Exhibit 99.3

Third Quarter 2010 Earnings Supplementary Slides

November 11, 2010

Safe Harbor Statement

2

Strong Business Performance

§ Beat Q3 forecast in both segments

§ Met cost reduction plan in fab and field

§ Demand greater than supply - record backlog

§ Strong Q3 Execution

– Record cell outs, OEE, average efficiency and yields in Fabs 1 and 2

– 22+% Gen 2 cells on first production run in Fab 3

– Installed more than 70 MW* of power plants

– Closed sale of Montalto 28 MW ac solar park

3

* Power plant capacity in MW ac

Q4 Confidence / 2011 Visibility

§ High confidence in Q4 execution

– R&C: Fully booked

– UPP: On plan to monetize Italian solar parks

§ Strong growth and high visibility for 2011

– Volume and price established for Commercial business and UPP

– ~70% booked in Commercial for 2011

– 95% booked in North American UPP for 2011

– On plan for $1.08/W Q4 11 efficiency adjusted panel cost v. 14% panels

4

Vertical Integration Strategy

Poly

Ingot

Wafer

Cell

Panel

Upstream

§ World’s highest efficiency panels

§ Sustainable differentiated advantage

§ Drive for scale and cost reduction

Install

Services

Downstream

§ Adjust rapidly to market conditions

§ Integrated cost reduction

§ Premium brand / superior service

BOS

5

SPWR Downstream Strategy

§ World’s highest efficiency panels

§ Sustainable differentiated advantage

§ Drive for scale and cost reduction

§ Multi-year fixed price contracts

§ NA, EMEA, emerging markets

§ Integrated cost reduction

§ NAC: Multi-Qtr fixed price contracts

§ RLC: global dealer/partner network

§ Integrated cost reduction

EPC

Services

UPP Segment

BOS

Sales/

Install

Services

R&C Segment

BOS

Poly

Ingot

Wafer

Cell

Panel

Upstream

6

Diversified Channel / Portfolio

§R&C Market Position

− Global footprint, #1 in US

− Residential: 8 countries

− Commercial: Direct sales force

− #1 in NA, expanding to EU

− T5 driving wins: 3.5 MW Macy’s

§UPP Market Position

− Global reach / direct sales force

− 5 GW pipeline (~1/3 in EMEA)

− Customers buy energy (¢/kWh)

− High energy density = low LCOE

7

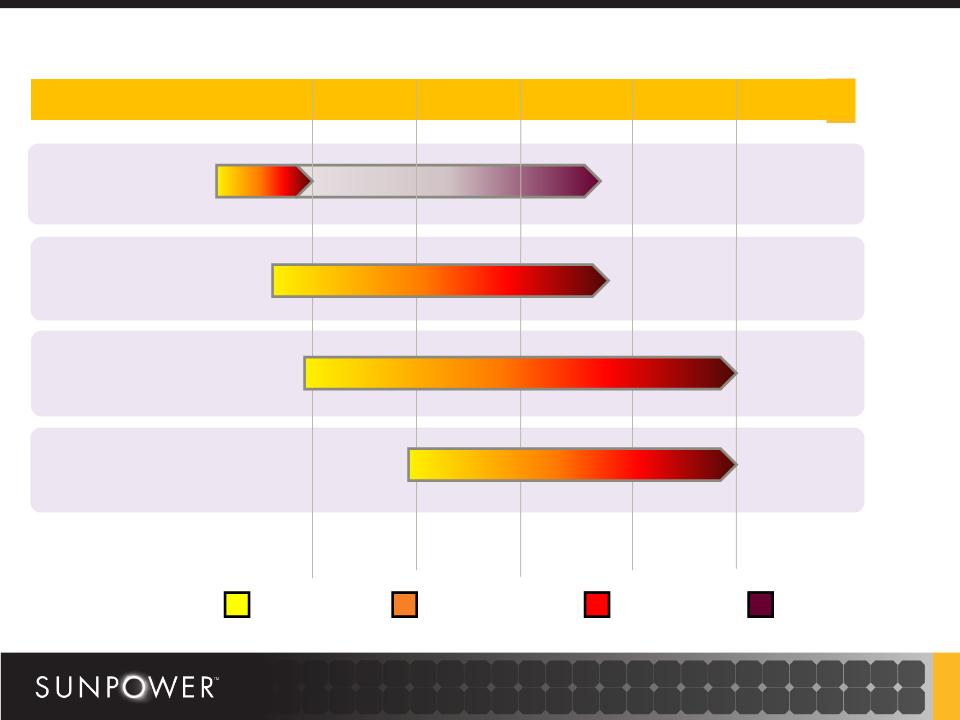

Italy Project Overview

2009 | Q1 ’10 | Q2 ’10 | Q3 ’10 | Q4 ’10 | Q1 ’11 |

Montalto 20

Montalto 8

Montalto 44

Solare Roma 13

Permitting

Construction

Financing

Sale

* MW’s in chart are listed in ac

8

Note: Illustrative 100 GWh / year power plant, Phoenix, AZ

SunPower LCOE Advantages

SunPower | 11% TF Fixed | |

GWh/yr | 100 | 100 |

MW | 37 | 46 |

Acres | 191 | 351 |

Inverters | 74 | 92 |

SunPower delivers

the same GWh using

far fewer acres and

less BOS leading to

lower O&M costs

the same GWh using

far fewer acres and

less BOS leading to

lower O&M costs

SunPower

Thin Film

9

SunPower LCOE Advantages

SunPower | 11% TF Fixed | |

GWh/yr | 100 | 100 |

Total $ | $200 MM | $200 MM |

$/Wp DC | $4.37 | $3.50 |

SunPower delivers

the same LCOE with

a 25% $/Wp price

premium

the same LCOE with

a 25% $/Wp price

premium

SunPower

Thin Film

Economically equivalent to customer

10

Note: Illustrative 100 GWh / year power plant, Phoenix, AZ

Efficiency Adjusted Cost/Watt*

Q4’09 | Q4’10 | Q4’11 | |

SunPower 19% Panel Cost / Watt** | $1.91 | $1.71 | $1.48 |

Efficiency Adjusted (vs. 14%) | $1.47 | $1.36 | $1.08 |

Efficiency Adjusted (vs. 11%) | $1.01 | $0.92 | $0.71 |

11

*Efficiency adjustments consider the BOS/tracking benefits of high efficiency panels.

**Base Cost/Watt excludes freight and pre-op expenses.

Comparison: 14% panel on T20 tracking system, 11% panel on fixed tilt.

§ Cost reduction drivers

− Fab 3 JV with AUO

− Leveraging R+D investments

− Improved manufacturing efficiency

− Increased ramp, yield and OEE

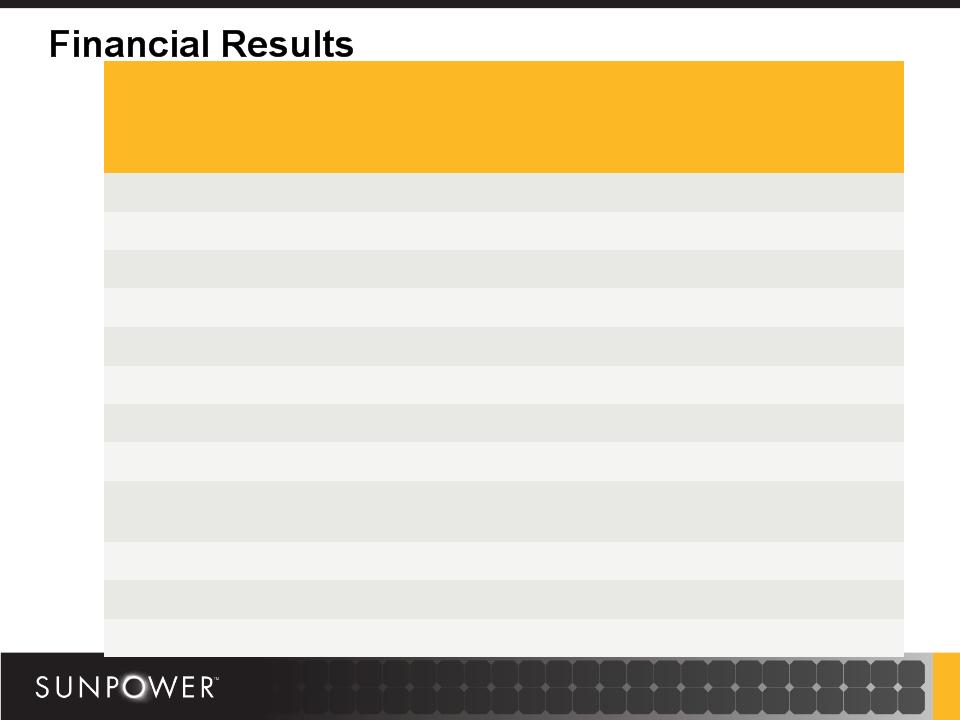

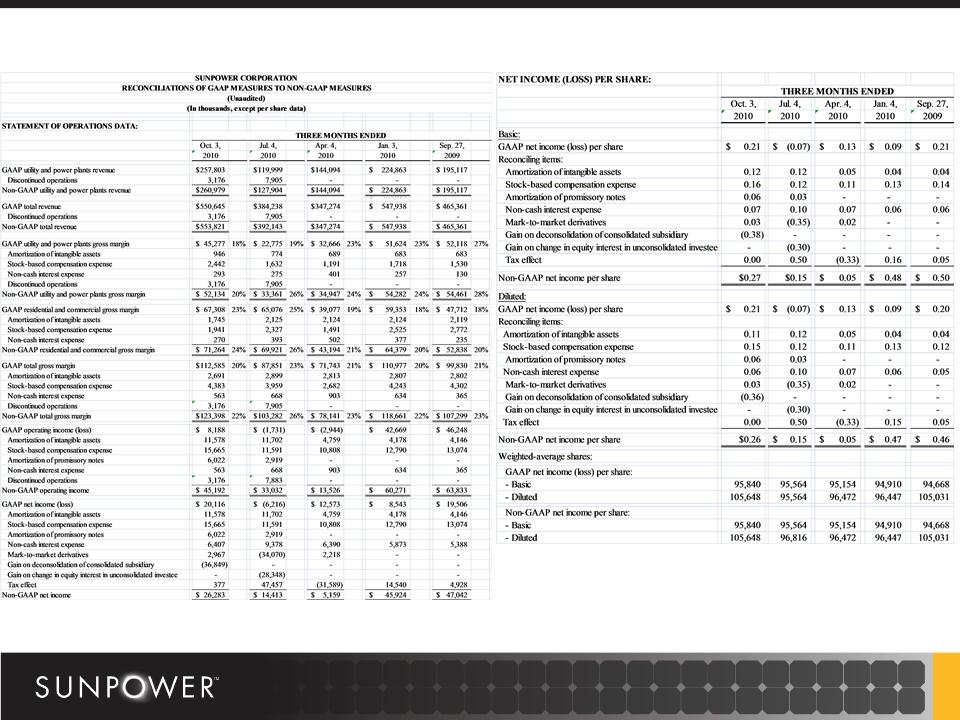

($ Millions except per share data) | Quarter Ending 10/3/10 | Quarter Ending 9/27/09 | Quarter Ending 7/4/10 |

Non-GAAP Revenues | $553.8 | $465.4 | $392.1 |

R+C | $292.8 | $270.2 | $264.2 |

UPP | $261.0 | $195.1 | $127.9 |

Gross Margin % (Non-GAAP) | 22.3% | 23.1% | 26.3% |

R+C | 24.3% | 19.6% | 26.5% |

UPP | 20.0% | 27.9% | 26.1% |

Tax Rate (non-GAAP) | 15.4% | 25.3% | 20.3% |

Net Income (Loss) (GAAP) | $20.1 | $19.5 | ($6.2) |

Net Income (Loss) (Non- GAAP) | $26.3 | $47.0 | $14.4 |

Diluted Wtg. Avg. Shares Out. | 105.6** | 105.0** | 96.8* |

EPS (GAAP) | $0.21 | $0.21 | ($0.07) |

EPS (Non-GAAP) | $0.26 | $0.46 | $0.15 |

Note: Non-GAAP figures are reconciled to comparable GAAP figures in appendix on company website

*not converted method **if converted method

Current and historical figures reflect Q2’10 change to new business unit segmentation

12

Balance Sheet and Financial Outlook

§ Liquidity

– Ended Q310 with $438 million in cash and investments

– Repaid $177 million in convertible debt and bank loans

– $145 million of additional liquidity available

– Shares in Woongjin Energy ~$360 million market value

§ Capital Expenditures of $4.3 million in Q3; 2010 plan of $125-$150 million

§ Q3 Free Cash Flow* of $78 million

§ Q4 FX exposure fully hedged at $1.37 to 1 Euro

§ Q3 production of 152 MW; 2010 on track to exceed 550 MW

*Free Cash Flow is net cash provided by (used in) operating activities less net cash provided by (used in) investing activities.

13

Italian Projects Update

§ On track to assemble, finance and monetize Italian projects in Q4

– Expect to complete and sell more than 80 MW in 2010

§ Montalto 44 MW

– Currently marketing €200 million in debt financing

– Industry’s first solar bond

– Provisional investment grade rating on both tranches of debt

– Debt transfers to new owner on sale

– Equity sale in negotiation for Q4 close

– On schedule for connection to grid in mid-December 2010

§ Solare Roma - 13 MW

– On schedule to connect and monetize project in December 2010

14

2010 Guidance

Q4 | FY 2010 | |

Revenue $MM | $870-$970 | $2,150-2,250 |

Gross Margin (Non-GAAP) | 20-22% | 22-23% |

EPS $/Share (Non-GAAP) | $0.95-$1.15 | $1.45-$1.65 |

EPS $/Share (GAAP) | $0.45-$0.60 | $0.75-$0.90 |

15

Third Quarter 2010 Earnings Supplementary Slides

November 11, 2010

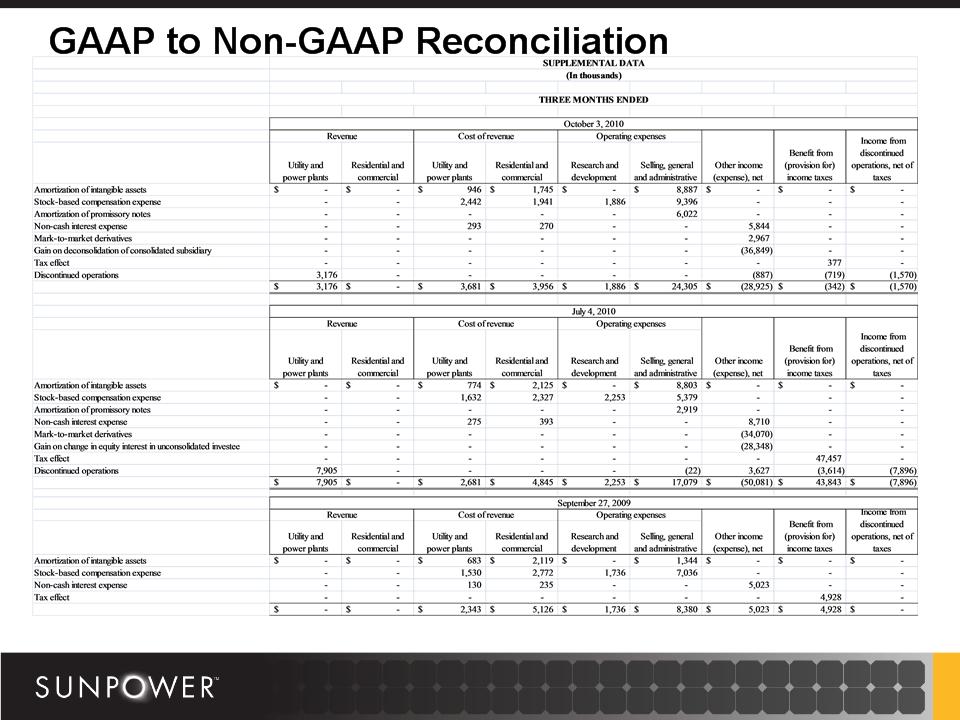

GAAP to Non-GAAP Reconciliation

17

18

Earnings Per Share Calculation

19

Three Months Ended October 3, 2010

GAAP

Non-GAAP

(in thousands)

If Converted Method

Not Converted

Method

Method

If Converted Method

Not Converted

Method

Method

Net income

$ 20,116

$ 20,116

$ 26,283

$ 26,283

Net income allocated to unvested restricted stock awards

(24)

(24)

(31)

(31)

Net income allocated to class A and class B common stock

20,092

20,092

26,252

26,252

Basic weighted-average shares

95,840

95,840

95,840

95,840

Net income per share - basic

$ 0.21

$ 0.21

$ 0.27

$ 0.27

Net income

$ 20,116

$ 20,116

$ 26,283

$ 26,283

(A)

Interest expense on 4.75% debentures, net of tax

1,666

-

1,666

-

Net income allocated to unvested restricted stock awards

(23)

(24)

(30)

(31)

Net income allocated to class A and class B common stock

21,759

20,092

27,919

26,252

Diluted weighted-average shares before consideration of 4.5% debentures

96,936

96,936

96,936

96,936

Shares issued if 100% of 4.5% Debentures are converted to equity

8,712

-

8,712

-

Diluted weighted-average shares

105,648

96,936

105,648

96,936

Net income per share - diluted

$ 0.21

$ 0.21

$ 0.26

$ 0.27

(A)

Under the "If Converted Method" we calculated diluted earnings per share using the more dilutive of the following two methods:

Method One:

Numerator = Income Available to Common Shareholders + Interest on 4.5% Debentures, Net of Tax

Denominator = Stock Outstanding + Common Shares Issued if 100% Coversion of 4.5% Debentures

Method Two:

Numerator = Income Available to Common Shareholders

Denominator = Stock Outstanding