UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2006

or

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File Number 1-10560

BENCHMARK ELECTRONICS, INC.

(Exact name of registrant as specified in its charter)

Texas | | 74-2211011 |

(State or other jurisdiction of | | (I.R.S. Employer |

incorporation or organization) | | Identification Number) |

|

3000 Technology Drive

Angleton, Texas 77515

(979) 849-6550 |

(Address, including zip code, and telephone number, including area code, of principal executive offices) |

|

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | | Name of each exchange on which registered |

Common Stock,

par value $0.10 per share | | New York Stock Exchange, Inc. |

Preferred Stock Purchase Rights | | New York Stock Exchange, Inc. |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, or a non-accelerated filer. See definition of “large accelerated filer and non-accelerated filer” in Rule 12b—2 of the Act.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b—2 of the Act).

Yes o No x

As of June 30, 2006, the number of outstanding Common Shares was 64,444,010. As of such date, the aggregate market value of the Common Shares held by non-affiliates, based on the closing price of the Common Shares on the New York Stock Exchange on such date, was approximately $1.5 billion.

As of February 28, 2007, there were 72,100,797 Common Shares of Benchmark Electronics, Inc., par value $0.10 per share, outstanding.

Documents Incorporated by Reference:

Portions of the Company’s Proxy Statement for the 2007 Annual Meeting of Shareholders (Part III, Items 10-13).

PART I

Item 1. Business

Background

Benchmark Electronics, Inc., formerly named Electronics, Inc., began operations in 1979 and was incorporated under Texas law in 1981 as a wholly-owned subsidiary of Intermedics, Inc., a medical implant manufacturer based in Angleton, Texas. In 1986, Intermedics sold 90% of the outstanding common shares of the Company to Electronic Investors Corp., a corporation formed by Donald E. Nigbor, Steven A. Barton and Cary T. Fu, three of our executive officers. In 1988, Electronic Investors Corp. was merged into Benchmark, and in 1990 we completed the initial public offering of our common shares.

General

We are in the business of manufacturing electronics and we provide our services to original equipment manufacturers (OEMs) of computers and related products for business enterprises, medical devices, industrial control equipment, testing and instrumentation products, and telecommunication equipment. The services that we provide are commonly referred to as electronics manufacturing services (EMS). We offer our customers comprehensive and integrated design and manufacturing services, from initial product design to volume production and direct order fulfillment. We also provide specialized engineering services, including product design, printed circuit board layout, prototyping and test development. We believe that we have developed strengths in the manufacturing process for large, complex, high-density printed circuit boards as well as the ability to manufacture high and low volume products in lower cost regions such as Brazil, China, Mexico, Romania and Thailand.

As our customers expand internationally, they increasingly require their EMS partners to have strategic regional locations and global procurement capabilities. We believe that our global manufacturing presence increases our ability to be responsive to our customers’ needs by providing accelerated time-to-market and time-to-volume production of high quality products. These capabilities should enable us to build stronger strategic relationships with our customers and to become a more integral part of their operations. Our customers face challenges in planning, procuring and managing their inventories efficiently due to fluctuations in customer demand, product design changes, short product life cycles and component price fluctuations. We employ production management systems to manage their procurement and manufacturing processes in an efficient and cost-effective manner so that, where possible, components arrive on a just-in-time, as-and-when needed basis. We are a significant purchaser of electronic components and other raw materials, and can capitalize on the economies of scale associated with our relationships with suppliers to negotiate price discounts, obtain components and other raw materials that are in short supply, and return excess components. Our expertise in supply chain management and our relationships with suppliers across the supply chain enable us to reduce our customers’ cost of goods sold and inventory exposure.

We currently operate a total of 64 surface mount production lines (where electrical components are soldered directly onto printed circuit boards) at our domestic facilities and 86 surface mount production lines at our international facilities. Our worldwide facilities include 1.5 million square feet in our domestic facilities in Alabama, California, Minnesota, New Hampshire, North Dakota, Oregon, Texas and Washington; and 1.4 million square feet in our international facilities in Brazil, China, Ireland, Mexico, the Netherlands, Romania, Singapore and Thailand.

Our capabilities have continued to grow through acquisitions and through internal expansion. On January 8, 2007, we completed the acquisition of Pemstar Inc. (Pemstar), a publicly traded EMS company headquartered in Rochester, Minnesota. With the acquisition of Pemstar, our global operations now include 24 facilities in nine countries. This acquisition expanded our customer base and deepened our engineering and systems integration

3

capabilities. The July 2002 acquisition of ACT Manufacturing (Thailand) Public Company Limited and ACT Manufacturing Holdings UK Limited provided us with additional manufacturing capacity in Thailand. We have expanded our manufacturing capacity in Thailand with a printed circuit board assembly (PCBA) facility in Korat in 2004 and a new systems integration facility in Ayudhaya in 2005. In January 2006, we opened a facility in Rochester, Minnesota. Additionally, we expanded our relationships with certain customers during 2003 and added a new systems integration facility in Redmond, Washington. In 2002, we opened a PCBA facility in Suzhou, China that began production during 2003.

We believe our primary competitive advantages are our design, manufacturing, testing and supply chain management capabilities. We offer our customers flexible manufacturing solutions throughout the life cycle of their products. These solutions provide accelerated time-to-market, time-to-volume production, and reduced production costs. As a result of working closely with our customers and responding promptly to their needs, we have become an integral part of their operations.

Our Industry

The EMS industry experienced rapid change and growth over most of the past decade as an increasing number of OEMs outsourced their manufacturing requirements. In mid-2001, the industry’s revenue declined as a result of significant cut backs in its customers’ production requirements, which was consistent with the overall global economic downturn. Nonetheless, OEMs have continued to turn to outsourcing in order to reduce product cost; achieve accelerated time-to-market and time-to-volume production; access advanced design and manufacturing technologies; improve inventory management and purchasing power; and reduce their capital investment in manufacturing resources. This enables OEMs to concentrate on what they believe to be their core strengths, such as new product definition, marketing and sales. We believe further growth opportunities exist for EMS providers to penetrate the worldwide electronics markets.

Our Strategy

Our goal is to be the EMS outsourcing provider of choice to leading OEMs in the electronics industry that we perceive from time to time to offer the greatest potential for growth. To meet this goal, we have implemented the following strategies:

· Maintain and Develop Close, Long-Term Relationships with Customers. Our core strategy is to maintain and establish long-term relationships with leading OEMs in expanding industries by becoming an integral part of our customers’ manufacturing operations. To accomplish this, we work closely with our customers throughout the design, manufacturing and distribution process, and we offer flexible and responsive services. We believe that we develop stronger customer relationships by relying on our local management teams that respond to frequently changing customer design specifications and production requirements.

· Focus on High-End Products in Growth Industries. EMS providers produce products for a wide range of OEMs in different industries, such as consumer electronics, Internet-focused businesses and information technology equipment. The product scope ranges from easy to assemble, low-cost high-volume products targeted for the consumer market to complicated state-of-the-art, mission critical electronic hardware targeted for military, medical and other high-end computer use. Similarly, OEMs’ customers range from consumer-oriented companies that compete primarily on price and redesign their products every year to manufacturers of high-end telecommunications equipment and computer and related products for business enterprises that compete on technology and quality. We currently offer state-of-the-art products for industry leaders who require specialized engineering design and production services, as well as high volume manufacturing capabilities to our customer base. Our ability to offer both of these types of services enables us to expand our business relationships.

4

· Deliver Complete High and Low Volume Manufacturing Solutions Globally. We believe OEMs are increasingly requiring a wide range of specialized engineering and manufacturing services from EMS providers in order to reduce costs and accelerate their time-to-market and time-to-volume production. Building on our integrated engineering and manufacturing capabilities, we offer services from initial product design and test to final product assembly and distribution to OEM customers. Our systems integration assembly and direct order fulfillment services allow our customers to reduce product cost and risk of product obsolescence by reducing their total work-in-process and finished goods inventory. These services are available at many of our manufacturing locations. We also offer our customers high volume production in low cost regions of the world, such as Brazil, China, Mexico, Romania and Thailand. These full service capabilities allow us to offer customers the flexibility to move quickly from design and initial product introduction to production and distribution. We offer our customers the opportunity to combine the benefits of low cost manufacturing (for the portions of their products or systems that can benefit from the use of these geographic areas) with the benefits and capabilities of our higher complexity support of systems integration in Asia, Europe or the United States.

· Leverage Advanced Technological Capabilities. In addition to traditional strengths in manufacturing large, complex high-density printed circuit boards we offer customers advanced design, technology and manufacturing solutions for their primary products. We provide this engineering expertise through our design capabilities in each of our facilities, and in our design centers. We believe our capabilities help our customers improve product performance and reduce costs.

· Continue to Seek Cost Savings and Efficiency Improvements. We seek to optimize our facilities to provide cost-efficient services for our customers. We provide operations in lower cost locations, including Brazil, China, Mexico, Romania and Thailand, and we continue to expand our presence in these lower cost locations to meet the needs of our customers.

· Continue Our Global Expansion. A network of strategically positioned facilities can reduce costs, simplify and shorten an OEM’s supply chain and thus reduce the time it takes to bring product to market. We are committed to geographic expansion in order to support our customers with cost-effective and timely delivery of quality products and services worldwide. Our acquisition of facilities in Romania and the Netherlands has expanded our service scope to provide a global manufacturing solution to our customers through our 24 facilities in nine countries located in Brazil, China, Ireland, Mexico, the Netherlands, Romania, Singapore, Thailand and the United States.

· Pursue Strategic Acquisitions. Our capabilities have continued to grow through acquisitions and we will continue to selectively seek acquisition opportunities. Our acquisitions, including the Pemstar acquisition, have enhanced our business in the following ways:

· expanded geographic presence;

· enhanced customer growth opportunities;

· developed strategic relationships;

· broadened service offerings;

· diversified into new market sectors; and

· added experienced management teams.

We believe that growth by selective acquisitions is critical for achieving the scale, flexibility and breadth of customer services required to remain competitive in the EMS industry.

5

Services We Provide

Engineering. We coordinate and integrate our design, prototype and other engineering capabilities. Through this approach, we provide a broad range of engineering services, including dedicated production lines for prototypes. These services strengthen our relationships with manufacturing customers and attract new customers requiring specialized engineering services.

To assist customers with initial design, we offer computer assisted engineering, computer aided design, engineering for manufacturability, circuit board layout and test development. We also provide industrial design and tooling for product manufacturing. After product design, we offer quickturn prototyping and we assist with the transition to volume production. By participating in product design and prototype development, we can reduce manufacturing costs and accelerate the cycle from product introduction to large-scale production.

Supply Chain Management. Supply chain management consists of planning, purchasing, expediting and warehousing components and materials. Our inventory management and volume procurement capabilities contribute to cost reductions and reduce total cycle time. Our materials strategy is focused on leveraging our procurement volume while providing local execution for maximum flexibility at the division level. In addition, our systems integration facilities have developed material processes required to support system integration operations.

Assembly and Manufacturing. Our manufacturing and assembly operations include printed circuit boards and subsystem assembly, box build and systems integration, the process of integrating sub-systems and downloading software before producing a fully configured product. We sometimes purchase the printed circuit boards used in our assembly operations from third parties. A substantial portion of our sales is derived from the manufacture and assembly of complete products. We employ various inventory management techniques, such as just-in-time, ship-to-stock and autoreplenish, which are programs designed to ensure timely, convenient and efficient delivery of assembled products to our customers. As OEMs seek greater functionality in smaller products, they increasingly require more sophisticated manufacturing technologies and processes. Our investment in advanced manufacturing equipment and our experience in innovative packaging and interconnect technologies enable us to offer a variety of advanced manufacturing solutions. These packaging and interconnect technologies include:

· chip scale packaging, the part of semiconductor manufacturing in which the semiconductor die is bonded and sealed into a ceramic or plastic package which physically protects the semiconductor device; and

· ball grid array, a method of attaching components to a printed circuit board through balls of solder that are arranged in a grid pattern.

Testing. We offer computer-aided testing of assembled printed circuit boards, subsystems and systems, which contributes significantly to our ability to consistently deliver high-quality products. We work with customers to develop product-specific test strategies. Our test capabilities include manufacturing defect analysis, in-circuit tests to assess the circuitry of the board and functional tests to confirm that the board or assembly operates in accordance with its final design and manufacturing specifications. We either custom design test equipment and software ourselves or use test equipment and software provided by our customers. In addition, we provide environmental stress tests of assemblies of boards or systems.

6

Final System Assembly and Test. We provide final system assembly and test in which assemblies and modules are combined to form complete, finished products. We often integrate printed circuit board assemblies manufactured by us with enclosures, electronic and mechanical subassemblies, cables and memory modules. We assemble systems to a specific customer order and we also build to standard configurations. The complex, finished products that we produce typically require extensive test protocols. Our test services include both functional and environmental tests. We also test products for conformity to applicable industry, product integrity and regulatory standards. Our test engineering expertise enables us to design functional test processes that assess critical performance elements, including hardware, software and reliability. By incorporating rigorous test processes into the manufacturing process, we can help to assure customers that their products will function as designed. We provide direct order fulfillment services shipping completed systems directly to the end consumer.

Distribution. We offer our customers flexible, just-in-time delivery programs allowing product shipments to be closely coordinated with customers’ inventory requirements. Increasingly, we ship products directly into customers’ distribution channels or directly to the end-user. We believe that this service can provide our customers with a more comprehensive solution and enable them to be more responsive to market demands.

Direct Order Fulfillment. We provide direct order fulfillment for certain of our OEM customers. Direct order fulfillment involves receiving customer orders, configuring products to quickly fill the orders and delivering the products either to the OEM, a distribution channel or directly to the end customer. We manage our direct order fulfillment processes using a core set of common systems and processes that receive order information from the customer and provide comprehensive supply chain management, including procurement and production planning. These systems and processes enable us to process orders for multiple system configurations, and varying production quantities, including single units. Our direct order fulfillment services include build-to-order (BTO) and configure-to-order (CTO) capabilities. BTO involves building a system having the particular configuration ordered by the OEM customer. CTO involves configuring systems to an end customer’s order. The end customer typically places this order by choosing from a variety of possible system configurations and options. We are capable of meeting a 20 to 48 hour turn-around-time for BTO and CTO by using advanced manufacturing processes. We support our direct order fulfillment services with logistics that include delivery of parts and assemblies to the final assembly site, distribution and shipment of finished systems, and processing of customer returns.

Marketing and Customers

We market our services through a direct sales force and independent marketing representatives. In addition, our divisional and executive management teams are an integral part of our sales and marketing teams. We generally enter into supply arrangements with our customers. These arrangements, similar to purchase orders, generally govern the conduct of business between our customer and ourselves relating to, among other things, the manufacture of products which in many cases were previously produced by the customer itself. Such arrangements generally identify the specific products to be manufactured, quality and production requirements, product pricing and materials management. There can be no assurance that at any time these arrangements will remain in effect or be renewed.

Our key customer accounts are supported by a dedicated team, including a global account manager who is directly responsible for account management. Global account managers coordinate activities across divisions to effectively satisfy customer requirements and have direct access to our executive management to quickly address customer concerns. Local customer account teams further support the global teams and are linked by a comprehensive communications and information management infrastructure. In addition, our executive management, including our chief executive officer, Cary Fu, and our president, Gayla Delly, are heavily involved in customer relations and devote significant attention to broadening existing, and developing new, customer relationships.

7

The following table sets forth the percentages of our sales by industry for 2006, 2005 and 2004.

| | 2006 | | 2005 | | 2004 | |

Computers & related products for business enterprises | | 58 | % | 56 | % | 58 | % |

Medical devices | | 13 | | 12 | | 9 | |

Telecommunication equipment | | 12 | | 14 | | 13 | |

Industrial control equipment | | 11 | | 12 | | 12 | |

Testing & instrumentation products | | 6 | | 6 | | 8 | |

A substantial percentage of our sales have been made to a small number of customers, and the loss of a major customer, if not replaced, would adversely affect us. During 2006, our largest customer, Sun Microsystems, Inc., represented 39% of our total sales, an increase from 30% of our sales in 2005. Sales to our two largest customers increased to $1.4 billion in 2006 from $997.8 million in 2005, an increase of 37%. Looking forward to 2007, we anticipate that revenues from our top customer will decline by approximately 25% of this customer’s 2006 revenues due to maturing products and second sourcing activity for certain products. Our future sales are dependent on the success of our customers, some of which operate in businesses associated with rapid technological change and consequent product obsolescence. Developments adverse to our major customers or their products, or the failure of a major customer to pay for components or services, could have an adverse effect on us.

Suppliers

We maintain a network of suppliers of components and other materials used in our operations. We procure components when a purchase order or forecast is received from a customer and occasionally utilize components or other materials for which a supplier is the single source of supply. If any of these single source suppliers were to be unable to provide these materials, a shortage of these components could temporarily interrupt our operations and lower our profits until such time as an alternate component could be identified and qualified for use. Although we experience component shortages and longer lead times for various components from time to time, we have generally been able to reduce the impact of the component shortages by working with customers to reschedule deliveries, by working with suppliers to provide the needed components using just-in-time inventory programs, or by purchasing components at somewhat higher prices from distributors, rather than directly from manufacturers. In addition, by developing long-term relationships with suppliers, we have been better able to minimize the effects of component shortages compared to manufacturers without such relationships. These procedures reduce, but do not eliminate, our inventory risk.

Backlog

We had a backlog of approximately $1.9 billion at December 31, 2006, as compared to the 2005 year-end backlog of $1.7 billion. Backlog consists of purchase orders received, including, in some instances, forecast requirements released for production under customer contracts. The increase in backlog is attributable to the organic growth of our business. Although we expect to fill substantially all of our year-end backlog during 2007, we currently do not have long-term agreements with all of our customers and customer orders can be canceled, changed or delayed by customers. The timely replacement of canceled, changed or delayed orders with orders from new customers cannot be assured, nor can there be any assurance that any of our current customers will continue to utilize our services. Because of these factors, our backlog is not a meaningful indicator of future financial results.

8

Competition

The electronics manufacturing services we provide are available from many independent sources as well as from the in-house manufacturing capabilities of current and potential customers. Our competitors include Celestica, Inc., Flextronics International Ltd., Hon Hai Precision Industry Co., Ltd., Jabil Circuit, Inc., Sanmina-SCI Corporation and Solectron Corporation, who may be more established in the industry and have substantially greater financial, manufacturing or marketing resources than we do. We believe that the principal competitive factors in our targeted markets are engineering capabilities, product quality, flexibility, cost and timeliness in responding to design and schedule changes, reliability in meeting product delivery schedules, pricing, technological sophistication and geographic location.

In addition, in recent years, original design manufacturers (ODMs) that provide design and manufacturing services to OEMs have significantly increased their share of outsourced manufacturing services provided to OEMs in markets such as notebook and desktop computers, personal computer motherboards, and consumer electronic products. Competition from ODMs may increase if our business in these markets grows or if ODMs expand further into or beyond these markets.

Governmental Regulation

Our operations, and the operations of businesses that we acquire, are subject to certain foreign, federal, state and local regulatory requirements relating to security clearance, environmental, waste management, and health and safety matters. We believe we operate in substantial compliance with all applicable requirements. However, material costs and liabilities may arise from these requirements or from new, modified or more stringent requirements, which could affect our earnings and competitive position. In addition, our past, current and future operations, and those of businesses we acquire, may give rise to claims of exposure by employees or the public or to other claims or liabilities relating to environmental, waste management or health and safety concerns.

We periodically generate and temporarily handle limited amounts of materials that are considered hazardous waste under applicable law. We contract for the off-site disposal of these materials and have implemented a waste management program to address related regulatory issues.

Employees

As of December 31, 2006, we employed 9,548 people, of whom 7,142 were engaged in manufacturing and operations, 1,110 in materials control and procurement, 609 in design and development, 268 in marketing and sales, and 419 in administration. None of our domestic employees are represented by a labor union. In certain international locations, our employees are represented by labor unions and by works councils. Some European countries also often have mandatory legal provisions regarding terms of employment, severance compensation and other conditions of employment that are more restrictive than U.S. laws. We have never experienced a strike or similar work stoppage and we believe that our employee relations are satisfactory.

9

Segments and International Operations

With the acquisition of Pemstar, Benchmark has 24 manufacturing facilities in the Americas, Europe, and Asia regions to serve its customers. Benchmark is operated and managed geographically and management evaluates performance and allocates Benchmark’s resources on a geographic basis. We currently operate outside the United States in Brazil, China, Ireland, Mexico, the Netherlands, Romania, Singapore and Thailand. During 2006 and 2005, 37% and 35%, respectively, of our sales were from our international operations. The increase in the percentage of international sales for 2006 as compared to 2005 primarily reflects the additional sales resulting from the operation of the facilities in Thailand, including the Thailand systems integration facility which began operations in August 2005. As a result of continuous customer demand overseas, we expect foreign sales to continue to increase. Our foreign sales and operations are subject to risk of doing business abroad, including fluctuations in the value of currency, export duties, import controls and trade barriers, including stoppages, longer payment cycles, greater difficulty in accounts receivable collection, burdens of complying with a wide variety of foreign laws and, in certain parts of the world, political instability. While, to date, these factors have not had a material adverse effect on Benchmark’s results of operations, we can make no assurances that there will not be an adverse impact in the future. See Note 8 and Note 12 of Notes to Consolidated Financial Statements in Item 8 of this report for segment and geographical information.

Available Information

Our internet address is www.bench.com. We make available free of charge through our internet website our filings with the Securities and Exchange Commission (SEC), including our annual reports on Form 10—K, quarterly reports on Form 10—Q, current reports on Form 8—K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after electronically filing such material with, or furnishing it to, the SEC. All reports we file with the SEC are also available free of charge via EDGAR through the SEC’s website at www.sec.gov or to read and copy at the SEC Public Reference Room located at 400 F Street, N.E., Washington, D.C. 20549. You can obtain information on the operation of the Public Reference Room by called the SEC at 1-800-SEC-0330.

Item 1A. Risk Factors

The loss of a major customer would adversely affect us.

A substantial percentage of our sales have been made to a small number of customers, and the loss of a major customer, if not replaced, would adversely affect us. During 2006, our largest customer represented 39% of our sales. Looking forward to 2007, we anticipate that revenues from our top customer will decline by approximately 25% of this customer’s 2006 revenues due to maturing products and second sourcing activity for certain products. Our future sales are dependent on the success of our customers, some of which operate in businesses associated with rapid technological change and consequent product obsolescence. Developments adverse to our major customers or their products, or the failure of a major customer to pay for components or services, could have an adverse effect on us.

We expect to continue to depend on the sales from our largest customers and any material delay, cancellation or reduction of orders from these or other significant customers would have a material adverse effect on our results of operations. In addition, we generate significant accounts receivables in connection with providing manufacturing services to our customers. If one or more of our customers were to become insolvent or otherwise unable to pay for the manufacturing services provided by us, our operating results and financial condition would be adversely affected.

10

We are dependent on the success of our customers.

We are dependent on the continued growth, viability and financial stability of our customers. Our customers are original equipment manufacturers of:

· computers and related products for business enterprises;

· medical devices;

· industrial control equipment;

· testing and instrumentation products; and

· telecommunication equipment.

Often, these industries are subject to rapid technological change, vigorous competition and short product life cycles. When our customers are adversely affected by these factors, we may be similarly affected.

We operate in a highly competitive industry.

We compete against many providers of electronics manufacturing services. Certain of our competitors have substantially greater resources and more geographically diversified international operations than we do. Our competitors include large independent manufacturers such as Celestica, Inc., Flextronics International Ltd., Hon Hai Precision Industry Co., Ltd., Jabil Circuit, Inc., Sanmina-SCI Corporation and Solectron Corporation. In addition, we may in the future encounter competition from other large electronic manufacturers that are selling, or may begin to sell, electronics manufacturing services.

We also face competition from the manufacturing operations of our current and future customers, who are continually evaluating the merits of manufacturing products internally against the advantages of outsourcing to electronics manufacturing services providers. In addition, in recent years, ODMs that provide design and manufacturing services to OEMs, have significantly increased their share of outsourced manufacturing services provided to OEMs in several markets, such as notebook and desktop computers, personal computer motherboards, and consumer electronic products. Competition from ODMs may increase if our business in these markets grows or if ODMs expand further into or beyond these markets.

During periods of recession in the electronics industry, our competitive advantages in the areas of quick turnaround manufacturing and responsive customer service may be of reduced importance to electronics OEMs, who may become more price sensitive. We may also be at a competitive disadvantage with respect to price when compared to manufacturers with lower cost structures, particularly those with more offshore facilities located where labor and other costs are lower.

We experience intense competition, which can intensify further as more companies enter the markets in which we operate, as existing competitors expand capacity and as the industry consolidates. The availability of excess manufacturing capacity at many of our competitors creates intense pricing and competitive pressure on the EMS industry as a whole and Benchmark in particular. To compete effectively, we must continue to provide technologically advanced manufacturing services, maintain strict quality standards, respond flexibly and rapidly to customers’ design and schedule changes and deliver products globally on a reliable basis at competitive prices. Our inability to do so could have an adverse effect on us.

11

The integration of Pemstar and other acquired operations may pose difficulties for us.

Our capabilities have continued to grow through acquisitions and we may pursue additional acquisitions over time. These acquisitions involve risks, including:

· integration and management of the operations;

· retention of key personnel;

· integration of purchasing operations and information systems;

· retention of the customer base of acquired businesses;

· management of an increasingly larger and more geographically disparate business; and

· diversion of management’s attention from other ongoing business concerns.

Our profitability will suffer if we are unable to successfully integrate the Pemstar acquisition and manage any future acquisitions that we might pursue, or if we do not achieve sufficient revenue to offset the increased expenses associated with these acquisitions.

Pemstar has a history of unprofitable operations.

Pemstar has incurred a net loss from continuing operations of $20.9 million during its fiscal year ended March 31, 2006 and had accumulated losses of $162.1 million as of March 31, 2006. Prior to our acquisition of Pemstar, Pemstar management took a number of actions intended to reduce its fixed and other costs and reverse its history of unprofitable operations. As a result of the actions taken during its fiscal year 2006, Pemstar incurred restructuring and related charges of $10.5 million for that year. Subsequent to our acquisition of Pemstar on January 8, 2007, we have implemented organizational changes, initiated overhead reduction efforts and streamlined the corporate structure. We cannot assure you that these actions will be sufficient to make the operations acquired from Pemstar profitable; therefore the operations acquired may continue to sustain losses.

We may experience fluctuations in quarterly results.

Our quarterly results may vary significantly depending on various factors, many of which are beyond our control. These factors include:

· the volume of customer orders relative to our capacity;

· customer introduction and market acceptance of new products;

· changes in demand for customer products;

· pricing and other competitive pressures;

· the timing of our expenditures in anticipation of future orders;

· our effectiveness in managing manufacturing processes;

· changes in cost and availability of labor and components;

· changes in our product mix;

· changes in economic conditions; and

· local factors and events that may affect our production volume, such as local holidays.

Additionally, as is the case with many high technology companies, a significant portion of our shipments typically occurs in the last few weeks of a quarter. As a result, our sales may shift from one quarter to the next, having a significant effect on reported results.

12

Most of our customers do not commit to long-term production schedules, which makes it difficult for us to schedule production and achieve maximum efficiency of our manufacturing capacity.

The volume and timing of sales to our customers may vary due to:

· variation in demand for our customers’ products;

· our customers’ attempts to manage their inventory;

· electronic design changes;

· changes in our customers’ manufacturing strategy; and

· acquisitions of or consolidations among customers.

Due in part to these factors, most of our customers do not commit to firm production schedules for more than one quarter in advance. Our inability to forecast the level of customer orders with certainty makes it difficult to schedule production and maximize utilization of manufacturing capacity. In the past, we have been required to increase staffing and other expenses in order to meet the anticipated demand of our customers. Anticipated orders from many of our customers have, in the past, failed to materialize or delivery schedules have been deferred as a result of changes in our customers’ business needs, thereby adversely affecting our results of operations. On other occasions, our customers have required rapid increases in production, which have placed an excessive burden on our resources. Such customer order fluctuations and deferrals have had a material adverse effect on us in the past, and we may experience such effects in the future. A business downturn resulting from any of these external factors could have a material adverse effect on our operating income.

Our customers may cancel their orders, change production quantities, delay production or change their sourcing strategy.

EMS providers must provide increasingly rapid product turnaround for their customers. We generally do not obtain firm, long-term purchase commitments from our customers and we continue to experience reduced lead-times in customer orders. Customers may cancel their orders, change production quantities, delay production or change their sourcing strategy for a number of reasons. The success of our customers’ products in the market affects our business. Cancellations, reductions, delays or changes in their sourcing strategy by a significant customer or by a group of customers could negatively impact our operating income.

In addition, we make significant decisions, including determining the levels of business that we will seek and accept, production schedules, component procurement commitments, personnel needs and other resource requirements, based on our estimate of customer requirements. The short-term nature of our customers’ commitments and the possibility of rapid changes in demand for their products reduces our ability to accurately estimate the future requirements of those customers.

On occasion, customers may require rapid increases in production, which can stress our resources and reduce operating margins. In addition, because many of our costs and operating expenses are relatively fixed, a reduction in customer demand can harm our gross profits and operating results.

13

Start-up costs and inefficiencies related to new or transferred programs can adversely affect our operating results and such costs may not be recoverable if such new programs or transferred programs are cancelled.

Start-up costs, the management of labor and equipment resources in connection with the establishment of new programs and new customer relationships, and the need to estimate required resources in advance can adversely affect our gross margins and operating results. These factors are particularly evident in the early stages of the life cycle of new products and new programs or program transfers and in the opening of new facilities such as our systems integration facility in Ayudhaya, Thailand. The effects of these start-up costs and inefficiencies can also occur when we re-open inactive facilities, such as our facility in Korat, Thailand, which began production in the third quarter of 2004. These factors also affect our ability to efficiently use labor and equipment. Due to the improved economy and our increased marketing efforts, we are currently managing a number of new programs and are expanding our capacity in Suzhou, China. Consequently, our exposure to these factors has increased. In addition, if any of these new programs or new customer relationships were terminated, our operating results could be harmed, particularly in the short term. We may not be able to recoup these start-up costs or replace anticipated new program revenues.

Complications with the implementation of our new information systems could disrupt our operations and cause unanticipated increases in our costs.

We have completed the installation of an Enterprise Resource Planning system in many of our manufacturing sites and in our corporate location. Complications with the implementation of these information systems in the remaining plants to replace the existing Manufacturing Resource Planning systems and financial information systems used by these sites could result in material adverse consequences, including disruption of operations, loss of information and unanticipated increases in cost.

We are exposed to general economic conditions, which could have a material adverse impact on our business, operating results and financial condition.

Our business is cyclical and has experienced economic and industry downturns. If the economic conditions and demand for our customers’ products deteriorate, we may experience a material adverse impact on our business, operating results and financial condition.

In cases where the evidence suggests a customer may not be able to satisfy its obligation to us, we set up reserves in an amount we determine appropriate for the perceived risk. There can be no assurance that our reserves will be adequate to meet this risk. If the financial condition of our customers were to deteriorate, resulting in an impairment of their ability to make payments, additional receivable and inventory reserves may be required.

We may encounter significant delays or defaults in payments owed to us by customers for products we have manufactured or components that are unique to particular customers.

We structure our agreements with customers to mitigate our risks related to obsolete or unsold inventory. However, enforcement of these contracts may result in material expense and delay in payment for inventory. If any of our significant customers become unable or unwilling to purchase such inventory, our business may be materially harmed.

14

We may be affected by consolidation in the electronics industry.

As a result of the current economic climate, consolidation in the electronics industry may increase. Consolidation in the electronics industry could result in an increase in excess manufacturing capacity as companies seek to close plants or take other steps to increase efficiencies and realize synergies of mergers. The availability of excess manufacturing capacity could create increased pricing and competitive pressures for the electronics manufacturing services industry as a whole and our business in particular. In addition, consolidation could also result in an increasing number of very large electronics companies offering products in multiple sectors of the electronics industry. The growth of these large companies, with significant purchasing and marketing power, could also result in increased pricing and competitive pressures for us. Accordingly, industry consolidation could harm our business.

We are subject to the risk of increased taxes.

We base our tax position upon the anticipated nature and conduct of our business and upon our understanding of the tax laws of the various countries in which we have assets or conduct activities. Our tax position, however, is subject to review and possible challenge by taxing authorities and to possible changes in law. We cannot determine in advance the extent to which some jurisdictions may assess additional tax or interest and penalties on such additional taxes.

Several countries in which we are located allow for tax holidays or provide other tax incentives to attract and retain business. We have obtained holidays or other incentives where available. Our taxes could increase if certain tax holidays or incentives are retracted, or if they are not renewed upon expiration, or tax rates applicable to us in such jurisdictions are otherwise increased. In addition, further acquisitions may cause our effective tax rate to increase.

We are exposed to intangible asset risk.

We have recorded goodwill in connection with business acquisitions. We are required to perform goodwill impairment tests at least on an annual basis and whenever events or circumstances indicate that the carrying value may not be recoverable from estimated future cash flows. As a result of our annual and other periodic evaluations, we may determine that the intangible asset values need to be written down to their fair values, which could result in material charges that could be adverse to our operating results and financial position.

There are inherent uncertainties involved in estimates, judgments and assumptions used in the preparation of financial statements in accordance with US GAAP. Any changes in estimates, judgments and assumptions could have a material adverse effect on our business, financial position and results of operations.

The consolidated financial statements included in the periodic reports we file with the SEC are prepared in accordance with accounting principles generally accepted in the United States (US GAAP). The preparation of financial statements in accordance with US GAAP involves making estimates, judgments and assumptions that affect reported amounts of assets (including intangible assets), liabilities and related reserves, revenues, expenses and income. Estimates, judgments and assumptions are inherently subject to change in the future, and any such changes could result in corresponding changes to the amounts of assets, liabilities, revenues, expenses and income. Any such changes could have a material adverse effect on our financial position and results of operations.

15

Our international operations may be subject to certain risks.

We currently operate outside the United States in Brazil, China, Ireland, Mexico, the Netherlands, Romania, Singapore and Thailand. During 2006, 2005 and 2004, 37%, 35% and 30%, respectively, of our sales were from our international operations. These international operations may be subject to a number of risks, including:

· difficulties in staffing and managing foreign operations;

· political and economic instability;

· unexpected changes in regulatory requirements and laws;

· longer customer payment cycles and difficulty collecting accounts receivable;

· export duties, import controls and trade barriers (including quotas);

· governmental restrictions on the transfer of funds;

· burdens of complying with a wide variety of foreign laws and labor practices;

· fluctuations in currency exchange rates, which could affect component costs, local payroll, utility and other expenses; and

· inability to utilize net operating losses incurred by our foreign operations to reduce our U.S. income taxes.

In addition, several of the countries where we operate have emerging or developing economies, which may be subject to greater currency volatility, negative growth, high inflation, limited availability of foreign exchange and other risks. These factors may harm our results of operations, and any measures that we may implement to reduce the effect of volatile currencies and other risks of our international operations may not be effective. In our experience, entry into new international markets requires considerable management time as well as start-up expenses for market development, hiring and establishing office facilities before any significant revenues are generated. As a result, initial operations in a new market may operate at low margins or may be unprofitable.

We cannot assure you that our international operations will contribute positively to our business, financial conditions or results of operations.

We are involved in various legal proceedings.

In the past, we have been notified of claims relating to various matters including intellectual property rights, contractual matters or other issues arising in the ordinary course of business. In the event of such a claim, we may be required to spend a significant amount of money to defend or otherwise address the claim. Any litigation, even where a claim is without merit, could result in substantial costs and diversion of resources. Accordingly, the resolution or adjudication of such disputes, even those encountered in the ordinary course of business, could have a material adverse effect on our business, consolidated financial conditions and results of operations. See Note 14 and 18 to the consolidated financial statements in Item 8 of this report.

Our success will continue to depend to a significant extent on our executives.

We depend significantly on certain key executives, including, but not limited to, Cary T. Fu, Donald F. Adam, Gayla J. Delly and Steven A. Barton. The unexpected loss of the services of any one of these executive officers would have an adverse effect on us.

16

We must maintain our technological and manufacturing process expertise.

The market for our manufacturing services is characterized by rapidly changing technology and continuing process development. We are continually evaluating the advantages and feasibility of new manufacturing processes. We believe that our future success will depend upon our ability to develop and provide manufacturing services which meet our customers’ changing needs. This requires that we maintain technological leadership and successfully anticipate or respond to technological changes in manufacturing processes on a cost-effective and timely basis. We cannot assure you that our process development efforts will be successful.

Environmental laws may expose us to financial liability and restrictions on operations.

We are subject to a variety of federal, state, local and foreign environmental laws and regulations relating to environmental, waste management, and health and safety concerns, including the handling, storage, discharge and disposal of hazardous materials used in or derived from our manufacturing processes. If we or companies we acquire have failed or fail in the future to comply with such laws and regulations, then we could incur liabilities and fines and our operations could be suspended. Such laws and regulations could also restrict our ability to modify or expand our facilities, could require us to acquire costly equipment, or could impose other significant expenditures. In addition, our operations may give rise to claims of property contamination or human exposure to hazardous chemicals or conditions.

Shortages or price increases of components specified by our customers would delay shipments and adversely affect our profitability.

Substantially all of our sales are derived from electronics manufacturing services in which we purchase components specified by our customers. In the past, supply shortages have substantially curtailed production of all assemblies using a particular component. In addition, industry-wide shortages of electronic components, particularly of memory and logic devices, have occurred. If shortages of these components occur or if components received are defective, we may be forced to delay shipments, which could have an adverse effect on our profit margins. Because of the continued increase in demand for surface mount components, we anticipate component shortages and longer lead times for certain components to occur from time to time. Also, we typically bear the risk of component price increases that occur between periodic repricings during the term of a customer contract. Accordingly, certain component price increases could adversely affect our gross profit margins.

Our stock price is volatile.

Our common shares have experienced significant price volatility, and such volatility may continue in the future. The price of our common shares could fluctuate widely in response to a range of factors, including variations in our reported financial results and changing conditions in the economy in general or in our industry in particular. In addition, stock markets generally experience significant price and volume volatility from time to time which may affect the market price of our common shares for reasons unrelated to our performance.

Provisions in our shareholder rights plan, our charter documents and state law may make it harder for others to obtain control of our company even though some shareholders might consider such a development to be favorable.

Our shareholder rights plan, provisions of our amended and restated articles of incorporation and the Texas Business Corporation Act may delay, inhibit or prevent someone from gaining control of our company through a tender offer, business combination, proxy contest or some other method. These provisions include:

· a “poison pill” shareholder rights plan;

· a statutory restriction on the ability of shareholders to take action by less than unanimous written consent; and

· a statutory restriction on business combinations with some types of interested shareholders.

17

Impact of Governmental Regulation

Our worldwide operations are subject to local laws and regulations. Of particular note at this time are two European Union (EU) directives, the first of which is the Restriction of Certain Hazardous Substances Directive (RoHS). This directive restricts the distribution of products within the EU containing certain substances, including lead. While the enabling legislation of most EU member countries has not yet been enacted, and the implementing details not yet known, it appears we will not be able to sell non-RoHS compliant products to most customers who intend to sell their finished goods into the EU after the effective date. In addition, industry analysts indicate that similar legislation in the U.S. and Asia will eventually follow.

The second directive is the Waste Electrical and Electronic Equipment Directive under which a manufacturer or importer will be required, at its own cost, to take back and recycle all of the products it manufactured in or imported into the EU.

Both directives will affect the worldwide electronics, and electronics components, industries as a whole, and collaborative efforts among suppliers, distributors and customers to develop compliant processes have begun. If we or our customers fail in the future to comply with such laws and regulations, then we could incur liabilities and fines and our operations could be suspended.

The Pemstar acquisition on January 8, 2007 increased our indebtedness.

As a direct result of the Pemstar acquisition, we assumed approximately $86 million of indebtedness. Since the acquisition date of January 8, 2007, this outstanding debt has been reduced by over $60 million. We have the ability to borrow approximately $100 million under our revolving credit line. In addition, we could incur additional indebtedness in the future in the form of bank loans, notes or convertible securities. An increase in the level of our indebtedness, among other things, could:

· make it difficult for us to obtain any necessary financing in the future for other acquisitions, working capital, capital expenditures, debt service requirements or other purposes;

· limit our flexibility in planning for, or reacting to changes in, our business; and

· make us more vulnerable in the event of a downturn in our business.

There can be no assurance that we will be able to meet any future debt service obligations.

We may be exposed to interest rate fluctuations.

We will have exposure to interest rate risk under our variable rate revolving credit facilities to the extent we incur indebtedness under such facilities. These facilities’ interest rates are based on the spread over the bank’s Eurodollar rate or its prime rate.

18

Changes in the securities laws and regulations are likely to increase our costs.

The Sarbanes-Oxley Act of 2002 has required changes in some of our corporate governance, securities disclosure and compliance practices. In response to the requirements of that Act, the Securities and Exchange Commission and the New York Stock Exchange have promulgated new rules on a variety of subjects. Compliance with these new rules has increased our legal and financial and accounting costs, and we expect these increased costs to continue indefinitely. These developments may make it more difficult and more expensive for us to obtain director and officer liability insurance, and we may be forced to accept reduced coverage or incur substantially higher costs to obtain coverage. Likewise, these developments may make it more difficult for us to attract and retain qualified members of our board of directors or qualified executive officers.

Our business may be impacted by geopolitical events.

As a global business, we operate and have customers located in many countries. Geopolitical events such as terrorist acts may effect the overall economic environment and negatively impact the demand for our customers’ products. As a result, customer orders may be lower and our financial results may be adversely affected.

Our business may be impacted by hurricanes, epidemics and other natural disasters.

Hurricanes, epidemics and other natural disasters could negatively impact our business. In some countries in which we operate, such as China and Thailand, potential outbreaks of severe acute respiratory syndrome and/or bird flu could disrupt our manufacturing operations, reduce demand for our customers’ products and increase supply chain costs. Some of our facilities, including our corporate headquarters, are located in areas which may be impacted by hurricanes and/or other natural disasters.

Item 1B. Unresolved Staff Comments

Not applicable.

19

Item 2. Properties

Our customers market numerous products throughout the world and therefore need to access manufacturing services on a global basis. To enhance our EMS offerings, we seek to locate our facilities either near our customers and our customers’ end markets in major centers for the electronics industry or, where appropriate, in lower cost locations. Many of our plants located near customers and their end markets are focused primarily on final system assembly and test, while plants located in lower cost areas are engaged primarily in less complex component and subsystem manufacturing and assembly.

The following chart summarizes our principal manufacturing facilities owned or leased by Benchmark and its subsidiaries:

Location | | Sq. Ft. | | Ownership | |

Almelo, the Netherlands (1) | | 132,000 | | Leased | |

Angleton, Texas | | 109,000 | | Owned | |

Austin, Texas (1) | | 93,000 | | Leased | |

Ayudhaya, Thailand (2) | | 243,000 | | Owned | |

Ayudhaya, Thailand (3) | | 60,000 | | Leased | |

Ayudhaya, Thailand (1) | | 180,000 | | Owned | |

Beaverton, Oregon | | 77,000 | | Leased | |

Brasov, Romania (1) | | 30,000 | | Leased | |

Campinas, Brazil | | 40,000 | | Leased | |

Dublin, Ireland | | 104,000 | | Leased | |

Dunseith, North Dakota (1) | | 47,000 | | Owned | |

Dunseith, North Dakota (1) | | 53,000 | | Leased | |

Guadalajara, Mexico | | 150,000 | | Leased | |

Hudson, New Hampshire | | 170,000 | | Leased | |

Huntsville, Alabama (2) | | 276,000 | | Owned | |

Huntsville, Alabama (3) | | 144,000 | | Leased | |

Korat, Thailand | | 126,000 | | Owned | |

Navan, Ireland (1) | | 26,000 | | Leased | |

Redmond, Washington | | 79,000 | | Leased | |

Rochester, Minnesota (1) | | 260,000 | | Leased | |

Rochester, Minnesota | | 35,000 | | Leased | |

San Jose, California (1) | | 17,000 | | Leased | |

Shenzhen, China (1) | | 141,000 | | Leased | |

Suzhou, China | | 115,000 | | Leased | |

Singapore (1) | | 48,000 | | Leased | |

Singapore (4) | | 8,000 | | Leased | |

Winona, Minnesota | | 199,000 | | Owned | |

| | | | | |

Total | | 2,962,000 | | | |

(1) Facility acquired as of January 8, 2007.

(2) PCBA facility.

(3) Systems integration facility.

(4) Engineering and international procurement facility.

We lease other facilities in Minnesota with a total of 41,000 sq. ft. that house individuals that provide engineering services. We also own facilities in Rangsit, Thailand wit

h a total of 90,000 sq. ft. and in Tianjin, China with a total of 306,000 sq. ft. that are currently not in operation. Our leased facility in Navan, Ireland will be combined into a single facility with our Dublin facility during 2007.

20

Item 3. Legal Proceedings

We are involved in various legal actions arising in the ordinary course of business. In the opinion of management, the ultimate disposition of these matters will not have a material adverse effect on our consolidated financial position or results of operations.

Pemstar is also involved in various legal actions arising in the ordinary course of business. In the opinion of management, the ultimate disposition of such matters will not have a material adverse effect on our consolidated financial position or results of operations.

Currently, Pemstar is subject to the following legal proceedings outside the ordinary course of business.

On June 16, 2005 a putative class action was filed by an individual shareholder against Pemstar and certain of its officers and directors. The lawsuit is pending in the United States District Court for the District Court of Minnesota and is captioned: In re PEMSTAR INC. Securities Litigation, Civil Action No. 05-CV-01182 — JMR/FLN. The lawsuit alleges violations of Section 10(b) and Section 20(a) of the Securities Exchange Act of 1934 and Section 11 of the Securities Act of 1933. An Amended Complaint was filed on November 28, 2005. The plaintiff alleges, in essence, that the defendants defrauded Pemstar’s shareholders by failing to timely disclose the circumstances around the discrepancies in the accounting of the Mexico facility that generated a restatement. The lawsuit also alleges that the registration statement filed by Pemstar in connection with a secondary offering contained false, material misrepresentations. The plaintiff seeks to represent a class of persons who purchased Pemstar stock from January 30, 2003 through and including January 12, 2005. The Amended Complaint does not specify an amount of damages. The Company and the individuals will vigorously defend against the claim and believe the lawsuit is without merit.

On July 26, 2005, an individual who claims to own Pemstar shares filed a derivative action in Olmsted County District Court captioned: Michael Tittle, et al. v. Allen Berning, et al. Civil No. 55-CO-05-003235. An Amended Complaint was filed on November 11, 2005. The lawsuit alleges that Pemstar’s Board of Directors breached their fiduciary duties by allowing circumstances to exist that generated a restatement. The lawsuit includes allegations that the defendants believe have been released as part of the settlement of a prior derivative lawsuit. On February 6, 2007, the Court entered an order and judgment to dismiss the action with prejudice.

Item 4. Submission of Matters to a Vote of Security Holders

No matters were submitted to a vote of security holders during the fourth quarter of 2006.

21

PART II

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

Our common shares are listed on the New York Stock Exchange under the symbol “BHE.” The following table shows the high and low sales prices for our common shares as reported on the New York Stock Exchange for the quarters (or portions thereof) indicated, as adjusted for the March 2006 three-for-two stock split.

| | High | | Low | |

2007 | | | | | |

First quarter (through February 28, 2007) | | $ | 25.26 | | $ | 21.16 | |

2006 | | | | | |

Fourth quarter | | $ | 29.92 | | $ | 23.62 | |

Third quarter | | $ | 27.39 | | $ | 20.95 | |

Second quarter | | $ | 28.90 | | $ | 21.54 | |

First quarter | | $ | 25.95 | | $ | 22.09 | |

2005 | | | | | |

Fourth quarter | | $ | 22.74 | | $ | 18.14 | |

Third quarter | | $ | 22.18 | | $ | 18.39 | |

Second quarter | | $ | 21.59 | | $ | 16.69 | |

First quarter | | $ | 22.97 | | $ | 20.11 | |

The last reported sale price of our common shares on February 28, 2007, as reported by the New York Stock Exchange, was $21.49. There were approximately 763 record holders of our common shares as of February 28, 2007.

We have not paid any cash dividends on our common shares in the past. In addition, our credit facility includes restrictions on the amount of dividends we may pay to shareholders.

22

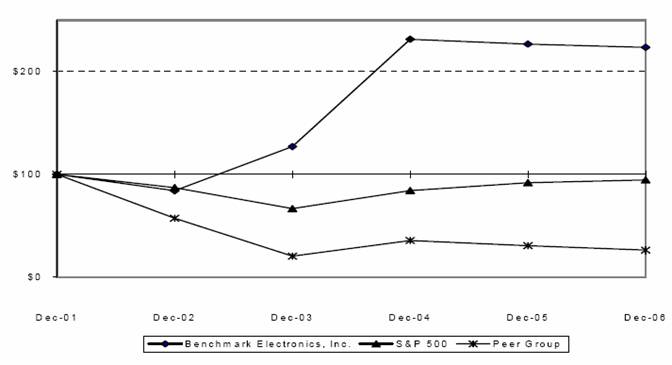

Performance Graph

The following Performance Graph compares the cumulative total shareholder return on our common shares for the five-year period commencing December 31, 2001 and ending December 31, 2006, with the cumulative total return of the Standard & Poor’s 500 Stock Index (which does not include Benchmark), and the Peer Group, which is composed of Celestica Inc., Suntron Corp (formerly EFTC Corp), Flextronics International, Ltd., Jabil Circuit, Inc., Plexus Corp, Sanmina-SCI Corp, and Solectron Corporation. Dividend reinvestment has been assumed.

NOTES: Assumes $100 invested on December 31, 2001 in Benchmark Electronics, Inc. Common Shares, in the S&P 500, and in the Peer Group Index. Reflects month-end dividend reinvestment, and annual reweighting of the Peer Group Index portfolios.

23

Item 6. Selected Financial Data

(in thousands, except per share data) | | Year Ended December 31, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Selected Statements of Income Data | | | | | | | | | | | |

Sales | | $ | 2,907,304 | | $ | 2,257,225 | | $ | 2,001,340 | | $ | 1,839,821 | | $ | 1,630,020 | |

Cost of sales | | 2,707,781 | | 2,095,623 | | 1,847,573 | | 1,689,548 | | 1,505,166 | |

Gross profit | | 199,523 | | 161,602 | | 153,767 | | 150,273 | | 124,854 | |

Selling, general and administrative expenses | | 69,299 | | 62,322 | | 61,108 | | 64,976 | | 64,191 | |

Contract settlement (1) | | — | | — | | — | | (8,108 | ) | — | |

Restructuring charges (2) | | 4,723 | | — | | — | | 2,815 | | — | |

Asset impairments (2) | | — | | — | | — | | — | | 1,608 | |

Income from operations | | 125,501 | | 99,280 | | 92,659 | | 90,590 | | 59,055 | |

Interest expense | | (354 | ) | (330 | ) | (1,705 | ) | (7,714 | ) | (11,385 | ) |

Interest income | | 8,824 | | 7,786 | | 4,516 | | 3,842 | | 4,430 | |

Other income (expense) | | (2,214 | ) | (922 | ) | (1,317 | ) | (3,708 | ) | 2,866 | |

Income tax expense (3) | | (20,080 | ) | (25,225 | ) | (23,162 | ) | (27,574 | ) | (19,073 | ) |

Net income | | $ | 111,677 | | $ | 80,589 | | $ | 70,991 | | $ | 55,436 | | $ | 35,893 | |

Earnings per share: (4) | | | | | | | | | | | |

Basic | | $ | 1.74 | | $ | 1.29 | | $ | 1.15 | | $ | 0.97 | | $ | 0.69 | |

Diluted | | $ | 1.71 | | $ | 1.25 | | $ | 1.11 | | $ | 0.93 | | $ | 0.67 | |

Weighted average number of shares outstanding: | | | | | | | | | | | |

Basic | | 64,306 | | 62,682 | | 61,701 | | 57,186 | | 51,606 | |

Diluted | | 65,121 | | 64,279 | | 63,697 | | 62,148 | | 53,397 | |

(in thousands) | | December 31, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Selected Balance Sheet Data | | | | | | | | | | | |

Working capital | | $ | 760,892 | | $ | 646,363 | | $ | 569,938 | | $ | 465,879 | | $ | 392,373 | |

Total assets | | 1,406,120 | | 1,298,408 | | 1,092,001 | | 1,038,038 | | 932,251 | |

Total debt | | — | | — | | — | | 21,028 | | 137,167 | |

Shareholders’ equity | | $ | 985,022 | | $ | 846,119 | | $ | 751,517 | | $ | 664,325 | | $ | 499,030 | |

(1) During the first quarter of 2003, the Company settled and released various claims arising out of customer manufacturing agreements. In connection with the settlement of these claims, the Company recorded a non-cash gain totaling $8.1 million.

(2) See Note 15 to the Consolidated Financial Statements for a discussion of the restructuring charges occurring in 2006. In connection with the closing of the Scotland facility in the fourth quarter of 2003, the Company recorded $2.8 million in restructuring charges. During 2002, the Company recorded asset impairments of approximately $1.6 million for the write-down of assets held for sale to fair value.

(3) During the first quarter of 2006, the Company recorded a $4.8 million tax benefit for the write-off of the investment in the Leicester, England subsidiary.

(4) See Note 1 to the Consolidated Financial Statements for the basis of computing earnings per share.

24

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

References in this report to “the Company,” “Benchmark,” “we,” or “us” mean Benchmark Electronics, Inc. together with its subsidiaries. The following Management’s Discussion and Analysis of Financial Condition and Results of Operations contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements are identified as any statement that does not relate strictly to historical or current facts. They use words such as “anticipate,” “believe,” “intend,” “plan,” “projection,” “forecast,” “strategy,” “position,” “continue,” “estimate,” “expect,” “may,” “will,” or the negative of those terms or other variations of them or comparable terminology. In particular, statements, express or implied, concerning future operating results or the ability to generate sales, income or cash flow are forward-looking statements. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions, including those discussed under Item 1A of this report. The future results of our operations may differ materially from those expressed in these forward-looking statements. Many of the factors that will determine these results are beyond our ability to control or predict. You should not put undue reliance on any forward-looking statements. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual outcomes may vary materially from those indicated.

The following discussion should be read in conjunction with the Consolidated Financial Statements and Notes thereto in Item 8 of this report.

OVERVIEW

We are in the business of manufacturing electronics and provide our services to original equipment manufacturers (OEMs) of computers and related products for business enterprises, medical devices, industrial control equipment, testing and instrumentation products, and telecommunication equipment. The services that we provide are commonly referred to as electronics manufacturing services (EMS). We offer our customers comprehensive and integrated design and manufacturing services, from initial product design to volume production and direct order fulfillment. We also provide specialized engineering services, including product design, printed circuit board layout, prototyping, and test development. We believe that we have developed strengths in the manufacturing process for large, complex, high-density printed circuit boards as well as the ability to manufacture high and low volume products in lower cost regions such as Brazil, China, Mexico, Romania and Thailand.

As our customers have continued to expand their globalization strategy during the past several years, we have continued to make the necessary changes to align our business operations with our customers’ demand. These changes include, among other activities, moving production between facilities, reducing staff levels, realigning our business processes and reorganizing our management. Restructuring charges associated with these realignment efforts, primarily related to the closure of our Leicester, England and Loveland, Colorado facilities, were approximately $4.7 million (pre-tax) during 2006. During 2007, we will continue to expand our low-cost capacity while realigning and further strengthening our global footprint to support continued business opportunities. We believe that our global manufacturing presence increases our ability to be responsive to our customers’ needs by providing accelerated time-to-market and time-to-volume production of high quality products. These capabilities should enable us to build stronger strategic relationships with our customers and to become a more integral part of their operations. Our customers face challenges in planning, procuring and managing their inventories efficiently due to customer demand fluctuations, product design changes, short product life cycles and component price fluctuations. We employ production management systems to manage their procurement and manufacturing processes in an efficient and cost-effective manner so that, where possible, components arrive on a just-in-time, as-and-when needed basis. We are a significant purchaser of electronic components and other raw materials, and can capitalize on the economies of scale associated with our relationships with suppliers to negotiate price discounts, obtain components and other raw materials that are in short supply, and return excess components. Our expertise in supply chain management and our relationships with suppliers across the supply chain enables us to reduce our customers’ cost of goods sold and inventory exposure.

25

We recognize revenue from the sale of circuit board assemblies, systems and excess inventory when the goods are shipped, title and risk of ownership have passed, the price to the buyer is fixed and determinable and recoverability is reasonably assured. To a lesser extent, revenue is also recognized from non-manufacturing services, such as product design, circuit board layout, and test development. Service related revenues are recognized when the service is rendered and the costs related to these services are expensed as incurred. We assume no significant obligations after product shipment as we typically warrant workmanship only. Therefore our warranty provisions are insignificant.