UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant To Section 14(a) of the

Securities Exchange Act of 1934 (Amendment No. )

Filed by the Registrant S

Filed by a Party other than the Registrant o

Check the appropriate box:

o Preliminary Proxy Statement

o Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

o Definitive Proxy Statement

S Definitive Additional Materials

o Soliciting Material Under § 240.14a-12

DELCATH SYSTEMS, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

S No fee required.

o Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

(3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

o Fee paid previously with preliminary materials.

o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number or the form or schedule and the date of its filing.

(1) Amount Previously Paid:

(2) Form, Schedule or Registration Statement No.:

(3) Filing Party:

(4) Date Filed:

Delcath Systems, Inc.

(NASDAQ: DCTH)

The Future of High-Dose Drug Delivery

September 2006

|  |

Forward-looking Statements

- --------------------------------------------------------------------------------

This presentation contains “forward-looking statements” which are subject to

certain risks and uncertainties that can cause actual results to differ

materially from those described. Factors that may cause such differences

include, but are not limited to, uncertainties relating to our ability to

successfully complete Phase 3 clinical trials and secure regulatory approval of

our current or future drug-delivery system and uncertainties regarding our

ability to obtain financial and other resources for any research, development

and commercialization activities. These factors, and others, are discussed from

time to time in our filings with the Securities and Exchange Commission. You

should not place undue reliance on these forward-looking statements, which speak

only as of the date they are made. Delcath undertakes no obligation to publicly

update or revise these forward-looking statements to reflect events or

circumstances after the date they are made.

- --------------------------------------------------------------------------------

2

|  |

Additional Information

- --------------------------------------------------------------------------------

On August 17, 2006, Laddcap Value Partners LP (“Laddcap”) filed a definitive

consent solicitation statement with the Securities and Exchange Commission

(“SEC”) relating to Laddcap’s proposal to, among other things, remove the

current Board of Directors and replace them with Laddcap’s nominees. In

response, on August 21, 2006, Delcath Systems Inc. (“Delcath”) filed a

definitive consent revocation statement on Form DEFC14A (the “Definitive Consent

Revocation Statement”) with the SEC in opposition to Laddcap’s consent

solicitation. Delcath shareholder should read the Definitive Consent Revocation

Statement (including any amendments and supplements thereto) because it contains

additional information important to the shareholders’ interests in

Laddcap’s consent solicitation.

The Definitive Consent Revocation Statement and other public filings made by

Delcath with the SEC are available free of charge at the SEC’s website at

www.sec.gov. Delcath also will provide a copy of these materials free of charge

upon request to Delcath, Attention: M.S. Koly, President and Chief Executive

Officer, (203) 323-8668.

- --------------------------------------------------------------------------------

3

|  |

Introduction

- --------------------------------------------------------------------------------

- - Thank you for this opportunity to speak with you about Delcath Systems

- - We are continuing to make significant progress towards our goal of

developing the first approved, repeatable high-dose, organ isolation

targeted therapy system

- - We strongly believe that the current board and management team is the

right group to fulfill this goal and to continue executing on Delcath’s

growth strategy

- --------------------------------------------------------------------------------

Do Not Turn Over Control of Delcath to Laddcap

DO NOT VOTE THE BLUE CARD

- --------------------------------------------------------------------------------

4

|  |

The Consent Solicitation

- --------------------------------------------------------------------------------

|  |

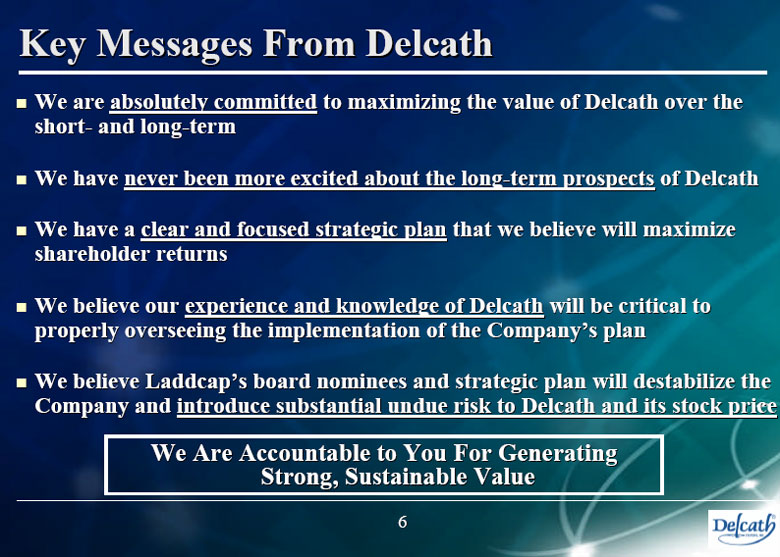

Key Messages From Delcath

- --------------------------------------------------------------------------------

- - We are absolutely committed to maximizing the value of Delcath over the

short- and long-term

- - We have never been more excited about the long-term prospects of Delcath

- - We have a clear and focused strategic plan that we believe will maximize

shareholder returns

- - We believe our experience and knowledge of Delcath will be critical to

properly overseeing the implementation of the Company’s plan

- - We believe Laddcap’s board nominees and strategic plan will destabilize

the Company and introduce substantial undue risk to Delcath and its stock

price

- --------------------------------------------------------------------------------

We Are Accountable to You For Generating

Strong, Sustainable Value

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

6

|  |

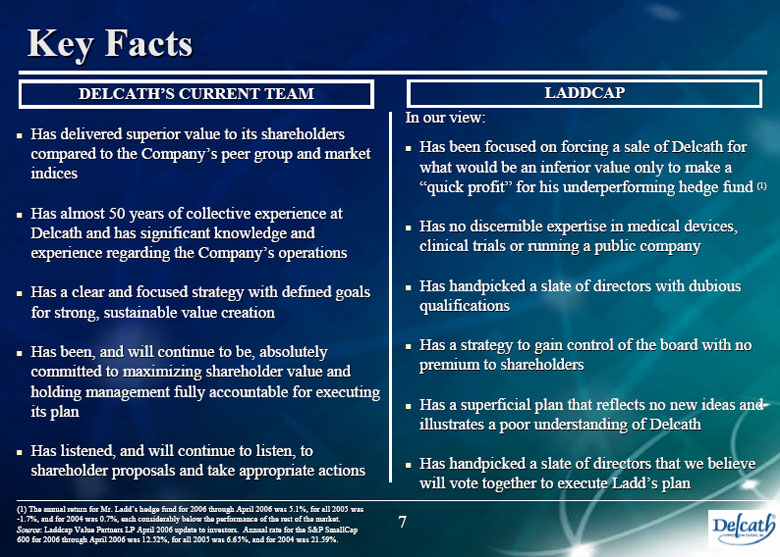

Key Facts

- --------------------------------------------------------------------------------

DELCATH’s CURRENT TEAM

- --------------------------------------------------------------------------------

- - Has delivered superior value to its shareholders compared to the Company’s

peer group and market indices

- - Has almost 50 years of collective experience at Delcath and has

significant knowledge and experience regarding the Company’s operations

- - Has a clear and focused strategy with defined goals for strong,

sustainable value creation

- - Has been, and will continue to be, absolutely committed to maximizing

shareholder value and holding management fully accountable for executing

its plan

- - Has listened, and will continue to listen, to shareholder proposals and

take appropriate actions

- --------------------------------------------------------------------------------

LADDCAP

- --------------------------------------------------------------------------------

In our view:

- - Has been focused on forcing a sale of Delcath for what would be an

inferior value only to make a “quick profit” for his underperforming hedge

fund (1)

- - Has no discernible expertise in medical devices, clinical trials or

running a public company

- - Has handpicked a slate of directors with dubious qualifications

- - Has a strategy to gain control of the board with no premium to

shareholders

- - Has a superficial plan that reflects no new ideas and illustrates a poor

understanding of Delcath

- - Has handpicked a slate of directors that we believe will vote together to

execute Ladd’s plan

- --------------------------------------------------------------------------------

(1) The annual return for Mr. Ladd’s hedge fund for 2006 through April 2006 was

5.1%, for all 2005 was -1.7%, and for 2004 was 0.7%, each considerably below the

performance of the rest of the market.

Source: Laddcap Value Partners LP April 2006 update to investors. Annual rate

for the S&P SmallCap 600 for 2006 through April 2006 was 12.52%, for all

2005 was 6.65%, and for 2004 was 21.59%.

7

|  |

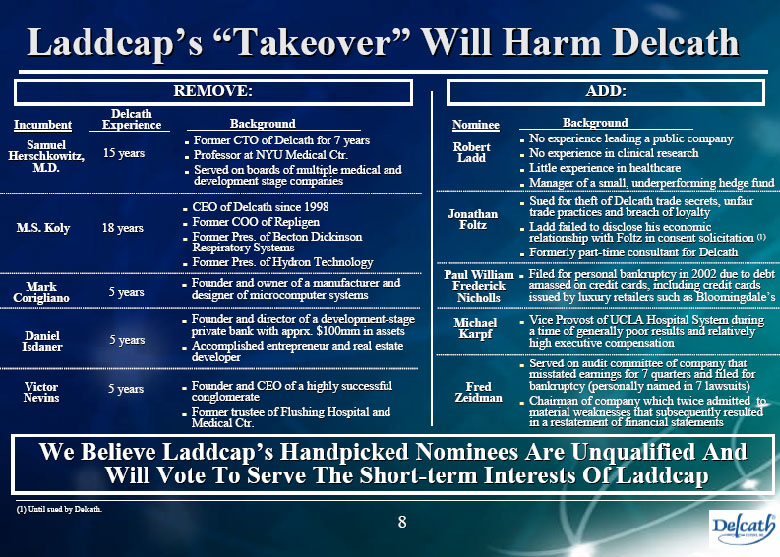

Laddcap’s “Takeover” Will Harm Delcath

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

REMOVE:

- --------------------------------------------------------------------------------

Delcath

Incumbent Experience Background

- --------- ---------- ----------------------------------------------

Samuel - Former CTO of Delcath for 7 years

Herschkowitz, 15 years - Professor at NYU Medical Ctr.

M.D. - Served on boards of multiple medical and

development stage companies

- -----------------------------------------------------------------------------------------

- CEO of Delcath since 1998

M.S. Koly 18 years - Former COO of Repligen

- Former Pres. of Becton Dickinson

Respiratory Systems

- Former Pres. of Hydron Technology

- -----------------------------------------------------------------------------------------

- Founder and owner of a manufacturer and

Mark 5 years designer of microcomputer systems

Corigliano

- -----------------------------------------------------------------------------------------

- Founder and director of a development-stage

Daniel private bank with apprx. $100mm in assets

Isdaner 5 years - Accomplished entrepreneur and real estate

developer

- -----------------------------------------------------------------------------------------

Victor 5 years - Founder and CEO of a highly successful

Nevins conglomerate

- Former trustee of Flushing Hospital and

Medical Ctr.

- --------------------------------------------------------------------------------

ADD:

- --------------------------------------------------------------------------------

Nominee Background

- ------- ------------------------------------------------------

- No experience leading a public company

Robert - No experience in clinical research

Ladd - Little experience in healthcare

- Manager of a small, underperforming hedge fund

- -----------------------------------------------------------------------------

- Sued for theft of Delcath trade secrets, unfair

Jonathan trade practices and breach of loyalty

Foltz - Ladd failed to disclose his economic

relationship with Foltz in consent solicitation (1)

- Formerly part-time consultant for Delcath

- -----------------------------------------------------------------------------

Paul William - Filed for personal bankruptcy in 2002 due to debt

Frederick amassed on credit cards, including credit cards

Nicholls issued by luxury retailers such as Bloomingdale’s

- -----------------------------------------------------------------------------

Michael - Vice Provost of UCLA Hospital System during

Karpf a time of generally poor results and relatively

high executive compensation

- -----------------------------------------------------------------------------

- Served on audit committee of company that

misstated earnings for 7 quarters and filed for

Fred bankruptcy (personally named in 7 lawsuits)

Zeidman - Chairman of company which twice admitted to

material weaknesses that subsequently resulted

in a restatement of financial statements

- --------------------------------------------------------------------------------

We Believe Laddcap’s Handpicked Nominees Are Unqualified And

Will Vote To Serve The Short-term Interests Of Laddcap

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

(1) Until sued by Delcath.

8

|  |

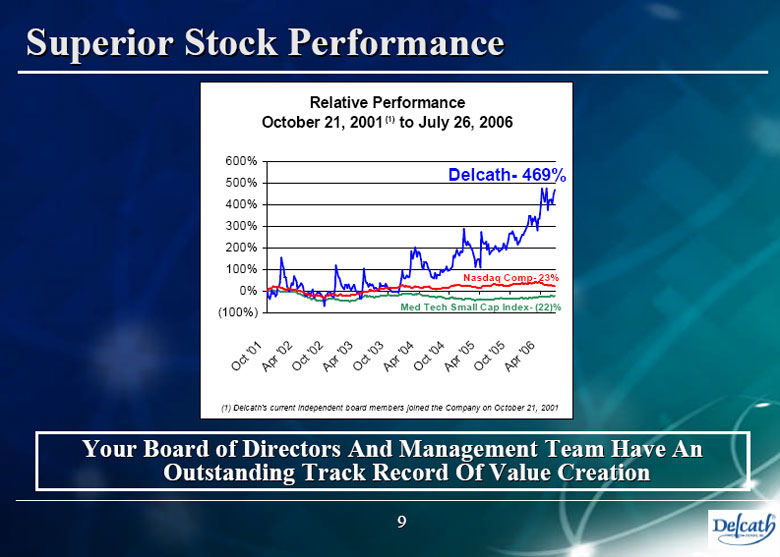

Superior Stock Performance

- --------------------------------------------------------------------------------

Relative Performance

October 21, 2001(1) to July 26, 2006

Med Tech Small Cap Index- (22)% Nasdaq Comp- 23% Delcath- 469%

Oct ’01

Apr ’02

Oct ’02

Apr ’03

Oct ’03

Apr ’04

Oct ’04

Apr ’05

Oct ’05

Apr ’06

(1) Delcath’s current independent board members joined the Company on October

21, 2001

- --------------------------------------------------------------------------------

Your Board of Directors And Management Team Have An

Outstanding Track Record Of Value Creation

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

9

|  |

Laddcap’s Poor Track Record (1)

- --------------------------------------------------------------------------------

Laddcap Value Partners Holdings

Delcath 40%

Other Holdings 60%

Almost 40% of Laddcap’s fund is invested in one stock - Delcath

LaddCap Fund vs. S&P SmallCap 600

Return

25.0% 20.0% 15.0% 10.0% 5.0% 0.0% (5.0%)

2004 2005 1/2006 - 4/2006

Laddcap Value Partners 0.7% (1.7%) 5.1%

S&P SmallCap 600 21.6% 6.7% 12.5%

The annual performance of Laddcap’s fund has been substantially lower than the

market

- --------------------------------------------------------------------------------

Protect Your Investment -

Don’t Let Laddcap Make Its Problems Yours

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

(1) Source: Laddcap Value Partners LP April 2006 update to investors.

10

|  |

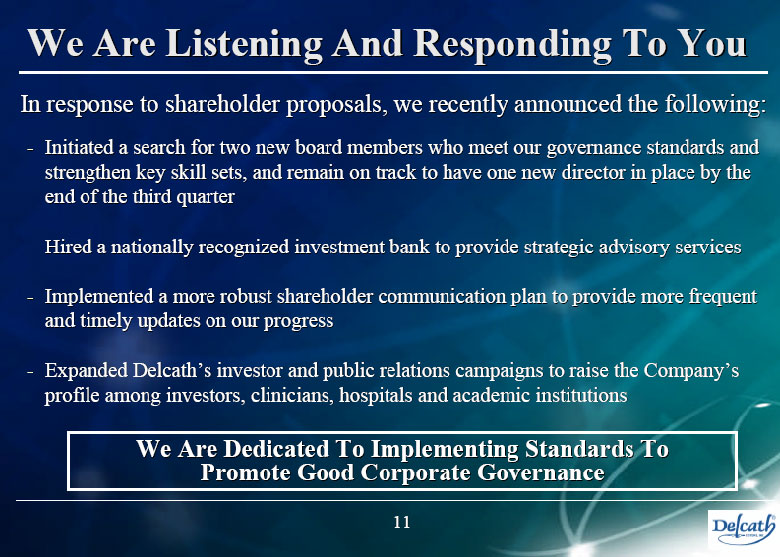

We Are Listening And Responding To You

- --------------------------------------------------------------------------------

In response to shareholder proposals, we recently announced the following:

- - Initiated a search for two new board members who meet our governance

standards and strengthen key skill sets, and remain on track to have one

new director in place by the end of the third quarter

- - Hired a nationally recognized investment bank to provide strategic

advisory services

- - Implemented a more robust shareholder communication plan to provide more

frequent and timely updates on our progress

- - Expanded Delcath’s investor and public relations campaigns to raise the

Company’s profile among investors, clinicians, hospitals and academic

institutions

- --------------------------------------------------------------------------------

We Are Dedicated To Implementing Standards To Promote Good Corporate Governance

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

11

|  |

Delcath Accomplishments

- --------------------------------------------------------------------------------

NCI - Developed a deep, long-standing relationship with the

Collaboration National Cancer Institute (NCI)

- Obtained the NCI’s sponsorship as the lead site for the

Melphalan Phase 3 trial

- Leveraged the NCI’s decade-long work on high dose liver

therapy

- --------------------------------------------------------------------------------

Fast Track - Received fast-track designation in April 2005

Designation - Expected to facilitate development and expedite the review of

the Delcath system

- --------------------------------------------------------------------------------

Special - Established, in conjunction with FDA, a viable Phase 3 trial

Protocol protocol in February 2006

Assessment - Expected to reduce time to approval

- Solved the control arm issue by allowing crossover from

control arm to treatment arm

- --------------------------------------------------------------------------------

Addition of - Announced on August 18 the addition of a new site in the

New Sites Doxorubicin Phase 3 trial

- Made significant progress in recruiting the Univ. of Maryland

for the Melphalan Phase 3 trial

- Discussions with U.S. and ex-U.S. medical centers to

participate in the Doxorubicin Phase 3 trial

- --------------------------------------------------------------------------------

Research & - Successfully recruiting and enrolling patients in Delcath’s

Development three ongoing Phase 2 and 3 trials

Progress - Enrolled 75% of total patients in the Phase 2a trial in

adenocarcinoma and 60% of total patients in the Phase 2a

trial in neuroendocrine cancer

- Ongoing dialogue investigating additional organs and drug

combinations

- --------------------------------------------------------------------------------

12

|  |

The Delcath Strategy

- --------------------------------------------------------------------------------

|  |

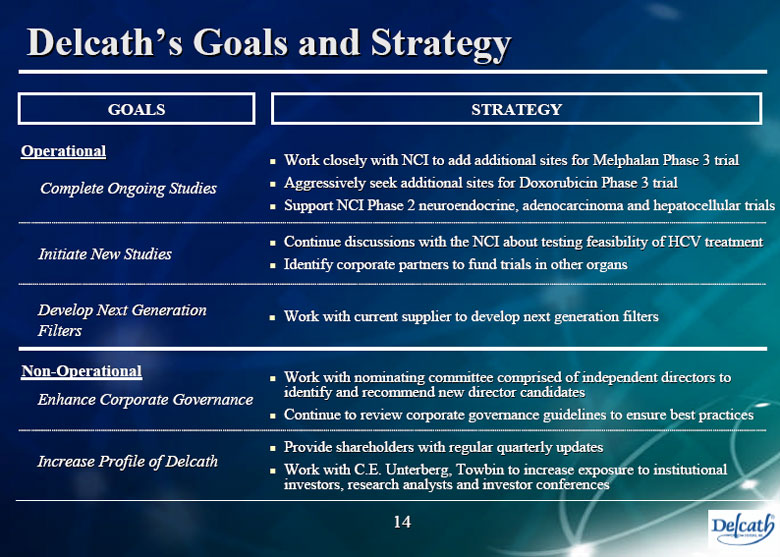

Delcath’s Goals and Strategy

- --------------------------------------------------------------------------------

GOALS STRATEGY

Operational

Complete Ongoing Studies - Work closely with NCI to add additional sites for

Melphalan Phase 3 trial

- Aggressively seek additional sites for Doxorubicin Phase

3 trial

- Support NCI Phase 2 neuroendocrine, adenocarcinoma and

hepatocellular trials

- --------------------------------------------------------------------------------

Initiate New Studies - Continue discussions with the NCI about testing

feasibility of HCV treatment

- Identify corporate partners to fund trials in other organs

- --------------------------------------------------------------------------------

Develop Next Generation Filters - Work with current supplier to develop next generation

filters

- --------------------------------------------------------------------------------

Non-Operational

- --------------------------------------------------------------------------------

Enhance Corporate Governance - Work with nominating committee comprised of independent

directors to identify and recommend new director candidates

- Continue to review corporate governance guidelines to

ensure best practices

- --------------------------------------------------------------------------------

Increase Profile of Delcath - Provide shareholders with regular quarterly updates

- Work with C.E. Unterberg, Towbin to increase exposure to

institutional investors, research analysts and investor

conferences

- --------------------------------------------------------------------------------

14

|  |

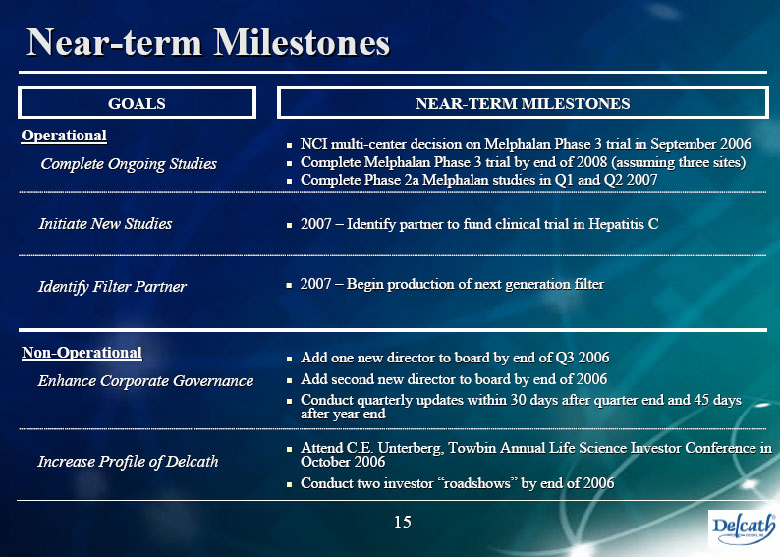

Near-term Milestones

- --------------------------------------------------------------------------------

GOALS NEAR-TERM MILESTONES

Operational

- NCI multi-center decision on Melphalan Phase 3 trial in September 2006

Complete Ongoing Studies - Complete Melphalan Phase 3 trial by end of 2008 (assuming three sites)

- Complete Phase 2a Melphalan studies in Q1 and Q2 2007

- --------------------------------------------------------------------------------

Initiate New Studies - 2007 - Identify partner to fund clinical trial in Hepatitis C

- --------------------------------------------------------------------------------

Identify Filter Partner - 2007 - Begin production of next generation filter

- --------------------------------------------------------------------------------

Non-Operational - Add one new director to board by end of Q3 2006

- --------------------------------------------------------------------------------

Enhance Corporate Governance - Add second new director to board by end of 2006

- Conduct quarterly updates within 30 days after quarter end and 45 days

after year end

- --------------------------------------------------------------------------------

Increase Profile of Delcath - Attend C.E. Unterberg, Towbin Annual Life Science Investor Conference in

October 2006

- Conduct two investor “roadshows” by end of 2006

- --------------------------------------------------------------------------------

15

|  |

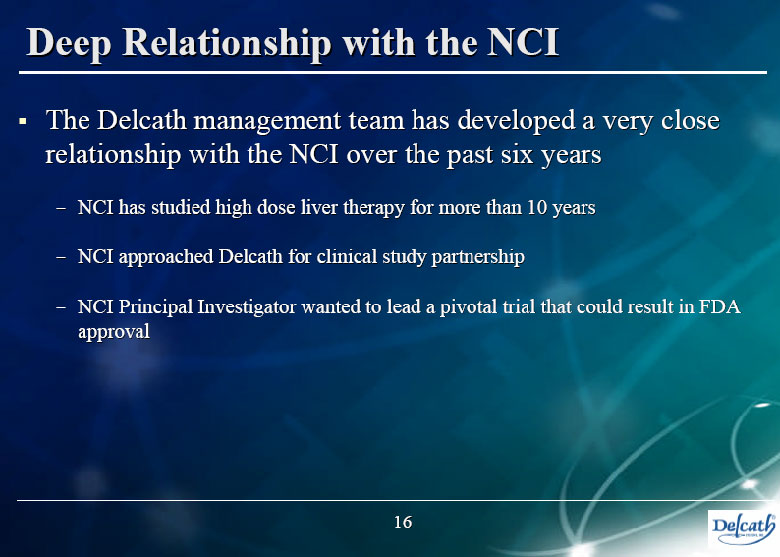

Deep Relationship with the NCI

- --------------------------------------------------------------------------------

- - The Delcath management team has developed a very close relationship with

the NCI over the past six years

- NCI has studied high dose liver therapy for more than 10 years

- NCI approached Delcath for clinical study partnership

- NCI Principal Investigator wanted to lead a pivotal trial that could

result in FDA approval

- --------------------------------------------------------------------------------

16

|  |

17

NCI Reports on Delcath System

H. Richard Alexander, M.D.

Associate Chair for Clinical Research

University of Maryland

Former Head of Surgical

Metabolism Section of the

National Cancer Institute

Text of Sound Clip by Richard Alexander M.D.:

Our interest in isolated perfusion started about eight years ago when there were a number of clinical trials evaluating various forms of regional therapies focused to the liver for individuals who had progressive unresectable cancers confined to that organ and that happens to be a significant clinical problem in this country. A large number of individuals with colorectal cancer for example will ultimately develop this problem and patients with other histologies will also develop the problem. So we looked at refining a technique that had been established long before we started this program of isolated hepatic perfusion in which basically the liver is physically prepared during an operative procedure and then catheters are inserted into the blood vessels going in and out of the liver then the catheters are connected to a heart lung machine and then when the machine is turned on we can deliver through the liver very high doses of anti-cancer agents to try and control the condition in the liver. Now our initial results with that kind of a program were very encouraging and we were able to see fairly significant reduction in the size of tumors often lasting for a considerable period of time in people who had very advanced and previously treated tumors. I think the major downside is that it is a major operative procedure it has certain risks attendant with it and it can only be done one time. Once it’s done, because of the scar tissue that develops around the liver, particularly in the spots where we need to place our catheters it can only be done one time. So we were looking for another mechanism by which we could focus therapy into the liver that might be a little bit more straight forward for any individual to undergo, so the Delcath System is a perfect, in my view, a perfect application to try and determine whether or not we can deliver a high dose melphalan using a less invasive technique than a major operative procedure.

It is possible with the Delcath System that patients could undergo treatments for potentially many months and in particular effects ratio that the tumors are in fact regressing after one or two therapies there’s no reason why they couldn’t undergo two or three or four more additional treatments in order to continually cause the tumors to regress. So I think the Delcath System has the beauty of being repeatable and I think it is a little bit more straightforward for any individual to get through.

There had been in the biomedical research community a long standing interest in identifying a technique, whether it be a physical technique or using gene delivery systems or other kinds of methods to hone a therapy directly to the tumor and I think that right now there have been no one kind of mechanism that has emerged to be so effective and superior that everyone is looking at that as the most promising avenue to pursue. So I look at physical methods of delivering therapies to cancer bearing regions of the body as valid as any of the others that might be considered more sophisticated techniques because they all have, when it ultimately comes down to medical practice, they all have a lot of issues that prevent them from being as effective as you would anticipate based upon theoretical consideration. I think that with the Delcath System, although it seems kind of a basic and more of an elementary method the realities are that it probably has as good of likelihood as any to focus a treatment to an important part of the body to intensify treatment.

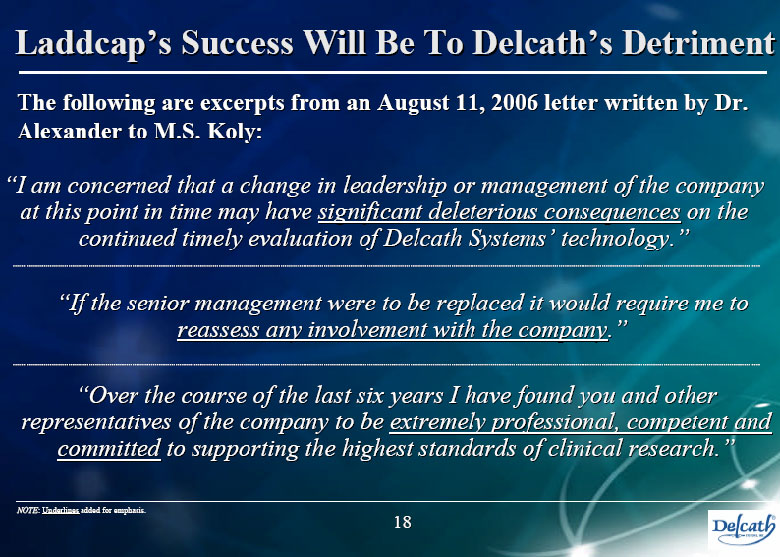

Laddcap’s Success Will Be To Delcath’s Detriment

- --------------------------------------------------------------------------------

The following are excerpts from an August 11, 2006 letter written by Dr.

Alexander to M.S. Koly:

“I am concerned that a change in leadership or management of the company at this

point in time may have significant deleterious consequences on the continued

timely evaluation of Delcath Systems’ technology.”

- --------------------------------------------------------------------------------

“If the senior management were to be replaced it would require me to

reassess any involvement with the company.”

- --------------------------------------------------------------------------------

“Over the course of the last six years I have found you and other

representatives of the company to be extremely professional, competent and

committed to supporting the highest standards of clinical research.”

- --------------------------------------------------------------------------------

NOTE: Underlines added for emphasis.

18

|  |

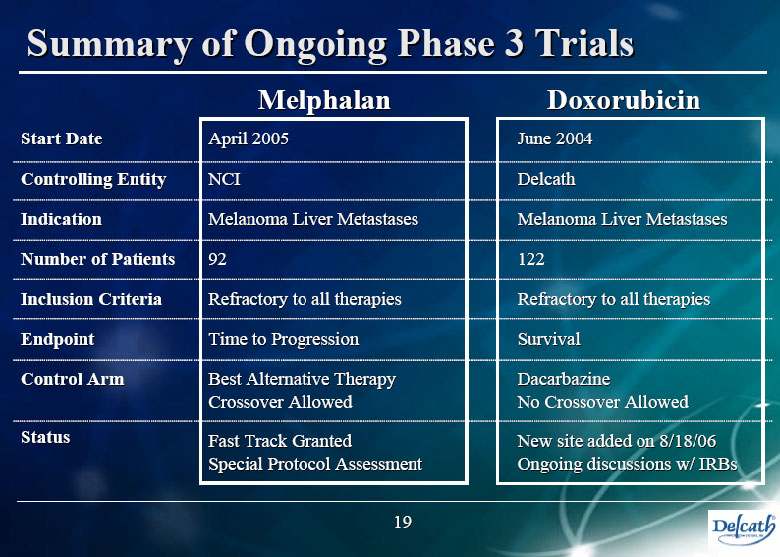

Summary of Ongoing Phase 3 Trials

- --------------------------------------------------------------------------------

Melphalan Doxorubicin

--------------------------- ---------------------------

Start Date April 2005 June 2004

- --------------------------------------------------------------------------------

Controlling Entity NCI Delcath

- --------------------------------------------------------------------------------

Indication Melanoma Liver Metastases Melanoma Liver Metastases

- --------------------------------------------------------------------------------

Number of Patients 92 122

- --------------------------------------------------------------------------------

Inclusion Criteria Refractory to all therapies Refractory to all therapies

- --------------------------------------------------------------------------------

Endpoint Time to Progression Survival

- --------------------------------------------------------------------------------

Control Arm Best Alternative Therapy Dacarbazine

Crossover Allowed No Crossover Allowed

- --------------------------------------------------------------------------------

Status Fast Track Granted New site added on 8/18/06

Special Protocol Assessment Ongoing discussions w/ IRBs

- --------------------------------------------------------------------------------

19

|  |

Strong Development Pipeline

- --------------------------------------------------------------------------------

2006 2007 2008 2009

---------------------------------------------------

3Q 4Q 1H 2H 1H 2H 1H 2H

---------- -------------- ------------- -----------

PHASE 3 MELPHALAN

NCI Multi-Center Decision

Patient Enrollment

File NDA/PMA

PHASE 3 DOXORUBICIN

Discussions w/ New IRBs

Patient Enrollment

OTHER INDICATIONS

Neuroendocrine & Adeno.

Phase 2a

Phase 2b

Phase 3

Hepatocellular.

Phase 2a

Phase 2b

Phase 3

- --------------------------------------------------------------------------------

20

|  |

Conclusions

- --------------------------------------------------------------------------------

|  |

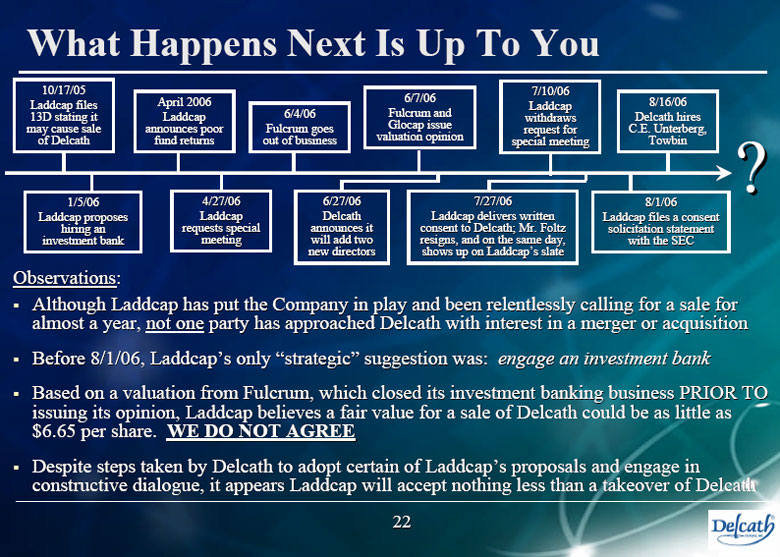

What Happens Next Is Up To You

- -------------------------------------------------------------------------------------------------------------------------------

10/17/05 7/10/06

Laddcap files April 2006 6/7/06 Laddcap 8/16/06

13D stating it Laddcap 6/4/06 Fulcrum and withdraws Delcath hires

may cause sale announces poor Fulcrum goes Glocap issue request for C.E. Unterberg,

of Delcath fund returns out of business valuation opinion special meeting Towbin

- -------------------------------------------------------------------------------------------------------------------------------

1/5/06 4/27/06 6/27/06 7/27/06 8/1/06

Laddcap proposes Laddcap Delcath Laddcap delivers written Laddcap files a consent

hiring an requests special announces it consent to Delcath; Mr. Foltz solicitation statement

investment bank meeting will add two resigns, and on the same day, with the SEC

new directors shows up on Laddcap’s slate

Observations:

- - Although Laddcap has put the Company in play and been relentlessly calling

for a sale for almost a year, not one party has approached Delcath with

interest in a merger or acquisition

- - Before 8/1/06, Laddcap’s only “strategic” suggestion was: engage an

investment bank

- - Based on a valuation from Fulcrum, which closed its investment banking

business PRIOR TO issuing its opinion, Laddcap believes a fair value for a

sale of Delcath could be as little as $6.65 per share. WE DO NOT AGREE

- - Despite steps taken by Delcath to adopt certain of Laddcap’s proposals and

engage in constructive dialogue, it appears Laddcap will accept nothing

less than a takeover of Delcath

- --------------------------------------------------------------------------------

22

|  |

23

23

L

a

dd

’

s

P

l

a

n

S

ho

w

s a

L

a

c

k

o

f

Und

e

rs

t

a

n

d

i

ng

L

ADDCAP

L

ADDCAP

’

’

S

P

R

O

P

O

S

E

D

S

P

R

O

P

O

S

E

D

“

“

S

T

R

A

TE

G

Y

S

T

R

A

TE

G

Y

”

”

(

1

)

T

H

E

R

E

A

LIT

Y

T

H

E

R

E

A

LIT

Y

“

“during the balance of fiscal year 2006, …establish at least two additional sites for Delcath’s ongoing Phase 3 trial using Melphalan”

R

ev

i

e

w

R

ev

i

e

w

“

“

w

h

e

t

h

e

r

co

n

t

i

n

u

i

n

g

t

o

d

ev

o

t

e

r

e

s

ou

r

ce

s

t

o

t

h

e

w

h

e

t

h

e

r

co

n

t

i

n

u

i

n

g

t

o

d

ev

o

t

e

r

e

s

ou

r

ce

s

t

o

t

h

e

D

o

x

o

r

u

b

i

c

i

n

P

h

a

s

e

3

t

r

i

a

l

s

u

n

d

e

r

m

i

n

e

s

t

h

e

D

o

x

o

r

u

b

i

c

i

n

P

h

a

s

e

3

t

r

i

a

l

s

u

n

d

e

r

m

i

n

e

s

t

h

e

M

e

l

p

h

a

l

a

n

M

e

l

p

h

a

l

a

n

P

ha

s

e

3

t

r

i

a

l

t

r

ea

t

i

n

g

t

h

e

s

a

m

e

p

a

t

i

en

t

p

o

p

u

l

a

t

i

o

n

.

P

ha

s

e

3

t

r

i

a

l

t

r

ea

t

i

n

g

t

h

e

s

a

m

e

p

a

t

i

en

t

p

o

p

u

l

a

t

i

o

n

.

”

”

E

s

t

a

b

l

i

s

h

E

s

t

a

b

l

i

s

h

“

“

a

co

l

l

a

b

o

r

a

t

i

o

n

w

i

t

h

a

f

i

l

t

e

r

ex

p

e

r

t

t

o

i

m

p

r

o

v

e

a

co

l

l

a

b

o

r

a

t

i

o

n

w

i

t

h

a

f

i

l

t

e

r

ex

p

e

r

t

t

o

i

m

p

r

o

v

e

a

n

d

c

u

s

t

o

m

i

z

e

t

h

e

f

i

lt

e

r

s

f

o

r

u

s

e

w

i

t

h

i

n

t

h

e

a

n

d

c

u

s

t

o

m

i

z

e

t

h

e

f

i

lt

e

r

s

f

o

r

u

s

e

w

i

t

h

i

n

t

h

e

D

e

l

c

a

t

h

D

e

l

c

a

t

h

s

y

s

t

e

m

,

a

s

w

e

l

l

a

s

f

o

r

f

u

t

u

r

e

fi

lt

e

r

v

a

r

i

a

t

i

on

s

t

o

a

dd

r

e

s

s

s

y

s

t

e

m

,

a

s

w

e

l

l

a

s

f

o

r

f

u

t

u

r

e

fi

lt

e

r

v

a

r

i

a

t

i

on

s

t

o

a

dd

r

e

s

s

a

l

t

e

r

n

a

t

i

v

e

u

s

e

s

o

f

a

l

t

e

r

n

a

t

i

v

e

u

s

e

s

o

f

D

e

l

c

a

t

h

D

e

l

c

a

t

h

’

’

s

s

d

ev

i

ce

.

d

ev

i

ce

.

”

”

C

on

s

i

d

e

r

C

on

s

i

d

e

r

“

“

t

e

s

t

i

n

g

t

h

e

f

e

a

s

i

b

il

it

y

o

f

u

s

i

n

g

it

s

d

e

v

i

c

e

i

n

t

e

s

t

i

n

g

t

h

e

f

e

a

s

i

b

il

it

y

o

f

u

s

i

n

g

it

s

d

e

v

i

c

e

i

n

t

h

e

t

r

e

a

t

m

en

t

o

f

H

e

p

a

t

it

i

s

C

.

t

h

e

t

r

e

a

t

m

en

t

o

f

H

e

p

a

t

it

i

s

C

.

”

”

N

C

I

h

a

s

n

o

c

on

t

r

o

l

ov

e

r

t

h

e

D

ox

o

r

u

b

i

c

i

n

t

r

i

a

l

N

C

I

h

a

s

n

o

c

on

t

r

o

l

ov

e

r

t

h

e

D

ox

o

r

u

b

i

c

i

n

t

r

i

a

l

D

oxo

r

u

b

i

c

i

n

t

r

i

a

l

d

oe

s

no

t

co

n

f

li

c

t

w

i

t

h

D

oxo

r

u

b

i

c

i

n

t

r

i

a

l

d

oe

s

no

t

co

n

f

li

c

t

w

i

t

h

M

e

l

ph

a

l

a

n

M

e

l

ph

a

l

a

n

t

r

i

a

l

t

r

i

a

l

D

oxo

r

u

b

i

c

i

n

Ph

a

s

e

1

a

n

d

2

t

r

i

a

l

s

s

h

o

w

e

d

po

s

i

t

i

v

e

r

e

s

u

lt

s

D

oxo

r

u

b

i

c

i

n

Ph

a

s

e

1

a

n

d

2

t

r

i

a

l

s

s

h

o

w

e

d

po

s

i

t

i

v

e

r

e

s

u

lt

s

D

e

l

ca

t

h

D

e

l

ca

t

h

a

l

r

ea

d

y

h

a

s

b

ee

n

p

u

rs

u

i

n

g

t

h

i

s

a

l

r

ea

d

y

h

a

s

b

ee

n

p

u

rs

u

i

n

g

t

h

i

s

P

r

o

g

r

e

s

s

w

i

l

l

b

e

l

o

s

t

i

f

P

r

o

g

r

e

s

s

w

i

l

l

b

e

l

o

s

t

i

f

L

a

dd

ca

p

L

a

dd

ca

p

s

e

i

ze

s

c

o

n

t

r

o

l

o

f

s

e

i

ze

s

c

o

n

t

r

o

l

o

f

D

e

l

ca

t

h

D

e

l

ca

t

h

D

e

l

ca

t

h

D

e

l

ca

t

h

a

l

r

ea

d

y

h

a

s

b

ee

n

p

u

rs

u

i

n

g

t

h

i

s

a

l

r

ea

d

y

h

a

s

b

ee

n

p

u

rs

u

i

n

g

t

h

i

s

M

.

S

.

M

.

S

.

K

o

l

y

K

o

l

y

h

a

s

h

a

d

d

i

s

cu

ss

i

on

s

w

i

t

h

N

C

I

h

a

s

h

a

d

d

i

s

cu

ss

i

on

s

w

i

t

h

N

C

I

P

r

o

g

r

e

s

s

w

i

l

l

b

e

l

o

s

t

i

f

P

r

o

g

r

e

s

s

w

i

l

l

b

e

l

o

s

t

i

f

L

a

dd

ca

p

L

a

dd

ca

p

s

e

i

ze

s

c

o

n

t

r

o

l

o

f

s

e

i

ze

s

c

o

n

t

r

o

l

o

f

D

e

l

ca

t

h

D

e

l

ca

t

h

N

C

I

h

a

s

no

t

ye

t

a

p

p

r

ov

e

d

a

m

u

lt

i

N

C

I

h

a

s

no

t

ye

t

a

p

p

r

ov

e

d

a

m

u

lt

i

-

-

s

i

t

e

t

r

i

a

l

s

i

t

e

t

r

i

a

l

D

e

l

ca

t

h

D

e

l

ca

t

h

i

s

a

l

r

e

a

d

y

h

a

v

i

n

g

t

a

l

k

s

w

i

t

h

po

t

e

n

t

i

a

l

n

e

w

s

it

e

s

i

s

a

l

r

e

a

d

y

h

a

v

i

n

g

t

a

l

k

s

w

i

t

h

po

t

e

n

t

i

a

l

n

e

w

s

it

e

s

P

r

o

g

r

e

s

s

o

n

n

e

w

s

i

t

e

s

w

il

l

b

e

l

o

s

t

i

f

P

r

o

g

r

e

s

s

o

n

n

e

w

s

i

t

e

s

w

il

l

b

e

l

o

s

t

i

f

L

ad

d

ca

p

L

ad

d

ca

p

s

e

i

ze

s

c

o

n

t

r

o

l

s

e

i

ze

s

c

o

n

t

r

o

l

L

a

dd

c

a

p

L

a

dd

c

a

p

’

’

s

s

N

o

m

i

n

ee

s

D

o

N

o

t

H

av

e A

Su

ff

i

c

i

e

n

t

U

nd

erst

a

nd

i

n

g

O

f

N

o

m

i

n

ee

s

D

o

N

o

t

H

av

e A

Su

ff

i

c

i

e

n

t

U

nd

erst

a

nd

i

n

g

O

f

D

e

lc

a

t

h

D

e

lc

a

t

h

,

,

W

h

i

l

e

Th

e

C

u

rre

n

t

B

o

a

r

d

H

a

s

Al

m

o

s

t

5

0

Y

e

a

r

s

O

f

E

x

p

erience

W

h

i

l

e

Th

e

C

u

rre

n

t

B

o

a

r

d

H

a

s

Al

m

o

s

t

5

0

Y

e

a

r

s

O

f

E

x

p

erience

(

1

)

(

1

)

S

ou

r

c

e

S

ou

r

c

e

:

:

L

a

d

d

c

a

p

L

a

d

d

c

a

p

V

a

l

u

e

P

a

r

t

n

e

r

s

L

P

D

e

f

i

n

i

t

i

v

e

C

o

n

s

e

n

t

S

o

l

i

c

i

t

a

ti

o

n

S

t

a

t

e

m

e

n

t

.

V

a

l

u

e

P

a

r

t

n

e

r

s

L

P

D

e

f

i

n

i

t

i

v

e

C

o

n

s

e

n

t

S

o

l

i

c

i

t

a

ti

o

n

S

t

a

t

e

m

e

n

t

.

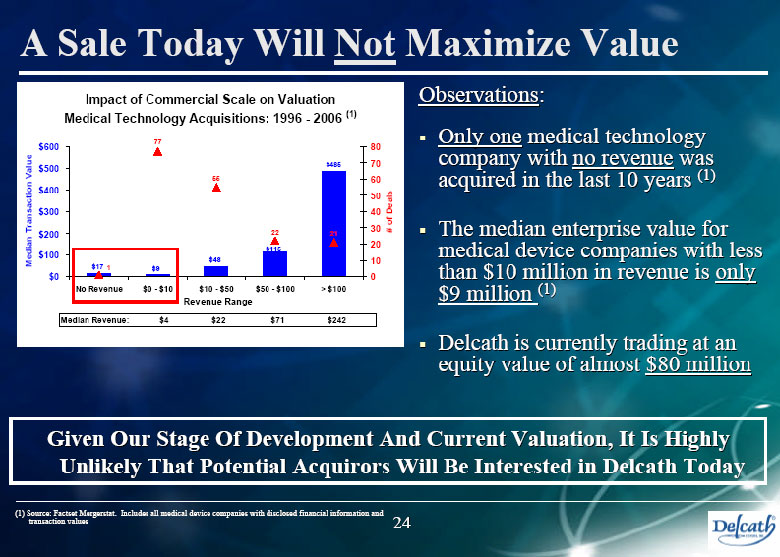

A Sale Today Will Not Maximize Value

- --------------------------------------------------------------------------------

Impact of Commercial Scale on Valuation

Medical Technology Acquisitions: 1996 - 2006 (1)

Median Transaction Value

$600 $500 $400 $300 $200 $100 $0

No Revenue $0 - $10 $10 - $50 $50 - $100 > $100

- ---------------------------------------------------------------

$17 $9 $48 $115 $485

1 77 55 22 21

Revenue Range

Median Revenue: $4 $22 $71 $242

# of Deals

80

70

60

50

40

30

20

10

0

Observations:

o Only one medical technology company with no revenue was acquired in the

last 10 years (1)

o The median enterprise value for medical device companies with less than

$10 million in revenue is only $9 million (1)

o Delcath is currently trading at an equity value of almost $80 million

- --------------------------------------------------------------------------------

Given Our Stage Of Development And Current Valuation, It Is Highly Unlikely That

Potential Acquirors Will Be Interested in Delcath Today

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

(1) Source: Factset Mergerstat. Includes all medical device companies with

disclosed financial information and transaction values

24

|  |

5

2

5

2

n

o

i

t

e

r

c

c

A

e

u

l

a

V

t

n

a

c

i

f

i

n

g

i

S

r

o

f

l

a

i

t

n

e

t

o

P

e

h

T

g

n

i

g

n

i

r

B

o

T

d

e

t

t

i

m

m

o

C

s

I

d

r

a

o

B

r

u

o

Y

e

h

T

g

n

i

g

n

i

r

B

o

T

d

e

t

t

i

m

m

o

C

s

I

d

r

a

o

B

r

u

o

Y

h

t

a

c

l

e

D

h

t

a

c

l

e

D

,

t

e

k

r

a

M

o

T

m

e

t

s

y

S

,

t

e

k

r

a

M

o

T

m

e

t

s

y

S

r

e

v

i

l

e

D

o

T

d

e

t

c

e

p

x

E

s

I

h

c

i

h

W

r

e

v

i

l

e

D

o

T

d

e

t

c

e

p

x

E

s

I

h

c

i

h

W

e

u

l

a

V

t

n

a

c

i

f

i

n

g

i

S

e

u

l

a

V

t

n

a

c

i

f

i

n

g

i

S

s

r

e

d

l

o

h

e

r

a

h

S

o

T

s

r

e

d

l

o

h

e

r

a

h

S

o

T

S

N

,

I

T

M

B

:

e

d

u

l

c

n

i

s

e

i

n

a

p

m

o

C

e

c

i

v

e

D

l

a

c

i

d

e

M

e

g

a

t

S

t

n

e

m

p

o

l

e

v

e

D

)

1

(

S

N

,

I

T

M

B

:

e

d

u

l

c

n

i

s

e

i

n

a

p

m

o

C

e

c

i

v

e

D

l

a

c

i

d

e

M

e

g

a

t

S

t

n

e

m

p

o

l

e

v

e

D

)

1

(

,

P

E

N

,

O

E

H

R

,

O

Y

R

C

,

I

V

C

M

,

R

T

,

P

E

N

,

O

E

H

R

,

O

Y

R

C

,

I

V

C

M

,

R

T

A

L

E

M

,

C

D

R

C

,

T

S

E

R

,

M

C

X

D

A

L

E

M

,

C

D

R

C

,

T

S

E

R

,

M

C

X

D

G

N

A

:

e

d

u

l

c

n

i

s

e

i

n

a

p

m

o

C

e

c

i

v

e

D

l

a

c

i

d

e

M

l

a

i

c

r

e

m

m

o

C

e

g

a

t

S

y

l

r

a

E

)

2

(

G

N

A

:

e

d

u

l

c

n

i

s

e

i

n

a

p

m

o

C

e

c

i

v

e

D

l

a

c

i

d

e

M

l

a

i

c

r

e

m

m

o

C

e

g

a

t

S

y

l

r

a

E

)

2

(

,

L

O

O

K

,

M

T

X

N

,

S

X

T

S

,

M

P

S

A

,

O

,

L

O

O

K

,

M

T

X

N

,

S

X

T

S

,

M

P

S

A

,

O

C

M

M

I

,

X

G

L

E

,

D

N

E

M

C

M

M

I

,

X

G

L

E

,

D

N

E

M

Impact of Commercialization on Valuation

8

.

2

7

$

0

.

6

4

2

$

3

.

3

8

$

0

$

0

5

$

0

0

1

$

0

5

1

$

0

0

2

$

0

5

2

$

0

0

3

$

e

g

a

t

S

t

n

e

m

p

o

l

e

v

e

D

e

c

i

v

e

D

l

a

c

i

d

e

M

s

e

i

n

a

p

m

o

C

l

a

i

c

r

e

m

m

o

C

e

g

a

t

S

y

l

r

a

E

Delcath

e

c

i

v

e

D

l

a

c

i

d

e

M

s

e

i

n

a

p

m

o

C

)

1

(

)

2

(

Do NOT Vote The BLUE Card

- --------------------------------------------------------------------------------

IF YOU ARE...

- --------------------------------------------------------------------------------

FOR

- --------------------------------------------------------------------------------

Continued Execution on Delcath’s Growth Plan - the Delcath Board is committed to

bringing the Company’s revolutionary technology to market and holding management

accountable for its performance

An Experienced and Knowledgeable Board - the Delcath Board has approximately 50

years of combined experience at the Company

Two New Independent Directors - who will be added before the end of 2006 and

will strengthen key skill sets

Sustainable Value Creation - strong price momentum is expected to continue as

Delcath advances its clinical programs

- --------------------------------------------------------------------------------

AGAINST

- --------------------------------------------------------------------------------

Laddcap’s Unqualified Slate of Nominees - who have dubious qualifications and

little-to-no experience with public, development stage, healthcare companies

Laddcap’s Flawed “Strategic” Plan - which demonstrates a lack of understanding

of Delcath’s business, offers no new ideas

Laddcap’s Selfish Agenda and Handpicked Bloc of Nominees - that will only serve

to force a sale of Delcath at an inferior value

Introducing Undue Risk - A change in leadership will completely destabilize

Delcath, delay its clinical progress and undo years of progress made by the

Company

...DISCARD THE BLUE CARD AND VOTE THE GOLD CARD.

- --------------------------------------------------------------------------------

26

|  |

Delcath Systems, Inc.

(NASDAQ: DCTH)

The Future of High-Dose Drug Delivery

1100 Summer Street, 3rd Floor

Stamford, CT 06905

(203) 323-8668

www.delcath.com

|  |