UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

__________________

FORM 20-F

_________________________

| [ ] | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934. |

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2003 |

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSACTION PERIOD FROM ______________ TO ___________________ |

Commission File Number 0-18939

BERKLEY RESOURCES INC.

(Exact name of Company as specified in its charter)

A CORPORATION FORMED UNDER THE LAWS OF BRITISH COLUMBIA, CANADA

(Jurisdiction of Incorporation or Organization)

455 Granville Street, Suite 400

Vancouver, British Columbia V6C 1T1

Canada

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act: NONE

Securities registered or to be registered pursuant to Section 12(g) of the Act:

________________________________

Common Shares, without Par Value (Title of Class) |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: NONE

The number of outstanding Common Shares as of December 31, 2003 was 6,810,934.

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark which financial statement item the Company has elected to follow.

Item 17 [X] Item 18 [ ]

(Applicable only to issuers involved in bankruptcy proceedings during the past five years)

Indicate by check mark whether the Company has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. NOT APPLICABLE

TABLE OF CONTENTS

| Introduction...................................................................................................................................................................................................................................................3 |

| Currency.........................................................................................................................................................................................................................................................3 |

| Forward-looking Statements......................................................................................................................................................................................................................3 |

| Part I................................................................................................................................................................................................................................................................4 |

| Item 1. Identity of Directors, Senior Management and Advisors.................................................................................................................................................4 |

| Item 2. Offer Statistics and Expected Timetable...............................................................................................................................................................................4 |

| Item 3. Key Information.......................................................................................................................................................................................................................4 |

| Item 4. Information on the Company.................................................................................................................................................................................................9 |

| Item 5. Operating and Financial Review and Prospects................................................................................................................................................................14 |

| Item 6. Directors, Senior Management and Employees................................................................................................................................................................17 |

| Item 7. Major Shareholders and Related Party Transactions.......................................................................................................................................................21 |

| Item 8. Financial Information.............................................................................................................................................................................................................21 |

| Item 9. The Offer and Listing............................................................................................................................................................................................................22 |

| Item 10. Additional Information........................................................................................................................................................................................................23 |

| Item 11. Quantitative and Qualitative Disclosures About Market Risk.....................................................................................................................................27 |

| Item 12. Description of Securities Other than Equity Securities..................................................................................................................................................27 |

| Part II............................................................................................................................................................................................................................................................27 |

| Item 13. Defaults, Dividend Arrearages and Delinquencies........................................................................................................................................................27 |

| Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds.......................................................................................................27 |

| Item 15. Controls and Procedures....................................................................................................................................................................................................27 |

| Item 16. [Reserved].............................................................................................................................................................................................................................28 |

| Item 16A. Audit Committee Financial Expert..................................................................................................................................................................................28 |

| Item 16B. Code of Ethics....................................................................................................................................................................................................................28 |

| Item 16C. Principal Accountant Fees and Services.......................................................................................................................................................................28 |

| Item 16D. Exemptions from the Listing Standards for Audit Committees..................................................................................................................................28 |

| Item 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers..................................................................................................................28 |

| Part III...........................................................................................................................................................................................................................................................29 |

| Item 17. Financial Statements............................................................................................................................................................................................................29 |

| Item 18. Financial Statements............................................................................................................................................................................................................29 |

| Item 19. Exhibits..................................................................................................................................................................................................................................29 |

2

Introduction

Berkley Resources Inc., which we refer to as the "Company", was organized under the Company Act of the Province of British Columbia, Canada on July 18, 1986 under the name of Berkley Resources Inc. by virtue of a statutory amalgamation among Fortune Island Mines Ltd., Kerry Mining Ltd. and Berkley Resources Inc. The principal executive office of the Company is located at 455 Granville Street, Suite 400, Vancouver, British Columbia V6C 1T1, and its telephone number is 604-682-3701. The principal business of the Company is that of a drilling participant in various oil and gas properties principally located in Alberta and Saskatchewan, Canada. In August 2001, the Company purchased the remaining interest in the office building that it occupies and became its sole owner. As a result, the Company now leases the other offices that it does not occupy to other businesses.

In this annual report on Form 20-F, which we refer to as the "Annual Report", except as otherwise indicated or as the context otherwise requires, the "Company", "we" or "us" refers to Berkley Resources Inc.

You should rely only on the information contained in this Annual Report. We have not authorized anyone to provide you with information that is different. The information in this Annual Report may only be accurate on the date of this Annual Report or on or as at any other date provided with respect to specific information.

Currency

Unless we otherwise indicate in this Annual Report, all references to "Canadian Dollars", "CDN$" or "$" are to the lawful currency of Canada and all references to "U.S. Dollars" or "U.S. $" are to the lawful currency of the United States

Forward-looking Statements

The following discussion contains forward-looking statements within the meaning of the United States Private Securities Legislation Reform Act of 1995 concerning the Company's plans which may affect the future operating results and financial position. Such statements are subject to risks and uncertainties that could cause our actual results and financial position to differ materially from those anticipated in the forward-looking statements. These factors include, but are not limited to, the factors set forth in the sections entitled "Risk Factors" in Item 3.D., and "Operating and Financial Review and Prospects" in Item 5. Statements concerning reserves and resources may also be deemed to constitute forward-looking statements to the extent that such statements reflect the conclusion that such reserves and resources may be economically exploitable. Any statements that express or involve discussions with respect to predictions, expectations, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as "expects" or "does not expect," "is expected," "anticipates," "does not anticipate," "plans," "estimates," or "intends," or stating that certain actions, events or results "may," "could," "would," or "will" be taken, occur or be achieved) are not statements of historical fact and may be "forward-looking statements."

3

Part I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. Selected Financial Data

The selected historical financial information presented in the table below for each of the years ended December 31, 2003, 2002, 2001, 2000 and 1999, is derived from the audited financial statements of the Company. The audited financial statements and notes for the balance sheets as at December 31, 2003 and December 31, 2002, and the statements of operations for each of the years in the three year period ended December 31, 2003, are included in this Annual Report. The selected historical financial information for the years ended December 31, 2000 and 1999, presented in the table below are derived from financial statements of the Company that are not included in this Annual Report. The selected financial information presented below should be read in conjunction with the Company's financial statements and the notes thereto (Item 17) and the Operating and Financial Review and Prospects (Item 5) included elsewhere in this Annual Report.

The selected financial information for each of the years ended December 31, 2003, 2002 and 2001 has been prepared in accordance with Canadian generally accepted accounting principles, which is referred to as "Canadian GAAP", and United States generally accepted accounting principles, which is referred to as "U.S. GAAP", and the selected financial data for each of the years ended December 31, 2000 and 1999 has been prepared in accordance with Canadian GAAP.

Canadian GAAP | Year Ended December 31 | ||||

2003 | 2002 | 2001 | 2000 | 1999 | |

Operations | |||||

| Oil and Gas Revenue | $606,133 | $406,138 | $637,497 | $678,789 | $488,022 |

| Oil and Gas Production Expense | 243,717 | 189,681 | 257,862 | 184,168 | 148,063 |

| Amortization and Depletion | 79,500 | 39,900 | 482,700 | 97,600 | 66,700 |

| Rental Revenue | 238,599 | 235,670 | 208,592 | 174,025 | 177,463 |

| Rental Operations Expense | 238,884 | 218,318 | 191,879 | 186,734 | 170,973 |

| Net Income (loss) | (255,456) | (127,647) | (292,576) | 201,165 | 62,514 |

| Net Income Per Share (loss) | (0.04) | (.02) | (.051) | .042 | .013 |

As at December 31 | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

Balance Sheet | |||||

| Total Assets | 3,615,691 | 3,829,235 | 3,855,897 | 4,367,927 | 3,773,678 |

| Short Term Debt | 711,222 | 758,102 | 909,017 | 894,059 | 287,665 |

| Shareholders' Equity | 2,767,967 | 3,015,933 | 2,893,580 | 2,986,156 | 2,784,991 |

| Number of shares issued and outstanding | 6,810,934 | 6,795,934 | 5,795,934 | 4,795,934 | 4,795,934 |

U.S. GAAP | Year Ended December 31 | ||||

2003 | 2002 | 2001 | 2000 | 1999 | |

Operations | |||||

| Oil and Gas Revenue | $606,133 | $406,138 | $637,497 | $678,789 | $488,022 |

| Rental Revenue | 238,599 | 235,670 | 208,592 | 174,025 | 177,463 |

| Net Income (loss) | (255,456) | (191,847) | (240,576) | 183,965 | 44,514 |

| Net Income Per Share (loss) | (0.04) | (0.03) | (0.042) | 0.038 | 0.009 |

As at December 31 | |||||

2003 | 2002 | 2001 | 2000 | 1999 | |

Balance Sheet | |||||

| Total Assets | 3,811,591 | 3,927,035 | 4,039,497 | 4,499,527 | 3,922,478 |

| Total Liabilities | 847,724 | 813,302 | 962,317 | 1,381,771 | 988,687 |

| Shareholders' Equity | 2,865,767 | 3,113,733 | 3,077,180 | 3,117,756 | 2,933,791 |

4

Exchange Rates

The following table sets forth information as to the period end, average, high and low exchange rate data for Canadian Dollars and U.S. Dollars for the periods indicated based on the noon buying rate in New York City for cable transfers in Canadian Dollars as certified for customs purposes by the Federal Reserve Bank of New York (Canadian dollar = U.S. $1).

Year Ended: December 31 | Average | Period End | High | Low |

| 2000 | 1.4855 | 1.4995 | 1.5600 | 1.4350 |

| 2001 | 1.5487 | 1.5925 | 1.6023 | 1.4933 |

| 2002 | 1.5704 | 1.5800 | 1.6128 | 1.5108 |

| 2003 | 1.4008 | 1.2923 | 1.5750 | 1.2923 |

| 2004 | 1.3017 | 1.2034 | 1.3970 | 1.1775 |

The following table sets forth the high and low exchange rate for the past six months. As of June 21, 2005, the exchange rate was $1.2310 for each U.S. $1.00.

Month | High | Low | |||||

| December 2004 | $ | 1.2401 | $ | 1.1856 | |||

| January 2005 | $ | 1.2422 | $ | 1.1982 | |||

| February 2005 | $ | 1.2562 | $ | 1.2294 | |||

| March 2005 | $ | 1.2463 | $ | 1.2017 | |||

| April 2005 | $ | 1.2568 | $ | 1.2146 | |||

| May 2005 | $ | 1.2703 | $ | 1.2373 | |||

5

B. Capitalization and Indebtedness

Not Applicable.

C. Reasons for the Offer and Use of Proceeds

Not Applicable.

D. Risk Factors

In addition to the other information presented in this Annual Report, the following should be considered carefully in evaluating the Company and its business. This Annual Report contains forward-looking statements that involve risk and uncertainties. The Company's actual results may differ materially from the results discussed in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed below and elsewhere in this Annual Report.

Failure to Locate Commercial Quantities of Hydrocarbons and Geological Risks. There is no assurance that commercial quantities of hydrocarbons will be discovered. Geological conditions are variable and of limited predictability. Even if production is commenced from a well or field, production will inevitably decline over the course of time, reducing the operating profitability of the enterprise and eventually causing its termination.

Oil and Natural Gas Prices.The Company has little control over the price it receives for its products. Prices are determined by the worldwide supply of and demand for energy. Levels of production maintained by the Organization of Petroleum Exporting Countries, referred to as "OPEC", member nations and other major oil producing countries are expected to continue to be a major determinant of oil price movements in the future. As a result, future oil price movements cannot be predicted with any certainty. Similarly, during the past several years, the market price for natural gas has been subject to significant fluctuations on a monthly basis as well as from year to year. These frequent changes in the market price make it impossible for the Company to predict natural gas price movements with any certainty. Oil prices started the year 2003 at U.S. $32.23 per barrel compared to 2002 at U.S. $19.80 per barrel for West Texas Intermediate, or "WTI". Oil prices held steady throughout 2003 to close at year-end 2003 at U.S. $32.78. The 2003 full year average price for WTI was U.S. $30.99 compared to $26.15 per barrel in 2002. Natural gas prices opened the year 2003 at Cdn $6.18 per thousand cubic feet, referred to as "mcf", and closed year-end at Cdn $6.38. The full year 2003 average price for natural gas at the Alberta Energy Company trading hub at Suffield, Alberta, referred to as "AECO", was Cdn $6.70 compared to an average of Cdn $4.07 for year 2002.

The Company cannot provide assurance that it will be able to market all oil or natural gas that the Company produces or, if such oil or natural gas can be marketed, that favorable price and contractual terms can be negotiated. Changes in oil and natural gas prices may significantly affect the revenues and cash flow of the Company and the value of its oil and natural gas properties. Further, significant declines in the prices of oil and natural gas may have a material adverse effect on the business and financial condition of the Company.

It May Be Difficult to Enforce Civil Liabilities Against the Company. Because the assets of the Company and its subsidiary, as well as the Company¢s jurisdiction of incorporation and the residences of its officers and directors, are mostly located outside of the United States, it may be difficult or impossible to enforce judgments granted by a court in the United States against the assets of the Company and its subsidiaries or the directors and officers of the Company who reside outside the United States.

Operating History and Significant Historical Operating Losses.We commenced operations in the early 1980’s. We have seven major areas in production. The majority of wells on the properties, proved reserves and future production attributable to these properties are more susceptible to estimation discrepancies than fields with larger reserves and longer production histories.

We experienced earnings in fiscal 1999 and 2000 of $62,514 and $201,165 respectively. In fiscal 2001, 2002 and 2003, we reported losses of $292,576, $127,647 and $255,456, respectively. As at December 31, 2003, we had an accumulated deficit of $563,849. Our future viability should be considered in light of the risks and difficulties frequently encountered by companies engaged in the junior stages of oil and gas exploration, development and production activities.

Penny Stock Rules May Make it More Difficult to Trade the Company's Common Shares.The Securities and Exchange Commission, which we refer to as the "SEC", has adopted regulations which generally define a "penny stock" to be any equity security that has a market price, as defined, of less than U.S.$5.00 per share or an exercise price of less than U.S.$5.00 per share, subject to certain exceptions. Our securities may be covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and accredited investors such as institutions with assets in excess of U.S.$5,000,000 or an individual with net worth in excess of U.S.$1,000,000 or annual income exceeding U.S.$200,000 or U.S.$300,000 jointly with his or her spouse. For transactions covered by this rule, the broker-dealers must make a special suitability determination for the purchase and receive the purchaser¢s written agreement of the transaction prior to the sale. Consequently, the rule may affect the ability of broker-dealers to sell our securities and also affect the ability of our investors to sell their shares in the secondary market.

6

No Reliable Information Regarding Reserves. The Company has engaged independent petroleum consultants to compile oil and gas reserve information with respect to its major properties and does have reliable information regarding the quantities of natural gas or oil that may be recoverable from these properties in future years, if any. There can be no assurance, however, that such information has been accurately compiled or is not based on assumptions which may prove to be inaccurate. Furthermore, if any one of our major properties stop producing, it could have a material adverse effect on our business, financial condition and operating results.

We are Dependent on Seven Areas. The Company currently receives substantially all of its income from seven discrete areas. If any one of the seven areas stop producing, it could have a material adverse effect on our business, financial condition and operating results.

Risks Pertaining to Acquisitions and Joint Ventures. Part of our business strategy is to expand through acquisitions and is therefore dependent upon our ability to complete suitable acquisitions and effectively integrate acquired assets into our operations. Suitable acquisitions, on terms acceptable to us, may not be available in the future or may require us to assume certain liabilities, including, without limitation, environmental liabilities, known or unknown.

Exploration and Development Risks. Exploration and development of natural gas and oil involves a high degree of risk that no commercial production will be obtained or that the production will be insufficient to recover drilling and completion costs. The costs of drilling, completing and operating wells is sometimes uncertain, and cost overruns in exploration and development operations can adversely affect the economics of a project. Our drilling operations may be curtailed, delayed or canceled as a result of numerous factors, including title problems, joint venture partner and/or operator decisions, equipment failures, weather conditions, marine accidents, fires and explosions, compliance with governmental requirements, and shortages or delays in the delivery of equipment. Furthermore, the completion of a well does not ensure a profit on the investment or a recovery of drill, completion and tie-in costs.

Replacement of Reserves. In general, the rate of production from natural gas and oil properties declines as reserves are depleted. The rate of decline depends on reservoir characteristics and other factors. Except to the extent we acquire properties containing proven reserves or conduct successful exploration and development activities, or both, our estimated proven reserves will decline as reserves are exploited. Our future natural gas and oil production, and therefore cash flow from operations and net earnings, are highly dependent upon our level of success in finding or acquiring additional economically recoverable reserves. The business of exploring for, developing and acquiring reserves is capital intensive. To the extent cash flow from operations is reduced and external sources of capital become limited or unavailable, our ability to make the necessary capital investment to maintain or expand our asset base of natural gas and oil reserves could be materially impaired.

Estimating of Reserves and Future Net Cash Flows Risk.Estimating natural gas, natural gas liquids and crude oil reserves, and future net cash flows includes numerous uncertainties, many of which may be beyond our control. Such estimates are essential in our decision-making as to whether further investment is warranted. These estimates are derived from several factors and assumptions, some of which are:

| · | reservoir characteristics based on variable geological, geophysical and engineering assessments; |

· future rates of production based on historical draw-down rates;

| · | future net cash flows based on commodity price/quality assumptions, production costs, taxes and investment decisions; |

· recoverable reserves based on estimated future net cash flows; and

| · | compliance expectations based on assumed federal, provincial and environmental laws and regulations. |

Ultimately, actual production rates, reserves recovered, commodity prices, production costs, government regulations or taxation may differ materially from those assumed in earlier reserve estimates. Higher or lower differences could materially impact our production, revenues, production costs, depletion expense, taxes and capital expenditures.

Reserve estimates and net present values reported by us elsewhere in this Annual Report are based on estimated commodity prices and associated production costs that are assumed constant for the life of the reserves. Actual future prices and costs may be materially higher or lower.

We have historically invested a significant portion of our capital budget in drilling exploratory wells in search of unproved oil and gas reserves. We cannot be certain that the exploratory wells we drill will be productive or that we will recover all or any portion of our investments. In order to increase the chances for exploratory success, we often invest in seismic or other geoscience data to assist us in identifying potential drilling objectives. Additionally, the cost of drilling, completing and testing exploratory wells is often uncertain at the time of our initial investment. Depending on complications encountered while drilling, the final cost of the well may significantly exceed that which we originally estimated.

Potential Variability in Quarterly Operating Results. Demand for our products will generally increase during the winter because they are often used as heating fuels. The amount of such increased demand will depend to some extent upon the severity of winter. Accordingly, our net operating revenues are likely to increase during winter months, although the amount of increase and its effect on profitability cannot be predicted. Because of the seasonality of our business and continuous fluctuations in the prices of our products, our operating results for any past quarterly period may not necessarily be indicative of results for future periods and there can be no assurance that we will be able to maintain steady levels of profitability on a quarterly or annual basis in the future.

Competition and Business Risk Management. The natural gas and oil industry is highly competitive. We experience competition in all aspects of our business, including: searching for, developing and acquiring reserves; obtaining pipeline and/or facilities processing capacity, leases, licenses and concessions; and obtaining the equipment and labor needed to conduct operations and market natural gas and oil. Our competitors include multinational energy companies, other independent natural gas and oil concerns and individual producers and operators. Because both natural gas and oil are fungible commodities, the principal form of competition with respect to product sales is price competition. Many competitors have financial and other resources substantially greater than those available to us and, accordingly, may be better able to respond to factors such as changes in worldwide natural gas or oil prices, levels of production, the cost and availability of alternative fuels or the application of government regulations. Such factors, which are beyond our control, may affect demand for our natural gas and oil production. We expect a high degree of competition to continue.

7

Shortage of Supplies and Equipment. Our ability to conduct operations in a timely and cost effective manner is subject to the availability of natural gas and crude oil field supplies, rigs, equipment and service crews. Although none are expected currently, any shortage of certain types of supplies and equipment could result in delays in our operations as well as in higher operating and capital costs.

Interruption from Severe Weather. Our operations are conducted principally in Alberta and Saskatchewan. The weather during colder seasons in these areas can be extreme and can cause interruption or delays in our drilling and construction operations.

Dependence on Third-Party Pipelines. Substantially all our sales of oil and natural gas were effected through deliveries to local third-party gathering systems to processing plants in Alberta and Saskatchewan. In addition, we rely on access to interprovincial pipelines for the sale and distribution of substantially all of our gas. As a result, a curtailment of our sale of natural gas by pipelines or by third-party gathering systems, an impairment of our ability to transport natural gas on interprovincial pipelines or a material increase in the rates charged to us for the transportation of natural gas by reason of a change in federal or provincial regulations or for any other reason, could have a material adverse effect upon us. In such event, we would have to obtain other transportation arrangements or we would have to construct alternative pipelines. There can be no assurance that we would have economical transportation alternatives or that it would be feasible for us to construct pipelines. In the event such circumstances were to occur, our field netbacks from the affected wells would be suspended until, and if, such circumstances could be resolved.

Operating Hazards and Uninsured Risks. The oil and gas business involves a variety of operating risks, including fire, explosion, pipe failure, casing collapse, abnormally pressured formations, adverse weather conditions, governmental and political actions, premature reservoir declines, and environmental hazards such as oil spills, gas leaks and discharges of toxic gases. The occurrences of any of these events with respect to any property operated or owned (in whole or in part) by us could have a material adverse impact on us. We, and the operators of our properties, maintain insurance in accordance with customary industry practices and in amounts that we believe to be reasonable. However, insurance coverage is not always economically feasible and is not obtained to cover all types of operational risks. The occurrence of a significant event that is not fully insured could have a material adverse effect on our financial condition.

As our reserves of natural gas, natural gas liquids and crude oil decline, our success at replacing and adding to them is highly reliant on further exploration and development. To the extent we succeed, our operating cash flows and other capital sources may become insufficient so as to impair our ability to re-invest capital.

Kyoto Protocol Risk. The Kyoto Protocol treaty, referred to as the "Protocol", was established in 1997 to reduce emissions of greenhouse gases, referred to as "GHG", that are believed to be responsible for increasing the earth's surface temperatures and affecting the global climate change. Canada ratified the Protocol in December 2002. Since the implementation of the Protocol, approximately 160 countries have committed to reduce GHG internationally. The Protocol was legally made effective internationally on February 16, 2005 and Canada has committed to meet a six percent reduction of emission over base-year 1990 during the period 2008 to 2012. Canadian government assurances of cost and volume limits suggest that incremental risks and liabilities attributable to addressing Protocol related policies are manageable. While we believe we are a low-emission producer, it is not possible to predict the impact of how Protocol-related issues will ultimately be resolved and to what extent their impact will affect our future unit operating costs and capital expenditures.

We will not be able to develop our reserves or make acquisitions if we are unable to generate sufficient cash flow or raise capital. If we are unable to increase our reserves, our business will be adversely affected because we will eventually run out of reserves.We will be required to make substantial capital expenditures to develop our existing reserves, to discover new oil and gas reserves and to make acquisitions. We will be unable to accomplish these tasks if we are unable to generate sufficient cash flow or raise capital in the future.

We are Subject to Government Regulation on the Removal of Natural Gas from Canada. The price of natural gas sold is not regulated and, therefore, is determined by negotiation between buyers and sellers. Exports of natural gas from Canada require the approval of the National Energy Board, or the "NEB". All exports of natural gas require the issuance by the NEB of a license and the approval of the Governor in Council. Exporters are free to negotiate prices with purchasers but natural gas export sales contracts, or any amendment, agreement or change pertaining thereto, requires NEB approval.

The government of Alberta also regulates the removal of natural gas from its province, based on such factors as reserve availability, transportation arrangements and market conditions. In each Canadian province, the relevant regulatory agency must approve any proposed export. The U.S. represents a significant market for Canadian natural gas and any significant change in access to such market will have an effect on the price of natural gas in Canada.

On January 1, 1994, the North American Free Trade Agreement, referred to as “NAFTA”, among the Governments of Canada, the U.S. and Mexico became effective. In the context of energy resources, Canada may only impose restrictions on the export of energy goods to the U.S. or Mexico where such restrictions do not: (i) reduce the proportion of energy resources exported relative to domestic use in Canada; (ii) impose an export price higher than the domestic price; or (iii) disrupt normal channels of supply. All three countries are prohibited from imposing minimum export or import price requirements.

NAFTA prohibits discriminatory border restrictions and export taxes. The agreement also requires each party to seek to ensure that, in the application of any energy regulatory measures, regulatory bodies avoid disruption of contractual arrangements and provide for orderly and equitable implementation appropriate to such measures.

The Company's Investments are Subject to Environmental Regulation. All phases of the oil and natural gas business are subject to environmental regulation pursuant to a variety of Canadian, U.S., federal, provincial, state and municipal laws and regulations, as well as international conventions, which are collectively referred to as the “Environmental Legislation”. Environmental Legislation regulates, among other things, the release, emission, handling, storage, use, transportation and disposal of various substances and wastes associated with the oil and natural gas industry. In addition, Environmental Legislation requires that refineries, pipelines, service stations, wells, facility sites and waste storage and disposal facilities be operated, maintained, decommissioned and reclaimed in accordance with prescribed provincial, territorial or federal standards. A breach of such Environmental Legislation may result in suspension or revocation of necessary licenses and authorizations, liability for clean-up costs, damages and the imposition of fines and penalties.

8

Where they are probable and can be reasonably estimated, future removal and site restoration costs (as those terms are used under the accounting recommendations of the Canadian Institute of Chartered Accountants), net of expected recoveries, are provided for in the Company's financial statements. Costs are estimated in current dollars based on current requirements of Environmental Legislation, costs, technology and industry standards and are included in the capital costs of the oil and gas properties. The liability for site restoration is adjusted annually for the passage of time and revisions to the original estimates. The annual charge is included in operations through depletion and accretion. Removal and site restoration expenditures are charged to the accumulated provision as incurred. Based on these parameters, estimated future removal and site restoration costs primarily related to upstream properties has been provided for in the financial statements of the Company. Not all future removal and site restoration costs are foreseeable and not all such costs, even if foreseeable, can be reasonably estimated based on the parameters noted above and, as such, are not included in the future removal and site restoration cost provisions. Although the Company currently does not expect that its future removal and site restoration costs will have a material adverse effect on its financial condition or results of operations, there can be no assurance that such costs could not have such an effect.

Environmental Legislation also imposes, among other things, restrictions and obligations in connection with the generation, handling, storage, transportation, treatment and disposal of hazardous materials and waste and in connection with spills, releases, and emissions of various substances into the air, soil, subsoil, water and groundwater. In addition, certain types of operations, including exploration and development projects and significant changes to certain existing projects, may require the submission and approval of environmental impact assessments, which could impose additional costs or delays or prevent the completion of a project. Compliance with Environmental Legislation can require significant expenditures, and failure to comply with Environmental Legislation may result in the imposition of fines and penalties. The Company is committed to protecting and conserving the natural environment and complying with applicable Environmental Legislation. The Company believes that it is currently in substantial compliance with all existing material Environmental Legislation. The Company does not believe that the costs of complying with Environmental Legislation will have a material adverse effect on its financial condition or results of operations. However, there can be no assurance that the costs of complying with Environmental Legislation will not have such an effect.

Item 4. Information on the Company

A. History and Development of the Company

The Company was organized under the Company Act of the Province of British Columbia, Canada on July 18, 1986 under the name of Berkley Resources Inc. by virtue of a statutory amalgamation among Fortune Island Mines Ltd., Kerry Mining Ltd. and Berkley Resources Inc. The principal executive office of the Company is located at 455 Granville Street, Suite 400, Vancouver, British Columbia V6C 1T1, and its telephone number is 604-682-3701. The principal business of the Company is that of a drilling participant in various oil and gas properties principally located in Alberta and Saskatchewan, Canada. In August 2001, the Company purchased the remaining interest in the office building that it occupies and became its sole owner. As a result, the Company now leases the other offices that it does not occupy to other businesses.

The Company presently participates in approximately 32 oil and gas wells in Alberta and Saskatchewan ranging from one percent to 35% working interests. Substantially all of the Company's oil and gas revenue is produced from seven discrete areas. Three are natural gas producers, three produce oil and one has a combination of oil and gas. Five areas have been producing for several years while two (one oil and one gas) are new developments. Since December 31, 2001, the Company has made principal capital expenditures of $25,458 for the year ended December 31, 2002, $582,707 for the year ended December 31, 2003 and $2,540,288 for the year ended December 31, 2004. In 2003, a major portion of the expenditures were in connection with the acquisition of the Dollard interest in southwestern Saskatchewan. In 2004, a major portion of the expenditures were incurred in connection with the drilling program conducted on the Brazeau area (as to approximately $1.3 million net) and the Senex area (as to approximately $1.0 million net). In 2005, approximately $1.7 million, gross, of capital expenditures have been made on the 3-D seismic program on the Senex area (as to approximately $0.340 million net) and the Brazeau area program (as to approximately $0.8 million net). In 2005, the Company also divested itself of its interests in a substantial portion of its Halkirk area leases for approximately $112,500. These capital expenditures were primarily financed through the issuance of 2,871,043 common shares for aggregate gross proceeds of $2,680,520.

Effective March 1, 2004, the Company swapped its±7.68% WI in most of its Skiff area leases and 25 oil and injection wells located thereon for a 15 to 20% interest in the Senex area of northern central Alberta. The Senex area now has four completed wells on the acquired lands, three of which are considered capable of producing oil in economic quantities. The Company also sold its interest in a substantial portion of its Halkirk area leases effective March 1, 2005. These were low interest properties with complex partnership issues. These transactions result in the Company presently holding participating interests in approximately 22 oil and gas wells in Alberta capable of production in economic quantities and ten in Saskatchewan.

The Company also owns a 100% interest in an office building and land in the downtown core of Vancouver, British Columbia, Canada.

B. Business Overview

The Company’s principal business activities are the acquisition, development and exploration, production, and marketing of petroleum and natural gas reserves and the management of the Company’s real estate holdings.

The investments made by the Company in petroleum and natural gas properties are chosen on the basis of, among other things: (i) the amount of cash available; (ii) the desired diversification of oil as contrasted by natural gas exploration; (iii) the geographical area in which the property is located; (iv) the nature and extent of available geological and geophysical data concerning the property; and (v) the time at which it is desirable to commence drilling activities, for reasons such as the availability of drilling equipment and the provisions of the drilling rights agreement and other relevant agreements.

9

In making an investment, the Company will enter into an operating agreement, which we refer to as an "Operating Agreement", with other investors. The Operating Agreement sets forth the participating interest of the parties and incorporates the operating procedures manual, referred to as the "Manual", adopted by the Canadian Association of Petroleum Landmen. According to the Manual, the parties' interest and liability in each investment is several, and not joint, with the other participants. The interest of the Company in the lands, wells and equipment is that of tenants in common. Each investor in a drilling property is deemed to be a "Joint Operator", and an "Operator" is the party appointed to carry out the operations of the drilling program for the joint account. The Company would be one of the Joint Operators in any Operating Agreement in which it participates. Each Joint Operator owns a share of the petroleum substances produced from the wells which is proportionate to that Joint Operator's ownership interest. Each Joint Operator, at its own expense, takes in kind and separately disposes of its proportionate share of production. If the Joint Operator fails or refuses to take its share of the products, the Operator has the authority to sell on behalf of that Joint Operator its share of the production. The Operator is delegated the authority to manage the exploration, development and operation of the joint lands. The Operator typically has the authority to commit on behalf of all Joint Operators up to $25,000 without separate written approval of all Joint Operators. Prior to commencement of work on any well covered by the Operating Agreement, the Operator must submit to each Joint Operator a program of drilling and an estimate of drilling costs and completion costs for approval by all Joint Operators.

Any assignment or transfer of the Company¢s interest in an Operating Agreement is subject to the procedures set forth in the Manual. The Company may be required to offer its interest to the Joint Operators prior to attempting a sale to a third party. In addition, the Company may "farmout" a portion of its interest and retain an overriding royalty on production.

The oil and gas industry deals in two basic forms of ownership interests, namely "Working Interest" and "Overriding Royalties":

| (i) | Working Interest, or "WI": WI means the percentage of undivided interest held by a Joint Operator (i.e. leaseholder) in a specific tract of land (i.e. joint lands). The WI held by all Joint Operators in any specific tract of joint lands must total 100%. Each WI party is responsible for its WI percentage share of costs incurred to conduct "work" (i.e. drilling, seismic, production etc.) on the joint lands. WI are always considered to be an active interest in the costs, risks and benefits associated with the joint lands and operations conducted thereon and the oil or gas produced therefrom. |

| (ii) | Overriding Royalties, or "ORR's": ORR's are a specified share of oil and/or gas as and when produced. ORR's are free and clear of costs, risk and expense to the holder of the ORR. Usually ORR's are based on gross production and as such are referred to as "Gross" ORR's or "GORR's". ORR's are considered a passive interest in as much as the holder of an ORR is not subject to any cost, risk or expense, nor is the ORR holder involved in any decision-making with respect to the royalty lands. |

The Company's program for investing in drilling programs is based on several factors. The Company endeavors to obtain and review geological opinions on the property involved and if it is not the Operator of the well, it considers the reputation of the Operator. The Company attempts to identify drilling programs offering a low to medium risk on its investments. The Company also tries to keep a balance between investments in oil and gas. The Company attempts to reduce its risks by spreading its investments over several drilling ventures. The Company has not borrowed money for purposes of investing in any oil or gas venture.

In each investment, the Operator maintains its own staff or retains independent operating personnel (including landmen, geologists, accountants and engineers) that are employed to conduct the oil and gas operations of each joint venture, including supervision of the drilling and producing activities of the joint venture, and therefore the Company does not maintain independent staff or employees. The Operator exercises general control over the activities of the joint venture and has the authority to determine the timing of commencing, completing or abandoning any particular well authorized for drilling by the Joint Operators. The Operator maintains all records which are available to the Company upon reasonable request and at its expense. Most geotechnical information (such as well logs, geological and geophysical interpretative data) remains in the possession of the Operator but is available to a Joint Operator upon request.

Operating Costs and Special Project Charges

In Canada, the relationship of all investors in a drilling program is that of Joint Operators. The property on which drilling is conducted is deemed "joint lands" and is held by the Joint Operators as tenants in common. The Joint Operators are owners of the undeveloped joint lands and each Joint Operator is entitled to its percentage of the production and can dispose of it as it deems necessary. Therefore, the gross revenue from oil or gas production is the percentage of oil and gas owned by the Company which it has sold to a buyer company. Each Joint Operator, such as the Company, must pay its share of the expenses incurred in extracting its share of the production from the well. The Company¢s investment in any one drilling program ranges from approximately $20,000 to $2,000,000, the majority of which must be paid prior to any production revenue being realized.

Company Activity

The Company continues to pursue its dual objectives: (i) to participate in developing new drilling prospects; and (ii) to purchase on-line production whenever the right opportunity is found. Areas of significant Company activity are as follows:

| 1. | John Lake, Alberta (Twp 55 Rge 1 W4M) - This sweet natural gas producing area is located in east central Alberta and was acquired by the Company through a farm in arrangement . The Company holds a 10.00% WI in this area which is operated by Crescent Point Energy Partnership. |

| 2. | Carbon Area, Alberta (Twp 29 Rge 22 W4M) - This natural gas producing area is operated by ATCO Gas and is located in central Alberta. It was acquired by the Company through a joint venture agreement. The Company’s interest is a 6.00% to 10.00% WI. |

| 3. | Halkirk Area, Alberta (Twp 38 Rge 16 W4M) - This oil/natural gas producing area is operated by Compton Petroleum Partnership and is located in east central Alberta. It was acquired by the Company pursuant to a joint venture agreement. The Company’s WI's range from 3.125% to 6.25%. This area is operationally complex due to partnership and processing issues. The Company sold its interest in a substantial portion of the Halkirk properties effective March 1, 2005 for approximately $112,500. |

10

| 4. | Zama/Virgo Area, Alberta (Twp 114 Rge 5 W6M) - The Company holds a 5.00% ORR on this oil production operated by Apache Canada Ltd. It is located in northwest Alberta and was acquired in the mid 1990s by the Company through a lease purchase and farm out arrangement. |

| 5. | Dollard Area, Saskatchewan (Twp 6 Rge 19 W3M) - This on-line oil production was purchased in late 2003 for a cash cost to the Company of $365,970. This property is located in southwestern Saskatchewan. Some infill drilling was conducted in 2004 which should increase the Company’s net daily production from this area to about 25 to 30 barrels per day. Infill drilling, retooling of some facilities and planned cleanup work will use up some cash in the short term. These expenditures are expected to provide increased production and cash flow into 2005 and beyond. |

| 6. | Senex Area, Alberta (Twp 92/93 Rge 6/7 W5M) - This multi-zone prospect was acquired by the Company on March 1, 2004 pursuant to the swap of its Skiff property discussed below. The Company holds a 15% to 20% WI in 14 sections over this oil and gas prospect. An extensive 3-D seismic program was conducted over the joint lands in early 2005 at a cost of approximately $1.7 million (the Company's 20% share amounted to $340,000). Drilling is expected to resume in the middle of 2005. Two suspended wells acquired in the swap were recompleted and placed into production at an initial monthly average of approximately 75 barrels per day. Three additional wells were drilled in late 2004. Two are producing oil while the third is suspended. |

| 7. | Leduc Area, Alberta (Twp 49 Rge 26 W4M) - This D-1 (Wabamun) gas prospect was completed and placed into production in August 2004. This single well produces at 1.4 million cubic feet per day, or "mmcf/d". The Company holds a 4.00% WI in this project. Additional wells are expected to be drilled or tested in 2005. |

| 8. | Crossfield Area, Alberta (Twp 28 Rge 1 W5M) - This natural gas prospect is located 50 miles north of Calgary and is near ready to drill. The property was acquired through a joint leasing program. We have surveyed the location and acquired the surface lease. Formal licencing procedures will take time to complete as this is a “sour-gas” prospect. The Company holds a 35% WI in this project, which has as its primary objective, natural gas in the Crossfield formation at a depth of approximately 9,800 feet. The test well has targeted projected reserves of 30 to 50 billion cubic feet of natural gas and drilling costs are estimated at $2.5 million of which the Company's share is estimated at approximately $875,000. |

| 9. | Brazeau Area, Alberta (Twp 46 Rge 13 W5M) - This Nisku (D-2) natural gas prospect was drilled in the second half of 2004. The Company participated with two major oil and gas operators in completing this project which was placed into production in February 2005 at the initial rate of 4.0 mmfc/d. The Company paid 30% of the well costs to earn its 19.50 % WI. The test well cost approximately $7.1 million of which the Company's share was approximately $2.13 million. |

| 10. | Sturgeon Lake Area, Alberta (Twp 70 Rge 24 W5M) -This oil prospect is a well-defined seismic opportunity with projected recoverable reserves of five to ten million barrels and is located in central Alberta. It was acquired by the Company through a direct joint lease purchase. The Company holds a 27.50% WI in this prospect and it proposes to participate for ±15% of the drilling costs and farm out the remaining ±12.50%. The person to which the Company has farmed out the remaining 12.5% WI expects to complete the purchase of a 28.25% WI and have this project drill-ready by the fourth quarter of 2004. The Company's level of participation in the well costs will be influenced by the surface location obtained by the person to whom the Company has farmed out the remaining 12.5% WI. The preferred but more difficult to obtain surface location closer to the bottom-hole target (which is under Sturgeon Lake) would see well costs of about $2.2 million. The fallback location which is more distant from the bottom-hole target would see drilling costs projected at $3.1 million. |

| 11. | Skiff Area, Alberta (Twp 5 Rge 14 W4M) - The Company swapped its 5% to 10% interests in this oil producing property for a 15% to 20% WI in the Senex area in northern central Alberta effective March 1, 2004. |

| 12. | Other Propects - The Company will continue to seekout and develop new drilling opportunities for its own account and jointly with other operators. |

As reported throughout 2004, high oil and gas prices have provided the larger oil and gas producers with huge amounts of unbudgeted cash which they are now using to purchase on-line production as well as conduct aggressive drilling programs. This is the first time in several years that conventional oil and gas companies have been able or willing to compete with Income Trust Funds for on-line production. The ever increasing prices paid for on-line production and the threat of increasing interest rates has cooled-down Income Trust Funds to some degree. Also, Income Trust Funds must, by design, distribute large amounts of their cash to unit holders. These distributions do not seem to be finding their way back to industry as quickly as in the past thus opening the field to cash strong conventional operators. The Company continues its watch for on-line production that may be found below the radar of both Income Trust Funds and cash strong mid-sized operators; however these opportunities are very limited.

Reserves

Through to December 31, 2003, the Company engaged independent petroleum consultants to compile oil and gas reserve information with respect to its two major producing properties, Skiff and John Lake. The Company had access to similar oil and gas reserve information from other Joint Operators or the Operator of the other major properties. Some information was obtained from the unrelated Joint Operator¢s independent petroleum consultants. Since the Joint Operator for whom the report was prepared had a different percentage ownership from that of the Company, it is necessary to adjust the numbers to reflect the Company¢s percentage of ownership. Furthermore, the oil and gas reserve information relied upon by the Company in its financial statements ascertains the reserves on pricing assumptions which are not permitted under SEC rules but are acceptable under Canadian accounting rules. Effective December 31, 2004, the Company had all of its major producing properties evaluated by independent petroleum consultants who assigned total recoverable reserves to the Company's interest of 541,000 barrels of oil equivalent, or "boe": 40% was comprised of natural gas and 60% was comprised of oil and liquids. Natural gas is converted to boe at the industry standard rate of 6:1. The Company has an average interest of 15.23% in 8.504 billion cubic feet of recoverable natural gas or 1.295 billion cubic feet net, which equates to 216,000 boe, and 20.17% in 1.614 million barrels of recoverable oil which equates to 325,000 barrels net.

11

Competition

The crude oil and natural gas industry, domestically and in the international arena, is highly competitive by nature. The Company must compete with integrated oil and natural gas companies and independent producers and marketers of crude oil and natural gas products in all aspects of the Company's business. This competition extends to exploration, property and asset acquisition and the selling of the Company's crude oil and natural gas products. The financial strength of the Company's competitors may be at times greater than that of the Company.

Government Regulation and Environmental Matters

Government Regulation

On March 28, 1985, an agreement regarding energy pricing and taxation, known as the Western Accord, was entered into by the Government of Canada and the Canadian provinces of Alberta, Saskatchewan and British Columbia. The Western Accord called for the deregulation of Canadian crude oil pricing and marketing, proposed changes to domestic natural gas pricing, and announced the elimination of an amendment to a number of federal oil and gas taxes, charges and incentives. Based on the Western Accord, crude oil pricing, including synthetic oil pricing, was deregulated June 1, 1985, so that prices would be negotiated between the buyer and seller.

On October 31, 1985, the Province of Alberta and the Canadian government reached an agreement that provided a framework for natural gas deregulation. The agreement established a mechanism to allow prices to be negotiated directly between consumers and producers. After November 1, 1985, the price of natural gas exported to the United States or sold in Canada was deregulated.

At the present time, Canadian natural gas is supplied to California by two pipelines: (i) a direct link through the San Francisco based Pacific Gas Transmission Company; and (ii) a displacement link via Pacific International Transmission Company. Both lines are presently committed. Pacific Gas Transmission has announced a proposed expansion of its pipeline which will deliver more Alberta natural gas to California. In 1998, construction of a new pipeline covering approximately 620 miles was completed, running from Alberta to the Montana border and to Opal, Wyoming, connecting with the Kern River Gas Transmission Co. pipeline which runs to southern California. California is an important market for Alberta natural gas producers because of the growing demand for natural gas in that state, but such importance has shifted slightly due to the integration of U.S. Midwest markets through the Alliance Pipeline system, which commenced operations in 1999.

Since 1974, the Province of Alberta has had a program entitled "Price-Sensitive Alberta Royalty Tax Credit Program", referred to as the "Tax Credit Program". The Tax Credit Program provided for a refund of portions of the royalties paid to the Province of Alberta by the producers on the sale of oil and gas produced in Alberta. The refund amount to producers is based on the price received for the oil and gas produced. For financial statement purposes, the Company accounts for the tax credit by reducing its operating expenses by the amount of the credit resulting in an increase in income before taxes. For tax purposes, since it is intended not to be taxed, the amount of the credit is reinstated as an operating expense and thus reduces taxable income. The maximum credit available to a company is $1.0 million.

Environmental Matters

Environmental regulations impose, among other things, restrictions, liabilities and obligations in connection with the generation, handling, use, storage, transportation, treatment and disposal of hazardous substances and waste, and in connection with spills, releases and emissions of various substances to the environment. Environmental regulation also requires that wells, facility sites and other properties associated with our operations be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. In addition, certain types of operations, including exploration and development projects and changes to certain existing projects, may require the submission and approval of environmental impact assessments or permit applications. Compliance with environmental regulation can require significant expenditures, including expenditures for clean up costs and damages arising out of contaminated properties and failure to comply with environmental regulations may result in the imposition of fines and penalties. We believe that we are in substantial compliance with such laws and regulations, however, such laws and regulations may change in the future in a manner which will increase the burden and cost of compliance.

In 1994, the United Nations' Framework Convention on Climate Change came into force and three years later led to the Protocol which requires, upon ratification, nations to reduce their emissions of carbon dioxide and other greenhouse gases. In December 2002, the Canadian federal government ratified the Protocol. If certain conditions are met and the Protocol enters into force internationally, Canada will be required to reduce its GHG emissions. Currently, the upstream crude oil and natural gas sector is in discussions with various provincial and federal levels of government regarding the development of GHG regulations for the industry. It is premature to predict what impact these potential regulations could have on the Company's sector but it is possible that the Company would face increases in operating costs in order to comply with a GHG emissions target.

Certain laws and governmental regulations may impose liability on us for personal injuries, clean-up costs, environmental damages and property damages, as well as administrative, civil and criminal penalties. We maintain limited insurance coverage for sudden and accidental environmental damages, but do not maintain insurance coverage for the full potential liability that could be caused by sudden and accidental environmental damage. Accordingly, we may be subject to liability or may be required to cease production from properties in the event of such damages.

Each province in Canada has its own regulatory authorities which oversee, licence and monitor all oil and gas activity including seismic, drilling, production, transportation, processing and environmental matters related thereto. In Alberta, where most of the Company’s assets are located, that authority is the Alberta Energy and Utilities Board or the "AEUB". In order to explore any claim or lease, it is necessary to obtain a geophysical or drilling license and it may be necessary to post a bond with notices to several Canadian governmental agencies, including the provincial environmental agency. The procurement of drilling licenses has had no material adverse impact on the Company¢s operations. In certain areas defined as "sensitive areas," the provincial environmental agency requires special work permits. The Company's investments do not include property located within any defined "sensitive areas".

12

Interruption from Severe Weather

Presently, our operations are conducted principally in the central region of Alberta and in Saskatchewan. The weather can be extreme at times due to cold or rain which can cause interruption or delays in our drilling and construction operations.

C. Organizational Structure

The Company has no subsidiaries.

D. Property, Plants and Equipment

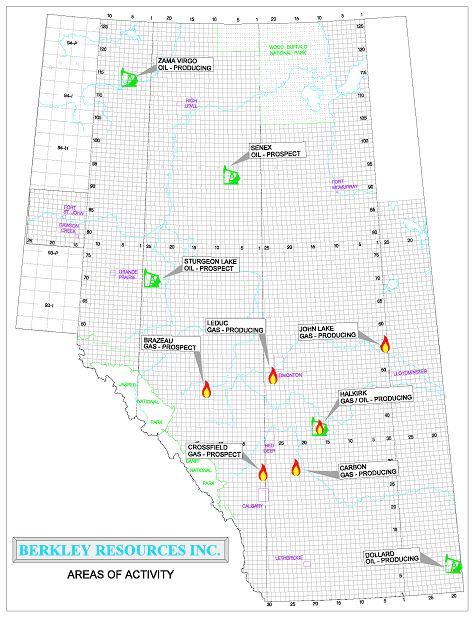

The Company is in the business of participating in various oil and gas drilling ventures in Alberta and Saskatchewan, by entering into Operating Agreements with other investors. Operating Agreements specify that each investors' ownership in the lands, wells and equipment is that of tenants-in-common. The following map sets forth the Company's more significant areas of activity:

The following is a description of the various interests of the Company in its oil and gas properties as at June 1, 2005:

Lease No. | Description | Interest | Status |

Berry | |||

34305 | Sec.29-27-13 W4M | 8.92867% | Not Producing |

Brazeau | Sec.13-46-13 W5M | 30.00% WI BPO | Producing - gas |

| 19.50% WI APO | |||

Carbon | |||

| 047790068 | Sec.29-29-22 W4M | 6%WI | Producing - gas |

| 32443 | Sec.32-29-22 W4M | 6.25%WI | Producing - gas |

| 25906 | Sec.28-29-22 W4M | 6.25%WI | Producing - gas |

| 0477010002 | Sec.31-29-22 W4M | 10%WI | Producing - gas |

Crossfield | Twp 28 Rge 1 W5M | 35% WI | Prep. to drill |

Dollard Economy Creek | Twp 6/7 Rge 19 W3M | 20% WI | Producing - oil |

5498120007 5498120007 5498120008 5498120008 | Sec.3-70-1W6M Sec.10-70-1W6M Secs.4, 5, 8&9-70-1W6M Sec.17-70-1W6M | 25%WI 50%WI 25%WI 50%WI | Not Producing Not Producing Not Producing Not Producing |

0598040371 | Secs.20&21-70-1 W6M | 50%WI | Not Producing |

North Halkirk | |||

| 34397 | Sec.14-39-16 W4M | 6.25%WI | Not Producing |

| 34398 | S1/2 & N1/2 Sec.22-39-16 W4M | 6.25%WI | Not Producing |

26457 | N/2 Sec.22-39-16 W4M | 6.25%WI | Not Producing |

South Halkirk | |||

| 34282 | Sec.16 38-16 W4M | 3.125%WI | Producing - gas/oil |

| 32298 | Sec.20-38-16 W4M | 6.25%WI | Producing - gas/oil |

| Freehold | Sec.E/2 19-38-16 W4M | 6.25%WI | Producing - gas/oil |

| Freehold A-8057 | Sec.8-38-16 W4M | 6.25%WI | Producing - gas/oil |

| PanCan PNG 16258 | NE/4 Sec.17-38-16 W4M | 6.25%WI | Producing - gas/oil |

| 0478020150 | S/2&NE/4 Sec.18-38-16 W4M | 3.125%WI | Producing - gas/oil |

0478080305 | SE/4 Sec.20-38-16 W4M | 0.75%WI | Producing - gas/oil |

Haven | |||

| 047939297 | Sec.12-25-4 W4M | 0.3%WI | Not Producing |

| Sec.7, 18-25-3 W4M | 0.3%WI | Not Producing | |

38054 | Sec.7, 18&20-25-4 W4M | 0.50%WI | Not Producing |

John Lake | |||

| 40852 | All Sec.26&27-55-1 W4M | 10%WI | Producing - gas |

| Sec.1-56-1 W4M | 10%WI | Producing - gas | |

| 485070102 | W/2 36-55-1 W4M | 10%WI | Producing - gas |

| 487040220 | E/2 Sec.36-55-1 W4M | 10%WI | Producing - gas |

| 40854 | NW/4 12-56-1 W4M SE/4 14-56-1-W4M | 10%WI 10%WI | Producing - gas Producing - gas |

| 40853A | All Sec.15-56-1-W4M | 10%WI | Producing - gas |

| 40855A | All Sec.24-56-1 W4M | 10%WI | Producing - gas |

| 40856 | All Sec.34-56-1 W4M | 10%WI | Producing - gas |

Leduc Manyberries | All Sec.33-49-26 W4M | 4% WI | Producing - gas |

| 35828 | SE Sec.23-5-5 W4M | 50%WI | Not Producing |

| 26592 | W/2 Sec.23-5-5 W4M | 50%WI | Not Producing |

| 01818 | NE/4 Sec.23-5-5 W4M | 50%WI | Not Producing |

Oyen | |||

| 30364 | S/2 Sec.16-29-4 W4M | 1%WI | Not Producing |

| 30365 | SW/4 Sec. 24-29-5 W4M | 0.750%WI | Not Producing |

| 29517 | N/2 Sec.24-29-5 W4M | 0.750%WI | Not Producing |

Senex | Twp 92/93 Rge 6/7 W5M | 15/20% WI | Producing - oil |

Sibbald | |||

| 39367 | Sec.2,4, E/2 9&10-28-1 W4M | 0.50%WI | Producing - gas |

| 0476122257 | W/2 9-28-1 W4M Sec.3-28-1 W4M | 0.25%WI 0.25%WI | Not Producing Not Producing |

| 29513 | S/2 Sec.15-28-1 W4M | 1.00%WI | Producing - gas |

| 6359A | N/2 Sec.15&S/2 Sec.22-28-1 | 1.00%WI | Not Producing |

Skiff | |||

| Sawtooth | NW1/4Sec.16,SE1/4Sec.20;Lsds 2, 7&8 & SW1/4Sec.21-5-14 W4M | 7.67%WI | Producing - oil |

| 0484080300 | NW1/4Sec.29-4-14 W4M | 10.526%WI | Producing - oil |

| W1/2Sec.32-4-14 W4M | 5.26315% | Producing - oil | |

| 048307070286 | Lsds.3,4&5 of Sec.5-5-14 | 5.50%WI | Producing - oil |

| Lsds.6 of Sec.5-5 14 W4M | 5.50%WI | Producing - oil | |

| NW1/4 of Sec.9-5-14 W4M | 5.50%WI | Producing - oil | |

| 32596 | Lsd.5 of Sec.16-5-14 W4M | 10%WI | Producing - oil |

| 0483030060 | NW1/4 of Sec.16-5-14-W4M | 10%WI | Producing - oil |

| 0496100384 | W1/2&Lsd.10,15-5-14 W4M | 10%WI | Producing - oil |

| 36854 | Lsd.1&NW1/4 of Sec.21-5-14 | 10%WI | Producing - oil |

| Lsds.2,7&8 & SW1/4 of Sec.21-5-14 W4M | 10%WI | Producing - oil | |

| 7865A | NE1/4 of Sec.21-5-14 W4M | 10%WI | Producing - oil |

| 0486070002 | NW1/4 of Sec.22-5-14 W4M | 6.30%WI | Producing - oil |

| 0477080167 | SW1/4 of Sec.28-5-14 W4M | 10%WI | Producing - oil |

Sturgeon Lake | |||

| 5495080092 | Sec.23,26,27,34,35-70-24 W5M | 27.5%WI | Not Producing |

Zama Virgo | |||

| 0591080261 | N/2 Sec.20-114-5 W6M | 5.00% GORR | Producing - oil |

| 091120175 | NW/4 Sec.26-114-5 W6M | 5.00% GORR | Producing - oil |

| 092020380 | W/2 Sec.22-115-5 W6M | Sliding Scale ORR | Producing - oil |

| 093020449 | SE/4 Sec.27-114-5 W6M | 50% of 10% GORR | Producing - oil |

Office Building | |||

455 Granville Street Vancouver, Canada | Lot B, Block 22, District Lot 541, Plan 8227 | 100% | N/A |

13

Productive Wells and Acreage

The following chart of the Company's total gross and net productive wells, expressed separately for oil and gas, and the total gross and net developed acres (i.e., acres spaced or assignable to productive wells) by the geographic areas is as at June 1, 2005.

GeographicRegion | Total GrossWells | Total Net ProductiveWells | Target OilOr Gas | Total GrossDeveloped Acres | Total NetDeveloped Acres |

| Alberta | 22 | 1.1 oil - 2.0 gas | both | 12,166 | 2,433 |

| Saskatchewan | 10 | 2 | oil | 4,480 | 850 |

Undeveloped Acreage

As at June 1, 2005, the amounts of undeveloped acreage, both leases and concessions, in the western Canada (Alberta) geographic area consists of 40,554 gross acres and 5,488 net acres. The remaining terms on the leases within those properties are variable. Producing leases continue for duration of productive lives.

Drilling Activity

The following table explains the number of productive and dry exploratory or development wells drilled in the last three fiscal years. A dry well (hole) is an exploratory or a development well found to be incapable of producing either oil or gas in sufficient quantities to justify completion as an oil or gas well. A productive well is an exploratory or a development well that is not a dry well. The number of wells drilled refers to the number of wells (holes) completed at any time during the fiscal years, regardless of when drilling was initiated. The term "completion" refers to the installation of permanent equipment for the production of oil or gas, or, in the case of a dry hole, to the reporting of abandonment to the appropriate agency.

Delivery Commitments

The Company has no obligation to provide a fixed and determinable quantity of oil or gas in the near future under existing contracts or agreements or material information concerning the estimated availability of oil and gas from any principal sources.See also Item 3. D. Risk Factors regarding quantity and price limitation by government agencies.

Item 5. Operating and Financial Review and Prospects

This discussion and analysis of the operating results and the financial position of the Company for the years ended December 31, 2003 and 2002 should be read in conjunction with the financial statements and the related notes attached hereto.

A. Operating Results

The Company's principal business is participating in various oil and gas drilling ventures in western Canada. The Company has interests in various wells which vary from 1.00% to 35% and covers, as at December 31, 2003, approximately 50 oil and gas wells. Based on its oil and gas revenues for the year ended December 31, 2003, the Company received substantially all of its income from five properties: (i) John Lake; (ii) Skiff; (iii) Zama/Virgo; (iv) Halkirk; and (v) Carbon. In December 2003 the Company purchased on-line oil production in Dollard, Saskatchewan which produces approximately 25 barrels per day net. The effect of this purchase will be reflected in the 2004 results.

Overall Performance

The Company operates in two distinct segments, oil and gas and real estate rental. An overview analysis by segment is as follows:

Oil and Gas

The Company has continued its commitment to prospect development with the objective of bringing prospects to drilling stage and then farming out the drilling to other parties. The strong cash position enjoyed by many operators due to high oil and gas prices has resulted in a strong demand for drillable prospects. The Company expects this situation to enable it to leverage-up its investment in prospects developed by it and brought to drilling stage.

During the year ended December 31, 2003, the Company participated in approximately 40 oil and gas wells in Alberta and ten in Saskatchewan ranging from 1% to 35% working interests. Substantially all of the oil and gas revenue the Company received in 2003 was from five major leases: John Lake; Halkirk; Carbon; Skiff; and Zama/Virgo. There are four producing gas wells in John Lake; four gas wells in Carbon; seven producing gas wells in Halkirk; 20 producing oil wells in Skiff and two producing oil wells in Zama/Virgo. All five areas have been producing for over ten years. The Company was not the Operator of any of these wells.

Oil and Gas Industry Overview

Sustained strong pricing for both oil and natural gas continued to be the dominant issue for the industry throughout the fiscal year 2003. Oil prices opened on January 1, 2003 at U.S. $32.23 per barrel for WTI and closed at December 31, 2003 at $32.78. Natural gas prices reflected the strong oil prices by increasing from Cdn. $6.18 per mcf at January 1, 2003 to close December 31, 2003 at $6.68. Natural gas storage throughout North America was filled on schedule which should provide a calming influence on prices into 2004. Regardless of this factor, the large amounts of unbudgeted cash accruing to the industry from high commodity prices is having an unsettling effect on everything from land prices to cost of field services. The Company has attempted to navigate a prudent course through these volatile circumstances, seeking out long-term opportunities in this overheated environment.

14

The Company has positioned itself to grow its cash flow by enhancing existing properties while at the same time investing in new opportunities that will expose the Company to substantial growth. The Company intends to continue with these dual objectives throughout 2004 and into 2005 with the awareness that success in one or more of its exploration projects will significantly enhance shareholder value and change the nature of the Company’s oil and gas operations.

Real estate

The office building continues to have near full occupancy, with consistent operating results within a narrow range. In all material respects, the building achieves breakeven on an operating and cash flow basis. There are no changes foreseen with respect to this segment.

Results of Operations

The Company's balance sheet as at December 31, 2003, as compared to December 31, 2002, reflects its expenditures on oil and gas properties and equipment and rental income for the period ended December 31, 2003 and the results of its operations for fiscal year December 31, 2003. Overall, total assets decreased by $213,544 and total liabilities increased by $34,422. The Company's working capital decreased from $431,740 at December 31, 2002 to a working capital deficiency of $280,293 at December 31, 2003.

Revenues