| 2013 | PROVINCE OF NEW BRUNSWICK | iii |

| | | |

TABLE OF CONTENTS

Audited Consolidated Financial Statements

| Introduction to Volume I | 1 |

| Statement of Responsibility | 2 |

| Results for the Year | 3 |

| Major Variance Analysis | 7 |

| Indicators of Financial Health | 14 |

| Independent Auditor's Report | 21 |

| Consolidated Statement of Financial Position | 23 |

| Consolidated Statement of Operations | 24 |

| Consolidated Statement of Cash Flow | 25 |

| Consolidated Statement of Change in Net Debt | 26 |

| Consolidated Statement of Change in Accumulated Deficit | 26 |

| Notes to the Consolidated Financial Statements | 27 |

| Schedules to the Consolidated Financial Statements | 67 |

| 2013 | PROVINCE OF NEW BRUNSWICK | 1 |

| | | |

INTRODUCTION

VOLUME I

The Public Accounts of the Province of New Brunswick are presented in two volumes.

This volume contains the audited consolidated financial statements of the Provincial Reporting Entity as described in Note 1 to the consolidated financial statements. They include a Consolidated Statement of Financial Position, a Consolidated Statement of Operations, a Consolidated Statement of Cash Flow, a Consolidated Statement of Change in Net Debt and a Consolidated Statement of Change in Accumulated Deficit. This volume also contains the Independent Auditor’s Report, Statement of Responsibility, management’s comments on the Results for the Year, Major Variance Analysis and a discussion of the Indicators of Financial Health of the Province.

Volume II contains unaudited supplementary information to the consolidated financial statements presented in Volume I. It presents summary statements for revenue and expenditure as well as five-year comparative statements. This volume also contains detailed information on Supplementary Appropriations, Funded Debt, statements of the General Sinking Fund and revenue and expenditure by government department.

In addition, the Government includes the following lists on the Office of the Comptroller web site at http://www.gnb.ca/0087 :

| • | Salary information of government employees and employees of certain government organizations in excess of $60,000. Salary information is for the calendar year and is reported under the department where the employee worked at 31 December; |

| • | Travel and other employee expenses in excess of $12,000 paid during the year to government employees, separated by department; |

| • | Payments made to suppliers during the year in excess of $25,000 separated by department as well as a global listing including payments made by all departments; |

| • | Loans disbursed to recipients during the year in excess of $25,000 separated by department. |

| 2013 | PROVINCE OF NEW BRUNSWICK | 3 |

| | | |

RESULTS FOR THE YEAR

General Comments

The Province's summary financial statements, contained in this volume of Public Accounts, report a deficit for the fiscal year ended 31 March 2013 of $507.7 million. This represents an increase of $324.8 million from the budgeted deficit of $182.9 million. The difference is the result of lower than budgeted revenues of $269.5 million and higher than budgeted expenses of $55.3 million.

Revenues were lower due to a $148.8 million shortfall in tax revenues attributable to a weakened economy, a reduction of $67.2 million in income from Government Business Enterprises primarily related to weaker-than-projected results for NB Power, and reduced royalty revenue of $35.6 million, reflecting lower world prices and volumes.

Expenses were $55.3 million higher than budget overall. A decrease in departmental spending throughout government contributed to lower than budgeted expenses in a number of areas, including Health, Social Development and Labour and Employment. These decreases were offset by higher than budgeted expenses elsewhere, including Education and Training and Central Government mainly due to higher than budgeted pension expense.

There are several other variances discussed in more detail in the major variance section that follows.

Summary Financial Information

(millions)

Consolidated Statement of Financial Position

| | | 2013 | | 2012 | | |

| | | | | | | |

| Financial Assets | $ | 7,690.7 | $ | 7,264.7 | | |

| | | | | | | |

| Liabilities | | (18,744.7) | | (17,386.9) | | |

| | | | | | | |

| Net Debt | | (11,054.0) | | (10,122.2) | | |

| | | | | | | |

| Tangible Capital Assets | | 7,977.6 | | 7,452.5 | | |

| | | | | | | |

| Other Non Financial Assets | | 280.5 | | 256.7 | | |

| | | | | | | |

| Total Non Financial Assets | | 8,258.1 | | 7,709.2 | | |

| | | | | | | |

| Accumulated Deficit | $ | (2,795.9) | $ | (2,413.0) | | |

| | | | | | |

| | | | | | | |

| Consolidated Statement of Operations | | | |

| | | | | | | |

| | | 2013 | | 2012 | | |

| | | | | | | |

| Revenue – Provincial Sources | $ | 4,781.2 | $ | 4,931.7 | | |

| | | | | | | |

| Revenue – Federal Sources | | 3,000.5 | | 2,874.2 | | |

| | | | | | | |

| Total Revenue | | 7,781.7 | | 7,805.9 | | |

| | | | | | | |

| Expenses | | 8,289.4 | | 8,051.2 | | |

| | | | | | | |

| Surplus / (Deficit) | $ | (507.7) | $ | (245.3) | | |

| | | | | |

| | | | | | | |

| Consolidated Statement of Change in Net Debt | | |

| | | | | | | |

| | | 2013 | | 2012 | | |

| | | | | | | |

| Opening Net Debt | $ | (10,122.2) | $ | (9,697.5) | | |

| | | | | | | |

| Increase in Net Debt From | | (931.8) | | (424.7) | | |

| Operations | | | | |

| | | | | | |

| | | | | | | |

| Ending Net Debt | $ | (11,054.0) | $ | (10,122.2) | | |

| | | | | | | |

| 2013 | PROVINCE OF NEW BRUNSWICK | 4 |

| | | |

Revenue

Revenues of the Province for the past ten years, as restated, are shown in the table below.

(millions)

| | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Provincial Sources | $3,594.1 | $3,688.6 | $3,994.2 | $4,225.4 | $4,469.7 | $4,467.4 | $4,179.7 | $4,612.5 | $ 4,931.7 | $ 4,781.2 |

| Federal Sources | $1,917.9 | $2,354.8 | $2,392.9 | $2,530.9 | $2,720.6 | $2,763.6 | $2,940.8 | $2,930.3 | $ 2,874.2 | $ 3,000.5 |

| Total Revenue | $5,512.0 | $6,043.4 | $6,387.1 | $6,756.3 | $7,190.3 | $7,230.9 | $7,120.5 | $7,542.8 | $ 7,805.9 | $ 7,781.7 |

Average annual revenue growth over the ten-year period is 4.0%. Over the last five years, revenue growth is notably lower than the first five years of this period, reflecting the slowdown in the economy, tax changes and other factors. In 2013, year-over-year revenue shrank by 0.3% or $24.2 million. Key contributing factors to this weakened revenue growth include a reduction in income from Government Business Enterprises totaling $127.5 million reflecting considerably lower net income for NB Power and a reduction in tax revenues related to a weakened economy, which served to offset increased federal revenue that reflected one-time funding related to the Route One Gateway Project.

Expense

Expenses of the Province for the past ten years, as restated, are shown in the table below.

(millions)

| | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Total Expense | $5,708.7 | $5,822.9 | $6,160.8 | $6,481.1 | $6,950.0 | $7,383.6 | $7,816.3 | $8,160.5 | $ 8,051.2 | $ 8,289.4 |

Average annual expense growth over the ten-year period is 4.3%. In 2013, expenses increased by $238.2 million year-over-year, a 3.0% increase. This was mainly due to increased program spending in Health, Social Development, and Education and Training, as well as increased pension expense. These increases were partially offset by decreased provision for losses expense.

Surplus / (Deficit)

Surpluses (or Deficits) of the Province for the past ten years, as restated, are shown in the table below.

(millions)

| | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Surplus/(Deficit) | $ (196.7) | $ 220.5 | $ 226.3 | $ 275.2 | $ 240.3 | $ (152.7) | $ (695.8) | $ (617.7) | $ (245.3) | $ (507.7) |

The deficit for the year ended 31 March 2013 was $507.7 million. The deficit was higher than the budgeted deficit of $182.9 million. The increase in the deficit was the result of a revenue shortfall from budget of $269.5 million – fueled by weakened tax and royalty revenue and lower results for NB Power – along with higher-than-budgeted expenses of $55.3 million.

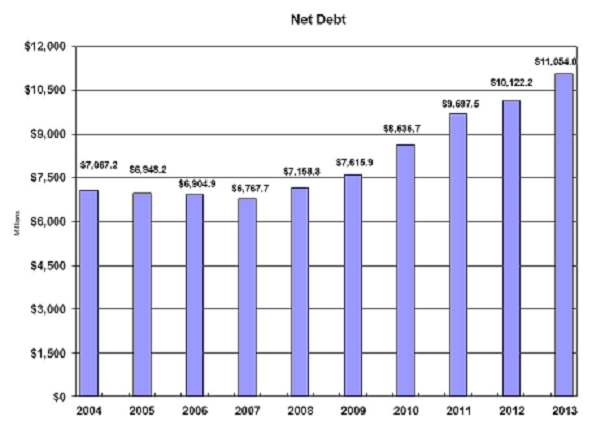

Net Debt

Net debt increased by $931.8 million during the year ended 31 March 2013. The increase in net debt is mainly related to the deficit of $507.7 million and $525.1 million for net capital asset transactions of highways, hospitals, schools and other buildings. In 2013, the Route One Gateway Project was added to the provincial debt. The following graph illustrates the net debt position as restated at the end of each of the past ten years.

| 2013 | PROVINCE OF NEW BRUNSWICK | 5 |

| | | |

(millions)

| | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Net Debt | $7,067.2 | $6,948.2 | $6,904.9 | $6,767.7 | $7,158.8 | $7,615.9 | $8,636.7 | $9,697.5 | $10,122.2 | $11,054.0 |

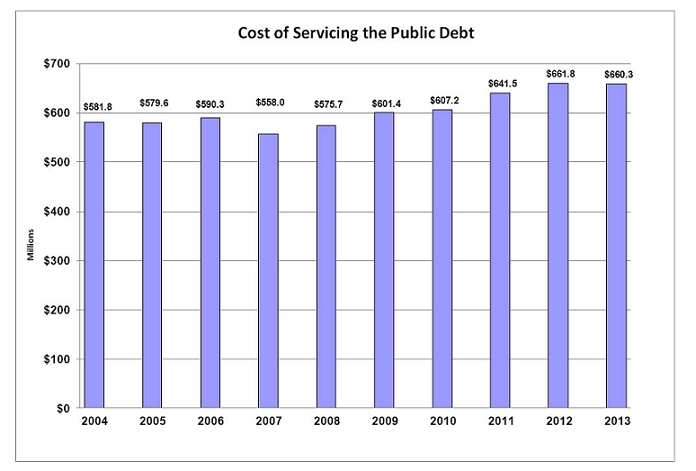

Cost of Servicing the Public Debt

The Province’s cost of servicing the Public Debt totaled $660.3 million for the year ended 31 March 2013. This represents a modest reduction of $1.5 million from 2012 due to timing differences in borrowing and financing maturing debt at lower interest rates and borrowing later in fiscal year than anticipated, which was partially offset by higher debt levels.

| 2013 | PROVINCE OF NEW BRUNSWICK | 6 |

| | | |

(millions)

| | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Cost of | | | | | | | | | | |

| Servicing the | $ 581.8 | $ 579.6 | $ 590.3 | $ 558.0 | $ 575.7 | $ 601.4 | $ 607.2 | $ 641.5 | $ 661.8 | $ 660.3 |

| Public Debt | | | | | | | | | | |

Results According to the Fiscal Responsibility and Balanced Budget Act

The Act’s stated objective is for balanced budgets over designated fiscal periods. The current fiscal period commenced 1 April 2011 and ends 31 March 2015. For 2013, the government incurred a $507.7 million deficit for a cumulative deficit of $768.3 million for balanced budget purposes. The government will introduce new legislation for balanced budgets during its mandate.

Surplus / (Deficit) According to Fiscal Responsibility and Balanced Budget Act

2011-12 to 2014-15

(millions)

| | | 2012 | | 2013 | Cumulative |

| Surplus/(Deficit) - FRBBA | $ | (260.6) | $ | (507.7) | $ | (768.3) |

| 2013 | PROVINCE OF NEW BRUNSWICK | 7 |

| | | |

MAJOR VARIANCE ANALYSIS

Explanations of major variances are described below, first for revenue, followed by expenses. In this analysis, comparisons are made between the actual results for 2013 and either the 2013 budget or actual results for 2012.

REVENUE

Budget 2013 to Actual 2013 Comparison

| 2013 Budget to Actual | | | |

| | ($ millions) | | | |

| | | | | | |

| Item | Budget | Actual | Variance | % Variance | |

| | | | | | |

| Provincial Sources | | | | | |

| | | | | |

| Taxes | 3,690.9 | 3,542.1 | (148.8) | (4.0) | |

| | | | | | |

| Licenses and Permits | 144.2 | 144.6 | 0.4 | 0.3 | |

| | | | | | |

| Royalties | 121.7 | 86.1 | (35.6) | (29.3) | |

| | | | | | |

| Income from Government Business Enterprises | 256.9 | 189.7 | (67.2) | (26.2) | |

| | | | | | |

| Other Provincial Revenue | 589.8 | 598.0 | 8.2 | 1.4 | |

| | | | | | |

| Sinking Fund Earnings | 221.0 | 220.7 | (0.3) | (0.1) | |

| | | | | | |

| Revenue from Provincial Sources | 5,024.5 | 4,781.2 | (243.3) | (4.8) | |

| | | | | | |

| Federal Sources | | | | | |

| | | | | |

| Fiscal Equalization | 1,597.7 | 1,597.7 | 0.0 | 0.0 | |

| | | | | | |

| Unconditional Grants | 901.9 | 894.2 | (7.7) | (0.9) | |

| | | | | | |

| Conditional Grants | 527.1 | 508.6 | (18.5) | (3.5) | |

| | | | | | |

| Revenue from Federal Sources | 3,026.7 | 3,000.5 | (26.2) | (0.9) | |

| | | | | |

| Total Revenues | 8,051.2 | 7,781.7 | (269.5) | (3.3) | |

| | | | | |

Taxes

Taxes are down $148.8 million from budget, primarily due to:

| · | Personal Income Tax is down $120.3 million due to a weakened tax base and a negative prior-year adjustment for the 2011 taxation year; |

| · | Metallic Minerals Tax revenue is down $27.7 million as a result of lower than anticipated world prices and production volumes; |

| · | Provincial Real Property Tax is down $15.4 million due to lower than anticipated growth in and adjustments to assessments; |

| · | Corporate Income Tax is down $14.3 million as a result of final determination of taxes for the 2011 taxation year which resulted in a negative prior-year adjustment; Tobacco Tax revenue fell $7.6 million due to lower than anticipated tobacco sales volumes; |

| · | Gasoline and Motive Fuel Tax revenue were down $6.2 million related to lower than anticipated gasoline volumes; |

| · | Harmonized Sales Tax is up $34.2 million mainly as a result of positive adjustments related to prior years. |

Royalties

Royalties fell $35.6 million from budget primarily due to a reduction of $32.2 million in mine royalties. Weakened prices for potash, a potash mine shutdown during the year and a new royalty structure for potash not being in place as anticipated resulted in the shortfall.

| 2013 | PROVINCE OF NEW BRUNSWICK | 8 |

| | | |

Income from Government Business Enterprises

Income from Government Business Enterprises is down $67.2 million from budget due to lower net income of $60.2 million for the New Brunswick Electric Finance Corporation due to weaker-than-anticipated results for NB Power. This is a result of higher costs for pensions, fuel, and purchased power. New Brunswick Liquor Corporation revenue is down $8.3 million related to lower than anticipated sales.

Conditional Grants

Conditional Grants are down $18.5 million from budget mainly due to lower than anticipated demand for federal provincial cost shared training.

Actual 2012 to Actual 2013 Comparison

2012 Actual to 2013 Actual

($ millions)

| Item | 2012 | 2013 | | % |

| | Actual | Actual | Change | Change |

| | | | | |

| Provincial Sources | | | | |

| | | | | |

| Taxes | 3,574.4 | 3,542.1 | (32.3) | (0.9) |

| | | | | |

| Licenses and Permits | 138.8 | 144.6 | 5.8 | 4.2 |

| | | | | |

| Royalties | 89.3 | 86.1 | (3.2) | (3.6) |

| | | | | |

| Income from Government Business Enterprises | 317.2 | 189.7 | (127.5) | (40.2) |

| | | | | |

| Other Provincial Revenue | 586.4 | 598.0 | 11.6 | 2.0 |

| | | | | |

| Sinking Fund Earnings | 225.6 | 220.7 | (4.9) | (2.2) |

| | | | | |

| Revenue from Provincial Sources | 4,931.7 | 4,781.2 | (150.5) | (3.1) |

| | | | | |

| Federal Sources | | | | |

| | | | | |

| Fiscal Equalization Payments | 1,632.6 | 1,597.7 | (34.9) | (2.1) |

| | | | | |

| Unconditional Grants | 865.7 | 894.2 | 28.5 | 3.3 |

| | | | | |

| Conditional Grants | 375.9 | 508.6 | 132.7 | 35.3 |

| | | | | |

| Revenue from Federal Sources | 2,874.2 | 3,000.5 | 126.3 | 4.4 |

| | | | | |

| Total Revenues | 7,805.9 | 7,781.7 | (24.2) | (0.3) |

| | | | | |

Taxes

Taxes are down $32.3 million over the previous year, mainly due to:

| · | Personal Income Tax was down by $38.0 million due to a negative prior-year adjustment in 2012-2013 and a weakened tax base. |

| · | Metallic Minerals Tax declined by $29.9 million related to lower world prices and production volumes. |

| · | Corporate Income Tax fell by $19.7 million as a result of a negative prior-year adjustment affecting 2012-2013. |

| · | Offsetting factors include: |

| o | Harmonized Sales Tax was up by $41.6 million due to federal payments based on the HST allocation formula. |

| o | Provincial Real Property Tax increased by $9.4 million related to growth in the assessment base. |

| o | Financial Corporation Capital Tax grew by $8.1 million reflecting a rate increase announced in the 2012-2013 Budget. |

Income From Government Business Enterprises

Income from Government Business Enterprises is down $127.5 million from the previous year attributable to a reduction in NBEFC net income of $127.2 million, reflective of weaker results for NB Power as a result of lower hydro flows and higher generating costs.

| 2013 | PROVINCE OF NEW BRUNSWICK | 9 |

| | | |

Fiscal Equalization Payments

Fiscal Equalization Payments are down $34.9 million reflecting a narrowing of fiscal disparities between New Brunswick and the national average.

Unconditional Grants

Unconditional Grants are up $28.5 million mainly due to the legislated growth in the federal cash funding for the Canada Health Transfer and the Canada Social Transfer.

Conditional Grants

Conditional Grants are up $132.7 million from the previous year mainly due to one-time capital revenue related to Route One Gateway Project.

EXPENSES

Budget 2013 to Actual 2013 Comparison

2013 Budget to Actual

($ millions)

| Item | Budget | Actual | Variance | % Variance |

| | | | | |

| Education and Training | 1,761.2 | 1,787.6 | 26.4 | 1.5 |

| | | | | |

| Health | 2,814.4 | 2,785.9 | (28.5) | (1.0) |

| | | | | |

| Social Development | 1,091.9 | 1,055.6 | (36.3) | (3.3) |

| | | | | |

| Protection Services | 239.4 | 237.3 | (2.1) | (0.9) |

| | | | | |

| Economic Development | 276.2 | 270.6 | (5.6) | (2.0) |

| | | | | |

| Labour and Employment | 128.3 | 100.5 | (27.8) | (21.7) |

| | | | | |

| Resources | 215.0 | 210.1 | (4.9) | (2.3) |

| | | | | |

| Transportation and Infrastructure | 531.5 | 547.7 | 16.2 | 3.0 |

| | | | | |

| Central Government | 504.2 | 633.8 | 129.6 | 25.7 |

| | | | | |

| Service of the Public Debt | 672.0 | 660.3 | (11.7) | (1.7) |

| | | | | |

| Total Expenses | 8,234.1 | 8,289.4 | 55.3 | 0.7 |

| | | | | |

Items in the table are reported by functional area. See the related schedule in the consolidated financial statements for additional details.

Education and Training

Education and Training expenses were $26.4 million higher than budget. This was mainly due to higher than budgeted pension expense. This was partially offset by a number of under-expenditures, including the following:

| · | Lower than budgeted expenses in the Elementary and Secondary Education and Early Childhood Development programs of the Department of Education and Early Childhood Development; |

| · | Lower than budgeted expenses under the Student Financial Assistance Program in the Department of Post-Secondary Education, Training and Labour due to lower interest costs and lower take-up in student debt reduction programs; |

| · | Lower than budgeted provision for losses expense. |

| 2013 | PROVINCE OF NEW BRUNSWICK | 10 |

| | | |

Health

Health expenses were $28.5 million lower than budget mainly due to the following:

| · | Lower than budgeted expenditures under the Corporate and Other Health Services program due to a number of factors, including IT-related expenditure reductions and lower than expected costs for blood products and out-of-province hospital payments; |

| · | Lower than anticipated billings for Medicare; |

| · | Lower than budgeted expenses under the Prescription Drug Program due in part to savings from generic drugs. |

These under-expenditures were partially offset by some over-expenditures, including a deficit in the Vitalité Health Network.

Social Development

Social Development expenses were $36.3 million less than budget mainly due to the following:

| · | Lower than budgeted expenses in the Long Term Care program due to construction delays for various nursing homes as well as lower program delivery expenses; |

| · | Lower than budgeted expenses in the Housing Services program as a result of delays associated with the Affordable Housing Program; |

| · | Lower than budgeted expenses in the Child Welfare and Youth Services program due to a reduction in caseload as well as accessing the federal disability tax credit on behalf of children in care; |

| · | Lower than budgeted expenses in the Special Purpose Account. |

These under-expenditures were partially offset by higher than budgeted expenses in the Income Security program due to an increase in the social assistance caseload as well as higher than budgeted provision for losses expense.

Protection Services

Protection Services expenses were $2.1 million lower than budget mainly due to expenditure restraint, vacant positions and the capitalization of computer hardware and software systems in the departments of Justice and Attorney General and Public Safety.

Economic Development

Economic Development expenses were $5.6 million lower than budget mainly due to the following:

| · | Lower than budgeted provision for losses expense; |

| · | Lower than anticipated expenses under Economic Development’s Strategic Assistance Program due to a number of projects not proceeding in the 2013 fiscal year as planned; |

| · | Lower than anticipated expenses under Invest NB’s Strategic Assistance Program due to the number and timing of assistance applications approved. |

These under-expenditures were partially offset by higher than budgeted expenses in the Regional Development Corporation Special Operating Agency due to the completion of federally-funded water treatment facilities.

Labour and Employment

Labour and Employment expenses were $27.8 million lower than budget mainly due to lower than expected demand for programs offered under the Labour Market Development Agreement, the Employment Development program, and the Labour Market Agreement.

Resources

Resources expenses were $4.9 million lower than budget due to a number of under-expenditures, including the following:

| · | Lower than anticipated demand in the Department of Agriculture, Aquaculture and Fisheries Strategic Assistance Program; |

| · | Under-expenditure in the Department of Natural Resources Forest Management program; |

| · | Lower than budgeted provision for loss. |

| 2013 | PROVINCE OF NEW BRUNSWICK | 11 |

| | | |

These decreases were partially offset by additional expenses due to the Energy Efficiency and Conservation Agency of New Brunswick’s use of accumulated surplus to maintain normal spending levels in 2013, a change respecting the consolidation of the Energy and Utilities Board and higher than budgeted amortization expense.

Transportation and Infrastructure

Transportation expenses were $16.2 million higher than budget mainly due to higher than budgeted expenses in the Department of Transportation and Infrastructure as a result of delays in achieving some government renewal savings initiatives and cost pressures related to increased commodity prices.

Central Government

Central Government expenses were $129.6 million higher than budget. This was mainly due to higher than budgeted pension expense due in part to updated actuarial valuations, particularly related to updated mortality tables. This increase was partially offset by lower than budgeted provision for losses expense.

Service of the Public Debt

Service of the Public Debt expenses were $11.7 million lower than budget primarily due to issuing bonds later in the fiscal year than anticipated and relying more on short-term financing at lower interest rates. This was partially offset by borrowing more to finance the larger than anticipated deficit.

Actual 2012 to Actual 2013 Comparison

2012 Actual to 2013 Actual

($ millions)

| Item | 2012 Actual | 2013 Actual | Change | % Change |

| | | | | |

| Education and Training | 1,749.3 | 1,787.6 | 38.3 | 2.2 |

| | | | | |

| Health | 2,730.0 | 2,785.9 | 55.9 | 2.0 |

| | | | | |

| Social Development | 1,029.9 | 1,055.6 | 25.7 | 2.5 |

| | | | | |

| Protection Services | 229.9 | 237.3 | 7.4 | 3.2 |

| | | | | |

| Economic Development | 257.3 | 270.6 | 13.3 | 5.2 |

| | | | | |

| Labour and Employment | 108.4 | 100.5 | (7.9) | (7.3) |

| | | | | |

| Resources | 214.6 | 210.1 | (4.5) | (2.1) |

| | | | | |

| Transportation and Infrastructure | 527.7 | 547.7 | 20.0 | 3.8 |

| | | | | |

| Central Government | 542.3 | 633.8 | 91.5 | 16.9 |

| | | | | |

| Service of the Public Debt | 661.8 | 660.3 | (1.5) | (0.2) |

| | | | | |

| Total Expenses | 8,051.2 | 8,289.4 | 238.2 | 3.0 |

| | | | | |

Items in the table are reported by functional area. See the related schedule in the consolidated financial statements for additional details.

Education and Training

Education and Training expenses were $38.3 million higher than the previous year mainly due to the following:

| · | Additional investments and salaries in K-12 education; |

| · | Increased pension expense. |

These increases were partially offset by a decrease in provision for losses expense.

| 2013 | PROVINCE OF NEW BRUNSWICK | 12 |

| | | |

Health

Health expenses were $55.9 million higher than the previous year mainly due to the following:

| · | An increase in expenses under the Medicare program due to the recruitment of additional physicians, growth, and increased wages; |

| · | An increase in expenses in the Regional Health Authorities associated with wages and inflation; |

| · | An increase in pension expense. |

These increases were partially offset by a decrease in expenses under the Prescription Drug Program mainly due to decreased costs for generic drugs.

Social Development

Social Development expenses were $25.7 million higher than the previous year mainly due to an increase in the Long Term Care program as a result of additional funding provided to nursing homes and home support agencies.

Protection Services

Protection Services expenses were $7.4 million higher than the previous year due to the following:

| · | Additional expenses in the Department of Public Safety’s Disaster Financial Assistance program, as well as a one-time pay out of severance to RCMP Members; |

| · | Increased expenses in the Court Services program of the Department of Justice and Attorney General; |

| · | Increased pension expense; |

| · | Increased amortization expense. |

Economic Development

Economic Development expenses were $13.3 million higher than the previous year mainly due to the following:

| · | Increased expenses by Invest NB as a result of 2013 being its first full year of operations; |

| · | Increased expenses under the Department of Economic Development’s Strategic Assistance |

Program due to projects that were postponed in 2012 proceeding in 2013;

| · | Additional economic development initiatives provided by the NB Immigrant Investor Fund. |

These increases were partially offset by decreased provision for losses expense.

Labour and Employment

Labour and Employment expenses were $7.9 million lower than the previous year mainly due to lower than expected demand for programs offered under the Labour Market Development Agreement and the Labour Market Agreement.

Resources

Resources expenses were $4.5 million lower than the previous year mainly due to the following:

| · | Decreased expenses by the Energy Efficiency and Conservation Agency of New Brunswick due to a leveling of program participation and changes made to the residential sector programs; |

| · | Decreased provision for losses expenses; |

| · | Decreased Public Works and Infrastructure expenses as a result of projects completed in the previous fiscal year. |

These decreases were partially offset by increased expenses in other areas, notably the Canada-New Brunswick Excess Moisture Initiative in the Department of Agriculture, Aquaculture and Fisheries.

Transportation and Infrastructure

Transportation expenses were $20.0 million higher than the previous year mainly due to increased amortization expense.

| 2013 | PROVINCE OF NEW BRUNSWICK | 13 |

| | | |

Central Government

Central Government expenses were $91.5 million higher than the previous year mainly due to increased pension expense under General Government, mainly as a result of updated actuarial information. These increases were partially offset by decreased provision for losses expense and expenses incurred by Algonquin Properties Limited in relation to the sale of the Algonquin Hotel & Golf Course in the previous fiscal year.

Service of the Public Debt

Service of the Public Debt expenses were $1.5 million less than the previous fiscal year primarily due to refinancing maturing debt at lower interest rates and delaying bond issuance until later in the fiscal year. This was partially offset by higher levels of debt.

| 2013 | PROVINCE OF NEW BRUNSWICK | 14 |

| | | |

INDICATORS OF FINANCIAL HEALTH

This section provides indicators of progress in the Province’s financial condition and follows Canadian Institute of Chartered Accountants (CICA) guidelines, using information provided in the Province’s consolidated financial statements as well as other standard socio-economic indicators such as nominal Gross Domestic Product (GDP) data from Statistics Canada.

The analysis provides results in a manner that improves transparency and provides a clearer understanding of recent trends in the Province’s financial health. Trends over the last ten years (2004 to 2013) are evaluated using sustainability, flexibility and vulnerability criteria established by the CICA. Though many potential indicators are available, those found to be the most relevant, measurable and transparent to users of government financial information are included. Similar data series are also widely used by banks and other financial institutions, investors and credit-rating agencies.

In evaluating a government’s financial health, it should be acknowledged that governments have exposure to a number of variables that are beyond their direct scope of control, but still can exert major influences on financial results and indicators. These include but are not limited to:

| · | Changing global economic conditions such as energy prices, commodity prices, investment valuation and inflation; |

| · | Changes to international financial conditions that impact interest rates, currency fluctuations or availability of credit; |

| · | Changes to federal transfers or programs; |

| · | Emergencies such as floods, forest fires and pandemics; |

| · | Developments affecting agencies such as NB Power that are reflected on the Province’s books and; |

| · | Changes in generally accepted accounting principles. |

Sustainability

Sustainability is defined by CICA as the degree to which a government can maintain its existing financial obligations both in respect of its service commitments to the public and financial commitments to creditors, employees and others without increasing the debt or tax burden relative to the economy within which it operates. It is measured in this analysis by:

| · | Net debt as a proportion of GDP; |

Net Debt as a Proportion of GDP:

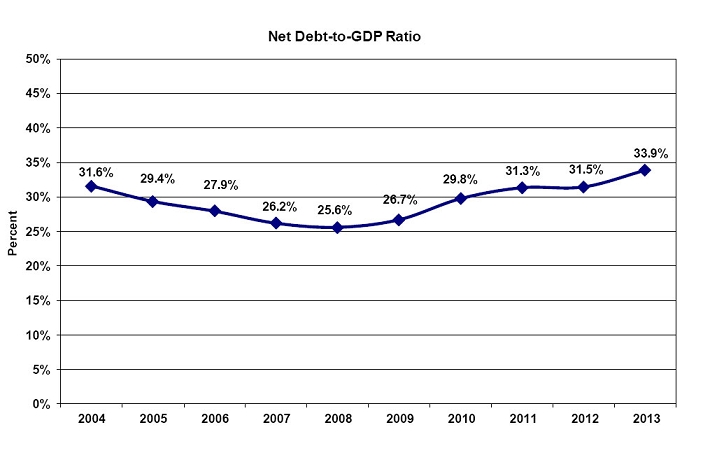

Net debt is an indication of the extent to which Provincial government liabilities exceed financial assets. The net debt-to-GDP ratio shows the relationship between net debt and the economy. If the ratio is declining, growth in the economy is exceeding growth in net debt, resulting in improved sustainability. Conversely, an increasing net debt-to-GDP ratio indicates net debt is increasing faster than growth in the economy and serving to reduce the provincial government’s financial sustainability.

Over the last ten years the Province’s ratio of net debt-to-GDP increased from 31.6% to 33.9%. The following graph reports a steady improvement (reduction) in the net debt-to-GDP ratio from 2004 to 2008. Beginning 2009, the ratio trended upwards related to economic circumstances, capital projects, tax changes and continued cost pressures for health and social programs. In 2012, the ratio stabilized from recent growth trends reflecting government efforts to manage the Province’s finances, however it spiked in 2013 in part related to the Route One Gateway project coming onto the Province’s books.

For purposes of the Fiscal Responsibility and Balanced Budget Act, an improvement in the net debt-to-GDP ratio over successive fiscal periods is targeted. This means the net debt-to-GDP ratio for the year ended 31 March 2015 must be lower than the year ended 31 March 2011. The government will be introducing new balanced budget legislation during its mandate.

| 2013 | PROVINCE OF NEW BRUNSWICK | 15 |

| | | |

| | Net Debt-to-GDP Ratio | |

| Fiscal Year Ending | Net Debt | GDP | Net Debt/GDP |

| | ($ millions) | ($ millions) | (%) |

| 2004 | 7,067.2 | 22,366 | 31.6% |

| 2005 | 6,948.2 | 23,672 | 29.4% |

| 2006 | 6,904.9 | 24,716 | 27.9% |

| 2007 | 6,767.7 | 25,847 | 26.2% |

| 2008 | 7,158.8 | 27,966 | 25.6% |

| 2009 | 7,615.9 | 28,533 | 26.7% |

| 2010 | 8,636.7 | 29,026 | 29.8% |

| 2011 | 9,697.5 | 30,941 | 31.3% |

| 2012 | 10,122.2 | 32,180 | 31.5% |

| 2013 | 11,054.0 | 32,631 | 33.9% |

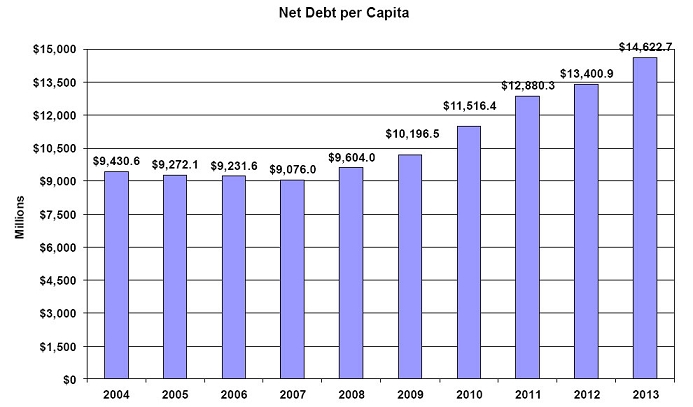

Net Debt per Capita:

Net debt per capita is a statement of the net debt attributable to each New Brunswick resident. A decrease in net debt per capita suggests the debt burden has improved while an increase implies the debt burden has increased. The level of net debt per capita made a steady improvement (reduction) from 2004 to 2007. Since 2008, the net debt per capita has trended upwards reflecting economic circumstances, capital projects, tax changes and continued cost pressures for health and social programs.

| 2013 | PROVINCE OF NEW BRUNSWICK | 16 |

| | | |

| | Net Debt per Capita | |

| Fiscal Year Ending | Net Debt | Population | Net Debt per Capita |

| | ($ millions) | (July 1) | ($) |

| 2004 | 7,067.2 | 749,389 | 9,430.6 |

| 2005 | 6,948.2 | 749,369 | 9,272.1 |

| 2006 | 6,904.9 | 747,960 | 9,231.6 |

| 2007 | 6,767.7 | 745,674 | 9,076.0 |

| 2008 | 7,158.8 | 745,398 | 9,604.0 |

| 2009 | 7,615.9 | 746,910 | 10,196.5 |

| 2010 | 8,636.7 | 749,945 | 11,516.4 |

| 2011 | 9,697.5 | 752,892 | 12,880.3 |

| 2012 | 10,122.2 | 755,335 | 13,400.9 |

| 2013 | 11,054.0 | 755,950 | 14,622.7 |

Flexibility

Flexibility is defined by CICA as the degree to which a government can change its debt or tax burden on the economy within which it operates to meet its existing financial obligations both in respect of its service commitments to the public and financial commitments to creditors, employees and others. It is measured in this analysis by:

| · | Own-source revenue as a proportion of GDP; |

| · | Cost of servicing the public debt as a proportion of total revenue. |

| 2013 | PROVINCE OF NEW BRUNSWICK | 17 |

| | | |

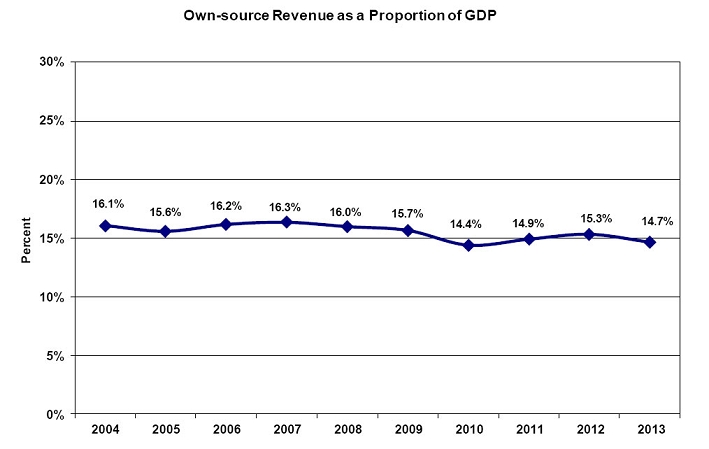

Own-source Revenue as a Proportion of GDP:

This ratio measures own-source revenues of the Provincial government as a percentage of the economy, as measured by nominal GDP. An increase in this ratio indicates that government own-source revenues are growing faster than the economy as a whole, reducing government’s flexibility to increase revenues without slowing growth in the economy. A decrease in the ratio is indicative of the government taking less revenue out of the economy on a relative basis, which increases its flexibility.

Own-source revenue includes revenues from taxation, natural resources, fees, return on investment, lotteries, fines and penalties, etc., and is essentially all revenue minus federal transfers. While more controllable than federal transfers, as the Province can influence revenues through its own tax rates and fiscal policy, own-source revenue is vulnerable to, among other factors:

| · | Net income or revenue of outside agencies whose revenue can fluctuate significantly due to price, volume, accounting changes, weather, etc (e.g. NB Power) |

| · | Variability in provincial revenues that are collected or estimated by the federal government such as personal and corporate income taxes and the Harmonized Sales Tax; |

| · | Commodity tax revenues such as Metallic Minerals Tax that are vulnerable to world prices. |

Own-source revenue as a proportion of GDP was relatively stable over the first six years of the ten-year period 2004 to 2013. Since that time the Province has been withdrawing a smaller share from the economy, reflective of the economic slowdown and lowered taxes, amongst other factors.

| 2013 | PROVINCE OF NEW BRUNSWICK | 18 |

| | | |

| | Own-source Revenue as a Proportion of GDP | |

| Fiscal Year Ending | Own-source Revenue | GDP | Own-source Revenue |

| | | | as a Proportion of |

| | | | GDP |

| | ($ millions) | ($ millions) | (%) |

| 2004 | 3,594.1 | 22,366 | 16.1% |

| 2005 | 3,688.6 | 23,672 | 15.6% |

| 2006 | 3,994.2 | 24,716 | 16.2% |

| 2007 | 4,225.4 | 25,847 | 16.3% |

| 2008 | 4,469.7 | 27,966 | 16.0% |

| 2009 | 4,467.4 | 28,533 | 15.7% |

| 2010 | 4,179.7 | 29,026 | 14.4% |

| 2011 | 4,612.5 | 30,941 | 14.9% |

| 2012 | 4,931.7 | 32,180 | 15.3% |

| 2013 | 4,781.2 | 32,631 | 14.7% |

Cost of Servicing the Public Debt as a Proportion of Total Revenue:

Debt service costs as a proportion of total revenue is an indicator of the Province’s ability to satisfy existing credit requirements in the context of the government’s overall revenue. Debt service costs can be impacted by variables outside the direct control of government, such as credit ratings, interest rates, financial markets and currency fluctuations. Investment in public infrastructure resulting in a change in the stock of debt can also influence borrowing requirements.

The Province’s proportion of debt service costs to revenue declined steadily over the 2004 to 2008 period, lowering the overall financial burden on the Provincial budget. A decrease in this ratio indicates that debt service costs are a smaller proportion of Provincial revenues overall, allowing the Province more financial resources to provide essential programs and services. For the last seven years, the ratio has been relatively stable.

| 2013 | PROVINCE OF NEW BRUNSWICK | 19 |

| | | |

| Cost of Servicing the Public Debt as a Proportion of Total Revenue |

| Fiscal Year Ending | Cost of Servicing the | Total Revenue | Cost of Servicing the |

| | Public Debt | | Public Debt as a |

| | | | Proportion of Total |

| | | | Revenue |

| | ($ millions) | ($ millions) | (%) |

| 2004 | 581.8 | 5,512.0 | 10.6% |

| 2005 | 579.6 | 6,043.4 | 9.6% |

| 2006 | 590.3 | 6,387.1 | 9.2% |

| 2007 | 558.0 | 6,756.3 | 8.3% |

| 2008 | 575.7 | 7,190.3 | 8.0% |

| 2009 | 601.4 | 7,230.9 | 8.3% |

| 2010 | 607.2 | 7,120.5 | 8.5% |

| 2011 | 641.5 | 7,542.8 | 8.5% |

| 2012 | 661.8 | 7,805.9 | 8.5% |

| 2013 | 660.3 | 7,781.7 | 8.5% |

Vulnerability

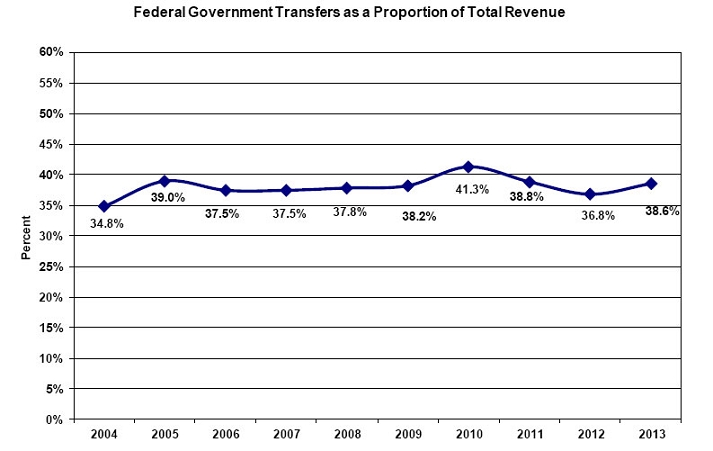

Vulnerability as defined by CICA is the degree to which a government is dependent on sources of funding outside its control or influence or is exposed to risks that could impair its ability to meet its existing financial obligations both in respect of its service commitments to the public and financial commitments to creditors, employees and others. A common measurement of vulnerability is federal government transfers as a proportion of revenue.

Federal Government Transfers as a Proportion of Total Revenue:

Revenue from federal sources is comprised of conditional and unconditional grants from the federal government, including:

| · | Fiscal Equalization Program payments; |

| · | The Canada Health Transfer and the Canada Social Transfer; |

| · | Conditional grants or capital revenue in support of economic development, infrastructure, education and labour training and other areas. |

Federal transfer payments can be affected by both federal fiscal policy decisions, as well as the normal annual estimate process that guides federal payments under the Equalization Program and Canada Health and Social Transfers. Both of these factors can contribute to year-to-year changes in the level of transfers.

Comparing the level of federal transfers to total revenue provides an indication of the vulnerability of the Province. Generally, if the ratio is increasing, the Province is increasingly reliant on federal transfers, resulting in increased vulnerability. If the ratio is declining, vulnerability is diminished.

Federal government transfers as a proportion of total revenue hovered in the 37-38 percent range from 2006 to 2009, before spiking in 2010. In that year, provincial-source revenues contracted as the effects of the economic slowdown hampered revenues and the NBEFC experienced a significant net loss. At the same time, federal stimulus funding supported federal-source revenue growth. The ratio declined the subsequent two years before increasing to 38.6% in 2013. This reflects weakened provincial-source revenues and a one-time capital revenue related to Route One Gateway.

| 2013 | PROVINCE OF NEW BRUNSWICK | 20 |

| | | |

| Federal Government Transfers as a Proportion of Total Revenue |

| Fiscal Year Ending | Federal Government | Total Revenue | Federal Government |

| | Transfers | | Transfers as a |

| | | | Proportion of Total |

| | | | Revenue |

| | ($ millions) | ($ millions) | (%) |

| 2004 | 1,917.9 | 5,512.0 | 34.8% |

| 2005 | 2,354.8 | 6,043.4 | 39.0% |

| 2006 | 2,392.9 | 6,387.1 | 37.5% |

| 2007 | 2,530.9 | 6,756.3 | 37.5% |

| 2008 | 2,720.6 | 7,190.3 | 37.8% |

| 2009 | 2,763.6 | 7,230.9 | 38.2% |

| 2010 | 2,940.8 | 7,120.5 | 41.3% |

| 2011 | 2,930.3 | 7,542.8 | 38.8% |

| 2012 | 2,874.2 | 7,805.9 | 36.8% |

| 2013 | 3,000.5 | 7,781.7 | 38.6% |

| 2013 | PROVINCE OF NEW BRUNSWICK | 24 |

| | | |

CONSOLIDATED STATEMENT OF OPERATIONS

for the fiscal year ended 31 March 2013

| | | | | | (millions) | | | |

| Schedule | | 2013 | | | 2013 | | | 2012 |

| | | | Budget | | | Actual | | | Actual |

| | REVENUE | | | | | | | | |

| | Provincial Sources | | | | | | | | |

| 14 | Taxes | $ | 3,690.9 | $ | 3,542.1 | $ | 3,574.4 |

| 15 | Licenses and Permits | | 144.2 | | | 144.6 | | | 138.8 |

| 16 | Royalties | | 121.7 | | | 86.1 | | | 89.3 |

| 17 | Income from Government Business Enterprises | | 256.9 | | | 189.7 | | | 317.2 |

| 18 | Other Provincial Revenue | | 589.8 | | | 598.0 | | | 586.4 |

| | Sinking Fund Earnings | | 221.0 | | | 220.7 | | | 225.6 |

| | | | 5,024.5 | | | 4,781.2 | | | 4,931.7 |

| | Federal Sources | | | | | | | | |

| | Fiscal Equalization Payments | | 1,597.7 | | | 1,597.7 | | | 1,632.6 |

| 19 | Unconditional Grants | | 901.9 | | | 894.2 | | | 865.7 |

| 20 | Conditional Grants | | 527.1 | | | 508.6 | | | 375.9 |

| | | | 3,026.7 | | | 3,000.5 | | | 2,874.2 |

| | | | 8,051.2 | | | 7,781.7 | | | 7,805.9 |

| | EXPENSE | | | | | | | | |

| 21 | Education and Training | | 1,761.2 | | | 1,787.6 | | | 1,749.3 |

| 22 | Health | | 2,814.4 | | | 2,785.9 | | | 2,730.0 |

| 23 | Social Development | | 1,091.9 | | | 1,055.6 | | | 1,029.9 |

| 24 | Protection Services | | 239.4 | | | 237.3 | | | 229.9 |

| 25 | Economic Development | | 276.2 | | | 270.6 | | | 257.3 |

| 26 | Labour and Employment | | 128.3 | | | 100.5 | | | 108.4 |

| 27 | Resources | | 215.0 | | | 210.1 | | | 214.6 |

| 28 | Transportation and Infrastructure | | 531.5 | | | 547.7 | | | 527.7 |

| 29 | Central Government | | 504.2 | | | 633.8 | | | 542.3 |

| | Service of the Public Debt (Note 11) | | 672.0 | | | 660.3 | | | 661.8 |

| | | | 8,234.1 | | | 8,289.4 | | | 8,051.2 |

| | ANNUAL DEFICIT | $ | (182.9) | | $ | (507.7) | | $ | (245.3) |

The accompanying notes are an integral part of these consolidated financial statements.

| 2013 | PROVINCE OF NEW BRUNSWICK | 25 |

| | | |

CONSOLIDATED STATEMENT OF CASH FLOW

for the fiscal year ended 31 March 2013

| | | (millions) | | |

| | | 2013 | | | 2012 | |

| OPERATING ACTIVITIES | | | | | | |

| Deficit | $ | (507.7) | $ | (245.3) | |

| Non Cash Items | | | | | | |

| Amortization of Premiums, Discounts and Issue Expenses | | 4.2 | | | 4.6 | |

| Foreign Exchange Expense | | (19.3) | | | (22.3) | |

| (Decrease) increase in Provision for Losses | | (77.5) | | | 33.7 | |

| Amortization of Tangible Capital Assets | | 349.9 | | | 327.3 | |

| Loss on Disposal or Impairment of Tangible Capital Assets | | 24.7 | | | 26.3 | |

| Sinking Fund Earnings | | (220.7) | | | (225.6) | |

| Losses on Foreign Exchange Settlements | | 6.5 | | | 6.9 | |

| Increase (decrease) in Net Pension Liability (Note 12) | | 110.0 | | | (39.6) | |

| (Decrease) increase in Deferred Revenue | | (50.0) | | | 25.7 | |

| Decrease (increase) in Working Capital | | 32.2 | | | (42.2) | |

| Net Cash From Operating Activities | | (347.7) | | | (150.5) | |

| INVESTING ACTIVITIES | | | | | | |

| Increase in Investments, Loans and Advances | | (159.2) | | | (166.1) | |

| Other Comprehensive Income of Government Business Enterprises | | 124.8 | | | (9.9) | |

| Net Cash Used in Investing Activities | | (34.4) | | | (176.0) | |

| CAPITAL TRANSACTIONS | | | | | | |

| Acquisition of Capital Assets (Note 8) | | (899.7) | | | (525.9) | |

| FINANCING ACTIVITIES | | | | | | |

| Proceeds from Issuance of Funded Debt | | 1,920.6 | | | 2,318.7 | |

| Purchase of NBEFC Debentures | | (451.6) | | | (531.1) | |

| Elimination of Debentures held by NB Immigrant Investor Fund | | (34.1) | | | (41.5) | |

| Received from Sinking Fund for Redemption of Debentures and | | | | | | |

| Payment of Exchange | | 628.5 | | | 502.9 | |

| Decrease in Obligations under Capital Leases | | (27.1) | | | (19.5) | |

| Sinking Fund Installments | | (126.6) | | | (172.9) | |

| Short Term Borrowing | | 697.0 | | | (152.5) | |

| Funded Debt Matured | | (903.3) | | | (908.4) | |

| Net Cash From Financing Activities | | 1,703.4 | | | 995.7 | |

| INCREASE IN CASH DURING YEAR | | 421.6 | | | 143.3 | |

| CASH POSITION - BEGINNING OF YEAR | | 875.0 | | | 731.7 | |

| CASH POSITION - END OF YEAR | $ | 1,296.6 | $ | 875.0 | |

| CASH REPRESENTED BY | | | | | | |

| | | | | | |

| Cash and Short Term Investments | $ | 1,296.6 | | $ | 875.0 | |

The accompanying notes are an integral part of these consolidated financial statements.

| 2013 | PROVINCE OF NEW BRUNSWICK | 26 |

| | | |

CONSOLIDATED STATEMENT OF CHANGE IN NET DEBT

for the fiscal year ended 31 March 2013

| | | | | | (millions) | | | |

| | | 2013 | | | 2013 | | | 2012 |

| | | Budget | | | Actual | | | Actual |

| RESTATED NET DEBT - BEGINNING OF YEAR (NOTE 18) | $ | (10,045.8) | $ | (10,122.2) | $ | (9,697.5) |

| CHANGES IN YEAR | | | | | | | | |

| Annual Deficit | | (182.9) | | | (507.7) | | | (245.3) |

| Other Comprehensive Income of Government | | | | | | | | |

| Business Enterprises | | --- | | | 124.8 | | | (9.9) |

| Acquisition of Tangible Capital Assets (Note 8) | | (895.0) | | | (899.7) | | | (525.9) |

| Amortization of Tangible Capital Assets (Note 8) | | 338.9 | | | 349.9 | | | 327.3 |

| Loss on Disposal or Impairment of Tangible Capital Assets | | --- | | | 24.7 | | | 26.3 |

| Net Change in Supplies Inventories | | --- | | | 3.7 | | | 3.7 |

| Net Change in Prepaid Expenses | | --- | | | (27.5) | | | (0.9) |

| INCREASE IN NET DEBT | | (739.0) | | | (931.8) | | | (424.7) |

| NET DEBT - END OF YEAR | $ | (10,784.8) | | $ | (11,054.0) | | $ | (10,122.2) |

CONSOLIDATED STATEMENT OF CHANGE IN ACCUMULATED DEFICIT

for the fiscal year ended 31 March 2013

| | | | | | (millions) | | | |

| | | 2013 | | | 2013 | | | 2012 |

| | | Budget | | | Actual | | | Actual |

| RESTATED ACCUMULATED DEFICIT - | $ | (3,368.0) | $ | (2,413.0) | $ | (2,157.8) |

| BEGINNING OF YEAR (NOTE 18) | | | | | | | | |

| Annual Deficit | | (182.9) | | | (507.7) | | | (245.3) |

| Other Comprehensive Income of Government | | | | | | | | |

| Business Enterprises | | --- | | | 124.8 | | | (9.9) |

| ACCUMULATED DEFICIT - END OF YEAR | $ | (3,550.9) | | $ | (2,795.9) | | $ | (2,413.0) |

The accompanying notes are an integral part of these consolidated financial statements.

| 2013 | PROVINCE OF NEW BRUNSWICK | 27 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a) Basis of Accounting

These consolidated financial statements are prepared in accordance with Canadian public sector accounting standards.

b) Changes in Accounting Policy

Adoption of Public Sector Accounting Standard PS 3410, Government Transfers

Effective 1 April 2012, the Province changed its policy for recording transfers for capital purposes. Previously, these transfer amounts were deferred and recognized as revenue over the useful life of the related tangible capital asset. As a result of this change in policy, the recognition of transfer revenues is only deferred when and to the extent that the transfer gives rise to an obligation that meets the definition of a liability. The new standard has been applied retrospectively, and prior periods have been adjusted accordingly. Note 18 discloses the impact of this change in accounting policy on prior periods.

Receivables have been established for transfers to which the Province is entitled under government legislation, regulation or agreement. Liabilities have been established for any transfers due at 31 March 2013 for which the intended recipients have met the eligibility criteria.

Adoption of Public Sector Accounting Standard PS 3510, Tax Revenue

During 2012-2013, the Province adopted Public Sector Accounting Standard PS 3510. Transfers for Tuition Rebate and the Child Tax Working Income Supplement previously paid through the tax system are now reported on a gross basis. For 2012-2013, these transfers represented $16.5 million and $11.1 million respectively. Tax concessions continue to be netted against the type of tax revenue for which they are providing relief.

Official estimates received from the federal government are used as the basis for determining federal tax revenue. Federal tax revenue amounts for the current year reflect prior year adjustments based on returns or more recent economic data.

Provincial real property tax is recognized based on the calculation of applying the relevant provincial and local service district tax rates to the assessed property value. Adjustments are made to current year revenue for future assessments and allowance for doubtful accounts.

Other provincial tax revenue is recognized based on the self-assessed returns of tax payers and tax collectors. This revenue is subsequently adjusted for future tax assessments and allowance for doubtful accounts. Other provincial tax revenue is also recognized from direct payments made by tax payers in completing certain types of transactions.

c) Specific Accounting Policies

Debt Charges

Interest and other debt service charges are reported in the Consolidated Statement of Operations as Service of the Public Debt except as described below:

Because government business enterprises are included in the Provincial Reporting Entity through modified equity accounting, the cost of servicing their debt is not included in the Service of the Public Debt expense. The cost of servicing the debt of government business enterprises is an expense included in the calculation of their net profit or loss for the year.

| 2013 | PROVINCE OF NEW BRUNSWICK | 28 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

Interest costs imputed on the Province’s Accrued Pension Liability are recorded as part of pension expense, which is included in various expense functions.

Interest on debt to finance the Student Loan Portfolio is recorded as part of the Education and Training expense function.

Interest earned on the assets of the General Sinking Fund and on other provincial assets is reported as revenue.

Note 11 to these consolidated financial statements reports the components of the Service of the Public Debt Expense function and total debt charges.

Asset Classification

Assets are classified as either financial or non-financial. Financial assets are assets that could be used to discharge existing liabilities or finance future operations and are not to be consumed in the normal course of operations. Non-financial assets are acquired, constructed or developed assets that do not provide resources to discharge existing liabilities but are employed to deliver government services, may be consumed in normal operations and are not for resale. Non-financial assets include tangible capital assets, prepaid and deferred charges and inventories of supplies.

Cash and Short Term Investments

Cash and short term investments include cash on hand and short term, highly liquid investments that are readily convertible to known amounts of cash, with maturity dates of three months or less. The market value of short term investments is not materially different from the carrying value.

Other Investments

Investments are recorded at cost. Where there has been a loss in the value of an investment that is other than a temporary decline, the investment is written down to recognize this loss.

Loans

Loans are initially recorded at cost, and reported at the lower of cost and net recoverable value through a valuation allowance. Changes in the valuation allowance are recognized in expense. Interest revenue is recognized on a loan when earned, and ceases to be accrued when the collectability of either the principal or interest is not reasonably assured.

Loans issued under the Economic Development Act, Agricultural Development Act, and Fisheries and Aquaculture Development Act facilitate the establishment, development, or maintenance of industry in a variety of areas. As such, the nature and terms of the loans under these Acts vary. Energy Efficiency Upgrade Loans issued to clients are repayable over a maximum six year term, and are interest free. Loans to Students are interest free while the student is in full-time studies and becomes repayable with interest six months after the student leaves post-secondary studies. The maximum repayment term is fifteen years. Loans issued under the New Brunswick Housing Act may offer concessionary interest rates, and are repayable over a period not to exceed twenty-five years.

Concessionary Loans

There are two situations where the Province charges loan disbursements entirely as expenses. These are:

| · | Loan agreements which commit the Province to provide future grants to the debtor to be used to repay the loan. |

| · | Loan agreements which include forgiveness provisions if the forgiveness is considered likely. |

| 2013 | PROVINCE OF NEW BRUNSWICK | 29 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

In both these situations, the loan is charged to expense when it is disbursed.

Loans that are significantly concessionary because they earn a low rate of return are originally recorded as assets at the net present value of the expected future cash flows. The net present value is calculated using the Province’s borrowing rate at the time the loan was issued. The difference between the nominal value of the loan and its net present value is recorded as an expense.

Inventories

Inventories are recorded at the lower of cost or net realizable value. Inventories include supplies for use, and goods and properties held for resale. Properties held for resale are reported as a financial asset and include land and fixtures acquired or constructed for the purpose of sale. Properties held for resale also include properties acquired through foreclosure. Inventories of supplies for use are reported as a non-financial asset.

Allowances

Allowances have been established for loans and accounts receivable, loan guarantees and other possible losses. These allowances are disclosed in the schedules to the consolidated financial statements.

Obligations resulting from guaranteed loans are recorded as liabilities when a loss is probable with changes in this allowance recorded annually. As with all provisions for loss, this is an estimate and reflects management’s best estimate of probable losses.

Each outstanding loan guarantee under the Economic Development Act is reviewed on a quarterly basis. An allowance for loss on loan guarantees is established when it is determined that a loss is probable. A loss is considered probable when one or more of the following factors is present:

| · | a decline in the financial position of the borrower; |

| · | economic conditions in which the borrower operates indicate the borrower’s inability to repay the loan; |

| · | collection experience for the loan. |

Losses on guaranteed loans under the Agriculture Development Act and the Fisheries and Aquaculture Development Act for classes that have similar standards are calculated using an average rate based on past experience and trends.

Amounts due to the Province but deemed uncollectible are written off from the accounts of the Province once the write-off has been approved by either the Board of Management or Secretary to the Board of Management depending on the dollar value involved.

Tangible Capital Assets

Tangible capital assets are assets owned by the Province which have useful lives greater than one year. Certain dollar thresholds have been established for practical purposes.

Tangible capital asset policies of government entities which are consolidated in these consolidated financial statements are not adjusted to conform to Provincial policies. The types of items which could differ include amortization rates, estimates of useful lives and dollar thresholds for capitalization.

Public Private Partnership Road Contracts

The Province, through the New Brunswick Highway Corporation (NBHC), contracts with independent organizations to provide rehabilitation and maintenance work on designated portions of the Provincial highway network. The contracts provide for annual payment amounts determined at the inception of the contracts for maintenance and rehabilitation (capital improvement) of the roads.

| 2013 | PROVINCE OF NEW BRUNSWICK | 30 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

The terms of the agreements provide for scheduled annual payments which reflect the expected timing of capital improvement work. The payments to the contractors are being accounted for as follows:

| · | as prepaid expenses when the rehabilitation work is expected to be completed after the payment has been made; |

| · | as accrued expenditures when the rehabilitation work is expected to occur prior to the payment being made; and |

| · | as the acquisition of tangible capital assets in the year the rehabilitation work is expected to be completed. |

Amortization of the capital improvement work commences in the year the rehabilitation work is expected to be performed. This may not reflect when the work is actually completed by the contractors. Accordingly, some measurement uncertainty exists relative to the timing of the amortization expense and the allocation of the payment amounts as prepaid expenses, tangible capital assets or accrued expenditures.

Sick Leave

The cost of accumulating, non-vesting sick leave benefits are determined by an actuarial valuation, using management’s best estimate of salary escalation, accumulated sick days at retirement, long term inflation rates and discount rates. In accordance with Canadian public sector accounting standards for post-employment benefits and compensated absences, the Province recognizes the liability.

Injured Worker Liability

The Province provides workers’ compensation benefits on a self-insured basis. WorkSafe New Brunswick administers the claims on the Province’s behalf and charges a fee for this service. The liability for workers’ compensation of $131.9 million as at 31 December 2012 ($132.4 million at 31 December 2011) is determined by an actuary and is included in the Employee Benefits Liability. Management estimates the amount of the liability as at 31 March is not materially different. Annual claim payments are expensed by each department and are included in the functional expense area related to the program in which the employee worked. The net change in the liability excluding the actual claims costs is a decrease of $0.5 million in the 2013 fiscal year ($0.3 million decrease in 2012) and is expensed in General Government.

Trusts Under Provincial Administration

Legally established trust funds which the Province administers but does not control are not included as Provincial assets or liabilities. These consolidated financial statements disclose the equity balances of the trust funds administered by the Province in Note 17.

Borrowing on Behalf of New Brunswick Electric Finance Corporation

The Province, as represented by the Consolidated Fund, has issued long term debt securities on behalf of New Brunswick Electric Finance Corporation in exchange for debentures with like terms and conditions.

The New Brunswick Electric Finance Corporation debentures received by the Province are reported in Note 10 of these consolidated financial statements as a reduction of Funded Debt. This financing arrangement was used to obtain more favourable debt servicing costs. The transactions involving these securities, including the debt servicing costs, are not part of the budget plan of the Province’s Consolidated Fund.

| 2013 | PROVINCE OF NEW BRUNSWICK | 31 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

Foreign Currency Translation and Risk Management

The Province's assets, liabilities and contingent liabilities denominated in foreign currencies are translated to Canadian dollars at the year-end rates of exchange, except where such items have been hedged or are subject to interest rate and currency swap agreements. In such cases, the rates established by the hedge or the agreements are used in the translation. Exchange gains and losses are included in the Consolidated Statement of Operations except for the unrealized exchange gains and losses arising on the translation of long term items, which are deferred and amortized on a straight line basis over the remaining life of the related assets or liabilities. Revenue and expense items are translated at the rates of exchange in effect at the respective transaction dates.

The Province borrows funds in both domestic and foreign capital markets and manages its existing debt portfolio to achieve the lowest debt costs within specified risk parameters. As a result, the Province may be exposed to foreign exchange risk. Foreign exchange or currency risk is the risk that the principal and interest payments on foreign debt will fluctuate in Canadian dollar terms due to fluctuations in foreign exchange rates.

In accordance with risk management policy guidelines, the Province uses various financial instruments and techniques to manage exposure to foreign currency risk. These financial instruments include currency forwards, cross-currency swaps and purchases of foreign denominated assets into the Province’s sinking fund.

As at March 31, 2013, the Province had outstanding $1,500 million US$ and 300 million Swiss Francs denominated debt. Of this total, $1,400 million US$ and 300 million Swiss Francs were hedged by entering into cross-currency swaps, which convert the interest and principal payable from the original currency to Canadian dollars.

The Province’s currency exposure was 0.7% of the total debt portfolio prior to netting out the US dollar denominated assets in the sinking fund. A one cent change in the US/CDN$ foreign exchange rate as of March 31, 2013 would result in a $1.0 million change in the principal amount of Provincial-purpose long term debt. The hypothetical change, a gain or loss, would be amortized over the remaining life of the related debt issue. A one cent change would also result in a change of $0.1 million on interest payments in Service of the Public Debt.

There is no net currency exposure when the US dollar denominated assets held in the sinking fund are netted from the total Provincial-purpose debt portfolio.

Sinking Funds

The General Sinking Fund is maintained by the Minister of Finance under the authority of section 12 of the Provincial Loans Act (“Act”). This Act provides that the Minister shall maintain one or more sinking funds for the payment of funded debt either at maturity or upon redemption in advance of maturity. Typically, redemptions are only made after the related Provincial purpose portion of the debt has been outstanding a minimum of twenty years.

Sinking fund investments in bonds and debentures are reported at par value less unamortized discounts less premiums and the unamortized balance of unrealized foreign exchange gains or losses. Short-term deposits are reported at cost. The Province’s sinking fund may be invested in eligible securities as defined in the Act.

Sinking fund installments are paid into the General Sinking Fund on or before the anniversary date of each issue of funded debt, at the prescribed rate of a minimum of 1% of the outstanding principal.

New Brunswick Electric Finance Corporation (NBEFC) is contractually obligated to pay to the Province the amount of the sinking fund installment required each year in respect of the debentures issued by the Province on behalf of New Brunswick Power Corporation prior to 1 October 2004 and on behalf of NBEFC after 30 September 2004.

The following table shows the allocation of various components of the Sinking Fund between the Consolidated Fund of the Province and NBEFC.

| 2013 | PROVINCE OF NEW BRUNSWICK | 32 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

| | | Consolidated | | | | | | |

| | | Fund | | | NBEFC | | | Total |

| Fund Equity, beginning of year | $ | 4,237.0 | $ | 378.2 | $ | 4,615.2 |

| Sinking Fund Earnings | | 220.7 | | | 20.5 | | | 241.2 |

| Installments | | 126.6 | | | 47.0 | | | 173.6 |

| Paid for Debt Retirement | | (628.5) | | | (69.3) | | | (697.8) |

| Fund Equity, end of year | $ | 3,955.8 | | $ | 376.4 | | $ | 4,332.2 |

Leases

Long term leases, under which the Province, as lessee, assumes substantially all the benefits and risks of ownership of leased property, are classified as capital leases although certain minimum dollar thresholds are in place for practical reasons. The present value of a capital lease is accounted for as a tangible capital asset and an obligation at the inception of the lease.

All leases under which the Province does not assume substantially all the benefits and risks of ownership related to the leased property are classified as operating leases. Each rental payment required by an operating lease is recorded as an expense when it is due.

Measurement Uncertainty

Measurement uncertainty is uncertainty in the determination of the amount at which an item is recognized in financial statements. This uncertainty exists when there is a variance between the recognized amount and another reasonably possible amount. Many items in these consolidated financial statements have been measured using estimates. Those estimates have been based on assumptions that reflect economic conditions. Actual results could differ from these estimates.

Significant estimates pertaining to these consolidated financial statements include the following:

| · | the determination of valuation allowances on investments; |

| · | the establishment of allowances for doubtful accounts and allowances for losses; |

| · | the determination of employee future benefits; |

| · | the determination of injured worker liability and related expense; |

| · | the allocation of payments under Public Private Partnership agreements for highway maintenance between prepaid expense and tangible capital assets; |

| · | the calculation of transition balances for tangible capital assets; |

| · | the determination of depreciation rates and residual values of tangible capital assets, and; |

| · | the determination of tax revenues due to the timing difference between tax collected and future tax assessments. |

| d) | Provincial Reporting Entity |

These consolidated financial statements include those entities which make up the Provincial Reporting Entity. The Provincial Reporting Entity is comprised of certain organizations that are controlled by the government. These organizations are the Consolidated Fund, the General Sinking Fund and the agencies, commissions and corporations listed below.

Transactions and balances of organizations are included in these consolidated financial statements through one of the following accounting methods:

| 2013 | PROVINCE OF NEW BRUNSWICK | 33 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

Consolidation Method

This method combines the accounts of distinct organizations. It requires uniform accounting policies for the organizations except that tangible capital asset policies of these organizations are not conformed to provincial policies. Inter-organizational balances and transactions are eliminated under this method. This method reports the organizations as if they were one organization. The organizations included through the consolidation method are:

Algonquin Golf Limited New Brunswick Credit Union Deposit

Algonquin Properties Limited Insurance Corporation

Ambulance New Brunswick Inc. New Brunswick Energy and Utilities Board

Arts Development Trust Fund New Brunswick Health Council

Atlantic Education International Inc. New Brunswick Highway Corporation

Collège communautaire du Nouveau-Brunswick New Brunswick Housing Corporation

Economic and Social Inclusion Corporation New Brunswick Immigrant Investor Fund (2009) Ltd.

Energy Efficiency and Conservation Agency New Brunswick Internal Services Agency

of New Brunswick New Brunswick Investment Management Corporation

Environmental Trust Fund New Brunswick Legal Aid Services Commission

FacilicorpNB Ltd. New Brunswick Lotteries and Gaming Corporation

Forest Protection Limited Provincial Holdings Ltd.

Horizon Health Network Recycle New Brunswick

Invest NB Regional Development Corporation

Kings Landing Corporation Service New Brunswick

New Brunswick Community College Sport Development Trust Fund

Vitalité Health Network

Modified Equity Method

This method is used for government business enterprises (GBE’s). GBE’s are defined in Note 7 to these consolidated financial statements. The modified equity method reports a GBE’s net assets as an investment on the Province’s Consolidated Statement of Financial Position. The net income of the GBE is reported as income from government business enterprises on the Province’s Consolidated Statement of Operations. Inter-organizational transactions and balances are not eliminated. All gains or losses arising from inter-organizational transactions between GBE’s and other government organizations are eliminated. The accounting policies of GBE’s are not adjusted to conform with those of other government organizations. The organizations that have been included through modified equity accounting are:

New Brunswick Electric Finance Corporation New Brunswick Power Group

New Brunswick Liquor Corporation New Brunswick Securities Commission

New Brunswick Municipal Finance Corporation

Transaction Method

This method records only transactions between the Province and the other organizations. The transaction method was used because the appropriate methods would not produce a materially different result. The organizations included through the transaction method are:

New Brunswick Agricultural Insurance New Brunswick Museum

Commission New Brunswick Public Libraries Foundation

New Brunswick Arts Board Premier's Council on the Status of Disabled Persons

New Brunswick Insurance Board Strait Crossing Finance Inc.

| 2013 | PROVINCE OF NEW BRUNSWICK | 34 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

NOTE 2 BUDGET

The budget figures included in these consolidated financial statements are the amounts published in the Main Estimates, adjusted for transfers from the Supplementary Funding Provision Program and elimination of inter-account transactions.

The Supplementary Funding Provision Program is an appropriation which provides funding to other programs for costs associated with contract settlements and other requirements not budgeted in a specific program.

Budget figures for the year ending 31 March 2013 reflect the acquisition of tangible capital assets and amortization expense. These amounts are disclosed in the Main Estimates as a separate schedule.

In addition, budget figures were restated to reflect the tax revenue accounting for the Tuition Rebate and the Child Tax Working Income Supplement tax transfers. In the 2012-2013 Main Estimates, these transfers through the tax system were budgeted net of tax revenue. Revenue and expense budgets were increased by $26.7 million (Tuition Rebate $15.5 million and Child Tax Working Income Supplement $11.2 million) in order to present budget and actual figures on a comparative basis.

Budget figures were also restated to comparatively reflect the revenue and expense for municipality RCMP service. In the 2012-2013 Main Estimates, municipality RCMP fee revenue was budgeted net of expenses. To present the budget and actual figures on a comparative basis, the revenue and expense budgets have been increased by $11.4 million. This change is also described in Note 18 to these consolidated financial statements.

NOTE 3 FISCAL RESPONSIBILITY AND BALANCED BUDGET ACT

The Province is required under the Fiscal Responsibility and Balanced Budget Act to report annually on the difference between the revenue and expenses, subject to the provisions of sections 4 and 5 of the Act, for the fiscal year to which the Public Accounts relate and the cumulative difference between revenues and expenses for the current fiscal period. 1 April 2011 marks the beginning of a new four year fiscal period. The previous fiscal period ended 31 March 2011.

Section 4 of the Act stipulates that for Balanced Budget purposes, the changes to accounting policies apply prospectively as of the first day of the fiscal year in which the change is implemented and do not affect any previous year.

Section 5(1) of the Act stipulates that any change made within the last fifteen months of the fiscal period or after completion of that period in relation to the official estimates by the Government of Canada for provincial entitlements under the Federal-Provincial Fiscal Arrangements Act (Canada), the Canada-New Brunswick Tax Collection Agreement or the Comprehensive Integrated Tax Coordination Agreement, shall not be taken into account.

Section 5(2) of the Act stipulates that any change made in relation to the first official estimates by the Government of Canada respecting provincial entitlements under the Federal-Provincial Fiscal Arrangements Act (Canada), the Canada-New Brunswick Tax Collection Agreement or the Comprehensive Integrated Tax Coordination Agreement for the last fiscal year of a fiscal period shall not be taken into account.

The deficit according to the Fiscal Responsibility and Balanced Budget Act for the fiscal period ending 31 March 2013 is as follows:

| 2013 | PROVINCE OF NEW BRUNSWICK | 35 |

| | | |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

31 March 2013

| | | (millions) |

| | | 2013 | | 2012 |

| | | Actual | | Actual |

| Revenue | $ | 7,781.7 | $ | 7,789.0 |

| Adjustments as per section 5(1) of the Act | | --- | | --- |

| Adjustments as per section 5(2) of the Act | | --- | | --- |

| Revenue as per Fiscal Responsibility and | | | | |

| Balanced Budget Act | | 7,781.7 | | 7,789.0 |

| Expense | | 8,289.4 | | 8,049.6 |

| Deficit for the year | | (507.7) | | (260.6) |

| Cumulative Deficit at beginning of year | | (260.6) | | --- |

| Cumulative Deficit at end of year | $ | (768.3) | $ | (260.6) |

The Province is required under the Act to report annually on the ratio of Net Debt to Gross Domestic Product (GDP) for the fiscal year to which the Public Accounts relate and the difference between that ratio and the ratio of Net Debt to GDP at the end of the previous fiscal period.

The following table presents the difference between the ratio for the fiscal period ending 31 March 2012 and for the year ended 31 March 2013.

| | | | (millions) | |

| | | 2013 | | 2012 | Difference |

| Net Debt | $ | 11,054.0 | $ | 10,122.2 | |

| GDP (31 December) | $ | 32,631.0 | $ | 32,180.0 | |