settings.

6

Large-Quantity Customers. Our marketing efforts to large-quantity customers are conducted by account executives that are also able to provide consulting services to assist our large-quantity customers in training their employees on safety issues and implementing programs to improve waste segregation.

OurBio Systems® sharps management offering can enhance our revenue and margins per large-quantity account. TheBio Systems® service can help our large-quantity customers eliminate plastic and cardboard from their waste stream while providing a safe and cost-effective way for them to deal with the disposal of their sharp objects (such as needles, syringes, etc.).

We offer hospital pharmacies an onsite collection service to assist them in accounting for and segregating expired or recalled pharmaceuticals.

National Accounts. As a result of our extensive geographic coverage, we are capable of servicing national account customers (i.e., customers requiring regulated waste services at various geographically dispersed locations).

Contracts. We have multi-year contracts with a large majority of our customers. We negotiate individual contracts with each large-quantity and small-quantity customer. Although we have a standard form of contract, particularly for small-quantity customers, terms may vary depending upon the customer’s service requirements and the volume of regulated waste generated and, in some jurisdictions, statutory and regulatory requirements. Substantially all of our contracts with small-quantity customers contain automatic renewal provisions.

International

We conduct regulated waste operations in Canada, Mexico, Argentina, the United Kingdom and Ireland as well as the United States. We began our operations in Canada and Mexico in 1998, in Argentina in 1999, in the United Kingdom in 2004 and in Ireland in 2006.

Processing Technologies

We currently use both non-incineration technologies (autoclaving, chemical treatment and our proprietary ETD technology) and incineration technologies for treating regulated waste.

Stericycle was founded on the belief that there was a need for safe, secure and environmentally responsible management of regulated waste. From our beginning we have championed the use of non-incineration treatment technologies such as our ETD process. While we recognize that some state regulations currently in force mandate that some types of regulated waste must be incinerated, we also know from years of experience working with our customers that there are ways to reduce the amount of regulated waste that is ultimately incinerated. The most effective strategy that we have seen involves comprehensive education of our customers in waste minimization and segregation. Working in cooperation with our customers, we have made tremendous strides in moving away from incineration and towards alternate treatment technologies. At the end of 2006, incineration constituted less than 8% of our treatment capacity in the United States, Canada and Mexico.

Autoclaving. Autoclaving treats regulated waste with steam at high temperature and pressure to kill pathogens. Autoclaving alone does not change the appearance of waste, and some landfill operators may not accept recognizable regulated waste, but autoclaving may be combined with a shredding or grinding process to render the regulated waste unrecognizable.

ETD. Our ETD treatment process includes a system for grinding regulated waste. After grinding, ETD uses an oscillating field of low-frequency radio waves to heat regulated waste to temperatures that destroy pathogens such as viruses, bacteria, fungi and yeast without melting the plastic content of the waste. ETD does not produce regulated air or water emissions.

7

Incineration. Incineration burns regulated waste at elevated temperatures and reduces it to ash. Incineration reduces the volume of waste, and it is the recommended treatment and disposal option for some types of regulated waste such as anatomical waste or residues from chemotherapy procedures. Air emissions from incinerators can contain certain byproducts that are subject to federal, state and, in some cases, local regulation. In some circumstances, the ash byproduct of incineration may be regulated.

Chem-Clav. Chemclaving treats regulated waste using high heat, pressure, and a steam auger to kill pathogens. The waste is treated in a sealed container while the auger shreds the waste, making it unrecognizable while exposing more surface area of the waste to the steam. After shredding and treatment, the waste residue is sterile and safe for landfill.

Competition

The regulated waste industry is highly competitive, and barriers to entry into the regulated waste collection and disposal business and the pharmaceutical returns business are very low. Our competitors consist of many different types of service providers, including a large number of regional and local companies. In the regulated waste industry, another major source of competition is the on-site treatment of regulated waste by some large-quantity generators, particularly hospitals.

In addition, in the regulated waste industry we face potential competition from businesses that are attempting to commercialize alternate treatment technologies or products designed to reduce or eliminate the generation of regulated waste, such as reusable or degradable medical products.

Governmental Regulation

The regulated waste industry is subject to extensive and frequently changing federal, state and local laws and regulations. This statutory and regulatory framework imposes a variety of compliance requirements, including requirements to obtain and maintain government permits. These permits grant us the authority, among other things:

| | • | | to construct and operate collection, transfer and processing facilities, |

| | • | | to transport regulated waste within and between relevant jurisdictions, and |

| | • | | to handle particular regulated substances. |

Our permits must be periodically renewed and are subject to modification or revocation by the issuing authority.

We are also subject to regulations that govern the definition, generation, segregation, handling, packaging, transportation, treatment, storage and disposal of regulated waste. We are also subject to extensive regulations designed to minimize employee exposure to regulated waste.

Domestic Federal Regulation. Five federal agencies have authority over regulated waste. These agencies are the U.S. Environmental Protection Agency (EPA), Occupational Safety and Health Administration (OSHA), U.S. Department of Transportation (DOT), the U.S. Postal Service (USPS) and the U.S. Drug Enforcement Administration (DEA). These agencies supervise regulated waste under a variety of statutes and regulations. The principal statutes and regulations are:

| | • | | Medical Waste Tracking Act of 1988. In the late 1980s, the EPA outlined a two-year demonstration program pursuant to the Medical Waste Tracking Act (MWTA), which was added to the Resource Conservation and Recovery Act of 1976. In regulations implementing the MWTA, the EPA defined medical waste and established guidelines for its segregation, handling, containment, labeling and transport. The MWTA demonstration program expired in 1991, but the MWTA established a model followed by many states in developing their specific medical waste regulatory framework. |

8

| | • | | Occupational Safety and Health Act of 1970. The Occupational Safety and Health Act of 1970 authorizes OSHA to issue occupational safety and health standards. Various standards apply to certain aspects of our operations and govern such matters as exposure to blood borne pathogens and other potentially infectious materials. |

| | • | | Resource Conservation and Recovery Act of 1976. The Resource Conservation and Recovery Act of 1976 (RCRA) created standards for the generation, transportation, treatment, storage and disposal of solid and hazardous wastes. Medical wastes are currently considered non-hazardous solid wastes under RCRA. However, some substances collected by us from some of our customers, including photographic fixer developer solutions, lead foils and dental amalgam, are considered hazardous wastes. |

| | • | | Clean Air Act Regulations. In August 1997, the EPA adopted regulations under the Clean Air Act Amendments of 1990 that limit the discharge into the atmosphere of pollutants released by regulated waste incineration. These regulations required every state to submit to the EPA for approval a plan to meet minimum emission standards for these pollutants. We currently operate seven incinerators in the United States. We believe these incinerators are in compliance with applicable state requirements. |

| | • | | DOT Regulations. DOT has adopted regulations under the Hazardous Materials Transportation Authorization Act of 1994 that require us to package and label regulated waste in compliance with designated standards, and which incorporate blood borne pathogens standards issued by OSHA. Under these standards, we must, among other things, identify our packaging with a “biohazard” marking on the outer packaging, and our regulated waste container must be sufficiently rigid and strong to prevent tearing or bursting. It must also be puncture-resistant, leak-resistant, properly sealed and impervious to moisture. |

| | | Expired or recalled pharmaceuticals are subject to the substantially same DOT regulations as medical waste. We identify these products by their National Drug Code number and classify them by their handling, transportation and disposal requirements. |

| | • | | Comprehensive Environmental Response, Compensation and Liability Act of 1980. The Comprehensive Environmental Response, Compensation and Liability Act of 1980, or CERCLA, established a regulatory and remedial program to provide for the investigation and cleanup of facilities that have released or threaten to release hazardous substances into the environment. CERCLA and state laws similar to it may impose strict, joint and several liability on the current and former owners and operators of facilities from which releases of hazardous substances have occurred and on the generators and transporters of the hazardous substances that come to be located at these facilities. |

| | • | | USPS Regulations. We have obtained permits from the USPS to conduct our “mail-back” program, pursuant to which customers mail approved containers of “sharps” (needles, knives, broken glass and the like) directly to our treatment facilities. |

| | • | | Controlled Substances Act. Our returns service for expired and recalled pharmaceuticals is required to comply with DEA regulations relating to the approval and permitting of processing facilities, management of employees engaged in the collection, processing and disposal of controlled substances, proper documentation and reporting to the DEA. |

We use landfills owned and operated by unrelated third parties for the disposal of waste from our processing facilities.

Domestic State and Local Regulation.We conduct business in 49 states and Puerto Rico. Each state has its own regulations related to the handling, treatment and storage of regulated waste. Although there are many differences among the various state laws and regulations, for regulated waste many states have followed the model under the MWTA and have implemented programs under RCRA. In each state where we operate a processing facility or a transfer station, we are required to comply with numerous state and local laws and

9

regulations as well as our operating plan for each site. In addition, many local governments have ordinances and regulations, such as zoning and health regulations that affect our operations.

We maintain numerous governmental permits and licenses to conduct our business. Our permits vary from state to state based upon our activities within that state and on the applicable state and local laws and regulations.

Foreign Regulation. We are subject to substantial regulation by the governments of the foreign jurisdictions in which we conduct regulated waste operations. The statutory and regulatory requirements vary from jurisdiction to jurisdiction.

Patents and Proprietary Rights

We consider the protection of our technology to be important to our business. Our policy is to protect our technology by a variety of means, including applying for patents in the United States and in other foreign countries.

We hold 14 United States patents relating to the ETD treatment process and other aspects of processing regulated waste. We have filed or have been assigned patent applications in several foreign countries and we have received patents in Australia, Canada, France, Mexico, Japan, South Korea, Brazil, Denmark, Italy, South Africa, Spain, Sweden and the United Kingdom.

The term of the first-to-end of our existing United States patents relating to our ETD treatment process will currently end in May 2009 and the term of the last-to-end will currently end in January 2019.

We own federal registrations of the trademarks “Steri-Fuel®”, “Steri-Plastic®”, “Steri-Tub®”, “Direct Return®”, “Steri-Safe®”, the service mark Stericycle® and a service mark consisting of a nine-circle design.

Potential Liability and Insurance

The regulated waste industry involves potentially significant risks of statutory, contractual, tort and common law liability claims. Potential liability claims could involve, for example:

| | • | | damage to the environment; |

| | • | | alleged negligence or professional errors or omissions in the planning or performance of work. |

We could also be subject to fines or penalties in connection with violations of regulatory requirements.

We carry $35 million of liability insurance (including umbrella coverage), and under a separate policy, $10 million of aggregate pollution and legal liability insurance ($5 million per incident), which we consider sufficient to meet regulatory and customer requirements and to protect our employees, assets and operations

Employees

As of December 31, 2006, we had 5,035 full-time and 219 part-time employees, of which 3,747 were employed in the United States and 1,507 internationally. Approximately 324 of our U.S. drivers, transportation helpers and plant workers are covered by a total of eight collective bargaining agreements with local unions of the International Brotherhood of Teamsters. These agreements expire at various dates from April 2007 to November 2010. We consider our employee relations to be satisfactory.

10

Website Access

We maintain an Internet website,www.stericycle.com, providing a variety of information about us. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, that we file with the Securities and Exchange Commission are available, as soon as reasonably practicable after filing, at the investors’ page on our website,www.stericycle.com/investor.htm, or by a direct link to our filings on the SEC’s free website,www.sec.gov.

Item 1A. Risk Factors

We are subject to extensive governmental regulation, which is frequently difficult, expensive and time-consuming to comply with.

The regulated waste management industry is subject to extensive federal, state and local laws and regulations relating to the collection, transportation, packaging, labeling, handling, documentation, reporting, treatment and disposal of regulated waste. Our business requires us to obtain many permits, authorizations, approvals, certificates or other types of governmental permission from every jurisdiction where we operate. We believe that we currently comply in all material respects with all applicable permitting requirements. State and local regulations change often, however, and new regulations are frequently adopted. Changes in the regulations could require us to obtain new permits or to change the way in which we operate under existing permits. We might be unable to obtain the new permits that we require, and the cost of compliance with new or changed regulations could be significant.

Many of the permits that we require, especially those to build and operate processing plants and transfer facilities, are difficult and time-consuming to obtain. They may also contain conditions or restrictions that limit our ability to operate efficiently, and they may not be issued as quickly as we need them (or at all). If we cannot obtain the permits that we need when we need them, or if they contain unfavorable conditions, it could substantially impair our operations and reduce our revenues.

The handling and treatment of regulated waste carries with it the risk of personal injury to employees and others.

Our business requires us to handle materials that may be infectious or hazardous to life and property in other ways. While we try to handle such materials with care and in accordance with accepted and safe methods, the possibility of accidents, leaks, spills, and acts of God always exists. Examples of possible exposure to such materials include:

| | • | | damaged or leaking containers; |

| | • | | improper storage of regulated waste by customers; |

| | • | | improper placement by customers of materials into the waste stream that we are not authorized or able to process, such as certain body parts and tissues; or |

| | • | | malfunctioning treatment plant equipment. |

Human beings, animals or property could be injured, sickened or damaged by exposure to regulated waste. This in turn could result in lawsuits in which we are found liable for such injuries, and substantial damages could be awarded against us.

While we carry liability insurance intended to cover these contingencies, particular instances may occur that are not insured against or that are inadequately insured against. An uninsured or underinsured loss could be substantial and could impair our profitability and reduce our liquidity.

11

The handling of regulated waste exposes us to the risk of environmental liabilities, which may not be covered by insurance.

As a company engaged in regulated waste management, we face risks of liability for environmental contamination. The federal Comprehensive Environmental Response, Compensation and Liability Act of 1980, or CERCLA, and similar state laws impose strict liability on current or former owners and operators of facilities that release hazardous substances into the environment as well as on the businesses that generate those substances and the businesses that transport them to the facilities. Responsible parties may be liable for substantial investigation and clean-up costs even if they operated their businesses properly and complied with applicable federal and state laws and regulations. Liability under CERCLA may be joint and several, which means that if we were found to be a business with responsibility for a particular CERCLA site, we could be required to pay the entire cost of the investigation and clean-up even though we were not the party responsible for the release of the hazardous substance and even though other companies might also be liable.

Our pollution liability insurance excludes liabilities under CERCLA. Thus, if we were to incur liability under CERCLA and if we could not identify other parties responsible under the law whom we are able to compel to contribute to our expenses, the cost to us could be substantial and could impair our profitability and reduce our liquidity. Our customer service agreements make clear that the customer is responsible for making sure that only appropriate materials are disposed of. If there were a claim against us that a customer might be legally liable for, we might not be successful in recovering our damages from the customer.

The level of governmental enforcement of environmental regulations has an uncertain effect on our business and could reduce the demand for our services.

We believe that the government’s strict enforcement of laws and regulations relating to regulated waste collection and treatment has been good for our business. These laws and regulations increase the demand for our services. A relaxation of standards or other changes in governmental regulation of regulated waste could increase the number of competitors or reduce the need for our services.

If we are unable to acquire other regulated waste businesses, our revenue and profit growth may be slowed.

Historically our growth strategy has been based in substantial part on our ability to acquire other regulated waste businesses. We do not know whether in the future we will be able to:

| | • | | identify suitable businesses to buy; |

| | • | | complete the purchase of those businesses on terms acceptable to us; |

| | • | | improve the operations of the businesses that we do buy and successfully integrate their operations into our own; or |

| | • | | avoid or overcome any concerns expressed by regulators. |

We compete with other potential buyers for the acquisition of other regulated waste companies. This competition may result in fewer opportunities to purchase companies that are for sale. It may also result in higher purchase prices for the businesses that we want to purchase.

We also do not know whether our growth strategy will continue to be effective. Our business is significantly larger than before, and new acquisitions may not have the desired benefits that we have obtained in the past.

The implementation of our acquisition strategy could be affected in certain instances by the concerns of state regulators, which could result in our not being able to realize the full synergies or profitability of particular acquisitions.

We may become subject to inquiries and investigations by state antitrust regulators from time to time in the course of completing acquisitions of other regulated waste businesses. In order to obtain regulatory clearance for

12

a particular acquisition, we could be required to modify certain operating practices of the acquired business or to divest ourselves of one or more assets of the acquired business. Changes in the terms of our acquisitions required by regulators or agreed to by us in order to settle regulatory investigations could impede our acquisition strategy or reduce the anticipated synergies or profitability of our acquisitions. The likelihood and outcome of inquiries and investigations from state regulators in the course of completing acquisitions cannot be predicted.

Aggressive pricing by existing competitors and the entrance of new competitors could drive down our profits and slow our growth.

The regulated waste industry is very competitive because of low barriers to entry, among other reasons. This competition has required us in the past to reduce our prices, especially to large account customers, and may require us to reduce our prices in the future. Substantial price reductions could significantly reduce our earnings.

We face direct competition from a large number of small, local competitors. Because it requires very little money or technical know-how to compete with us in the collection and transportation of regulated waste, there are many regional and local companies in the industry. We face competition from these businesses, and competition from them is likely to exist in the new locations to which we may expand in the future. In addition, large national companies with substantial resources may decide to enter the regulated waste industry. For example, Waste Management, Inc., a major solid waste treatment company, announced in February 2005 that it intended to begin offering regulated waste management services to hospitals and possibly other large quantity generators of regulated waste.

Our competitors could take actions that would hurt our growth strategy, including the support of regulations that could delay or prevent us from obtaining or keeping permits. They might also give financial support to citizens’ groups that oppose our plans to locate a treatment or transfer facility at a particular location.

Restrictions in our senior unsecured credit facility may limit our ability to pay dividends, incur additional debt, make acquisitions and make other investments.

Our senior unsecured credit facility contains covenants that restrict our ability to make distributions to stockholders or other payments unless we satisfy certain financial tests and comply with various financial ratios.

It also contains covenants that limit our ability to incur additional indebtedness, acquire other businesses and make capital expenditures, and imposes various other restrictions. These covenants could affect our ability to operate our business and may limit our ability to take advantage of potential business opportunities as they arise.

The loss of our senior executives could affect our ability to manage our business profitably.

We depend on a small number of senior executives. Our future success will depend upon, among other things, our ability to keep these executives and to hire other highly qualified employees at all levels. We compete with other potential employers for employees, and we may not be successful in hiring and keeping the executives and other employees that we need. We do not have written employment agreements with any of our executive officers, and officers and other key employees could leave us with little or no prior notice, either individually or as part of a group. Our loss of or inability to hire key employees could impair our ability to manage our business and direct its growth.

Our expansion into foreign countries exposes us to unfamiliar regulations and may expose us to new obstacles to growth.

We plan to grow both in the United States and in foreign countries. We have established operations in Argentina, Canada, Mexico, Ireland and the United Kingdom. Foreign operations carry special risks. Although

13

our business in foreign countries has not yet been affected, our business in the countries in which we currently operate and those in which we may operate in the future could be limited or disrupted by:

| | • | | import and export license requirements; |

| | • | | political or economic instability; |

| | • | | changes in tariffs and taxes; |

| | • | | exchange rate fluctuations; |

| | • | | our unfamiliarity with local laws, regulations, practices and customs; |

| | • | | restrictions on repatriating foreign profits back to the United States; |

| | • | | difficulties in staffing and managing international operations. |

Foreign governments and agencies often establish permit and regulatory standards different from those in the United States. If we cannot obtain foreign regulatory approvals, or if we cannot obtain them when we expect, our growth and profitability from international operations could be limited. Fluctuations in currency exchange could have similar effects.

Our earnings could decline if we write-off intangible assets, such as goodwill.

As a result of purchase accounting for our various acquisitions, our balance sheet at December 31, 2006 contains goodwill of $814.0 million and other intangible assets, net of accumulated amortization, of $115.91 million (including indefinite lived intangibles of $32.2 million). In accordance with Statement of Financial Accounting Standards No. 142 “Goodwill and Other Intangible Assets” (“SFAS No. 142”), we evaluate on an ongoing basis, using the fair value of reporting units, whether facts and circumstances indicate any impairment of the value of indefinite-lived intangible assets such as goodwill. As circumstances after an acquisition can change, we may not realize the value of these intangible assets. If we were to determine that a significant impairment has occurred, we would be required to incur non-cash write-offs of the impaired portion of goodwill and other unamortized intangible assets, which could have a material adverse effect on our results of operations in the period in which the write-off occurs.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We lease office space for our corporate offices in Lake Forest, Illinois. In North America we own or lease three ETD treatment facilities, 11 incineration processing facilities, 34 autoclave processing facilities and five other processing facilities. All of our processing facilities also serve as collection sites. We own or lease 100 additional transfer and collection sites and nine additional sales/administrative sites. In Europe we own or lease 13 incineration processing facilities and 9 autoclave processing facilities. We also lease four additional transfer and collection sites and three administrative sites. In Argentina we own one processing facility, which uses a combination of both incineration and autoclave treatments. We consider that these processing facilities are adequate for our present and anticipated needs.

We do not own or operate any landfills or any other type of disposal site. After processing, all remaining waste materials are transported to unaffiliated third parties for permanent disposal.

14

Item 3. Legal Proceedings

We operate in a highly regulated industry and must deal with regulatory inquiries or investigations from time to time that may be instituted for a variety of reasons. We are also involved in a variety of civil litigation from time to time.

In June 2006, the United Kingdom Office of Fair Trading (“OFT”) referred to the United Kingdom Competition Commission (the “Competition Commission”) the acquisition by our subsidiary, Stericycle International, LLC, in February 2006 of all of the stock of The Sterile Technologies Group Limited (“STG”), an Irish company providing regulated waste management services in Ireland and the United Kingdom. Under the terms of the OFT’s referral, the Competition Commission was to decide whether, as a result of the STG acquisition, there has been or is expected to be a substantial lessening of competition in one or more markets in the United Kingdom for healthcare risk waste services, and if so, what remedial or other actions, if any, should be taken or recommended by the Competition Commission.

On October 19, 2006, the Competition Commission issued provisional findings that the STG acquisition has resulted, or may be expected to result, in a substantial lessening of competition in the market for healthcare risk waste services requiring incineration in five geographical areas. The Competition Commission also issued a notice of possible remedies, including (i) a complete divestiture of STG’s operations in England and Wales, (ii) a complete divestiture of STG’s incinerators in England and Wales or (iii) a divestiture of STG’s incinerators serving customers in the affected geographical areas.

On December 12, 2006, the Competition Commission published its final report on the STG acquisition. The Competition Commission confirmed its provisional findings and concluded that the STG acquisition has resulted, and may be expected to continue to result, in a substantial lessening of competition in the market for healthcare risk waste services requiring incineration in five geographical areas of England and Wales: northern England, the north Midlands, north Wales, the West Midlands and southeast Wales.

The Competition Commission accepted as a remedy our proposal to be allowed an initial period in which to sell three STG incinerators serving the affected geographical areas together with the associated customer contracts, subject to the Competition Commission’s approval of the terms of sale and suitability of the purchaser. We completed the sale of the three incinerators in February 2007, within the period allowed by the Competition Commission.

Item 4. Submission of Matters to a Vote of Security Holders

No matter was submitted to a vote of our stockholders during the fourth quarter of 2006.

Supplemental Information

Executive Officers of the Registrant

The following table contains certain information regarding our five current executive officers:

| | | | |

Name | | Position | | Age |

Mark C. Miller | | President, Chief Executive Officer and a Director | | 51 |

Richard T. Kogler | | Executive Vice President and Chief Operating Officer | | 47 |

Frank J.M. ten Brink | | Executive Vice President and Chief Financial Officer | | 50 |

Richard L. Foss | | Executive Vice President, Corporate Development | | 52 |

Shan S. Sacranie | | Executive Vice President, International | | 54 |

Michael J. Collins | | President, Stericycle Return Management Services | | 50 |

Mark C. Miller has served as our President and Chief Executive Officer and a director since joining us in May 1992. From May 1989 until he joined us, Mr. Miller served as vice president for the Pacific, Asia and Africa

15

in the International Division of Abbott Laboratories, which he joined in 1976 and where he held a number of management and marketing positions. He is a director of Ventana Medical Systems, Inc. Mr. Miller received a B.S. degree in computer science from Purdue University, where he graduated Phi Beta Kappa.

Richard T. Kogler joined us as Chief Operating Officer in December 1998. From May 1995 through October 1998, Mr. Kogler was vice president and chief operating officer of American Disposal Services, Inc., a solid waste management company. From October 1984 through May 1995, Mr. Kogler served in a variety of management positions with Waste Management, Inc. Mr. Kogler received a B.A. degree in chemistry from St. Louis University.

Frank J.M. ten Brink has served as our Executive Vice President, Finance and Chief Financial Officer since June 1997. From 1991 until 1996 he served as chief financial officer of Hexacomb Corporation, and from 1996 until joining us, he served as chief financial officer of Telular Corporation. Prior to 1991, he held various financial management positions with Interlake Corporation and Continental Bank of Illinois. Mr. ten Brink received a B.B.A. degree in international business and a M.B.A. degree in finance from the University of Oregon.

Richard L. Foss has served as our Executive Vice President for Corporate Development since February 2003. From 1999 to 2002, Mr. Foss was a vice president and director of worldwide product marketing in the personal communication sector at Motorola Inc., and from 1977 until 1999, he held a number of management and marketing positions at The Procter & Gamble Company, including serving as a vice president and general manager in the health care segment. Mr. Foss received a B.S. degree in chemistry and an M.B.A degree from Rensselear Polytechnic Institute.

Shan S. Sacranie joined us in May 2003 and became our Executive Vice President, International in November 2003. From 2001 to 2002 he was chief executive for Appliance Controls Group, Inc. and from 1995 to 2001, he was president of Oak Industries Inc. From 1978 to 1995 he held a number of management positions for Honeywell. Mr. Sacranie holds a BA degree (Hons) in economics from the University of Bombay, an M.B.A. degree from Minnesota State University and a J.D. from the William Mitchell College of Law.

Michael J. Collins has served as President of our Return Management Services Division since June 2006. Prior to joining us, he served at Abbott Laboratories, a diversified health care company, which he joined in 1982 and where he held a number of management and marketing positions, most recently as vice president, medical products group health systems. Mr. Collins received a B.A. degree in business and education from the University of New Haven and a M.B.A. degree in business administration from National University

16

PART II

Item 5. Market Price of and Dividends on the Registrant’s Common Equity and Related Stockholder Matters

As of February 22, 2007, we had approximately 180 stockholders of record. The Company’s stock trades on the NASDAQ National Market under the ticker symbol SRCL.

The following table provides the high and low sales prices of our Common Stock for each calendar quarter during our two most recent fiscal years:

| | | | |

Quarter | | High | | Low |

First quarter 2005 | | 51.60 | | 44.20 |

Second quarter 2005 | | 53.82 | | 43.92 |

Third quarter 2005 | | 59.47 | | 50.58 |

Fourth quarter 2005 | | 63.52 | | 54.36 |

| | |

First quarter 2006 | | 67.62 | | 57.28 |

Second quarter 2006 | | 69.00 | | 61.30 |

Third quarter 2006 | | 69.79 | | 61.07 |

Fourth quarter 2006 | | 75.62 | | 65.03 |

We did not pay any cash dividends during 2006 and have never paid any dividends on our capital stock. We currently expect that we will retain future earnings for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

In May 2002 our Board of Directors authorized the Company to repurchase up to 3,000,000 shares of our common stock, in the open market or through privately negotiated transactions, at times and in amounts in the Company’s discretion. In February 2005, at a time when we had purchased a cumulative total of 1,478,430 shares, the Board authorized the Company to purchase up to an additional 1,478,430 shares, thereby giving the Company the authority to purchase up to a total of 3,000,000 additional shares. In February 2007, at a time when we had purchased an additional 1,571,040 shares since the 2005 stock purchase authorization, the Board authorized the Company to purchase up to an additional 1,571,040 shares, thereby giving the Company the authority to purchase up to a total of 3,000,000 additional shares. The following table provides information about our purchases during the year ended December 31, 2006 of shares of our common stock.

Issuer Purchases of Equity Securities

| | | | | | | | |

Period | | Total

Number of Shares

(or Units)

Purchased | | Average

Price

Paid per

Share

(or Unit) | | Number of Shares

(or Units)

Purchased as Part

of Publicly

Announced Plans

or Programs | | Maximum

Number (or Approximate

Dollar Value) of Units) that May Yet Be

Purchased Under

the Plans or

Programs |

January 1 - January 31, 2006 | | 181,800 | | 57.99 | | 181,800 | | 1,914,700 |

February 1 - February 28, 2006 | | 11,300 | | 58.01 | | 11,300 | | 1,903,400 |

March 1 - March 31, 2006 | | 0 | | 0 | | 0 | | 1,903,400 |

April 1 - April 30, 2006 | | 0 | | 0 | | 0 | | 1,903,400 |

May 1 - May 31, 2006 | | 2,000 | | 59.45 | | 2,000 | | 1,901,400 |

June 1 - June 30, 2006 | | 60,600 | | 62.71 | | 60,600 | | 1,840,800 |

July 1 - July 31, 2006 | | 164,945 | | 62.45 | | 164,945 | | 1,675,855 |

August 1 - August 31, 2006 | | 0 | | 0 | | 0 | | 1,675,855 |

September 1 - September 30, 2006 | | 9,913 | | 67.5 | | 9,913 | | 1,665,942 |

October 1 - October 31, 2006 | | 54,406 | | 67.75 | | 54,406 | | 1,611,536 |

November 1 - November 30, 2006 | | 24,117 | | 69.47 | | 24,117 | | 1,587,419 |

December 1 - December 31, 2006 | | 158,459 | | 71.38 | | 158,459 | | 1,428,960 |

17

Equity Compensation Plans

The following table summarizes information as of December 31, 2006 relating to our equity compensation plans pursuant to which stock option grants, restricted stock awards or other rights to acquire shares of our common stock may be made or issued:

Equity Compensation Plan Information

| | | | | | | |

Plan Category | | Number of Securities

To Be Issued Upon

Exercise Warrants

and Rights (a) | | Weighted-Average

Exercise Price of

Outstanding Options,

Warrants and Rights

(b) | | Number of Securities

Remaining Available

for Future Issuance

Under Equity

Compensation Plans

(Excluding

Securities Reflected

in Column (a)) (c) |

Equity compensation plans approved by our security holders(1) | | 1,947,331 | | $ | 43.36 | | 1,953,893 |

Equity compensation plans not approved by our security holders(2) | | 1,571,324 | | $ | 40.14 | | 191,894 |

| (1) | These plans consist of our 2005 Plan, 1997 Plan, 1995 Plan, Directors Plan and ESPP. |

| (2) | The only plan in this category is our 2000 Plan. |

In 2000, our Board of Directors approved the 2000 Nonstatutory Stock Option Plan (the “2000 Plan”), which in total now provides for the granting of 3,500,000 shares of our common stock in the form of stock options to employees, (but not to officers or directors).

18

Performance Graph

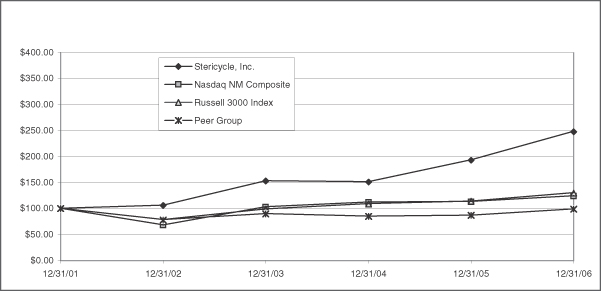

The following graph compares the cumulative total return (i.e., stock price appreciation plus dividends) on our common stock over the five-year period ending December 31, 2006 with the cumulative total return for the same period on the Nasdaq National Market Composite Index, the Russell 3000 Index and an index of a peer group of companies that we selected consisting of Allied Waste Industries, Inc., SRI/Surgical Express, Inc. (formerly Sterile Recoveries, Inc.), Steris Corporation and Waste Management, Inc. The graph assumes that $100 was invested on December 31, 2001 in our common stock and in the stock represented by each of the three indexes, and that all dividends were reinvested.

The stock price performance of our common stock reflected in the following graph is not necessarily indicative of future performance.

19

Item 6. Selected Consolidated Financial Data

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2006(3) | | | 2005 | | | 2004 | | | 2003 | | | 2002 | |

| | | (Dollars in thousands, except per share amounts) | |

Statements of Income Data(1) | | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 789,637 | | | $ | 609,457 | | | $ | 516,228 | | | $ | 453,225 | | | $ | 401,519 | |

Income from operations | | | 201,762 | | | | 166,532 | | | | 145,655 | | | | 126,397 | | | | 100,832 | |

Net income | | | 105,270 | | | | 67,154 | | | | 78,178 | | | | 65,781 | | | | 45,724 | |

Net income applicable to common stock | | | 105,270 | | | | 67,154 | | | | 78,178 | | | | 65,781 | | | | 45,037 | |

Diluted net income per share of common stock(2) | | | 2.33 | | | | 1.48 | | | | 1.69 | | | | 1.43 | | | | 1.01 | |

Depreciation and amortization | | | 27,036 | | | | 21,431 | | | | 21,803 | | | | 17,255 | | | | 14,981 | |

| | | | | |

Other Data | | | | | | | | | | | | | | | | | | | | |

Cash provided by operating activities | | $ | 160,162 | | | $ | 94,327 | | | $ | 114,611 | | | $ | 123,887 | | | $ | 98,731 | |

Cash used in investing activities | | | (201,425 | ) | | | (156,001 | ) | | | (105,093 | ) | | | (57,635 | ) | | | (49,470 | ) |

Cash provided by (used in) financing activities | | | 52,547 | | | | 59,500 | | | | (6,941 | ) | | | (66,820 | ) | | | (53,705 | ) |

| | | | | |

Balance Sheet Data (at December 31)(1) | | | | | | | | | | | | | | | | | | | | |

Cash, cash equivalents and short-term investments | | $ | 16,040 | | | $ | 8,545 | | | $ | 7,949 | | | $ | 7,881 | | | $ | 8,887 | |

Total assets | | | 1,327,906 | | | | 1,047,660 | | | | 834,141 | | | | 707,462 | | | | 667,095 | |

Long-term debt, net of current maturities | | | 443,115 | | | | 348,841 | | | | 190,431 | | | | 163,016 | | | | 224,124 | |

Convertible redeemable preferred stock | | | — | | | | — | | | | — | | | | 20,944 | | | | 28,049 | |

Shareholders’ equity | | $ | 625,081 | | | $ | 521,634 | | | $ | 495,372 | | | $ | 407,820 | | | $ | 326,729 | |

| (1) | See Note 4 to the Consolidated Financial Statements for information concerning our acquisitions during the three years ended December 31, 2006. |

| (2) | See Note 10 to the Consolidated Financial Statements for information concerning the computation of net income per common share. In 2006, net income includes costs (net of tax) related to stock compensation expense of $6.5 million, a fixed asset write-down of equipment of $0.2 million, write-down of an investment in securities of $0.6 million, acquisition-related costs of $2.1 million, partially offset by income recorded from insurance proceeds related to the 3CI settlement of $0.6 million that in total negatively impacted EPS by $0.19 per share. Of the total of $8.8 million of such items, $7.3 million were non-cash items. In 2005, net income includes costs (net of tax) related to the 3CI preliminary settlement of class action litigation of $23.4 million, South Africa note receivable write-down of $1.5 million, fixed asset impairments of $0.5 million, acquisition-related costs of $0.5 million, settlement of licensing litigation of $1.1 million, and items related to debt restructuring of $0.3 million which negatively impacted EPS by $0.60 per share. Of the total of $27.3 million of such items, $3.4 million were non-cash items. In 2004, net income includes acquisition-related costs of $0.5 million, fixed asset write-offs of $0.7 million, and items related to debt restructuring and redemption of senior subordinated debt of $2.8 million that negatively impacted EPS by $0.09 per share. Of the total of $4.0 million of such items, $1.4 million were non-cash items. In 2003, net income includes acquisition-related costs (net of tax) of $0.4 million and items related to debt restructuring and subordinated debt repurchase of $2.0 million, which negatively impacted EPS by $0.04 per share. Of the total of $2.4 million of such items, $0.5 million were non-cash items. In 2002, net income includes acquisition-related costs (net of tax) of $0.2 million, fixed asset write-offs of $1.8 million and items related to debt restructuring and subordinated debt repurchases of $1.4 million, which negatively impacted EPS by $0.08 per share. Of the total of $3.4 million of such items, $2.0 million were non-cash items. |

| (3) | On January 1, 2006, we adopted the provisions of SFAS No. 123R, “Share-Based Payment” (“SFAS No. 123R”) using the modified prospective method to account for stock compensation costs. SFAS No. 123R requires the measurement and recognition of compensation expense for all stock-based payment awards made to our employees and directors. During the year ended December 31, 2006, we recognized stock compensation expense of $6.5 million, net of tax. See Note 11 to the Consolidated Financial Statements for additional information related to stock compensation expense. |

20

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation

The following discussion of our financial condition and results of operations should be read in conjunction with our consolidated financial statements and related notes in Item 8 of this Report.

Introduction

We are in the business of managing regulated waste and providing an array of related services. We operate in the United States, the United Kingdom, Mexico, Canada, Ireland, and Argentina.

For large-quantity generators of regulated waste such as hospitals and for pharmaceutical companies and distributors, we offer: our institutional medical waste management services; ourBio Systems® sharps management services to reduce the risk of needle sticks; a variety of products and services for infection control; and our regulated returns management services for expired or recalled health care products.

For small-quantity generators of regulated waste such as doctors’ offices and for retail pharmacies, we offer: our medical waste management services; ourSteri-Safe® Occupational Safety and Health Act and Health Insurance Portability and Accountability Act (HIPAA) compliance programs; a variety of products and services for infection control; and our pharmaceutical returns services for expired or recalled pharmaceuticals.

We operate integrated national medical waste management networks in the United States, Canada, Mexico, Argentina, the United Kingdom and Ireland. Our national networks include a total of 76 processing or combined processing and collection sites and 104 additional transfer, collection or combined transfer and collection sites.

Our medical waste processing technologies include autoclaving, our proprietary electro-thermal-deactivation system (ETD), chemical treatment and incineration.

As of December 31, 2006, we served approximately 351,700 customers, of which approximately 343,100 were small quantity customers and approximately 8,600 were large quantity customers.

Critical Accounting Policies and Procedures

Our discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires that we make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and the related disclosure of contingent assets and liabilities. We believe that of our significant accounting policies (see Note 2 to our consolidated financial statements), the following ones may involve a higher degree of judgment on our part and greater complexity of reporting.

Revenue Recognition.We recognize revenue for our regulated waste services at the time of waste collection. Revenues from regulated returns management services are recorded at the time services are performed. Royalty revenues are calculated based on measurements specified in each contract or license and revenues are recognized at the end of each reporting period when the activity being measured has been completed. Revenues from product sales are recognized at the time the goods are shipped to the ordering customer. Software licensing revenues are recognized on a prorated basis over the term of the license agreement. Revenue and costs on contracts to supply our proprietary ETD treatment equipment are recognized based on shipment of equipment and services provided for in the individual contract. We had no revenues related to ETD sales in 2006 or 2005. We do not have any contracts in a loss position. Losses would be recorded when known and estimable for any contracts that should go into a loss position. Payments received in advance are deferred and recognized as services are provided.

Goodwill and Other Identifiable Intangible Assets.Goodwill associated with the excess purchase price over the fair value of assets acquired is not amortized. We have determined that our permits have indefinite lives and, accordingly are not amortized. This position is in accordance with Statement of Financial Accounting

21

Standards (“SFAS”) No. 142, which became effective for fiscal years beginning after December 15, 2001. See Note 8 Goodwill and Other Intangible Assets for additional information.

Our balance sheet at December 31, 2006 contains goodwill of $814.0 million. In accordance with SFAS No. 142, we evaluate on at least an annual basis, using the fair value of reporting units, whether goodwill is impaired. If we were to determine that a significant impairment has occurred, we would be required to incur non-cash write-offs of the impaired portion of goodwill that could have a material adverse effect on our results of operations in the period in which the write-off occurs. We use the market value of our stock as a measure of fair value and compare that to the ratio of earnings before income tax expense, depreciation expense, and amortization expense, to book value of each of our reporting unit when testing for goodwill impairment, and any unforeseen material drop in our stock price may be an indicator of a potential impairment of goodwill. The results of the 2006 impairment test conducted in June 2006 did not show any impairment of goodwill, and no events have occurred since that time that indicate that an impairment situation exists.

Our permits are currently tested for impairment annually at December 31, or more frequently if circumstances indicate that they may be impaired. We use a discounted cash flow model as the current measurement of the fair value of the permits. The estimate of cash flow is based upon, among other things, certain assumptions about expected future operating performance and an appropriate discount rate determined by management. Our estimates of discounted cash flow may differ from actual cash flow due to, among other things, inaccuracies in economic estimates, and actual cash flow could materially affect the future financial value of the permits. The results of the 2006 impairment test did not show any impairment of our permits and no events have occurred since that time that would indicate an impairment situation exists.

Other identifiable intangible assets, such as customer lists, tradenames and covenants not-to-compete, are currently amortized using the straight-line method over their estimated useful lives. We have determined that our regulated waste customer lists have between 20-year and 40-year lives based on the specific type of relationship. These assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may be less than the undiscounted cash flows. There have been no indicators of impairment of these intangibles (see Note 8 to our consolidated financial statements).

Income Taxes. Deferred income tax liabilities and assets are determined based on the differences between the financial statement and income tax basis of assets and liabilities using enacted tax rates in effect for the year in which the differences are expected to reverse. To provide for certain potential tax exposures, we maintain a reserve for specific tax contingencies, the balance of which management believes is adequate.

Accounts Receivable.Accounts receivable consist primarily of amounts due to us from our normal business activities. Accounts receivable balances are determined to be delinquent when the amount is past due based on the contractual terms with the customer. We maintain an allowance for doubtful accounts to reflect the expected uncollectibility of accounts receivable based on past collection history and specific risks identified among uncollected accounts. Accounts receivable are charged to the allowance for doubtful accounts when we have determined that the receivable will not be collected and/or when the account has been referred to a third party collection agency. No single customer accounts for more than 2% of our revenues.

Insurance. Our insurance for worker’s compensation, vehicle liability and physical damage, and employee-related health care benefits is obtained using high deductible insurance polices. A third-party administrator is used to process all such claims. We require all workers’ compensation, vehicle liability and physical damage claims to be reported within 24 hours. As a result, we accrue our worker’s compensation, vehicle and physical damage liability based upon the claim reserves established by the third-party administrator at the end of each reporting period. Our employee health insurance benefit liability is based on our historical claims experience rate. Our earnings would be impacted to the extent that actual claims vary from historical experience. We review our accruals associated with the exposure to these liabilities for adequacy at the end of each reporting period.

Litigation. We operate in a highly regulated industry and deal with regulatory inquiries or investigations from time to time that may be instituted for a variety of reasons. We are also involved in a variety of civil litigation from time to time. Settlements from litigation would be recorded when known, probable and estimable.

22

Stock Option Plans. We have issued stock options to employees and directors as an integral part of our compensation programs. On January 1, 2006, we adopted the provisions of SFAS No. 123R, “Share-Based Payment” (“SFAS No. 123R”) using the modified prospective method to account for stock compensation costs. SFAS No. 123R requires the measurement and recognition of compensation expense for all stock-based payment awards made to our employees and directors. Under the fair value recognition provisions of SFAS No. 123R, stock-based compensation cost is measured at the grant date based on the value of the award and is recognized as expense over the vesting period. Determining the fair value of stock-based awards at the grant date requires considerable judgment, including estimating expected volatility, expected term and risk-free rate. Our expected volatility is based upon historical experience. The expected term of the stock options is based upon historical experience. The risk-free interest rate assumption is based upon the average of the U.S. Treasury three and five-year yield rates. If factors change and we employ different assumptions, stock-based compensation expense may differ significantly from what we have recorded in the past.

Year Ended December 31, 2006 Compared to Year Ended December 31, 2005

The following summarizes (in thousands except per share amounts) our operations:

| | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2006 | | | 2005 | |

Revenues | | $ | 789,637 | | | 100.0 | % | | $ | 609,457 | | 100.0 | % |

Cost of revenues | | | 419,689 | | | 53.1 | % | | | 324,988 | | 53.3 | % |

Depreciation | | | 20,081 | | | 2.5 | % | | | 16,432 | | 2.7 | % |

| | | | | | | | | | | | | |

Total cost of revenues | | | 439,770 | | | 55.7 | % | | | 341,420 | | 56.0 | % |

| | | | | | | | | | | | | |

Gross profit | | | 349,867 | | | 44.3 | % | | | 268,037 | | 44.0 | % |

Selling, general and administrative | | | 137,411 | | | 17.4 | % | | | 93,033 | | 15.3 | % |

Depreciation | | | 3,989 | | | 0.5 | % | | | 3,403 | | 0.6 | % |

Amortization | | | 2,966 | | | 0.4 | % | | | 1,596 | | 0.3 | % |

| | | | | | | | | | | | | |

Total selling, general and administrative expenses | | | 144,366 | | | 18.3 | % | | | 98,032 | | 16.1 | % |

| | | | | | | | | | | | | |

Licensing legal settlement | | | — | | | — | | | | 1,823 | | 0.3 | % |

Write off fixed assets | | | 300 | | | 0.0 | % | | | 872 | | 0.1 | % |

Acquisition integration related expenses | | | 3,439 | | | 0.4 | % | | | 778 | | 0.1 | % |

| | | | | | | | | | | | | |

Income from operations | | | 201,762 | | | 25.6 | % | | | 166,532 | | 27.3 | % |

Write-down of investment in securities | | | 1,000 | | | 0.2 | % | | | — | | — | |

Write-down of note receivable with former joint venture | | | — | | | — | | | | 2,495 | | 0.4 | % |

3CI legal settlement(2005)/proceeds from insurance(2006) | | | (1,025 | ) | | -0.1 | % | | | 36,481 | | 6.0 | % |

Net interest expense | | | 27,061 | | | 3.4 | % | | | 12,247 | | 2.0 | % |

Income tax expense | | | 67,304 | | | 8.5 | % | | | 44,826 | | 7.4 | % |

Net income | | $ | 105,270 | | | 13.3 | % | | $ | 67,154 | | 11.0 | % |

| | | | | | | | | | | | | |

Earnings per share—diluted | | $ | 2.33 | | | | | | $ | 1.48 | | | |

| | | | | | | | | | | | | |

Revenues. Our revenues increased $180.2 million, or 29.6%, to $789.6 million in 2006 from $609.5 million in 2005. Revenues primarily increased as a result of domestic and international acquisitions. During 2006, acquisitions less than one year old contributed approximately $116.1 million to the increase in our revenues from 2005. In addition, strong revenue growth was exhibited in our Steri-SafeSM product offerings as a result of increased market penetration in the small quantity generator markets, continued success in the rollout of ourBio Systems sharps management program and growth in returns management services revenues. For the year, internal growth for small account customers increased approximately 11% while revenues from large quantity customers increased by approximately 9%.

23

During 2006, the size of the regulated waste market in the United States for the services we provide remained relatively stable. Through our acquisition of STG and Habitat Ecologico S.A. in February 2006, we were able to expand our geographic presence outside of North America.

Cost of Revenues. Our cost of revenues increased $98.4 million or 28.8%, to $439.8 million during 2006, from $341.4 million during 2005. This was primarily due to an increase in incremental expenses as a result of business acquisitions completed during 2006 and 2005. Our gross margin percentage increased to 44.3% during 2006 from 44.0% during 2005 due to an increase in gross margins on our domestic business as we continued to realize efficiencies from ongoing programs to improve the gross margins on our large and small quantity business. Domestic energy and transportation costs increased in 2006, which were partially offset by higher revenues related to fuel surcharges.