UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark one)

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

For the quarterly period ended March 31, 2021

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from: ____________________ to ____________________ |

Commission File No. 1-13219

OCWEN FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Florida | | 65-0039856 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 1661 Worthington Road, Suite 100 | | 33409 |

| West Palm Beach, | Florida | |

| (Address of principal executive office) | | (Zip Code) |

(561) 682-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 Par Value | OCN | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ | | | Smaller reporting company | ☒ |

| | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ☐ No x

Number of shares of common stock outstanding as of April 30, 2021: 8,708,271 shares

OCWEN FINANCIAL CORPORATION

FORM 10-Q

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Quarterly Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact included in this report, including statements regarding our financial position, business strategy and other plans and objectives for our future operations, are forward-looking statements.

Forward-looking statements may be identified by a reference to a future period or by the use of forward-looking terminology. Forward-looking statements are typically identified by words such as “expect”, “believe”, “foresee”, “anticipate”, “intend”, “estimate”, “goal”, “strategy”, “plan”, “target” and “project” or conditional verbs such as “will”, “may”, “should”, “could” or “would” or the negative of these terms, although not all forward-looking statements contain these words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. Readers should bear these factors in mind when considering forward-looking statements and should not place undue reliance on such statements. Forward-looking statements involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially from those suggested by such statements. In the past, actual results have differed from those suggested by forward-looking statements and this may happen again. Important factors that could cause actual results to differ include, but are not limited to, the risks discussed or referenced under Part II, Item 1A, Risk Factors and the following:

•uncertainty relating to the continuing impacts of the Coronavirus 2019 (COVID-19) pandemic, including with respect to the response of the U.S. government, state governments, the Federal National Mortgage Association (Fannie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac) (together, the GSEs), the Government National Mortgage Association (Ginnie Mae) and regulators;

•the potential for ongoing COVID-19 related disruption in the financial markets and in commercial activity generally, increased unemployment, and other financial difficulties facing our borrowers;

•the proportion of borrowers who enter into forbearance plans, the financial ability of borrowers to resume repayment and their timing for doing so;

•the extent to which our mortgage servicing right (MSR) joint venture with Oaktree Capital Management L.P. and its affiliates (Oaktree), other recent transactions and our enterprise sales initiatives will generate additional subservicing volume;

•our ability to deploy the proceeds of the senior secured notes in suitable investments at appropriate returns;

•our ability to close announced bulk acquisitions of MSRs, including the ability to obtain regulatory approvals, enter into definitive financing arrangements, and satisfy closing conditions, and the timing for doing so;

•our ability to enter into definitive agreements relating to MSR acquisitions and other transactions under negotiation or subject to letters of intent;

•the timing of our MSR joint venture’s receipt of Fannie Mae approval;

•the adequacy of our financial resources, including our sources of liquidity and ability to sell, fund and recover servicing advances, forward and reverse whole loans, and Home Equity Conversion Mortgage (HECM) and forward loan buyouts and put-backs, as well as repay, renew and extend borrowings, borrow additional amounts as and when required, meet our MSR or other asset investment objectives and comply with our debt agreements, including the financial and other covenants contained in them;

•increased servicing costs based on rising borrower delinquency levels or other factors;

•reduced collection of servicing fees and ancillary income and delayed collection of servicing revenue as a result of forbearance plans and moratoria on evictions and foreclosure proceedings;

•our ability to continue to improve our financial performance through cost re-engineering initiatives and other actions;

•our ability to continue to grow our lending business and increase our lending volumes in a competitive market and uncertain interest rate environment;

•uncertainty related to our long-term relationship and remaining agreements with New Residential Investment Corp. (NRZ), our largest servicing client;

•uncertainty related to claims, litigation, cease and desist orders and investigations brought by government agencies and private parties regarding our servicing, foreclosure, modification, origination and other practices, including uncertainty related to past, present or future investigations, litigation, cease and desist orders and settlements with state regulators, the Consumer Financial Protection Bureau (CFPB), State Attorneys General, the Securities and Exchange Commission (SEC), the Department of Justice or the Department of Housing and Urban Development (HUD);

•adverse effects on our business as a result of regulatory investigations, litigation, cease and desist orders or settlements and the reactions of key counterparties, including lenders, the GSEs and Ginnie Mae;

•our ability to comply with the terms of our settlements with regulatory agencies and the costs of doing so;

•any adverse developments in existing legal proceedings or the initiation of new legal proceedings;

•our ability to effectively manage our regulatory and contractual compliance obligations;

•uncertainty related to changes in legislation, regulations, government programs and policies, industry initiatives, best servicing and lending practices, and media scrutiny of our business and industry;

•the extent to which a recent judicial interpretation of the Fair Debt Collection Practices Act may require us to modify our business practices and expose us to increased expense and litigation risk;

•our ability to interpret correctly and comply with liquidity, net worth and other financial and other requirements of regulators, the GSEs and Ginnie Mae, as well as those set forth in our debt and other agreements;

•our ability to comply with our servicing agreements, including our ability to comply with our agreements with, and the requirements of, the GSEs and Ginnie Mae and maintain our seller/servicer and other statuses with them;

•our servicer and credit ratings as well as other actions from various rating agencies, including the impact of prior or future downgrades of our servicer and credit ratings;

•failure of our information technology or other security systems or breach of our privacy protections, including any failure to protect customers’ data;

•our reliance on our technology vendors to adequately maintain and support our systems, including our servicing systems, loan originations and financial reporting systems, and uncertainty relating to our ability to transition to alternative vendors, if necessary, without incurring significant cost or disruption to our operations;

•the loss of the services of our senior managers and key employees;

•uncertainty related to the actions of loan owners and guarantors, including mortgage-backed securities investors, the GSEs, Ginnie Mae and trustees regarding loan put-backs, penalties and legal actions;

•uncertainty related to the GSEs substantially curtailing or ceasing to purchase our conforming loan originations or the Federal Housing Administration (FHA) of the HUD or Department of Veterans Affairs (VA) ceasing to provide insurance;

•uncertainty related to our ability to continue to collect certain expedited payment or convenience fees and potential liability for charging such fees;

•uncertainty related to our reserves, valuations, provisions and anticipated realization of assets;

•uncertainty related to the ability of third-party obligors and financing sources to fund servicing advances on a timely basis on loans serviced by us;

•the characteristics of our servicing portfolio, including prepayment speeds along with delinquency and advance rates;

•our ability to successfully modify delinquent loans, manage foreclosures and sell foreclosed properties;

•uncertainty related to the processes for judicial and non-judicial foreclosure proceedings, including potential additional costs or delays or moratoria in the future or claims pertaining to past practices;

•our ability to adequately manage and maintain real estate owned (REO) properties and vacant properties collateralizing loans that we service;

•our ability to realize anticipated future gains from future draws on existing loans in our reverse mortgage portfolio;

•our ability to effectively manage our exposure to interest rate changes and foreign exchange fluctuations;

•our ability to effectively transform our operations in response to changing business needs, including our ability to do so without unanticipated adverse tax consequences;

•uncertainty related to the political or economic stability of the United States and of the foreign countries in which we have operations; and

•our ability to maintain positive relationships with our large shareholders and obtain their support for management proposals requiring shareholder approval.

Further information on the risks specific to our business is detailed within this report and our other reports and filings with the SEC including our Annual Report on Form 10-K for the year ended December 31, 2020 and our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K since such date. Forward-looking statements speak only as of the date they were made and we disclaim any obligation to update or revise forward-looking statements whether because of new information, future events or otherwise.

PART I – FINANCIAL INFORMATION

ITEM 1. UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEETS

(Dollars in thousands, except per share data)

| | | | | | | | | | | |

| | March 31, 2021 | | December 31, 2020 |

| Assets | | | |

| Cash and cash equivalents | $ | 259,108 | | | $ | 284,802 | |

| Restricted cash (amounts related to variable interest entities (VIEs) of $9,809 and $16,791) | 77,319 | | | 72,463 | |

| Mortgage servicing rights (MSRs), at fair value | 1,400,217 | | | 1,294,817 | |

| Advances, net (amounts related to VIEs of $623,570 and $651,576) | 786,678 | | | 828,239 | |

| | | |

| Loans held for sale ($500,814 and $366,364 carried at fair value) | 517,823 | | | 387,836 | |

| Loans held for investment, at fair value (amounts related to VIEs of $8,820 and $9,770) | 7,053,194 | | | 7,006,897 | |

| Receivables, net | 178,209 | | | 187,665 | |

| | | |

| Premises and equipment, net | 14,369 | | | 16,925 | |

| | | |

| | | |

| | | |

| | | |

| Other assets ($17,307 and $25,476 carried at fair value) (amounts related to VIEs of $3,221 and $4,544) | 484,871 | | | 571,483 | |

| | | |

| Total assets | $ | 10,771,788 | | | $ | 10,651,127 | |

| | | |

| Liabilities and Equity | | | |

| Liabilities | | | |

| Home Equity Conversion Mortgage-Backed Securities (HMBS) related borrowings, at fair value | $ | 6,778,195 | | | $ | 6,772,711 | |

| Advance match funded liabilities (related to VIEs) | 550,437 | | | 581,288 | |

| Other financing liabilities, at fair value (amounts related to VIEs of $8,820 and $9,770) | 559,184 | | | 576,722 | |

| Other secured borrowings, net | 1,066,022 | | | 1,069,161 | |

| Senior notes, net | 542,927 | | | 311,898 | |

| | | |

| Other liabilities ($10,012 and $4,638 carried at fair value) | 835,013 | | | 923,975 | |

| | | |

| Total liabilities | 10,331,778 | | | 10,235,755 | |

| | | |

| Commitments and Contingencies (Notes 20 and 21) | 0 | | 0 |

| | | |

| Stockholders’ Equity | | | |

| | | |

| Common stock, $.01 par value; 13,333,333 shares authorized; 8,701,530 and 8,687,750 shares issued and outstanding at March 31, 2021 and December 31, 2020, respectively | 87 | | | 87 | |

| | | |

| Additional paid-in capital | 572,500 | | | 556,062 | |

| Accumulated deficit | (123,139) | | | (131,682) | |

| Accumulated other comprehensive loss, net of income taxes | (9,438) | | | (9,095) | |

| | | |

| | | |

| Total stockholders’ equity | 440,010 | | | 415,372 | |

| Total liabilities and stockholders’ equity | $ | 10,771,788 | | | $ | 10,651,127 | |

The accompanying notes are an integral part of these unaudited consolidated financial statements

4

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per share data)

| | | | | | | | | | | | | | | |

| For the Three Months Ended March 31, | | |

| 2021 | | 2020 | | | | |

| Revenue | | | | | | | |

| Servicing and subservicing fees | $ | 171,738 | | | $ | 211,483 | | | | | |

| Reverse mortgage revenue, net | 21,826 | | | 22,797 | | | | | |

| Gain on loans held for sale, net | 5,721 | | | 13,331 | | | | | |

| | | | | | | |

| Other revenue, net | 8,309 | | | 6,231 | | | | | |

| Total revenue | 207,594 | | | 253,842 | | | | | |

| | | | | | | |

| MSR valuation adjustments, net | 21,208 | | | (174,120) | | | | | |

| | | | | | | |

| Operating expenses | | | | | | | |

| Compensation and benefits | 68,281 | | | 60,728 | | | | | |

| Servicing and origination | 27,470 | | | 20,256 | | | | | |

| Professional services | 17,322 | | | 25,637 | | | | | |

| Technology and communications | 13,143 | | | 15,193 | | | | | |

| Occupancy and equipment | 8,852 | | | 11,969 | | | | | |

| | | | | | | |

| | | | | | | |

| Other expenses | 4,561 | | | 3,431 | | | | | |

| Total operating expenses | 139,629 | | | 137,214 | | | | | |

| | | | | | | |

| Other income (expense) | | | | | | | |

| Interest income | 3,936 | | | 5,395 | | | | | |

| Interest expense | (28,452) | | | (29,982) | | | | | |

| Pledged MSR liability expense | (37,850) | | | (6,594) | | | | | |

| Loss on extinguishment of debt | (15,458) | | | 0 | | | | | |

| | | | | | | |

| | | | | | | |

| Other, net | 290 | | | 1,328 | | | | | |

| Total other expense, net | (77,534) | | | (29,853) | | | | | |

| | | | | | | |

| Income (loss) before income taxes | 11,639 | | | (87,345) | | | | | |

| Income tax expense (benefit) | 3,096 | | | (61,856) | | | | | |

| Net income (loss) | $ | 8,543 | | | $ | (25,489) | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| Earnings (loss) per share | | | | | | | |

| Basic | $ | 0.98 | | | $ | (2.84) | | | | | |

| Diluted | $ | 0.96 | | | $ | (2.84) | | | | | |

| | | | | | | |

| Weighted average common shares outstanding | | | | | | | |

| Basic | 8,688,009 | | | 8,990,589 | | | | | |

| Diluted | 8,877,492 | | | 8,990,589 | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements

5

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Dollars in thousands)

| | | | | | | | | | | | | | | |

| | For the Three Months Ended March 31, | | |

| | 2021 | | 2020 | | | | |

| Net income (loss) | $ | 8,543 | | | $ | (25,489) | | | | | |

| | | | | | | |

| Other comprehensive income, net of income taxes: | | | | | | | |

| | | | | | | |

| | | | | | | |

| Change in unfunded pension plan obligation liability | (367) | | | 46 | | | | | |

| Other | 24 | | | 36 | | | | | |

| Comprehensive income (loss) | $ | 8,200 | | | $ | (25,407) | | | | | |

| | | | | | | |

| | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements

6

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

FOR THE THREE MONTHS ENDED MARCH 31, 2021 AND 2020

(Dollars in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional Paid-in Capital | | (Accumulated Deficit) Retained Earnings | | Accumulated Other Comprehensive Income (Loss), Net of Income Taxes | | | | Total |

| | Shares | | Amount | | | | | |

| | | | | | | | | | | | | |

| Balance at December 31, 2020 | 8,687,750 | | | $ | 87 | | | $ | 556,062 | | | $ | (131,682) | | | $ | (9,095) | | | | | $ | 415,372 | |

| Net income | — | | | — | | | — | | | 8,543 | | | — | | | | | 8,543 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Issuance of common stock warrants, net of issuance costs | — | | | — | | | 15,753 | | | — | | | — | | | | | 15,753 | |

| Equity-based compensation and other | 13,780 | | | 0 | | | 685 | | | — | | | — | | | | | 685 | |

| Other comprehensive loss, net of income taxes | — | | | — | | | — | | | — | | | (343) | | | | | (343) | |

| Balance at March 31, 2021 | 8,701,530 | | | $ | 87 | | | $ | 572,500 | | | $ | (123,139) | | | $ | (9,438) | | | | | $ | 440,010 | |

| | | | | | | | | | | | | |

| Balance at December 31, 2019 | 8,990,816 | | | $ | 90�� | | | $ | 558,057 | | | $ | (138,542) | | | $ | (7,594) | | | | | $ | 412,011 | |

| Net loss | — | | | — | | | — | | | (25,489) | | | — | | | | | (25,489) | |

| | | | | | | | | | | | | |

| Cumulative effect of adoption of Financial Accounting Standards Board (FASB) Accounting Standards Update (ASU) No. 2016-13 | — | | | — | | | — | | | 47,038 | | | — | | | | | 47,038 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Repurchase of common stock | (377,484) | | | (4) | | | (4,601) | | | — | | | — | | | | | (4,605) | |

| | | | | | | | | | | | | |

| Equity-based compensation and other | 25,486 | | | 0 | | | 820 | | | — | | | — | | | | | 820 | |

| Other comprehensive income, net of income taxes | — | | | — | | | — | | | — | | | 82 | | | | | 82 | |

| Balance at March 31, 2020 | 8,638,818 | | | $ | 86 | | | $ | 554,276 | | | $ | (116,993) | | | $ | (7,512) | | | | | $ | 429,857 | |

The accompanying notes are an integral part of these unaudited consolidated financial statements

7

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Dollars in thousands)

| | | | | | | | | | | |

| For the Three Months Ended March 31, |

| 2021 | | 2020 |

| Cash flows from operating activities | | | |

| Net income (loss) | $ | 8,543 | | | $ | (25,489) | |

| Adjustments to reconcile net income (loss) to net cash (used in) provided by operating activities: | | | |

| MSR valuation adjustments, net | (21,208) | | | 174,120 | |

| Loss (gain) on sale of MSRs, net | 25 | | | (286) | |

| | | |

| Provision for bad debts | 6,545 | | | 4,879 | |

| Depreciation | 2,859 | | | 3,997 | |

| | | |

| | | |

| Amortization of debt issuance costs and discount | 1,624 | | | 2,662 | |

| Equity-based compensation expense | 863 | | | 746 | |

| Loss on extinguishment of debt | 15,458 | | | 0 | |

| | | |

| | | |

| | | |

| Loss (gain) on valuation of Pledged MSR financing liability | 1,551 | | | (30,697) | |

| Net gain on valuation of loans held for investment and HMBS-related borrowings | (6,513) | | | (17,910) | |

| Gain on loans held for sale, net | (5,721) | | | (13,331) | |

| | | |

| Origination and purchase of loans held for sale | (3,333,999) | | | (831,474) | |

| Proceeds from sale and collections of loans held for sale | 3,179,487 | | | 843,178 | |

| Changes in assets and liabilities: | | | |

| Decrease in advances, net | 38,704 | | | 29,428 | |

| (Increase) decrease in receivables and other assets, net | (2,447) | | | 13,642 | |

| (Decrease) increase in other liabilities | (13,245) | | | 18,033 | |

| Other, net | (2,833) | | | (521) | |

| Net cash (used in) provided by operating activities | (130,307) | | | 170,977 | |

| | | |

| Cash flows from investing activities | | | |

| Origination of loans held for investment | (326,735) | | | (294,932) | |

| Principal payments received on loans held for investment | 315,105 | | | 175,095 | |

| Purchase of MSRs | (41,556) | | | (29,828) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Proceeds from sale of real estate | 2,306 | | | 2,814 | |

| | | |

| | | |

| Other, net | (1,952) | | | (476) | |

| Net cash used in investing activities | (52,832) | | | (147,327) | |

| | | |

| Cash flows from financing activities | | | |

| Repayment of advance match funded liabilities, net | (30,851) | | | (53,158) | |

| | | |

| Repayment of other financing liabilities | (18,566) | | | (50,427) | |

| Proceeds from (repayment of) mortgage loan warehouse facilities, net | 157,720 | | | (43,103) | |

| Proceeds from MSR financing facilities | 64,098 | | | 61,028 | |

| Repayment of MSR financing facilities | (44,661) | | | (115,447) | |

| Repayment of Senior notes | (319,156) | | | 0 | |

| Proceeds from issuance of Senior notes and warrants | 572,944 | | | 0 | |

| Repayment of senior secured term loan (SSTL) borrowings | (188,700) | | | (126,066) | |

| Payment of debt issuance costs | (6,795) | | | (7,267) | |

| | | |

| Proceeds from sale of Home Equity Conversion Mortgages (HECM, or reverse mortgages) accounted for as a financing (HMBS-related borrowings) | 287,830 | | | 312,249 | |

| Repayment of HMBS-related borrowings | (311,562) | | | (172,429) | |

| | | |

| | | |

| Repurchase of common stock | 0 | | | (4,605) | |

| | | |

| | | |

| Other, net | 0 | | | (33) | |

| Net cash provided by (used in) financing activities | 162,301 | | | (199,258) | |

| | | |

| Net decrease in cash, cash equivalents and restricted cash | (20,838) | | | (175,608) | |

| Cash, cash equivalents and restricted cash at beginning of year | 357,265 | | | 492,340 | |

| Cash, cash equivalents and restricted cash at end of period | $ | 336,427 | | | $ | 316,732 | |

| | | |

| Supplemental non-cash investing and financing activities: | | | |

| | | |

| | | |

| | | |

| | | |

| Recognition of gross right-of-use asset and lease liability: | | | |

| Right-of-use asset | $ | 292 | | | $ | 2,695 | |

| Lease liability | 292 | | | 2,695 | |

| Transfers of loans held for sale to real estate owned (REO) | $ | 2,052 | | | $ | 768 | |

| Transfer from loans held for investment to loans held for sale | 901 | | | 578 | |

| | | |

| Derecognition of MSRs and financing liabilities: | | | |

| MSRs | $ | 0 | | | $ | (263,344) | |

| Financing liability - MSRs pledged (Rights to MSRs) | 0 | | | (263,344) | |

| Recognition of future draw commitments for HECM loans at fair value upon adoption of FASB ASU No. 2016-13 | $ | 0 | | | $ | 47,038 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within the unaudited consolidated balance sheets and the unaudited consolidated statements of cash flows:

| | | | | | | | | | | |

| March 31, 2021 | | March 31, 2020 |

| Cash and cash equivalents | $ | 259,108 | | | $ | 263,555 | |

| Restricted cash and equivalents: | | | |

| Debt service accounts | 15,930 | | | 15,868 | |

| Other restricted cash | 61,389 | | | 37,309 | |

| Total cash, cash equivalents and restricted cash reported in the statements of cash flows | $ | 336,427 | | | $ | 316,732 | |

The accompanying notes are an integral part of these unaudited consolidated financial statements

8

OCWEN FINANCIAL CORPORATION AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2021

(Dollars in thousands, except per share data and unless otherwise indicated)

| | |

| Note 1 - Organization and Basis of Presentation |

Organization

Ocwen Financial Corporation (NYSE: OCN) (Ocwen, OFC, we, us and our) is a non-bank mortgage servicer and originator providing solutions to homeowners, investors and others through its primary operating subsidiary, PHH Mortgage Corporation (PMC). We are headquartered in West Palm Beach, Florida with offices and operations in the United States (U.S.), the United States Virgin Islands (USVI), India and the Philippines. Ocwen is a Florida corporation organized in February 1988.

Ocwen directly or indirectly owns all of the outstanding common stock of its operating subsidiaries, including PMC since its acquisition on October 4, 2018, Ocwen Financial Solutions Private Limited (OFSPL) and Ocwen USVI Services, LLC (OVIS).

We perform servicing activities related to our own MSR portfolio (primary) and on behalf of other servicers (subservicing), the largest being New Residential Investment Corp. (NRZ), and investors (primary and master servicing), including the Federal National Mortgage Association (Fannie Mae) and Federal Home Loan Mortgage Corporation (Freddie Mac) (collectively, the GSEs), the Government National Mortgage Association (Ginnie Mae) and private-label securitizations (PLS, or non-Agency). As a subservicer or primary servicer, we may be required to make advances for certain property tax and insurance premium payments, default and property maintenance payments and principal and interest payments on behalf of delinquent borrowers to mortgage loan investors before recovering them from borrowers. Most, but not all, of our subservicing agreements provide for us to be reimbursed for any such advances by the owner of the servicing rights. Advances made by us as primary servicer are generally recovered from the borrower or the mortgage loan investor. As master servicer, we collect mortgage payments from primary servicers and distribute the funds to investors in the mortgage-backed securities. To the extent the primary servicer does not advance the scheduled principal and interest, as master servicer we are responsible for advancing the shortfall, subject to certain limitations.

We source our servicing portfolio through multiple channels, including recapture, retail, wholesale, correspondent, flow MSR purchase agreements, the GSE Cash Window programs and bulk MSR purchases. We originate, sell and securitize conventional (conforming to the underwriting standards of Fannie Mae or Freddie Mac; collectively referred to as Agency or GSE) loans and government-insured (Federal Housing Administration (FHA) or Department of Veterans Affairs (VA)) forward mortgage loans, generally with servicing retained. The GSEs or Ginnie Mae guarantee these mortgage securitizations. We originate and purchase Home Equity Conversion Mortgage (HECM) loans, or reverse mortgages, that are mostly insured by the FHA and we are an approved issuer of Home Equity Conversion Mortgage-Backed Securities (HMBS) that are guaranteed by Ginnie Mae.

We had a total of approximately 4,900 employees at March 31, 2021 of which approximately 3,000 were located in India and approximately 400 were based in the Philippines. Our operations in India and the Philippines primarily provide internal support services, principally to our loan servicing business and our corporate functions. Of our foreign-based employees, approximately 69% were engaged in supporting our loan servicing operations as of March 31, 2021.

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared in conformity with the instructions of the Securities and Exchange Commission (SEC) to Form 10-Q and SEC Regulation S-X, Article 10, Rule 10-01 for interim financial statements. Accordingly, they do not include all of the information and footnotes required by accounting principles generally accepted in the United States of America (GAAP) for complete financial statements. In our opinion, the accompanying unaudited consolidated financial statements contain all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation. The results of operations and other data for the three months ended March 31, 2021 are not necessarily indicative of the results that may be expected for any other interim period or for the year ending December 31, 2021. The unaudited consolidated financial statements presented herein should be read in conjunction with the audited consolidated financial statements and related notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2020.

In August 2020, Ocwen implemented a reverse stock split of its shares of common stock in a ratio of one-for-15. The number of shares, loss per share amounts, repurchase price per share amounts, and Common stock and Additional paid-in capital balances have been retroactively adjusted for all periods presented in this Quarterly Report on Form 10-Q to give effect

to the reverse stock split as if it occurred at the beginning of the first period presented. See Note 13 – Equity for additional information.

Use of Estimates and Assumptions

The preparation of financial statements in conformity with GAAP requires that management make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Such estimates and assumptions include, but are not limited to, those that relate to fair value measurements, income taxes and the provision for losses that may arise from contingencies including litigation proceedings. In developing estimates and assumptions, management uses all available information; however, actual results could materially differ from those estimates and assumptions.

Recently Adopted Accounting Standards

Income Taxes (ASC Topic 740): Simplifying the Accounting for Income Taxes (ASU 2019-12)

The FASB issued this ASU to ASC Topic 740, Income Taxes, as part of its overall simplification initiative to reduce costs and complexity of applying accounting standards while maintaining or improving the usefulness of the information provided to users of financial statements. Amendments include the removal of certain exceptions to the general principles of ASC Topic 740 in such areas as intraperiod tax allocation, year to date losses in interim periods and deferred tax liabilities related to outside basis differences. Amendments also include simplification in other areas such as interim recognition of enactment of tax laws or rate changes and accounting for a franchise tax (or similar tax) that is partially based on income.

Our adoption of this standard on January 1, 2021 did not have a material impact on our consolidated financial statements.

Debt—Debt with Conversion and Other Options and Derivatives and Hedging—Contracts in Entity's Own Equity—Accounting for Convertible Instruments and Contracts in an Entity's Own Equity (ASU 2020-06)

The amendments in this ASU simplify the accounting for certain financial instruments with characteristics of liabilities and equity by reducing the number of accounting models for convertible debt and convertible preferred stock instruments. In addition, this ASU amended the derivative guidance for the “own stock” scope exception and certain aspects when calculating earnings per share. The amendments in this ASU affect entities that issue convertible instruments and/or contracts in an entity’s own equity.

The amendments in this ASU are effective on January 1, 2022, with early adoption permitted on January 1, 2021. Our early adoption of this standard on January 1, 2021 did not have a material impact on our consolidated financial statements.

Investments—Equity Securities (ASC Topic 321), Investments—Equity Method and Joint Ventures (ASC Topic 323), and Derivatives and Hedging (ASC Topic 815) (ASU 2020-01)

The amendments in this ASU affect all entities that apply the guidance in ASC Topics 321, 323, and 815 and (1) elect to apply the measurement alternative or (2) enter into a forward contract or purchase an option to purchase securities that, upon settlement of the forward contract or exercise of the purchased option, would be accounted for under the equity method of accounting. The amendments clarify that forward or option contracts to purchase investments that will be accounted for using the equity method that do not meet the definition of a derivative under ASC Topic 815 are in the scope of ASC Topic 321. Therefore, when the purchase contract is considered a forward or option contract in the scope of this guidance, the investor would account for changes in the contract’s fair value prior to closing through earnings, unless the contract qualifies for the measurement alternative and it is elected. If the measurement alternative is elected, the change in the fair value of the contract would be reflected in earnings upon closing. In addition, if there are observable transactions or impairments before closing, the guidance would require remeasurement of the contract to fair value.

The guidance in this ASU also specifies that when applying the measurement alternative in ASC Topic 321, observable

transactions include those transactions by the investor that result in the application or discontinuation of the equity method

of accounting.

The amendments under this ASU are effective prospectively. Our adoption of this standard on January 1, 2021 did not have a material impact on our consolidated financial statements.

| | |

| Note 2 – Securitizations and Variable Interest Entities |

We securitize, sell and service forward and reverse residential mortgage loans and regularly transfer financial assets in connection with asset-backed financing arrangements. We have aggregated these transfers of financial assets and asset-backed financing arrangements using special purpose entities (SPEs) or variable interest entities (VIEs) into three groups: (1)

securitizations of residential mortgage loans, (2) financings of advances and (3) MSR financings. Financing transactions that do not use SPEs or VIEs are disclosed in Note 11 – Borrowings.

Securitizations of Residential Mortgage Loans

Transfers of Forward Loans

We sell or securitize forward loans that we originate or purchase from third parties, generally in the form of mortgage-backed securities guaranteed by the GSEs or Ginnie Mae. Securitization typically occurs within 30 days of loan closing or purchase. We act only as a fiduciary and do not have a variable interest in the securitization trusts. As a result, we account for these transactions as sales upon transfer.

The following table presents a summary of cash flows received from and paid to securitization trusts related to transfers of loans accounted for as sales that were outstanding:

| | | | | | | | | | | | | | |

| | Three Months Ended March 31, | |

| 2021 | | 2020 | | | |

| Proceeds received from securitizations | $ | 3,248,918 | | | $ | 820,001 | | | | |

| Servicing fees collected (1) | 13,178 | | | 12,252 | | | | |

| Purchases of previously transferred assets, net of claims reimbursed | (3,239) | | | (2,607) | | | | |

| $ | 3,258,857 | | | $ | 829,646 | | | | |

(1)We receive servicing fees based upon the securitized loan balances and certain ancillary fees, all of which are reported in Servicing and subservicing fees in the unaudited consolidated statements of operations.

In connection with these transfers, we retained MSRs of $34.3 million and $6.6 million during the three months ended March 31, 2021 and 2020, respectively. We securitize forward and reverse residential mortgage loans involving the GSEs and loans insured by the FHA or VA through Ginnie Mae.

Certain obligations arise from the agreements associated with our transfers of loans. Under these agreements, we may be obligated to repurchase the loans, or otherwise indemnify or reimburse the investor or insurer for losses incurred due to material breach of contractual representations and warranties.

The following table presents the carrying amounts of our assets that relate to our continuing involvement with forward loans that we have transferred with servicing rights retained as well as an estimate of our maximum exposure to loss including the UPB of the transferred loans:

| | | | | | | | | | | |

| March 31, 2021 | | December 31, 2020 |

| Carrying value of assets | | | |

| MSRs, at fair value | $ | 194,600 | | | $ | 137,029 | |

| | | |

| Advances | 140,720 | | | 143,361 | |

| UPB of loans transferred (1) | 20,175,148 | | | 18,062,856 | |

| Maximum exposure to loss | $ | 20,510,468 | | | $ | 18,343,246 | |

(1)Includes $4.0 billion and $4.1 billion of loans delivered to Ginnie Mae as of March 31, 2021 and December 31, 2020, respectively, and includes loan modifications delivered through the Ginnie Mae Early Buyout Program (EBO).

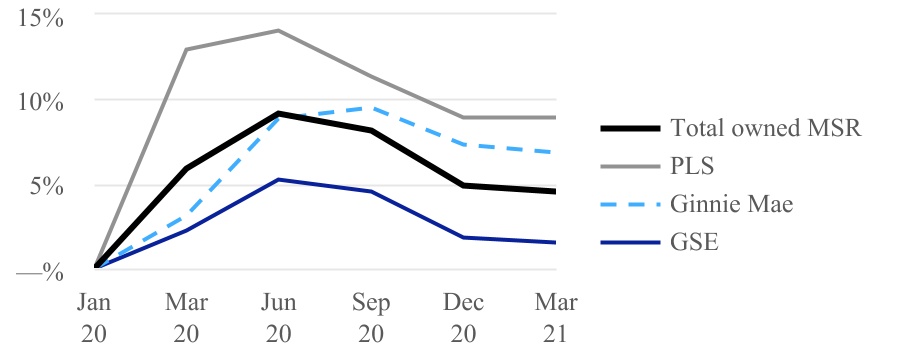

At March 31, 2021 and December 31, 2020, 5.5% and 6.8%, respectively, of the transferred residential loans that we service were 60 days or more past due, including 60 days or more past due loans under forbearance. This includes 15.2% and 17.1%, respectively, of loans delivered to Ginnie Mae that are 60 days or more past due.

Transfers of Reverse Mortgages

We pool HECM loans into HMBS that we sell into the secondary market with servicing rights retained or we sell the loans to third parties with servicing rights released. We have determined that loan transfers in the HMBS program do not meet the definition of a participating interest because of the servicing requirements in the product that require the issuer/servicer to absorb some level of interest rate risk, cash flow timing risk and incidental credit risk. As a result, the transfers of the HECM loans do not qualify for sale accounting, and therefore, we account for these transfers as financings. Under this accounting treatment, the HECM loans are classified as Loans held for investment, at fair value, on our unaudited consolidated balance sheets. Holders of participating interests in the HMBS have no recourse against the assets of Ocwen, except with respect to standard representations and warranties and our contractual obligation to service the HECM loans and the HMBS.

Financings of Advances using SPEs

Match funded advances, i.e., advances that are pledged as collateral to our advance facilities, result from our transfers of residential loan servicing advances to SPEs in exchange for cash. We consolidate these SPEs because we have determined that Ocwen is the primary beneficiary of the SPEs. These SPEs issue debt supported by collections on the transferred advances, and we refer to this debt as Advance match funded liabilities. Holders of the debt issued by the SPEs have recourse only to the assets of the SPE for satisfaction of the debt.

The table below presents the carrying value and classification of the assets and liabilities of the advance financing facilities:

| | | | | | | | | | | |

| March 31, 2021 | | December 31, 2020 |

| Match funded advances (Advances, net) | $ | 623,570 | | | $ | 651,576 | |

| Debt service accounts (Restricted cash) | 7,186 | | | 14,195 | |

| Unamortized deferred lender fees (Other assets) | 2,957 | | | 4,253 | |

| Prepaid interest (Other assets) | 263 | | | 291 | |

| Advance match funded liabilities | 550,437 | | | 581,288 | |

MSR Financings using SPEs

In 2019, we entered into a financing facility with a third-party secured by certain Fannie Mae and Freddie Mac MSRs (Agency MSRs). Two SPEs (trusts) were established in connection with this facility.

We determined that the trusts are VIEs for which we are the primary beneficiary. Therefore, we have included the trusts in our consolidated financial statements. We have the power to direct the activities of the VIEs that most significantly impact the VIE’s economic performance given that we are the servicer of the Agency MSRs that result in cash flows to the trusts. In addition, we have designed the trusts at inception to facilitate the third-party funding facility under which we have the obligation to absorb the losses of the VIEs that could be potentially significant to the VIEs.

The table below presents the carrying value and classification of the assets and liabilities of the Agency MSR financing facility:

| | | | | | | | | | | |

| March 31, 2021 | | December 31, 2020 |

| | | |

| MSRs pledged (MSRs, at fair value) | $ | 584,872 | | | $ | 476,371 | |

| Unamortized deferred lender fees (Other assets) | 606 | | | 1,183 | |

| Debt service account (Restricted cash) | 213 | | | 211 | |

| Outstanding borrowings (Other secured borrowings, net) | 250,000 | | | 210,755 | |

| | | |

| | | |

In 2019, we issued Ocwen Excess Spread-Collateralized Notes, Series 2019-PLS1 Class A (PLS Notes) secured by certain of PMC’s private label MSRs (PLS MSRs). An SPE, PMC PLS ESR Issuer LLC (PLS Issuer), was established in this connection as a wholly owned subsidiary of PMC. Ocwen guarantees the obligations of PLS Issuer under the facility.

We determined that PLS Issuer is a VIE for which we are the primary beneficiary. Therefore, we have included PLS Issuer in our consolidated financial statements. We have the power to direct the activities of the VIE that most significantly impact the VIE’s economic performance given that we are the servicer of the MSRs that result in cash flows to PLS Issuer. In addition, PMC has designed PLS Issuer at inception to facilitate the funding for general corporate purposes. Separately, in return for the participation interests, PMC received the proceeds from issuance of the PLS Notes. PMC is the sole member of PLS Issuer, thus PMC has the obligation to absorb the losses of the VIE that could be potentially significant to the VIE.

The table below presents the carrying value and classification of the assets and liabilities of the PLS Notes facility:

| | | | | | | | | | | |

| March 31, 2021 | | December 31, 2020 |

| | | |

| MSRs pledged (MSRs, at fair value) | $ | 123,422 | | | $ | 129,204 | |

| Debt service account (Restricted cash) | 2,410 | | | 2,385 | |

| Outstanding borrowings (Other secured borrowings, net) | 62,297 | | | 68,313 | |

| Unamortized debt issuance costs (Other secured borrowings, net) | 764 | | | 894 | |

| | | |

Fair value is estimated based on a hierarchy that maximizes the use of observable inputs and minimizes the use of unobservable inputs. Observable inputs are inputs that reflect the assumptions that market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The fair value hierarchy prioritizes the inputs to valuation techniques into three broad levels whereby the highest priority is given to Level 1 inputs and the lowest to Level 3 inputs.

The carrying amounts and the estimated fair values of our financial instruments and certain of our nonfinancial assets measured at fair value on a recurring or non-recurring basis or disclosed, but not measured, at fair value are as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | March 31, 2021 | | December 31, 2020 |

| | Level | | Carrying Value | | Fair Value | | Carrying Value | | Fair Value |

| Financial assets | | | | | | | | | |

| Loans held for sale | | | | | | | | | |

| Loans held for sale, at fair value (a) (e) | 3, 2 | | $ | 500,814 | | | $ | 500,814 | | | $ | 366,364 | | | $ | 366,364 | |

| Loans held for sale, at lower of cost or fair value (b) | 3 | | 17,009 | | | 17,009 | | | 21,472 | | | 21,472 | |

| Total Loans held for sale | | | $ | 517,823 | | | $ | 517,823 | | | $ | 387,836 | | | $ | 387,836 | |

| | | | | | | | | |

| Loans held for investment | | | | | | | | | |

| Loans held for investment - Reverse mortgages (a) | 3 | | $ | 7,044,374 | | | $ | 7,044,374 | | | $ | 6,997,127 | | | $ | 6,997,127 | |

| Loans held for investment - Restricted for securitization investors (a) | 3 | | 8,820 | | | 8,820 | | | 9,770 | | | 9,770 | |

| Total loans held for investment | | | $ | 7,053,194 | | | $ | 7,053,194 | | | $ | 7,006,897 | | | $ | 7,006,897 | |

| | | | | | | | | |

| Advances, net (c) | 3 | | $ | 786,678 | | | $ | 786,678 | | | $ | 828,239 | | | $ | 828,239 | |

| | | | | | | | | |

| Receivables, net (c) | 3 | | 178,209 | | | 178,209 | | | 187,665 | | | 187,665 | |

| Mortgage-backed securities (a) | 3 | | 1,613 | | | 1,613 | | | 2,019 | | | 2,019 | |

| | | | | | | | | |

| Corporate bonds (a) | 2 | | 211 | | | 211 | | | 211 | | | 211 | |

| | | | | | | | | |

| Financial liabilities: | | | | | | | | | |

| Advance match funded liabilities (c) | 3 | | $ | 550,437 | | | $ | 550,862 | | | $ | 581,288 | | | $ | 581,997 | |

| Financing liabilities: | | | | | | | | | |

| HMBS-related borrowings (a) | 3 | | $ | 6,778,195 | | | $ | 6,778,195 | | | $ | 6,772,711 | | | $ | 6,772,711 | |

| Financing liability - MSRs pledged (Rights to MSRs) (a) | 3 | | 550,364 | | | 550,364 | | | 566,952 | | | 566,952 | |

| Financing liability - Owed to securitization investors (a) | 3 | | 8,820 | | | 8,820 | | | 9,770 | | | 9,770 | |

| | | | | | | | | |

| Total Financing liabilities | | | $ | 7,337,379 | | | $ | 7,337,379 | | | $ | 7,349,433 | | | $ | 7,349,433 | |

| Other secured borrowings: | | | | | | | | | |

| Senior secured term loan (c) (d) | 2 | | $ | 0 | | | $ | 0 | | | $ | 179,776 | | | $ | 184,639 | |

| Mortgage warehouse and MSR financing (c) (d) | 3 | | 1,066,022 | | | 1,037,199 | | | 889,385 | | | 858,573 | |

| Total Other secured borrowings | | | $ | 1,066,022 | | | $ | 1,037,199 | | | $ | 1,069,161 | | | $ | 1,043,212 | |

| | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | March 31, 2021 | | December 31, 2020 |

| | Level | | Carrying Value | | Fair Value | | Carrying Value | | Fair Value |

| Senior notes: | | | | | | | | | |

| Senior notes (c) (d) (f) | 2 | | 391,377 | | | 399,537 | | | 311,898 | | | 320,879 | |

| OFC Senior notes due 2027 (c) (d) (f) | 3 | | 151,550 | | | 180,318 | | | 0 | | | 0 | |

| Total Senior notes | | | $ | 542,927 | | | $ | 579,855 | | | $ | 311,898 | | | $ | 320,879 | |

| | | | | | | | | |

| Derivative financial instrument assets (liabilities) | | | | | | | | | |

| Interest rate lock commitments (a) | 3 | | $ | 14,589 | | | $ | 14,589 | | | $ | 22,706 | | | $ | 22,706 | |

| Forward trades - Loans held for sale (a) | 2 | | (52) | | | (52) | | | (50) | | | (50) | |

| TBA / Forward mortgage-backed securities (MBS) trades (a) | 1 | | 480 | | | 480 | | | (4,554) | | | (4,554) | |

| Interest rate swap futures (a) | 1 | | (9,532) | | | (9,532) | | | 504 | | | 504 | |

| Other | 3 | | (14) | | | (14) | | | 0 | | | 0 | |

| | | | | | | | | |

| MSRs (a) | 3 | | $ | 1,400,217 | | | $ | 1,400,217 | | | $ | 1,294,817 | | | $ | 1,294,817 | |

| | | | | | | | | |

| | | | | | | | | |

(a)Measured at fair value on a recurring basis.

(b)Measured at fair value on a non-recurring basis.

(c)Disclosed, but not measured, at fair value.

(d)The carrying values are net of unamortized debt issuance costs and discount. See Note 11 – Borrowings for additional information.

(e)Loans repurchased from Ginnie Mae securitizations with a fair value of $71.4 million and $51.1 million at March 31, 2021 and December 31, 2020, respectively, are classified as Level 3. The remaining balance of loans held for sale at fair value is classified as Level 2.

(f)On March 4, 2021, PMC completed the issuance and sale of $400.0 million aggregate principal amount of senior secured notes. Fair value is based on valuation data obtained from a pricing service. Therefore, these notes are classified as Level 2. Additionally on March 4, 2021, Ocwen completed the private placement of $199.5 million aggregate principal amount of senior secured second lien notes. These notes are classified as Level 3 as we determine fair value based on valuations provided by third parties involved in the issuance and placement of the notes. These methodologies are consistent with our current fair value policies. See Note 11 – Borrowings for additional information.

The following tables present a reconciliation of the changes in fair value of Level 3 assets and liabilities that we measure at fair value on a recurring basis:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Loans Held for Investment - Restricted for Securitization Investors | | Financing Liability - Owed to Securitization Investors | | Loans Held for Sale - Fair Value | | Mortgage-Backed Securities | | | | IRLCs | | | | |

| Three months ended March 31, 2021 |

| Beginning balance | | | | | $ | 9,770 | | | $ | (9,770) | | | $ | 51,072 | | | $ | 2,019 | | | | | $ | 22,706 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Purchases, issuances, sales and settlements | | | | | | | | | | | | | | | | | | | |

| Purchases | | | | | 0 | | | 0 | | | 58,916 | | | 0 | | | | | 0 | | | | | |

| Issuances | | | | | 0 | | | 0 | | | 0 | | | 0 | | | | | 134,370 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Sales | | | | | 0 | | | 0 | | | (32,889) | | | 0 | | | | | 0 | | | | | |

| Settlements | | | | | (950) | | | 950 | | | 0 | | | 0 | | | | | 0 | | | | | |

| Transfers (to) from: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Loans held for sale, at fair value | | | | | 0 | | | 0 | | | 0 | | | 0 | | | | | (128,564) | | | | | |

| Other assets | | | | | 0 | | | 0 | | | (96) | | | 0 | | | | | 0 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | (950) | | | 950 | | | 25,931 | | | 0 | | | | | 5,806 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Change in fair value included in earnings | | | | | 0 | | | 0 | | | (5,640) | | | (406) | | | | | (13,923) | | | | | |

| Calls and other | | | | | 0 | | | 0 | | | 4 | | | 0 | | | | | 0 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | 0 | | | 0 | | | (5,636) | | | (406) | | | | | (13,923) | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Ending balance | | | | | $ | 8,820 | | | $ | (8,820) | | | $ | 71,367 | | | $ | 1,613 | | | | | $ | 14,589 | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Loans Held for Investment - Restricted for Securitization Investors | | Financing Liability - Owed to Securitization Investors | | Loans Held for Sale - Fair Value | | Mortgage-Backed Securities | | | | IRLCs | | | | |

| Three months ended March 31, 2020 |

| Beginning balance | | | | | $ | 23,342 | | | $ | (22,002) | | | $ | 0 | | | $ | 2,075 | | | | | $ | 0 | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Settlements | | | | | (781) | | | 637 | | | — | | | 0 | | | | | — | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Change in fair value included in earnings | | | | | 0 | | | 0 | | | | | (405) | | | | | — | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Transfers in and / or out of Level 3 | | | | | 0 | | | 0 | | | 25,582 | | | — | | | | | 10,478 | | | | | |

| Ending balance | | | | | $ | 22,561 | | | $ | (21,365) | | | $ | 25,582 | | | $ | 1,670 | | | | | $ | 10,478 | | | | | |

A rollforward of the beginning and ending balances of Loans Held for Investment and HMBS-related borrowings, MSRs and Financing liability - MSRs pledged that we measure at fair value on a recurring and non-recurring basis is provided in Note 5 – Reverse Mortgages, Note 7 – Mortgage Servicing and Note 8 — Rights to MSRs, respectively.

During the three months ended March 31, 2021, there have been no changes to the methodologies that we use in estimating fair values or classifications under the valuation hierarchy as disclosed in our Annual Report on Form 10-K for the year ended December 31, 2020. The significant unobservable assumptions that we make to estimate the fair value of significant assets and liabilities classified as Level 3 and measured at fair value on a recurring or non-recurring basis are provided below.

Loans Held for Sale

The fair value of loans we purchased from Ginnie Mae guaranteed securitizations is estimated using both observable and unobservable inputs, including published forward Ginnie Mae prices or existing sale contracts, as well as estimated default, prepayment, and discount rates. The significant unobservable input in estimating fair value is the estimated default rate. Accordingly, these repurchased Ginnie Mae loans are classified as Level 3 within the valuation hierarchy.

Loans Held for Investment - Reverse Mortgages

Reverse mortgage loans held for investment are carried at fair value and classified as Level 3 within the valuation hierarchy. Significant unobservable assumptions include voluntary prepayment speeds, defaults and discount rate. The

conditional prepayment speed assumption displayed in the table below is inclusive of voluntary (repayment or payoff) and involuntary (inactive/delinquent status and default) prepayments. The discount rate assumption is primarily based on an assessment of current market yields on reverse mortgage loan and tail securitizations, expected duration of the asset and current market interest rates.

| | | | | | | | | | | |

| Significant unobservable assumptions | March 31,

2021 | | December 31,

2020 |

| Life in years | | | |

| Range | 0.9 to 7.9 | | 0.9 to 8.0 |

| Weighted average | 5.5 | | 5.9 | |

| Conditional prepayment rate, including voluntary and involuntary prepayments | | | |

| Range | 10.7% to 37.6% | | 10.6% to 28.8% |

| Weighted average | 16.5 | % | | 15.4 | % |

| Discount rate | 2.4 | % | | 1.9 | % |

Significant increases or decreases in any of these assumptions in isolation could result in a significantly lower or higher fair value, respectively. The effects of changes in the assumptions used to value the loans held for investment, excluding future draw commitments, are partially offset by the effects of changes in the assumptions used to value the HMBS-related borrowings that are associated with these loans.

MSRs

MSRs are carried at fair value and classified within Level 3 of the valuation hierarchy. The fair value is determined using the mid-point of the range of prices provided by third-party valuation experts, without adjustment, except in the event we have a potential or completed sale, including transactions where we have executed letters of intent, in which case the fair value of the MSRs is recorded at the estimated sale price.

A change in the valuation inputs or assumptions may result in a significantly higher or lower fair value measurement. Changes in market interest rates predominantly impact the fair value for Agency MSRs via prepayment speeds by altering the borrower refinance incentive and the non-Agency MSRs due to the impact on advance costs. The significant unobservable assumptions used in the valuation of these MSRs include prepayment speeds, delinquency rates, cost to service and discount rates.

| | | | | | | | | | | | | | | | | | | | | | | |

| Significant unobservable assumptions | March 31, 2021 | | December 31, 2020 |

| Agency | | Non-Agency | | Agency | | Non-Agency |

| Weighted average prepayment speed | 10.0 | % | | 11.4 | % | | 11.8 | % | | 11.5 | % |

| Weighted average lifetime delinquency rate | 2.6 | % | | 27.8 | % | | 3.0 | % | | 28.0 | % |

| | | | | | | |

| | | | | | | |

| Weighted average discount rate | 9.2 | % | | 11.5 | % | | 9.2 | % | | 11.4 | % |

| Weighted average cost to service (in dollars) | $ | 76 | | | $ | 270 | | | $ | 79 | | | $ | 270 | |

Because the mortgages underlying these MSRs permit the borrowers to prepay the loans, the value of the MSRs generally tends to diminish in periods of declining interest rates, an improving housing market or expanded product availability (as prepayments increase) and increase in periods of rising interest rates, a deteriorating housing market or reduced product availability (as prepayments decrease). The following table summarizes the estimated change in the value of the MSRs as of March 31, 2021 given hypothetical shifts in lifetime prepayments and yield assumptions:

| | | | | | | | | | | |

| Adverse change in fair value | 10% | | 20% |

| Weighted average prepayment speeds | $ | (42,029) | | | $ | (82,863) | |

| Weighted average discount rate | (30,387) | | | (58,785) | |

The sensitivity analysis measures the potential impact on fair values based on hypothetical changes, which in the case of our portfolio at March 31, 2021 are increased prepayment speeds and an increase in the yield assumption.

Financing Liabilities

HMBS-Related Borrowings

HMBS-related borrowings are carried at fair value and classified as Level 3 within the valuation hierarchy. These borrowings are not actively traded, and therefore, quoted market prices are not available.

Significant unobservable assumptions include yield spread and discount rate. The yield spread and discount rate assumption for these liabilities are primarily based on an assessment of current market yields for newly issued HMBS, expected duration and current market interest rates.

| | | | | | | | | | | |

| Significant unobservable assumptions | March 31,

2021 | | December 31,

2020 |

| Life in years | | | |

| Range | 0.9 to 8.0 | | 0.9 to 8.0 |

| Weighted average | 5.9 | | 5.9 | |

| Conditional prepayment rate | | | |

| Range | 10.7% to 37.6% | | 10.6% to 28.8% |

| Weighted average | 16.5 | % | | 15.4 | % |

| Discount rate | 2.3 | % | | 1.7 | % |

Significant increases or decreases in any of these assumptions in isolation could result in a significantly higher or lower fair value, respectively. The effects of changes in the assumptions used to value the HMBS-related borrowings are partially offset by the effects of changes in the assumptions used to value the associated pledged loans held for investment, excluding future draw commitments.

MSRs Pledged (Rights to MSRs)

These liabilities carried at fair value and classified as Level 3 within the valuation hierarchy. We determine the fair value of the pledged MSR liability consistent with the mid-point of the range of prices provided by third-party valuation experts for the related MSR.

| | | | | | | | | | | |

| Significant unobservable assumptions | March 31,

2021 | | December 31,

2020 |

| Weighted average prepayment speed | 11.4 | % | | 11.5 | % |

| Weighted average delinquency rate | 29.5 | % | | 29.8 | % |

| | | |

| | | |

| Weighted average discount rate | 11.5 | % | | 11.4 | % |

| Weighted average cost to service (in dollars) | $ | 286 | | | $ | 287 | |

Significant increases or decreases in these assumptions in isolation would result in a significantly higher or lower fair value.

Derivative Financial Instruments

Interest rate lock commitments (IRLCs) are classified as Level 3 assets as fallout rates were determined to be significant unobservable assumptions.

| | |

| Note 4 – Loans Held for Sale |

| | | | | | | | | | | |

| Loans Held for Sale - Fair Value | Three Months Ended March 31, |

| 2021 | | 2020 |

| Beginning balance | $ | 366,364 | | | $ | 208,752 | |

| Originations and purchases | 3,333,901 | | | 831,474 | |

| Proceeds from sales | (3,169,015) | | | (805,202) | |

| Principal collections | (5,418) | | | (6,833) | |

| Transfers from (to): | | | |

| Loans held for investment, at fair value | 901 | | | 578 | |

| | | |

| Receivables, net | (8,633) | | | (31,302) | |

| REO (Other assets) | (2,052) | | | (768) | |

| Gain (loss) on sale of loans | (13,732) | | | 6,418 | |

| Decrease in fair value of loans | (5,256) | | | (1,642) | |

| Other | 3,754 | | | 2,117 | |

Ending balance (1) | $ | 500,814 | | | $ | 203,592 | |

(1)At March 31, 2021 and 2020, the balances include $(12.0) million and $(9.4) million, respectively, of fair value adjustments.

| | | | | | | | | | | |

| Loans Held for Sale - Lower of Cost or Fair Value | Three Months Ended March 31, |

| 2021 | | 2020 |

| Beginning balance - before Valuation Allowance | $ | 27,652 | | | $ | 73,160 | |

| Purchases | 98 | | | 0 | |

| Proceeds from sales | (4,840) | | | (30,492) | |

| Principal collections | (214) | | | (651) | |

| Transfers from (to): | | | |

| Receivables, net | 0 | | | 266 | |

| | | |

| | | |

| Gain on sale of loans | 389 | | | 1,842 | |

| | | |

| Other | (614) | | | 5,079 | |

| Ending balance - before Valuation Allowance | 22,471 | | | 49,204 | |

| | | |

| Beginning balance - Valuation Allowance | $ | (6,180) | | | $ | (6,643) | |

| Provision | 703 | | | (570) | |

| Transfer to (from) Liability for indemnification obligations (Other liabilities) | 15 | | | (25) | |

| Sales of loans | 0 | | | 457 | |

| | | |

| Ending balance - Valuation Allowance | (5,462) | | | (6,781) | |

| | | |

| Ending balance, net | $ | 17,009 | | | $ | 42,423 | |

| | | | | | | | | | | | | | | |

| Gain on Loans Held for Sale, Net | Three Months Ended March 31, | | |

| 2021 | | 2020 | | | | |

| Gain on sales of loans, net | | | | | | | |

| MSRs retained on transfers of forward mortgage loans | $ | 34,260 | | | $ | 6,561 | | | | | |

| | | | | | | |

| Gain (loss) on sale of forward mortgage loans | (18,567) | | | 6,418 | | | | | |

| Gain on sale of repurchased Ginnie Mae loans | 4,900 | | | 1,842 | | | | | |

| | | | | | | |

| | 20,593 | | | 14,821 | | | | | |

| Change in fair value of IRLCs | (8,618) | | | 5,714 | | | | | |

| Change in fair value of loans held for sale | (4,981) | | | 159 | | | | | |

| Gain (loss) on economic hedge instruments (1) | 0 | | | (7,192) | | | | | |

| Other | (1,273) | | | (171) | | | | | |

| $ | 5,721 | | | $ | 13,331 | | | | | |

(1)Excludes $35.4 million gain on inter-segment economic hedge derivative presented within MSR valuation adjustments, net for the three months ended March 31, 2021. Third-party derivatives are hedging the net exposure of MSR and pipeline, and the change in fair value of derivatives are reported within MSR valuation adjustments, net. Inter-segment derivatives are established to transfer risk and allocate hedging gains/losses to the pipeline separately from the MSR portfolio. Refer to Note 18 – Business Segment Reporting.

| | | | | | | | | | | | | | |

| Note 5 – Reverse Mortgages |

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, |

| 2021 | | 2020 |

| Loans Held for Investment - Reverse Mortgages | | HMBS - Related Borrowings | | Loans Held for Investment - Reverse Mortgages | | HMBS - Related Borrowings |

| Beginning balance | $ | 6,997,127 | | | $ | (6,772,711) | | | $ | 6,269,596 | | | $ | (6,063,434) | |

| Cumulative effect of fair value election (1) | — | | | — | | | 47,038 | | | — | |

| Originations | 326,735 | | | — | | | 294,932 | | | — | |

| Securitization of HECM loans accounted for as a financing | — | | | (287,830) | | | — | | | (312,249) | |

| Additional proceeds from securitization of HECM loans and tails | — | | | (12,565) | | | — | | | (8,414) | |

| Repayments (principal payments received) | (314,153) | | | 311,562 | | | (175,095) | | | 172,429 | |

| Transfers to: | | | | | | | |

| Loans held for sale, at fair value | (901) | | | — | | | (578) | | | — | |

| Receivables, net | (116) | | | — | | | (129) | | | — | |

| Other assets | (111) | | | — | | | (265) | | | — | |

| Change in fair value included in earnings | 35,793 | | | (16,651) | | | 133,322 | | | (111,423) | |

| Ending Balance | $ | 7,044,374 | | | $ | (6,778,195) | | | $ | 6,568,821 | | | $ | (6,323,091) | |

| Securitized loans (pledged to HMBS-Related Borrowings) | $ | 6,874,880 | | | $ | (6,778,195) | | | $ | 6,438,810 | | | $ | (6,323,091) | |

| Unsecuritized loans | 169,494 | | | | | 130,011 | | | |

| Total | $ | 7,044,374 | | | | | $ | 6,568,821 | | | |

(1)In conjunction with the adoption of ASU 2016-13, we elected the fair value option for future draw commitments (tails) on HECM reverse mortgage loans purchased or originated before December 31, 2018, which resulted in the recognition of the fair value of such tails through stockholders’ equity on January 1, 2020.

| | | | | | | | | | | | | | | |

| Reverse Mortgage Revenue, net | Three Months Ended March 31, | | |

| 2021 | | 2020 | | | | |

| Gain on new originations (1) | $ | 17,107 | | | $ | 16,784 | | | | | |

| Change in fair value of securitized loans held for investment and HMBS-related borrowings, net | 2,035 | | | 5,115 | | | | | |

| | | | | | | |

| Change in fair value included in earnings, net | 19,142 | | | 21,899 | | | | | |

| Loan fees and other | 2,684 | | | 898 | | | | | |

| $ | 21,826 | | | $ | 22,797 | | | | | |

(1)Includes the changes in fair value of newly originated loans held for investment in the period through securitization date.

| | | | | | | | | | | |

| | March 31, 2021 | | December 31, 2020 |

| Principal and interest | $ | 258,428 | | | $ | 277,132 | |

| Taxes and insurance | 348,659 | | | 364,593 | |

| Foreclosures, bankruptcy, REO and other | 185,750 | | | 192,787 | |

| | 792,837 | | | 834,512 | |

| Allowance for losses | (6,159) | | | (6,273) | |

| Advances, net | $ | 786,678 | | | $ | 828,239 | |

The following table summarizes the activity in net advances:

| | | | | | | | | | | |

| Three Months Ended March 31, |

| | 2021 | | 2020 |

| Beginning balance | $ | 828,239 | | | $ | 1,056,523 | |

| | | |

| | | |

| | | |

| New advances | 203,400 | | | 243,545 | |

| Sales of advances | (133) | | | (228) | |

| Collections of advances and other | (244,942) | | | (277,585) | |

| | | |

| Net decrease in allowance for losses | 114 | | | 2,552 | |

| Ending balance | $ | 786,678 | | | $ | 1,024,807 | |

| | | | | | | | | | | | | | | |

| Allowance for Losses | Three Months Ended March 31, | | |

| 2021 | | 2020 | | | | |

| Beginning balance | $ | 6,273 | | | $ | 9,925 | | | | | |

| Provision | 1,502 | | | (761) | | | | | |

| Net charge-offs and other | (1,616) | | | (1,791) | | | | | |

| Ending balance | $ | 6,159 | | | $ | 7,373 | | | | | |

| | |

| Note 7 – Mortgage Servicing |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| MSRs – Fair Value Measurement Method | Three Months Ended March 31, |

| 2021 | | 2020 |

| Agency | | Non-Agency | | Total | | Agency | | Non-Agency | | Total |

| Beginning balance | $ | 578,957 | | | $ | 715,860 | | | $ | 1,294,817 | | | $ | 714,006 | | | $ | 772,389 | | | $ | 1,486,395 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Sales and other transfers | 0 | | | 0 | | | 0 | | | 0 | | | (56) | | | (56) | |

| Additions: | | | | | | | | | | | |

| Recognized on the sale of residential mortgage loans | 34,260 | | | 0 | | | 34,260 | | | 5,930 | | | 0 | | | 5,930 | |

| Purchase of MSRs | 36,778 | | | 0 | | | 36,778 | | | 31,490 | | | 0 | | | 31,490 | |

| Servicing transfers and adjustments (1) | 29 | | | (557) | | | (528) | | | (263,630) | | | (893) | | | (264,523) | |

| Changes in fair value: | | | | | | | | | | | |

| Changes in valuation inputs or assumptions (2) | 82,486 | | | 1,529 | | | 84,015 | | | (166,532) | | | 5,871 | | | (160,661) | |

| Realization of expected cash flows (2) | (23,847) | | | (25,278) | | | (49,125) | | | (27,037) | | | (21,310) | | | (48,347) | |

| Ending balance | $ | 708,663 | | | $ | 691,554 | | | $ | 1,400,217 | | | $ | 294,227 | | | $ | 756,001 | | | $ | 1,050,228 | |

(1)Servicing transfers and adjustments include a $263.7 million derecognition of MSRs effective with the February 20, 2020 notice of termination of the subservicing agreement between NRZ and PMC. See Note 8 — Rights to MSRs for further information.

(2)Effective January 1, 2021, changes in fair value due to actual vs. model variances are presented as Changes in valuation inputs or assumptions. Activity for the three months ended March 31,2020 in the table above has been recast to conform to current year disclosure, resulting in a $4.5 million loss reclassified from Realization of expected cash flows to Changes in valuation inputs or assumptions.

MSR UPB

| | | | | | | | | | | | | | | | | |

| March 31, 2021 | | December 31, 2020 | | March 31, 2020 |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Owned MSRs | 91,284,985 | | | $ | 90,174,495 | | | $ | 70,741,200 | |

| NRZ pledged MSRs (1) | 61,841,181 | | | 64,061,198 | | | 70,914,910 | |

| Total MSR UPB | $ | 153,126,166 | | | $ | 154,235,693 | | | $ | 141,656,110 | |

(1)MSRs subject to sale agreements with NRZ that do not meet sale accounting criteria. See Note 8 — Rights to MSRs.

We purchased MSRs with a UPB of $6.0 billion and $2.9 billion during the three months ended March 31, 2021 and 2020, respectively. We sold MSRs with a UPB of $7.2 million and $17.6 million during the three months ended March 31, 2021 and 2020, respectively, mostly to Freddie Mac under the Voluntary Partial Cancellation (VPC) program for delinquent loans.

At March 31, 2021, the S&P Global Ratings, Inc.’s (S&P’s) servicer ratings outlook for PMC is stable. On March 24, 2020, Fitch Ratings, Inc. (Fitch) placed all U.S Residential Mortgage Backed Securities (RMBS) servicer ratings on Outlook Negative, resulting from a rapidly evolving economic and operating environment due to the sudden impact of the COVID-19 virus. On April 28, 2021, Fitch affirmed PMC’s servicer ratings and revised its outlook from Negative to Stable as PMC’s performance in this evolving environment has not raised any elevated concerns. According to Fitch, the affirmation and stable outlook reflected PMC’s diligent response to the coronavirus pandemic and its impact on servicing operations, effective enterprise-wide risk environment and compliance management framework, satisfactory loan servicing performance metrics, special servicing expertise, and efficient servicing technology. The ratings also consider the financial condition of PMC’s parent, OFC.

| | | | | | | | | | | | | | | |

| Servicing Revenue | Three Months Ended March 31, | | |

| 2021 | | 2020 | | | | |

| Loan servicing and subservicing fees | | | | | | | |

| Servicing | $ | 63,892 | | | $ | 55,408 | | | | | |

| Subservicing | 3,487 | | | 5,190 | | | | | |

| NRZ | 80,385 | | | 119,669 | | | | | |

| 147,764 | | | 180,267 | | | | | |

| Ancillary income | | | | | | | |

| Late charges | 9,231 | | | 14,639 | | | | | |

| Custodial accounts (float earnings) | 1,008 | | | 6,141 | | | | | |

| Loan collection fees | 2,949 | | | 4,256 | | | | | |

| | | | | | | |

| Recording fees | 3,651 | | | 2,558 | | | | | |

| Other, net | 7,135 | | | 3,622 | | | | | |

| 23,974 | | | 31,216 | | | | | |

| | $ | 171,738 | | | $ | 211,483 | | | | | |

Float balances (balances in custodial accounts, which represent collections of principal and interest that we receive from borrowers) are held in escrow by unaffiliated banks and are excluded from our unaudited consolidated balance sheets. Float balances amounted to $2.4 billion, $1.7 billion and $1.9 billion at March 31, 2021, December 31, 2020 and March 31, 2020, respectively.