1

Morgan Stanley

Energy Conference

Energy Conference

July 8, 2009

2

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of

1933 and Section 21E of the Securities Exchange Act of 1934. All such statements, other than statements of

historical fact, are statements that could be deemed “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995, including, without limitation, any projections of revenue, gross margin,

expenses, earnings or losses from operations, or other financial items; future production volumes, results of

exploration, exploitation, development, acquisition and operations expenditures, and prospective reserve levels of

property or wells; any statements of the plans, strategies and objectives of management for future operations; any

statements concerning developments, performance or industry rankings; and any statements of assumptions

underlying any of the foregoing. Although we believe that the expectations set forth in these forward-looking

statements are reasonable, they do involve risks, uncertainties and assumptions that could cause our results to differ

materially from those expressed or implied by such forward-looking statements. The risks, uncertainties and

assumptions referred to above include the performance of contracts by suppliers, customers and partners; employee

management issues; complexities of global political and economic developments; geologic risks and other risks

described from time to time in our reports filed with the Securities and Exchange Commission (“SEC”), including the

Company’s Annual Report on Form 10-K for the year ended December 31, 2008 and subsequent quarterly reports

on Form 10-Q. You should not place undue reliance on these forward-looking statements which speak only as of the

date of this presentation and the associated press release. We assume no obligation or duty and do not intend to

update these forward-looking statements except as required by the securities laws.

1933 and Section 21E of the Securities Exchange Act of 1934. All such statements, other than statements of

historical fact, are statements that could be deemed “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995, including, without limitation, any projections of revenue, gross margin,

expenses, earnings or losses from operations, or other financial items; future production volumes, results of

exploration, exploitation, development, acquisition and operations expenditures, and prospective reserve levels of

property or wells; any statements of the plans, strategies and objectives of management for future operations; any

statements concerning developments, performance or industry rankings; and any statements of assumptions

underlying any of the foregoing. Although we believe that the expectations set forth in these forward-looking

statements are reasonable, they do involve risks, uncertainties and assumptions that could cause our results to differ

materially from those expressed or implied by such forward-looking statements. The risks, uncertainties and

assumptions referred to above include the performance of contracts by suppliers, customers and partners; employee

management issues; complexities of global political and economic developments; geologic risks and other risks

described from time to time in our reports filed with the Securities and Exchange Commission (“SEC”), including the

Company’s Annual Report on Form 10-K for the year ended December 31, 2008 and subsequent quarterly reports

on Form 10-Q. You should not place undue reliance on these forward-looking statements which speak only as of the

date of this presentation and the associated press release. We assume no obligation or duty and do not intend to

update these forward-looking statements except as required by the securities laws.

The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC,

to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation

tests to be economically and legally producible under existing economic and operating conditions. Statements of

proved reserves are only estimates and may be imprecise. Any reserve estimates provided in this presentation that

are not specifically designated as being estimates of proved reserves may include not only proved reserves but also

other categories of reserves that the SEC’s guidelines strictly prohibit the Company from including in filings with the

SEC. Investors are urged to consider closely the disclosure in the Company’s 2008 Form 10-K.

to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation

tests to be economically and legally producible under existing economic and operating conditions. Statements of

proved reserves are only estimates and may be imprecise. Any reserve estimates provided in this presentation that

are not specifically designated as being estimates of proved reserves may include not only proved reserves but also

other categories of reserves that the SEC’s guidelines strictly prohibit the Company from including in filings with the

SEC. Investors are urged to consider closely the disclosure in the Company’s 2008 Form 10-K.

Forward-Looking Statements

3

Helix Profile

4

The Helix Mission

Helix Energy Solutions Group provides life-of-field services and development

solutions to offshore energy producers worldwide. Helix actively reduces

finding and development costs through a unique mix of offshore production

assets, service methodologies, and highly skilled personnel.

solutions to offshore energy producers worldwide. Helix actively reduces

finding and development costs through a unique mix of offshore production

assets, service methodologies, and highly skilled personnel.

5

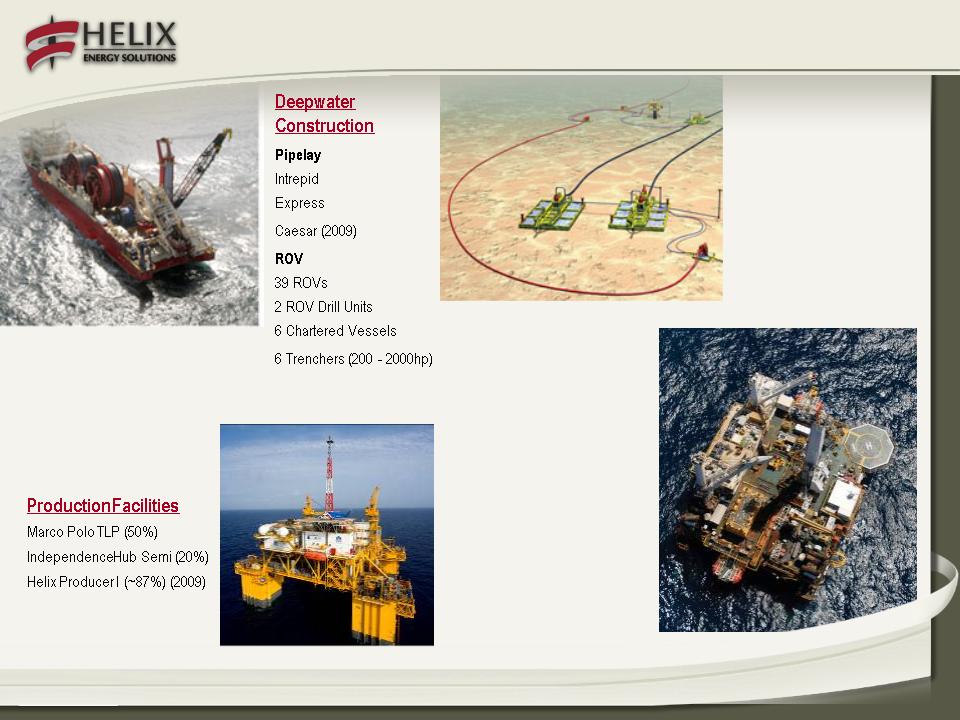

Deepwater

Well Intervention

Well Intervention

Q4000

Seawell

Well Enhancer (2009)

Mobile SILs

Helix Oil & Gas / ERT

GOM shelf and deepwater

PV-10 $1.9 billion @

12/31/2008

12/31/2008

Proved reserves = 665 bcfe

(12/31/2008)

(12/31/2008)

2009 projected production

45 - 55 bcfe

45 - 55 bcfe

Helix Business Segments

6

The Helix Fleet

7

MSV DP2 Well Enhancer

Well Intervention Fleet

MSV DP2 Seawell

Helix provides well operation and decommissioning services with the

Q4000 and Seawell well intervention vessels, with the Well Enhancer joining

the fleet in 2009.

Q4000 and Seawell well intervention vessels, with the Well Enhancer joining

the fleet in 2009.

8

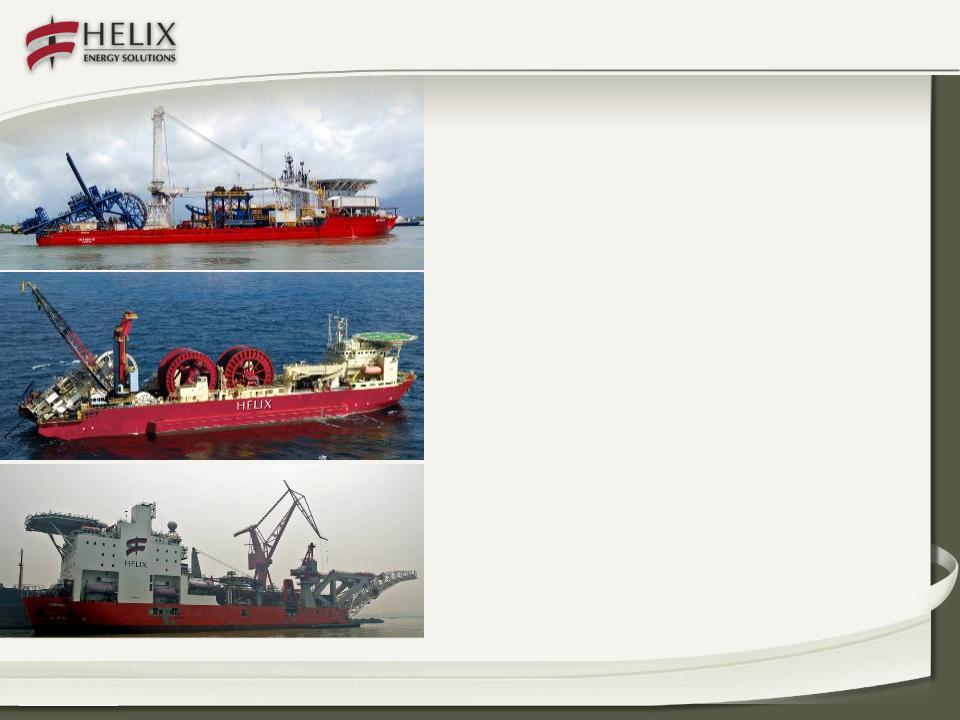

DP Reel Lay Vessel

Express

Express

DP S-Lay Vessel

Caesar (Q4 2009)

Caesar (Q4 2009)

Subsea Construction Vessels

DP Reel Lay Vessel

Intrepid

Intrepid

Caesar’s onboard pipe welding and testing

capability allows the vessel to lay pipeline with out

the need for a spoolbase.

capability allows the vessel to lay pipeline with out

the need for a spoolbase.

Helix’s pipelay and subsea construction vessel has

established an extensive track record of field

installation projects around the world.

established an extensive track record of field

installation projects around the world.

Intrepid has the flexibility to be deployed as a

pipelay, installation or saturation diving vessel.

pipelay, installation or saturation diving vessel.

9

Helix ROV Systems

Helix is an industry leading provider of ROV and subsea trenching

services to deepwater operators worldwide.

services to deepwater operators worldwide.

The Helix ROV fleet

consists of 39 vehicles,

covering the spectrum of

deepwater construction

services.

consists of 39 vehicles,

covering the spectrum of

deepwater construction

services.

The 600 hp Supertrencher II

system is designed to

operate at water depths in

excess of 6,500 feet.

system is designed to

operate at water depths in

excess of 6,500 feet.

The I-Trencher system can be

used in various jetting and

cutting operating modes, in

shallow and deepwater.

used in various jetting and

cutting operating modes, in

shallow and deepwater.

10

Island Pioneer

Olympic Triton

Olympic Canyon

Seacor Canyon

Northern Canyon

ROV / Construction Support Vessel Fleet

Chartered support vessels allows Helix to adjust the size and

capability of its fleet to cost-effectively meet industry demands.

capability of its fleet to cost-effectively meet industry demands.

REM Forza

11

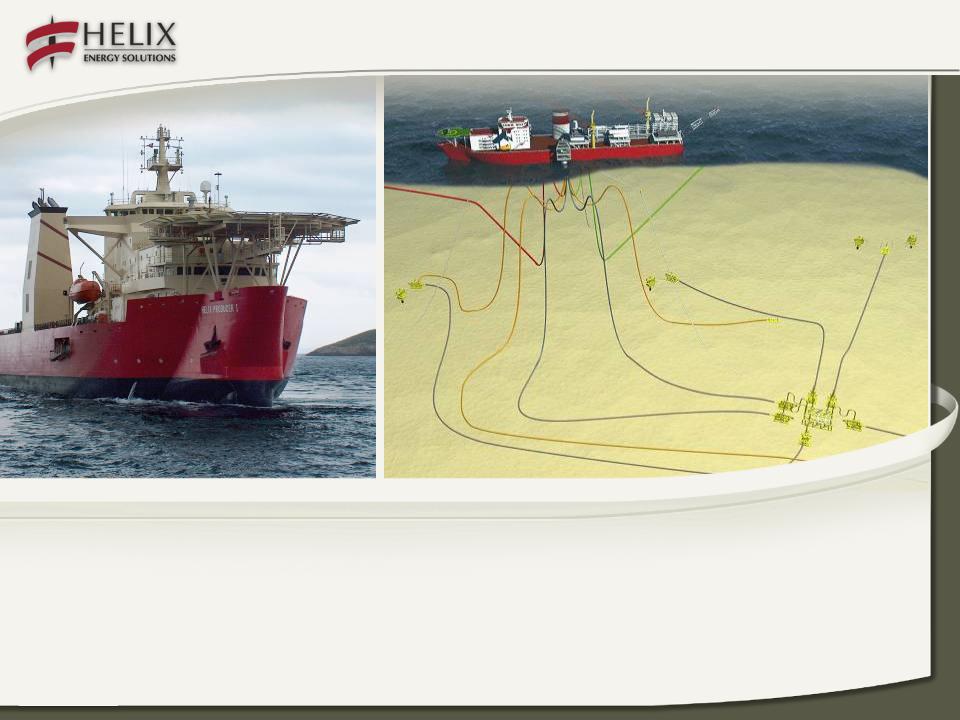

Helix Producer I

Helix Producer I is a floating production facility designed to serve small

deepwater fields over the life of the property, such as Helix’s Phoenix

field in the Gulf of Mexico. The dynamically-positioned vessel can

produce up to a maximum of 45,000 BOPD and 72 MMCFD via a

disconnectable transfer buoy system.

deepwater fields over the life of the property, such as Helix’s Phoenix

field in the Gulf of Mexico. The dynamically-positioned vessel can

produce up to a maximum of 45,000 BOPD and 72 MMCFD via a

disconnectable transfer buoy system.

12

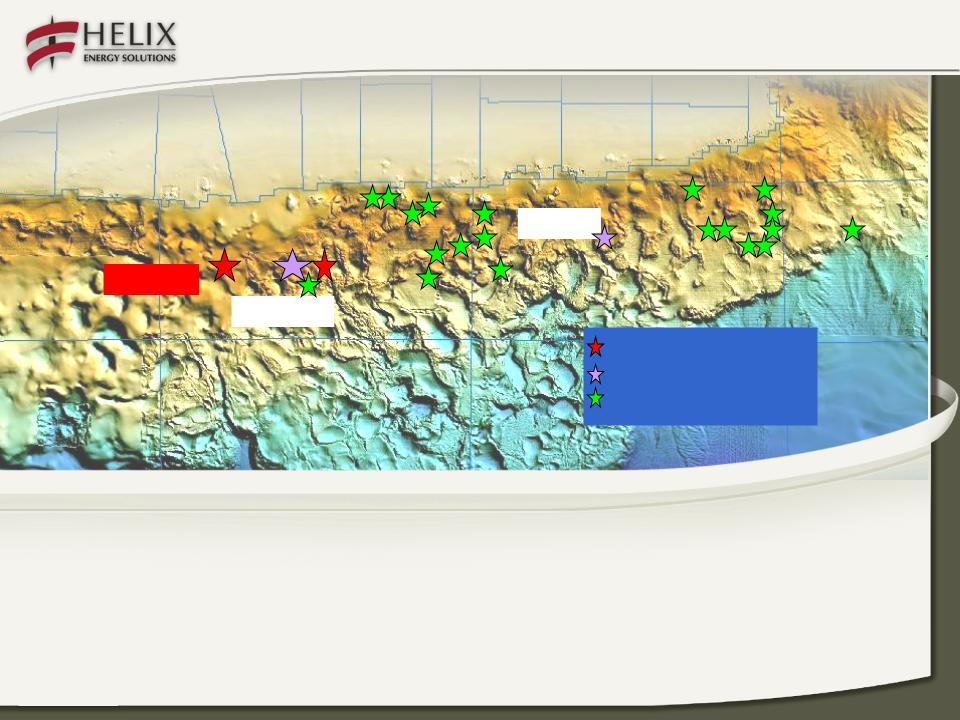

Helix Oil & Gas

13

Producing Field

Non Producing Field

Prospect

Gunnison

Bushwood

Phoenix

ERT Deepwater Portfolio

Interests in 44 Deepwater Blocks -12 Developed, 32 Undeveloped

2.7 Net TCFE Un-Risked Reserve Potential, 1.0 TCFE Risked

Internal Prospect Generation via Large, In-House 3-D Seismic Library Large,

Recent Long Offset 3-D Seismic Database,+1,500 Blocks

Recent Long Offset 3-D Seismic Database,+1,500 Blocks

Experienced Exploration/Drilling/Operations Team - 25+ years avg.

14

O&G - - 2008 Reserve Report Highlights

15

O&G - - 2009 Deepwater Capital Projects

Phoenix Field

16

17

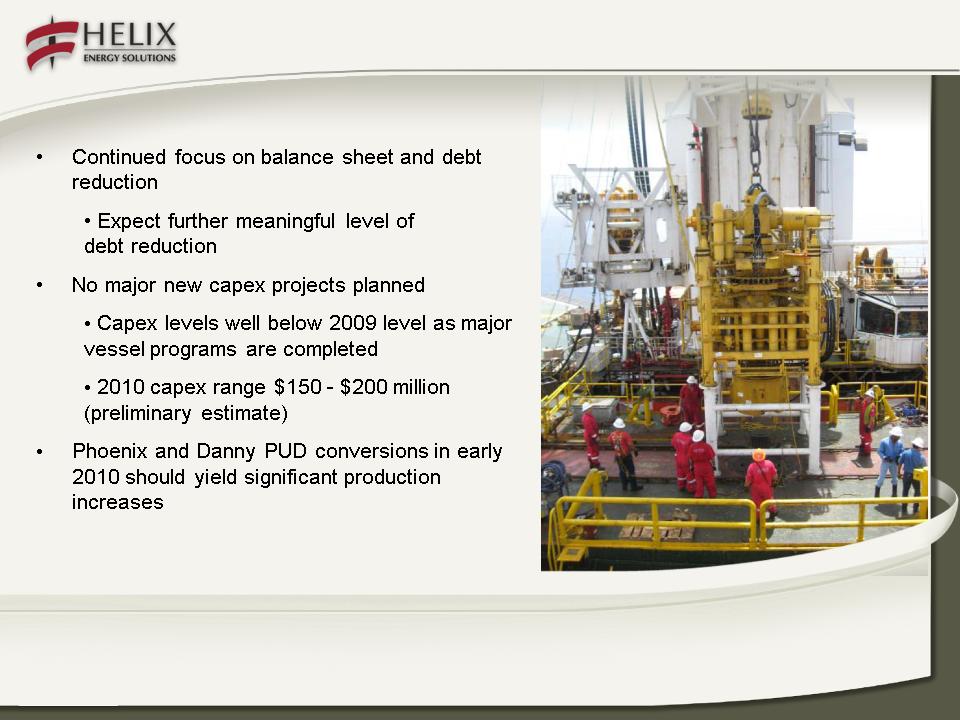

• Good Contracting Services visibility in 1H 2009

• 2009 backlog of $360 million

• Expect 2H 2009 to soften

• Capital expenditures of approximately $360 million

• $200 million relates to completion of three major

vessel projects (Well Enhancer, Caesar and Helix

Producer I)

vessel projects (Well Enhancer, Caesar and Helix

Producer I)

• $60 million relates to development of Danny

and Phoenix oil fields

and Phoenix oil fields

• Most of remaining CAPEX is maintenance

• Significant improvement in liquidity and debt levels

(see slide 20)

(see slide 20)

2009 Outlook

18

2009 Outlook (continued)

19

2010 Preview

20

Liquidity and

Capital

Resources

Capital

Resources

21

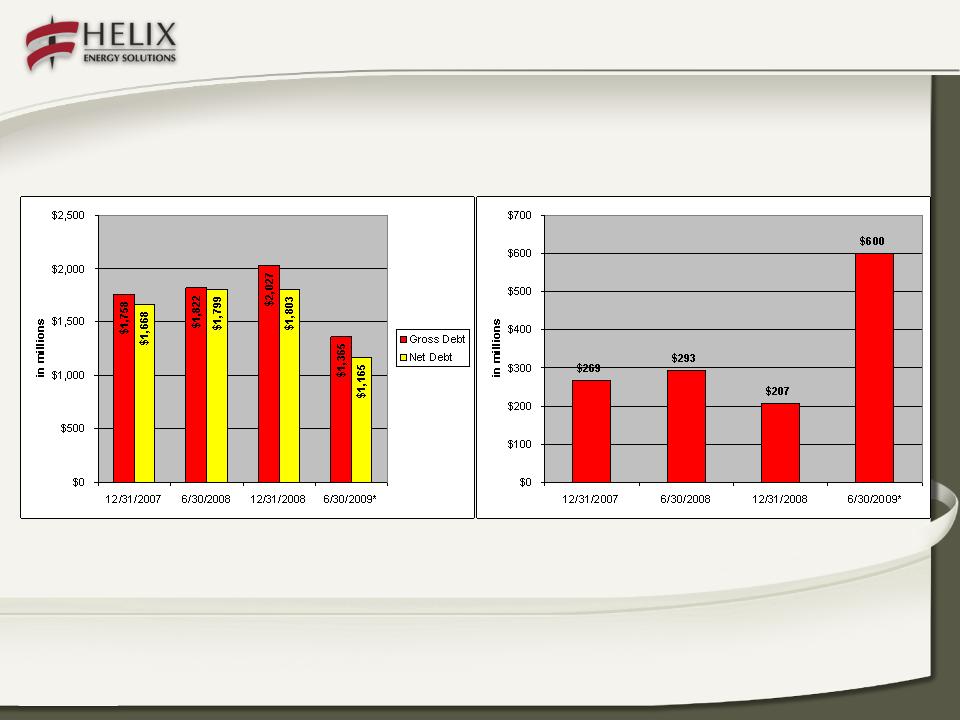

Significant Balance Sheet Improvements

* estimated

Debt

Liquidity

22

• Company is focused on efforts to monetize non-core assets and businesses

• Oil and gas assets

• Bass Lite sale December 08 & January 09 ($49 million)

• EC 316 sale in February 09 ($18 million)

• Production facilities

• Cal Dive (approximate 26% owned subsidiary)

• Sold 15.2 million shares of CDI common stock to Cal Dive for proceeds

of $100 million in January and June 2009

of $100 million in January and June 2009

• Sold 22.6 million CDI shares in secondary offering for proceeds of

≈ $182 million in June 2009

≈ $182 million in June 2009

• Sold Helix RDS in April 2009 for $25 million

• Approximately 80% of total 2009 oil and gas production hedged

Liquidity and Capital Resources

Monetization of some or all remaining non-core assets would further

accelerate debt reduction and increase liquidity

accelerate debt reduction and increase liquidity

23

Company is in compliance as of 3/31/2009, and forecasts

continuing compliance throughout 2009

continuing compliance throughout 2009

Liquidity and Capital Resources

Covenant | Test | Explanation |

Collateral Coverage Ratio | > 1.75 : 1 | Basket of collateral to Senior Secured Debt |

Fixed Charge Coverage Ratio | > 2.75 : 1 | Consolidated EBITDA (incl. Cal Dive %) to consolidated interest charges |

Consolidated Leverage Ratio | < 3.5 : 1 | Consolidated EBITDA (incl. Cal Dive %) to consolidated debt |

Key Credit Facility Covenants

24

Liquidity and Capital Resources

Credit Facilities, Commitments and Amortization

– $420 Million Revolving Credit Facility - committed facility through June 2011. No

required amortization. Fully paid down as of 6/30/2009.

required amortization. Fully paid down as of 6/30/2009.

– $418 Million Term Loan B - committed facility through June 2013. $4.3 million

amortization annually.

amortization annually.

– $550 Million High Yield Notes - Interest only until maturity (2016) or called by Helix.

First Helix call date is 2012.

First Helix call date is 2012.

– $300 Million Convertible Notes - Interest only until put by noteholders or called by

Helix. First put/call date is 2012, although noteholders have the right to convert prior

to that date if certain stock price triggers are met ($38.56).

Helix. First put/call date is 2012, although noteholders have the right to convert prior

to that date if certain stock price triggers are met ($38.56).

– $121 Million MARAD - Original 25 year term; matures February 2027. $4.3 million

principal payments annually.

principal payments annually.

25

26

Consistent Top Line Growth

($ amounts in millions)

$2,148

$1,767

$1,367

$799

$543

$303

$227

$181

$396

Note: Includes Cal Dive

27

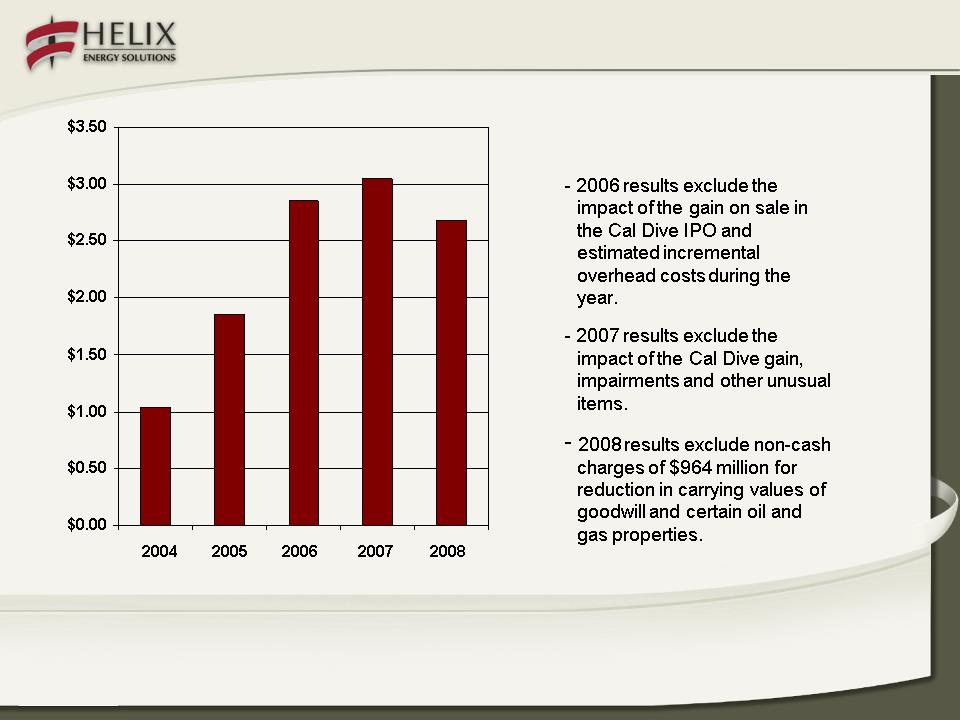

Earnings Per Share

$1.03

$2.68

$2.85

$3.05

$1.86

*See Non-GAAP reconciliation at www.HelixESG.com

28

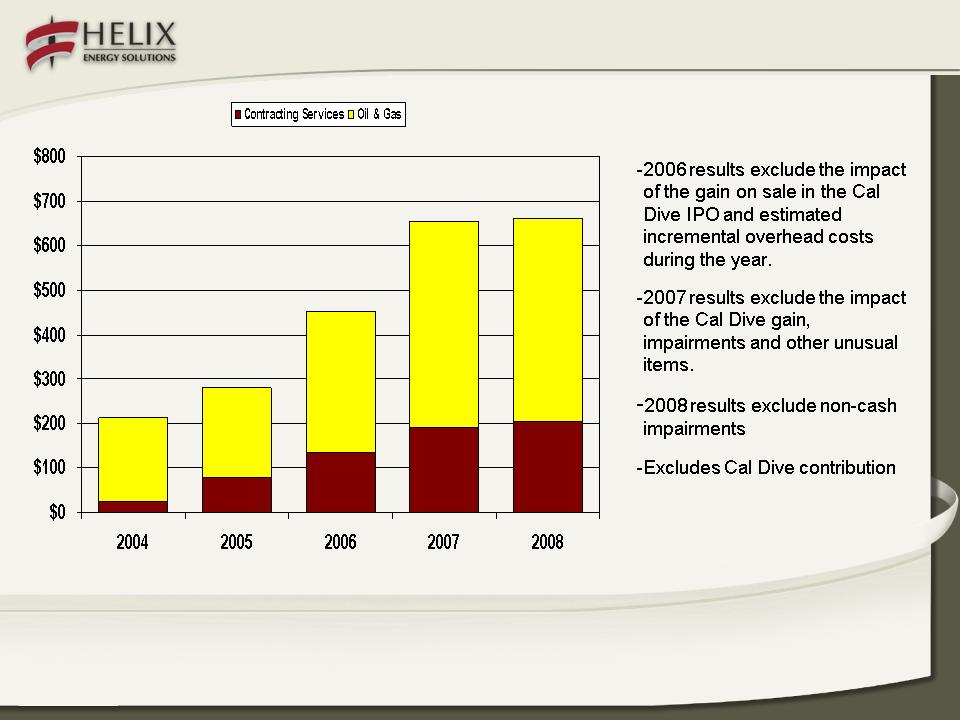

Significant Cash Generation - EBITDAX*

*See Non-GAAP reconciliation at www.HelixESG.com

($ amounts in millions)

$212

$279

$452

$655

$662

29