10-YEAR PERFORMANCE

Ambac Financial Group, Inc.

| 1 | Return on equity is defined as net income excluding realized gains and losses and non-recurring items, divided by average stockholders’ equity, exclusive of unrealized gains/losses in the investment portfolio. |

| 2 | Expense ratio is computed as financial guarantee underwriting and operating expenses divided by net premiums earned and other credit enhancement fees. |

10/11

FINANCIAL HIGHLIGHTS

Ambac Financial Group, Inc. and Subsidiaries

| | | | | | | | | | | | |

(Dollars in millions, except per share amounts)

| | 2003

| | | 2002

| | | 2001

| |

STATEMENT OF OPERATIONS HIGHLIGHTS | | | | | | | | | | | | |

Gross premiums written | | $ | 1,143.7 | | | $ | 904.0 | | | $ | 683.3 | |

Net premiums earned and other credit enhancement fees | | | 667.3 | | | | 500.3 | | | | 400.4 | |

Net investment income | | | 321.1 | | | | 297.3 | | | | 267.8 | |

Interest income from investment and payment agreements | | | 212.0 | | | | 255.0 | | | | 249.9 | |

Financial services - other revenue | | | 20.6 | | | | 17.4 | | | | 24.2 | |

Total revenue | | | 1,272.2 | | | | 958.6 | | | | 946.8 | |

Losses and loss expenses | | | 53.4 | | | | 26.7 | | | | 20.0 | |

Financial guarantee underwriting and operating expenses | | | 92.0 | | | | 76.5 | | | | 68.0 | |

Interest expense from investment and payment agreements | | | 196.3 | | | | 231.3 | | | | 235.4 | |

Financial services - other expenses | | | 12.1 | | | | 9.9 | | | | 8.9 | |

Interest expense | | | 54.2 | | | | 43.7 | | | | 40.4 | |

Net income | | | 618.9 | | | | 432.6 | | | | 432.9 | |

Net income per share: | | | | | | | | | | | | |

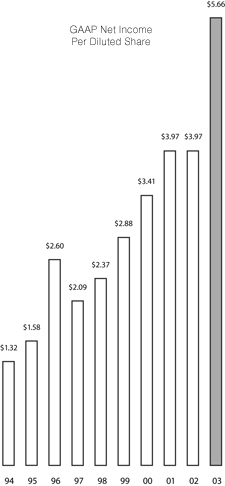

Basic | | | 5.81 | | | | 4.08 | | | | 4.10 | |

Diluted | | | 5.66 | | | | 3.97 | | | | 3.97 | |

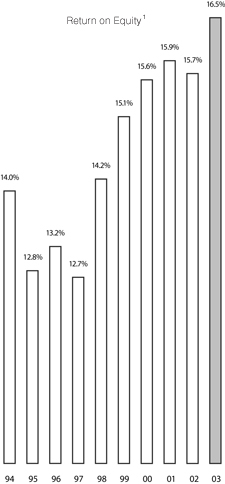

Return on equity1 | | | 15.7 | % | | | 13.1 | % | | | 15.5 | % |

Return on equity2 | | | 16.5 | % | | | 15.7 | % | | | 15.9 | % |

Cash dividends declared per common share | | | 0.420 | | | | 0.380 | | | | 0.340 | |

| | |

|

|

| |

|

|

| |

|

|

|

BALANCE SHEET HIGHLIGHTS | | | | | | | | | | | | |

Total investments, at fair value | | $ | 13,776.3 | | | $ | 12,539.3 | | | $ | 10,287.9 | |

Prepaid reinsurance | | | 325.5 | | | | 296.1 | | | | 267.7 | |

Total assets | | | 16,747.3 | | | | 15,355.5 | | | | 12,339.5 | |

Unearned premiums | | | 2,545.5 | | | | 2,128.8 | | | | 1,780.3 | |

Losses and loss expense reserve | | | 189.4 | | | | 172.1 | | | | 151.1 | |

Obligations under investment agreements, investment repurchase agreements and payment agreements | | | 7,076.4 | | | | 7,282.9 | | | | 5,511.9 | |

Debentures | | | 791.8 | | | | 616.7 | | | | 619.3 | |

Total stockholders’ equity | | | 4,254.6 | | | | 3,625.2 | | | | 2,983.7 | |

| 1 | Defined as net income divided by average stockholders’ equity. |

| 2 | Defined as net income excluding realized gains and losses and non-recurring items, divided by average stockholders’ equity, exclusive of unrealized gains/losses in the investment portfolio. |

Ambac Financial Group, Inc.

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

(Dollars in millions, except per share amounts)

| | 2000

| | | 1999

| | | 1998

| | | 1997

| | | 1996

| | | 1995

| | | 1994

| |

STATEMENT OF OPERATIONS HIGHLIGHTS | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross premiums written | | $483.1 | | | $ | 445.2 | | | $ | 361.0 | | | $ | 286.2 | | | $ | 247.2 | | | $ | 193.3 | | | $ | 189.9 | |

Net premiums earned and other credit enhancement fees | | 323.4 | | | | 268.3 | | | | 213.0 | | | | 154.0 | | | | 136.6 | | | | 111.8 | | | | 117.5 | |

Net investment income | | 241.0 | | | | 209.3 | | | | 186.2 | | | | 159.7 | | | | 144.9 | | | | 131.0 | | | | 117.1 | |

Interest income from investment and payment agreements | | 303.2 | | | | 323.2 | | | | 281.9 | | | | 200.3 | | | | 165.2 | | | | 137.4 | | | | 106.0 | |

Financial services - other revenue | | 29.7 | | | | 16.9 | | | | 20.4 | | | | 12.1 | | | | 11.2 | | | | 3.4 | | | | 2.8 | |

Total revenue | | 891.5 | | | | 821.8 | | | | 709.8 | | | | 559.0 | | | | 607.4 | | | | 409.9 | | | | 366.4 | |

Losses and loss expenses | | 15.0 | | | | 11.0 | | | | 6.0 | | | | 2.9 | | | | 3.8 | | | | 3.4 | | | | 2.6 | |

Financial guarantee underwriting and operating expenses | | 55.2 | | | | 48.8 | | | | 46.7 | | | | 40.7 | | | | 37.2 | | | | 34.5 | | | | 32.8 | |

Interest expense from investment and payment agreements | | 283.0 | | | | 299.5 | | | | 263.6 | | | | 186.7 | | | | 154.5 | | | | 127.7 | | | | 92.4 | |

Financial services - other expenses | | 12.2 | | | | 12.3 | | | | 20.3 | | | | 15.2 | | | | 8.5 | | | | 7.8 | | | | 6.1 | |

Interest expense | | 37.5 | | | | 36.5 | | | | 32.8 | | | | 21.3 | | | | 20.9 | | | | 20.9 | | | | 18.8 | |

Net income | | 366.2 | | | | 307.9 | | | | 254.0 | | | | 223.0 | | | | 276.3 | | | | 167.6 | | | | 141.1 | |

Net income per share: | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Basic | | 3.49 | | | | 2.94 | | | | 2.42 | | | | 2.12 | | | | 2.63 | | | | 1.59 | | | | 1.34 | |

Diluted | | 3.41 | | | | 2.88 | | | | 2.37 | | | | 2.09 | | | | 2.60 | | | | 1.58 | | | | 1.32 | |

Return on equity1 | | 15.9 | % | | | 15.0 | % | | | 12.8 | % | | | 12.8 | % | | | 18.3 | % | | | 13.8 | % | | | 13.2 | % |

Return on equity2 | | 15.6 | % | | | 15.1 | % | | | 14.2 | % | | | 12.7 | % | | | 13.2 | % | | | 12.8 | % | | | 14.0 | % |

Cash dividends declared per common share | | 0.307 | | | | 0.280 | | | | 0.253 | | | | 0.230 | | | | 0.205 | | | | 0.185 | | | | 0.165 | |

| | |

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

BALANCE SHEET HIGHLIGHTS | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total investments, at fair value | | $8,323.9 | | | $ | 8,962.5 | | | $ | 8,748.4 | | | $ | 6,915.1 | | | $ | 5,200.5 | | | $ | 4,441.6 | | | $ | 3,764.2 | |

Prepaid reinsurance | | 242.6 | | | | 218.0 | | | | 199.9 | | | | 183.5 | | | | 168.8 | | | | 153.4 | | | | 139.9 | |

Total assets | | 10,120.2 | | | | 11,344.6 | | | | 11,212.3 | | | | 8,291.7 | | | | 5,876.4 | | | | 5,309.3 | | | | 4,287.0 | |

Unearned premiums | | 1,546.3 | | | | 1,431.1 | | | | 1,294.2 | | | | 1,179.0 | | | | 991.2 | | | | 903.0 | | | | 836.6 | |

Losses and loss expense reserve | | 132.4 | | | | 121.0 | | | | 115.8 | | | | 103.3 | | | | 60.6 | | | | 66.0 | | | | 65.7 | |

Obligations under investment agreements, investment repurchase agreements and payment agreements | | 4,892.9 | | | | 6,140.3 | | | | 5,956.8 | | | | 4,321.0 | | | | 2,754.6 | | | | 2,426.9 | | | | 2,025.3 | |

Debentures | | 424.1 | | | | 424.0 | | | | 423.9 | | | | 223.9 | | | | 223.8 | | | | 223.7 | | | | 223.7 | |

Total stockholders’ equity | | 2,596.1 | | | | 2,018.5 | | | | 2,096.1 | | | | 1,872.5 | | | | 1,615.0 | | | | 1,404.0 | | | | 1,033.5 | |

| 1 | Defined as net income divided by average stockholders’ equity. |

| 2 | Defined as net income excluding realized gains and losses and non-recurring items, divided by average stockholders’ equity, exclusive of unrealized gains/losses in the investment portfolio. |

Ambac Financial Group, Inc.

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

OVERVIEW

Ambac Financial Group, Inc. is a holding company whose subsidiaries provide financial guarantees and financial services to clients in both the public and private sectors around the world.

Ambac’s principal operating subsidiary, Ambac Assurance Corporation, a leading provider of financial guarantees for public finance and structured finance obligations, has earned triple-A ratings, the highest ratings available from Moody’s Investors Service, Inc., Standard & Poor’s Ratings Services, Fitch Inc., and Ratings and Investment Information, Inc. Ambac Assurance provides financial guarantees for bond issues and other forms of debt financing. Financial guarantee insurance is a promise to pay scheduled interest and principal if the issuer fails to meet its obligations. A bond guaranteed by Ambac receives triple-A ratings, typically resulting in lower financing costs for the issuer and generally makes the issue more marketable, both in the primary and secondary markets.

Ambac’s Financial Services segment provides financial and investment products including investment agreements, interest rate swaps, total return swaps and funding conduits, principally to clients of the financial guarantee business, which includes municipalities and other public entities, health care organizations and asset-backed issuers. Ambac focuses on these businesses due to the complimentary nature of the products to its core financial guarantee product.

Ambac breaks out its core business product into Public Finance, Structured Finance and International Finance. Public Finance includes all U.S. municipal issuance including, for example, general obligations, lease and tax-backed obligations, health care, public utilities, transportation and higher education, as well as certain public/private backed transactions, such as stadium financings, military housing and student housing. Structured Finance covers U.S. structured finance transactions including mortgage-backed securities and other consumer asset-backed securities, commercial asset-backed securities, collateralized debt obligations, investor-owned utilities and asset-backed commercial paper conduits. International Finance covers both public finance initiatives and the structured finance markets outside of the U.S. Ambac has concentrated its international efforts in countries and regions where the capital markets are most advanced, primarily Western Europe, Australia and Japan.

Management believes that the Financial Guarantee business thrives on economic cycles. For example, a strong economic environment with a good or improving credit environment is beneficial to our financial guarantee portfolio. However, such conditions, if in place for an extended period of time, will reduce credit spreads and result in lower pricing. Conversely, in a deteriorating credit environment, credit spreads widen out and pricing for our product improves. However, if the weakening environment is prolonged, the stresses on our portfolio could result in claims payments in excess of normal expectations. Ambac’s management believes that its business is well positioned to withstand, and in fact prosper, within the normal economic and business cycles witnessed over the past several years. Further, Ambac’s Financial Guarantee business today enjoys a strong competitive position in a variety of product segments on a global scale and is well positioned for further geographic product expansion. Management believes that geographic product expansion will be driven, over the long term, by critical infrastructure needs worldwide and the expansion of global credit markets.

Ambac has stated its long-term financial goals of achieving earnings (exclusive of realized gains/losses in its investment portfolio and mark-to-market gains/losses in its credit derivatives portfolio and the impact of refundings) growth in the range of 14% to 16% and return on equity of 15%. These long-term goals will be missed from time to time, either higher or lower. Ambac’s success in achieving its long-term goals will be influenced by the economic and market environments in which we operate.

FORWARD-LOOKING STATEMENTS

Materials in this annual report may contain information that includes or is based upon forward-looking statements within the meaning of the Securities Litigation Reform Act of 1995. Forward-looking statements present Ambac’s expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts and relate to future operating or financial performance.

Any or all of Ambac’s forward-looking statements here or in other publications may turn out to be wrong and are based on current expectations and the current economic environment. Ambac’s actual results may vary materially, and there are no guarantees about the performance of Ambac’s securities. Among factors that could cause actual results to differ materially are: (1) changes in the economic, credit or interest rate environment in the United States and abroad; (2) the level of activity within the national and worldwide debt markets; (3) competitive conditions and pricing levels; (4) legislative and regulatory developments; (5) changes in tax laws; (6) the policies and actions of the United States and other governments and (7) other risks and uncertainties that have not been identified at this time. Ambac is not obligated to publicly correct or update any forward-looking statement if we later become aware that it is not likely to be achieved, except as required by law. You are advised, however, to consult any further disclosures we make on related subjects in Ambac’s reports to the Securities and Exchange Commission.

24/25

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of these financial statements requires us to make estimates and judgments that affect the reported amount of assets and liabilities, revenues and expenses and related disclosure of contingent assets and liabilities at the date of our financial statements. Actual results may differ from these estimates under different assumptions or conditions.

Critical accounting policies are defined as those that are reflective of significant judgments and uncertainties, and could potentially result in materially different results under different assumptions and conditions. Management has identified the accounting for loss and loss expenses and the valuation of financial instruments as critical accounting policies. This discussion should be read in conjunction with the consolidated financial statements and notes thereon included elsewhere in this report. Management has discussed each of these critical accounting policies and estimates with the Audit Committee of the Board of Directors.

Losses and loss expenses.Losses and loss expenses are based upon estimates of the ultimate aggregate losses inherent in the Financial Guarantee portfolio. In most instances, claim payments are forecasted in advance as a result of Ambac’s active surveillance of the insured book of business. Based upon company and industry experience, claim payments become probable and estimable once the issuer’s credit profile has migrated to certain impaired credit levels. The insured party has the right to a claim under Ambac’s financial insurance policy at the first scheduled debt service date of the defaulted obligation. The trustee for the insured obligation notifies Ambac of the payment default so that a claim payment can be made. The trustee reports payment defaults at or prior to the scheduled payment date. Subsequent claims would be paid if payment defaults continue and would be based on the scheduled interest and principal payment.

The liability for losses and loss expenses consists of case basis credit and active credit reserves. Case basis credit reserves are established for losses on guaranteed obligations that have already defaulted. These reserves are established in an amount that is sufficient to cover the present value of the anticipated defaulted debt service payments over the expected period of default and estimated expenses associated with settling the claims, less estimated recoveries under collateral and subrogation rights. As noted above, the payment pattern and ultimate costs are determinable on an individual claim basis (i.e., the scheduled debt service of the insured obligation). Ambac discounts these reserves in accordance with discount rates prescribed or permitted by state regulatory authorities. Net case basis credit reserves were $54.7 million and $49.0 million at December 31, 2003 and 2002, respectively. Consistent with industry practice, we also establish and accrue an active credit reserve, which is separate from the case basis credit reserves noted above. We believe, based on our active surveillance of the insured portfolio, along with historical defaults and related loss data and current economic factors, that additional losses are inherent in our portfolio. Current economic factors considered include estimates of current defaults and recovery values from collateral or subrogation rights. The active credit reserve is established based upon probable debt service defaults from incurred losses, as a result of credit deterioration. Reserve amounts are reasonably estimated based on management’s review of each credit. Active surveillance of the insured portfolio enables Ambac to track credit migration of insured obligations from period to period. Our Surveillance group, which is comprised of senior credit professionals, all of whom are independent from transaction execution, is responsible for extensive ongoing review of every credit to which Ambac has exposure. At least monthly, Senior Finance and Credit Management meets with Surveillance to review the status of their work. During the monthly review, Senior Management determines the adequacy of Ambac’s loss reserves and makes any necessary adjustments. Active credit reserves were $132.2 million and $118.6 million at December 31, 2003 and 2002, respectively.

Ambac’s management believes that the reserves for losses and loss expenses are adequate to cover the ultimate net cost of claims, but the reserves are necessarily based on estimates and there can be no assurance that the ultimate liability will not exceed such estimates.

Valuation of Financial Instruments.The fair market values of financial instruments held are determined by using independent market information when available and valuation models when market quotes are not available. Ambac’s financial instruments categorized as assets are mainly comprised of investments in fixed income securities and are accounted for in accordance with Statement of Financial Accounting Standards (“SFAS”) 115, “Accounting for Certain Investments in Debt and Equity Securities.” SFAS 115 requires that all debt instruments and certain equity instruments be classified in Ambac’s balance sheet according to their purpose and, depending on that classification, be carried at either cost or fair market value.

The fair values of fixed income investments are based primarily on quoted market prices received from a nationally recognized pricing service or dealer quotes. When quotes are not available, fair values are estimated based upon internal valuation models. The percentage of the investment portfolio that is based upon internal valuation models was 1% at December 31, 2003 and 2002.

Ambac Financial Group, Inc.

Ambac has a formal review process for all securities in its investment portfolio, including a review for impairment losses. Factors considered when assessing impairment include: (i) securities whose fair values have declined by 20% or more below amortized cost for a continuous period of at least six months; (ii) recent credit downgrades by rating agencies; (iii) the financial condition of the issuer; (iv) whether scheduled interest payments are past due; and (v) whether Ambac has the ability and intent to hold the security for a sufficient period of time to allow for anticipated recoveries in fair value. If we believe a decline in the value of a particular investment is temporary, we record the decline as an unrealized loss, net of tax, in Accumulated Other Comprehensive Income in stockholders’ equity on our Consolidated Balance Sheets. If we believe the decline is “other than temporary,” we write-down the carrying value of the investment and record a loss on our Consolidated Statements of Operations. Ambac’s assessment of a decline in value includes management’s current judgment of the factors noted above. If that judgment changes in the future, Ambac may ultimately record a loss after having originally concluded that the decline in value was temporary.

Ambac’s exposure to derivative instruments is created through interest rate, currency, total return and credit default swaps. These contracts are accounted for under SFAS 133 “Accounting for Derivative Instruments and Certain Hedging Activities,” as amended. When available, quotes are obtained from independent market sources. However, when quotes are not available, Ambac uses a combination of internally developed models and market driven inputs, primarily credit spreads, current yield curves and tax-exempt interest ratios. For additional information regarding the sensitivity of these instruments, see “Risk Management—Market Risk” below.

RESULTS OF OPERATIONS

The following paragraphs describe the consolidated results of operations of Ambac and its subsidiaries for 2003, 2002 and 2001, and its financial condition as of December 31, 2003 and 2002. These results are presented for Ambac’s two reportable segments: Financial Guarantee and Financial Services.

Income From Continuing Operations.Ambac’s income from continuing operations in 2003 was $628.1 million or $5.74 per diluted share, an increase of $196.2 million, compared to $431.9 million or $3.96 per diluted share in 2002. Ambac’s income before income taxes was $849.6 million in 2003, an increase of 51% from income before income taxes of $563.3 million in 2002. Of the $849.6 million of income (loss) before income taxes in 2003, $888.1 million was from Financial Guarantee, $23.0 million from Financial Services and $(61.5) million from Corporate. Corporate consists primarily of Ambac’s interest expense. That compares to income (loss) before income taxes in 2002 of $712.9 million, $(103.7) million and $(45.9) million from Financial Guarantee, Financial Services and Corporate, respectively. Financial guarantee income before income taxes increased as a result of (i) higher net premiums earned and other credit enhancement fees, (ii) higher net investment income and (iii) higher net mark-to-market gains on credit derivative contracts, partially offset by (i) a higher provision for losses and loss expenses and (ii) higher operating expenses. Financial Services increase is primarily attributable to the net realized investment losses of $134.1 million in 2002.

Ambac’s income from continuing operations in 2002 was relatively flat compared to $433.0 million and $3.97 per diluted share, in 2001. Ambac’s income before income taxes in 2002 was down 1% from income before income taxes of $568.0 million in 2001. This decrease was attributable to a decline in the Financial Services segment primarily attributable to higher net realized investment losses, partially offset by growth in the Financial Guarantee segment. Income (loss) before income taxes in 2001 consisted of $583.9 million from Financial Guarantee, $26.7 million from Financial Services and $(42.6) million from Corporate.

Net (Loss) Income From Discontinued Operations.In November 2003, Ambac announced that it had entered into an agreement to sell the operations of Cadre Financial Services, Inc. and Ambac Securities, Inc., its investment advisory and cash management business. This business had been part of the Financial Services segment. The decision to sell this business will enable Ambac to focus on its core financial guarantee business.

Included in the net loss from discontinued operations of $9.2 million for 2003, is a write-down of goodwill of $4.7 million. Excluding the goodwill write-down, the net (loss) income from discontinued operations would have been $(4.5) million, $0.7 million and $(0.1) million for 2003, 2002 and 2001, respectively.

FINANCIAL GUARANTEE

Ambac provides financial guarantees for debt obligations through its principal operating subsidiary Ambac Assurance Corporation, as well as credit protection in the form of structured credit derivatives through Ambac Credit Products LLC, a wholly-owned subsidiary of Ambac Assurance. Ambac provides these services in three principal markets: public finance, structured finance and international finance.

Public finance obligations are bonds issued by states, municipalities and other governmental or not-for-profit entities located in the United States (“Public Finance”). Bond proceeds are used to finance or refinance a broad spectrum of public purpose initiatives, including education, utility, transportation, health care and other general purpose projects. Although Ambac generally guarantees the full range of Public Finance obligations, Ambac concentrates on those deals that require more structuring skills. Certain projects, which had been financed by the local or U.S. government alone are now being financed through public-private partnerships. In these transactions, debt service on the bonds, rather than being paid solely by tax revenues or other governmental funds, are being paid from a variety of revenue sources, including revenues derived from the project itself. Examples of these deals include stadium financings, student housing and military housing.

26/27

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Structured finance obligations include the securitization of a variety of asset types such as mortgages, home equity loans, leases and pooled debt obligations originated in the United States (“Structured Finance”). Currently, the largest component of Ambac’s Structured Finance business relates to the securitization of mortgages and home equity loans. Another target area in Structured Finance is the credit enhancement of pooled debt obligations including structured credit derivatives. These transactions involve the securitization of a diverse portfolio of corporate bonds and loan obligations and asset-backed securities (the “Securitized Assets”). Ambac’s exposure to these Securitized Assets is mitigated through first loss protection. Typically, first loss protection is either in the form of over-collateralization (i.e., the principal amount of the Securitized Assets exceeds the principal amount of the structured finance obligations guaranteed by Ambac Assurance), or excess spread (i.e., interest cash flows on the Securitized Assets is in excess of the interest on the debt obligations guaranteed by Ambac Assurance), which allows the transaction to experience defaults among the Securitized Assets before a default is experienced on the structured finance obligations.

International finance obligations include public purpose infrastructure projects and asset-backed securities originated outside of the United States (“International Finance”). Ambac’s emphasis internationally has been on Western Europe, Japan and Australia. In the United Kingdom, Ambac has participated extensively in the Private Finance Initiative whereby the government has been privatizing certain activities. Ambac also participates in developing markets through certain structures such as pooled debt obligations or future flow transactions. Future flow transactions essentially securitize future revenue streams derived from operating receivables or the sale of commodities.

Gross Par Value Written.Ambac Assurance guaranteed $115.3 billion of par value bonds during 2003, a decrease of 1% from $116.4 billion in 2002. Par value written during 2002 increased 29% compared to $90.1 billion written during 2001. Par value written during 2003 comprised $44.7 billion from the guarantee of Public Finance obligations, $48.5 billion from Structured Finance obligations and $22.1 billion from International Finance obligations, versus $43.7 billion, $47.5 billion and $25.2 billion, respectively, in 2002 and $33.2 billion, $37.4 billion and $19.5 billion, respectively, in 2001. The 2003 increase in guaranteed Public Finance obligations was affected by an 8% increase in total Public Finance issuance and an increase in insured market penetration from 49% in 2002 to 50% in 2003. Ambac’s Public Finance market share was flat compared to 2002 at 21%. The increase in total issuance was largely the result of the lower interest rate environment causing an increase in both the refinancing and new money components of the market during 2003. Also contributing to the increased issuance are the budget deficits of municipalities throughout the United States. The increase in guaranteed Structured Finance obligations during 2003 resulted from a large unique structured transaction, partially offset by lower mortgage-backed and investor-owned utilities guarantees. International Finance obligations guaranteed during 2003 decreased primarily due to significantly lower pooled debt obligations, partially offset by higher transportation revenue and mortgage-backed and home equity guarantees.

The following table provides a breakdown of guaranteed net par outstanding by market sector:

| | | | | | |

(Dollars in billions)

| | 2003

| | 2002

|

Public Finance | | $ | 224.2 | | $ | 206.5 |

Structured Finance | | | 115.2 | | | 105.0 |

International Finance | | | 86.4 | | | 67.7 |

| | |

|

| |

|

|

Total net par outstanding | | $ | 425.8 | | $ | 379.2 |

| | |

|

| |

|

|

Gross Premiums Written.Ambac receives insurance premiums either upfront at policy issuance or on an installment basis over the life of the transaction. The collection method is determined at the time of policy issuance. Gross premiums written in 2003 were $1,143.7 million, an increase of 27% from $904.0 million in 2002. Up-front premiums written in 2003 were $739.0 million, an increase of 34% from $552.6 million in 2002. This increase is a result of increased business activity in all market sectors — Public, Structured and International Finance. Installment premiums written in 2003 were $404.7 million, an increase of 15% from $351.4 million in 2002. The growth in installment premiums is due to the growing book of business in the Structured and International Finance sector, partially offset by lower Public Finance installment premiums written. Gross premiums written in 2002 increased 32% from $683.3 million in 2001. This is a

Ambac Financial Group, Inc.

result of increased business activity in Public and Structured Finance, partially offset by lower International Finance premiums written. The following table sets forth the amounts of gross premiums written and related gross par written by type:

| | | | | | | | | | | | | | | | | | |

(Dollars in millions)

| | 2003

| | 2002

| | 2001

|

| | | Gross Premiums Written

| | Gross Par

Written

| | Gross

Premiums

Written

| | Gross Par

Written

| | Gross

Premiums

Written

| | Gross Par Written

|

Public Finance: | | | | | | | | | | | | | | | | | | |

Up-front | | $ | 576.7 | | $ | 41,428 | | $ | 462.1 | | $ | 39,283 | | $ | 323.7 | | $ | 30,414 |

Installment | | | 25.9 | | | 3,259 | | | 42.2 | | | 4,448 | | | 25.4 | | | 2,797 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total Public Finance | | | 602.6 | | | 44,687 | | | 504.3 | | | 43,731 | | | 349.1 | | | 33,211 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Structured Finance: | | | | | | | | | | | | | | | | | | |

Up-front | | | 81.7 | | | 5,683 | | | 57.9 | | | 3,498 | | | 40.6 | | | 3,016 |

Installment | | | 229.0 | | | 42,859 | | | 204.6 | | | 43,947 | | | 152.5 | | | 34,437 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total Structured Finance | | | 310.7 | | | 48,542 | | | 262.5 | | | 47,445 | | | 193.1 | | | 37,453 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

International Finance: | | | | | | | | | | | | | | | | | | |

Up-front | | | 80.6 | | | 3,459 | | | 32.6 | | | 1,662 | | | 76.5 | | | 2,965 |

Installment | | | 149.8 | | | 18,652 | | | 104.6 | | | 23,539 | | | 64.6 | | | 16,504 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total International Finance | | | 230.4 | | | 22,111 | | | 137.2 | | | 25,201 | | | 141.1 | | | 19,469 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total | | $ | 1,143.7 | | $ | 115,340 | | $ | 904.0 | | $ | 116,377 | | $ | 683.3 | | $ | 90,133 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total up-front | | $ | 739.0 | | $ | 50,570 | | $ | 552.6 | | $ | 44,443 | | $ | 440.8 | | $ | 36,395 |

Total installment | | | 404.7 | | | 64,770 | | | 351.4 | | | 71,934 | | | 242.5 | | | 53,738 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total | | $ | 1,143.7 | | $ | 115,340 | | $ | 904.0 | | $ | 116,377 | | $ | 683.3 | | $ | 90,133 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Adjusted Gross Premiums.Adjusted gross premiums written, which is not promulgated under GAAP, is used by management, equity analysts and investors as an indication of premium production. Adjusted gross premiums written, which Ambac reports as analytical data, is defined as gross (direct and assumed) up-front premiums written plus the present value of estimated future installment premiums written on insurance policies and structured credit derivatives issued in the period.

The following table reconciles adjusted gross premiums written to gross premiums written for the years ended 2003, 2002 and 2001:

| | | | | | | | | | | | |

(Dollars in millions)

| | 2003

| | | 2002

| | | 2001

| |

Adjusted gross premiums written | | $ | 1,488.9 | | | $ | 1,299.5 | | | $ | 974.3 | |

Present value of estimated installment premiums written on insurance policies and structured credit derivatives issued in the period | | | (749.9 | ) | | | (746.9 | ) | | | (533.5 | ) |

| | |

|

|

| |

|

|

| |

|

|

|

Gross up-front premiums written | | | 739.0 | | | | 552.6 | | | | 440.8 | |

Gross installment premiums written on insurance policies | | | 404.7 | | | | 351.4 | | | | 242.5 | |

| | |

|

|

| |

|

|

| |

|

|

|

Gross premiums written | | $ | 1,143.7 | | | $ | 904.0 | | | $ | 683.3 | |

| | |

|

|

| |

|

|

| |

|

|

|

Adjusted gross premiums written were $1,488.9 million in 2003, up 15% from $1,299.5 million in 2002. The increase was due to increased activity in all markets. Public Finance adjusted gross premiums were $669.3 million in 2003, up 21% from $552.8 million in 2002. This increase resulted from higher issuance and higher insured penetration, as discussed above under “Gross Par Value Written.” Structured Finance adjusted gross premiums were $454.8 million in 2003, up 3% from $441.2 million in 2002. International Finance adjusted gross premiums were $364.8 million in 2003, up 19% from $305.5 million in 2002. International Finance business continues to be dominated by large transactions with the top ten deals comprising $268.2 million and $149.1 million in 2003 and 2002, respectively. These deals represent 74% and 49% of total International Finance adjusted gross premiums written for 2003 and 2002, respectively. The activity in 2003 was represented by a broad spectrum of bond types, specifically transportation, utilities, and private finance initiatives in the United Kingdom. Adjusted gross premiums written in 2002 increased 33% from $974.3 million in 2001. The increase in 2002 was due to increased activity in all markets. The aggregate net present value, calculated at a 7% discount rate, of estimated future installment premiums was $1,555.6 million at December 31, 2003, up 16% from $1,342.2 million at December 31, 2002.

Ceded Premiums Written.Ambac’s reinsurance program is comprised of a surplus share treaty and facultative reinsurance. The surplus share treaty requires Ambac to cede covered transactions while retaining flexibility to cede those transactions within a predefined range. Certain types of transactions are excluded from the surplus share treaty and management may use facultative reinsurance to cede such risks. Ceded premiums written in 2003 were $138.1 million, up 22% from $113.5 million in 2002. Ceded premiums as a percentage of gross premiums written were 12.1% and 12.6% for 2003 and 2002, respectively. Ceded premiums written in 2002 were up 19% from $95.5 million in 2001, which represented ceded premiums as percentage of gross premiums written of 14.0%. The decline in ceded premiums as a percentage of gross premiums written from 2001 to 2002 were primarily due to lower ceded premiums of Public Finance transactions.

28/29

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

The reinsurance of risk does not relieve Ambac of its original liability to its policyholders. In the event that any of Ambac’s reinsurers are unable to meet their obligations under reinsurance contracts, Ambac would be liable for such defaulted amounts. To minimize exposure to significant losses from reinsurers, Ambac (i) monitors the financial condition of its reinsurers; (ii) has collateral provisions in certain reinsurance contracts and (iii) has certain termination triggers that can be exercised by Ambac in the event of a rating downgrade of a reinsurer. Ambac held letters of credit and collateral amounting to approximately $141.8 million from its reinsurers as of December 31, 2003. The following table provides ceded par outstanding by financial strength rating of Ambac’s reinsurers, on a Standard and Poor’s (“S&P”) basis:

| | | | | | |

(Dollars in billions)

| | 2003

| | 2002

|

AAA | | $ | 19.3 | | $ | 23.8 |

AA | | | 15.9 | | | 20.4 |

A | | | 7.7 | | | — |

Not rated | | | 6.7 | | | — |

| | |

|

| |

|

|

Total | | $ | 49.6 | | $ | 44.2 |

| | |

|

| |

|

|

In January 2003, S&P lowered the financial strength rating of AXA Re Finance S.A. from AAA to BBB. The ratings were subsequently withdrawn at AXA Re Finance S.A. management’s request. This downgrade was attributable to AXA Re Finance S.A.’s decision to cease writing new financial guarantee business. During 2003, S&P lowered the financial strength rating of American Re-Insurance Company from AA- to A. The downgrade was the result of the downgrade of American Re-Insurance Co.’s ultimate parent, Munich Reinsurance Company. The downgrades give Ambac the contractual right to terminate all reinsurance agreements with both AXA Re Finance S.A. and American Re-Insurance Company. Ambac is currently exploring whether or not to exercise this contractual right. When a reinsurer is downgraded, less capital credit is given to Ambac under rating agency models. The reduced capital credit has not and is not expected to have a material adverse effect on Ambac.

Net Premiums Earned and Other Credit Enhancement Fees.Net premiums earned and other credit enhancement fees during 2003 were $667.3 million, an increase of 33% from $500.3 million in 2002. This increase was primarily the result of the larger Financial Guarantee book of business, higher refundings, calls, and accelerations of previously insured obligations (collectively referred to as “refundings”) during the year and higher credit enhancement fees earned from the structured credit derivatives business.

When an issue insured by Ambac Assurance has been refunded or called, any remaining unearned premium (net of refunding credits, if any) is earned at that time. Earnings on refundings typically relate to transactions where the premium is paid up-front for the life of the policy. Refunding levels vary depending upon a number of conditions, primarily the relationship between current interest rates and interest rates on outstanding debt. Net premiums earned included $82.2 million and $52.0 million from refundings of previously insured issues during 2003 and 2002, respectively. The current low interest rate environment has prompted the relatively high level of accelerated earnings. When interest rates rise in the future, accelerated earnings should decline.

Excluding the effect of accelerated earnings related to refundings, normal net premiums earned (which is defined as net premiums earned less refundings) in 2003 were $538.2 million, an increase of 28% from $419.5 million in 2002. Normal net premiums earned for the year ended December 31, 2003, increased 18%, 30% and 43% for Public, Structured and International Finance, respectively, from the year ended December 31, 2002. Public Finance earned premium growth resulted from increased activity in that market over the year, enhanced by the continued focus on structured municipal transactions. Normal earned premium growth for Structured Finance continues to be driven by strong writings in consumer asset-backed transactions partially offset by the continued high level of pay-downs of the existing mortgage-backed book. International Finance net earned premium growth resulted from the effect of strong underwriting results in both 2003 and 2002.

Other credit enhancement fees in 2003, which is primarily comprised of fees received from the structured credit derivatives product, were $46.9 million, an increase of 63% from $28.8 million in 2002. This increase was due to rapid growth in the structured credit derivative business during the past several years.

Ambac Financial Group, Inc.

Net premiums earned and other credit enhancement fees during 2002 increased 25% from $400.4 million in 2001. This increase was primarily the result of the larger Financial Guarantee book of business, higher refundings and higher other credit enhancement fees earned from structured credit derivatives. Net premiums earned in 2001 included $38.6 million from refundings. Excluding the effect of accelerated earnings related to refundings, normal net premiums earned in 2002 increased 23% from $340.1 million in 2001. Other credit enhancement fees increased 33% from $21.7 million in 2001.

The following table provides a breakdown of net premiums earned by market sector and other credit enhancement fees:

| | | | | | | | | |

(Dollars in millions)

| | 2003

| | 2002

| | 2001

|

Public Finance | | $ | 184.4 | | $ | 156.3 | | $ | 137.2 |

Structured Finance | | | 226.9 | | | 174.7 | | | 146.3 |

International Finance | | | 126.9 | | | 88.5 | | | 56.6 |

| | |

|

| |

|

| |

|

|

Total normal premiums earned | | | 538.2 | | | 419.5 | | | 340.1 |

Refundings | | | 82.2 | | | 52.0 | | | 38.6 |

| | |

|

| |

|

| |

|

|

Total net premiums earned | | | 620.4 | | | 471.5 | | | 378.7 |

Other credit enhancement fees | | | 46.9 | | | 28.8 | | | 21.7 |

| | |

|

| |

|

| |

|

|

Total net premiums earned and other credit enhancement fees | | $ | 667.3 | | $ | 500.3 | | $ | 400.4 |

| | |

|

| |

|

| |

|

|

Net Investment Income.Net investment income in 2003 was $321.1 million, an increase of 8% from $297.3 million in 2002. The increase was attributable to: (i) the growth of the investment portfolio resulting from the growth in the Financial Guarantee book of business, partially offset by a lower reinvestment rate due to the current interest rate environment; and (ii) a capital contribution from Ambac Financial Group, Inc. to Ambac Assurance totaling approximately $75 million during the first quarter of 2003. The capital contribution is a result of Ambac Financial Group’s issuance of $175.0 million of debentures in February 2003. Investments in tax-exempt securities amounted to 72% of the total fair value of the portfolio as of December 31, 2003, versus 71% and 65% as of December 31, 2002 and December 31, 2001, respectively. The average pre-tax yield-to-maturity on the investment portfolio was 4.93% as of December 31, 2003 compared with 5.18% and 5.74% at December 31, 2002 and 2001, respectively. Net investment income in 2002 increased 11% from $267.8 million in 2001. This increase was primarily attributable to the growth of the investment portfolio resulting from the growth in the Financial Guarantee book of business, partially offset by a lower reinvestment rate due to the interest rate environment, and a capital contribution from Ambac Financial Group, Inc. to Ambac Assurance totaling approximately $176 million during the fourth quarter 2001. The contribution was in the form of taxable investment securities.

Net Realized Investment Gains.Net realized investment gains in 2003 were $40.2 million, compared to net realized gains of $40.9 million and $2.1 million in 2002 and 2001, respectively. The following table details amounts included in net realized gains:

| | | | | | | | | | |

(Dollars in millions)

| | 2003

| | 2002

| | 2001

| |

Net gains on securities sold | | $ | 30.8 | | $ | 39.1 | | $ | 5.3 | |

Foreign exchange gains (losses) on investments | | | 9.4 | | | 1.8 | | | (3.2 | ) |

| | |

|

| |

|

| |

|

|

|

Net realized gains | | $ | 40.2 | | $ | 40.9 | | $ | 2.1 | |

| | |

|

| |

|

| |

|

|

|

Net gains on securities sold are generated as a result of the ongoing management of the investment portfolio. Foreign exchange gains and losses primarily result from investing in short-term foreign currency denominated securities.

Net Mark-to-Market Gains (Losses) on Credit Derivative Contracts.Net mark-to-market gains on credit derivative contracts in 2003 were $0.0 million, compared to net mark-to-market losses of $27.9 million and $3.6 million in 2002 and 2001, respectively. The change in estimated fair value of structured credit derivative contracts reflects net mark-to-market gains and losses due to changes in credit spreads on the underlying obligations. Realized net losses paid on structured credit derivatives totaled $1.2 million, $5.8 million and none for the years ended December 31, 2003, 2002 and 2001, respectively.

Other Income.Other income in 2003 was $5.0 million, a decrease of 9% from $5.5 million in 2002. Included in other income are deal structuring fees and commitment fees. Other income increased 6% in 2002 from $5.2 million in 2001.

Losses and Loss Expenses.Losses and loss expenses in 2003 were $53.4 million, versus $26.7 million in 2002 and $20.0 million in 2001. This increase was the result of credit deterioration in the insured portfolio. Credit deterioration during 2003 is primarily related to credits in the domestic structured finance business.

The following tables provide details of losses paid, net of recoveries received for the years ended December 31, 2003, 2002 and 2001 and net case reserves at December 31, 2003 and December 31, 2002:

| | | | | | | | | |

(Dollars in millions)

| | 2003

| | 2002

| | 2001

|

Net losses paid: | | | | | | | | | |

Public Finance | | $ | 5.8 | | $ | 6.0 | | $ | 1.3 |

Structured Finance | | | 26.9 | | | 3.2 | | | — |

International Finance | | | 1.4 | | | — | | | — |

| | |

|

| |

|

| |

|

|

Total | | $ | 34.1 | | $ | 9.2 | | $ | 1.3 |

| | |

|

| |

|

| |

|

|

| | | | | | |

(Dollars in millions)

| | 2003

| | 2002

|

Net case basis credit reserves(*): | | | | | | |

Public Finance | | $ | 22.6 | | $ | 19.0 |

Structured Finance | | | 26.7 | | | 26.1 |

International Finance | | | 5.4 | | | 3.9 |

| | |

|

| |

|

|

Total | | $ | 54.7 | | $ | 49.0 |

| | |

|

| |

|

|

| * | After netting reinsurance recoverables on unpaid losses amounting to $2.5 million and $4.6 million in 2003 and 2002, respectively. |

30/31

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

The following table summarizes Ambac’s loss reserves split between case basis credit loss reserves and active credit reserves at December 31, 2003 and 2002:

| | | | | | |

(Dollars in millions)

| | 2003

| | 2002

|

Net loss and loss expense reserves: | | | | | | |

Case basis credit reserves | | $ | 54.7 | | $ | 49.0 |

Active credit reserves | | | 132.2 | | | 118.6 |

| | |

|

| |

|

|

Total | | $ | 186.9 | | $ | 167.6 |

| | |

|

| |

|

|

The following table summarizes the changes in the total net loss reserves for the years ended December 31, 2003 and 2002:

| | | | | | | | |

(Dollars in millions)

| | 2003

| | | 2002

| |

Beginning balance of net loss reserves | | $ | 167.6 | | | $ | 150.1 | |

Additions to loss reserves | | | 53.4 | | | | 26.7 | |

Losses paid | | | (45.6 | ) | | | (11.1 | ) |

Recoveries of paid losses from reinsurers | | | 4.0 | | | | 1.3 | |

Other recoveries | | | 7.5 | | | | 0.6 | |

| | |

|

|

| |

|

|

|

Ending balance of net loss reserves | | $ | 186.9 | | | $ | 167.6 | |

| | |

|

|

| |

|

|

|

At December 31, 2003, estimated claim payments, net of estimated recoveries, through 2018 totaled $64.6 million. Related future payments are $2.4 million, $37.9 million, $5.5 million, $3.4 million and $3.4 million for 2004, 2005, 2006, 2007 and 2008, respectively. Additions (reductions) made to the case basis credit reserve totaled $5.7 million, $25.6 million and $(0.1) million in 2003, 2002 and 2001, respectively. The increase in the 2003 case basis credit reserve is primarily attributable to credit deterioration on certain domestic structured finance obligations.

Underwriting and Operating Expenses.Underwriting and operating expenses of $92.0 million in 2003 increased by 20% from $76.5 million in 2002. Underwriting and operating expenses in 2002 increased 13% from $68.0 million in 2001. Underwriting and operating expenses consist of gross underwriting and operating expenses, less the deferral to future periods of expenses and reinsurance commissions related to the acquisition of new insurance contracts, plus the amortization of previously deferred expenses and reinsurance commissions. In 2003, gross underwriting and operating expenses were $135.8 million, an increase of 15% from $117.7 million in 2002. During 2002, gross underwriting and operating expenses increased 19% from $99.3 million in 2001. The increases in gross underwriting and operating expenses in both 2003 and 2002 reflect the overall increased business activity in those years and are primarily attributable to higher compensation costs related to the addition of staff and the expensing of stock options that began in 2003 which totaled $6.2 million. Underwriting and operating expenses deferred were $79.5 million, $73.1 million, and $59.5 million in 2003, 2002 and 2001, respectively. The amortization of previously deferred expenses and reinsurance commissions was $38.5 million, $32.3 million, and $28.2 million in 2003, 2002 and 2001, respectively. The high level of refundings contributed to the increase in amortization of previously deferred expenses in both 2003 and 2002, as any deferred costs associated with a refunded issue is fully amortized at the time of refunding.

FINANCIAL SERVICES

Through its Financial Services subsidiaries, Ambac provides financial and investment products including investment agreements, interest rate swaps, total return swaps and funding conduits, which include municipalities and their authorities, health care organizations and asset-backed issuers.

Financial Services net revenue is defined and analyzed by management as gross interest income less gross interest expense from investment and payment agreements plus revenue from derivative products, and excludes net realized and unrealized losses. Net revenues in 2003 decreased 12% to $36.3 million from $41.1 million in 2002. This decrease is primarily due to lower investment agreement net interest income, which has been adversely impacted by the continued decline in interest rates. The decline in interest rates results in lower income on cash held for liquidity purposes. Additionally, certain mortgage-backed investments tend to prepay causing the related proceeds to be reinvested at lower yields. The decrease in investment agreement net interest income was partially offset by higher derivative product revenues. Net revenues in 2002 increased 6% from $38.6 million in 2001. This increase in net revenue from 2001 to 2002 was primarily due to higher investment agreement net interest income due to higher interest rate spreads and higher volume, partially offset by lower derivative product revenue.

Net realized investment losses in 2003 were $2.0 million compared to net realized investment losses of $134.1 million in 2002. The 2003 and 2002 realized investment loss resulted primarily from a write-down of asset-backed notes issued by National Century Financial Enterprises, Inc. (“NCFE”). These notes, which were rated triple-A until October 25, 2002, defaulted and NCFE filed for protection under Chapter 11 of the U.S. Bankruptcy Code in November 2002. The NCFE notes, which are backed by health care receivables were initially written down by $139.7 million to 20% of par value at December 31,2002. NCFE was further written down by $10.5 million in 2003 to approximately 14% of par value at December 31, 2003. This value represents Ambac’s best estimate of its future recovery from assets in the trust based on existing facts and circumstances and presumes no recovery from litigation.

Ambac Financial Group, Inc.

Financial Services other expenses in 2003 were $12.1 million, an increase of 22% from $9.9 million in 2002, primarily due to higher compensation expenses. Other expenses in 2002 increased 11% from $8.9 million in 2001.

CORPORATE ITEMS

Interest Expense.Interest expense was $54.2 million, $43.7 million and $40.4 million in 2003, 2002 and 2001, respectively. The increase in 2003 is primarily attributable to Ambac’s issuance of $200 million, 5.95% debt, due February 28, 2103, issued in February 2003 and the issuance of $175 million, 5.875%, due March 24, 2103, issued in March 2003. This was partially offset by the redemption at par of Ambac’s $200 million, 7.08% debentures in April 2003. For additional information, please refer to “Liquidity and Capital Resources — Ambac Financial Group, Inc. Liquidity” section. The 2002 increase is primarily attributable to Ambac’s issuance of $200 million in debentures in October 2001, partially offset by lower bank fees associated with capital facilities.

Provision for Income Taxes.Income taxes for continuing operations for 2003 were at an effective rate of 26.1%, compared to 23.3% and 23.8% for 2002 and 2001, respectively. The increase in the effective tax rate in 2003 as compared to 2002 is primarily due to increased underwriting profits in 2003 and the NCFE loss and the related reduction in taxable profits in 2002. The decrease in the effective tax rate in 2002 as compared to 2001 is due to the NCFE loss mentioned above, partially offset by increasing underwriting profits in 2002 and a favorable tax settlement of a state income tax audit in 2001.

LIQUIDITY AND CAPITAL RESOURCES

Ambac Financial Group, Inc. Liquidity.Ambac’s liquidity, both on a short-term basis (for the next twelve months) and a long-term basis (beyond the next twelve months), is largely dependent upon: (i) Ambac Assurance’s ability to pay dividends or make other payments to Ambac; (ii) external financings and (iii) investment income from its investment portfolio. Pursuant to Wisconsin insurance laws, Ambac Assurance may declare dividends, provided that, after giving effect to the distribution, it would not violate certain statutory equity, solvency and asset tests. Based upon these tests, without regulatory approval, the maximum amount that will be available during 2004 for payment of dividends by Ambac Assurance is approximately $274.0 million. During 2003, Ambac Assurance paid dividends of $89.6 million on its common stock to Ambac.

Ambac’s principal uses of liquidity are for the payment of its operating expenses, income taxes, interest on its debt, dividends on its shares of common stock, purchases of its common stock in the open market and capital investments in its subsidiaries. Ambac contributed $210.4 million to Ambac Assurance Corporation during 2003.

The following table includes aggregated information about contractual obligations. These contractual obligations impact Ambac’s short- and long-term liquidity and capital resource needs. The table includes information about payments due under specified contractual obligations, aggregated by type of contractual obligation, including the maturity profile of Ambac’s consolidated long-term debt obligations, investment agreement obligations, payment agreement obligations and operating leases. Purchase obligations are agreements to purchase goods or services that are enforceable and legally binding on Ambac.

| | | | | | | | | | | | | | | | | | |

| | | Contractual Obligations by Year

|

(Dollars in millions)

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

| | Thereafter

|

Long-term debt obligations(1) | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 791.8 |

Investment agreement obligations | | | 1,513.9 | | | 634.7 | | | 711.9 | | | 681.7 | | | 705.4 | | | 1,773.6 |

Payment agreement obligations | | | 23.6 | | | 17.2 | | | 21.6 | | | 23.4 | | | 31.4 | | | 804.8 |

Operating lease obligations | | | 8.0 | | | 7.4 | | | 7.2 | | | 6.3 | | | 6.6 | | | 84.2 |

Purchase obligations(2) | | | 7.1 | | | 2.1 | | | 1.7 | | | — | | | — | | | — |

Pension and post retirement benefits(3) | | | 2.9 | | | 2.7 | | | 2.8 | | | 2.9 | | | 3.0 | | | 17.2 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Total | | $ | 1,555.5 | | $ | 664.1 | | $ | 745.2 | | $ | 714.3 | | $ | 746.4 | | $ | 3,471.6 |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

| (1) | For additional information about long-term debt, see Note 14 to the Consolidated Financial Statements. |

| (2) | Purchase obligations includes various technology related maintenance agreements, rating agency fees and other outside services. |

| (3) | Amount represents expected contributions to the funded defined benefit pension plan and benefit payments on unfunded pension and other postretirement plans for the next 10 years. Contributions to the funded pension plan are equal to the maximum amount that can be deducted for Federal income tax purposes, under current tax laws. |

Based on the amount of dividends that it expects to receive from Ambac Assurance and other subsidiaries during 2004, and the income it expects to receive from its investment portfolio, management believes that Ambac will have sufficient liquidity to satisfy its needs over the next twelve months, including the ability to pay dividends on its common stock in accordance with its dividend policy. Beyond the next twelve months, Ambac Assurance’s ability to declare and pay dividends to Ambac may be influenced by a variety of factors including adverse market changes, insurance regulatory changes and changes in general economic conditions. Consequently, although management believes that Ambac will continue to have sufficient liquidity to meet its debt service and other obligations over the long term, no guarantee can be given that Ambac Assurance will be able to dividend amounts sufficient to pay all of Ambac’s operating expenses, debt service obligations and dividends on its common stock.

32/33

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Ambac Assurance Liquidity.The principal uses of Ambac Assurance’s liquidity are the payment of operating expenses, claim payments, reinsurance premiums, taxes, dividends to Ambac, and capital investments in its subsidiaries. Management believes that Ambac Assurance’s operating liquidity needs can be funded exclusively from its operating cash flow. The principal sources of Ambac Assurance’s liquidity are gross premiums written, scheduled investment maturities, net investment income and receipts from structured credit derivatives.

Financial Services Liquidity.The principal uses of liquidity by Financial Services subsidiaries are payment of investment and payment agreement obligations pursuant to defined terms, net obligations under interest rate swaps and related hedges, operating expenses and income taxes. Management believes that its Financial Services liquidity needs can be funded primarily from its operating cash flow and the maturity of its invested assets. The principal sources of this segment’s liquidity are proceeds from issuance of investment agreements, net investment income, maturities of securities from its investment portfolio (which are invested with the objective of matching the maturity schedule of its obligations under the investment agreements) and net receipts from interest rate swaps and related hedges. Additionally, from time to time, liquidity needs of the Financial Services subsidiaries are satisfied by short-term intercompany loans from Ambac Assurance. The investment objectives with respect to investment agreements are to achieve the highest after-tax total return, subject to a minimum average quality rating of Aa/AA on invested assets, and to maintain cash flow matching of invested assets to funded liabilities to minimize interest rate and liquidity exposure. Financial Services subsidiaries maintain a portion of their assets in short-term investments and repurchase agreements in order to meet unexpected liquidity needs.

Credit Facilities.Ambac and Ambac Assurance have a revolving credit facility with eight major international banks for $300 million, which expires in July 2004 and provides a two-year term loan provision. The facility is available for general corporate purposes, including the payment of claims. As of December 31, 2003 and 2002, no amounts were outstanding under this credit facility. This facility’s financial covenants require that Ambac: (i) maintain as of the end of each fiscal quarter a debt to capital ratio of not more than 30% and (ii) maintain at all times total stockholders’ equity equal to or greater than $2.0 billion. At December 31, 2003, Ambac met all of these requirements.

Capital Support.Ambac Assurance has a series of perpetual put options on its own preferred stock. The counterparty to these put options are trusts established by a major investment bank. The trusts were created as a vehicle for providing capital support to Ambac Assurance by allowing it to obtain immediate access to new capital at its sole discretion at any time through the exercise of the put option. If the put option were exercised, the preferred stock holdings of Ambac Assurance would give investors the rights of an equity investor in Ambac Assurance. Such rights are subordinate to insurance claims, as well as to the general unsecured creditors of Ambac Assurance. If exercised, Ambac Assurance would receive up to $800 million in return for the issuance of its own perpetual preferred stock, the proceeds of which may be used for any purpose including the payment of claims. Dividend payments on the preferred stock are cumulative only if Ambac Assurance pays dividends on its common stock. Each trust is restricted to holding high quality short-term commercial paper investments to ensure that it can meet its obligations under the put option. To fund these investments, each trust has issued its own auction market perpetual preferred stock. Ambac Assurance pays a put option fee. Each trust is rated AA/Aa2 by Standard & Poor’s and Moody’s, respectively.

From time to time Ambac accesses the capital markets to support the growth of its businesses. In April 2003, Ambac filed Form S-3 with the SEC utilizing a “shelf” registration process. Under this process, Ambac may issue up to $500 million of the securities described in the prospectus filed as part of the registration, namely, common stock, preferred stock and debt securities of Ambac.

Balance Sheet.Total assets as of December 31, 2003 were $16.75 billion, an increase of 9% from total assets of $15.36 billion at December 31, 2002. This increase was due primarily to cash generated from business written during 2003 and proceeds from debt issuances. Stockholders’ equity as of December 31, 2003 was $4.25 billion, an increase of 17% from $3.63 billion at year-end 2002. The increase stemmed primarily from net income generated for the year.

Ambac Financial Group, Inc.

The following table summarizes the composition of the fair value of Ambac’s investment portfolio by segment at December 31, 2003 and 2002:

| | | | | | | | | | | | | | | | |

(Dollars in millions)

| | Financial Guarantee

| | | Financial Services

| | | Corporate

| | | Total

| |

2003 : | | | | | | | | | | | | | | | | |

Fixed income securities: | | | | | | | | | | | | | | | | |

Municipal obligations | | $ | 5,305.3 | | | $ | 428.7 | | | $ | — | | | $ | 5,734.0 | |

Corporate obligations | | | 465.0 | | | | 621.2 | | | | — | | | | 1,086.2 | |

Foreign obligations | | | 177.2 | | | | — | | | | — | | | | 177.2 | |

U.S. government obligations | | | 83.8 | | | | 6.2 | | | | — | | | | 90.0 | |

Mortgage and asset-backed securities (includes U.S. government agency obligations) | | | 1,092.2 | | | | 4,663.3 | | | | 17.2 | | | | 5,772.7 | |

Other | | | 3.3 | | | | — | | | | 1.1 | | | | 4.4 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | 7,126.8 | | | | 5,719.4 | | | | 18.3 | | | | 12,864.5 | |

Short-term | | | 208.1 | | | | 6.0 | | | | 36.3 | | | | 250.4 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | 7,334.9 | | | | 5,725.4 | | | | 54.6 | | | | 13,114.9 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| Fixed income securities pledged as collateral: | | | | | | | | | | | | | | | | |

U.S. government obligations | | | — | | | | 12.3 | | | | — | | | | 12.3 | |

Mortgage and asset-backed securities (includes U.S. government agency obligations) | | | — | | | | 649.1 | | | | — | | | | 649.1 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | — | | | | 661.4 | | | | — | | | | 661.4 | |

Total investments | | $ | 7,334.9 | | | $ | 6,386.8 | | | $ | 54.6 | | | $ | 13,776.3 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Percent total | | | 53.2 | % | | | 46.4 | % | | | 0.4 | % | | | 100 | % |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

2002 : | | | | | | | | | | | | | | | | |

Fixed income securities: | | | | | | | | | | | | | | | | |

Municipal obligations | | $ | 4,470.1 | | | $ | 417.8 | | | $ | — | | | $ | 4,887.9 | |

Corporate obligations | | | 432.5 | | | | 1,136.8 | | | | — | | | | 1,569.3 | |

Foreign obligations | | | 120.6 | | | | — | | | | — | | | | 120.6 | |

U.S. government obligations | | | 101.6 | | | | 6.6 | | | | — | | | | 108.2 | |

Mortgage and asset-backed securities (including U.S. government agency obligations) | | | 846.0 | | | | 4,048.0 | | | | 17.6 | | | | 4,911.6 | |

Other | | | 1.7 | | | | — | | | | 0.6 | | | | 2.3 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | 5,972.5 | | | | 5,609.2 | | | | 18.2 | | | | 11,599.9 | |

Short-term | | | 284.3 | | | | 71.6 | | | | 39.9 | | | | 395.8 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | 6,256.8 | | | | 5,680.8 | | | | 58.1 | | | | 11,995.7 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| Fixed income securities pledged as collateral: | | | | | | | | | | | | | | | | |

U.S. government obligations | | | — | | | | — | | | | — | | | | — | |

Mortgage and asset-backed securities (including U.S. government agency obligations) | | | — | | | | 543.6 | | | | — | | | | 543.6 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | — | | | | 543.6 | | | | — | | | | 543.6 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total investments | | $ | 6,256.8 | | | $ | 6,224.4 | | | $ | 58.1 | | | $ | 12,539.3 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Percent total | | | 49.9 | % | | | 49.6 | % | | | 0.5 | % | | | 100 | % |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

The following table summarizes the total pre-tax gross unrealized loss recorded in Accumulated Other Comprehensive Income in stockholders’ equity at December 31, 2003 and 2002 by investment category:

| | | | | | |

(Dollars in millions)

| | 2003 Gross

Unrealized

Losses

| | 2002 Gross

Unrealized

Losses

|

Fixed income securities: | | | | | | |

Municipal obligations | | $ | 6.4 | | $ | 4.6 |

Corporate obligations | | | 6.4 | | | 27.8 |

Foreign obligations | | | 0.7 | | | — |

U.S. government obligations | | | 0.4 | | | 0.3 |

Mortgage and asset-backed securities | | | 22.0 | | | 4.3 |

| | |

|

| |

|

|

Total | | $ | 35.9 | | $ | 37.0 |

| | |

|

| |

|

|

34/35

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

The following table summarizes, for all securities in an unrealized loss position as of December 31, 2003 and 2002, the aggregate fair value and gross unrealized loss by length of time those securities have been continuously in an unrealized loss position:

| | | | | | | | | | | | |

| | | 2003

| | 2002

|

(Dollars in millions)

| | Estimated

Fair

Value

| | Gross

Unrealized

Losses

| | Estimated Fair Value

| | Gross

Unrealized

Losses

|

Municipal obligations in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | $ | 208.8 | | $ | 1.2 | | $ | 146.1 | | $ | 2.4 |

7 – 12 months | | | 225.1 | | | 4.8 | | | 0.9 | | | 0.3 |

Greater than 12 months | | | 6.5 | | | 0.4 | | | 26.9 | | | 1.9 |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 440.4 | | | 6.4 | | | 173.9 | | | 4.6 |

| | |

|

| |

|

| |

|

| |

|

|

Corporate obligations in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | | 100.6 | | | 1.8 | | | 461.1 | | | 7.5 |

7 – 12 months | | | — | | | — | | | 18.5 | | | 2.2 |

Greater than 12 months | | | 100.8 | | | 4.6 | | | 106.7 | | | 18.1 |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 201.4 | | | 6.4 | | | 586.3 | | | 27.8 |

| | |

|

| |

|

| |

|

| |

|

|

Foreign government obligations in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | | 36.6 | | | 0.7 | | | 1.6 | | | — |

7 – 12 months | | | — | | | — | | | — | | | — |

Greater than 12 months | | | — | | | — | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 36.6 | | | 0.7 | | | 1.6 | | | — |

| | |

|

| |

|

| |

|

| |

|

|

U.S. government obligations in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | | 50.2 | | | 0.4 | | | 15.9 | | | 0.3 |

7 – 12 months | | | — | | | — | | | — | | | — |

Greater than 12 months | | | — | | | — | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 50.2 | | | 0.4 | | | 15.9 | | | 0.3 |

| | |

|

| |

|

| |

|

| |

|

|

Mortgage and asset-backed securities in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | | 969.6 | | | 10.7 | | | 576.8 | | | 3.2 |

7 – 12 months | | | 616.2 | | | 9.6 | | | 11.7 | | | 0.1 |

Greater than 12 months | | | 166.0 | | | 1.7 | | | 33.1 | | | 1.0 |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 1,751.8 | | | 22.0 | | | 621.6 | | | 4.3 |

| | |

|

| |

|

| |

|

| |

|

|

Other in continuous unrealized loss for: | | | | | | | | | | | | |

0 – 6 months | | | — | | | — | | | — | | | — |

7 – 12 months | | | 0.2 | | | — | | | — | | | — |

Greater than 12 months | | | 1.5 | | | 0.4 | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 1.7 | | | 0.4 | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

Total | | $ | 2,482.1 | | $ | 36.3 | | $ | 1,399.3 | | $ | 37.0 |

| | |

|

| |

|

| |

|

| |

|

|

There were no individual securities with material unrealized losses as of December 31, 2003 and 2002. As of December 31, 2003 below investment grade securities and non-rated securities which were in an unrealized loss position had a fair value of $9.5 million and unrealized loss of $0.8 million, which represented 0.4% of the total fair value and 2.2% of total pre-tax unrealized losses shown in the above table. As of December 31, 2002 below investment grade securities and non-rated securities which were in an unrealized loss position had a fair value of $46.7 million and an unrealized loss of $5.0 million, which represented 3% of the total fair value and 14% of total pre-tax unrealized loss as shown in the above table.

Ambac Financial Group, Inc.

The following table summarizes amortized cost and fair value for all securities in an unrealized loss position as of December 31, 2003 and 2002, by contractual maturity date:

| | | | | | | | | | | | |

| | | 2003

| | 2002

|

(Dollars in millions)

| | Amortized

Cost

| | Estimated

Fair

Value

| | Amortized

Cost

| | Estimated

Fair

Value

|

Municipal obligations: | | | | | | | | | | | | |

Due in one year or less | | $ | — | | $ | — | | $ | — | | $ | — |

Due after one year through five years | | | — | | | — | | | — | | | — |

Due after five years through ten years | | | 38.8 | | | 38.3 | | | 10.8 | | | 10.6 |

Due after ten years | | | 408.0 | | | 402.1 | | | 167.7 | | | 163.3 |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 446.8 | | | 440.4 | | | 178.5 | | | 173.9 |

| | |

|

| |

|

| |

|

| |

|

|

Corporate obligations: | | | | | | | | | | | | |

Due in one year or less | | | — | | | — | | | — | | | — |

Due after one year through five years | | | 12.6 | | | 11.9 | | | 228.7 | | | 223.0 |

Due after five years through ten years | | | — | | | — | | | 29.6 | | | 29.3 |

Due after ten years | | | 195.2 | | | 189.5 | | | 355.8 | | | 334.0 |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 207.8 | | | 201.4 | | | 614.1 | | | 586.3 |

| | |

|

| |

|

| |

|

| |

|

|

Foreign government obligations: | | | | | | | | | | | | |

Due in one year or less | | | — | | | — | | | 1.6 | | | 1.6 |

Due after one year through five years | | | 19.5 | | | 19.2 | | | — | | | — |

Due after five years through ten years | | | 17.8 | | | 17.4 | | | — | | | — |

Due after ten years | | | — | | | — | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 37.3 | | | 36.6 | | | 1.6 | | | 1.6 |

| | |

|

| |

|

| |

|

| |

|

|

U.S. government obligations: | | | | | | | | | | | | |

Due in one year or less | | | — | | | — | | | — | | | — |

Due after one year through five years | | | — | | | — | | | 16.2 | | | 15.9 |

Due after five years through ten years | | | 25.6 | | | 25.6 | | | — | | | — |

Due after ten years | | | 25.0 | | | 24.6 | | | — | | | — |

| | |

|

| |

|

| |

|

| |

|

|

| | | | 50.6 | | | 50.2 | | | 16.2 | | | 15.9 |

| | |

|

| |

|

| |

|

| |

|

|