U. S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

| þ | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 2009

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from ______ to ______.

Commission File Number 0-18731

Forlink Software Corporation, Inc.

(Exact name of small business issuer as specified in its charter)

| Nevada | 98-0398666 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification number) |

Shenzhou Mansion 9F, ZhongGuanCun South Street, No. 31,

Haidian District, Beijing, China 100081

(Address of principal executive offices and zip code)

0086-10 6811 8866

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ¨ NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ¨ |

| | |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO þ

Number of shares of common stock outstanding as of November 6, 2009: 4,651,173

FORLINK SOFTWARE CORPORATION, INC.

FORM 10-Q

INDEX

| | Page Number |

| | |

| SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS | |

| | |

| PART I. FINANCIAL INFORMATION | |

| | | |

| Item 1. | Financial Statements (unaudited) | 1 |

| | | |

| | Consolidated Balance Sheet as of September 30, 2009 | 2 |

| | | |

| | Consolidated Statements of Operations | 3 |

| | | |

| | Consolidated Statements of Cash Flows | 4 |

| | | |

| | Notes to the Consolidated Financial Statements as of September 30, 2009 | 5-21 |

| | | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22-31 |

| | | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 31 |

| | | |

| Item 4. | Controls and Procedures | 31 |

| | | |

| PART II. OTHER INFORMATION | 33 |

| | | |

| Item 1. | Legal Proceedings | 33 |

| | | |

| Item 1A. | Risk Factors | 33 |

| | | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 34 |

| | | |

| Item 3. | Defaults Upon Senior Securities | 34 |

| | | |

| Item 4. | Submission of Matters to a Vote of Security Holders | 34 |

| | | |

| Item 5. | Other Information | 34 |

| | | |

| Item 6. | Exhibits | 35 |

| | | |

| SIGNATURES | |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains certain statements of a forward-looking nature. Such forward-looking statements, including but not limited to growth and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond the control of the Company. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “will,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties that could cause actual results to differ materially from those projected or anticipated.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update this forward-looking information. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Form 10-Q. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

PART I. FINANCIAL INFORMATION

| ITEM 1. | FINANCIAL STATEMENTS. |

The information required by Item 1 commences on the next page.

Forlink Software Corporation, Inc.

Consolidated Balance Sheets

| (Expressed in US Dollars) | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | (unaudited) | | | | |

| ASSETS | | | | | | |

| | | | | | | |

| Current assets | | | | | | |

| | | | | | | |

| Cash and cash equivalents | | $ | 970,930 | | | $ | 2,543,430 | |

| Accounts receivable | | | 1,767,636 | | | | 898,005 | |

| Other receivables, deposits and prepayments (Note 3) | | | 886,676 | | | | 1,627,555 | |

| Inventories (Note 4) | | | 1,206,655 | | | | 1,019,713 | |

| Deferred taxes assets | | | 115 | | | | 3,160 | |

| | | | | | | | | |

| Total current assets | | | 4,832,012 | | | | 6,091,863 | |

| | | | | | | | | |

| Property, plant and equipment (Note 6) | | | 434,973 | | | | 593,805 | |

| Long term investments (Note 7) | | | 5,005,898 | | | | 5,074,622 | |

| | | | | | | | | |

| Total assets | | $ | 10,272,883 | | | $ | 11,760,290 | |

| | | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

| | | | | | | | | |

| Current liabilities | | | | | | | | |

| Accounts payable | | $ | 1,964,126 | | | $ | 2,050,321 | |

| Amounts due to stockholders (Note 5) | | | 401,926 | | | | 378,672 | |

| Customer deposits | | | 1,105,358 | | | | 1,123,060 | |

| Other payables and accrued expenses (Note 9) | | | 714,451 | | | | 605,319 | |

| Income tax payable | | | 0 | | | | 16 | |

| Other tax payable | | | 999,488 | | | | 973,588 | |

| Deferred taxes debt | | | 0 | | | | 0 | |

| | | | | | | | | |

| Total current liabilities | | $ | 5,185,349 | | | $ | 5,130,976 | |

| | | | | | | | | |

| Commitments and contingencies | | | | | | | | |

| | | | | | | | | |

| Minority interest (Note 9) | | $ | 146,286 | | | $ | 193,295 | |

| | | | | | | | | |

| Stockholders’ equity | | | | | | | | |

| Common stock, par value $0.001 per share; | | | | | | | | |

| 200,000,000 and 200,000,000 shares authorized; | | | | | | | | |

4,966,173 and 4,966,173 shares issued and 4,651,173 and 4,651,173 shares outstanding, respectively | | $ | 99,322 | | | $ | 99,322 | |

| Treasury stock | | | (163,800 | ) | | | (163,800 | ) |

| Additional paid-in capital | | | 10,195,693 | | | | 10,195,693 | |

| Accumulated losses | | | (6,274,495 | ) | | | (4,759,592 | ) |

| Accumulated other comprehensive income | | | 1,084,528 | | | | 1,064,396 | |

| | | | | | | | | |

| Total stockholders’ equity | | $ | 4,941,248 | | | $ | 6,436,019 | |

| | | | | | | | | |

| Total liabilities and stockholders’ equity | | $ | 10,272,883 | | | $ | 11,760,290 | |

See accompanying notes to unaudited consolidated condensed financial statements.

Forlink Software Corporation, Inc.

Consolidated Statements of Operations

(unaudited)

(Expressed in US Dollars)

| | | Three Months ended | | | Nine Months Ended | |

| | | September 30, | | | September 30, | |

| | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| | | | | | | | | | | | | |

| Net sales | | | 822,658 | | | | 1,667,319 | | | | 2,647,012 | | | | 4,661,218 | |

| Cost of sales | | | (465,358 | ) | | | (542,687 | ) | | | (1,944,179 | ) | | | (1,362,161 | ) |

| | | | | | | | | | | | | | | | | |

| Gross profit | | | 357,300 | | | | 1,124,632 | | | | 702,833 | | | | 3,299,057 | |

| | | | | | | | | | | | | | | | | |

| Selling expenses | | | (240,680 | ) | | | (255,746 | ) | | | (853,208 | ) | | | (962,643 | ) |

| Research and development expenses | | | (272,104 | ) | | | (115,972 | ) | | | (756,843 | ) | | | (421,768 | ) |

| General and administrative expenses | | | (288,694 | ) | | | (334,817 | ) | | | (781,171 | ) | | | (1,374,779 | ) |

| | | | | | | | | | | | | | | | | |

| Total operating expenses | | | (801,478 | ) | | | (706,535 | ) | | | (2,391,222 | ) | | | (2,759,190 | ) |

| | | | | | | | | | | | | | | | | |

| Operating profit/(loss) | | | (444,178 | ) | | | 418,097 | | | | (1,688,389 | ) | | | 539,867 | |

| | | | | | | | | | | | | | | | | |

| Income from equity method investee | | | 18,262 | | | | 57,826 | | | | 38,591 | | | | 65,656 | |

| Income from cost method investee | | | 1,615 | | | | 4,685 | | | | 8,919 | | | | 247,631 | |

| Interest income | | | 1,446 | | | | 3,854 | | | | 8,281 | | | | 13,128 | |

| | | | | | | | | | | | | | | | | |

| Other income, net | | | 1,123 | | | | 23,992 | | | | 89,882 | | | | 37,626 | |

| | | | | | | | | | | | | | | | | |

| Profit / (Loss) before tax | | | (421,732 | ) | | | 508,454 | | | | (1,542,716 | ) | | | 903,908 | |

| | | | | | | | | | | | | | | | | |

| Income tax | | | 9,562 | | | | (205,715 | ) | | | (19,196 | ) | | | (214,169 | ) |

| Minority interest | | | (12,948 | ) | | | (17,298 | ) | | | (47,009 | ) | | | (54,622 | ) |

| | | | | | | | | | | | | | | | | |

| Net profit/(loss) | | | (399,222 | ) | | | 320,037 | | | | (1,514,903 | ) | | | 744,361 | |

| | | | | | | | | | | | | | | | | |

| Profit/(loss) per share | | | (0.09 | ) | | | 0.07 | | | | (0.33 | ) | | | 0.16 | |

| | | | | | | | | | | | | | | | | |

| Weighted average common shares outstanding -basic and diluted | | | 4,651,173 | | | | 4,644,431 | | | | 4,651,173 | | | | 4,642,209 | |

See accompanying notes to unaudited consolidated condensed financial statements.

Forlink Software Corporation, Inc.

Consolidated Statements of Cash Flows

Increase in Cash and Cash Equivalents

(unaudited)

| (Expressed in US Dollars) | | Nine Months Ended September 30, | |

| | | 2009 | | | 2008 | |

| Cash flows from operating activities | | | | | | |

| Net profit/(loss) | | $ | (1,514,903 | ) | | $ | 744,361 | |

| Adjustments to reconcile net profit/(loss) to | | | | | | | | |

| net cash provided by/(used in) operating activities | | | | | | | | |

| Minority interest | | | (47,009 | ) | | | (54,622 | ) |

| (Gain)/loss from write-off of property, plant and equipment | | | | | | | | |

| Depreciation of property, plant and equipment | | | 155,146 | | | | 188,991 | |

| Non-cash compensation expense | | | - | | | | - | |

| Income from equity method investee | | | | | | | | |

| Loss from equity method investee | | | (38,591 | ) | | | (65,656 | ) |

| Dividend received from investee | | | (8,919 | ) | | | (247,631 | ) |

| Effect of deferred taxes | | | 22,209 | | | | 13,098 | |

| | | | | | | | | |

| Change in: | | | | | | | | |

| Accounts receivable | | | (870,282 | ) | | | (819,132 | ) |

| Other receivables, deposits and prepayments | | | 743,516 | | | | (72,973 | ) |

| Inventories | | | (187,747 | ) | | | (570,554 | ) |

| Accounts payable | | | (84,577 | ) | | | 15,289 | |

| Amounts due to stockholders | | | 23,553 | | | | (112,675 | ) |

| Customer deposits | | | (16,816 | ) | | | (754,305 | ) |

| Other payables and accrued expenses | | | 154,052 | | | | (66,709 | ) |

| Income tax payable | | | (16 | ) | | | 201,991 | |

| Other taxes payable | | | 26,668 | | | | 31,396 | |

| | | | | | | | | |

| Net cash provided by/(used in) operating activities | | | (1,643,714 | ) | | | (1,569,131 | ) |

| | | | | | | | | |

| Cash flows from investing activities | | | | | | | | |

| Purchase of long term investment | | | | | | | | |

| Acquisition of property, plant and equipment | | | (15,013 | ) | | | (84,902 | ) |

| Proceeds from disposal of long term investment | | | - | | | | - | |

| Dividend from investee | | | 111,272 | | | | 452,885 | |

| | | | | | | | | |

| Net cash used in investing activities | | | 96,259 | | | | 367,983 | |

| | | | | | | | | |

| Cash flows from financing activities | | | | | | | | |

| Repayment to short term borrowings | | | - | | | | - | |

| (Repayments to)/advances from stockholders | | | - | | | | - | |

| Proceeds from issuances of common stock under Plan 2002 | | | - | | | | 200 | |

| Increase/decrease in additional paid in capital | | | - | | | | 9,800 | |

| | | | | | | | | |

| Net cash provided by financing activities | | | - | | | | 10,000 | |

| | | | | | | | | |

| Effect of exchange rate changes | | | (25,045 | ) | | | 310,529 | |

| | | | | | | | | |

| Net increase/(decrease) in cash and cash equivalents | | | (1,572,500 | ) | | | (880,619 | ) |

| | | | | | | | | |

| Cash and cash equivalents at beginning of period | | | 2,543,430 | | | | 2,400,901 | |

| | | | | | | | | |

| Cash and cash equivalents at end of period | | $ | 970,930 | | | $ | 1,520,282 | |

| Supplemental disclosure of cash flow information | | | | | | | | |

| Income tax paid | | $ | 28,755 | | | $ | 1,666 | |

| Interest paid | | $ | - | | | $ | - | |

See accompanying notes to unaudited consolidated condensed financial statements.

NOTE 1 - ORGANIZATION AND DESCRIPTION OF BUSINESS

Forlink Software Corporation, Inc. (the "Company" or the "Registrant" or "Forlink"), is a Nevada corporation which was originally incorporated on January 7, 1986 as "Why Not?, Inc." under the laws of the State of Utah and subsequently reorganized under the laws of Nevada on December 30, 1993. From 1996 until 1999, the Company continued as an unfunded venture in search of a suitable business acquisition or business combination.

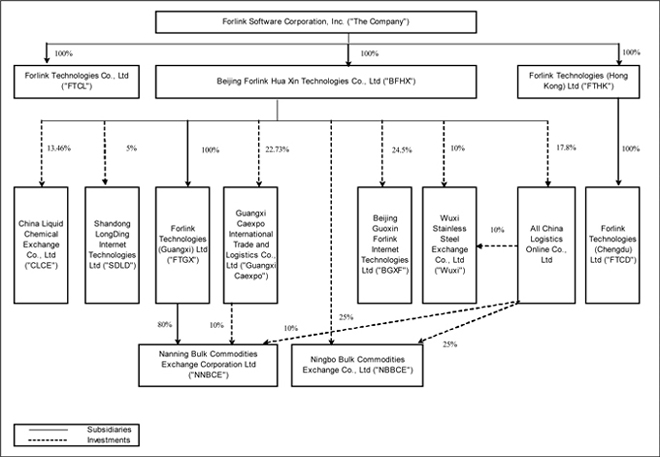

On November 3, 1999, the Company entered into a Plan of Reorganization with Beijing Forlink Software Technology Co., Ltd., (hereinafter "BFSTC"), a limited liability company organized under the laws of the People’s Republic of China (“PRC” or “China”), under the terms of which BFSTC gained control of the Company. Pursuant to the Plan of Reorganization, the Company acquired 100% of the registered and fully paid-up capital of BFSTC in exchange for 20,000,000 shares of the Company's authorized, but unissued, common stock. BFSTC is engaged in the provision of computer software consultancy and engineering services and the development and sale of computer software in the PRC. As a part of its computer consultancy and engineering services, BFSTC is also engaged in the sale of computer hardware. In June 2001, BFSTC changed its name to Forlink Technologies Co. Ltd. (“FTCL”). FTCL is the Company’s major operating subsidiary in China.

In August 2001, the Company acquired Beijing Slait Science & Technology Development Limited Co. (“SLAIT”) pursuant to a Plan of Reorganization dated January 11, 2001. The Company issued 59,430,000 shares of its common stock to SLAIT’s original beneficial owners in exchange for 100% of the outstanding equity of SLAIT. As a result of the share exchange, the former beneficial owners of SLAIT own approximately 70% of the issued and outstanding shares of the Company, and SLAIT became a wholly-owned subsidiary of the Company. The Company also agreed to transfer 1,085,000 RENMINBI (“RMB”) (approximately US$131,039) to the former owners of SLAIT. A change in control occurred in which all but one of the officers and directors of the Company resigned and two former directors (also former owners) of SLAIT became officers and directors of the Company. Prior to its dissolution in 2004, SLAIT provided application system integration technology and specializes in large volume transaction processing software for networks such as mobile phone billing and band operation. Subsequent to the acquisition, the principal activities of SLAIT were gradually shifted to those of FTCL. On February 13, 2004, SLAIT was officially dissolved in accordance with relevant PRC regulations.

On June 18, 2003, Forlink Technologies (Hong Kong) Limited (“FTHK”) was incorporated in Hong Kong Special Administrative Region as a limited liability company. In December 2003, FTHK became a wholly owned subsidiary of Forlink. FTHK is an investment holding company set up to take advantage of the favorable business environment in Hong Kong and to facilitate the Company’s investment transactions. Through FTHK, on December 18, 2003, the Company invested $760,870 in All China Logistics Online Co., Ltd. ("All China Logistics"), a privately held PRC company providing logistic services in China, in exchange for a 17.8% equity interest.

On June 14, 2004, Forlink Technologies (Chengdu) Limited ("FTCD") was established as a limited liability company in Chengdu, PRC and subsequently became a wholly owned subsidiary of FTHK in September 2004. FTCD is in the business of providing software outsourcing services and software development. The registered capital of FTCD is $5,000,000 and the fully paid up capital was $750,000 as of December 31, 2005. In April 2006, FTHK further invested $130,000 in FTCD. FTCD commenced operations in late 2005. The registered capital of FTCD was reduced to $200,000 in December 2007, which amount was fully paid as of December 2007.

In compliance with China’s foreign investment restrictions on telecom value-added services and other laws and regulations, the Company conducts telecom value-added services and application integration services for government organizations in China via Beijing Forlink Hua Xin Technology Co. Ltd. ("BFHX"). BFHX was established in the PRC on September 19, 2003 as a limited liability company. The registered capital of BFHX is $120,733 (RMB 1,000,000) and was fully paid up as of March 31, 2005. Mr. Yi He and Mr. Wei Li have been entrusted as nominee owners of BFHX to hold 70% and 30%, respectively, of the fully paid up capital of BFHX on behalf of the Company as the primary beneficiary. BFHX is considered a variable interest entity ("VIE"), and because the Company is the primary beneficiary, the Company’s consolidated financial statements include BFHX. Upon the request of the Company, Mr. Yi He and Mr. Wei Li are required to transfer their ownership interests in BFHX to the Company or its designees at any time for the amount of the fully paid registered capital of BFHX. Mr. Yi He is the Chief Executive Officer, a director and a major stockholder of the Company. Mr. Wei Li is the administration manager of FTCL.

On October 24, 2005, the Company entered into a definitive agreement to acquire a 17.5% equity interest of China Liquid Chemical Exchange Company Limited (“CLCE”), a PRC limited liability company, in exchange for deployment of the Company’s For-online Electronic Trading System. In early 2007, CLCE increased its share capital to $1,708,526 (RMB 13,000,000). As the Company did not subscribe for the new shares, the Company’s shareholding of CLCE was diluted and as of September 30 2009 was 13.46%. CLCE commenced operations fully in early 2007.

On October 3, 2006, the Company entered into a Transfer of Right to Invest and Project Cooperation Agreement (“Statelink Agreement”) with Statelink International Group, Ltd., a British Virgin Islands company (“Statelink”), pursuant to which the Company acquired 22.73% registered capital in Guangxi Caexpo International Trade and Logistics Co., Ltd. (“Guangxi Caexpo”), a PRC limited liability company in the businesses of real estate development, advertising and computer distribution, for cash consideration of $2,557,545 (RMB 20,000,000) from BFHX and stock consideration of 13,000,000 shares of the Company’s restricted common stock. On October 26, 2006, BFHX established Forlink Technologies (Guangxi) Limited (“FTGX”), a PRC limited liability company, to carry out a contract from Guangxi Caexpo to build an “Electronic Trade and Logistics Information Platform and Call Center” (the “Project”). At the time of incorporation, BFHX injected RMB 20,000,000 (approximately US$2,557,545) as registered capital to FTGX.

On October 12, 2006, the Company invested $31,969 (RMB 250,000) in Wuxi Stainless Steel Exchange Co., Ltd. (“Wuxi Exchange”), a PRC limited liability company, and deployed a proprietary, integrated software solution to support Wuxi Exchange’s operations in December 2006, for a 12.5% equity interest. On January 14, 2007, the Company entered into an agreement with a major shareholder of Wuxi Exchange to transfer 2.5% of the Company’s interest in Wuxi Exchange to the major shareholder for a cash payment of RMB 500,000.

On January 25, 2007, the board of directors and the majority holders of the Company’s common stock jointly approved an amendment to the Company’s Articles of Incorporation by written consent, to increase the number of authorized shares of common stock from 100,000,000 to 200,000,000. The Certificate of Amendment to the Articles of Incorporation to effect the increase of the number of the Company’s authorized common shares was filed with Nevada’s Secretary of State on April 4, 2007.

On April 29, 2007, the Company invested, through BFHX, $138,158 (RMB 1,050,000) in Beijing GuoXin Forlink Internet Technologies Limited (“BGXF”), a privately held PRC company that operates a finance study website, for a 35% equity interest. The investment in BGXF is accounted for under the equity method of accounting due to the Company’s significant influence over the operational and financial policies of BGXF. BGXF commenced operations on March 9 2008. On October 14, 2008, the registered capital of BGXF was increased to RMB 4,285,700, and since the Company did not invest additional funds into BGFX, the ratio of its holding was diluted to a 24.5% equity interest.

On July 12, 2007, the Company invested through FTGX, $1,063,830 (RMB 8,000,000) in Nanning Bulk Commodities Exchange Corporation Limited (“NNBCE”), a privately held PRC company, for an 80% equity interest, and NNBCE became a subsidiary of FTGX. Set up on April 29, 2007, NNBCE commenced operations on March 28, 2008, and provides logistical e-commerce service.

On September 5, 2007, the Company invested $465,425 (RMB 3,500,000), through NNBCE, in Guangxi Bulk Sugar & Ethanol Exchange Corporation Limited (“GBSEE”), a PRC limited liability company established on September 12, 2007, for a 35% equity interest. Concurrently, All China Logistics was entrusted as nominee owner of GBSEE to hold 20% of the fully paid up capital of GBSEE on behalf of NNBCE as the primary beneficiary. Upon the request of NNBCE, All China Logistics is required to transfer its ownership interests in GBSEE to NNBCE or its designees at any time for the amount of the 20% fully paid up capital. In accordance with Financial Accounting Standards Board (“FASB”) Interpretation No. 46R “Consolidation of Variable Interest Entities - An Interpretation of ARB No. 51” (“FIN 46R”), NNBCE is deemed to hold the primary beneficial interest of 55% equity interest in GBSEE. GBSEE was established to provide logistical e-commerce service, but it was dissolved on December 16, 2007 before it commenced any operations and NNBCE received payments back of its investment in GBSEE of $410,397 (RMB 3,000,000) in December 2007; $66,211 (RMB 484,000) in February 2008, and $2,189 (RMB 16,000) in September 2008.

On December 24, 2007, the board of directors and the majority holders of the Company’s common stock jointly approved an amendment to the Company’s Articles of Incorporation by written consent, to effect a 1-for-20 reverse stock split. The Certificate of Amendment to the Articles of Incorporation to effect the reverse split was filed with Nevada’s Secretary of State on February 21, 2008.

On March 20, 2008, the Company invested $71,124 (RMB 500,000), through BFHX, in Shandong LongDong Internet Technologies Limited (“SDLD”), a PRC limited liability company established on October 24, 2007, for a 5% equity interest. SDLD, which commenced operations in December 2007, is in the business of providing of providing primary products e-commerce services. The purpose of this investment is to gain cash dividends from SDLD.

Forlink, its subsidiaries and VIE (hereinafter collectively referred to as the “Company”), are all operating companies. Set forth below is a diagram illustrating the Company’s corporate structure as of September 30, 2009:

NOTE 2 - BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Accounting and Principles of Consolidation

The consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America that include the financial statements of Forlink and its subsidiaries and VIE, namely, FTCL, FTHK, BFHX, FTCD, FTGX, and NNBCE. All inter-company transactions and balances have been eliminated.

Minority interests at the balance sheet date, being the portion of the net assets of subsidiaries attributable to equity interests that are not owned by Forlink, whether directly or indirectly through subsidiaries, are presented in the consolidated balance sheet separately from liabilities and the shareholders’ equity. Minority interests in the results of the Company for the years are also separately presented in the income statement.

Use of Estimates

The preparation of financial statements in accordance with generally accepted accounting principles requires management to make estimates and assumptions that affect reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Foreign Currency Translation and Transactions

The functional currency of Forlink is US Dollar (“US$”) and the financial records are maintained and the financial statements prepared in US$. The functional currency of FTHK is HK Dollar (“HK$”) and its financial records are maintained, and its financial statements prepared, in HK$. The functional currency of FTCL, BFHX, FTCD, FTGX, and NNBCE is RENMINBI (“RMB”) and their financial records are maintained, and their financial statements are prepared, in RMB.

Foreign currency transactions during the period are translated into each company’s denominated currency at the exchange rates at the transaction dates. Gain and loss resulting from foreign currency transactions are included in the consolidated statement of operations. Assets and liabilities denominated in foreign currencies at the balance sheet date are translated into each company’s denominated currency at the yearend exchange rates. All exchange differences are dealt with in the consolidated statements of operations.

The financial statements of the Company’s operations based outside of the United States have been translated into US$ in accordance with SFAS 52. Management has determined that the functional currency for each of the Company’s foreign operations is its applicable local currency. When translating functional currency financial statements into US$, year-end exchange rates are applied to the consolidated balance sheets, while average period rates are applied to consolidated statements of operations. Translation gains and losses are recorded in translation reserve as a component of stockholders’ equity.

The value of the RMB is subject to changes in China’s central government policies and to international economic and political developments affecting supply and demand in the China Foreign Exchange Trading System market. Since 1994, the conversion of RMB into foreign currencies, including US$, has been based on rates set by the People’s Bank of China, which are set daily based on the previous day’s inter-bank foreign exchange market rates and current exchange rates on the world financial markets. Since 1994, the official exchange rate generally has been stable. In July 2005, the Chinese government announced that it will no longer peg its currency exclusively to US$ but will switch to a managed floating exchange rate based on market supply and demand with reference to a basket of currencies which will likely increase the volatility of RMB as compared to US$. The exchange rate of RMB to US$ changed from RMB8.28 to RMB8.11 in late July 2005.

The exchange rates used as of September 30, 2009 and December 31, 2008 are US$1:HK$7.78:RMB6.84, and US$1:HK$7.78:RMB6.83, respectively. The weighted average rates ruling for the periods ended September 30, 2009 and September 30, 2008 are US$1:HK$7.78:RMB6.84, and US$1:HK$7.82:RMB6.91, respectively.

Foreign Currency Risk

The RMB is not a freely convertible currency. The State Administration for Foreign Exchange, under the authority of the People’s Bank of China, controls the conversion of RMB into foreign currencies. The value of the RMB is subject to changes in central government policies and to international economic and political developments affecting supply and demand in the China Foreign Exchange Trading System market.

The PRC subsidiaries conduct their business substantially in the PRC, and their financial performance and position are measured in terms of RMB. Any devaluation of the RMB against the USD would consequently have an adverse effect on the financial performance and asset values of the Company when measured in terms of USD. The PRC subsidiaries’ products are primarily procured, sold and delivered in the PRC for RMB. Thus, their revenues and profits are predominantly denominated in RMB. Should the RMB devalue against USD, such devaluation could have a material adverse effect on the Company’s profits and the foreign currency equivalent of such profits repatriated by the PRC entities to the Company.

Cash and Cash Equivalents

Cash and cash equivalents include cash in hand and all highly liquid investments with an original maturity of three months or less.

Allowance for Doubtful Accounts

We record an allowance for doubtful accounts based on specifically identified amounts that the Company believes to be uncollectible. We have a limited number of customers with individually large amounts due at any given balance sheet date. Any unanticipated change in one of those customers’ credit worthiness or other matters affecting the collectability of amounts due from such customers could have a material effect on the results of operations in the period in which such changes or events occur. After all attempts to collect a receivable have failed, the receivable is written off against the allowance.

Inventories

Inventories are stated at the lower of cost or market. For inventory used in system integration services, cost is calculated using the specific identification method. For the sale of computer hardware, cost is calculated using first-in, first-out method. Cost includes all costs of purchase, cost of conversion and other costs incurred in bringing the inventories to their present location and condition. Market value is determined by reference to the sales proceeds of items sold in the ordinary course of business after the balance sheet date or to management estimates based on prevailing market conditions.

Property, Plant, Equipment and Depreciation

Property, plant and equipment are stated at cost. Depreciation is computed using the straight-line method to allocate the cost of depreciable assets over the estimated useful lives of the assets as follows:

| | | Estimated useful life (in years) | |

| | | | |

| Building | | | 20 | |

| Computer equipment | | | 3 | |

| Office equipment | | | 5 | |

| Motor vehicle | | | 10 | |

Major improvements of property, plant and equipment are capitalized, while expenditures for repair and maintenance and minor renewals and betterments are charged directly to the statements of operations as incurred. When assets are disposed of, the related cost and accumulated depreciation thereon are removed from the accounts and any resulting gain or loss is included in the statement of operations.

Computer Software Development Costs

In accordance with SFAS No. 86 “Accounting for the Cost of Computer Software to be Sold, Leased or Otherwise Marketed” software development costs are expensed as incurred until technological feasibility in the form of a working model has been established. Deferred software development costs will be amortized over the estimated economic life of the software once the product is available for general release to customers. For the current software products, the Company determined that technological feasibility was reached at the point in time it was available for general distribution. Therefore, no costs were capitalized.

Long term investments

The Company’s long term investments consist of (1) equity investments which are accounted for in accordance with the equity method and (2) cost investments which are accounted for under the cost method. Under the equity method, each such investment is reported at cost plus the Company’s proportionate share of the income or loss or other changes in stockholders’ equity of each such investee since its acquisition. The consolidated results of operations include such proportionate share of income or loss. See Note 8.

Fair Values of Financial Instruments

The carrying amounts of financial instruments (cash and cash equivalents, investments, accounts receivable and accounts payable) approximate their fair values as of September 30, 2009 and December 31, 2008 because of the relatively short-term maturity of these instruments.

Revenue Recognition

The Company generally provides services under multiple element arrangements, which include software license fees, hardware and software sales, and the provision of system integration services including consulting, implementation, and software maintenance. The Company evaluates revenue recognition on a contract-by-contract basis as the terms of each arrangement vary. The evaluation of the contractual arrangements often requires judgments and estimates that affect the timing of revenue recognized in the statements of operations. Specifically, the Company may be required to make judgments about:

| | · | whether the fees associated with our products and services are fixed or determinable; |

| | | whether collection of our fees is reasonably assured; |

| | | whether professional services are essential to the functionality of the related software product; |

| | | whether we have the ability to make reasonably dependable estimates in the application of the percentage-of-completion method; and |

| | | whether we have verifiable objective evidence of fair value for our products and services. |

The Company recognizes revenues in accordance with the provisions of Statements of Position, or SOP, No. 97-2, “Software Revenue Recognition,” as amended by SOP No. 98-9, “Modification of SOP 97-2, Software Revenue Recognition, with respect to Certain Transactions,” Staff Accounting Bulletin, or SAB, 104, “Revenue Recognition.” SOP 97-2 and SAB 104 require among other matters, that there be a signed contract evidencing an arrangement exists, delivery has occurred, the fee is fixed or determinable, and collectability is probable.

Software license revenue is recognized over the accounting periods contained in the terms of the relevant agreements, commencing upon the delivery of the software provided that (1) there is evidence of an arrangement, (2) the fee is fixed or determinable and (3) collection of the fee is considered probable.

Revenue from non-software, multiple-element arrangements is recognized in accordance with Emerging Issues Task Force No. 00-21, “Revenue Arrangements with Multiple Deliverables” (“EITF 00-21”). Under EITF 00-21, the Company recognizes revenue from the multiple-deliverables which has value to the customer on a stand-alone basis. Deliverables in an arrangement that do not meet the separation criteria in EITF 00-21 are treated as one unit of accounting for purposes of revenue recognition.

In the case of maintenance revenues, vendor-specific objective evidence, or VSOE, of fair value is based on substantive renewal prices, and the revenues are recognized ratably over the maintenance period.

In the case of consulting and implementation services revenues, where VSOE is based on prices from stand-alone sale transactions, the revenues are recognized as services that are performed pursuant to paragraph 65 of SOP 97-2.

For hardware transactions where software is incidental, the Company does not apply separate accounting guidance to the hardware and software elements. The Company applies the provisions of EITF 03-05, “Applicability of AICPA Statement of Position 97-2, Software Revenue Recognition, to Non-Software Deliverables in an Arrangement Containing More-Than-Incidental Software” (“EITF 03-05”). Per EITF 03-05, if the software is considered not essential to the functionality of the hardware, then the hardware is not considered “software related” and is excluded from the scope of SOP 97-2. Such sale of computer hardware is recognized as revenue on the transfer of risks and rewards of ownership, which generally coincides with the time when the goods are delivered to customers and title has passed, pursuant to SAB 104.

Remote hosting services, where VSOE is based upon consistent pricing charged to customers based on volumes and performance requirements on a stand-alone basis and substantive renewal terms, are recognized ratably over the contract term as the services are performed. The remote hosting arrangements generally require the Company to perform one-time set-up activities and include a one-time set-up fee. This one-time set-up fee is generally paid by the customer at contract execution. The Company has determined that these set-up activities do not constitute a separate unit of accounting, and accordingly, the related set-up fees are recognized protractedly over the term of the contract.

The Company is considering the applicability of EITF 00-3, “Application of AICPA Statement of SOP 97-2 to Arrangements That Include the Right to Use Software Stored on Another Entity’s Hardware,” to the hosting services arrangements on a contract-by-contract basis. If the Company determines that the customer does not have the contractual right to take possession of the Company’s software at any time during the hosting period without significant penalty, SOP 97-2 would not apply to these contracts in accordance with EITF 00-3. Accordingly, these contracts would be accounted for pursuant to SAP 104.

Stock Based Compensation

Effective January 1, 2006, we adopted Statement of Financial Accounting Standards 123(R), “Share-Based Payment” (“SFAS 123(R)”), using the modified prospective application transition method. Before we adopted SFAS 123(R), we accounted for share-based compensation in accordance with Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees.”

SFAS 123(R) requires the Company to record the cost of stock options and other equity-based compensation in its income statement based upon the estimated fair value of those rewards. The Company elected to use the modified prospective method for adoption, which requires compensation expense to be recorded for all unvested stock options and other equity-based compensation beginning in the first quarter of adoption. Accordingly, prior periods have not been restated to reflect stock based compensation. On January 1, 2006, the Company adopted SFAS 123(R) using the modified prospective method, and the adoption of this standard did not have a material impact on the Company’s consolidated financial statements because most of the Company’s outstanding stock options were vested as of December 31, 2005 and the unvested portion of the stock options was considered immaterial.

SFAS 123(R) also requires the Company to estimate forfeitures in calculating the expense relating to share-based compensation as opposed to recognizing forfeitures as an expense reduction as they incur. The adjustment to apply estimated forfeitures to previously share-based compensation was considered immaterial by the Company and as such was not classified as a cumulative effect of a change in accounting principle. As of January 1, 2006, the Company had no unrecognized compensation cost remaining associated with existing stock option grants. Also, the Company made no modifications to outstanding stock option grants prior to the adoption of Statement No. 123(R), and there were no changes in valuation methodologies or assumptions compared to those used by the Company prior to January 1, 2006.

In November 2005, the FASB issued FSP No. 123(R)-3, “Transition Election Related to Accounting for the Tax Effects of Share-Based Payment Awards.” The Company adopted the alternative transition method provided in the FSP for calculating the tax effects of share-based compensation pursuant to FAS 123(R) in the fourth quarter of fiscal 2006. The alternative transition method includes simplified methods to establish the beginning balance of the Additional Paid-in Capital (“APIC”) pool related to the tax effects of employee share-based compensation, and to determine the subsequent impact on the APIC pool and Consolidated Statements of Cash Flows of the tax effects of employee share-based compensation awards that are outstanding upon adoption of FAS 123(R). The adoption did not have a material impact on the Company’s results of operations and financial position.

In February 2006, the FASB issued FASB Staff Position No. FAS 123(R)-4, “Classification of Options and Similar Instruments Issued as Employee Compensation That Allow for Cash Settlement upon the Occurrence of a Contingent Event.” This position amended SFAS 123(R) to incorporate that a cash settlement feature that can be exercised only upon the occurrence of a contingent event that is outside the employee’s control does not meet certain conditions in SFAS 123(R) until it becomes probable that the event will occur. The guidance in this FASB Staff Position was required to be applied upon initial adoption of Statement No. 123(R). The Company does not have any option grants that allow for cash settlement.

The Company did not adopt any new share-based compensation plans in 2008. 200,000 stock options issued under the Company’s 2002 Stock Plan were exercised during the year 2008.

Advertising costs

All advertising costs incurred in the promotion of the Company’s products and services are expensed as incurred. Advertising expenses were insignificant for the nine months ended September 30, 2009 and 2008.

Income Taxes

The Company accounts for income taxes in accordance with SFAS No. 109 “Accounting for Income Taxes.” Under SFAS No. 109, deferred tax liabilities or assets at the end of each period are determined using the tax rate expected to be in effect when taxes are actually paid or recovered. Valuation allowances are established when it is more likely than not that some or all of the deferred tax assets not be realized.

In July, 2006, the FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes-an interpretation of FASB Statement No. 109” (“FIN 48”). This Interpretation provides guidance for recognizing and measuring uncertain tax positions, as defined in SFAS No. 109, “Accounting for Income Taxes.” FIN 48 prescribes a threshold condition that a tax position must meet for any of the benefit of the uncertain tax position to be recognized in the financial statements. Guidance is also provided regarding derecognition, classification and disclosure of these uncertain tax positions.

Earnings Per Common Share

The Company computes net earnings per share in accordance with SFAS No. 128, “Earnings per Share” and SEC Staff Accounting Bulletin No. 98 (“SAB 98”). Under the provisions of SFAS No. 128 and SAB 98, basic net earnings per share is computed by dividing the net earnings available to common shareholders for the period by the weighted average number of shares of common stock outstanding during the period. The calculation of diluted net earnings per share gives effect to common stock equivalents, however, potential common stock in the diluted EPS computation are excluded in net loss periods, as their effect is anti-dilutive.

Recent Accounting Pronouncements

On February 15, 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities: Including an amendment of FASB Statement No. 115” (“SFAS 159”). SFAS 159 permits all entities to elect to measure many financial instruments and certain other items at fair value with changes in fair value reported in earnings. SFAS 159 is effective as of the beginning of the first fiscal year that begins after November 15, 2007, with earlier adoption permitted.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements—an amendment of ARB No. 51”. The objective of this Statement is to improve the relevance, comparability, and transparency of the financial information that a reporting entity provides in its consolidated financial statements by establishing accounting and reporting standards. This Statement is effective for fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2008 (that is, January 1, 2009, for entities with calendar year-ends). Earlier adoption is prohibited. The effective date of this Statement is the same as that of the related Statement 141(R).

On December 21, 2007, SEC issued Staff Accounting Bulletin (“SAB”) No. 110. This staff accounting bulletin ("SAB") expresses the views of the staff regarding the use of a "simplified" method, as discussed in SAB No. 107 ("SAB 107"), in developing an estimate of expected term of "plain vanilla" share options in accordance with Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payment.” In particular, the staff indicated in SAB 107 that it will accept a company's election to use the simplified method, regardless of whether the company has sufficient information to make more refined estimates of expected term. At the time SAB 107 was issued, the staff believed that more detailed external information about employee exercise behavior (e.g., employee exercise patterns by industry and/or other categories of companies) would, over time, become readily available to companies. Therefore, the staff stated in SAB 107 that it would not expect a company to use the simplified method for share option grants after December 31, 2007. The staff understands that such detailed information about employee exercise behavior may not be widely available by December 31, 2007. Accordingly, the staff will continue to accept, under certain circumstances, the use of the simplified method beyond December 31, 2007.

In March 2008, the FASB issued FAS 161, “Disclosures about Derivative Instruments and Hedging Activities—an amendment of FASB Statement No. 133”. The use and complexity of derivative instruments and hedging activities have increased significantly over the past several years. Constituents have expressed concerns that the existing disclosure requirements in FASB Statement No. 133, Accounting for Derivative Instruments and Hedging Activities, do not provide adequate information about how derivative and hedging activities affect an entity’s financial position, financial performance, and cash flows. Accordingly, this Statement requires enhanced disclosures about an entity’s derivative and hedging activities and thereby improves the transparency of financial reporting. This Statement is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged. This Statement encourages, but does not require, comparative disclosures for earlier periods at initial adoption.

In May 2008, the FASB issued FAS 162, “The Hierarchy of Generally Accepted Accounting Principles”. This Statement identifies the sources of accounting principles and the framework for selecting the principles to be used in the preparation of financial statements of nongovernmental entities that are presented in conformity with generally accepted accounting principles (GAAP) in the United States (the GAAP hierarchy).

In May 2008, the FASB also issued FAS 163, “Accounting for Financial Guarantee Insurance Contracts—an interpretation of FASB Statement No. 60.” Diversity exists in practice in accounting for financial guarantee insurance contracts by insurance enterprises under FASB Statement No. 60, Accounting and Reporting by Insurance Enterprises. That diversity results in inconsistencies in the recognition and measurement of claim liabilities because of differing views about when a loss has been incurred under FASB Statement No. 5, Accounting for Contingencies. This Statement requires that an insurance enterprise recognize a claim liability prior to an event of default (insured event) when there is evidence that credit deterioration has occurred in an insured financial obligation. This Statement also clarifies how Statement 60 applies to financial guarantee insurance contracts, including the recognition and measurement to be used to account for premium revenue and claim liabilities. Those clarifications will increase comparability in financial reporting of financial guarantee insurance contracts by insurance enterprises. This Statement requires expanded disclosures about financial guarantee insurance contracts. The accounting and disclosure requirements of the Statement will improve the quality of information provided to users of financial statements. This Statement is effective for financial statements issued for fiscal years beginning after December 15, 2008, and all interim periods within those fiscal years, except for some disclosures about the insurance enterprise’s risk-management activities. This Statement requires that disclosures about the risk-management activities of the insurance enterprise be effective for the first period (including interim periods) beginning after issuance of this Statement. Except for those disclosures, earlier application is not permitted.

In April 2009, the FASB issued FAS 164, “Not-for-Profit Entities: Mergers and Acquisitions—Including an amendment of FASB Statement No. 142”. The objective of this Statement is to improve the relevance, representational faithfulness, and comparability of the information that a not-for-profit entity provides in its financial reports about a combination with one or more other not-for-profit entities, businesses, or nonprofit activities.

In May 2009, the FASB issued FAS 165, “Subsequent Events” The objective of this Statement is to establish general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued.

In June 2009, the FASB issued FAS 166, “Accounting for Transfers of Financial Assets—an amendment of FASB Statement No. 140”, FAS 167, “Amendments to FASB Interpretation No. 46(R)” and FAS 168, “The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles—a replacement of FASB Statement No. 162”.

The Company does not anticipate that the adoption of these statements will have a material effect on the Company's financial condition and results of operations.

NOTE 3 - OTHER RECEIVABLES, DEPOSITS AND PREPAYMENTS

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Other receivables | | $ | 794,794 | | | $ | 1,545,025 | |

| Deposits | | | 64,058 | | | | 58,875 | |

| Prepayments | | | 27,824 | | | | 23,655 | |

| | | | | | | | | |

| | | $ | 886,676 | | | $ | 1,627,555 | |

Other receivables include deposits for operating leases and advances to employee for traveling outlays.

NOTE 4 - INVENTORIES

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Computer hardware and software | | $ | 76,224 | | | $ | 13,335 | |

| Work-in-progress | | | 1,130,431 | | | | 1,006,378 | |

| | | | | | | | | |

| | | $ | 1,206,655 | | | $ | 1,019,713 | |

All the inventories were purchased for identified system integration contracts.

Work-in-progress includes payroll and other operating expenses associated with various contracts in progress.

NOTE 5 – RELATED PARTY TRANSACTIONS

The Company, from time to time, borrowed money from and made repayment to one major stockholder who is also a management member of the Company. The amounts due to this stockholder do not bear any interest and do not have clearly defined terms of repayment.

As of September 30, 2009 and December 31, 2008, the amounts due to this stockholder were $401,926 and $378,672, respectively, representing advances from this stockholder for our working capital.

NOTE 6 - PROPERTY, PLANT AND EQUIPMENT, NET

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Building | | $ | 213,705 | | | $ | 213,705 | |

| Computer and office equipment | | | 1,055,775 | | | | 1,060,165 | |

| Motor vehicles | | | 211,698 | | | | 211,698 | |

| | | | 1,481,178 | | | | 1,485,568 | |

| Less: Accumulated depreciation | | | (1,046,205 | ) | | | (891,763 | ) |

| | | | | | | | | |

| | | $ | 434,973 | | | | 593,805 | |

The building is located in Chengdu, PRC and was purchased on behalf of the Company by Mr. Yi He, one of the stockholders and directors of the Company. By a stockholders’ resolution passed on March 8, 1999, it was ratified that the title to the building belonged to the Company. In 2005, the title to the building was transferred to FTCD.

NOTE 7 - LONG TERM INVESTMENTS

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Equity investments | | $ | 170,801 | | | $ | 236,344 | |

| Cost investments | | | 4,835,097 | | | | 4,838,278 | |

| | | | | | | | | |

| | | $ | 5,005,898 | | | | 5,074,622 | |

The Company has recorded its investment for 17.8% equity interest of All China Logistics at cost because it does not have the ability to exercise significant influence over the investee.

The Company’s investment for 17.5% of CLCE was made in the form of the Company-developed “For-Online Electronic Trading System” without any cash outflow. Therefore, the Company has recorded the contribution of software at the lower of its carrying amount or fair value, and accounted for under the equity method under SOP 78-9. For the quarter ended September 30, 2009, our share of profit was RMB 284,740, which has been recorded in the accompanying financial statements.

The Company’s acquisition of 22.73% of registered capital in Guangxi Caexpo included a cash payment of $2,557,545 (RMB 20,000,000) by BFHX and 13,000,000 shares of the Company’s restricted common stock. The acquisition cost of the common shares issued is based on a per share price of $0.075, which is the average market price of the Company’s common shares over a 10-day period before and after the terms of the acquisition were agreed to. The overall acquisition cost of this acquisition was $3,529,450. The Company recorded the investment at cost because it does not have the ability to exercise significant influence over Guangxi Caexpo; in fact, Guangxi Caexpo’s strategic and business decisions are dominated by other major shareholders.

In exchange for 12.5% registered capital of Wuxi Exchange, the Company contributed cash of $31,969 (RMB 250,000), and deployed a proprietary, integrated software solution estimated at RMB 1,000,000 to support Wuxi Exchange’s operations. The Company recorded the investment at cost because it does not have the ability to exercise significant influence over Wuxi. On January 14, 2007, the Company entered into a Share Transfer Agreement with a major shareholder of Wuxi to transfer 2.5% interest in Wuxi held by the Company to the shareholder for a cash payment of RMB 500,000. After this transfer, the Company continues to hold 10% equity interest in Wuxi.

The Company’s investment for 35% equity interest of BGXF is accounted for under the equity method of the accounting due to the Company’s significant influence over the operational and financial policies of BGXF. On March 9, 2008, BGXF commenced operations. On October 14, 2008, BGXF increased its registered capital to RMB 4,285,700, and since we did not invest additional funds into BGXF, the ratio of our holding was diluted to a 24.5% equity interest.

The Company’s investment for 25% equity interest of NBBCE is recorded at cost because the Company does not have the ability to exercise significant influence over NBBCE. In fact, NBBCE’s strategic and business decisions are dominated by another major shareholder.

The Company’s investment for 5% of SDLD is recorded at cost because the Company does not have the ability to exercise significant influence over SDLD.

NOTE 8 - OTHER PAYABLES AND ACCRUED EXPENSES

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Other payables | | $ | 554,455 | | | $ | 428,334 | |

| Accrued salaries & wages | | | 159,996 | | | | 176,985 | |

| | | | | | | | | |

| | | $ | 714,451 | | | $ | 605,319 | |

Other payables include wages payable to employees, rental payable, and utilities payable.

NOTE 9 - MINORITY INTEREST

The minority interest balance of $146,286 represents equity value held by minority shareholders of NNBCE.

NOTE 10 - INCOME TAX

According to the relevant PRC tax rules and regulations, FTCL, recognized as New Technology Enterprises operating within a New and High Technology Development Zone, is entitled to an Enterprise Income Tax (“EIT”) rate of 15%.

Pursuant to approval documents dated September 23, 1999 and August 2, 2000, respectively, issued by the Beijing Tax Bureau and State Tax Bureau, FTCL was fully exempted from EIT for fiscal years 1999, 2000, 2001 and 2002. FTCL received a 50% EIT reduction at the rate of 7.5% for fiscal years 2003, 2004 and 2005. As of September 30, 2009, FTCL was entitled to an EIT rate of 15%.

Pursuant to an approval document dated January 19, 2004 issued by the State Tax Bureau, BFHX was fully exempted from EIT for fiscal years 2004, 2005 and 2006. As of September 30, 2009, BFHX was entitled to an EIT rate of 25%.

Hong Kong profits tax is calculated at 17.5% on the estimated assessable profits of FTHK for the period. The EIT rates for FTCD, BFKT and NNBCE range from 9% to 33%. No provision for EIT and Hong Kong profits tax were made for FTCL, BFHX, FTCD, FTGX, NNBCE and FTHK as they have not gained taxable income for the periods.

On January 1, 2007, the Company adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes-an interpretation of FASB Statement No. 109” (“FIN 48”). This Interpretation provides guidance for recognizing and measuring uncertain tax positions, as defined in SFAS No. 109, “Accounting for Income Taxes.” FIN 48 prescribes a threshold condition that a tax position must meet for any of the benefits of the uncertain tax position to be recognized in the financial statements. Guidance is also provided regarding derecognition, classification and disclosure of these uncertain tax positions. The Company classified all interest and penalties related to tax uncertainties as income tax expense. The Company’s liability for income taxes includes the liability for unrecognized tax benefits, interest and penalties which relate to tax years still subject to review by taxing authorities. Audit periods remain open for review until the statute of limitations has passed. The completion of review or the expiration of the statute of limitations for a given audit period could result in an adjustment to our liability for income taxes. Any such adjustment could be material to the Company’s results of operations for any given quarterly or annual period based, in part, upon the results of operations for the given period. As of September 30, 2009, the Company does not have any liability for uncertain tax positions. The adoption of FIN 48 did not have a material impact on the Company’s results operations, financial position or liquidity.

On March 16, 2007, the 5th Plenary Session of the 10th National People's Congress passed the Corporate Income Tax Law of the PRC (the "Corporate Income Tax Law"), which took effect on January 1, 2008. Beginning on that date, the EIT rate is to gradually increase to the standard rate of 25% over a five-year transition period. However, the Corporate Income Tax Law does not specify how the existing preferential tax rate will gradually increase to the standard rate of 25%. Also, under the Corporate Income Tax Law, certain high technology enterprises would continue to be entitled to a reduced tax rate of 15%. The Company was designated as a high technology enterprise under the Corporate Income Tax Law on December 28, 2008. The enactment of the Corporate Income Tax Law is not expected to have any financial effect on the amounts accrued in the balance sheet in respect of current tax payable.

NOTE 11 - OTHER TAXES RECOVERABLE/(PAYABLE)

Other taxes payable comprise mainly of Valued-Added Tax (“VAT”) and Business Tax (“BT”). The Company is subject to output VAT levied at the rate of 17% of its operating revenue. The input VAT paid on purchases of materials and other direct inputs can be used to offset the output VAT levied on operating revenue to determine the net VAT payable or recoverable. BT is charged at a rate of 5% on the revenue from other services.

As part of the PRC government’s policy of encouraging software development in the PRC, companies that fulfill certain criteria set by the relevant authorities, and which develop their own software products and have the software products registered with the relevant authorities in the PRC, are entitled to a refund of VAT equivalent to the excess over 3% of revenue paid in the month when output VAT exceeds input VAT (excluding export sales). The excess portion of the VAT is refundable and is recorded by the Company on an accrual basis. The VAT rebate included in other income was $13,025 and $23,992 for the three months ended September 30, 2009 and 2008, respectively.

NOTE 12 – COMPREHENSIVE INCOME/(LOSS)

The components of comprehensive income/(loss) were as follows:

| | | Three Months Ended September 30, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Net profit/(loss) | | $ | (399,222 | ) | | $ | 320,037 | |

| Foreign currency translation adjustment | | | 32,995 | | | | 37,457 | |

| Comprehensive income/(loss) | | $ | (366,227 | ) | | $ | 357,494 | |

NOTE 13 - STOCK PLAN

On August 16, 2002, the Company established a plan of stock-based compensation incentives for selected eligible participants of the Company and its affiliated corporations known as the “Forlink Software Corporation, Inc. 2002 Stock Plan” (the “2002 Plan”). The total number of shares of common stock reserved for issuance by Forlink either directly as stock awards or underlying options granted under the 2002 Plan shall not be more than 8,000,000. Under the terms of the 2002 Plan, options can be issued to purchase shares of Forlink’s common stock. The Board of Directors shall determine the terms and conditions of each option granted to eligible participants, which terms shall be set forth in writing. The terms and conditions so set by the Board of Directors may vary from one eligible participant to another.

The following table summarizes the activity on stock options under the 2002 Plan:

| | | Number of shares | | | Weighted average exercise price | |

| | | | | | | |

| Granted on September 7, 2004 | | | 3,315,000 | | | $ | 0.10 | |

| Exercised | | | (15,000 | ) | | $ | (0.10 | ) |

| Forfeited or Cancelled | | | 0 | | | $ | 0.00 | |

| Outstanding at December 31, 2004 | | | 3,300,000 | | | $ | 0.10 | |

| Exercised | | | (136,500 | ) | | $ | (0.10 | ) |

| Forfeited or Cancelled | | | (132,500 | ) | | $ | (0.10 | ) |

| Outstanding at December 31, 2005 | | | 3,031,000 | | | $ | 0.10 | |

| Exercised | | | 0 | | | $ | 0.00 | |

| Forfeited or Cancelled | | | (1,734,000 | ) | | $ | (0.10 | ) |

| Outstanding at December 31, 2006 | | | 1,297,000 | | | $ | 0.10 | |

| Exercised | | | (897,000 | ) | | $ | (0.10 | ) |

| Forfeited or Cancelled | | | 0 | | | $ | 0.00 | |

| Outstanding at December 31, 2007 | | | 400,000 | | | $ | 0.10 | |

| Exercised | | | (200,000 | ) | | $ | 0.00 | |

| Forfeited or Cancelled | | | (200,000 | ) | | $ | 0.00 | |

| Outstanding at December 31, 2008 | | | 0 | | | $ | 0.00 | |

| Exercised | | | 0 | | | $ | 0.00 | |

| Forfeited or Cancelled | | | 0 | | | $ | 0.00 | |

| Outstanding at September 30, 2009 | | | 0 | | | $ | 0.00 | |

| Fully vested and exercisable at September 30, 2009 | | | 0 | | | $ | 0.10 | |

On September 7, 2004, 3,315,000 options were granted to the Company’s employees to purchase the Company’s shares of common stock, $0.001 par value, at an exercise price of $0.10 per share. Of the 3,315,000 options, 800,000 options with a 5-year vesting period were granted to an employee, and 2,515,000 options with a 3-year vesting period were granted to selected employees. Of the 2,515,000 options with the 3-year vesting period, 2,385,000 options were to expire on December 30, 2006 (the “December 2006 Options”), while the remaining 130,000 options expired on June 30, 2007 (the “June 2007 Options”). The expiration date for 800,000 options with the 5-year vesting period is June 30, 2009 (the “June 2009 Options”). On September 7, 2004, January 1, 2005, January 1, 2006 and January 1, 2007, 854,500 (the “December 2006 Options”), 904,500, 1,156,000 (400,000 of “June 2009 Options”; 130,000 of “June 2007 Options”; and 626,000 of “December 2006 Options”) and 200,000 (the “June 2009 Options”) options were vested to employees respectively. The market price of the stock as of September 7, 2004 and January 1, 2005 was $0.10 per share. In December 2006, the Company extended the expiration date of the December 2006 Options by one month to the end of January 2007, but there was no additional compensation expense as the Company considered the amount was immaterial. On January 29, 2007, 367,000 options of the “December 2006 Options” and 400,000 of the “June 2009 options” were exercised. On July 6, 2007, 130,000 options of the “June 2007 Options” were exercised. On July 15, 2008, 200,000 options of “June 2009 Options” were exercised.

The following table summarizes the cumulative activities up to September 30, 2009 of the options issued under the 2002 Plan with different expiration dates:

| | | Granted | | | Exercised | | | Forfeited or Cancelled | | | Outstanding at September 30, 2009 | |

| December 2006 Options | | | 2,385,000 | | | | 518,500 | | | | 1,866,500 | | | | 0 | |

| June 2007 Options | | | 130,000 | | | | 130,000 | | | | 0 | | | | 0 | |

| June 2009 Options | | | 800,000 | | | | 600,000 | | | | 200,000 | | | | 0 | |

| | | | 3,315,000 | | | | 1,248,500 | | | | 2,066,500 | | | | 0 | |

The weighted average fair value of the December 2006 Options, the June 2007 Options and the June 2009 Options granted on the date of grant, were $0.042, $0.046 and $0.058 per option, respectively. At December 31, 2007, all future compensation expenses were recognized.

There was no aggregate intrinsic value of options outstanding and exercisable as of December 31 2007 and December 31, 2006. The aggregate intrinsic value represents the intrinsic value, based on options with an exercise price less than the market value of the Company’s stock on December 31, 2007 and December 31, 2006, which would have been received by the option holders had those option holders exercised those options at of that date.

The Company calculated the fair value of each option award on the date of grant using the Black-Scholes option pricing model. The following assumptions were used for each respective option.

| | | The Value of Options | |

| | | December 2006 Options | | | June 2007 Options | | | June 2009 Options | |

| | | | | | | | | | |

| Risk-free interest rate | | | 2.17 | % | | | 2.28 | % | | | 2.66 | % |

| Expected lives (in years) | | | 1.167 | | | | 1.417 | | | | 2.417 | |

| Dividend yield | | | 0 | % | | | 0 | % | | | 0 | % |

| Expected volatility | | | 100 | % | | | 100 | % | | | 100 | % |

NOTE 14 - CONCENTRATION OF CUSTOMERS

During the year, the following customers accounted for more than 10% of total sales:

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

| | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| Net sales derived from: | | | | | | | | | | | | |

| Customer A | | | 84,435 | | | | 1,000,242 | | | | 530,930 | | | | 2,319,379 | |

| Customer B | | | * | | | | * | | | | 264,737 | | | | * | |

| Customer C | | | * | | | | * | | | | * | | | | * | |

| Customer D | | | 71,037 | | | | * | | | | 146,799 | | | | * | |

| Customer E | | | 229,019 | | | | 271,594 | | | | 302,072 | | | | 1,595,085 | |

| | | | | | | | | | | | | | | | | |

| % to total net sales from: | | | | | | | | | | | | | | | | |

| Customer A | | | 10 | % | | | 60 | % | | | 20 | % | | | 50 | % |

| Customer B | | | * | | | | * | | | | 10 | % | | | * | |

| Customer C | | | * | | | | * | | | | * | | | | * | |

| Customer D | | | 9 | % | | | * | | | | 6 | % | | | * | |

| Customer E | | | 28 | % | | | 16 | % | | | 11 | % | | | 34 | % |

| | | | | | | | | | | | | | | | | |

| Account receivable from: | | | | | | | | | | | | | | | | |

| Customer A | | | | | | | | | | | 80,242 | | | | 1,129,182 | |

| Customer B | | | | | | | | | | | 743,682 | | | | 387,009 | |

| Customer C | | | | | | | | | | | 668,351 | | | | 490,241 | |

| Customer D | | | | | | | | | | | * | | | | * | |

| Customer E | | | | | | | | | | | * | | | | 108,681 | |

| | | | | | | | | | | | | | | | | |

| % to total accounts receivable from: | | | | | | | | | | | | | | | | |

| Customer A | | | | | | | | | | | 5 | % | | | 47 | % |

| Customer B | | | | | | | | | | | 42 | % | | | 16 | % |

| Customer C | | | | | | | | | | | 38 | % | | | 20 | % |

| Customer D | | | | | | | | | | | 3 | % | | | * | |

| Customer E | | | | | | | | | | | * | | | | 5 | % |

* less than 10%

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

Statements contained herein that are not historical facts are forward-looking statements as that term is defined by the Private Securities Litigation Reform Act of 1995. Although we believe that the expectations reflected in such forward looking statements are reasonable, the forward looking statements are subject to risks and uncertainties that could cause actual results to differ from those projected. We caution investors that any forward looking statements made by us are not guarantees of future performance and that actual results may differ materially from those in the forward-looking statements. Such risks and uncertainties include, without limitation: well-established competitors who have substantially greater financial resources and longer operating histories, regulatory delays or denials, ability to compete as a company in a highly competitive market, and access to sources of capital.

The following discussion and analysis should be read in conjunction with our financial statements and notes thereto included elsewhere in this Form 10-Q. Except for the historical information contained herein, the discussion in this Form 10-Q contains certain forward-looking statements that involve risks and uncertainties, such as statements of our plans, objectives, expectations and intentions. The cautionary statements made in this Form 10-Q should be read as being applicable to all related forward looking statements wherever they appear in this Form 10-Q. The Company's actual results could differ materially from those discussed here. We undertake no obligation to update publicly any forward-looking statements for any reason even if new information becomes available or other events occur in the future.

Overview

We are a leading provider of software solutions and information technology services in China (the “PRC” or “China”). We focus on providing Enterprise Application Integration (EAI) solutions for large companies in the telecom, finance, and logistics industries. In May 2004, we launched For-online, which delivers enterprise applications and services over the Internet to small and medium-sized enterprises (SMEs) in China. Since its launch, For-Online has become an important channel for delivering and distributing our products and services to more customers. In August 2007, we launched our integrated e-business application platform For-Online 4.0, and based on this platform, we also released new versions of For-eMarket 3.0 in September 2007, ForCRM in October 2007 and ForOA in October 2007. We released For-eMarketPlace 3.1 in August 2008. We released Forlink-RMIS 1.0 in April 2009.

Revenues

Our business includes Forlink’s “For-series” brand software system sales such as ForOSS, ForRMS, For-Mail and their copyright licensing, and “For-series” related system integration, which consists of hardware sales and other related services rendered to customers. The following table shows our revenue breakdown by business line:

| | | Three Months Ended September 30, | |

| | | 2009 | | | 2008 | |

| | | | | | | |

| Sales of For-series software | | $ | 626,786 | | | $ | 1,616,382 | |

| as a percentage of net sales | | | 76 | % | | | 97 | % |

| | | | | | | | | |

| For-series related system integration | | $ | 195,872 | | | $ | 50,937 | |

| as a percentage of net sales | | | 24 | % | | | 3 | % |

As indicated in the foregoing table, sales of For-series software decreased by 61% to $626,786 in the third quarter of 2009 from $1,616,382 in the comparable quarter of 2008. For-series related system integration as a percentage of net sales increased from 3% in the comparable quarter of 2008 to 24% in the third quarter of 2009. The gross margins for the three months ended September 30, 2009 and 2008 were 43% and 67%, respectively.

Generally, we offer our products and services to our customers on a total-solutions basis. Most of the contracts we undertake for our customers include revenue from hardware and software sales and professional services.

Sources of Revenue

Hardware Revenue: Revenues from sales of products are mainly derived from sales of hardware. Normally, the hardware that we procure is in connection with total-solutions basis system integration contracts.

Service Revenue: Service revenue consists of revenue for the professional services we provide to our customers for network planning, design and systems integration, software development, modification and installation, and related training services.

Software License Revenue: We generate revenue in the form of fees received from customers to whom we issue licenses for the use of our software products over an agreed period of time.

Cost of Revenue

Our cost of revenue includes hardware costs, software-related costs and compensation and travel expenses for the professionals involved in the relevant projects. Hardware costs consist primarily of third party hardware costs. We recognize hardware costs in full upon delivery of the hardware to our customers. Software-related costs consist primarily of packaging and written manual expenses for our proprietary software products and software license fees paid to third-party software providers for the right to sublicense their products to our customers as part of our solutions offerings. The costs associated with designing and modifying our proprietary software are classified as research and development expenses as such costs are incurred.

Operating Expenses

Operating expenses are comprised of selling expenses, research and development expenses and general and administrative expenses.

Selling expenses include compensation expenses for employees in our sales and marketing departments, third party advertising expenses, as well as sales commissions and sales agency fees.

Research and development expenses relate to the development of new software and the modification of existing software. We expense such costs as they are incurred.

General and administrative expenses include salaries and wages in the management section, office expenses and traveling expenses.

Taxes

According to the relevant PRC tax rules and regulations, FTCL, recognized as New Technology Enterprises operating within a New and High Technology Development Zone, is entitled to an Enterprise Income Tax (“EIT”) rate of 15%.

Pursuant to approval documents dated September 23, 1999 and August 2, 2000 issued by the Beijing Tax Bureau and the State Tax Bureau respectively, FTCL received full exemption from EIT for fiscal years 1999 through 2002, and a 50% EIT reduction at the rate of 7.5% for fiscal years 2003 through 2005. As of September 30, 2009, FTCL was entitled to an EIT rate of 15%.