UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2014

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number: 0-27122

ADEPT TECHNOLOGY, INC.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 94-2900635 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| |

| 5960 Inglewood Drive, Pleasanton, CA | | 94588 |

| (Address of principal executive office) | | (Zip Code) |

Registrant’s telephone number, including area code: (925) 245-3400

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

Common Stock, $0.001 par value | | NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

Large accelerated filer ¨ | | Accelerated filer x | | Non-accelerated filer ¨ | | Smaller reporting company ¨ |

| | | | (Do not check if a smaller reporting company) | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold on the Nasdaq Global Market as of the last business day of the registrant’s most recently completed second fiscal quarter (December 28, 2013) was $122,913,993. Shares of common stock held by each officer and director and by each person who beneficially owns 10% or more of common equity of the registrant may be deemed to be affiliates of the registrant.

As of August 15, 2014, approximately 13.1 million shares of the registrant’s common stock, $0.001 par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the 2014 Annual Meeting of Stockholders to be held on November 13, 2014, referred to as the Proxy Statement, are incorporated by reference into Parts I and III hereof.

ADEPT TECHNOLOGY, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

i

PART I

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements principally but not exclusively in the sections entitled “Business,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Controls and Procedures.” In some cases, you can identify forward-looking statements by terms such as “may,” “intend,” “might,” “will,” “should,” “could,” “would,” “expect,” “believe,” “estimate,” “predict,” “potential,” or the negative of these terms, and similar expressions intended to identify forward-looking statements. These statements reflect our current views with respect to future events. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Given these uncertainties, you should not place undue reliance on these statements. We discuss many of these risks and uncertainties in this Annual Report onForm 10-K in greater detail under the heading “Risk Factors.” Also, these statements represent our estimates and assumptions only as of the date of the filing of this Annual Report on Form 10-K with the SEC, and we undertake no obligation to publicly update or revise these forward-looking statements.

In this report, unless the context indicates otherwise, the terms “Adept,” the “Company,” “we,” “us,” and “our” refer to Adept Technology, Inc., a Delaware corporation, and its subsidiaries.

This report contains trademarks and trade names of Adept and other companies. Adept has 203 trademarks of which 12 are registered trademarks, some of which include the Adept Technology logo. Our trademarks include (among others): Adept®, AIM® , HexSight® , AdeptVision® , Motivity® , Adept Cobra™, AdeptQuattro™, AdeptViper™, Adept Python™, Adept SmartServo™, AdeptOne™, AdeptSix™, Adept Anyfeeder™, Adept ACE™, Adept PAC™, SoftPic™, Lynx™, Enterprise Manager™, Motivity™, Seekur™, and PatrolBot™.

Adept is a global, robotics-based automation supplier. Through our integrated offerings of both industrial and mobile robots we help our customers improve the speed, quality and efficiency of their production environments. We design and manufacture industrial and mobile robots along with a complementary suite of control and vision systems and software which are used for assembly, packaging, handling, testing and logistics applications in both fixed repetitive and unstructured environments. These products are offered to our customers along with a broad range of service and support options.

Adept helped pioneer the robotics industry, and with more than 30 years of operating expertise, we continue to lead in the development of innovative robotics solutions to meet the changing needs of automation. Our robotic solutions are targeted at automated applications and processes that require precision, flexibility and high productivity. Through sales to systems integrators, distributors, original equipment manufacturer (“OEM”) partners and end-user companies, we provide flexible, cost-effective robotics systems, software and services to a variety of markets, including electronics, food, semiconductor, warehouse/logistics, medical, and automotive.

Our headquarters are located in Pleasanton, California, and we maintain facilities in New Hampshire, France, Germany, Singapore and China for business operations, sales and customer support. We were founded and incorporated in California in 1983 and reincorporated in Delaware in 2005. Our common stock is traded on the NASDAQ Capital Market under the symbol “ADEP.”

We operate in two segments: Robotics and Services and Support. Revenue from our Robotics segment accounted for approximately 78%, 78%, and 83% of our total revenues in fiscal 2014, 2013 and 2012, respectively. Revenue from our Services and Support segment accounted for approximately 22%, 22%, and 17% of our total revenues in fiscal 2014, 2013 and 2012, respectively. Additional information for these segments is provided in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K.

1

Overview

Key benefits of automation include improved process control, efficiency and productivity, higher and more consistent quality, and improved traceability. For decades, industries such as automotive assembly and electronics have used robotic systems in their manufacturing operations to stay competitive, reduce costs and provide a safer environment for workers. Such industries are heavily dependent on automation to manufacture, assemble and package their products. In many other industries, the use of automation is only just beginning, spurred by changes in the regulatory and competitive environment, and always with a focus on achieving greater productivity at a lower cost.

We classify robots into two categories, fixed (industrial) robots (multi-axis) and mobile robots (autonomous vehicles). Adept manufactures both types of robots and offers many options such as vision and automation control software and related hardware, parts feeding and enterprise-level software. Each application typically has specific capability requirements and the broad technical depth at Adept allows us to offer a diverse selection of products into existing and new high-growth opportunities.

The industrial robots we supply include:

| | • | | SCARA (Selective Compliance Assembly Robot Arm)/four axis |

| | • | | Linear module/Cartesian |

The mobile robots we supply include:

| | • | | Autonomous mobile robots for the transportation of materials |

| | • | | Autonomous mobile robots with an integrated conveyor |

| | • | | Autonomous mobile robots with integrated SCARA for the handling and transport of materials |

| | • | | Autonomous mobile robots for research applications in a non-commercial environment |

Robotic automation continues to be a key enabler for a broad range of applications and industries. Adept robots are ideal in situations that are either hazardous or too repetitive/tedious for non-automated handling by humans, and applications that require high precision and speed, including:

| | • | | Manufacturing parts assembly |

| | • | | Handling - parts/food/packages |

| | • | | Warehouse - order fulfillment |

Markets

Semiconductor

In a semiconductor fab, the two main cost reduction challenges are labor and yield. The Adept Lynx® mobile robot allows labor to be redeployed to high value-add tasks in a fab. In terms of yield, the Lynx reduces errors and drops of SMIF pods (containing expensive semiconductor wafers); eliminates rough handling of SMIF pods;

2

eliminates human “dust”; improves cycle time with automated, optimized wafer movement. Adept’s mobile robots provide unique, cost-effective solutions for both of these challenges.

Packaging

The use of packaging around commercial products continues to increase, as factors such as expediency, variety and safety have become more important to consumers. Additionally, automated packaging can deliver benefits such as convenience, branding or market differentiation. Increased use of packaging in various consumer products is fueling the need for automation to address the challenges that arise in the packaging process. These challenges include the need for flexibility, the need to maintain a clean or sterile environment, the ability to process high volumes and the ability to track products that are perishable or that may pose future unknown risks. Cost considerations are also an important catalyst for automated packaging, particularly in applications such as food, where products are often packaged locally for various reasons including freshness, regional branding or specific regulatory requirements. Automation is often a more cost efficient alternative to maintaining a relatively larger number of employees as productivity can be achieved more quickly, in less space and with less risk of contamination.

Electronics

The combination of high product volumes and continual price erosion in the electronics market has long created demand for the use of automation to ensure the highest yields at the lowest cost. Automation solutions are used to help manufacture and assemble a host of electronic products such as computer disk drives, cell phones and printer cartridges and components. This market is very cyclical in terms of its investment in automation technology, with periods of significant investment in adding capacity or enhancing existing systems typically followed by periods of relatively low investment. As the product lifecycle for consumer electronics continues to shorten, manufacturers need increasingly flexible automation lines enabled by robotic solutions.

Automotive and Industrial

Automation enables important benefits in the automotive and industrial markets, including higher yields, better and more consistent quality and lower cost. In automotive applications, automation can provide the speed and precision required to handle small, high-volume components such as sensors and electronic components. In industrial manufacturing applications, the automation of machine tools and other industrial equipment provides a more productive and safer environment while allowing human labor to be re-deployed to higher value added tasks. This is particularly true in the use of mobile robots to eliminate personnel pushing carts in a factory. Additionally, automation plays an important role in containing costs in high labor cost regions such as Europe, where governmental policies have encouraged automotive and industrial manufacturing to remain local.

Logistics/Warehouse

One of the largest sectors where logistics is of primary consideration is in warehousing and distribution. Managers of these processes are faced with multiple operational and environmental challenges while simultaneously facing ever increasing customer requirements. Automation is often a financially attractive alternative to manual processes for not only the labor cost savings, but also due to the potential improvements in productivity, order accuracy, reduced space requirements, increased volume capacity, and control of inventory. While this growth in automation is occurring, there is also a need for supply chains to become more agile to serve rapidly changing markets. To address these divergent requirements, automation is being required to offer heightened levels of flexibility. This is increasingly achieved through the use of mobile robot technologies such as the Lynx mobile robot to autonomously transport materials as instructed directly by the warehouse enterprise software.

3

Food

Driven by global competition, changes in consumer buying habits and tightening of governmental safety and hygiene requirements, food processors worldwide are turning from hard automation and manual packing towards robotics in order to achieve food safety, manufacturing flexibility and improved sanitation in their food packaging lines. Primary food packaging sectors, where robots come in direct contact with food, include raw and processed meats and poultry, seafood, raw and processed fruits and vegetables, baked goods and confectionary. Secondary food application sectors, where packaged food is placed into larger packages, include kitting, cartoning and palletizing.

Flexible Manufacturing

As manufacturers worldwide strive to respond to both B2B and B2C markets that are constantly demanding new and more varied products, designing processes that support multiple product lines or numerous short life-cycle products are major challenges. Companies that manufacture consumer products have SKUs that number in the hundreds with updates, changeovers and short delivery times requiring high adaptability. Faster, more accurate and multi-arm robotic cells bring the ability to run different products on a production line, perform a wide variety of repeatable tasks, and handle multiple applications, contributing greatly to flexible work cells. These capabilities, along with more sophisticated robotic end effectors, flexible feeders instead of hard automation and autonomous indoor vehicles instead of hard conveyances, are enabling efficient product changeover and flexibility that reduce costs and time to market.

Scientific and Academic Research

Governments promote funding for robotics research as a way to increase manufacturing competitiveness and productivity. Investigations are carried out within university engineering and computer science departments, as well as standalone government and military research labs. Disciplines include mapping and navigation, machine vision, multi-robot systems control, human-robot interaction, mobile manipulation and robot-enabled medical applications. When possible, laboratories will use pre-built robotic assemblies in favor of developing specialized hardware. Platforms are programmable with open architecture and can be modified for specific investigations and integrated with customized effectors and sensors.

4

Market Applications

Adept designs and manufactures industrial and mobile robots along with related control and vision systems and software for a diverse group of customers:

| | | | |

Market | | Application | | Adept Product |

Semiconductor | | Solar | | Cobra™, Viper™, Python™, Quattro™ |

| | Wafer Transport | | Lynx®, Cobra™, Viper™ |

| | Reticle Handling | | Lynx®, Cobra™ |

| | |

Packaging | | Kitting | | Cobra™, Viper™, Python™, Quattro™ |

| | Cartoning | | Cobra™, Viper™, Python™, Quattro™ |

| | Palletizing | | Viper™ |

| | |

Electronics | | Assembly | | Cobra™, Viper™, Python™, AnyFeeder™, Flexibowl® |

| | Packaging | | Cobra™, Viper™, Python™, Quattro™ |

| | WIP Replenishment | | Lynx®™, Enterprise Manager™ |

| | Transport of Finished Goods | | Lynx®™, Enterprise Manager™ |

| | |

Automotive/Industrial | | Component Assembly | | Cobra™, Viper™, Python™, AnyFeeder™, Flexibowl® |

| | Material Transfer | | Cobra™, Viper™, Python™, Quattro™ |

| | Machine Tending | | Viper™ |

| | WIP Replenishment | | Lynx®™, Enterprise Manager™ |

| | Transport of Finished Goods | | Lynx®™, Enterprise Manager™ |

| | |

Logistics/Warehouse | | Order fulfillment | | Lynx®, Enterprise Manager™ |

| | Inventory picking | | Lynx®, Enterprise Manager™, Cobra™, Viper™ |

| | WIP Replenishment | | Lynx®, Enterprise Manager™ |

| | |

Food | | Primary Packaging | | Quattro™, Cobra™ |

| | Secondary Packaging | | Quattro™, Cobra™, Viper™ |

| | Palletizing | | Viper™ |

| | Transport of Finished Goods | | Lynx®™, Enterprise Manager™ |

| | |

Flexible Manufacturing | | Assembly | | Cobra™, Viper™, Python™, Quattro |

| | Dispensing | | Cobra™, Viper™ |

| | Flexible Feeding | | AnyFeeder™, Flexibowl® |

| | WIP Replenishment | | Lynx®™, Enterprise Manager™ |

Products

Controllers

Adept SmartController

The Adept SmartController™ is an ultra-compact robot motion controller, featuring distributed architecture for scalability, embedded software for real-time operations, high-speed communication for belt encoder and camera

5

support, and a fast processor for high performance. The Adept SmartController™ integrates robots with conveyors, cameras, grippers, and software.

Adept SmartVision

The Adept SmartVision™ is a high-performance vision processor, optimized to run Adept ACE™ software and its extensions. It can be used as a standalone solution for vision guidance and inspection applications or seamlessly integrated with multiple robots, conveyors, grippers, cameras and sensors.

Software

Adept ACE

Adept ACE (Automation Control Environment) is PC-based software for configuring, calibrating, and managing equipment in a workcell. This functionality is accessed through a user-friendly graphical user interface (GUI). Adept ACE software is built on a modular framework, which reduces the cost of programming complex applications with conveyor tracking and vision guidance.

ACE PackXpert

ACE PackXpert™ is an extension of Adept ACE, designed to rapidly deploy flexible automation solutions. PackXpert™ speeds the configuration of applications by setting up the number of robots, controllers, conveyors, vision tools, and the sequencing of process steps. The software generates all the underlying robot programming based on the user’s application.

AdeptSight

AdeptSight™ is an extension of Adept ACE, designed for vision guidance and inspection applications. AdeptSight™ makes it easy to calibrate and synchronize cameras, conveyors, grippers and robots. The software is capable of identifying randomly oriented products of various sizes and colors at very fast cycle times.

Adept ePLC Connect

The Adept ePLC Connect server software provides seamless connectivity with a customer supplied Programmable Logic Controller (PLC). All robotic application programs and locations are defined and reside within the user’s PLC. The ePLC Connect software runs on the Adept SmartController and interprets PLC ladder logic programming, and commands the robot to move accordingly. Customers new to robotics can install, program, operate and support high-performance robots with the familiar interface and programming language of their existing PLC.

Fixed Robots

Adept Quattro Parallel Robots

The Adept Quattro™ robot is the world’s fastest parallel robot. The patented four-arm design, advanced control algorithms, embedded amplifier, and large work envelope make Quattro™ the ideal robot for high-speed assembly, processing, packaging, and other manufacturing applications. Quattro™ comes with a 650 or 800 mm reach, a minimal footprint, and delivers sustainable, smooth motions at high speeds. The Adept Quattro™ s650HS version is USDA-accepted for meat and poultry processing.

Adept Viper 6-axis Robots

The Adept Viper™ robot is a high-performance 6-axis robot with a 650, 850, 1300, or 1700 mm reach. Adept Viper robots have the added flexibility afforded by their 6-axis design. Adept Viper robots include the Adept SmartController, equipping each with conveyor tracking and vision guidance capabilities. All Viper robots are available in wash-down configurations, and the Viper s650 and s850 are available in cleanroom configurations.

6

Adept Cobra SCARA Robots

The Adept Cobra™ robot is a high-performance four-axis SCARA robot with a 350, 600, or 800 mm reach. Adept Cobra robots offer an industry-leading combination of speed, accuracy and repeatability. Adept Cobra s-Series robots (s350, s600, and s800) include the Adept SmartController, equipping each with conveyor tracking and vision guidance capabilities. Adept Cobra i-Series robots (i600 and i800) feature embedded controls and amplifiers in the robot’s base, simplifying the design, reducing the cost, and increasing the footprint efficiency. The Adept Cobra s800 inverted robot is the ceiling-mount version of the Cobra SCARA robot. The inverted Cobra robot delivers high performance, an 800-mm reach, and a minimal footprint.

Adept Python Linear Modules

Adept Python™ linear modules are designed for scalability and flexibility. Adept Python modules incorporate unique design features, making them one of the most robust modules for single-axis, dual- axis, three-axis, or four-axis applications with rotation, gantry, and cantilever configurations. Adept Python modules have a manufacturing process that delivers a fully-assembled and tested system. All Python modules are available in both cleanroom and ESD versions.

Mobile Robots

Adept Lynx

The Adept Lynx® is an autonomous indoor vehicle with a configurable payload for the transport and handling of goods. The Lynx includesMobile Planner™, Adept’s proprietary self-navigation software ideal for use in crowded and highly dynamic environments, tight hallways and applications where a highly flexible, fully autonomous vehicle is advantageous. Adept OEM partners and payload developers (integrators) enjoy access to a reliable drive system, an on-board power supply, automated self-charging, and I/O for integrating payload hardware onto the mobile platform. The Adept Lynx is capable of transporting up to 130 kg with an uninterrupted runtime of up to 10 hours a day and a rapid recharge cycle less than 4 hours.

Adept Lynx Courier

The Adept Lynx® Courier is an intelligent mobile transporter that combines a high payload autonomous platform with an onboard controller and software for map generation and vehicle guidance. Material transports can be initiated from a wireless call box located at operator stations and dispatched using pre-programmed destination buttons located on the vehicle. The Lynx Courier, with its wireless communication capability and payload compartment, can be used for applications in logistics, warehouse, offices, biotech, and manufacturing facilities. The Adept Lynx Courier reduces or eliminates manual transport tasks, shortens turnaround time, and increases operational efficiency by re-applying labor from moving goods to higher-value tasks.

Adept Lynx Transporter-Semi

The Adept Lynx® Transporter-Semi combines a Lynx autonomous indoor vehicle with a multi-wafer pod carrier to move wafer pods throughout a semiconductor fab. It is designed to transport up to four wafer pods in a dynamic cleanroom environment while operating safely and collaboratively alongside people. The vehicle’s on-board intelligence eliminates the need for additional infrastructure such as tracks, reflectors, floor tape, cameras or magnets. The Lynx Transporter improves production yield by eliminating human-generated dust particles and by following instructions from the fab production software system, ensuring no errors in the location of wafer pods. It enables implementation of lean methodologies in the workflow and allows redeployment of a limited labor pool to higher value-add tasks.

Adept Lynx Handler-Semi

The Adept Lynx® Handler-Semi combines a Lynx autonomous indoor vehicle with a collaborative 4-axis robot to produce a highly versatile mobile robot designed to pick, place and move semiconductor wafer pods throughout a wafer fab. The Lynx Handler can exchange wafer pods from a variety of processing equipment, stockers and storage (work in progress, or WIP) racks. The Lynx Handler moves nimbly within narrow aisles,

7

operates safely alongside people, and operates collaboratively within a fleet of Lynx vehicles. The vehicle’s on-board intelligence eliminates the need for additional infrastructure such as tracks, reflectors, floor tape, cameras or magnets. The Lynx Handler-Semi improves production yield by eliminating human-generated dust particles and by following instructions from the fab production software system, ensuring no errors in the physical handling or the identification of wafer pods.

Adept Lynx Conveyor

The Adept Lynx® Conveyor combines a Lynx autonomous indoor vehicle with a motorized conveyor platform, producing a highly versatile mobile robot designed to receive, transport and deliver materials or goods throughout warehouses, distribution centers and manufacturing environments. The vehicle’s on-board intelligence eliminates the need for additional infrastructure such as tracks, reflectors, floor tape, cameras or magnets. The Lynx Conveyor moves nimbly within narrow aisles and operates safely alongside people. As an alternative to fixed conveyors, the Lynx Conveyor offers flexibility to existing work environments where material flow changes periodically. It also dramatically reduces manual transport tasks, shortens turnaround time, enables lean workflow processes and increases operational efficiency by allowing redeployment of personnel to higher value-add tasks.

Adept Enterprise Manager

When multiple Lynx® vehicles operate within an area, to achieve high levels of efficiency they require a management system capable of supervising the fleet and interfacing with the operational environment and its associated infrastructure. Enterprise Manager provides the critical role of managing activities for traffic control and job allocation by communicating with existing IT systems, interfacing with I/O on internal devices and equipment, and storing navigation parameters for the entire system. Adept Enterprise Manager is a management system that operates on Adept‘s SmartFleetEX hardware and uses a systems-network approach for the coordination of autonomous indoor vehicles while providing traceability, job allocation, and traffic control across the entire fleet.

Infeeds

Adept AnyFeeder

The Adept AnyFeeder™ paired with an Adept robot and integrated vision guidance supports a high degree of product variation and brings true flexibility to part feeding. Using an AnyFeeder to present parts to a robot increases the overall throughput of the system and improves the cost-per-pick ratio. AnyFeeders are designed to handle a wide array of loose small parts, including parts of different shapes and materials, minimizing product changeover times and increasing line utilization.

Adept FlexiBowl

The Adept FlexiBowl™ is an innovative feed solution for use with any Adept robot and vision system. The feeder is designed to handle a wide array of loose small parts, including parts of different shapes and materials. The feeder is capable of carefully and quickly feeding parts that are tangled or made of different materials such as rubber or silicone or parts that are fragile, cylindrical or even oiled. Utilizing a direct-drive motor, the Adept FlexiBowl operates reliably and quietly and is easy to operate. Its circular band tracking permits the removal of parts during movement, delivering higher throughput, and its unique design delivers a more flexible and efficient alternative to traditional vibration feeders. The Adept FlexiBowl is available in a 350 mm and 500 mm diameter models.

Sales and Marketing

Adept markets and sells its products worldwide through a network of systems integrators, distributors and OEMs as well as through its direct sales force directly to end customers. Systems integrators and OEMs may add their own application-specific hardware and software to Adept products, resulting in solutions that are sold to companies across a range of industries.

8

No one customer accounted for greater than 10% of total revenues in any of the years ended June 30, 2014, 2013 and 2012. Our business is not generally dependent upon any single customer, such that the loss of a single customer in the future would not be expected to have a material adverse effect on the Company; however, at June 30, 2014 and 2013, one customer accounted for 7% of accounts receivable and one customer accounted for 21% of accounts receivable, respectively.

To support our sales efforts we maintain application technology centers around the world, where our team of application engineers collaborates with customers to validate robotic concepts and test technologies. Locations include facilities in the Pleasanton, California; Amherst, New Hampshire; Dortmund, Germany; Annecy, France and Singapore.

Service and Support

We maintain customer support and field service staff in major markets within the United States, Europe, and Asia. Adept supplements our staff by using in-market distributors. This organization works intimately with customers, system integrators and independent representatives to service equipment. We also train customers to use our products and explore additional applications of our technologies.

Adept offers on-site field service, comprehensive training courses, applications support, field upgrades, factory repair and remanufactured products. Many of Adept’s customers have manufacturing facilities that are operated 24 hours a day. Adept provides year round 24/7 support to customers. We provide parts and service warranties on our equipment, software and services. Warranties on some of our products and services may be shorter or longer than one year.

Research and Development

We focus our research and development efforts on the development of an integrated product line, which reduces the cost of factory automation, enhances performance, and improves ease of use for our customers. Research and development activities are focused on the design of our motion and vision control hardware and the robotic mechanisms that utilize them along with advanced software for vision, motion control and applications.

In both our primary research and development facility in Pleasanton, California, our development facilities in Amherst, New Hampshire, and Annecy, France, we focus on the development of motion controls, mobile robots, robot arms, robot mechanisms, vision software, autonomous navigation software, and real-time application software.

We have devoted, and intend to devote in the future, a significant portion of our resources to research and development programs. As of June 30, 2014, we had 35 employees engaged in research, development and engineering. Our research, development and engineering expenses were $6.8 million in fiscal 2014, $7.6 million in fiscal 2013, and $8.7 million in fiscal 2012.

Manufacturing

One of our core manufacturing strategies is to tightly control our supply of key parts, components, sub-assemblies and outsourcing partners. We primarily utilize vertical integration when we have proprietary internal capabilities that are not available from external sources in a cost-effective manner. We believe this is essential to maintain high quality products and enable rapid development and deployment of new products and technologies. We provide customers with 24-hour technical expertise and quality that is International Organization for Standardization (“ISO”) certified at our principal manufacturing sites.

We have a strong commitment to quality and customer satisfaction. We design and produce many of our own components and sub- assemblies in order to retain intellectual property, performance and product innovation quality. We have also outsourced certain components, sub-assemblies and finished goods where we can maintain our high quality standards while improving our cost structure.

9

We proactively monitor single source supply parts, and we endeavor to ensure that adequate inventory is available to maintain manufacturing schedules should the supply of any part be interrupted. Although we seek to reduce our dependence on sole or limited source suppliers, we have not qualified a second source for some of these products and the partial or complete loss of certain of these sources could have a materially negative impact on our results of operations and could damage customer relationships.

Intellectual Property

Because our success and competitiveness depends to an extent on the technical expertise, creativity, and knowledge of our personnel, we utilize patent, trademark, copyright, and trade secret protection to safeguard our competitive position. At June 30, 2014, we had 18 patents issued and current on various innovations in the field of robotics, motion control, and machine vision technology. In addition, we use non-disclosure agreements with customers, suppliers, employees, and consultants. We attempt to protect our intellectual property by restricting access to proprietary information through a combination of technical and internal security measures. There can be no assurance, however, that any of the above measures will be adequate to protect the proprietary technology of Adept. Further, effective patent, trademark, copyright, and trade secret protection may be unavailable in certain foreign countries.

Competition

The market for robotics-based automation is very competitive. Adept competes against a number of global companies, including ABB, Epson, Fanuc, Kuka, Yaskawa, Denso, Motoman, Staubli, Amazon (Kiva), Aethon, MetraLabs Seegrid, Savant and Neobotix. We also compete with individual country-based vendors. We compete globally based on our integrated industrial/mobile product offering, performance capability, capacity, reliability, cost of ownership, and performance advantages for the widest range of commercial and scientific research applications. Other considerations by our customers include warranty, global service and support and distribution.

Seasonality

Historically, orders have been lower in the first half of our fiscal year and higher in the second half of our fiscal year, with a decline during the first quarter of each fiscal year due, in part, to the concentration of sales into the European market, which typically experiences a pronounced summer holiday season. Revenues in each quarter will vary based on European market seasonality and on the particular timing of major programs to key customers.

Foreign Operations

We operate globally, with corporate headquarters in Pleasanton, California and European headquarters in Dortmund, Germany. Our principal executive offices are located at 5960 Inglewood Drive, Pleasanton, California 94588 and our telephone number at that address is (925) 245-3400. Additionally, we lease sales and operations facilities in New Hampshire, France, Singapore and China. See “Properties” for a further discussion of our offices and facilities.

Employees

At June 30, 2014 , we had 152 employees worldwide. Of the total, 35 were engaged in research and development, 42 in sales and marketing, 29 in service and support, 25 in operations, and 21 in administration.

See Part III of this Form 10-K regarding information about our Executive Officers.

Government Regulation

As of June 30, 2014, we have no principal products or services pending government approval. Furthermore, there are no existing or probable government regulations material to our business. We have one product with USDA accreditation for use in meat and poultry packaging.

10

Availability of SEC Filings

We make available through our website our Annual Reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports free of charge as soon as reasonably practicable after we electronically file such material with the Securities and Exchange Commission. Our Internet address is www.adept.com. Our Form 10-K and proxy statement are made available on our website promptly after filing with the SEC and many of our corporate governance documents, including our Code of Business Conduct, are also available on our corporate website. The content on our website is not, nor should be deemed to be, incorporated by reference into this Annual Report on Form 10-K. Additionally, documents filed by us with the SEC may be read and copied at the Public Reference Section of the SEC, 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at1-800-SEC-0330. Our filings with the SEC are also available to the public through the SEC’s website at www.sec.gov.

11

Our operating results fluctuate due to factors that are difficult to forecast, are often out of our control, and can be volatile.

Our past operating results may not accurately indicate our future performance. Our operating results have fluctuated significantly in the past, and could fluctuate in the future. Factors that may contribute to fluctuations include:

| | • | | changes in aggregate capital spending, cyclicality and other economic conditions, or demand in the industries we serve; |

| | • | | impact of our restructuring activities on our operations; |

| | • | | management of our working capital; |

| | • | | changes in our products’ market acceptance or demand; |

| | • | | new products or changes in pricing, by us, our distribution channels, or our competitors; |

| | • | | pricing and availability of components and raw materials; |

| | • | | changes in our product mix from quarter to quarter affecting our gross margins; |

| | • | | our failure to manufacture a sufficient volume of products in a timely and cost-effective manner; |

| | • | | our inability to decrease certain fixed costs and expenses to address changes in demand; |

| | • | | currency exchange rate fluctuations; |

| | • | | shifts in geographic concentration of our sales; |

| | • | | our ability to expand our product offerings; and |

| | • | | extraordinary events such as litigation, claims, information security breaches or mergers and acquisitions. |

We generally recognize revenues upon shipment, or in certain cases upon receipt by customers. As a result, our revenues and results of operations are affected by the timing of orders received and shipped. A significant percentage of our shipments occur in the last month of each quarter, making reliable forecasting of demand level for our products for a particular quarter difficult. Further, an order cancellation, reduction or delay in shipments near the end of a fiscal period may cause sales to fall below expectations and harm our operating results for that period. We have and may also enter into agreements requiring us to accept certain orders meeting agreed criteria and to hold specified levels of inventory. To address this, we periodically stock inventory levels of completed robots, machine controllers and certain strategic components. As a result, our operating results vary, our stock price is volatile, and we may not be able to achieve or sustain our profitability on a quarterly or annual basis.

We have experienced operating losses and negative cash flow in the past, and have limited liquidity resources, which could impair our ability to invest in growth and adversely affect our operations.

We have experienced operating losses and negative cash flow, and if our projected revenue fails to increase or our expenses exceed current expectations, we may not be able to take advantage of market opportunities, adequately respond to competitive pressures or fully execute our business plan. In June 2012, we raised approximately $3.1 million in connection with our public offering of common stock, and in September 2012, we raised approximately $7.6 million of net proceeds, after estimated expenses, in connection with our redeemable convertible preferred stock financing, which has been fully converted into common stock. These financings increased our cash resources and allowed us to pay off our previous line of credit, but our liquidity remains

12

limited and restrictions and tax consequences may limit our access to existing cash balances from our foreign operations. We have historically relied on a line of credit which expires in March 2016. We depend on the cash raised from our recent financings and funds generated from operating activities to sustain and grow our business. We do not anticipate paying any dividends on our common stock. If we are unable to obtain sufficient capital on favorable terms, it could undermine our ability to pursue expansion opportunities and could limit the working capital available to our business, harming our operating results.

Our restructuring efforts may not be effective, might have unintended consequences, and could negatively impact our business.

We have restructured our operations in response to changes in the economic environment, our industry and demand, including restructuring programs in the second quarters of fiscal years 2012 and 2013 to streamline operations, consolidate facilities and reduce our work force. We reviewed and aligned our strategic priorities and rebalanced our investments to maintain sufficient liquidity and to focus on growth in our core markets. Despite our planning, some cost-cutting measures could have unexpected negative consequences, including loss of key personnel, or the loss of customers.

In connection with our restructurings, we have reduced our work force and experienced additional attrition, which may expose the Company to legal claims against the Company and loss of necessary human resources. If we face costly employee or contract termination claims, our operations and prospects could be harmed.

If we are unable to build and effectively integrate our new management team, our business could be harmed.

Our management team, including our Chief Executive Officer, is new and we are experiencing other significant personnel changes, including the addition of our Chief Financial Officer and Chief Business Development and Strategy Officer. Integrating new management into existing operations always carries risk. If we are unable to effectively build our new management team or integrate our new team members, our operations and prospects could be harmed.

We depend on outsourced manufacturing and information technology capabilities and single source suppliers, and if we experience disruptions in this supply or prices increase, our business may suffer.

We outsource most of our manufacturing functions, and obtain many key components, materials and mechanical sub-systems from sole or single source suppliers. We have limited contracts or guaranteed supply arrangements with these suppliers, and the lack of alternate sources and lengthy qualification process for replacement suppliers involves significant risks. These risks include whether or not new suppliers will provide adequate quantities with sufficient quality on a timely basis, and the risk that supplier pricing may be higher than anticipated. If we are unable to obtain necessary items on a timely basis, at acceptable prices, and of sufficient quality, we could lose current or future business. In the past, we have experienced quality control or specification problems with certain components provided by sole source suppliers, and have had to design around flawed items. Any quality issues could result in customer dissatisfaction, lost sales, or increased warranty costs, and could harm our results of operations.

Any significant price increase or disruption of our supply sources could interrupt our product shipments, require reengineering, and damage customer relationships. If our suppliers cease manufacturing components that we require, we may need to purchase a significant amount of inventory that could lead to an increased risk of inventory obsolescence. Finally, if we incorrectly forecast product mix for a particular period and we are unable to obtain sufficient supplies of any components or mechanical sub-systems on a timely and cost-effective basis due to long procurement lead times, our business could be substantially impaired.

13

Global economic conditions currently affecting our customers and suppliers may also negatively affect our financial results by decreasing our revenues and increasing our risk of credit-related losses.

The global economic downturn has created a widespread slowdown in capital investment, manufacturing, and demand for consumer products particularly in the disk-drive and solar markets. In response, our suppliers have or may increase their prices or reduce their output. Some of our customers (including systems integrators) have, and may continue to, defer, reduce or cease to place orders for our products, or may delay or default on their payment obligations, reducing our revenues or increasing our credit losses, which would negatively affect our financial results.

Our inability to accurately forecast, or react quickly and adequately to increases or decreases in demand for our products could harm our business and results of operations.

Intelligent automation systems using our products can range in price from $25,000 to $500,000. Accordingly, our success depends upon the capital expenditure budgets of our customers, which tend to be cyclical. The economic downturn resulted in cutbacks in capital spending in some of our major markets, and our business has been, and may continue to be, negatively affected. Industry downturns have been characterized by reduced demand for devices and equipment, production over-capacity, and accelerated declines in average selling prices. During periods of declining demand, we have implemented several worldwide restructuring programs to realign our business and lower our expenses. However, our ability to reduce expenses is limited by our need to retain and motivate key employees, and by our need for continued investment in product engineering, research and development. We also have extensive ongoing customer service and support requirements, must maintain inventory to satisfy potential customer commitments, and have certain fixed administrative costs. Further, our failure to effectively manage product transitions or accurately forecast customer demand, in terms of both volume and configuration, may lead to an increased risk of excess or obsolete inventory.

We also must maintain the ability to quickly increase our manufacturing capacity upon an increase in orders or general upturn in any of our markets. Typically, upturns in markets such as disk drive or electronics have been characterized by abrupt demand increases, and production under-capacity. We must be able to ramp up in times of increased demand and hire sufficiently to service our customers.

Our international operations and reliance on foreign suppliers subject us to risks outside of our control that may harm our operating results.

We have significant and expanding operations outside the United States, including a presence in Asia. A substantial majority of our revenue is derived from non-U.S. sales: international sales represented 77% and 74% of revenues for fiscal 2014 and fiscal 2013 , respectively. We expect that revenue from our international sales and operations will continue to be a significant portion of our total revenue. We also purchase some critical components from foreign suppliers. As a result, our operating results are subject to the risks inherent in international sales, purchases, and operations, including:

| | • | | difficulties ensuring compliance with applicable regulatory regimes; |

| | • | | unexpected changes in regulatory requirements; |

| | • | | political, military, and economic instability or turmoil; |

| | • | | restrictive governmental actions, such as tariff regulations and other trade barriers; |

| | • | | transportation costs and delays; |

| | • | | local rules favoring local business and organized labor; |

| | • | | longer payment cycles and greater difficulty collecting accounts receivables from foreign jurisdictions; |

| | • | | potentially adverse tax rates and tax treatment of our intercompany transactions; and |

| | • | | difficulty obtaining appropriate personnel. |

14

We face exposure to fluctuations in foreign currency exchange rates, as a significant portion of our revenues, expenses, assets, and liabilities are denominated in foreign currencies. Additionally, we make foreign currency-denominated purchases from some suppliers, and thus remain subject to the transaction exposures that arise from foreign exchange movements between the date that the transactions are recorded and the date cash is paid. Continued fluctuations in foreign currencies could negatively impact us.

As we are subject to the regulatory regimes of numerous governments, we must ensure that our operations comply with all applicable requirements, including changing requirements affecting business and tax audits by foreign authorities. It is not possible to assess the associated amount of financial or operational exposure at this time.

In 2011, we opened a facility in Shanghai, China to capitalize on significant opportunities presented by the Asian markets. We face all the risks inherent in operating in a foreign emerging market where we have not previously operated a facility. Our China-based activities are subject to greater political, regulatory, legal and economic risks than those faced by other operations. There can be no assurance that our operations in China will be successful.

The long sales cycle, customer evaluation and implementation processes of our products may increase the costs of securing sales and reduce the predictability of our earnings.

Our products are technologically complex, and prospective customers generally must commit significant resources to test and evaluate performance, and to install and integrate our products into larger systems. As a result, our sales process is often subject to evaluation and approval delays typically associated with large capital expenditures. The sales cycles for our products often last for months or years, and orders expected in one quarter may shift to another or be canceled because of a customer’s budgetary constraints or internal acceptance reviews. Longer sales cycles require us to invest significant resources in attempting to secure sales that may not be realized in the short term, and therefore may delay or prevent revenue generation. The time required for our customers to incorporate our product into their system can also vary significantly, which further complicates our planning processes and reduces the predictability of our operating results.

Our failure to keep up with rapid technological change and new product development would harm our ability to compete.

The intelligent automation industry is characterized by rapid technological change and new product introductions and enhancements. We must anticipate trends in our customers’ industries and develop products before our customers’ products are commercialized, because many of our products are used by our customers to develop, manufacture, and test their own products. If we do not accurately predict our customers’ needs, we may invest substantial development resources in products that do not achieve broad market acceptance. Further, if we are unable to develop new and enhanced products meeting customers’ changing technical specifications on a timely and cost-effective basis, our products may become uncompetitive or obsolete. We also must make decisions about whether or not to develop and offer products to a given market, and if our judgment of that market is incorrect, our business could be harmed.

The market for intelligent automation products is intensely competitive, which may make it difficult to grow our business or to maintain or enhance our profitability.

Our competitors include robot, motion control, machine vision, and simulation software companies, many of which have substantially greater resources than we do. Our competitors in the robot market also include integrated manufacturers that produce robotics equipment for internal use, and also compete with our products for sales to other customers. Because they can generate substantial unit volumes to satisfy internal demand, these competitors may have greater pricing flexibility. During the recent economic downturn, we experienced aggressive price reductions and other accommodations by our competitors, in addition to increased

15

price sensitivity by our customers. We believe that the principal competitive factors affecting the market for our products are:

| | • | | product features, functionality, and ease of use; |

| | • | | brand quality perception; |

| | • | | timeliness, predictability, and reliability of delivery. |

Increased competitive pressure and declining barriers to market entry could result in a loss of sales or market share or force us to lower prices. Failure to enhance our brand would impair our ability to increase or maintain our customer base, and we may not be able to compete successfully in the future.

The growth of our business depends upon the successful development and commercial acceptance of our new products.

Our failure to develop, manufacture, and sell new products in quantities sufficient to offset a decline in revenue from existing products or to successfully manage product and related inventory transitions could harm our business. We depend upon a variety of factors to ensure that our new and enhanced products are successfully commercialized, including timely and efficient completion of design and development, implementation of manufacturing processes, and effective sales, marketing, and customer service. Because of the complexity of our products, significant delays may occur in introducing new products, or between a product’s initial introduction and volume production.

The development and commercialization of new products involve many difficulties, including:

| | • | | identifying new product opportunities; |

| | • | | retaining and hiring appropriate research and development personnel; |

| | • | | determining the product’s technical specifications; |

| | • | | successfully completing the development process; |

| | • | | successfully marketing the new product and achieving customer acceptance; |

| | • | | managing inventory levels; and |

| | • | | additional customer service and warranty costs associated with supporting new product introductions or affecting subsequent field upgrades. |

We must expend significant financial and management resources to develop new products. We cannot assure that we will receive meaningful revenue from these investments. If we are unable to continue to successfully develop new products in response to customer requirements or technological changes, or our new products are not commercially successful, our business may be harmed.

Our acquisitions of MobileRobots and InMoTx expanded our business with new technologies and solutions for additional markets commencing in fiscal 2011. We had little or no experience in these markets prior to the completion of these acquisitions and are unable to accurately forecast the future commercial acceptance of these product lines. In response to a decline in sales across our business beginning at the end of fiscal 2012, we have focused our efforts on our core competencies and sources of revenue generation and have invested fewer resources in new businesses which take longer to build revenue. In connection with our restructuring, we have focused on our core and mobile businesses and we have also altered our sales model for our packaging business to a channel focus. This may negatively impact the growth of our new businesses and revenue potentially earned from related new products.

16

We generally have no long-term customer contracts and our backlog cannot be relied upon as a future indicator of sales.

We generally do not have long-term contracts with our customers, and existing contracts and purchase commitments may be canceled under certain circumstances. As a result, we are exposed to competitive price pressures on every order, and our agreements with customers do not provide assurance of future sales. Our customers are not required to make minimum purchases and may cease purchasing our products at any time without penalty. Our backlog should not be relied on as a measure of anticipated demand or future revenue, because the orders constituting our backlog may be subject to changes in delivery schedules or cancellation without significant penalty to the customer. Any reductions, cancellations or deferrals in customer orders would negatively impact our business.

We market and sell our products primarily through an indirect channel comprised of third-party resellers not under our control.

We believe that our ability to sell products to systems integrators and OEMs will continue to be important to our success. However, our relationships with these partners are generally not exclusive, and we cannot control the timing or amount of their procurement or marketing of our products. Some systems integrators and OEMs who sell our products also sell products of our competitors. If they choose to promote competing products or simply fail to market our products successfully, our revenue could decrease.

As we enter new geographic and applications markets, we must locate and establish relationships with systems integrators and OEMs to assist us in building sales in those markets. Because of product integration expenses and the large amount of training required, significant time and resources may be required to establish a profitable relationship with a systems integrator or OEM. We may not be successful in establishing or maintaining an effective relationship with new systems integrators or OEMs, which would adversely affect our business.

Any future acquisitions may disrupt our business and harm our operating results.

We have acquired technologies and companies in the past and may acquire other businesses and technologies to further our strategic objectives. These new businesses may require investment to introduce new products to customers without any guarantee of revenues sufficient to fund these investments and to make these businesses successful.

Acquisitions present risks, including:

| | • | | significant expenditures of cash and dilutive stock issuances; |

| | • | | difficulties in integrating product offerings, operations, or workforce; |

| | • | | difficulties in establishing and maintaining effective uniform standards, controls, procedures and policies; |

| | • | | the loss of key personnel or customers from either our current business or the acquired company’s business; |

| | • | | adverse effects on existing supplier relationships; |

| | • | | disruptions of our on-going businesses and diversion of resources and management’s attention; |

| | • | | difficulties in realizing our financial and strategic objectives for the acquired business; |

| | • | | negative impact on results of operations due to goodwill impairment write-offs, amortization of intangible assets other than goodwill, or assumption of anticipated liabilities; |

| | • | | risks of entering new markets, geographic areas, and distribution channels in which we have limited or no previous experience; and |

17

| | • | | assumption of unanticipated liabilities, such as problems with the quality of the acquired company’s product. |

The risks above could significantly harm our business. The failure to successfully evaluate and execute acquisitions or adequately address these risks could materially harm our financial results.

Our products could have unknown defects which may give rise to claims against us, increase our expenses, or harm our reputation.

Our products and enhancements are complex and, despite testing, may contain defects, errors or performance problems. Any defects or errors could result in expensive and time-consuming design modifications or warranty charges, harmed customer relationships, and loss of market share. Newly released products, which have not seen as much use and testing in the marketplace as older products, are more susceptible to undetected defects. As we aim to generate increasing revenues from sales of recently released products, the negative impact on our business resulting from defects in such products could be significant.

The existence of any defects, errors, or failures in our products could also lead to product liability claims against us, our channel partners, or our customers. Although we maintain product liability insurance, the coverage limits of these policies may not adequately cover future claims. Any claim could result in significant legal defense costs, divert resources, harm our reputation, and damage our business.

Our failure to protect our intellectual property and proprietary technology may impair our competitive advantage.

Our success depends in part upon protecting our proprietary technology and trade secrets. We primarily rely on a combination of patents, trademarks, copyrights, trade secret protection, licenses, and nondisclosure agreements to protect our proprietary rights, but have not always sought patent, registration, or similar protection on our technology where it may have been available. The steps we have taken may not be sufficient to prevent the misappropriation of our intellectual property or to provide us with any commercial advantage. The process of obtaining patent protection can be time consuming and costly, and our ability to enforce our intellectual property rights is subject to uncertainty and litigation risks.

We may face costly intellectual property infringement claims.

Allegations of intellectual property infringement by our products may arise and could include claims against us, our manufacturers, suppliers, or customers. Because there are numerous patents in the automation industry, it is not always practicable to determine in advance whether a product or any of its components infringes intellectual property rights. As a result, we may be forced to respond to intellectual property infringement claims to protect our rights. Regardless of merit, these claims could consume management time, result in costly litigation, or cause product shipment delays. In settling these claims, we may be required to cease selling products or services, pay damages, redesign the challenged technology, or enter into unfavorable royalty or licensing agreements. Any of these could seriously harm our business.

Information security breaches or business system disruptions may adversely affect our business.

We rely on our information technology infrastructure and management information systems to run our business. Although we take measures to protect our information assets, our security measures may not detect or prevent every attempted breach. We may be subject to information security breaches caused by, among other things, illegal hacking, computer viruses, or acts of vandalism or terrorism. A breach could result in an interruption in our operations, unauthorized publication of our confidential business or proprietary information, unauthorized release of customer or employee data, violation of privacy or other laws, and exposure to litigation. Any such breach could materially harm our business and operating results.

18

Our investments in certain new markets subject us to increased regulation and potential product liability, and there is no guarantee that we will be successful in these markets or that risks related to these industries will not have an adverse effect on our business.

Our systems and controls are sold in a variety of industries, including semiconductor, food, packaging and medical, among others. We have increased our strategic focus on sales for certain applications that are more highly regulated, including the automation of repetitive operations in diagnostic and pharmaceutical labs. As we seek sales in the medical and food packaging industries, we must ensure that our products and systems comply with applicable regulatory requirements. This will increase our costs and our failure to comply with these requirements could damage our ability to sell our products or subject us to regulatory actions or fines.

Our failure to comply with environmental laws and regulations could harm our business.

We are subject to a variety of environmental regulations relating to the use, storage, handling, and disposal of hazardous substances used in the manufacturing and assembly of our products. We believe that we are in compliance with material environmental regulations and have all necessary environmental permits. However, our failure to comply with present or future regulations could result in penalties or liabilities, and could curtail our operations.

Our success depends on our continuing ability to attract, train, motivate and retain highly-qualified personnel.

Our inability to attract, train, motivate, and retain qualified management, sales, and technical personnel could adversely affect our ability to design, manufacture, market and sell our products, and to meet our requirements as a public company. Many companies with which we compete for qualified personnel have greater resources than we do. In addition, in making employment decisions in the technology industry, job candidates often consider the value of the equity they receive in connection with their employment. Therefore, volatility in the price of our stock may adversely affect our ability to attract or retain technical personnel, which could harm our business.

Compliance with recently passed health care legislation and potential increases in the cost of providing health care plans to our employees may adversely affect our business.

The Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act (collectively, the “Acts”) became law in March 2010. The Acts contain provisions that will affect employer-sponsored health care plans, but it remains uncertain whether and by how much the Acts will increase health care costs of employers. Significant annual increases in the cost of providing employee health coverage may adversely affect our business and results of operations.

If we fail to maintain adequate internal controls over financial reporting, our business could be materially and adversely affected.

Under the Sarbanes-Oxley Act, our management must establish, maintain and make certain assessments and certifications regarding our disclosure controls and internal controls over financial reporting. We have dedicated significant resources to comply with these requirements, including significant actions to develop, evaluate, and test our internal controls, but cannot provide absolute assurances. A failure to maintain adequate internal controls could result in inaccurate or late reporting of our financial results, an investigation by regulatory authorities, a loss of investor confidence, a decrease in the trading price of our common stock and exposure to costly litigation or regulatory proceedings.

Our concentration of our equity ownership among few stockholders could adversely affect the liquidity and market price of our securities, and may permit a few stockholders to influence the results of stockholder decisions.

We have 13,066,054 shares of common stock outstanding as of August 15, 2014. A small number of holders own the substantial majority of our outstanding equity. These securities are generally freely tradable or subject to

19

registration statements, permitting their sale with little or no restriction. The potential sale of these securities creates meaningful overhang on the market for our securities and sales by any of these large holders would increase the current volatility of our common stock, the market price of which is affected by our low trading volume. This may affect the trading market for our stock, and could control the results of matters requiring stockholder approval, which may delay or prevent a change of control or negatively affect our stock price.

Stockholders may experience dilution of their ownership interests and the market price of our common stock may be depressed by future issuances of additional shares of our equity securities.

We issued 920,000 shares of our common stock in a public offering in June 2012 and 8,000 shares of redeemable convertible preferred stock in September 2012, all of which was converted into common stock in 2014. We may issue additional common or preferred stock or other equity securities for various reasons, including financing our operations, fund acquisitions or hire or retain employees. Issuances of our equity securities, or the perception that such issuances may occur, could dilute the interests of our stockholders and have a material negative effect on the trading price of our common stock. The rights and preferences of any preferred stock we issue may decrease the perceived value, and thus the trading price, of our common stock. The preferred stock may be convertible at the holder’s option and the issuance of common stock upon such conversion could require us to issue a significant number of shares of our common stock and dilute existing shareholders.

At June 30, 2014, options to purchase approximately 1.2 million shares of our common stock were outstanding under our equity compensation plans, and approximately an additional 0.4 million shares of common stock were reserved for future grant and issuance under such plans. We can also issue shares under our employee stock purchase plan, which had approximately 0.3 million shares available for issuance at June 30, 2014. Shares of common stock issued under these plans are generally freely tradable in the public market, subject to certain limitations applicable to our affiliates. Option exercises and employee stock purchase plan purchases could increase the number of common shares outstanding and could adversely affect the prevailing market price of our common stock, due to our low trading volume. Our use of equity to raise additional financing or as consideration in connection with a future acquisition or other transaction could also result in the dilution of our stockholders’ equity interest.

Our stock price may fluctuate widely, making resale of our common stock difficult.

The market price of our common stock has fluctuated substantially. Our stock price may continue to fluctuate significantly in response to factors including:

| | • | | fluctuating operating results; |

| | • | | our liquidity needs and constraints; |

| | • | | our restructuring activities and changes in management and other personnel; |

| | • | | changes in our business focus and operational organization; |

| | • | | our limited public float and the limited trading volume of our common stock on NASDAQ; |

| | • | | the business environment, including the operating results and stock prices of companies in the industries we serve; |

| | • | | general conditions in the intelligent automation and packaging industries; |

| | • | | the introduction of new products or changes in product pricing by us or our competitors; |

| | • | | litigation or claims relating to the volatility of our common stock, internal controls, proprietary rights or other matters; |

| | • | | developments in the financial markets; and |

| | • | | perceived dilution from stock issuances in financing or acquisition transactions. |

20

The effects of new regulations relating to conflict minerals may adversely affect our business.

In August 2012, the SEC adopted new requirements applicable to companies manufacturing or contracting for the manufacture of products which require specific minerals, known as conflict minerals. Such companies will have to disclose annually whether they used any conflict minerals originating from the Democratic Republic of Congo or adjoining countries. If a company uses conflict minerals from those countries, additional requirements will be triggered. We may face increased costs of regulatory compliance, potential risks to our reputation, difficulty satisfying any customers that insist on conflict-free products and harm to our business.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable.

Our headquarters and our U.S. research and development and manufacturing operations are located in two leased buildings of approximately 56,891 square feet in Pleasanton, California, covered by two lease agreements, both of which expire in December 2015. Other leased facilities include Amherst, New Hampshire; Dortmund, Germany; Annecy, France; Shanghai, China and Singapore. All of our facilities are used by both of our two reportable business segments and are sufficient for our business needs in fiscal 2015.

From time to time, Adept is party to various legal proceedings or claims, either asserted or unasserted, which arise in the ordinary course of our business. We have reviewed pending legal matters and believe that the resolution of these matters will not have a material effect on our business, financial condition or results of operations.

In March 2014, the Commercial Court of Lorient, France held that Adept did not fulfill certain obligations relating to a contract between Adept and a sub-contractor. Adept reached agreement to settle this matter, subject to judicial approval, and accrued in 2014 $159,000 relating to the settlement.

Adept has in the past received communications from third parties asserting that we have infringed certain patents and other intellectual property rights of others, or seeking indemnification against alleged infringement. While it is not feasible to predict or determine the likelihood or outcome of any actual or potential actions from such assertions against us or other matters, we believe the ultimate resolution of these matters will not have a material adverse effect on our financial position, results of operations or cash flows.

| ITEM 4. | Mine Safety Disclosure |

Not applicable

21

PART II

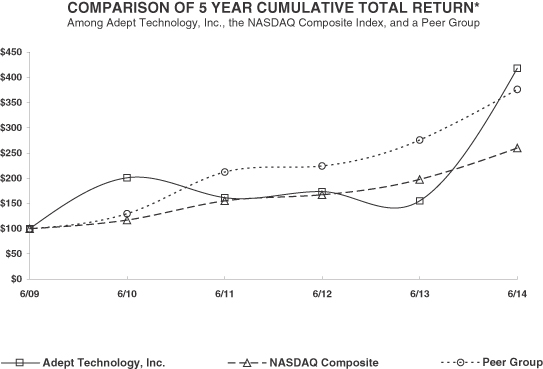

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market for Registrant’s Common Stock and Related Stockholder Matters

Our common stock is traded on the NASDAQ Capital Market under the symbol ADEP.

The following table reflects the range of high and low sales prices for Adept common stock for each full quarterly period within the two most recent fiscal years as reported for trading on the NASDAQ Capital Market.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

| | | Jun 30,

2013 | | | Mar 30,

2013 | | | Dec 29,

2012 | | | Sep 29,

2012 | | | Jun 30,

2014 | | | Mar 31,

2014 | | | Dec 31,

2013 | | | Oct 1,

2013 | |

| | | Fiscal Year 2013 | | | Fiscal Year 2014 | |

High | | $ | 4.06 | | | $ | 4.39 | | | $ | 4.36 | | | $ | 4.69 | | | $ | 21.27 | | | $ | 21.90 | | | $ | 17.00 | | | $ | 7.50 | |

Low | | $ | 2.65 | | | $ | 2.38 | | | $ | 2.39 | | | $ | 3.40 | | | $ | 9.78 | | | $ | 14.37 | | | $ | 6.53 | | | $ | 3.11 | |

At August 13, 2014, there were approximately 127 stockholders of record of our common stock.

To date, we have neither declared nor paid cash dividends on shares of our common stock. In addition, our line of credit restricts our ability to pay dividends on our common stock. Accordingly, our shareholders may not realize a return on their investment unless the trading price of our common stock appreciates.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers