UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant¨ Filed by a Party other than the Registrantx

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

Tandy Brands Accessories, Inc.

(Name of Registrant as Specified In Its Charter)

Golconda Capital Portfolio, LP

Golconda Capital Management, LLC

William D. Summitt

Jedd M. Fowers

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Mr. Summitt provided the attached slide presentation to certain corporate governance organizations today and may use it to make presentations to these organizations and Tandy Brands Accessories, Inc. stockholders on a going forward basis.

SECURITY HOLDERS ARE ADVISED TO READ THE DEFINITIVE PROXY STATEMENT RELATED TO THE SOLICITATION OF PROXIES BY GOLCONDA CAPITAL PORTFOLIO, LP FROM THE STOCKHOLDERS OF TANDY BRANDS ACCESSORIES, INC. (“TANDY”) FOR USE AT TANDY’S ANNUAL MEETING BECAUSE IT CONTAINS IMPORTANT INFORMATION, INCLUDING INFORMATION RELATING TO THE PARTICIPANTS IN SUCH PROXY SOLICITATION. THE DEFINITIVE PROXY STATEMENT AND A FORM OF PROXY ARE AVAILABLE AT NO CHARGE AT THE SECURITIES AND EXCHANGE COMMISSION’S WEBSITE ATHTTP://WWW.SEC.GOV

Golconda Capital Portfolio, LP Shareholder Advocacy and Proxy Contest at Tandy Brands Accessories, Inc. October 11, 2007 wsummitt@golcondalp.com | www.tandybrandsvalue.com |

Golconda Capital Portfolio, LP • page 2 What We Are Trying to Accomplish at Tandy Brands What We Are Trying to Accomplish at Tandy Brands • A greater sense of responsiveness to stockholders • A greater sense of urgency regarding Tandy Brands’ poor financial performance and languishing stock price • Institute a share repurchase program • Management accountability for performance • An emphasis on returns on invested capital • Explore strategic opportunities – First and foremost: Is a sale of the Company the best option for maximizing the value of Tandy Brands? |

Golconda Capital Portfolio, LP • page 3 Who We Are Who We Are • Golconda is a small, private investment partnership • We take a long-term, fundamental approach to investing • Golconda is not an activist fund – We did not go out looking for a “target” • But if we think we can contribute in a productive way we will step up as we have done at Tandy Brands |

Golconda Capital Portfolio, LP • page 4 Why We’re Waging a Proxy Contest Why We’re Waging a Proxy Contest • In 2005 we took a hard look at our investment in Tandy Brands – We felt that we could contribute to the discussion of various value maximizing alternatives • We began to advocate for specific initiatives taking our case to the Board, management and fellow stockholders – We met resistance from the Tandy Brands Board and management – We perceived support among the stockholders • We continued to advocate in incremental steps – We tried to avoid a costly proxy contest • Unfortunately, the Tandy Brands Board continued to resist our advocacy efforts until there was only one step left – a proxy contest |

Golconda Capital Portfolio, LP • page 5 Our History at Tandy Brands Our History at Tandy Brands • Bill Summitt has been a Tandy Brands shareholder since 2000 • Attended annual meetings and corresponded with the Company over the years • Made various suggestions from time to time but remained a passive investor • In 2005, we began to advocate for specific initiatives more strongly • We perceived that many stockholders were responding favorably to our advocacy efforts – However, the Board and management seemed unresponsive to stockholder concerns • The “tipping point” was the Board’s rejection of our stockholder proposal to eliminate the poison pill which passed with a 73% stockholder vote |

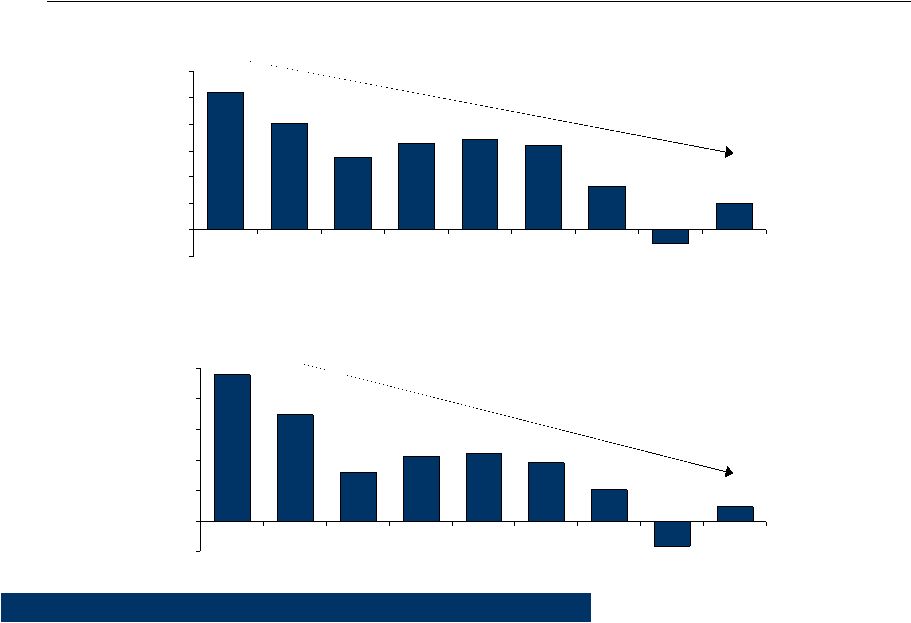

Golconda Capital Portfolio, LP • page 6 Tandy Brands’ Tandy Brands’ Operating Margins and Returns on Equity Have Been Operating Margins and Returns on Equity Have Been Declining For Several Years . . . Declining For Several Years . . . *Based on information provided by Tandy Brands in public filings with the Securities & Exchange Commission (SEC). Tandy Brands Operating Margins* 10.4% 8.0% 5.5% 6.5% 6.8% 6.4% 3.3% 2.0% -1.1% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 1999 2000 2001 2002 2003 2004 2005 2006 2007 Tandy Brands Return on Beginning Equity* 19.1% 13.9% 6.4% 8.5% 8.8% 7.7% 4.0% 1.8% -3.3% -4.0% 0.0% 4.0% 8.0% 12.0% 16.0% 20.0% 1999 2000 2001 2002 2003 2004 2005 2006 2007 |

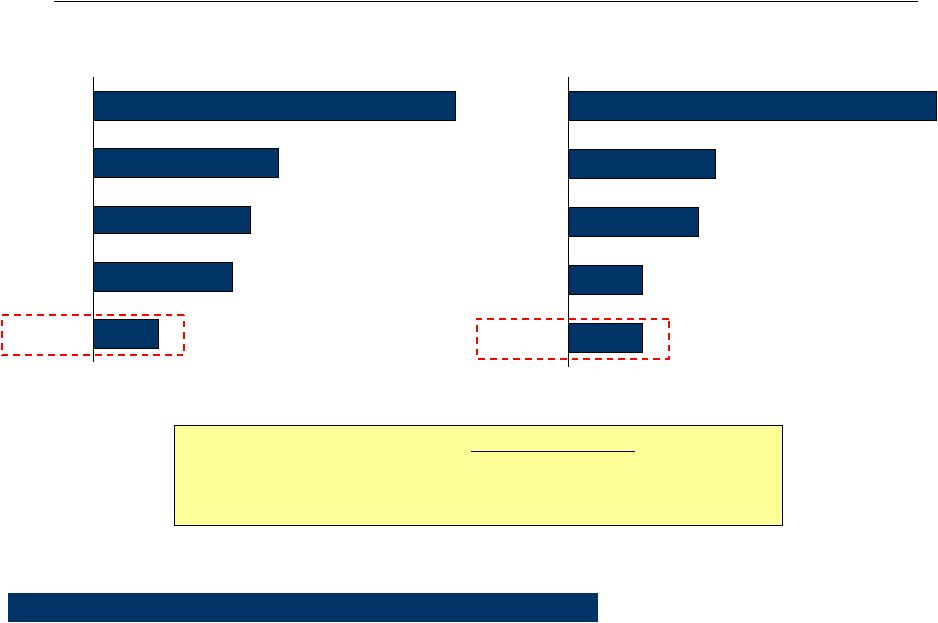

Golconda Capital Portfolio, LP • page 7 0.4 0.4 0.7 0.8 2 Tandy Brands Swank Liz Claiborne Kenneth Cole Fossil . . . And Tandy Brands’ . . . And Tandy Brands’ Valuation Ratios Fall At The Bottom End of Its Valuation Ratios Fall At The Bottom End of Its Peer Group Peer Group Tandy Brands stock is trading below book value, which causes us to believe that investors share our doubts about the Company’s ability to generate sufficient returns on invested capital if Tandy Brands continues along the same course *Data Source: Morningstar, September 28, 2007. Peer group includes publicly-traded companies listed as competitors in Tandy Brands’ 2007 10-K filing with the SEC. Price/Book* Price/Sales* 0.7 1.5 1.7 2 3.9 Tandy Brands Kenneth Cole Liz Claiborne Swank Fossil |

Golconda Capital Portfolio, LP • page 8 Over Three- Over Three- and Five-Year Periods, Tandy Brands’ and Five-Year Periods, Tandy Brands’ Total Returns Have Total Returns Have Significantly Trailed Those of Its Peer Group and the Broader Market Significantly Trailed Those of Its Peer Group and the Broader Market Over three years, Tandy Brands has underperformed the S&P Apparel, Accessories, and Luxury Goods index by a cumulative 64.9 percentage points Over five years, Tandy Brands has underperformed the S&P Apparel, Accessories, and Luxury Goods index by a cumulative 49.3 percentage points *Data provided by Bespoke Investment Group, LLC. Values are total returns, including reinvestment of dividends. Period ending August 31, 2007. |

Golconda Capital Portfolio, LP • page 9 Over a Ten-Year Over a Ten-Year Horizon, Tandy Brands’ Horizon, Tandy Brands’ Total Returns Have Significantly Total Returns Have Significantly Trailed Those Of Its Peer Group & the Broader Market Trailed Those Of Its Peer Group & the Broader Market Over ten years, Tandy Brands has underperformed the S&P Apparel, Accessories, and Luxury Goods index by a cumulative 85.4 percentage points! A $100 investment in Tandy Brands would have declined in value to $88.30 over the decade ending August 31, 2007. This represents a negative 1.24 percent compounded annual return over 10 years. *Data provided by Bespoke Investment Group, LLC. Values are total returns, including reinvestment of dividends. Period ending August 31, 2007. |

Golconda Capital Portfolio, LP • page 10 Golconda’s Influence to Date at Tandy Brands Golconda’s Influence to Date at Tandy Brands • Tandy Brands has taken several steps in recent months that Golconda has been advocating for, including: – Acceleration of the expiration of the poison pill and adoption of a policy to put future pills to a vote of stockholders – Declassification of the Board – Exploration of Strategic Alternatives • We believe that the following timelines detailing these and other initiatives should cause stockholders to ask: – Did Golconda create a greater sense of urgency for action? – Did the Tandy Brands Board feel forced to act on our corporate governance and strategic alternatives recommendations because of the increasing possibility of a proxy contest? |

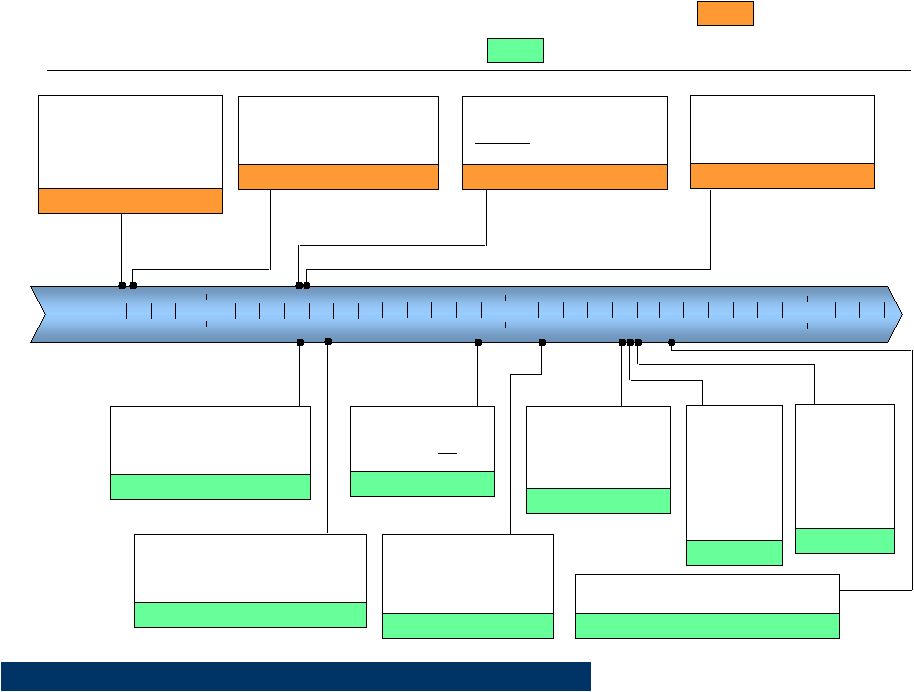

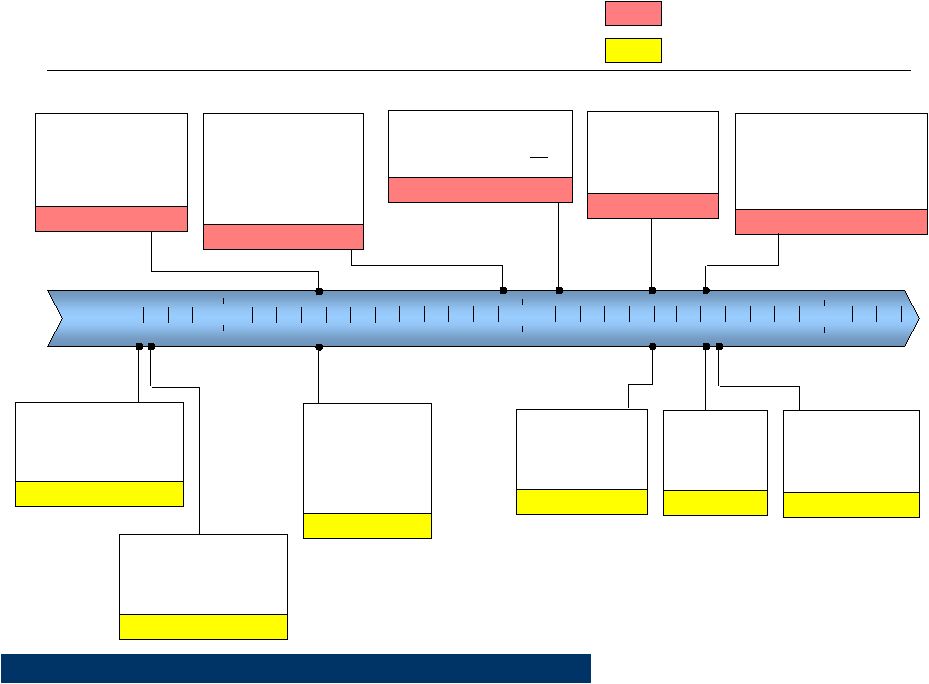

Golconda Capital Portfolio, LP • page 11 Timelines: Timelines: Eliminate Unprofitable Product Lines Eliminate Unprofitable Product Lines Eliminate Poison Pill Eliminate Poison Pill Sep 2005 2006 2007 2008 Golconda sends letter to Tandy Brands Board with recommendations, including elimination of underperforming product lines in women’s segment September 28, 2005 Mr. Summitt meets with Tandy Brands management and directors to discuss this recommendation and others Early October, 2005 In a letter to the full Board of Directors, Golconda recommends aggressive action be taken in the women’s segment April 24, 2006 Company announces it is eliminating several underperforming product lines in the women’s segment April 26, 2006 Golconda sends letter to Tandy Brands Board in which it recommends that the Company eliminate its poison pill April 24, 2006 Golconda submits non-binding shareholder proposal to eliminate poison pill and put future poison pills to a shareholder vote May 22, 2006 Golconda’s shareholder proposal passes with 73% of shareholder votes October 31, 2006 Despite strong shareholder mandate, Company informs Golconda that it has no intention of eliminating poison pill February 9, 2007 Tandy Brands changes course and announces plans to accelerate the poison pill expiration date May 16, 2007 Golconda submits non- binding shareholder proposal to put future poison pills to a shareholder vote May 18, 2007 Board of Directors announces policy to put future poison pills to a shareholder vote July 12, 2007 Golconda nominates two candidates for election to the Tandy Brands Board of Directors May 31, 2007 |

Golconda Capital Portfolio, LP • page 12 Timelines: Timelines: Declassify Board of Directors Declassify Board of Directors Explore Strategic Alternatives Explore Strategic Alternatives Sep 2005 2006 2007 2008 Golconda sends letter to Tandy Brands Board in which Golconda recommends declassification of board of directors April 24, 2006 Golconda sends second letter to Tandy Brands Board in which it reemphasizes the importance of declassifying the Board of Directors December 6, 2006 Tandy Brands Chairman sends letter to Golconda indicating that the Board would not eliminate its staggered board February 9, 2007 The same day Golconda publicly announces its intent to launch a proxy contest, the Company again changes course and announces plans to declassify its Board of Directors August 8, 2007 Golconda nominates two candidates for election to the Tandy Brands Board of Directors May 31, 2007 Golconda sends letter in which it recommends Tandy Brands consider a possible sale of the Company September 28, 2005 Mr. Summitt meets with Tandy Brands management and directors to discuss this recommendation and others Early October, 2005 Golconda sends second letter to the Tandy Brands Board in which it recommends that the Board consider a sale of Company April 24, 2006 Golconda publishes its intent to launch a proxy contest August 8, 2007 Tandy Brands announces it has hired an investment bank to evaluate strategic alternatives August 22, 2007 Golconda nominates two candidates for election to the Tandy Brands Board of Directors May 31, 2007 |

Golconda Capital Portfolio, LP • page 13 Are the Incumbents Committed to Strong Corporate Governance Are the Incumbents Committed to Strong Corporate Governance Principles? Board Declassification Example: Principles? Board Declassification Example: This doesn’t sound to us like the action of a Board “committed to strong corporate governance” but rather it sounds like a Board reacting to the increasing likelihood that Golconda would launch a proxy contest. In a notice to shareholders dated August 8, 2007—just six months later—the Board of Directors reversed course: In a February 9, 2007 letter, the Tandy Brands Chairman explicitly rejected Golconda’s recommendation to declassify the Board of Directors: February 9, 2007 “…giving particular weight to the fact that having a staggered Board is expressly permitted by Delaware law, the Board has concluded not to eliminate its staggered board.” August 8, 2007 “…your Board of Directors is committed to strong corporate governance principles, as demonstrated by the Company’s proposal to de-classify the Board of Directors…” HOWEVER… |

Golconda Capital Portfolio, LP • page 14 The Board’s Declassification Proposal Leaves Something to Be Desired The Board’s Declassification Proposal Leaves Something to Be Desired • Declassification doesn’t begin until 2008 • The declassification will be phased in • This is a phased in declassification with a one year lag • If a declassified board is good corporate governance, why not have the entire Board stand for election in 2008? • We had advocated for a full and swift declassification but the Board opted for a delayed and phased declassification |

Golconda Capital Portfolio, LP • page 15 What Objections Might the Company Have to the Golconda Nominees? What Objections Might the Company Have to the Golconda Nominees? • They might say: “The Golconda nominees have no industry experience” – We don’t plan to run the Company - that’s management’s job – We have the experience and knowledge necessary to represent the interests of Tandy Brands stockholders • Mr. Summitt has over nine years of investment management experience • Mr. Fowers has over 11 years of corporate experience in multiple business disciplines – The Tandy Brands Board has had plenty of industry experience on the board over the past decade • But that experience has not resulted in acceptable financial results • And that experience has not kept the stock price from declining and languishing at a low valuation – We will be owner-directors with a perspective that is closely aligned with outside stockholders |

Golconda Capital Portfolio, LP • page 16 What Objections Might the Company Have to the Golconda Nominees? What Objections Might the Company Have to the Golconda Nominees? • They might say: “The Golconda Nominees will be replacing two valuable incumbent Board members” – The incumbent board is lacking in the owner-director perspective that the Golconda Nominees will add – We tried to avoid an outright proxy contest – The Tandy Brands Board can be expanded to nine members – We urged the Company to expand the Board to accommodate the Golconda Nominees without losing any incumbent directors • The Board rejected this option |

Golconda Capital Portfolio, LP • page 17 What Objections Might the Company Have to the Golconda Nominees What Objections Might the Company Have to the Golconda Nominees? • They might say: “We are already doing the things that the shareholders are requesting” – Many of the steps Tandy Brands has taken have come only after Golconda continued to apply pressure • Corporate governance changes were initially rejected in writing by the Board (see correspondence in the appendix to this presentation) • Poison pill changes were rejected even after a 73% stockholder vote in favor of the changes – Strategic alternatives exploration only announced after we publicly announced our intent to launch a proxy contest – The Tandy Brands Board has not acted on certain other recommendations: • The haven’t used cash flow to repurchase shares even with the stock price below tangible book value • They haven’t indicated a clear willingness to seek a value- maximizing sale of the company |

Golconda Capital Portfolio, LP • page 18 We Will Be Valuable Contributors to Board Deliberations We Will Be Valuable Contributors to Board Deliberations • The Company’s actions in the face of our advocacy effort indicates that we are in tune with the issues facing the Company – We will be valuable contributors to Board deliberations and work constructively with the incumbent Board members – We will approach deliberations from a perspective different than the incumbent Board members – We will be persistent in continuing to propel Tandy Brands toward the goal of maximizing stockholder value |

Golconda Capital Portfolio, LP • page 19 The Golconda Nominees Will Bring an Owner’s Perspective to Board The Golconda Nominees Will Bring an Owner’s Perspective to Board Deliberations Deliberations • Golconda owns more shares than the six non-management directors combined – Golconda and the Golconda nominees own 78,421 shares • 1.14% of shares outstanding – The six non-management directors combined own less than 1% of shares outstanding. • Our shares were purchased on the open market with our own capital – In contrast, many of the shares held by incumbent directors were simply granted to them by the Company • We have significant “skin in the game” |

Golconda Capital Portfolio, LP • page 20 Golconda’s Continuing Plan for Tandy Brands Golconda’s Continuing Plan for Tandy Brands • Explore strategic alternatives – Emphasis on a possible sale of the Company – Discontinue major acquisition activity until a possible sale of the Company has been fully explored • Establish a more liberal policy of returning free cash flow to the stockholders – As long as the stock price remains depressed, emphasis should be on share repurchases – In Tandy Brands’ case, this is not financial engineering, just good financial math • Continue to advocate for positive change – Emphasis on increasing returns on invested capital – Hold management accountable for financial performance As Tandy Brands Board members, we will maintain the positive momentum we have created to see value-maximizing initiatives through to fruition |

Golconda Capital Portfolio, LP • page 21 Appendix Appendix • Exhibit A: Golconda Letter to Board following 2006 Vote on Poison Pill Proposal • Exhibit B: Response letter from Chairman Gaertner regarding Proposed Corporate Governance changes |

Golconda Capital Management, LLC

Bill Summitt • Managing Member

P.O. Box 570507 • Dallas, TX 75357

Phone: 214-367-0784 • Fax: 214-853-4733

E-mail: wsummitt@golcondalp.com

December 6, 2006

Board of Directors*

Tandy Brands Accessories

c/o Assistant Secretary

690 East Lamar Blvd.

Suite 200

Arlington, TX 76011

Ladies and Gentlemen of the Board of Directors:

I am writing to follow up on the proposal to eliminate the Tandy Brands Accessories Preferred Share Purchase Rights Plan. As you know, this proposal passed by a significant margin. I urge you to acknowledge the wishes of the shareholders by eliminating this poison pill without delay.

Regarding any future poison pill that the board may put in place, such a pill should include the following shareholder friendly features:

| • | It should have a two to three year sunset provision. |

| • | It should be put to a shareholder vote within twelve months of adoption by the board (as recommended in the proposal). |

| • | It should contain a provision that allows shareholders to redeem the pill if an offer is received to purchase the company. |

| • | The pill should have a trigger of no less than 20% of shares outstanding. |

If any of these features are missing in a future pill, it would be cause for shareholder concern.

In addition to eliminating the poison pill, I also call on you to proactively take the necessary steps to declassify the board of directors and have all directors stand for election each year. I am aware that some of you feel that having a classified board helps to ensure board continuity and that this benefits shareholders. This may be true in some cases, but that is a decision for the shareholders to make on an election by election basis. Shareholders should determine for themselves if they desire board continuity by voting each year in such a way to provide that continuity or, as the case may be, to disrupt continuity.

1

Another problem with a classified board is that shareholders cannot select specific directors that they wish to replace, if any, each year. With our classified board, shareholders could be required to wait up to three years to replace board members that they feel are no longer representing their interests.

Finally, I urge you to establish a majority vote standard for election of directors in uncontested elections. The current plurality system reduces uncontested director elections to nothing more than a ceremonial affair. A majority vote standard would give the shareholders some teeth in holding directors accountable. A plurality vote standard should still apply for contested elections.

We should strive for corporate governance practices that allow shareholders to hold directors and managers accountable for their performance. The changes that I have proposed will take us toward this goal.

| Sincerely, |

/s/ Bill Summitt |

| Bill Summitt |

| * | Board of Directors |

| • | James F. Gaertner, Ph.D., Chairman of the Board |

| • | J.S.B. Jenkins, President, Chief Executive Officer |

| • | Roger R. Hemminghaus |

| • | Gene Stallings |

| • | Colombe M. Nicholas |

| • | George C. Lake |

| • | W. Grady Rosier |

2

February 9, 2007

Mr. Bill Summitt

Managing Member

Golconda Capital Management, LLC

P.O. Box 570507

Dallas, TX 75357

| Re: | Letter to Board of Directors of Tandy Brands Accessories, Inc. |

Dear Mr. Summitt:

Thank you for your letter of December 6, 2006, to the Board of Directors (the “Board”) of Tandy Brands Accessories, Inc. (the “Company”).

The Board met on January 31, 2007, and authorized the Company to address the substantive provisions of your letter.

We will begin by addressing the last item of your letter urging the Board to establish a majority vote standard for directors in uncontested elections.

That standard has always existed for the election of Tandy Brands Accessories directors, dating back to the Company’s incorporation on November 1, 1990. Specifically, as clearly stated in this year’s proxy statement on page 3 under the caption“How many votes are necessary to re-elect a nominee as a director?”, which is printed in the proxy statement in bold-face type:

Each nominee for director must receive the affirmative vote of amajority of the shares present at the meeting, either in person or represented by proxy, to be re-elected to our Board of Directors. (Emphasis added.)

Your reference to “a current plurality system,” is, therefore, incorrect.

You also asked the Board “to proactively take the necessary steps to declassify the board of directors.”

You state that board continuity “is a decision for the shareholders to make on an election by election basis.” The Board has been advised by counsel that Delaware law, the state of the Company’s incorporation, expressly permits staggered board terms. Consequently, Delaware law does not provide shareholders with the right to determine director continuity on an election-by-election basis.

| 690 E. Lamar Blvd., Suite 200 Arlington, Texas 76011 (817) 548-0090 Fax: (817) 548-1144 | ||||||

Mr. Bill Summitt

February 9, 2007

Page 2

You further state that, by eliminating the staggered board terms, shareholders could “disrupt continuity.” The Board was understandably concerned as to why you, a shareholder of the Company, would want to “disrupt continuity.” Nonetheless, the Board was advised by counsel that, in an uncontested election of directors, a shareholder of a Delaware corporation has the right to withhold his or her vote for one or more director nominees. (Delaware law does not presently permit voting against a nominee in an uncontested election.) Even if a director nominee were not to receive the affirmative vote of a majority of the shares present at the meeting, either in person or represented by proxy, to be re-elected to the Board, Delaware law provides that the non-reelected director nominee continues as a holdover director until his or her successor is elected and qualified. Delaware law, as well as all other state laws, goes to great lengths to make certain board continuity isnot disrupted. That is precisely why the Delaware legislature expressly provided for the holdover of non-reelected directors.

You further state “that shareholders cannot replace specific directors that they wish to replace,” and that “shareholders could be required to wait up to three years to replace board members that they feel are no longer representing their interests.” The Board has been advised by counsel that under no circumstance could a director be replaced in an uncontested election. In an uncontested election, if a director nominee were not to receive the affirmative vote of a majority of the shares present at the meeting, either in person or represented by proxy, to be reelected to the Board, Delaware law provides that the non-reelected director nominee continues as a holdover director until his or her successor is elected and qualified. That director is not replaced by the shareholder vote.

You also state that “shareholders could be required to wait up to three years to replace board members that they feel are no longer representing their interests.” The terms are for a period of three years. Why would shareholders elect a board member that they feel is no longer representing their interests? You assume in your letter that your fellow shareholders will do exactly that. That appears to be the only mathematically possible answer that would require shareholders “to wait up to three years.”

In addition to the foregoing, please be advised that the New York Stock Exchange has proposed an amendment to its rules that would eliminate discretionary voting by brokers in director elections. The Securities and Exchange Commission has also proposed amendments to the proxy rules under the Securities Exchange Act of 1934 that would require issuers and other soliciting persons to furnish proxy materials to shareholders by posting them on an Internet Web site and providing shareholders with notice of the availability of the proxy materials.

Based upon a consideration of the foregoing, and giving particular weight to the fact that having a staggered Board is expressly permitted by Delaware law, the Board has concluded not to eliminate its staggered board.

We address now your statements about your “proposal to eliminate the Tandy Brands Accessories Preferred Shares Rights Plan.” As you will recall, your specific proposal read in pertinent part as follows:

Mr. Bill Summitt

February 9, 2007

Page 3

“Resolved, that the shareholders of Tandy Brands Accessories Inc. (“the Company”)urge the Board of Directors to take the necessary steps to rescind the Company’s Preferred Share Purchase Rights Plan....” (Emphasis added.)

The shareholders passed a resolution urging the Board to take the necessary steps to rescind the Company’s Preferred Share Rights Plan (the “Plan”). Your proposal did not require the Company or the Board to do so.

The Board again considered this proposal at its recent meeting.

First, please refer to the information from our last proxy statement explaining why the Board recommended a vote against your proposal at the Annual Meeting, a copy of which is attached as Exhibit A to this letter. The Board still believes its reasons to be valid.

In addition, as you know, the Plan expires on October 19, 2009, which is less than three years from today.

As you also must know, the Company would incur costs and expenses in redeeming the rights issued under the Plan, which could be significant.

Accordingly, based upon the reasons set forth in the proxy statement and upon the additional facts set forth in this letter, the Board has determined not to redeem the rights issued under the Plan at this time. The Board does not intend to consider this issue again until its meeting preceding the October 19, 2009, expiration date. When the Board next meets to consider this issue, please be advised that the Board expressly reserves all its rights, including the right to renew and extend the rights under the Plan.

| Very truly Yours |

/s/ James F. Gaertner |

| James F. Gaertner |

| Chairman of the Board |

Poison pills amount to a major defacto shift of voting rights away from the shareholders on matters pertaining to a sale of the company. Accordingly, shareholders should be asked if they want to temporarily relinquish such power before a poison pill is implemented.

Additional information regarding this proposal can be found at www.golcondalp.com.

We urge all shareholders to vote FOR this resolution.

Board of Directors’ Response to Stockholder Proposal

The Board of Directors believes, and independent evidence suggests, that rights plans actually enhance value for stockholders. For example:

| • | According to the Investor Responsibility Reach Center, an independent source of impartial information on corporate governance and social responsibility issues, worldwide rights plans have been adopted by over 2,200 U.S. companies, consistent with an increasing number of studies demonstrating the economic benefits that rights plans provide for stockholders. |

| • | Institutional Shareholder Services, Inc., a major institutional stockholder advocacy group, commissioned a study released in February 2004 designed to test the correlation between corporate governance and stockholder value. The study found that companies with strong anti-takeover defenses, including rights plans, achieved higher stockholder returns of three-, five- and ten-year periods, higher return on equity, and higher performance on a number of other key financial and operating statistics. |

| • | A study by J.P. Morgan (now JP Morgan Chase & Co.), a global financial services provider, published in 2001, analyzing 397 acquisitions of U.S. public companies from 1997 to 2000 where the purchase price exceeded $1 billion, found that companies with rights plans in place received a median premium of 35.9% compared to 31.9% for companies without a rights plan. |

| • | In addition, a study published in 1997 by Georgeson & Company Inc. (now Georgeson Stockholder Communications, Inc.), a nationally recognized proxy solicitation and investor relations firm, analyzed takeover data between 1992 and 1996 to determine whether rights plans had any measurable impact on stockholder value. The study found that takeover premiums paid to target companies with rights plans were an average of eight percentage points higher than those paid to companies without rights plans, rights plans contributed an additional $13 billion in stockholder value in takeover situations over the study period, and stockholders of acquired companies without rights plans gave up $14.5 billion in potential premiums over the same period. The study also noted that the presence of a rights plan at a target company did not increase the likelihood of the withdrawal of a friendly takeover bid or the defeat of a hostile one, and did not reduce the likelihood of a company becoming a takeover target. |

The Company’s current preferred share purchase rights plan (the “Rights Plan”) is designed to strengthen the Board of Directors’ ability, in the exercise of its fiduciary duties, to protect our stockholders’ interests and to ensure that each stockholder is treated fairly in any transaction that involves a change of control of the Company. The Rights Plan does not prevent suitors from making offers to the Board or our stockholders, nor is it a deterrent to a stockholder’s initiation of a proxy contest. Instead, it is designed to encourage potential purchasers to negotiate directly with the Board and to give the Board sufficient time to evaluate the merits of every takeover proposal it receives, consistent with its fiduciary duties. This affords the Board the ability to respond to acquisition proposals, and the ability to attempt to negotiate a higher bid from a suitor, and flexibility to develop and pursue alternatives that may better enhance stockholder value. The Board believes that as the elected representative of the stockholders, it is in the best position to assess the intrinsic value of the Company and to negotiate on behalf of all stockholders evaluate the adequacy of any potential offer, and protect stockholders against potential abuses during the takeover process.

Potential takeover abuses that the Company’s Rights Plan is designed to protect against include the following:

| • | Compressed Time Frame — The traditional function of the Board of Directors is to act and negotiate in the best interest of and on behalf of the Company’s stockholders in connection with a merger or other business combination. The commencement of a tender offer, as opposed to negotiation with the Board of Directors, |

8

could leave the Company with a highly compressed time frame for considering alternatives and no meaningful bargaining power to seek a higher price or better terms for stockholders. |

| • | Creeping Tender Offer — By use of the so-called “creeping tender offer,” a potential hostile acquirer, through selective open-market purchases in which it offers different prices to different stockholders, could gain control of the Company without affording stockholders the protections of the Federal tender offer rules which require, among other things, that all stockholders receive the same price in a tender offer. |

| • | Street Sweep — The commencement of a tender offer by a hostile acquiror could result in professional short- term stock traders (arbitrageurs) acquiring large numbers of shares. Once this takes place, the hostile acquiror could terminate the tender offer (possibly causing the stock price to fall) and “sweep the street,” thereby acquiring control from the arbitrageurs but leaving other public stockholders as minority stockholders. |

| • | Partial Tender Offer — The takeover of the Company by a hostile acquiror through a creeping or partial tender offer would enable the hostile acquiror to take advantage of the public minority stockholders through self-dealing and conflict transactions or to squeeze out the public stockholders, forcing them to accept questionable securities. |

The Company’s Rights Plan was adopted by the Board in order to enhance its ability, in a manner consistent with its fiduciary duties, to preserve and enhance the value of every stockholder’s investment in the Company. The Board carefully reviewed the arguments for and against adopting such a plan before making its decision and continues to periodically review the matter, in consultation with outside counsel, to consider whether maintaining the Rights Plan continues to be in the best interests of the Company’s stockholders. In fact, on October 18, 2005, the Board of Directors considered whether maintaining the Rights Plan was in the best interests of stockholders, and determined that it was. The Board of Directors, following receipt of this stockholder proposal, again considered whether maintaining the Rights Plan was in the best interests of stockholders, and determined that it was.

The Board of Directors believes redemption of the Rights Plan at this time would be premature and would remove any incentive for a potential purchaser to negotiate with the Board of Directors, leaving the stockholders unprotected from potentially coercive and unfair offers. In addition, the Company stockholders should understand that stockholder approval of the adoption or maintenance of our Rights Plan is not required by any applicable law, regulation or rule or any rule of The NASDAQ Stock Market. The stockholder approval process is long and costly, and a requirement to seek stockholder approval for a rights plan could seriously jeopardize the Company’s negotiating position and leverage in a hostile situation, leaving the stockholders vulnerable to coercive and unfair acquisition tactics.

Finally, it is not clear how giving up the important bargaining tool created by our Rights Plan would respond to any of the corporate governance issues raised by the proponent. The Board of Directors is comprised entirely of independent outside directors, with the exception of the Company’s President and Chief Executive Officer. The Board of Directors believes that this independence, in conjunction with the requirement to maintain a majority of independent directors on the Board of Directors, and the Board of Directors’ duty to act in good faith and in the best interests of Company and its stockholders, provides adequate assurance against the Rights Plan being utilized for management entrenchment. In addition: the office of Chairman of the Board of Directors is separate from the office of President and is held by an independent director; all of the key committees of the Board of Directors consist solely of independent directors; we have adopted a Code of Business Conduct and Ethics applicable to the Board of Directors, a copy of which is posted on our website; and the Board evaluates its effectiveness and performance on an annual basis.

Based on the foregoing reasons, the Board of Directors believes the proposal is not in the best interests of the Company’s stockholders and recommends a vote AGAINST it.

9