Exhibit 99.1

| [LOGO] |

| Safe Harbor Statement Investor Presentation Safe Harbor Statement Rider Certain oral and written statements in this presentation and in response to questions may constitute forward-looking statements for purposes of the safe harbor provisions of The Private Securities Litigation Reform Act of 1995, including statements in connection with or related to any discussion of or reference to management’s expectations with respect to our future operations, opportunities or financial performance and other future events. Management cautions that these statements are based on management’s current knowledge and expectations and are subject to certain risks and uncertainties, many of which are outside of the control of the Company that could cause actual results and events to differ materially from the statements made herein. Such risks and uncertainties include, but are not limited to, the following: unanticipated litigation concerning the Company’s products; the current uncertainty and volatility in the national and global economy; changes in consumer preferences; changes in demand due to both domestic and international economic conditions; activities and strategies of competitors, including the introduction of new products and competitive pricing and/or marketing of similar products; actual performance of the parties under the new distribution agreements; potential disruptions arising out of the transition of certain territories to new distributors; changes in sales levels by existing distributors; unanticipated costs incurred in connection with the termination of existing distribution agreements or the transition to new distributors; changes in the price and/or availability of raw materials; other supply issues, including the availability of products and/or suitable production facilities; product distribution and placement decisions by retailers; changes in governmental regulation; the imposition of new and/or increased excise and/or sales or other taxes on our products; criticism of energy drinks and/or the energy drink market generally; the impact of proposals to limit or restrict the sale of energy drinks to minors and/or persons below a specified age and/or restrict the venues and/or the size of containers in which energy drinks can be sold; political, legislative or other governmental actions or events, including the outcome of any state attorney general and/or government or quasi-government agency inquiries, in one or more regions in which we operate. For a more detailed discussion of these and other risks that could affect our operating results, see the Company’s reports filed with the Securities and Exchange Commission including our most recent annual report on Form 10-K filed on February 29, 2012 and our most recent quarterly reports on Form 10-Q. The Company’s actual results could differ materially from those contained in the forward-looking statements. The Company assumes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. |

| Monster Energy Products Are Safe Tens of billions of energy drinks have been sold and safely consumed worldwide for approximately 25 years including more than 8 billion cans of Monster Energy that have been sold and safely consumed in the U.S. and around the world since 2002. The FDA has stated that there is a long history of safe use of other caffeine containing products in the United States and that the average amount of caffeine consumed by the U.S. population has remained relatively stable despite the entry of energy drinks into the marketplace. Monster energy products generally contain approximately 10 mg of caffeine per ounce from all sources. The leading brands of coffeehouse-brewed coffee contain on average in excess of 20 mg of caffeine per ounce. With respect to taurine and guarana, common energy drink ingredients, the FDA has stated that “FDA searched the literature but did not find any information that calls into question the safety of these ingredients as currently used in beverages.” Energy drinks are fully regulated by the FDA regardless of whether the drink is marketed as a conventional food or as a dietary supplement. Monster Energy products could be labeled and sold as a food. The FDA has made it clear that it has not established any causal link between Monster Energy products and any of the limited number of events reported in the adverse event reports database. Monster Beverage Corporation monitors consumer communications it receives, and is not aware of any fatality anywhere that has been caused by its products. The current frenzy of attacks directed against energy drinks is not supported by the facts or the science. |

| [LOGO] |

| [LOGO] |

| [LOGO] |

| [LOGO] |

| [LOGO] |

| Any powerful drug, such as caffeine is acknowledged to be, should not be offered indiscriminately to the public in other than its natural condition, and certainly not without the knowledge of the consumer In this 1912 Good Housekeeping cartoon, Harvey Wiley warns a gullible public against the gremlins of indigestion, nervousness, and addiction lurking in Coca-Cola. |

| Solid Financial Results 20 consecutive years of increased sales since acquisition of the Hansen beverage business in 1992. Achieved $1.95 billion in gross sales in 2011. Net sales for the third quarter of 2012 increased to $541.9 million, up 14.2% from the same quarter last year. Net income for the third quarter of 2012 increased to $86.1 million, up 4.6% from the same quarter last year. |

| Source: Nielsen Convenience Retailer YTD Month Ending 09/29/12 Convenience Store RTD Beverage Category Performance 2012 Total Beverage Market in Convenience |

| Convenience Store RTD Beverage Category Performance 2012 Energy is outpacing the beverage category in both percentage increase and total incremental dollars, YTD 9/2/12 Source: Nielsen Convenience Retailer YTD Month Ending 09/29/12 Total Beverage Market $ % Chg 9.2% $ Vol Chg (Millions) $1,567.1 |

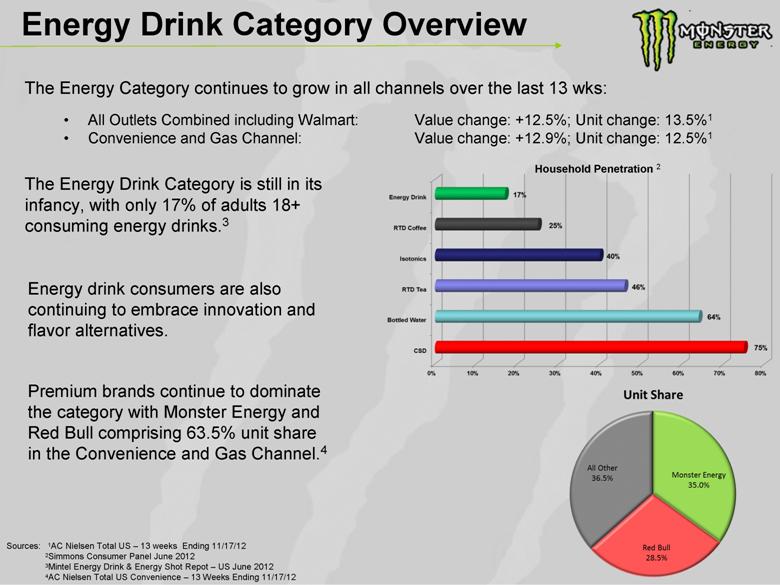

| Energy Drink Category Overview The Energy Category continues to grow in all channels over the last 13 wks: All Outlets Combined including Walmart: Value change: +12.5%; Unit change: 13.5%1 Convenience and Gas Channel: Value change: +12.9%; Unit change: 12.5%1 Premium brands continue to dominate the category with Monster Energy and Red Bull comprising 63.5% unit share in the Convenience and Gas Channel.4 Sources: 1AC Nielsen Total US – 13 weeks Ending 11/17/12 2Simmons Consumer Panel June 2012 3Mintel Energy Drink & Energy Shot Repot – US June 2012 4AC Nielsen Total US Convenience – 13 Weeks Ending 11/17/12 The Energy Drink Category is still in its infancy, with only 17% of adults 18+ consuming energy drinks.3 Household Penetration 2 Energy drink consumers are also continuing to embrace innovation and flavor alternatives. |

| Energy Drink Category Monster is leading growth in the Energy Category, up +19.1% vs Total NA Energy +12.5%. Monster has gained 1.7 share points, leading the growth of all key competitors. AOC Conv Food Drug Mass incl WM $ Vol $ Vol Year Ago $ % ? vs Year Ago $ ? vs Year Ago $ Share $ Share ? vs Year Ago TNA TOTAL NON-ALCOHOL ENERGY 2,382,401,592 2,116,777,986 12.5% 265,623,606 100.0% 0.0 1 TOTAL RED BULL 795,855,050 692,459,349 14.9% 103,395,701 33.4% 0.7 2 TOTAL MONSTER 755,903,376 634,747,583 19.1% 121,155,793 31.7% 1.7 3 TOTAL 5-HOUR ENERGY 286,296,948 285,178,658 0.4% 1,118,290 12.0% (1.5) 4 TOTAL ROCKSTAR 190,302,505 175,590,720 8.4% 14,711,785 8.0% (0.3) 5 TOTAL AMP 73,087,711 81,136,208 -9.9% (8,048,497) 3.1% (0.8) 6 TOTAL STARBUCKS COFFEE 67,869,536 56,995,279 19.1% 10,874,257 2.8% 0.2 7 TOTAL NOS 60,724,173 53,932,560 12.6% 6,791,613 2.5% 0.0 8 TOTAL FULL THROTTLE 29,207,101 27,324,066 6.9% 1,883,035 1.2% (0.1) 9 TOTAL PRIVATE LABEL 15,278,168 15,272,049 0.0% 6,119 0.6% (0.1) 10 TOTAL STARBUCKS REFRESHERS 13,103,320 201,365 6407.2% 12,901,955 0.6% 0.5 All Other 94,773,704 93,940,149 0.9% 833,555 4.0% (0.5) Source: AC Nielsen 13 Weeks Ending 11/17/12 - All Outlets Combined [Convenience, Grocery, Drug and Mass (including Wal Mart)] All Outlets Combined Snapshot |

| 2012 Channel Trends Source: 1AC Nielsen Total US Convenience – 13 Weeks Ending 11/17/12 Monster continues to outpace Energy Category growth across all channels. Per Nielsen, Monster sales are up +19.6% for the 13 weeks ending November 17, 2012, versus Category growth of +12.9%, in the Convenience and Gas channel.1 |

| Source: AC Nielsen Total US Convenience – 4 Weeks Ending 11/17/12 Energy Drink Category Share Trends The Monster Energy brand continues to widen the share gap with Red Bull, expanding the gap 5.5 share points in the latest 4 week Nielsen period. |

| Energy Drink Category Share Trends Source: AC Nielsen Total US Convenience – 4 Weeks Ending 11/17/12 |

| Monster Drives Energy Category Growth Sources: 1AC Nielsen Total US Convenience – YTD Ending 11/17/12 Monster continues to drive Energy Category growth in the Convenience and Gas channel. The Monster brand contributed over $366 million to the growth in the Energy Category year to date.1 While total Monster growth makes up 44.2% of the total Energy Category growth, Monster Innovation products have accounted for over $112 million of the growth in the Energy Category year to date.1 Successful innovation such as the Monster Rehab line extensions, Monster Zero Ultra, and Monster Cuba Lima have provided strong growth and attracted new consumers to the Energy Category. All Other Brands 55.8% Monster Innovation 13.5% Monster Established 30.6% Monster 44.2% % of Dollar Growth Energy Category Monster Brand Monster Innovation $828,870,884 $366,089,915 $112,166,960 Dollar Sales Chg vs YA |

| 2012 Key Accomplishments Monster Energy’s latest 13 week performance is outpacing the Energy Category growth in units by a wide margin. Category Monster All Outlets Combined including Walmart1 +13.5% +20.4% Convenience and Gas Channel1 +12.5% +19.3% Source: 1AC Nielsen Total US– 13 Weeks Ending 11/17/12 2AC Nielsen Total US Convenience – 4 Weeks Ending 11/17/12 3AC Nielsen Total US Convenience – 13 Weeks Ending 9/29/12 Monster Rehab Tea+Lemonade+Energy is the #1 sku in the RTD Tea Category in the Convenience and Gas Channel.3, and Monster Rehab as a brand is the #2 brand in that Category.3 Consumers continue to embrace Monster Energy’s innovation. Of Monster’s 34.7% unit share in the Convenience and Gas Channel in the latest 4 weeks, the Rehab line makes up 4.2 points, Absolutely Zero makes up 2.8 points, while newer entries Cuba Lima and Zero Ultra make up 2.1 points together.2 Monster Java is the #1 Energy Coffee brand in the RTD Energy Coffee Category in the Convenience and Gas Channel and is up +29% in units, outpacing that Category at +20.2%.1 Monster’s Original 16oz continues to be one of the fastest growing products in the Energy Drink Category, in particular up +18.8% in units and 21.3% in $’s over a year ago in the Convenience and Gas Channel.1 |

| Monster 2012 Champions Heath Frisby First Snow Mobile Front Flip Taka Higashino X Games Free Style MX Gold Ryan Villopoto 2011 & ‘12 Supercross World Champion Josh Hayes 2010, 2011 & 2012 Pro Superbike Champion Stephane Peterhansel Dakar Rally Champion Nyjah Huston Street League of Skate Board Champion Jamie Bestwick Six Consecutive X Games Metals Jamie Whincup V8 Super Car Champ Australia |

| New Initiatives Kyle & Kurt Bush Nationwide NASCAR Team Kyle Bush Sprint Cup NASCAR Damon Bradshaw Monster Jam Robson Palmero PBR World Finals Champion |

| New Products Q1 2012 Q3 2012 Q3 2012 1H 2013 1H 2013 |

| New Products Q1 2013 Monster Mini’s 8oz. |

| New Products 1H 2013 15.5 oz. |

| Global Expansion |

| 2012: EMEA Value Share Gain Source: Aggregated Nielsen value sales for Great Britain, Ireland, Belgium, France, Netherlands, Norway, Sweden, Denmark, Germany, Poland, Italy, Switzerland, Austria, Greece, Hungary, Czech Republic, Bulgaria, Slovakia, Baltics, South Africa to end September 2012 Monster takes value share across our markets in Europe + South Africa |

| Monster now accounts for 25% of Red Bull value sales in our markets, with an average age in market at less than 3 years 2012: Outpacing the competition Monster widens its lead as the #1 challenger brand to Red Bull in Europe + South Africa Source: Aggregated Nielsen value sales for Great Britain, Ireland, Belgium, France, Netherlands, Norway, Sweden, Denmark, Germany, Poland, Italy, Switzerland, Austria, Greece, Hungary, Czech Republic, Bulgaria, Slovakia, Baltics, South Africa to end September 2012. |

| Monster represents €62m of the 12% YTD growth of the Energy Category in our markets 2012: Driving Category Growth Monster represents 27% of the Energy Drink Market Growth in our European + South African markets Source: Aggregated Nielsen value sales for Great Britain, Ireland, Belgium, France, Netherlands, Norway, Sweden, Denmark, Germany, Poland, Italy, Switzerland, Austria, Greece, Hungary, Czech Republic, Bulgaria, Slovakia, Baltics, South Africa to end September 2012. YTD Value Growth drivers |

| Great Britain's energy category: +9% YTD. Monster’s value growth: +46% YTD. Monster’s market share is 10.6% in the latest 4 weeks*. Effective Monster TDM program. Selected Market Great Britain Source: Nielsen scantrack data to 6th October 2012* Tesco Nielsen reads grocery and convenience (excluding gas stations) in GB |

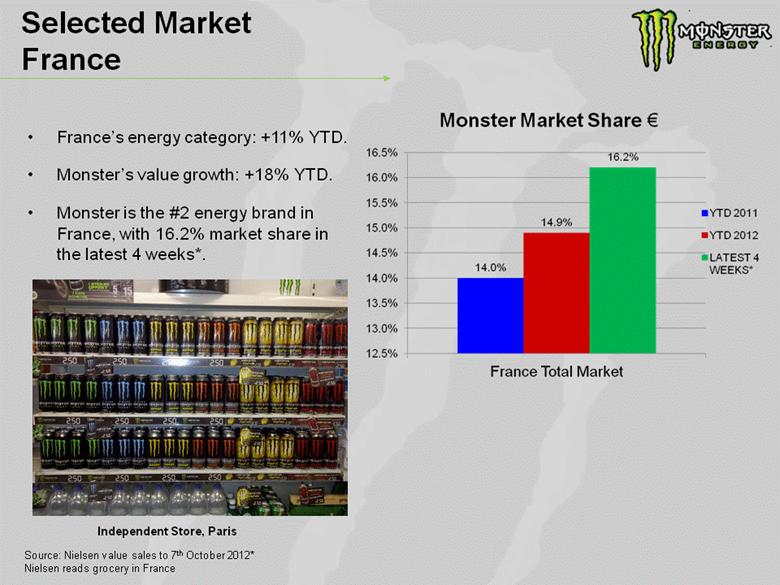

| Selected Market France France’s energy category: +11% YTD. Monster’s value growth: +18% YTD. Monster is the #2 energy brand in France, with 16.2% market share in the latest 4 weeks*. Source: Nielsen value sales to 7th October 2012* Nielsen reads grocery in France Independent Store, Paris |

| Selected Market Spain Spain’s energy category: +11% YTD. Monster’s value growth: +105% YTD. Monster’s market share is 12.9% in the latest 4 weeks*. Red Bull declined 3% year on year and lost 5.3% market share, despite launching their three “Red Bull Editions” The Monster TDM program in Spain is delivering good execution across the retail environment. Source: Nielsen value sales to 7th October 2012* Mercadona Nielsen reads grocery and convenience (excluding gas stations) in Spain |

| Selected Market Germany Germany’s energy category: +22% YTD. Monster’s value growth: +114% YTD. Monster’s market share is 8.4% in the latest 4 weeks*. Monster Energy launched 5 new SKUs in Germany: every new SKU has generated incremental volume. Monster is the #2 Energy Drink brand in Germany, overtaking Rockstar in June 2012. Red Bull grew behind the market at 16% and lost 2.4% share, despite the launch of their three “Red Bull Editions” Effective Monster TDM program. Source: Nielsen value sales excluding Hard Discounters to end Sept. 2012* Germany: Edeka Nielsen reads grocery in Germany |

| Selected Market Greece Greece’s energy category: +7% YTD. Monster’s market share is 28.1% in the latest 4 weeks*. In just two years, Monster has achieved the position of the #2 Energy drink in Greece at 55% the size of Red Bull. Source: Nielsen value sales to end Sept. 2012* Carrefour Carrefour Nielsen reads grocery and convenience (excluding gas stations) in Greece |

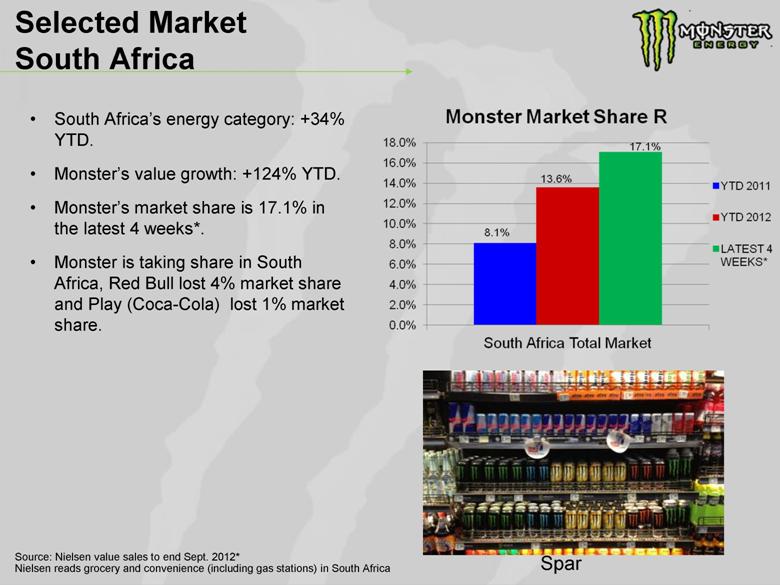

| Selected Market South Africa South Africa’s energy category: +34% YTD. Monster’s value growth: +124% YTD. Monster’s market share is 17.1% in the latest 4 weeks*. Monster is taking share in South Africa, Red Bull lost 4% market share and Play (Coca-Cola) lost 1% market share. Source: Nielsen value sales to end Sept. 2012* Spar Nielsen reads grocery and convenience (including gas stations) in South Africa |

| European Motor Sports Nico Rosberg & Micheal Schumacher Formula 1 Title Sponsor MotoGP Le Mans Valentino Rossi Moto GP Legend Liam Doran British Rally Cross Buttsy Butler Drift Team X Raid Dakar Rally Champions MX1 Motocross Chris Holder Speedway Champion Ken Block Gymkahana Grid |

| European Action Sports Marc Lacomare Surf Harry Main BMX Brendan Fairclough Down Hill Mountain Bike Kjersti Buaas Snowboard Sam Beckett Vert Skate Nassim Guammaz Street Skate Nick Davies Wake Board Sam Pilgrim Free Style Mountain Bike Kevin Rolland Ski |

| Sampling Teams – Western Europe Madrid Barcelona Stuttgart Belgium London Paris Athens Netherlands Portugal |

| Sampling Teams – Eastern Europe Czech Republic Hungary Slovakia |

| Mexico Mexico’s Energy drink category is up +14.9% YTD. 2 Monster Energy is outpacing the category with +25.2% YTD growth. 2 The Monster Energy Brand is #1 in value share, reaching 37.7%1 in the most recent month September 2012 In the Modern Trade Channel, which includes Convenience stores, Monster’s value share is 43.2%1 in September 2012. Source: 1AC Nielsen Total Mexico Modern Trade – September 2012 2AC Nielsen Total Mexico All Outlets Combined incl. Drug – YTD thru September 2012 Monster Energy has attained Preferred Supplier status with the influential Oxxo Convenience chain. Oxxo has nearly 10,000 outlets throughout Mexico and 94% ACV in the Convenience Channel. All Outlets Combined Including drug |

| Mexico Sponsorships Hugo Oliveras NASCAR Monster Army Skate Jam World Rally Motocross |

| Mexico Sponsorships Music X Pilots Freestyle Show DJ Endorsements |

| Sampling Teams – Latin America Puerto Rico Los Cabos Colombia Guadalajara Monterey Brazil |

| Japan Monster Energy launched in Japan in May 2012. Strong retail execution from Asahi achieved 90% distribution on Monster Green and Khaos in the Convenience Channel. Obtained retail authorization for the four largest convenience chains; 7-Eleven, Lawson, Family Mart and Circle K. Monster is the #2 brand in Japan, with 27% convenience channel market share in only eight months1. Research Study Commissioned by Asahi indicated 40% brand awareness for Monster in only six months. 7- Eleven Lawson Independent Retailer Source: Asahi Data |

| Japan Sponsorships Akira Narita #1 Motocross Rider Night Life – DJ Endorsements Kazahiro Kukubu Japanese Olympic Team Member Noriyuki Haga Moto GP Taka Higashino X Games Free Style Champion Ozzy Skate |

| Japan Sponsorships Air Jam Action Sports and Music Festival Sampling 50,000 Fans Athlete Signings Monster Energy Skate Park |

| Sampling Teams - Japan Tokyo |

| Social Media 20 million Facebook fans Monster’s Facebook fans over-index in brand interaction versus other beverage brands. Monster has 9.45% of Facebook beverage fans, but 12.75% of the chatter. Monster Energy’s Facebook effort was grown organically. Company % Engagement % Social Market Share % Share of Voice Monster Energy 13.21% 9.45% 12.75% Red Bull 7.22% 16.09% 11.87% Coke 2.17% 26.24% 5.81% Starbucks 3.80% 15.53% 6.03% Pepsi 15.96% 4.3% 7.06% Source: Blitzmetrics.com |

| Monster’s International Footprint |

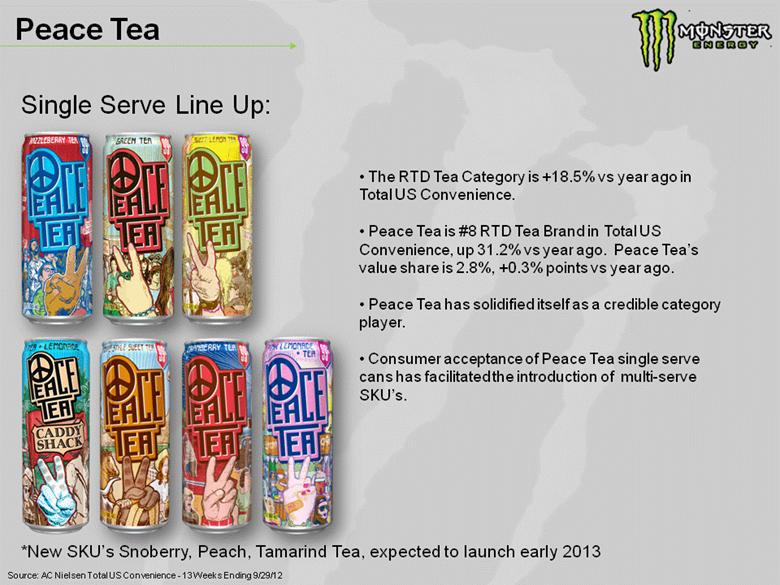

| Peace Tea Single Serve Line Up: *New SKU’s Snoberry, Peach, Tamarind Tea, expected to launch early 2013 The RTD Tea Category is +18.5% vs year ago in Total US Convenience. Peace Tea is #8 RTD Tea Brand in Total US Convenience, up 31.2% vs year ago. Peace Tea’s value share is 2.8%, +0.3% points vs year ago. Peace Tea has solidified itself as a credible category player. Consumer acceptance of Peace Tea single serve cans has facilitated the introduction of multi-serve SKU’s. Source: AC Nielsen Total US Convenience - 13 Weeks Ending 9/29/12 |

| New Peace Tea Products Multi-Serve Line Up: 12pk/ 8oz Fridge Pack 64oz Growler Q1 2013 Fridge Pack will be available in the four most popular flavors |

| Warehouse Division Highlights New Sales Management Team Hubert’s became fastest growing lemonade brand in the Grocery & C-Store Channels and has potential to achieve meaningful success in addressing DSD opportunity1 Hubert’s Lemonade program with Hubert’s 4 packs at Wal-Mart in 2012 is expected to lead to expanded distribution in 2013. Maintained apple juice share leadership in California2 Challenges with apple juice concentrate costs going forward |

| Warehouse Division Product Line Expansion 2012 Hansen’s 7.5oz “Smart Size” Soda package Hansen’s Natural Coconut Waters aseptic boxes Continued expansion of Hubert’s brand Hubert’s Cherry Limeade & Blackberry Lemonade Hubert’s 16oz Glass Half&Half Lemonade Teas Hubert’s 4-Packs 12oz CSD |

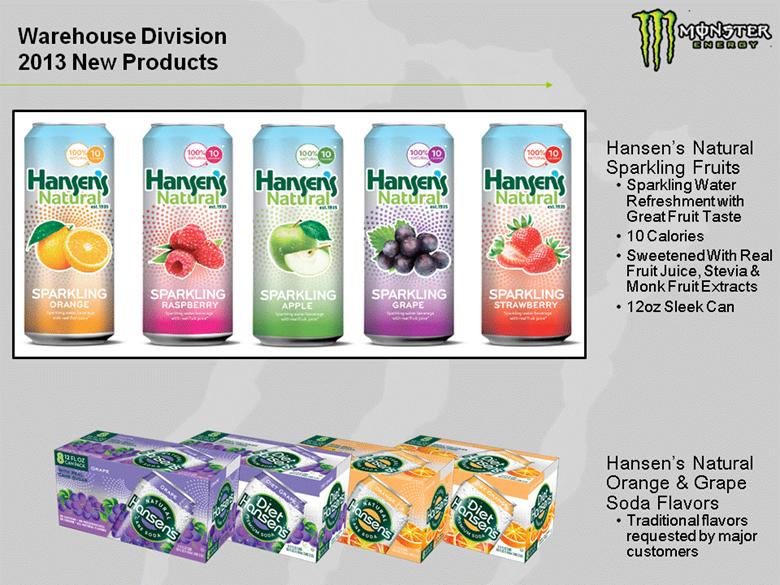

| Warehouse Division 2013 New Products Hansen’s Natural Orange & Grape Soda Flavors Traditional flavors requested by major customers Hansen’s Natural Sparkling Fruits Sparkling Water Refreshment with Great Fruit Taste 10 Calories Sweetened With Real Fruit Juice, Stevia & Monk Fruit Extracts 12oz Sleek Can |

| Monster Beverage Corporation Net Sales ($ in millions) 40.8% CAGR to December 2011 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 9/30/12 9Months 2012 $110.4 $180.3 $348.9 $605.8 $904.5 $1,033.8 $1,143.3 $1,303.9 $1,703.2 $1,589.2 |

| Monster Beverage Corporation Reported Operating Income ($ in millions) 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 9/30/12 9Months 2012 $9.8 $33.9 $103.4 $158.6 $231.0 $163.6 $337.3 $347.8 $456.4 $436.7 |

| Monster Beverage Corporation Adjusted Operating Income (“OI”) ($ in millions) 66.4% CAGR to December 2010 61.7% CAGR to December 2011 9Months 2012 Reported OI $9.8 $33.9 $103.4 $158.6 $231.0 $163.6 $337.3 $347.8 $456.4 $436.7 *Adjustments - 16.5 25.0 117.9 - 2.8 - 1.8 1.1 .6 Adjusted OI $9.8 $33.9 $103.4 $175.1 $256.0 $281.5 $334.5 $346.0 $457.5 $437.3 * Adjusted operating income is a non-GAAP financial measure that includes adjustments for termination costs to prior distributors and for professional service fees, net of insurance reimbursements, associated with the review of stock option grants and granting practices, related litigation and other related matters. Non-GAAP financial measures are not prepared in accordance with GAAP and may be different from non-GAAP financial measures used by other companies. Non-GAAP financial measures should not be considered as a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP. We include these non-GAAP financial measures because we believe they are useful to investors in allowing for greater transparency relat0ed to our ongoing operations. Investors are encouraged to review the reconciliation of the non-GAAP financial measures used to their most directly comparable GAAP financial measures as provided in the table below. 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 9/30/12 $9.8 $33.9 $103.4 $175.1 $256.0 $281.5 $334.5 $346.0 $457.5 $436.8 |

| Monster Beverage Corporation Reported Net Income ($ in millions) 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 9/30/12 9Months 2012 $5.9 $20.4 $62.8 $97.9 $149.4 $108.0 $208.70 $212.0 $286.2 $272.0 |

| Monster Beverage Corporation Reported Diluted Earnings Per Share As adjusted for February 16, 2012 2:1 Stock Split 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 9/30/12 9Months 2012 $0.04 $0.11 $0.33 $0.50 $0.76 $0.56 $1.10 $1.14 $1.53 $1.47 |

| Monster Beverage Corporation Balance Sheet Highlights ($ in thousands) September 30, 2012 December 31, 2011 Percentage Change Cash and cash equivalents $ 283,054 $ 359,331 -21% Investments: Short-term investments $ 307,654 $ 411,282 -25% Long-term investments $ 19,882 $ 23,194 -14% Total Investments $ 327,536 $ 434,476 -25% Total cash and investments $ 610,590 $ 793,807 -23% Trade accounts receivable, net $ 288,584 $ 218,072 32% Inventories $ 193,934 $ 155,613 25% Current liabilities $ 317,038 $ 266,090 19% Deferred revenue $ 112,209 $ 117,151 -4% Total stockholders’ equity $ 889,675 $ 979,158 -9% Shares repurchased during period 6,854,543 4,950,716 (9 Months to September 30, 2012, 12 months to December 31, 2011) |

| Monster Beverage Corporation 3rd Quarter Results (in millions except per share data) 3Q11 3Q12 $82.4 $86.1 Net Income 4.6% 3Q11 3Q12 $474.7 $541.9 Net Sales 14.2% 3Q11 3Q12 $132.1 $140.7 Operating Income 6.5% |

| Shares Purchased Avg. Price (excluding broker's commission) Gross Amount (excluding broker's commission) Activity to 06/30/12 - - - Activity to 09/30/12 6,854,543 $57.99 $397,494,594.44 Activity since 09/30/2012 6,071,535 $50.77 $308,221,727.81 12,926,078 $54.60 $705,716,322.25 2012 Share Repurchases (through December 10, 2012) |