| UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES |

Investment Company Act file number: (811- 06257 )

Exact name of registrant as specified in charter: Putnam Limited Duration Government Income Fund

Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109

| Name and address of agent for service: | Beth S. Mazor, Vice President |

| One Post Office Square | |

| Boston, Massachusetts 02109 | |

| Copy to: | John W. Gerstmayr, Esq. |

| Ropes & Gray LLP | |

| One International Place | |

| Boston, Massachusetts 02110 | |

Registrant’s telephone number, including area code: (617) 292-1000

Date of fiscal year end: November 30, 2006

Date of reporting period: December 1, 2005— May 31, 2006

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

What makes Putnam different?

In 1830, Massachusetts Supreme Judicial Court Justice Samuel Putnam established The Prudent Man Rule, a legal foundation for responsible money management.

THE PRUDENT MAN RULE

All that can be required of a trustee to invest is that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

A time-honored tradition in money management

Since 1937, our values have been rooted in a profound sense of responsibility for the money entrusted to us.

A prudent approach to investing

We use a research-driven team approach to seek consistent, dependable, superior investment results over time, although there is no guarantee a fund will meet its objectives.

Funds for every investment goal

We offer a broad range of mutual funds and other financial products so investors and their financial representatives can build diversified portfolios.

A commitment to doing what’s right for investors

We have below-average expenses and stringent investor protections, and provide a wealth of information about the Putnam funds.

Industry-leading service

We help investors, along with their financial representatives, make informed investment decisions with confidence.

| Putnam Limited Duration Government Income Fund |

| 5| 31| 06 Semiannual Report |

| Message from the Trustees | 2 |

| About the fund | 4 |

| Report from the fund managers | 7 |

| Performance | 13 |

| Expenses | 17 |

| Portfolio turnover | 19 |

| Risk | 20 |

| Your fund’s management | 21 |

| Terms and definitions | 24 |

| Trustee approval of management contract | 26 |

| Other information for shareholders | 31 |

| Financial statements | 32 |

Cover photograph: © Richard H. Johnson

| Message from the Trustees |

Dear Fellow Shareholder

Investors continue to keep a close watch on the course of the economy. Globally, it appears that, assuming economic growth exceeds 4% in 2006, we will have seen the strongest economic performance over a four-year period in over thirty years. Corporate profits have boomed around the world, business capacity utilization rates have moved up, and unemployment rates have come down. Given such a sustained period of robust growth, it is not surprising that prices have begun to rise, inflation rates have crept up, and central banks in many countries, particularly the Federal Reserve (the Fed) in the United States, have pushed interest rates higher.

In recent weeks, investors have worried that these higher rates could threaten the fundamentals of the global economy, prompting a widespread sell-off. However, we believe that today’s higher interest rates, far from being a threat to global economic fundamentals, are in fact an integral part of them. Higher interest rates are bringing business borrowing costs closer to the rate of return available from investments. In our view, this should help provide the basis for a longer and more durable business expansion and a continued healthy investment environment.

You can be assured that the investment professionals managing your fund are closely monitoring the factors that influence the performance of the securities in which your fund invests. Moreover, Putnam Investments’ management team, under the leadership of Chief Executive Officer Ed Haldeman, continues to focus on investment performance and remains committed to putting the interests of shareholders first.

2

In the following pages, members of your fund’s management team discuss the fund’s performance and strategies for the fiscal period ended May 31, 2006, and provide their outlook for the months ahead. As always, we thank you for your support of the Putnam funds.

| Putnam Limited Duration Government Income Fund: investing in government and mortgage-backed securities |

The U.S. government raises capital through the Bureau of the Public Debt. Every year, the Bureau holds more than 100 auctions for various government bonds (called Treasuries). U.S. Treasuries are considered a safe investment because they are backed by the full faith and credit of the federal government. For this very reason, however, Treasuries also tend to generate relatively low returns. In addition, they are not readily available to individual investors.

Putnam Limited Duration Government Income Fund is a convenient way for individuals to take advantage of the quality and relative stability of U.S. Treasuries while pursuing a higher level of income than would generally be available from Treasuries alone. The fund also invests in mortgage-backed securities (MBSs). MBSs represent a stake in the principal from and interest paid on a collection of mortgages. Most MBSs are created when government agencies, including Fannie Mae, Ginnie Mae, and Freddie Mac, buy mortgages from financial institutions and package them together by the thousands. These pools of mortgages act as collateral for the MBSs that agencies sell to financial entities, such as your fund. Because MBSs other than Ginnie Maes are not guaranteed directly by the U.S. government, and therefore carry a higher degree of risk than Treasury bonds, they also offer opportunities for higher returns.

By investing in high-quality Treasuries and MBSs as well as by limiting the fund's duration, your fund’s management team seeks to maintain a relatively low risk profile. Duration is a measure of a fund’s sensitivity to changes in interest rates. Having a shorter- or limited-duration portfolio may help protect

| Government bonds with limited durations have historically been less volatile than stocks. |

principal when interest rates are rising, but it can reduce the fund’s potential for appreciation when rates fall.

Putnam Limited Duration Government Income Fund pursues its income and capital preservation objectives by employing multiple income-generating strategies across government bond security types, and by carefully managing risks such as interest-rate risk.

Mutual funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Mutual funds that invest in bonds are subject to certain risks, including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. The use of derivatives involves special risks and may result in losses.

The ABCs of MBSs

MBSs (Mortgage-backed securities): MBSs are pools of mortgages used as collateral for issuing a security. These securities represent claims on the principal and interest payments made by the borrowers whose loans are in the pool.

Fannie Mae (Federal National Mortgage Association): Fannie Mae is a public company established by the U.S. government in 1938 to help make mortgage funds available to buyers. Fannie Mae does business with primary mortgage lenders (savings and loans, commercial banks, credit unions, and housing finance agencies).

Freddie Mac (Federal Home Loan Mortgage Corporation): Freddie Mac is another public company chartered by Congress to increase the funds available to mortgage financiers. Freddie Mac buys mortgages from primary lenders and develops MBSs that offer a guarantee on the payment of principal and interest.

Ginnie Mae (Government National Mortgage Association): Ginnie Mae is a government-owned corporation established in 1968 whose mortgage securities are backed by the full faith and credit of the U.S. government.

Putnam Limited Duration Government Income Fund seeks as high a level of current income as Putnam Management believes is consistent with preservation of capital by allocating its assets among intermediate-maturity U.S. Treasuries, mortgage-backed securities, and other U.S. government agency securities. The fund may be appropriate for investors seeking current income.

Highlights

* During the semiannual period ended May 31, 2006, Putnam Limited Duration Government Income Fund’s class A shares had a total return of 0.24% without sales charges.

* The fund’s primary benchmark, the Lehman Intermediate Government Bond Index, returned 0.43% .

* The average return for the fund’s Lipper category, Short-Intermediate U.S. Government Funds, was 0.48% .

* Additional fund performance, comparative performance, and Lipper data can be found in the performance section beginning on page 13.

Performance

Total return for class A shares for periods ended 5/31/06

| Since the fund’s inception (2/16/93), average annual return is 4.68% at NAV and 4.42% at POP. | |||||

| Average annual return | Cumulative return | ||||

| NAV | POP | NAV | POP | ||

| 10 years | 4.75% | 4.40% | 59.03% | 53.86% | |

| 5 years | 3.08 | 2.39 | 16.37 | 12.51 | |

| 3 years | 0.61 | –0.51 | 1.83 | –1.52 | |

| 1 year | –0.56 | –3.74 | –0.56 | –3.74 | |

| 6 months | — | — | 0.24 | –3.03 | |

Data is historical. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Returns at NAV do not reflect a sales charge of 3.25% . For the most recent month-end performance, visit www.putnam.com. For a portion of the period, this fund limited expenses, without which returns would have been lower. A short-term trading fee of up to 2% may apply.

6

| Report from the fund managers |

The period in review

Your fund delivered a modestly positive return at net asset value (NAV, or without sales charges) for the first half of its 2006 fiscal year, amid a challenging environment for bonds. Bond markets struggled in the face of a solidly growing economy, continued increases in the federal funds rate by the Fed, and rising inflationary pressures. The fund underperformed both its benchmark and Lipper peer group. An underweight to Ginnie Maes versus its benchmark hurt relative results as did an overweight to current-coupon MBSs at the expense of stronger-performing premium-coupon MBSs. These were the primary reasons for the fund’s underperformance of its benchmark. A shorter-than-benchmark duration contributed to relative returns. Duration is a measure of sensitivity to interest-rate changes; the shorter a fund’s duration, the less sensitive the portfolio is to changes in interest rates. We continued to keep duration conservatively short to protect against potential loss of principal in the event of rising interest rates. However, other funds in your fund’s peer group had even shorter durations and were less affected as interest rates rose slightly during the period. We believe this is the primary reason why your fund underperformed the average for its Lipper category.

Market overview

Over the six-month period, the U.S. economy continued to perform in robust fashion. Inflation was also stronger, more so than it has been in many years, stemming from sharp increases in commodity prices, especially crude oil and metals. Growth in the housing market, a long-term mainstay of the U.S. economy, seemed to level off. Corporations, benefiting from reduced debt levels and stronger balance sheets, began to increase capital spending in some areas, though not yet as broadly as economists might have liked. Acting on its primary mandate to maintain price stability in the face of inflationary pressures, the Fed continued to raise short-term

7

interest rates at each Federal Open Market Committee meeting during the period. These actions extended the cycle of monetary tightening initiated in June 2004 as the Fed sought to slow the pace of economic growth and restrain inflation. Part of the Fed’s wish since mid-2004 has been to see longer-term rates (which the Fed has no direct control over) increase in order to cool the “economic engine.” After a long wait, these rates did finally begin to rise during this period, 60 basis points on average. (A basis point is one one-hundredth of a percentage point.) Historically, though, yield spreads (the difference in yield between short- and long-term rates) are still narrow: Longer-term fixed-income investors, i.e., those purchasing securities with maturities from two to 10 years, have typically been paid an extra 1% in yield relative to shorter-term securities. As of the end of May, this yield spread was only 20 basis points.

Another factor that continued to keep long-term interest rates stubbornly low was strong demand for U.S. government bonds from Asia. This demand has been seen primarily through large purchases of Treasury bonds by China and Taiwan in an effort to keep the Chinese yuan pegged to the U.S. dollar. (This helps to maintain low prices for Chinese exports within the United States.) With the relatively modest across-the-board increase in interest rates during the fund’s fiscal period,

Market sector performance

These indexes provide an overview of performance in different market sectors for the six months ended 5/31/06.

| Bonds | |

| Lehman Intermediate Government Bond Index | |

| (intermediate-maturity U.S. government bonds) | 0.43% |

| Lehman Aggregate Bond Index (broad bond market) | 0.01% |

| Lehman Municipal Bond Index (tax-exempt bonds) | 1.51% |

| JP Morgan Global High Yield Index (global high-yield corporate bonds) | 4.56% |

| Equities | |

| S&P 500 Index (broad stock market) | 2.60% |

| Russell 1000 Index (large-company stocks) | 2.77% |

| MSCI EAFE Index (international stocks) | 15.30% |

8

most bond indices posted positive returns, reflecting the earning of higher levels of interest in a somewhat negative environment for bond prices.

Strategy overview

We make two key strategic decisions in managing your fund. The first is to estimate the direction of interest rates based on factors such as economic indicators, Fed statements and strategy, and market sentiment. Based on these estimates, we then strive to position the portfolio to benefit from expected changes in interest rates and in the shape of the yield curve. The yield curve is a graphical representation of yields for bonds of comparable quality plotted from the shortest to the longest maturity.

Our second major decision is to allocate portfolio holdings by market sector. We assess the relative attractiveness not only of sectors included in the benchmark (U.S. Treasuries and agencies) but also of sectors that are not in the benchmark but that are allowable investments within fund guidelines (MBSs, for example).

In addition, we make several strategic decisions related specifically to MBSs. We evaluate the relative appeal of pass-through securities issued by the Government National Mortgage Association (known as Ginnie Maes), the Federal National Mortgage Association (Fannie Maes), and the

Portfolio composition comparison

This chart shows how the fund’s weightings have changed over the last six months. Weightings are shown as a percentage of net assets. Holdings will vary over time. A portion of the short-term investments reflects amount used to settle TBA (“to be announced”) purchase commitments, which are described in detail on page 53 .

9

Federal Home Loan Mortgage Corporation (Freddie Macs). We also consider the maturity (e.g., 30-year, 15-year, or adjustable-rate), coupon level (e.g., 5.5%, 6.5%, 7%), and seasoning (length of time in the market) of these securities in order to determine what we believe are the best risk/return trade-offs for the portfolio.

Your fund’s holdings

In keeping with its objective of capital preservation, the fund maintained a duration profile that was shorter than that of its benchmark throughout the period. As mentioned earlier in this report, this conservative positioning helped the fund’s relative performance versus its benchmark. However, its positioning was less conservative than many of the fund’s competitors.

In terms of sector allocations, the fund’s holdings in Treasury securities benefited performance. However, the fund had an underweight position in agency securities during the period, reflecting our belief that comparable risk/reward potential could be obtained in the mortgage-backed securities (MBS) market at more attractive prices. This underweight positioning helped the fund’s performance. We believe that over the long term, MBSs offer better relative value than agencies. Another, longer-term reason for preferring MBSs over agencies is that foreign central banks are gradually expanding their investment universe beyond Treasuries and agencies

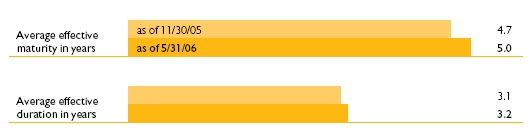

Comparison of the fund’s maturity and duration

This chart compares changes in the fund’s average effective maturity (a weighted average of the holdings’ maturities) and its average effective duration (a measure of its sensitivity to interest-rate changes).

Average effective duration and average effective maturity take into account put and call features, where applicable, and reflect prepayments for mortgage-backed securities. Duration is usually shorter than maturity because it reflects interest payments on a bond prior to its maturity.

10

to MBSs as they become more knowledgeable about the different types of U.S. government securities. This trend could lead to increased demand for these securities and, in turn, higher prices.

In terms of issuers, we continued to prefer Fannie Maes over Ginnie Maes and Freddie Macs during the period, a strategy that hindered returns because of strong demand from Asian banks for Ginnie Maes. In our view, however, Ginnie Maes have tended to be overpriced due to the Asian demand, as well as their constricted supply. The market for Fannie Maes continues to be larger and more liquid than markets for Ginnie Maes and Freddie Macs. The larger size of the market helps facilitate transactions.

The portfolio’s emphasis on longer-maturity securities (specifically, 30-year versus 15-year securities) benefited performance. We also continued to favor older, more seasoned securities, a positioning that was especially beneficial with regard to the fund’s “reperforming mortgage” holdings. These securities are repackaged mortgages that had previously incurred a default; payment of principal and interest for these mortgages is now guaranteed by Fannie Mae. Reperform-ing mortgages are notable for their lack of volatility stemming from prepayments.

During the six-month period, our emphasis on current-coupon MBSs over premium-coupon MBSs detracted slightly from performance. (Premium-coupon securities have coupons higher than current market rates whereas current-coupon securities, as their name indicates, reflect current rates.) Because investors sought higher yields, riskier premium-coupon mortgages outperformed.

Lastly, the fund benefited from its holdings in collateralized mortgage obligations (CMOs), mortgage instruments that separate mortgage pools (interest, principal, or a combination of the two) into different classes or “tranches.” Within the CMO universe we seek to take advantage of inconsistent pricing that results from different prepayment options among the various mortgage pools that make up the CMO. We look for opportunities to create cash flows that are similar to mortgages but have higher yields or cash flows that we believe carry less risk than mortgages with similar yields. The fund’s holdings in CMOs underperformed over the six-month period, but longer-term we believe they will prove to be beneficial.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future.

11

| The outlook for your fund |

The following commentary reflects anticipated developments that could affect your fund over the next six months, as well as your management team’s plans for responding to them.

We believe the housing market could well be the principal influence determining the direction of the U.S. economy over the coming months. Over the past several years, sustained spending by consumers — with their confidence boosted by ever-increasing property values — has kept the economy on track while corporations retrenched. If housing continues to stall, consumers may be stretched too thin to keep their spending at current levels. The first signs of a possible economic slowdown came at the end of the period, when job growth faltered. In addition, there could be increased volatility within the fixed-income markets in the coming months: With the Fed under new leadership, market participants are so far having difficulty assessing how much more Chairman Bernanke will tighten credit in order to restrain inflation.

With regard to sectors, we will continue to emphasize MBSs over agencies as we believe that select MBSs offer attractive value. Among the major issuers, we continue to favor Fannie Mae over Ginnie Mae and Freddie Mac. We also maintain a preference for longer-maturity instruments, whose higher yields support their prices while enhancing fund income, and for more seasoned securities, as they are less exposed to prepayment risk.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

Mutual funds that invest in bonds are subject to certain risks, including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. Mutual funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. The use of derivatives involves special risks and may result in losses.

12

Your fund’s performance

This section shows your fund’s performance for periods ended May 31, 2006, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance as of the most recent calendar quarter-end. Performance should always be considered in light of a fund’s investment strategy. Data represents past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. For the most recent month-end performance, please visit www.putnam.com or call Putnam at 1-800-225-1581. Class Y shares are generally only available to corporate and institutional clients. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance

Total return for periods ended 5/31/06

| Class A | Class B | Class C | Class M | Class R | Class Y | |||||

| (inception dates) | (2/16/93) | (2/16/93) | (7/26/99) | (4/3/95) | (12/1/03) | (10/1/97) | ||||

| NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV | |

| Annual average | ||||||||||

| (life of fund) | 4.68% | 4.42% | 4.06% | 4.06% | 3.86% | 3.86% | 4.54% | 4.38% | 4.43% | 4.84% |

| 10 years | 59.03 | 53.86 | 49.97 | 49.97 | 46.78 | 46.78 | 57.09 | 53.86 | 55.02 | 62.23 |

| Annual average | 4.75 | 4.40 | 4.14 | 4.14 | 3.91 | 3.91 | 4.62 | 4.40 | 4.48 | 4.96 |

| 5 years | 16.37 | 12.51 | 12.89 | 12.89 | 12.09 | 12.09 | 15.65 | 13.36 | 15.01 | 17.85 |

| Annual average | 3.08 | 2.39 | 2.45 | 2.45 | 2.31 | 2.31 | 2.95 | 2.54 | 2.84 | 3.34 |

| 3 years | 1.83 | –1.52 | 0.01 | –1.87 | –0.44 | –0.44 | 1.35 | –0.72 | 1.11 | 2.63 |

| Annual average | 0.61 | –0.51 | 0.00 | –0.63 | –0.15 | –0.15 | 0.45 | –0.24 | 0.37 | 0.87 |

| 1 year | –0.56 | –3.74 | –1.15 | –4.04 | –1.30 | –2.26 | –0.71 | –2.77 | –0.80 | –0.30 |

| 6 months | 0.24 | –3.03 | –0.05 | –3.00 | –0.12 | –1.11 | 0.17 | –1.77 | 0.13 | 0.38 |

Performance assumes reinvestment of distributions and does not account for taxes. Returns at public offering price (POP) for class A and M shares reflect a sales charge of 3.25% and 2.00%, respectively. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC the first year that is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and, except for class Y shares, the higher operating expenses for such shares.

For a portion of the period, this fund limited expenses, without which returns would have been lower.

A 2% short-term trading fee may be applied to shares exchanged or sold within 5 days of purchase.

13

Comparative index returns

For periods ended 5/31/06

| Lehman | Lipper Short- | |

| Intermediate | Intermediate | |

| Government | U.S. Government Funds | |

| Bond Index | category average* | |

| Annual average | ||

| (life of fund) | 5.39% | 4.78% |

| 10 years | 72.26 | 59.01 |

| Annual average | 5.59 | 4.74 |

| 5 years | 22.50 | 17.54 |

| Annual average | 4.14 | 3.28 |

| 3 years | 3.36 | 2.17 |

| Annual average | 1.11 | 0.71 |

| 1 year | 0.22 | 0.17 |

| 6 months | 0.43 | 0.48 |

Index and Lipper results should be compared to fund performance at net asset value.

* Over the 6-month and 1-, 3-, 5-, and 10-year periods ended 5/31/06, there were 79, 77, 69, 64, and 48 funds, respectively, in this Lipper category.

14

Fund price and distribution information

For the six-month period ended 5/31/06

| Distributions* | Class A | Class B | Class C | Class M | Class R | Class Y | ||

| Number | 6 | 6 | 6 | 6 | 6 | 6 | ||

| Income | $0.089638 | $0.074650 | $0.070974 | $0.085856 | $0.083364 | $0.095846 | ||

| Capital gains | ||||||||

| Long-term | 0.003000 | 0.003000 | 0.003000 | 0.003000 | 0.003000 | 0.003000 | ||

| Short-term | — | — | — | — | — | — | ||

| Total | $0.092638 | $0.077650 | $0.073974 | $0.088856 | $0.086364 | $0.098846 | ||

| Share value: | NAV | POP | NAV | NAV | NAV | POP | NAV | NAV |

| 11/30/05 | $5.02 | $5.19 | $5.03 | $5.02 | $5.04 | $5.14 | $5.02 | $5.01 |

| 5/31/06 | 4.94 | 5.11 | 4.95 | 4.94 | 4.96 | 5.06 | 4.94 | 4.93 |

| Current yield | ||||||||

| (end of period) | ||||||||

| Current | ||||||||

| dividend rate1 | 4.12% | 3.98% | 3.51% | 3.37% | 3.95% | 3.87% | 3.86% | 4.37% |

| Current 30-day | ||||||||

| SEC yield2,3 | ||||||||

| (with expense | ||||||||

| limitation) | 4.12 | 3.98 | 3.52 | 3.37 | 3.97 | 3.89 | 3.87 | 4.37 |

| Current 30-day | ||||||||

| SEC yield3 | ||||||||

| (without | ||||||||

| expense | ||||||||

| limitation) | 4.00 | 3.87 | 3.40 | 3.25 | 3.85 | 3.78 | 3.75 | 4.25 |

* Dividend sources are estimated and may vary based on final tax calculations after the fund’s fiscal year-end.

1 Most recent distribution, excluding capital gains, annualized and divided by NAV or POP at end of period.

2 For a portion of the period, this fund limited expenses, without which yields would have been lower.

3 Based only on investment income, calculated using SEC guidelines.

15

Fund performance for most recent calendar quarter

Total return for periods ended 6/30/06

| Class A | Class B | Class C | Class M | Class R | Class Y | |||||

| (inception dates) | (2/16/93) | (2/16/93) | (7/26/99) | (4/3/95) | (12/1/03) | (10/1/97) | ||||

| NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV | |

| Annual average | ||||||||||

| (life of fund) | 4.64% | 4.38% | 4.04% | 4.04% | 3.82% | 3.82% | 4.52% | 4.36% | 4.39% | 4.80% |

| 10 years | 57.35 | 52.28 | 48.68 | 48.68 | 45.48 | 45.48 | 55.43 | 52.27 | 53.37 | 60.56 |

| Annual average | 4.64 | 4.30 | 4.05 | 4.05 | 3.82 | 3.82 | 4.51 | 4.29 | 4.37 | 4.85 |

| 5 years | 15.96 | 12.11 | 12.71 | 12.71 | 11.70 | 11.70 | 15.48 | 13.19 | 14.58 | 17.45 |

| Annual average | 3.01 | 2.31 | 2.42 | 2.42 | 2.24 | 2.24 | 2.92 | 2.51 | 2.76 | 3.27 |

| 3 years | 1.60 | -1.74 | -0.01 | -1.89 | -0.66 | -0.66 | 1.32 | -0.73 | 0.89 | 2.39 |

| Annual average | 0.53 | -0.58 | 0.00 | -0.63 | -0.22 | -0.22 | 0.44 | -0.24 | 0.30 | 0.79 |

| 1 year | -0.69 | -3.88 | -1.27 | -4.16 | -1.43 | -2.39 | -0.64 | -2.52 | -0.94 | -0.43 |

| 6 months | -0.43 | -3.68 | -0.51 | -3.45 | -0.79 | -1.77 | -0.30 | -2.23 | -0.54 | -0.29 |

16

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund limited these expenses; had it not done so, expenses would have been higher. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial advisor.

Review your fund’s expenses

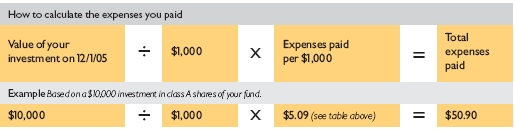

The table below shows the expenses you would have paid on a $1,000 investment in Putnam Limited Duration Government Income Fund from December 1, 2005, to May 31, 2006. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Expenses paid per $1,000* | $ 5.09 | $ 8.08 | $ 8.82 | $ 5.84 | $ 6.34 | $ 3.85 |

| Ending value (after expenses) | $1,002.40 | $999.50 | $998.80 | $1,001.70 | $1,001.30 | $1,003.80 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of net assets for the six months ended 5/31/06. The expense ratio may differ for each share class (see the table at the bottom of the next page). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year. Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, expenses for each share class would have been lower.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended May 31, 2006, use the calculation method below. To find the value of your investment on December 1, 2005, go to www.putnam.com and log on to your account. Click on the “Transaction History” tab in your Daily Statement and enter 12/01/2005 in both the “from” and “to” fields. Alternatively, call Putnam at 1-800-225-1581.

17

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Expenses paid per $1,000* | $ 5.14 | $ 8.15 | $ 8.90 | $ 5.89 | $ 6.39 | $ 3.88 |

| Ending value (after expenses) | $1,019.85 | $1,016.85 | $1,016.11 | $1,019.10 | $1,018.60 | $1,021.09 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of net assets for the six months ended 5/31/06. The expense ratio may differ for each share class (see the table at the bottom of this page). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year. Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, expenses for each share class would have been lower.

Compare expenses using industry averages

You can also compare your fund’s expenses with the average of its peer group, as defined by Lipper, an independent fund-rating agency that ranks funds relative to others that Lipper considers to have similar investment styles or objectives. The expense ratio for each share class shown below indicates how much of your fund’s net assets have been used to pay ongoing expenses during the period.

| Class A | Class B | Class C | Class M | Class R | Class Y | |

| Your fund's annualized | ||||||

| expense ratio* | 1.02% | 1.62% | 1.77% | 1.17% | 1.27% | 0.77% |

| Average annualized expense | ||||||

| ratio for Lipper peer group† | 1.05% | 1.65% | 1.80% | 1.20% | 1.30% | 0.80% |

* Does not reflect the effect of a non-recurring reimbursement by Putnam. If this amount had been reflected in the table above, the expense ratio for each share class would have been lower.

† Simple average of the expenses of all front-end load funds in the fund’s Lipper peer group, calculated in accordance with Lipper’s standard method for comparing fund expenses (excluding 12b-1 fees and without giving effect to any expense offset and brokerage service arrangements that may reduce fund expenses). This average reflects each fund’s expenses for its most recent fiscal year available to Lipper as of 3/31/06. To facilitate comparison, Putnam has adjusted this average to reflect the 12b-1 fees carried by each class of shares other than class Y shares, which do not incur 12b-1 fees. The peer group may include funds that are significantly smaller or larger than the fund, which may limit the comparability of the fund’s expenses to the simple average, which typically is higher than the asset-weighted average.

18

| Your fund’s portfolio turnover |

Putnam funds are actively managed by teams of experts who buy and sell securities based on intensive analysis of companies, industries, economies, and markets. Portfolio turnover is a measure of how often a fund’s managers buy and sell securities for your fund. A portfolio turnover of 100%, for example, means that the managers sold and replaced securities valued at 100% of a fund’s assets within a one-year period. Funds with high turnover may be more likely to generate capital gains and dividends that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance.

Funds that invest in bonds or other fixed-income instruments may have higher turnover than funds that invest only in stocks. Short-term bond funds tend to have higher turnover than longer-term bond funds, because shorter-term bonds will mature or be sold more frequently than longer-term bonds. You can use the table below to compare your fund’s turnover with the average turnover for funds in its Lipper category.

Turnover comparisons

Percentage of holdings that change every year

| 2005 | 2004 | 2003 | 2002 | 2001 | |

| Putnam Limited Duration | |||||

| Government Income Fund | 389%* | 263% | 509%† | 539%† | 224%† |

| Lipper Short-Intermediate | |||||

| U.S. Government Funds | |||||

| category average | 124% | 130% | 166% | 145% | 166% |

* Portfolio turnover excludes dollar roll transactions.

† Portfolio turnover excludes certain transactions executed in connection with a short-term trading strategy.

Turnover data for the fund is calculated based on the fund’s fiscal-year period, which ends on November 30. Turnover data for the fund’s Lipper category is calculated based on the average of the turnover of each fund in the category for its fiscal year ended during the indicated year. Fiscal years vary across funds in the Lipper category, which may limit the comparability of the fund’s portfolio turnover rate to the Lipper average. Comparative data for 2005 is based on information available as of 12/31/05.

19

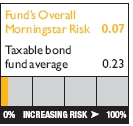

Your fund’s risk

This risk comparison is designed to help you understand how your fund compares with other funds. The comparison utilizes a risk measure developed by Morningstar, an independent fund-rating agency. This risk measure is referred to as the fund’s Overall Morningstar Risk.

Your fund’s Overall Morningstar® Risk

Your fund’s Overall Morningstar Risk is shown alongside that of the average fund in its broad asset class, as determined by Morningstar. The risk bar broadens the comparison by translating the fund’s Overall Morningstar Risk into a percentile, which is based on the fund’s ranking among all funds rated by Morningstar as of June 30, 2006. A higher Overall Morningstar Risk generally indicates that a fund’s monthly returns have varied more widely.

Morningstar determines a fund’s Overall Morningstar Risk by assessing variations in the fund’s monthly returns — with an emphasis on downside variations — over 3-, 5-, and 10-year periods, if available. Those measures are weighted and averaged to produce the fund’s Overall Morningstar Risk. The information shown is provided for the fund’s class A shares only; information for other classes may vary. Overall Morningstar Risk is based on historical data and does not indicate future results. Morningstar does not purport to measure the risk associated with a current investment in a fund, either on an absolute basis or on a relative basis. Low Overall Morningstar Risk does not mean that you cannot lose money on an investment in a fund. Copyright 2006 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

20

| Your fund’s management |

Your fund is managed by the members of the Putnam Core Fixed-Income Team. Kevin Cronin is the Portfolio Leader of the fund. Rob Bloemker and Daniel Choquette are Portfolio Members. The Portfolio Leader and Portfolio Members coordinate the team’s management of the fund.

For a complete listing of the members of the Putnam Core Fixed-Income Team, including those who are not Portfolio Leaders or Portfolio Members of your fund, visit Putnam’s Individual Investor Web site at www.putnam.com.

Fund ownership by the Portfolio Leader and Portfolio Members

The table below shows how much the fund’s current Portfolio Leader and Portfolio Members have invested in the fund (in dollar ranges). Information shown is as of May 31, 2006, and May 31, 2005.

| $1 – | $10,001 – | $50,001 – | $100,001 – | $500,001 – | $1,000,001 | |||

| Year | $0 | $10,000 | $50,000 | $100,000 | $500,000 | $1,000,000 | and over | |

| Kevin Cronin | 2006 | * | ||||||

| Portfolio Leader | 2005 | * | ||||||

| Rob Bloemker | 2006 | * | ||||||

| Portfolio Member | 2005 | * | ||||||

| Daniel Choquette | 2006 | * | ||||||

| Portfolio Member | 2005 | * | ||||||

21

Fund manager compensation

The total 2005 fund manager compensation that is attributable to your fund is approximately $480,000. This amount includes a portion of 2005 compensation paid by Putnam Management to the fund managers listed in this section for their portfolio management responsibilities, calculated based on the fund assets they manage taken as a percentage of the total assets they manage. The compensation amount also includes a portion of the 2005 compensation paid to the Chief Investment Officer of the team and the Group Chief Investment Officer of the fund’s broader investment category for their oversight responsibilities, calculated based on the fund assets they oversee taken as a percentage of the total assets they oversee. This amount does not include compensation of other personnel involved in research, trading, administration, systems, compliance, or fund operations; nor does it include non-compensation costs. These percentages are determined as of the fund’s fiscal period-end. For personnel who joined Putnam Management during or after 2005, the calculation reflects annualized 2005 compensation or an estimate of 2006 compensation, as applicable.

| Other Putnam funds managed by the Portfolio Leader and Portfolio Members |

Kevin Cronin is also a Portfolio Leader of Putnam American Government Income Fund, Putnam Global Income Trust, Putnam Income Fund, and Putnam U.S. Government Income Trust. He is also a Portfolio Member of Putnam Equity Income Fund.

Rob Bloemker is also a Portfolio Member of Putnam American Government Income Fund, Putnam Diversified Income Trust, Putnam Income Fund, Putnam Master Intermediate Income Trust, Putnam Premier Income Trust, and Putnam U.S. Government Income Trust.

Daniel Choquette is also a Portfolio Member of Putnam American Government Income Fund and Putnam U.S. Government Income Trust.

Kevin Cronin, Rob Bloemker, and Daniel Choquette may also manage other accounts and variable trust funds advised by Putnam Management or an affiliate.

Changes in your fund’s Portfolio Leader and Portfolio Members

Your fund’s Portfolio Leader and Portfolio Members did not change during the year ended May 31, 2006.

22

Fund ownership by Putnam’s Executive Board

The table below shows how much the members of Putnam’s Executive Board have invested in the fund (in dollar ranges). Information shown is as of May 31, 2006, and May 31, 2005.

| $1 – | $10,001 – | $50,001– | $100,001 | |||

| Year | $0 | $10,000 | $50,000 | $100,000 | and over | |

| Philippe Bibi | 2006 | * | ||||

| Chief Technology Officer | 2005 | * | ||||

| Joshua Brooks | 2006 | * | ||||

| Deputy Head of Investments | 2005 | * | ||||

| William Connolly | 2006 | * | ||||

| Head of Retail Management | N/A | |||||

| Kevin Cronin | 2006 | * | ||||

| Head of Investments | 2005 | * | ||||

| Charles Haldeman, Jr. | 2006 | * | ||||

| President and CEO | 2005 | * | ||||

| Amrit Kanwal | 2006 | * | ||||

| Chief Financial Officer | 2005 | * | ||||

| Steven Krichmar | 2006 | * | ||||

| Chief of Operations | 2005 | * | ||||

| Francis McNamara, III | 2006 | * | ||||

| General Counsel | 2005 | * | ||||

| Richard Robie, III | 2006 | * | ||||

| Chief Administrative Officer | 2005 | * | ||||

| Edward Shadek | 2006 | * | ||||

| Deputy Head of Investments | 2005 | * | ||||

| Sandra Whiston | 2006 | * | ||||

| Head of Institutional Management | N/A | |||||

N/A indicates the individual was not a member of Putnam's Executive Board as of 5/31/05.

23

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 3.25% maximum sales charge for class A shares and 2.00% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC. Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge). Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to eligible purchasers, including eligible defined contribution plans or corporate IRAs.

24

Comparative indexes

JP Morgan Global High Yield Index is an unmanaged index of global high-yield fixed-income securities.

Lehman Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

Lehman Intermediate Government Bond Index is an unmanaged index of U.S. Treasury and agency securities with maturities between 1 and 10 years.

Lehman Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

Morgan Stanley Capital International (MSCI) EAFE Index is an unmanaged index of equity securities from developed countries in Western Europe, the Far East, and Australasia.

Russell 1000 Index is an unmanaged index of the 1,000 largest companies in the Russell 3000 Index.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

25

| Trustee approval of management contract |

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Management. In this regard, the Board of Trustees, with the assistance of its Contract Committee consisting solely of Trustees who are not “interested persons” (as such term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (the “Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances. Over the course of several months beginning in March and ending in June 2005, the Contract Committee met five times to consider the information provided by Putnam Management and other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of this information with all of the Independent Trustees. Upon completion of this review, the Contract Committee recommended and the Independent Trustees approved the continuance of your fund’s management contract, effective July 1, 2005.

This approval was based on the following conclusions:

* That the fee schedule currently in effect for your fund represents reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds and the costs incurred by Putnam Management in providing such services, and

* That such fee schedule represents an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the fee arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that certain aspects of such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements in prior years.

26

Model fee schedules and categories; total expenses

The Trustees’ review of the management fees and total expenses of the Putnam funds focused on three major themes:

* Consistency. The Trustees, working in cooperation with Putnam Management, have developed and implemented a series of model fee schedules for the Putnam funds designed to ensure that each fund’s management fee is consistent with the fees for similar funds in the Putnam family of funds and compares favorably with fees paid by competitive funds sponsored by other investment advisors. Under this approach, each Putnam fund is assigned to one of several fee categories based on a combination of factors, including competitive fees and perceived difficulty of management, and a common fee schedule is implemented for all funds in a given fee category. The Trustees reviewed the model fee schedule then in effect for your fund, including fee levels and breakpoints, and the assignment of the fund to a particular fee category under this structure. (“Breakpoints” refer to reductions in fee rates that apply to additional assets once specified asset levels are reached.) The Trustees concluded that no changes should be made in the fund’s current fee schedule at this time.

* Competitiveness. The Trustees also reviewed comparative fee and expense information for competitive funds, which indicated that, in a custom peer group of competitive funds selected by Lipper Inc., your fund ranked in the 42nd percentile in management fees and in the 50th percentile in total expenses (less any applicable 12b-1 fees) as of December 31, 2004 (the first percentile being the least expensive funds and the 100th percentile being the most expensive funds). (Because the fund’s custom peer group is smaller than the fund’s broad Lipper Inc. peer group, this expense comparison may differ from the Lipper peer expense information found elsewhere in this report.) The Trustees noted that expense ratios for a number of Putnam funds, which show the percentage of fund assets used to pay for management and administrative services, distribution (12b-1) fees and other expenses, had been increasing recently as a result of declining net assets and the natural operation of fee breakpoints. They noted that such expense ratio increases were currently being controlled by expense limitations implemented in January 2004 and which Putnam Management, in consultation with the Contract Committee, had committed to maintain at least through 2006. The Trustees expressed their intention to monitor this information closely to ensure that fees and expenses of the Putnam funds continue to meet evolving competitive standards.

* Economies of scale. The Trustees concluded that the fee schedule currently in effect for your fund represents an appropriate sharing of economies of scale at current asset levels. Your fund currently has the benefit of breakpoints in its management fee that provide shareholders with significant economies of scale, which means that the effective management fee rate of a fund (as a percentage of fund assets) declines as a fund grows in size and crosses specified asset thresholds. The Trustees examined the existing breakpoint structure of the Putnam funds’ management fees in light of competitive industry practices. The Trustees considered

27

various possible modifications to the Putnam funds’ current breakpoint structure, but ultimately concluded that the current breakpoint structure continues to serve the interests of fund shareholders. Accordingly, the Trustees continue to believe that the fee schedules currently in effect for the funds represent an appropriate sharing of economies of scale at current asset levels. The Trustees noted that significant redemptions in many Putnam funds, together with significant changes in the cost structure of Putnam Management, have altered the economics of Putnam Management’s business in significant ways. In view of these changes, the Trustees intend to consider whether a greater sharing of the economies of scale by fund shareholders would be appropriate if and when aggregate assets in the Putnam funds begin to experience meaningful growth.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services to be provided and profits to be realized by Putnam Management and its affiliates from the relationship with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability with respect to the funds’ management contracts, allocated on a fund-by-fund basis.

| Investment performance |

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the funds’ investment process and performance by the work of the Investment Oversight Committees of the Trustees, which meet on a regular monthly basis with the funds’ portfolio teams throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — as measured by the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to such personnel, and in general the ability of Putnam Management to attract and retain high-quality personnel — but also recognize that this does not guarantee favorable investment results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time periods and considered information comparing the fund’s performance with various benchmarks and with the performance of competitive funds. The Trustees noted the satisfactory investment performance of many Putnam funds. They also noted the disappointing investment performance of certain funds in recent years and continued to discuss with senior management of Putnam Management the factors contributing to such underperformance and actions being taken to improve performance. The Trustees recognized that, in recent years, Putnam Management has made significant changes in its investment personnel and processes and in the fund product line to address areas of underperformance. The Trustees indicated their intention to continue to

28

monitor performance trends to assess the effectiveness of these changes and to evaluate whether additional remedial changes are warranted.

In the case of your fund, the Trustees considered that your fund’s class A share cumulative total return performance at net asset value was in the following percentiles of its Lipper Inc. peer group (Lipper Short-Intermediate U.S. Government Funds) for the one-, three-, and five-year periods ended December 31, 2004 (the first percentile being the best-performing funds and the 100th percentile being the worst-performing funds):

| One-year period | Three-year period | Five-year period |

| 24th | 47th | 50th |

(Because of the passage of time, these performance results may differ from the performance results for more recent periods shown elsewhere in this report. Over the one-, three-, and five-year periods ended December 31, 2004, there were 83, 74, and 70 Lipper Short-Intermediate U.S. Government Funds, respectively, in your fund’s Lipper peer group.* Past performance is no guarantee of future performance.)

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance problems. The Trustees believe that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on the responsiveness of Putnam Management in the recent past to Trustee concerns about investment performance, the Trustees believe that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of terminating a management contract and engaging a new investment advisor for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations; other benefits

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include principally benefits related to brokerage and soft-dollar allocations, whereby a portion of the commissions paid by a fund for brokerage is earmarked to pay for research services that may be utilized by a fund’s investment advisor, subject to the obligation to seek best execution. The Trustees believe that soft-dollar credits and other potential benefits associated with the allocation of fund brokerage, which pertains mainly to funds investing in equity securities, represent assets of

* The percentile rankings for your fund’s class A share annualized total return performance in the Lipper Short-Intermediate U.S. Government Funds category for the one-, five-, and ten-year periods ended June 30, 2006, were 77%, 64%, and 58%, respectively. Over the one-, five-, and ten-year periods ended June 30, 2006, the fund ranked 60th out of 77, 41st out of 64, and 28th out of 48 funds, respectively. Note that this more recent information was not available when the Trustees approved the continuance of your fund’s management contract.

29

the funds that should be used for the benefit of fund shareholders. This area has been marked by significant change in recent years. In July 2003, acting upon the Contract Committee’s recommendation, the Trustees directed that allocations of brokerage to reward firms that sell fund shares be discontinued no later than December 31, 2003. In addition, commencing in 2004, the allocation of brokerage commissions by Putnam Management to acquire research services from third-party service providers has been significantly reduced, and continues at a modest level only to acquire research that is customarily not available for cash. The Trustees will continue to monitor the allocation of the funds’ brokerage to ensure that the principle of “best price and execution” remains paramount in the portfolio trading process.

The Trustees’ annual review of your fund’s management contract also included the review of its distributor’s contract and distribution plan with Putnam Retail Management Limited Partnership and the custodian agreement and investor servicing agreement with Putnam Fiduciary Trust Company, all of which provide benefits to affiliates of Putnam Management.

Comparison of retail and institutional fee schedules

The information examined by the Trustees as part of their annual contract review has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, etc. This information included comparison of such fees with fees charged to the funds, as well as a detailed assessment of the differences in the services provided to these two types of clients. The Trustees observed, in this regard, that the differences in fee rates between institutional clients and the mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients reflect to a substantial degree historical competitive forces operating in separate market places. The Trustees considered the fact that fee rates across all asset sectors are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to institutional clients of the firm, but have not relied on such comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

30

| Other information for shareholders |

Important notice regarding delivery of shareholder documents

In accordance with SEC regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

| Proxy voting |

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2005, are available on the Putnam Individual Investor Web site, www.putnam.com/individual, and on the SEC’s Web site, www.sec.gov. If you have questions about finding forms on the SEC’s Web site, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

| Fund portfolio holdings |

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s Web site at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s Web site or the operation of the Public Reference Room.

31

| Financial statements |

| A guide to financial statements |

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and noninvestment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlight table also includes the current reporting period.

32

| The fund’s portfolio 5/31/06 (Unaudited) | ||||

| U.S. GOVERNMENT AND AGENCY MORTGAGE OBLIGATIONS (12.6%)* | ||||

| Principal amount | Value | |||

| U.S. Government Guaranteed Mortgage Obligations (2.5%) | ||||

| Government National Mortgage Association | ||||

| Adjustable Rate Mortgages | ||||

| 4 3/4s, July 20, 2026 | $ | 71,513 | $ | 71,961 |

| 4 1/2s, August 20, 2034 | 10,471,010 | 10,336,230 | ||

| Government National Mortgage Association | ||||

| Pass-Through Certificates | ||||

| 7 1/2s, with due dates from December 15, 2023 | ||||

| to March 15, 2032 | 1,120,253 | 1,172,647 | ||

| 7s, with due dates from July 15, 2029 to May 15, 2032 | 175,157 | 181,843 | ||

| 11,762,681 | ||||

| U.S. Government Agency Mortgage Obligations (10.1%) | ||||

| Federal Home Loan Mortgage Corporation | ||||

| Pass-Through Certificates | ||||

| 7 1/2s, with due dates from April 1, 2016 | ||||

| to December 1, 2017 | 33,132 | 34,154 | ||

| 5 1/2s, October 1, 2018 | 741,735 | 731,536 | ||

| Federal National Mortgage Association | ||||

| Pass-Through Certificates | ||||

| 7 1/2s, with due dates from October 1, 2022 | ||||

| to November 1, 2030 | 222,653 | 231,076 | ||

| 7s, with due dates from December 1, 2031 to | ||||

| December 1, 2035 | 5,632,645 | 5,775,515 | ||

| 7s, with due dates from September 1, 2007 to | ||||

| January 1, 2015 | 459,096 | 467,567 | ||

| 6 1/2s, August 1, 2034 | 1,092,629 | 1,104,324 | ||

| 6 1/2s, with due dates from February 1, 2014 | ||||

| to February 1, 2017 | 1,218,786 | 1,240,305 | ||

| 6s, with due dates from March 1, 2014 to October 1, 2016 | 568,813 | 573,008 | ||

| 6s, TBA, June 1, 2036 | 7,500,000 | 7,408,008 | ||

| 5 1/2s, with due dates from April 1, 2036 to | ||||

| May 1, 2036 | 5,211,008 | 5,019,462 | ||

| 5 1/2s, with due dates from January 1, 2009 | ||||

| to February 1, 2021 | 5,068,639 | 4,999,972 | ||

| 5s, with due dates from August 1, 2035 to May 1, 2036 | 3,900,058 | 3,659,218 | ||

| 5s, December 1, 2020 | 59,777 | 57,734 | ||

| 4 1/2s, with due dates from November 1, 2020 | ||||

| to October 1, 2035 | 15,478,264 | 14,611,522 | ||

| 4 1/2s, with due dates from March 1, 2020 | ||||

| to September 1, 2020 | 1,249,461 | 1,182,496 | ||

| 47,095,897 | ||||

| Total U.S. government and agency mortgage obligations (cost $59,741,912) | $ | 58,858,578 | ||

33

| U.S. GOVERNMENT AGENCY OBLIGATIONS (8.9%)* | ||||

| Principal amount | Value | |||

| Fannie Mae 4 1/4s, August 15, 2010 | $ | 9,600,000 | $ | 9,199,186 |

| Freddie Mac | ||||

| 6 7/8s, September 15, 2010 | 6,752,000 | 7,134,508 | ||

| 6 5/8s, September 15, 2009 | 23,980,000 | 24,886,689 | ||

| Total U.S. government agency obligations (cost $42,952,146) | $ | 41,220,383 | ||

| U.S. TREASURY OBLIGATIONS (35.2%)* | ||||

| Principal amount | Value | |||

| U.S. Treasury Notes | ||||

| 4 1/4s, August 15, 2014 | $ | 1,300,000 | $ | 1,225,656 |

| 4 1/4s, August 15, 2013 | 53,596,000 | 50,899,451 | ||

| 4s, February 15, 2014 | 25,000,000 | 23,246,095 | ||

| 3 1/4s, August 15, 2008 | 92,000,000 | 88,600,315 | ||

| Total U.S. treasury obligations (cost $171,503,796) | $ | 163,971,517 | ||

| COLLATERALIZED MORTGAGE OBLIGATIONS (35.2%)* | ||||

| Principal amount | Value | |||

| Banc of America Commercial Mortgage, Inc. | ||||

| FRB Ser. 05-1, Class A5, 5.135s, 2042 | $ | 207,000 | $ | 198,858 |

| Ser. 04-4, Class A6, 4.877s, 2042 | 34,000 | 31,855 | ||

| Commercial Mortgage Pass-Through | ||||

| Certificates | ||||

| Ser. 06-C7, Class A4, 5.769s, 2046 | 6,752,000 | 6,761,453 | ||

| FRB Ser. 04-LB3A, Class A5, 5.281s, 2037 | 20,000 | 19,446 | ||

| CS First Boston Mortgage Securities Corp. | ||||

| FRB Ser. 04-C3, Class A5, 5.113s, 2036 | 76,000 | 72,499 | ||

| Ser. 05-C4, Class A5, 5.104s, 2038 | 64,000 | 60,749 | ||

| FRB Ser. 05-C5, Class A4, 5.1s, 2038 | 64,000 | 60,661 | ||

| Ser. 04-C3, Class A3, 4.302s, 2036 | 161,000 | 155,216 | ||

| Fannie Mae | ||||

| FRB Ser. 05-45, Class FG, 22.306s, 2035 | 347,861 | 373,946 | ||

| Ser. 03-W6, Class PT1, 9.544s, 2042 | 2,029,734 | 2,146,056 | ||

| FRB Ser. 06-62, Class PS, 9.42s, 2036 | 656,000 | 687,191 | ||

| Ser. 06-20, Class IP, Interest Only (IO), 8s, 2030 | 372,491 | 81,825 | ||

| IFB Ser. 03-130, Class SJ, 7.675s, 2034 | 206,441 | 195,661 | ||

| IFB Ser. 06-42, Class PS, 7.55s, 2036 | 645,000 | 614,476 | ||

| Ser. 05-W3, Class 1A, 7 1/2s, 2045 | 1,759,546 | 1,831,181 | ||

| Ser. 04-W8, Class 3A, 7 1/2s, 2044 | 2,961,117 | 3,077,218 | ||

| Ser. 04-W11, Class 1A4, 7 1/2s, 2044 | 588,045 | 610,856 | ||

| Ser. 04-W2, Class 5A, 7 1/2s, 2044 | 608,053 | 631,702 | ||

| Ser. 04-T3, Class 1A4, 7 1/2s, 2044 | 1,592,042 | 1,653,360 | ||

| Ser. 04-T2, Class 1A4, 7 1/2s, 2043 | 349,518 | 362,985 | ||

| Ser. 03-W1, Class 2A, 7 1/2s, 2042 | 839,706 | 868,184 | ||

| Ser. 03-W4, Class 4A, 7 1/2s, 2042 | 512,597 | 530,194 | ||

| Ser. 02-T18, Class A4, 7 1/2s, 2042 | 1,000,969 | 1,037,412 | ||

34

| COLLATERALIZED MORTGAGE OBLIGATIONS (35.2%)* continued | ||||

| Principal amount | Value | |||

| Fannie Mae | ||||

| Ser. 03-W3, Class 1A3, 7 1/2s, 2042 | $ | 2,782,134 | $ | 2,883,465 |

| Ser. 02-T16, Class A3, 7 1/2s, 2042 | 5,707,810 | 5,915,369 | ||

| Ser. 02-T19, Class A3, 7 1/2s, 2042 | 1,128,859 | 1,170,035 | ||

| Ser. 03-W2, Class 1A3, 7 1/2s, 2042 | 512,624 | 531,349 | ||

| Ser. 02-W4, Class A5, 7 1/2s, 2042 | 2,459,945 | 2,546,739 | ||

| Ser. 02-W1, Class 2A, 7 1/2s, 2042 | 69,726 | 71,954 | ||

| Ser. 02-14, Class A2, 7 1/2s, 2042 | 267,397 | 276,695 | ||

| Ser. 01-T10, Class A2, 7 1/2s, 2041 | 1,595,437 | 1,648,459 | ||

| Ser. 02-T4, Class A3, 7 1/2s, 2041 | 1,096,999 | 1,133,712 | ||

| Ser. 02-T6, Class A2, 7 1/2s, 2041 | 381,827 | 394,125 | ||

| Ser. 01-T12, Class A2, 7 1/2s, 2041 | 2,696,210 | 2,785,816 | ||

| Ser. 01-T8, Class A1, 7 1/2s, 2041 | 434,890 | 448,730 | ||

| Ser. 01-T7, Class A1, 7 1/2s, 2041 | 2,691,721 | 2,775,804 | ||

| Ser. 01-T3, Class A1, 7 1/2s, 2040 | 10,007 | 10,323 | ||

| Ser. 99-T2, Class A1, 7 1/2s, 2039 | 148,608 | 154,254 | ||

| Ser. 03-W10, Class 1A1, 7 1/2s, 2032 | 1,336,976 | 1,383,230 | ||

| Ser. 02-T1, Class A3, 7 1/2s, 2031 | 1,984,229 | 2,052,396 | ||

| Ser. 00-T6, Class A1, 7 1/2s, 2030 | 930,078 | 959,132 | ||

| Ser. 02-W7, Class A5, 7 1/2s, 2029 | 271,247 | 280,963 | ||

| Ser. 02-W3, Class A5, 7 1/2s, 2028 | 262,862 | 272,002 | ||

| Ser. 02-26, Class A1, 7s, 2048 | 1,145,981 | 1,172,318 | ||

| Ser. 04-W12, Class 1A3, 7s, 2044 | 824,351 | 846,168 | ||

| Ser. 04-T3, Class 1A3, 7s, 2044 | 1,421,158 | 1,458,232 | ||

| Ser. 04-T2, Class 1A3, 7s, 2043 | 470,848 | 483,161 | ||

| Ser. 03-W8, Class 2A, 7s, 2042 | 4,805,519 | 4,925,302 | ||

| Ser. 03-W3, Class 1A2, 7s, 2042 | 445,551 | 456,417 | ||

| Ser. 02-T16, Class A2, 7s, 2042 | 3,216,199 | 3,294,361 | ||

| Ser. 02-T19, Class A2, 7s, 2042 | 2,138,216 | 2,190,885 | ||

| Ser. 01-T10, Class A1, 7s, 2041 | 903,519 | 923,548 | ||

| Ser. 02-T4, Class A2, 7s, 2041 | 2,199,933 | 2,249,341 | ||

| Ser. 04-W1, Class 2A2, 7s, 2033 | 3,318,568 | 3,404,103 | ||

| IFB Ser. 05-74, Class CP, 6.119s, 2035 | 1,066,058 | 1,019,366 | ||

| IFB Ser. 05-76, Class SA, 6.119s, 2034 | 754,610 | 713,667 | ||

| IFB Ser. 05-74, Class CS, 6.047s, 2035 | 1,215,471 | 1,159,587 | ||

| IFB Ser. 06-27, Class SP, 5.935s, 2036 | 651,000 | 615,802 | ||

| IFB Ser. 06-8, Class HP, 5.935s, 2036 | 836,695 | 780,607 | ||

| IFB Ser. 06-8, Class WK, 5.935s, 2036 | 1,255,250 | 1,168,191 | ||

| IFB Ser. 05-106, Class US, 5.935s, 2035 | 1,291,171 | 1,231,644 | ||

| IFB Ser. 05-99, Class SA, 5.935s, 2035 | 632,663 | 597,913 | ||

| IFB Ser. 05-74, Class DM, 5.752s, 2035 | 1,221,794 | 1,143,901 | ||

| IFB Ser. 05-114, Class SP, 5.607s, 2036 | 357,203 | 326,171 | ||

| IFB Ser. 05-95, Class CP, 4.796s, 2035 | 101,747 | 95,049 | ||

| IFB Ser. 05-106, Class JC, 4.368s, 2035 | 516,134 | 430,407 | ||

| IFB Ser. 05-83, Class QP, 4.183s, 2034 | 404,274 | 351,679 | ||

| IFB Ser. 05-93, Class AS, 4.172s, 2034 | 282,556 | 243,164 | ||

| IFB Ser. 05-57, Class MN, 3.919s, 2035 | 896,663 | 824,894 | ||

| IFB Ser. 05-56, Class TP, 2.906s, 2033 | 231,260 | 196,447 | ||

| IFB Ser. 03-66, Class SA, IO, 2.569s, 2033 | 1,228,408 | 94,242 | ||

| IFB Ser. 03-48, Class S, IO, 2.469s, 2033 | 547,440 | 38,748 | ||

35

| COLLATERALIZED MORTGAGE OBLIGATIONS (35.2%)* continued | ||||

| Principal amount | Value | |||

| Fannie Mae | ||||

| IFB Ser. 05-113, Class DI, IO, 2.149s, 2036 | $ | 8,528,591 | $ | 490,750 |

| IFB Ser. 04-51, Class S0, IO, 1.969s, 2034 | 308,857 | 14,478 | ||

| IFB Ser. 05-65, Class KI, IO, 1.919s, 2035 | 12,419,340 | 652,786 | ||

| IFB Ser. 05-90, Class SP, IO, 1.669s, 2035 | 2,007,491 | 109,810 | ||

| IFB Ser. 05-82, Class SW, IO, 1.649s, 2035 | 4,608,727 | 181,829 | ||

| IFB Ser. 05-82, Class SY, IO, 1.649s, 2035 | 5,864,011 | 231,354 | ||

| IFB Ser. 05-45, Class EW, IO, 1.639s, 2035 | 8,946,415 | 400,082 | ||

| IFB Ser. 05-47, Class SW, IO, 1.639s, 2035 | 3,038,503 | 117,267 | ||

| IFB Ser. 05-105, Class S, IO, 1.619s, 2035 | 900,085 | 40,926 | ||

| IFB Ser. 05-95, Class CI, IO, 1.619s, 2035 | 1,342,572 | 70,240 | ||

| IFB Ser. 05-84, Class SG, IO, 1.619s, 2035 | 2,351,606 | 134,452 | ||

| IFB Ser. 05-87, Class SG, IO, 1.619s, 2035 | 2,990,530 | 135,041 | ||

| IFB Ser. 05-89, Class S, IO, 1.619s, 2035 | 8,301,708 | 321,043 | ||

| IFB Ser. 05-69, Class AS, IO, 1.619s, 2035 | 613,092 | 29,984 | ||

| IFB Ser. 05-104, Class NI, IO, 1.619s, 2035 | 401,395 | 23,694 | ||

| IFB Ser. 04-92, Class S, IO, 1.619s, 2034 | 1,903,823 | 93,704 | ||

| IFB Ser. 05-104, Class SI, IO, 1.619s, 2033 | 3,036,919 | 154,694 | ||

| IFB Ser. 05-83, Class QI, IO, 1.609s, 2035 | 335,130 | 19,284 | ||

| IFB Ser. 06-45, Class SM, IO, 1.6s, 2035 | 1,971,000 | 82,228 | ||

| IFB Ser. 05-92, Class SC, IO, 1.599s, 2035 | 3,164,535 | 169,106 | ||

| IFB Ser. 06-20, Class PI, IO, 1.599s, 2030 | 2,922,624 | 119,133 | ||

| IFB Ser. 05-83, Class SL, IO, 1.589s, 2035 | 6,184,883 | 288,111 | ||