QuickLinks -- Click here to rapidly navigate through this document

MORGAN STANLEY SPECTRUM SERIES

Morgan Stanley Spectrum Select L.P.

Morgan Stanley Spectrum Technical L.P.

Morgan Stanley Spectrum Strategic L.P.

Morgan Stanley Spectrum Global Balanced L.P.

Morgan Stanley Spectrum Currency L.P.

SUPPLEMENT

TO

PROSPECTUS DATED MAY 1, 2006

You should read this supplement together with the prospectus dated May 1, 2006. All page and section references in this supplement relate to the prospectus, except references to pages preceded by "S-", which relate to this supplement.

The date of this Supplement is January 18, 2007.

| | Page | |

|---|---|---|

Summary | S-1 | |

| Risk Factors | S-2 | |

| Fiduciary Responsibility and Liability | S-4 | |

| Description of Charges | S-4 | |

| Use of Proceeds | S-5 | |

| The Spectrum Series | S-6 | |

| Selected Financial Data and Selected Quarterly Financial Data | S-9 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | S-14 | |

| Quantitative and Qualitative Disclosures About Market Risk | S-25 | |

| The General Partner | S-32 | |

| The Trading Advisors | S-33 | |

| Litigation | S-40 | |

| The Limited Partnership Agreements | S-41 | |

| Certain ERISA Considerations | S-41 | |

| Material Federal Income Tax Considerations | S-41 | |

| Experts | S-41 | |

| Potential Advantages | S-42 | |

| Supplemental Performance Information | S-47 | |

| Financial Statements | S-82 | |

| Exhibit A: Form of Amended and Restated Limited Partnership Agreements | S-122 |

(i)

The following updates the information about the escrow agent for the Morgan Stanley Spectrum Series on the cover page and pages 4 and 137.

Due to an October 1, 2006, transaction that united the corporate trust businesses of JPMorgan Chase and The Bank of New York, the escrow agent for the Morgan Stanley Spectrum Series is now The Bank of New York.

The following replaces the second sentence under the sub-caption "—Investment Considerations" on page 3.

You should purchase units in a partnership only if you have considered the risks involved in the investment and only if your financial condition permits you to bear those risks, including the risk of losing all or substantially all of your investment in the partnership.

The following updates the information under the sub-caption "—Fees to be Paid by the Partnerships" on page 7.

Effective November 1, 2006, the monthly management fee payable to each of EMC and Rabar was reduced from 1/4 of 1% (a 3% annual rate) to 5/24 of 1% (a 2.5% annual rate). Also, effective November 1, 2006, the monthly incentive fee payable to each of EMC and Rabar was increased from 15% to 17.5% of the trading profits experienced with respect to the net assets allocated to EMC and Rabar, respectively, as of the end of each calendar month.

The following updates and replaces the break even analysis contained on the cover page, page 8 and in the risk factor "—Each partnership incurs substantial changes" beginning on page 12.

Following is a table that sets forth the fees and expenses that you would incur on an initial investment of $5,000 in each partnership and the amount that your investment must earn, after taking into account estimated interest income, in order to break even after one year and after more than two years. The fees and expenses applicable to each partnership are described under the sub-caption "—Fees to be Paid by the Partnership" on page 7 of the prospectus and above in the supplement to the prospectus.

| | $5,000 Investment | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | Spectrum Select | Spectrum Technical | Spectrum Strategic | Spectrum Global Balanced | Spectrum Currency | ||||||

| | $ | $ | $ | $ | $ | ||||||

| Management Fee(1) | 131.50 | 130.50 | 140.00 | 62.50 | 100.00 | ||||||

| Brokerage Fee | 300.00 | 300.00 | 300.00 | 230.00 | 230.00 | ||||||

| Less: Interest Income(2) | (200.00 | ) | (200.00 | ) | (200.00 | ) | (250.00 | ) | (200.00 | ) | |

| Incentive Fee(3) | — | — | — | — | — | ||||||

| Redemption Charge(4) | 102.04 | 102.04 | 102.04 | 102.04 | 102.04 | ||||||

| Amount of trading profits a partnership must earn for you to recoup your initial investment at the end of one year after paying a redemption charge | 333.54 | 332.54 | 342.04 | 144.54 | 232.04 | ||||||

| Trading profits as percentage of net assets that a partnership must earn for you to recoup your initial investment at the end of one year after paying a redemption charge | 6.67 | % | 6.65 | % | 6.84 | % | 2.89 | % | 4.64 | % | |

| Amount of trading profits a partnership must earn each year for you to recoup your initial investment after two years with no redemption charge | 231.50 | 230.50 | 240.00 | 42.50 | 130.00 | ||||||

| Trading profits as percentage of net assets that a partnership must earn each year for you to recoup your initial investment after two years with no redemption charge | 4.63 | % | 4.61 | % | 4.80 | % | 0.85 | % | 2.60 | % | |

- (1)

- Due to the varying management fees payable to each trading advisor for Spectrum Select, Spectrum Technical and Spectrum Strategic a blended rate of 2.63%, 2.61% and 2.80% was used for Spectrum Select, Spectrum Technical and Spectrum Strategic, respectively, for this calculation.

- (2)

- The partnerships do not directly invest in interest-bearing instruments. Instead, each partnership is paid interest by Morgan Stanley DW at the blended rate Morgan Stanley DW earns on its U.S. Treasury bill investments with all customer segregated funds, as if 80% (100% in the case of Spectrum Global Balanced) of the partnership's average daily net assets for the month were invested at that rate. The rate used in each calculation was estimated based upon current Treasury bill rates of approximately 5.00%. Investors should be aware that the break even analysis will fluctuate as interest rates fluctuate, with the break even percentage declining as interest rates increase or increasing as interest rates decline.

- (3)

- Incentive fees are paid to a trading advisor only on trading profits earned on the assets of the partnership managed by that trading advisor. Trading profits are determined after deducting all partnership expenses attributable to the partnership assets managed by the trading advisor, other than any extraordinary expenses, and do not include interest income. Therefore, incentive fees will be zero at the partnership's break even point on the assets managed by the trading advisor. Note, however, that because one trading advisor to a partnership could be profitable and earn an incentive fee while the other trading advisors are unprofitable such that the partnership has an overall trading loss, it is possible for a partnership to pay an incentive fee at a time when it has incurred overall losses.

- (4)

- Units redeemed at the end of 12 months from the date of purchase are generally subject to a 2% redemption charge; after 24 months there is no redemption charge.

S-1

The following updates and replaces the following risk factors on pages 10-12.

The partnerships' trading is highly leveraged, which accentuates the trading profit or trading loss on a trade. The trading advisors for each partnership use substantial leverage when trading, which could result in immediate and substantial losses. For example, if 10% of the face value of a contract is deposited as margin for that contract, a 10% decrease in the value of the contract would cause a total loss of the margin deposit. A decrease of more than 10% in the value of the contract would cause a loss greater than the amount of the margin deposit.

The leverage employed by the partnerships in their trading can vary substantially from month to month and can be significantly higher or lower than the averages set forth below. As an example of the leverage employed by the partnerships, set forth below, is the average of the underlying value of each partnership's month-end positions for the period November 2005 through October 2006, as compared to the average month-end net assets of the partnership during such period. While the leverage employed on a trade will accentuate the trading profit or loss on that trade, one partnership's overall leverage as compared to another partnership's overall leverage does not necessarily mean that it will be more volatile than the other partnership. This can be seen by a review of the monthly rates of return for the partnerships on pages S-66 to S-80.

| Spectrum Select | 15.0 times net assets | |

| Spectrum Technical | 16.7 times net assets | |

| Spectrum Strategic | 5.8 times net assets | |

| Spectrum Global Balanced | 8.5 times net assets | |

| Spectrum Currency | 4.6 times net assets |

Options trading can be more volatile than futures trading.Each partnership may trade options on futures. Although successful options trading requires many of the same skills as successful futures trading, the risks are different. Successful options trading requires a trader to accurately assess near-term market volatility because that volatility is immediately reflected in the price of outstanding options. Correct assessment of market volatility can therefore be of much greater significance in trading options than it is in many long-term futures strategies where volatility does not have as great an effect on the price of a futures contract.

During the period November 2005 through October 2006, only Spectrum Strategic engaged in any significant options trading. Solely for the purpose of quantifying each partnership's options trading as compared to their overall trading, the general partner has calculated a margin level for each partnership's month-end options positions on a futures equivalent basis. Set forth below for Spectrum Strategic is the average month-end margin level for its options positions as a percent of its total average month-end margin requirements for the period November 2005 through October 2006. You should be aware, however, that in the future the level of each partnership's options trading could vary significantly.

| | % | |

|---|---|---|

| Spectrum Strategic | 4.2 |

S-2

Trading on non-U.S. exchanges presents greater risks to each partnership than trading on U.S. exchanges.

- •

- Each partnership trades on exchanges located outside the U.S. Trading on U.S. exchanges is subject to CFTC regulation and oversight, including, for example, minimum capital requirements for commodity brokers, regulation of trading practices on the exchanges, prohibitions against trading ahead of customer orders, prohibitions against filling orders off exchanges, prescribed risk disclosure statements, testing and licensing of industry sales personnel and other industry professionals, and record keeping requirements. Trading on non-U.S. exchanges is not regulated by the CFTC or any other U.S. governmental agency or instrumentality and may be subject to regulations that are different from those to which U.S. exchange trading is subject, provide less protection to investors than trading on U.S. exchanges and may be less vigorously enforced than regulations in the U.S.

- •

- Positions on non-U.S. exchanges also are subject to the risk of exchange controls, expropriation, excessive taxation or government disruptions.

- •

- A partnership could incur losses when determining the value of its non-U.S. positions in U.S. dollars because of fluctuations in exchange rates.

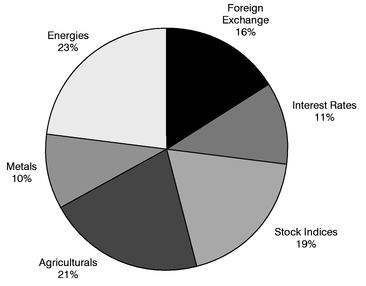

Each partnership must deposit margin with respect to the partnership's futures and options contracts on both U.S. exchanges and on non-U.S. exchanges and must deposit margin with respect to its foreign currency forward contracts to assure the partnership's performance on those contracts. Set forth below for each partnership is the average percentage of month-end estimated margin requirements for the period November 2005 through October 2006, that relate to futures and options contracts on non-U.S. exchanges as compared to the partnership's total average month-end estimated margin requirements. This information will provide you with a sense of the magnitude of each partnership's trading on non-U.S. exchanges, and, therefore, the relevance of the risks described in the prior paragraph to each partnership. You should be aware, however, that the percentage of each partnership's margin requirements that relate to positions on non-U.S. exchanges varies from month to month and can be significantly higher or lower than the percentages set forth below.

| | % | |

|---|---|---|

| Spectrum Select | 38.5 | |

| Spectrum Technical | 36.4 | |

| Spectrum Strategic | 22.5 | |

| Spectrum Global Balanced | 50.3 | |

| Spectrum Currency | 0.0 |

The unregulated nature of the forward markets creates counterparty risks that do not exist in futures trading on exchanges.Unlike futures contracts, forward contracts are entered into between private parties off an exchange and are not regulated by the CFTC or by any other U.S. government agency. Because forward contracts are not traded on an exchange, the performance of those contracts is not guaranteed by an exchange or clearinghouse and the partnership is at risk to the ability of the counterparty to the trade to perform on the forward contract. Because trading in the forward markets is not regulated, there are no specific standards or regulatory supervision of trade pricing and other trading activities that occur in those markets. Because the partnerships trade forward contracts in foreign currency with Morgan Stanley & Co., they are at risk to the creditworthiness and trading practices of Morgan Stanley & Co., as the counterparty to the trades.

As the counterparty to all of the partnerships' foreign currency forward contracts, Morgan Stanley & Co. requires the partnerships to make margin deposits to assure the partnerships' performance on those contracts. Set forth below for each partnership is the average month-end estimated margin requirements for foreign currency forward contracts for the period November 2005 through October 2006, as compared to the partnership's total average month-end estimated margin requirements. Although such contracts are not exchange-traded, and therefore not subject to exchange-set margin requirements, the estimated margin requirements for foreign currency forward contracts used in the percentages below are representative of the margin requirements for similar contracts traded on an exchange. This information will provide you

S-3

with a sense of the magnitude of those partnerships' trading in the forward contracts markets as compared to its trading of futures and options contracts on regulated exchanges, and, therefore, the relevance of the risks described in the prior paragraphs to each partnership. You should be aware that the percentage of each partnership's margin requirements that relate to forward contracts varies from month to month and can be significantly higher or lower than the percentages set forth below.

| | % | |

|---|---|---|

| Spectrum Select | 18.3 | |

| Spectrum Technical | 17.2 | |

| Spectrum Strategic | 19.7 | |

| Spectrum Global Balanced | 1.1 | |

| Spectrum Currency | 100.0 |

FIDUCIARY RESPONSIBILITY AND LIABILITY

The following updates and supplements the first full paragraph on page 20.

It is the position of the SEC and some state securities regulators that indemnification in connection with violations of the securities laws is against public policy and void.

The following updates the information under the sub-caption "—Charges to Each Partnership—Spectrum Select" relating to the fees payable to the trading advisors on page 21.

Effective November 1, 2006, the monthly management fee payable to each of EMC and Rabar was reduced from1/4 of 1% (a 3% annual rate) to5/24 of 1% (a 2.5% annual rate). Also, effective November 1, 2006, the monthly incentive fee payable to each of EMC and Rabar was increased from 15% to 17.5% of the trading profits experienced with respect to the net assets allocated to EMC and Rabar, respectively, as of the end of each calendar month.

S-4

The following updates and replaces the table presented on page 30.

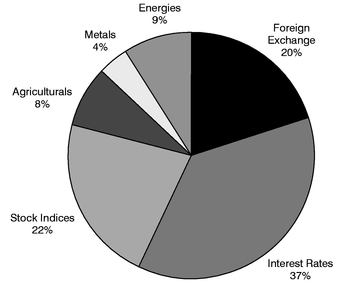

At each monthly closing, the trading advisors for each partnership will be allocated the net proceeds from additional investments received by that partnership, and redemptions from that partnership, in the following proportions:

| Spectrum Select | Additions as of January 31, 2007 | Redemptions as of January 31, 2007 | Percentage of net assets allocated to each trading advisor as of October 31, 2006 | ||||

|---|---|---|---|---|---|---|---|

| | % | % | % | ||||

| EMC Capital Management, Inc. | 10 | 0 | 10.75 | ||||

| Northfield Trading L.P. | 0 | 0 | 6.40 | ||||

| Rabar Market Research, Inc. | 30 | 33 | 1/3 | 34.27 | |||

| Sunrise Capital Management, Inc. | 30 | 33 | 1/3 | 34.40 | |||

| Graham Capital Management, L.P. | |||||||

| Selective Trading Program* | 0 | 0 | 6.10 | ||||

| Global Diversified Program | 30 | 33 | 1/3 | 8.08 | |||

Spectrum Technical | |||||||

| Campbell & Company, Inc. | 0 | 0 | 27.83 | ||||

| Chesapeake Capital Corporation | 30 | 40 | 33.47 | ||||

| John W. Henry & Company, Inc. | 20 | 40 | 18.72 | ||||

| Winton Capital Management Limited | 50 | 20 | 19.98 | ||||

Spectrum Strategic | |||||||

| Blenheim Capital Management, L.L.C. | 40 | 30 | 55.91 | ||||

| Eclipse Capital Management, Inc. | 25 | 40 | 24.36 | ||||

| FX Concepts (Trading Advisor), Inc. | 35 | 30 | 19.73 | ||||

Spectrum Global Balanced | |||||||

| SSARIS Advisors, LLC | 100 | 100 | 100 | ||||

Spectrum Currency | |||||||

| John W. Henry & Company, Inc. | 50 | 50 | 50.09 | ||||

| Sunrise Capital Partners, LLC | 50 | 50 | 49.91 | ||||

- *

- Effective January 31, 2007, Spectrum Select's net assets, with the consent of the general partner, will no longer trade pursuant to Graham's Selective Trading Program. The withdrawal of Spectrum Select's net assets from Graham's Selective Trading Program will be reallocated to Graham's Global Diversified Program.

S-5

The following updates and replaces the table under the sub-caption "—General" on page 31.

Following is a summary of information relating to the sale of units of each partnership through October 31, 2006:

| | Units Sold | Units Available For Sale | Total Proceeds Received | General Partner Contributions | Number of Limited Partners | Net Asset Value Per Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | $ | $ | | $ | ||||||

| Spectrum Select* | 41,444,360.809 | 15,169,606.291 | 921,273,862 | 5,070,000 | 45,722 | 28.25 | ||||||

| Spectrum Technical | 61,131,042.610 | 22,868,957.390 | 1,094,382,601 | 6,311,984 | 54,984 | 21.97 | ||||||

| Spectrum Strategic | 25,487,172.672 | 12,012,827.328 | 321,606,156 | 1,731,000 | 19,390 | 15.91 | ||||||

| Spectrum Global Balanced | 8,408,837.363 | 8,091,162.637 | 119,487,312 | 533,234 | 5,881 | 15.58 | ||||||

| Spectrum Currency | 27,005,699.518 | 24,994,300.482 | 352,388,910 | 4,191,645 | 23,630 | 10.54 |

- *

- The number of units sold has been adjusted to reflect a 100-for-1 unit conversion that took place on June 1, 1998, when Spectrum Select became part of the Spectrum Series of partnerships.

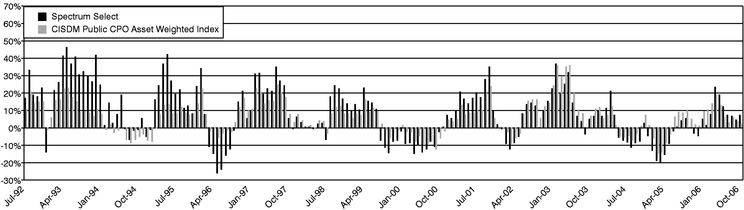

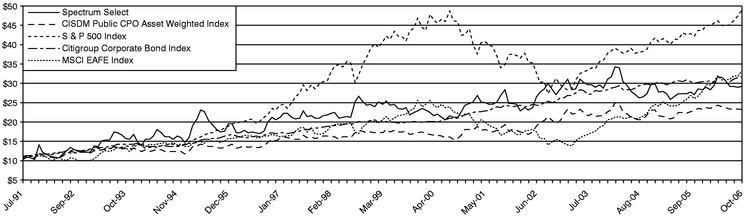

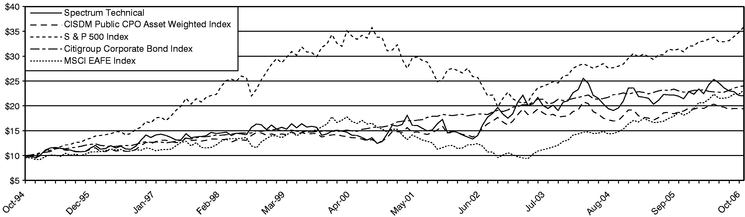

The following updates, through October 31, 2006, and replaces the performance capsules under the sub-caption "—Performance Records" beginning on page 35. You should read the footnotes on page 38, which are an integral part of the following capsules.

Capsule I

Performance of Spectrum Select

Type of pool: publicly-offered fund

Inception of trading: August 1991

Aggregate subscriptions: $926,343,862

Current capitalization: $533,857,388

Current net asset value per unit: $28.25

Worst monthly % drawdown past five years: (13.12)% (November 2001)

Worst monthly % drawdown since inception: (13.72)% (January 1992)

Worst month-end peak-to-valley drawdown past five years: (25.20)% (15 months, February 2004-April 2005)

Worst month-end peak-to-valley drawdown since inception: (26.77)% (15 months, May 1995-August 1996)

Cumulative return since inception: 182.50%

| | Monthly Performance | |||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | 1993 | 1992 | 1991 | ||||||||||||||||

| | % | % | % | % | % | % | % | % | % | % | % | % | % | % | % | % | ||||||||||||||||

| January | 2.59 | (7.31 | ) | 2.14 | 4.70 | (1.25 | ) | 1.36 | 2.86 | (2.90 | ) | 0.87 | 3.93 | (0.38 | ) | (8.13 | ) | (11.67 | ) | 0.31 | (13.72 | ) | ||||||||||

| February | (2.31 | ) | 1.27 | 8.17 | 4.11 | (6.89 | ) | 1.93 | (2.17 | ) | 5.45 | 2.16 | 4.75 | (12.11 | ) | 9.61 | (6.79 | ) | 14.85 | (6.09 | ) | |||||||||||

| March | 3.53 | (2.43 | ) | (0.90 | ) | (8.99 | ) | 3.77 | 7.27 | (2.08 | ) | (2.50 | ) | 0.23 | 0.31 | (0.22 | ) | 20.58 | 12.57 | (0.60 | ) | (3.91 | ) | |||||||||

| April | 8.36 | (5.29 | ) | (10.67 | ) | 1.02 | (3.11 | ) | (6.93 | ) | (3.78 | ) | 3.70 | (6.72 | ) | (5.46 | ) | 4.07 | 9.06 | (0.95 | ) | 10.35 | (1.86 | ) | ||||||||

| May | (0.71 | ) | 2.95 | (3.95 | ) | 8.99 | 3.48 | (0.53 | ) | 1.58 | (4.38 | ) | 1.78 | (1.18 | ) | (3.65 | ) | 11.08 | 6.84 | 1.95 | (1.42 | ) | ||||||||||

| June | (2.94 | ) | 2.83 | (4.71 | ) | (2.91 | ) | 12.00 | (1.78 | ) | (4.44 | ) | 0.34 | 0.93 | 0.16 | 1.37 | (1.70 | ) | 10.30 | 0.21 | 7.19 | |||||||||||

| July | (4.67 | ) | (0.41 | ) | (3.24 | ) | (1.98 | ) | 4.67 | (0.13 | ) | (2.42 | ) | (4.40 | ) | (0.97 | ) | 9.74 | (1.44 | ) | (10.61 | ) | (4.91 | ) | 13.90 | 10.72 | ||||||

| August | (0.11 | ) | 0.27 | (2.97 | ) | 0.31 | 3.42 | 2.53 | 4.71 | (0.44 | ) | 19.19 | (6.22 | ) | (0.46 | ) | (4.81 | ) | (6.95 | ) | (0.95 | ) | 6.69 | (6.20) | ||||||||

| September | (0.60 | ) | 1.55 | 0.12 | (2.77 | ) | 5.18 | 6.70 | (1.84 | ) | 1.69 | 6.24 | 0.93 | 3.34 | (7.76 | ) | 1.25 | (4.13 | ) | (5.24 | ) | 6.32 | ||||||||||

| October | 0.36 | (2.08 | ) | 3.72 | 2.78 | (6.12 | ) | 6.01 | 0.44 | (8.39 | ) | (5.14 | ) | (3.77 | ) | 13.30 | (3.35 | ) | (4.78 | ) | (4.97 | ) | (3.17 | ) | (2.28) | |||||||

| November | 5.01 | 8.39 | (3.02 | ) | (4.56 | ) | (13.12 | ) | 6.47 | 3.29 | (4.16 | ) | 0.62 | 6.76 | 1.37 | 5.68 | (1.30 | ) | 1.39 | (2.93) | ||||||||||||

| December | (0.72 | ) | 0.70 | 8.48 | 5.57 | 0.25 | 8.52 | 1.62 | 1.19 | 3.35 | (3.36 | ) | 11.19 | (2.72 | ) | 8.13 | (3.58 | ) | 38.67 | |||||||||||||

| Compound Annual/ Period Rate of Return | 2.91 | (4.95 | ) | (4.72 | ) | 9.62 | 15.40 | 1.65 | 7.14 | (7.56 | ) | 14.17 | 6.22 | 5.27 | 23.62 | (5.12 | ) | 41.62 | (14.45 | ) | 31.19 | |||||||||||

| (10 months) | (5 months) | |||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

S-6

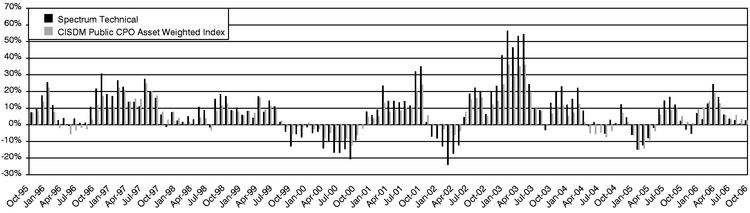

Capsule II

Performance of Spectrum Technical

Type of pool: publicly-offered fund

Inception of trading: November 1994

Aggregate subscriptions: $1,100,694,585

Current capitalization: $710,782,305

Current net asset value per unit: $21.97

Worst monthly % drawdown past five years: (15.59)% (November 2001)

Worst monthly % drawdown since inception: (15.59)% (November 2001)

Worst month-end peak-to-valley drawdown past five years: (26.56)% (13 months, March 2001-April 2002)

Worst month-end peak-to-valley drawdown since inception: (26.56)% (13 months, March 2001-April 2002)

Cumulative return since inception: 119.70%

| | Monthly Performance | ||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | |||||||||||||||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | |||||||||||||||

| | % | % | % | % | % | % | % | % | % | % | % | % | % | ||||||||||||||

| January | 4.52 | (7.49 | ) | 2.74 | 12.76 | (1.88 | ) | (0.81 | ) | 1.21 | (4.96 | ) | (1.16 | ) | 3.67 | 4.78 | (1.84 | ) | |||||||||

| February | (3.94 | ) | (0.55 | ) | 9.85 | 6.60 | (3.41 | ) | 1.94 | (1.19 | ) | 2.48 | 0.41 | 1.13 | (6.39 | ) | 5.10 | ||||||||||

| March | 7.88 | (1.10 | ) | (3.91 | ) | (9.17 | ) | (2.90 | ) | 11.38 | (1.54 | ) | (2.48 | ) | 1.31 | (1.82 | ) | 1.24 | 10.21 | ||||||||

| April | 4.46 | (5.35 | ) | (9.90 | ) | 1.44 | (3.20 | ) | (11.10 | ) | (4.02 | ) | 7.18 | (4.62 | ) | (2.93 | ) | 4.82 | 3.60 | ||||||||

| May | (2.81 | ) | 3.69 | (2.76 | ) | 6.38 | 5.64 | (0.37 | ) | (0.43 | ) | (5.00 | ) | 3.28 | (3.75 | ) | (3.84 | ) | 0.69 | ||||||||

| June | (3.86 | ) | 5.69 | (5.21 | ) | (7.42 | ) | 15.02 | (3.62 | ) | (2.78 | ) | 5.13 | (1.10 | ) | 0.69 | 3.21 | (1.12 | ) | ||||||||

| July | (2.66 | ) | (0.40 | ) | (4.76 | ) | (3.04 | ) | 9.65 | (3.36 | ) | (3.96 | ) | (3.90 | ) | (0.98 | ) | 9.33 | (4.80 | ) | (2.44 | ) | |||||

| August | (0.74 | ) | 0.00 | (1.96 | ) | 3.39 | 4.40 | 1.34 | 3.74 | 0.95 | 10.29 | (5.97 | ) | (0.35 | ) | (0.63 | ) | ||||||||||

| September | (3.28 | ) | (1.13 | ) | 2.94 | (5.41 | ) | 6.43 | 8.19 | (8.61 | ) | (1.51 | ) | 4.35 | 1.85 | 5.50 | (3.33 | ) | |||||||||

| October | (0.54 | ) | (2.41 | ) | 6.89 | 9.14 | (6.75 | ) | 5.37 | 2.90 | (9.96 | ) | (0.73 | ) | 0.36 | 9.92 | (0.09 | ) | |||||||||

| November | 6.77 | 12.51 | 1.20 | (4.68 | ) | (15.59 | ) | 12.28 | 1.84 | (6.17 | ) | 1.01 | 8.34 | 0.93 | (0.90 | ) | |||||||||||

| December | (2.27 | ) | 0.25 | 7.66 | 5.20 | 2.47 | 12.06 | 3.83 | 5.98 | 4.57 | (3.88 | ) | 6.09 | (1.31 | ) | ||||||||||||

| Compound Annual/Period Rate of Return | (1.74 | ) | (5.37 | ) | 4.37 | 22.98 | 23.31 | (7.15 | ) | 7.85 | (7.51 | ) | 10.18 | 7.49 | 18.35 | 17.59 | (2.20 | ) | |||||||||

| (10 months) | (2 months) | ||||||||||||||||||||||||||

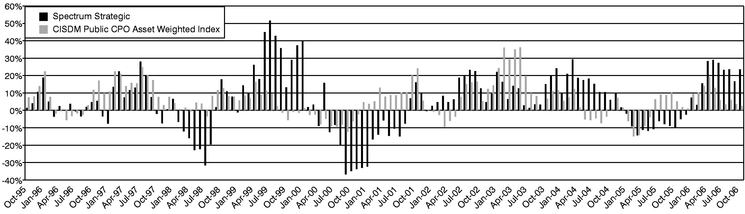

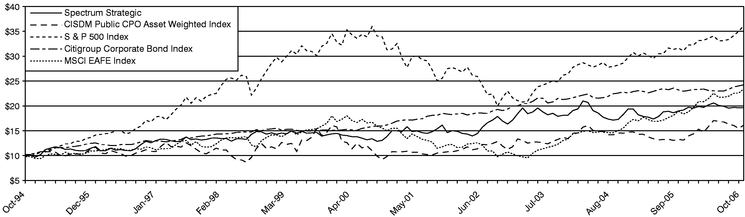

Capsule III

Performance of Spectrum Strategic

Type of pool: publicly-offered fund

Inception of trading: November 1994

Aggregate subscriptions: $323,337,156

Current capitalization: $194,164,887

Current net asset value per unit: $15.91

Worst monthly % drawdown past five years: (7.13)% (October 2002)

Worst monthly % drawdown since inception: (18.47)% (February 2000)

Worst month-end peak-to-valley drawdown past five years: (19.03)% (17 months, March 2004-August 2005)

Worst month-end peak-to-valley drawdown since inception: (43.28)% (10 months, December 1999-October 2000)

Cumulative return since inception: 59.10%

| | Monthly Performance | |||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | ||||||||||||||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | ||||||||||||||

| | % | % | % | % | % | % | % | % | % | % | % | % | % | |||||||||||||

| January | 6.56 | (3.23 | ) | 0.49 | 13.78 | 2.09 | (0.94 | ) | (1.96 | ) | (3.55 | ) | 5.32 | (0.66 | ) | 3.71 | (3.50 | ) | ||||||||

| February | (4.04 | ) | (0.14 | ) | 7.86 | (2.21 | ) | 2.51 | 0.48 | (18.47 | ) | 11.76 | (3.37 | ) | 10.09 | (10.29 | ) | 1.45 | ||||||||

| March | 8.00 | (3.55 | ) | 2.32 | (4.28 | ) | 4.62 | 1.04 | (2.05 | ) | (3.45 | ) | 0.37 | 6.77 | (0.97 | ) | 7.86 | |||||||||

| April | 7.73 | (2.95 | ) | (6.49 | ) | 1.87 | (4.94 | ) | (1.69 | ) | (10.15 | ) | 2.00 | (11.06 | ) | (6.90 | ) | 6.08 | 0.00 | |||||||

| May | (1.13 | ) | (1.75 | ) | (1.01 | ) | 0.00 | 1.37 | (0.10 | ) | 10.13 | (13.38 | ) | (7.40 | ) | 0.78 | (3.05 | ) | (0.66 | ) | ||||||

| June | (0.66 | ) | 0.70 | (0.54 | ) | (1.28 | ) | 8.00 | (3.34 | ) | (7.82 | ) | 21.85 | (0.89 | ) | (1.63 | ) | (2.86 | ) | (6.38 | ) | |||||

| July | (2.66 | ) | 0.46 | (4.38 | ) | (1.86 | ) | (0.42 | ) | (1.38 | ) | 3.71 | (1.00 | ) | (5.26 | ) | 7.65 | (4.91 | ) | (0.81 | ) | |||||

| August | (1.61 | ) | (1.83 | ) | (0.07 | ) | 4.29 | 2.26 | (0.60 | ) | (8.26 | ) | 5.31 | 11.82 | (4.93 | ) | 1.14 | 4.00 | ||||||||

| September | (3.84 | ) | 1.87 | 3.01 | 3.00 | 3.10 | 3.83 | (10.40 | ) | 13.27 | 19.03 | (6.03 | ) | 5.11 | (0.39 | ) | ||||||||||

| October | 4.26 | (1.60 | ) | (0.63 | ) | 3.45 | (7.13 | ) | 1.07 | (6.84 | ) | (9.55 | ) | 8.44 | (6.24 | ) | 2.92 | 0.30 | ||||||||

| November | 6.68 | 1.33 | (2.23 | ) | (5.97 | ) | 1.15 | 6.56 | 4.85 | (7.94 | ) | (2.22 | ) | 3.49 | 2.76 | 0.10 | ||||||||||

| December | 3.20 | 0.55 | 8.57 | 4.72 | 0.09 | 10.75 | 9.39 | 2.76 | 5.62 | (2.65 | ) | 6.24 | 0.00 | |||||||||||||

| Compound Annual/Period Rate of Return | 12.20 | (2.61 | ) | 1.75 | 24.00 | 9.38 | (0.57 | ) | (33.06 | ) | 37.23 | 7.84 | 0.37 | (3.53 | ) | 10.49 | 0.10 | |||||||||

| (10 months) | (2 months) | |||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

S-7

Capsule IV

Performance of Spectrum Global Balanced

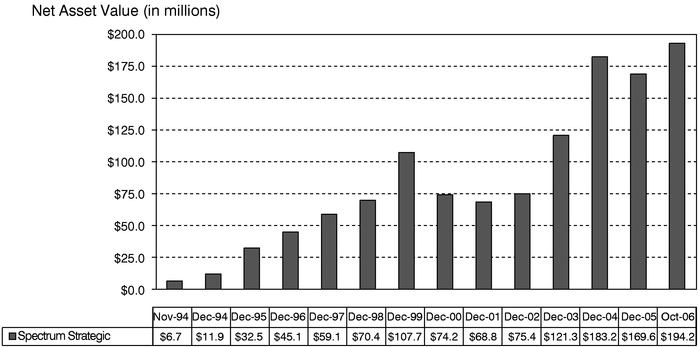

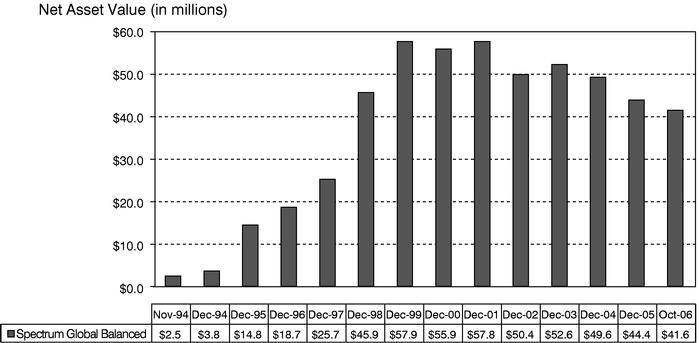

Type of pool: publicly-offered fund

Inception of trading: November 1994

Aggregate subscriptions: $120,020,546

Current capitalization: $41,640,607

Current net asset value per unit: $15.58

Worst monthly % drawdown past five years: (4.16)% (September 2002)

Worst monthly % drawdown since inception: (7.92)% (February 1996)

Worst month-end peak-to-valley drawdown past five years: (15.49)% (52 months, January 2001-April 2005)

Worst month-end peak-to-valley drawdown since inception: (17.43)% (71 months, April 1999-April 2005)

Cumulative return since inception: 55.80%

| | Monthly Performance | ||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | |||||||||||||||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | |||||||||||||||

| | % | % | % | % | % | % | % | % | % | % | % | % | % | ||||||||||||||

| January | 1.05 | (2.33 | ) | (0.90 | ) | 0.34 | (1.23 | ) | 0.55 | (0.93 | ) | (0.06 | ) | 2.25 | 3.35 | 0.41 | 1.32 | ||||||||||

| February | (0.39 | ) | 0.42 | 2.09 | 2.67 | (1.69 | ) | (3.36 | ) | 0.94 | (0.06 | ) | 1.49 | 3.16 | (7.92 | ) | 4.62 | ||||||||||

| March | 2.09 | (1.54 | ) | (1.85 | ) | (2.60 | ) | 0.25 | 2.91 | 3.10 | 0.00 | 2.24 | (2.50 | ) | (1.08 | ) | 2.88 | ||||||||||

| April | 3.71 | (2.62 | ) | (3.58 | ) | 2.19 | (2.09 | ) | (0.31 | ) | (4.57 | ) | 4.13 | (1.78 | ) | (1.65 | ) | 1.27 | 2.15 | ||||||||

| May | (2.46 | ) | 4.00 | (1.08 | ) | 4.89 | (0.19 | ) | 0.25 | (1.32 | ) | (4.99 | ) | (0.35 | ) | 1.68 | (3.13 | ) | 4.38 | ||||||||

| June | (2.21 | ) | 0.91 | (0.07 | ) | (0.19 | ) | 1.30 | (3.08 | ) | (0.26 | ) | 2.28 | 0.00 | 3.64 | 0.46 | 0.79 | ||||||||||

| July | (2.78 | ) | 1.25 | (2.53 | ) | (1.09 | ) | (0.83 | ) | 0.00 | (2.18 | ) | (1.67 | ) | (1.19 | ) | 11.89 | 0.83 | (1.39 | ) | |||||||

| August | 2.66 | 0.34 | 0.28 | 0.00 | 0.97 | 0.51 | 3.01 | (0.19 | ) | 2.55 | (5.92 | ) | (0.82 | ) | (1.41 | ) | |||||||||||

| September | 0.52 | 0.41 | (0.21 | ) | (1.16 | ) | (4.16 | ) | (1.20 | ) | (3.94 | ) | (0.50 | ) | 5.11 | 3.26 | 2.30 | 1.61 | |||||||||

| October | 0.32 | 0.14 | 0.42 | (0.92 | ) | (0.80 | ) | 2.75 | 2.25 | (1.77 | ) | 1.18 | (1.69 | ) | 3.77 | 0.26 | |||||||||||

| November | 3.33 | 1.05 | (1.32 | ) | 2.08 | (0.06 | ) | (0.52 | ) | 1.93 | 2.66 | (0.37 | ) | 4.76 | 2.72 | (0.50 | ) | ||||||||||

| December | 0.07 | 0.83 | 3.48 | (4.02 | ) | 0.93 | 5.79 | 1.96 | 1.27 | 3.07 | (3.88 | ) | 2.99 | (1.21 | ) | ||||||||||||

| Compound Annual/ Period Rate of Return | 2.30 | 4.24 | (5.56 | ) | 6.18 | (10.12 | ) | (0.31 | ) | 0.87 | 0.75 | 16.36 | 18.23 | (3.65 | ) | 22.79 | (1.70 | ) | |||||||||

| (10 months) | (2 months) | ||||||||||||||||||||||||||

Capsule V

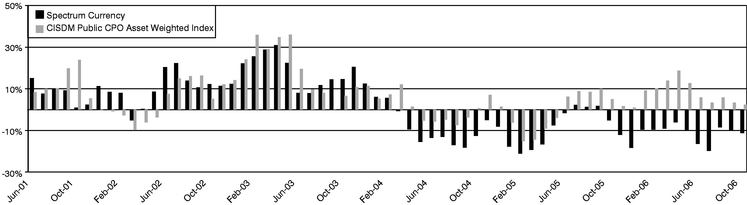

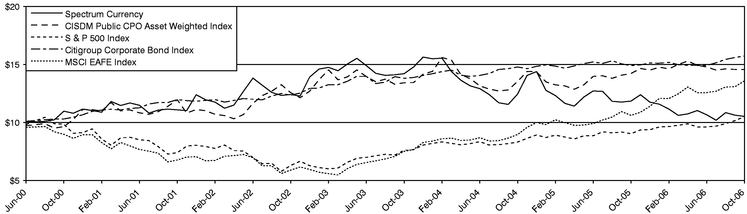

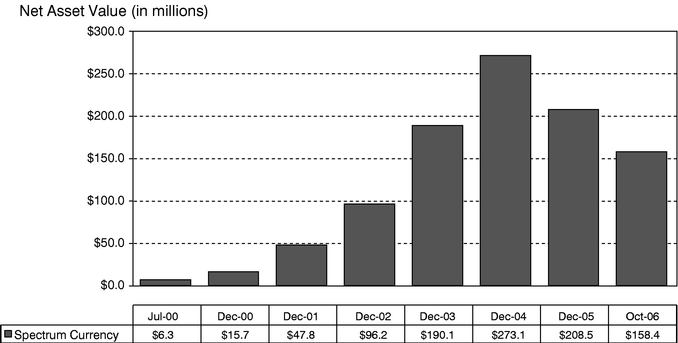

Performance of Spectrum Currency

Type of pool: publicly-offered fund

Inception of trading: July 2000

Aggregate subscriptions: $356,580,555

Current capitalization: $158,400,218

Current net asset value per unit: $10.54

Worst monthly % drawdown past five years: (11.24)% (January 2005)

Worst monthly % drawdown since inception: (11.24)% (January 2005)

Worst month-end peak-to-valley drawdown past five years: (34.80) (31 months, December 2003-July 2006)

Worst month-end peak-to-valley drawdown since inception: (34.80)% (31 months, December 2003-July 2006)

Cumulative return since inception: 5.40%

| | Monthly Performance | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | |||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | |||||||||

| | % | % | % | % | % | % | % | ||||||||

| January | (1.61 | ) | (11.24 | ) | (0.89 | ) | 5.03 | (3.46 | ) | (1.07 | ) | ||||

| February | (3.54 | ) | (3.60 | ) | 0.39 | 0.96 | (1.75 | ) | (1.36 | ) | |||||

| March | (5.01 | ) | (5.43 | ) | (7.51 | ) | (1.96 | ) | (4.50 | ) | 8.44 | ||||

| April | 1.22 | (2.06 | ) | (5.14 | ) | 4.07 | 2.40 | (2.88 | ) | ||||||

| May | 2.70 | 6.92 | (3.58 | ) | 3.19 | 10.34 | 1.92 | ||||||||

| June | (3.26 | ) | 4.34 | (1.90 | ) | (3.99 | ) | 8.98 | (1.71 | ) | |||||

| July | (4.40 | ) | (0.31 | ) | (3.87 | ) | (4.49 | ) | (4.41 | ) | (5.91 | ) | 0.60 | ||

| August | 6.46 | (6.69 | ) | (5.79 | ) | (1.26 | ) | (4.69 | ) | 2.40 | 0.40 | ||||

| September | (2.12 | ) | (0.59 | ) | (1.11 | ) | 0.43 | (1.98 | ) | 0.90 | 1.39 | ||||

| October | (0.94 | ) | 0.68 | 7.69 | 0.64 | 0.57 | (0.81 | ) | 7.32 | ||||||

| November | 4.64 | 12.99 | 4.08 | (1.05 | ) | (0.36 | ) | (1.64 | ) | ||||||

| December | (5.08 | ) | 2.27 | 5.74 | 13.25 | 12.31 | 3.33 | ||||||||

Compound Annual/ Period Rate of Return | (10.53 | ) | (18.25 | ) | (7.98 | ) | 12.42 | 12.25 | 11.10 | 11.70 | |||||

| (10 months) | (6 months) | ||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

S-8

SELECTED FINANCIAL DATA

AND SELECTED QUARTERLY FINANCIAL DATA

The following updates and replaces the information contained on pages 39-43.

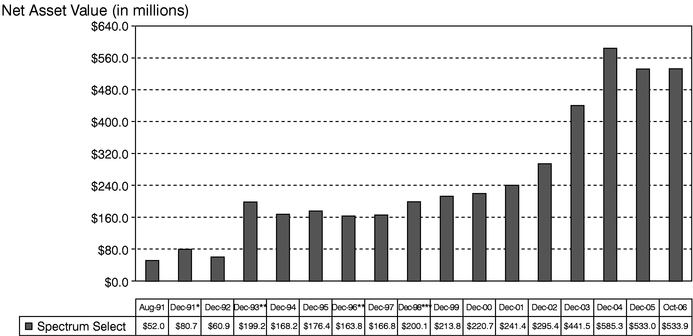

Spectrum Select

Selected Financial Data

| | For the Nine Months Ended September 30, | For the Years Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2006 | 2005 | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||

| | $ | $ | $ | $ | $ | $ | $ | |||||||

| | (Unaudited) | (Unaudited) | | | | | | |||||||

Total Trading Results including interest | 50,536,443 | 61,306 | 23,039,815 | 33,923,907 | 74,213,042 | 67,605,728 | 30,468,895 | |||||||

Net Income (Loss) | 13,961,811 | (40,197,293 | ) | (29,214,513 | ) | (23,311,900 | ) | 34,186,905 | 40,823,199 | 3,165,349 | ||||

Net Income (Loss) Per Unit (Limited & General Partners) | 0.70 | (1.99 | ) | (1.43 | ) | (1.43 | ) | 2.66 | 3.69 | 0.39 | ||||

Total Assets | 546,681,053 | 567,632,365 | 550,467,763 | 595,823,205 | 449,549,242 | 299,604,379 | 246,043,382 | |||||||

Total Limited Partners' Capital | 528,636,162 | 545,947,373 | 527,198,790 | 579,155,164 | 436,666,633 | 292,226,000 | 238,821,840 | |||||||

Net Asset Value Per Unit | 28.15 | 26.89 | 27.45 | 28.88 | 30.31 | 27.65 | 23.96 | |||||||

Selected Quarterly Financial Data (Unaudited)

Quarter ended | Total Trading Results including interest | Net income (loss) | Net income (loss) per unit of limited partnership interest | ||||

|---|---|---|---|---|---|---|---|

| | $ | $ | $ | ||||

2006 | |||||||

| March 31 | 31,802,353 | 19,972,754 | 1.03 | ||||

| June 30 | 36,753,206 | 24,144,618 | 1.26 | ||||

| September 30 | (18,019,116 | ) | (30,155,561 | ) | (1.59 | ) | |

| Total | 50,536,443 | 13,961,811 | 0.70 | ||||

2005 | |||||||

| March 31 | (35,305,346 | ) | (49,599,774 | ) | (2.43 | ) | |

| June 30 | 15,493,277 | 1,766,194 | 0.07 | ||||

| September 30 | 19,873,375 | 7,636,287 | 0.37 | ||||

| December 31 | 22,978,509 | 10,982,780 | 0.56 | ||||

| Total | 23,039,815 | (29,214,513 | ) | (1.43 | ) | ||

2004 | |||||||

| March 31 | 61,318,726 | 43,063,158 | 2.88 | ||||

| June 30 | (89,312,298 | ) | (102,519,477 | ) | (6.05 | ) | |

| September 30 | (17,696,888 | ) | (30,110,417 | ) | (1.63 | ) | |

| December 31 | 79,614,367 | 66,254,836 | 3.37 | ||||

| Total | 33,923,907 | (23,311,900 | ) | (1.43 | ) | ||

S-9

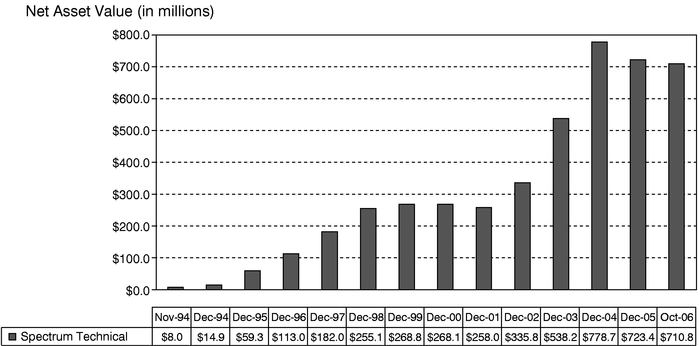

Spectrum Technical

Selected Financial Data

| | For the Nine Months Ended September 30, | For the Years Ended December 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2006 | 2005 | 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||

| | $ | $ | $ | $ | $ | $ | $ | ||||||||

| | (Unaudited) | (Unaudited) | | | | | | ||||||||

Total Trading Results including interest | 46,301,226 | 1,507,043 | 30,949,285 | 110,010,090 | 142,093,478 | 92,648,909 | 9,867,449 | ||||||||

Net Income (Loss) | (9,380,940 | ) | (53,971,562 | ) | (40,418,141 | ) | 36,141,651 | 87,941,888 | 60,775,435 | (19,283,369 | ) | ||||

Net Income (Loss) Per Unit (Limited & General Partners) | (0.27 | ) | (1.67 | ) | (1.27 | ) | 0.99 | 4.23 | 3.48 | (1.15 | ) | ||||

Total Assets | 731,664,884 | 768,525,121 | 751,683,687 | 791,452,599 | 550,066,920 | 341,596,812 | 262,442,204 | ||||||||

Total Limited Partners' Capital | 709,221,657 | 738,950,421 | 715,669,731 | 770,511,257 | 532,266,109 | 332,124,550 | 255,122,417 | ||||||||

Net Asset Value Per Unit | 22.09 | 21.96 | 22.36 | 23.63 | 22.64 | 18.41 | 14.93 | ||||||||

Selected Quarterly Financial Data (Unaudited)

| Quarter ended | Total Trading Results including interest | Net income (loss) | Net income (loss) per unit of limited partnership interest | ||||

|---|---|---|---|---|---|---|---|

| | $ | $ | $ | ||||

2006 | |||||||

| March 31 | 78,543,020 | 59,352,374 | 1.86 | ||||

| June 30 | 2,012,092 | (18,349,825 | ) | (0.58 | ) | ||

| September 30 | (34,253,886 | ) | (50,383,489 | ) | (1.55 | ) | |

| Total | 46,301,226 | (9,380,940 | ) | (0.27 | ) | ||

2005 | |||||||

| March 31 | (51,293,719 | ) | (70,324,779 | ) | (2.13 | ) | |

| June 30 | 47,155,337 | 28,358,931 | 0.80 | ||||

| September 30 | 5,645,425 | (12,005,714 | ) | (0.34 | ) | ||

| December 31 | 29,442,242 | 13,553,421 | 0.40 | ||||

| Total | 30,949,285 | (40,418,141 | ) | (1.27 | ) | ||

2004 | |||||||

| March 31 | 72,341,653 | 45,902,418 | 1.91 | ||||

| June 30 | (99,601,270 | ) | (115,245,895 | ) | (4.16 | ) | |

| September 30 | (8,501,516 | ) | (23,227,074 | ) | (0.79 | ) | |

| December 31 | 145,771,223 | 128,712,202 | 4.03 | ||||

| Total | 110,010,090 | 36,141,651 | 0.99 | ||||

S-10

Spectrum Strategic

Selected Financial Data

| | For the Nine Months Ended September 30, | For the Years Ended December 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2006 | 2005 | 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||

| | $ | $ | $ | $ | $ | $ | $ | ||||||||

| | (Unaudited) | (Unaudited) | | | | | | ||||||||

Total Trading Results including interest | 30,084,871 | (6,082,972 | ) | 12,799,043 | 17,867,892 | 31,984,167 | 14,078,687 | 6,855,809 | |||||||

Net Income (Loss) | 12,646,156 | (18,974,673 | ) | (5,545,967 | ) | 1,248,814 | 20,513,412 | 6,314,416 | (480,543 | ) | |||||

Net Income (Loss) Per Unit (Limited & General Partners) | 1.08 | (1.47 | ) | (0.38 | ) | 0.25 | 2.77 | 0.99 | (0.06 | ) | |||||

Total Assets | 190,202,096 | 170,218,829 | 177,063,684 | 186,645,900 | 123,656,595 | 77,094,809 | 71,489,275 | ||||||||

Total Limited Partners' Capital | 184,252,374 | 163,659,266 | 167,774,452 | 181,218,795 | 119,976,992 | 74,487,934 | 68,012,216 | ||||||||

Net Asset Value Per Unit | 15.26 | 13.09 | 14.18 | 14.56 | 14.31 | 11.54 | 10.55 | ||||||||

Selected Quarterly Financial Data (Unaudited)

| Quarter ended | Total Trading Results including interest | Net income (loss) | Net income (loss) per unit of limited partnership interest | ||||

|---|---|---|---|---|---|---|---|

| | $ | $ | $ | ||||

2006 | |||||||

| March 31 | 24,410,672 | 17,585,840 | 1.48 | ||||

| June 30 | 17,117,577 | 10,768,053 | 0.91 | ||||

| September 30 | (11,443,378 | ) | (15,707,737 | ) | (1.31 | ) | |

| Total | 30,084,871 | 12,646,156 | 1.08 | ||||

2005 | |||||||

| March 31 | (7,718,402 | ) | (12,643,570 | ) | (0.99 | ) | |

| June 30 | (2,689,402 | ) | (6,996,443 | ) | (0.54 | ) | |

| September 30 | 4,324,832 | 665,340 | 0.06 | ||||

| December 31 | 18,882,015 | 13,428,706 | 1.09 | ||||

| Total | 12,799,043 | (5,545,967 | ) | (0.38 | ) | ||

2004 | |||||||

| March 31 | 19,386,598 | 14,056,323 | 1.56 | ||||

| June 30 | (9,056,217 | ) | (12,686,034 | ) | (1.26 | ) | |

| September 30 | 773,705 | (2,350,517 | ) | (0.23 | ) | ||

| December 31 | 6,763,806 | 2,229,042 | 0.18 | ||||

| Total | 17,867,892 | 1,248,814 | 0.25 | ||||

S-11

Spectrum Global Balanced

Selected Financial Data

| | For the Nine Months Ended September 30, | For the Years Ended December 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2006 | 2005 | 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||

| | $ | $ | $ | $ | $ | $ | $ | ||||||||

| | (Unaudited) | (Unaudited) | | | | | | ||||||||

Total Trading Results including interest | 2,820,587 | 2,272,658 | 4,496,558 | (51,621 | ) | 6,038,905 | (2,566,396 | ) | 3,150,268 | ||||||

Net Income (Loss) | 903,727 | 222,831 | 1,792,690 | (3,017,628 | ) | 3,077,508 | (5,786,918 | ) | (152,599 | ) | |||||

Net Income (Loss) Per Unit (Limited & General Partners) | 0.30 | 0.10 | 0.62 | (0.86 | ) | 0.90 | (1.64 | ) | (0.05 | ) | |||||

Total Assets | 43,308,346 | 46,275,666 | 45,422,180 | 50,433,972 | 53,920,384 | 51,559,238 | 58,790,758 | ||||||||

Total Limited Partners' Capital | 41,816,164 | 44,616,133 | 43,870,162 | 49,068,822 | 52,064,431 | 49,814,229 | 57,127,967 | ||||||||

Net Asset Value Per Unit | 15.53 | 14.71 | 15.23 | 14.61 | 15.47 | 14.57 | 16.21 | ||||||||

Selected Quarterly Financial Data (Unaudited)

Quarter ended | Total Trading Results including interest | Net income (loss) | Net income (loss) per unit of limited partnership interest | ||||

|---|---|---|---|---|---|---|---|

| | $ | $ | $ | ||||

2006 | |||||||

| March 31 | 1,856,523 | 1,209,477 | 0.42 | ||||

| June 30 | 204,424 | (446,087 | ) | (0.17 | ) | ||

| September 30 | 759,640 | 140,337 | 0.05 | ||||

| Total | 2,820,587 | 903,727 | 0.30 | ||||

2005 | |||||||

| March 31 | (962,202 | ) | (1,674,009 | ) | (0.50 | ) | |

| June 30 | 1,666,960 | 996,591 | 0.31 | ||||

| September 30 | 1,567,900 | 900,249 | 0.29 | ||||

| December 31 | 2,223,900 | 1,569,859 | 0.52 | ||||

| Total | 4,496,558 | 1,792,690 | 0.62 | ||||

2004 | |||||||

| March 31 | 387,222 | (388,480 | ) | (0.11 | ) | ||

| June 30 | (1,720,563 | ) | (2,481,729 | ) | (0.72 | ) | |

| September 30 | (531,920 | ) | (1,250,231 | ) | (0.36 | ) | |

| December 31 | 1,813,640 | 1,102,812 | 0.33 | ||||

| Total | (51,621 | ) | (3,017,628 | ) | (0.86 | ) | |

S-12

Spectrum Currency

Selected Financial Data

| | For the Nine Months Ended September 30, | For the Years Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2006 | 2005 | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||

| | $ | $ | $ | $ | $ | $ | $ | |||||||

| | (Unaudited) | (Unaudited) | | | | | | |||||||

Total Trading Results including interest | (10,490,138 | ) | (37,938,406 | ) | (34,033,766 | ) | 2,632,707 | 28,185,655 | 16,183,891 | 7,353,454 | ||||

Net Income (Loss) | (19,515,723 | ) | (49,926,426 | ) | (49,703,859 | ) | (11,908,707 | ) | 16,796,809 | 10,283,120 | 4,336,339 | |||

Net Income (Loss) Per Unit (Limited & General Partners) | (1.14 | ) | (2.63 | ) | (2.63 | ) | (1.25 | ) | 1.73 | 1.52 | 1.24 | |||

Total Assets | 168,788,253 | 229,982,176 | 216,070,006 | 277,046,143 | 192,464,641 | 98,379,320 | 49,112,223 | |||||||

Total Limited Partners' Capital | 161,903,717 | 221,144,309 | 206,199,270 | 270,231,305 | 188,042,673 | 93,891,619 | 45,598,611 | |||||||

Net Asset Value Per Unit | 10.64 | 11.78 | 11.78 | 14.41 | 15.66 | 13.93 | 12.41 | |||||||

Selected Quarterly Financial Data (Unaudited)

Quarter ended | Total Trading Results including interest | Net income (loss) | Net income (loss) per unit of limited partnership interest | ||||

|---|---|---|---|---|---|---|---|

| | $ | $ | $ | ||||

2006 | |||||||

| March 31 | (16,774,307 | ) | (20,086,896 | ) | (1.16 | ) | |

| June 30 | 4,149,434 | 1,215,123 | 0.06 | ||||

| September 30 | 2,134,735 | (643,950 | ) | (0.04 | ) | ||

| Total | (10,490,138 | ) | (19,515,723 | ) | (1.14 | ) | |

2005 | |||||||

| March 31 | (48,508,520 | ) | (52,693,364 | ) | (2.75 | ) | |

| June 30 | 25,201,383 | 21,375,686 | 1.08 | ||||

| September 30 | (14,631,269 | ) | (18,608,748 | ) | (0.96 | ) | |

| December 31 | 3,904,640 | 222,567 | — | ||||

| Total | (34,033,766 | ) | (49,703,859 | ) | (2.63 | ) | |

2004 | |||||||

| March 31 | (13,624,011 | ) | (17,153,573 | ) | (1.25 | ) | |

| June 30 | (19,529,341 | ) | (23,130,916 | ) | (1.48 | ) | |

| September 30 | (19,847,451 | ) | (23,397,173 | ) | (1.35 | ) | |

| December 31 | 55,633,510 | 51,772,955 | 2.83 | ||||

| Total | 2,632,707 | (11,908,707 | ) | (1.25 | ) | ||

S-13

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

The following updates, for the nine months ended September 30, 2006 and 2005, and supplements the information for each partnership under the sub-captions "Results of Operations" on pages 44-64.

Morgan Stanley Spectrum Select L.P.

For the Nine Months Ended September 30, 2006.

The most significant trading gains of approximately 6.5% were recorded in the metals markets primarily during the first six months of the year from long futures positions in copper, nickel, zinc, and aluminum as base metals prices rallied on strong global demand and reports of falling inventories. As a result, copper and nickel prices hit new-record highs during the month of May. Further gains in the metals markets were experienced from long positions in gold and silver futures as prices reached 25-year highs in May, benefiting from strong demand and lagging supply. Demand for precious metals increased on continued geopolitical concerns and inflation fears due to high energy prices. Additional gains of approximately 4.8% were experienced within the global interest rates sector, during March and April, from short positions in U.S., European, and Australian interest rate futures as global bond prices trended lower throughout a majority of the first quarter amid strength in regional equity markets and investor sentiment that interest rates in the United States, the European Union, and Australia would rise. U.S. fixed-income futures continued to move lower into the second quarter following the release of consistently strong U.S. economic data. Similarly in Germany, rising equity prices, strong economic growth, and concerns about rising oil prices pressured German fixed-income futures prices even lower in the second quarter. Smaller gains of approximately 1.0% were recorded within the global stock index markets from long positions in European and Australian stock index futures as global equity prices trended higher throughout the first quarter on strong corporate earnings and solid economic data. Long positions in Hong Kong equity index futures also recorded gains as prices moved higher during April on positive performance in the technology sector and amid speculation that the U.S. Federal Reserve could be near the end of its interest rate tightening campaign. During July, long positions in Hong Kong stock index futures experienced gains as prices moved higher on news that Gross Domestic Product in China surged to 10.9% in the first six months of this year. Gains were also experienced during September from long positions in European equity index futures as prices were supported higher on merger and acquisition activity and solid corporate earnings. A portion of the partnership's overall gains for the first nine months of the year was offset by losses of approximately 2.7% in the currency markets primarily during the first six months of the year from short positions in the Swiss franc and Japanese yen versus the U.S. dollar. Throughout a majority of the first half of the year, the U.S. dollar moved lower on news that foreign central banks were beginning to diversify their currency reserves away from U.S. dollar-denominated assets, as well as uncertainty regarding the future of the U.S. Federal Reserve's interest rate tightening campaign. The Swiss franc and Japanese yen moved higher against the U.S. dollar during January and February as strong economic data out of Switzerland and Japan increased speculation that the Swiss National Bank and Bank of Japan might raise interest rates. During April, the Swiss franc moved higher on the political tensions in the Middle East, which increased the demand for the safe-haven currency, while the Japanese yen strengthened on speculation of a possible Bank of Japan interest rate hike in the near-future. Short positions in the Australian dollar relative to the U.S. dollar also incurred losses as the value of the Australian dollar moved higher from May to July on an unexpected interest rate hike by the Reserve Bank of Australia. Additional losses of approximately 1.8% were incurred within the energy markets throughout the first nine months of the year from futures positions in crude oil and its related products, as well as in natural gas. During February, long futures positions in crude oil and its related products recorded losses as prices declined after Chinese government authorities announced that China would place an emphasis on prospecting alternative energy sources in the future, reports of larger-than-expected supplies from the International Energy Agency, and mild weather in the U.S. Northeast. Further losses in the energy markets were recorded during March from short positions as prices reversed higher early in the month on supply fears. During May, losses were incurred from long futures positions in crude oil and its related products as prices fell after supply data showed an increase in domestic gasoline and crude oil inventories. Losses were also incurred from short positions in natural gas as prices moved higher on fears of a possible supply shortage. During June, newly established long positions in natural gas futures recorded losses as prices reversed lower on reports of a supply surplus

S-14

and fears of a slowing global economy. During July and August, losses were experienced from long futures positions in crude oil and its related products as prices moved lower after weaker-than-expected U.S. economic data led investors to believe that energy demand would be negatively affected and the U.S. Department of Labor reported an unexpected climb in domestic gasoline supplies. Prices were pressured further lower after news of an official cease-fire between Israel and Hezbollah militants in Lebanon and news that the Organization of Petroleum Exporting Countries reduced its 2006 oil demand growth forecast. Finally, the agricultural complex experienced losses of approximately 1.5% from positions in wheat, soybeans, and cocoa futures. Losses were incurred from long positions in wheat futures as prices fell in March, April, and June on forecasts for favorable weather in U.S. wheat-growing regions, while short futures positions in soybeans recorded losses as prices moved higher in March on speculative buying and increased demand. During the third quarter, losses were incurred primarily during July from long futures positions in wheat and soybean oil as prices decreased on forecasts of improved weather conditions across the growing regions of the U.S.

Spectrum Select recorded total trading results including interest income totaling $50,536,443 and expenses totaling $36,574,632, resulting in net income of $13,961,811 for the nine months ended September 30, 2006. The partnership's net asset value per unit increased from $27.45 at December 31, 2005 to $28.15 at September 30, 2006.

For the Nine Months Ended September 30, 2005.

The most significant trading losses of approximately 6.0% were incurred in the currency markets, primarily during the first quarter and August, from positions in foreign currencies versus the U.S. dollar. During January, long positions in Swiss franc and euro versus the U.S. dollar incurred losses after the U.S. dollar's value reversed sharply higher amid conflicting economic data, improvements in U.S. trade deficit numbers, and speculation for higher U.S. interest rates. The U.S. dollar's value also advanced in response to expectations that the Chinese government would announce postponement of Chinese yuan revaluation for the foreseeable future. Additional losses were recorded during February from short positions in the Swiss franc and euro versus the U.S. dollar as the U.S. dollar weakened in response to concern for the considerable U.S. Current-Account deficit expressed by U.S. Federal Reserve Chairman Alan Greenspan. The value of the U.S. dollar was further weakened during the remainder of February by a larger-than-expected drop in January leading economic indicators and news that South Korea's Central Bank would be reducing its U.S. dollar currency reserves. Long European currency positions versus the U.S. dollar also recorded losses during March after the value of the U.S. dollar reversed sharply higher benefiting from higher U.S. interest rates and consumer prices. During August, long U.S. dollar positions against the British pound, euro, and Swiss franc resulted in losses, as the value of the U.S. dollar declined amid higher crude oil prices, lower durable goods orders reported by the U.S. Commerce Department, the U.S. trade imbalance, and economic warnings from U.S. Federal Reserve Chairman Alan Greenspan. Losses of approximately 1.3% resulted in the metals markets from positions in both precious and base metals held primarily during the second quarter. During April and May, long futures positions in base metals recorded losses as prices fell due to news of increases in supply, fears that a slowing global economy would weaken demand, and a stronger U.S. dollar. During June, losses were recorded from short gold positions after prices reversed higher amid technically-based buying, while long futures positions in silver experienced losses amid strength in the U.S. dollar. In the agricultural markets, losses of approximately 0.8% were experienced primarily during the second quarter and July from long futures positions in corn, wheat, and cotton. During April, long futures positions in wheat resulted in losses as prices fell in response to favorable weather in growing regions, improved crop conditions, and reduced foreign demand. During May, losses stemmed from long futures positions in cotton as prices moved lower on supply increases and the lack of damage to crops by the touchdown of a hurricane in U.S. growing regions. During July, long futures positions in cotton incurred losses as prices moved lower earlier in the month amid news that the Bush Administration asked Congress to repeal a federal cotton subsidy in an effort to comply with a World Trade Organization ruling against the program. Prices also declined further after the U.S. Department of Agriculture reported weak demand. Long positions in corn futures also experienced losses later in the month after prices weakened in response to higher silo rates. Smaller partnership losses of approximately 0.3% were experienced in the global interest rate sector primarily during the third quarter from positions in U.S., Canadian, and Australian interest rates. During July, long U.S. interest rate futures positions experienced losses as prices declined following a rise in interest rates and after the U.S. Labor Department released its June employment report. During September, long positions in U.S. fixed-

S-15

income futures incurred losses as prices weakened after it was revealed that measurements of Hurricane Katrina's economic impact were not weak enough to deter the U.S. Federal Reserve from its policy of raising interest rates. Long positions in Canadian interest rate futures recorded losses as prices finished lower on strength in the equity markets and as the Bank of Canada raised its key interest rate for the first time in 11 months. Additional losses stemmed from long positions in Australian bonds as prices declined after Australia's largest ever annual jobs gain initiated speculation that the Reserve Bank of Australia would perhaps reconsider its stance on interest rates and lean towards future interest rate tightening. A portion of the partnership's overall losses for the first nine months of the year was offset by gains of approximately 4.1% recorded in the global stock index markets, primarily during the third quarter, from long positions in Pacific Rim and European stock index futures. During July, positive economic data out of the U.S. and Japan pushed global equity prices higher in the beginning of the month as a strong U.S. jobs number and better-than-expected Japanese corporate earnings supported growth estimates. Prices continued to strengthen after China reformed its U.S. dollar currency peg policy, leading market participants to conclude that a revaluation in the Chinese yuan would likely ease trade tensions between China, the U.S., Europe, and Japan. Finally, strong corporate earnings out of the European Union and the U.S. resulted in optimistic investor sentiment and pushed prices further. During September, long positions in Japanese stock index futures experienced gains as prices increased on positive comments from Bank of Japan Governor Toshihiko Fukui, who said that the Japanese economy was in the process of emerging from a soft patch. Additional sector gains resulted from long positions in European stock index futures as oil prices declined and investors embraced signs that the global economy could move forward despite Hurricane Katrina's devastation of the U.S. Gulf Coast. Additional partnership gains of approximately 2.8% were achieved in the energy markets primarily during August from long positions in natural gas, crude oil and its related products, as prices climbed higher on supply and demand concerns. After Hurricane Katrina struck the Gulf of Mexico, prices advanced further to touch record highs amid concern for heavily damaged, or even possibly destroyed, refineries and production facilities.

Spectrum Select recorded total trading results including interest income totaling $61,306 and expenses totaling $40,258,599, resulting in a net loss of $40,197,293 for the nine months ended September 30, 2005. The partnership's net asset value per unit decreased from $28.88 at December 31, 2004 to $26.89 at September 30, 2005.

Morgan Stanley Spectrum Technical L.P.

For the Nine Months Ended September 30, 2006.

The most significant trading losses of approximately 6.2% were recorded in the currency markets, primarily during the first half of the year, from short positions in the Japanese yen, Swiss franc, and Australian dollar versus the U.S. dollar. Throughout a majority of the first half of the year, the U.S. dollar moved lower on news that foreign central banks were beginning to diversify their currency reserves away from U.S. dollar-denominated assets, as well as uncertainty regarding the future of the U.S. Federal Reserve's interest rate tightening campaign. In addition, the Japanese yen and Swiss franc moved higher against the U.S. dollar during January and February as strong economic data out of Japan and Switzerland increased speculation that the Bank of Japan and Swiss National Bank might raise interest rates. During April, the Japanese yen strengthened on speculation of a possible Bank of Japan interest rate hike in the near-future, while the Swiss franc moved higher on political tensions in the Middle East, which increased the demand for the safe-haven currency. The Australian dollar also moved higher on an unexpected interest rate hike by the Reserve Bank of Australia in May. Losses in the currency markets were also incurred during February and March from long positions in the British pound relative to the U.S. dollar as the value of the pound finished lower after news that Gross Domestic Product in the United Kingdom for 2005 was weaker-than-expected. Smaller losses were experienced during March from short positions in the Norwegian krone versus the U.S. dollar as the value of the krone moved higher after the release of generally positive economic data from the euro-zone reinforced expectations that European interest rates would continue to rise. Additional losses of approximately 2.9% were incurred within the energy markets during February from long futures positions in crude oil and its related products as prices declined after Chinese government authorities announced that China would place an emphasis on prospecting alternative energy sources in the future, reports of larger-than-expected supplies from the International Energy Agency, and mild weather in the U.S. Northeast. During August and September, long futures positions in crude oil and its related products also incurred losses as prices moved lower after

S-16

weaker-than-expected U.S. economic data led investors to believe that energy demand would be negatively affected and the U.S. Department of Labor reported an unexpected climb in domestic gasoline supplies. Prices were pressured further lower after news of an official cease-fire between Israel and Hezbollah militants in Lebanon and news that the Organization of Petroleum Exporting Countries reduced its 2006 oil demand growth forecast. Finally, within the agricultural markets, losses of approximately 1.9% were incurred during the second and third quarter, primarily from short positions in live cattle futures as prices moved higher on strong demand. Meanwhile, losses were incurred during July and August from long positions in cocoa futures as prices fell on news from the International Cocoa Organization that global supplies were still adequate to meet demand. Elsewhere in the agricultural complex, losses were recorded from long positions in wheat futures as prices moved lower on forecasts of improved weather conditions across the wheat-growing regions of the U.S. Midwest. A portion of the partnership's overall losses for the first nine months of the year was offset by gains of approximately 8.2% in the metals markets throughout the first half of the year from long positions in copper, nickel, zinc, and aluminum futures as base metals prices rallied from March until May on strong global demand and on reports of falling inventories. Within precious metals, long positions in gold and silver futures experienced gains as gold and silver prices reached 25-year highs in May, benefiting from strong demand and lagging supply. Demand for gold was supported higher by continued geopolitical concerns regarding Iran's nuclear program, inflation concerns due to high energy prices, and solid global economic growth. Additional gains of approximately 3.7% were experienced in the global stock index markets primarily during January, March, April, and July from long positions in European, U.S., and Australian stock index futures as prices trended higher on strong corporate earnings and solid economic data. Additional gains in the global stock index markets were recorded during the third quarter from long positions in Hong Kong equity index futures as prices moved higher during July on news that Gross Domestic Product in China surged to 10.9% in the first six months of this year. During September, gains were experienced from long positions in European equity index and S&P 500 Index futures as prices increased on falling energy prices. In addition, the S&P 500 Index closed at a five-and-a-half-year high after the U.S. Conference Board reported a stronger-than-expected rebound in consumer confidence in September. Meanwhile, European equity index futures prices were supported higher on merger and acquisition activity and solid corporate earnings. Smaller gains of approximately 2.7% were recorded in the global interest rates markets primarily during the first and second quarter. Short positions in U.S., European, and Australian fixed-income futures experienced gains as prices trended lower throughout a majority of the first quarter amid strength in regional equity markets and investor sentiment that interest rates in the United States, the European Union, and Australia would rise. U.S. fixed-income futures prices continued to move lower into the second quarter following the release of stronger-than-expected U.S. economic data and the sixteenth consecutive interest rate hike by the U.S. Federal Reserve. Similarly in Germany, rising equity prices and strong economic growth pressured German fixed-income futures prices lower in the second quarter. Within the Australian interest rate market, prices were also pressured lower on an unexpected interest rate hike by the Reserve Bank of Australia.

Spectrum Technical recorded total trading results including interest income totaling $46,301,226 and expenses totaling $55,682,166, resulting in a net loss of $9,380,940 for the nine months ended September 30, 2006. The partnership's net asset value per unit decreased from $22.36 at December 31, 2005 to $22.09 at September 30, 2006.

For the Nine Months Ended September 30, 2005.

The most significant trading losses of approximately 5.8% were incurred in the currency markets during January, March, and August. During the first quarter, losses were recorded from long positions in the British pound and Swiss franc versus the U.S. dollar after the U.S. dollar's value advanced in response to speculation that China would move toward a flexible exchange and amid expectations for higher U.S. interest rates. During August, long U.S. dollar positions against the British pound and Swiss franc resulted in losses as the value of the U.S. dollar declined amid higher crude oil prices, lower durable goods orders, the U.S. trade imbalance, and economic warnings from U.S. Federal Reserve Chairman Alan Greenspan. Losses in the agricultural markets of approximately 5.2% resulted from positions in lean hogs, live cattle, the soybean complex, wheat, cocoa, sugar, and cotton. During the first quarter, losses were experienced from short futures positions in the soybean complex, wheat, and corn as prices reversed higher on news of extremely cold weather in the growing regions of the United States and rumors of a reduction on world output during 2005. Additional losses were experienced from long futures positions in lean hogs as prices weakened on news of a reduction in demand. Long lean hog futures experienced further losses during

S-17

March as prices declined on speculative selling. During April, long futures positions in cocoa and sugar resulted in losses after prices reversed lower on technically-based selling. Long futures positions in lean hogs and live cattle also incurred losses as prices finished lower on news of a reduction in foreign export demand. Long futures positions in lean hogs continued to incur losses as prices moved lower during May in response to continued weakening demand. Additional losses during the second quarter stemmed from short futures positions in corn as prices increased due to weather-related concerns for newly-planted crops in U.S. growing regions. Losses were also recorded late in the second quarter from short futures positions in sugar as prices declined on technically-based selling. In the global interest rate markets, losses of approximately 1.0% were incurred primarily during the third quarter from positions in Australian and U.S. interest rate futures. During July, long positions in U.S. interest rate futures resulted in losses as prices declined following a rise in interest rates and after the U.S. Labor Department released its June employment report. During August, short positions in U.S. fixed-income futures incurred losses as prices reversed higher on worries about the global economic impact of Hurricane Katrina and growing speculation that the U.S. Federal Reserve would stop raising interest rates sooner than previously thought. During September, long positions in Australian bond futures recorded losses as prices declined after Australia's largest ever annual jobs gain initiated speculation that the Reserve Bank of Australia would perhaps reconsider its stance on interest rates and lean towards future interest rate tightening. Additional losses stemmed from long positions in U.S. fixed-income futures as prices weakened after measurements of Hurricane Katrina's economic impact revealed that they were not weak enough to deter the U.S. Federal Reserve from its policy of raising interest rates. Smaller partnership losses of approximately 0.3% were incurred in the metals markets, primarily during the second quarter, from long futures positions in precious metals as prices reversed lower due to strength in the U.S. dollar. A portion of the partnership's overall losses for the first nine months of the year was offset by gains of approximately 6.0% achieved in the energy markets, primarily during August, from long positions in crude oil and its related products, and natural gas as prices climbed higher on supply and demand concerns. After Hurricane Katrina struck the Gulf of Mexico, prices advanced further to touch record highs amid concern for heavily damaged, or even possibly destroyed, refineries and production facilities. Additional gains of approximately 4.7% were experienced in the global stock index markets, primarily during the third quarter, from long positions in European and Pacific Rim stock index futures as prices increased amid positive economic data out of the U.S. and Japan, a strong U.S. jobs number, and better-than-expected Japanese corporate earnings. Prices continued to strengthen after China reformed its U.S. dollar currency peg policy. Finally, strong corporate earnings out of the European Union and the U.S. resulted in optimistic investor sentiment and pushed prices further. During September, long positions in Japanese stock index futures continued to gain as prices increased on positive comments from Bank of Japan Governor Toshihiko Fukui, who said that the Japanese economy was in the process of emerging from a soft patch. Additional sector gains resulted from long positions in European stock index futures as oil prices declined and investors embraced signs that the global economy could move forward despite Hurricane Katrina's devastation of the U.S. Gulf Coast.

Spectrum Technical recorded total trading results including interest income totaling $1,507,043 and expenses totaling $55,478,605, resulting in a net loss of $53,971,562 for the nine months ended September 30, 2005. The partnership's net asset value per unit decreased from $23.63 at December 31, 2004 to $21.96 at September 30, 2005.

Morgan Stanley Spectrum Strategic L.P.

For the Nine Months Ended September 30, 2006.

The most significant trading gains of approximately 18.7% were recorded in the metals markets throughout the first half of the year from long positions in copper, zinc, and aluminum futures as base metals prices rallied on strong global demand and reports of falling inventories. As a result, copper prices rose to all-time record highs during the month of May. Long positions in gold futures experienced gains as well as prices reached 25-year highs amid continued geopolitical concerns, inflation concerns, and solid global economic growth. Additional gains of approximately 2.7% were experienced within the global interest rate markets during the first quarter from short positions in U.S., European, and Japanese interest rate futures as prices trended lower amid strength in regional equity markets and investor sentiment that interest rates in the United States, the European Union, and Japan would rise. U.S. fixed-income futures continued to move lower into the second quarter following the release of stronger-than-expected U.S. economic data. Similarly, strong equity markets, solid economic growth, and concerns about rising oil

S-18

prices pressured European fixed-income futures prices lower. Smaller gains of approximately 1.6% were experienced within the global stock index markets primarily during the first quarter from long positions in European, U.S., and Japanese stock index futures as global equity markets trended higher on strong corporate earnings and solid economic data. Long positions in Hong Kong equity index futures recorded additional gains during April, July, and August as prices moved higher amid positive performance in the technology sector and speculation that the U.S. Federal Reserve's interest rate tightening campaign would come to an end in the near future. A portion of the partnership's overall gains for the first nine months of the year was offset by losses of approximately 3.1% in the currency markets from short positions in the Japanese yen, Swiss franc, and Australian dollar. During the first half of the year, the U.S. dollar moved lower on news that foreign central banks were beginning to diversify their currency reserves away from U.S. dollar-denominated assets, as well as uncertainty regarding the future of the U.S. Federal Reserve's interest rate tightening campaign. The Japanese yen and Swiss franc moved higher against the U.S. dollar during January and February as strong economic data out of Japan and Switzerland increased speculation that the Bank of Japan and Swiss National Bank might raise interest rates. During April, the Japanese yen strengthened on speculation of a possible Bank of Japan interest rate hike, while the Swiss franc moved higher on the political tensions in the Middle East, which increased the demand for the safe-haven currency. Meanwhile, the Australian dollar also moved higher on an unexpected interest rate hike by the Reserve Bank of Australia. Finally, currency losses were also incurred during February, March, and August from long positions in the British pound relative to the U.S. dollar as the value of the pound finished lower after news that Gross Domestic Product in the United Kingdom for 2005 was weaker-than-expected. Additional losses of approximately 3.0% were incurred throughout the third quarter within the agricultural markets from long positions in sugar futures as prices moved lower after a U.S. Department of Agriculture report showed that the cost of ethanol-production using sugarcane was higher-than-expected. Prices continued to fall under pressure from low physical demand and high inventories. Losses were also incurred from long positions in cocoa futures as prices moved lower during July and August after the International Cocoa Organization increased its world cocoa production estimates for the year amid signs of a bumper harvest in the Ivory Coast, the world's largest producer. Elsewhere in the agricultural complex, long futures positions in soybeans and soybean meal recorded losses during July and August as prices decreased on weak export data and cooler weather forecasted for the soybean-growing regions of the U.S. Finally, long positions in cotton futures incurred losses throughout the first nine months of the year as prices were pressured lower as the U.S. harvest progressed with favorable weather forecasted. Finally, losses of approximately 0.6% were incurred within the energy markets during February and May from both long and short positions in heating oil futures as prices experienced short-term volatility due to conflicting news regarding supply and demand.

Spectrum Strategic recorded total trading results including interest income totaling $30,084,871 and expenses totaling $17,438,715, resulting in net income of $12,646,156 for the nine months ended September 30, 2006. The partnership's net asset value per unit increased from $14.18 at December 31, 2005 to $15.26 at September 30, 2006.

For the Nine Months Ended September 30, 2005.