UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________________

FORM 10-K

___________________________________________

(Mark One)

|

| |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 2, 2013

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 0-18632

THE WET SEAL, INC.

(Exact name of registrant as specified in its charter)

|

| |

| Delaware | 33-0415940 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 26972 Burbank, Foothill Ranch, CA | 92610 |

| (Address of principal executive offices) | (Zip Code) |

(949) 699-3900

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| |

| Title of Each Class | Name of Each Exchange on Which Registered |

| Class A Common Stock, $0.10 par value per share | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a nonaccelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “small reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer: ¨ Accelerated filer: þ Nonaccelerated filer: ¨ Smaller reporting company: ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of voting stock held by nonaffiliates of the registrant as of July 28, 2012 was approximately $235,632,000 based on the closing sale price of $2.72 per share as reported on the NASDAQ Global Select Market on July 27, 2012.

The number of shares outstanding of the registrant’s Class A common stock, par value $0.10 per share, at March 21, 2013, was 89,683,504. There were no shares outstanding of the registrant’s Class B common stock, par value $0.10 per share, at March 21, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

PART III of this Annual Report incorporates information by reference to the registrant’s definitive Proxy Statement for its 2013 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days of February 2, 2013.

THE WET SEAL, INC.

Annual Report on Form 10-K

For the Fiscal Year Ended February 2, 2013

TABLE OF CONTENTS

|

| | |

| | | Page |

| Part I | |

| | | |

| Item 1. | | |

| | | |

| Item 1A. | | |

| | | |

| Item 1B. | | |

| | | |

| Item 2. | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

| | |

| Part II | |

| | | |

| Item 5. | | |

| | | |

| Item 6. | | |

| | | |

| Item 7. | | |

| | | |

| Item 7A. | | |

| | | |

| Item 8. | | |

| | | |

| Item 9. | | |

| | | |

| Item 9A. | | |

| | | |

| Item 9B. | | |

| | |

| Part III | |

| | | |

| Item 10. | | |

| | | |

| Item 11. | | |

| | | |

| Item 12. | | |

| | | |

| Item 13. | | |

| | | |

| Item 14. | | |

| | |

| Part IV | |

| | | |

| Item 15. | | |

| | |

| |

101.INS XBRL Instance Document

101.SCH XBRL Taxonomy Extension Schema Document

101.CAL XBRL Taxonomy Extension Calculation Linkbase Document

101.DEF XBRL Taxonomy Extension Definition Linkbase Document

101.LAB XBRL Taxonomy Extension Label Linkbase Document

101.PRE XBRL Taxonomy Extension Presentation Linkbase Document

PART I

Item 1. Business

Forward-Looking Statements

Certain sections of this Annual Report on Form 10-K (the “Annual Report”), including “Item 1. Business” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contain various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), which represent our expectations or beliefs concerning future events.

Forward-looking statements include statements that are predictive in nature, which depend upon or refer to future events or conditions, and/or which include words such as “believes,” “plans,” “intends,” “anticipates,” “estimates,” “expects,” “may,” “will” or similar expressions. In addition, any statements concerning future financial performance, ongoing strategies or prospects, and possible future actions, which may be provided by our management, are also forward-looking statements. Forward-looking statements are based on current expectations and projections about future events and are subject to risks, uncertainties, and assumptions about our company, economic and market factors, and the industry in which we do business, among other things. These statements are not guarantees of future performance, and we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events, or otherwise.

Actual events and results may differ materially from those expressed or forecasted in forward-looking statements due to a number of factors. Factors that could cause our actual performance, future results and actions to differ materially from any forward-looking statements include, but are not limited to, those discussed in “Item 1A. Risk Factors” below and elsewhere in this Annual Report.

All references to “we,” “our,” “us” and “our company” in this Annual Report mean The Wet Seal, Inc. and its wholly owned subsidiaries. All references in this Annual Report to “fiscal 2013,” “fiscal 2012,” “fiscal 2011,” “fiscal 2010,” “fiscal 2009,” and “fiscal 2008” mean the fiscal year ending February 1, 2014, and the fiscal years ended February 2, 2013, January 28, 2012, January 29, 2011, January 30, 2010, and January 31, 2009, respectively.

Available Information

Our Annual Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports and the proxy statement for our annual meeting of stockholders are made available, free of charge, on our corporate web site, www.wetsealinc.com, as soon as reasonably practicable after such reports have been electronically filed with or furnished to the Securities and Exchange Commission, or the “SEC.” Our Code of Business Ethics and Conduct and our Code of Ethics For Senior Financial Officers are also located within the Corporate Information section of our corporate web site. These documents are also available in print to any stockholder who requests a copy from our Investor Relations department. The public may also read and copy any materials that we have filed with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Members of the general public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, these materials may be obtained at the web site maintained by the SEC at www.sec.gov. The content of our web sites (www.wetsealinc.com, www.wetseal.com, and www.ardenb.com) is not intended to be incorporated by reference in this Annual Report.

General

Incorporated in the State of Delaware in 1990, we are a national multi-channel specialty retailer selling fashion apparel and accessory items designed for female customers aged 13 to 39 years old through our stores and e-commerce websites. As of February 2, 2013, we operated 530 retail stores in 47 states and Puerto Rico.

The names “Wet Seal” and “Arden B” (which are registered in the retail store services and other classes) are trademarks and service marks of our company. Each trademark, trade name, or service mark of any other company appearing in this Annual Report belongs to its respective owner.

Business Segments

We operate two nationwide, primarily mall-based, chains of retail stores under the names “Wet Seal” and “Arden B.” Although the two operating segments have many similarities in their products, production processes, distribution methods, and

regulatory environment, there are differences in most of these areas and distinct differences in their economic characteristics. As a result, we consider these segments to be two distinct reportable segments.

Wet Seal. Wet Seal is a junior apparel brand for girls who seek fashion apparel and accessories at affordable prices, with a target customer age range of 13 to 23 years old. Wet Seal seeks to provide its customer base with a balance of trend right and fashion basic apparel and accessories that are budget-friendly.

Arden B. Arden B is a fashion brand at affordable prices for the contemporary woman. Arden B targets customers aged 21 to 39 years old and seeks to deliver differentiated contemporary fashion, dresses, sportswear separates and accessories for many occasions of the customers’ lifestyles.

We maintain a Web-based store located at www.wetseal.com, offering Wet Seal merchandise comparable to that carried in our stores, to customers over the Internet. We also maintain a Web-based store located at www.ardenb.com, offering Arden B merchandise comparable to that carried in our stores, to customers over the Internet. Our e-commerce stores are designed to serve as an extension of the in-store experience and offer an expanded selection of merchandise, with the goal of growing both e-commerce and in-store sales. We continue to develop our Wet Seal and Arden B websites to increase their effectiveness in marketing our brands. We do not consider our Web-based business to be a distinct reportable segment. The Wet Seal and Arden B reportable segments include, in addition to data from their respective stores, data from their respective e-commerce operations.

See Note 12 - "Segment Reporting," to the consolidated financial statements included in this Annual Report for financial information regarding segment reporting, which information is incorporated herein by reference.

Our Stores

Wet Seal stores average approximately 4,000 square feet in size and in fiscal 2012 had average sales per square foot of $245. As of February 2, 2013, we operated 468 Wet Seal stores. Arden B stores average approximately 3,100 square feet in size and in fiscal 2012 had average sales per square foot of $296. As of February 2, 2013, we operated 62 Arden B stores.

During fiscal 2012, we opened 13 and closed 17 Wet Seal stores and closed 24 Arden B stores.

As we continue to focus on turning around the Wet Seal business, we currently plan to open 19 new Wet Seal stores primarily to replace the approximately14 to18 stores that will be closing upon lease expiration in fiscal 2013, with openings primarily in outlet centers, in which we have experienced relatively strong sales productivity and profitability. We currently plan to close approximately 9 Arden B stores in fiscal 2013 upon lease expiration, as we focus efforts on improving merchandising and marketing strategies in that business. We have approximately 81 existing Wet Seal store leases scheduled to expire in fiscal 2013. Additionally, approximately 67 of these leases expire in the last few days of fiscal 2013, and we expect to remodel or relocate a portion of these Wet Seal stores during fiscal 2014. For the remaining expiring leases, we expect to negotiate new leases that will allow us to remain in all but a small number of these Wet Seal locations.

Our ability to increase the number of Wet Seal stores in the future will depend, in part, on satisfactory cash flows from existing operations, the demand for our merchandise, and our ability to find suitable mall or other locations with acceptable sites and satisfactory lease terms, and general business conditions. Our management does not believe there are significant geographic constraints within the U.S. on the locations of future stores.

Competitive Strengths

Experienced Management Team. We believe our new chief executive officer, Mr. John D. Goodman, and other key members of our management team have the requisite experience and knowledge in the fast fashion retail apparel sector, which will be instrumental in managing our company through its transition back to a fast fashion strategy and driving our company in the next phase of its growth cycle. Mr. Goodman joined our company in January 2013, and prior to joining us he held executive leadership roles at Charlotte Russe, Gap Inc., Levi Strauss & Co. and Bloomingdale's, and most recently served as the executive vice president and chief apparel and home officer at Sears Holdings. Our chief financial officer, Mr. Steven H. Benrubi, served as our corporate controller for over two years prior to his appointment as chief financial officer in September 2007.

Ms. Sharon Hughes, our president and chief merchandise officer for the Arden B division, served as a consultant to our Arden B merchandising team from February 2008 to November 2009, at which time she became an employee of our company in her current role.

Ms. Kim Bajrech and Ms. Debbie Shinn, our SVP General Merchandise Managers for the Wet Seal division, joined us in July 2009, and both have a strong knowledge of fast fashion and a proven history of operating that model successfully at our company.

Merchandising Models at Wet Seal and Arden B are Focused on Fashion at Affordable Prices, Speed and Flexibility. At Wet Seal, we have developed considerable expertise in identifying, sourcing and selling a broad assortment of fast fashion apparel and accessories at competitive prices for our customers. At Arden B we continue to focus on offering unique fashion apparel and accessories for our young contemporary customers and have shifted the merchandising model over recent years to be quicker and more flexible. Additionally, Arden B has been established as a preferred destination for dresses and other social occasion fashion needs for our customers. Our buyers work closely with senior management to evaluate the optimal merchandise assortments and promotion and pricing strategies. A significant portion of our merchandise is sourced domestically or from domestic importers. This sourcing strategy is intended to enable us to ship new merchandise to stores with a high frequency and to react quickly to changing fashion trends. We also take regular markdowns with the objective of ensuring the rapid sale of slow-moving inventory.

Strong Financial Position. In recent years, we have maintained strong levels of cash, cash equivalents and investments, extinguished our debt and repurchased a significant number of shares of our Class A common stock. Through fiscal 2010, $56 million in principal amount of our convertible notes and $24.6 million in face amount of our convertible preferred stock had been converted into shares of our Class A common stock. Also, in fiscal 2012, 2011, 2010, and 2009, we repurchased 0.2 million, 12.3 million, 2.3 million, and 2.0 million shares of our Class A common stock for $0.6 million, $54.5 million, $8.2 million, and $7.3 million, respectively, under our share repurchase programs and through tendering employee shares upon restricted share vesting for tax obligations. We repurchased no common stock during fiscal 2008. As of February 2, 2013, our cash, cash equivalents and investments were $110.0 million, with no debt, and our stockholders’ equity was $128.7 million. Our strong balance sheet allows us the ability to execute on our current strategic initiatives and growth plans.

Strategy

As part of a strategic review of business operations, we have identified what we believe are significant opportunities to turnaround our recent business trends, drive sales productivity and merchandise margin, and grow our existing store base and e-commerce business. The key elements of our opportunities are to:

Strengthen Customer Engagement and Focus. During fiscal 2012, in conjunction with a mid-2011 strategic shift geared toward providing elevated product and a narrower assortment to an older target customer, we lost our focus on our previous core fast fashion customer at Wet Seal. To regain our focus and strengthen our engagement with our core customer in both divisions, we have begun planning and implementing social media strategies highly focused on them. We have also begun to identify other methods, including customer focus groups and ongoing panels, that will allow us to achieve frequent interaction with our customers in both divisions to gain insight into their fashion needs and lifestyles to allow us to better align our organizational goals and marketing efforts with them. We have only recently begun many of these initiatives and will continue to further develop and refine them in fiscal 2013.

Re-establish and Strengthen our Brands. Through intensified customer engagement and interaction, we will be informed of how customers perceive our brands and will react with initiatives to re-establish and strengthen customer perception of our brands in both of our divisions. During fiscal 2013, we intend to first focus on offering trend right apparel and accessories that meet our customers' fashion needs. Concurrently, we will focus on improving how we communicate with our customers, both in our stores and through e-commerce, through "playfully disruptive" lease-line marketing, improved visual merchandising, and targeted social media outreach, as well as through empowering our employees providing the information and training necessary to better understand and engage our customers. Through these efforts, we believe we can regain our customers' attention and confidence in our brands.

Improve Merchandise Margin. In both our Wet Seal and Arden B divisions, we intend to improve merchandise margin by focusing on growing key categories that are more profitable, establishing formal test and re-order programs for portions of our fashion assortments, broadening our assortments to minimize category risks and providing our merchants with more flexibility to shift inventory into trending categories. We plan to enhance our planned promotional strategies, more aggressively manage inventory, continue to improve our sourcing processes and expand and strengthen our sourcing base.

Improve Store Operations and Develop a Selling Culture. We are improving customer service and strengthening customer engagement through the development of more precise labor scheduling tools to allow our store associates to focus more on our customers to increase store productivity and comparable store sales growth. We intend to increase store productivity and efficiency through streamlined operational tasks and reduced non-selling activities, and by providing our store

associates with the key performance metrics needed to manage and build their business. We also will perform more detailed analysis and monitoring to identify improvement opportunities for underperforming stores. In addition, we intend to improve our employee selling skills through stronger partnerships with the merchandising organization in addition to new e-learning training and development programs.

Conservatively Grow Wet Seal Store Base and Position for Future Growth. We plan to open 19 new Wet Seal stores primarily to replace the approximately 14 to 18 stores that will be closing upon lease expiration in fiscal 2013, with openings primarily in outlet centers, in which we have experienced relatively strong sales productivity and profitability. Additionally, during fiscal 2013 we plan to remodel or relocate approximately 24 Wet Seal stores upon lease renewals. As we open new Wet Seal stores, or remodel our existing Wet Seal stores, in fiscal 2013, we intend to take advantage of favorable store construction costs for outlet centers and utilize elements of a refreshed store design that was developed in fiscal 2012. As part of a strategic planning process in fiscal 2013, we intend to further refine our real estate strategy to focus on market-by-market growth targets, target malls and/or other locations within those markets that best align with our core customer and brands. We believe these efforts should position Wet Seal for store base growth beyond fiscal 2013.

Improve Marketing. We believe we have an opportunity to improve our marketing strategies and execution. We intend to re-direct our marketing investments at both Wet Seal and Arden B in fiscal 2013 to more effectively focus on driving store and e-commerce traffic and conversion and to re-establish and strengthen our brands with our customers. We also intend to continue to enhance our e-commerce sites as marketing vehicles for our stores, including a broader utilization of social media, and to focus on direct marketing programs and improved in-store visual merchandising.

Realize Comparable Store Sales Growth Opportunity. We are focused on regaining sales productivity lost through our comparable stores sales declines experienced in fiscal 2012 and prior years, as a result of our unsuccessful strategy change in mid-2011 through fiscal 2012 and the challenging economic environment over the past several years. Sales productivity at both Wet Seal and Arden B remains below historical peaks. In fiscal 2013, we will seek to achieve comparable store sales improvement through implementing strategies noted above, which, among other things, include strengthening customer engagement and focus, re-establishing and strengthening our brands, improving merchandising, promotional and marketing practices, offering broader merchandise assortments and exploiting key merchandise category opportunities.

Continue to Manage Business Conservatively in the Near Term Through our Turnaround. We have taken many recent strategic actions intended to increase our financial strength during our turnaround and to position ourselves to capitalize on our company’s growth and operating leverage opportunities when we have stabilized the business. In concert with our turnaround efforts, our near term goals include preserving a strong balance sheet, improving existing sales trends, continuing conservative growth of our Wet Seal division store base only in channels that have proven to generate strong sales productivity and profitably, pursuing capital expenditure investments that are accretive or provide efficiencies to the business and maintaining clean and more productive inventory levels. Additionally, we intend to continue to identify opportunities to further leverage our planning and allocation and merchandising systems and our distribution center sorter system, and plan to continue to closely monitor inventory positions during fiscal 2013, while seeking to have the appropriate inventory mix and levels in new trend opportunities.

Improve Arden B Business. Beginning in fiscal 2008, we significantly reduced the size and cost of the Arden B merchandising organization, refined the product development and sourcing processes to include more partnering with merchandise suppliers, and adjusted our merchandise mix and pricing and promotional strategies. The changes to the pricing and promotional strategies at Arden B included significant reductions in price points across all categories. In response to these changes, Arden B experienced positive comparable store sales results and improved merchandise margins in fiscal 2009, intermittent improvement in fiscal 2010 and early fiscal 2011, and then decline in the business in latter fiscal 2011 that continued in fiscal 2012. We closed 24 Arden B stores in fiscal 2012, and we plan to close approximately 9 additional Arden B stores in fiscal 2013 as we focus efforts on improving merchandising and marketing strategies in that brand. We believe Arden B has opportunity to generate more consistent financial growth and performance. We aim to drive further sales and profitability improvement at Arden B by better leveraging our distinctive dress business positioning into other product categories, maintaining our value-pricing strategy, and continually improving the in-store customer experience.

Expand our E-commerce Business. We stabilized our e-commerce business in fiscal 2012 and began to see growth in the latter part of the year. This stabilization was a result of employing several initiatives, including aligning our e-commerce and store shopping experiences, employing multi-channel marketing strategies, such as synergizing e-commerce customer

relationship management with our store loyalty programs, expanding e-commerce-only offerings in certain key merchandise categories, significantly growing our customer contact channels, and improving e-commerce inventory planning and allocation practices. These initiatives are ongoing. We believe establishing consistent shopping and brand experiences between the e-commerce and store channels is instrumental to driving growth in our multi-channel customer base. We believe this will lead to greater long-term growth potential in our e-commerce business and add more value from our e-commerce channel as a marketing vehicle for our stores. Also, we continue to focus on and implement enhancements to our websites that will improve the customer experience.

Buying

Our buying teams are responsible for quickly identifying evolving fashion trends and developing themes to guide our merchandising strategy. Each retail division has a separate buying team. The merchandising teams for each division develop fashion themes and strategies by identifying trends and assessing how they best apply to our target customer, shopping appropriate domestic and international markets, using fashion services, and gathering references from industry publications. The buying teams then work closely with vendors to use colors, materials, and designs that create images consistent with the themes for our product offerings.

Since fiscal 2004 for our Wet Seal division, and beginning in fiscal 2008 for our Arden B division, the majority of our merchandise is designed externally. This allows us more flexibility to respond to the changing fashion trends of our target customers, to buy in smaller lots, and to reduce sourcing lead times. See also “Allocation and Distribution of Merchandise” below.

Marketing, Advertising, and Promotion

We believe that our brands are among our most important assets. Our ability to successfully increase brand awareness is dependent upon our ability to address the changing needs and priorities of each brand’s target customers. To that end, we focus many of our marketing efforts to better understand our customers and their needs and ensure we align our brand messages in our marketing, and the channels through which we deliver these messages, to our target customers. We will also continue our emphasis on visual merchandising in our stores and e-commerce sites, and in our direct marketing. As discussed further in Note 1, "Summary of Significant Accounting Policies," to the consolidated financial statements included elsewhere in this Annual Report, we also offer customer loyalty programs in both of our brands. At Wet Seal, we offer a frequent buyer program in order to build loyalty to the brand, increase the frequency of visits, promote multiple item purchases, and gain direct access to the customer. At Arden B, we offer a loyalty program, “B Rewarded,” designed for the same purposes as those of our Wet Seal division. We intend to implement marketing strategies to build upon the past successes of these loyalty programs, synergize these programs with our e-commerce customer relationship management efforts, and ensure they align with our brands for each division. We also plan to more aggressively pursue customer acquisitions and to increase our use of e-commerce marketing to drive increased store traffic.

During fiscal 2012, 2011, and 2010, we spent 1.0%, 0.8%, and 0.6%, respectively, of net sales on advertising. In fiscal 2012, our primary marketing focus was on visual merchandising, including in-store promotion programs and events, and on e-commerce. We expect to decrease marketing and advertising spending modestly in fiscal 2013, and re-direct spend toward what we expect to be more effective marketing investments in support of our business strategies.

Sourcing and Vendor Relationships

We purchase our merchandise primarily from domestic vendors. For fiscal 2012, we directly imported approximately 14% of our retail merchandising receipts from foreign vendors. Although in fiscal 2012 no single vendor provided more than 10% of our merchandise, management believes we are one of the largest customers of many of our smaller vendors. Quality control is monitored and merchandise is inspected upon arrival at our Foothill Ranch, California facility.

We do not maintain any long-term or exclusive commitments or arrangements to purchase merchandise from any single supplier, and there are many vendors who could supply our merchandise.

Allocation and Distribution of Merchandise

Our merchandising strategies depend heavily on maintaining a regular flow of fashionable merchandise into our stores. Successful execution depends largely on our integrated buying, planning, allocation, and distribution functions. By working closely with store operations management and merchandise buyers, our teams of planners and allocators manage inventory levels and coordinate allocation of merchandise to each of our stores based on sales volume and store size, demographics,

climate, and other factors that may influence an individual store’s product mix. We utilize merchandise planning software that assists us in streamlining the planning process. We also utilize size optimization software to support allocation of sizes to better align with each store’s needs.

All merchandise is received from vendors at our Foothill Ranch, California distribution center, where items are inspected and prepared for shipping to our stores. We ship merchandise to our stores by common carrier. Consistent with our goal of maintaining a regular flow of our product offerings, we frequently ship new merchandise to stores, and markdowns are taken regularly to ensure acceptable rates of sale of slow-moving inventory. We also utilize a markdown optimization system at our Wet Seal division to improve the speed of selling through slow product and improve merchandise margins. Marked-down merchandise that remains unsold is either sent to select stores for deep discounting and sale, sent to our e-commerce sites for sale, sold to an outside clearance company, or given to charity. The fulfillment process and distribution of merchandise for our e-commerce business is performed at our Foothill Ranch, California distribution center.

Information and Control Systems

Our merchandise, financial, and store computer systems are integrated and operate using primarily Oracle® technology. We maintain a large data warehouse that provides management, buyers, and planners comprehensive data that helps us identify emerging trends and manage inventories. The core systems supporting our business are frequently enhanced to support strategic business initiatives.

Our stores have a point-of-sale system operating on software provided by Oracle®. This system facilitates bar-coded ticket scanning, automatic price lookups, and centralized credit authorizations. Stores are networked to the corporate office via a centrally managed virtual private network. We utilize a store portal/intranet that is integrated with the corporate merchandise enterprise resource planning system to provide the stores and corporate staff with current information regarding sales, promotions, inventory, and shipments, and enables more efficient communications with the corporate office. We utilize wide area networking hardware at our stores, which guards against security breaches to our stores’ point-of-sale system.

We also recently upgraded our merchandising systems. In fiscal 2009, in order to further improve gross margin through the use of technology, we completed implementation of Oracle® Markdown Optimization and SAS® Size Optimization systems for our Wet Seal business. In fiscal 2010, to maximize the benefits of size optimization, we completed installation of a distribution center automated sorter system to allow automated picking of customized size ranges for each store. A major upgrade to the Oracle® Retail Merchandising system began in fiscal 2010 and was completed in early fiscal 2011. Additionally, several enhancements and upgrades were completed in fiscal 2011 to the point-of-sale systems to create more efficiency within the store environment. In fiscal 2012, to improve our in store point-of-sale process, we replaced our aging PSC® Scanners with new tablets in approximately 100 Wet Seal stores and may decide to complete roll-out of this technology to additional stores in 2013. We also completed several upgrades which included store routers, Cisco Equipment purchases and installation of a new storage area network.

Seasonality and Inflation

Our business is seasonal in nature, with the Christmas season, beginning the week of Thanksgiving and ending the first Saturday after Christmas, and the back-to-school season, beginning the last week of July and ending during September, historically accounting for a large percentage of our sales volume. For the past three fiscal years, the Christmas and back-to-school seasons together accounted for an average of slightly less than 30% of our annual sales.

We do not believe that inflation has had a material effect on our results of operations during the past three years. However, we began to experience cost pressures in the fourth quarter of fiscal 2010 and saw further cost increases through fiscal 2011 and most of fiscal 2012, as a result of rising commodity prices, primarily for cotton, increased labor costs, due to labor shortages in China, from which a majority of our merchandise is sourced by our vendors, and increasing fuel costs. Although cotton prices have stabilized, the other sourcing cost pressures are expected to continue into fiscal 2013. The rising value of the currency in China relative to the U.S. dollar may also have an impact on future product costs. In response to the costs increases, we leverage our large vendor base to lower costs, are identifying new vendors and are assessing ongoing promotional strategies in efforts to maintain or improve upon historical merchandise margin levels. We cannot be certain that our business will not be affected by inflation in the future.

Trademarks

We own numerous trademarks, several of which are important to our business. Our primary and most significant trademarks and service marks are WET SEAL and ARDEN B, which are registered in the United States Patent and Trademark Office. We also have registered, or have applications pending for, a number of other trademarks including, but not limited to, B. REWARDED, BLINK by WET SEAL, BLUE ASPHALT, BUTTERFLY DESIGN, CHIC BOUTIQUE, CONTEMPO CASUALS, ENR EVOLUTION NOT REVOLUTION, FASHION INSIDER, FASHION RIGHT.ALL DAY ALL NIGHT., FIT IN. STAND OUT., iRUNWAY, LOVE THE TREND-HATE TO SPEND, LIFE'S A BLUR.FOCUS ON FASHION, ROCK THESE BLUES and URBAN VIBE. Additionally, we have registered, or have pending applications for the following international trademarks including but not limited to, WET SEAL, BLUE ASPHALT, THE WET SEAL, URBAN VIBE, ARDEN B, and CONTEMPO CASUALS. In general, the registrations for these trademarks and service marks are renewable indefinitely as long as the marks are used as required under applicable regulations. We are not aware of any significant adverse claims or infringement actions relating to our trademarks or service marks.

Competition

The women’s retail apparel industry is highly competitive, with fashion, quality, price, location, and service being the principal competitive factors. Our Wet Seal and Arden B stores compete with specialty apparel retailers, department stores, and other apparel retailers, including Abercrombie & Fitch, Aeropostale, American Eagle, Anthropologie, Banana Republic, BCBG, bebe, Body Central, Charlotte Russe, Express, Forever 21, Gap, Guess?, H&M, Nordstrom, Old Navy, Pacific Sunwear, rue21, Target, Urban Outfitters, Zara, and other regional retailers. Many of our competitors are large national chains that have substantially greater financial, marketing, and other resources than we do. While we believe we compete effectively for favorable site locations and lease terms, competition for prime locations within malls and power centers is intense, and we cannot ensure that we will be able to obtain new locations on terms favorable to us, if at all.

Customers

Our company’s business is not dependent upon a single customer or small group of customers.

Environmental Matters

We are not aware of any federal, state, or local environmental laws or regulations that will materially affect our earnings or competitive position, or result in material capital expenditures. However, we cannot predict the effect on our operations of possible future environmental legislation or regulations. During fiscal 2012, we did not make any material capital expenditures for environmental control facilities and no such material expenditures are anticipated for fiscal 2013.

Government Regulation

Our company is subject to various federal, state, and local laws affecting our business, including those relating to advertising, consumer protection, privacy, health care, tax, environmental and zoning and occupancy. Each of our company’s stores must comply with licensing and regulation by a number of governmental authorities in jurisdictions in which the store is located. To date, our company has not been significantly affected by any difficulty, delay, or failure to obtain required licenses or approvals.

Our company is also subject to federal and state laws governing such matters as employment and pay practices, overtime, and working conditions. The bulk of our company's employees are paid on an hourly basis at rates related to the federal and state minimum wages. In the past, we have been assessed penalties or paid settlements to gain dismissal of lawsuits for noncompliance with certain of these laws, and future noncompliance could result in a material adverse effect on our company's operations. In July 2006, May 2007, September 2008, May 2011, and October 2011, we were served with class action complaints alleging violations under certain State of California labor laws and on April 24, 2009, the U.S. Equal Employment Opportunity Commission (the “EEOC”) requested information and records relevant to several charges of discrimination by us against our employees. In November 2006, we reached an agreement to settle the July 2006 class action complaint for approximately $0.3 million. In March 2013, we paid $0.2 million to settle the May 2007 class action complaint. On February 4, 2013, the Court of Appeals issued a remittitur to send the September 2008 case back to the trial court where it will proceed on behalf of only the three named plaintiffs and not as a class action. On September 20, 2012, the NLRB dismissed the plaintiffs claims for the May 2011 matter; however, the matter is still pending in state court and Plaintiffs' are appealing the Court's order granting our motion to compel arbitration. On March 28, 2012, the court entered an Order denying our motion to compel arbitration for the October 2011 class action complaint, and on September 21, 2012, we filed a notice of appeal. On November 14, 2012, we reached resolution with the EEOC and several of the individual complainants that concludes the

EEOC's investigation. Between November 2012 and March 2013, we paid approximately $0.8 million to settle with individual complainants. We also agreed to programmatic initiatives that are consistent with our diversity plan. We will report progress on our initiatives and results periodically to the EEOC. Claimants with whom we did not enter into a settlement had an opportunity to bring a private lawsuit within ninety days from the date they received their November 26, 2012 right-to-sue notice from the EEOC, however, that time period is tolled for those individuals who are putative class members in a race discrimination class action filed on July 12, 2012 in the United States District Court for the Central District of California with respect to any race discrimination claims they have that are within the scope of the putative class action.

We continue to monitor our facilities for compliance with the Americans with Disabilities Act, or the ADA, in order to conform to its requirements. Under the ADA, we could be required to expend funds to modify stores to better provide service to, or make reasonable accommodation for the employment of, disabled persons. We believe that expenditures, if required, would not have a material adverse effect on our company’s operations.

Employees

As of February 2, 2013, we had 7,012 employees, consisting of 1,850 full-time employees and 5,162 part-time employees. Full-time personnel consisted of 647 salaried employees and 1,203 hourly employees. All part-time personnel are hourly employees. Of all employees, 6,758 were sales personnel and 254 were administrative and distribution center personnel. Personnel at all levels of store operations are provided various opportunities for cash and/or other incentives based upon various individual store sales and other performance targets. All of our employees are nonunion and, in management’s opinion, are paid competitively at current industry standards. We believe that our relationship with our employees is good.

Item 1A. Risk Factors

Risks Related to our Business

General economic conditions, perceptions of such conditions by our customers and the impact on consumer confidence and consumer spending have adversely impacted our results of operations and may continue to do so.

Our performance is subject to general economic conditions and their impact on levels of consumer confidence and consumer spending. Consumer purchases of discretionary items, including our merchandise, generally decline during periods when disposable income is adversely affected or there is economic uncertainty. As a result of recent increases in payroll taxes and increasing fuel costs, disposable income has decreased, which may lead to a decrease in demand for our merchandise. In addition, continued difficult economic conditions may impact many facets of our operations, including, among other things, the ability of one or more of our vendors to deliver their merchandise in a timely manner or otherwise meet their obligations to us. If pressures on disposable income and poor economic conditions in the U.S. and world economic markets continue, or if they deteriorate further, our business, financial condition, and results of operations may be adversely affected.

We may continue to experience declines in comparable store sales in our Wet Seal division, and there can be no guarantee that the strategic initiatives we are implementing to improve our results will be successful.

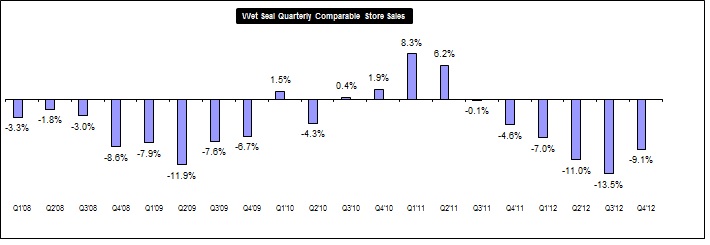

During fiscal 2012 our comparable store sales declined by 10.1% in our Wet seal division. We have taken steps to return to our core expertise of fast fashion merchandising which long supported our success in the past in the Wet Seal division. However, there can be no guarantee that our financial results will improve and, if they do, there can be no guarantee as to the timing, duration or significance of such improvement.

We have experienced poor comparable store sales and operating results in our Arden B division, and we cannot assure that we will be able to re-establish and sustain improvements in the future.

In fiscal 2011 and 2012, we experienced weak comparable same store sales and operating results in the Arden B division due to not having the appropriate inventory levels in key performing categories and fashion content weakness. We began to see improvement in January 2013. There can be no guarantee that our efforts to improve results will be successful and that the financial performance of our Arden B division will improve.

We have experienced losses and relied on our cash reserves to fund our operations and implement our strategic growth plans. If we are unable to improve cash flow from operations or obtain additional capital to meet our liquidity and capital resource requirements and pursue our growth strategy, our business may be adversely affected.

In recent years, we have maintained strong levels of cash, cash equivalents and investments and extinguished our debt. However, in fiscal 2012, we incurred a net loss of $113.2 million and negative cash flow from operations of $26.2 million. If we continue to experience negative cash flow from operations, we will need to continue to rely on our cash reserves to fund our

business or seek additional capital. There can be no assurance that any such capital would be available to us. Accordingly, if our business does not generate sufficient cash flow from operations to fund our working capital needs and planned capital expenditures, and our cash reserves are depleted, we may need to take various actions, such as down-sizing and/or eliminating certain operations, which could include exit costs, or reducing or delaying capital expenditures, strategic investments or other actions, and our business may be adversely affected.

If we are unable to anticipate and react to new fashion and product demand trends, our financial condition and results of operations could be adversely affected.

We rely on a limited demographic customer base for a large percentage of our sales. Our brand image is dependent upon our ability to anticipate, identify and provide fresh inventory reflecting current fashion trends.

Furthermore, the continued difficult economic conditions make it increasingly difficult for us to accurately predict product demand trends. If we fail to anticipate, identify or react appropriately or in a timely manner to these fashion and product demand trends, we could experience reduced consumer acceptance of our products, a diminished brand image and higher markdowns. These factors could adversely affect our financial condition and results of operations.

If we decrease the price that we charge for our products or offer extensive, continued promotions on our products, we may earn lower gross margins and our revenues and profitability may be adversely affected.

The prices that we are able to charge for our products depend on, among other things, the type of product offered, the consumer response to the product and the prices charged by our competitors. To the extent that we are forced to lower our prices, our gross margins will be lower and our revenues and profitability may be adversely affected.

We have recorded asset impairment charges in the past and we may record material asset impairment charges in the future.

Quarterly, we assess whether events or changes in circumstances have occurred that potentially indicate the carrying value of long-lived assets may not be recoverable. If we determine that the carrying value of long-lived assets is not recoverable, we will be required to record impairment charges relating to those assets. For example, our assessments during fiscal 2012 indicated that operating losses or insufficient operating income existed at certain retail stores, with a projection that the operating losses or insufficient operating income for those locations would continue. As such, we recorded non-cash charges of $27.0 million during fiscal 2012 within asset impairment in the consolidated statements of operations to write down the carrying values of these stores' long-lived assets to their estimated fair values.

Our quarterly evaluation of store assets includes consideration of current and historical performance and projections of future profitability. The profitability projections rely upon estimates made by us, including store-level sales, gross margins, and direct expenses, and, by their nature, include judgments about how current strategic initiatives will impact future performance. If we are not able to achieve the projected key financial metrics for any reason, including because any of the strategic initiatives being implemented do not result in significant improvements in our current financial performance trend, we would incur additional impairment of assets in the future.

In the event we record additional impairment charges, this could have a material adverse effect on our results of operations and financial condition.

We may face risks associated with the transition of our senior management, newly appointed chief executive officer and our new board of directors.

In general, our success depends to a significant extent on the performance of our senior management, particularly personnel engaged in merchandising and store operations, and on our ability to identify, hire and retain additional key management personnel. We have had significant changes in management in the beginning of fiscal 2013 and during fiscal 2012, 2011, and 2010, and these changes may impact our ability to execute our business strategy.

On July 23, 2012, our previous Chief Executive Officer was terminated. On October 19, 2012, our previous Executive Vice President and Chief Merchandise Officer of our Wet Seal division resigned from our Company. On February 1, 2013, our previous President and Chief Operating Officer resigned from our Company. On February 20, 2013, our previous Senior Vice President of Store Operations resigned from our Company.

Effective January 7, 2013, we appointed Mr. John D. Goodman as our new chief executive officer. While Mr. Goodman immediately became involved in the day-to-day activities of our company, we anticipate that we will experience a transition period before he is fully integrated into the organization. During this transition period, we may experience a disruption to our customer relationships, employee morale and/or business.

In addition, our recent appointment of six new members to our Board and the resulting transition and integration of these individuals may impact our ability to execute our business strategy in the near term. On September 18, 2012, we appointed two new directors to our Board, Ms. Kathy Bronstein and Mr. John D. Goodman, who subsequently was appointed our chief executive officer, as noted above. On October 4, 2012, we entered into an agreement (“Settlement Agreement”) with Clinton Group, Inc. (“CGI”), for the purpose of resolving a pending consent solicitation and effecting an orderly change in the composition of our Board. Pursuant to the Settlement Agreement, four of the members of our Board resigned, Mr. Harold Kahn, Mr. Jonathan Duskin, Mr. Sidney Horn and Mr. Henry Winterstern, and four new directors, Ms. Dorrit Bern, Ms. Lynda Davey, Ms. Mindy Meads and Mr. John Mills, were appointed as directors of the Board to fill the four vacancies created by the resignations. While all of the recently appointed directors have become immediately engaged in our business, we expect that we will continue to experience a transition period until they are fully integrated into their roles. We cannot provide any assurance that there will not be any disruption that adversely impacts our business during such transition period.

Our business could be negatively affected as a result of the actions of activist stockholders.

Over the last few years, proxy contests and other forms of stockholder activism have been directed against numerous public companies in retail businesses, including us. As noted in the preceding risk factor, in 2012, we were engaged in a proxy contest with CGI which resulted in our entering into the Settlement Agreement and appointing four new directors to fill vacancies created by director resignations, and led to a significant increase in our operating expenses, which contributed to our net loss in fiscal 2012. Although the proxy contest was settled, we could become engaged in another proxy contest, or experience other stockholder activism, in the future. For example, on February 13, 2013, CGI delivered a letter to our Board of Directors expressing appreciation for recent measures implemented by the Board, but suggesting the return of additional capital to the Company's stockholders via a Dutch Auction share repurchase program. Our Board considered CGI's suggestion and advised CGI that it believed that our existing strategies and plans were prudent and in the best interests of the Company and its stockholders.

If stockholder activism continues or increases, particularly with respect to matters which our Board of Directors, in exercising their fiduciary duties, disagree with or have determined not to pursue, our business could be adversely affected because:

| |

| • | responding to actions by activist stockholders can be costly and time-consuming, disrupting our operations and diverting the attention of management; and |

| |

| • | perceived uncertainties as to our future direction may result in the loss of potential business opportunities, and may make it more difficult to attract and retain qualified personnel, business partners and customers. |

In addition, if faced with another proxy contest, we may not be able to respond successfully to the contest or dispute, which would be disruptive to our business. Even if we are successful, if individuals are elected to our Board with a differing agenda, our ability to effectively and timely implement our strategic plan and create additional value for our stockholders may be adversely affected.

These actions could cause our stock price to experience periods of volatility.

Our company's ability to attract customers to our stores depends heavily on the success of the shopping centers in which many of our stores are located.

Substantially all of our stores are located in regional mall shopping centers. Factors beyond our control impact mall traffic, such as general economic conditions and consumer spending levels. Consumer spending and mall traffic remain depressed due to the continued difficult economic conditions. As a result, mall operators have been facing increasing operational and financial difficulties. The increasing inability of mall “anchor” tenants and other area attractions to generate consumer traffic around our stores, the increasing inability of mall operators to attract “anchor” tenants and maintain viable operations and the increasing departures of existing “anchor” and other mall tenants due to declines in the sales volume and in the popularity of certain malls as shopping destinations, have reduced and may continue to reduce our sales volume and, consequently, adversely affect our financial condition, results of operations and cash flows.

Our ability to procure merchandise could be adversely affected by changes in our vendors' factoring arrangements.

Changes in our vendors' factoring arrangements may threaten the factors' financial viability and ability to provide factoring services to its customers. Although we do not have a direct relationship with factors, a portion of our vendors who supply our company with merchandise have direct factoring arrangements. Vendors who engage in factoring transactions will typically sell their accounts receivable to a factor at a discount in exchange for cash payments, which can be used to finance the business and operations of the vendors.

If the financial condition of our vendors' factors were to deteriorate and certain of our vendors were unable to procure alternative factoring arrangements from competitors of their factor on the same or substantially similar terms, our ability to timely procure merchandise for our stores could be adversely affected. This could require the devotion of significant time and attention by our management to adequately resolve such matters. In turn, our results of operations and financial condition could suffer.

Our ability to use net operating loss carryforwards to offset future taxable income for U.S. federal or state income tax purposes is subject to limitations.

We believe that our net operating losses (“NOLs”) are a valuable asset and we intend to take actions to protect the value of our NOLs. However, Section 382 of the Internal Revenue Code (“Section 382”) contains provisions that may limit the availability of federal net operating loss carryforwards to be used to offset taxable income in any given year upon the occurrence of certain events, including significant changes in our stockholders' ownership interests in our company. Under Section 382, potential limitations on NOLs are triggered when there has been an “ownership change” (generally defined as a greater than 50% change (by value) in our stock ownership over a three-year period).

We incurred ownership changes in April 2005 and December 2006, which resulted in Section 382 limitations applying to NOLs generated prior to those dates, which were approximately $150.6 million. Despite these ownership changes, we may utilize all of our $121.5 million of NOLs as of February 2, 2013, to offset future taxable income. Future transactions involving the sale or other transfer of our stock may result in additional ownership changes for purposes of Section 382. The occurrence of such additional ownership changes could limit our ability to utilize our remaining NOLs and possibly other tax attributes. Limitations imposed on our ability to use NOLs and other tax attributes to offset future taxable income could cause us to pay U.S. federal income taxes earlier than we otherwise would if such limitations were not in effect. Any further ownership change also could cause such NOLs and other tax attributes to expire unused, thereby reducing or eliminating the benefit of such NOLs and other tax attributes to us and adversely affecting our future cash flows.

In addition, we may determine that varying state laws with respect to NOL utilization may result in lower limits, or an inability to utilize NOLs in some states altogether, which could result in us incurring additional state income taxes. During fiscal 2008, the State of California passed legislation that suspended our ability to utilize NOLs to offset taxable income in fiscal 2008 and 2009. In late 2010, the State of California extended such legislation, which further suspended use of NOLs to fiscal 2010 and 2011. As a result, we incurred additional cash state income taxes in California. In the event that state law results in lower limits, or an inability to utilize loss carryforwards, or we become subject to federal alternative minimum tax, this could adversely affect our future cash flows.

We may suffer negative publicity and our business may be harmed if we need to recall any products we sell.

Each of our Wet Seal and Arden B divisions has in the past needed to, and may in the future need to, recall products that we determine may present safety issues. If products we sell have safety problems of which we are not aware, or if we or the Consumer Product Safety Commission recall a product sold in our stores, we may suffer negative publicity and, potentially, product liability lawsuits, which could have a material adverse impact on our reputation, financial condition and results of operations or cash flows.

If we are unable to pass through increases in raw material, labor and energy costs to our customers through price increases, our financial condition and results of operations could be adversely affected.

Our product costs rise from time to time due to increasing commodity prices, primarily for cotton, as well as due to higher production labor and energy costs. We may not be able to, or may elect not to, pass these increases on to our customers through price increases, which may adversely affect our financial condition and results of operations.

We depend upon a single center for our corporate offices and distribution activities, and any significant disruption in the operation of this center could harm our business, financial condition, results of operations and/or cash flows.

Our corporate offices and the distribution functions for all of our stores and e-commerce business are handled from a single, leased facility in Foothill Ranch, California. In general, this area of California is subject to earthquakes and wildfires. Any significant interruption in the operation of this facility due to a natural disaster, arson, accident, system failure or other unforeseen event could delay or impair our ability to distribute merchandise to our stores and, consequently, lead to a decrease in sales. Furthermore, we have little experience operating essential functions away from our main corporate offices and are uncertain what effect operating satellite facilities might have on our business, personnel and results of operations. The financial

losses incurred may exceed our insurance for earthquake damages and business interruption costs related to any such disruption. As a result, our business, financial condition, results of operations and cash flows could be adversely affected.

Fluctuations in our revenues for the "back-to-school" season in the third fiscal quarter and the "holiday" season in the fourth fiscal quarter have a disproportionate effect on our overall financial condition, results of operations and cash flows.

We experience seasonal fluctuations in revenues, with a disproportionate amount of our revenues being generated in the third fiscal quarter “back-to-school” season, which begins the last week of July and ends during September, and the fourth fiscal quarter “holiday” season. In addition, any factors that harm our third and fourth fiscal quarter operating results, including adverse weather or unfavorable economic conditions, could have a disproportionate effect on our results of operations for the entire fiscal year.

In order to prepare for our peak shopping seasons, we must order and keep in stock significantly more merchandise than we would carry at other times of the year. An unanticipated decrease in demand for our products during our peak shopping seasons could require us to sell excess inventory at a substantial markdown, which could reduce our net sales and gross profit. Alternatively, an unanticipated increase in demand for certain of our products could leave us unable to fulfill customer demand and result in lost sales and customer dissatisfaction.

Our quarterly results of operations may also fluctuate significantly as a result of a variety of other factors, including the merchandise mix and the timing and level of inventory markdowns. As a result, historical period-to-period comparisons of our revenues and operating results are not necessarily indicative of future period-to-period results. Reliance should not be placed on the results of a single fiscal quarter, particularly the third fiscal quarter “back-to-school” season or fourth fiscal quarter “holiday” season, as an indication of our annual results or our future performance.

Extreme or unseasonable weather conditions could adversely affect our business.

Extreme weather conditions in the areas in which our stores are located could adversely affect our business. For example, frequent or unusually heavy snowfall, ice storms, rainstorms or other extreme weather conditions over a prolonged period could make it difficult for our customers to travel to our stores and thereby reduce our sales and profitability. Our business is also susceptible to unseasonable weather conditions. For example, extended periods of unseasonably warm temperatures during the winter season or cool weather during the summer season could render a portion of our inventory incompatible with those unseasonable conditions. Reduced sales from extreme or prolonged unseasonable weather conditions could adversely affect our business.

Our failure to effectively compete with other retailers for sales and locations could have a material adverse effect on our financial condition, results of operations and cash flows.

The women's retail apparel industry is highly competitive, with fashion, quality, price, location and service being the principal competitive factors. Our Wet Seal and Arden B stores compete with specialty apparel retailers, department stores and certain other apparel retailers, including Abercrombie & Fitch, Aeropostale, American Eagle, Anthropologie, Banana Republic, BCBG, bebe, Body Central, Charlotte Russe, Express, Forever 21, Gap, Guess?, H&M, Macy's, Nordstrom, Old Navy, Pacific Sunwear, rue21, Target, Urban Outfitters, Zara, and other regional retailers. Many of our competitors are large national chains that have substantially greater financial, marketing and other resources than we do. We face a variety of competitive challenges, including:

| |

| • | anticipating and quickly responding to changing consumer demands; |

| |

| • | maintaining favorable brand recognition and effectively marketing our products to consumers in narrowly-defined market segments; |

| |

| • | sourcing innovative, high-quality products in sizes, colors and styles that appeal to consumers in our target markets and maintaining a sufficient quantity of these items for which there is the greatest demand; |

| |

| • | obtaining favorable site locations within malls on reasonable terms; |

| |

| • | sourcing merchandise efficiently; |

| |

| • | pricing our products competitively and achieving customer perception of value; |

| |

| • | offering attractive promotional incentives while maintaining profit margins; and |

| |

| • | withstanding periodic downturns in the apparel industry. |

Our industry has low barriers to entry that allow the introduction of new products or new competitors at a fast pace. Any of these factors could result in reductions in sales or the prices of our products which, in turn, could have a material adverse effect on our financial condition, results of operations and cash flows.

In fiscal 2013, we currently plan to open 19 new Wet Seal stores primarily to replace the approximately 14 to 18 stores that will be closing upon lease expiration in fiscal 2013, with openings primarily in outlet centers, in which we have experienced relatively strong sales productivity and profitability. We currently plan to close approximately 9 Arden B stores in fiscal 2013 upon lease expiration, as we focus efforts on improving merchandising and marketing strategies in that business. While we compete effectively for favorable site locations and lease terms, competition for prime locations within malls and outlet centers, in particular, and within other locations is intense and we cannot assure that we will be able to obtain new locations on terms favorable to us, if at all.

In addition, actions of our competitors, particularly increased promotional activity, can negatively impact our business. In light of the continued difficult economic conditions, pricing is a significant driver of consumer choice in our industry and we regularly engage in price competition, particularly through our promotional programs. To the extent that our competitors lower prices, through increased promotional activity or otherwise, our ability to maintain gross profit margins and sales levels may be negatively impacted. There can be no assurance that our competitors' increased promotional activity will not negatively impact our business.

The upcoming expiration of leases for approximately 90 of our Wet Seal and Arden B existing stores could lead to increased costs associated with renegotiating our leases and/or relocating our stores.

We have approximately 90 existing store leases scheduled to expire in fiscal 2013. In connection with the expiration of these leases, we will have to renegotiate new leases, which could result in higher rental amounts for each store. We may not be able to obtain new lease terms that are favorable to us. In addition, as a result of renewal negotiations, we may be required by the landlord to remodel as a condition for renewal, which could result in significant capital expenditures. In addition, some landlords may refuse to renew our leases due to our lower sales per square foot as compared with other prospective tenants. If we are unable to agree to new terms with our landlords, we will have to close or relocate these stores, which could result in a significant expenditure and could lead to an interruption in the operation of our business at the affected stores, and we could be required to relocate to less desirable locations or may not be able to find viable locations at all.

Our computer hardware and software systems are vital to the efficient operation of our retail and Web-based stores, and damage to these systems could harm our business.

We rely on our computer hardware and software systems for the efficient operation of our retail and Web-based stores. Our information systems provide our management with real-time inventory, sales and cost information that is essential to the operation of our business. Due to our number of stores, geographic diversity and other factors, we would be unable to generate this information in a timely and accurate manner in the event our hardware or software systems were unavailable. These systems are vulnerable to damage or interruption from a number of factors, including earthquake, fire, flood and other natural disasters and power loss, computer systems failure, security breaches, and Internet, telecommunications or data network failure.

A significant information systems failure could reduce the quality or quantity of operating data available to our management. If this information were unavailable for any extended period of time, our management would be unable to efficiently run our business, which would result in a reduction in our net sales.

A cybersecurity incident could have a material adverse effect on our financial condition, results of operations and cash flows.

A cyberattack may bypass the security for our information systems, causing an information system security breach and leading to a material disruption of our information systems, the loss of business information and/or the loss of e-commerce sales. Such a cyberattack could result in any of the following:

| |

| • | theft, destruction, loss, misappropriation or release of confidential data or intellectual property; |

| |

| • | operational or business delays resulting from the disruption of our information systems and subsequent clean-up and mitigation activities; |

| |

| • | negative publicity resulting in reputation or brand damage with our customers, partners or industry peers; and |

| |

| • | loss of sales generated through our Internet websites through which we sell merchandise to customers to the extent these websites are affected by a cyberattack. |

As a result, our business, financial condition, results of operations and cash flows could be materially and adversely affected.

Government regulation of the Internet and e-commerce is evolving and unfavorable changes could harm our business.

We are subject to general business regulations and laws, as well as regulations and laws specifically governing the Internet and e-commerce. Existing and future laws and regulations may impede the growth of our Internet or e-commerce services. These regulations and laws may cover taxation, privacy, data protection, pricing, content, copyrights, distribution, mobile communications, electronic contracts and other communications, consumer protection, the provision of e-commerce payment services, unencumbered Internet communications, consumer protection, the provision of e-commerce payment services, unencumbered Internet access to our services, the design and operation of websites and the characteristics and quality of products and services. It is not clear how certain existing laws governing issues such as property ownership, libel and personal privacy apply to the Internet and e-commerce. Unfavorable regulations and laws could diminish the demand for our products and services and increase our costs of doing business.

If we fail to comply with Payment Card Industry Data Security Standards, we may be subject to fines or penalties, which could adversely affect our business, financial condition and results of operations.

We are highly dependent on the use of credit cards to complete sale transactions in our stores and through our websites. If we fail to comply with Payment Card Industry Data Security Standards, we may become subject to fines or limitations on our ability to accept credit cards. Through our sale transactions, loyalty programs and other methods, we may obtain information about our customers which is subject to federal and state privacy laws. These laws and the judicial interpretation of such laws are constantly evolving. If we fail to comply with these laws, we may be subject to fines or penalties, which could impact our business, financial condition and results of operations.

Our inability or failure to protect our intellectual property or our infringement of other's intellectual property could have a negative impact on our operating results.

Our trademarks and other proprietary rights are important to our success and our competitive position. We have registered trademarks for Wet Seal and Arden B (which are registered in the retail store services and other classes). We take actions to establish and protect our intellectual property. However, others may infringe on our intellectual property rights. If we fail to adequately protect our intellectual property rights, we may lose market share to our competitors, the value of our brands could be diminished and our business and results of operations could be adversely affected.

We are also subject to the risk that claims will be brought against us for infringement of the intellectual property rights of third parties, seeking to block the sale of our products as violative of their intellectual property rights or payment of monetary amounts. In particular, we are subject to copyright infringement claims for which we may not be entitled to indemnification from our suppliers. In addition, in recent years, companies in the retail industry, including us, have been subject to patent infringement claims from non-practicing entities, or “patent trolls.” Any infringement or other intellectual property claim made against us, whether or not it has merit, could be time-consuming and result in costly litigation. As a result, any such claim, or the combination of multiple claims, could have a material adverse effect on our operating results. If we are required to stop using any of our registered or nonregistered trademarks, our sales could decline and, consequently, our business and results of operations could be adversely affected.

Covenants contained in agreements governing our senior credit facility restrict the manner in which we conduct our business, under certain circumstances, and our failure to comply with these covenants could result in a default under these agreements, which would have a material adverse effect on our business, financial condition, growth prospects and ability to procure merchandise for our stores.

Our senior revolving credit facility contains covenants that restrict the manner in which we conduct our business under certain circumstances. Subject to certain exceptions, these covenants restrict or limit our ability to, among other things:

| |

| • | incur or guarantee additional indebtedness or refinance our existing indebtedness; |

| |

| • | make certain investments or acquisitions; |

| |

| • | merge, consolidate, dissolve or liquidate; |

| |

| • | engage in certain asset sales (including the sale of stock); |

A breach of any of these covenants could result in a default under the agreements governing our existing indebtedness, acceleration of any amounts then outstanding, the foreclosure upon collateral securing the debt obligations, or the unavailability of the line of credit.

We do not authenticate the license rights of our suppliers.

We purchase merchandise from a number of vendors who purport to hold manufacturing and distribution rights under the terms of license agreements or that assert that their products are not subject to any restrictions as to distribution. We generally rely upon each vendor's representation concerning those manufacturing and distribution rights and do not independently verify whether each vendor legally holds adequate rights to the licensed properties they are manufacturing or distributing. If we acquire unlicensed merchandise or merchandise violating a registered trademark, we could be obligated to remove it from our stores, incur costs associated with destruction of the merchandise if the vendor is unwilling or unable to reimburse us and be subject to civil and criminal liability. The occurrence of any of these events could adversely affect our financial condition, results of operations and/or cash flows.