Cash Management Fund

Institutional Shares

Annual Report

to Shareholders

December 31, 2011

Contents

Cash Management Fund 3 Portfolio Management Review 7 Statement of Assets and Liabilities 8 Statement of Operations 9 Statement of Changes in Net Assets 11 Notes to Financial Statements 15 Report of Independent Registered Public Accounting Firm 16 Information About Your Fund's Expenses Cash Management Portfolio 36 Statement of Assets and Liabilities 37 Statement of Operations 38 Statement of Changes in Net Assets 40 Notes to Financial Statements 44 Report of Independent Registered Public Accounting Firm 45 Investment Management Agreement Approval 50 Summary of Management Fee Evaluation by Independent Fee Consultant 54 Board Members and Officers 59 Account Management Resources |

This report must be preceded or accompanied by a prospectus. To obtain a summary prospectus, if available, or prospectus for any of our funds, refer to the Account Management Resources information provided in the back of this booklet. We advise you to consider the fund's objectives, risks, charges and expenses carefully before investing. The summary prospectus and prospectus contain this and other important information about the fund. Please read the prospectus carefully before you invest.

An investment in this fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or by any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund. The share price of money market funds can fall below the $1.00 share price. You should not rely on or expect the Advisor to enter into support agreements or take other actions to maintain the fund's $1.00 share price. The credit quality of the fund's holdings can change rapidly in certain markets, and the default of a single holding could have an adverse impact on the fund's share price. The fund's share price can also be negatively affected during periods of high redemption pressures and/or illiquid markets. The actions of a few large investors of the fund may have a significant adverse effect on the share price of the fund. See the prospectus for specific details regarding the fund's risk profile.

DWS Investments is part of Deutsche Bank's Asset Management division and, within the U.S., represents the retail asset management activities of Deutsche Bank AG, Deutsche Bank Trust Company Americas, Deutsche Investment Management Americas Inc. and DWS Trust Company.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

Portfolio Management Review

Market Overview

All performance information below is historical and does not guarantee future results. Investment return and principal fluctuate, so your shares may be worth more or less when redeemed. Current performance may differ from performance data shown. Please visit www.dbadvisorsliquidity.com/US for the fund's most recent month-end performance. The 7-day current yield refers to the income paid by the fund over a 7-day period expressed as an annual percentage rate of the fund's shares outstanding. Yields fluctuate and are not guaranteed.

Over the fund's most recent 12-month period ended December 31, 2011, money markets were responding to alternating degrees of perceived risk in the global financial markets, with short-term rates rising or falling slightly in response to the current state of the European sovereign debt crisis. During the summer, the political standoff in the United States related to the raising of the U.S. debt ceiling spurred volatility in financial markets. The extreme difficulties that Congress encountered in coming to agreement regarding the debt ceiling made up a large part of the rationale cited by Standard & Poor's® in deciding to downgrade U.S. debt from AAA to AA+ on August 5, 2011. However, the United States' role as a perceived "safe haven" for fixed-income investors worldwide has thus far remained unchanged. In addition, credit downgrades of various domestic and international banks and "credit watches" instituted by ratings agencies on some European countries exerted pressure on the money markets. Encouragingly, the European Central Bank (ECB) has made some extraordinary efforts over the past several months to head off additional problems for European governments and banks by securing funding access for the major banks in Europe.

Positive Contributors to Fund Performance

We were able to maintain a competitive yield for the fund during the period.

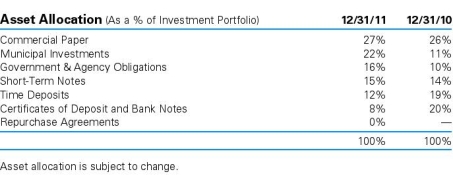

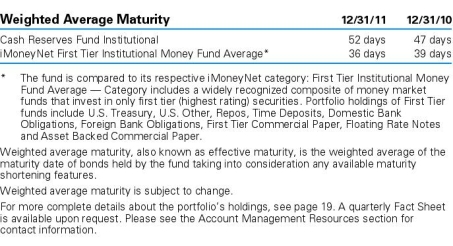

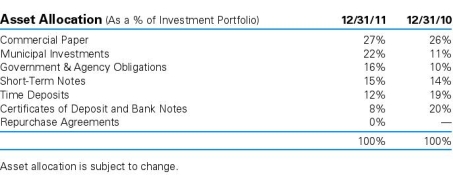

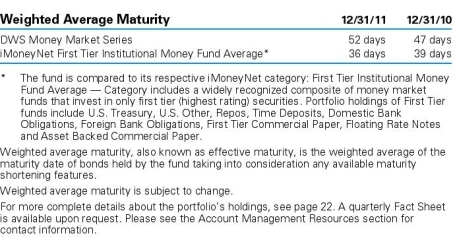

Over the period, we continued to hold a large percentage of portfolio assets in short-maturity instruments for liquidity purposes as well as for high quality and yield. We also maintained a higher than average maturity, with fund assets broadly diversified among a number of different sectors, including banks, corporate issues, U.S. government securities and municipal debt, though diversification neither assures a profit nor guarantees against loss. In addition, we focused on more favorable geographical areas for money market investment, such as Canada, Australia and the Nordic region. Lastly, given market uncertainty and our desire to maintain larger cash positions in the fund, we found value in municipal Variable Rate Demand Notes compared with taxable alternatives of the same maturity, such as bank Certificates of Deposit.

Fund Performance (as of December 31, 2011)

Performance is historical and does not guarantee future results. Current performance may be lower or higher than the performance data quoted.

An investment in this fund is not insured or guaranteed by the FDIC or by any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund. The share price of money market funds can fall below the $1.00 share price.

| 7-Day Current Yield |

| December 31, 2011 | .01%* |

| December 31, 2010 | .02%* |

| * The investment advisor has agreed to waive fees/reimburse expenses. Without such fee waivers/expense reimbursements, the 7-day current yield would have been lower. |

Yields are historical, will fluctuate and do not guarantee future performance. The 7-day current yield refers to the income paid by the portfolio over a 7-day period expressed as an annual percentage rate of the fund's shares outstanding. Please visit our Web site at www.dbadvisorsliquidity.com/US for the product's most recent month-end performance.

Negative Contributors to Fund Performance

The types of securities that we were investing in during the period ended December 31, 2011, tended to have shorter maturities and lower yields than issues carrying more risk. We preferred to be cautious during a time of market fluctuation. In the end this cost the fund some yield, but we believe that this represented a prudent approach to preserving principal.

| "Encouragingly, the European Central Bank (ECB) has made some extraordinary efforts over the past several months to head off additional problems for European governments and banks by securing funding access for the major banks in Europe." |

Outlook and Positioning

Positive news for U.S. markets has come recently in the form of improved economic reports, including a pickup in manufacturing activity and some declines in domestic unemployment. The U.S. Federal Reserve Board (the Fed) has been doing its part by continuing its accommodative monetary policy and hinting at additional transparency for financial market participants in the near term. The main headwind to improved economic and financial market prospects comes from uncertainty over the European sovereign debt crisis. With several European countries facing austerity measures, we tend to believe that Europe is on the precipice of a recession. Market participants are urgently wishing for concrete and permanent solutions to the European crisis in the hopes that such a result would encourage further global economic progress and reduce financial market uncertainty.

We continue our insistence on the highest credit quality within the fund. We also continue to apply a careful approach to investing on behalf of the fund and to seek competitive yield for our shareholders.

Portfolio Management Team

A group of investment professionals is responsible for the day-to-day management of the fund. These investment professionals have a broad range of experience managing money market funds.

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team's views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

Terms to Know

Municipal debt is state and local government bonds issued to finance capital expenditures.

Credit quality measures a bond issuer's ability to repay interest and principal in a timely manner. Rating agencies assign letter designations, such as AAA, AA and so forth. The lower the rating, the higher the probability of default. Credit quality does not remove market risk and is subject to change.

Statement of Assets and Liabilities | as of December 31, 2011 | |

| Assets | |

| Investment in Cash Management Portfolio, at value | | $ | 2,270,908,089 | |

| Receivable for Fund shares sold | | | 408 | |

| Due from Advisor | | | 12,427 | |

| Other assets | | | 17,644 | |

| Total assets | | | 2,270,938,568 | |

| Liabilities | |

| Payable for Fund shares redeemed | | | 1,407,188 | |

| Distributions payable | | | 8,735 | |

| Other accrued expenses and payables | | | 372,406 | |

| Total liabilities | | | 1,788,329 | |

| Net assets, at value | | $ | 2,269,150,239 | |

| Net Assets Consist of | |

| Accumulated net realized gain (loss) | | | (197,391 | ) |

| Paid-in capital | | | 2,269,347,630 | |

| Net assets, at value | | $ | 2,269,150,239 | |

| Net Asset Value | |

Institutional Shares Net Asset Value, offering and redemption price per share ($2,269,150,239 ÷ 2,269,421,063 outstanding shares of beneficial interest, $.01 par value, unlimited number of shares authorized) | | $ | 1.00 | |

The accompanying notes are an integral part of the financial statements.

| for the year ended December 31, 2011 | |

| Investment Income | |

Income and expenses allocated from Cash Management Portfolio: Interest | | $ | 5,311,121 | |

| Expenses* | | | (3,213,064 | ) |

| Net investment income allocated from Cash Management Portfolio | | | 2,098,057 | |

Expenses: Administration fee | | | 2,137,929 | |

| Services to shareholders | | | 171,894 | |

| Service fees | | | 1,193,280 | |

| Professional fees | | | 35,433 | |

| Reports to shareholders | | | 48,837 | |

| Registration fees | | | 31,905 | |

| Trustees' fees and expenses | | | 4,551 | |

| Other | | | 27,720 | |

| Total expenses before expense reductions | | | 3,651,549 | |

| Expense reductions | | | (1,796,469 | ) |

| Total expenses after expense reductions | | | 1,855,080 | |

| Net investment income (loss) | | | 242,977 | |

| Net realized gain (loss) allocated from Cash Management Portfolio | | | 105,324 | |

| Net increase (decrease) in net assets resulting from operations | | $ | 348,301 | |

* Net of $215,611 Advisor reimbursement allocated from Cash Management Portfolio for the year ended December 31, 2011.

The accompanying notes are an integral part of the financial statements.

Statement of Changes in Net Assets | | | Years Ended December 31, | |

| Increase (Decrease) in Net Assets | | 2011 | | | 2010 | |

Operations: Net investment income | | $ | 242,977 | | | $ | 1,157,839 | |

| Net realized gain (loss) | | | 105,324 | | | | 229,420 | |

| Net increase (decrease) in net assets resulting from operations | | | 348,301 | | | | 1,387,259 | |

Distributions to shareholders from: Net investment income | | | (251,515 | ) | | | (1,222,839 | ) |

Fund share transactions: Proceeds from shares sold | | | 14,897,455,866 | | | | 13,959,569,610 | |

| Reinvestment of distributions | | | 207,268 | | | | 1,106,246 | |

| Payments for shares redeemed | | | (15,161,351,369 | ) | | | (13,464,962,553 | ) |

| Net increase (decrease) in net assets from Fund share transactions | | | (263,688,235 | ) | | | 495,713,303 | |

| Increase (decrease) in net assets | | | (263,591,449 | ) | | | 495,877,723 | |

| Net assets at beginning of period | | | 2,532,741,688 | | | | 2,036,863,965 | |

| Net assets at end of period (including undistributed net investment income of $0 and $0, respectively) | | $ | 2,269,150,239 | | | $ | 2,532,741,688 | |

| Other Information | |

| Shares outstanding at beginning of period | | | 2,533,109,298 | | | | 2,037,395,995 | |

| Shares sold | | | 14,897,455,866 | | | | 13,959,569,610 | |

| Shares issued to shareholders in reinvestment of distributions | | | 207,268 | | | | 1,106,246 | |

| Shares redeemed | | | (15,161,351,369 | ) | | | (13,464,962,553 | ) |

| Net increase (decrease) in Fund shares | | | (263,688,235 | ) | | | 495,713,303 | |

| Shares outstanding at end of period | | | 2,269,421,063 | | | | 2,533,109,298 | |

The accompanying notes are an integral part of the financial statements.

| Institutional Shares | |

| | | Years Ended December 31, | |

| | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| Selected Per Share Datac | |

| Net asset value, beginning of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

Income from investment operations: Net investment income | | | .000 | a | | | .001 | | | | .004 | | | | .027 | | | | .051 | |

Net realized gain (loss)a | | | .000 | | | | .000 | | | | .000 | | | | .000 | | | | .000 | |

| Total from investment operations | | | .000 | a | | | .001 | | | | .004 | | | | .027 | | | | .051 | |

Less distributions from: Net investment income | | | (.000 | )a | | | (.001 | ) | | | (.004 | ) | | | (.027 | ) | | | (.051 | ) |

| Net asset value, end of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

Total Return (%)b | | | .01 | | | | .05 | | | | .37 | | | | 2.70 | | | | 5.22 | |

| Ratios to Average Net Assets and Supplemental Data | |

| Net assets, end of period ($ millions) | | | 2,269 | | | | 2,533 | | | | 2,037 | | | | 2,668 | | | | 2,594 | |

| Ratio of expenses before expense reductions, including expenses allocated from Cash Management Portfolio (%) | | | .33 | | | | .34 | | | | .38 | | | | .34 | | | | .35 | |

| Ratio of expenses after expense reductions, including expenses allocated from Cash Management Portfolio (%) | | | .24 | | | | .28 | | | | .26 | | | | .24 | | | | .23 | |

| Ratio of net investment income (%) | | | .01 | | | | .05 | | | | .34 | | | | 2.68 | | | | 5.10 | |

a Amount is less than $.0005. b Total return would have been lower had certain expenses not been reduced. | |

Notes to Financial Statements

A. Organization and Significant Accounting Policies

Cash Management Fund (the "Fund'') is a series of DWS Money Market Trust (the "Trust''), which is registered under the Investment Company Act of 1940, as amended (the "1940 Act''), as an open-end management investment company organized as a Massachusetts business trust. The Fund offers one class of shares, Institutional Shares, to investors. The Fund is the successor to Cash Management Fund, a series of DWS Institutional Funds (the "Predecessor Fund"). On April 29, 2011, the Predecessor Fund transferred all of its assets and liabilities to the Trust, while retaining the same fund name. The transaction had no material effect on an investment in the Fund. All financial and other information contained herein for periods prior to April 29, 2011, is that of the Predecessor Fund.

The Fund, a feeder fund, seeks to achieve its investment objective by investing all of its investable assets in a master portfolio, the Cash Management Portfolio (the "Portfolio''), an open-end management investment company registered under the 1940 Act and organized as a New York business trust advised by Deutsche Investment Management Americas Inc. ("DIMA'' or the "Advisor''), an indirect, wholly owned subsidiary of Deutsche Bank AG. A master/feeder fund structure is one in which a fund (a "feeder fund"), instead of investing directly in a portfolio of securities, invests most or all of its investment assets in a separate registered investment company (the "master fund") with substantially the same investment objective and policies as the feeder fund. Such a structure permits the pooling of assets of two or more feeder funds, preserving separate identities or distribution channels at the feeder fund level. At December 31, 2011, the Fund owned approximately 11% of the Portfolio.

The Fund's financial statements are prepared in accordance with accounting principles generally accepted in the United States of America which require the use of management estimates. Actual results could differ from those estimates. The policies described below are followed consistently by the Fund in the preparation of its financial statements. The financial statements of the Portfolio, including the Investment Portfolio, are contained elsewhere in this report and should be read in conjunction with the Fund's financial statements.

Security Valuation. The Fund records its investment in the Portfolio at value, which reflects its proportionate interest in the net assets of the Portfolio. Valuation of the securities held by the Portfolio is discussed in the notes to the Portfolio's financial statements included elsewhere in this report.

Disclosure about the classification of fair value measurements is included in a table following the Portfolio's Investment Portfolio.

Federal Income Taxes. The Fund's policy is to comply with the requirements of the Internal Revenue Code, as amended, which are applicable to regulated investment companies, and to distribute all of its taxable income to its shareholders.

Under the Regulated Investment Company Modernization Act of 2010, net capital losses may be carried forward indefinitely, and their character is retained as short-term and/or long-term. Previously, net capital losses were carried forward for eight years and treated as short-term losses. As a transition rule, the Act requires that post-enactment net capital losses be used before pre-enactment net capital losses.

At December 31, 2011, the Fund had a net tax basis capital loss carryforward of approximately $197,000 of pre-enactment losses, which may be applied against any realized net taxable capital gains of each succeeding year until fully utilized or until December 31, 2016, the expiration date, whichever occurs first.

The Fund has reviewed the tax positions for the open tax years as of December 31, 2011 and has determined that no provision for income tax is required in the Fund's financial statements. The Fund's federal tax returns for the prior three fiscal years remain open subject to examination by the Internal Revenue Service.

Distribution of Income and Gains. Net investment income of the Fund is declared as a daily dividend and is distributed to shareholders monthly. The Fund may take into account capital gains and losses in its daily dividend declarations. The Fund may also make additional distributions for tax purposes if necessary.

Permanent book and tax differences relating to shareholder distributions will result in reclassifications to paid in capital. Temporary book and tax differences will reverse in a subsequent period. There were no significant book to tax differences for the Fund.

At December 31, 2011, the Fund's components of distributable earnings (accumulated losses) on a tax basis were as follows:

| Capital loss carryforward | | $ | (197,000 | ) |

In addition, the tax character of distributions paid to shareholders by the Fund is summarized as follows:

| | | Years Ended December 31, | |

| | | 2011 | | | 2010 | |

| Distributions from ordinary income | | $ | 251,515 | | | $ | 1,222,839 | |

Contingencies. In the normal course of business, the Fund may enter into contracts with service providers that contain general indemnification clauses. The Fund's maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet been made. However, based on experience, the Fund expects the risk of loss to be remote.

Other. The Fund receives an allocation of the Portfolio's net investment income and net realized gains and losses in proportion to its investment in the Portfolio. Expenses directly attributed to a fund are charged to that fund, while expenses which are attributable to the Trust are allocated among the funds in the Trust on the basis of relative net assets.

B. Fees and Transactions with Affiliates

Management Agreement. Under the Investment Management Agreement with Deutsche Investment Management Americas Inc. ("DIMA" or the "Advisor"), an indirect, wholly owned subsidiary of Deutsche Bank AG, the Advisor serves as the investment manager to the Fund. The Advisor receives a management fee from the Portfolio pursuant to the master/feeder structure listed above in Note A.

Administration Fee. Pursuant to an Administrative Services Agreement, DIMA provides most administrative services to the Fund. For all services provided under the Administrative Services Agreement, the Fund pays the Advisor an annual fee ("Administration Fee") of 0.10% of the Fund's average daily net assets, computed and accrued daily and payable monthly.

For the period from January 1, 2011 through September 30, 2012, DIMA has contractually agreed to waive its fees and/or reimburse certain operating expenses of the Fund, including expenses of the Portfolio allocated to the Fund, to the extent necessary to maintain the operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage and interest) at 0.30% of the Fund's average daily net assets.

Accordingly, for the year ended December 31, 2011, the Administration Fee was $2,137,929, of which $443,808 was waived and $144,380 is unpaid.

In addition, the Advisor has agreed to voluntarily waive additional expenses. The waiver may be changed or terminated at any time without notice. Under this arrangement, the Advisor waived certain expenses of the Fund.

Service Provider Fees. DWS Investments Service Company ("DISC"), an affiliate of the Advisor, is the transfer agent, dividend-paying agent and shareholder service agent for the Fund. Pursuant to a sub-transfer agency agreement between DISC and DST Systems, Inc. ("DST"), DISC has delegated certain transfer agent, dividend-paying agent and shareholder service agent functions to DST. DISC compensates DST out of the shareholder servicing fee it receives from the Fund. For the year ended December 31, 2011, the amount charged to the Fund by DISC aggregated $73,024, all of which was waived.

In addition, for the year ended December 31, 2011, the Advisor reimbursed the fund $86,357 of sub-recordkeeping expense.

Shareholder Servicing Fee. DWS Investments Distributors, Inc. ("DIDI"), an affiliate of the Advisor, provides information and administrative services for a fee ("Service Fee") to shareholders at an annual rate of up to 0.25% of average daily net assets. DIDI in turn has various agreements with financial services firms that provide these services and pays these fees based upon the assets of shareholder accounts the firm services. For the year ended December 31, 2011, the Service Fee was as follows:

| | | Total Aggregated | | | Waived | | | Annual Effective Rate | |

| Cash Management Fund | | $ | 1,193,280 | | | $ | 1,193,280 | | | | .00 | % |

Typesetting and Filing Service Fees. Under an agreement with DIMA, DIMA is compensated for providing typesetting and certain regulatory filing services to the Fund. For the year ended December 31, 2011, the amount charged to the Fund by DIMA included in the Statement of Operations under "reports to shareholders" aggregated $21,332, of which $8,777 is unpaid.

Trustees' Fees and Expenses. The Fund paid each Trustee not affiliated with the Advisor retainer fees plus specified amounts for various committee services and for the Board Chairperson.

C. Concentration of Ownership

From time to time, the Fund may have a concentration of several shareholder accounts holding a significant percentage of shares outstanding. Investment activities of these shareholders could have a material impact on the Fund.

At December 31, 2011, there was one shareholder account that held approximately 23% of the outstanding shares of the Fund.

Report of Independent Registered Public Accounting Firm

To the Trustees of DWS Money Market Trust and Shareholders of Cash Management Fund:

In our opinion, the accompanying statement of assets and liabilities and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Cash Management Fund (hereafter referred to as the "Fund'') at December 31, 2011, and the results of its operations, the changes in its net assets and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements'') are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

Boston, Massachusetts February 24, 2012 | PricewaterhouseCoopers LLP |

Information About Your Fund's Expenses

As an investor of the Fund, you incur two types of costs: ongoing expenses and transaction costs. Ongoing expenses include management fees and other Fund expenses. Examples of transaction costs include account maintenance fees, which are not shown in this section. The following tables are intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to help you compare these expenses with the ongoing expenses of investing in other mutual funds. In the most recent six-month period, the Fund limited these expenses; had it not done so, expenses would have been higher. The example in the table is based on an investment of $1,000 invested at the beginning of the six-month period and held for the entire period (July 1, 2011 to December 31, 2011).

The tables illustrate your Fund's expenses in two ways:

·Actual Fund Return. This helps you estimate the actual dollar amount of ongoing expenses (but not transaction costs) paid on a $1,000 investment in the Fund using the Fund's actual return during the period. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the "Expenses Paid per $1,000" line under the share class you hold.

·Hypothetical 5% Fund Return. This helps you to compare your Fund's ongoing expenses (but not transaction costs) with those of other mutual funds using the Fund's actual expense ratio and a hypothetical rate of return of 5% per year before expenses. Examples using a 5% hypothetical fund return may be found in the shareholder reports of other mutual funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in these tables are meant to highlight your ongoing expenses only and do not reflect any transaction costs. The "Expenses Paid per $1,000" line of the tables is useful in comparing ongoing expenses only and will not help you determine the relative total expense of owning different funds. If these transaction costs had been included, your costs would have been higher.

Expenses and Value of a $1,000 Investment for the six months ended December 31, 2011 | |

| Actual Fund Return* | | Institutional Shares | |

| Beginning Account Value 7/1/11 | | $ | 1,000.00 | |

| Ending Account Value 12/31/11 | | $ | 1,000.05 | |

| Expenses Paid per $1,000** | | $ | 1.06 | |

| Hypothetical 5% Fund Return* | | Institutional Shares | |

| Beginning Account Value 7/1/11 | | $ | 1,000.00 | |

| Ending Account Value 12/31/11 | | $ | 1,024.15 | |

| Expenses Paid per $1,000** | | $ | 1.07 | |

* Expenses include amounts allocated proportionally from the master portfolio.

** Expenses are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by 365.

| Annualized Expense Ratio | | Institutional Shares | |

| Cash Management Fund | | | .21 | % |

For more information, please refer to the Fund's prospectus.

Tax Information (Unaudited)

A total of 4.12% of the dividends distributed during the fiscal year was derived from interest on U.S. government securities, which is generally exempt from state income tax.

Please contact a tax advisor if you have questions about federal or state income tax laws, or on how to prepare your tax returns. If you have specific questions about your account, please call (800) 621-1048

(The following financial statements of the Cash Management Portfolio should be read in conjunction with the Fund's financial statements.)

Investment Portfolio as of December 31, 2011 | | | Principal Amount ($) | | | Value ($) | |

| | | | |

| Certificates of Deposit and Bank Notes 7.5% | |

| ANZ National International Ltd., 144A, 3.25%, 4/2/2012 | | | 49,000,000 | | | | 49,336,289 | |

| Banco del Estado de Chile, 0.5%, 1/17/2012 | | | 20,000,000 | | | | 20,000,000 | |

| Bank Nederlandse Gemeenten, 6.0%, 3/26/2012 | | | 35,000,000 | | | | 35,455,384 | |

| Bank of Nova Scotia, 0.28%, 1/4/2012 | | | 100,000,000 | | | | 100,000,000 | |

| China Construction Bank Corp., 0.3%, 1/3/2012 | | | 37,451,000 | | | | 37,451,000 | |

| Commonwealth Bank of Australia, 144A, 2.4%, 1/12/2012 | | | 43,132,000 | | | | 43,157,466 | |

| Credit Suisse, 0.38%, 1/3/2012 | | | 97,000,000 | | | | 97,000,000 | |

| DnB Bank ASA, 0.35%, 1/17/2012 | | | 79,500,000 | | | | 79,500,000 | |

| General Electric Capital Corp., 6.0%, 6/15/2012 | | | 12,500,000 | | | | 12,810,030 | |

| Industrial & Commercial Bank of China: | |

| 0.7%, 1/3/2012 | | | 100,000,000 | | | | 100,000,000 | |

| 0.7%, 1/4/2012 | | | 99,500,000 | | | | 99,500,000 | |

| 0.7%, 1/6/2012 | | | 39,600,000 | | | | 39,600,000 | |

| Mizuho Corporate Bank Ltd., 0.42%, 2/6/2012 | | | 50,000,000 | | | | 50,003,492 | |

| Nederlandse Waterschapsbank NV, 1.375%, 2/17/2012 | | | 44,700,000 | | | | 44,756,807 | |

| Nordea Bank Finland PLC: | |

| 0.35%, 1/13/2012 | | | 69,500,000 | | | | 69,500,000 | |

| 0.4%, 2/15/2012 | | | 45,000,000 | | | | 45,000,561 | |

| Rabobank Nederland NV: | |

| 0.4%, 2/15/2012 | | | 133,500,000 | | | | 133,500,000 | |

| 0.43%, 2/24/2012 | | | 45,000,000 | | | | 45,000,000 | |

| 0.43%, 3/2/2012 | | | 160,000,000 | | | | 160,000,000 | |

| Skandinaviska Enskilda Banken AB: | |

| 0.35%, 1/11/2012 | | | 49,700,000 | | | | 49,700,000 | |

| 0.36%, 1/6/2012 | | | 46,500,000 | | | | 46,500,000 | |

| 0.45%, 2/13/2012 | | | 138,500,000 | | | | 138,500,000 | |

| Sumitomo Mitsui Banking Corp., 0.35%, 1/13/2012 | | | 50,000,000 | | | | 50,000,332 | |

| Svenska Handelsbanken AB, 0.385%, 1/23/2012 | | | 15,000,000 | | | | 15,000,091 | |

Total Certificates of Deposit and Bank Notes (Cost $1,561,271,452) | | | | 1,561,271,452 | |

| | |

| Commercial Paper 26.3% | |

| Issued at Discount** 24.7% | |

| ASB Finance Ltd., 0.585%, 4/27/2012 | | | 981,000 | | | | 979,135 | |

| Australia & New Zealand Banking Group Ltd., 0.25%, 2/7/2012 | | | 200,000 | | | | 199,949 | |

| Bank of Nova Scotia, 0.1%, 1/17/2012 | | | 600,000 | | | | 599,973 | |

| Barclays Bank PLC: | |

| 0.2%, 1/3/2012 | | | 1,000,000 | | | | 999,989 | |

| 0.33%, 1/20/2012 | | | 145,000,000 | | | | 144,974,746 | |

| 0.36%, 1/6/2012 | | | 30,000,000 | | | | 29,998,500 | |

| 0.38%, 1/4/2012 | | | 153,000,000 | | | | 152,995,155 | |

| 0.46%, 2/1/2012 | | | 77,000,000 | | | | 76,969,499 | |

| 0.52%, 2/27/2012 | | | 33,500,000 | | | | 33,472,418 | |

| BNZ International Funding Ltd: | |

| 144A, 0.57%, 4/10/2012 | | | 60,000,000 | | | | 59,905,000 | |

| 144A, 0.58%, 4/10/2012 | | | 50,000,000 | | | | 49,919,444 | |

| Coca-Cola Co.: | |

| 0.18%, 6/1/2012 | | | 29,888,000 | | | | 29,865,285 | |

| 0.2%, 4/10/2012 | | | 30,350,000 | | | | 30,333,139 | |

| Erste Abwicklungsanstalt: | |

| 0.35%, 1/30/2012 | | | 20,000,000 | | | | 19,994,361 | |

| 0.36%, 1/30/2012 | | | 50,000,000 | | | | 49,985,500 | |

| 0.37%, 1/9/2012 | | | 50,000,000 | | | | 49,995,889 | |

| 0.37%, 1/17/2012 | | | 50,000,000 | | | | 49,991,778 | |

| 0.39%, 2/16/2012 | | | 50,000,000 | | | | 49,975,083 | |

| 0.4%, 3/14/2012 | | | 35,000,000 | | | | 34,971,611 | |

| 0.42%, 1/3/2012 | | | 55,500,000 | | | | 55,498,705 | |

| Erste Finance Delaware LLC, 0.16%, 1/3/2012 | | | 154,540,000 | | | | 154,538,626 | |

| General Electric Capital Corp., 0.25%, 2/2/2012 | | | 150,000,000 | | | | 149,966,667 | |

| General Electric Capital Services, Inc.: | |

| 0.23%, 2/6/2012 | | | 42,000,000 | | | | 41,990,340 | |

| 0.26%, 2/2/2012 | | | 50,000,000 | | | | 49,988,444 | |

| 0.3%, 2/13/2012 | | | 75,000,000 | | | | 74,973,125 | |

| Johnson & Johnson: | |

| 144A, 0.02%, 1/13/2012 | | | 25,000,000 | | | | 24,999,833 | |

| 144A, 0.04%, 2/27/2012 | | | 75,000,000 | | | | 74,995,250 | |

| 144A, 0.05%, 4/3/2012 | | | 10,000,000 | | | | 9,998,708 | |

| 144A, 0.06%, 2/17/2012 | | | 100,000,000 | | | | 99,992,167 | |

| 144A, 0.07%, 4/2/2012 | | | 280,000,000 | | | | 279,947,867 | |

| 144A, 0.08%, 4/2/2012 | | | 70,000,000 | | | | 69,985,689 | |

| 144A, 0.08%, 4/3/2012 | | | 40,000,000 | | | | 39,991,733 | |

| 144A, 0.15%, 3/7/2012 | | | 33,175,000 | | | | 33,165,877 | |

| Kells Funding LLC: | |

| 144A, 0.29%, 1/12/2012 | | | 125,000,000 | | | | 124,988,924 | |

| 144A, 0.3%, 1/26/2012 | | | 25,000,000 | | | | 24,994,792 | |

| 144A, 0.35%, 2/17/2012 | | | 43,100,000 | | | | 43,080,306 | |

| 144A, 0.37%, 3/19/2012 | | | 25,700,000 | | | | 25,679,397 | |

| 144A, 0.37%, 4/10/2012 | | | 80,000,000 | | | | 79,917,778 | |

| 144A, 0.38%, 4/17/2012 | | | 25,000,000 | | | | 24,971,764 | |

| 144A, 0.45%, 1/20/2012 | | | 75,687,000 | | | | 75,669,024 | |

| 144A, 0.48%, 1/19/2012 | | | 57,014,000 | | | | 57,000,317 | |

| 144A, 0.52%, 2/1/2012 | | | 72,500,000 | | | | 72,467,536 | |

| 144A, 0.52%, 2/16/2012 | | | 37,000,000 | | | | 36,975,416 | |

| Merck & Co., Inc.: | |

| 0.06%, 1/9/2012 | | | 7,750,000 | | | | 7,749,897 | |

| 0.06%, 1/11/2012 | | | 86,000,000 | | | | 85,998,567 | |

| New York Life Capital Corp.: | |

| 144A, 0.12%, 2/3/2012 | | | 3,725,000 | | | | 3,724,590 | |

| 144A, 0.13%, 2/1/2012 | | | 37,900,000 | | | | 37,895,757 | |

| 144A, 0.15%, 3/2/2012 | | | 20,000,000 | | | | 19,994,917 | |

| 144A, 0.16%, 2/14/2012 | | | 25,000,000 | | | | 24,995,111 | |

| 144A, 0.16%, 3/8/2012 | | | 40,000,000 | | | | 39,988,089 | |

| 144A, 0.16%, 3/19/2012 | | | 38,000,000 | | | | 37,986,827 | |

| Nieuw Amsterdam Receivables Corp.: | |

| 144A, 0.32%, 1/4/2012 | | | 100,000,000 | | | | 99,997,333 | |

| 144A, 0.33%, 1/3/2012 | | | 653,000 | | | | 652,988 | |

| NRW.Bank: | |

| 0.24%, 1/17/2012 | | | 30,062,000 | | | | 30,058,793 | |

| 0.4%, 1/6/2012 | | | 61,000,000 | | | | 60,996,611 | |

| Oversea-Chinese Banking Corp., Ltd., 0.29%, 1/17/2012 | | | 45,000,000 | | | | 44,994,200 | |

| PepsiCo, Inc., 0.04%, 1/18/2012 | | | 95,000,000 | | | | 94,998,206 | |

| Pfizer, Inc.: | |

| 0.03%, 1/5/2012 | | | 58,000,000 | | | | 57,999,807 | |

| 0.04%, 1/12/2012 | | | 40,000,000 | | | | 39,999,511 | |

| Proctor & Gamble Co.: | |

| 0.08%, 1/3/2012 | | | 100,000,000 | | | | 99,999,556 | |

| 0.08%, 1/31/2012 | | | 40,000,000 | | | | 39,997,333 | |

| 0.08%, 2/24/2012 | | | 34,000,000 | | | | 33,995,920 | |

| 0.08%, 3/23/2012 | | | 60,000,000 | | | | 59,989,067 | |

| 0.09%, 1/25/2012 | | | 40,000,000 | | | | 39,997,600 | |

| 0.09%, 2/14/2012 | | | 75,000,000 | | | | 74,991,750 | |

| 0.09%, 3/30/2012 | | | 25,000,000 | | | | 24,994,437 | |

| 0.1%, 4/9/2012 | | | 25,000,000 | | | | 24,993,125 | |

| 0.11%, 5/4/2012 | | | 30,000,000 | | | | 29,988,633 | |

| 0.11%, 5/21/2012 | | | 23,000,000 | | | | 22,990,091 | |

| 0.12%, 4/2/2012 | | | 67,800,000 | | | | 67,779,208 | |

| 0.12%, 5/4/2012 | | | 128,000,000 | | | | 127,947,093 | |

| 0.13%, 4/12/2012 | | | 75,000,000 | | | | 74,972,375 | |

| 0.13%, 4/30/2012 | | | 80,000,000 | | | | 79,965,333 | |

| 0.15%, 3/30/2012 | | | 25,000,000 | | | | 24,990,729 | |

| Rabobank U.S.A. Financial Corp., 0.4%, 2/8/2012 | | | 19,250,000 | | | | 19,241,872 | |

| SBAB Bank AB: | |

| 144A, 0.5%, 1/4/2012 | | | 50,000,000 | | | | 49,997,917 | |

| 144A, 0.55%, 1/13/2012 | | | 15,000,000 | | | | 14,997,250 | |

| 144A, 0.55%, 1/30/2012 | | | 26,000,000 | | | | 25,988,481 | |

| Sheffield Receivables Corp.: | |

| 144A, 0.3%, 1/27/2012 | | | 24,000,000 | | | | 23,994,800 | |

| 144A, 0.4%, 2/7/2012 | | | 61,000,000 | | | | 60,974,922 | |

| Standard Chartered Bank: | |

| 0.37%, 1/5/2012 | | | 100,000,000 | | | | 99,995,889 | |

| 0.38%, 2/7/2012 | | | 135,750,000 | | | | 135,696,982 | |

| Straight-A Funding LLC: | |

| 144A, 0.12%, 1/11/2012 | | | 30,105,000 | | | | 30,103,996 | |

| 144A, 0.19%, 1/31/2012 | | | 60,061,000 | | | | 60,051,490 | |

| 144A, 0.19%, 2/13/2012 | | | 27,999,000 | | | | 27,992,646 | |

| Sumitomo Mitsui Banking Corp., 0.355%, 1/6/2012 | | | 77,050,000 | | | | 77,046,201 | |

| Swedbank AB, 0.44%, 1/13/2012 | | | 35,000,000 | | | | 34,994,867 | |

| Toyota Motor Credit Corp., 0.27%, 1/6/2012 | | | 107,000,000 | | | | 106,995,987 | |

| Unilever Capital Corp., 0.08%, 3/6/2012 | | | 30,000,000 | | | | 29,995,667 | |

| Victory Receivables Corp.: | |

| 144A, 0.35%, 1/19/2012 | | | 50,000,000 | | | | 49,991,250 | |

| 144A, 0.36%, 1/9/2012 | | | 75,106,000 | | | | 75,099,992 | |

| Walt Disney Co., 0.09%, 2/23/2012 | | | 95,000,000 | | | | 94,987,412 | |

| | | | | 5,125,675,814 | |

| Issued at Par 1.6% | |

| DnB Bank ASA, 144A, 0.43%*, 4/2/2012 | | | 50,000,000 | | | | 50,000,000 | |

| Westpac Banking Corp., 144A, 0.426%*, 4/11/2012 | | | 282,900,000 | | | | 282,893,007 | |

| | | | | 332,893,007 | |

Total Commercial Paper (Cost $5,458,568,821) | | | | 5,458,568,821 | |

| | |

| Government & Agency Obligations 15.0% | |

| U.S. Government Sponsored Agencies 1.9% | |

| Federal Home Loan Bank: | |

| 0.13%, 1/23/2012 | | | 11,000,000 | | | | 10,999,782 | |

| 0.13%, 2/24/2012 | | | 28,225,000 | | | | 28,224,444 | |

| 0.13%, 5/15/2012 | | | 26,500,000 | | | | 26,494,841 | |

| 0.16%, 4/30/2012 | | | 103,320,000 | | | | 103,309,653 | |

| 0.16%**, 11/13/2012 | | | 24,000,000 | | | | 23,966,187 | |

| 0.23%, 8/24/2012 | | | 15,670,000 | | | | 15,674,189 | |

| 0.27%, 7/6/2012 | | | 20,600,000 | | | | 20,600,105 | |

| Federal Home Loan Mortgage Corp.: | |

| 0.099%**, 2/23/2012 | | | 50,000,000 | | | | 49,992,639 | |

| 0.111%**, 1/11/2012 | | | 25,000,000 | | | | 24,999,167 | |

| Federal National Mortgage Association: | |

| 0.132%**, 1/3/2012 | | | 20,000,000 | | | | 19,999,789 | |

| 0.137%**, 2/17/2012 | | | 11,500,000 | | | | 11,497,898 | |

| 0.148%**, 3/1/2012 | | | 20,000,000 | | | | 19,995,000 | |

| 0.159%**, 10/1/2012 | | | 10,000,000 | | | | 9,987,822 | |

| 0.189%**, 10/1/2012 | | | 17,500,000 | | | | 17,474,693 | |

| | | | | 383,216,209 | |

| U.S. Treasury Obligations 13.1% | |

| U.S. Treasury Bills: | |

| 0.005%**, 1/26/2012 | | | 503,000 | | | | 502,998 | |

| 0.035%**, 5/17/2012 | | | 2,500,000 | | | | 2,499,667 | |

| 0.051%**, 4/19/2012 | | | 921,000 | | | | 920,858 | |

| U.S. Treasury Notes: | |

| 0.375%, 8/31/2012 | | | 212,478,000 | | | | 212,794,495 | |

| 0.375%, 9/30/2012 | | | 18,000,000 | | | | 18,034,370 | |

| 0.375%, 10/31/2012 | | | 360,000,000 | | | | 360,730,389 | |

| 0.625%, 6/30/2012 | | | 84,924,000 | | | | 85,135,391 | |

| 0.625%, 7/31/2012 | | | 433,130,000 | | | | 434,394,582 | |

| 0.75%, 5/31/2012 | | | 212,478,000 | | | | 213,053,545 | |

| 1.375%, 10/15/2012 | | | 212,000,000 | | | | 214,035,648 | |

| 1.5%, 7/15/2012 | | | 480,000,000 | | | | 483,642,949 | |

| 1.875%, 6/15/2012 | | | 250,000,000 | | | | 252,038,171 | |

| 4.75%, 5/31/2012 | | | 98,500,000 | | | | 100,373,472 | |

| 4.875%, 6/30/2012 | | | 342,512,000 | | | | 350,642,757 | |

| | | | | 2,728,799,292 | |

Total Government & Agency Obligations (Cost $3,112,015,501) | | | | 3,112,015,501 | |

| | |

| Short-Term Notes* 14.1% | |

| Australia & New Zealand Banking Group Ltd., 144A, 0.31%, 1/20/2012 | | | 72,000,000 | | | | 72,000,000 | |

| Bank of Nova Scotia: | |

| 0.35%, 4/2/2012 | | | 32,500,000 | | | | 32,500,000 | |

| 0.38%, 3/13/2012 | | | 134,500,000 | | | | 134,500,000 | |

| 0.39%, 6/11/2012 | | | 107,000,000 | | | | 107,000,000 | |

| Bayerische Landesbank, 0.353%, 11/23/2012 | | | 40,000,000 | | | | 40,000,000 | |

| Caisse d'Amortissement de la Dette Sociale, 144A, 0.432%, 5/25/2012 | | | 315,000,000 | | | | 314,986,168 | |

| Canadian Imperial Bank of Commerce, 0.373%, 4/26/2012 | | | 200,000,000 | | | | 200,000,000 | |

| Coca-Cola Co., 0.507%, 5/15/2012 | | | 48,000,000 | | | | 48,027,583 | |

| Commonwealth Bank of Australia: | |

| 144A, 0.376%, 2/3/2012 | | | 135,000,000 | | | | 135,000,000 | |

| 144A, 0.455%, 4/30/2012 | | | 40,000,000 | | | | 40,000,000 | |

| JPMorgan Chase Bank NA, 0.57%, 1/8/2013 | | | 250,000,000 | | | | 250,000,000 | |

| Kells Funding LLC: | |

| 144A, 0.361%, 5/4/2012 | | | 125,000,000 | | | | 125,000,000 | |

| 144A, 0.37%, 2/27/2012 | | | 56,000,000 | | | | 56,000,000 | |

| 144A, 0.377%, 1/9/2012 | | | 64,000,000 | | | | 63,999,885 | |

| 144A, 0.384%, 1/19/2012 | | | 27,000,000 | | | | 27,000,000 | |

| 144A, 0.423%, 2/24/2012 | | | 147,500,000 | | | | 147,500,000 | |

| 144A, 0.468%, 4/16/2012 | | | 150,000,000 | | | | 150,000,000 | |

| Nordea Bank Finland PLC: | |

| 0.681%, 2/3/2012 | | | 35,000,000 | | | | 35,006,457 | |

| 0.737%, 9/13/2012 | | | 20,000,000 | | | | 20,034,002 | |

| 0.941%, 9/13/2012 | | | 50,000,000 | | | | 50,085,207 | |

| Rabobank Nederland NV: | |

| 0.356%, 1/10/2012 | | | 108,250,000 | | | | 108,250,000 | |

| 0.388%, 4/24/2012 | | | 133,000,000 | | | | 133,000,000 | |

| 0.46%, 5/16/2012 | | | 50,000,000 | | | | 50,000,000 | |

| 144A, 0.6%, 12/14/2012 | | | 75,000,000 | | | | 75,000,000 | |

| 144A, 0.668%, 2/29/2012 | | | 50,000,000 | | | | 50,007,960 | |

| Svenska Handelsbanken AB, 144A, 0.577%, 8/7/2012 | | | 80,000,000 | | | | 80,000,000 | |

| Toronto-Dominion Bank, 0.296%, 5/11/2012 | | | 130,500,000 | | | | 130,500,000 | |

| Westpac Banking Corp.: | |

| 0.34%, 1/10/2012 | | | 85,000,000 | | | | 85,000,000 | |

| 0.366%, 5/9/2012 | | | 60,000,000 | | | | 60,000,000 | |

| 0.452%, 2/13/2012 | | | 49,000,000 | | | | 49,000,000 | |

| 144A, 0.965%, 10/23/2012 | | | 61,110,000 | | | | 61,280,869 | |

Total Short-Term Notes (Cost $2,930,678,131) | | | | 2,930,678,131 | |

| | |

| Time Deposits 11.3% | |

| Citibank NA, 0.1%, 1/4/2012 | | | 350,000,000 | | | | 350,000,000 | |

| Nordea Bank Finland PLC, 0.02%, 1/3/2012 | | | 400,000,000 | | | | 400,000,000 | |

| State Street Bank & Trust Co., 0.01%, 1/3/2012 | | | 800,000,000 | | | | 800,000,000 | |

| Svenska Handelsbanken AB, 0.01%, 1/3/2012 | | | 800,000,000 | | | | 800,000,000 | |

Total Time Deposits (Cost $2,350,000,000) | | | | 2,350,000,000 | |

| | |

| Municipal Investments 21.1% | |

| Allegheny County, PA, Industrial Development Authority, UPMC Children's Hospital, Series A, 0.08%***, 10/1/2032, LOC: Bank of America NA | | | 20,460,000 | | | | 20,460,000 | |

| Allegheny County, PA, RBC Municipal Products, Inc. Trust Certificates, Series E-16, 144A, 0.1%***, 4/15/2039, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 22,165,000 | | | | 22,165,000 | |

| Appleton, WI, Redevelopment Authority Revenue, Fox Cities Performing Arts Center, Inc., Series B, 0.1%***, 6/1/2036, LOC: JPMorgan Chase Bank NA | | | 18,400,000 | | | | 18,400,000 | |

| Arizona, State Health Facilities Authority Revenue, Catholic West: | | | | | | | | |

| Series A, 0.08%***, 7/1/2035, LOC: JPMorgan Chase Bank NA | | | 23,100,000 | | | | 23,100,000 | |

| Series B, 0.08%***, 7/1/2035, LOC: JPMorgan Chase Bank NA | | | 17,680,000 | | | | 17,680,000 | |

| Austin, TX, Water & Wastewater Systems Revenue, 0.07%***, 5/15/2031, LOC: Bank of Tokyo-Mitsubishi UFJ, Sumitomo Mitsui Banking | | | 25,920,000 | | | | 25,920,000 | |

| BlackRock Municipal Intermediate Duration Fund, Inc., Series W-7-2871, 144A, AMT, 0.23%***, 3/1/2041, LIQ: JPMorgan Chase Bank NA | | | 30,000,000 | | | | 30,000,000 | |

| BlackRock MuniHoldings New Jersey Quality Fund, Inc., Series W-7-1727, 144A, AMT, 0.3%***, 7/1/2041, LIQ: Bank of America NA | | | 30,000,000 | | | | 30,000,000 | |

| BlackRock MuniHoldings New York Quality Fund, Inc., Series W-7-2436, 144A, AMT, 0.3%***, 7/1/2041, LIQ: Bank of America NA | | | 40,000,000 | | | | 40,000,000 | |

| BlackRock MuniYield California Quality Fund, Inc., Series W-7-1665, 144A, AMT, 0.22%***, 5/1/2041, LIQ: Citibank NA | | | 13,500,000 | | | | 13,500,000 | |

| BlackRock MuniYield Fund, Inc., Series W-7-2514, 144A, AMT, 0.3%***, 7/1/2041, LIQ: Bank of America NA | | | 25,000,000 | | | | 25,000,000 | |

| BlackRock MuniYield New York Quality Fund, Inc., Series W-7-2477, 144A, AMT, 0.22%***, 5/1/2041, LIQ: Citibank NA | | | 26,300,000 | | | | 26,300,000 | |

| BlackRock MuniYield Quality Fund III, Inc., 144A, AMT, 0.24%***, 6/1/2041, LIQ: Citibank NA | | | 44,500,000 | | | | 44,500,000 | |

| BlackRock MuniYield Quality Fund, Inc., Series W-7-1766, 144A, AMT, 0.26%***, 10/1/2041, LIQ: Morgan Stanley Bank | | | 57,000,000 | | | | 57,000,000 | |

| Blount County, TN, Public Building Authority, Local Government Public Improvement, Series E-5-A, 0.12%***, 6/1/2030, LOC: Branch Banking & Trust | | | 45,400,000 | | | | 45,400,000 | |

| Cabell County, WV, University Facilities, Provident Group Marshall Properties, Series A, 0.13%***, 7/1/2039, LOC: Bank of America NA | | | 19,995,000 | | | | 19,995,000 | |

| Calhoun County, TX, Navigation Industrial Development Authority, Formosa Plastics Corp. Project, Series C, 144A, AMT, 0.12%***, 9/1/2031, LOC: Sumitomo Mitsui Banking | | | 10,000,000 | | | | 10,000,000 | |

| Calhoun, TX, Port Authority, Environmental Facilities Revenue, Formosa Plastics Corp. Project, Series B, 144A, AMT, 0.12%***, 9/1/2041, LOC: Sumitomo Mitsui Banking | | | 21,300,000 | | | | 21,300,000 | |

| California, Housing Finance Agency Revenue, Home Mortgage, Series D, 144A, AMT, 0.1%***, 2/1/2040, LOC: Fannie Mae, Freddie Mac | | | 29,130,000 | | | | 29,130,000 | |

| California, RBC Municipal Products, Inc. Trust, Series E-24, 144A, 0.14%**, Mandatory Put 4/2/2012 @ 100, 7/1/2031, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 9,250,000 | | | | 9,250,000 | |

| California, State Kindergarten, Series A5, 0.05%***, 5/1/2034, LOC: Citibank NA & California State Teacher's Retirement System | | | 18,250,000 | | | | 18,250,000 | |

| California, Statewide Communities Development Authority, Multi-Family Housing Revenue, Bay Vista At Meadow Park, Series NN-1, AMT, 0.09%***, 11/15/2037, LIQ: Fannie Mae | | | 29,320,000 | | | | 29,320,000 | |

| California, The Olympic Club Revenue, 0.46%***, 9/30/2032, LOC: Bank of America NA (a) | | | 52,100,000 | | | | 52,100,000 | |

| California, Wells Fargo State Trusts: | | | | | | | | |

| Series 16C, 144A, 0.1%***, 9/1/2029, LIQ: Wells Fargo Bank NA | | | 42,515,000 | | | | 42,515,000 | |

| Series 72C, 144A, 0.1%***, 8/15/2039, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 28,275,000 | | | | 28,275,000 | |

| Series 25C, 144A, 0.1%***, 11/1/2041, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 9,525,000 | | | | 9,525,000 | |

| Channahon, IL, Morris Hospital Revenue, 0.1%***, 12/1/2034, LOC: U.S. Bank NA | | | 5,220,000 | | | | 5,220,000 | |

| Charlotte, NC, Certificates of Participation, Series D, 0.25%***, 6/1/2035, LOC: Bank of America NA (a) | | | 19,600,000 | | | | 19,600,000 | |

| Chattanooga, TN, Industrial Development Board Revenue, BlueCross Corp. Project, 0.22%***, 1/1/2028, LOC: Bank of America NA (a) | | | 99,000,000 | | | | 99,000,000 | |

| Chicago, IL, Midway Airport Revenue, Series A-1, 0.1%***, 1/1/2021, LOC: Bank of Montreal (a) | | | 22,000,000 | | | | 22,000,000 | |

| Clark County, NV, Passenger Facility Charge Revenue, McCarran International Airport, Series F-2, 0.1%***, 7/1/2022, LOC: Union Bank NA | | | 18,000,000 | | | | 18,000,000 | |

| Cleveland, OH, Airport Systems Revenue, Series D, 0.07%***, 1/1/2024, LOC: PNC Bank NA | | | 9,725,000 | | | | 9,725,000 | |

| Cleveland-Cuyahoga County, OH, Port Authority Revenue, Carnegie/89th Garage Project, 0.1%***, 1/1/2037, LOC: JPMorgan Chase Bank | | | 17,730,000 | | | | 17,730,000 | |

| Colorado, Health Facilities Authority Revenue, Fraiser Meadows Community Project, 0.08%***, 6/1/2038, LOC: JPMorgan Chase Bank NA | | | 14,000,000 | | | | 14,000,000 | |

| Colorado, Housing Finance Authority, Single Family Mortgage Revenue: | | | | | | | | |

| "I", Series B-1, 0.15%***, 5/1/2038, LOC: Fannie Mae, Freddie Mac (a) | | | 18,935,000 | | | | 18,935,000 | |

| "I", Series A-2, 0.16%***, 5/1/2038, LOC: Fannie Mae, Freddie Mac (a) | | | 10,185,000 | | | | 10,185,000 | |

| Colorado, Meridian Village Metropolitan, RBC Municipal Products, Inc. Trust, Series C-11, 144A, 0.1%***, 12/1/2031, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 17,580,000 | | | | 17,580,000 | |

| Colorado, RBC Municipal Products, Inc. Trust, Series E-25, 144A, AMT, 0.13%***, 11/15/2025, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 22,000,000 | | | | 22,000,000 | |

| Colorado, State Educational & Cultural Facilities Authority, Linfield Christian School Project, 0.08%***, 5/1/2030, LOC: Evangelical Christian Credit Union | | | 16,000,000 | | | | 16,000,000 | |

| Colorado, Wells Fargo Stage Trust, Series 42C, 144A, AMT, 0.11%***, 11/15/2023, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 9,835,000 | | | | 9,835,000 | |

| Colorado Springs, CO, Utilities Revenue: | |

| Series C, 0.08%***, 11/1/2040, SPA: JPMorgan Chase Bank NA | | | 29,415,000 | | | | 29,415,000 | |

| Series B, 0.1%***, 11/1/2026, SPA: Barclays Bank PLC | | | 11,000,000 | | | | 11,000,000 | |

| Series A, 0.11%***, 11/1/2038, SPA: Bank of America NA | | | 31,645,000 | | | | 31,645,000 | |

| County of Carroll, KY, Environmental Facilities Revenue, Utilities Company Project, Series A, AMT, 0.11%***, 2/1/2032, LOC: Sumitomo Mitsui Banking | | | 27,800,000 | | | | 27,800,000 | |

| Covina, CA, Redevelopment Agency, Multi-Family Housing, ShadowHills Apartments, Inc., Series A, 0.08%***, 12/1/2015, LIQ: Fannie Mae | | | 12,825,000 | | | | 12,825,000 | |

| Eclipse Funding Trust, Solar Eclipse, Springfield, IL Electric Revenue, Series 2006-0007, 144A, 0.09%***, 3/1/2030, LIQ: U.S. Bank NA, LOC: U.S. Bank NA | | | 22,545,000 | | | | 22,545,000 | |

| Florida, Capital Trust Agency Housing Revenue, Atlantic Housing Foundation, Series A, 0.1%***, 7/15/2024, LIQ: Fannie Mae | | | 19,000,000 | | | | 19,000,000 | |

| Florida, Development Finance Corp., Enterprise Board Industrial Development Program, Out of Door Academy, 0.11%***, 7/1/2038, LOC: Northern Trust Co. | | | 12,910,000 | | | | 12,910,000 | |

| Florida, State Board of Public Education, Series 3834Z, 144A, 0.1%***, 12/1/2015, LIQ: JPMorgan Chase Bank NA | | | 9,000,000 | | | | 9,000,000 | |

| Florida, Sunshine State Governmental Financing Commission Revenue, Miami Dade County Program, Series B, 0.08%***, 9/1/2032, LOC: JPMorgan Chase Bank NA | | | 28,500,000 | | | | 28,500,000 | |

| Georgia, Main Street Natural Gas, Inc., Gas Revenue, Series A, 0.09%***, 8/1/2040, SPA: Royal Bank of Canada | | | 84,000,000 | | | | 84,000,000 | |

| Georgia, Private Colleges & Universities Authority Revenue, Mercer University Project, Series A, 0.1%***, 10/1/2036, LOC: Branch Banking & Trust | | | 10,240,000 | | | | 10,240,000 | |

| Hawaii, State Department of Budget & Finance Special Purpose Revenue, Series 2135, 144A, AMT, 0.1%***, 3/1/2037, GTY: Wells Fargo & Co., INS: FGIC, LIQ: Wells Fargo & Co. | | | 19,485,000 | | | | 19,485,000 | |

| Hawaii, Wells Fargo Stage Trust, Series 54C, 144A, 0.11%***, 4/1/2029, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 9,240,000 | | | | 9,240,000 | |

| Hayward, CA, Multi-Family Housing Revenue, Shorewood Bay Waterford Inc., Series A, 0.08%***, 7/15/2014, LIQ: Fannie Mae | | | 20,000,000 | | | | 20,000,000 | |

| Houston, TX, Airport Systems Revenue, 0.09%***, 7/1/2030, LOC: Barclays Bank PLC | | | 8,000,000 | | | | 8,000,000 | |

| Houston, TX, RBC Municipal Products, Inc. Trust Certificates, Utility Systems Revenue, Series E-14, 144A, 0.1%***, 5/15/2034, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 24,070,000 | | | | 24,070,000 | |

| Houston, TX, Utility Systems Revenue, Series D-1, 0.16%***, 5/15/2034, INS: AGMC, LOC: JPMorgan Chase Bank NA (a) | | | 44,000,000 | | | | 44,000,000 | |

| Houston, TX, Water & Sewer Systems Revenue, Series 27TPZ, 144A, 0.09%***, 12/1/2028, INS: AGMC, LIQ: Wells Fargo Bank NA, LOC: Wells Fargo Bank NA | | | 15,865,000 | | | | 15,865,000 | |

| Illinois, Development Finance Authority Revenue, Chicago Symphony Project, 0.08%***, 12/1/2033, LOC: Bank One NA | | | 12,500,000 | | | | 12,500,000 | |

| Illinois, Finance Authority Revenue, Series A, 0.1%***, 11/15/2022, INS: Radian, LOC: JPMorgan Chase Bank NA | | | 12,045,000 | | | | 12,045,000 | |

| Illinois, State Finance Authority Revenue, Methodist Medical Center, Series B, 0.1%***, 11/15/2041, LOC: PNC Bank NA | | | 10,000,000 | | | | 10,000,000 | |

| Illinois, State Toll Highway Authority Revenue, Series A-1A, 0.13%***, 1/1/2031, INS: AGMC, SPA: JPMorgan Chase Bank NA | | | 50,000,000 | | | | 50,000,000 | |

| Illinois, State Toll Highway Authority, Senior Priority, Series A-2A, 0.09%***, 7/1/2030, LOC: Bank of Tokyo-Mitsubishi UFJ | | | 15,000,000 | | | | 15,000,000 | |

| Illinois, Wells Fargo Stage Trust: | | | | | | | | |

| Series 50C, 144A, 0.11%***, 11/15/2035, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 9,110,000 | | | | 9,110,000 | |

| Series 15C, 144A, 0.11%***, 10/1/2040, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 24,405,000 | | | | 24,405,000 | |

| Indiana, State Finance Authority Hospital Revenue, Indiana University Health: | | | | | | | | |

| Series A, 0.06%***, 3/1/2033, LOC: Northern Trust Co. | | | 10,000,000 | | | | 10,000,000 | |

| Series K, 0.09%***, 3/1/2033, LOC: JPMorgan Chase Bank NA (a) | | | 31,700,000 | | | | 31,700,000 | |

| Series J, 0.14%***, 3/1/2033, LOC: JPMorgan Chase Bank NA (a) | | | 15,625,000 | | | | 15,625,000 | |

| Indiana, State Municipal Power Agency, Series A, 0.09%***, 1/1/2018, LOC: Citibank NA | | | 3,800,000 | | | | 3,800,000 | |

| Indiana, Wells Fargo Stage Trust, Series 41C, 144A, 0.11%***, 1/1/2021, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 16,750,000 | | | | 16,750,000 | |

| Iowa, State Finance Authority, Series C, AMT, 0.13%***, 1/1/2036, SPA: State Street Bank & Trust Co. | | | 5,700,000 | | | | 5,700,000 | |

| Iowa, State Finance Authority, Single Family Mortgage, Series C, AMT, 0.12%***, 1/1/2036, SPA: State Street Bank & Trust Co. | | | 8,100,000 | | | | 8,100,000 | |

| Johnson City, TN, Health & Educational Facilities Board Hospital Revenue, Series B3, 0.24%***, 7/1/2033, LOC: Mizuho Corporate Bank (a) | | | 11,400,000 | | | | 11,400,000 | |

| Kansas, State Department of Transportation Highway Revenue, Series C-3, 0.06%***, 9/1/2023, SPA: JPMorgan Chase Bank NA | | | 10,750,000 | | | | 10,750,000 | |

| Kentucky, State Housing Corp. Revenue, Series O, 0.6%***, 1/1/2036, SPA: State Street Bank & Trust Co. (a) | | | 19,160,000 | | | | 19,160,000 | |

| Long Island, NY, Power Authority, Series 3A, 0.28%***, 5/1/2033, LOC: JPMorgan Chase Bank NA & Landesbank Baden-Wurttemberg | | | 15,000,000 | | | | 15,000,000 | |

| Los Angeles County, CA, Multi-Family Housing Authority Revenue, Canyon Country Villas Project, Series H, 0.09%***, 12/1/2032, LIQ: Freddie Mac | | | 8,200,000 | | | | 8,200,000 | |

| Louisiana, Wells Fargo Stage Trust, Series 11C, 144A, 0.11%***, 5/1/2045, LIQ: Wells Fargo Bank NA | | | 17,310,000 | | | | 17,310,000 | |

| Maine, State Housing Authority Mortgage Revenue, Series B-3, AMT, 0.14%***, 11/15/2038, SPA: State Street Bank & Trust Co. | | | 3,310,000 | | | | 3,310,000 | |

| Maine, State Housing Authority, Mortgage Revenue, Series E-2, AMT, 0.12%***, 11/15/2041, SPA: State Street Bank & Trust Co. | | | 8,000,000 | | | | 8,000,000 | |

| Maricopa County, AZ, Industrial Development Authority, Senior Living Facilities Revenue, Christian Care Apartments, Series A, 0.09%***, 9/15/2035, LIQ: Fannie Mae | | | 10,845,000 | | | | 10,845,000 | |

| Massachusetts, State Department of Transportation, Metropolitan Highway Systems Revenue, Contract Assistance, Series A3, 0.09%***, 1/1/2039, LOC: Bank of America NA | | | 38,845,000 | | | | 38,845,000 | |

| Massachusetts, State Development Finance Agency Revenue, Milton Academy, Series B, 0.17%***, 3/1/2039, LOC: TD Bank NA (a) | | | 5,225,000 | | | | 5,225,000 | |

| Massachusetts, State Development Finance Agency Revenue, Wentworth Institute of Technology, 0.1%***, 10/1/2030, LOC: RBS Citizens NA | | | 26,390,000 | | | | 26,390,000 | |

| Massachusetts, State Development Finance Agency Revenue, YMCA of Greater Worcester, 0.08%***, 9/1/2041, LOC: TD Bank NA | | | 11,615,000 | | | | 11,615,000 | |

| Massachusetts, State General Obligation, Series B, 0.25%***, 8/1/2015, SPA: JPMorgan Chase Bank NA | | | 33,000,000 | | | | 33,000,000 | |

| Massachusetts, State Health & Educational Facilities Authority Revenue, Boston University, Series N, 0.16%***, 10/1/2034, LOC: Bank of America NA (a) | | | 13,410,000 | | | | 13,410,000 | |

| Massachusetts, State Water Resources Authority: | |

| Series C-2, 0.08%***, 11/1/2026, SPA: Barclays Bank PLC | | | 20,200,000 | | | | 20,200,000 | |

| Series A-1, 0.08%***, 8/1/2037, SPA: JPMorgan Chase Bank NA | | | 20,000,000 | | | | 20,000,000 | |

| Michigan, Finance Authority, School Loan: | |

| Series B, 0.19%***, 9/1/2050, LOC: PNC Bank NA (a) | | | 25,000,000 | | | | 25,000,000 | |

| Series C, 0.19%***, 9/1/2050, LOC: Bank of Montreal (a) | | | 21,000,000 | | | | 21,000,000 | |

| Michigan, Higher Education Facilities Authority Revenue, Limited Obligation, Hope College, Series B, 0.09%***, 4/1/2032, LOC: PNC Bank NA | | | 17,430,000 | | | | 17,430,000 | |

| Michigan, RBC Municipal Products, Inc. Trust: | | | | | | | | |

| Series L-23, 144A, AMT, 0.13%***, 3/1/2028, INS: AMBAC, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 31,000,000 | | | | 31,000,000 | |

| Series L-25, 144A, AMT, 0.13%***, 9/1/2033, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 66,745,000 | | | | 66,745,000 | |

| Michigan, State Strategic Fund Limited Obligation Revenue, Kroger Co., Recovery Zone Facility, 0.1%***, 1/1/2026, LOC: Bank of Tokyo-Mitsubishi UFJ | | | 9,500,000 | | | | 9,500,000 | |

| Michigan, Wells Fargo Stage Trust, Series 90C, 144A, 0.11%***, 7/1/2035, LIQ: Wells Fargo Bank NA | | | 14,510,000 | | | | 14,510,000 | |

| Minnesota, RBC Municipal Products, Inc. Trust, Series E-19, 144A, 0.17%***, Mandatory Put 4/2/2012 @ 100, 11/15/2047, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 10,000,000 | | | | 10,000,000 | |

| Minnesota, State Housing Finance Agency, Residential Housing Finance, Series C, AMT, 0.12%***, 7/1/2048, LIQ: Federal Home Loan Bank | | | 8,000,000 | | | | 8,000,000 | |

| Minnesota, State Office of Higher Education Revenue, Supplementary Student, Series A, 0.17%***, 12/1/2043, LOC: U.S. Bank NA (a) | | | 11,500,000 | | | | 11,500,000 | |

| Mississippi, State Business Finance Commission, Gulf Opportunity Zone, Chevron U.S.A., Inc. Project, Series C, 0.03%***, 12/1/2030, GTY: Chevron Corp. | | | 8,295,000 | | | | 8,295,000 | |

| Mississippi, State Business Finance Corp., Gulf Opportunity Zone Revenue, Tindall Corp. Project, 0.09%***, 4/1/2028, LOC: Wells Fargo Bank NA | | | 9,005,000 | | | | 9,005,000 | |

| Missouri, State Health & Educational Facilities Authority, Ascension Health, Series C-3, 0.07%***, 11/15/2039 | | | 14,000,000 | | | | 14,000,000 | |

| Missouri, State Health & Educational Facilities Authority, SSM Health Care Corp., Series E, 0.04%***, 6/1/2045, LOC: PNC Bank NA | | | 22,660,000 | | | | 22,660,000 | |

| Monroe County, GA, Development Authority Pollution Control Revenue, Oglethorpe Power Corp., Series B, 0.08%***, 1/1/2036, LOC: JPMorgan Chase Bank NA | | | 27,530,000 | | | | 27,530,000 | |

| Montgomery County, TN, Public Building Authority, Pooled Financing Revenue, Tennessee County Loan Pool, 0.23%***, 11/1/2027, LOC: Bank of America NA | | | 30,790,000 | | | | 30,790,000 | |

| Nashville & Davidson County, TN, Metropolitan Government Health & Educational Facilities Board, Multi-Family Housing, Weatherly Ridge Apartments, Series A, AMT, 0.13%***, 12/1/2041, LOC: U.S. Bank NA | | | 3,000,000 | | | | 3,000,000 | |

| Nevada, Housing Division, Multi-Unit Housing, Apache Project, Series A, AMT, 0.1%***, 10/15/2032, LIQ: Fannie Mae | | | 11,815,000 | | | | 11,815,000 | |

| New Hampshire, State Health & Education Facilities Authority Revenue, Higher Education Loan Corp., Series A, 0.18%***, 12/1/2032, LOC: Royal Bank of Canada (a) | | | 24,401,000 | | | | 24,401,000 | |

| New Jersey, State Health Care Facilities Financing Authority Revenue, Saint Barnabas Health, Series C, 0.09%***, 7/1/2038, LOC: JPMorgan Chase Bank NA (a) | | | 21,495,000 | | | | 21,495,000 | |

| New Mexico, Educational Assistance Foundation, Series A-1, AMT, 0.12%***, 4/1/2034, LOC: Royal Bank of Canada | | | 19,485,000 | | | | 19,485,000 | |

| New Mexico, Wells Fargo Stage Trust, Series 40C, 144A, 0.11%***, 8/1/2039, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 9,265,000 | | | | 9,265,000 | |

| New York, State Dormitory Authority Revenues, Non State Supported Debt, Series 47C, 144A, 0.11%***, 7/1/2050, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 20,595,000 | | | | 20,595,000 | |

| New York, State Dormitory Authority Revenues, Non-State Supported Debt, St. John's University, Series B-2, 0.08%***, 7/1/2037, LOC: Bank of America NA | | | 32,000,000 | | | | 32,000,000 | |

| New York, State Dormitory Authority Revenues, Secondary Issues, Series R-12121, 0.1%***, 4/1/2015, LIQ: Citibank NA | | | 15,830,000 | | | | 15,830,000 | |

| New York, State Energy Research & Development Authority Facilities Revenue, Consolidated Edison Co. of New York, Inc.: | | | | | | | | |

| Series A-2, 144A, 0.06%***, 5/1/2039, LOC: Mizuho Corporate Bank | | | 21,100,000 | | | | 21,100,000 | |

| Series A-1, 144A, 0.07%***, 5/1/2039, LOC: Mizuho Corporate Bank | | | 22,300,000 | | | | 22,300,000 | |

| Series C-3, 144A, AMT, 0.08%***, 11/1/2039, LOC: Mizuho Corporate Bank | | | 27,000,000 | | | | 27,000,000 | |

| Series C-1, 144A, AMT, 0.09%***, 11/1/2039, LOC: Mizuho Corporate Bank | | | 11,200,000 | | | | 11,200,000 | |

| New York, State Housing Finance Agency Revenue, 100 Maiden Lane Properties, Series A, 0.08%***, 5/15/2037, LIQ: Fannie Mae | | | 29,660,000 | | | | 29,660,000 | |

| New York, State Housing Finance Agency Revenue, 88 Leonard Street, Series A, 144A, 1.25%***, 11/1/2037, LOC: Landesbank Hessen-Thuringen (a) | | | 11,750,000 | | | | 11,750,000 | |

| New York, State Housing Finance Agency Revenue, West 38 Street, Series A, AMT, 0.09%***, 5/15/2033, LIQ: Fannie Mae | | | 16,000,000 | | | | 16,000,000 | |

| New York, State Housing Finance Agency, Affordable Housing Revenue, Clinton Park Housing, Series A, 0.1%***, 11/1/2044, LOC: Wells Fargo Bank NA | | | 21,750,000 | | | | 21,750,000 | |

| New York, State Housing Finance Agency, Affordable Housing Revenue, Clinton Park Phase II, Series A-1, 0.09%***, 11/1/2049, LOC: Wells Fargo Bank NA | | | 19,000,000 | | | | 19,000,000 | |

| New York, State Mortgage Agency, Homeowner Revenue, Series 153, AMT, 0.11%***, 4/1/2047, SPA: Barclays Bank PLC | | | 25,000,000 | | | | 25,000,000 | |

| New York City, NY, Municipal Water Finance Authority, Water & Sewer Systems Revenue, Series TR-T30001-I, 144A, 0.3%***, 6/15/2044, LIQ: Citibank NA (a) | | | 8,000,000 | | | | 8,000,000 | |

| North Carolina, Capital Facilities Finance Agency, Educational Facilities Revenue, Forsyth Country Day School, 0.12%***, 12/1/2031, LOC: Branch Banking & Trust | | | 12,190,000 | | | | 12,190,000 | |

| North Carolina, State Capital Facilities Finance Agency Revenue, ELON University, 0.11%***, 1/1/2035, LOC: Bank of America NA | | | 19,935,000 | | | | 19,935,000 | |

| Nuveen Arizona Premium Income Municipal Fund, Inc., Series T30017-I, 144A, 0.3%***, 8/1/2014, LIQ: Citibank NA (a) | | | 27,900,000 | | | | 27,900,000 | |

| Nuveen Dividend Advantage Municipal Fund, Series T30016-I, 144A, 0.3%***, 8/1/2014, LIQ: Citibank NA (a) | | | 70,300,000 | | | | 70,300,000 | |

| Nuveen Select Quality Municipal Fund, Inc., Series 1-2525, 144A, AMT, 0.25%***, 5/1/2041, LIQ: Barclays Bank PLC | | | 40,000,000 | | | | 40,000,000 | |

| Ohio, Housing Finance Agency, Residential Mortgage-Backed Revenue, Series F, AMT, 0.15%***, 3/1/2037, SPA: Citibank NA | | | 31,930,000 | | | | 31,930,000 | |

| Ohio, State Housing Finance Agency, Residental Mortgage Revenue, Series M, AMT, 0.15%***, 9/1/2036, SPA: Citibank NA | | | 32,000,000 | | | | 32,000,000 | |

| Ohio, State Housing Finance Agency, Residential Mortgage Revenue, Mortgage-Backed Securities Program, Series N, AMT, 0.15%***, 9/1/2036, SPA: State Street Bank & Trust Co. | | | 68,405,000 | | | | 68,405,000 | |

| Oklahoma, State Turnpike Authority Revenue, Series B, 0.08%***, 1/1/2028, SPA: Royal Bank of Canada | | | 20,330,000 | | | | 20,330,000 | |

| Orlando & Orange County, FL, Expressway Authority, Series C-1, 0.1%***, 7/1/2025, INS: AGMC, LOC: JPMorgan Chase Bank NA | | | 26,000,000 | | | | 26,000,000 | |

| Palm Beach County, FL, Solid Waste Authority Revenue, 1.0%, Mandatory Put 1/12/2012 @ 100, 10/1/2031 | | | 100,000,000 | | | | 100,017,369 | |

| Philadelphia, PA, Authority for Industrial Development, Series B-3, 0.07%***, 10/1/2030, LOC: PNC Bank NA | | | 10,655,000 | | | | 10,655,000 | |

| Philadelphia, PA, Gas Works Revenue, Series D, 0.07%***, 8/1/2031, LOC: Bank of America NA | | | 25,000,000 | | | | 25,000,000 | |

| Raleigh Durham, NC, Airport Authority Revenue, Series C, 0.1%***, 5/1/2036, LOC: U.S. Bank NA | | | 10,595,000 | | | | 10,595,000 | |

| Salem, OR, Hospital Facility Authority Revenue, Salem Hospital Project, Series C, 0.12%***, 8/15/2036, LOC: Bank of America NA | | | 12,500,000 | | | | 12,500,000 | |

| San Jose, CA, Financing Authority, Series E2, 0.16%***, 6/1/2025, LOC: U.S. Bank NA (a) | | | 12,455,000 | | | | 12,455,000 | |

| San Jose, CA, Financing Authority Lease Revenue, Hayes Mansion, Series D, 0.17%***, 6/1/2025, LOC: U.S. Bank NA (a) | | | 40,985,000 | | | | 40,985,000 | |

| San Jose, CA, Financing Authority Lease Revenue, Ice Center, Series E1, 0.2%***, 6/1/2025, LOC: Bank of America NA (a) | | | 12,460,000 | | | | 12,460,000 | |

| South Carolina, State Jobs-Economic Development Authority, Economic Development Revenue, Bon Secours Health Systems, 0.1%***, 11/1/2042, INS: AGMC, LOC: JPMorgan Chase Bank NA | | | 17,500,000 | | | | 17,500,000 | |

| Southern California, Metropolitan Water District, State Authorization, Series B, 0.07%***, 7/1/2028, SPA: Landesbank Hessen-Thuringen | | | 16,600,000 | | | | 16,600,000 | |

| St. James Parish, LA, Nustar Logistics, Series A, 0.09%***, 10/1/2040, LOC: JPMorgan Chase Bank NA | | | 12,500,000 | | | | 12,500,000 | |

| Stafford County, VA, Industrial Development Authority Revenue, Series B-1, 0.15%***, 8/1/2028, LOC: Bank of America NA | | | 21,505,000 | | | | 21,505,000 | |

| Sweetwater County, WY, Pollution Control Revenue, PacifiCorp Project, Series A, 144A, 0.09%***, 7/1/2015, LOC: Barclays Bank PLC | | | 12,550,000 | | | | 12,550,000 | |

| Texas, Alliance Airport Authority, Inc., Special Facilities Revenue, Series 2088, 144A, AMT, 0.1%***, 4/1/2021, GTY: Wells Fargo & Co., LIQ: Wells Fargo & Co. | | | 24,570,000 | | | | 24,570,000 | |

| Texas, Capital Area Housing Finance Corp., Cypress Creek at River Apartments, AMT, 0.13%***, 10/1/2039, LOC: Citibank NA | | | 10,895,000 | | | | 10,895,000 | |

| Texas, Lower Neches Valley Authority, Industrial Development Corp., Series B-2, AMT, 0.03%***, 12/1/2039, GTY: Exxon Mobil Corp. | | | 7,880,000 | | | | 7,880,000 | |

| Texas, RBC Municipal Products, Inc. Trust, Series E-27, 144A, 0.1%***, 6/1/2027, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 10,000,000 | | | | 10,000,000 | |

| Texas, State General Obligation: | |

| Series E, 0.14%***, 12/1/2026, SPA: JPMorgan Chase Bank NA (a) | | | 19,000,000 | | | | 19,000,000 | |

| Series E, 0.15%***, 6/1/2032, LOC: Sumitomo Mitsui Banking (a) | | | 24,435,000 | | | | 24,435,000 | |

| Texas, State Higher Education Authority, Series L-46, 144A, AMT, 0.13%***, 12/1/2034, LIQ: Royal Bank of Canada, LOC: Royal Bank of Canada | | | 52,995,000 | | | | 52,995,000 | |

| Texas, State Veterans Housing Assistance Fund II: | |

| Series C, 0.14%***, 6/1/2031, SPA: JPMorgan Chase & Co. (a) | | | 11,255,000 | | | | 11,255,000 | |

| Series A, 144A, AMT, 0.14%***, 6/1/2034, SPA: Landesbank Hessen-Thuringen | | | 18,395,000 | | | | 18,395,000 | |

| Texas, Tax & Revenue Anticipation Notes: | |

| Series 3945, 144A, 0.07%***, 8/30/2012, LIQ: JPMorgan Chase & Co. | | | 95,000,000 | | | | 95,000,000 | |

| Series 3946, 144A, 0.07%***, 8/30/2012, LIQ: JPMorgan Chase & Co. | | | 90,975,000 | | | | 90,975,000 | |

| Series 3953, 144A, 0.07%***, 8/30/2012, LIQ: JPMorgan Chase & Co. | | | 166,075,000 | | | | 166,075,000 | |

| Series 3964, 144A, 0.07%***, 8/30/2012, LIQ: JPMorgan Chase & Co. | | | 195,000,000 | | | | 195,000,000 | |

| Texas, University of Houston Revenues, Consolidated Systems, 0.08%***, 2/15/2024 | | | 8,860,000 | | | | 8,860,000 | |

| Texas, Wells Fargo Stage Trust, Series 20C, 144A, AMT, 0.11%***, 5/1/2038, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 16,120,000 | | | | 16,120,000 | |

| Travis County, TX, Health Facilities Development Corp., Retirement Facilities Revenue, Longhorn Village Project, Series B, 0.1%***, 7/1/2037, LOC: Bank of Scotland | | | 20,430,000 | | | | 20,430,000 | |

| Troy, NY, Capital Resource Corp. Revenue, Series 4C, 144A, 0.11%***, 9/1/2040, LIQ: Wells Fargo Bank NA | | | 18,715,000 | | | | 18,715,000 | |

| Tulsa, OK, Airports Improvement Trust, Special Facility Revenue, Bizjet International Sales & Support, Inc., 144A, AMT, 0.14%***, 8/1/2018, LOC: Landesbank Hessen-Thuringen | | | 10,120,000 | | | | 10,120,000 | |

| Union County, NC, Enterprise Systems Revenue, 0.07%***, 6/1/2034, LOC: Bank of America NA | | | 13,700,000 | | | | 13,700,000 | |

| University of California Revenue, Series R-12236, 0.07%***, 10/1/2015, INS: AGMC, FGIC, LIQ: Citibank NA | | | 15,000,000 | | | | 15,000,000 | |

| University of New Mexico, Systems Improvement Revenues, 0.1%***, 6/1/2026, SPA: JPMorgan Chase Bank NA | | | 33,625,000 | | | | 33,625,000 | |

| Vermont, State Educational & Health Buildings Financing Agency Revenue, Fletcher Allen Health Care, Series A, 0.08%***, 12/1/2030, LOC: TD BankNorth NA | | | 7,070,000 | | | | 7,070,000 | |

| Volusia County, FL, Housing Finance Authority, Multi-Family Housing Revenue, Cape Morris Cove Apartments, Series A, AMT, 0.12%***, 10/15/2042, LOC: JPMorgan Chase Bank NA | | | 6,140,000 | | | | 6,140,000 | |

| Washington, State Economic Development Finance Authority, Solid Waste Disposal Revenue, Waste Management, Inc. Project, Series D, AMT, 0.15%***, 7/1/2030, LOC: JPMorgan Chase Bank NA | | | 20,000,000 | | | | 20,000,000 | |

| Washington, State Health Care Facilities Authority, Swedish Health Services: | | | | | | | | |

| Series B, 0.09%***, 11/15/2046, LOC: Citibank NA | | | 13,000,000 | | | | 13,000,000 | |

| Series C, 0.09%***, 11/15/2046, LOC: Citibank NA | | | 14,000,000 | | | | 14,000,000 | |

| Washington, State Housing Finance Commission, Rolling Hills Apartments Project, Series A, 144A, AMT, 0.13%***, 6/15/2037, LIQ: Fannie Mae | | | 6,125,000 | | | | 6,125,000 | |

| Washington, Wells Fargo Stage Trust, Series 21C, 144A, 0.11%***, 12/1/2037, GTY: Wells Fargo Bank NA, LIQ: Wells Fargo Bank NA | | | 10,360,000 | | | | 10,360,000 | |

| Wayne County, MI, Airport Authority Revenue, Detroit Metropolitan Airport: | | | | | | | | |

| Series E2, AMT, 0.1%***, 12/1/2028, LOC: PNC Bank NA | | | 16,000,000 | | | | 16,000,000 | |

| Series E1, AMT, 0.11%***, 12/1/2028, LOC: JPMorgan Chase Bank NA | | | 25,000,000 | | | | 25,000,000 | |

| Wisconsin, Housing & Economic Development Authority, Home Ownership Revenue, Series B, 0.15%***, 3/1/2033, LOC: Fannie Mae, Freddie Mac (a) | | | 13,905,000 | | | | 13,905,000 | |

| Wisconsin, State Health & Educational Facilities Authority Revenue, Mercy Alliance, Inc., 0.06%***, 6/1/2039, LOC: U.S. Bank NA | | | 23,000,000 | | | | 23,000,000 | |

| Wisconsin, State Health & Educational Facilities Authority Revenue, Oakwood Village Apartments, Inc., 0.06%***, 8/15/2028, LOC: BMO Harris Bank NA | | | 9,095,000 | | | | 9,095,000 | |

| Woodstock, IL, Multi-Family Housing Revenue, Willow Brooke Apartments, AMT, 0.12%***, 4/1/2042, LOC: Wells Fargo Bank NA | | | 24,600,000 | | | | 24,600,000 | |

| Wyoming, Student Loan Corp. Revenue, Series A-3, 0.08%***, 12/1/2043, LOC: Royal Bank of Canada | | | 40,000,000 | | | | 40,000,000 | |

Total Municipal Investments (Cost $4,389,093,369) | | | | 4,389,093,369 | |

| | |

| Repurchase Agreements 0.5% | |

| JPMorgan Securities, Inc., 0.16%, dated 12/30/2011, to be repurchased at $100,001,778 on 1/3/2012 (b) (Cost $100,000,000) | | | 100,000,000 | | | | 100,000,000 | |

| | | % of Net Assets | | | Value ($) | |

| | | | |

Total Investment Portfolio ($19,901,627,274)+ | | | 95.8 | | | | 19,901,627,274 | |

| Other Assets and Liabilities, Net | | | 4.2 | | | | 882,549,401 | |

| Net Assets | | | 100.0 | | | | 20,784,176,675 | |

* Floating rate securities' yields vary with a designated market index or market rate, such as the coupon-equivalent of the U.S. Treasury Bill rate. These securities are shown at their current rate as of December 31, 2011.

** Annualized yield at time of purchase; not a coupon rate.

*** Variable rate demand notes and variable rate demand preferred shares are securities whose interest rates are reset periodically at market levels. These securities are payable on demand and are shown at their current rates as of December 31, 2011.

+ The cost for federal income tax purposes was $19,901,627,274.

(a) Taxable issue.

(b) Collateralized by:

| Principal Amount ($) | | Security | | Rate (%) | | Maturity Date | | Collateral Value ($) | |

| | 50,870,000 | | Federated Republic of Brazil | | | 8.875-12.75 | | 1/15/2020- 4/15/2024 | | | 84,676,763 | |

| | 20,000,000 | | Republic of South Africa | | | 7.375 | | 4/25/2012 | | | 20,325,000 | |

| Total Collateral Value | | | 105,001,763 | |

144A: Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

AGMC: Assured Guaranty Municipal Corp.

AMBAC: Ambac Financial Group, Inc.