TELUS Corporation — Management’s discussion and analysis — 2019

Caution regarding forward-looking statements

The terms TELUS, the Company, we, us and our refer to TELUS Corporation and, where the context of the narrative permits or requires, its subsidiaries.

This document contains forward-looking statements about expected events and our financial and operating performance. Forward-looking statements include any statements that do not refer to historical facts. They include, but are not limited to, statements relating to our objectives and our strategies to achieve those objectives, our targets, outlook, updates, and our multi-year dividend growth program. Forward-looking statements are typically identified by the words assumption, goal, guidance, objective, outlook, strategy, target and other similar expressions, or future or conditional verbs such as aim, anticipate, believe, could, expect, intend, may, plan, predict, seek, should, strive and will. These statements are made pursuant to the “safe harbour” provisions of applicable securities laws in Canada and the United States Private Securities Litigation Reform Act of 1995.

By their nature, forward-looking statements are subject to inherent risks and uncertainties and are based on assumptions, including assumptions about future economic conditions and courses of action. These assumptions may ultimately prove to have been inaccurate and, as a result, our actual results or events may differ materially from expectations expressed in or implied by the forward-looking statements. Our general outlook and assumptions for 2020 are presented in Section 9 General trends, outlook and assumptions, and regulatory developments and proceedings in this Management’s discussion and analysis (MD&A).

Risks and uncertainties that could cause actual performance or events to differ materially from the forward-looking statements made herein and in other TELUS filings include, but are not limited to, the following:

· Regulatory decisions and developments including changes to our regulatory regime (the timing of announcement or implementation of which are uncertain) or the outcomes of proceedings, cases or inquiries relating to its application, including but not limited to those set out in Section 9.4 Communications industry regulatory developments and proceedings in this MD&A, such as the potential for government intervention to further increase competition, for example, through mandated wholesale access; the potential for additional government intervention on pricing as committed in the 2019 federal election; federal and provincial consumer protection legislation and regulation; amendments to existing federal legislation; potential threats to unitary federal regulatory authority over telecommunications; regulatory action by the Competition Bureau or other regulatory agencies; spectrum and compliance with licences, including our compliance with licence conditions, changes to spectrum licence fees, spectrum policy determinations such as restrictions on the purchase, sale, subordination and transfer of spectrum licences, the cost and availability of spectrum, and ongoing and future consultations and decisions on spectrum allocation; the impact on us and other Canadian telecommunications carriers of government or regulatory actions with respect to certain countries or suppliers, including the executive order signed by U.S. President Donald Trump permitting the Secretary of Commerce to block certain technology transactions deemed to constitute national security risks and the imposition of additional licence requirements on the export, re-export and transfer of goods, services and technology to Huawei Technologies Co. Ltd. and its non-U.S. affiliates; restrictions on non-Canadian ownership and control of TELUS Common Shares and the ongoing monitoring of and compliance with such restrictions; unanticipated changes to the current copyright regime; and our ability to comply with complex and changing regulation of the healthcare and medical devices industry in the jurisdictions in which we operate, including as an operator of health clinics.

· Competitive environment including: our ability to continue to retain customers through an enhanced customer service experience, including through the deployment and operation of evolving wireless and wireline infrastructure; intense wireless competition, including the ability of industry competitors to successfully combine a mix of internet services and, in some cases, wireless services under one bundled and/or discounted monthly rate, along with their existing broadcast or satellite-based TV services; the success of new products, services and supporting systems, such as home automation security and Internet of Things (IoT) services for internet-connected devices; wireline voice and data competition, including continued intense rivalry across all services among wireless and wireline telecommunications companies, cable companies, other communications companies and over-the-top (OTT) services, which, among other things, places pressures on current and future mobile phone average billing per subscriber per month (ABPU), mobile phone average revenue per subscriber per month (ARPU), cost of acquisition, cost of retention and churn rate for all services, as do customer usage patterns, increased data bucket sizes or flat-rate pricing trends for voice and data, such as our Peace of Mind™ plans and comparable plans recently launched, inclusive rate plans for voice and data and availability of Wi-Fi networks for data; mergers and acquisitions of industry competitors; pressures on internet and TV ARPU and churn rate resulting from market conditions, government actions and customer usage patterns; residential voice and business network access line losses; subscriber additions and retention volumes, and associated costs for wireless, TV and internet services; our ability to obtain and offer content on a timely basis across multiple devices on wireless and TV platforms at a reasonable cost as content costs per unit continue to grow; vertical integration in the broadcasting industry resulting in competitors owning broadcast content services, and timely and effective enforcement of related regulatory safeguards; our ability to compete successfully in customer care and business services (CCBS) given our competitors’ brand recognition, consolidation and strategic alliances, as well as technology development; in our TELUS Health business, our ability to compete with other providers of electronic medical records and pharmacy management products, systems integrators and health service providers including those that own a vertically integrated mix of health services delivery, IT solutions, and related services, and global providers that could achieve expanded Canadian footprints; and our ability to successfully develop our smart data solutions business.

![]()

· Technological substitution including: reduced utilization and increased commoditization of traditional wireline voice services (local and long distance) resulting from impacts of OTT applications and wireless substitution; a declining overall market for paid TV services, including as a result of content piracy and signal theft, a rise in OTT direct-to-consumer video offerings and virtual multichannel video programming distribution platforms; the increasing number of households that have only wireless and/or internet-based telephone services; potential declines in mobile phone ABPU and ARPU as a result of, among other factors, substitution by messaging and OTT applications; substitution by increasingly available Wi-Fi services; and disruptive technologies, such as OTT IP services, including software-defined networks in the business market, that may displace or cause us to reprice our existing data services.

· Challenges to our ability to deploy technology including: high subscriber demand for data that challenges wireless networks and spectrum capacity levels and may be accompanied by increases in delivery cost; our reliance on information technology and our ability to streamline our legacy systems; the roll-out and evolution of wireless broadband technologies and systems, including video distribution platforms and telecommunications network technologies (broadband initiatives, such as fibre to the premises (FTTP), wireless small-cell deployment, 5G wireless and availability of resources and our ability to build out adequate broadband capacity); our reliance on wireless network access agreements, which have facilitated our deployment of wireless technologies; our choice of suppliers and those suppliers’ ability to maintain and service their product lines, which could affect the success of upgrades to, and evolution of, technology that we offer; supplier limitations and concentration and market power for products such as network equipment, TELUS TV® and wireless handsets; our expected long-term need to acquire additional spectrum capacity through future spectrum auctions and from third parties to address increasing demand for data and our ability to utilize spectrum we acquire; deployment and operation of new wireline broadband network technologies at a reasonable cost and the availability and success of new products and services to be rolled out using such network technologies; network reliability and change management; and our deployment of self-learning tools and automation that may change the way we interact with customers.

· Capital expenditure levels and potential outlays for spectrum licences in auctions or purchases from third parties, affect and are affected by: our broadband initiatives, including connecting more homes and businesses directly to fibre; our ongoing deployment of newer wireless technologies, including wireless small cells to improve coverage and capacity and prepare for a more efficient and timely evolution to 5G wireless services; investments in network resiliency and reliability; the allocation of resources to acquisitions and future wireless spectrum auctions held by Innovation, Science and Economic Development Canada (ISED), including the 3500 MHz and millimetre wave spectrum auctions expected to take place in 2020 and 2021, respectively, and the announcement of a formal consultation on the auctioning of 3800 MHz spectrum, expected to take place in 2022. Our capital expenditure levels could be impacted if we do not achieve our targeted operational and financial results or by changes to our regulatory environment.

· Operational performance and business combination risks including: our reliance on legacy systems and ability to implement and support new products and services and business operations in a timely manner; our ability to manage the requirements of large enterprise deals; our ability to implement effective change management for system replacements and upgrades, process redesigns and business integrations (such as our ability to successfully integrate acquisitions, complete divestitures or establish partnerships in a timely manner and realize expected strategic benefits, including those following compliance with any regulatory orders); our ability to identify and manage new risks inherent in new service offerings that we may provide, including as a result of acquisitions, which could result in damage to our brand, our business in the relevant area or as a whole, and additional exposure to litigation or regulatory proceedings.

· Data protection including risks that malfunctions or unlawful acts could result in unauthorized access to, change, loss, or distribution of data, which may compromise the privacy of individuals and could result in financial loss and harm to our reputation and brand.

· Security threats including intentional damage or unauthorized access to our physical assets or our IT systems and networks, which could prevent us from providing reliable service or result in unauthorized access to our information or that of our customers.

· Ability to successfully implement cost reduction initiatives and realize planned savings, net of restructuring and other costs, without losing customer service focus or negatively affecting business operations. Examples of these initiatives are: our operating efficiency and effectiveness program to drive improvements in financial results; business integrations; business product simplification; business process automation and outsourcing; offshoring and reorganizations; procurement initiatives; and real estate rationalization.

· Foreign operations and our ability to successfully manage operations in foreign jurisdictions, including managing risks such as currency fluctuations.

· Business continuity events including: our ability to maintain customer service and operate our network in the event of human error or human-caused threats, such as cyberattacks and equipment failures that could cause various degrees of network outages; supply chain disruptions, delays and economics, including as a result of government restrictions or trade actions; natural disaster threats; epidemics; pandemics; political instability in certain international locations; information security and privacy breaches, including data loss or theft of data; and the completeness and effectiveness of business continuity and disaster recovery plans and responses.

· Human resource matters including: recruitment, retention and appropriate training in a highly competitive industry, and the level of our employee engagement.

· Financing and debt requirements including: our ability to carry out financing activities, refinance our maturing debt and/or maintain investment grade credit ratings in the range of BBB+ or the equivalent. Our business plans and growth could be negatively affected if existing financing is not sufficient to cover our funding requirements.

![]()

· Lower than planned free cash flow could constrain our ability to invest in operations, reduce leverage or return capital to shareholders, and could affect our ability to sustain our dividend growth program through 2022. This program may be affected by factors such as the competitive environment, economic performance in Canada, our earnings and free cash flow, our levels of capital expenditures and spectrum licence purchases, acquisitions, the management of our capital structure, and regulatory decisions and developments. Quarterly dividend decisions are subject to assessment and determination by our Board of Directors based on our financial position and outlook. Shares may be purchased under our normal course issuer bid (NCIB) when and if we consider it opportunistic, based on our financial position and outlook, and the market price of TELUS Common Shares. There can be no assurance that our dividend growth program or any NCIB will be maintained, not changed and/or completed.

· Taxation matters including: interpretation of complex domestic and foreign tax laws by the relevant tax authorities that may differ from our interpretations; the timing and character of income and deductions, such as tax depreciation and operating expenses; tax credits or other attributes; changes in tax laws, including tax rates; tax expenses being materially different than anticipated, including the taxability of income and deductibility of tax attributes; elimination of income tax deferrals through the use of different tax year-ends for operating partnerships and corporate partners; and changes to the interpretation of tax laws, including those resulting from changes to applicable accounting standards or the adoption of more aggressive auditing practices by tax authorities , tax reassessments or adverse court decisions impacting the tax payable by us.

· Litigation and legal matters including: our ability to successfully respond to investigations and regulatory proceedings; our ability to defend against existing and potential claims and lawsuits (including intellectual property infringement claims and class actions based on consumer claims, data, privacy or security breaches and secondary market liability), or to negotiate and execute upon indemnity rights or other protections in respect of such claims and lawsuits; and the complexity of legal compliance in domestic and foreign jurisdictions, including compliance with competition, anti-bribery and foreign corrupt practices laws.

· Health, safety and the environment including: lost employee work time resulting from illness or injury, public concerns related to radio frequency emissions, environmental issues affecting our business, including climate change, waste and waste recycling, risks relating to fuel systems on our properties, and changing government and public expectations regarding environmental matters and our responses.

· Economic growth and fluctuations including: the state of the economy in Canada, which may be influenced by economic and other developments outside of Canada, including potential outcomes of yet unknown policies and actions of foreign governments; expectations of future interest rates; inflation; unemployment levels; effects of fluctuating oil prices; effects of low business spending (such as reducing investments and cost structure); pension investment returns, funding and discount rates; fluctuations in foreign exchange rates of the currencies in the regions in which we operate; the impact of tariffs on trade between Canada and the U.S., and global implications of the trade dynamic between major world economies.

These risks are described in additional detail in Section 9 General trends, outlook and assumptions, and regulatory developments and proceedings and Section 10 Risks and risk management in this MD&A. Those descriptions are incorporated by reference in this cautionary statement but are not intended to be a complete list of the risks that could affect the Company.

Many of these factors are beyond our control or our current expectations or knowledge. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also have a material adverse effect on our financial position, financial performance, cash flows, business or reputation. Except as otherwise indicated in this document, the forward-looking statements made herein do not reflect the potential impact of any non-recurring or special items or any mergers, acquisitions, dispositions or other business combinations or transactions that may be announced or that may occur after the date of this document.

Readers are cautioned not to place undue reliance on forward-looking statements. Forward-looking statements in this document describe our expectations, and are based on our assumptions, as at the date of this document and are subject to change after this date. Except as required by law, we disclaim any intention or obligation to update or revise any forward-looking statements.

This cautionary statement qualifies all of the forward-looking statements in this MD&A.

![]()

Management’s discussion and analysis (MD&A)

February 13, 2020

Contents

Section |

| Page |

| Subsection | ||

1. |

| Introduction |

| 6 |

| 1.1 Preparation of the MD&A |

|

|

|

| 6 |

| 1.2 The environment in which we operate |

|

|

|

| 7 |

| 1.3 Highlights of 2019 |

|

|

|

| 13 |

| 1.4 Performance scorecard (key performance measures) |

2. |

| Core business and strategy |

| 16 |

| 2.1 Core business |

|

|

|

| 75 |

| 2.2 Strategic imperatives |

3. |

| Corporate priorities |

| 17 |

|

|

4. |

| Capabilities |

| 21 |

| 4.1 Principal markets addressed and competition |

|

|

|

| 24 |

| 4.2 Operational resources |

|

|

|

| 28 |

| 4.3 Liquidity and capital resources |

|

|

|

| 30 |

| 4.4 Disclosure controls and procedures and changes in internal control over financial reporting |

5. |

| Discussion of operations |

| 31 |

| 5.1 General |

|

|

|

| 33 |

| 5.2 Summary of consolidated quarterly results, trends and fourth quarter recap |

|

|

|

| 37 |

| 5.3 Consolidated operations |

|

|

|

| 41 |

| 5.4 Wireless segment |

|

|

|

| 45 |

| 5.5 Wireline segment |

6. |

| Changes in financial position |

| 49 |

|

|

7. |

| Liquidity and capital resources |

| 50 |

| 7.1 Overview |

|

|

|

| 51 |

| 7.2 Cash provided by operating activities |

|

|

|

| 51 |

| 7.3 Cash used by investing activities |

|

|

|

| 52 |

| 7.4 Cash provided (used) by financing activities |

|

|

|

| 54 |

| 7.5 Liquidity and capital resource measures |

|

|

|

| 56 |

| 7.6 Credit facilities |

|

|

|

| 58 |

| 7.7 Sale of trade receivables |

|

|

|

| 58 |

| 7.8 Credit ratings |

|

|

|

| 58 |

| 7.9 Financial instruments, commitments and contingent liabilities |

|

|

|

| 60 |

| 7.10 Outstanding share information |

|

|

|

| 60 |

| 7.11 Transactions between related parties |

8. |

| Accounting matters |

| 61 |

| 8.1 Critical accounting estimates and judgments |

|

|

|

| 65 |

| 8.2 Accounting policy developments |

9. |

| General trends, outlook and assumptions, and regulatory developments and proceedings |

| 66 |

| 9.1 Telecommunications industry in 2019 |

67 |

| 9.2 Telecommunications industry general outlook and trends | ||||

70 |

| 9.3 TELUS assumptions for 2020 | ||||

71 |

| 9.4 Communications industry regulatory developments and proceedings | ||||

10. |

| Risks and risk management |

| 75 |

| 10.1 Overview |

|

|

|

| 75 |

| 10.2 Principal risks and uncertainties |

|

|

|

| 77 |

| 10.3 Regulatory matters |

|

|

|

| 79 |

| 10.4 Competitive environment |

|

|

|

| 81 |

| 10.5 Technology |

|

|

|

| 83 |

| 10.6 Suppliers |

|

|

|

| 84 |

| 10.7 Organizational change |

|

|

|

| 84 |

| 10.8 Customer service delivery |

|

|

|

| 85 |

| 10.9 Our systems and processes |

|

|

|

| 86 |

| 10.10 Security and data protection |

|

|

|

| 87 |

| 10.11 Our team |

|

|

|

| 88 |

| 10.12 Our environment |

|

|

|

| 89 |

| 10.13 Financing, debt and dividends |

|

|

|

| 90 |

| 10.14 Tax matters |

|

|

|

| 91 |

| 10.15 The economy |

|

|

|

| 92 |

| 10.16 Litigation and legal matters |

11. |

| Definitions and reconciliations |

| 93 |

| 11.1 Non-GAAP and other financial measures |

|

|

|

| 96 |

| 11.2 Operating indicators |

Copyright © 2020 TELUS Corporation. All rights reserved. Certain products and services named in this report are trademarks. The symbols TM and ® indicate those owned by TELUS Corporation or its subsidiaries. All other trademarks are the property of their respective owners.

![]()

1. Introduction

The forward-looking statements in this section, including estimates regarding economic growth, unemployment rates and housing starts, are qualified by the Caution regarding forward-looking statements at the beginning of this Management’s discussion and analysis (MD&A).

1.1 Preparation of the MD&A

The following sections are a discussion of our consolidated financial position and financial performance for the year ended December 31, 2019, and should be read together with our December 31, 2019, audited consolidated statements of income and other comprehensive income, statements of financial position, statements of changes in owners’ equity and statements of cash flows, and the related notes (collectively referred to as the Consolidated financial statements). The generally accepted accounting principles (GAAP) that we use are International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) and Canadian GAAP. In this MD&A, the term IFRS refers to these standards. We adopted IFRS 16, Leases, on January 1, 2019, with retrospective application, and the cumulative effect of the initial application of the new standard was recognized at the date of initial application, January 1, 2019. This method of application does not result in the retrospective adjustment of amounts reported for periods prior to fiscal 2019. The most significant effect of the new standard is the lessee’s recognition of the initial present value of unavoidable future lease payments as right-of-use lease assets and lease liabilities, including those for most leases that would previously have been accounted for as operating leases. This results in depreciation of right-of-use lease assets and financing costs arising from lease liabilities, rather than as part of Goods and services purchased. The adoption of the new standard has resulted in an increase of approximately $1.0 billion in Property, plant and equipment and an increase of approximately $1.4 billion in long-term debt as at January 1, 2019. However, the implementation of IFRS 16 does not have any impact on economics or cash flows. In our discussion, we also use certain non-GAAP financial measures to evaluate our performance, monitor compliance with debt covenants and manage our capital structure. These measures are defined, qualified and reconciled with their nearest GAAP measures in Section 11.1. All currency amounts are in Canadian dollars, unless otherwise specified.

Additional information relating to the Company, including our annual information form and other filings with securities commissions or similar regulatory authorities in Canada, is available on SEDAR (sedar.com). Our filings with the Securities and Exchange Commission in the United States, including Form 40-F, are available on EDGAR (sec.gov).

Our disclosure controls and procedures are designed to provide reasonable assurance that all relevant information is gathered and reported to senior management on a timely basis, so that appropriate decisions can be made regarding public disclosure. This MD&A and the Consolidated financial statements were reviewed by our Audit Committee and authorized by our Board of Directors (Board) for issuance on February 13, 2020.

In this MD&A, unless otherwise indicated, results for the year ended December 31, 2019, are compared with results for the year ended December 31, 2018.

1.2 The environment in which we operate

The success of our business and the challenges we face can best be understood with reference to the environment in which we operate, including broader economic factors that affect our customers and us, and the competitive nature of our operations. Our estimates regarding our environment, including economic growth, unemployment rates and housing starts, also form an important part of the assumptions on which our targets are based. The extent to which these estimates affect us and the timing of their impact will depend upon the actual experience of specific sectors of the Canadian economy.

2019 Canadian telecom |

| TELUS 2019 revenues |

| TELUS subscriber |

| TELUS 2019 dividends | |

Est. 2% |

| $ | 14.7 billion |

| 15.2 million |

| $1.4 billion / 8.4% |

![]()

|

| Economic growth |

| Unemployment |

| Housing starts |

| ||||||||||||

|

| (Percentage points) |

| (Percentage points) |

| (000s of units) |

| ||||||||||||

|

| Estimated gross |

| Our |

| Unemployment rates |

| Our |

| Seasonally adjusted |

| Our estimated |

| ||||||

|

|

|

|

|

|

|

| For the month of |

|

|

| For the month of |

|

|

| ||||

|

|

|

|

|

|

|

| December |

| December |

|

|

| December |

| December |

|

|

|

|

| 2020 |

| 2019 |

| 2020 |

| 20193 |

| 20183 |

| 2020 |

| 2019 |

| 2018 |

| 2020 |

|

Canada |

| 1.6 | 4 | 1.5 | 4 | 1.6 |

| 5.6 |

| 5.6 |

| 5.9 |

| 197 |

| 214 |

| 201 |

|

B.C. |

| 1.9 | 5 | 1.7 | 5 | 2.3 |

| 4.8 |

| 4.4 |

| 4.7 |

| 43 |

| 51 |

| 39 |

|

Alberta |

| 2.7 | 5 | 0.6 | 5 | 1.9 |

| 7.0 |

| 6.4 |

| 6.9 |

| 40 |

| 19 |

| 27 |

|

Ontario |

| 1.6 | 5 | 1.4 | 5 | 1.6 |

| 5.3 |

| 5.4 |

| 5.7 |

| 57 |

| 70 |

| 73 |

|

Quebec |

| 1.5 | 5 | 1.8 | 5 | 1.6 |

| 5.3 |

| 5.5 |

| 5.0 |

| 37 |

| 53 |

| 46 |

|

(1) Assumptions are as of October 25, 2019 and are based on a composite of estimates from Canadian banks and other sources.

(2) Source: Statistics Canada. Table 34-10-0158-01 Canada Mortgage and Housing Corporation, housing starts, all areas, Canada and provinces, seasonally adjusted at annual rates, monthly (x 1,000).

(3) Source: Statistics Canada Labour Force Survey, December 2019 and December 2018, respectively.

(4) Source: Bank of Canada Monetary Policy Report, January 2020.

(5) Source: British Columbia Ministry of Finance, 2019/20 First Quarterly Report, September 2019; Alberta Ministry of Treasury Board and Finance, 2019 — 23 Fiscal Plan, October 2019; Ontario Ministry of Finance, 2019 Ontario Budget, April 2019; and Ministère des Finances du Québec, Budget 2019 — 2020, March 2019, respectively.

Canadian telecommunications industry growth

We estimate that Canadian telecommunications industry revenues (including TV revenue and excluding media revenue) grew by approximately 2% in 2019 (4% in 2018). We estimate that the Canadian wireless industry added approximately 1.9 million subscribers in 2019 and experienced network revenue growth of approximately 1.6%. Wireless revenues continued to account for the largest portion of telecommunications sector revenues. Key drivers of subscriber growth included the increased demand for data services; immigration and population growth; the trend toward multiple devices, including tablets and Internet of Things (IoT) offerings; the expanding functionality of data and related applications; and mobile adoption by both younger and older generations. With respect to the wireline industry, the Western Canadian consumer high-speed internet penetration rate grew by approximately 1% to 87% in 2019 and subscriber growth is expected to continue. More Canadians are subscribing to internet services, as they continued to use more data, subscribe to faster and larger packages, and allocate more money to internet services. Competitive pressures continued in both the wireline consumer and business markets, while declines in higher-margin legacy voice services were ongoing, partially attributable to technological substitution. (See Section 9 General trends, outlook and assumptions, and regulatory developments and proceedings, Section 10.4 Competitive environment and Section 10.15 The economy.)

1.3 Highlights of 2019

Spectrum

On April 10, 2019, we announced that we were the successful bidder on 12 wireless spectrum licences in B.C., Alberta, Saskatchewan, Ontario and Quebec in the Innovation, Science and Economic Development Canada (ISED) 600 MHz wireless spectrum auction. The 600 MHz band is important for its ability to travel long distances in rural areas and infiltrate barriers to better reach in-building locations, such as elevators and parking garages, making it highly conducive to 5G deployment. The licences, acquired for $931 million ($2.35 per MHz-pop, where pop refers to the population in a licence area), equate to a national average of 11.3 MHz and will enable us to deliver enhanced mobile broadband connectivity as the industry transitions from 4G LTE to 5G. The design of the combinatorial clock auction (CCA), coupled with a 30 MHz set-aside for regional carriers (representing 43% of the spectrum at auction), led to national carriers paying a 134% premium over regional operators, and according to our analysis, the highest prices for 600 MHz spectrum in the world. Outside of Canada, set-asides are very rare, and in the few instances of CCAs with set-asides, the set-asides have represented only approximately 5% of the spectrum at auction.

During the third quarter of 2019, we obtained the use of certain AWS-4 spectrum licences from the original licensee (for approximately $1.16 per MHz-pop) and have accounted for them as intangible assets with indefinite lives; such subordination of licences has been approved by ISED. Additionally, we obtained AWS-1 and AWS-3 spectrum licences in Northern Ontario.

![]()

Telecommunications business acquisition

On January 14, 2019, we acquired a telecommunications business that is complementary to our existing lines of business, for consideration consisting of cash and accounts payable and accrued liabilities of $75 million and TELUS Corporation Common Shares of $38 million. The investment was made with a view to growing our managed network, cloud, security and unified communications services.

Smart data solutions business acquisition

On August 12, 2019, we acquired a business that is complementary to, and with a view to growing, our existing smart data solutions business, for consideration consisting of cash and accounts payable and accrued liabilities of $135 million.

ADT Security Services Canada, Inc.

On November 5, 2019, we acquired the customers, assets and operations of ADT Security Services Canada, Inc. (ADT Canada) for approximately $700 million. This acquisition furthers our commitment to leverage the power of technology to enhance convenience, control and safety in the lives, homes and businesses of more Canadians.

Business acquisition — subsequent to 2019

On December 4, 2019, we announced that we had entered into an agreement to acquire 100% of German-headquartered Competence Call Center (CCC) for approximately $1.3 billion (€915 million), less debt assumed and subject to customary closing conditions, including regulatory approvals. Subsequently, the requisite regulatory approvals were obtained and the transaction closed on January 31, 2020. CCC is a provider of higher-value-added business services with a focus on customer relationship management and content moderation. CCC offers its services across 11 European countries and partners with industry-leading global brands primarily from fast-growing technology, media and telecommunications, retail, and travel and hospitality sectors.

Endless data, device financing and family discounts

As part of our commitment to putting customers first, on July 3, 2019, we introduced mobile phone endless data in combination with device financing and family discounts. Our Peace of Mind rate plans give customers access to endless data starting at $75 per month for 10 GB of high-speed data. If a customer reaches their high-speed data threshold within the monthly billing cycle, data speeds will be reduced to 512 Kbps without the customer being charged for any overages. TELUS Easy Payment®, our device financing program, gives customers access to any smartphone for as little as $0 upfront, with financing options over 24 months. TELUS Family Discounts provide incremental savings, ranging from $5 to $15, off the monthly rate plan with every new family member who signs up (up to a maximum of nine lines).

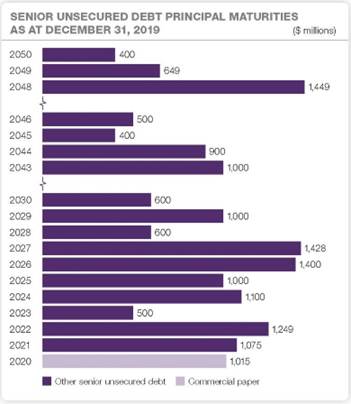

Long-term debt issue and early redemption of 2020 Notes, lengthening our average term to maturity and lowering our weighted average cost

On April 3, 2019, we issued $1.0 billion of senior unsecured 3.30% Notes, Series CY, which will mature on May 2, 2029. The net proceeds were used to repay outstanding indebtedness, including outstanding commercial paper, for the reduction of cash amounts outstanding under an arm’s-length securitization trust and for general corporate purposes.

On May 28, 2019, we issued US$500 million of senior unsecured 4.30% Notes, which will mature on June 15, 2049. The net proceeds were used to repay outstanding indebtedness, including outstanding commercial paper, to redeem $650 million of the $1.0 billion aggregate principal amount of our 5.05% Notes, Series CH, due July 23, 2020, and for general corporate purposes. We have fully hedged the principal and interest obligations of the notes by entering into a foreign exchange derivative (a cross currency interest rate exchange agreement), which effectively converted the principal payments and interest obligations to Canadian dollar obligations with a fixed interest rate of 4.27% and an issued and outstanding amount of $672 million (reflecting a fixed exchange rate of $1.3435).

On July 2, 2019, we issued $800 million of senior unsecured 2.75% Notes, Series CZ, which will mature on July 8, 2026. The net proceeds were used to redeem the remaining $350 million of our 5.05% Notes, Series CH, to repay outstanding indebtedness, including outstanding commercial paper, and for general corporate purposes.

On December 16, 2019, we issued $600 million of senior unsecured 3.15% Notes, Series CAA, which will mature on February 19, 2030, and $400 million of senior unsecured 3.95% Notes, Series CAB, which will mature on February 16, 2050. The net proceeds were used to repay outstanding indebtedness, to finance the acquisition of ADT Canada, to fund capital expenditures and for general corporate purposes.

On July 23, 2019, we early redeemed $650 million of our 5.05% Notes, Series CH. On August 7, 2019, we early redeemed the remaining $350 million that was not redeemed on July 23, 2019. The long-term debt prepayment premium for the entire $1.0 billion Series CH notes redemption was $28 million before income taxes ($0.03 per share after income taxes) (pre-share split — see Share split — subsequent to 2019 in Section 1.3 below). Subsequent to this early redemption, we no longer have any TELUS Corporation notes maturing in 2020.

![]()

Collectively, these transactions lengthened the average term to maturity of our long-term debt (excluding commercial paper, the revolving component of the TELUS International (Cda) Inc. credit facility, lease liabilities and other long-term debt) from approximately 12.2 years at December 31, 2018, to approximately 12.8 years at December 31, 2019, and lowered the weighted average cost of our long-term debt (excluding commercial paper, the revolving component of the TELUS International (Cda) Inc. credit facility, lease liabilities and other long-term debt) from 4.18% at December 31, 2018 to 3.94% at December 31, 2019.

Multi-year dividend growth program

On May 9, 2019, we announced our intention to target ongoing semi-annual dividend increases, with the annual increase in the range of 7 to 10% from 2020 through to the end of 2022. This announcement further extends our dividend program, which was originally announced in May 2011 and extended for three additional years in each of May 2013 and May 2016. So as to be consistent with the way we manage our business, we have revised our target guideline, effective January 1, 2020, to be calculated as 60 to 75% of free cash flow on a prospective basis (free cash flow is a non-GAAP measure, see Section 11.1). Notwithstanding this target, dividend decisions will continue to be subject to our Board’s assessment and the determination of our financial situation and outlook on a quarterly basis. There can be no assurance that we will maintain a dividend growth program through 2022. See Section 4.3 Liquidity and capital resources.

Changes to the Board of Directors

Bill MacKinnon retired from our Board in May 2019. Bill had been a director since 2009, and served as the chair of the Audit Committee from 2011 to May 2018 and as a member of the Corporate Governance Committee from 2013 to 2015.

Sabi Marwah also retired from our Board in May 2019. Sabi joined the Board in 2015 and served on both the Audit and Corporate Governance Committees.

During the third quarter of 2019, Claude Mongeau stepped down from our Board. Claude joined the Board in 2017 and served on both the Audit and Corporate Governance Committees.

We thank Bill, Sabi and Claude for their outstanding contributions and service to TELUS.

Share split — subsequent to 2019

Subsequent to December 31, 2019, we announced a subdivision of our Common Shares on a two-for-one basis to be effected March 17, 2020. In all instances, unless otherwise indicated, the number of shares authorized, the number of shares outstanding, the number of shares reserved, per share amounts and share-based compensation information in the MD&A have not been retrospectively restated to reflect the impact of the subdivision; such restatement would take place subsequent to the subdivision.

![]()

Consolidated highlights

Years ended December 31 ($ millions, except footnotes and unless noted otherwise) |

| 2019 |

| 2018 |

| Change |

|

Consolidated statements of income |

|

|

|

|

|

|

|

Revenues arising from contracts with customers |

| 14,589 |

| 14,095 |

| 3.5 | % |

Other operating income1 |

| 69 |

| 273 |

| (74.7 | )% |

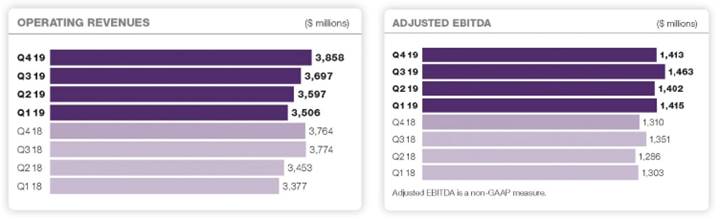

Operating revenues1 |

| 14,658 |

| 14,368 |

| 2.0 | % |

Operating income2 |

| 2,977 |

| 2,837 |

| 4.9 | % |

Income before income taxes2 |

| 2,244 |

| 2,176 |

| 3.1 | % |

Net income2 |

| 1,776 |

| 1,624 |

| 9.4 | % |

Net income attributable to Common Shares2 |

| 1,746 |

| 1,600 |

| 9.1 | % |

Adjusted Net income3 |

| 1,727 |

| 1,703 |

| 1.4 | % |

|

|

|

|

|

|

|

|

Earnings per share (EPS)4 ($) |

|

|

|

|

|

|

|

Basic EPS2 |

| 2.90 |

| 2.68 |

| 8.2 | % |

Adjusted basic EPS3 |

| 2.86 |

| 2.85 |

| 0.4 | % |

Diluted EPS |

| 2.90 |

| 2.68 |

| 8.2 | % |

Dividends declared per Common Share4 ($) |

| 2.2525 |

| 2.1000 |

| 7.3 | % |

|

|

|

|

|

|

|

|

Basic weighted-average Common Shares outstanding (millions) |

| 602 |

| 597 |

| 0.8 | % |

Consolidated statements of cash flows |

|

|

|

|

|

|

|

Cash provided by operating activities |

| 3,927 |

| 4,058 |

| (3.2 | )% |

|

|

|

|

|

|

|

|

Cash used by investing activities |

| (5,044 | ) | (2,977 | ) | 69.4 | % |

Acquisitions |

| (1,105 | ) | (280 | ) | n/m |

|

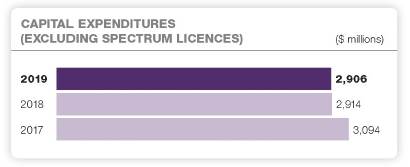

Capital expenditures5 |

| (2,906 | ) | (2,914 | ) | (0.3 | )% |

|

|

|

|

|

|

|

|

Cash provided (used) by financing activities |

| 1,238 |

| (1,176 | ) | n/m |

|

Other highlights |

|

|

|

|

|

|

|

Subscriber connections6,7 (thousands) |

| 15,166 |

| 13,947 |

| 8.7 | % |

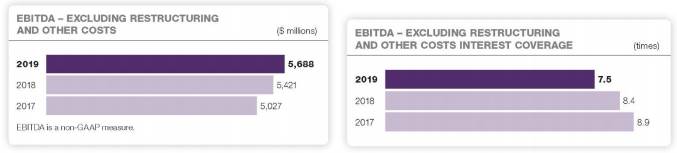

Earnings before interest, income taxes, depreciation and amortization (EBITDA)2,3 |

| 5,554 |

| 5,104 |

| 8.8 | % |

Restructuring and other costs3.8 |

| 134 |

| 317 |

| (57.7 | )% |

Adjusted EBITDA3,9 |

| 5,693 |

| 5,250 |

| 8.4 | % |

Adjusted EBITDA margin3,10 (%) |

| 38.8 |

| 37.0 |

| 1.8 | pts. |

Free cash flow3 |

| 932 |

| 1,207 |

| (22.8 | )% |

Net debt to EBITDA — excluding restructuring and other costs3 (times) |

| 3.20 |

| 2.54 |

| 0.66 |

|

Notations used in MD&A: n/m — not meaningful; pts. — percentage points.

(1) In the third quarter of 2018, we recorded equity income related to real estate joint ventures of $171 million arising from the sale of TELUS Garden. Excluding the effect of this third quarter 2018 equity income, Other operating income decreased by 32.4% in 2019, and Operating revenues increased by 3.2% in 2019.

(2) Excluding the third quarter 2018 equity income described in footnote 1 and the third quarter 2018 donation described in footnote 8, in 2019, Operating income increased by 6.9%, Income before income taxes increased by 5.7%, Net income increased by 13.6%, Net income attributable to Common Shares increased by 13.4%, basic EPS increased by 12.4% (pre-share split) and EBITDA increased by 10.0%.

(3) �� These are non-GAAP and other financial measures. See Section 11.1 Non-GAAP and other financial measures.

(4) Pre-share split — see Share split — subsequent to 2019 in Section 1.3.

(5) Capital expenditures include assets purchased, excluding right-of-use lease assets, but not yet paid for, and consequently differ from Cash payments for capital assets, excluding spectrum licences, as reported in the Consolidated financial statements. Refer to Note 31 of the Consolidated financial statements for further information.

(6) The sum of active mobile phone subscribers, mobile connected device subscribers, internet subscribers, residential voice subscribers, TV subscribers and security subscribers, measured at the end of the respective periods based on information in billing and other source systems. During the first quarter of 2019, we adjusted cumulative internet subscriber connections to add approximately 16,000 subscribers from acquisitions undertaken during the quarter. Effective for the third quarter of 2019, with retrospective application to the launch of TELUS-branded security services at the beginning of the third quarter of 2018, we have added security subscriber connections to our total subscriber connections. December 31, 2019 security subscriber connections have been increased to include approximately 490,000 subscribers related to our acquisition of ADT Canada (acquired on November 5, 2019).

(7) Effective for the first quarter of 2019, with retrospective application, we revised our definition of a wireless subscriber and now report mobile phones and mobile connected devices as separate subscriber bases so as to be consistent with the way we manage our business and to align with global peers. As a result of the change, total subscribers and associated operating statistics (gross additions, net additions, churn, average billing per subscriber per month or ABPU, and average revenue per subscriber per month or ARPU) were adjusted to reflect (i) the movement of certain subscribers from the mobile phones subscriber base to the newly created mobile connected devices subscriber base, and (ii) the inclusion of previously undisclosed IoT and mobile health subscribers in our mobile connected devices subscriber base. For additional information on our subscriber definitions, see Section 11.2 Operating indicators.

(8) In the third quarter of 2018, we recorded a donation to the TELUS Friendly Future Foundation™ of $118 million as part of other costs.

(9) Adjusted EBITDA for all periods excludes restructuring and other costs (see Section 11.1 for restructuring and other costs amounts). Adjusted EBITDA for all periods excludes non-recurring losses and equity losses (gains and equity income) related to real estate joint ventures.

(10) Adjusted EBITDA margin is Adjusted EBITDA divided by Operating revenues, where the calculation of Operating revenues excludes non-recurring gains and equity income related to real estate joint ventures.

![]()

Operating highlights

· Consolidated operating revenues increased by $290 million in 2019. Excluding the effect of the non-recurring third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million, consolidated operating revenues increased by $461 million in 2019:

Service revenues increased by $518 million in 2019, due to growth in wireless network revenue and wireline data services revenue. This growth was partly offset by the ongoing declines in wireline legacy voice and legacy data service revenues.

Equipment revenues decreased by $24 million in 2019, reflecting lower wireless contracted volumes and lower wireline data and voice equipment sales.

Other operating income decreased by $204 million in 2019, primarily due to the non-recurrence of third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million, in addition to the non-recurrence of gains on sale of certain assets in the fourth quarter of 2018.

For additional details on operating revenues, see Section 5.4 Wireless segment and Section 5.5 Wireline segment.

· During 2019, our total subscriber connections increased by 1,219,000, reflecting a 3.2% increase in mobile phone subscribers, a 21.6% increase in mobile connected device subscribers, a 6.6% increase in internet subscribers, a 6.1% increase in TV subscribers and an increase of 536,000 security subscribers, partly offset by a 3.5% decline in residential voice subscribers.

Effective for the first quarter of 2019, with retrospective application, we have revised our definition of a mobile phone subscriber. (See Section 11.2 Operating indicators for definitions.) Our mobile phone net additions were 274,000 in 2019, up 10,000 driven by growth in high-value customer additions, growth in the Canadian population, successful promotions and expanded channels, partly offset by higher mobile phone churn. Mobile connected device net additions were 263,000 in 2019, up 70,000 due to growth in our IoT offerings, including the connected device growth arising from our subscribers expanding their IoT services to their growing customer bases, partially offset by reduced loading of low or negative-margin tablets. Our mobile phone churn rate was 1.08% in 2019, up slightly from 1.06% in 2018, reflecting heightened competitive intensity. (See Section 5.4 Wireless segment for additional details.)

Internet net additions were 107,000 in 2019, down 8,000, as continued net new demand from consumers and businesses was offset by increased deactivations resulting from heightened competitive intensity. TV net additions were 67,000 in 2019, up 4,000, in contrast with market-reported declines in traditional television viewing habits, reflecting higher gross additions as a result of our diverse product offerings, partly offset by heightened competitive intensity. Our continued focus on expanding our addressable high-speed internet and Optik TV® footprint, connecting more homes and businesses directly to fibre, diversifying our product offerings, and bundling these products and services together, as well as our ongoing focus on our customer service and reliability, contributed to combined internet and TV subscriber growth of 190,000 or 6.4% over the last 12 months. We had made TELUS PureFibre® available to approximately 70% of our broadband footprint by the end of 2019. Residential voice net losses improved by 13.7% in 2019 due to our expanding fibre footprint and bundled product offerings and the success of our stronger retention efforts, including lower-priced offerings. Excluding the effects of ADT Canada, security net additions were 46,000, reflecting strong organic growth. (See Section 5.5 Wireline segment for additional details.)

· Operating income increased by $140 million in 2019. Excluding the effects of the third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million and the non-recurring third quarter 2018 donation to the TELUS Friendly Future Foundation of $118 million, Operating income increased by $193 million in 2019, reflecting higher wireless network growth driven by a growing subscriber base, in addition to growth in wireline data service margins and a higher EBITDA contribution from our customer care and business services (CCBS) and health businesses, and the effects of implementing IFRS 16 described in Section 1.1. All of these factors were partly offset by declines in wireline legacy voice and legacy data services, as well as lower gains on sales of certain assets.

EBITDA, which includes restructuring and other costs and non-recurring losses and equity losses (or gains and equity income) related to real estate joint ventures, increased by $450 million or 8.8% in 2019. Excluding the effects of the third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million and the third quarter 2018 donation to the TELUS Friendly Future Foundation of $118 million, EBITDA increased by $503 million or 10.0% in 2019. The impact of IFRS 16 on EBITDA was an increase of $301 million in 2019.

![]()

Adjusted EBITDA, which excludes restructuring and other costs and non-recurring losses and equity losses (or gains and equity income) related to real estate joint ventures, increased by $443 million or 8.4% in 2019, reflecting higher wireless network revenue driven by a growing subscriber base, growth in wireline data service margins and a higher EBITDA contribution from our CCBS and health businesses. Additionally, upon the application of IFRS 16, Goods and services purchased decreased and, correspondingly, Adjusted EBITDA increased. These factors were partly offset by declines in wireline legacy voice and legacy data services and a decline in the EBITDA contribution from our legacy business services. Applying a retrospective IFRS 16 simulation to fiscal 2018 results, which are cash-based proxy adjustments, all as used by our Chief Executive Officer (our chief operating decision-maker) to assess performance, pro forma consolidated Adjusted EBITDA growth was approximately 4.0% in 2019. (See Section 5.3 Consolidated operations for additional details.)

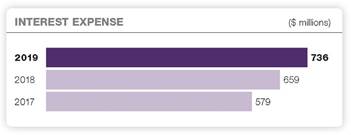

· Income before income taxes increased by $68 million in 2019. Excluding the effects of the third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million and the third quarter 2018 donation to the TELUS Friendly Future Foundation of $118 million, Income before income taxes increased by $121 million in 2019. Higher Operating income, as noted above, was partly offset by an increase in Financing costs. The increase in Financing costs resulted primarily from the financing costs recorded that arose from lease liabilities upon the application of IFRS 16 (described in Section 1.1) and from higher average long-term debt outstanding. (See Financing costs in Section 5.3.)

· Income taxes decreased by $84 million in 2019. The effective tax rate decreased from 25.4% to 20.8% predominantly attributable to the revaluation of the deferred income tax liability for the multi-year reduction in the Alberta provincial corporate tax rate that was substantively enacted in the second quarter of 2019.

· Net income attributable to Common Shares increased by $146 million in 2019. Excluding the effects of the third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million and the third quarter 2018 donation to the TELUS Friendly Future Foundation of $118 million, Net income attributable to Common Shares increased by $206 million, driven by higher Operating income and lower Income taxes, partly offset by increased Financing costs.

Adjusted Net income, which excludes the effects of restructuring and other costs, income tax-related adjustments, non-recurring losses and equity losses (or gains and equity income) related to real estate joint ventures, and long-term debt prepayment premiums, increased by $24 million or 1.4% in 2019.

Reconciliation of adjusted Net income

Years ended December 31 ($ millions) |

| 2019 |

| 2018 |

| Change |

|

Net income attributable to Common Shares |

| 1,746 |

| 1,600 |

| 146 |

|

Add (deduct): |

|

|

|

|

|

|

|

Restructuring and other costs, after income taxes1 |

| 98 |

| 235 |

| (137 | ) |

Favourable income tax-related adjustments |

| (142 | ) | (7 | ) | (135 | ) |

Non-recurring losses and equity losses (gains and equity income) related to real estate joint ventures, after income taxes2 |

| 5 |

| (150 | ) | 155 |

|

Long-term debt prepayment premium, after income taxes |

| 20 |

| 25 |

| (5 | ) |

Adjusted Net income |

| 1,727 |

| 1,703 |

| 24 |

|

(1) Includes our third quarter 2018 committed donation to the TELUS Friendly Future Foundation of $90 million after income taxes.

(2) Includes equity income arising from the third quarter 2018 sale of TELUS Garden of $150 million after income taxes.

· Basic EPS increased by $0.22 or 8.2% (pre-share split — see Share split — subsequent to 2019 in Section 1.3) in 2019. Excluding the effects of the third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million and the third quarter 2018 donation to the TELUS Friendly Future Foundation of $118 million, basic EPS increased by $0.32 or 12.4% (pre-share split), driven by higher Operating income and lower Income taxes, partly offset by increased Financing costs and the effect of a higher number of Common Shares outstanding.

Adjusted basic EPS, which excludes the effects of restructuring and other costs, income tax-related adjustments, non-recurring gains and equity income related to real estate joint ventures, and long-term debt prepayment premiums, increased by $0.01 or 0.4% (pre-share split) in 2019.

![]()

Reconciliation of adjusted basic EPS1

Years ended December 31 ($) |

| 2019 |

| 2018 |

| Change |

|

Basic EPS |

| 2.90 |

| 2.68 |

| 0.22 |

|

Add (deduct): |

|

|

|

|

|

|

|

Restructuring and other costs, after income taxes, per share2 |

| 0.16 |

| 0.39 |

| (0.23 | ) |

Favourable income-tax related adjustments, per share |

| (0.24 | ) | (0.01 | ) | (0.23 | ) |

Non-recurring losses and equity losses (gains and equity income) related to real estate joint ventures, after income taxes3 |

| 0.01 |

| (0.25 | ) | 0.26 |

|

Long-term debt prepayment premium, after income taxes, per share |

| 0.03 |

| 0.04 |

| (0.01 | ) |

Adjusted basic EPS |

| 2.86 |

| 2.85 |

| 0.01 |

|

(1) Pre-share split — see Share split — subsequent to 2019 in Section 1.3.

(2) Includes our third quarter 2018 committed donation to the TELUS Friendly Future Foundation of $0.15 per share after income taxes (pre-share split).

(3) Includes equity income arising from the third quarter 2018 sale of TELUS Garden of $0.25 per share after income taxes (pre share split).

· Dividends declared per Common Share were $2.2525 (pre-share split — see Share split — subsequent to 2019 in Section 1.3) in 2019, up 7.3% from 2018. Consistent with our target of increasing dividends between 7 to 10% in the near term, the Board declared a first quarter dividend of $0.5825 per share (pre-share split) on our issued and outstanding Common Shares, payable on April 1, 2020, to shareholders of record at the close of business on March 11, 2020. The first quarter dividend increased by $0.0375 per share (pre-share split) or 6.9% from the $0.5450 (pre-share split) per share dividend declared one year earlier, consistent with our multi-year dividend growth program described in Section 4.3 Liquidity and capital resources.

Liquidity and capital resource highlights

· Net debt to EBITDA — excluding restructuring and other costs ratio was 3.20 times at December 31, 2019, up from 2.54 times at December 31, 2018, as the increase in net debt, partly attributed to the acquisition of spectrum licences, and which includes the $1.7 billion recognition of lease liabilities upon the application of IFRS 16, exceeded the effect of the increase in EBITDA — excluding restructuring and other costs. As at December 31, 2019, the acquisition of spectrum licences increased the ratio by approximately 0.22; business acquisitions over the last 12 months increased the ratio by approximately 0.18; and the implementation of IFRS 16 had the effect of increasing the ratio by approximately 0.14. (See Section 4.3 Liquidity and capital resources and Section 7.5 Liquidity and capital resource measures.)

· Cash provided by operating activities decreased by $131 million in 2019, largely attributable to increased income tax payments, which mainly reflected a higher final income tax payment of $270 million in the first quarter of 2019 for the 2018 income tax year; other operating working capital changes; higher restructuring and other costs disbursements, net of expense and Shares settled from Treasury; and increased interest paid. All of these were partially offset by growth in EBITDA. Additionally, repayments of lease liabilities under IFRS 16 increased Cash provided by operating activities by $236 million in 2019, as described in Section 7.2 Cash provided by operating activities.

· Cash used by investing activities increased by $2,067 million in 2019, largely attributable to acquisitions and the cash payment for the 600 MHz spectrum acquisition of $931 million. Acquisitions increased by $825 million in 2019 as we made larger cash payments for business acquisitions including ADT Canada on November 5, 2019. Capital expenditures decreased by $8 million in 2019, primarily due to the timing of our fibre build activities, partially offset by increased 5G investments, which began in the fourth quarter of 2018. We had made TELUS PureFibre available to approximately 70% of our broadband footprint by December 31, 2019. (See Section 7.3 Cash used by investing activities.)

· Cash provided by financing activities increased by $2,414 million in 2019, primarily reflecting increased issues of long-term debt, net of redemptions and repayment. (See Section 7.4 Cash provided (used) by financing activities.)

· Free cash flow decreased by $275 million in 2019, resulting primarily from increased income tax payments, which mainly reflected a higher final income tax payment of $270 million in the first quarter of 2019 for the 2018 income tax year, as described in Cash provided by operating activities, and increased interest paid. The free cash flow decrease in 2019 was partly offset by higher Adjusted EBITDA, the timing related to device subsidy repayments and associated revenue recognition and our TELUS Easy Payment device financing program, and lower capital expenditures. Our definition of free cash flow, for which there is no industry alignment, is unaffected by accounting changes that do not impact cash, such as IFRS 15 and IFRS 16. (See calculation in Section 11.1 Non-GAAP and other financial measures.)

![]()

1.4 Performance scorecard (key performance measures)

In 2019, we achieved three of four consolidated targets, which were announced on February 14, 2019.

We achieved our consolidated revenue target, primarily due to growth in wireless network revenue resulting from growth in our wireless subscriber base. Additionally, we experienced increased wireline data service revenues resulting from growth in CCBS business volumes, increased internet and third-wave data services, increased health revenues inclusive of acquisitions, increased home and business smart technology (including security) revenues, and increased TV revenues, partly offset by the ongoing decline in legacy wireline voice revenue.

We met our Adjusted EBITDA target largely from higher wireless network revenue growth driven by a growing customer base, in addition to growth in EBITDA contribution from our CCBS and health business. These factors were partly offset by declines in wireline legacy voice and legacy data services and a decline in EBITDA contribution from our legacy business services. Although we experienced an increase in Adjusted EBITDA due to the adoption of IFRS 16 on January 1, 2019, our 2019 Adjusted EBITDA target incorporated the effects of the new accounting standard.

Our basic EPS fell within our target range, driven by higher Operating income and lower income taxes, partly offset by increased Financing costs.

Our capital expenditures in 2019 exceeded our consolidated target by 2.0%, as we advanced the timing of certain investments in our broadband infrastructure and made incremental capital expenditures related to our various business acquisitions in 2019. Our investments in broadband infrastructure, including connecting more homes and businesses directly to our fibre-optic infrastructure, resulted in TELUS PureFibre reaching approximately 70% of our broadband footprint at year-end. These investments also support our systems reliability and operational efficiency and effectiveness efforts, as well as our small-cell technology strategy to improve coverage and prepare for a more efficient and timely evolution to 5G.

Our capital structure financial policies and report on financing and capital structure management plans are included in Section 4.3.

The following scorecard compares TELUS’ performance to our consolidated 2019 targets. For information related to our 2019 targets, see Section 9 General trends, outlook and assumptions, and regulatory developments and proceedings.

Scorecard

|

| 2019 performance | ||||

|

| Consolidated targets and growth |

| Actual results |

| Result |

Consolidated |

|

|

|

|

|

|

Revenues1 |

| An increase of |

| $14.66 billion |

| Ö |

Adjusted EBITDA2 |

| An increase of |

| $5.69 billion |

| Ö |

Basic EPS4 |

| An increase of |

| $2.90 |

| Ö |

Capital expenditures (excluding spectrum licences) |

| Approx. $2.85 billion |

| $2.91 billion |

| X |

Met target Ö

Missed target X

(1) The 2019 revenue target and actual results were calculated using operating revenues, excluding the non-recurring third quarter 2018 equity income related to real estate joint ventures arising from the sale of TELUS Garden of $171 million.

(2) See description in Section 11.1 Non-GAAP and other financial measures.

(3) The 2019 Adjusted EBITDA target reflected the non-cash impacting implementation of IFRS 16, Leases on January 1, 2019.

(4) Pre-share split — see Share split — subsequent to 2019 in Section 1.3.

![]()

We made the following key assumptions when we announced the 2019 targets in February 2019.

Assumptions for 2019 targets and results

· Our economic assumptions are based on a composite of estimates from Canadian banks and other sources. Our original assumptions for 2019 were: (i) slightly slower rate of economic growth in Canada of 2.0%; (ii) for our incumbent local exchange carrier (ILEC) provinces in Western Canada, economic growth in B.C. of 2.3%, and economic growth in Alberta of 2.1%.

In our first quarter 2019 MD&A, we revised our 2019 economic growth assumptions to 1.5% in Canada and 1.2% in Alberta. In our third quarter 2019 MD&A, we further revised our 2019 economic growth assumptions for 1.6% in Canada, 1.9% in B.C. and 0.7% in Alberta.

We estimate that economic growth in 2019 was 1.6% in Canada, 1.9% in B.C. and 0.7% in Alberta.

· With respect to unemployment rates, our original assumptions for 2019 were 5.8% in Canada, 4.9% in B.C. and 6.2% in Alberta.

In our first quarter 2019 MD&A, we revised our 2019 unemployment rate assumptions to 4.5% in B.C. and 6.8% in Alberta. In our third quarter 2019 MD&A, we further revised our 2019 unemployment rate assumptions to 5.7% in Canada and 4.6% in B.C.

We estimate that unemployment rates in 2019 were 5.7% in Canada, 4.6% in B.C. and 6.8% in Alberta.

· With respect to the pace of housing starts, on an unadjusted basis, our original assumption for 2019 was 196,000 units in Canada.

In our third quarter 2019 MD&A, on an unadjusted basis, we revised our 2019 assumption for the pace of housing starts to 207,000 in Canada.

We estimate that the annual rate of housing starts on an unadjusted basis for 2019 was 207,000 units.

· Our assumption for 2019 restructuring and other costs was approximately $100 million. Our actual 2019 restructuring and other costs was $134 million, as we incurred costs for continuing operational effectiveness initiatives, with margin enhancement initiatives to mitigate pressures related to intense competition, technological substitution, repricing of our services, increasing subscriber growth and retention costs, and integration costs associated with business acquisitions.

· Our assumption was for stabilization in the average Canadian dollar: U.S. dollar exchange rate, which was $1.30 in 2018. The average Canadian dollar: U.S. dollar exchange rate was $1.33 in 2019 and closed at $1.30 on December 31, 2019, compared to $1.36 on December 31, 2018.

Confirmed:

· No material adverse regulatory rulings or government actions. See Section 9.4 for further information.

· Continued intense wireless and wireline competition in both consumer and business markets.

· Continued increase in wireless industry penetration of the Canadian market.

· Ongoing subscriber adoption of, and upgrades to, data-intensive smartphones, as customers seek more mobile connectivity to the internet.

· Wireless revenue growth resulting from improvements in subscriber loading, with continued competitive pressure on blended ARPU.

· Continued pressure on wireless acquisition and retention expenses, dependent on gross loading and customer renewal volumes, competitive intensity and customer preferences.

· Continued growth in wireline data revenue, reflecting an increase in internet and TV subscribers, speed upgrades, rate plans with larger data usage and expansion of our broadband infrastructure, as well as growth in CCBS, healthcare solutions and home and business security offerings.

· Continued erosion of wireline voice revenues, resulting from technological substitution and greater use of inclusive long distance.

· Continued focus on our customers first initiatives and maintaining our customers’ likelihood-to-recommend.

· Pension plans assumptions for 2019: defined benefit pension plan expense of approximately $79 million recorded in Employee benefits expense; a rate of 3.90% for discounting the obligation (2018 — 3.90%) and a rate of 4.00% for current service costs for employee defined benefit pension plan accounting purposes (2018 — 3.50%); and defined benefit pension plan funding of approximately $52 million. Actual results were: $78 million recorded in Employee benefits expense, a rate of 3.90% for discounting the obligation, a rate of 3.90% for current service costs for employee defined benefit pension plan accounting purposes, and defined benefit pension plan funding of $41 million.

· Our assumption for 2019 income taxes was computed at a statutory rate of 26.7 to 27.3%, and cash income tax payments of approximately $600 million to $680 million. Our actual results were at a statutory income tax rate of 26.9% and cash income tax payments in respect of comprehensive income were $629 million.

· Further investments in broadband infrastructure, as we have reached approximately 70% of our broadband footprint at December 31, 2019, including fibre-optic network expansion and 4G LTE capacity and upgrades, as well as investments in network and systems resiliency and reliability.

· Participation in ISED’s 600 MHz wireless spectrum auction in March to April 2019. We acquired 12 wireless spectrum licences in B.C., Alberta, Saskatchewan, Ontario and Quebec which equate to a national average of 11.3 MHz.

· Continued deployment of access-agnostic technology in our network.

![]()

2. Core business and strategy

2.1 Core business

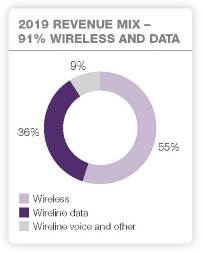

We provide a wide range of telecommunications products and services. Wireless products and services include network revenue (data and voice) and equipment sales arising from mobile technologies. Wireline products and services include data revenues (which include revenues from internet protocol; television; hosting, managed information technology and cloud-based services; customer care and business services (CCBS) (formerly business process outsourcing); home and business smart technology (including security); and certain healthcare solutions), voice revenues, and other telecommunications services and equipment revenues. We currently earn the majority of our revenue from access to, and usage of, our telecommunications infrastructure, and from providing services and products that facilitate access to, and usage of, our infrastructure.

2.2 Strategic imperatives

Since 2000, we have maintained a proven national growth strategy. Our strategic intent is to unleash the power of the internet to deliver the best solutions to Canadians at home, in the workplace and on the move.

We also developed six strategic imperatives in 2000 that remain relevant for future growth, despite changing regulatory, technological and competitive environments. We believe that a consistent focus on these imperatives guides our actions and contributes to the achievement of our financial goals. To advance these long-term strategic imperatives and address near-term opportunities and challenges, we confirm or set new corporate priorities each year, as further described in Section 3. Our six strategic imperatives are listed below.

· Focusing relentlessly on growth markets of data, IP and wireless

· Providing integrated solutions that differentiate TELUS from our competitors

· Building national capabilities across data, IP, voice and wireless

· Partnering, acquiring and divesting to accelerate the implementation of our strategy and focus our resources on core business

· Going to market as one team under a common brand, executing a single strategy

· Investing in internal capabilities to build a high-performance culture and efficient operation.

![]()

3. Corporate priorities

We confirm or set new corporate priorities each year in order to advance our long-term strategic imperatives (see Section 2.2) and address near-term opportunities and challenges. The following table provides a discussion of activities and initiatives that relate to our 2019 corporate priorities.

Honouring our customers, communities and social purpose by our team delivering on our brand promise

· Each year, we conduct team member Pulsecheck engagement surveys to gather confidential team member feedback about TELUS as a place to work in order to measure our progress in creating a high-performance culture. Following each survey, leaders share results with team members and use fair process to build and refine action plans focused on high-priority areas where improvement is required based on Pulsecheck results. In 2019, our employee engagement score was 84%, which is an encouraging accomplishment against a backdrop of change across our organization over the course of the past year. This result continues to place our Company within the top 10% of all employers surveyed on a global basis.

· In November 2019, the Commission for Complaints for Telecom-television Services (CCTS) issued its annual report for the 12-month period ended July 31, 2019, and TELUS again was the subject of the fewest customer complaints among national carriers, while Koodo® again was the subject of the fewest complaints among the national flanker brands. TELUS, Koodo and Public Mobile were named in 8.3%, 3.9% and 1.0% of the total customer complaints accepted by the CCTS, respectively, or 13.2% of total customer complaints, in aggregate. Additionally, TELUS had the highest rate of complaint resolution of any national carrier at 91.5%.

· We were named one of Canada’s Top 100 Employers (2020) by Mediacorp Canada Inc.

· Throughout 2019, we continued to expand our Connecting for Good™ program portfolio to build stronger, more resilient communities.

· We expanded our Mobility for Good™ program to support 10,000 more youth in B.C., Alberta, Manitoba and New Brunswick. Mobility for Good provides youth transitioning out of foster care with fully subsidized smartphones and data plans to stay connected to their vital support networks.

· Through our Internet for Good™ program and in support of the federal government’s Connecting Families program, an additional 198,000 Internet for Good offers were mailed to eligible households in B.C., Alberta and Quebec. Internet for Good offers low-income families access to low-cost high-speed internet and a computer.

· We piloted our Welcome to Canada initiative, which offers our Internet and Mobility for Good programs to government-assisted refugees arriving in B.C. TELUS provides refurbished phones, wireless plans and internet service to enable refugees to stay in touch with family abroad and access support networks and employment opportunities in Canada. The program aims to ensure a warmer welcome and smoother transition, enabling better outcomes for newcomers to Canada.

· We expanded our Health for Good™ program by establishing seven new strategic partnerships to deploy new mobile health clinics. Our Health for Good program funds TELUS Mobile Health Clinics, powered by TELUS Health technology, to improve the way health practitioners deliver care to the most vulnerable among us.

· We introduced our Tech for Good™ program to help Canadians with disabilities use smartphones and wireless devices so they can live more independent, connected lives. Currently available in B.C. and Alberta, this program is designed to help people with disabilities who require a customized solution involving assistive technology to independently access their TELUS smartphone or tablet.

· At the end of 2019, close to 65,000 Canadians had participated in our Connecting for Good programs.