UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06110

Western Asset Funds, Inc.

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-877-721-1926

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

December 31, 2012

Annual

Repor t

Western Asset

Global Multi-Sector

Fund

INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

| | |

| II | | Western Asset Global Multi-Sector Fund |

Fund objective

The Fund seeks to maximize return through income and capital appreciation.

Fund name change

Prior to May 1, 2012, the Fund was known as Western Asset Global Multi-Sector Portfolio. There was no change in the Fund’s investment objective or investment policies as a result of the name change.

Letter from the president

Dear Shareholder,

We are pleased to provide the annual report of Western Asset Global Multi-Sector Fund for the twelve-month reporting period ended December 31, 2012. Please read on for a detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

Special shareholder notice

Effective September 1, 2012, the individuals responsible for day-to-day portfolio management, development of investment strategy, oversight and coordination of the Fund are Stephen A. Walsh, S. Kenneth Leech, Michael C. Buchanan, Ian R. Edmonds, Keith J. Gardner, Andrew J. Belshaw, Gordon S. Brown and Christopher Orndorff. Messrs. Walsh, Leech, Buchanan, Edmonds, and Gardner have been responsible for the day-to-day management of the Fund since it commenced operations in 2011. Messrs. Belshaw, Brown and Orndorff have been responsible for the day-to-day management of the Fund since September 2012. Messrs. Walsh, Leech, Buchanan, Edmonds and Gardner have been employed by Western Asset Management Company (“Western Asset”) as investment professionals for at least the past five years. Mr. Belshaw has been employed by Western Asset in the capacity of investment professional since 2009 and was Managing Director, Head of Investment Management at BlackRock Investment Management from 2004 to 2009. Mr. Orndorff has been employed by Western Asset in the capacity of investment professional since 2010. Prior to joining Western Asset, Mr. Orndorff was Managing Principal and Executive Committee Member at Payden & Rygel for over 19 years. Mr. Brown has been employed by Western Asset in the capacity of investment professional since 2011 and was Senior Investment Manager, Emerging Market Rates and Currencies at Baillie Gifford & Co. from 2001 to 2011. These individuals work together with the broader Western Asset investment management team on portfolio structure, duration weighting and term structure decisions.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish

| | | | |

| Western Asset Global Multi-Sector Fund | | | III | |

this is through our website, www.leggmason.com/individualinvestors. Here you can gain immediate access to market and investment information, including:

| Ÿ | | Fund prices and performance, |

| Ÿ | | Market insights and commentaries from our portfolio managers, and |

| Ÿ | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

President

January 31, 2013

| | |

| IV | | Western Asset Global Multi-Sector Fund |

Investment commentary

Economic review

The U.S. economy continued to grow over the twelve months ended December 31, 2012, but it did so at an uneven pace. U.S. gross domestic product (“GDP”)i growth, as reported by the U.S. Department of Commerce, was 2.0% in the first quarter of 2012. The economy then slowed in the second quarter, as GDP growth was a tepid 1.3%. Economic growth accelerated to 3.1% in the third quarter, partially due to increased private inventory investment, higher federal government spending and moderating imports. However, this was a temporary uptick, as the Commerce Department’s initial estimate showed that fourth quarter GDP contracted 0.1%. This was the first negative reading since the second quarter of 2009, and was driven by a reversal of the above factors, as private inventory investment and federal government spending weakened.

While there was some improvement in the U.S. job market, unemployment remained elevated throughout the reporting period. When the period began, unemployment, as reported by the U.S. Department of Labor, was 8.3%. Unemployment then generally declined and was 7.8% in September 2012, the lowest rate since January 2009, but still high by historical standards. The unemployment rate then rose to 7.9% in October, before falling to 7.8% in November, where it remained in December. The number of longer-term unemployed continued to be a headwind for the economy, as roughly 39% of the 12.2 million people without a job have been out of work for more than six months.

Meanwhile, the housing market brightened, as sales generally improved and home prices continued to rebound. According to the National Association of Realtors (“NAR”), while existing-home sales dipped 1.0% on a seasonally adjusted basis in December 2012 versus the previous month, they were still 12.8% higher than in December 2011. In addition, the NAR reported that the median existing-home price for all housing types was $180,800 in December 2012, up 11.5% from December 2011. This marked the tenth consecutive month that home prices rose compared to the same period a year earlier. Furthermore, the inventory of homes available for sale fell 8.5% in December, which represents a 4.4 month supply at the current sales pace. This represents the lowest inventory since May 2005.

The manufacturing sector expanded during much of the reporting period, although it experienced several soft patches. Based on the Institute for Supply Management’s PMI (“PMI”)ii, after expanding 34 consecutive months, the PMI fell to 49.7 in June 2012, which represented the first contraction in the manufacturing sector since July 2009 (a reading below 50 indicates a contraction, whereas a reading above 50 indicates an expansion). Manufacturing continued to contract in July and August before ticking up to 51.5 in September and 51.7 in October. The PMI fell back to contraction territory with a reading of 49.5 in November, its lowest level since July 2009. However, manufacturing again expanded in December, with the PMI increasing to 50.7.

Growth generally moderated overseas and, in some cases, fell back into a recession. But in its January 2013 World Economic Outlook Update, after the reporting period ended, the International Monetary Fund (“IMF”) stated that “Global growth is projected to increase during 2013, as the factors underlying soft global activity are expected to subside. However, this upturn is projected to be more gradual than in the October 2012 World Economic Outlook projections.” The IMF projects that global growth will increase from 3.2% in 2012 to 3.5% in 2013. From a regional perspective, the IMF anticipates 2013 growth will be -0.2% in the Eurozone. Growth in emerging market countries is expected to remain

| | | | |

| Western Asset Global Multi-Sector Fund | | | V | |

higher than in their developed country counterparts, and the IMF projects that emerging market growth will increase from 5.1% in 2012 to 5.5% in 2013. In particular, China’s economy is expected to grow 8.2% in 2013, versus 7.8% in 2012. Elsewhere, the IMF projects that growth in India will increase from 4.5% in 2012 to 5.9% in 2013.

The Federal Reserve Board (“Fed”)iii took a number of actions as it sought to meet its dual mandate of fostering maximum employment and price stability. As has been the case since December 2008, the Fed kept the federal funds rateiv at a historically low range between zero and 0.25%. In January 2012, the Fed extended the period it expects to keep rates on hold until at least through late 2014. At its June 2012 meeting, the Fed announced that it would continue its program of purchasing longer-term Treasury securities and selling an equal amount of shorter-term Treasury securities (often referred to as “Operation Twist”) until the end of 2012. In September, the Fed announced a third round of quantitative easing (“QE3”), which involves purchasing $40 billion each month of agency mortgage-backed securities on an open-end basis. In addition, the Fed further extended the duration that it expects to keep the federal funds rate on hold, until at least mid-2015. Finally, at its meeting in December, the Fed announced that it would continue purchasing $40 billion per month of agency mortgage-backed securities, as well as initially purchasing $45 billion a month of longer-term Treasuries. The Fed also said that it would keep the federal funds rate on hold “…as long as the unemployment rate remains above 6.5%, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2.0% longer-run goal, and longer-term inflation expectations continue to be well anchored.”

Given the economic challenges in the Eurozone, the European Central Bank (“ECB”)v lowered interest rates from 1.50% to 1.25% in November 2011 and to 1.00% the following month. In July 2012, the ECB cut rates from 1.00% to 0.75%, a record low. In September the ECB introduced its Outright Monetary Transactions program (“OMT”). With the OMT, the ECB can purchase an unlimited amount of bonds that are issued by troubled Eurozone countries, provided the countries formally ask to participate in the program and agree to certain conditions. In other developed countries, the Bank of England kept rates on hold at 0.50% during the reporting period, as did Japan at a range of zero to 0.10%, its lowest level since 2006. In September, the Bank of Japan announced that it would increase its asset-purchase program and extend its duration by six months until the end of 2013. Elsewhere, with growth rates declining, both China and India lowered their cash reserve ratio for banks. China also cut its key interest rate in early June and again in July.

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

R. Jay Gerken, CFA

President

January 31, 2013

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. Forecasts and predictions are inherently limited and should not be relied upon as an indication of actual or future performance.

| | |

| VI | | Western Asset Global Multi-Sector Fund |

Investment commentary (cont’d)

| i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| ii | The Institute for Supply Management’s PMI is based on a survey of purchasing executives who buy the raw materials for manufacturing at more than 350 companies. It offers an early reading on the health of the manufacturing sector. |

| iii | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| iv | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| v | The European Central Bank (“ECB”) is responsible for the monetary system of the European Union and the euro currency. |

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 1 | |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund’s investment objective is to maximize return through income and capital appreciation. To achieve its investment objective, the Fund invests primarily in various types of U.S. dollar denominated and non-U.S. dollar denominated fixed-income securities.

The Fund may invest up to 70% of its net assets in securities not rated Baa or BBB or above at the time of purchase by one or more nationally recognized statistical rating organizations (“NRSROs”) or unrated securities that we determine to be of comparable quality at the time of purchase. Securities rated Baa or BBB or above by one or more NRSROs or unrated securities of comparable quality are known as “investment grade securities.” Securities rated below investment grade are commonly known as “junk bonds” or “high-yield securities.” Under normal market conditions, the Fund will invest at least 80% of its net assets in securities of issuers representing at least three countries (one of which may be the U.S.).

The Fund may also enter into various derivative transactions for both hedging and non-hedging purposes, including for purposes of enhancing returns. These derivative transactions include, but are not limited to, futures, options, swaps and forwards.

In particular, the Fund may use interest rate swaps, credit default swaps (on individual securities and/or baskets of securities), futures contracts, options, corporate loans and/or mortgage-backed securities to a significant extent, although the amounts invested in these instruments may change from time to time. Other instruments may also be used to a significant extent from time to time.

At Western Asset Management Company (“Western Asset”), the Fund’s subadviser, we utilize a fixed-income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio management personnel, research analysts and an in-house economist. Under this team approach, management of client fixed-income portfolios will reflect a consensus of interdisciplinary views within the Western Asset organization.

Q. What were the overall market conditions during the Fund’s reporting period?

A. The spread sectors (non-Treasuries) overcame several periods of heightened risk aversion and outperformed equal-durationi Treasuries over the twelve months ended December 31, 2012. To a great extent, demand for the spread sectors was robust during the first two months of the reporting period. This was due to several factors, including signs that the U.S. economy was gathering momentum and some progress in the European sovereign debt crisis. However, concerns that the economy may be experiencing a soft patch and contagion fears from Europe led to flights to quality during portions of March, April and May 2012. The spread sectors then generally rallied over the last seven months of the period as investor sentiment was largely positive.

Short-term U.S. Treasury yields fluctuated in 2012, but ended the year where they began. In contrast, 10-year Treasury yields fell from 1.89% to 1.78% during the twelve months ended December 31, 2012. On July 25, 2012, ten-year Treasuries closed at an all-time low of 1.43%. U.S. yields then moved higher due to some positive developments in Europe and additional Federal Reserve Board (“Fed”)ii actions to stimulate the economy. In Europe, the European Central Bank (“ECB”)iii cut its official lending rate by 0.25% to 0.75% during the third quarter of 2012 and announced details of

| | |

| 2 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Fund overview (cont’d)

its Outright Monetary Transactions (“OMT”) program aimed at driving down rates in peripheral countries. German government bond yields declined from 0.82% at the start of the reporting period to 0.30% at the end of 2012, and they outperformed their U.S. counterparts during the year as a whole.

All told, the Barclays U.S. Aggregate Indexiv returned 4.22% for the twelve months ended December 31, 2012. Comparatively, riskier fixed-income securities, including high-yield bonds and emerging market debt, produced superior results. Over the fiscal year, the Barclays U.S. Corporate High Yield — 2% Issuer Cap Indexv, gained 15.78%. During this period, as measured by the Barclays U.S. Corporate High Yield — 2% Issuer Cap Index, lower-quality CCC-rated bonds outperformed higher-quality BB-rated securities, as they returned 18.34% and 14.49%, respectively. The emerging market debt asset class, as measured by the JPMorgan Emerging Markets Bond Index Plus (“EMBI+”)vi, returned 18.04% over the same period.

Q. How did we respond to these changing market conditions?

A. A number of adjustments were made to the Fund during the reporting period. The primary adjustments were taking advantage of the strong returns in the credit markets to reduce our allocations to investment grade corporate bonds and U.S. dollar-denominated high-yield bonds. In contrast, we increased our exposure to select European high-yield issuers, as well as U.S. dollar-denominated emerging market sovereign and corporate debt. We also added to the Fund’s exposure to select emerging market local currency bonds, such as South Africa, and increased our allocation to higher yielding emerging market currencies, including the Indian rupee, the Brazilian real and the Mexican peso. Within the U.S., we increased our allocation to agency mortgage-backed securities (“MBS”). We reduced our exposure to U.S. Treasuries in favor of German government bonds in anticipation of more accommodative monetary policy from the ECB. Within the currency market, we moved to an underweight position in the Japanese yen. Finally, the Fund’s allocation to cash position was decreased during the reporting period.

The Fund used U.S. Treasury futures to manage our duration and yield curvevii exposure. The use of these instruments detracted from performance. Currency forwards, which were used to manage our foreign currency exposure, were also negative for results. We used credit default swaps to hedge out some of the high-yield exposure in the Fund. These also detracted from performance. Currency put options were also used, which had a positive impact on performance.

Performance review

For the twelve months ended December 31, 2012, Class I shares of Western Asset Global Multi-Sector Fund returned 9.78%. The Fund’s unmanaged benchmarks, the Barclays Global Aggregate Indexviii, the EMBI+ and the Barclays U.S. Corporate High Yield — 2% Issuer Cap Index, returned 4.32%, 18.04% and 15.78%, respectively, for the same period. The Lipper Multi-Sector Income Funds Category Average1 returned 11.21% over the same time frame.

| 1 | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the twelve-month period ended December 31, 2012, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 229 funds in the Fund’s Lipper category, and excluding sales charges. |

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 3 | |

| | | | | | | | |

Performance Snapshot as of December 31, 2012

(unaudited) | |

| (excluding sales charges) | | 6 months | | | 12 months | |

| Western Asset Global Multi-Sector Fund: | |

Class A | | | 5.67 | % | | | N/A | |

Class C | | | 5.29 | % | | | N/A | |

Class FI | | | 5.82 | % | | | 9.41 | % |

Class R | | | 5.58 | % | | | N/A | |

Class I | | | 5.92 | % | | | 9.78 | % |

Class IS | | | 6.00 | % | | | 9.80 | % |

| Barclays Global Aggregate Index | | | 2.78 | % | | | 4.32 | % |

| EMBI+ | | | 10.41 | % | | | 18.04 | % |

| Barclays U.S. Corporate High Yield — 2% Issuer Cap Index | | | 7.97 | % | | | 15.78 | % |

| Lipper Multi-Sector Income Funds1 | | | 5.99 | % | | | 11.21 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value, investment returns and yields will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, please visit our website at www.leggmason.com/individualinvestors.

All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all Fund expenses. Returns have not been adjusted to include sales charges that may apply or the deduction of taxes that a shareholder would pay on Fund distributions. If sales charges were reflected, the performance quoted would be lower. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

Fund performance figures reflect fee waivers and/or expense reimbursements, without which the performance would have been lower.

The 30-Day SEC Yields for the period ended December 31, 2012 for Class A, Class C, Class FI, Class R, Class I and Class IS shares were 2.03%, 1.38%, 2.17%, 1.93%, 2.87% and 2.62%, respectively. Absent fee waivers and/or expense reimbursements, the 30-Day SEC Yields for Class A, Class C, Class R and Class IS shares would have been 1.26%, 0.46%, 0.92% and 1.73%, respectively. The 30-Day SEC Yield is subject to change and is based on the yield to maturity of the Fund’s investments over a 30-day period and not on the dividends paid by the Fund, which may differ.

|

| Total Annual Operating Expenses (unaudited) |

As of the Fund’s current prospectus dated May 1, 2012, as supplemented on May 31, 2012, the gross total annual operating expense ratios for Class A, Class C, Class FI, Class R, Class I and Class IS shares were 1.78%, 2.53%, 2.86%, 2.08%, 2.61% and 1.38%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Fund expense ratios are more likely to increase when markets are volatile.

As a result of expense limitation arrangements, the ratio of expenses, other than interest, brokerage commissions, taxes, extraordinary expenses and deferred organizational expenses, to average net assets is not expected to exceed 1.25% for Class A shares, 2.00% for Class C shares, 1.20% for Class FI shares, 1.45% for Class R shares, 0.85% for Class I shares and 0.75% for Class IS shares. These expense limitation arrangements cannot be terminated prior to December 31, 2014 without the Board of Directors’ consent.

The manager is permitted to recapture amounts waived and/or reimbursed to a class within two years after the fiscal year in which the manager earned the fee or incurred the expense if the class’ total annual operating expenses have fallen to a level below the expense limitation (“expense cap”) in effect at the time the fees were earned or the expenses incurred. In no case will the manager recapture any amount that would result, on any particular business day of the Fund, in the class’ total annual operating expenses exceeding the expense cap or any other lower limit then in effect.

| 1 | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the period ended December 31, 2012, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 249 funds for the six-month period and among the 229 funds for the twelve-month period in the Fund’s Lipper category, and excluding sales charges. |

| | |

| 4 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Fund overview (cont’d)

Q. What were the leading contributors to performance?

A. The largest contributor to the Fund’s relative performance during the reporting period was our duration positioning in the U.S. and Europe. We increased our short duration position in the U.S. during the first half of the year. This was beneficial as U.S. rates moved higher during the second half of the period. Increasing duration in Europe was also beneficial, as their rates declined during the reporting period as a whole.

Also contributing to performance was our underweight to Japanese government bonds given their weak performance. An overweight to local emerging market government bonds was also rewarded during the period.

Currency positioning, overall, was another area of strength for the Fund. Adding the most value was our underweight position in the yen. It fell sharply in December as newly elected Prime Minister Shinzo Abe vowed to take “truly meaningful measures” to weaken the yen to help boost the country’s weakening economy.

Q. What were the leading detractors from performance?

A. The largest detractor from the Fund’s relative performance for the period was our underweight to U.S.-denominated emerging market sovereign bonds, as they outperformed both emerging market corporate bonds within the EMBI+.

Our yield curve positioning was a slight negative for results. In particular, our focus on the long end of the U.S. curve was detrimental, as those rates moved higher compared to shorter dated bonds during the reporting period.

Elsewhere, moving to an overweight to agency mortgage-backed securities during the second half of the year detracted from performance as they performed poorly over that period.

Thank you for your investment in Western Asset Global Multi-Sector Fund. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company

January 18, 2013

RISKS: Fixed-income securities involve interest rate, credit, inflation and reinvestment risks. As interest rates rise, the value of fixed-income securities falls. High-yield securities possess greater price volatility, illiquidity and possibility of default. Asset-backed, mortgage-backed or mortgage-related securities are subject to prepayment and extension risks. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Derivatives, such as options and futures, can be illiquid, may disproportionately increase losses and have a potentially large impact on Fund performance. The Fund is a “non-diversified” fund. As a result, the value of its shares will be more susceptible to any single economic, political or regulatory event affecting one or a small umber of issuers than shares of a “diversified fund.” Please see the Fund’s prospectus for a more complete discussion of these and other risks, and the Fund’s investment strategies.

Portfolio holdings and breakdowns are as of December 31, 2012 and are subject to change and may not be representative of the Portfolio managers’ current or future investments. Please refer to pages 12 through 19 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 5 | |

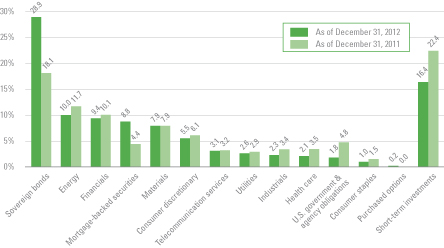

sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio managers’ current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2012 were: Sovereign Bonds (29.8%), Energy (10.3%), Financials (9.6%), Mortgage-Backed Securities (9.1%) and Materials (8.2%). The Fund’s portfolio composition is subject to change at any time.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| i | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| ii | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| iii | The European Central Bank is responsible for the monetary system of the European Union and the euro currency. |

| iv | The Barclays U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| v | The Barclays U.S. Corporate High Yield — 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Barclays U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. |

| vi | The JPMorgan Emerging Markets Bond Index Plus (“EMBI+”) is a total return index that tracks the traded market for U.S. dollar-denominated Brady and other similar sovereign restructured bonds traded in the emerging markets. |

| vii | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

| viii | The Barclays Global Aggregate Index is an index comprised of several other Barclays indices that measure fixed-income performance of regions around the world. |

| | |

| 6 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Fund at a glance† (unaudited)

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of December 31, 2012 and December 31, 2011 and does not include derivatives such as futures contracts, swap contracts and forward foreign currency contracts. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 7 | |

Fund expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments; and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on July 1, 2012 and held for the six months ended December 31, 2012.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Based on actual total return1 | | | | | Based on hypothetical total return1 | |

| | | Actual

Total Return

Without

Sales

Charge2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

the

Period3 | | | | | | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

the

Period3 | |

Class A | | | 5.67 | % | | $ | 1,000.00 | | | $ | 1,056.70 | | | | 1.25 | % | | $ | 6.46 | | | | | Class A | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,018.85 | | | | 1.25 | % | | $ | 6.34 | |

Class C | | | 5.29 | | | | 1,000.00 | | | | 1,052.90 | | | | 2.00 | | | | 10.32 | | | | | Class C | | | 5.00 | | | | 1,000.00 | | | | 1,015.08 | | | | 2.00 | | | | 10.13 | |

Class FI | | | 5.82 | | | | 1,000.00 | | | | 1,058.20 | | | | 1.20 | | | | 6.21 | | | | | Class FI | | | 5.00 | | | | 1,000.00 | | | | 1,019.10 | | | | 1.20 | | | | 6.09 | |

Class R | | | 5.58 | | | | 1,000.00 | | | | 1,055.80 | | | | 1.44 | | | | 7.44 | | | | | Class R | | | 5.00 | | | | 1,000.00 | | | | 1,017.90 | | | | 1.44 | | | | 7.30 | |

Class I | | | 5.92 | | | | 1,000.00 | | | | 1,059.20 | | | | 0.79 | | | | 4.09 | | | | | Class I | | | 5.00 | | | | 1,000.00 | | | | 1,021.17 | | | | 0.79 | | | | 4.01 | |

Class IS | | | 6.00 | | | | 1,000.00 | | | | 1,060.00 | | | | 0.75 | | | | 3.88 | | | | | Class IS | | | 5.00 | | | | 1,000.00 | | | | 1,021.37 | | | | 0.75 | | | | 3.81 | |

| 1 | For the six months ended December 31, 2012. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charge (“CDSC”) with respect to Class C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 366. |

| | |

| 8 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Fund performance (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | |

| Average annual total returns | | | | | | | | | | | | | | | | |

| Without sales charges1 | | Class A† | | | Class C† | | | Class FI | | | Class R† | | | Class I | | | Class IS | |

| Twelve Months Ended 12/31/12 | | | N/A | | | | N/A | | | | 9.41 | % | | | N/A | | | | 9.78 | % | | | 9.80 | % |

| Inception* through 12/31/12 | | | 5.38 | % | | | 4.88 | % | | | 6.31 | | | | 5.26 | % | | | 6.65 | | | | 6.74 | |

| | | | | | |

| With sales charges2 | | Class A† | | | Class C† | | | Class FI | | | Class R† | | | Class I | | | Class IS | |

| Twelve Months Ended 12/31/12 | | | N/A | | | | N/A | | | | 9.41 | % | | | N/A | | | | 9.78 | % | | | 9.80 | % |

| Inception* through 12/31/12 | | | 0.94 | % | | | 3.88 | % | | | 6.31 | | | | 5.26 | % | | | 6.65 | | | | 6.74 | |

| | | | |

| Cumulative total returns | | | |

| Without sales charges1 | | | |

| Class A (Inception date of 4/30/12 through 12/31/12) | | | 5.38 | % |

| Class C (Inception date of 4/30/12 through 12/31/12) | | | 4.88 | |

| Class FI (Inception date of 7/29/11 through 12/31/12) | | | 9.12 | |

| Class R (Inception date of 4/30/12 through 12/31/12) | | | 5.26 | |

| Class I (Inception date of 7/29/11 through 12/31/12) | | | 9.62 | |

| Class IS (Inception date of 7/29/11 through 12/31/12) | | | 9.75 | |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

| 1 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class C shares. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. In addition, Class A shares reflect the deduction of the maximum initial sales charge of 4.25%. Class C shares reflect the deduction of a 1.00% CDSC, which applies if shares are redeemed within one year from purchase payment. |

| * | Inception dates for Class A, C, FI, R, I and IS shares are April 30, 2012, April 30, 2012, July 29, 2011, April 30, 2012, July 29, 2011 and July 29, 2011, respectively. |

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 9 | |

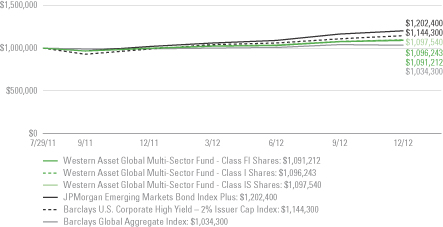

Historical performance

Value of $1,000,000 invested in

Class FI, I and IS Shares of Western Asset Global Multi-Sector Fund vs. Barclays Global Aggregate Index, JPMorgan Emerging Markets Bond Index Plus and Barclays U.S. Corporate High Yield – 2% Issuer Cap Index† — July 29, 2011 - December 2012

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

| † | Hypothetical illustration of $1,000,000 invested in Class FI, I and IS shares of Western Asset Global Multi-Sector Fund on July 29, 2011 (inception date), assuming the reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2012. The hypothetical illustration also assumes a $1,000,000 investment the Barclays Global Aggregate Index, the JPMorgan Emerging Markets Bond Index Plus and the Barclays U.S. Corporate High Yield – 2% Issuer Cap Index. The Barclays Capital Global Aggregate Index is an index comprised of several other Barclays indices that measure fixed-income performance of regions around the world. The JPMorgan Emerging Markets Bond Index Plus (“EMBI+”) is a total return index that tracks the traded market for U.S. dollar-denominated Brady and other similar sovereign restructured bonds traded in the emerging markets. The Barclays U.S. Corporate High Yield – 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Barclays U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. The Indices are unmanaged and not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. The performance of the Fund’s other classes may be greater or less than the performance of Class IS, I and FI shares indicated on this chart, depending on whether greater or lesser sales charges and fees were incurred by shareholders investing in the other classes. |

| | |

| 10 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

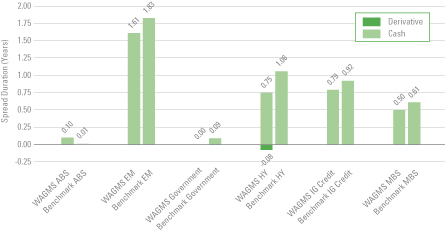

Spread duration (unaudited)

Economic exposure — December 31, 2012

Spread duration measures the sensitivity to changes in spreads. The spread over Treasuries is the annual risk-premium demanded by investors to hold non-Treasury securities. Spread duration is quantified as the % change in price resulting from a 100 basis points change in spreads. For a security with positive spread duration, an increase in spreads would result in a price decline and a decline in spreads would result in a price increase. This chart highlights the market sector exposure of the Fund’s sectors relative to the selected benchmark sectors as of the end of the reporting period.

| | |

| ABS | | — Asset-Backed Securities |

| Benchmark | | — 50% Barclays Global Aggregate Index, 25% JPMorgan Emerging Markets Bond Index Plus and 25% Barclays U.S. Corporate High Yield — 2% Issuer Cap Index |

| EM | | — Emerging Markets |

| HY | | — High Yield |

| IG Credit | | — Investment Grade Credit |

| MBS | | — Mortgage-Backed Securities |

| WAGMS | | — Western Asset Global Multi-Sector Fund |

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 11 | |

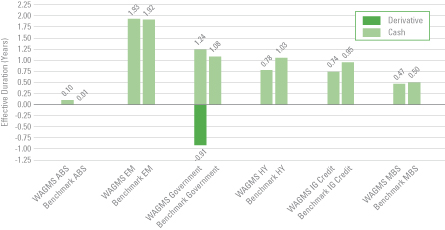

Effective duration (unaudited)

Interest rate exposure — December 31, 2012

Effective duration measures the sensitivity to changes in relevant interest rates. Effective duration is quantified as the % change in price resulting from a 100 basis points change in interest rates. For a security with positive effective duration, an increase in interest rates would result in a price decline and a decline in interest rates would result in a price increase. This chart highlights the interest rate exposure of the Fund’s sectors relative to the selected benchmark sectors as of the end of the reporting period.

| | |

| ABS | | — Asset-Backed Securities |

| Benchmark | | — 50% Barclays Global Aggregate Index, 25% JPMorgan Emerging Markets Bond Index Plus and 25% Barclays U.S. Corporate High Yield — 2% Issuer Cap Index |

| EM | | — Emerging Markets |

| HY | | — High Yield |

| IG Credit | | — Investment Grade Credit |

| MBS | | — Mortgage-Backed Securities |

| WAGMS | | — Western Asset Global Multi-Sector Fund |

| | |

| 12 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Schedule of investments

December 31, 2012

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount† | | | Value | |

| Corporate Bonds & Notes — 45.3% | | | | | | | | | | | | | | |

| Consumer Discretionary — 5.6% | | | | | | | | | | | | | | |

Auto Components — 0.5% | | | | | | | | | | | | | | |

Continental Rubber of America Corp., Senior Secured Notes | | | 4.500 | % | | 9/15/19 | | | 150,000 | | | $ | 153,509 | (a) |

Automobiles — 1.3% | | | | | | | | | | | | | | |

Ford Motor Credit Co., LLC, Senior Notes | | | 8.125 | % | | 1/15/20 | | | 100,000 | | | | 128,138 | |

Ford Motor Credit Co., LLC, Senior Notes | | | 5.875 | % | | 8/2/21 | | | 250,000 | | | | 291,134 | |

Total Automobiles | | | | | | | | | | | | | 419,272 | |

Hotels, Restaurants & Leisure — 0.4% | | | | | | | | | | | | | | |

Codere Finance Luxembourg SA, Senior Secured Notes | | | 8.250 | % | | 6/15/15 | | | 50,000 | EUR | | | 54,448 | (a) |

Marstons Issuer PLC, Secured Bonds | | | 5.177 | % | | 7/15/32 | | | 50,000 | GBP | | | 75,681 | (b) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | 130,129 | |

Media — 2.8% | | | | | | | | | | | | | | |

CCO Holdings LLC/CCO Holdings Capital Corp., Senior Notes | | | 7.000 | % | | 1/15/19 | | | 100,000 | | | | 107,875 | |

Comcast Corp., Senior Notes | | | 5.150 | % | | 3/1/20 | | | 50,000 | | | | 59,263 | |

DISH DBS Corp., Senior Notes | | | 6.750 | % | | 6/1/21 | | | 100,000 | | | | 114,000 | |

Grupo Televisa SA, Senior Bonds | | | 6.625 | % | | 1/15/40 | | | 100,000 | | | | 127,579 | |

Nara Cable Funding Ltd., Senior Secured Notes | | | 8.875 | % | | 12/1/18 | | | 80,000 | | | | 81,400 | (a) |

Time Warner Cable Inc., Senior Notes | | | 4.125 | % | | 2/15/21 | | | 50,000 | | | | 54,756 | |

Time Warner Inc., Senior Notes | | | 4.000 | % | | 1/15/22 | | | 20,000 | | | | 21,894 | |

UPCB Finance III Ltd., Senior Secured Notes | | | 6.625 | % | | 7/1/20 | | | 150,000 | | | | 160,687 | (a) |

Virgin Media Finance PLC, Senior Notes | | | 5.125 | % | | 2/15/22 | | | 100,000 | GBP | | | 164,882 | |

Total Media | | | | | | | | | | | | | 892,336 | |

Specialty Retail — 0.6% | | | | | | | | | | | | | | |

Edcon Proprietary Ltd., Senior Notes | | | 3.433 | % | | 6/15/14 | | | 70,000 | EUR | | | 88,701 | (a)(b) |

Gymboree Corp., Senior Notes | | | 9.125 | % | | 12/1/18 | | | 100,000 | | | | 89,000 | |

Total Specialty Retail | | | | | | | | | | | | | 177,701 | |

Total Consumer Discretionary | | | | | | | | | | | | | 1,772,947 | |

| Consumer Staples — 1.1% | | | | | | | | | | | | | | |

Beverages — 0.6% | | | | | | | | | | | | | | |

Pernod-Ricard SA, Senior Notes | | | 4.450 | % | | 1/15/22 | | | 150,000 | | | | 165,897 | (a) |

Food Products — 0.1% | | | | | | | | | | | | | | |

Ahold Finance USA LLC | | | 6.500 | % | | 3/14/17 | | | 21,000 | GBP | | | 39,661 | |

Tobacco — 0.4% | | | | | | | | | | | | | | |

Alliance One International Inc., Senior Notes | | | 10.000 | % | | 7/15/16 | | | 70,000 | | | | 73,675 | |

Altria Group Inc., Senior Notes | | | 4.750 | % | | 5/5/21 | | | 50,000 | | | | 56,664 | |

Total Tobacco | | | | | | | | | | | | | 130,339 | |

Total Consumer Staples | | | | | | | | | | | | | 335,897 | |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 13 | |

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount† | | | Value | |

| Energy — 10.3% | | | | | | | | | | | | | | |

Energy Equipment & Services — 0.3% | | | | | | | | | | | | | | |

Key Energy Services Inc., Senior Notes | | | 6.750 | % | | 3/1/21 | | | 100,000 | | | $ | 100,000 | |

Oil, Gas & Consumable Fuels — 10.0% | | | | | | | | | | | | | | |

Anadarko Finance Co., Senior Notes | | | 7.500 | % | | 5/1/31 | | | 50,000 | | | | 66,153 | |

Arch Coal Inc., Senior Notes | | | 7.000 | % | | 6/15/19 | | | 250,000 | | | | 232,500 | |

Chesapeake Energy Corp., Senior Notes | | | 6.775 | % | | 3/15/19 | | | 40,000 | | | | 40,050 | |

Chesapeake Energy Corp., Senior Notes | | | 6.625 | % | | 8/15/20 | | | 20,000 | | | | 21,450 | |

Compagnie Generale de Geophysique-Veritas, Senior Notes | | | 9.500 | % | | 5/15/16 | | | 300,000 | | | | 321,750 | |

Devon Energy Corp., Senior Notes | | | 5.600 | % | | 7/15/41 | | | 50,000 | | | | 59,392 | |

Ecopetrol SA, Senior Notes | | | 7.625 | % | | 7/23/19 | | | 100,000 | | | | 129,250 | |

Enterprise Products Operating LLP, Subordinated Notes | | | 7.034 | % | | 1/15/68 | | | 80,000 | | | | 91,600 | (b) |

EXCO Resources Inc., Senior Notes | | | 7.500 | % | | 9/15/18 | | | 100,000 | | | | 97,000 | |

Hiland Partners LP/Hiland Partners Finance Corp., Senior Notes | | | 7.250 | % | | 10/1/20 | | | 30,000 | | | | 32,100 | (a) |

LUKOIL International Finance BV, Bonds | | | 6.656 | % | | 6/7/22 | | | 200,000 | | | | 243,500 | (a) |

Pan American Energy LLC, Senior Notes | | | 7.875 | % | | 5/7/21 | | | 92,000 | | | | 79,350 | (a) |

Peabody Energy Corp., Senior Notes | | | 6.500 | % | | 9/15/20 | | | 100,000 | | | | 107,250 | |

Pemex Project Funding Master Trust, Senior Bonds | | | 6.625 | % | | 6/15/35 | | | 220,000 | | | | 279,400 | |

Petrobras International Finance Co., Senior Notes | | | 6.875 | % | | 1/20/40 | | | 10,000 | | | | 12,704 | |

Petrobras International Finance Co., Senior Notes | | | 6.750 | % | | 1/27/41 | | | 200,000 | | | | 253,418 | |

Petroleos Mexicanos, Senior Notes | | | 6.500 | % | | 6/2/41 | | | 30,000 | | | | 37,650 | |

Plains Exploration & Production Co., Senior Notes | | | 8.625 | % | | 10/15/19 | | | 100,000 | | | | 113,750 | |

QEP Resources Inc., Senior Notes | | | 5.375 | % | | 10/1/22 | | | 190,000 | | | | 203,775 | |

Quicksilver Resources Inc., Senior Notes | | | 11.750 | % | | 1/1/16 | | | 30,000 | | | | 29,625 | |

Range Resources Corp., Senior Notes | | | 5.000 | % | | 8/15/22 | | | 120,000 | | | | 125,400 | |

Range Resources Corp., Senior Subordinated Notes | | | 5.750 | % | | 6/1/21 | | | 10,000 | | | | 10,700 | |

Regency Energy Partners LP/Regency Energy Finance Corp., Senior Notes | | | 6.500 | % | | 7/15/21 | | | 150,000 | | | | 164,250 | |

Southern Gas Networks PLC, Senior Notes | | | 4.875 | % | | 12/21/20 | | | 80,000 | GBP | | | 147,093 | |

Tesoro Logistics LP/Tesoro Logistics Finance Corp., Senior Notes | | | 5.875 | % | | 10/1/20 | | | 60,000 | | | | 62,250 | (a) |

TNK-BP Finance SA, Senior Notes | | | 7.875 | % | | 3/13/18 | | | 110,000 | | | | 133,529 | (a) |

WPX Energy Inc., Senior Notes | | | 6.000 | % | | 1/15/22 | | | 40,000 | | | | 43,100 | |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | 3,137,989 | |

Total Energy | | | | | | | | | | | | | 3,237,989 | |

| Financials — 9.6% | | | | | | | | | | | | | | |

Capital Markets — 1.9% | | | | | | | | | | | | | | |

Boparan Finance PLC, Senior Notes | | | 9.875 | % | | 4/30/18 | | | 100,000 | GBP | | | 183,563 | (a) |

See Notes to Financial Statements.

| | |

| 14 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Schedule of investments (cont’d)

December 31, 2012

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount† | | | Value | |

Capital Markets — continued | | | | | | | | | | | | | | |

Goldman Sachs Group Inc., Subordinated Notes | | | 4.750 | % | | 10/12/21 | | | 50,000 | EUR | | $ | 70,179 | |

Merrill Lynch & Co. Inc., Notes | | | 5.500 | % | | 11/22/21 | | | 60,000 | GBP | | | 103,934 | |

Morgan Stanley, Senior Notes | | | 4.375 | % | | 10/12/16 | | | 50,000 | EUR | | | 71,400 | |

Thames Water Kemble Finance PLC, Senior Secured Notes | | | 7.750 | % | | 4/1/19 | | | 100,000 | GBP | | | 176,253 | (a) |

Total Capital Markets | | | | | | | | | | | | | 605,329 | |

Commercial Banks — 2.6% | | | | | | | | | | | | | | |

Abbey National Treasury Services PLC, Senior Secured Notes | | | 5.125 | % | | 4/14/21 | | | 100,000 | GBP | | | 192,037 | |

Barclays Bank PLC, Senior Notes | | | 6.000 | % | | 1/14/21 | | | 160,000 | EUR | | | 238,724 | (a) |

HSBC Capital Funding LP, Junior Subordinated Bonds | | | 5.369 | % | | 3/24/14 | | | 100,000 | EUR | | | 131,731 | (b)(c) |

Lloyds TSB Bank PLC, Subordinated Notes | | | 6.500 | % | | 3/24/20 | | | 100,000 | EUR | | | 150,765 | |

Wachovia Capital Trust III, Junior Subordinated Bonds | | | 5.570 | % | | 2/19/13 | | | 100,000 | | | | 99,500 | (b)(c) |

Total Commercial Banks | | | | | | | | | | | | | 812,757 | |

Consumer Finance — 1.8% | | | | | | | | | | | | | | |

Ally Financial Inc., Senior Notes | | | 8.300 | % | | 2/12/15 | | | 100,000 | | | | 111,375 | |

Ally Financial Inc., Senior Notes | | | 5.500 | % | | 2/15/17 | | | 90,000 | | | | 96,279 | |

Ally Financial Inc., Senior Notes | | | 8.000 | % | | 3/15/20 | | | 200,000 | | | | 245,000 | |

SLM Corp., Medium-Term Notes | | | 8.000 | % | | 3/25/20 | | | 100,000 | | | | 114,250 | |

Total Consumer Finance | | | | | | | | | | | | | 566,904 | |

Diversified Financial Services — 2.3% | | | | | | | | | | | | | | |

Bank of America Corp., Senior Notes | | | 5.000 | % | | 5/13/21 | | | 100,000 | | | | 114,165 | |

Citigroup Inc., Senior Notes | | | 7.375 | % | | 9/4/19 | | | 100,000 | EUR | | | 173,249 | |

General Electric Capital Corp., Senior Notes | | | 6.875 | % | | 1/10/39 | | | 100,000 | | | | 135,930 | |

International Lease Finance Corp., Senior Notes | | | 8.625 | % | | 9/15/15 | | | 20,000 | | | | 22,475 | |

JPMorgan Chase & Co., Senior Notes | | | 4.250 | % | | 10/15/20 | | | 100,000 | | | | 111,213 | |

JPMorgan Chase & Co., Senior Notes | | | 4.500 | % | | 1/24/22 | | | 150,000 | | | | 169,686 | |

Total Diversified Financial Services | | | | | | | | | | | | | 726,718 | |

Insurance — 1.0% | | | | | | | | | | | | | | |

American International Group Inc., Senior Notes | | | 6.400 | % | | 12/15/20 | | | 90,000 | | | | 111,672 | |

ELM BV | | | 5.252 | % | | 5/25/16 | | | 100,000 | EUR | | | 135,295 | (b)(c) |

Hannover Finance Luxembourg SA, Bonds | | | 5.750 | % | | 9/14/40 | | | 50,000 | EUR | | | 75,735 | (b) |

Total Insurance | | | | | | | | | | | | | 322,702 | |

Total Financials | | | | | | | | | | | | | 3,034,410 | |

| Health Care — 2.2% | | | | | | | | | | | | | | |

Biotechnology — 0.3% | | | | | | | | | | | | | | |

Amgen Inc., Senior Notes | | | 3.875 | % | | 11/15/21 | | | 75,000 | | | | 82,364 | |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 15 | |

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount† | | | Value | |

Health Care Providers & Services — 1.2% | | | | | | | | | | | | | | |

Acadia Healthcare Co. Inc., Senior Notes | | | 12.875 | % | | 11/1/18 | | | 40,000 | | | $ | 48,400 | |

HCA Inc., Senior Secured Notes | | | 6.500 | % | | 2/15/20 | | | 200,000 | | | | 225,000 | |

Tenet Healthcare Corp., Senior Secured Notes | | | 8.875 | % | | 7/1/19 | | | 100,000 | | | | 112,000 | |

Total Health Care Providers & Services | | | | | | | | | | | | | 385,400 | |

Pharmaceuticals — 0.7% | | | | | | | | | | | | | | |

ConvaTec Healthcare E SA, Senior Notes | | | 10.875 | % | | 12/15/18 | | | 100,000 | EUR | | | 149,154 | (a) |

Valeant Pharmaceuticals International, Senior Notes | | | 6.375 | % | | 10/15/20 | | | 60,000 | | | | 64,350 | (a) |

Total Pharmaceuticals | | | | | | | | | | | | | 213,504 | |

Total Health Care | | | | | | | | | | | | | 681,268 | |

| Industrials — 2.4% | | | | | | | | | | | | | | |

Aerospace & Defense — 0.3% | | | | | | | | | | | | | | |

Wyle Services Corp., Senior Subordinated Notes | | | 10.500 | % | | 4/1/18 | | | 100,000 | | | | 109,000 | (a) |

Airlines — 0.5% | | | | | | | | | | | | | | |

Continental Airlines Inc., Senior Secured Notes | | | 6.750 | % | | 9/15/15 | | | 140,000 | | | | 147,000 | (a) |

Building Products — 0.5% | | | | | | | | | | | | | | |

Spie BondCo 3 SCA, Senior Notes | | | 11.000 | % | | 8/15/19 | | | 100,000 | EUR | | | 144,204 | (a) |

Construction & Engineering — 0.7% | | | | | | | | | | | | | | |

Odebrecht Finance Ltd. | | | 6.000 | % | | 4/5/23 | | | 200,000 | | | | 231,250 | (a) |

Road & Rail — 0.4% | | | | | | | | | | | | | | |

Kansas City Southern de Mexico SA de CV, Senior Notes | | | 6.125 | % | | 6/15/21 | | | 100,000 | | | | 113,000 | |

Total Industrials | | | | | | | | | | | | | 744,454 | |

| Materials — 8.2% | | | | | | | | | | | | | | |

Chemicals — 0.4% | | | | | | | | | | | | | | |

Braskem Finance Ltd., Senior Notes | | | 7.000 | % | | 5/7/20 | | | 100,000 | | | | 112,750 | (a) |

Construction Materials — 0.7% | | | | | | | | | | | | | | |

Cemex SAB de CV, Senior Secured Notes | | | 9.000 | % | | 1/11/18 | | | 200,000 | | | | 216,500 | (a) |

Containers & Packaging — 1.3% | | | | | | | | | | | | | | |

Ardagh Glass Finance PLC, Senior Bonds | | | 7.125 | % | | 6/15/17 | | | 70,000 | EUR | | | 94,360 | (a) |

Ball Corp., Senior Notes | | | 7.375 | % | | 9/1/19 | | | 100,000 | | | | 111,250 | |

Reynolds Group Issuer Inc./Reynolds Group Issuer LLC/Reynolds Group Issuer (Luxembourg) SA, Senior Notes | | | 9.000 | % | | 4/15/19 | | | 100,000 | | | | 104,000 | |

Reynolds Group Issuer Inc./Reynolds Group Issuer LLC/Reynolds Group Issuer (Luxembourg) SA, Senior Secured Notes | | | 5.750 | % | | 10/15/20 | | | 10,000 | | | | 10,325 | (a) |

Suzano Trading Ltd., Senior Notes | | | 5.875 | % | | 1/23/21 | | | 100,000 | | | | 104,000 | (a) |

Total Containers & Packaging | | | | | | | | | | | | | 423,935 | |

Metals & Mining — 4.3% | | | | | | | | | | | | | | |

ArcelorMittal, Senior Notes | | | 4.250 | % | | 2/25/15 | | | 30,000 | | | | 30,302 | |

See Notes to Financial Statements.

| | |

| 16 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Schedule of investments (cont’d)

December 31, 2012

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount† | | | Value | |

Metals & Mining — continued | | | | | | | | | | | | | | |

ArcelorMittal, Senior Notes | | | 4.250 | % | | 8/5/15 | | | 40,000 | | | $ | 40,403 | |

Cliffs Natural Resources Inc., Senior Notes | | | 3.950 | % | | 1/15/18 | | | 60,000 | | | | 60,389 | |

CSN Resources SA, Senior Bonds | | | 6.500 | % | | 7/21/20 | | | 100,000 | | | | 108,500 | (a) |

Evraz Group SA, Senior Notes | | | 9.500 | % | | 4/24/18 | | | 110,000 | | | | 125,400 | (a) |

FMG Resources (August 2006) Pty Ltd., Senior Notes | | | 6.375 | % | | 2/1/16 | | | 100,000 | | | | 103,500 | (a) |

Gerdau Holdings Inc., Senior Notes | | | 7.000 | % | | 1/20/20 | | | 100,000 | | | | 116,250 | (a) |

Mirabela Nickel Ltd., Senior Notes | | | 8.750 | % | | 4/15/18 | | | 200,000 | | | | 172,000 | (a) |

Southern Copper Corp., Senior Notes | | | 6.750 | % | | 4/16/40 | | | 120,000 | | | | 144,465 | |

Southern Copper Corp., Senior Notes | | | 5.250 | % | | 11/8/42 | | | 70,000 | | | | 70,058 | |

Vale Overseas Ltd., Notes | | | 6.875 | % | | 11/21/36 | | | 110,000 | | | | 136,354 | |

Vedanta Resources PLC, Senior Notes | | | 9.500 | % | | 7/18/18 | | | 200,000 | | | | 230,760 | (a) |

Total Metals & Mining | | | | | | | | | | | | | 1,338,381 | |

Paper & Forest Products — 1.5% | | | | | | | | | | | | | | |

Celulosa Arauco y Constitucion SA, Senior Notes | | | 7.250 | % | | 7/29/19 | | | 100,000 | | | | 118,641 | |

Fibria Overseas Finance Ltd., Senior Notes | | | 6.750 | % | | 3/3/21 | | | 200,000 | | | | 221,500 | (a) |

Inversiones CMPC SA, Senior Notes | | | 4.750 | % | | 1/19/18 | | | 130,000 | | | | 137,047 | (a) |

Total Paper & Forest Products | | | | | | | | | | | | | 477,188 | |

Total Materials | | | | | | | | | | | | | 2,568,754 | |

| Telecommunication Services — 3.2% | | | | | | | | | | | | | | |

Diversified Telecommunication Services — 1.9% | | | | | | | | | | | | | | |

AT&T Inc., Senior Notes | | | 5.350 | % | | 9/1/40 | | | 100,000 | | | | 116,455 | |

Axtel SAB de CV, Senior Notes | | | 9.000 | % | | 9/22/19 | | | 80,000 | | | | 42,400 | (a) |

Intelsat Jackson Holdings SA, Senior Notes | | | 7.250 | % | | 4/1/19 | | | 100,000 | | | | 107,500 | |

Telemar Norte Leste SA, Senior Notes | | | 5.500 | % | | 10/23/20 | | | 100,000 | | | | 104,000 | (a) |

UBS Luxembourg SA for OJSC Vimpel Communications, Loan Participation Notes | | | 8.250 | % | | 5/23/16 | | | 200,000 | | | | 225,760 | (a) |

Verizon Communications Inc., Senior Notes | | | 4.600 | % | | 4/1/21 | | | 10,000 | | | | 11,672 | |

Total Diversified Telecommunication Services | | | | | | | | | | | | | 607,787 | |

Wireless Telecommunication Services — 1.3% | | | | | | | | | | | | | | |

Phones4u Finance PLC, Senior Secured Notes | | | 9.500 | % | | 4/1/18 | | | 100,000 | GBP | | | 169,755 | (a) |

Sprint Capital Corp., Senior Notes | | | 8.750 | % | | 3/15/32 | | | 200,000 | | | | 244,500 | |

Total Wireless Telecommunication Services | | | | | | | | | | | | | 414,255 | |

Total Telecommunication Services | | | | | | | | | | | | | 1,022,042 | |

| Utilities — 2.7% | | | | | | | | | | | | | | |

Electric Utilities — 0.2% | | | | | | | | | | | | | | |

FirstEnergy Corp., Notes | | | 7.375 | % | | 11/15/31 | | | 50,000 | | | | 64,579 | |

Gas Utilities — 0.7% | | | | | | | | | | | | | | |

Empresa de Energia de Bogota SA, Senior Notes | | | 6.125 | % | | 11/10/21 | | | 200,000 | | | | 224,500 | (a) |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 17 | |

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity Date | | Face

Amount† | | | Value | |

Independent Power Producers & Energy Traders — 1.2% | | | | | | | | | | | |

AES Corp., Senior Notes | | | 7.750 | % | | 10/15/15 | | | 20,000 | | | $ | 22,450 | |

AES Corp., Senior Notes | | | 9.750 | % | | 4/15/16 | | | 20,000 | | | | 23,900 | |

AES Gener SA, Notes | | | 5.250 | % | | 8/15/21 | | | 100,000 | | | | 110,985 | (a) |

Atlantic Power Corp., Senior Notes | | | 9.000 | % | | 11/15/18 | | | 70,000 | | | | 73,150 | |

Calpine Construction Finance Co. LP and CCFC Finance Corp., Senior Secured Notes | | | 8.000 | % | | 6/1/16 | | | 150,000 | | | | 159,375 | (a) |

Total Independent Power Producers & Energy Traders | | | | | | | 389,860 | |

Water Utilities — 0.6% | | | | | | | | | | | | | | |

Anglian Water Osprey Financing PLC, Senior Secured Notes | | | 7.000 | % | | 1/31/18 | | | 100,000 | GBP | | | 176,009 | |

Total Utilities | | | | | | | | | | | | | 854,948 | |

Total Corporate Bonds & Notes (Cost — $13,309,157) | | | | | | | 14,252,709 | |

| Mortgage-Backed Securities — 9.1% | | | | | | | | | | | | | | |

FHLMC — 0.4% | | | | | | | | | | | | | | |

Federal Home Loan Mortgage Corp. (FHLMC) | | | 3.500 | % | | 8/1/42 | | | 99,052 | | | | 105,723 | |

FNMA — 7.7% | | | | | | | | | | | | | | |

Federal National Mortgage Association (FNMA) | | | 3.000 | % | | 1/17/28-1/14/43 | | | 1,400,000 | | | | 1,469,235 | (d) |

Federal National Mortgage Association (FNMA) | | | 3.500 | % | | 1/17/28-1/14/43 | | | 700,000 | | | | 745,222 | (d) |

Federal National Mortgage Association (FNMA) | | | 4.000 | % | | 1/14/43 | | | 200,000 | | | | 214,375 | (d) |

Total FNMA | | | | | | | | | | | | | 2,428,832 | |

GNMA — 1.0% | | | | | | | | | | | | | | |

Government National Mortgage Association (GNMA) I | | | 3.000 | % | | 1/22/43 | | | 300,000 | | | | 318,891 | (d) |

Total Mortgage-Backed Securities (Cost — $2,854,849) | | | | | | | 2,853,446 | |

| Sovereign Bonds — 29.8% | | | | | | | | | | | | | | |

Argentina — 0.3% | | | | | | | | | | | | | | |

Republic of Argentina, Senior Bonds | | | 7.000 | % | | 10/3/15 | | | 100,000 | | | | 89,269 | |

Brazil — 0.8% | | | | | | | | | | | | | | |

Federative Republic of Brazil, Senior Notes | | | 4.875 | % | | 1/22/21 | | | 200,000 | | | | 241,000 | |

Colombia — 0.8% | | | | | | | | | | | | | | |

Republic of Colombia, Senior Notes | | | 7.375 | % | | 3/18/19 | | | 200,000 | | | | 262,900 | |

Germany — 16.4% | | | | | | | | | | | | | | |

Bundesobligation | | | 0.750 | % | | 2/24/17 | | | 850,000 | EUR | | | 1,148,134 | |

Bundesobligation, Bonds | | | 2.000 | % | | 2/26/16 | | | 500,000 | EUR | | | 700,864 | |

Bundesrepublik Deutschland, Bonds | | | 3.250 | % | | 1/4/20 | | | 1,045,000 | EUR | | | 1,611,515 | |

Bundesrepublik Deutschland, Bonds | | | 3.250 | % | | 7/4/21 | | | 1,100,000 | EUR | | | 1,706,569 | |

Total Germany | | | | | | | | | | | | | 5,167,082 | |

See Notes to Financial Statements.

| | |

| 18 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Schedule of investments (cont’d)

December 31, 2012

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity Date | | Face

Amount† | | | Value | |

India — 0.3% | | | | | | | | | | | | | | |

ICICI Bank Ltd., Subordinated Bonds | | | 6.375 | % | | 4/30/22 | | | 100,000 | | | $ | 100,875 | (a)(b) |

Indonesia — 0.7% | | | | | | | | | | | | | | |

Republic of Indonesia, Notes | | | 5.250 | % | | 1/17/42 | | | 200,000 | | | | 232,250 | (a) |

Malaysia — 1.1% | | | | | | | | | | | | | | |

Government of Malaysia, Senior Bonds | | | 4.262 | % | | 9/15/16 | | | 990,000 | MYR | | | 336,469 | |

Mexico — 1.7% | | | | | | | | | | | | | | |

Mexican Bonos, Bonds | | | 8.000 | % | | 6/11/20 | | | 5,680,000 | MXN | | | 515,654 | |

Mexican Bonos, Bonds | | | 6.500 | % | | 6/9/22 | | | 361,400 | MXN | | | 30,250 | |

Total Mexico | | | | | | | | | | | | | 545,904 | |

Panama — 0.1% | | | | | | | | | | | | | | |

Republic of Panama | | | 6.700 | % | | 1/26/36 | | | 16,000 | | | | 22,720 | |

Peru — 1.3% | | | | | | | | | | | | | | |

Republic of Peru | | | 8.750 | % | | 11/21/33 | | | 130,000 | | | | 225,875 | |

Republic of Peru, Bonds | | | 7.840 | % | | 8/12/20 | | | 396,000 | PEN | | | 195,525 | |

Total Peru | | | | | | | | | | | | | 421,400 | |

Russia — 1.8% | | | | | | | | | | | | | | |

Russian Federation | | | 5.625 | % | | 4/4/42 | | | 200,000 | | | | 248,500 | (a) |

Russian Foreign Bond — Eurobond, Senior Bonds | | | 7.500 | % | | 3/31/30 | | | 232,500 | | | | 298,623 | (a) |

Total Russia | | | | | | | | | | | | | 547,123 | |

South Africa — 1.8% | | | | | | | | | | | | | | |

Republic of South Africa, Bonds | | | 10.500 | % | | 12/21/26 | | | 3,770,000 | ZAR | | | 569,618 | |

Turkey — 0.4% | | | | | | | | | | | | | | |

Republic of Turkey, Senior Bonds | | | 5.625 | % | | 3/30/21 | | | 100,000 | | | | 118,750 | |

Venezuela — 2.3% | | | | | | | | | | | | | | |

Bolivarian Republic of Venezuela, Senior Bonds | | | 9.250 | % | | 9/15/27 | | | 158,000 | | | | 158,000 | |

Bolivarian Republic of Venezuela, Senior Notes | | | 7.750 | % | | 10/13/19 | | | 588,000 | | | | 554,190 | (a) |

Total Venezuela | | | | | | | | | | | | | 712,190 | |

Total Sovereign Bonds (Cost — $8,934,074) | | | | | | | | | | | | | 9,367,550 | |

| U.S. Government & Agency Obligations — 1.8% | | | | | | | | | | | | | | |

U.S. Government Obligations — 1.8% | | | | | | | | | | | | | | |

U.S. Treasury Bonds | | | 3.500 | % | | 2/15/39 | | | 340,000 | | | | 384,360 | |

U.S. Treasury Notes | | | 0.750 | % | | 10/31/17 | | | 30,000 | | | | 30,098 | |

U.S. Treasury Notes | | | 1.250 | % | | 10/31/19 | | | 50,000 | | | | 50,414 | |

U.S. Treasury Notes | | | 2.000 | % | | 2/15/22 | | | 110,000 | | | | 113,756 | |

Total U.S. Government & Agency Obligations (Cost — $492,989) | | | | | | | | | | 578,628 | |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 19 | |

Western Asset Global Multi-Sector Fund

| | | | | | | | | | | | | | |

| Security | | | | | Expiration

Date | | Contracts | | | Value | |

| Purchased Options — 0.2% | | | | | | | | | | | | | | |

U.S. Dollar/Eurodollar, Put @ $1.25 | | | | | | 2/4/13 | | | 2,088,000 | | | $ | 913 | |

U.S. Dollar/Japanese Yen, Put @ $83.00 | | | | | | 2/4/13 | | | 1,490,000 | | | | 60,979 | |

Total Purchased Options (Cost — $23,422) | | | | | | | | | | | | | 61,892 | |

Total Investments before Short-Term Investments (Cost — $25,614,491) | | | | | | | 27,114,225 | |

| | | | |

| | | Rate | | | Maturity

Date | | Face

Amount† | | | | |

| Short-Term Investments — 16.9% | | | | | | | | | | | | | | |

Time Deposits — 7.3% | | | | | | | | | | | | | | |

Commerzbank AG | | | 0.100 | % | | 1/2/13 | | | 500,647 | | | | 500,647 | |

ING Bank | | | 0.130 | % | | 1/2/13 | | | 300,525 | | | | 300,525 | |

Rabobank London | | | 0.060 | % | | 1/2/13 | | | 500,297 | | | | 500,297 | |

Royal Bank of Scotland PLC | | | 0.080 | % | | 1/2/13 | | | 500,534 | | | | 500,534 | |

UBS AG London | | | 0.020 | % | | 1/2/13 | | | 500,359 | | | | 500,359 | |

Total Time Deposits (Cost — $2,302,362) | | | | | | | | | | | | | 2,302,362 | |

Repurchase Agreements — 9.6% | | | | | | | | | | | | | | |

Barclays Capital Inc. repurchase agreement dated 12/31/12; Proceeds at maturity — $3,000,027; (Fully collateralized by U.S. government obligations, 0.250% due 9/15/15; Market value — $3,060,092)

(Cost — $3,000,000) | | | 0.160 | % | | 1/2/13 | | | 3,000,000 | | | | 3,000,000 | |

Total Short-Term Investments (Cost — $5,302,362) | | | | | | | | | | | | | 5,302,362 | |

Total Investments — 103.1% (Cost — $30,916,853#) | | | | | | | | | | | | | 32,416,587 | |

Liabilities in Excess of Other Assets — (3.1)% | | | | | | | | | | | | | (987,283 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | $ | 31,429,304 | |

| † | Face amount denominated in U.S. dollars, unless otherwise noted. |

| (a) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted. |

| (b) | Variable rate security. Interest rate disclosed is as of the most recent information available. |

| (c) | Security has no maturity date. The date shown represents the next call date. |

| (d) | This security is traded on a to-be-announced (“TBA”) basis (See Note 1). |

| # | Aggregate cost for federal income tax purposes is $30,917,429. |

| | |

Abbreviations used in this schedule: |

| EUR | | — Euro |

| GBP | | — British Pound |

| MXN | | — Mexican Peso |

| MYR | | — Malaysian Ringgit |

| OJSC | | — Open Joint Stock Company |

| PEN | | — Peruvian Nuevo Sol |

| ZAR | | — South African Rand |

See Notes to Financial Statements.

| | |

| 20 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Statement of assets and liabilities

December 31, 2012

| | | | |

| |

| Assets: | | | | |

Investments, at value (Cost — $30,916,853) | | $ | 32,416,587 | |

Foreign currency, at value (Cost — $140,581) | | | 141,218 | |

Cash | | | 885,157 | |

Interest receivable | | | 408,860 | |

Receivable for securities sold | | | 604,962 | |

Unrealized appreciation on forward foreign currency contracts | | | 43,421 | |

Deposits with brokers for open futures contracts | | | 40,009 | |

Receivable from broker — variation margin on open futures contracts | | | 7,766 | |

Receivable from investment manager | | | 6,220 | |

Receivable for Fund shares sold | | | 2,500 | |

Foreign currency collateral for open futures contract, at value (Cost — $69,381) | | | 71,054 | |

Prepaid expenses | | | 46,566 | |

Total Assets | | | 34,674,320 | |

| |

| Liabilities: | | | | |

Payable for securities purchased | | | 2,853,527 | |

Unrealized depreciation on forward foreign currency contracts | | | 331,821 | |

Payable for offering and organization costs | | | 9,720 | |

Swaps, at value (premiums paid — $16,163) | | | 3,923 | |

Payable for open swap contracts | | | 937 | |

Service and/or distribution fees payable | | | 39 | |

Accrued expenses | | | 45,049 | |

Total Liabilities | | | 3,245,016 | |

| Total Net Assets | | $ | 31,429,304 | |

| |

| Net Assets: | | | | |

Par value (Note 7) | | $ | 3,009 | |

Paid-in capital in excess of par value | | | 30,253,883 | |

Overdistributed net investment income | | | (11,035) | |

Accumulated net realized loss on investments, futures contracts, swap contracts and foreign currency transactions | | | (30,537) | |

Net unrealized appreciation on investments, futures contracts, swap contracts and foreign currencies | | | 1,213,984 | |

| Total Net Assets | | $ | 31,429,304 | |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 21 | |

| | | | |

| |

| Shares Outstanding: | | | | |

Class A | | | 1,394 | |

Class C | | | 1,002 | |

Class FI | | | 10,422 | |

Class R | | | 1,005 | |

Class I | | | 10,470 | |

Class IS | | | 2,985,081 | |

| |

| Net Asset Value: | | | | |

Class A (and redemption price) | | | $10.47 | |

Class C* | | | $10.47 | |

Class FI (and redemption price) | | | $10.47 | |

Class R (and redemption price) | | | $10.47 | |

Class I (and redemption price) | | | $10.47 | |

Class IS (and redemption price) | | | $10.44 | |

| Maximum Public Offering Price Per Share: | | | | |

Class A (based on maximum initial sales charge of 4.25%) | | | $10.93 | |

| * | Redemption price per share is NAV of Class C shares reduced by 1.00% CDSC, if shares are redeemed within one year from purchase payment (See Note 2). |

See Notes to Financial Statements.

| | |

| 22 | | Western Asset Global Multi-Sector Fund 2012 Annual Report |

Statement of operations

For the Year Ended December 31, 2012

| | | | |

| |

| Investment Income: | | | | |

Interest | | $ | 1,124,303 | |

| |

| Expenses: | | | | |

Investment management fee (Note 2) | | | 176,825 | |

Registration fees | | | 58,230 | |

Legal fees | | | 43,964 | |

Audit and tax | | | 42,615 | |

Shareholder reports (Note 5) | | | 38,251 | |

Fees recaptured by investment manager (Note 2) | | | 29,637 | |

Fund accounting fees | | | 21,455 | |

Custody fees | | | 17,310 | |

Transfer agent fees (Note 5) | | | 3,132 | |

Directors’ fees | | | 1,144 | |

Insurance | | | 459 | |

Service and/or distribution fees (Notes 2 and 5) | | | 382 | |

Miscellaneous expenses | | | 4,517 | |

Total Expenses | | | 437,921 | |

Less: Fee waivers and/or expense reimbursements (Notes 2 and 5) | | | (233,178) | |

Net Expenses | | | 204,743 | |

| Net Investment Income | | | 919,560 | |

| |

| Realized and Unrealized Gain (Loss) on Investments, Futures Contracts, Swap Contracts and Foreign Currency Transactions (Notes 1, 3 and 4): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investment transactions | | | 230,006 | |

Futures contracts | | | (47,400) | |

Swap contracts | | | (64,313) | |

Foreign currency transactions | | | 62,830 | |

Net Realized Gain | | | 181,123 | |

Change in Net Unrealized Appreciation (Depreciation) From: | | | | |

Investments | | | 1,743,772 | |

Futures contracts | | | 16,346 | |

Swap contracts | | | (20,086) | |

Foreign currencies | | | (374,398) | |

Change in Net Unrealized Appreciation (Depreciation) | | | 1,365,634 | |

| Net Gain on Investments, Futures Contracts, Swap Contracts and Foreign Currency Transactions | | | 1,546,757 | |

| Increase in Net Assets from Operations | | $ | 2,466,317 | |

See Notes to Financial Statements.

| | | | |

| Western Asset Global Multi-Sector Fund 2012 Annual Report | | | 23 | |

Statements of changes in net assets

| | | | | | | | |

For the Year Ended December 31, 2012

and the Period Ended December 31, 2011 | | 2012 | | | 2011† | |

| | |

| Operations: | | | | | | | | |

Net investment income | | $ | 919,560 | | | $ | 271,073 | |

Net realized gain (loss) | | | 181,123 | | | | (134,482) | |

Change in net unrealized appreciation (depreciation) | | | 1,365,634 | | | | (151,650) | |