UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2021

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from: ____________________ to ____________________ |

Commission File No. 1-13219

OCWEN FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Florida | | 65-0039856 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 1661 Worthington Road, Suite 100 | | 33409 |

| West Palm Beach, | Florida | |

| (Address of principal executive office) | | (Zip Code) |

(561) 682-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 Par Value | OCN | New York Stock Exchange |

Securities registered pursuant to Section 12 (g) of the Act: Not applicable.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | | | | | | | | | | |

| | Large Accelerated filer | ☐ | | | Accelerated filer | ☒ |

| | Non-accelerated filer | ☐ | | | Smaller reporting company | ☐ |

| | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ☐ No x

Aggregate market value of the voting and non-voting common equity of the registrant held by non-affiliates as of June 30, 2021: $277,835,518

Number of shares of common stock outstanding as of February 22, 2022: 9,208,312 shares

Documents incorporated by reference: Portions of our definitive Proxy Statement with respect to our Annual Meeting of Shareholders, which will be filed with the Securities and Exchange Commission within 120 days after the end of our fiscal year ended December 31, 2021, are incorporated by reference into Part III, Items 10 - 14.

OCWEN FINANCIAL CORPORATION

2021 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact included in this report, including, statements regarding our financial position, business strategy and other plans and objectives for our future operations, are forward-looking statements.

Forward-looking statements may be identified by a reference to a future period or by the use of forward-looking terminology. Forward-looking statements are typically identified by words such as “expect”, “believe”, “foresee”, “anticipate”, “intend”, “estimate”, “goal”, “strategy”, “plan” “target” and “project” or conditional verbs such as “will”, “may”, “should”, “could” or “would” or the negative of these terms, although not all forward-looking statements contain these words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. Readers should bear these factors in mind when considering forward-looking statements and should not place undue reliance on such statements. Forward-looking statements involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially from those suggested by such statements. In the past, actual results have differed from those suggested by forward-looking statements and this may happen again. Important factors that could cause actual results to differ include, but are not limited to, the risks discussed in Part I, Item 1A., Risk Factors and the following:

•uncertainty relating to the continuing impacts of the COVID-19 pandemic, including with respect to the response of the U.S. government, state governments, the Federal National Mortgage Association (Fannie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac) (together, the GSEs), the Government National Mortgage Association (Ginnie Mae) and regulators;

•the potential for ongoing COVID-19 related disruption in the financial markets and in commercial activity generally, employment disruption, and other financial difficulties facing our borrowers;

•the proportion of borrowers who enter into forbearance plans, the financial ability of borrowers to resume repayment and their timing for doing so;

•the extent to which our mortgage servicing right (MSR) joint venture with Oaktree Capital Management L.P. and its affiliates (Oaktree), other recent transactions and our enterprise sales initiatives will generate additional subservicing volume and result in increased profitability;

•our ability, and the ability of MSR Asset Vehicle LLC (MAV), to bid competitively for, and close acquisitions of, MSRs on terms that will enable us to achieve our growth objectives and a favorable return on our investment in MAV;

•our ability to reach an agreement to upsize MAV and the timing and terms of any such agreement;

•our ability to identify, enter into and close additional strategic transactions, including the ability to obtain regulatory approvals, enter into definitive financing arrangements, and satisfy closing conditions, and the timing for doing so;

•our ability to efficiently integrate the operations and assets of acquired businesses and to retain their employees and customers over time;

•the extent to which we will be able to execute call rights transactions, and whether such transactions will generate the returns anticipated;

•the adequacy of our financial resources, including our sources of liquidity and ability to sell, fund and recover servicing advances, forward and reverse whole loans, and Home Equity Conversion Mortgage (HECM) and forward loan buyouts and put-backs, as well as repay, renew and extend borrowings, borrow additional amounts as and when required, meet our MSR or other asset investment objectives and comply with our debt agreements, including the financial and other covenants contained in them;

•increased servicing costs based on rising borrower delinquency levels or other factors, including an increase in severe weather events resulting in property damage and financial hardship to our borrowers;

•reduced collection of servicing fees and ancillary income and delayed collection of servicing revenue as a result of forbearance plans and moratoria on evictions and foreclosure proceedings;

•our ability to continue to improve our financial performance through cost re-engineering initiatives and other actions;

•our ability to maintain and increase market share in our target markets;

•uncertainty related to our relationship and remaining agreements with New Residential Investment Corp. (NRZ), our largest servicing client, including the time horizon on which our subservicing agreements will renew or terminate;

•uncertainty related to past, present or future claims, litigation, cease and desist orders and investigations relating to our business practices, including those brought by private parties and state regulators, the Consumer Financial Protection Bureau (CFPB), State Attorneys General, the Securities and Exchange Commission (SEC), the Department of Justice or the Department of Housing and Urban Development (HUD);

•adverse effects on our business as a result of regulatory investigations, litigation, cease and desist orders or settlements and the reactions of key counterparties, including lenders, the GSEs and Ginnie Mae;

•the costs of complying with the terms of our settlements with regulatory agencies and disputes as to whether we have fully complied;

•any adverse developments in existing legal proceedings or the initiation of new legal proceedings;

•our ability to efficiently manage our regulatory and contractual compliance obligations and fully comply with all applicable requirements;

•uncertainty related to changes in legislation, regulations, government programs and policies, industry initiatives, best servicing and lending practices, and media scrutiny of our business and industry;

•the extent to which changes in the law as well as changes in the interpretation of law may require us to modify our business practices and expose us to increased expense and litigation risk;

•our ability to interpret correctly and comply with current or future liquidity, net worth and other financial and other requirements of regulators, the GSEs and Ginnie Mae, as well as those set forth in our debt and other agreements;

•our ability to comply with our servicing agreements, including our ability to comply with our agreements with the GSEs and Ginnie Mae and maintain our seller/servicer and other statuses with them;

•our servicer and credit ratings as well as other actions from various rating agencies, including the impact of prior or future downgrades of our servicer and credit ratings;

•failure of our, or our vendors’, information technology or other security systems or breach of our, or our vendors’, privacy protections, including any failure to protect customers’ data;

•our reliance on our technology vendors to adequately maintain and support our systems, including our servicing systems, loan originations and financial reporting systems, and uncertainty relating to our ability to transition to alternative vendors, if necessary, without incurring significant cost or disruption to our operations;

•increased difficulty recruiting and retaining existing or new senior managers and key employees;

•increased compensation and benefits expense as a result of rising inflation and labor market trends;

•uncertainty related to the actions of loan owners and guarantors, including mortgage-backed securities investors, the GSEs, Ginnie Mae and trustees regarding loan put-backs, penalties and legal actions;

•uncertainty related to the GSEs substantially curtailing or ceasing to purchase our conforming loan originations or the Federal Housing Administration (FHA) of the HUD or Department of Veterans Affairs (VA) ceasing to provide insurance;

•uncertainty related to our ability to continue to collect certain expedited payment or convenience fees and potential liability for charging such fees;

•uncertainty related to our reserves, valuations, provisions and anticipated realization of assets;

•uncertainty related to the ability of third-party obligors and financing sources to fund servicing advances on a timely basis on loans serviced by us;

•the characteristics of our servicing portfolio, including prepayment speeds along with delinquency and advance rates;

•our ability to successfully modify delinquent loans, manage foreclosures and sell foreclosed properties;

•uncertainty related to the processes for judicial and non-judicial foreclosure proceedings, including potential additional costs or delays or moratoria in the future or claims pertaining to past practices;

•our ability to adequately manage and maintain real estate owned (REO) properties and vacant properties collateralizing loans that we service;

•our ability to realize anticipated future gains from future draws on existing loans in our reverse mortgage portfolio;

•our ability to effectively manage our exposure to interest rate changes and foreign exchange fluctuations;

•uncertainty relating to the likely replacement of the London Interbank Offered Rate (LIBOR) with the Secured Overnight Financing Rate (SOFR) and its impact on our credit arrangements;

•our ability to effectively transform our operations in response to changing business needs, including our ability to do so without unanticipated adverse tax consequences;

•increasingly frequent and costly disruptions to our operations as a result of severe weather events;

•uncertainty related to the political or economic stability of the United States and of the foreign countries in which we have operations; and

•our ability to maintain positive relationships with our large shareholders and obtain their support for management proposals requiring shareholder approval.

Further information on the risks specific to our business is detailed within this report, including under “Risk Factors.” Forward-looking statements speak only as of the date they were made and we disclaim any obligation to update or revise forward-looking statements whether because of new information, future events or otherwise.

PART I

ITEM 1. BUSINESS

When we use the terms “Ocwen,” “OCN,” “we,” “us” and “our,” we are referring to Ocwen Financial Corporation and its consolidated subsidiaries.

OVERVIEW

We are a financial services company that services and originates both forward and reverse mortgage loans, through our primary brands, PHH Mortgage and Liberty Reverse Mortgage. We have a strong track record of success as a leader in the servicing industry in foreclosure prevention and loss mitigation that helps homeowners stay in their homes and improves financial outcomes for mortgage loan investors. This long-standing core competency will continue to be a guiding principle as we seek to grow our business and improve our financial performance. We are a leader in the reverse mortgage business with a strong brand and have expanded our reverse mortgage servicing competitive advantage with our acquisition of the Reverse Mortgage Servicing platform in the fourth quarter of 2021.

We are headquartered in West Palm Beach, Florida with offices and operations in the U.S., in the United States Virgin Islands (USVI), in India and the Philippines. At December 31, 2021, approximately 64% of our workforce is located outside the U.S. Ocwen Financial Corporation is a Florida corporation organized in February 1988. With our predecessors, we have been servicing residential mortgage loans since 1988. We have been originating forward mortgage loans since 2012 and reverse mortgage loans since 2013. We currently provide solutions through our primary operating, wholly-owned subsidiary, PHH Mortgage Corporation (PMC).

BUSINESS MODEL AND SEGMENTS

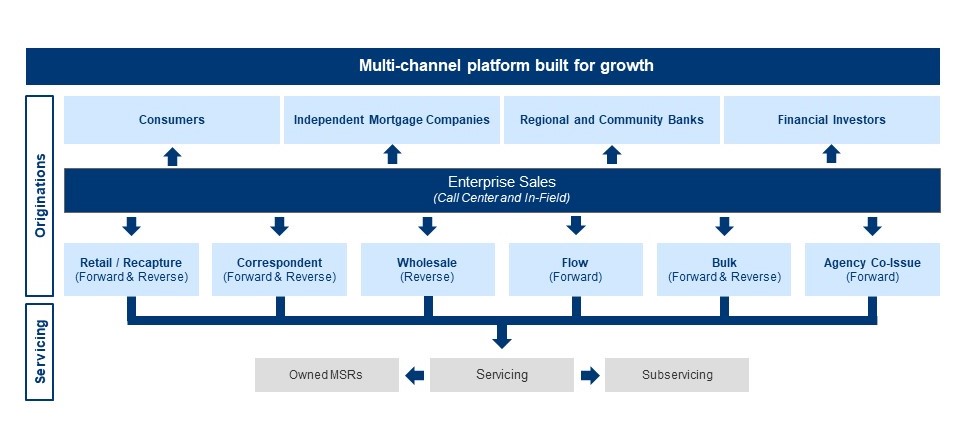

Ocwen’s business model is designed to create value and maximize returns for our shareholders, and effectively allocate our resources. Following the acquisition and integration of PHH Corporation (PHH) in late 2018 and 2019, we have transformed into a balanced and diversified business. We seek to create value for shareholders through profitable growth, service excellence and high quality operational execution. Our core competencies revolve around our Servicing business and we have developed a profitable Originations platform to replenish and pursue growth of our servicing portfolio.

Our Servicing business is comprised of two components, our owned MSRs and our subservicing portfolio that complement each other’s when managing scale. We invest our capital to fund purchases and originations of our owned MSRs and servicing advances, for which we establish a targeted return on investment. Our net return includes servicing revenue net of servicing costs, less MSR portfolio runoff, and less our MSR and advance funding cost. Our net return also includes fair value changes of our owned MSR that vary based on market conditions. Our subservicing portfolio generates a relatively stable source of revenue. While subservicing fees are relatively lower, we do not incur any significant capital utilization or funding of advances and are not exposed to fair value volatility. In 2021, we expanded our servicing portfolio with the launch of our MSR joint venture with Oaktree, MAV. At December 31, 2021, PMC serviced residential mortgage loans on behalf of MAV with an unpaid principal balance (UPB) of $33.0 billion or 12% of our total servicing portfolio - see the “Oaktree Relationship” section below for further details. Our MAV and NRZ servicing portfolios are effectively subservicing relationships. We target a balanced mix of our portfolio between servicing and subservicing based on capital allocation and returns. Our servicing operations and customer interactions do not differentiate whether loans are serviced or subserviced. Our leadership and experience in dealing with distressed economic conditions and non-performing loans allowed us to quickly adapt to the COVID-19 pandemic and provide payment relief and assistance to borrowers enduring financial hardship, and loan modification or other solutions to exit forbearance in a relatively seamless manner. In 2021, we expanded our capability in reverse servicing by acquiring the Mortgage Assets Management, LLC (formerly known as Reverse Mortgage Solutions, Inc.) (MAM (RMS)) servicing platform - see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Overview for further details.

Our Originations business’ strategy is to provide self-sustained replenishment opportunities to our servicing portfolio and profitable growth. Our Originations success is built on our relationships with borrowers, lenders and other market participants. We purchase MSRs through bulk portfolio purchases, through flow purchase agreements with our network of mortgage companies and financial institutions, and through participation in the Agency Cash Window (or Co-Issue) programs. In order to diversify our sources of servicing and reduce our reliance on others, we have been developing our origination of MSRs through different channels, including our portfolio recapture channel, retail, wholesale and correspondent lending. In 2021, we expanded our correspondent lending channel by acquiring TCB’s network of approximately 220 correspondent lenders.

The chart below summarizes our current business model:

We report our activities in three segments, Servicing, Originations and Corporate Items and Other, which reflect other business activities that are currently individually insignificant. Our business segments reflect the internal reporting that we use to evaluate operating performance of services and to assess the allocation of our resources. The financial information of our segments is presented in our financial statements in Note 23 — Business Segment Reporting and discussed in the individual business operations sections of Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Servicing

Our Servicing business is primarily comprised of our residential forward mortgage servicing business that currently accounts for the majority of our total revenues, our reverse mortgage servicing business, and our small commercial mortgage servicing business. Our servicing clients include some of the largest financial institutions in the U.S., including the GSEs, Ginnie Mae, NRZ and non-Agency residential mortgage-backed securities (RMBS) trusts, MAV and MAM (RMS).

As of December 31, 2021, our servicing portfolio consisted of approximately 1.4 million loans with a UPB of $268.0 billion.

Servicing involves the collection of principal and interest payments from borrowers, the administration of tax and insurance escrow accounts, the collection of insurance claims, the management of loans that are delinquent or in foreclosure or bankruptcy, including making servicing advances, evaluating loans for modification and other loss mitigation activities and, if necessary, foreclosure referrals and the sale of the underlying mortgaged property following foreclosure (REO) on behalf of mortgage loan investors or other servicers. Master servicing involves the collection of payments from servicers and the distribution of funds to investors in mortgage and asset-backed securities and whole loan packages. We earn contractual monthly servicing fees (which are typically payable as a percentage of UPB) pursuant to servicing agreements as well as other ancillary fees relating to our servicing activities such as late fees and, in certain circumstances, REO referral commissions.

We own MSRs outright, where we typically receive all the servicing economics, and we subservice on behalf of other institutions that own the MSRs, in which case we typically earn a smaller fee for performing the subservicing activities. Special servicing is a form of subservicing where we generally manage only delinquent loans on behalf of a loan owner. We typically earn subservicing and special servicing fees either as a percentage of UPB or on a per loan basis based on delinquency status.

Servicing advances are an important component of our business and are amounts that we, as MSR owner, are required to advance to, or on behalf of, investors if we do not receive such amounts from borrowers. These amounts include principal and interest payments, property taxes and insurance premiums and amounts to maintain, repair and market real estate properties on behalf of our servicing clients. Most of our advances have the highest reimbursement priority such that we are entitled to repayment of the advances from the loan or property liquidation proceeds before most other claims on these proceeds. Advances are contractually non-interest bearing. The costs incurred by servicers in meeting advancing obligations consist principally of the interest expense incurred in financing the advance receivables and the costs of arranging such financing. Under subservicing agreements, Ocwen is promptly reimbursed by the owners of the MSRs who generally finance the advances and incur the associated financing cost.

Reducing delinquencies is important to our business because it enables us to recover advances and recognize additional ancillary income, such as late fees, which we do not recognize on delinquent loans until they are brought current. Performing loans also require less work and thus are generally less costly to service. While increasing borrower participation in loan modification programs is a critical component of our ability to reduce delinquencies, borrower compliance with those modifications is also an important factor.

Our servicing portfolio naturally decreases over time as homeowners make regularly scheduled mortgage payments, prepay loans prior to maturity, refinance with a mortgage loan not serviced by us or involuntarily liquidate through foreclosure or other liquidation process. In addition, existing clients may determine to terminate their servicing and subservicing arrangements with us and transfer the servicing to others. Therefore, our ability to maintain or grow our servicing revenue or the size of our servicing portfolio depends on our ability to acquire the right to service or subservice additional mortgage loans at a rate that exceeds portfolio runoff and any client terminations. Our Originations segment is focused on profitably replenishing and growing our servicing and subservicing portfolios.

Originations

The primary source of revenue of our Originations segment is our gain on sale of loans. We originate and purchase residential mortgage loans that we sell to Agencies or securitize on a servicing retained basis, thereby generating mortgage servicing rights. Our mortgage loans are conventional (conforming to the underwriting standards of the GSEs, collectively Agency loans) and government-insured loans (insured by the FHA or VA). We generally package and sell the loans in the secondary mortgage market, through GSE and Ginnie Mae guaranteed securitizations and whole loan transactions. We originate forward mortgage loans directly with customers (consumer direct channel, previously recapture) as well as through correspondent lending arrangements since the second quarter of 2019. We originate reverse mortgage loans in all three channels, through our correspondent lending arrangements, broker relationships (wholesale) and retail channels. Per-loan margins vary by channel, with correspondent typically being the lowest margin and retail the highest, commensurate with fulfillment costs.

In addition to our originated MSRs, we acquire MSRs through multiple channels, including flow purchase agreements, the Agency Cash Window programs and bulk MSR purchases. Our Originations business also includes the sourcing and acquisition of new subservicing clients.

In 2021, our Originations business generated a total volume of $152.0 billion in UPB (refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Overview for further details).

Retail Lending. We originate forward and reverse mortgage loans directly with borrowers through our retail lending business. Our forward lending business benefits from our servicing portfolio by offering refinance options to qualified borrowers seeking to lower their mortgage payments. Depending on borrower eligibility, we refinance eligible customers into conforming or government-insured products. We are focused on increasing recapture rates on our existing servicing portfolio to grow this business. We also are increasing our ability to originate retail loans to non-Ocwen servicing customers through various marketing channels. Through lead campaigns and direct marketing, the retail channel seeks to convert leads into loans in a cost-efficient manner.

Correspondent Lending. Our correspondent lending operation purchases forward and reverse mortgage loans that have been originated by a network of approved third-party lenders. All the lenders participating in our correspondent lending program are approved by senior management members of our lending and risk management teams. We also employ an ongoing monitoring and renewal process for participating lenders that includes an evaluation of the performance of the loans they have sold to us. We perform a variety of pre- and post-funding review procedures to ensure that the loans we purchase conform to our requirements and to the requirements of the investors to whom we sell loans.

Wholesale Lending. We originate reverse mortgage loans through a network of approved brokers. Brokers are subject to a formal approval and monitoring process. We underwrite all loans originated through this channel consistent with the underwriting standards required by the ultimate investor prior to funding.

We provide customary origination representations and warranties to investors in connection with our loan sales and securitization activities. We receive customary origination representations and warranties from our network of approved originators relating to loans we purchase through our correspondent lending channel. In the event we cannot remedy a breach of a representation or warranty, we may be required to repurchase the loan or provide an indemnification payment to the investor. To the extent that we have recourse against a third-party originator, we may recover part or all of any loss we incur.

MSR Purchases. We purchase MSRs through flow purchase agreements, the Agency Cash Window programs and bulk MSR purchases. The Agency Cash Window programs we participate in, and purchase MSRs from, allow mortgage companies and financial institutions to sell whole loans to the respective Agency and sell the MSR to the winning bidder servicing released. In addition, we partner with other originators to replenish our MSR through flow purchase agreements. We do not

provide any origination representations and warranties in connection with our MSR purchases through MSR flow purchase agreements or Agency Cash Window programs.

New Servicing and Subservicing Acquisitions. Our enterprise sales department strives to expand our network of servicing and subservicing clients and source new flow and co-issue or subservicing agreements. We compete as a low cost provider with our demonstrated expertise to service mortgage assets across borrowers of every credit level and with our recapture ability.

REGULATION

Our business is subject to extensive regulation and supervision by federal, state, local and foreign governmental authorities, including the CFPB, HUD, the SEC and various state agencies that license and conduct examinations of our loan servicing, origination and collection activities. From time to time, we also receive information requests and other inquiries, both formal and informal in nature, (including requests in the form of subpoenas and civil investigative demands) from federal, state and local agencies for records, documents and information relating to the policies, procedures and practices of our loan servicing, origination and collection activities. Many of our regulatory engagements arise from a complaint that the entity is investigating, although some are formal investigations or proceedings. The GSEs and their conservator, the Federal Housing Finance Authority (FHFA), HUD, FHA, VA, Ginnie Mae, the United States Treasury Department, various investors, non-Agency securitization trustees and others also subject us to periodic reviews and audits.

In the current regulatory environment, we have faced and expect to continue to face heightened regulatory and public scrutiny as an organization as well as stricter and more comprehensive regulation of the entire mortgage sector. We continue to work diligently to assess and understand the implications of the regulatory environment in which we operate and to meet the requirements of this constantly changing environment. In the normal course of business, we incur significant costs to address regulatory requirements in each of our three lines of defense. We devote substantial resources to regulatory compliance, while, at the same time, striving to meet the needs and expectations of our customers, clients and other stakeholders. See Item 1A. Risk Factors – Legal and Regulatory Risks for further information.

We must comply with a large number of federal, state and local consumer protection and other laws and regulations, including, among others, the CARES Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act), the Telephone Consumer Protection Act (TCPA), the Gramm-Leach-Bliley Act, the Fair Debt Collection Practices Act (FDCPA), the Real Estate Settlement Procedures Act (RESPA), the Truth in Lending Act (TILA), the Servicemembers Civil Relief Act, the Homeowners Protection Act, the Federal Trade Commission Act, the Fair Credit Reporting Act, the Equal Credit Opportunity Act, as well as individual state laws pertaining to licensing, general mortgage origination and servicing practices and foreclosure, and federal and local bankruptcy rules. These laws and regulations apply to all facets of our business, including, but not limited to, licensing, loan originations, consumer disclosures, default servicing and collections, foreclosure, filing of claims, registration of vacant or foreclosed properties, handling of escrow accounts, payment application, interest rate adjustments, assessment of fees, loss mitigation, use of credit reports, handling of unclaimed property, safeguarding of non-public personally identifiable information about our customers, and the ability of our employees to work remotely. These complex requirements can and do change as laws and regulations are enacted, promulgated, amended, interpreted and enforced, and the requirements applicable to our business have been changing especially rapidly in response to the COVID-19 pandemic, as discussed below.

In recent years, the general trend among federal, state and local legislative bodies and regulatory agencies as well as state attorneys general has been toward increasing laws, regulations, investigative proceedings and enforcement actions with regard to residential mortgage lenders and servicers. The CFPB continues to take a very active role in the mortgage industry, and its rule-making and regulatory agenda relating to loan servicing and origination continues to evolve. Individual states have also been active, as have other regulatory organizations such as the Multistate Mortgage Committee (MMC), a multistate coalition of various mortgage banking regulators. In addition to their traditional focus on licensing and examination matters, certain regulators make observations, recommendations or demands with respect to areas such as corporate governance, safety and soundness and risk and compliance management.

The CFPB and state regulators have also focused on the use and adequacy of technology in the mortgage servicing industry, privacy concerns and other topical issues, such as likely discontinuation of the London Interbank Offered Rate (LIBOR), communications from debt collectors, and the ability of borrowers to repay mortgage loans. Further, in 2020 we became subject to additional regulations and requirements as the GSEs, Ginnie Mae, the United States Treasury Department and state regulators responded to the COVID-19 pandemic. In March 2020, the CARES Act was signed into law, allowing borrowers affected by COVID-19 to request temporary loan forbearance for federally backed mortgage loans. In addition, multiple forbearance programs, moratoria of foreclosure and eviction and other requirements to assist borrowers enduring financial hardship due to COVID-19 were implemented by states, agencies and regulators. Further, the CFPB promulgated certain amendments to RESPA (Regulation X) that became effective on August 31, 2021 and that impose certain additional COVID-19-related requirements with respect to loss mitigation, early intervention call requirements, and initiating new

foreclosures. The CFPB moratorium on new foreclosures sunset on January 1, 2022, although some states continue to impose certain foreclosure moratoria, including in connection with their respective Homeowner Assistance Fund programs.

Our licensed entities are required to renew their licenses, typically on an annual basis, and to do so they must satisfy the license renewal requirements of each jurisdiction, which generally include financial requirements such as providing audited financial statements or satisfying minimum net worth requirements and non-financial requirements such as satisfactorily completing examinations as to the licensee’s compliance with applicable laws and regulations. The minimum net worth requirements to which our licensed entities are subject are unique to each state and type of license. See Item 1A. Risk Factors – Legal and Regulatory Risks for further information.

In recent years, we have been subject to significant state and federal regulatory actions against us, including the following:

•We are currently in litigation with the CFPB after the CFPB filed a lawsuit in the federal district court for the Southern District of Florida against Ocwen, Ocwen Mortgage Servicing, Inc. (OMS) and Ocwen Loan Servicing, LLC (OLS) alleging violations of federal consumer financial laws relating to our servicing business. In April 2021, following the filing of motions by the parties and a number of procedural developments, the court entered final judgment in our favor and closed the case. The CFPB thereafter filed a notice of appeal. Appellate briefing concluded August 26, 2021, and oral argument before the Eleventh Circuit occurred on February 10, 2022. We expect the CFPB to resume its supervision activities of Ocwen upon conclusion of this matter.

•In recent years we have settled state regulatory actions against us by 29 states and the District of Columbia and a lawsuit brought by the Florida Attorney General and the State of Florida Office of Financial Regulation after these states and the District of Columbia alleged deficiencies in our compliance with laws and regulations relating to our servicing and lending activities. We have also entered into regulatory settlements with the NY DFS and the California Department of Financial Protection and Innovation (CA DFPI) relating to our servicing practices and other aspects of our business, and we have entered into a settlement agreement with the MMC and consent orders with certain state attorneys general to resolve and close out findings of an MMC examination of PMC’s legacy mortgage servicing practices.

We have incurred significant costs to comply with the terms of the settlements into which we have entered. In addition, the restrictions imposed under these settlements have impacted how we run our business.

We continue to be subject to a number of ongoing federal and state regulatory examinations, consent orders, inquiries, subpoenas, civil investigative demands, requests for information and other actions, which could result in adverse regulatory action against us. See Item 1A. Risk Factors – Legal and Regulatory Risks for further information.

Finally, there are a number of foreign laws and regulations that are applicable to our operations outside of the U.S., including laws and regulations that govern licensing, privacy, employment, safety, payroll and other taxes and insurance and laws and regulations that govern the creation, continuation and the winding up of companies as well as the relationships between shareholders, our corporate entities, the public and the government in these countries.

COMPETITION

The financial services markets in which we operate are highly competitive and fragmented, and we expect them to remain so. We compete with large and small financial services companies, including bank and non-bank entities, in the servicing, lending and MSR transaction markets. Our competitors include large and regional banks, large non-bank servicers and mortgage originators, and real estate investment trusts. In both our servicing and originations business, new competitors continue to emerge, including companies that developed new technology around customer interactions and process automation.

In our Servicing business, we compete based on price, operating performance, service quality and customer and client satisfaction. Potential counterparties also (1) assess our regulatory compliance track record and examine our systems and processes for maintaining and demonstrating regulatory compliance, (2) consider our customer satisfaction rankings, and (3) consider our third-party servicer ratings. Certain of our competitors, especially large banks, may have substantially lower costs of capital and greater financial resources, which makes it challenging to compete. We believe that our competitive strengths flow from our ability to control and drive down delinquencies using proprietary processes, our superior operating performance, our lower cost to service non-performing loans and our deep know-how as a long-time operator of servicing loans. During 2021, PMC was recognized by the GSEs for the quality of its servicing performance. Freddie Mac awarded PMC the Gold Sharp Award for Top Tier Servicing Group. PMC was one of only two mortgage servicers to be recognized by Fannie Mae in 2021 in all three categories of the Servicer Total Achievement Rewards (STAR) Program. Notwithstanding these strengths, we have suffered reputational damage as a result of previous regulatory settlements and the associated scrutiny of our business. We believe this has weakened our competitive position against both our bank and non-bank servicing competitors.

In our Originations business, we face intense competition in most areas, including rates, margin, fees, customer service and name recognition. Some of our competitors, including the larger banks, have substantially lower costs of capital and strong

retail presence, which makes it challenging to compete. We believe that we will continue to face increased competitive pressures in the future as the refinance opportunities contract with rising interest rates. We also believe our competitive strengths flow from our existing customer relationships and from our focus on providing strong customer service.

The forward and reverse lending markets face many of the same competitive pressures. However, the reverse market is significantly smaller than the forward market with a higher market share concentration among the top five Ginnie Mae HMBS issuers. These higher concentration levels can, at times, lead to significant price competition. We believe the competitive advantage of our Liberty Reverse Mortgage business flows from our focus on customer experience and service levels, our significant experience and name recognition, our strategic partnerships and our use of technology to produce higher levels of productivity to drive down per-loan costs.

THIRD-PARTY SERVICER RATINGS

Like other servicers, we are the subject of mortgage servicer ratings or rankings (collectively, ratings) issued and revised from time to time by rating agencies including Moody’s Investors Service, Inc. (Moody’s), S&P Global Ratings, Inc. (S&P) and Fitch Ratings, Inc. (Fitch). Favorable ratings from these agencies are important to the conduct of our loan servicing and lending businesses.

The following table summarizes our key servicer ratings:

| | | | | | | | | | | | | | | | | |

| PHH Mortgage Corporation (PMC) |

| | Moody’s | | S&P | | Fitch |

| Residential Prime Servicer | SQ3 | | Average | | RPS3 |

| Residential Subprime Servicer | SQ3 | | Average | | RPS3 |

| Residential Special Servicer | SQ3 | | Average | | RSS3 |

| Residential Second/Subordinate Lien Servicer | SQ3 | | Average | | RPS3 |

| Residential Home Equity Servicer | — | | — | | RPS3 |

| Residential Alt-A Servicer | — | | — | | RPS3 |

| Master Servicer | SQ3+ | | Above Average | | RMS3 |

| Ratings Outlook | N/A | | Stable | | Stable |

| | | | | |

| Date of last action | September 28, 2021 | | June 29, 2021 | | April 28, 2021 |

In addition to servicer ratings, each of the agencies will from time to time assign an outlook (or a ratings watch such as Moody’s review status) to the rating status of a mortgage servicer. A negative outlook is generally used to indicate that a rating “may be lowered,” while a positive outlook is generally used to indicate a rating “may be raised.” On September 28, 2021, Moody’s upgraded the servicer quality (SQ) assessment for PMC as a master servicer of residential mortgage loans from SQ3 to SQ3+, reflecting solid reporting and remitting processes and proactive servicer oversight. On June 29, 2021, S&P affirmed PMC’s servicer rating as Average, raising management and organization ranking to Above Average. In addition, S&P raised PMC’s master servicer rating from Average to Above Average reflecting the industry experience of PMC’s management, multiple levels of internal controls to monitor operations, and resolution of regulatory actions, among other factors mentioned by S&P. On March 24, 2020, Fitch placed all U.S RMBS servicer ratings on Negative outlook resulting from a rapidly evolving economic and operating environment due to the sudden impact of the COVID-19 virus.

On April 28, 2021, Fitch affirmed PMC’s servicer ratings and revised its outlook from Negative to Stable as PMC’s performance in this evolving environment has not raised any elevated concerns. According to Fitch, the affirmation and stable outlook reflected PMC’s diligent response to the coronavirus pandemic and its impact on servicing operations, effective enterprise-wide risk environment and compliance management framework, satisfactory loan servicing performance metrics, special servicing expertise, and efficient servicing technology. The ratings also consider the financial condition of PMC’s parent, Ocwen Financial Corporation.

See Item 1A. Risk Factors - Risks Relating to Our Business for further discussion of the adverse effects that a failure to maintain minimum servicer ratings could have on our business, financing activities, financial condition or results of operations.

In addition to the above servicer ratings, PMC was recognized by the GSEs for the quality of its servicing performance in 2021. Freddie Mac awarded PMC the Gold Sharp Award for Top Tier Servicing Group. PMC was one of only two mortgage servicers to be recognized by Fannie Mae in 2021 in all three categories of the STAR Program.

NEW RESIDENTIAL INVESTMENT CORP. RELATIONSHIP

Ocwen has a legacy relationship with NRZ and we acquired PMC’s legacy relationship with NRZ when we acquired PHH in October 2018. As a result, we service loans on behalf of NRZ under various agreements, including traditional subservicing agreements, where NRZ is the legal owner of the MSRs, and in connection with Rights to MSRs, where Ocwen retains legal title to the underlying MSRs but NRZ has generally assumed risks and rewards consistent with an MSR owner. See Note 8 — MSR Transfers Not Qualifying for Sale Accounting.

NRZ is our largest servicing client, accounting for $55.8 billion of UPB or 21% of the UPB of our total servicing portfolio as of December 31, 2021, approximately 66% of all delinquent loans that Ocwen serviced, and approximately 19% of our total servicing and subservicing fees in 2021, net of servicing fees remitted to NRZ (excluding ancillary income). On February 20, 2020, we received a notice of termination from NRZ with respect to the legacy PMC subservicing agreement. We continued to service these loans until deboarding on October 1, 2020. A total of 270,218 loans were deboarded representing $34.2 billion of UPB.

In addition to a base servicing fee, we receive ancillary income, which primarily includes late fees, loan modification fees and Speedpay® fees. We may also receive certain incentive fees or pay penalties tied to various contractual performance metrics. NRZ receives all float earnings and deferred servicing fees related to delinquent borrower payments, as well as certain REO-related income, including REO referral commissions. As legal MSR owner, or in compliance with the Rights to MSRs agreements, NRZ is responsible for financing all servicing advance obligations in connection with the loans underlying the MSRs.

The legacy Ocwen agreements with NRZ have an initial term ending in July 2022. The underlying loans are almost exclusively non-Agency loans, involving a higher level of operational and regulatory risk, and requiring substantial direct and oversight staffing relative to Agency loans. NRZ may terminate the agreements for convenience, subject to Ocwen’s right to receive a termination fee and 180 days’ notice at any time during the initial term. As of the date this Annual Report on Form 10-K is filed with the SEC, we have not received any such notice of termination. After the initial term, these agreements can be renewed for three-month terms at NRZ’s option by providing proper notice.

In the ordinary course and as we approach the end of the initial term in July 2022, we share information with NRZ and discuss various aspects of our relationship. With respect to the Rights to MSRs, our existing agreements provide that the Rights to MSRs could (i) remain in the existing Rights to MSR structure, (ii) be acquired by Ocwen or (iii) be sold or transferred to a third party together with Ocwen’s title to the related MSRs. In addition, the Rights to MSRs could be transferred to NRZ under the Transfer Agreement and become subserviced by PMC. The agreements may not be renewed by NRZ in July 2022 or at the end of any three-month renewal term after July 2022. In our business planning efforts, we have assessed the potential impact of such actions by NRZ in light of the current and predicted future economics of the NRZ relationship generally. Because of the large percentage of our servicing business that is represented by agreements with NRZ, if NRZ exercised all or a significant portion of these termination rights, we would need to rapidly scale our servicing business.

ALTISOURCE VENDOR RELATIONSHIP

Ocwen is a party to a number of long-term agreements with Altisource S.à r.l., and certain of other subsidiaries of Altisource Portfolio Solutions, S.A. (Altisource), including a Services Agreement, under which Altisource provides various services, such as property valuation services, property preservation and inspection services, title services and real estate sales related services, among other things. Certain services provided by Altisource under the Services agreements are charged to the borrower and/or mortgage loan investor. Accordingly, such services, while derived from our loan servicing portfolio, are not reported as expenses by Ocwen.

In May 2021, Ocwen and Altisource signed a Binding Term Sheet under which the parties agreed to extend the term of the Services Agreement through August 2030. In addition, the parties agreed to fully release each other from liability with respect to any and all claims related to Ocwen’s transfer of service referrals and services to providers other than Altisource.

Based on public filings, we believe one of our shareholders holding more than 5% of our common stock has a direct or indirect material interest in Altisource.

OAKTREE RELATIONSHIP

We established a strategic alliance with Oaktree in 2020 to support refinancing our corporate debt and help advance our growth initiatives. The Oaktree relationship includes the launch of an MSR investment vehicle to scale up our servicing business in a capital efficient manner and investments in our debt and equity.

On December 21, 2020, we entered into the Transaction Agreement with Oaktree to form a joint venture for the purpose of investing in GSE MSRs subserviced by PMC. Effective with the closing of the transaction on May 3, 2021, Oaktree and Ocwen hold 85% and 15% interests in MAV Canopy, and agreed to invest equity up to $250.0 million over three years. As of December 31, 2021, the total members’ capital contributions to MAV Canopy amounted to $131.2 million, net of distributions,

or approximately 52% of capacity. We are currently discussing with Oaktree a potential upsize of the capital commitment to MAV.

Pursuant to an agreement with Oaktree executed on February 2021, we issued to Oaktree in a private placement $285.0 million of Ocwen senior secured notes in two separate tranches. The initial tranche of $199.5 million senior secured notes was completed on March 4, 2021 and the additional $85.5 million tranche was completed following the launch of the MSR joint venture on May 3, 2021. In addition:

•On March 4, 2021, we issued 1,184,768 warrants to Oaktree to purchase shares of our common stock equal to 12% of our then outstanding common stock at an exercise price of $26.82 per share, subject to anti-dilution adjustments.

•On May 3, 2021, we issued 261,248 warrants to Oaktree to purchase additional common stock equal to 3% of our then outstanding common stock at an exercise price of $24.31 per share, subject to anti-dilution adjustments.

•On May 3, 2021, we issued to Oaktree 426,705 shares, or 4.9% of our fully diluted outstanding common stock, or at a purchase price of $23.15 per share.

The net proceeds before expenses from the issuance to Oaktree of the initial tranche of senior secured notes and the warrants was $175.0 million (after $24.5 million of original issue discount) and was used, together with the proceeds from the additional debt financing, to repay in full an aggregate of $498 million of existing indebtedness, including Ocwen’s $185.0 million Senior Secured Term Loan, $21.5 million 6.375% senior unsecured notes due 2021 and $291.5 million 8.375% senior secured second lien notes due 2022. The net proceeds before expenses from the issuance to Oaktree of the additional tranche of senior secured notes and the warrants was approximately $75.0 million (after $10.5 million of original issue discount) and was used to fund our investment in the MSR joint venture and for general corporate purposes, including to accelerate the growth of our Originations and Servicing businesses.

In 2021 as part of the launch of the MSR joint venture, PMC entered into a number of definitive agreements with MAV, the licensed mortgage subsidiary of MAV Canopy which govern the terms of their business relationship, including a Subservicing Agreement, Joint Marketing Agreement and Recapture Agreement, and Administrative Services Agreement.

PMC has exclusive rights to subservice the MSR owned by MAV and is compensated with subservicing fees in accordance with the Subservicing Agreement. The Subservicing Agreement will continue until terminated by mutual agreement of the parties or for cause, as defined. We are currently discussing with MAV certain amendments to the terms and conditions of the Subservicing Agreement and related agreements.

PMC entered into the following MSR sale transactions with MAV pursuant to certain MSR purchase and sale agreements in 2021:

•Sales of MSR portfolios to MAV in bulk transactions;

•Flow sales to MAV of certain MSRs PMC purchased from a GSE Cash Window program; and

•Flow sales to MAV of MSRs PMC recaptured from borrowers that were previously serviced on behalf of MAV. Under the Recapture Agreement, PMC sells the originated MSR for nil proceeds but retains the realized gain on loan sales.

These transactions accelerated the launch of MAV. At December 31, 2021, MAV’s servicing portfolio comprised $8.9 billion of MSRs acquired from unrelated third parties and $24.0 billion MSRs acquired from PMC.

These MSR sale transactions between PMC and MAV did not achieve sale accounting criteria due to the Subservicing Agreement termination restrictions. Although the servicer compensation is the same under the Subservicing Agreement, our financial statements reflect two distinct portfolios, depending on whether the MSRs were previously sold by PMC to MAV. PMC recognizes subservicing revenue from those MSRs MAV acquired from third parties. PMC recognizes servicing revenue together with MSR pledged liability expense for servicing fees PMC collects and remits to MAV as it relates to those MSRs sold by PMC to MAV.

See Note 11 — Investment in Equity Method Investee, Note 14 — Borrowings, and Note 16 — Stockholders’ Equity to the Consolidated Financial Statements for additional information.

USVI OPERATIONS

The majority of our USVI operations and assets were transferred to the U.S. during 2019 as a result of our legal entity simplification. Our current USVI operations mostly supports our Servicing segment, including a servicing call center for customer service and home retention.

In 2012, Ocwen formed OMS under the laws of the USVI in a federally recognized economic development zone where qualified entities are eligible for certain tax benefits granted by the USVI Economic Development Commission (“EDC Benefits”). We were approved as a Category IIA service business, and are therefore entitled to receive significant benefits that may have a favorable impact on our effective tax rate. We conducted a substantial portion of our servicing business through

OLS, a wholly-owned subsidiary of OMS. Although we are eligible for a reduced tax rate in the USVI, the reduced tax rate has not provided Ocwen with a foreign tax benefit in recent tax years as we have been incurring taxable losses in the USVI.

During 2019, OLS merged into PMC. As a result of this reorganization, the majority of our USVI operations and assets were transferred to the U.S. We continue to maintain some operations in the USVI. However, it is possible that we may not be able to retain our qualifications for the EDC Benefits, or that our past and future EDC Benefits could be adversely impacted by our reorganization, or that changes in U.S. federal, state, local, territorial or USVI taxation statutes or applicable regulations may cause a reduction in or an elimination of the value of the EDC Benefits, all of which could result in an increase to our tax expense, including a loss of anticipated income tax refunds, and, therefore, adversely affect our financial condition and results of operations.

HUMAN CAPITAL RESOURCES

We believe the success of our organization is highly dependent on the quality and engagement of our human capital resources. Our workforce is dedicated to creating positive outcomes for homeowners, communities and investors through caring service and innovative solutions. We strive to develop a working environment and culture that fosters our company values:

•Integrity: Do What’s Right – Always

•Service Excellence: Consistently Delivering on Our Commitments

•People: Develop, Grow and Value All Employees

•Teamwork: Succeed Together as a Global Team

•Embracing Change: Value Innovation and New Thinking

We had a total of approximately 5,700 employees at December 31, 2021. Approximately 2,000 of our employees were employed in the U.S. and USVI, and approximately 3,700 of our employees were employed in our operations in India and the Philippines. Of our foreign-based employees, approximately 66% were engaged in our Servicing operations. Ocwen currently operates through a secure remote workforce model for approximately 95% of its global workforce due to the COVID-19 pandemic.

Our Board of Directors and executive leadership team places significant focus on our human capital resources through fostering and measuring employee engagement, committing to comprehensive Diversity, Equity, and Inclusion initiatives, and engaging with both internal and external groups and organizations to ensure that our culture enables employees to consistently demonstrate our company values. Important attributes of our human capital strategy include:

Diversity, Equity and Inclusion (DE&I). We are committed to be a globally diverse and inclusive workplace where every voice is heard. Diversity, inclusiveness and respect are integral parts of our culture and work environment. DE&I training for all employees and unconscious bias training for leaders are mandatory parts of our learning programs to increase awareness, and employees at all levels are annually evaluated on sustaining an inclusive work environment. The pillars of our diversity program are:

•Leadership: Embrace and foster a culture of inclusion throughout Ocwen and be held accountable for achieving diversity and inclusion goals and objectives.

•Workforce: Attract, develop, retain and advance the best and brightest from all walks of life and backgrounds at all levels of the organization.

•Vendor Diversity: Achieve a range of suppliers, vendors and service providers who align with our diversity and inclusion strategies.

•Community Engagement: Ensure that Ocwen has a significant presence in and supports a core group of diverse, community-based organizations and philanthropies.

As of December 31, 2021, 48% of our employees globally are women, and 33% of our U.S. leadership roles (Director and above) are filled by women. 62% of our U.S. employees are women and 45% are people of color. Our affinity groups like the Ocwen Global Women’s Network (OGWN), LEAP Black professionals network, FREE affinity group for LGBTQ+ employees and mentoring programs, when coupled with a culture of appreciation, help provide a comprehensive ecosystem for diversity to flourish.

Ocwen sponsors several organizations focused on under-represented groups, including the American Mortgage Diversity Council and the National Association of Minority Mortgage Bankers of America. We are also committed to hiring graduates from historically Black colleges and universities through the HomeFree-USA Center for Financial Advancement program.

Talent Development. We continue to foster an environment in which every team member has the opportunity to grow and achieve his or her professional goals, with support and encouragement. We regularly measure employee engagement – our employees’ pride, energy and optimism that fuels their effort – and implement action plans that respond to employee feedback. Our most recent employee survey indicated 84% favorable engagement levels. Our training platform focuses not only on the technical domain skills essential to role success, but includes competency-based programs to develop leadership capabilities

and skills needed for the future. In 2021, our voluntary turnover was 16.8%. Succession planning occurs annually and is reviewed by the CEO and the Compensation and Human Capital Committee. Strategic talent reviews to identify, develop and promote top talent are part of our performance management processes. The Aspire mentoring program provides aspiring women leaders at mid-level with a platform to build skill, knowledge and expertise while achieving professional development goals through focused guidance and insight from a network of mentors.

Rewards. Our total rewards (compensation and benefits) programs are developed to attract, motivate and retain employees. They demonstrate the value the employee provides to the organization, are designed to be competitive to the marketplace, and connect directly to key business strategies. Our compensation programs, including salaries and short- and long-term incentives, are centered on our pay-for-performance philosophy, aligning the interests of employees and stakeholders by rewarding both individual and overall company performance. Ocwen’s health and welfare benefit programs strive to keep employees productive and engaged at work by serving the total well-being of employees and their families. We are committed to and regularly evaluate our practices to ensure pay is fair and equitable, and competitive to the marketplace.

Environmental, Social and Corporate Governance (ESG) Practices and Corporate Sustainability

Our Board of Directors and our management are committed to ensuring Ocwen has responsible practices to address the needs of its customers, employees and the communities it serves. Our comprehensive approach to ESG and corporate sustainability is detailed in our report “Environmental, Social and Corporate Governance (ESG) and Corporate Sustainability” on our website at www.ocwen.com in the “Shareholders” section under “Corporate Governance.” Our approach is represented by the following policies and programs:

Policy on non-discrimination. Ocwen’s non-discrimination policy provides equal employment opportunities for all qualified individuals without discrimination based upon the following legally protected characteristics: race, religious creed, color, national origin, ancestry, physical or mental disability, medical condition, genetic information, marital status (including registered domestic partnership status), sex (including pregnancy, childbirth, lactation and related medical conditions), gender (including gender identity and expression), age (40 and over), sexual orientation, Civil Air Patrol status, military and veteran status and any other consideration protected by federal, state or local law (collectively referred to as “protected characteristics”). Underlying this policy is Ocwen’s culture and values, including employees’ rights to be free from unlawful discrimination, and its commitment to providing a safe, secure and productive work environment.

Ocwen’s hiring, salary administration, promotion and transfer policies are based solely on job requirements, job performance and job-related criteria. In addition, every effort is made to ensure that Ocwen’s personnel policies and practices (including those relating to compensation, benefits, transfer, retention, termination, training and self-development opportunities, as well as social and recreational programs) are administered without discrimination on the basis of any legally protected characteristic.

Promoting equal opportunity and diversity. Ocwen is committed to providing equal opportunity in all areas of employment, compensation, training and promotion. Company policies prohibit discrimination of any form in all of the locations in which Ocwen operates. Ocwen strives to foster an environment in which all stakeholders can participate and contribute to the success of the organization’s enterprise, taking full advantage of the collective sum of individual differences, life experiences, inventiveness, self-expression and unique capabilities, knowledge and talent. Our Diversity, Equity and Inclusion Council meets quarterly to review progress related to the Ocwen’s Diversity, Equity and Inclusion Roadmap. Diversity, Equity and Inclusion updates are provided to the Executive Leadership Team on a monthly basis and to the Board of Directors as necessary. Ocwen’s Global Diversity, Equity and Inclusion Policy is reviewed on an annual basis and diversity training is mandatory for all employees globally. Additionally, all leaders are required to complete a training course on Unconscious Bias, and Diversity and Inclusion goals are incorporated into annual performance evaluations for all managers.

In 2017, Ocwen formed the Ocwen Global Women’s Network (OGWN), an affinity group whose mission is to support recruitment, development and retention initiatives for women across the organization. This affinity group serves as a sounding board for business insights, and supports the attainment of company goals in diversity, inclusion and talent development. Integrating Diversity, Equity and Inclusion into Ocwen’s culture is critical for our success and allows us to make the most of the full range of our talent. More than 2,300 employees are OGWN members. In 2021, Ocwen launched two new affinity groups, LEAP and FREE, that respectively foster a safe place, promote belonging and drive inclusion for Black and LGBTQ+ employees. LEAP stands for Leading with Education Action and Purpose and its mission is to educate Ocwen employees globally about Black culture and the Black experience to increase inclusion across the organization. LEAP also enhances the professional development of Black employees through formal and informal mentoring, networking, learning opportunities and leadership development. The mission of FREE, which stands for Freedom, Respect, Expression and Equality, is to create a safe, inclusive and affirming office climate that fosters professional and personal growth for employees of all genders and sexualities through education, advocacy, outreach and support. FREE promotes a fully equitable environment that is free of judgment and strives for knowledge, challenges barriers, and seeks to help and empower LGBTQ+ employees.

Ocwen tracks and monitors representation of women and people of color across the organization. As of December 31, 2021, 48% of our global workforce is made up of women. In the U.S., women make up 62% of our workforce and 33% of our leadership team at the Director level and above. Additionally, in the U.S., people of color make up 45% of our workforce and 18% of our leadership team at the Director level and above. We also take action to support the recruitment, development and retention of our diverse talent. These programs include requiring diverse candidates as part of our hiring process, tracking minority hiring, promotion, retention and representation at all levels, and assessing diverse talent as part of our succession planning.

Ocwen sponsors several organizations focused on under-represented groups, including the American Mortgage Diversity Council, Florida Association of Women Lawyers and the National Association of Minority Mortgage Bankers of America. We are also committed to hiring graduates from historically black colleges and universities through the HomeFree-USA Center for Financial Advancement program.

Pay equity is an important component of Ocwen’s employment value proposition, commitment to DE&I and legal and regulatory compliance. We regularly evaluate our performance management, merit increase incentive award and promotion processes for race and gender equality, and remediate any identified compensation gaps.

Commitment to Ethics. We have adopted a robust Code of Business Conduct and Ethics that applies to all employees and our Board of Directors, as well as an additional Code of Ethics for Senior Financial Officers that applies to our Chief Executive Officer, Chief Financial Officer, and Chief Accounting Officer. We provide multiple anonymous methods for any employee or other person to report a suspected ethical violation, including whistleblower complaints relating to accounting, internal controls, audit matters or securities law, and our policies prohibit retaliation against any person for making a good faith complaint. We also provide methods for interested individuals to contact the members of our Board of Directors and communicate directly with the Chair of our Audit Committee. Our General Counsel serves as our Chief Ethics Officer and works with members of our Internal Audit function to ensure every ethics complaint and communication to our Board is addressed in accordance with our company policies.

Dependent care and special leave. Ocwen’s benefits programs strive to keep employees productive and engaged at work by serving the total well-being of employees’ and their families’ physical, mental and financial health. Our comprehensive benefits plan includes company-sponsored medical, dental and vision; company-paid basic life, accident and disability coverage; 401(k) with company match; and supplemental group coverage for critical illness, accident, auto, home, pet, legal, identity protection, childcare/eldercare and tutoring. The medical plans include 100% coverage for all preventive care services and all generic preventive medications.

Our wellness programs offer incentives for completing preventive health screenings, participating in online and telephonic health coaching, improving or reaching targeted health scores, and increasing physical activity. Additionally, we provide employees with a comprehensive employee assistance program that includes virtual counseling, personalized health coaching for chronic conditions, diabetes and ergonomics, stress management and financial planning workshops, online guided meditation and yoga, and more. Ocwen also provides a generous paid time off (PTO) program to support employees’ need to rest and recharge. Our medical and family leave programs offer paid disability absences and paid parental/adoption leave, in addition to FMLA-required schedule flexibility and job security.

Training and development. Ocwen is committed to providing our employees with high quality training and learning experiences targeted to increase industry knowledge levels, improve process efficiency and promote personal growth, which in turn helps improve customer experience, reduce foreclosures and contribute to our success as an organization. Ocwen facilitates professional development through the lifecycle of employees through functional business training, regulatory and compliance training, and skill and competency development programs. We also provide individualized one-on-one coaching to help customer-facing staff guide customers to positive experiences. In addition to learning programs designed to build functional and leadership competency for all levels of leadership throughout the organization, Ocwen offers a Leadership Development Training curriculum specifically designed to prepare employees at the Supervisor level and above with the competencies to make them successful in their roles as leaders. Training courses are housed in our continuously reviewed and updated learning management system.

Community development. At Ocwen, we believe homeownership is an important part of achieving financial independence, and our philosophy in this regard is “helping homeowners is what we do.” This philosophy is what guides us in our commitment to the communities we serve. We organize a variety of community outreach programs and events with local and national organizations around the country to assist homeowners, particularly in communities of color. Our outreach events began during the 2008 mortgage crisis and have continued since then. At the onset of the pandemic in 2020, Ocwen shifted to a virtual borrower outreach model to assist struggling homeowners. We continued this model throughout 2021 and, in partnership with the NAACP, we hosted 52 virtual borrower outreach events across the country. In recognition of our efforts, Ocwen was named the 2021 External Partner of the Year by Neighborhood Housing Services of New York City for our focus on helping New York homeowners stay in their homes.

To better serve our communities, Ocwen created a Community Advisory Council in 2014, consisting of 15 leaders from a diverse group of national non-profit organizations, consumer advocacy groups and civil rights organizations, as a platform to collaborate and share ideas on how to help homeowners. Ocwen provides grants and sponsorship funding to a number of local and national nonprofit organizations each year, in support of the work they do to help distressed communities and homeowners. Since 2012, Ocwen has contributed over $25 million to these organizations.

Charitable activity. Ocwen continues to find meaningful ways to give back to the communities where we live and work. The charitable events at our office locations around the globe included distributing meals and supporting local food banks, helping economically disadvantaged children and at-risk youth, helping schools for hearing-impaired children, holding toy drives and back-to-school supply drives, helping the homeless, supporting victims of crimes, providing financial assistance to families impacted by cancer, making donations to first responders, helping communities impacted by the pandemic with donations and medical equipment, hosting blood drives through the American Red Cross and making donations to the Mortgage Bankers Association’s (MBA) Opens Doors Foundation to help families with a critically ill or injured child.

Responsible information security management. We believe Ocwen has a robust information security program in place to ensure the confidentiality, integrity and availability of data and information systems. Ocwen’s Board of Directors is briefed regularly on information security risks, which are managed by a combination of strong policies, appropriate tools and technologies and continuous people awareness. Ocwen’s cyber security controls utilize a layered defense-in-depth approach to thwart any attempts to compromise the integrity of the network. Our employees are provided regular training to identify, prevent and report cyber security risks and incidents. Our third-party risk management program evaluates and monitors our vendors’ information security practices, and all third-party vendors that process data on our behalf are required to maintain a documented information security program that meets our stringent security requirements. Ocwen’s cyber security preparedness is tested on a regular basis through a variety of assessments, including internal and external vulnerability assessments, penetration tests, incident response table top tests, breach readiness and response tests, among others.

Environmental Impact. Ocwen is committed to operating through a primarily remote working model for a significant majority of our workforce that requires only a small percentage of employees to commute to work on a daily basis. We expect this remote model will allow Ocwen to use significantly fewer natural resources in our facilities and generate fewer employee commute-related carbon emissions than a comparatively-sized business that does not operate remotely. We recycle office supplies at all U.S. facilities, and are in the process of converting our facilities to LED lighting. We have also implemented a digital mailroom process reducing the need for envelopes and shipping of documents between locations. In 2021, working with customers, we replaced over 3 million paper mailings through electronic notice delivery and process automations, reducing our carbon footprint by an average of 20-29 g of CO2 per mailing.

AVAILABLE INFORMATION

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports are made available free of charge through our website (www.ocwen.com) as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers, including Ocwen, that file electronically with the SEC. The address of that site is www.sec.gov. We have also posted on our website, and have available in print upon request (1) the charters for our Audit Committee, Compensation and Human Capital Committee, Nomination/Governance Committee and Risk and Compliance Committee, (2) our Corporate Governance Guidelines, (3) our Code of Business Conduct and Ethics and (4) our Code of Ethics for Senior Financial Officers.

ITEM 1A. RISK FACTORS